-

8/6/2019 Draft Study Bulgaria

1/23

DRAFT/7 December 2004

UNITED NATIONS CONFERENCE ON TRADE AND DEVELOPMENT

BULGARIA: EXPERIENCE IN SYSTEMIC TRANSITIONAND REFORMS

CASE STUDY

DFID/UNCTAD Joint Project "Supporting Developing Countries'

Assessment of the Non-Agricultural Market Access Negotiations"

Geneva, 2004

-

8/6/2019 Draft Study Bulgaria

2/23

2

TABLE OF CONTENTS

I. Introduction and overview of the country

________________________________ 3

Introduction

_______________________________________________________________

3

1. Economic and trade environment

_______________________________________ 3

2. Role of trade in Bulgarias

economy________________________________ 10

II. Trade liberalization and its economic impacts

___________________________ 12

1. Trade liberalization

process_______________________________________ 12

2. Economic impact

_____________________________________________________ 18

III. Policy lessons and implications

_______________________________________ 21

1. Conclusions and Policy lessons

________________________________________ 21

2. Major country issues in current Doha

negotiations____________________ 21

References

Annexes: Tables

-

8/6/2019 Draft Study Bulgaria

3/23

3

I. Introduction and overview of the country

Introduction

Bulgaria has been undergoing almost 15 years of profound reforms

in the process

of transition to a market economy from a previously

centrally-planned system, in whichtrade liberalization and

integration in the multilateral trading system were among

toppriorities as major elements of the reform strategy. The country

is also pursuing its maincurrent strategic goal to accede to the

European Union (EU) by 1 January 2007. On thisway, Bulgarias

accession to the World Trade Organization in December 1996 was

animportant milestone. Thus, Bulgarias has a rather comprehensive

and unique experiencethat may be of substantial interest to

developing and other transition countries.

This paper attempts to present, explain and analyze Bulgarias

case in the contextof the DFID/UNCTAD Joint Project "Supporting

Developing Countries' Assessment of the Non-Agricultural Market

Access Negotiations".

1. Economic and trade environment

(i) Main features of the economy

Population

The population of Bulgaria went on contracting in the beginning

of the XXI st century. In 2001 1, some 7 932 984 people resided

permanently in the country. Thepopulation of Bulgaria had decreased

by 544 333 people relative to the previous censuscarried out on 4

December 1992. The population decrease - the most dramatic since

the

Second World War was the second in a row monitored since the

1980s.2

The ageing of Bulgarias population has been persisting as a

result of the

unfavourable trends of development of demographic processes in

the last three decades.In 2001, the share of population aged under

15 years declined to 15.2% (1 216 841people) of the entire

population. In contrast, the share of persons aged over 65

reached17.4% of the population. In absolute terms, working age

population contracted to5 382 804 persons since 1992, but its

relative share rose by 1.1 percentage point to 67.4%of the

population total.

GDP growth and per capita

Following negative real GDP growth in 1996 and 1997, the

Bulgarianeconomy kept on growing between 1998 and 2003 by around 4%

on average. RealGDP growth in 2003 was evaluated at 4.3%. Against

this background, it is worth

1 The latest official census was carried out by NSI on 1 March

2001. According to NSI estimates,Bulgarias population amounted to 7

973 671 people as of 31 December 2001.2 The first intercensal

population decrease was reported in the period 1986-1992 amounting

to some 460000 people.

-

8/6/2019 Draft Study Bulgaria

4/23

4

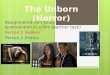

mentioning that in the earlier stage of transition, GDP fell

almost steadily through 1997, whenit was 40 percent below its 1990

level.

40

50

60

70

80

90

100

110

120

1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

2002

Real GDP Employment Consumption Gross Fixed Capital

Formation

Trends in selected macroeconomic variables, 1989-2002

a

Source:

Indices, 1989=100 for all variables except gross fixed capital

formation where 1990=100.

UNECE Common Database; 2001 and 2002 data based on projections

from AEAF (2003).

Index 1989=100 a

In terms of real GDP per capita (in euro, PPS 3), Bulgaria with

euro 6 500 PPS(US$7,059) is reaching only 27.9% of the average per

capita GDP in the EU. At marketexchange rate, GDP per capita was

US$1,986 in 2002.

Education

One of Bulgarias main assets is a relatively well-educated and

trained workforce,in particular regarding engineering and natural

sciences, while there is less of a traditionin social sciences and

management. 75.6% of young people aged 20 to 24 haveattained at

least upper secondary education attainment level. The main

challenge in theeducation sector is to adjust the system to a

declining school-age population

following the general demographic decline and emigration, among

whom many bettereducated and younger people. A further weakness is

that the education system producesgraduates with qualifications

which do not always match the demand of the labourmarket. Education

spending increased from a crisis-related low of 2.6% in 1997 to

3.7%of GDP in 2001, which is still a fairly low rate by

international comparison.

3 Purchasing Power Standard.

-

8/6/2019 Draft Study Bulgaria

5/23

-

8/6/2019 Draft Study Bulgaria

6/23

6

industry has remained at between 28% and 30% over this period,

services haveexpanded from 44% in 1997 to 59% in 2003. This

sectoral shift was much lesspronounced in terms of employment, with

employment in agriculture increasingfrom 25% to 28% and in services

from 43% to 45%, while there was a decrease inindustrial employment

from 32% to 28%.

Table A. Bulgaria - Selected Indicators of Economic Structure

(2003)

Population (average) Million 7.82 GDP per headof EU-25

average

PPS%

628029.4

Gross fixed capital formation % of GDP 19.6Gross foreign debt of

the whole economy % of GDP 49.4Exports of goods and services % of

GDP 53.2Stock of foreign direct investment Million

per head 5583695

Employment rate % of 25-64 age group 52.5Long-term unemployment

rate % of labour force 8.9Source: Eurostat

(ii) Overview of recent economic developments

Following the severe economic crisis in 1996-97, the currency

boardarrangement (CBA) introduced in July 1997 and economic reforms

have been crucialfor stabilizing the economy on a continued growth

path. The CBA has been underpinnedby a conservative fiscal policy

and a sharp acceleration of structural reforms thatencompassed

agriculture, energy, privatization, completing price and trade

liberalization,

reform of the social sectors and restructuring and financial

discipline in the enterprisesector.

Since then, substantial progress has been made in the

restructuring of theeconomy. A large number of state-owned

enterprises have been sold or liquidated,but several major

enterprises still remain to be privatized. The financial sector

isnow basically completely in private hands and to a large extent

foreign-owned.Conditions for business in Bulgaria have improved

although substantial efforts arestill required to enhance the

efficiency of the public administration and judicial systemsand the

regulatory environment, and in particular to improve the prospects

for smalland medium-sized enterprises.

The reforms implemented since 1997 have been ambitious by any

standards, butthere are visible signs of reform fatigue in the

population. While there is a broadpolitical consensus on the

fundamentals of economic policies, such as maintaining thecurrency

board arrangement and preparing for EU accession, there are

diverging viewsbetween political parties about the affordability of

alleviating the social consequences.Opinion polls suggest that many

people in Bulgaria fail to see progress in their

economicsituation.

-

8/6/2019 Draft Study Bulgaria

7/23

7

The recovery of the economy after 1997 was accompanied by an

increase of the

BoP current account deficit. In 2001, the current account

deficit had risen to 6.2% of GDP (i.e. close to the levels at the

start of transition) from 0.5% of GDP in 1998 mainlydue to the

deterioration of the trade in goods deficit, indicative of the

insufficientcompetitiveness of the economy. Although financed by

net inflows of foreign directinvestment in most years, the current

account deficit has become a chronic factor,perhaps, reflecting the

inadequate level of competitiveness of the Bulgarian economy. Atits

heart is the high trade deficit (12.5% of GDP in 2003).

Total foreign debt, which is to a large extent a public debt,

declined from 100% of GDP in 1997 to below 60% of GDP at the end of

2003.

Bulgaria heavily relies on the volume of foreign direct

investment (FDI) not onlyfor the financing of the current account

deficit but also for investment in up-to-datetechnologies and

modern enterprise management. Over the 1991-2001, FDI in

Bulgariaamounted to some USD 4 billion. About 60% of total FDI

inflows had come from the EUcountries. Germany, Greece, Belgium and

Italy are currently the largest foreign investorsin Bulgaria. In

the 1990s, the bulk of FDI was directed to manufacturing, trade and

thefinancial sector whereas telecommunications, agriculture and

infrastructure attracted onlya considerably smaller portion of FDI

flows.

The general government deficit has been below 1% of GDP in all

years and was inbalance or in surplus in some years. In 2003, the

general government sector was running acash surplus peaking at 2.8%

of GDP in October, and a similar trend occurred in the firsthalf of

2004 with a surplus of 2.3% of projected GDP.

Table B. Government Revenue Structure (in % of total revenues

and grants)

1998 1999 2000 2001 2002

Tax revenues 79.4 77.3 78.7 77.6 76.6

Income tax 11.5 10.9 9.9 9.0 8.4

Profits tax 9.6 7.6 6.5 9.5 7.6

Indirect taxes (VAT and excises) 28.1 27.0 31.5 30.1 32.0

VAT 20.6 19.9 21.3 20.7 21.5

Customs duties and levies 5.0 2.7 2.0 1.7 1.5

Public social security receipts 22.9 24.5 26.6 25.2 24.6 Other

2.3 4.6 2.2 2.2 2.4

Non-tax revenues 19.0 20.6 19.5 19.3 21.0

Grants 1.6 2.1 1.8 3.1 2.4

Source: Bulgarian Ministry of Finance

-

8/6/2019 Draft Study Bulgaria

8/23

8

Revenues from customs duties have taken a steady downward trend

to account fora decreasing relative share within tax and total

budget revenues. A major reason behindthe contraction in revenues

is caused by the fact that Bulgaria has concluded free

tradeagreements with about 70% of the importers of Bulgarian

goods.

Private ownership has become predominant in the economy. The

share of employees working in the private sector increased from 46%

in 1999 to 73.4% in2003. The private sectors share in gross value

added grew from 63.4% in 1997 to73.3% in 2003. Between January 1993

and June 2004, 5,107 privatization deals wereconcluded.

Bulgarias CPI-based real effective exchange rate (REER) has

recentlyappreciated more rapidly than the currencies of other CEE

countries whose exchangerates are not rigidly pegged to the euro.

However, a comparison with the eurozoneindicates that unit labour

costs (ULCs) in manufacturing have declined strongly. Also,ULCs in

manufacturing decreased, while the manufacturing producer price

index (PPI)

increased, suggesting increasing profitability of Bulgarian

producers of tradables.While economy-wide productivity growth

turned negative in 2003, this partly

reflected government-sponsored employment creation. Productivity

declined only in theservices sector, while it has continued to

increase in manufacturing, above the rate of realwage growth.

However, low wages are also a reflection of Bulgarias apparent lag

behindother CEE countries in qualitative productivity indicators,

as suggested for example inthe recent Lisbon review of

competitiveness.

(iii) Accession to the European Union (EU)

Negotiations on accession to the EU were opened in February 2000

and became amajor factor of Bulgarias economic and trade

environment.

Trade with the EU

According to the latest EU data, the share of the European

Community inBulgarias foreign trade has stabilized in 2003.

Turnover in trade with the EU-15 in 2003was 7.0% up on 2002 and

accounted for 52.4% of Bulgarias overall trade. In 2003,exports to

the EU-15 were 3.1% up on 2002, accounting for 56.5% (3.61 billion)

of Bulgarias total export sales. Its main industrial exports to the

EU-15 were textilesand clothing, iron and steel. Bulgarias

agricultural exports to the EU-15 werecereals, oil seeds and

oleaginous fruit, and meat. In 2003, imports from the EU-15 wereup

by 10.5% on 2002, accounting for 49.6% (4.7 billion) of Bulgarias

total imports.Its main industrial imports from the EU-15 were

textiles and clothing. Its mainagricultural imports from the EU-15

were meat, fats and oils, fruits and nuts.

A new round of trade liberalization for agricultural products

between theCommunity and Bulgaria was concluded at technical level

in June 2004. The newAgreement incorporates existing CEFTA

concessions between Bulgaria and the new

-

8/6/2019 Draft Study Bulgaria

9/23

9

Member States into the Europe Agreement. However, the Agreement

goes further,granting Bulgaria unlimited duty-free access to the

EU25 market for non-sensitiveproducts and covering traditional, and

in some cases potential, Bulgarian exports of sensitive products,

such as live bovines, dairy and cereals, within duty-free tariff

quotas. In March 2004, trade negotiations for a double zero

agreement in the

sector of processed agricultural products were concluded at

technical level betweenBulgaria and Commission representatives. The

main objective of the negotiations was toprogressively prepare

Bulgaria for accession to the EU. The new trade arrangementsprovide

for the immediate or progressive abolition of import duties. In the

case of sensitive products, if not excluded, duty- free quotas are

provided, covering traditionaltrade. The two parties agreed to

implement the new trade arrangements by autonomousmeasures before

the end of 2004.

On the basis of a Council Decision of May 1997, modified in

September 2002,the Commission was mandated to open formal

negotiations with Bulgaria on aPECA (Protocol to the Europe

Agreement on Conformity Assessment and

Acceptance of Industrial Products). Such negotiations are still

continuing.

As regards the common commercial policy, upon accession Bulgaria

will berequired to align its tariffs with those of the EC.

Bulgarias applied tariffs in 2004 wereon average of 12% (MFN Most

Favoured Nation) on all products. Applied tariffs onagricultural

products were 24.9% on average, while tariffs on fishery products

andon industrial products remained stable at 11.7% and 8.7%

respectively. By comparison,EC tariffs currently stand at 6.3% on

all products, 16.2% on agricultural products, 12.4%on fishery

products and 3.6% on industrial products.

EU Assistance

Three pre-accession instruments have been financed by the

EuropeanCommunity to assist the applicant countries of Central and

Eastern Europe with theirpre-accession preparations: the Phare

programme; SAPARD , which provides aid foragricultural and rural

development; and ISPA , which finances infrastructure projectsin

the fields of environment and transport. The support provided by

these programmes isfocused on the Accession Partnership priorities,

which are intended to help the candidatecountries meet the criteria

for membership. For the years 2000-2004, total financialassistance

to Bulgaria amounts to around 178 million annually from Phare,

57.6million from SAPARD, and between 93 and 127 million from

ISPA.

Status of accession

In its first, 1997 Opinion on Bulgarias application for EU

membership, thecommission concluded: Bulgarias progress in the

creation of a market economy hasbeen limited by the absence of a

commitment to market-oriented economic policies; it would not be

able to cope with competitive pressure and market forces within the

Unionin the medium term. However, in its 2003 Regular Report the

Commission found that:Bulgaria is a functioning market economy. It

should be able to cope with

-

8/6/2019 Draft Study Bulgaria

10/23

10

competitive pressure and market forces within the Union in the

near term, provided that it continues implementing its reform

programme to remove remainingdifficulties.

2. Role of trade in Bulgarias economy

Trade plays an important role in Bulgarias economy. As a small

country with arelatively open trade regime Bulgaria is highly

dependent on foreign trade and this isreflected in the high share

of imports and exports of goods and services in the GDP (over80% in

the recent years). Total external trade increased by 40.1% in the

period 1996-2002. Export growth, which averaged 12.5% over 2000-02,

was the main contributor togrowth in GDP in 2000 and 2001 and the

second largest contributor in 2002 afterdomestic consumption.

Annual import growth averaged 12.8% over the same period.

Bulgaria has undergone a rather dramatic re-orientation of its

trade. Before the

transition, over half of Bulgaria's foreign trade was with

members of the CMEA. In 2003,the EU accounted for 52.4% of

Bulgaria's total trade up from 38.5% in 1995. Otherpreferential

partners (EFTA, CEFTA, and Turkey) accounted together for some

16.5% of exports and 13.6% of imports in 2002. The Russian

Federation accounted for 1.6% of exports and 14.5% of imports. The

United States share was 4.7% in exports and 2.2% inimports.

In the pre-transition period Bulgaria was a major exporter of

capital goods andprocessed food to the CMEA, it is currently a net

importer of these products and isproving competitive in exports of

footwear, textiles, and apparel. In general, the evolutionof

Bulgaria's trade structure reveals a movement in comparative

advantage towards

labour- and resource-intensive manufacturing products.

In 1989, before the transition, Bulgaria's exports were

estimated at US$8.3 billion,of which $5.1 billion went to the CMEA

and about US$3.2 billion to other countries. Thecollapse of the

CMEA led to a drastic fall in the value and volume of exports, such

thatby 1992, total exports were estimated at US$3.9 billion. Since

the beginning of transitionreforms in 1991, export values have in

general fluctuated in accordance with theperformance of the

economy. In 1992-94, they averaged around US$3.9 billion; after

arise to some US$5 billion in 1995, they fell back to US$4 billion

in 1999. Recentestimates show a rising trend: in 2001 exports were

estimated at US$5.1 billion and in2002 at US$5.7 billion.

Similarly, the value of total imports has fluctuated

considerably since the pre-transition period. In 1989, the total

value of imports was about US$9 billion, of whichUS$4.6 billion

from the CMEA. By 1992, total imports had fallen to US$ 4.5

billion,mainly due to the drastic fall in real incomes that

occurred during the early transitionperiod. Imports rose to US$5.3

billion in 1995; however, as with exports, this trend wascurtailed

by the 1996/97 economic crisis and imports fell to about US$ 4.9

billion in1997. Since the resumption of economic growth, imports

have resumed their rising trend.

-

8/6/2019 Draft Study Bulgaria

11/23

11

In 2001 and 2002 total imports were estimated at US$7.3 billion

and US$7.9 billionrespectively.

Trade in agriculture

Food and agriculture have historically been major components of

Bulgaria'sforeign trade, contributing up to a quarter of total

exports. The value of agriculturalexports fell between 1990 and

1997 by two thirds and continued to decline up to 2000. In2001,

Bulgarias agricultural and food exports were estimated at US$504

million, anincrease of 3% over 2000 but still only one-quarter of

their 1990 value. The mainagricultural export products were

cereals; tobacco and processed tobacco substitutes;non-alcoholic

and alcoholic beverages (mainly wine) and vinegar; meat and offal

forconsumption; oilseeds and fruits, and animal feed.

Trade in manufactures

Export performance of the manufacturing sector has been the

major vehicle of tradegrowth and contributes now up to 54% of total

export earnings. The main manufacturedexports include clothing,

man-made fibres, basic metals, metal products, and, to a

lesserextent, machinery and equipment.

Services

Bulgaria has recorded a positive balance on its services account

since 1994. In2002, this amounted to US$598 million. Tourism is the

main services sector which iscontributing to the positive balance

of services trade.

-

8/6/2019 Draft Study Bulgaria

12/23

12

II. Trade liberalization and its economic impacts

1. Trade liberalization process

Background

Previously, the Bulgarian economy, like other former socialist

countries, had beendominated by state ownership and governed by

centralized planning. The centralplanning body determined and fixed

the quantities and prices of commodities andservices produced.

Monetary flows in the economy were merely a consequence of

thepreset commodity flows and did not play the role of an

adjustment in investment andoutput. A large part of Bulgarias GDP

was created and realized in the framework of theCouncil for Mutual

Economic Assistance (CMEA). Following its de facto disintegrationin

1989-1990, the countrys export revenues drastically declined and in

March 1990 thegovernment declared a unilateral moratorium on

external debt service payments. Most of Bulgarias large enterprises

were specialized exporters to the CMEA regional market and,mainly,

to the market of the former USSR. According to regional standards,

theseenterprises were considered to be efficient producers, able to

exploit economies of scaleas they also managed to sell part of

their products on the world market.

In 1990-1997, there was no political consensus in the country on

the economicpolicy priorities at both macro- and micro-level

resulting in a stop-and-go transformationtowards a market economy.

The result was that in 1990-1997, GDP shrank by 40% inreal terms,

while in 1997 consumer prices soared almost 20 times relative to

1990.Inflation averaged 233 percent per year during 1990-97, and

turned into hyperinflation inlate 1996-early 1997, at the peak of a

major banking and exchange rate crisis. This, inturn, led to the

collapse in real incomes and wealth, as well as to growth of

poverty levelsThus, Bulgarias transition started and initially

proceeded under more difficult and evendramatic circumstances than

in most other central and eastern European (CEE)

countries,reflecting a legacy of stricter central planning, higher

exposure to CMEA trade, and alarger external debt burden. Political

factors such as the national consensus on the reformpolicies were

also less favourable.

Some positive elements of transition in the first half of 1990s

had mainly to dowith some foreign policy and foreign economic

developments. In 1990, the country

joined the IMF and concluded its first stand-by agreement that

provided some resourcesto start-up of the reform process. At the

end of 1993, Bulgaria signed the EuropeAgreement with EU Member

States, a preferential trade agreement, which was probablythe most

important initial catalyst for trade policy reforms. However, the

asymmetricliberalization of trade regimes under this Agreement

appeared to be, at least initially,insufficient for expanding

Bulgarian exports to the EU. This was mainly caused by thefact that

Bulgarias exports, particularly of agricultural products, was in

the group of so-called sensitive goods in the EU and thus strongly

protected.

The crisis triggered a change not only in government, but also a

switch to a newpolicy strategy focused on a currency board

arrangement (CBA), tight fiscal and incomes

-

8/6/2019 Draft Study Bulgaria

13/23

13

policies, comprehensive structural reforms and trade

liberalization, particularly at theregional level as described

below. This strategy succeeded in restoring macroeconomicstability

and growth.

The National Economic Development Plan of the Republic of

Bulgaria for 2000-

2006 (NEDP) was the first document drafted after the onset of

the transition to a marketeconomy, addressing a number of

longer-term issues of Bulgarias socio-economicdevelopment,

including further trade liberalization. The plan, which was updated

betweenSeptember 2002 and April 2003, also sets a vision of the

countrys future development inline with the laid down national

priorities, the progress achieved in the negotiations withthe EU

and the changes in the economic and external environment since

1999. Alongside,the NEDP is the basis of multi-annual programming

of assistance under the EU pre-accession funds. In addition to

trade liberalization, the improvement of competitivenessof the

national economy is set as a key national priority by the NEDP to

attain sustainableand balanced growth and development.

Tariff policy

During the transition process, Bulgaria's overall trade policy

objective was gearedto the gradual liberalization of its trade

regime. This was pursued at multilateral, regional,and bilateral

levels. However, its main trade liberalization efforts have been

implementedthrough a network of regional and bilateral agreements

(FTAs). Bulgaria acceded to theWTO on 1 December 1996 on rather

balanced terms. However, in contrast with FTAs,Bulgaria managed to

negotiate ceiling bindings as its tariff concessions, both

inagriculture and industrial goods (i.e. WTO bound tariff levels

were generally higher thanthe applied levels).

In fact, such dichotomy was foreseen by the trade policy

strategy for two reasons.First, regional and bilateral trade

liberalization was reciprocal and aimed to re-reorienttrade

principally towards the EU, EFTA and CEE countries. Secondly,

ceiling bindingson MFN tariffs achieved in the WTO accession were

considered as convenient safetynets for the future (in case urgent

protection was required), but also to serve twoimportant trade

policy objectives: to make transition to the EU tariff levels (as

part of theEU accession process) as smooth as possible and also to

ensure that Bulgaria has anadequate negotiating basis for the

eventual multilateral trade liberalization on a reciprocalbasis

with its MFN trading partners (in contrast to the WTO accession

negotiations whichare conducted on a strictly unilateral basis

market access commitments are undertakenonly by acceding

countries).

On accession to the WTO, Bulgaria bound all its MFN tariffs

under GATT 1994. SinceBulgarias WTO accession, trade liberalization

has been much faster for industrialproducts than for agricultural

goods Simple average on agricultural products is 47.6%,while on

non-agricultural items simple average is 22.7%. However, Applied

MFN tariff rates were reduced to a simple average of less than 12%

in 2003 (17.2% in 1996): appliedsimple average MFN rate amounted to

21.7% for agricultural products and 8.6% forindustrial products.

Applied duties range from 0% to maxima of 40% in industrial and

-

8/6/2019 Draft Study Bulgaria

14/23

14

80% in agricultural products. Bulgaria applied ad valorem duties

for all the industrialproducts with the exception of one tariff

line with a specific rate and for 83.9% of theagricultural products

(Tables C and D). Average applied MFN tariff rates are well

abovepreferential rates; the average preferential rates for all

products range between 2.5% to5.9% depending on the agreement (see

below).

Since 1999, zero duty rates have been introduced on an

autonomous basis foralmost the whole range of goods covered by the

Information Technology Agreement(ITA) and since the formal adoption

by Bulgaria of this Agreement on 1 January 2002 -zero duties for

all covered products.

Tariff escalation: on the basis of the International Standard

IndustrialClassification (ISIC), the tariff structure shows

escalation; the first and semi-processedstage of manufacturing

attract average rates of 7.8% and 8.8% respectively and

fullyprocessed products attract an average tariff of 13.4%. Tariff

escalation appears to berelatively marked in the food, beverage and

tobacco, textile and leather, wood and

furniture, and chemicals sectors.In comparison, on services,

upon WTO accession, Bulgaria made commitments

across all major service sectors and in more than 90 out of 155

sub-sectors.

Table C. Bulgaria: bound and applied tariffs, 2003

Bound Applied

N of tariff lines 10,606 10,606

Unweighted average 28.2 11.6

Minimum 0.0 0.0Maximum 200.0 80.0By stage of processing:

- Stage 1 (raw materials) AverageMinimumMaximum

29.10.0

200.0

9.60.0

80.0- Stage 2 (semi-

manufactures)AverageMinimumMaximum

21.60.0

128.0

8.80.0

50.0- Stage 3 (finished products) Average

MinimumMaximum

31.40.0

200.0

13.40.0

74.0

By HS Chapter:HS 01-24 Average

MinimumMaximum

47.60.0

200.0

21.70.0

80.0HS 25-97 Average

MinimumMaximum

22.70.0

128.0

8.60.0

40.0

Source: WTO Secretariat calculations.

-

8/6/2019 Draft Study Bulgaria

15/23

15

Bulgaria also provides more favourable market access under the

GeneralizedSystem of Preferences to 118 developing and least

developed countries. For a large list of goods originating in

developing countries Bulgaria applies preferential duties at the

rateof 70% of the MFN duty rate and for imported goods originating

in LDCs - zero dutyrates.

FTAs

The Europe Agreement establishing an Association between the

European Unionand its members States (EAA) and the Republic of

Bulgaria was signed in March 1993and entered into force on 1

February 1995. The Interim Agreement on Trade and TradeRelated

Matters covering trade components came into force on 31 December

1993. Inaccordance with the trade provisions of the EAA, the

imports into the EU of industrialproducts originating in Bulgaria

(since 1 January 1998) and the imports into Bulgaria of industrial

products originating in the EU (since 1 January 2002) is completely

liberalized.The measures having equivalent effect to customs duties

and non-tariff restrictionsregarding trade in industrial goods are

also completely abolished. However, trade inagriculture is

liberalized selectively.

Bulgaria has also a free trade agreement with the member states

of EFTA and hasalso acceded to CEFTA as of 1 January 1999.

Bilateral free trade agreements have beenconcluded with Turkey, FYR

of Macedonia, Israel, Lithuania, Latvia and Estonia. Thelatter

three countries are now EU members. In 2001, Bulgaria signed a

Memorandum of Understanding on Trade Liberalization and

Facilitation between countries in South-Eastern Europe within the

framework of the Stability Pact. Hence in accordance with

itsobligations, Bulgaria finalized the negotiations on conclusion

of free trade agreementswith Serbia and Montenegro, and Bosnia and

Herzegovina. The FTA with Albania wassigned on 26 March 2003 and

its entry into force is pending. Likewise, in all FTAs, tradein

industrial goods is duty-free, while agricultural trade is

liberalized partially.

Table D. Structure of MFN tariffs in Bulgaria(Per cent)

1998 2002 2003

1. Bound tariff lines (% of all tariff lines) 100.0 100.0

100.02. Duty-free tariff lines (% of all tariff lines) 5.2 15.0

14.63. Non- ad valorem tariffs (% of all tariff lines) 3.6 3.6

3.74. Tariff quotas (% of all tariff lines) 2.4 2.2 2.15. Non- ad

valorem tariffs with no AVEs (% of alltariff lines)

3.6 3.6 3.7

6. Domestic tariff "spikes" (% of all tariff lines) a 0.7 5.1

5.17. International tariff "peaks" (% of all tariff lines) b 39.7

25.3 25.38. Overall standard deviation 11.7 10.9 11.09. "Nuisance"

applied rates (% of all tariff lines) c 0.4 0.7 0.7

a Domestic tariff spikes are defined as those exceeding three

times the overall simple averageapplied rate.b International tariff

peaks are defined as those exceeding 15%.

-

8/6/2019 Draft Study Bulgaria

16/23

16

c Nuisance rates are those greater than zero, but less than or

equal to 2%.Source: WTO Secretariat calculations, based on data

provided by the Bulgarian authorities.

Other trade policy measures

Imports

Bulgaria applies a 20% value-added tax on most goods and

services, includingimports. Excise duties are levied on a limited

number of products for mainly health andenvironmental reasons.

Since 1 January 1997, the customs clearance fee of 1% advalorem has

been eliminated. On 1 July 1998, the temporary import surcharge

introducedfor balance of payments purposes was reduced and on 1

January 1999 it was completelyeliminated, ahead of schedule and in

spite of a negative trade balance.

Bulgaria's import licensing regime has been liberalized. It

currently does notapply any automatic licences on imports.

Remaining non-automatic licences aremaintained in conformity with

Bulgaria's commitments under various internationalagreements

related to trade in arms, and protection of human, animal, and

plant life.Liberalization of other non-tariff measures includes the

abolition of the use of automaticlicences, and the reduction of

non-automatic licences and import and export prohibitionsto a

minimum, in most cases in accordance with Bulgaria's obligations

underinternational agreements, for safety and environmental

concerns.

Table E. Goods requiring non-automatic licences

Bulgarian Customs Tariff No. Description of products

1 Nuclear materials, radioactive substances and other sources of

ionizing

radiation2 2524, ex. 6811,

6812, ex 6813Asbestos, asbestos products and asbestos containing

materials andproducts

3 ex. 490700,ex. 4911

Polygraph production for public supply, which can be used

assecurities

4 from Chapter 36,ex.290420001

Powder, explosive and pyrotechnical materials and products

thereof of civil application, Trinitrotoluene (TNT)

5 ex. 9013ex 930400000

Telescopic sights and laser targets, gas spray

6 ex 9303,ex 930400000, ex 9305, ex9306 and ex 95069990

Smooth-barrel weapons, weapons using only ammunition

withperipheral inflammation and pneumatic weapons for hunting

andsports purposes and unadjusted to fully automated fire, gas- and

signal-

guns and revolvers and ammunition for these.7 Medicaments for

human medicine8 from Chapter 28

from Chapter 29ex 3808

Products for plant protection

9 Veterinary-medical products10 Live game and its genetic

material11 Wild flora and fauna species included in the Washington

Convention

-

8/6/2019 Draft Study Bulgaria

17/23

17

Bulgarian Customs Tariff No. Description of products

on International Trade in Endangered Species of Wild Fauna and

Flora(CITES), including live or dead species as well as parts and

productsthereof.

12 Alien flora and fauna species designated for propagation and

breeding(except for some parrot species)13 Military and special

production and products and technologies of

possible dual (civil and military) use14 Narcotic and

psychotropic substances15 Chemical substances under control used

for the production of narcotic

and psychotropic substances16 Goods the importation of which is

regulated by intergovernmental

agreements and protocols and generates budget expenditure17

Certain types of wastes according to the Basel Convention on

hazardous wastes18 Ozone-depleting substances, according to the

obligations of Bulgaria

under the Montreal and Kyoto Protocols, implemented under

Councilof Ministers Regulation No 254 of 1999

Source: Bulgarian Ministry of Economy.

During the process of its accession to the WTO, Bulgaria

introduced new anti-dumping, countervailing and safeguard

legislation, in conformity with WTO disciplines.Bulgaria has not

introduced any countervailing measure. It has so far initiated one

anti-dumping action, and six safeguard investigations, two of which

have resulted in increasedduties.

Bulgaria is gradually harmonizing its national standards with

international andregional standards, in particular those of the EU.

Some 2% of standards in force aremandatory technical regulations.

In 2002, 52% of Bulgaria's standards were harmonizedwith those of

the EU and it intends to achieve 80% harmonization by

2004-2005.

Exports

Bulgaria no longer imposes any duties, taxes or other charges on

exported goods.At the time of its WTO accession in 1996, Bulgaria

applied a range of export taxes forthe purpose of preventing or

relieving critical shortages of foodstuffs and other

essentialproducts. However, it undertook commitments to minimize

the use of such measuresupon accession. In 1998, export taxes on 24

products, including wheat, barley, and maize

were eliminated; export taxes on live cattle, skins, wool, paper

waste, metal scrap andmetal products were eliminated in 1999; and

the remaining export taxes, on unprocessedwood products, were

abolished in January 2000.

Since January 2000, Bulgaria has liberalized its export

licensing procedures.Currently, non-automatic export licenses are

required in a limited number of cases suchas fulfillment of

international treaties and conventions to which Bulgaria is a

signatory;protecting public morals; maintaining public order and

national security; and

-

8/6/2019 Draft Study Bulgaria

18/23

18

safeguarding national artistic, historical, and architectural

masterpieces. Automaticlicensing (registration) is applied to

precious metals and unsown timber exports.

In 2003-2004, quantitative export restrictions remained only on

exports of textileand apparel products under quotas in the United

States and Canada. Export restraints onBulgarian clothing, under

the Agreement on Textiles and Clothing (ATC), covered sixcategories

in Canada (coats and jackets; winter outerwear; mens suits, jackets

andblazers; ladies jackets/blazers, dresses and skirts; sweaters;

and combed wool fabric),and six in the United States (woven wool or

man-made-fibre fabric containing more than15% wool, with a

sub-limit for fabric containing over 36% wool; mens and boys

suit-type coats; womens and girls coats; womens and girls suits

with over 23% wool,womens woollen skirts; and womens and girls

trousers, breeches, and shorts). Allthese QRs are to disappear

completely after the termination of the ATC as from 1

January2005.

Bulgaria does not apply any export subsidies. In line with the

Government'sconservative fiscal stance, the amount of state aid

offered has declined both in absoluteand relative levels in recent

years. As a percentage of GDP, state aid declined from 3.3 in1999

to 0.7% in 2001. Similarly, direct subsidies have declined, from

2.5% of GDP to0.6% in 2002. The mining and transport sectors have

benefited the most from state aid;with assistance for the

production of coal (29.5%) and provision of transport

services(29.0%) accounted for almost 60% of the total in 2001.

2. Economic impact

As a result of reforms, Bulgaria's industries have undergone

significant structuraltransformation. Trade liberalization and

privatization reforms have led to significantchanges in resource

allocation, and consequent effects on the dynamics of

tradespecialization. Most significant is the dramatic reduction in

exports of machines andequipment, from about half of Bulgaria's

exports in 1989 to less than 14% in 2003. Theshare of consumer

goods in exports rose from around 10% in 1989 to some 27% in

1995and 36.6% in 2003; this increase is largely being driven by

rapid export growth inclothing and footwear, whose value increased

five fold from US$313 million (6.3% of exports) in 1995 to US$1.6

billion (21.9% of exports) in 2003. Among other exports,metals

accounted for some 16.1% and chemicals for around 3.4%.

With improved economic performance in recent years, Bulgarias

trade balancehas fallen from a surplus of US$321 million in 1997 to

a deficit of US$2.5billion in 2003.In relation to GDP, its share

has moved from +3.1% to 13.1%. Correspondingly, thecurrent account

of the balance of payments steadily deteriorated from a surplus of

US$1.046 billion in 1997 (10.1% of the GDP) to a deficit of

US$1.648 billion in 2003(8.7% of the GDP). Although the savings

rate rose up to 14.5% of GDP in 2001, it is stilllow by all

standards and has grown into an important factor for the current

accountdeficit. Other reasons behind the low saving rate have to do

with low incomes and the

-

8/6/2019 Draft Study Bulgaria

19/23

19

absence of diversified financial instruments for the

mobilization of local and foreignsavings. The persistent current

account deficit represents a major challenge and alsoreflects the

insufficient competitiveness of the Bulgarian economy.

The leading role of trade in spurring growth in the Bulgarian

economy is expected

to continue. On the other hand, the rise in the oil prices will

have a negative effect to theBulgarian energy intensive economy.

Furthermore, potential accession to the EU in 2007is likely to

attract further FDI, with expected positive impacts on

competitiveness of Bulgarias productive sectors and their ability

to access new markets. The trend of higher growth rate of labour

productivity compared to average wages will alsocontribute to a

more competitive economy.

3. Development impact

Despite recent positive trends, real GDP and consumption were in

2002 stillbelow their pre-transition (1989) levels by 17% and 13%

respectively. The level of

inflation has been brought under control from high levels of

double digits (11-16%) in1998-2000 to moderate single digits (3-6%)

in 2003-2004.

The transition process and more open economy resulted in a high

and persistentlevel of unemployment and high share of long-term

unemployed. On the other hand, inthe last three years unemployment

was decreasing, but still stood at a high rate of 14.3%at the end

of 2003. Unemployment among young people, ethnic minorities and

otherdisadvantaged groups remains high. Among other challenges are:

insufficient level of education and lack of resources to preserve

the current high accessibility of highereducation; relatively low

standard of living and poverty; and broadening of

regionaldisproportions in the development of human resources.

The living standard in Bulgaria remains the lowest in comparison

to the other EUnew member or applicant States. Per capita income

(purchasing power parity) in Bulgariain 2001 was estimated at 24%

and 28% of the EU average per capita income in 2000 andin 2001

respectively 4, or average incomes are ten times lower than EU

averages andtwice as low as EU new members or other acceding

countries. 5 At the same time,unemployment in Bulgaria is estimated

as being twice as high as that of the EU average.The low level of

real incomes is a key social problem predetermining the large

number of people in need of social protection and assistance, and

the relative and absolute povertylevels and, respectively, the

share of the population living close to the poverty line

inBulgaria. 6

4 See Real Convergence in Candidate Countries Past Performance

and Scenarios in the Pre-accessionEconomic Programmes, ECFIN/708/01

EN, November 2001.5 See Millennium Development Goals: Bulgaria

2003, UNDP, Sofia, 2003.6 See Integrated Study of Bulgarian

Households, carried out by the World Bank and NSI in 1995, 1997,and

2001.

-

8/6/2019 Draft Study Bulgaria

20/23

20

Poverty and Inequality Trends 7

1995 1997 2001Measure of poverty

Level 5.5 36.0 12.8Difference 1.7 11.4 4.2Sharpness 0.8 5.3

1.9

Average consumption per capita(June 1997, BGN) 117 208 62 804 99

035

Gini coefficient 27.1 31.4 29.6

Sources: World Bank, 2002

Over the years of transition and reforms, the poverty indicators

have deterioratedin terms of average monthly incomes, proportion of

the poor (with incomes under 60%of the average monthly income) and

poverty threshold (60% of the average monthlyincome). However,

income inequality in Bulgaria is lower than in the EU and even

lowerthan in most other transition economies, although the Gini

coefficient grew slightly overthe last ten years. 8

The current national targets to reduce poverty between 2001 and

2015 include:

(a) raising the average monthly income from euro 91 to euro 280;

and (b) raising thepoverty threshold from euro 54.6 to euro 170,

while keeping the proportion of peoplewith incomes lower than

poverty threshold to no more than 15%; (c) reducing

youthunemployment from 35.34% to 25%; and (d) reducing long-term

unemployment from9.59% to 7%.

7 Poverty level means the percentage of population under the

poverty line, poverty difference denotesthe average distance from

the poverty line, and sharpness or depth of poverty is the square

of averageconsumption deficit as a percentage of the poverty line

and is more sensitive to the inequality among thepoor.8 See

Millennium Development Goals: Bulgaria 2003, UNDP, Sofia, 2003.

-

8/6/2019 Draft Study Bulgaria

21/23

21

III. Policy lessons and implications

1. Conclusions and Policy lessons

Significant macroeconomic and structural reforms implemented in

Bulgaria since1997, membership in the WTO (1996) and the process of

accession to the EU had allcontributed to the transition process.

Major reforms implemented included trade andinvestment

liberalization and wide scale privatization. These had contributed

to ratherhigh rates of economic growth in the past five years.

However, problems of widespreadpoverty and high levels of

unemployment remained to be major challenges, althoughthere were

recent signs of improvement in social indicators. Another important

challengeis the persistent current account and trade deficits,

which reflect the relatively low levelof competitiveness.

The process of accession to the EU has contributed to improving

the

competitiveness of the economy and its recovery, including

increased trade on a regionalbasis. Furthermore, this process,

through disbursement of the EU funds (representingannually in

2000-2004 up to 2% of Bulgarian GDP, served as an important safety

net fortrade liberalization and structural adjustment of the

national economy.

Bulgaria has been pursuing a rather interesting experience in

its tradeliberalization strategy, which has been carried out

predominantly at the regional andbilateral levels through

preferential FTAs on reciprocal basis. As a result, more than 70%of

Bulgarian trade is now with FTA partners, including the EU, EFTA

and CEFTA. Onthe multilateral level, in the process of accession to

the WTO, Bulgaria proceeded in arather cautious manner. Its market

access commitments in goods are kept at ceilingbindings levels

which are substantially above applied tariff levels. In view of

Bulgaria,such terms of accession represented an additional safety

net for the conduct of tradeliberalization policies and also were

needed for future multilateral trade negotiations asbargaining

chips, as well as for a smoother adaptation to the EU bound

tariffs, which aresubstantially lower on both industrial and

agricultural products. Such strategy would alsoallow to minimize

compensation negotiations with other WTO members after

Bulgariasaccession to the EU, when Bulgarias tariffs will be

replaced by the EU CommonExternal Tariff (CET).

On the national level, Bulgaria is pursuing the strategy of

encouraging innovativemanufacturing and improvement of

competitiveness of industrial enterprises that willallow them to

achieve sustainable growth and cope with competitive pressures on

the freeEuropean market.

2. Major country issues in the current Doha negotiations

As a recently acceded member, Bulgaria undertook considerable

commitmentsunder all WTO Agreements upon its accession to the WTO

in 1996. NeverthelessBulgaria, in line with the EU position,

strongly supported the launch of the Doha

-

8/6/2019 Draft Study Bulgaria

22/23

22

negotiations. The areas of a greater importance for Bulgaria in

the Doha negotiations arethe agricultural issues, improvement of

market access for agricultural and non-agricultural products,

further enhancement of trade in services, and extension of

theprotection of geographical indications under the TRIPS

Agreement. Bulgaria alsoattaches importance to the reduction of

high tariffs for industrial products and elimination

of non-tariff barriers. Basically, as a country in accession to

the EU, Bulgaria, being asmall trading partner, is aligning its

positions with those of the EU.

-

8/6/2019 Draft Study Bulgaria

23/23

23

REFERENCES

2002-2004 Regular Reports on Bulgarias progress towards

accession , EU Commission,Brussels, 2002-2004.

Bulgaria: 2004 Article IV Consultation and Ex Post Assessment of

Longer-TermProgram Engagement Staff Reports; Staff Statement; and

Public Information Notice onthe Executive Board Discussion, June

2004, IMF Country Report No. 04/176.

Bulgaria: The Dual Challenge of Transition and Accession, World

Bank, 2001.

Economic Survey of Europe, No.1-2, 2004, Economic Commission for

Europe, Geneva,2004.

Georgi Pirinski, Bulgarias Experience with WTO Accession and the

First Years of Membership in: WTO Accessions and Development

policies, UNCTAD/DITC/TNCD/11,New York and Geneva, 2001.

Memorandum of the President of the International Bank For

Reconstruction and Development and the International Finance

Corporation to the Executive Directors on aCountry Assistance

Strategy of the World Bank Group for Bulgaria , Report No.

23927-BUL, World Bank, 2002.

Millennium Development Goals: Bulgaria 2003 , UNDP, Sofia,

2003.

National Economic Development Plan of the Republic of Bulgaria

over the 2000-2006 Period (Update, June 2003), Bulgarian Agency for

Economic Analysis and ForecastingAgency for Economic Analysis and

Forecasting, Sofia, June 2003.

OECD Economic Surveys - 1996-97, Bulgaria , Paris, 1997.

Pre-Accession Economic Programme over the 2003 2006 Period ,

Bulgarian Agency forEconomic Analysis and Forecasting, Sofia,

2003.

Stefan Stefanov , The competitiveness of the Bulgarian economy ,

South-East EuropeReview, 3/2001.

WTO Trade Policy Review of Bulgaria , Report by the Government,

WT/TPR/G/121,WTO, 15 September 2003.

WTO Trade Policy Review of Bulgaria , Report by the Secretariat,

WT/TPR/S/121, WTO,15 September 2003.

WTO Trade Policy Review of Bulgaria , Minutes of Meeting,

WT/TPR/M/121 and Add.1,WTO, 20 November 2003.