Embed Size (px)

Citation preview

32%

20% 14%

9%

6%

4%

3% 12%

Earnings Contribution

BFI

BFT

DIV

TLE

MFG

P&E

OIL

OTHERS

25%

20%

20%

7%

5%

5%

4%

14%

Market capitalization composition

BFI

BFT

DIV

TLE

MFG

H&T

OIL

OTHERS

-10.00%

-5.00%

0.00%

5.00%

10.00%

15.00%

20.00%

OIL

F&T

MFG

L&P

C&

E

BFI

TLE

C&

P

H&

T

PLT

S&S

SRV

INV

MTR

TRD

DIV

BFT

P&

E IT

HLT

Sector Index Performance (Quarter)

5000

5500

6000

6500

7000

7500

10

11

12

13

14

15

16

09/24/13 12/24/13 03/24/14 06/24/14

ASPI Index and P/E Ratio

PE Ratio ASPI

-100.00%

-50.00%

0.00%

50.00%

100.00%

150.00%

200.00%

TLE

INV IT

S&S

DIV BFI

OIL

SRV

C&

E

BFT

MFG

H&

T

HLT

L&P

P&

E

MTR

TRD

Earnings Growth (Quarter)

Analysts:

Damith Wasantha +94 117 880837

Hiruni Perera +94 117 880809

Earnings Insight Special Report

Period ending 30th June 2014 23rd October 2014

Positive earnings drive the market

Overall interim results for the quarter ended 30th June have shown an increase of 26.84%, while for the 3 months (period) the results have increased by 19.76%. Majority of the sectors have posted positive earnings growths due to various industry specific reasons. The report is based on interim results of a sample of 242 counters. During the three months ended 30th June 2014 economy performed well with healthy economic factors such as low inflation, increase in GDP and improved external sector performance. Inflation for the June 2014 drops further to 2.8% from 4.9 % in April 2014, while external sector further improved. Proposed consolidation plans were submitted by banks and finance and leasing companies (NBFIs), and those were reviewed and evaluated by the Central Bank during the quarter.

Quarter profit increased by

26.84% QOQ to post a figure

of LKR 45Bn, while for the

period (6 months or 12

months) earnings have

increased by 19.76% to post a

figure of LKR 59 Bn.

Only Six sectors (H&T, HLT,

L&P, P&E, MTR and TRD)

provided negative earnings

growths.

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

3/6 months Quarter

LKR

Mn

Earnings Growth

2013 2014

Most of the sectors have

performed well during the

quarter ended 30th June

while oil palm and health

care has become the

highest and lowest index

performers respectively.

Special Report: Earnings Insight |23 October 2014

2 | LOLC Securities Limited

-3000.00%

-2000.00%

-1000.00%

0.00%

1000.00%

PABC HDFC CTCE ARPI CSF SFS

Gainers and losers (Earnings growth -Quarter)

11000

12000

13000

14000

15000

16000

17000

18000

9/23/13 12/23/13 3/23/14 6/23/14 9/23/14

Sector Index (12 months)

0

5,000

10,000

15,000

3/6 Months Quarter

LKR

Mn

Earnings Growth

2013 2014

-300.00%

-200.00%

-100.00%

0.00%

100.00%

200.00%

BREW CCS RWSL LMF LION CARG

Gainers and losers (Earnings growth -Quarter)

17%

15%

10%

8% 7%

43%

Earnings contribution (Quarter)

HNB

COMB

SAMP

DFCC

LOLC

others

49%

20%

11%

6%

5% 9%

Earnings Contribution (Quarter)

CTC

DIST

NEST

KFP

LION

others0

5000

10000

15000

20000

25000

09/23/13 12/23/13 03/23/14 06/23/14 09/23/14

Sector index (12 months)

0

10,000

20,000

30,000

3/6 Months Quarter

LKR

Mn

Earnings Growth

2013 2014

Bank, Finance and Insurance

Graph Set 1: Sector analysis

6 months

Source: CSE, Bloomberg, LOLC SEC Research

Beverage, Food & Tobacco

Graph Set 2: Sector analysis Source: CSE, Bloomberg, LOLC SEC Research

Bank, Finance and Insurance sector is the

largest sector with a market cap of LKR

693Bn (25% of the total market cap).

COMB, HNB and DFCC are biggest market

cap counters.

Quarterly earnings improved by 31.37%

while 3 or 6 months earnings have

increased by 28%. Most of the banks

recovered from previous quarter low

earnings due to gold loan provisions

while specialized finance companies like

SFS continued to suffer.

Finance sector consolidation process

triggered major deals in the market

whilst most of the merger proposals

were finalized. CBSL continued to have a

dovish outlook on the monetary policy

and decided to bring down the Standing

Deposit Rate to 5% from 6.5%, when the

number of deposit times exceeds 3 times

during a month. We believe this would

help curtail down the excess liquidity.

Beverage, Food and Tobacco sector has

a market cap of LKR 554Bn (19.98% of

the total market cap) while CTC, NEST

and DIST are the largest big cap

counters of the sector.

QOQ and 3 or 6 months earnings have

increased by 10.36% and 11.84%

respectively. CTC and DIST contributed

70% to the sector earnings. Inflation

remained under 4% during the quarter

helping volume driven FMCG categories

to grow. Beverage related counters

performed comparatively well.

Super market chains were affected with

the negative VAT difference such as

CARG.

Special Report: Earnings Insight |23 October 2014

3 | LOLC Securities Limited

-50

0

50

100

150

3/6 Months QuarterLK

R M

n

Earnings Growth

2013 2014-100.00%

-50.00%

0.00%

50.00%

100.00%

150.00%

200.00%

UCAR LCEY HAYC ASPH MULL MORI

Gainers and losers (Earnings growth- Quarter)

4000

5000

6000

7000

8000

9/23/13 12/23/13 3/23/14 6/23/14 9/23/14

Sector Index (12 months)

-200.00%

-150.00%

-100.00%

-50.00%

0.00%

50.00%

100.00%

150.00%

KAPI AEL LDEV DOCK

Gainers and Losers (Earnings growth- Quarter)

2000

2500

3000

3500

4000

9/23/13 12/23/13 3/23/14 6/23/14 9/23/14

Sector Index (12 months)

0

500

1,000

1,500

3/6 Months Quarter

LKR

Mn

Earnings Growth

2013 2014

50% 42%

4% 2% 2%

Earnings Contribution (Quarter)

CIC

HAYC

MORI

UCAR

MULL

0

2,000

4,000

6,000

8,000

10,000

2013 2014

LKR

Mn

Revenue for the period

AEL

KAPI

LDEV

DOCK

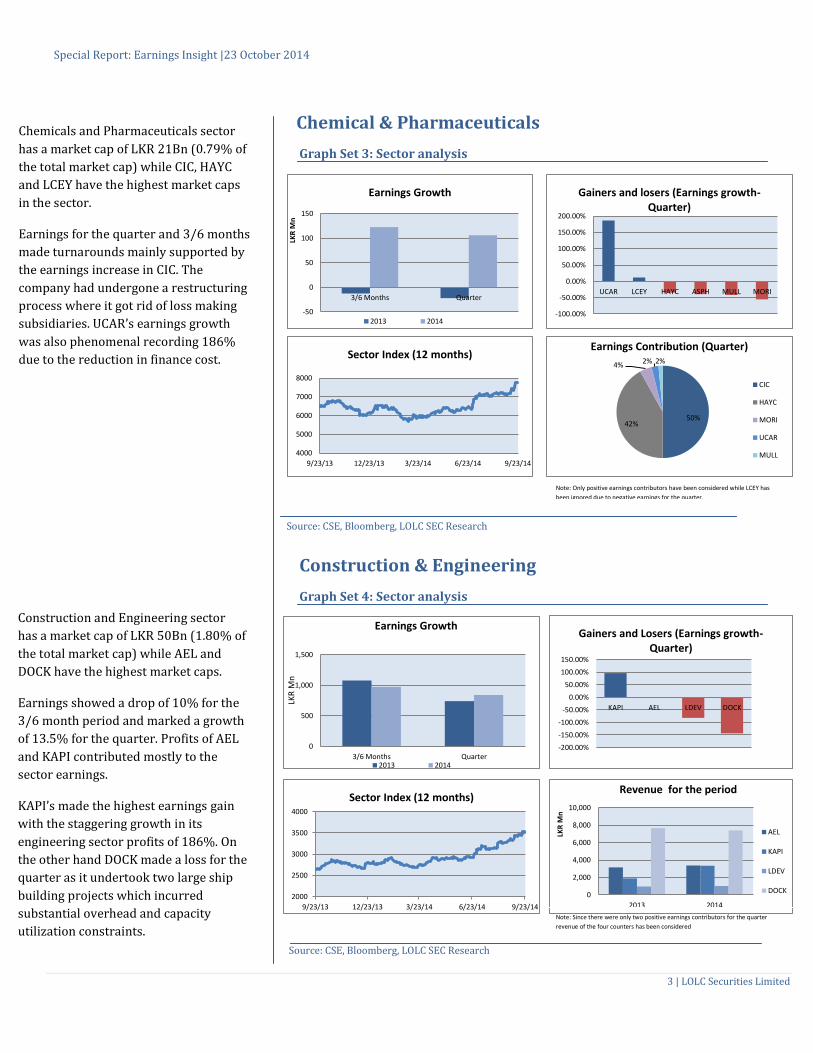

Chemical & Pharmaceuticals

Graph Set 3: Sector analysis Source: CSE, Bloomberg, LOLC SEC Research

Construction & Engineering

Graph Set 4: Sector analysis

Source: CSE, Bloomberg, LOLC SEC Research

Chemicals and Pharmaceuticals sector

has a market cap of LKR 21Bn (0.79% of

the total market cap) while CIC, HAYC

and LCEY have the highest market caps

in the sector.

Earnings for the quarter and 3/6 months

made turnarounds mainly supported by

the earnings increase in CIC. The

company had undergone a restructuring

process where it got rid of loss making

subsidiaries. UCAR’s earnings growth

was also phenomenal recording 186%

due to the reduction in finance cost.

Construction and Engineering sector

has a market cap of LKR 50Bn (1.80% of

the total market cap) while AEL and

DOCK have the highest market caps.

Earnings showed a drop of 10% for the

3/6 month period and marked a growth

of 13.5% for the quarter. Profits of AEL

and KAPI contributed mostly to the

sector earnings.

KAPI’s made the highest earnings gain

with the staggering growth in its

engineering sector profits of 186%. On

the other hand DOCK made a loss for the

quarter as it undertook two large ship

building projects which incurred

substantial overhead and capacity

utilization constraints.

Note: Only positive earnings contributors have been considered while LCEY has

been ignored due to negative earnings for the quarter.

Note: Since there were only two positive earnings contributors for the quarter

revenue of the four counters has been considered

Special Report: Earnings Insight |23 October 2014

4 | LOLC Securities Limited

0

5,000

10,000

3/6 Months QuarterLK

R M

n

Earnings Growth

2013 2014-1000.00%

0.00%

1000.00%

2000.00%

3000.00%

CSEC SUN CARS EXPO CFLB BIL

Gainers and Losers (Earnings growth -Quarter)

1500

1700

1900

2100

2300

9/23/13 12/23/13 3/23/14 6/23/14 9/23/14

Sector Index (12 months)

35%

22%

13%

12%

7%

11%

Earnings Contribution (Quarter)

JKH

CARS

HAYL

SPEN

RICH

others

-150.00%

-100.00%

-50.00%

0.00%

50.00%

CLPL ODEL

Gainers and Losers (Earnings growth-Quarter)

-1,000

-500

0

500

3/6 Months QuarterLKR

Mn

Earnings Growth

2013 2014

0

200

400

600

800

1000

1200

09/23/13 12/23/13 03/23/14 06/23/14 09/23/14

Sector Index (12 months)

55% 38%

7%

Earnings Contribution (Quarter)

CLPL

MGT

KURU

Diversified Graph Set 5: Sector analysis

Source: CSE, Bloomberg, LOLC SEC Research

Footwear and Textiles

Graph Set 6: Sector analysis Source: CSE, Bloomberg, LOLC SEC Research

Diversified sector has a market cap of

LKR 544Bn (19.62% of the total market

cap) while JKH, CARS and SPEN are the

big cap counters.

3/6 months earnings increased by

32.42% while QOQ earnings increased by

32.74%. JKH, CARS and HAYL

contributed mostly to the sector earnings

while growth was more or less stagnant

during the quarter.

However, CSEC profits had a staggering

growth as profits of the financial services

unit, First Capital Holdings PLC were LKR

218 Mn compared to LKR 66 Mn in the

previous year. This significant increase in

profits was due to the capital gain in

fixed income securities trading

opportunities on decline of interest rates.

Market Capitalization of Footwear &

Textile sector is over LKR 14Bn (0.51%

of the total market Cap), while ODEL &

MGT contribute most to the Market

Capitalization of the sector.

F&T sector has shown a turnaround for

the period while reducing the negative

earnings figure for the quarter. CLPL

and MGT contributed mostly to the

sector earnings while KURU got delisted

during the quarter.

MGT experienced a turnaround from the

loss during the previous quarter

recording a profit of LKR 4.5 Mn

compared to a loss of LKR 92.6 Mn

during the corresponding previous

quarter.

Note: Only positive earnings contributors for the quarter has been considered

while ODEL has been ignored due to negative earnings

Special Report: Earnings Insight |23 October 2014

5 | LOLC Securities Limited

47%

15%

14%

11%

8% 5%

Earnings Contribution (Quarter) ASIR

AMSL

LHCL

CHL

NHL

ASHA

550

600

650

700

3/6 Months Quarter

LKR

Mn

Earnings growth

2013 2014

-600.00%

-400.00%

-200.00%

0.00%

200.00%

SHOT HUNA SIGV TANG KHC EDEN

Gainers and Losers (Earnings Growth Quarter)

-80.00%

-60.00%

-40.00%

-20.00%

0.00%

20.00%

40.00%

ASIR CHL AMSL NHL LHCL

Gainers and Losers (Earnings growth Quarter)

0

200

400

600

800

1,000

3/6 Months QuarterLK

R M

n

Earnings Growth

2013 2014

0

200

400

600

800

1000

09/23/13 12/23/13 03/23/14 06/23/14 09/23/14

Sector Index (12 months)

2800

3000

3200

3400

3600

3800

09/23/13 12/23/13 03/23/14 06/23/14 09/23/14

Sector Index (12 months)

57%

43%

Earnings Contribution- (Quarter)

AHPL

OTHERS

Healthcare Graph Set 7: Sector analysis

Source: CSE, Bloomberg, LOLC SEC Research

Hotels & Travels

Graph Set 8: Sector analysis Source: CSE, Bloomberg, LOLC SEC Research

Healthcare sector captures around 2.20%

of the total market capitalization with

market cap of over LKR 60Bn.

Sector earnings have dropped down for

both the quarter and for the period by

16.57% and 17% respectively.

ASIR was the only counter that posted an

earnings growth for both the periods

while all other counters have

experienced profit declines. ASIR’s

earnings increased for quarter as well as

3/6 period mainly due to foreign

exchange gain. ASIR, AMSL and LHCL

contributed mostly to the sector earnings

Hotels and Travel sector contributes

around 5.19% of the total market

capitalization. AHPL, AHUN and TRAN

are the biggest market caps in the

sector.

QOQ earnings have posted a drop 2.71%

while for the period of 3/6 months

earnings made a gain of 11.90%.

EDEN generated the lowest growth in

earnings to record a 124Mn loss for the

quarter due to increase in operating

expenses. Refurbishment activities

made an impact on the earnings as some

counters made a positive gain after the

closure for refurbishments during the

previous quarter such as SHOT.

Tourist boom continued as the number

of arrivals surpassed 1.1 Mn mark (1.5

Mn target for 2014) while the reduction

of gas prices could also benefit the

margins of the sector.

Special Report: Earnings Insight |23 October 2014

6 | LOLC Securities Limited

-200.00%

-100.00%

0.00%

100.00%

200.00%

300.00%

SHAW GUAR CINV CIT RHL CFI

Gainers and Losers (Earnings growth Quarter)

0

50

100

150

9/23/13 12/23/13 3/23/14 6/23/14 9/23/14

Sector index (12 months)

50%

32%

5%

5% 6%

2%

Earnings Contribution (Quarter)

GUAR

CINV

RHL

SHAW

GREG

OTHERS

0

500

1,000

1,500

3/6 Months QuarterLK

R M

n

Earnings Growth

2013 2014

0

10,000

20,000

30,000

40,000

50,000

2013 2014

Revenue for the period

0

5000

10000

15000

20000

25000

9/23/13 12/23/13 3/23/14 6/23/14 9/23/14

Sector Index (12 months)

0

10

20

30

3/6 Months Quarter

LKR

Mn

Earnings Growth

2013 20140.00%

50.00%

100.00%

Gainers and Losers (Earnings Growth -Quarter)

ECL

Investment Trusts Graph Set 9: Sector analysis

Source: CSE, Bloomberg, LOLC SEC Research

Information Technology

Graph Set 10: Sector analysis

Source: CSE, Bloomberg, LOLC SEC Research

Investment Trust Sector is with a Market

Capitalization of LKR 39Bn (1.41% of the

total market cap) where GUAR, CINV and

GUAR have contributed mostly to the

earnings.

Sector has posted a growth of 80.77% for

the quarter as well as for the 3/6 period

mainly due to increase in counters such

as SHAW, GUAR and CINV by 227.31%,

112.67% and 97.07%.

SHAW’s revenue increased by 513% for

the quarter while interest income

increased by 169%.

Positive growth in the stock market

raised the values of quoted investments

of most of these companies.

Information Technology sector

comprises of two counters, ECL and PCH

while ECL accounts for LKR 1.7Bn and

PCH accounts for LKR 1.8 Bn in the

market capitalization.

As at the date of preparing the report,

only ECL interim results had been

published. ECL’s 3/6 period as well as

quarter earnings increased by 71.73%.

Sector index has been stagnant while

revenue for the 3/6 month period grew

by 25.63%.

*Note: Revenue is there since only one counter has published results as at

preparing this report.

Earnings figure

Special Report: Earnings Insight |23 October 2014

7 | LOLC Securities Limited

0

500

1,000

1,500

2,000

3/6 Months Quarter

LKR

Mn

Earnings Growth

2013 2014

-400.00%

-200.00%

0.00%

200.00%

400.00%

ETWO YORK EQIT EAST KDL CLND

Gainers and Losers (Earnings growth-Quarter)

0

200

400

600

800

1000

9/23/13 12/23/13 3/23/14 6/23/14 9/23/14

Sector Index (12 months)

0

1,000

2,000

3,000

4,000

3/6 Months Quarter

LLK

R M

n

Earnings Growth

2013 2014-500.00%

0.00%

500.00%

1000.00%

LALU SIL BOGA GLAS SWAD SINI

Gainers and Losers (Earnings growth -Quarter)

24%

19%

8% 7%

6%

36%

Earnings Contributution (Quarter)

LLUB

TKYO

DIPD

CERA

TJL

OTHERS0

1000

2000

3000

4000

5000

9/23/13 12/23/13 3/23/14 6/23/14 9/23/14

Sector Index (12 months)

69%

10%

7%

5% 3%

6%

Earnings Contribution (Quarter)

OSEA

PDL

CABO

CTLD

COMD

others

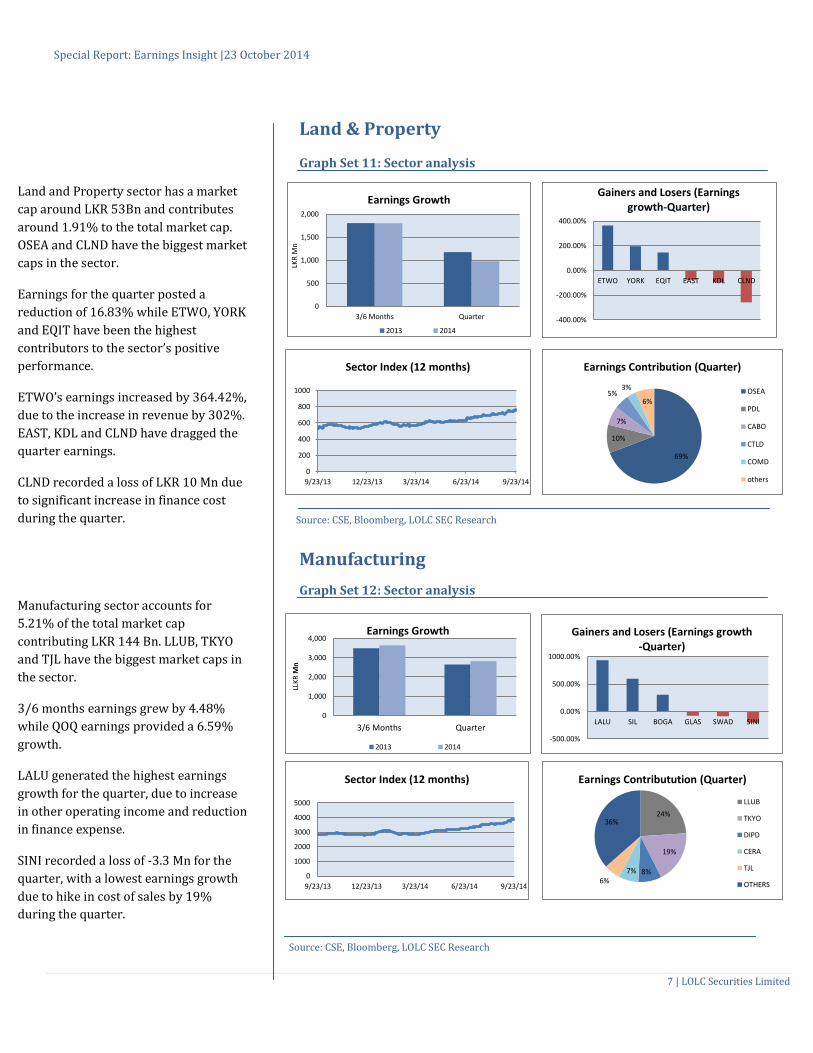

Land & Property Graph Set 11: Sector analysis

Source: CSE, Bloomberg, LOLC SEC Research

Manufacturing

Graph Set 12: Sector analysis Source: CSE, Bloomberg, LOLC SEC Research

Land and Property sector has a market

cap around LKR 53Bn and contributes

around 1.91% to the total market cap.

OSEA and CLND have the biggest market

caps in the sector.

Earnings for the quarter posted a

reduction of 16.83% while ETWO, YORK

and EQIT have been the highest

contributors to the sector’s positive

performance.

ETWO’s earnings increased by 364.42%,

due to the increase in revenue by 302%.

EAST, KDL and CLND have dragged the

quarter earnings.

CLND recorded a loss of LKR 10 Mn due

to significant increase in finance cost

during the quarter.

Manufacturing sector accounts for

5.21% of the total market cap

contributing LKR 144 Bn. LLUB, TKYO

and TJL have the biggest market caps in

the sector.

3/6 months earnings grew by 4.48%

while QOQ earnings provided a 6.59%

growth.

LALU generated the highest earnings

growth for the quarter, due to increase

in other operating income and reduction

in finance expense.

SINI recorded a loss of -3.3 Mn for the

quarter, with a lowest earnings growth

due to hike in cost of sales by 19%

during the quarter.

Special Report: Earnings Insight |23 October 2014

8 | LOLC Securities Limited

0

200

400

600

800

3/6 Months QuarterLK

R M

n

Earnings Growth

2013 2014 -100.00%

0.00%

100.00%

200.00%

300.00%

COLO AUTO DIMO SMOT ASHO UML

Gainers and Losers ( Earnings growth -Quarter)

10000

12000

14000

16000

18000

20000

9/23/13 12/23/13 3/23/14 6/23/14 9/23/14

Sector Index -12 months

-100.00%

-50.00%

0.00%

50.00%

100.00%

150.00%

BUKI SELI SHAL GOOD INDO

Gainers and Losers (Earnings Growth -Quarter)

46%

31%

10%

7%

4% 2%

Earnings Contribution (Quarter)

UML

COLO

SMOT

DIMO

ASHO

OTHERS

0

500

1,000

1,500

3/6 Months Quarter

LKR

Mn

Earnings Growth

2013 2014

0

20000

40000

60000

80000

100000

120000

140000

9/23/13 12/23/13 3/23/14 6/23/14 9/23/14

Sector Index (12 months)

90%

2% 2% 2% 4%

Earnings Contribution (Quarter)

BUKI

SELI

SHAL

GOOD

INDO

Motors Graph Set 13: Sector analysis

Source: CSE, Bloomberg, LOLC SEC Research

Oil Palms

Graph Set 14: Sector analysis

Source: CSE, Bloomberg, LOLC SEC Research

Motors sector has a market cap of LKR

26Bn (0.96% of the total market cap).

UML, ASHO and DIMO are the biggest

counters in term of market cap.

All the counters (except UML, ASHO)

posted earning growths while COLO have

turned around. However the sector

performance has been dragged down by

profit decline of UML.

COLO’s earnings for the quarter

increased due to increase in sales by 29%

and other gains by 7379%.

UML recorded a negative growth in

earnings of 65% mainly due to decrease

in sales revenue, income sources and

finance income and increase in

distribution expenses.

Oil Palm sector has a market cap of LKR

124Bn (4.48% of the market cap). BUKI

has the biggest market cap while all the

other companies come under the same

group of BUKI.

QOQ and period earnings showed a

growth of 25.73% mainly due to

increase in earnings in BUKI by

120.50%.

Other companies such as SELI, SHAL,

GOOD and INDO recorded negative

earnings growth for the quarter.

Special Report: Earnings Insight |23 October 2014

9 | LOLC Securities Limited

0

1,000

2,000

3,000

3/6 Months Quarter

LKR

Mn

Earnings Growth

2013 2014

-200.00%

-100.00%

0.00%

100.00%

LGL LIOC VLL VPEL PAP HPWR

Gainers and Losers (Earnings Growth- Quarter)

100

120

140

160

180

9/23/13 12/23/13 3/23/14 6/23/14 9/23/14

Sector Index (12 months)

500

600

700

800

900

9/23/13 12/23/13 3/23/14 6/23/14 9/23/14

Sector Index (12 months)

-500

0

500

1,000

3/6 Months Quarter

LKR

Mn

Earnings Growth

2013 2014-1000.00%

0.00%

1000.00%

2000.00%

3000.00%

4000.00%

UDPL WATA TPL KGAL KOTA KVAL

Gainers and Losers (Earnings Growth - Quarter)

30%

12%

11% 10%

9%

28%

Earnings Contribution (Quarter)

WATA

MAL

ELPL

HAPU

UDPL

OTHERS

68%

19%

9%

2% 1% 1%

Earnings Contribution (Quarter)

LIOC

LGL

VPEL

VLL

FLCH

PAP

Plantations

Graph Set 15: Sector analysis

Source: CSE, Bloomberg, LOLC SEC Research

Power & Energy Graph Set 16: Sector analysis

Source: CSE, Bloomberg, LOLC SEC Research

Plantation sector has a market cap of LKR

27Bn (0.99% of the total market cap)

while WATA, KAHA, KVAL KGAL are the

big cap counters.

3/6 earnings improved by 138.49%

while quarter earnings increased

significantly.

UDPL, WATA and TPL generated highest

earnings growth for the quarter while

KGAL, KOTA and KVAL generated lowest

earnings growth due to the decline in

revenue caused by decrease in rubber

prices.

Main reason for UDPL’s significant profit

growth of 3546% is due to reduction in

cost of sales due to strategies

implemented to make operations more

effective and efficient during the period

under review.

Power and Energy sector has a market

cap of LKR 52Bn (1.90% of the market

cap) while LIOC, LGL and VPEL have the

biggest market caps.

Quarter and 3/6 months period

earnings dropped by 17.63% led by

decline in earnings in HPWR by

167.58%. HPWR generated a loss of

68.89 Mn , mainly owing to the loss of

Rs.77 million in its joint venture with

Heladhanavi.

Only LGL has achieved an earnings

growth for the quarter while other

counters have experienced a decline in

earnings growth.

Special Report: Earnings Insight |23 October 2014

10 | LOLC Securities Limited

-100.00%

-50.00%

0.00%

50.00%

100.00%

HUNT GEST EBCR

Gainers and Losers (Earnings Growth-Quarter)

-300

-200

-100

0

3/6 Months Quarter

LKR

Mn

Earnings Growth

2013 2014

-50.00%

0.00%

50.00%

100.00%

150.00%

200.00%

LPRT MSL CTBL JKL

Gainers and Losers (Earnings Growth- Quarter)

0

5000

10000

15000

20000

25000

30000

9/23/13 12/23/13 3/23/14 6/23/14 9/23/14

Sector Index (12 month)

0

5000

10000

15000

20000

25000

30000

9/23/13 12/23/13 3/23/14 6/23/14 9/23/14

Sector Index (12 months)

45

50

55

60

3/6 Months Quarter

LKR

Mn

Earnings Growth

2013 2014

76%

17%

7%

Earnings Contribution (Quarter)

JKL

CTBL

LPRT

93%

5% 2%

Revenue for the period

EBCR

HUNT

GEST

Services Graph Set 17: Sector analysis

Source: CSE, Bloomberg, LOLC SEC Research

Stores & Supplies

Graph Set 18: Sector analysis Source: CSE, Bloomberg, LOLC SEC Research

Services Sector has a market

capitalization of LKR 6.8Bn (0.25%),

while JKL and CTBL consist of highest

market cap of the sector.

Sector performance for the quarter as

well as for the period posted positive

growth.

LPRT generated the highest earnings

growth for the quarter with a profit of

LKR 6.266 Mn due to increase in revenue

and other income sources.

Market Capitalization of Stores &

Supplies sector amounts to LKR 5.5 Bn

while EBCR and HUNT being the big cap

counters of the sector.

Quarter earnings as well as 3/6

earnings showed a decrease in losses.

EBCR generated a loss of -86.28Mn due

to increase in admin, distribution,

finance and other expenses.

Note: PHAR’s revenue has not been considered since it is a small

figure when compared with other counters.

MSL has been ignored due to negative earnings contribution

during the quarter

Special Report: Earnings Insight |23 October 2014

11 | LOLC Securities Limited

100

150

200

250

09/23/13 12/23/13 03/23/14 06/23/14 09/23/14

Sector Index (12 months)

60%

40%

Earnings Contribution (Quarter)

SLTL

DIAL

11000

13000

15000

17000

9/23/13 12/23/13 3/23/14 6/23/14 9/23/14

Sector Index (12 months)

0

500

1,000

1,500

3/6 Months Quarter

LKR

Mn

Earnings Growth

2013 2014

0.00%

50.00%

100.00%

150.00%

200.00%

250.00%

DIAL SLTL

Gainers and Losers (Earnings Growth-Quarter)

0

2,000

4,000

6,000

8,000

3/6Months Quarter

LKR

Mn

Earnings Growth

2013 2014

45%

42%

11%

2%

Earnings Contribution (Quarter)

BRWN

SINS

CWM

CFT

-200.00%

-100.00%

0.00%

100.00%

RGEM SINS CFT BRWN EMER

Gainers and Losers (Earnings Growth- Quarter)

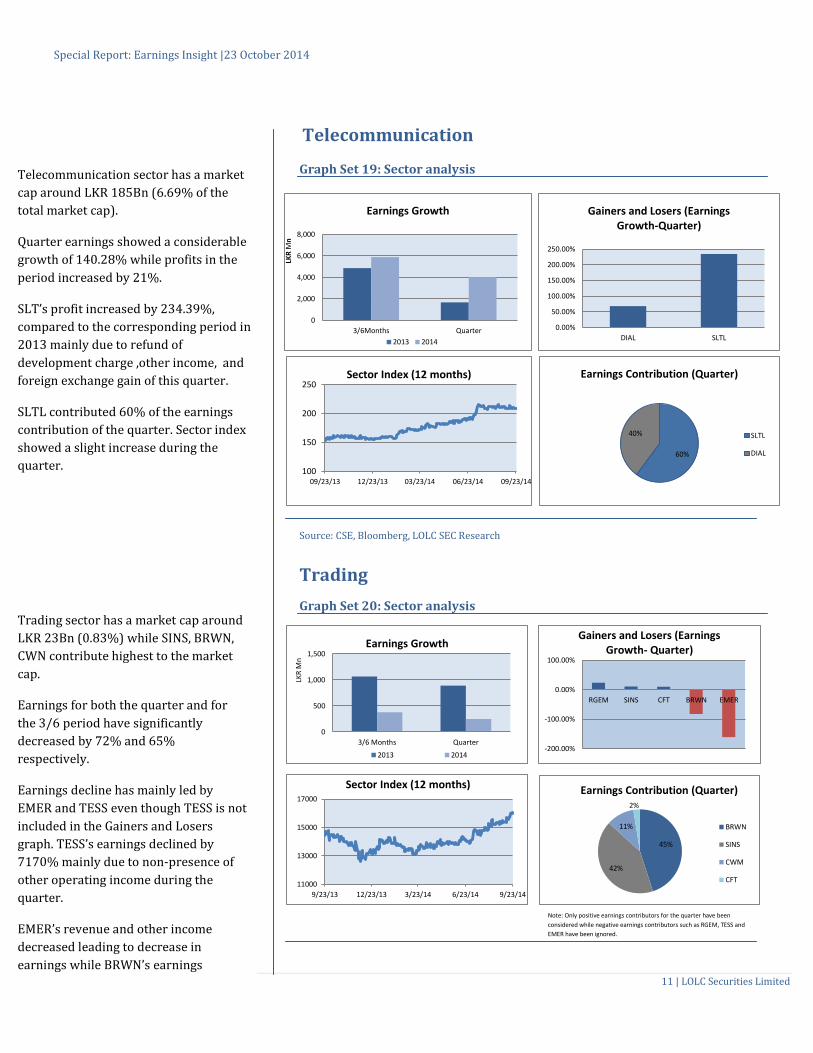

Telecommunication Graph Set 19: Sector analysis

Source: CSE, Bloomberg, LOLC SEC Research

Trading

Graph Set 20: Sector analysis

Source: CSE,

Telecommunication sector has a market

cap around LKR 185Bn (6.69% of the

total market cap).

Quarter earnings showed a considerable

growth of 140.28% while profits in the

period increased by 21%.

SLT’s profit increased by 234.39%,

compared to the corresponding period in

2013 mainly due to refund of

development charge ,other income, and

foreign exchange gain of this quarter.

SLTL contributed 60% of the earnings

contribution of the quarter. Sector index

showed a slight increase during the

quarter.

Trading sector has a market cap around

LKR 23Bn (0.83%) while SINS, BRWN,

CWN contribute highest to the market

cap.

Earnings for both the quarter and for

the 3/6 period have significantly

decreased by 72% and 65%

respectively.

Earnings decline has mainly led by

EMER and TESS even though TESS is not

included in the Gainers and Losers

graph. TESS’s earnings declined by

7170% mainly due to non-presence of

other operating income during the

quarter.

EMER’s revenue and other income

decreased leading to decrease in

earnings while BRWN’s earnings

decreased mainly due to decline in other

income, increase in other expenses and

negative fair valuation in the investment

properties.

Note: Only positive earnings contributors for the quarter have been

considered while negative earnings contributors such as RGEM, TESS and

EMER have been ignored.

Special Report: Earnings Insight |23 October 2014

12 | LOLC Securities Limited

Contact us

LOLC Securities Limited, a trading member of the Colombo Stock Exchange (CSE), is engaged in facilitating stock trading transactions at Colombo Stock Exchange,

providing investment research on Sri Lankan equity, providing investment planning advices with services such as portfolio construction & formulation of IPS

(Investment Policy Statement) and facilitating other investment opportunities in the country including private equity.

Disclaimer: This report is based on information from sources that LOLC Securities Limited believes to be reliable. Whilst reasonable care has been taken to ensure

accuracy of the information presented in the report, LOLC Securities Limited does not give a guarantee on the accuracy of the information presented in the paper nor

will take the responsibility on investment decisions taken based on the information provided by the report and hence LOLC Securities Limited nor its employees

accepts any liability whatsoever for any loss arising from investments decisions taken using the information provided in this paper. The reader also should note this

paper does not give recommendations to any particular category of investors and investor should consult investment advisors for further clarifications regarding risks

involved in investing in equity market. LOLC Securities Limited or its employees may or may not hold positions in the securities discussed in the report and the

information provided in the report should not be construed as a buy or sell instruction for any securities mentioned in the report.

LOLC SEC Research Reports are also available at Bloomberg LOLC <GO>

Head Office

LOLC Securities Limited

Level 18, West Tower,

World Trade Center

Colombo 01

Sri Lanka

Tel: +94 11 7880880

Fax: +94 11 2434771

Branches

Kurunegala Branch

No 06, 1st Floor,

Union Assurance Building,

Rajapilla Mawatha

Kurunegala,

Sri Lanka

Tel: +94 377 201221

Fax: +94 372 225511

Galle Branch

No 18,

Sri Dewamitta Mawatha,

Galle

Sri Lanka

Tel : +94 773 409243

Matara Branch

1st Floor,

E.H. Cooray Towers,

No.24,

Anagarika Dharmapala

Mawatha,

Matara, Sri Lanka

Tel: +94 414 936079

Sriyan Gurusinghe CEO/Managing Director

011 7880888 / 077 7891871 sriyang@ lolcsecurities.com

SALES Head Office

Maniesh Rodrigo Assistant General Manager 011 7880805 / 077 7896064 manieshr@ lolcsecurities.com

Samadhi Jayasinghe Manager Institutional Sales 011 7880806 / 077 3954993 samadhij@ lolcsecurities.com

Dinusha Gomes Assistant Manager – International Sales 011 7880812 / 077 1562193 dinushago@ lolcsecurities.com

Imesh Fernando Senior Investment Advisor 011 7880814 / 077 3954992 imeshf@ lolcsecurities.com

Balendiran Janegan Senior Investment Advisor 011 7880811 / 077 5619827 janeganb@ lolcsecurities.com

Naleen Sadeesh Investment Advisor 011 7880839 / 077 2383209 naleensa@ lolcsecurities.com

Damith Chaminda

Investment Advisor 011 7880819 / 077 3367313 damithc@ lolcsecurities.com

Dinuka Niwantha

Investment Advisor 011 7880838 / 077 3947928 dinukan@ lolcsecurities.com

Niraj Jayamanne Investment Advisor 011 7880813 / 077 5965645 [email protected]

Kurunegala Branch

Rohana Chandrasiri Assistant General Manager 037 7201221 / 077 3623001 rohanac@ lolcsecurities.com

Anurudda Rajakaruna Investment Advisor 037 7201221 / 077 3409464 anuruddhar@ lolcsecurities.com

Nuwan Fernando Investment Advisor 037 7201221 / 077 8365921 nuwanfe@ lolcsecurities.com

Galle Branch

Bimal Malinda Branch Head 091 7200852/ 077 3409243 bimalm@ lolcsecurities.com

Matara Branch

Lalinda Liyanapathirana Investment Advisor 041 4936079/ 077 3692257 lalindal@ lolcsecurities.com

Ahamed Aadil Investment Advisor 041 4936079/ 077 7538986 aadila@ lolcsecurities.com

RESEARCH

Shehan Bartholomeuz Head of Research 011 7880835 / 077 7699148 shehanb@ lolcsecurities.com

Damith Wasantha Research Analyst 011 7880837 / 077 7519416 damithwa@ lolcsecurities.com

Hiruni Perera Associate Research Analyst 011 7880809 / 077 4805784 hirunipe@ lolcsecurities.com

Rehan Ariyaratne Business Development Asosciate 011 7880831/ 0765446255 [email protected]