Embed Size (px)

Citation preview

Economic Overview

Melissa K. Peralta

Senior Economist

April 27, 2017

Copyright © TTX Company. Confidential: Not For Distribution

TTX OverviewTTX functions as the industry’s railcar cooperative, operating under

pooling authority granted by the Surface Transportation Board

» $1.5 billion company, serves/owned by North America’s leading railroads

» The Company owns/maintains a national pool of over 230,000 railcars/wells:

» Owners enjoy financial/operational benefits matched to business needs:

» Rail customers benefit from a consistent fleet of free-running cars

» TTX is not a leasing company – TTX is a pooling company

o Intermodal o Automotive o General Merchandise

o Capital outlay elimination

o Empty mile reduction

o Risk mitigation

o Operating cost control

2

Copyright © TTX Company. Confidential: Not For Distribution

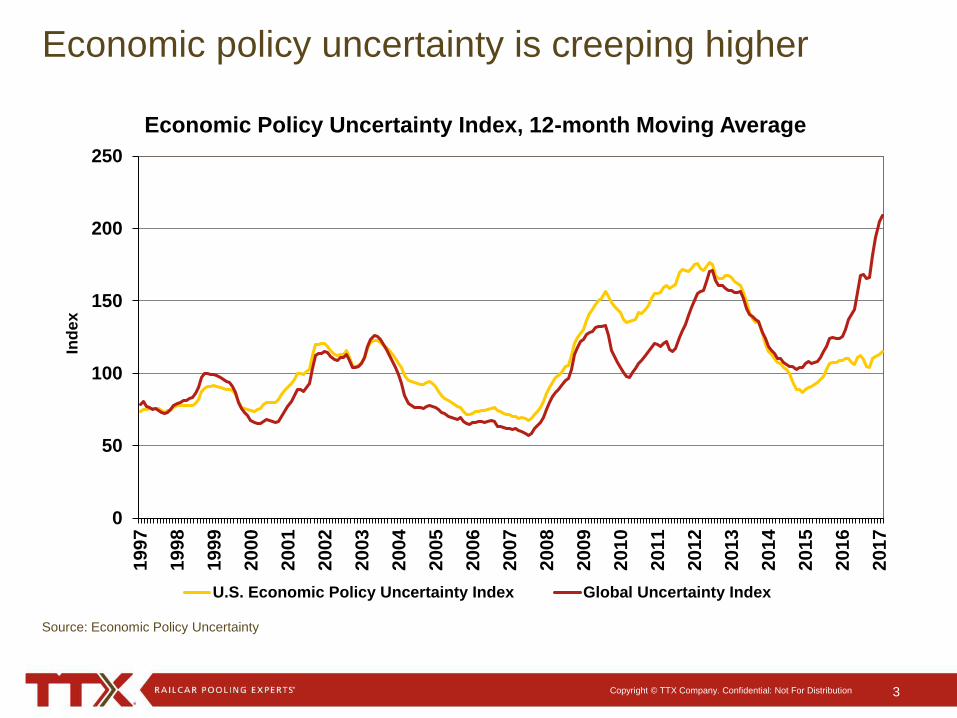

Economic policy uncertainty is creeping higher

0

50

100

150

200

2501997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

Ind

ex

Economic Policy Uncertainty Index, 12-month Moving Average

U.S. Economic Policy Uncertainty Index Global Uncertainty Index

Source: Economic Policy Uncertainty

3

Copyright © TTX Company. Confidential: Not For Distribution

Some proposed policy changes are likely to pose

risks to the economy, some opportunities

Source: National Association of Business Economists

0% 20% 40% 60% 80% 100%

Renegotiate Existing Trade Deals

Implement a "Border Adjustment" Tax

Reduce the Effective Corporate TaxRate

Increase Infrastructure Spending

Pursue Deregulation

Restrict Immigration

Risk Opportunity

4

Copyright © TTX Company. Confidential: Not For Distribution

0%

5%

10%

15%

20%

25%

Jan

-16

Feb

-16

Mar-

16

Ap

r-1

6

Ma

y-1

6

Ju

n-1

6

Ju

l-1

6

Au

g-1

6

Se

p-1

6

Oc

t-1

6

No

v-1

6

De

c-1

6

Ja

n-1

7

Fe

b-1

7

Probability of the U.S. Falling into Recession in 6 Months

A recession in coming months is unlikely

Source: Moody’s Analytics

5

Copyright © TTX Company. Confidential: Not For Distribution

Recent Economic Indicator Trends

Strong Flat to Weak

Consumer & Business Confidence Retail Sales

Employment Growth Vehicle Sales

Industrial Production Total Personal Spending

Housing (Starts, Sales and Prices) Construction Spending

Inventories Durable Goods Orders

Inflation

Fuel Prices

Personal Income

6

Copyright © TTX Company. Confidential: Not For Distribution

Consumer confidence turned up 2016, but will it

translate to a stronger economy?

30

40

50

60

70

80

90

100

110

120

130

Feb

-10

Ma

y-1

0

Au

g-1

0

No

v-1

0

Feb

-11

Ma

y-1

1

Au

g-1

1

No

v-1

1

Fe

b-1

2

Ma

y-1

2

Au

g-1

2

No

v-1

2

Fe

b-1

3

Ma

y-1

3

Au

g-1

3

No

v-1

3

Fe

b-1

4

Ma

y-1

4

Au

g-1

4

No

v-1

4

Fe

b-1

5

Ma

y-1

5

Au

g-1

5

No

v-1

5

Fe

b-1

6

Ma

y-1

6

Au

g-1

6

No

v-1

6

Fe

b-1

7

Ind

ex

19

85

=1

00

, S

A

Consumer Confidence Index

Source: The Conference Board

7

Copyright © TTX Company. Confidential: Not For Distribution

Employment in the U.S. continues to gain strength

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

% U

ne

mp

loye

d

Baseline and U6 Unemployment Rate

Baseline "Unemployed and marginally attached for economic reasons"

Source: U.S. Bureau of Labor Statistics

8

Copyright © TTX Company. Confidential: Not For Distribution

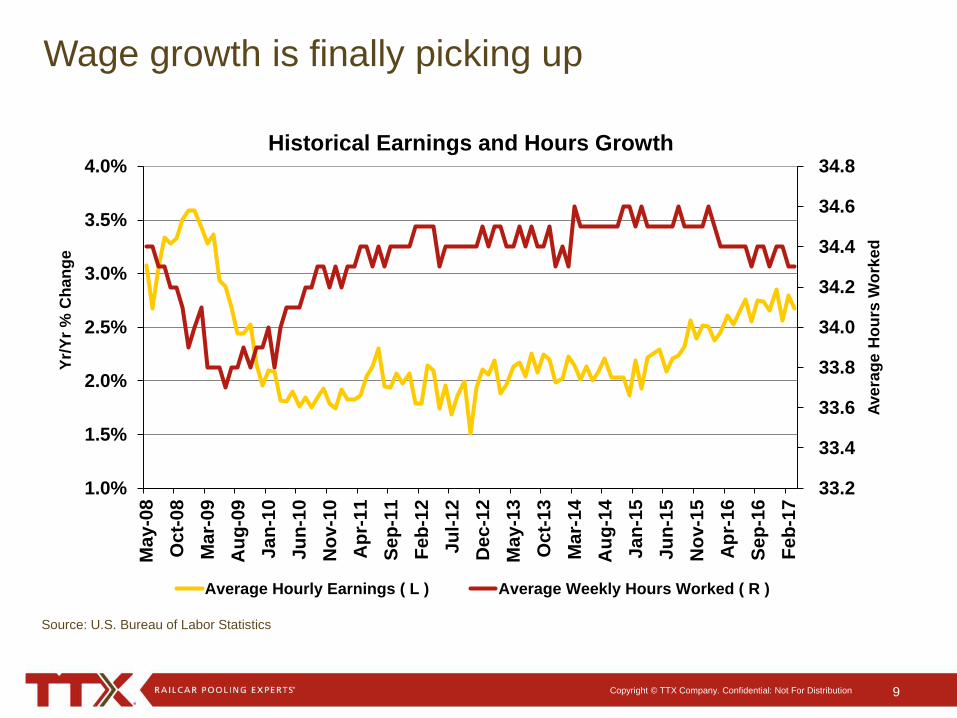

Wage growth is finally picking up

33.2

33.4

33.6

33.8

34.0

34.2

34.4

34.6

34.8

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%M

ay

-08

Oc

t-0

8

Ma

r-0

9

Au

g-0

9

Ja

n-1

0

Ju

n-1

0

No

v-1

0

Ap

r-1

1

Se

p-1

1

Fe

b-1

2

Ju

l-1

2

De

c-1

2

Ma

y-1

3

Oc

t-1

3

Ma

r-1

4

Au

g-1

4

Ja

n-1

5

Ju

n-1

5

No

v-1

5

Ap

r-16

Se

p-1

6

Fe

b-1

7

Ave

rag

e H

ou

rs W

ork

ed

Yr/

Yr

% C

ha

ng

e

Historical Earnings and Hours Growth

Average Hourly Earnings ( L ) Average Weekly Hours Worked ( R )

Source: U.S. Bureau of Labor Statistics

9

Copyright © TTX Company. Confidential: Not For Distribution

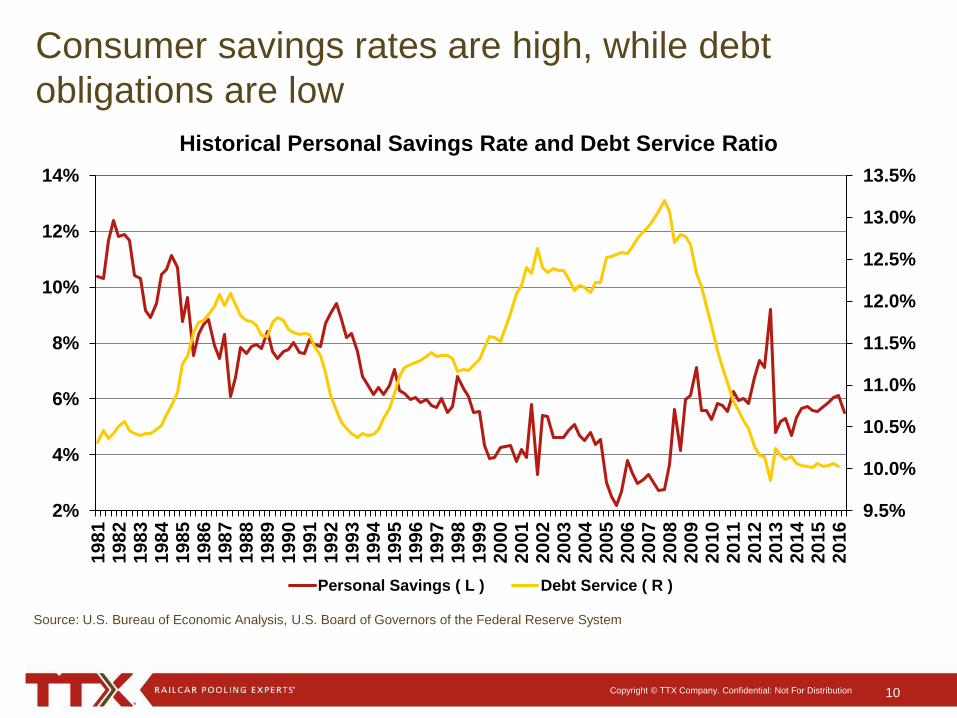

Consumer savings rates are high, while debt

obligations are low

9.5%

10.0%

10.5%

11.0%

11.5%

12.0%

12.5%

13.0%

13.5%

2%

4%

6%

8%

10%

12%

14%

19

81

19

82

19

83

19

84

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

Historical Personal Savings Rate and Debt Service Ratio

Personal Savings ( L ) Debt Service ( R )

Source: U.S. Bureau of Economic Analysis, U.S. Board of Governors of the Federal Reserve System

10

Copyright © TTX Company. Confidential: Not For Distribution

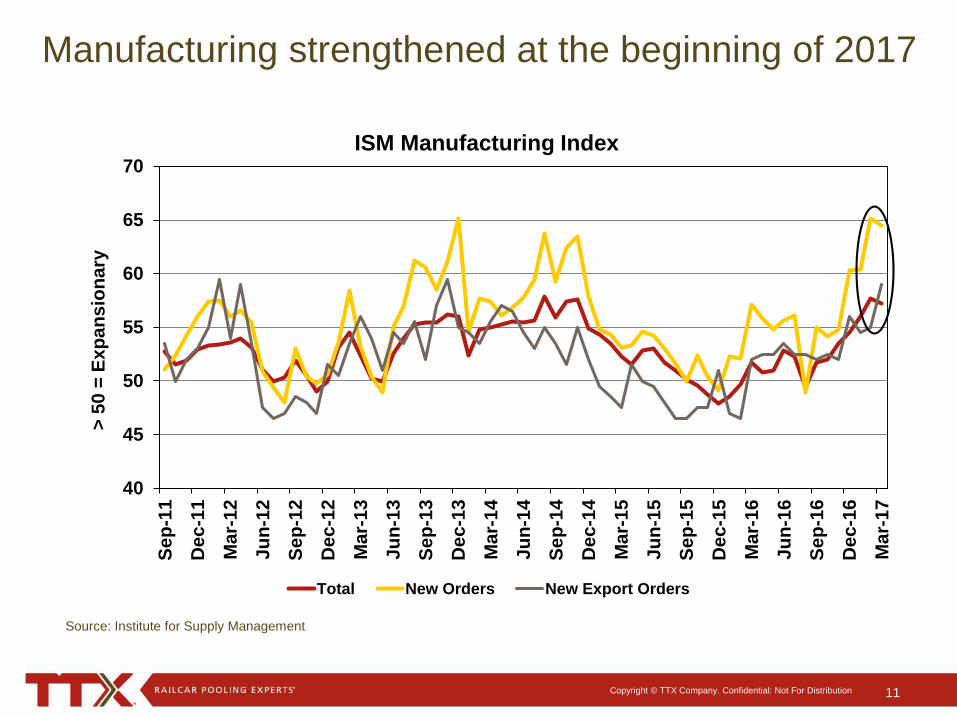

Manufacturing strengthened at the beginning of 2017

40

45

50

55

60

65

70S

ep

-11

De

c-1

1

Ma

r-1

2

Ju

n-1

2

Se

p-1

2

De

c-1

2

Ma

r-1

3

Ju

n-1

3

Se

p-1

3

Dec-1

3

Ma

r-1

4

Ju

n-1

4

Se

p-1

4

De

c-1

4

Ma

r-1

5

Ju

n-1

5

Se

p-1

5

De

c-1

5

Ma

r-1

6

Ju

n-1

6

Se

p-1

6

De

c-1

6

Mar-

17

> 5

0 =

Ex

pa

ns

ion

ary

ISM Manufacturing Index

Total New Orders New Export Orders

Source: Institute for Supply Management

11

Copyright © TTX Company. Confidential: Not For Distribution

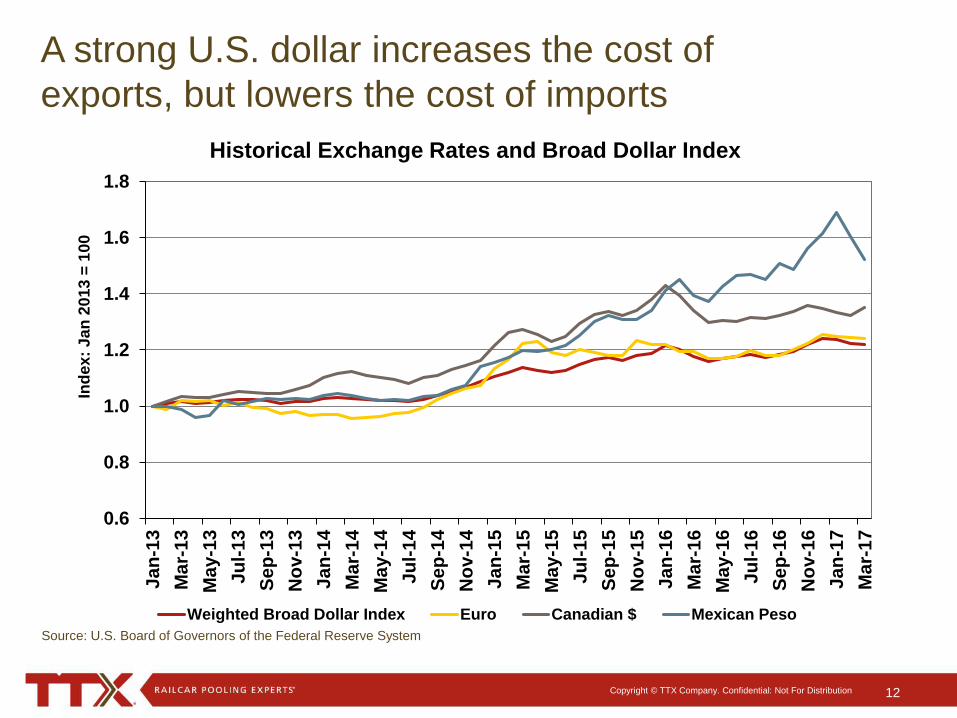

A strong U.S. dollar increases the cost of

exports, but lowers the cost of imports

0.6

0.8

1.0

1.2

1.4

1.6

1.8

Ja

n-1

3

Mar-

13

Ma

y-1

3

Ju

l-1

3

Se

p-1

3

No

v-1

3

Ja

n-1

4

Ma

r-1

4

Ma

y-1

4

Ju

l-1

4

Se

p-1

4

No

v-1

4

Ja

n-1

5

Ma

r-1

5

May-1

5

Ju

l-1

5

Se

p-1

5

No

v-1

5

Ja

n-1

6

Ma

r-1

6

Ma

y-1

6

Ju

l-1

6

Se

p-1

6

No

v-1

6

Ja

n-1

7

Ma

r-1

7

Ind

ex

: J

an

20

13

= 1

00

Historical Exchange Rates and Broad Dollar Index

Weighted Broad Dollar Index Euro Canadian $ Mexican Peso

Source: U.S. Board of Governors of the Federal Reserve System

12

Copyright © TTX Company. Confidential: Not For Distribution

GDP growth is expected to remain modest in 2017

0%

1%

2%

3%

4%

15Q

1

15Q

2

15Q

3

15Q

4

16Q

1

16Q

2

16Q

3

16Q

4

17Q

1

17Q

2

17Q

3

17Q

4

Yr/

Yr

% C

ha

ng

e

GDP, Actual GDP, Forecast

Source: U.S. Bureau of Economic Analysis, Moody’s Analytics

13

Copyright © TTX Company. Confidential: Not For Distribution

Has GDP growth slowed?

Source: Commerce Department

3.6%

4.3%

3.2%

3.4%

3.4%

1.7%

2.0%

0% 1% 2% 3% 4% 5%

1951-60

1961-70

1971-80

1981-90

1991-00

2001-10

2011-16

14

Copyright © TTX Company. Confidential: Not For Distribution

More and more Americans will be leaving

the labor force for retirement

0%

5%

10%

15%

20%

25%

30%

35%

40%1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

2015

2017

2019

% o

f th

e p

op

ula

tio

n in

ea

ch

ag

e b

rac

ke

t

0-19 20-39 40-64 65+

Source: U.S. Census Bureau, Moody's Analytics

15

Copyright © TTX Company. Confidential: Not For Distribution

Productivity growth remains stubbornly low

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

1950s

1960s

1970s

1980s

1990s

2000s

20

10

DT

D

% C

ha

ng

e

Average Annual Labor Productivity Growth

Source: U.S. Bureau of Labor Statistics

16

Copyright © TTX Company. Confidential: Not For Distribution

-2%

-1%

0%

1%

2%

3%

4%

5%

6%

7%

1950

1952

1954

1956

1958

1960

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

Yr/

Yr

% C

ha

ng

e

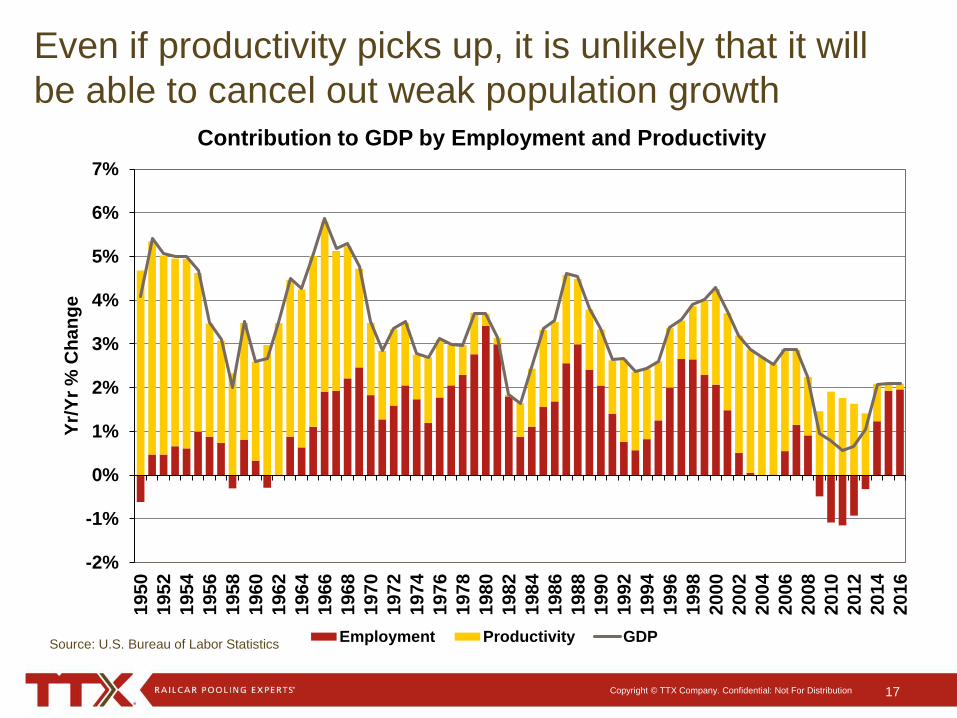

Contribution to GDP by Employment and Productivity

Employment Productivity GDPSource: U.S. Bureau of Labor Statistics

Even if productivity picks up, it is unlikely that it will

be able to cancel out weak population growth

17

Copyright © TTX Company. Confidential: Not For Distribution

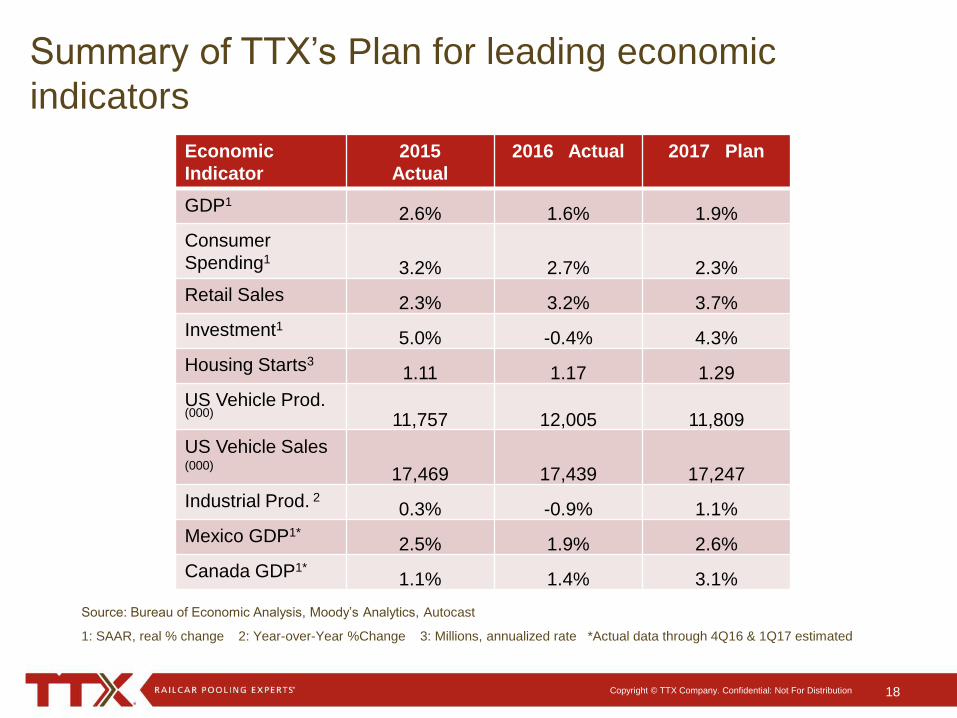

Source: Bureau of Economic Analysis, Moody’s Analytics, Autocast

Economic

Indicator

2015

Actual

2016 Actual 2017 Plan

GDP12.6% 1.6% 1.9%

Consumer

Spending13.2% 2.7% 2.3%

Retail Sales 2.3% 3.2% 3.7%

Investment1 5.0% -0.4% 4.3%

Housing Starts3 1.11 1.17 1.29

US Vehicle Prod.(000)

11,757 12,005 11,809

US Vehicle Sales(000)

17,469 17,439 17,247

Industrial Prod. 20.3% -0.9% 1.1%

Mexico GDP1*2.5% 1.9% 2.6%

Canada GDP1*1.1% 1.4% 3.1%

1: SAAR, real % change 2: Year-over-Year %Change 3: Millions, annualized rate *Actual data through 4Q16 & 1Q17 estimated

Summary of TTX’s Plan for leading economic

indicators

18