Embed Size (px)

Citation preview

Introduction

This should be quite short (less than 10% of your word count), introduce the

topic this means say why you are looking at your chosen firm and explain why

strategy is important. You should then briefly outline the structure of the rest

of the essay, e.g. “during the second section of the work, a five forces of the

car industry will be presented..........”

Industry analysis

I would recommend that you conduct a Five Forces/ or a PESTEL analysis of

the industry that your chosen firm operates in. Try and provide some data (e.g.

concentration ratio, profits etc.). You then need to explain which of the five

forces in the most important in terms of shaping changes in the industry.

http://www.quickmba.com/strategy/porter.shtml

http://wiki.mbalib.com/wiki/%E6%B3%A2%E7%89%B9%E4%BA%94%E5%8A%9B%E5%88%86%E6%9E%90%E6%A8%A1%E5%9E%8B

Firm Analysis

You now need to move from the whole industry and focus on one firm. I would

suggest that you use one or two tools of analysis from the module teaching

materials (e.g. value chain, generic strategies). You need to indentify the

firm’s strategy and analysis it using one/two of the tools. Try and give some

data. Remember, you need to say if you think the firm’s strategy will be successful

over the next five years. Remember to link this part to the key findings from

your industry analysis. How is the industry changing and will the firm’s chosen

strategy still be successful in the future given that change.

http://wiki.mbalib.com/zh-tw/%E5%9F%BA%E6%9C%AC%E7%AB%9E%E4%BA%89%E6%88%98%E7%95%A5

http://www.quickmba.com/strategy/generic.shtml

Conclusion

Should explain what you did in each section of the work and what your key

finding are. There should be no new analysis in the section you are just

bringing you ideas together.

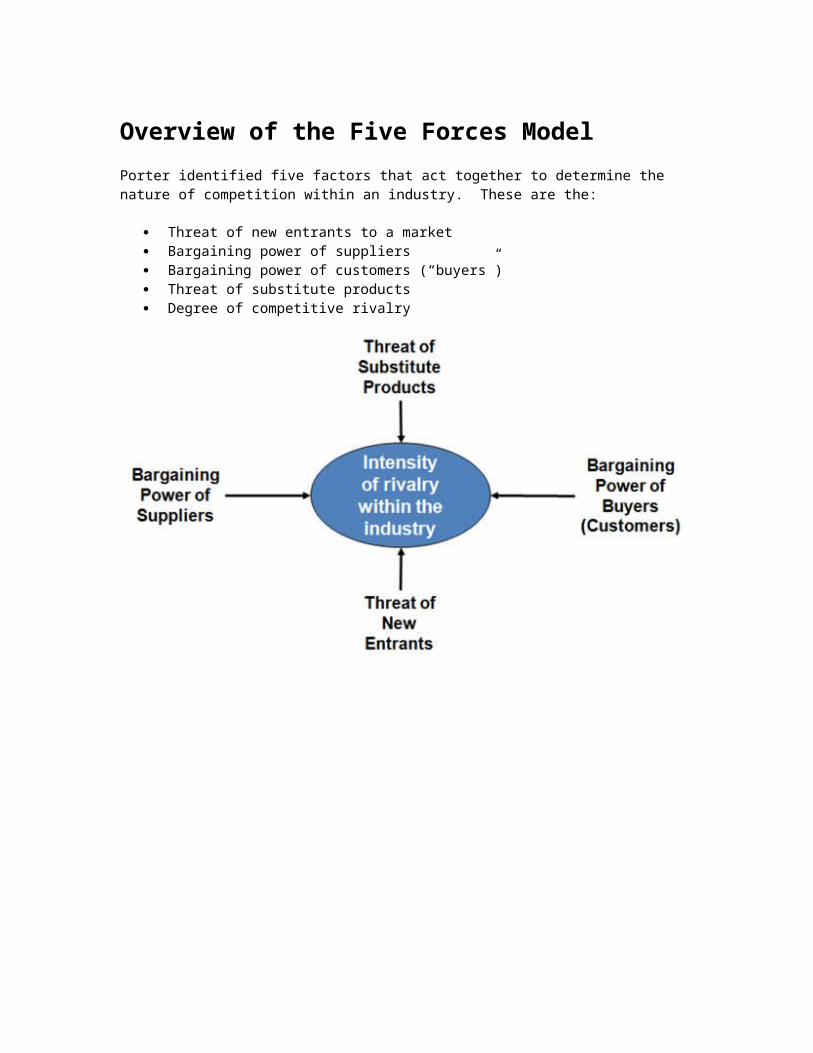

Overview of the Five Forces Model

Porter identified five factors that act together to determine the nature of competition within an industry. These are the:

Threat of new entrants to a market Bargaining power of suppliers Bargaining power of customers (“buyers”) Threat of substitute products Degree of competitive rivalry

Let’s look at each one of the five forces in a little more detail to explain how they work.

Threat of new entrants to an industry

If new entrants move into an industry they will gain market share & rivalry will intensify

The position of existing firms is stronger if there are barriers to entering the market

If barriers to entry are low then the threat of new entrants will be high, and vice versa

Barriers to entry are, therefore, very important in determining the threat of new entrants. An industry can have one or more barriers. The following are common examples of successful barriers:

Barrier Notes

Investment cost High cost will deter entryHigh capital requirements might mean that only large businesses can compete

Economies of scale available to existing firms

Lower unit costs make it difficult for smaller newcomers to break into the market and compete effectively

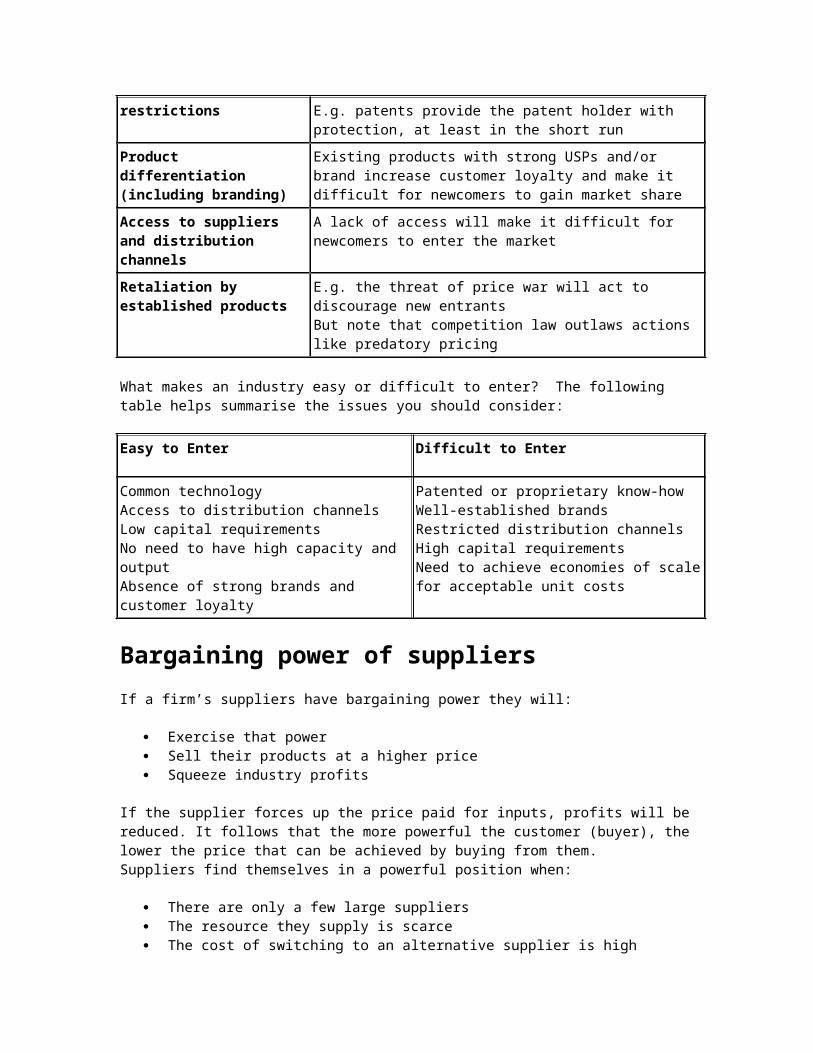

Regulatory and legal restrictions

Each restriction can act as a barrier to entryE.g. patents provide the patent holder with protection, at least in the short run

Product differentiation (including branding)

Existing products with strong USPs and/or brand increase customer loyalty and make it difficult for newcomers to gain market share

Access to suppliers and distribution channels

A lack of access will make it difficult for newcomers to enter the market

Retaliation by established products

E.g. the threat of price war will act to discourage new entrantsBut note that competition law outlaws actions like predatory pricing

What makes an industry easy or difficult to enter? The following table helps summarise the issues you should consider:

Easy to Enter Difficult to Enter

Common technologyAccess to distribution channelsLow capital requirementsNo need to have high capacity and

Patented or proprietary know-howWell-established brandsRestricted distribution channelsHigh capital requirements

outputAbsence of strong brands and customer loyalty

Need to achieve economies of scale for acceptable unit costs

Bargaining power of suppliers

If a firm’s suppliers have bargaining power they will:

Exercise that power Sell their products at a higher price Squeeze industry profits

If the supplier forces up the price paid for inputs, profits will be reduced. It follows that the more powerful the customer (buyer), the lower the price that can be achieved by buying from them.Suppliers find themselves in a powerful position when:

There are only a few large suppliers The resource they supply is scarce The cost of switching to an alternative supplier is high The product is easy to distinguish and loyal customers are reluctant to

switch The supplier can threaten to integrate vertically The customer is small and unimportant There are no or few substitute resources available

Just how much power the supplier has is determined by factors such as:

Factor Note

Uniqueness of the input supplied

If the resource is essential to the buying firm and no close substitutes are available, suppliers are in a powerful position

Number and size of firms supplying the resources

A few large suppliers can exert more power over market prices that many smaller suppliers each with a small market share

Competition for the input from other industries

If there is great competition, the supplier will be in a stronger position

Cost of switching to alternative sources

A business may be “locked in” to using inputs from particular suppliers – e.g. if certain components or raw materials are designed into their production processes. To change the supplier may mean changing a significant part of production

Bargaining power of customers

Powerful customers are able to exert pressure to drive down prices, or increase the required quality for the same price, and therefore reduce profits in an industry.

A great example in the UK currently is the dominant grocery supermarkets which are able exert great power over supply firms. You can see a great video about this issue here.

Several factors determine the bargaining power of customers, including:

Factor Note

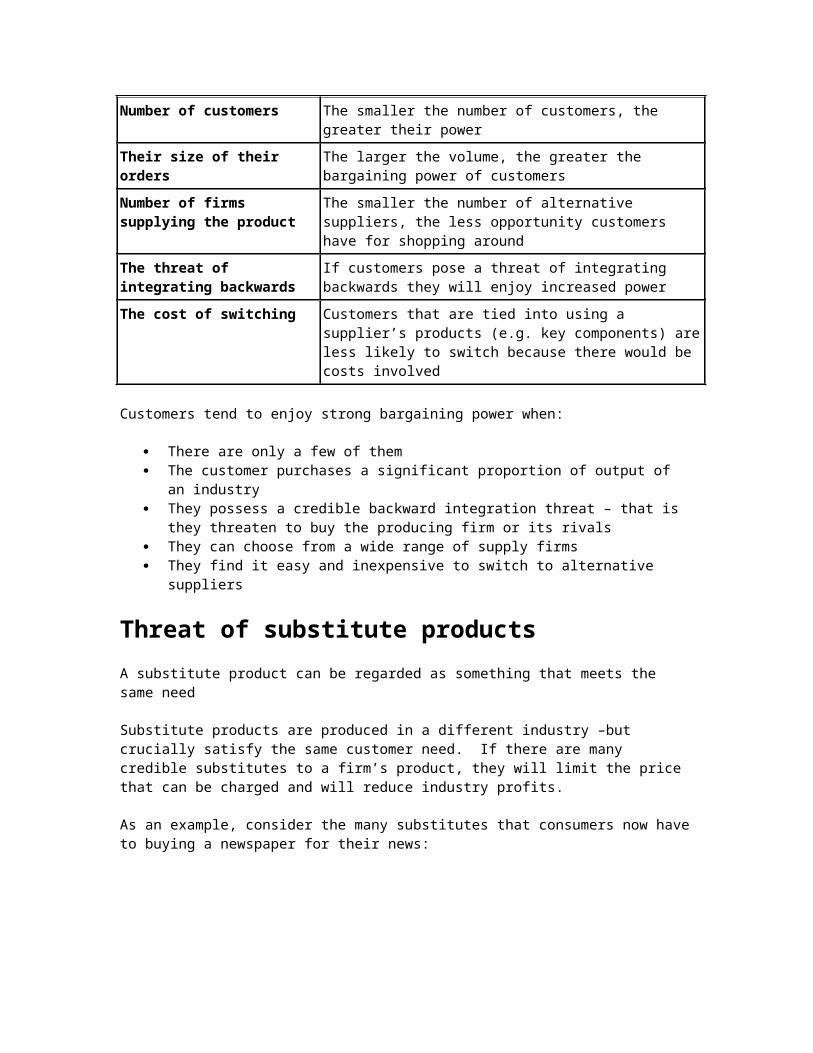

Number of customers The smaller the number of customers, the greater their power

Their size of their orders The larger the volume, the greater the bargaining power of customers

Number of firms supplying the product

The smaller the number of alternative suppliers, the less opportunity customers have for shopping around

The threat of integrating backwards

If customers pose a threat of integrating backwards they will enjoy increased power

The cost of switching Customers that are tied into using a supplier’s products (e.g. key components) are less likely to switch because there would be costs involved

Customers tend to enjoy strong bargaining power when:

There are only a few of them The customer purchases a significant proportion of output of an industry They possess a credible backward integration threat – that is they

threaten to buy the producing firm or its rivals They can choose from a wide range of supply firms They find it easy and inexpensive to switch to alternative suppliers

Threat of substitute products

A substitute product can be regarded as something that meets the same need

Substitute products are produced in a different industry –but crucially satisfy the same customer need. If there are many credible substitutes to a firm’s product, they will limit the price that can be charged and will reduce industry profits.

As an example, consider the many substitutes that consumers now have to buying a newspaper for their news:

The extent of the threat depends upon

The extent to which the price and performance of the substitute can match the industry’s product

The willingness of customers to switch Customer loyalty and switching costs

If there is a threat from a rival product the firm will have to improve the performance of their products by reducing costs and therefore prices and by differentiation.

Degree of competitive rivalry

If there is intense rivalry in an industry, it will encourage businesses to engage in

Price wars (competitive price reductions), Investment in innovation & new products Intensive promotion (sales promotion and higher spending on advertising)

All these activities are likely to increase costs and lower profits.

Several factors determine the degree of competitive rivalry; the main ones are:

Factor Note

Number of competitors in the market

Competitive rivalry will be higher in an industry with many current and potential competitors

Market size and growth prospects

Competition is always most intense in stagnating markets

Product differentiation and brand loyalty

The greater the customer loyalty the less intense the competitionThe lower the degree of product differentiation the greater the intensity of price competition

The power of buyers and the availability of substitutes

If buyers are strong and/or if close substitutes are available, there will be more intense competitive rivalry

Capacity utilisation The existence of spare capacity will increase the intensity of competition

The cost structure of the industry

Where fixed costs are a high percentage of costs then profits will be very dependent on volumeAs a result there will be intense competition over market shares

Exit barriers If it is difficult or expensive to exit an industry, firms will remain thus adding to the intensity of competition

Compare the SWOT Analyses of the viable strategic options with the results of your Five Forces analysis. For each strategic option, ask yourself how you could use that strategy to:

Reduce or manage supplier power.

Reduce or manage buyer/customer power.

Come out on top of the competitive rivalry.

Reduce or eliminate the threat of substitution.

Reduce or eliminate the threat of new entry.

Select the generic strategy that gives you the strongest set of options.

Generic Strategies

These three approaches are examples of "generic strategies," because they can be applied to products or services in all industries, and to organizations of all sizes. They were first set out by Michael Porter in 1985 in his book "Competitive Advantage: Creating and Sustaining Superior Performance."Porter called the generic strategies "Cost Leadership" (no frills), "Differentiation" (creating uniquely desirable products and services) and "Focus" (offering a specialized service in a niche market). He then subdivided the Focus strategy into two parts: "Cost Focus" and "Differentiation Focus". These are shown in Figure 1 below.

Tip:

The terms "Cost Focus" and "Differentiation Focus" can be a little confusing, as they could be interpreted as meaning "a focus on cost" or "a focus on differentiation." Remember that Cost Focus means emphasizing cost-minimization within a focused market, and Differentiation Focus means pursuing strategic differentiation within a focused market.

The Cost Leadership Strategy

Porter's generic strategies are ways of gaining competitive advantage – in other words, developing the "edge" that gets you the sale and takes it away from your competitors. There are two main ways of achieving this within a Cost Leadership strategy:

Increasing profits by reducing costs, while charging industry-average prices.

Increasing market share through charging lower prices, while still making a reasonable profit on each sale because you've reduced costs.

Tip:

Remember that Cost Leadership is about minimizing the cost to the organization of delivering products and services. The cost or price paid by the customer is a separate issue!The Cost Leadership strategy is exactly that – it involves being the leader in terms of cost in your industry or market. Simply being amongst the lowest-cost producers is not good enough, as you leave yourself wide open to attack by other low-cost producers who may undercut your prices and therefore block your attempts to increase market share.

You therefore need to be confident that you can achieve and maintain the number one position before choosing the Cost Leadership route. Companies that are successful in achieving Cost Leadership usually have:

Access to the capital needed to invest in technology that will bring costs down.

Very efficient logistics.

A low-cost base (labor, materials, facilities), and a way of sustainably cutting costs below those of other competitors.

The greatest risk in pursuing a Cost Leadership strategy is that these sources of cost reduction are not unique to you, and that other competitors copy your cost reduction strategies. This is why it's important to continuously find ways of reducing every cost. One successful way of doing this is by adopting the Japanese Kaizen philosophy of "continuous improvement."

The Differentiation Strategy

Differentiation involves making your products or services different from and more attractive those of your competitors. How you do this depends on the exact nature of your industry and of the products and services themselves, but will typically involve features, functionality, durability, support and also brand image that your customers value.

To make a success of a Differentiation strategy, organizations need:

Good research, development and innovation.

The ability to deliver high-quality products or services.

Effective sales and marketing, so that the market understands the benefits offered by the differentiated offerings.

Large organizations pursuing a differentiation strategy need to stay agile with their new product development processes. Otherwise, they risk attack on several fronts by competitors pursuing Focus Differentiation strategies in different market segments.

The Focus Strategy

Companies that use Focus strategies concentrate on particular niche markets and, by understanding the dynamics of that market and the unique needs of customers within it, develop uniquely low-cost or well-specified products for the market. Because they serve customers in their market uniquely well, they tend to build strong brand loyalty amongst their customers. This makes their particular market segment less attractive to competitors.

As with broad market strategies, it is still essential to decide whether you will pursue Cost Leadership or Differentiation once you have selected a Focus strategy as your main approach: Focus is not normally enough on its own.

But whether you use Cost Focus or Differentiation Focus, the key to making a success of a generic Focus strategy is to ensure that you are adding something extra as a result of serving only that market niche. It's simply not enough to focus on only one market segment because your organization is too small to serve a broader market (if you do, you risk competing against better-resourced broad market companies' offerings.)

The "something extra" that you add can contribute to reducing costs (perhaps through your knowledge of specialist suppliers) or to increasing differentiation (though your deep understanding of customers' needs).

To Do List:

P.27+37/p.40+54

P.74/112

http://wiki.mbalib.com/zh-tw/%E5%9F%BA%E6%9C%AC%E7%AB%9E%E4%BA%89%E6%88%98%E7%95%A5

Product life cycle image

INTRO.

All business owner works with his staff to create business strategies for marketing, sales, customer service and internal accounting functions. A business strategy is a definition of the tactics and methods you will use to manage your business, according to the online business resource More Business. It is important to have efficient and effective business strategies in place.

From its inception as a small export business in Taegu, Korea, Samsung has grown to become one of the world's leading electronics companies, specializing in digital appliances and media, semiconductors, memory, and system integration. Today Samsung's innovative and top quality products and processes are world recognized. This timeline captures the major milestones in Samsung's history, showing how the company expanded its product lines and reach, grew its revenue and market share

Just a few years ago Samsung was struggling to catch up in the smartphone market.Now it makes more of them than anybody else and has Apple on the back foot, in addition to being the world's largest technology company by revenue.

ABOUT SAMSUNG

The ultimate fast follower

Samsung is better than anybody else at learning from its competitors. "A market reader is sort of the classic fast follower," explains Barry Jaruzelski, senior partner at Booz&Co and the co-author of the Global Innovation 1000. "It doesn't mean they ignore their customers, but they're very attuned to what competitors are doing and what other people are bringing to market first and observing what seems to be gaining traction, then very rapidly coming up with their own version of that innovation."

Samsung's aggression has gotten it into trouble in the past, losing a high profile case to Apple for imitating its design. But the reputation hit and the fine were a small price to pay.

The company pivots and produces quickly, coming out with a variety of devices. It sees what the market responds to, pushes successes, and kills failures. And now, rather than just providing a cheaper and lesser iPhone, it's differentiated itself with larger screens, different features, successful marketing, and delivering what consumers want.

The Note is a perfect example. The company found through market research that Asian-language speakers in particular wanted a device that they could hand-write on, because drawing characters is easier with a pen. The result was a combination phone/tablet ("phablet") that's been an unexpected hit.

The company combines market research and unparalleled execution with, despite its reputation, a lot of innovation of its own. Samsung was second only to IBM in the number of U.S. patents filed last year, and filed 150 patents related to the new technology in the Galaxy S4.

When you've got cash, use it aggressively, or risk falling behind

Apple has a huge cash pile, but Samsung seems to be more willing and able to put their money to use. Samsung's research spend is 5.7 percent of its revenue, compared to 2.4 percent for Apple.

Samsung is a diverse business with chips, displays, and other technology. This pays dividends, allowing it to compete on price and increasingly, offer features Apple hasn't gotten to. Although, many would argue that Apple chooses not to include certain features Samsung offers.

When Samsung wants to get behind something, it can do so with considerable weight.

That's certainly been the case for its flagship Galaxy phones. Samsung's advertising push has been absolutely massive. In the U.S., where the iPhone is still pretty dominant, last year the company increased its advertising budget five-fold, to $401 million from $78 million. That's $68 million ahead of Apple, and more than $200 million ahead of its nearest competitor in the Android market. And that's only a fraction of its ad budget.

This push has paid off too, with Samsung scoring many points at Apple's expense.

Supply chain and distribution

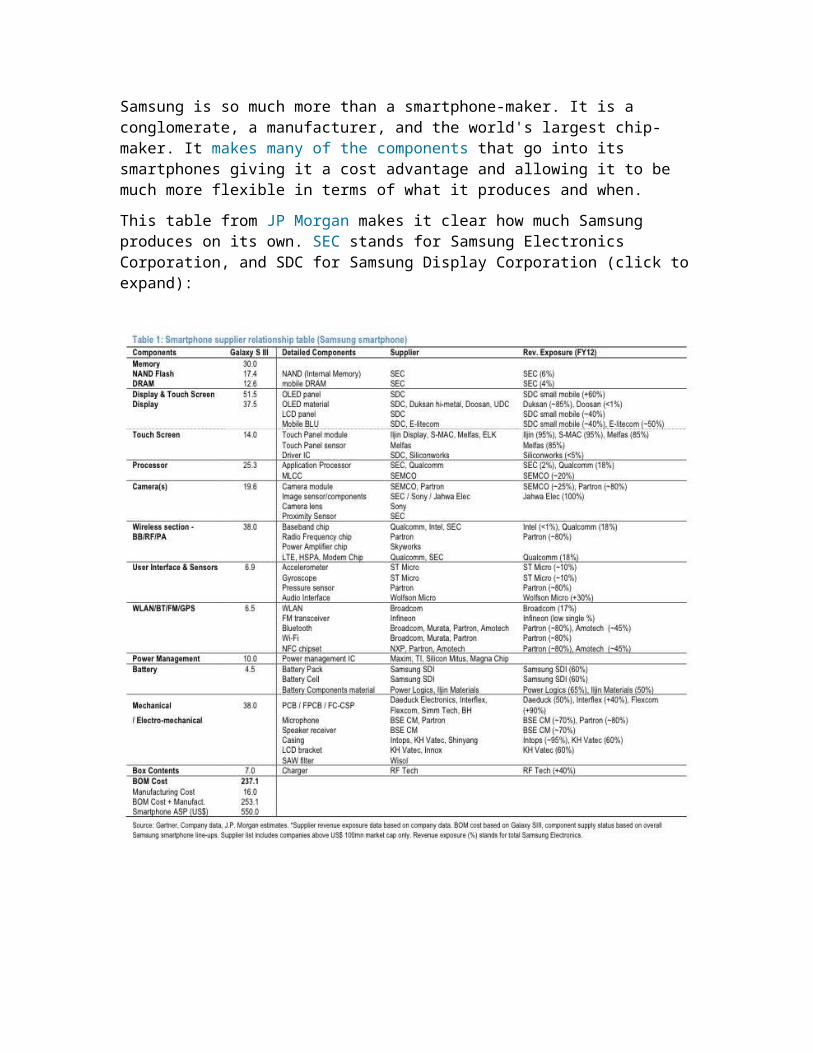

Samsung is so much more than a smartphone-maker. It is a conglomerate, a manufacturer, and the world's largest chip-maker. It makes many of the

components that go into its smartphones giving it a cost advantage and allowing it to be much more flexible in terms of what it produces and when.

This table from JP Morgan makes it clear how much Samsung produces on its own. SEC stands for Samsung Electronics Corporation, and SDC for Samsung Display Corporation (click to expand):

About industry

The global smartphone race is now between Samsung Electronics Co

Ltd, Apple Inc and an assortment of Chinese firms. As smartphone shipment

size continues to swell in Asian and African countries, the local brands are

gaining market share at the expense of global vendors. According to new data

from Strategy Analytics for both global smartphone vendors in Q2 2014 and

global smartphone market share by operating systems in Q2 2014, three of the

top five smartphone vendors in the world are now Chinese riding high on success

with Android OS. The most interesting rise is that of four-year old Chinese

smartphone vendor Xiaomi, which recently ventured into the India smartphone

market with its highly successful Mi3.

The meteoric rise of Chinese firms is due to the country’s expertise in large-scale

manufacturing and huge smartphone subscriber base of almost 800 million

users. As the market matures, these brands will gain an even larger market

share due to their low-cost smartphones powered by Android OS. This, in turn,

has allowed Google Inc. owned Android to reach a market share of 85%.

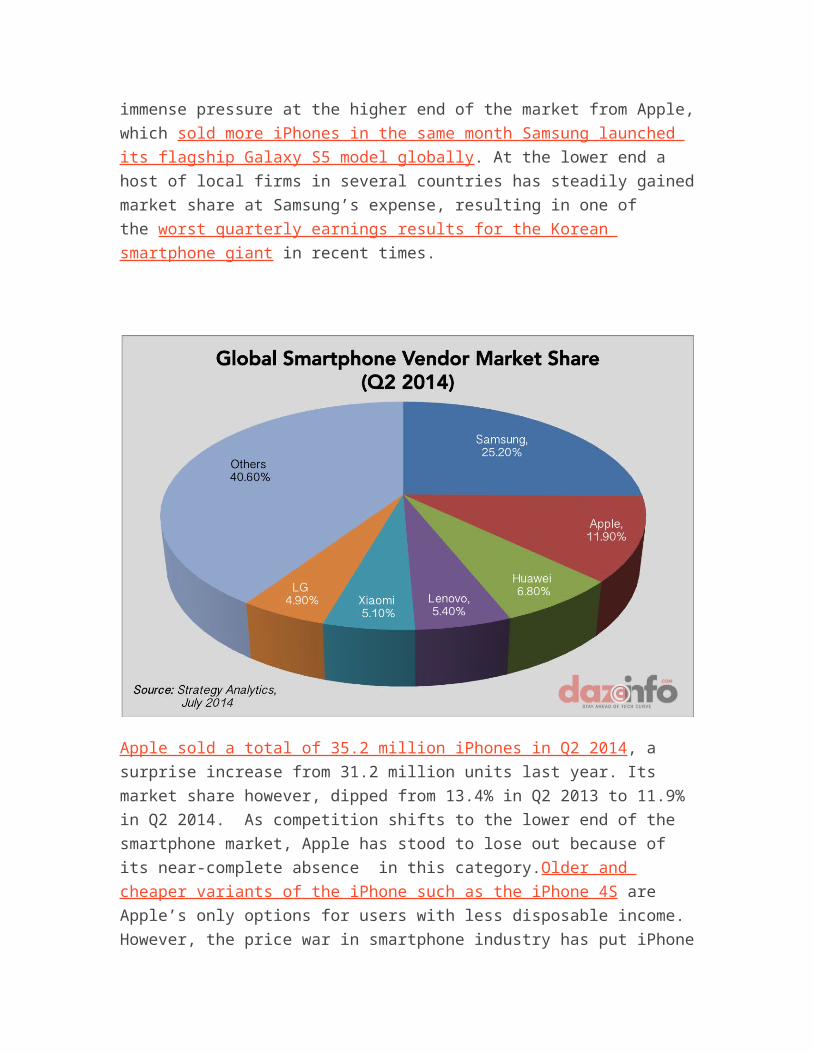

Apple and Samsung Struggle To Retain Market ShareA total of 295.2 million smartphones was shipped in Q2 2014, an increase of

27% from the 233 million units last year. A fourth of these shipments came from

Samsung, whose market share has nose-dived from 32.6% in Q2 2013 to 25.6%

in Q2 2014, largely due to the arrival of the Chinese brands. The Koran firm

shipped a total of 74.5 million smartphones in Q2 2014, a slight decline from 76

million during the same period last year. The company is facing immense

pressure at the higher end of the market from Apple, which sold more iPhones in

the same month Samsung launched its flagship Galaxy S5 model globally. At the

lower end a host of local firms in several countries has steadily gained market

share at Samsung’s expense, resulting in one of the worst quarterly earnings

results for the Korean smartphone giant in recent times.

Apple sold a total of 35.2 million iPhones in Q2 2014, a surprise increase from

31.2 million units last year. Its market share however, dipped from 13.4% in Q2

2013 to 11.9% in Q2 2014. As competition shifts to the lower end of the

smartphone market, Apple has stood to lose out because of its near-complete

absence in this category.Older and cheaper variants of the iPhone such as the

iPhone 4S are Apple’s only options for users with less disposable income.

However, the price war in smartphone industry has put iPhone 4S in a mid-range

category, while the market is flooded with more powerful, bigger screen

smartphones at half of its price. Besides, the availability of iPhone 4S in few

selected countries is another factor behind Apple’s poor performance in low-end

smartphone category.

Xiaomi’s Performance Causes Tremors in The MarketThe remaining three companies in the top five are Huawei Technology Co

Ltd(SHE:002502) , Lenovo Group Limited (ADR) (OTCMKTS : LNVGY ) and

Xiaomi. Huawei secured third position with a 6.8% market share while Lenovo

reached fourth place with a market share of 5.4%. The biggest gainer among all

brands was Xiaomi with a market share of 5.1% with a total of 15.1 million

smartphone shipments. The firm has already outsold Apple in China and its rise

has been astonishingly quick, with shipments growing three-fold in just one year.

Its Android models are widely popular in China and other Asian markets, due to

its low-cost-high-performance strategy and extensive shipments through online

and operator channels.

Xiaomi is aiming to venture into several international markets later this year, but

its main focus continues to remain in China and India, which are already the

world’s fastest growing smartphone market. Apple is aiming to sell several million

large screen iPhone 6 in China through China mobile network, and regain its

market share. The next stage of the smartphone race will take place in Asia, with

China as the centerpiece.

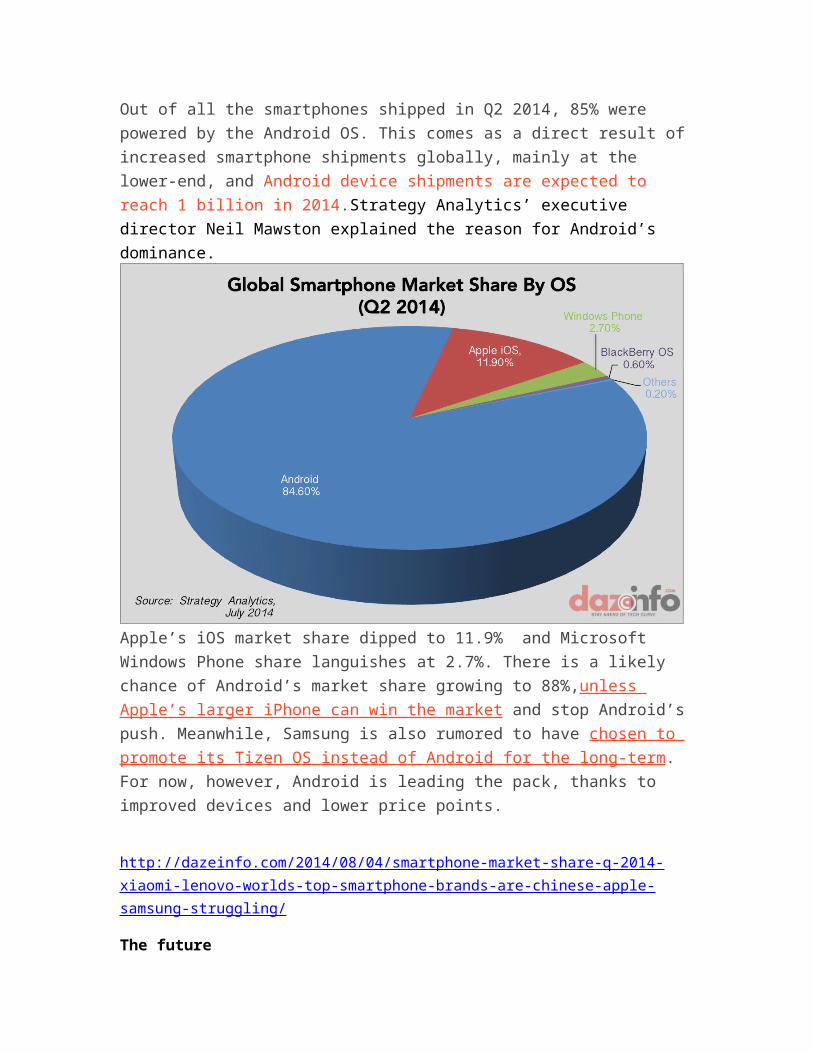

85% Of Devices Sold In Q2 2014 Powered By AndroidOut of all the smartphones shipped in Q2 2014, 85% were powered by the

Android OS. This comes as a direct result of increased smartphone shipments

globally, mainly at the lower-end, and Android device shipments are expected to

reach 1 billion in 2014.Strategy Analytics’ executive director Neil Mawston

explained the reason for Android’s dominance.

Apple’s iOS market share dipped to 11.9% and Microsoft Windows Phone share

languishes at 2.7%. There is a likely chance of Android’s market share growing

to 88%,unless Apple’s larger iPhone can win the market and stop Android’s

push. Meanwhile, Samsung is also rumored to have chosen to promote its Tizen

OS instead of Android for the long-term. For now, however, Android is leading

the pack, thanks to improved devices and lower price points.

http://dazeinfo.com/2014/08/04/smartphone-market-share-q-2014-xiaomi-lenovo-worlds-top-smartphone-brands-are-chinese-apple-samsung-struggling/

The future

The management lesson: You have to commit

Samsung is very much a Korean company, and has been, at times, accused of being overly hierarchical and dominated by its founding family. That also provides some advantages. You can fault some things the company does, but not its ambition or commitment.

When Samsung decides to get into a business, it goes hard. Within the past decade, it went from just beginning to invest in making batteries for digital devices and flash memory to being a global leader.

Former P&G CEO A.G. Lafley argues that companies fail because they're hesitant to make decisions and hesitant to commit because they fear failure and want simply to play rather than win.

Samsung wants to be the dominant player in the smartphone market, it has a strategy to do so, and it's using every tool it has as it attempts to succeed at it.

The key test of whether Samsung can move from a close-and-gaining second to becoming truly dominant is whether it can deliver products that are truly game-changing. To really start pulling customers away from iPhones in droves, it needs to differentiate itself beyond marketing and a bigger screen.

It's aggressively investing in Silicon Valley with several big campuses to help it start to lead in software as it already does with hardware.

http://www.businessinsider.com/samsung-corporate-strategy-2013-3

Tizen

http://en.wikipedia.org/wiki/Tizen

Samsung isn’t the first smartphone manufacturer in the world, but over the past few

years, it has been consolidating its leadership with many smartphones in an attempt

to cover all segment (in terms of price and hardware specifications) of the market.

The success of Samsung is not a secret, and recently DigiTimes says in a report that

the South Korean company holds 65% of total Android market share.

In the largest slice of Android share snatched by Samsung, almost 30% devices

belong to the Galaxy S lineup, in which the S3 and S4 grasp 15% and 10%, whereas

the S2 and the original S cover up 4% and 1%, respectively.

The report cites that Android has surpassed one billion activations across the globe,

and 650 million more or less are Samsung smartphones, followed by LG, HTC,

Motorola and Sony with market shares of 7%, 6%, 5% and 4%, respectively. The

rest of 13% is taken by small manufacturers, which are moving barely.

Additionally, another report reveals that Lenovo and Motorola have become the

second-largest smartphone maker in the world, although the percentage of

smartphone market share hasn’t been disclosed yet. In any case, Motorola may

have contributed the success in the US and Europe, and Lenovo in Asia.

The statistics clearly indicates Samsung is the key player of Android ecosystem, but

reportedly they’re ditching Android, adopting Tizen OS, in order to reduce

dependence on Android as well as taking control from Google.

http://www.inferse.com/13447/samsung-crushing-android-rivals-65-global-market/