Embed Size (px)

Citation preview

1

Earned Value Management Principles & Techniques

FACILITATOR: Kevin in’t Veld PMP ([email protected]) LDP (Cum Laude) UNISA 17+ years Experience in Project Management & Controls serving

Construction, Engineering, Mining, Military and others

Why?

The Project Life - Cycle

Excitement

Reality Check

Panic

Blame the innocent

Praise the non-participants

Why Does Project Management Fail

Standish Research

189% Cost Overruns

222% Time Overruns

Why Does Project Management Fail

Why do Projects Fail

3 Major Reasons

Why Does Project Management Fail

Poor Scope Management

Poor Planning Poor Systems Integration

Why do Projects Fail

Admin Stakeholders Competent Priorities Commitment

Poly Ticks

Why Does Project Management Fail

Earned Value Management (EVM)

“Aim for nothing, and you’ll hit it

every time.”- Shawn Sherrick

17

EVMS Quotable’ s

“That which gets measured, gets

done.”- Tom Peters

What is EVM?

CollectionBest

Management Practices

Measure

Analyse

Variance

Project End

What is EVM?

Integrates Scope Schedule

Cost Planning and Control Decisions

EVMS Principles

Baseline Scope WBS Breakdown Performance

Control changes to the baseline

EVMS Principles

Integration

Scope Cost Time

EVMS Principles

IMMEDIATELY

23

EVMS Principles (cont)

Use actual costs incurred and recorded for accomplishing the work performed

Objectively assess accomplishments at the work performance level

Analyze significant variances from the plan, forecastimpacts, and prepare an estimate at completion based on performance to date and work to be performed

24

Early 1900’s – Value of factory output compared to actual unit cost and planned output

1959 - PERT / Time & Cost (Polaris)

1963 - Earned Value Concept (Minuteman)

History of EVMS

History of EVMS

1967 - Cost / Schedule Control System Criteria (C/SCSC) (DOD 7000.2)

• A DOD and DOE set of 35 criteria relating to Cost & Schedule Management

EVMS Criteria 1996 - National Security Industrial Association (private industry) developed the:

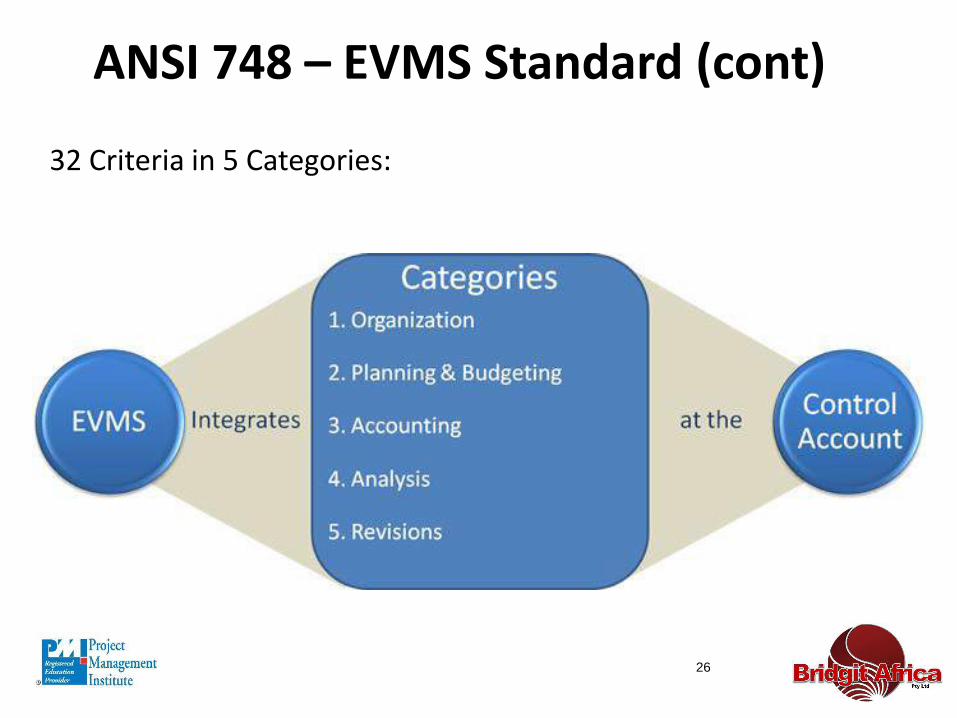

ANSI – 5 Categories

ANSI – 32 Criteria

26

32 Criteria in 5 Categories:

ANSI 748 – EVMS Standard (cont)

27

ANSI 748 – EVMS Standard

Early Warning System

• Course corrections are easier to make when you have time to make small adjustments

• It’s too late when your next to the iceberg

Management by Exception

• Focus on the areas that are not performing

Good news should travel fast, bad news should travel faster

Why EVMS

29

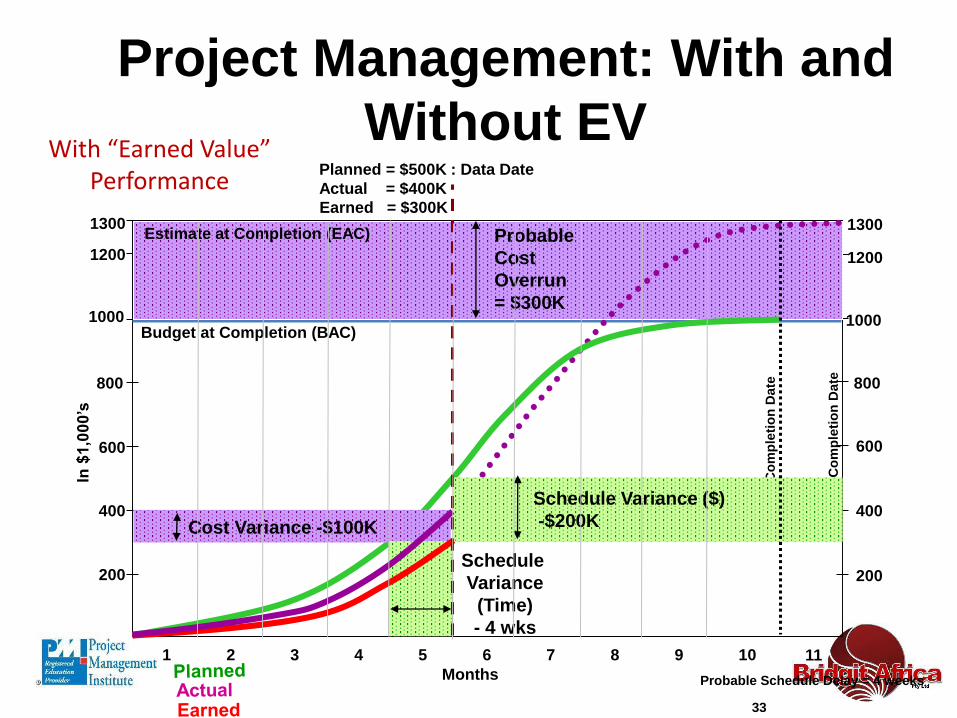

Project Management: With and Without EV

Project Management with EV has clear difference to the Traditional Management approach (without EV)

Project Management with EV seeks to accomplish work within the customer’s parameters of scope, cost, and schedule, called

the Performance Measurement Baseline (PMB)

Project Management with EV utilizes tools and techniques to evaluate performance against the PMB and to forecast future performance based on trending

30

Traditional Management: Without EV

Planned costs are compared to actual costs

• Actual to-date costs less the planned to-date costs (under-run) seemingly indicates a healthy project and an expectation that the project will complete under-budget

• Planned Progress is compared to Actual Progress

“ Well start digging from this side of the mountain. You and your gang start digging from the other side. When we meet in the middle, we will have made a tunnel. And if

we don’t meet, we will have made two

tunnels”.

32

Conventional Progress“Without EV”

Months

In $

1,0

00’s

Budget at Completion (BAC)

1 2 3 4 5 6 7 8 9 10

Tar

get

Co

mp

leti

on

Dat

e

200

400

600

800

1000

1200

11

1300

Planned = $500K : Data DateActual = $400K

200

400

600

800

1000

1200

1300

Project Management: With and Without EV

33

With “Earned Value” Performance

In $

1,0

00’s

Budget at Completion (BAC)

1 2 3 4 5 6 7 8 9 10Months

Tar

get

Co

mp

leti

on

Dat

e

200

400

600

800

1000

1200

11

1300

Planned = $500K : Data DateActual = $400K

200

400

600

800

1000

1200

1300

Cu

rren

t C

om

ple

tio

n D

ate

Probable Schedule Delay = 4 weeks

Probable CostOverrun= $300K

Estimate at Completion (EAC)

Cost Variance -$100K

Schedule Variance

(Time)- 4 wks

Schedule Variance ($)-$200K

Earned = $300K

Project Management: With and Without EV

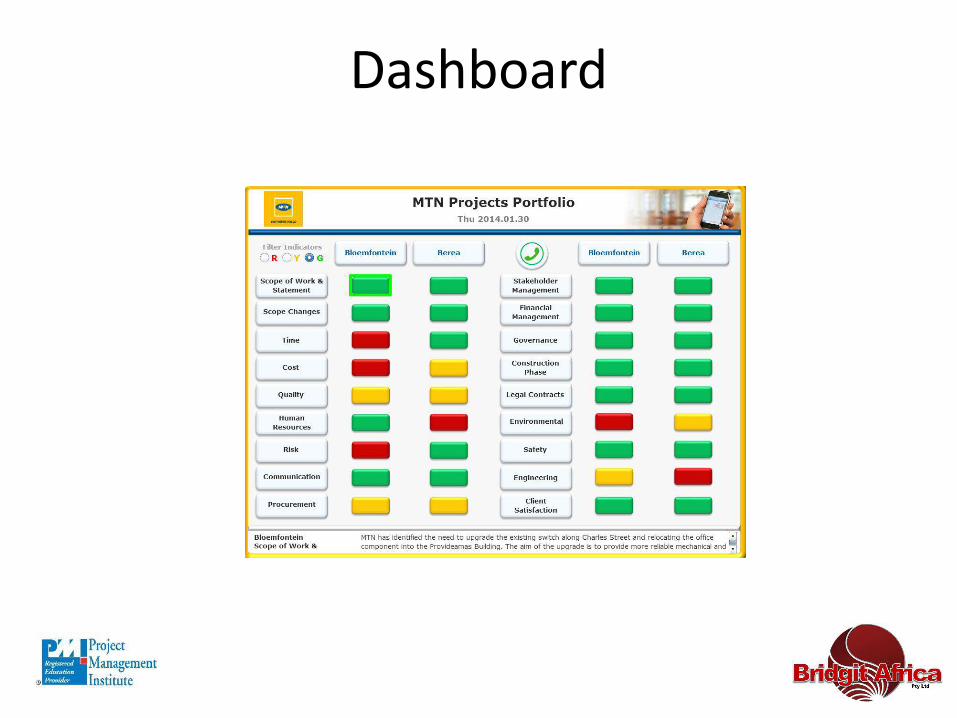

Dashboard

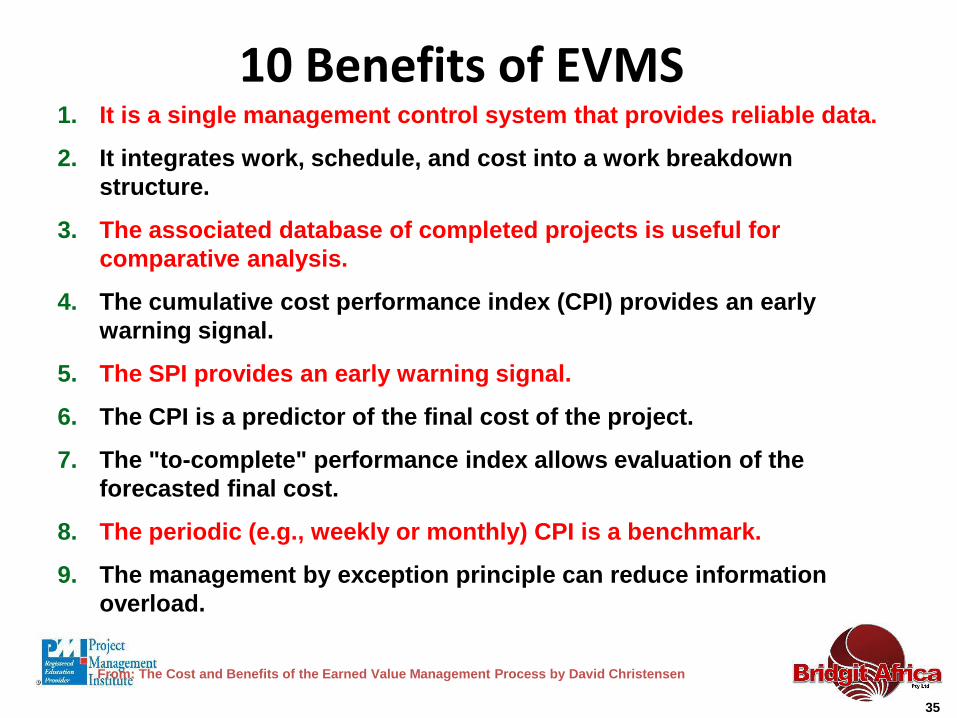

1. It is a single management control system that provides reliable data.

2. It integrates work, schedule, and cost into a work breakdown structure.

3. The associated database of completed projects is useful for comparative analysis.

4. The cumulative cost performance index (CPI) provides an early warning signal.

5. The SPI provides an early warning signal.

6. The CPI is a predictor of the final cost of the project.

7. The "to-complete" performance index allows evaluation of the forecasted final cost.

8. The periodic (e.g., weekly or monthly) CPI is a benchmark.

9. The management by exception principle can reduce information overload.

35

10 Benefits of EVMS

From: The Cost and Benefits of the Earned Value Management Process by David Christensen

36

EVM Can and Should be Utilized!

• Should not be seen as a cost driver

• Should not be seen as a cost saver!

• Should always make common sense

• Should always reflect how projects are managed on a daily basis

The Bottom Line

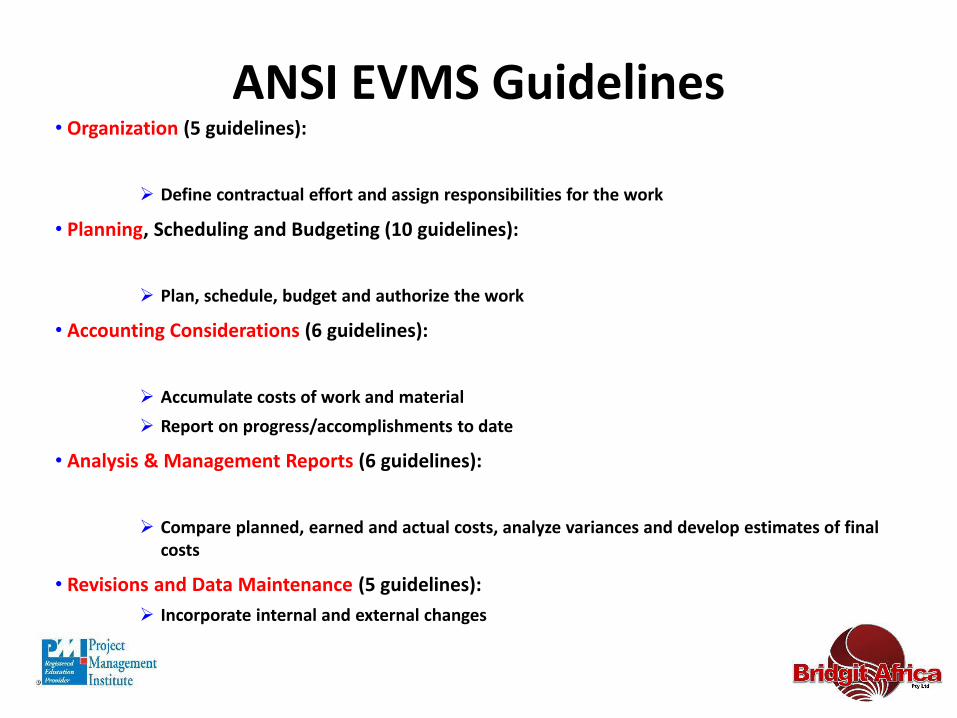

ANSI/EIA -748EVMS 32 Guidelines

ANSI EVMS Guidelines• Organization (5 guidelines):

Define contractual effort and assign responsibilities for the work

• Planning, Scheduling and Budgeting (10 guidelines):

Plan, schedule, budget and authorize the work

• Accounting Considerations (6 guidelines):

Accumulate costs of work and material

Report on progress/accomplishments to date

• Analysis & Management Reports (6 guidelines):

Compare planned, earned and actual costs, analyze variances and develop estimates of final costs

• Revisions and Data Maintenance (5 guidelines):

Incorporate internal and external changes

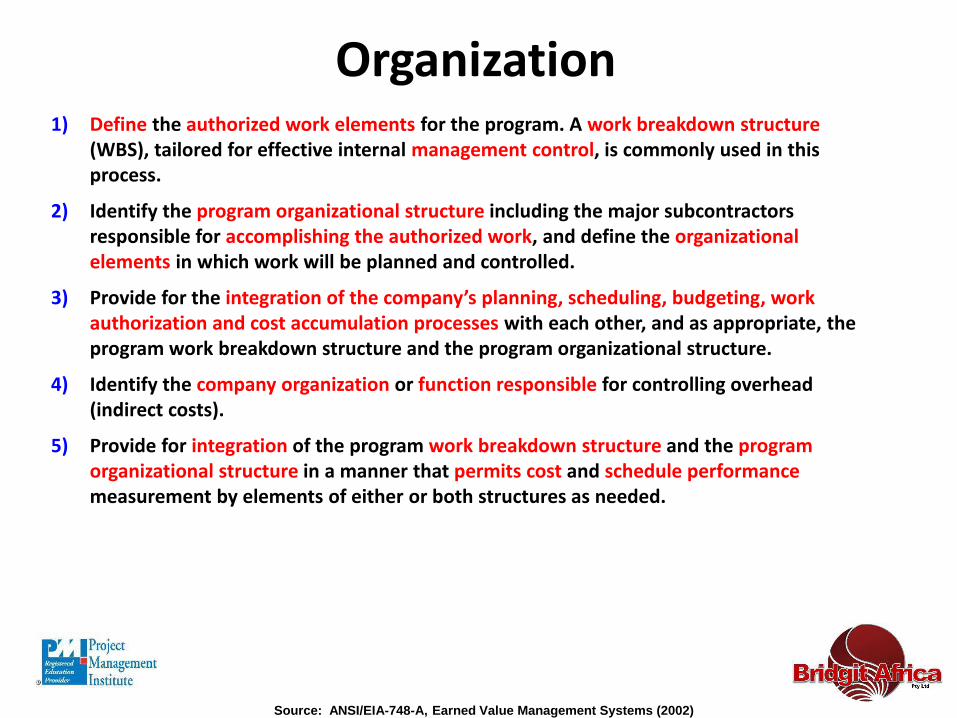

Organization1) Define the authorized work elements for the program. A work breakdown structure

(WBS), tailored for effective internal management control, is commonly used in this process.

2) Identify the program organizational structure including the major subcontractors responsible for accomplishing the authorized work, and define the organizational elements in which work will be planned and controlled.

3) Provide for the integration of the company’s planning, scheduling, budgeting, work authorization and cost accumulation processes with each other, and as appropriate, the program work breakdown structure and the program organizational structure.

4) Identify the company organization or function responsible for controlling overhead (indirect costs).

5) Provide for integration of the program work breakdown structure and the programorganizational structure in a manner that permits cost and schedule performance measurement by elements of either or both structures as needed.

Source: ANSI/EIA-748-A, Earned Value Management Systems (2002)

Planning, Scheduling, and Budgeting

1) Schedule the authorized work in a manner which describes the sequence of work and identifies significant task interdependencies required to meet the requirements of the program.

2) Identify physical products, milestones, technical performance goals, or other indicators that will be used to measure progress.

3) Establish and maintain a time-phased budget baseline, at the control account level, against which program performance can be measured. Initial budgets established for performance measurement will be based on either internal management goals or the external customer negotiated target cost including estimates for authorized but undefined work. Budget for far-term efforts may be held in higher level accounts until an appropriate time for allocation at the control account level.

4) Establish budgets for authorized work with identification of significant cost elements (labor, material, etc.) as needed for internal management and for control of subcontractors.

5) To the extent it is practicable to identify the authorized work in discrete work packages, establish budgets for this work in terms of dollars, hours, or other measurable units. Where the entire control account is not subdivided into work packages, identify the far term effort in larger planning packages for budget and scheduling purposes.

Source: ANSI/EIA-748-A, Earned Value Management Systems (2002)

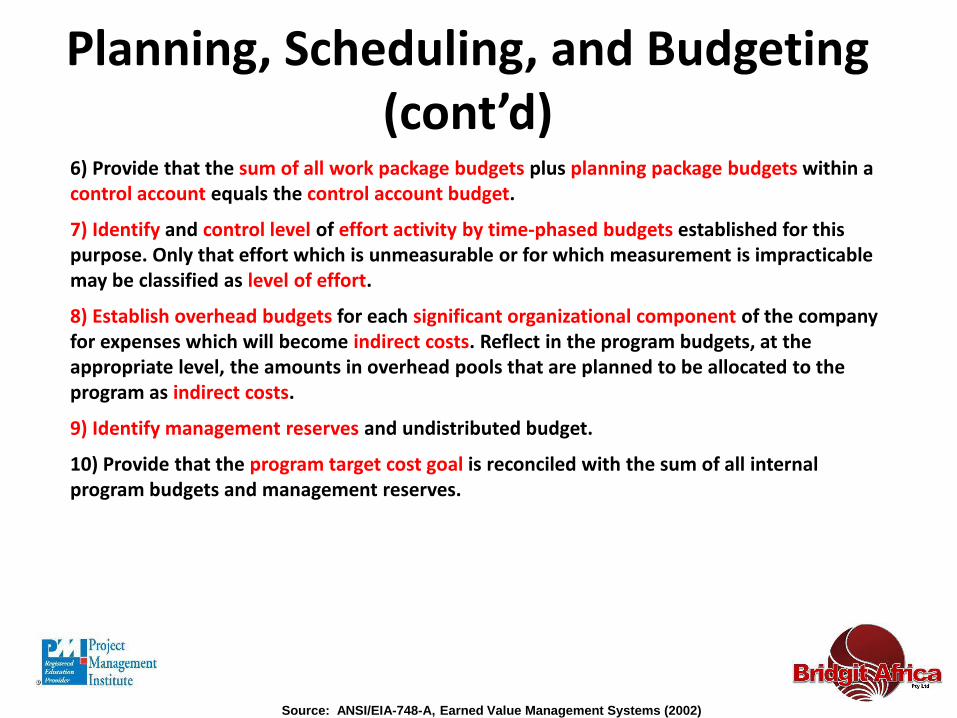

Planning, Scheduling, and Budgeting (cont’d)

6) Provide that the sum of all work package budgets plus planning package budgets within a control account equals the control account budget.

7) Identify and control level of effort activity by time-phased budgets established for this purpose. Only that effort which is unmeasurable or for which measurement is impracticable may be classified as level of effort.

8) Establish overhead budgets for each significant organizational component of the company for expenses which will become indirect costs. Reflect in the program budgets, at the appropriate level, the amounts in overhead pools that are planned to be allocated to the program as indirect costs.

9) Identify management reserves and undistributed budget.

10) Provide that the program target cost goal is reconciled with the sum of all internal program budgets and management reserves.

Source: ANSI/EIA-748-A, Earned Value Management Systems (2002)

Accounting Considerations1) Record direct costs in a manner consistent with the budgets in a formal system controlled by the general books of account.

2) When a work breakdown structure is used, summarize direct costs from control accounts into the work breakdown structure without allocation of a single control account to two or more work breakdown structure elements.

3) Summarize direct costs from the control accounts into the contractor’s organizational elements without allocation of a single control account to two or more organizational elements.

4) Record all indirect costs which will be allocated to the contract.

5) Identify unit costs, equivalent unit costs, or lot costs when needed.

6) For EVMS, the material accounting system will provide for:

Accurate cost accumulation and assignment of costs to control accounts in a manner consistent with the budgets using recognized, acceptable, costing techniques.

Cost performance measurement at the point in time most suitable for the category of material involved, but no earlier than the time of progress payments or actual receipt of material.

Full accountability of all material purchased for the program including the residual inventory.

Source: ANSI/EIA-748-A, Earned Value Management Systems (2002)

Analysis and Management Reports1) At least on a monthly basis, generate the following information at the control account and other levels as necessary for management control using actual cost data from, or reconcilable with, the accounting system:

Comparison of the amount of planned budget and the amount of budget earned for work accomplished. This comparison provides the schedule variance.

Comparison of the amount of the budget earned and the actual (applied where appropriate) direct costs for the same work. This comparison provides the cost variance.

2) Identify, at least monthly, the significant differences between both planned and actual schedule performance and planned and actual cost performance, and provide the reasons for the variances in the detail needed by program management.

3) Identify budgeted and applied (or actual) indirect costs at the level and frequency needed by management for effective control, along with the reasons for any significant variances.

4) Summarize the data elements and associated variances through the program organization and/or work breakdown structure to support management needs and any customer reporting specified in the contract.

5) Implement managerial actions taken as the result of earned value information.

6) Develop revised estimates of cost at completion based on performance to date, commitment values for material, and estimates of future conditions. Compare this information with the performance measurement baseline to identify variances at completion important to company management and any applicable customer reporting requirements including statements of funding requirements.

Source: ANSI/EIA-748-A, Earned Value Management Systems (2002)

Revisions & Data Management

1) Incorporate authorized changes in a timely manner, recording the effects of such changes in budgets and schedules. In the directed effort prior to negotiation of a change, base such revisions on the amount estimated and budgeted to the program organizations.

2 Reconcile current budgets to prior budgets in terms of changes to the authorized work and internal replanning in the detail needed by management for effective control.

3) Control retroactive changes to records pertaining to work performed that would change previously reported amounts for actual costs, earned value, or budgets. Adjustments should be made only for correction of errors, routine accounting adjustments, effects of customer or management directed changes, or to improve the baseline integrity and accuracy of performance measurement data.

4) Prevent revisions to the program budget except for authorized changes.

5) Document changes to the performance measurement baseline.

Source: ANSI/EIA-748-A, Earned Value Management Systems (2002)

EVM Systems

EVM Systems