Embed Size (px)

Citation preview

Economic freedom and cross-border venture capital performance

Lanfang Wang a,⁎, Susheng Wang b

a Institute of Accounting and Finance, Shanghai University of Finance and Economics,Chinab Hong Kong University of Science and Technology, Hong Kong

a r t i c l e i n f o a b s t r a c t

Article history:Received 15 September 2010Received in revised form 16 October 2011Accepted 21 October 2011Available online 30 October 2011

We investigate the determinants of cross-border venture capital (VC) performance using alarge sample of 10,205 cross-border VC investments by 1906 foreign VC firms (VCs) in 6535domestic portfolio companies. We focus on the impact of a domestic country's economic free-dom on the performance of both VC investments and portfolio companies using a probit modeland the Cox hazard model. After controlling for other related factors of domestic countries,portfolio companies, VCs and the global VC market, as well as year and industry fixed effects,we find that a domestic country's economic freedom is crucial to cross-border VC performance.In particular, in a more economically free country, as measured by the raw values of, quartilesof or the ranking in the index of economic freedom (IEF), a foreign VC-backed portfolio com-pany is more likely to pull off a successful exit through an IPO (initial public offering) or anM&A (merger and acquisition), and a foreign VC firm is likely to spend a shorter investmentduration in the portfolio company. We also identify interesting evidence on the impact ofmany other level factors of domestic countries, portfolio companies, VCs and the global VCmarket on cross-border VC performance.

© 2011 Elsevier B.V. All rights reserved.

JEL classification:G15G24G34

Keywords:Cross-border VCEconomic freedomLegalityEntrepreneurial activity

1. Introduction

Venture capital (VC) is widely regarded as an active driving force in fostering entrepreneurship, financing startups, creatingpublic companies and encouraging innovations in the U.S. over the past several decades (Barry et al., 1990; Kaplan andStrömberg, 2003; Kortum and Lerner, 2000; Lerner, 1994; Sahlman, 1990). It is widely believed that VC is instrumental in bringinginnovations to markets at a rapid pace, thereby enhancing economic growth. VC has been increasingly internationalized, asmarked by an increasing number of cross-border entries of VCs starting from the mid-1990s. Cross-border VC is crucial togrowth-oriented but high-risk new ventures, especially in countries where the domestic supply of private equity is limited.

Our focus is to examine the impact of a domestic country's economic freedom on cross-border VC performance. The idea thateconomic freedom is essential for economic efficiency has been a cornerstone in economic theory since Smith (1776), who arguesfor the role of “the invisible hand” in well-functioning markets. In theory, a free economy is defined as the so-called “Arrow–

Debreu world,” where economic efficiency is guaranteed in general equilibrium (Arrow and Debreu, 1954; Hart, 1980;McKenzie, 1959). In empirical studies, economic freedom has been widely observed to be important to economic growth(Gwartney et al., 1999; Haan and Sturm, 2000; Heckelman, 2000; Wu and Davis, 1999), income equality (Berggren, 1999;Scully, 2002) and employment (Feldmann, 2007, 2008).

For VC investments, the role of economic freedom lies in two aspects. On the one hand, free markets are widely believed toprovide more opportunities for early stage and mostly not-yet-profitable companies, which is essential to VC investments(BjØrnskov and Foss, 2008; Kreft and Sobel, 2005; Nyström, 2008; Sobel et al., 2007; Wennekers et al., 2002). The more

Journal of Empirical Finance 19 (2012) 26–50

⁎ Corresponding author.E-mail addresses: [email protected] (L. Wang), [email protected] (S. Wang).

0927-5398/$ – see front matter © 2011 Elsevier B.V. All rights reserved.doi:10.1016/j.jempfin.2011.10.002

Contents lists available at SciVerse ScienceDirect

Journal of Empirical Finance

j ourna l homepage: www.e lsev ie r .com/ locate / jempf in

constraints there are on the allocation of resources in production and consumption, the fewer growth opportunities and chancesof success for VCs. On the other hand, the government is more likely to act as a “helping hand” instead of a “grabbing hand” in freemarkets, which is also essential for the survival and success of VCs. In an economically free market, the burden of bureaucracy andcorruption would be smaller and the government would try to provide a steady and reliable monetary environment, a free andopen investment environment and a transparent and open financial system. Contract enforcement and investor protection, espe-cially regarding private properties, also tend to be better in free markets. For cross-border VC investments, economic freedom isparticularly important since investment risk, transaction costs, asymmetric information and agency problems are much more se-vere, which makes these types of investments more sensitive to the domestic country's economic environment (Cumming et al.,2006; Gompers et al., 2003; Jeng and Wells, 2000).

Using a large sample of 10,205 cross-border VC investments from 1906 foreign VCs in 6535 domestic portfolio companiescovering 35 countries, we investigate the impact of a domestic country's economic freedom on cross-border VC performance.We provide analysis of both VC investments and portfolio companies using both a probit model and the Cox hazard model.After controlling for other related factors of domestic countries, portfolio companies, VCs and the global VC market, as well asindustry and year fixed effects, we find that a domestic country's economic freedom is crucial to the performance of cross-border VC. In particular, in an economically free country, as measured by either the raw values of, quartiles of or the ranking ineconomic freedom over the investment period, a foreign VC-backed portfolio company is more likely to pull off a successfulexit through an IPO (initial public offering) or an M&A (merger and acquisition), and a foreign VC firm is likely to spend a shorterinvestment duration in a portfolio company. Specifically, a one standard deviation increase in our measure of economic freedom—

Index of Economic Freedom, Economic Freedom Quartile or Ranking in Economic Freedom—at the mean level increases the likelihoodof a successful exit by 2.02%, 2.76% or 3.02%, and the hazard of a successful exit by 5.35%, 12.59% or 13.69%, respectively.

Our main findings are robust to many tests, including tests on a change in economic freedom, tests on exit choices (IPO versusM&A), tests on decomposed effects of economic freedom, tests considering domestic country fixed effects and tests using subsam-ples and alternative measures.

We further find several interesting results from other related factors of domestic countries, portfolio companies, VCs and theglobal VC market. For example, we find legal quality to be positively related to the likelihood of a successful exit through an IPO oran M&A, which is consistent with the empirical work by Cumming et al. (2006). GDP per capital is found to be negatively relatedto cross-border VC performance, which is somewhat consistent with the well-known convergence hypothesis in the exogenousgrowth literature (Barro, 1991, 1996). Also, a domestic country's entrepreneurial activity as measured by the number of VCdeals and the number of patents granted over the investment period is positively associated with the likelihood of a successfulexit through an IPO or an M&A. Further, our results provide evidence confirming the positive impact of portfolio company qualityand local VCs' participation and the negative impact of early stage investments and VCs' portfolio size on cross-border VC perfor-mance, which has been examined in previous studies (Cumming, 2006; Cumming and Dai, 2010, 2011; Dai et al., 2010; Mäkeläand Maula, 2008; Tykvová and Schertler, 2011). In particular, our finding that market conditions have a strong impact on theexit choice between an IPO and an M&A sheds light on the exit timing of cross-border VCs.

There are few studies on cross-border VC performance that are closely related to ours.1 Wang and Wang (2011) investigatethe determinants of cross-border VC performance in China using a small sample of 495 VC investments in 243 portfolio compa-nies by 84 foreign VCs. They document that foreign VCs' human capital has little importance to the likelihood of successful exits.In contrast, the domestic entrepreneurs' experience is crucial to VC performance. Our study differs significantly from that of Wangand Wang (2011) in that we provide an international study on cross-border VC performance covering 35 domestic countries,while Wang andWang (2011) focus on one domestic country, China. Also, we investigate the impact of a domestic country's eco-nomic freedom on cross-border VC performance after controlling for many other level factors of domestic countries, portfoliocompanies, VCs and the global VC market, while Wang and Wang (2011) focus on foreign VCs' human capital and domesticentrepreneurs' experience.

Dai et al. (2010) partially address cross-border VC performance using a sample of 4254 rounds of VC financing by 468 VCs in sixAsian countries. They suggest a positive role of local VCs; that is, cooperation with local VCs helps mitigate information asymmetryand contributes to the likelihood of a portfolio company's successful exit through an IPO. Different fromDai et al. (2010),we emphasizethe role of a country-level factor, namely the domestic country's economic freedom, in cross-border VC performancewhile controllingfor many other factors including local VCs' participation which is also examined in their study. Our results on the impact of local VCs'participation are quite consistent with those of Dai et al. (2010), and provide supporting evidence to their finding.

Another closely related study is that of Watson and George (2010), who examine the influence of several country-level factors,such as the size of the economy, business freedom, trade protection, burden of taxation, government size, price stability, open-ness, corruption and cultural distance, on the rate of return in 72 foreign acquisitions from 144 transactions in 24 different coun-tries. Even though the research question addressed byWatson and George (2010) is similar to ours, there are substantial differencesbetween the two studies. First, they use a small sample consisting of only foreign acquisitions of private equity, which cannot repre-sent the bulk of cross-border VC investments. We use a large sample of 10,205 cross-border VC investments by 1906 foreign VCs in

1 For a comparison of VC investment characteristics in different countries, see Black and Gilson (1998), Lockett et al. (2002), Cumming and MacIntosh (2003),Bruton et al. (2004), Lerner and Schoar (2005), Mayer et al. (2005), Ahlstrom and Bruton (2006), Cumming et al. (2006), Schwienbacher (2008), Cumming et al.(2010), etc. For other aspects of cross-border VC investments (such as economic factors in attracting funding from foreign VCs and the role of local investors), seeMäkelä and Maula (2008), Balcarcel et al. (2009), Schertler and Tykvová (2011), Chemmanur et al. (2011), Tykvová and Schertler (2011), etc. For determinants ofdomestic VC performance, see Hochberg et al. (2007), Zarutskie (2007), Bottazzi et al. (2008), Gompers et al. (2008), Nahata (2008), etc.

27L. Wang, S. Wang / Journal of Empirical Finance 19 (2012) 26–50

6535 domestic portfolio companies during 1995–2005 covering 35 domestic countries. Second, their model is quite simple. Manyrelated factors of countries, investors, investees and the global market that have been examined in existing studies are not con-sidered. Also, they put all nine country-level factors into a regression at the same time, which may result in multicollinearity.Lastly, most of the country-level factors they estimate are captured by the economic freedom variable in our paper. We havedone a robustness study on the decomposed effects of economic freedom (Section 5.3) and our findings confirm some oftheir results.

Our study is also related to studies on economic freedom. Economic freedom is widely investigated in macroeconomicanalyses, especially those on long-term economic development across countries. The general equilibrium theory shows thateconomic efficiency can be achieved in the Arrow–Debreu world, where the market is complete, perfect and competitive.Economic freedommeasures the degree to which an economy is consistent with these underlying assumptions. Empirical studieshave found that economic freedom indeed contributes significantly to economic growth. In a study of 98 countries for the pe-riod 1960–1985, Barro (1991) suggests that economic growth is inversely related to market distortions. Barro (1996) furtherfinds that economic freedom has a favorable impact on economic growth. Using an augmented Solow model with cross-sectional data, Vanssay and Spindler (1994) also find that economic freedom has a significant and substantial effect on econom-ic growth.

Over the last decade or so, a number of indicators on economic freedom have become available and they have subsequentlybeen applied to empirical growth models. Wu and Davis (1999) identify the role of economic freedom in enhancing economicgrowth after controlling for political freedom. In contrast, Gwartney et al. (1999) and Haan and Sturm (2000) find that the level ofeconomic freedom does not contribute significantly to economic growth; instead, a positive change in economic freedom does.Also, Heckelman (2000) suggests that the average level of freedom in a nation, aswell asmany of the specific underlying componentsof freedom, precedes economic growth, after addressing the possibility of reverse causality with a series of Granger-causality tests.

The existing studies also explore the role of economic freedom in income equality, employment and welfare. Berggren (1999)finds that during the period 1975–1985, the higher the degree of economic freedom, the higher the degree of income equality in acountry. Scully (2002) uses a structural model and a reduced-form model to show that economic freedom is beneficial to botheconomic growth and income equality. Feldmann (2007, 2008) confirms a positive role of economic freedom in employment.Esposto and Zaleski (1999) conclude that the quality of life is positively associated with economic freedom.

However, the empirical literature on economic freedom has focused on its long-term macroeconomic consequences. Thispaper investigates the impact of economic freedom on cross-border VC performance at the VC investment level and the portfoliocompany level. The theoretical link between economic freedom and cross-border VC performance, as implied by the general equi-librium theory, is that an economically free economy ensures free markets for early stage companies and in turn improves theeconomic efficiency of resource allocation. More specifically, a more economically free country can provide better growth oppor-tunities, greater chances of success, and more protection with less grabbing from the government for cross-border VCs. Indeed,we find a positive association between a domestic country's economic freedom and cross-border VC performance after controllingfor other related factors of domestic countries, portfolio companies, VCs and the global VC market.

We contribute to the literature in several ways. First, we investigate the role of a domestic country's economic freedom oncross-border VC performance. This is our main contribution. The literature on economic freedom has focused on long-term effects,typically economic growth, at the macro level. We provide an analysis of economic freedom at the micro level, specifically onindividual cross-border VC investments and domestic portfolio companies. Such an analysis has policy implications for fosteringcross-border VC investments. Second, our study deepens the understanding of cross-border VC investments around the world andenriches the literature on the internationalization of VC. Studies on cross-border VC investments are rare. With rapid globalizationin recent years, cross-border VC investments have become a significant phenomenon. Such investments can have a huge impacton the countries involved in innovations, technology transfers and entrepreneurship. Third, we also document the effects of othercountry-level factors on cross-border VC performance, especially such factors as economic development, stock market capitaliza-tion, stock market performance, legal quality and entrepreneurial activity. Our results also address the influence of many otherrelated factors of portfolio companies, VCs and the global VC market.

The remainder of this paper is organized as follows. Section 2 describes the sample and the research methodology. Sec-tions 3 and 4 provide analyses of cross-border VC performance at the VC investment level and at the portfolio companylevel, respectively. Section 5 conducts extensive robustness tests. Section 6 concludes the paper with a summary of ourmain results.

2. Sample and methodology

2.1. Sample

For cross-border VC investments, we rely primarily on the SDC VentureXpert database from Thomson Financial.2 We focus onthe cross-border VC investments made by foreign VCs in domestic portfolio companies. Here, the VCs and portfolio companies are

2 An advantage of using the SDC VentureXpert database is its comprehensive coverage. This database claims to cover over 2300 VC funds worldwide. Accordingto Kaplan et al. (2002), the SDC VentureXpert database captures around 85% of the financing rounds made by American VCs. Du and Vertinsky (2008) point outthat this database also includes most of the venture-related VC deals in Europe and most of the big VC deals in Asia. Aizenman and Kendall (2008) consider thisdatabase to be a comprehensive data source for VC deals worldwide, with over 30 years of historical data.

28 L. Wang, S. Wang / Journal of Empirical Finance 19 (2012) 26–50

located in different countries.3 The primary sample comprises all cross-border VC investments made during 1995–2005 inportfolio companies that received their initial VC funding in the same period. We have employed the following sample selectionprocedure to obtain the final sample of VC investments: (1) we exclude those investments made by angels and buyout funds andconcentrate on the investments made by VC funds; (2) we exclude those investments made in the buyout/acquisition stage or anunknown stage of portfolio companies; (3) we focus on the first investment made by each VC firm in a portfolio company,because the performance in later rounds depends heavily on investments in earlier rounds; and (4) we exclude those investmentsfor which we do not have matching data for our regression variables. We ended up with 10,205 cross-border VC investmentobservations involving 1906 foreign VCs in 6535 domestic portfolio companies. The sample covers 35 domestic countries—Argentina, Australia, Austria, Belgium, Brazil, Canada, Chile, China,4 Denmark, Finland, France, Germany, Hong Kong, India,Indonesia, Ireland, Israel, Italy, Japan, Malaysia, Mexico, the Netherlands, New Zealand, Norway, Philippines, Portugal, Singapore,South Africa, South Korea, Spain, Sweden, Switzerland, Thailand, the U.K. and the U.S.

Table 1 presents the distribution of 10,205 VC investments by funding year and development stage of a portfolio company, thedistribution of 6535 portfolio companies by country and industry, and the distribution of 1906 VCs by global region and organi-zational type. The number of observations and the corresponding percentages (in parentheses) are given. As shown, the internetbubble in the late 1990s has affected the timing of cross-border VC investments. The cross-border VC investments peaked in 2000and then decreased during 2001–2003. Around 38.1% of VC investments occurred at the early or seed stage of development of aportfolio company. The U.S. is the most active in VC imports, constituting roughly 40.9% of our sample. Those countries followingthe U.S., with each constituting just over 3% of our sample, are the UK, Germany, France, Canada, China, and Israel in that order.Our sample spans the following six industries based on the Venture Economics Industry Classification: biotechnology, communi-cation and media, computer-related, medical/health/life science, semiconductors/other electronics, and non-high technology.Similar to the situation in the U.S., the majority of VC-backed portfolio companies belong to high-tech sectors, such as the com-munications and media sector and the computer-related sector, which constitute about 19.5% and 40.1% of our sample, respec-tively. As indicated in the table, VCs from Asia, Europe and North America constitute respectively 31.4%, 23.4% and 41.1% of thesample. VCs from other regions constitute only 4.1% of the sample. Following the literature on VC strategies (Bottazzi et al.,2008; Hellmann et al., 2008; Nahata, 2008), we identify four VC firm types: independent VCs, and VCs affiliated with financialinstitutions, corporations, or governments. For simplicity, we refer to them respectively as traditional VCs, institutional VCs,corporate VCs and government VCs. As presented in the table, around 58.5% of VCs are traditional VCs, whereas institutionalVCs, corporate VCs and government VCs constitute respectively 18.3%, 17.6% and 4.7% of the sample.

2.2. Methodology

Wemeasure VC performance using the likelihood of a successful exit by the end of 2009, and call this Investment Success. A portfoliocompany is treated as successful if it went public orwas acquired by the end of 2009.We conduct analyses of the likelihood and timing ofsuccessful exits at both theVC investment level and the portfolio company level. Specifically,we conduct a probit analysiswith InvestmentSuccess as the dependent variable and a survival analysis using a Cox hazard model with Investment Duration as the dependent variable.The Cox hazardmodel allows for right-censored data and time-varying variables, and it is a semi-parametric model in which the hazardfunction is not dependent on a specific distribution of the survival time. A positive (or negative) coefficient indicates that the variable in-creases (or decreases) the hazard of a successful exit and shortens (or lengthens) the expected duration.We take three alternative mea-sures of a domestic country's economic freedom during the investment period—Index of Economic Freedom, Economic Freedom Quartileand Ranking in Economic Freedom—as our primary explanatory variables.

Following the literature and taking into account the characteristics of cross-border VC markets, we further control for otherrelated factors of domestic countries, portfolio companies, VCs and the global VC market, as well as industry and year fixed effects.Specifically, the domestic country-related factors are GDP per Capital, Market Capitalization, Market Return, Legality, Foreign Coun-try Legality, Same Legal Indicator, VC Deals and Patents. The portfolio company-related factors are Total VC Funding, ValuationDisclosure Indicator, Early Investment Indicator and Distance. The VC firm-related factors are Local VC Ratio, VC Experience, VCSize, VC Size Squared, VC Portfolio Size, Institutional VC Indicator, Corporate VC Indicator, Asia VC Indicator and Europe VC Indicator.The global VC market-related factors are VC Industry Competition, IPO Market Conditions and M&A Market Conditions.

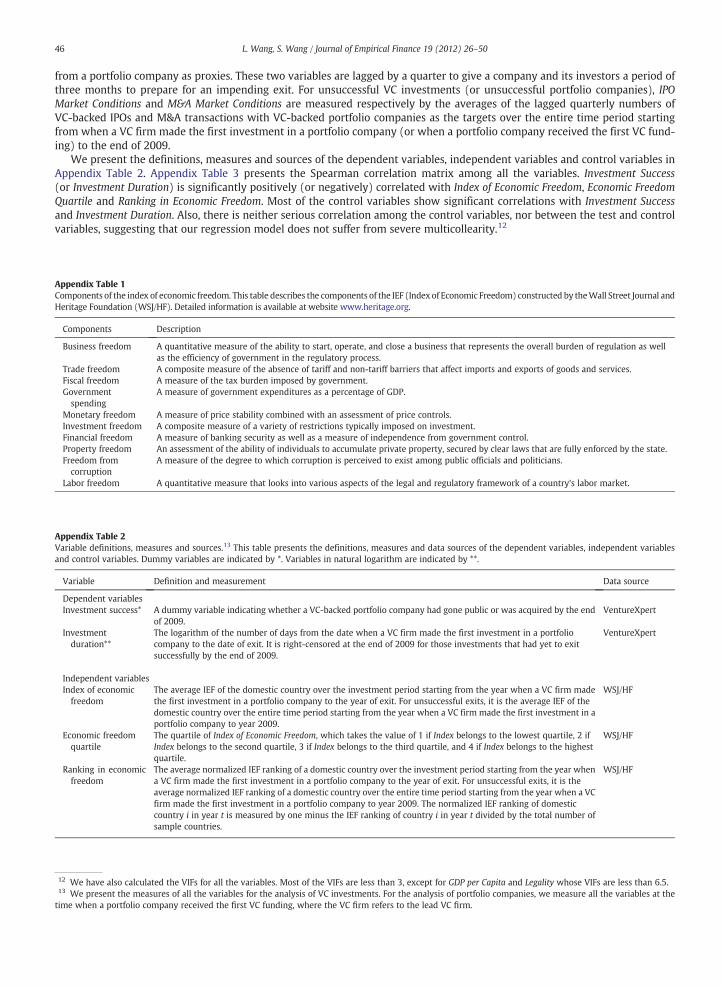

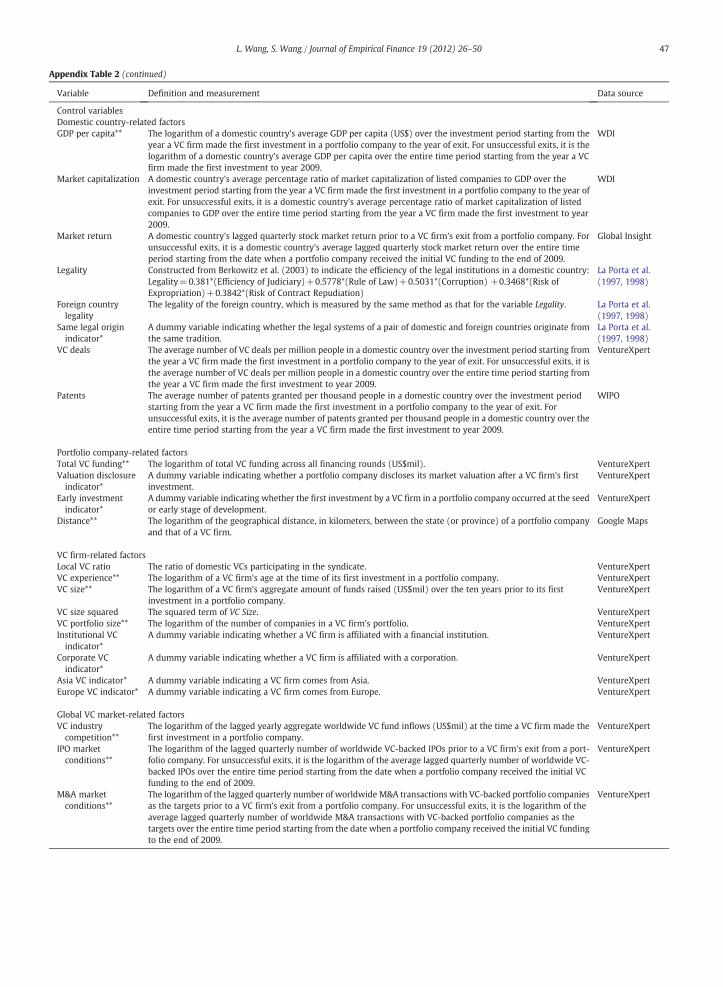

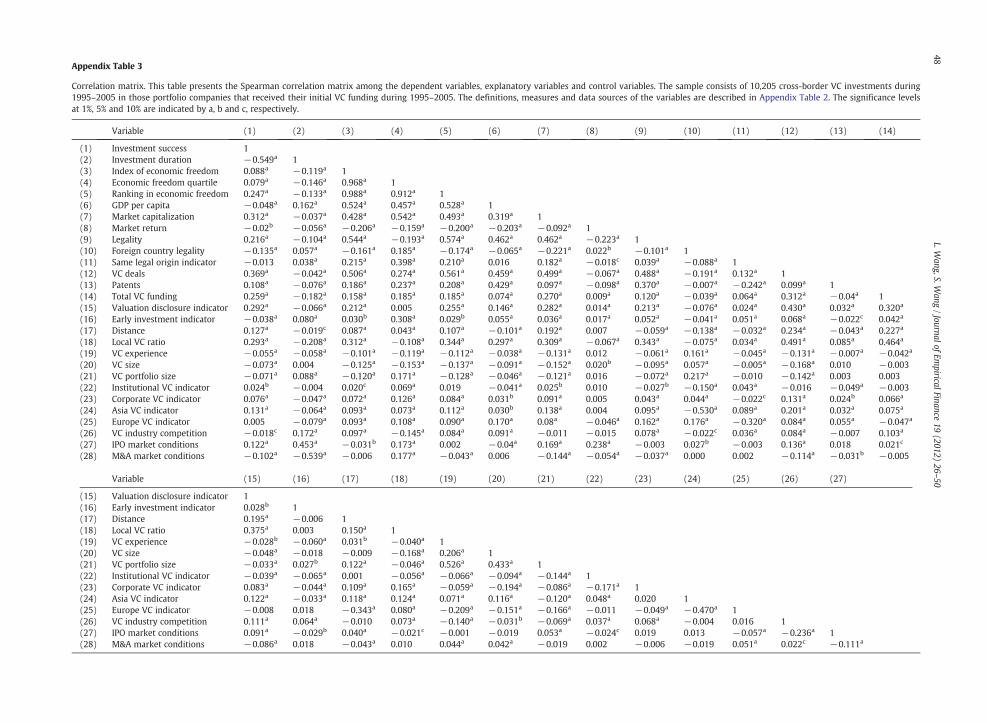

The Appendix provides a detailed discussion of our methods and the definitions of all regression variables. Appendix Tables 1–3describe the components of economic freedom, the measures of variables and the correlation matrix, respectively.

3 Since the SDC VentureXpert database only provides updated information on the location of portfolio companies and VCs, we use such information to identifycross-border VC investment observations, an approach that is consistent with existing studies on cross-border VC investments using public data sources(Balcarcel et al., 2009; Dai et al., 2010; Schertler and Tykvová, 2011; Wang and Wang, 2011; Watson and George, 2010). We do not have historical informationfor each portfolio company at the time of VC funding and the time of exit. Therefore, we cannot define cross-border VC investments as investments by foreign VCsin domestic portfolio companies at the time of investment. There might be a bias here since Cumming et al. (2009) find that relocation to the U.S. implies muchgreater returns to Asia-Pacific VCs than investing in companies already based in the U.S. at the time of VC investment using a hand-collected sample of 468 port-folio companies. As suggested by Cumming et al. (2009) that most relocations (all but three in their sample) were moves to the U.S., we have tried to rule out theinfluence of relocation on our findings by excluding the U.S. portfolio companies in a robustness test.

4 La Porta et al. (1997, 1998) do not provide legality values for China. Considering China's importance in cross-border VC investments, and in line withCumming et al. (2006), we employ the average German legal origin values for China. These values are somewhat consistent with the legal index estimates forChina by Allen et al. (2005) and Durnev and Kim (2005). In a robustness test, after excluding China from our sample, all our results remain unchanged.

29L. Wang, S. Wang / Journal of Empirical Finance 19 (2012) 26–50

Table 1The sample distribution. The sample consists of 10,205 identifiable cross-border VC investments by 1906 VCs in 6535 portfolio companies that received their initial VC funding during 1995–2005 and for which relevant dataare available. The table presents the distribution of VC investments by funding year and the development stage of portfolio companies, the distribution of VC-backed portfolio companies by country and industry, and thedistribution of VCs by global region and type. The number of observations and the corresponding percentages (in parentheses) are reported.

VC investments Portfolio companies VCs

Year Obs. Stage Obs. Country Obs. Industry Obs. Global region Obs. Type Obs.

1995 134 (1.31) Seed/Startup 1191 (11.67) U.S. 2670 (40.86) Biotechnology 503 (7.70) Asia 599 (31.43) Traditional VC 1114 (58.45)1996 309 (3.03) Early stage 2698 (26.44) U.K 595 (9.10) Communications and media 1273 (19.48) Europe 445 (23.35) Institutional VC 348 (18.26)1997 359 (3.52) Expansion stage 5217 (51.12) Germany 323 (4.94) Computer related 2621 (40.11) North America 783 (41.08) Corporate VC 336 (17.63)1998 531 (5.20) Later stage 1099 (10.77) France 316 (4.84) Medical/health/life science 521 (7.97) Other 79 (4.14) Government VC 89 (4.67)1999 1187 (11.63) Total 10,205 (100) Canada 312 (4.77) Semiconductors/other electronics 562 (8.60) Total 1906 (100) Total 1906 (100)2000 2456 (24.07) China 274 (4.19) Non-high technology 1055 (16.14)2001 1601 (15.69) Israel 219 (3.35) Total 6535 (100)2002 955 (9.36) India 173 (2.65)2003 859 (8.42) Sweden 169 (2.59)2004 1024 (10.03) Japan 153 (2.34)2005 790 (7.74) Other 1331 (20.37)Total 10,205 (100) Total 6535 (100)

30L.W

ang,S.Wang

/JournalofEm

piricalFinance19

(2012)26

–50

We avoid an investigation using aggregate data at the country level, which is often subject to the simultaneous critique. It ismuch more sensible to examine data at the VC investment level and the portfolio company level where the environment is con-stant and much finer controls are available. For the analysis of VC investments, we focus only on each VC firm at the time of itsfirst investment in a portfolio company, with a sample size of 10,205; and likewise, for the analysis of portfolio companies, wefocus only on each portfolio company at the time of its receiving the initial VC funding, with a sample size of 6535. The reasonfor this treatment is that there is typically a substantial time gap between a VC firm's first investment and its exit, as well as be-tween a portfolio company's first VC funding and its exit. This methodology can effectively address concerns regarding reversecausality where better cross-border VC performance can conversely lead to more economic freedom in the domestic country.Similar approaches have been adopted by Hochberg et al. (2007), Nahata (2008), etc.

In the Cox hazard analysis, we further allow for time variation of the variables Index of Economic Freedom, Economic FreedomQuartile, Ranking in Economic Freedom, GDP per Capita, Market Capitalization, Market Return, VC Deals, Patents, IPO Market Condi-tions and M&A Market Conditions to alleviate the problem of measuring unsuccessful exits. The hazard framework has theadded advantage of being able to capture the market conditions at the time of a domestic country's macroeconomic developmentand exit to determine their impact on the likelihood of a successful exit, for which a simple probit model cannot do.

In summary, our basic regression models are:

The probit model:

Investment Success ¼ α0 þ α1 Economic Freedomþ α2 Country�related f actorsþ α3 Portf olio company�related f actorsþ α4VC f irm�related f actorsþ α5Global VC market�related f actorsþ Industry dummiesþ Year dummies: ð1Þ

The Cox hazard model:

Investment Duration ¼ β1 Economic Freedomþ β2 Country�related f actorsþ β3 Portf olio company�related f actorsþ β4 VC f irm�related f actorsþ β5Global VC market�related f actorsþ Industry dummiesþ Year dummies: ð2Þ

Here, “Economic Freedom” is either Index of Economic Freedom, Economic Freedom Quartile or Ranking in Economic Freedom.

2.3. Summary statistics and univariate analysis

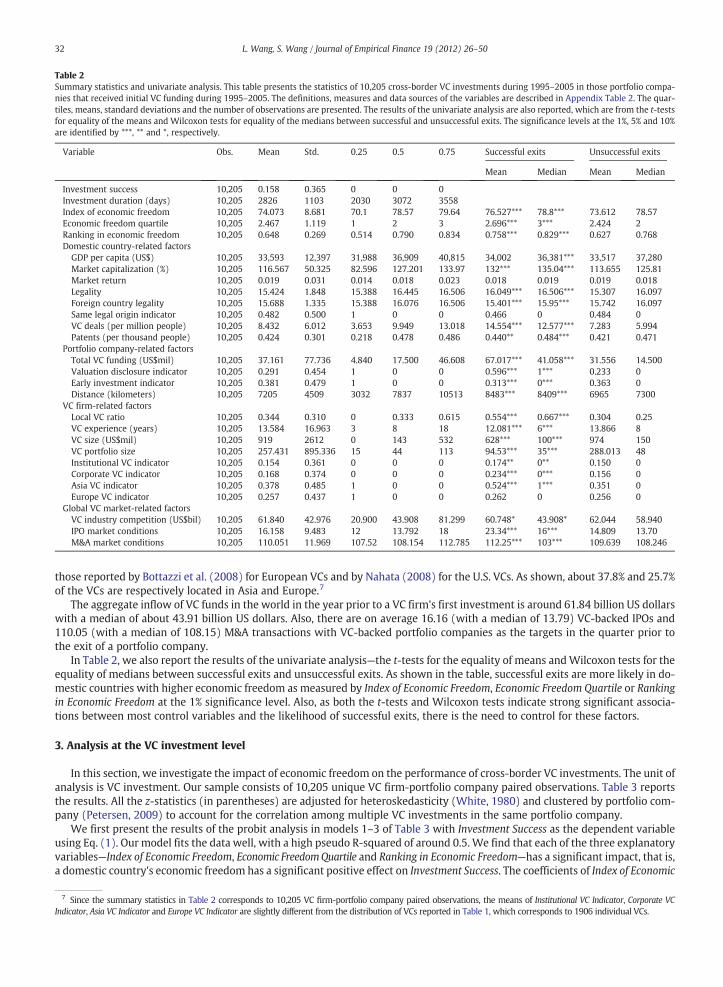

Table 2 presents the summary statistics at the VC investment level.5 The quartiles, means, standard deviations and the numberof observations are presented. We have very similar data distributions at the portfolio company level (not reported).

Only 15.8% of the cross-border VC investments exit successfully through IPOs or acquisitions, a level that is much lower thanthe 33.5% reported by Nahata (2008) and the 41.8% reported by Cochrane (2005) for U.S. domestic VC investments. The averageInvestment Duration is 2826 days with a median of 3072 days.6 The means (medians) of Index of Economic Freedom, EconomicFreedom Quartile and Ranking in Economic Freedom are respectively 74.07 (78.57), 2.47 (2) and 0.65 (0.79).

The means (medians) of GDP per Capita, Market Capitalization, Market Return, Legality, Foreign Country Legality, VC Deals andPatents are respectively 33,593 (36,909) US dollars, 116.57% (127.2%), 1.9% (1.8%), 15.42 (16.45), 15.68 (16.08), 8.43 (9.95) permillion people and 0.42 (0.48) per thousand people. Around 48.2% of domestic countries' legal systems originate from thesame tradition as that of the corresponding foreign countries.

The total VC funding across all financing rounds in a portfolio company is 37.16 million US dollars on averagewith amedian of about17.50 million US dollars. About 29.1% of portfolio companies voluntarily disclose their market valuation after VCs' first investment inthem, which is slightly lower than the 34.4% reported by Cumming and Dai (2011) for the U.S. VC investments made during1991–2006. Further, 38.1% of first investments by a VC firm in a portfolio company occur at the seed or early stage of development,which is much lower than the 63.7% reported by Nahata (2008) and the 62% reported by Gompers et al. (2010) for the U.S. VC industry.The average geographical distance between a portfolio company and a VC firm is 7205 km with a median of 7837 km.

On average, 34.4% of VCs participating in the syndicate of a portfolio company are domestic VCs. The average VC age is about13.58 years old at the time of its first investment in a portfolio company with a median of about 8 years old. The aggregate amountof funds raised by a VC firm over the ten years prior to its first investment in a portfolio company is about 919 million US dollarswith a median of only 143 million US dollars. The mean (median) number of companies in a VC firm's portfolio is 257.43 (44). Thereported portfolio size is much larger than that suggested by Cumming (2006) since our unit of analysis is VC firm instead of VCfund. Around 15.4% and 16.8% of VCs are respectively institutional and corporate VCs; these percentages are slightly larger than

5 We report the original values for all the variables in Table 2, even though we have taken logarithms of some variables in our regressions (as indicated by “**”in Appendix Table 2).

6 The average Investment Duration of VC investments is only 1239 days for successful exits and is 2826 days for all VC investments (taking into account the factthat we do not know the exact time of unsuccessful exits and that Investment Duration of unsuccessful exits is right-censored at the end of 2009).

31L. Wang, S. Wang / Journal of Empirical Finance 19 (2012) 26–50

those reported by Bottazzi et al. (2008) for European VCs and by Nahata (2008) for the U.S. VCs. As shown, about 37.8% and 25.7%of the VCs are respectively located in Asia and Europe.7

The aggregate inflow of VC funds in the world in the year prior to a VC firm's first investment is around 61.84 billion US dollarswith a median of about 43.91 billion US dollars. Also, there are on average 16.16 (with a median of 13.79) VC-backed IPOs and110.05 (with a median of 108.15) M&A transactions with VC-backed portfolio companies as the targets in the quarter prior tothe exit of a portfolio company.

In Table 2, we also report the results of the univariate analysis—the t-tests for the equality of means andWilcoxon tests for theequality of medians between successful exits and unsuccessful exits. As shown in the table, successful exits are more likely in do-mestic countries with higher economic freedom as measured by Index of Economic Freedom, Economic Freedom Quartile or Rankingin Economic Freedom at the 1% significance level. Also, as both the t-tests and Wilcoxon tests indicate strong significant associa-tions between most control variables and the likelihood of successful exits, there is the need to control for these factors.

3. Analysis at the VC investment level

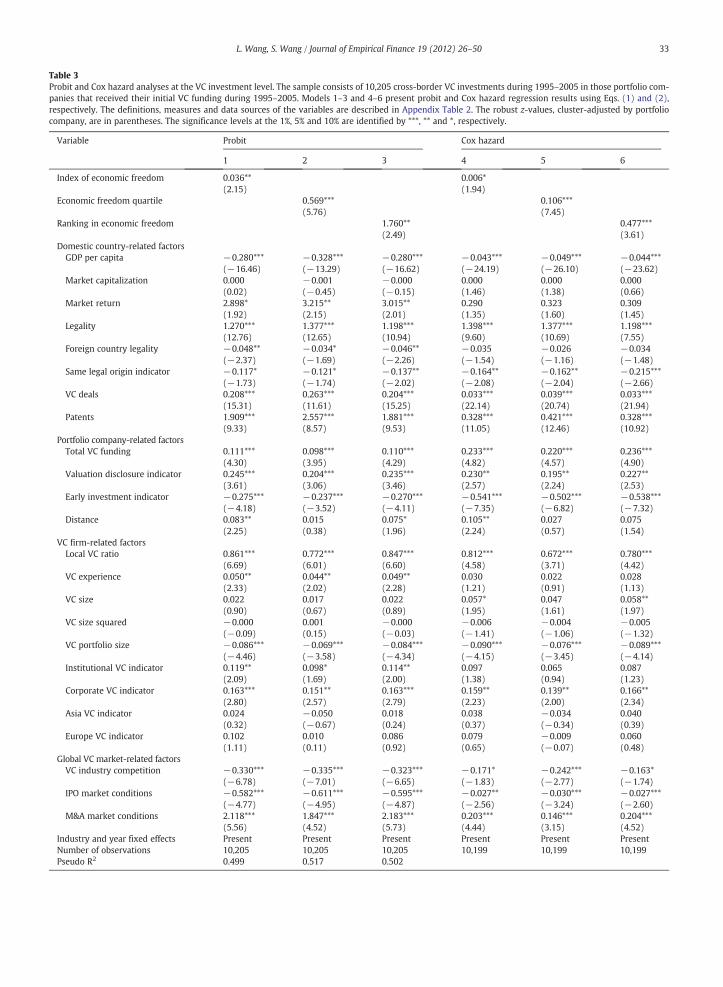

In this section, we investigate the impact of economic freedom on the performance of cross-border VC investments. The unit ofanalysis is VC investment. Our sample consists of 10,205 unique VC firm-portfolio company paired observations. Table 3 reportsthe results. All the z-statistics (in parentheses) are adjusted for heteroskedasticity (White, 1980) and clustered by portfolio com-pany (Petersen, 2009) to account for the correlation among multiple VC investments in the same portfolio company.

We first present the results of the probit analysis in models 1–3 of Table 3 with Investment Success as the dependent variableusing Eq. (1). Our model fits the data well, with a high pseudo R-squared of around 0.5. We find that each of the three explanatoryvariables—Index of Economic Freedom, Economic FreedomQuartile and Ranking in Economic Freedom—has a significant impact, that is,a domestic country's economic freedom has a significant positive effect on Investment Success. The coefficients of Index of Economic

Table 2Summary statistics and univariate analysis. This table presents the statistics of 10,205 cross-border VC investments during 1995–2005 in those portfolio compa-nies that received initial VC funding during 1995–2005. The definitions, measures and data sources of the variables are described in Appendix Table 2. The quar-tiles, means, standard deviations and the number of observations are presented. The results of the univariate analysis are also reported, which are from the t-testsfor equality of the means and Wilcoxon tests for equality of the medians between successful and unsuccessful exits. The significance levels at the 1%, 5% and 10%are identified by ***, ** and *, respectively.

Variable Obs. Mean Std. 0.25 0.5 0.75 Successful exits Unsuccessful exits

Mean Median Mean Median

Investment success 10,205 0.158 0.365 0 0 0Investment duration (days) 10,205 2826 1103 2030 3072 3558Index of economic freedom 10,205 74.073 8.681 70.1 78.57 79.64 76.527*** 78.8*** 73.612 78.57Economic freedom quartile 10,205 2.467 1.119 1 2 3 2.696*** 3*** 2.424 2Ranking in economic freedom 10,205 0.648 0.269 0.514 0.790 0.834 0.758*** 0.829*** 0.627 0.768Domestic country-related factors

GDP per capita (US$) 10,205 33,593 12,397 31,988 36,909 40,815 34,002 36,381*** 33,517 37,280Market capitalization (%) 10,205 116.567 50.325 82.596 127.201 133.97 132*** 135.04*** 113.655 125.81Market return 10,205 0.019 0.031 0.014 0.018 0.023 0.018 0.019 0.019 0.018Legality 10,205 15.424 1.848 15.388 16.445 16.506 16.049*** 16.506*** 15.307 16.097Foreign country legality 10,205 15.688 1.335 15.388 16.076 16.506 15.401*** 15.95*** 15.742 16.097Same legal origin indicator 10,205 0.482 0.500 1 0 0 0.466 0 0.484 0VC deals (per million people) 10,205 8.432 6.012 3.653 9.949 13.018 14.554*** 12.577*** 7.283 5.994Patents (per thousand people) 10,205 0.424 0.301 0.218 0.478 0.486 0.440** 0.484*** 0.421 0.471

Portfolio company-related factorsTotal VC funding (US$mil) 10,205 37.161 77.736 4.840 17.500 46.608 67.017*** 41.058*** 31.556 14.500Valuation disclosure indicator 10,205 0.291 0.454 1 0 0 0.596*** 1*** 0.233 0Early investment indicator 10,205 0.381 0.479 1 0 0 0.313*** 0*** 0.363 0Distance (kilometers) 10,205 7205 4509 3032 7837 10513 8483*** 8409*** 6965 7300

VC firm-related factorsLocal VC ratio 10,205 0.344 0.310 0 0.333 0.615 0.554*** 0.667*** 0.304 0.25VC experience (years) 10,205 13.584 16.963 3 8 18 12.081*** 6*** 13.866 8VC size (US$mil) 10,205 919 2612 0 143 532 628*** 100*** 974 150VC portfolio size 10,205 257.431 895.336 15 44 113 94.53*** 35*** 288.013 48Institutional VC indicator 10,205 0.154 0.361 0 0 0 0.174** 0** 0.150 0Corporate VC indicator 10,205 0.168 0.374 0 0 0 0.234*** 0*** 0.156 0Asia VC indicator 10,205 0.378 0.485 1 0 0 0.524*** 1*** 0.351 0Europe VC indicator 10,205 0.257 0.437 1 0 0 0.262 0 0.256 0

Global VC market-related factorsVC industry competition (US$bil) 10,205 61.840 42.976 20.900 43.908 81.299 60.748* 43.908* 62.044 58.940IPO market conditions 10,205 16.158 9.483 12 13.792 18 23.34*** 16*** 14.809 13.70M&A market conditions 10,205 110.051 11.969 107.52 108.154 112.785 112.25*** 103*** 109.639 108.246

7 Since the summary statistics in Table 2 corresponds to 10,205 VC firm-portfolio company paired observations, the means of Institutional VC Indicator, Corporate VCIndicator, Asia VC Indicator and Europe VC Indicator are slightly different from the distribution of VCs reported in Table 1, which corresponds to 1906 individual VCs.

32 L. Wang, S. Wang / Journal of Empirical Finance 19 (2012) 26–50

Table 3Probit and Cox hazard analyses at the VC investment level. The sample consists of 10,205 cross-border VC investments during 1995–2005 in those portfolio com-panies that received their initial VC funding during 1995–2005. Models 1–3 and 4–6 present probit and Cox hazard regression results using Eqs. (1) and (2),respectively. The definitions, measures and data sources of the variables are described in Appendix Table 2. The robust z-values, cluster-adjusted by portfoliocompany, are in parentheses. The significance levels at the 1%, 5% and 10% are identified by ***, ** and *, respectively.

Variable Probit Cox hazard

1 2 3 4 5 6

Index of economic freedom 0.036**(2.15)

0.006*(1.94)

Economic freedom quartile 0.569***(5.76)

0.106***(7.45)

Ranking in economic freedom 1.760**(2.49)

0.477***(3.61)

Domestic country-related factorsGDP per capita −0.280***

(−16.46)−0.328***(−13.29)

−0.280***(−16.62)

−0.043***(−24.19)

−0.049***(−26.10)

−0.044***(−23.62)

Market capitalization 0.000(0.02)

−0.001(−0.45)

−0.000(−0.15)

0.000(1.46)

0.000(1.38)

0.000(0.66)

Market return 2.898*(1.92)

3.215**(2.15)

3.015**(2.01)

0.290(1.35)

0.323(1.60)

0.309(1.45)

Legality 1.270***(12.76)

1.377***(12.65)

1.198***(10.94)

1.398***(9.60)

1.377***(10.69)

1.198***(7.55)

Foreign country legality −0.048**(−2.37)

−0.034*(−1.69)

−0.046**(−2.26)

−0.035(−1.54)

−0.026(−1.16)

−0.034(−1.48)

Same legal origin indicator −0.117*(−1.73)

−0.121*(−1.74)

−0.137**(−2.02)

−0.164**(−2.08)

−0.162**(−2.04)

−0.215***(−2.66)

VC deals 0.208***(15.31)

0.263***(11.61)

0.204***(15.25)

0.033***(22.14)

0.039***(20.74)

0.033***(21.94)

Patents 1.909***(9.33)

2.557***(8.57)

1.881***(9.53)

0.328***(11.05)

0.421***(12.46)

0.328***(10.92)

Portfolio company-related factorsTotal VC funding 0.111***

(4.30)0.098***(3.95)

0.110***(4.29)

0.233***(4.82)

0.220***(4.57)

0.236***(4.90)

Valuation disclosure indicator 0.245***(3.61)

0.204***(3.06)

0.235***(3.46)

0.230**(2.57)

0.195**(2.24)

0.227**(2.53)

Early investment indicator −0.275***(−4.18)

−0.237***(−3.52)

−0.270***(−4.11)

−0.541***(−7.35)

−0.502***(−6.82)

−0.538***(−7.32)

Distance 0.083**(2.25)

0.015(0.38)

0.075*(1.96)

0.105**(2.24)

0.027(0.57)

0.075(1.54)

VC firm-related factorsLocal VC ratio 0.861***

(6.69)0.772***(6.01)

0.847***(6.60)

0.812***(4.58)

0.672***(3.71)

0.780***(4.42)

VC experience 0.050**(2.33)

0.044**(2.02)

0.049**(2.28)

0.030(1.21)

0.022(0.91)

0.028(1.13)

VC size 0.022(0.90)

0.017(0.67)

0.022(0.89)

0.057*(1.95)

0.047(1.61)

0.058**(1.97)

VC size squared −0.000(−0.09)

0.001(0.15)

−0.000(−0.03)

−0.006(−1.41)

−0.004(−1.06)

−0.005(−1.32)

VC portfolio size −0.086***(−4.46)

−0.069***(−3.58)

−0.084***(−4.34)

−0.090***(−4.15)

−0.076***(−3.45)

−0.089***(−4.14)

Institutional VC indicator 0.119**(2.09)

0.098*(1.69)

0.114**(2.00)

0.097(1.38)

0.065(0.94)

0.087(1.23)

Corporate VC indicator 0.163***(2.80)

0.151**(2.57)

0.163***(2.79)

0.159**(2.23)

0.139**(2.00)

0.166**(2.34)

Asia VC indicator 0.024(0.32)

−0.050(−0.67)

0.018(0.24)

0.038(0.37)

−0.034(−0.34)

0.040(0.39)

Europe VC indicator 0.102(1.11)

0.010(0.11)

0.086(0.92)

0.079(0.65)

−0.009(−0.07)

0.060(0.48)

Global VC market-related factorsVC industry competition −0.330***

(−6.78)−0.335***(−7.01)

−0.323***(−6.65)

−0.171*(−1.83)

−0.242***(−2.77)

−0.163*(−1.74)

IPO market conditions −0.582***(−4.77)

−0.611***(−4.95)

−0.595***(−4.87)

−0.027**(−2.56)

−0.030***(−3.24)

−0.027***(−2.60)

M&A market conditions 2.118***(5.56)

1.847***(4.52)

2.183***(5.73)

0.203***(4.44)

0.146***(3.15)

0.204***(4.52)

Industry and year fixed effects Present Present Present Present Present PresentNumber of observations 10,205 10,205 10,205 10,199 10,199 10,199Pseudo R2 0.499 0.517 0.502

33L. Wang, S. Wang / Journal of Empirical Finance 19 (2012) 26–50

Freedom, Economic Freedom Quartile and Ranking in Economic Freedom are respectively 0.036, 0.569 and 1.760, with the z-statisticsrespectively at the 5%, 1% and 5% significance levels. For the marginal effects, a one standard deviation increase in Index of Econom-ic Freedom, Economic Freedom Quartile or Ranking in Economic Freedom at the mean level increases the likelihood of a successfulexit by 2.02%, 2.76% or 3.02%, respectively.

Some other variables also affect the performance of VC investments, mostly as expected. First, GDP per Capita is negativelyassociated with the likelihood of a successful exit, which is consistent with the well-known convergence hypothesis in the exog-enous growth literature (Barro, 1991, 1996). Market Return is found to be positively associated with the likelihood of a successfulexit, which is consistent with the studies on the impact of stock market performance on IPO volume (Loughran et al., 1994; Lowry,2003). Legality is found to be significantly positively related to VC performance, which is consistent with Armour and Cumming(2006), Cumming et al. (2006) and Cumming andWalz (2010). The higher legality is, the more protected an investor's legal rightsand the higher the likelihood of a successful exit. We also find that the coefficients of Foreign Country Legality and Same LegalOrigin Indicator are typically negative, suggesting that the legal qualities of a domestic country and a foreign country complementeach other. Also, we find a strong positive association between a domestic country's entrepreneurial activity and the likelihood ofa successful exit. The greater the number of VC deals or patents granted in a domestic country, the higher the likelihood of a suc-cessful exit. However, the relationship between a domestic country's stock market capitalization and the likelihood of a successfulexit is typically insignificant, which is inconsistent with the findings of Black and Gilson (1998) and Cumming (2008), but con-sistent with those of Cumming et al. (2006), who show that a country's stock market capitalization has no significant impacton exit choices in 12 Asia-Pacific countries.

Second, our results on the coefficients of portfolio company-related factors are quite consistent with our expectations. Total VCFunding and Valuation Disclosure Indicator positively affect cross-border VC performance at the 1% significance level. The better thequality of a portfolio company, the larger the VC investment amount, the higher the likelihood of a voluntary disclosure of post-investment valuation, and the higher the likelihood of a successful exit. Also, Early Stage Indicator is found to be strongly negatively as-sociatedwith the likelihood of a successful exit at the 1% significance level. Unexpectedly, the variableDistance is found to be positivelyassociated with the likelihood of a successful exit, but at a low significance level. In later estimations, we generally find insignificantresults on Distance at the portfolio company level. Later in Section 5.2, after a robustness check of the exit choices between an IPOand an acquisition, we further find a different role of Distance in exits through IPOs than in exits through acquisitions. 8

Third, Local VC Ratio is positively related to the likelihood of a successful exit at the 1% significance level. This is consistent withthe value-added view of domestic investors on cross-border VC investments (Dai et al., 2010; Mäkelä and Maula, 2008; Tykvováand Schertler, 2011). VC Experience is found to be positively related to the likelihood of a successful exit at the 5% significancelevel, which is consistent with the findings for the U.S. domestic market, such as those by Sorensen (2007), Gompers et al.(2008) and Nahata (2008). We find a significantly negative relationship between VC Portfolio Size and the likelihood of a successfulexit, which is quite consistent with the findings of Kanniainen and Keuschnigg (2003, 2004) and Cumming (2006). Also, InstitutionalVC Indicator and Corporate VC Indicator have positive effects on Investment Success, due possibly to the value-added services offered byVCs toportfolio companies. As shown, there is no statistically significant associationbetweenVC SizeorVC Size Squared and the likelihoodof a successful exit. Also, neither Asia VC Indicator nor Europe VC Indicator has a significant effect on the likelihood of a successful exit.

Fourth, the global VC market-related factor VC Industry Competition is negatively associated with Investment Success at the 1%significance level. The greater the worldwide inflow of VC funds, the more severe VC competition is in the international marketand the less likely it is for a successful exit to occur. However, the global market conditions affect the likelihood of a successfulexit in different ways. Specifically, IPO Market Conditions is negatively related to the probability of a successful exit, contrary toour expectations. M&A Market Conditions is positively related to the probability of a successful exit at the 1% significance level,consistent with our expectations. Later in Section 5.2, after a robustness check of the exit choices between an IPO and an M&A,we find that the negative coefficient of IPO Market Conditions arises from its other role in the choice between an IPO and an M&A.

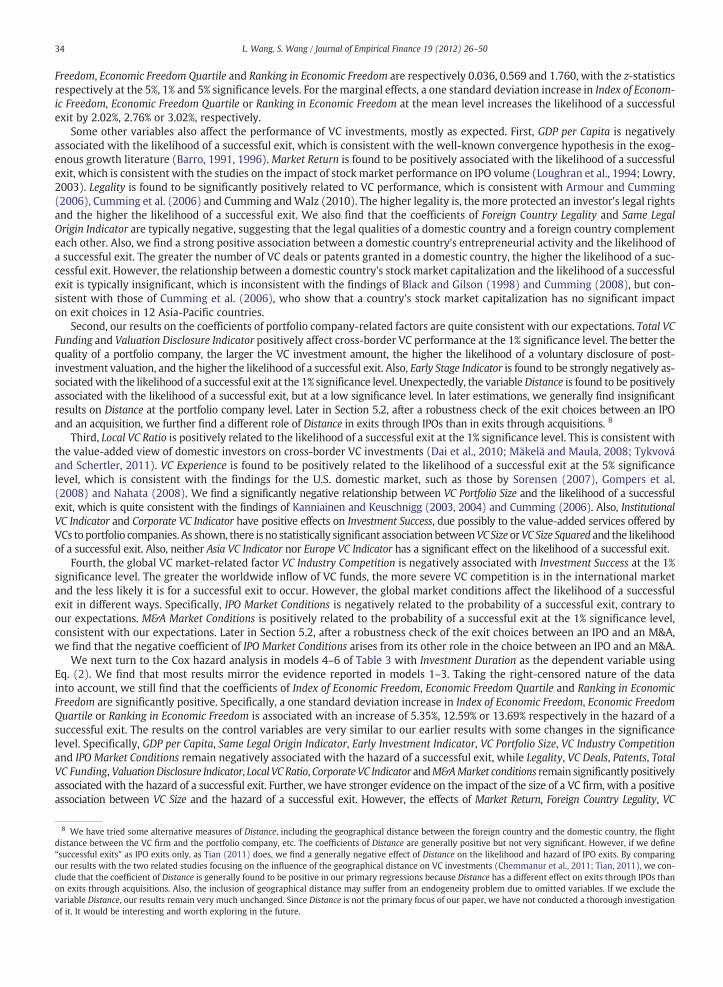

We next turn to the Cox hazard analysis in models 4–6 of Table 3 with Investment Duration as the dependent variable usingEq. (2). We find that most results mirror the evidence reported in models 1–3. Taking the right-censored nature of the datainto account, we still find that the coefficients of Index of Economic Freedom, Economic Freedom Quartile and Ranking in EconomicFreedom are significantly positive. Specifically, a one standard deviation increase in Index of Economic Freedom, Economic FreedomQuartile or Ranking in Economic Freedom is associated with an increase of 5.35%, 12.59% or 13.69% respectively in the hazard of asuccessful exit. The results on the control variables are very similar to our earlier results with some changes in the significancelevel. Specifically, GDP per Capita, Same Legal Origin Indicator, Early Investment Indicator, VC Portfolio Size, VC Industry Competitionand IPO Market Conditions remain negatively associated with the hazard of a successful exit, while Legality, VC Deals, Patents, TotalVC Funding, ValuationDisclosure Indicator, Local VC Ratio,Corporate VC Indicator andM&AMarket conditions remain significantly positivelyassociated with the hazard of a successful exit. Further, we have stronger evidence on the impact of the size of a VC firm, with a positiveassociation between VC Size and the hazard of a successful exit. However, the effects of Market Return, Foreign Country Legality, VC

8 We have tried some alternative measures of Distance, including the geographical distance between the foreign country and the domestic country, the flightdistance between the VC firm and the portfolio company, etc. The coefficients of Distance are generally positive but not very significant. However, if we define“successful exits” as IPO exits only, as Tian (2011) does, we find a generally negative effect of Distance on the likelihood and hazard of IPO exits. By comparingour results with the two related studies focusing on the influence of the geographical distance on VC investments (Chemmanur et al., 2011; Tian, 2011), we con-clude that the coefficient of Distance is generally found to be positive in our primary regressions because Distance has a different effect on exits through IPOs thanon exits through acquisitions. Also, the inclusion of geographical distance may suffer from an endogeneity problem due to omitted variables. If we exclude thevariable Distance, our results remain very much unchanged. Since Distance is not the primary focus of our paper, we have not conducted a thorough investigationof it. It would be interesting and worth exploring in the future.

34 L. Wang, S. Wang / Journal of Empirical Finance 19 (2012) 26–50

Experience and Institutional VC Indicator on the hazard of a successful exit aremuchweaker comparedwith our earlier estimations. Othervariables, such asMarket Capitalization, VC Size Squared, Asia VC Indicator and Europe VC Indicator, remain insignificant as before.

4. Analysis at the portfolio company level

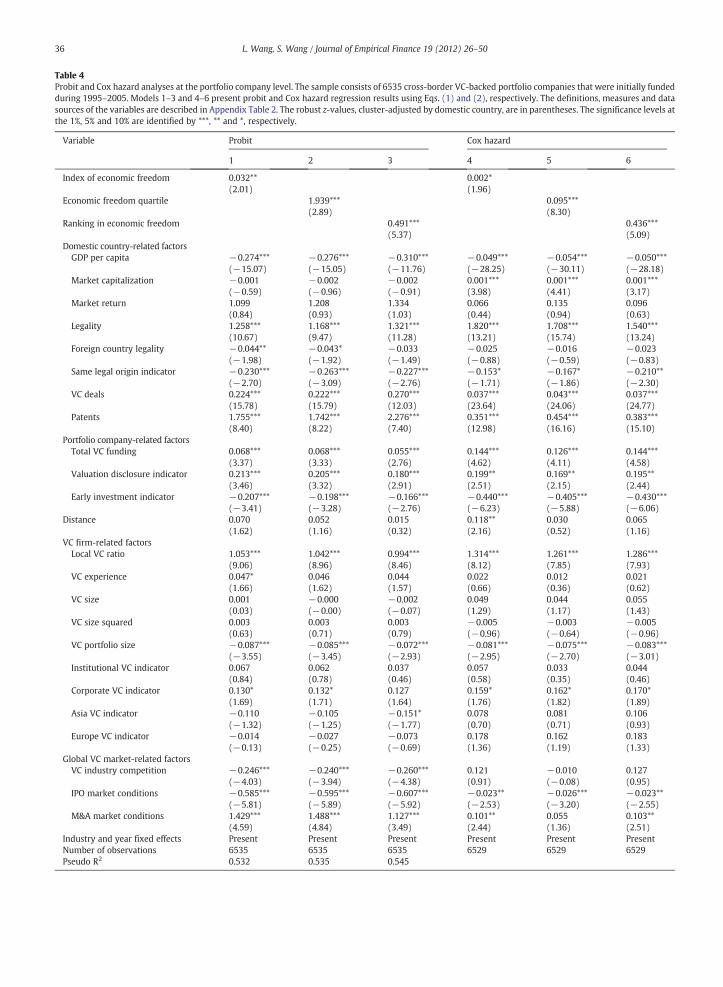

In this section,we conduct a performance analysis at the portfolio company level using the probitmodel and the Cox hazardmodelin Eqs. (1) and (2). The unit of analysis is portfolio company, with one observation for each portfolio company. The sample size is6535. Table 4 reports the results. All the z-statistics (in parentheses) are adjusted for heteroskedasticity (White, 1980) and clusteredby domestic country (Petersen, 2009) to account for correlation among multiple VC investments in the same portfolio company.

Models 1–3 in Table 4 report the results of our probit analysis of portfolio companies with Investment Success as the dependentvariable using Eq. (1). Our model fits the data well, with a high pseudo R-squared of greater than 0.53. The results on a domesticcountry's economic freedom are consistent with the earlier results on VC investments. In particular, a one standard deviation in-crease in Index of Economic Freedom, Economic Freedom Quartile or Ranking in Economic Freedom at the mean raises the probabilityof a successful exit by 1.38%, 10.06% or 4.72%, respectively.

The impact of the control variables on Investment Success is largely the same as that implied by the results in Table 3. We findsignificantly positive impacts from Legality, VC Deals, Patents, Total VC Funding, Valuation Disclosure Indicator, Local VC Ratio, Cor-porate VC Indicator and M&A Market Conditions, and significantly negative impacts from GDP per Capita, Foreign Country Legality,Same Legal Origin Indicator, Early Investment Indicator, VC Portfolio Size, VC Industry Competition and IPO Market Conditions. Othercontrol variables are generally insignificantly associated with Investment Success.

Models 4–6 in Table 4 report the results of our Cox hazard analysis of portfolio companies with Investment Duration as the de-pendent variable using Eq. (2). As in the previous section, a domestic country's economic freedom continues to be a good predic-tor of Investment Duration with a large marginal effect. Specifically, a one standard deviation increase in Index of EconomicFreedom, Economic Freedom Quartile or Ranking in Economic Freedom is associated with an increase of 1.73%, 10.96% or 12.33%respectively in the hazard of a successful exit. Taking the right-censored nature of the data into account, we further find thatLegality, VC Deals, Patents, Total VC Funding, Valuation Disclosure Indicator, Local VC Ratio, Corporate VC Indicator and M&A MarketConditions reduce Investment Duration and hence increase the hazard of a successful exit, while GDP per Capita, Same Legal OriginIndicator, Early Investment Indicator and VC Portfolio Size increase Investment Duration and hence decrease the hazard of a success-ful exit. Other control variables are generally insignificantly associated with the hazard of a successful exit.

In summary, the results of our analyses of VC investments and portfolio companies in Tables 3 and 4 indicate that the degree ofa domestic country's economic freedom is positively related to cross-border VC performance after controlling for other relatedfactors of domestic countries, portfolio companies, VCs and the global VCmarket, aswell as year and industry fixed effects. In addition,we provide interesting evidence on many level factors of domestic countries, portfolio companies, VCs and the global VC market thataffect cross-border VC performance. This is consistentwith existing studies on factors such as a domestic country's economic develop-ment, legal quality, entrepreneurial activity, portfolio company quality, local VCs' participation and VCs' portfolio size.

Our findings have policy implications for VC imports. One key implication is that a high degree of freedom is essential for suc-cessful investments in a country, especially for foreign investments.

5. Robustness checks

In the above analyses, a domestic country's economic freedom has emerged as a consistent predictor of cross-border VC per-formance. In this section, we conduct many robustness tests, other than those mentioned in prior sections, to ensure reliability ofour results. To save space, we report a selection of results only. Details of our other tests are available upon request.

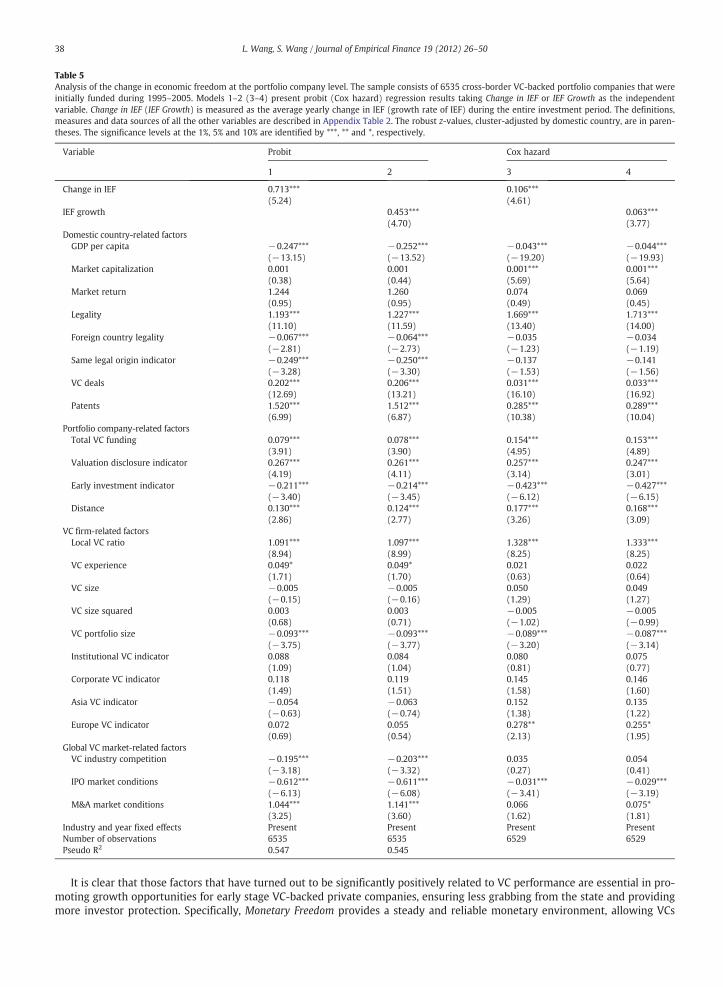

5.1. Change in economic freedom

Up to now, we have applied a level model to investigate the impact of a domestic country's economic freedom on cross-borderVC performance. In other words, we have only focused on the cross-sectional difference. In this section, we provide further evi-dence on effects of a change in economic freedom to strengthen our findings. This exercise may mitigate the influence of missingfactors and self-selection concerns. We define two variables, Change in IEF and IEF Growth (%), to measure a change in economicfreedom, which are calculated in a similar way to the three primary independent variables, Index of Economic Freedom, EconomicFreedom Quartile and Ranking in Economic Freedom. Specifically, Change in IEF measures the average yearly change in IEF, and IEFGrowthmeasures the average yearly growth rate of IEF over the entire investment period. The means (and standard deviations) ofChange in IEF and IEF Growth (%) at the portfolio company level are respectively 0.233 (and 0.436) and 0.339 (and 0.628), whichare quite similar to those at the VC investments level.9 These statistics are consistent with our expectation that economic freedomtends to be persistent and does not change dramatically over our sample period.

9 Since IEF is only available before 1995, we assume that IEF in 1994 is the same as that in 1995. Hence, the change in IEF and the change in growth rate of IEF in1995 are both set to zero.

35L. Wang, S. Wang / Journal of Empirical Finance 19 (2012) 26–50

Table 4Probit and Cox hazard analyses at the portfolio company level. The sample consists of 6535 cross-border VC-backed portfolio companies that were initially fundedduring 1995–2005. Models 1–3 and 4–6 present probit and Cox hazard regression results using Eqs. (1) and (2), respectively. The definitions, measures and datasources of the variables are described in Appendix Table 2. The robust z-values, cluster-adjusted by domestic country, are in parentheses. The significance levels atthe 1%, 5% and 10% are identified by ***, ** and *, respectively.

Variable Probit Cox hazard

1 2 3 4 5 6

Index of economic freedom 0.032**(2.01)

0.002*(1.96)

Economic freedom quartile 1.939***(2.89)

0.095***(8.30)

Ranking in economic freedom 0.491***(5.37)

0.436***(5.09)

Domestic country-related factorsGDP per capita −0.274***

(−15.07)−0.276***(−15.05)

−0.310***(−11.76)

−0.049***(−28.25)

−0.054***(−30.11)

−0.050***(−28.18)

Market capitalization −0.001(−0.59)

−0.002(−0.96)

−0.002(−0.91)

0.001***(3.98)

0.001***(4.41)

0.001***(3.17)

Market return 1.099(0.84)

1.208(0.93)

1.334(1.03)

0.066(0.44)

0.135(0.94)

0.096(0.63)

Legality 1.258***(10.67)

1.168***(9.47)

1.321***(11.28)

1.820***(13.21)

1.708***(15.74)

1.540***(13.24)

Foreign country legality −0.044**(−1.98)

−0.043*(−1.92)

−0.033(−1.49)

−0.025(−0.88)

−0.016(−0.59)

−0.023(−0.83)

Same legal origin indicator −0.230***(−2.70)

−0.263***(−3.09)

−0.227***(−2.76)

−0.153*(−1.71)

−0.167*(−1.86)

−0.210**(−2.30)

VC deals 0.224***(15.78)

0.222***(15.79)

0.270***(12.03)

0.037***(23.64)

0.043***(24.06)

0.037***(24.77)

Patents 1.755***(8.40)

1.742***(8.22)

2.276***(7.40)

0.351***(12.98)

0.454***(16.16)

0.383***(15.10)

Portfolio company-related factorsTotal VC funding 0.068***

(3.37)0.068***(3.33)

0.055***(2.76)

0.144***(4.62)

0.126***(4.11)

0.144***(4.58)

Valuation disclosure indicator 0.213***(3.46)

0.205***(3.32)

0.180***(2.91)

0.199**(2.51)

0.169**(2.15)

0.195**(2.44)

Early investment indicator −0.207***(−3.41)

−0.198***(−3.28)

−0.166***(−2.76)

−0.440***(−6.23)

−0.405***(−5.88)

−0.430***(−6.06)

Distance 0.070(1.62)

0.052(1.16)

0.015(0.32)

0.118**(2.16)

0.030(0.52)

0.065(1.16)

VC firm-related factorsLocal VC ratio 1.053***

(9.06)1.042***(8.96)

0.994***(8.46)

1.314***(8.12)

1.261***(7.85)

1.286***(7.93)

VC experience 0.047*(1.66)

0.046(1.62)

0.044(1.57)

0.022(0.66)

0.012(0.36)

0.021(0.62)

VC size 0.001(0.03)

−0.000(−0.00)

−0.002(−0.07)

0.049(1.29)

0.044(1.17)

0.055(1.43)

VC size squared 0.003(0.63)

0.003(0.71)

0.003(0.79)

−0.005(−0.96)

−0.003(−0.64)

−0.005(−0.96)

VC portfolio size −0.087***(−3.55)

−0.085***(−3.45)

−0.072***(−2.93)

−0.081***(−2.95)

−0.075***(−2.70)

−0.083***(−3.01)

Institutional VC indicator 0.067(0.84)

0.062(0.78)

0.037(0.46)

0.057(0.58)

0.033(0.35)

0.044(0.46)

Corporate VC indicator 0.130*(1.69)

0.132*(1.71)

0.127(1.64)

0.159*(1.76)

0.162*(1.82)

0.170*(1.89)

Asia VC indicator −0.110(−1.32)

−0.105(−1.25)

−0.151*(−1.77)

0.078(0.70)

0.081(0.71)

0.106(0.93)

Europe VC indicator −0.014(−0.13)

−0.027(−0.25)

−0.073(−0.69)

0.178(1.36)

0.162(1.19)

0.183(1.33)

Global VC market-related factorsVC industry competition −0.246***

(−4.03)−0.240***(−3.94)

−0.260***(−4.38)

0.121(0.91)

−0.010(−0.08)

0.127(0.95)

IPO market conditions −0.585***(−5.81)

−0.595***(−5.89)

−0.607***(−5.92)

−0.023**(−2.53)

−0.026***(−3.20)

−0.023**(−2.55)

M&A market conditions 1.429***(4.59)

1.488***(4.84)

1.127***(3.49)

0.101**(2.44)

0.055(1.36)

0.103**(2.51)

Industry and year fixed effects Present Present Present Present Present PresentNumber of observations 6535 6535 6535 6529 6529 6529Pseudo R2 0.532 0.535 0.545

36 L. Wang, S. Wang / Journal of Empirical Finance 19 (2012) 26–50

Table 5 reports the probit and Cox hazard analyses at the portfolio company level as in Table 4 but taking Change in IEF orIEF Growth as the explanatory variable. We find positive coefficients on Change in IEF and IEF Growth in all the models with thez-statistics at the 1% significance level. For the marginal effects, a one standard deviation increase in Change in IEF or IEFGrowth at the mean level increases the likelihood of a successful exit by 1.58% or 1.45%, respectively. Also, a one standarddeviation increase in Change in IEF or IEF Growth is associated with an increase of 4.71% or 4.01% respectively in the hazardof a successful exit. These findings further strengthen our argument that economic freedom plays a vital role in cross-border VCsuccess.

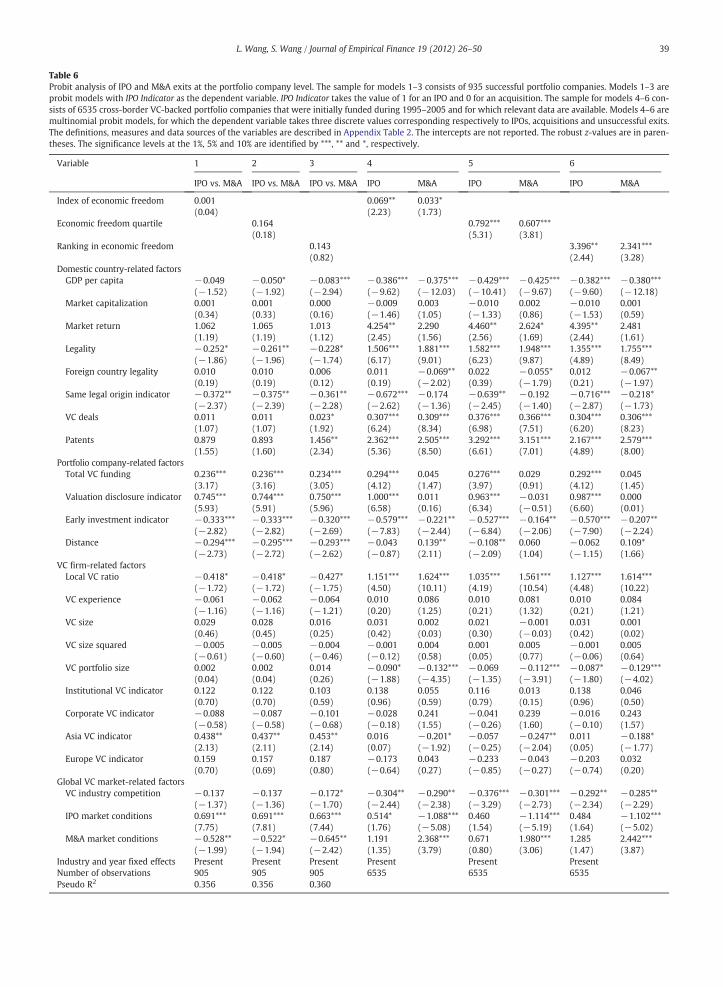

5.2. IPOs versus acquisitions

In this section, we focus on the choice of exit between an IPO and an acquisition. IPOs and acquisitions are the two primarymethods by which privately-held firms can become public companies. Existing studies that focus on exit choices of entrepreneursand VCs include those of Brau et al. (2003), Cumming et al. (2006), Poulsen and Stegemoller (2008) and Bayar and Chemmanur(forthcoming). Using a much larger set of sample data that includes many more countries, we provide further empirical analysesof the determinants of whether to exit through an IPO or an acquisition.

For brevity, we report only the probit results on portfolio companies in Table 6. In models 1–3, we focus on the subsample con-sisting of successful portfolio companies only and analyze whether a domestic country's economic freedom has any impact on thechoice of exit between an IPO and an acquisition. The dependent variable is a dummy variable indicating whether a VC-backedportfolio company had gone public by the end of 2009. The number of observations in the subsample is 935. As shown, economicfreedom has no significant impact on the choice between an IPO and an acquisition. The coefficients of Index of Economic Freedom,Economic Freedom Quartile and Ranking in Economic Freedom are respectively 0.001, 0.164 and 0.143 with z-statistics 0.04, 0.18and 0.82. In other words, a domestic country's economic freedom has an almost equal influence on the decision to exit throughan IPO and the decision to exit through an acquisition.

In addition, the results on someof the other variables are interesting.We find that Total VC Funding,ValuationDisclosure Indicator,AsiaVC Indicator and IPO Market Conditions have a significantly positive impact on the choice between an IPO and an acquisition, while GDPper Capita, Legality, Same Legal Origin Indicator, Early Investment Indicator,Distance, Local VC Ratio andM&AMarket Conditions have a sig-nificantly negative impact. Most of these results make sense. One result that requires an explanation is the negative impact of Legality.Cumming et al. (2006) claim that Legality is positively related to the decision to exit through an IPO andnegatively related to the decisionto exit through a private exit. It seems that we have an opposite result. However, their sample is much smaller and covers only 12 Asia-Pacific countries. Further, the choice of “private exits” in their study includes acquisitions, secondary sales and buybacks. In contrast, wefocus on two successful exit routes only, namely IPOs and acquisitions, since our attention is on VC performance.

As a further robustness check, we have also investigated the likelihood of a portfolio company exiting through one of thethree major exit routes—IPOs, acquisitions and liquidations—in a multinomial probit model using the full sample. The depen-dent variable takes three discrete values corresponding to IPOs, acquisitions and liquidations. The results from models 4–6are consistent with those from models 1–3. We see a similar impact of economic freedom on the decision to exit through anIPO and the decision to exit through an acquisition. Specifically, the coefficients of Index of Economic Freedom (or Economic FreedomQuartile, or Ranking in Economic Freedom) are respectively 0.069 (or 0.792, or 3.396) and 0.033 (or 0.607, or 2.341) with z-statistics2.23 (or 5.31, or 2.44) and 1.73 (or 3.81, or 3.28) for exiting through IPOs and through acquisitions respectively. In addition, wesee a different role of IPO Market Conditions and Distance in the two exit choices. Specifically, IPO Market Conditions (Distance) is pos-itively (negatively) associated with exits through IPOs and negatively (positively) associated with exits through acquisitions,which may explain the negative (positive) and sometimes insignificant coefficients of IPO Market Conditions (Distance) inTables 3 and 4.

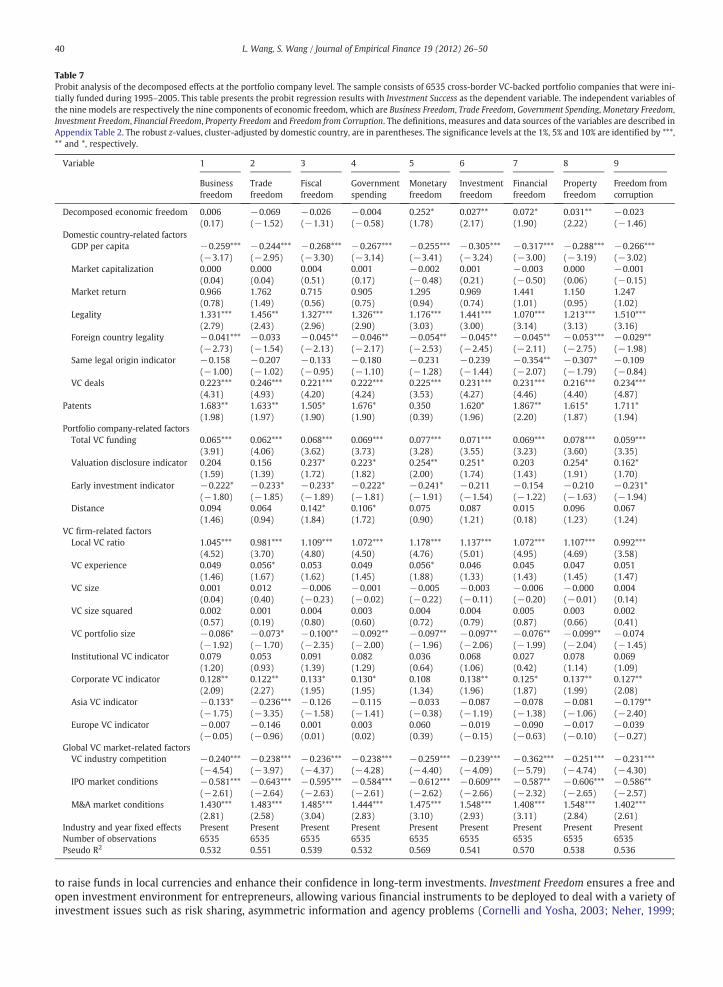

5.3. Decomposing the effects of economic freedom

We have provided evidence that economic freedom has a positive impact on cross-border VC performance. However, our anal-ysis is so far based on an integrated index of economic freedom (IEF). One drawback is that a single measure may not be able toproperly represent a complex economic environment, and a highly aggregated index makes it difficult to draw policy conclusions.In this section, we investigate the effects of the individual components of the IEF on cross-border VC performance.

The IEF consists of 10 different components—business freedom, trade freedom, fiscal freedom, government spending, mone-tary freedom, investment freedom, financial freedom, property freedom, freedom from corruption and labor freedom. A briefdescription of each component is presented in Appendix Table 1. Since labor freedom only became available after 2005, wefocus on the other nine components in this section. We define the nine variables in the same way as we did for Index of EconomicFreedom—by taking the average of the raw values of each variable over the investment period.

Table 7 reports the probit analysis of the decomposed economic freedom effects at the portfolio company level. The results ofthe Cox hazard analysis are quite similar. Not every component of the IEF has a positive impact on cross-border VC performance.Specifically, Trade Freedom, Fiscal Freedom, Government Spending and Freedom from Corruption are negatively but insignificantlyassociated with cross-border VC performance. Monetary Freedom, Investment Freedom, Financial Freedom and Property Freedomare significantly positively associated with cross-border VC performance, while Business Freedom is positively but insignificantlyassociated with cross-border VC performance.

37L. Wang, S. Wang / Journal of Empirical Finance 19 (2012) 26–50

It is clear that those factors that have turned out to be significantly positively related to VC performance are essential in pro-moting growth opportunities for early stage VC-backed private companies, ensuring less grabbing from the state and providingmore investor protection. Specifically, Monetary Freedom provides a steady and reliable monetary environment, allowing VCs

Table 5Analysis of the change in economic freedom at the portfolio company level. The sample consists of 6535 cross-border VC-backed portfolio companies that wereinitially funded during 1995–2005. Models 1–2 (3–4) present probit (Cox hazard) regression results taking Change in IEF or IEF Growth as the independentvariable. Change in IEF (IEF Growth) is measured as the average yearly change in IEF (growth rate of IEF) during the entire investment period. The definitions,measures and data sources of all the other variables are described in Appendix Table 2. The robust z-values, cluster-adjusted by domestic country, are in paren-theses. The significance levels at the 1%, 5% and 10% are identified by ***, ** and *, respectively.

Variable Probit Cox hazard

1 2 3 4

Change in IEF 0.713***(5.24)

0.106***(4.61)

IEF growth 0.453***(4.70)

0.063***(3.77)

Domestic country-related factorsGDP per capita −0.247***

(−13.15)−0.252***(−13.52)

−0.043***(−19.20)

−0.044***(−19.93)

Market capitalization 0.001(0.38)

0.001(0.44)

0.001***(5.69)

0.001***(5.64)

Market return 1.244(0.95)

1.260(0.95)

0.074(0.49)

0.069(0.45)

Legality 1.193***(11.10)

1.227***(11.59)

1.669***(13.40)

1.713***(14.00)

Foreign country legality −0.067***(−2.81)

−0.064***(−2.73)

−0.035(−1.23)

−0.034(−1.19)

Same legal origin indicator −0.249***(−3.28)

−0.250***(−3.30)

−0.137(−1.53)

−0.141(−1.56)

VC deals 0.202***(12.69)

0.206***(13.21)

0.031***(16.10)

0.033***(16.92)

Patents 1.520***(6.99)

1.512***(6.87)

0.285***(10.38)

0.289***(10.04)

Portfolio company-related factorsTotal VC funding 0.079***

(3.91)0.078***(3.90)

0.154***(4.95)

0.153***(4.89)

Valuation disclosure indicator 0.267***(4.19)

0.261***(4.11)

0.257***(3.14)

0.247***(3.01)

Early investment indicator −0.211***(−3.40)

−0.214***(−3.45)

−0.423***(−6.12)

−0.427***(−6.15)

Distance 0.130***(2.86)

0.124***(2.77)

0.177***(3.26)

0.168***(3.09)

VC firm-related factorsLocal VC ratio 1.091***

(8.94)1.097***(8.99)

1.328***(8.25)

1.333***(8.25)

VC experience 0.049*(1.71)

0.049*(1.70)

0.021(0.63)

0.022(0.64)

VC size −0.005(−0.15)

−0.005(−0.16)

0.050(1.29)

0.049(1.27)

VC size squared 0.003(0.68)

0.003(0.71)

−0.005(−1.02)

−0.005(−0.99)

VC portfolio size −0.093***(−3.75)

−0.093***(−3.77)

−0.089***(−3.20)

−0.087***(−3.14)

Institutional VC indicator 0.088(1.09)

0.084(1.04)

0.080(0.81)

0.075(0.77)

Corporate VC indicator 0.118(1.49)

0.119(1.51)

0.145(1.58)

0.146(1.60)

Asia VC indicator −0.054(−0.63)

−0.063(−0.74)

0.152(1.38)

0.135(1.22)

Europe VC indicator 0.072(0.69)

0.055(0.54)

0.278**(2.13)

0.255*(1.95)

Global VC market-related factorsVC industry competition −0.195***

(−3.18)−0.203***(−3.32)

0.035(0.27)

0.054(0.41)

IPO market conditions −0.612***(−6.13)

−0.611***(−6.08)

−0.031***(−3.41)

−0.029***(−3.19)

M&A market conditions 1.044***(3.25)

1.141***(3.60)

0.066(1.62)

0.075*(1.81)

Industry and year fixed effects Present Present Present PresentNumber of observations 6535 6535 6529 6529Pseudo R2 0.547 0.545

38 L. Wang, S. Wang / Journal of Empirical Finance 19 (2012) 26–50

Table 6Probit analysis of IPO and M&A exits at the portfolio company level. The sample for models 1–3 consists of 935 successful portfolio companies. Models 1–3 areprobit models with IPO Indicator as the dependent variable. IPO Indicator takes the value of 1 for an IPO and 0 for an acquisition. The sample for models 4–6 con-sists of 6535 cross-border VC-backed portfolio companies that were initially funded during 1995–2005 and for which relevant data are available. Models 4–6 aremultinomial probit models, for which the dependent variable takes three discrete values corresponding respectively to IPOs, acquisitions and unsuccessful exits.The definitions, measures and data sources of the variables are described in Appendix Table 2. The intercepts are not reported. The robust z-values are in paren-theses. The significance levels at the 1%, 5% and 10% are identified by ***, ** and *, respectively.

Variable 1 2 3 4 5 6

IPO vs. M&A IPO vs. M&A IPO vs. M&A IPO M&A IPO M&A IPO M&A

Index of economic freedom 0.001(0.04)

0.069**(2.23)

0.033*(1.73)

Economic freedom quartile 0.164(0.18)

0.792***(5.31)

0.607***(3.81)

Ranking in economic freedom 0.143(0.82)

3.396**(2.44)

2.341***(3.28)

Domestic country-related factorsGDP per capita −0.049

(−1.52)−0.050*(−1.92)

−0.083***(−2.94)

−0.386***(−9.62)

−0.375***(−12.03)

−0.429***(−10.41)

−0.425***(−9.67)

−0.382***(−9.60)

−0.380***(−12.18)

Market capitalization 0.001(0.34)

0.001(0.33)

0.000(0.16)

−0.009(−1.46)

0.003(1.05)

−0.010(−1.33)

0.002(0.86)

−0.010(−1.53)

0.001(0.59)

Market return 1.062(1.19)

1.065(1.19)

1.013(1.12)

4.254**(2.45)

2.290(1.56)

4.460**(2.56)

2.624*(1.69)

4.395**(2.44)

2.481(1.61)

Legality −0.252*(−1.86)

−0.261**(−1.96)

−0.228*(−1.74)

1.506***(6.17)

1.881***(9.01)

1.582***(6.23)

1.948***(9.87)

1.355***(4.89)

1.755***(8.49)

Foreign country legality 0.010(0.19)

0.010(0.19)

0.006(0.12)

0.011(0.19)

−0.069**(−2.02)

0.022(0.39)

−0.055*(−1.79)

0.012(0.21)

−0.067**(−1.97)

Same legal origin indicator −0.372**(−2.37)

−0.375**(−2.39)

−0.361**(−2.28)

−0.672***(−2.62)

−0.174(−1.36)

−0.639**(−2.45)

−0.192(−1.40)

−0.716***(−2.87)

−0.218*(−1.73)

VC deals 0.011(1.07)

0.011(1.07)

0.023*(1.92)

0.307***(6.24)

0.309***(8.34)

0.376***(6.98)

0.366***(7.51)

0.304***(6.20)

0.306***(8.23)

Patents 0.879(1.55)

0.893(1.60)

1.456**(2.34)

2.362***(5.36)

2.505***(8.50)

3.292***(6.61)

3.151***(7.01)

2.167***(4.89)

2.579***(8.00)

Portfolio company-related factorsTotal VC funding 0.236***

(3.17)0.236***(3.16)

0.234***(3.05)

0.294***(4.12)

0.045(1.47)

0.276***(3.97)

0.029(0.91)

0.292***(4.12)

0.045(1.45)

Valuation disclosure indicator 0.745***(5.93)

0.744***(5.91)

0.750***(5.96)

1.000***(6.58)

0.011(0.16)

0.963***(6.34)

−0.031(−0.51)

0.987***(6.60)

0.000(0.01)

Early investment indicator −0.333***(−2.82)

−0.333***(−2.82)

−0.320***(−2.69)

−0.579***(−7.83)

−0.221**(−2.44)

−0.527***(−6.84)

−0.164**(−2.06)

−0.570***(−7.90)

−0.207**(−2.24)

Distance −0.294***(−2.73)

−0.295***(−2.72)

−0.293***(−2.62)

−0.043(−0.87)

0.139**(2.11)

−0.108**(−2.09)

0.060(1.04)

−0.062(−1.15)

0.109*(1.66)

VC firm-related factorsLocal VC ratio −0.418*

(−1.72)−0.418*(−1.72)

−0.427*(−1.75)

1.151***(4.50)

1.624***(10.11)

1.035***(4.19)

1.561***(10.54)

1.127***(4.48)

1.614***(10.22)

VC experience −0.061(−1.16)

−0.062(−1.16)

−0.064(−1.21)

0.010(0.20)

0.086(1.25)

0.010(0.21)

0.081(1.32)

0.010(0.21)

0.084(1.21)

VC size 0.029(0.46)

0.028(0.45)

0.016(0.25)

0.031(0.42)

0.002(0.03)

0.021(0.30)

−0.001(−0.03)

0.031(0.42)

0.001(0.02)

VC size squared −0.005(−0.61)

−0.005(−0.60)

−0.004(−0.46)

−0.001(−0.12)

0.004(0.58)

0.001(0.05)

0.005(0.77)

−0.001(−0.06)

0.005(0.64)

VC portfolio size 0.002(0.04)

0.002(0.04)

0.014(0.26)

−0.090*(−1.88)

−0.132***(−4.35)

−0.069(−1.35)

−0.112***(−3.91)

−0.087*(−1.80)

−0.129***(−4.02)

Institutional VC indicator 0.122(0.70)

0.122(0.70)

0.103(0.59)

0.138(0.96)

0.055(0.59)

0.116(0.79)

0.013(0.15)

0.138(0.96)

0.046(0.50)

Corporate VC indicator −0.088(−0.58)

−0.087(−0.58)

−0.101(−0.68)

−0.028(−0.18)

0.241(1.55)

−0.041(−0.26)

0.239(1.60)

−0.016(−0.10)

0.243(1.57)

Asia VC indicator 0.438**(2.13)

0.437**(2.11)

0.453**(2.14)

0.016(0.07)

−0.201*(−1.92)

−0.057(−0.25)

−0.247**(−2.04)

0.011(0.05)

−0.188*(−1.77)

Europe VC indicator 0.159(0.70)

0.157(0.69)

0.187(0.80)

−0.173(−0.64)

0.043(0.27)

−0.233(−0.85)

−0.043(−0.27)

−0.203(−0.74)

0.032(0.20)

Global VC market-related factorsVC industry competition −0.137

(−1.37)−0.137(−1.36)

−0.172*(−1.70)

−0.304**(−2.44)

−0.290**(−2.38)

−0.376***(−3.29)

−0.301***(−2.73)

−0.292**(−2.34)

−0.285**(−2.29)

IPO market conditions 0.691***(7.75)

0.691***(7.81)

0.663***(7.44)

0.514*(1.76)

−1.088***(−5.08)

0.460(1.54)

−1.114***(−5.19)

0.484(1.64)

−1.102***(−5.02)

M&A market conditions −0.528**(−1.99)

−0.522*(−1.94)

−0.645**(−2.42)

1.191(1.35)

2.368***(3.79)

0.671(0.80)

1.980***(3.06)

1.285(1.47)

2.442***(3.87)

Industry and year fixed effects Present Present Present Present Present PresentNumber of observations 905 905 905 6535 6535 6535Pseudo R2 0.356 0.356 0.360

39L. Wang, S. Wang / Journal of Empirical Finance 19 (2012) 26–50