Embed Size (px)

Citation preview

EBCC MEETING

25th October 2013

AGENDA

1.0 Introduction2.0 Minutes and Actions3.0 Operational Update4.0 Modification Proposals5.0 Significant Code Review Update6.0 Bank Ratings7.0 Review since April 20138.0 Focus for 2013/149.0 AOB

- EU Update - Winter Planning Prep - Risk Register - Voluntary Discontinuances

10.0 Date of Next Meeting

Operational Update

September 2013

Modifications

Modifications

• Mod 0429 Customer Settlement Error Claims Process– Implementation effective at April 2014– Xoserve to develop internal process – Energy Adjustments to be processed via ADS at average SAP

Market Operator Security Provisions

• Meeting was held with the MO on 17th October 2013.

• MO agreed to the final drafting approved by EBCC members and are happy to sign and approve the Prepayment Agreement

• Confirmation that the Deposit Deed will be in place with the required level of Security.

Significant Code Review Update

Security of Supply Significant Code Review

• OFGEM are now consulting further on DSR auctions with the industry and taking further interest in the impact on credit arrangements. – Meeting held on 14th October 2013 minutes published on Ofgem’s website.

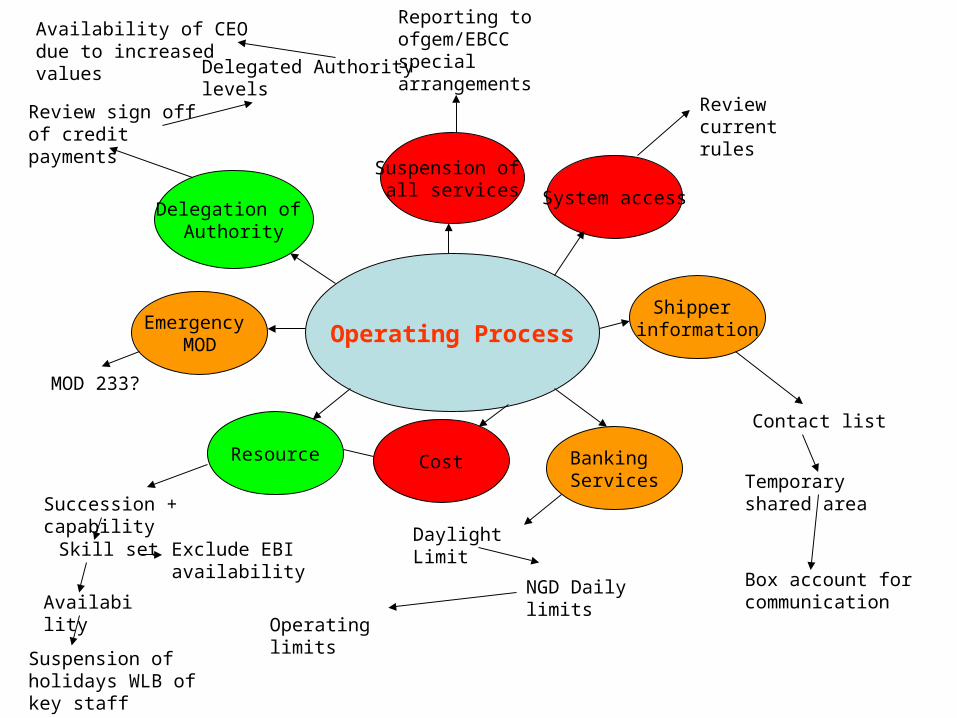

Operating Process

Delegation of Authority

Shipper information

System access

Suspension of all services

Emergency MOD

Resource Cost Banking Services

Review sign off of credit payments

Reporting to ofgem/EBCC special arrangements

Review current rules

Succession + capability

MOD 233?

Skill set Exclude EBI availability

Availability

Suspension of holidays WLB of key staff

Daylight Limit

NGD Daily limits

Operating limits

Availability of CEO due to increased values

Contact list

Temporary shared area

Box account for communication

Delegated Authority levels

Priority of ScoringFor EBCC meetings Portfolio

growth

Communication interaction

commercial intelligence

reporting

Downgrade risk factor risk

Security arrangements

Party underwriting

Payment trends

Over or under delivery trends

FSRs number of cash calls over previous

period

Level of helpfulness

How they act in market

Ability to pay

D + B

Moody’s

S + P

EBCC Operation

National Grid input

Establish who from Xoserve

required

Conflict of interest

INCIDENTROOM

Ofgem’s role

Chair Availability

Quoracy

Gemserve members

appointment

Communication

Agree Adhoc appointment

process

Consider membership ofgem/another party

Priorities on orderOf discussion

Factors

Minutes

Checklists

Recording

Review timing

Resources

Relaxing current arrangements Business rules

Security

Cash collectionMarket Operator

EBCC Meetings

Cash calls

No changes proposed.

Existing rules apply- due to arrangements drafting + under UK termination process S.1.7.

timing for convention of meeting

Appeal ProcessResource issues

Extend time?

Reduce or suspend appeal notice

No appeal criteria

Still issue

Payment terms extend ?

Timing extend?- 4pm – end of gas day

Agree with EBCC members no validation

FSR

Consider suspension for a period beyond invoices issued and paid

Validate cash call suite

System solution for manual adjustment

Manually update letters/notices as we do currently

Cost of funding change

Communication of delivery

Faxes? Scan, email or file interface

Aggregate exposure

Accepting LOC from lower rated organisations

% of exposure underwriting

Process going forward

Suspending/ excluding peak SAP calc

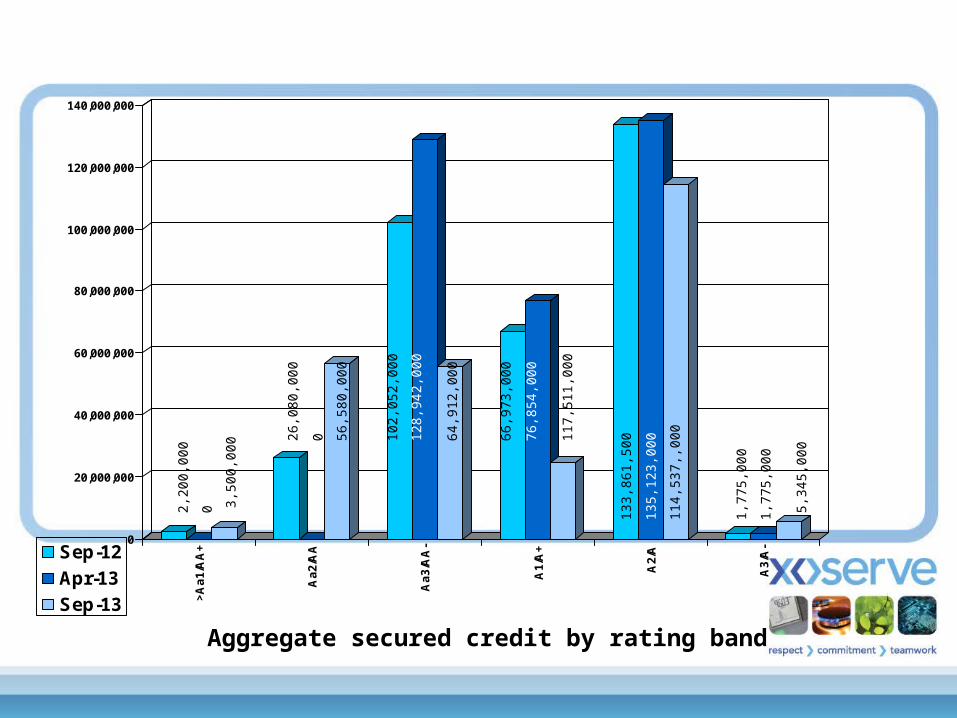

Bank Ratings

Current Position

• Since April 2013 the global economic markets have remained fairly stable resulting in no significant downgrades.

• Royal Bank of Scotland, National Westminster are on possible downgrade and Citibank are currently on possible upgrade with Moodys, non of the FI’s are currently on watch with S & P.

• RBS, Loan to deposit ratio is currently on 100% in 2009 it was 130%.

0

20,000,000

40,000,000

60,000,000

80,000,000

100,000,000

120,000,000

140,000,000

>A

a1

/AA

+

Aa

2/A

A

Aa

3/A

A-

A1

/A+

A2

/A

A3

/A-Sep-12

Apr-13

Sep-13

Aggregate secured credit by rating band

2,20

0,00

0

0

26,0

80,0

00

0 102,

052,

000

128,

942,

000

66,9

73,0

00

76,8

54,0

00

133,

861,

500

135,

123,

000

1,77

5,00

0

1,77

5,00

0

3,50

0,00

0

64,9

12,0

00

56,5

80,0

00

117,

511,

000

114,

537,

,000

5,34

5,00

0

Impact of ratings review

• 4% of all FIs currently providing Security have been subject to a downgrade change during the previous 12 months by Standard and Poors and Moody’s Rating Agencies.

• Currently 61% of FIs are in the lowest categories of investment grade rating.

>AA+/Aa1

>AA/Aa2

>AA-/Aa3

>A+/A1

>A/A2

>A-/A3

FI Ratings April 2013

32%

20%

2%

8%

21%

8%

57%

4%

13%

100%

0%

Outlook

10% Possible Downgrade

90% Not on Watch

Moody’s Outlook

63% Negative

37% Stable

S & P’s Outlook

• Having completed a significant rating review throughout 2012 and again in June 2013. 10% of FIs are currently reported as possible downgrade.

• S&P are commencing significant reviews across a large number of FIs, with 63% showing a negative outlook.

10%

90%

37%

63%

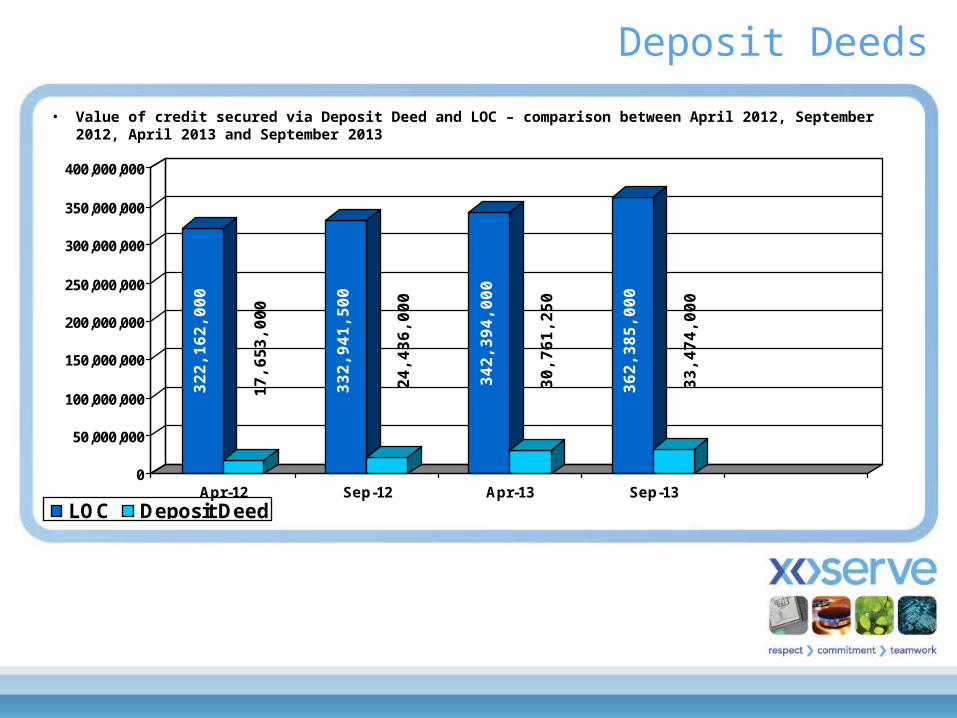

Deposit Deeds

• Value of credit secured via Deposit Deed and LOC – comparison between April 2012, September 2012, April 2013 and September 2013

0

50,000,000

100,000,000

150,000,000

200,000,000

250,000,000

300,000,000

350,000,000

400,000,000

Apr-12 Sep-12 Apr-13 Sep-13

LOC Deposit Deed

32

2,1

62

,00

0

33

2,9

41

,50

0

17

,65

3,0

00

24

,43

6,0

00

34

2,3

94

,00

0

30

,76

1,2

50

36

2,3

85

,00

0

33

,47

4,0

00

Conclusions

• Security value whilst it has increased we have only seen a small increase on the Deposit Deeds since April 2013. Most Users are very settled with the Deposit Deed since they were introduced.

• Since the EBCR were revised in December 2011, we are continuing to see a movement from the higher banding A1 to A2.

• Continue to monitor those FI’s which are currently on possible downgrade

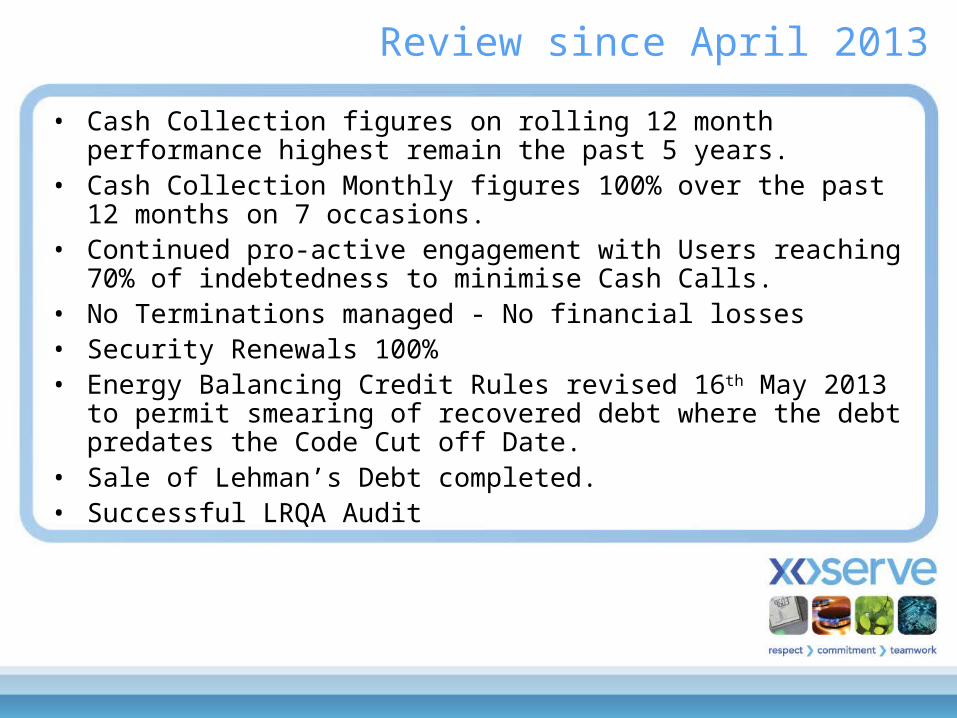

Review since April 2013

Review since April 2013

• Cash Collection figures on rolling 12 month performance highest remain the past 5 years.

• Cash Collection Monthly figures 100% over the past 12 months on 7 occasions.

• Continued pro-active engagement with Users reaching 70% of indebtedness to minimise Cash Calls.

• No Terminations managed - No financial losses• Security Renewals 100%• Energy Balancing Credit Rules revised 16th May 2013 to permit

smearing of recovered debt where the debt predates the Code Cut off Date.

• Sale of Lehman’s Debt completed.• Successful LRQA Audit

Focus for 2013/14 Update

Focus for 2013/14 addressed at April 2013 meeting

• From the meeting held in April 2013, the following key areas were identified to focus on :-

– Increase the profile of the committee

– Emergency Credit Rules

– Watching brief on European

• Members to review if there are any other significant areas that they would like the committee to focus on.

Focus 2013/14

• EBCC Customer Satisfaction

EBCC Customer Satisfaction (Nov12)

92.00%

100.00%

92.00%

96.00%

92.00%

100.00%

92.00%

84.00%

96.00%

92.00%

100.00%

84.00%

93.33%

75.00% 80.00% 85.00% 90.00% 95.00% 100.00% 105.00%

Accountability

Customer Focused

Delivery of Commitments

Expertise

Flexibility

Professionalism

Partnership

Quality of Deliverables

Skill

Strategic Objectives

Trust

Value Added

Overall Average

Year on Year Comparison

EBCC Customer Satisfaction Overall Average

85.00%

92.50%

93.33%

80.00% 82.00% 84.00% 86.00% 88.00% 90.00% 92.00% 94.00%

2010

2011

2012

Nov-12

Nov-11

Nov-10

AOB

EU Third Energy Package

Update

Current Position

• Congestion Management Procedures NC – Adopted in August 2012, first implementation is due to take place in October 2013 (MOD 449). Final stage of implementation is due July 2016.

• Capacity Allocation Mechanisms NC – Due to be formerly adopted imminently with a likely implementation date of October 2015. This encompasses the Gas Day Change and the European trading platform (PRISMA).

Current Position Cont.

• Balancing NC – Adopted in October. Implementation has been set as 1st October 2015.

• Interoperability and Data Exchange NC – Final Draft of the NC submitted to ACER on 10 September 2013. No indicative implementation date, but it is likely to coincide with CAM.

• Tariffs – The Framework Guidelines are still in consultation, the NC has not yet commenced drafting. There is uncertainty about the implementation – ideally this should coincide with CAM.

UK Progress

• Modifications raised for the Gas Day change and to implement new Code definitions ie Interconnection Point.

• NG scoping PRISMA (European trading platform) to facilitate ‘bundled’ cross border trades. Feedback to recent consultations has been positive and NG are looking to join PRISMA in 2014.

Winter Planning

• An updated pack will be issued to members in due course to include a meeting template

• Meeting/ teleconference will be held with newly appointed members to run through the operation of an emergency meeting during November 13

Risk Register

Update

Register Part 1

Risk Register as at 26/4/13 :

Risk Likelihood - comments Likelihood

H1loss of Gemini system - sustained loss for

1 working day or more

Once in 10 years – to date Gemini over 2 years Gemini has had 1 short overnight outage. Also due to Oracle Software Upgrade, Gemini affected between 22nd and 25th October. Loss of Gemini on 14th and 15th May due to Server problems. GRP implementation planned 9th June.

Suggest move

from a 2 to a 3

H2Calculation for IMS is found to be

incorrect.

Has happened in Dec 05 and also recently when during Oracle OS upgrade UAT it was found that accruals not included in a D-1 or D-2 recalculation – twice in last 6 to 7 years – once in 5 years. April 08 data was uploaded incorrectly. Recent issues identified on the 7th of March and 6th April following batch job issues.

Suggest move

from a 3 to a 5

H3APX Gas files containing system prices

and trades arrives late.

Pre Gemini IMS this used to stop PIMS jobs running – since introduction of Gemini IMS this has not happened – once in 5 years. Controls and monitors are now in place to ensure files are received. 3

Register Part 2

Risk Register as at 26/4/13 :

Risk Likelihood - comments Likelihood

H8User’s unable to provide CVA data due to the CVA system / website being down

This happened once on 13/03/07 – Once in 5 years. Controls in place that would receive notification from CVA. 3

H9

In the absence of being unable to adjust the ABI calculation the industry could be unduly exposed to avoidable financial debt. Should NGD be aware of more up to date information.

Due to SCR Mod 233 this was put on hold to await outcome of SCR consultations. Potential implementation of OFGEM SCR proposal has the potential to increase the likelihood and impact of this issue.

Suggest move from 3

to 4

H10

Due to the current European financial climate, there is a risk that the number of FI’s meeting the relevant criteria to provide security could reduce significantly.

Moody’s are currently have a schedule to review all FI’s current rating in June 2012. Moody’s review of FIs completed over the summer of 2012, S&P now anticipate conducting their own review. 4

Voluntary Discontinuance

AOB

• Questions/ Any further business?