Embed Size (px)

Citation preview

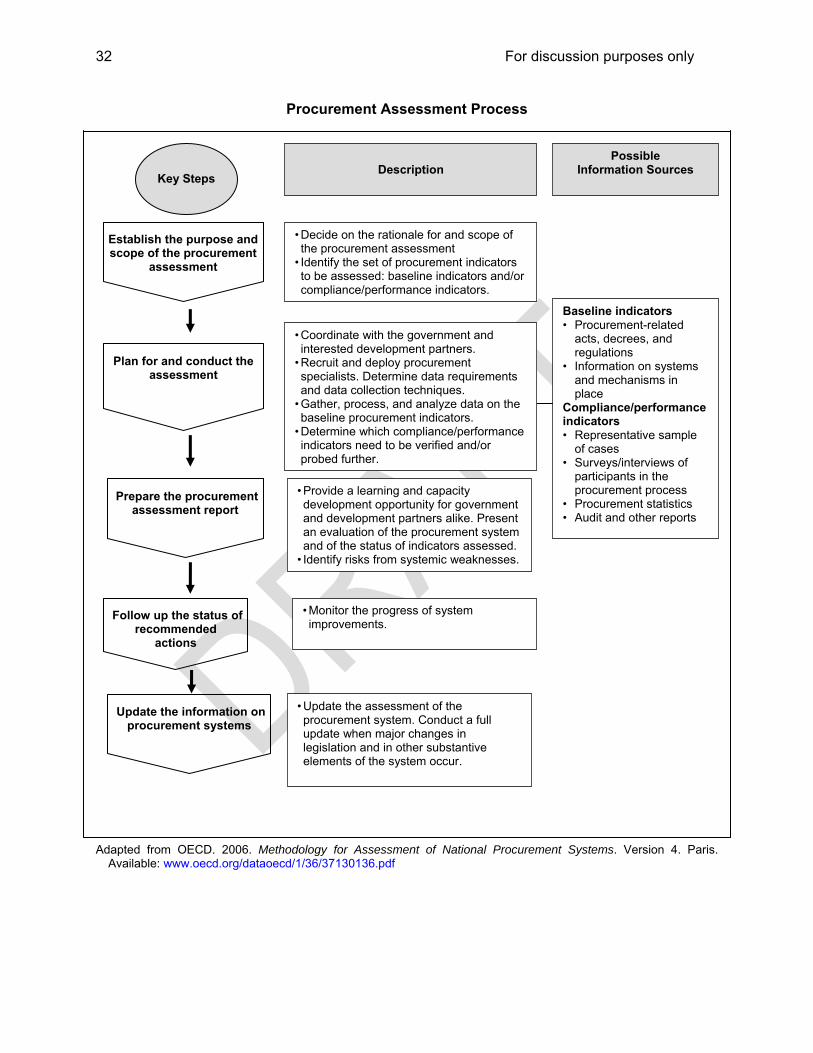

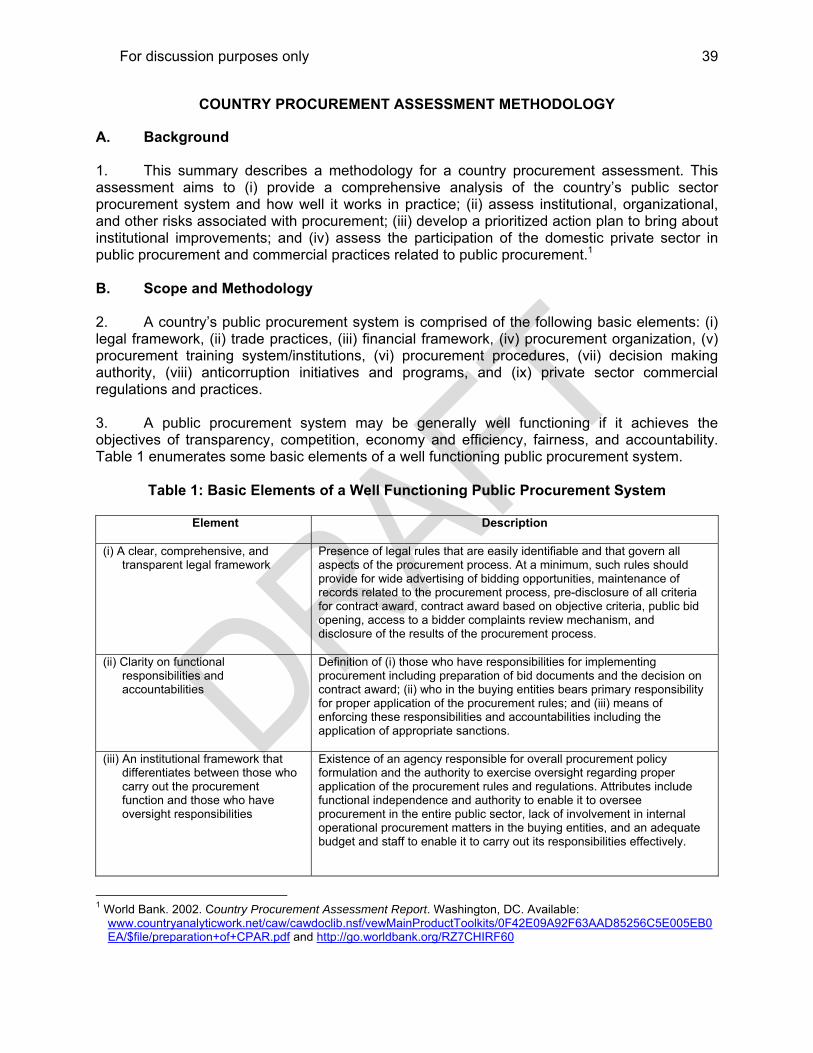

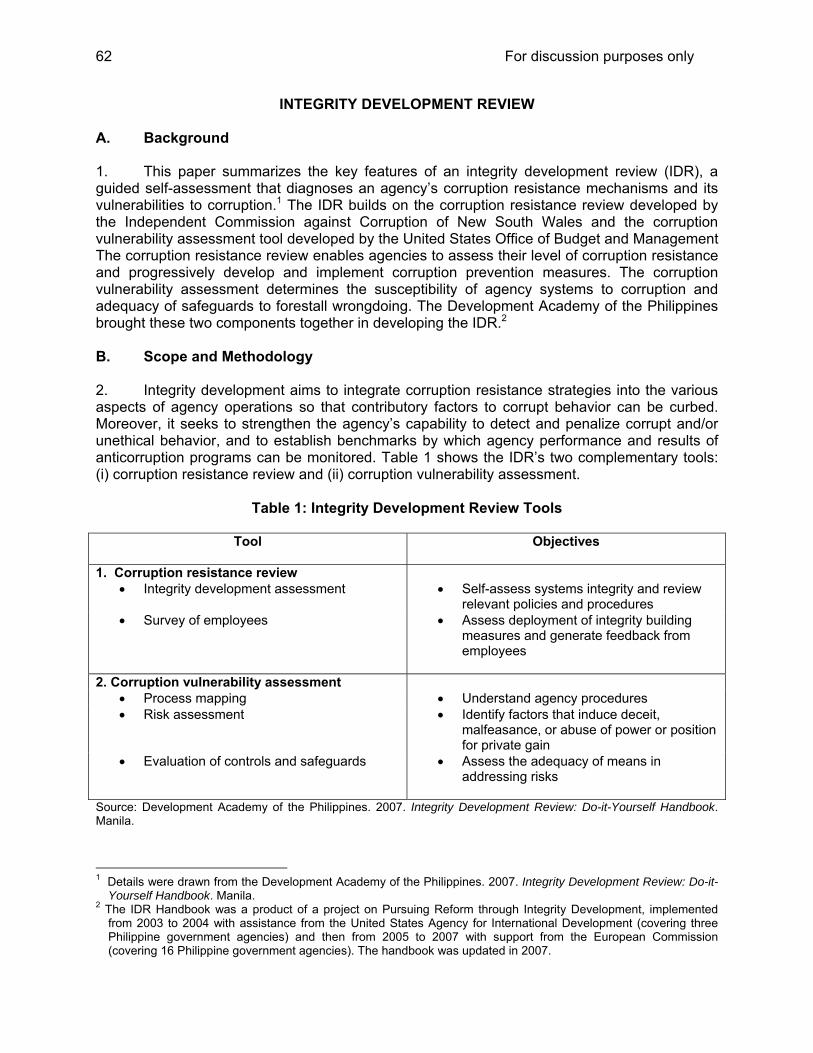

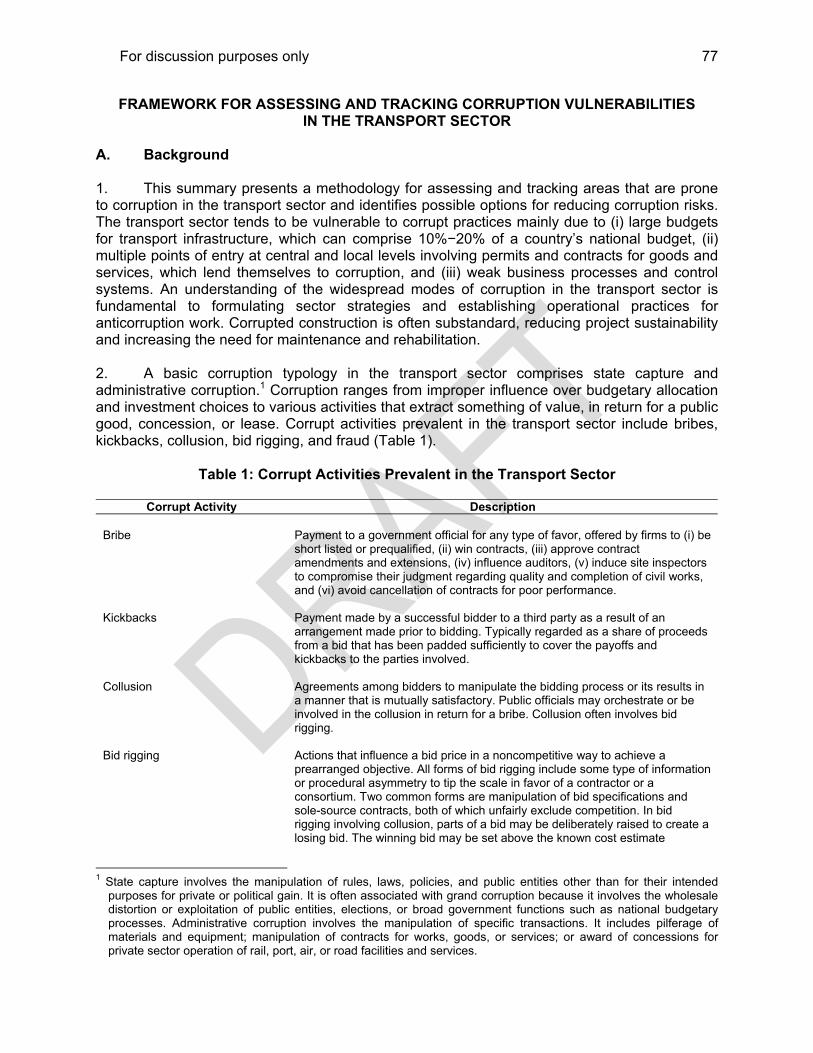

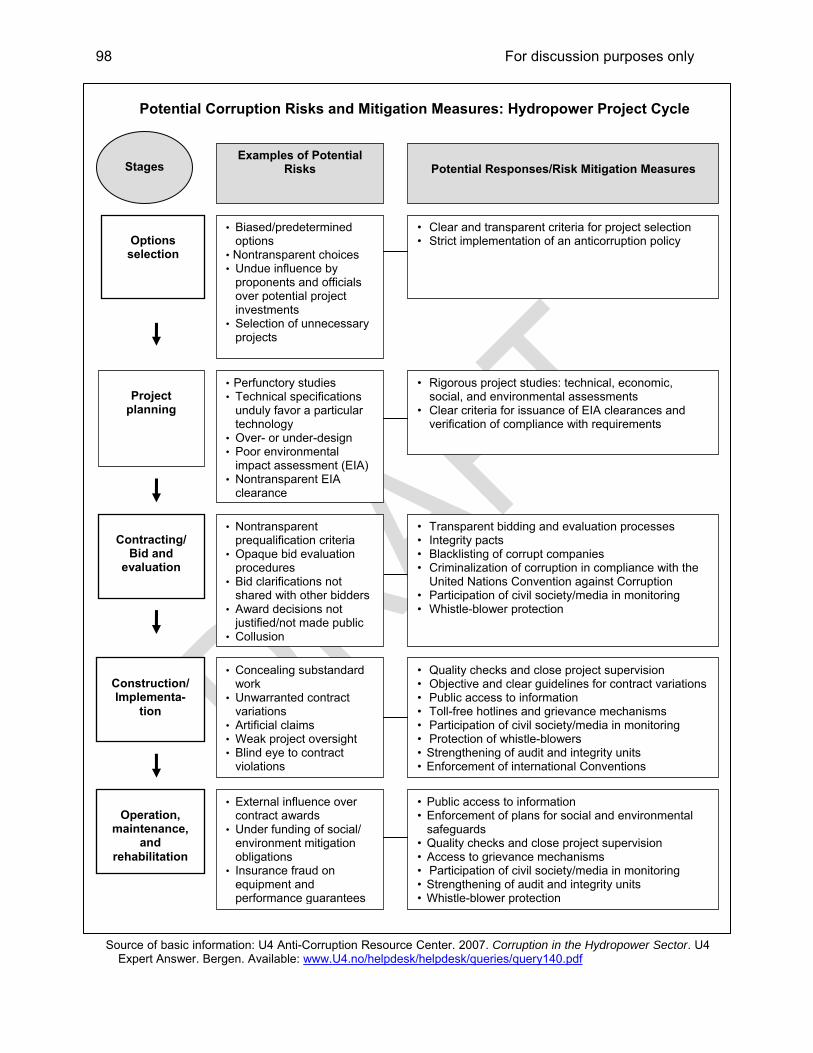

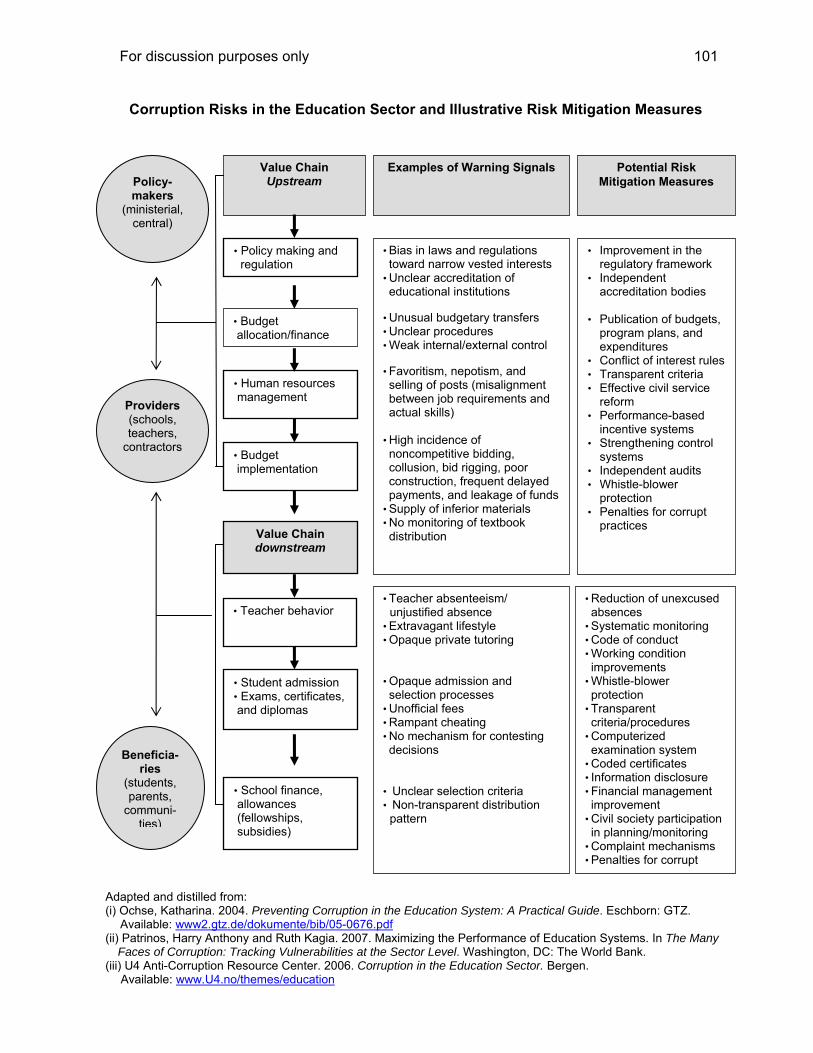

SOURCEBOOK

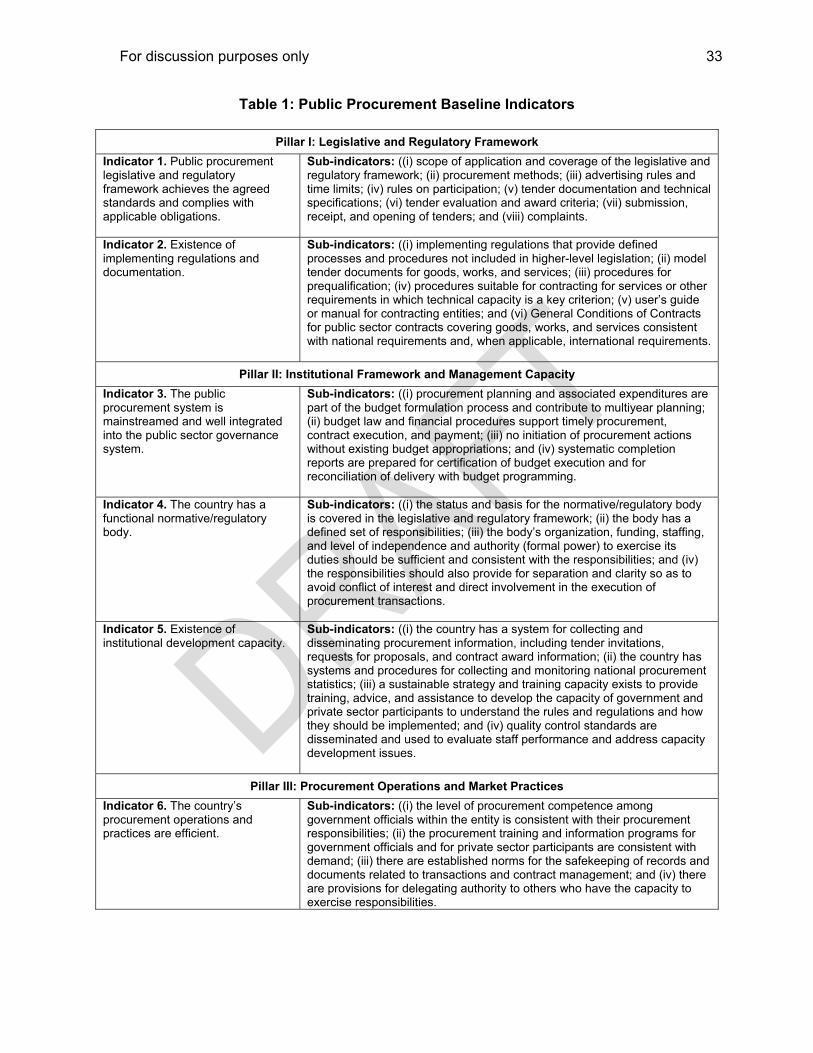

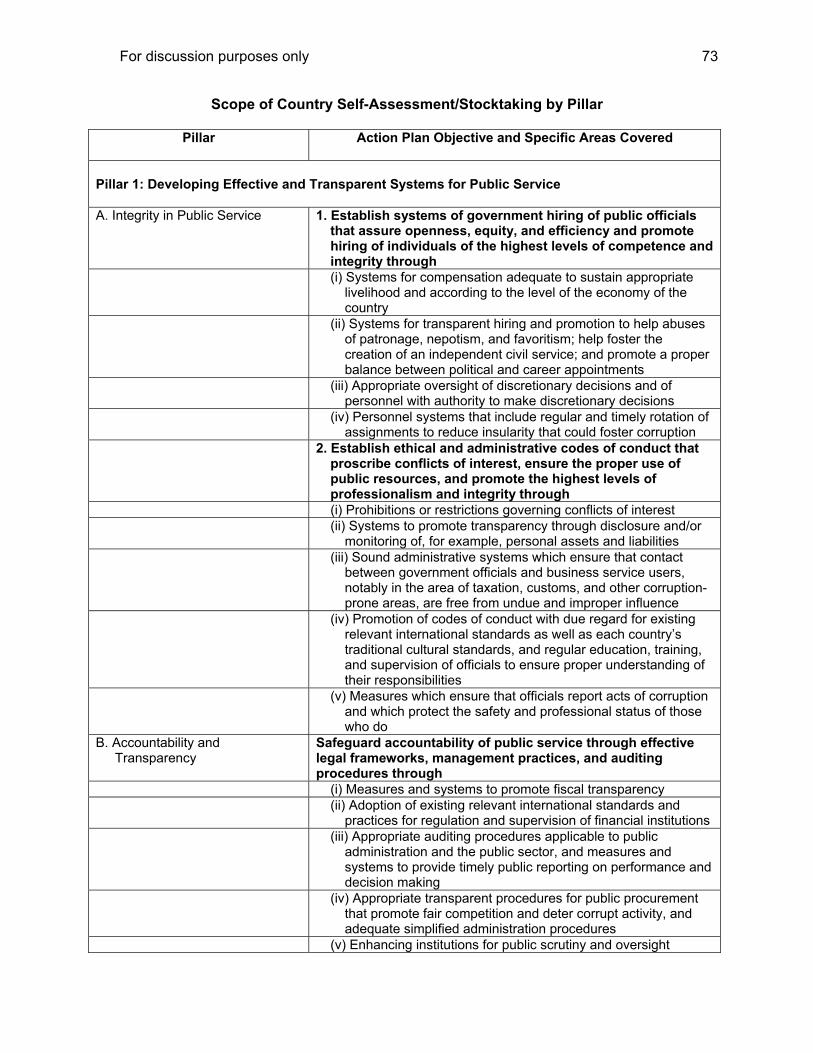

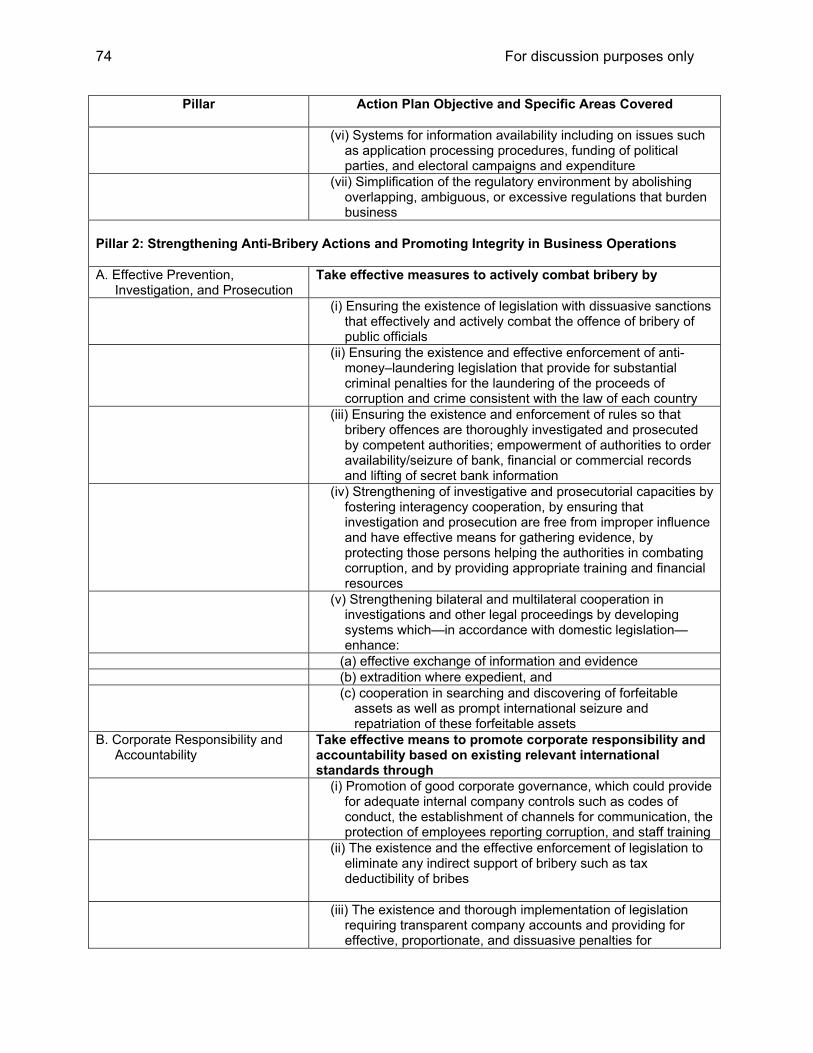

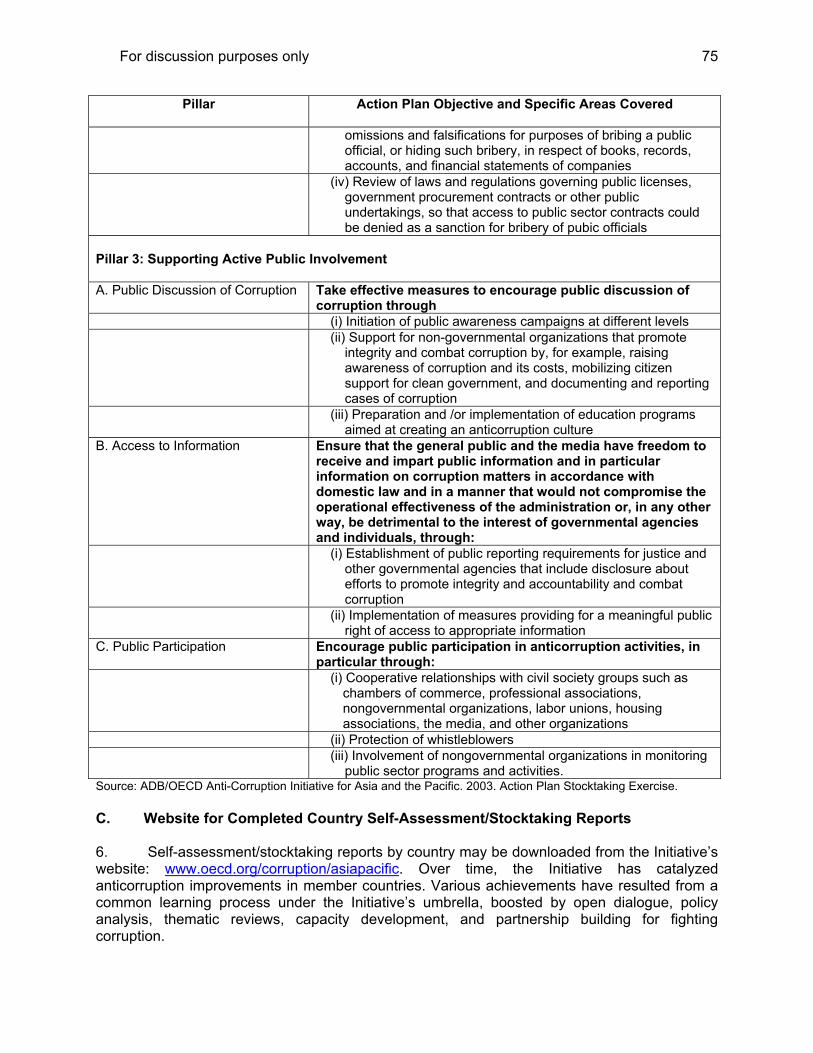

Diagnostics to Assist Preparation of Governance Risk Assessments

Draft December 2008

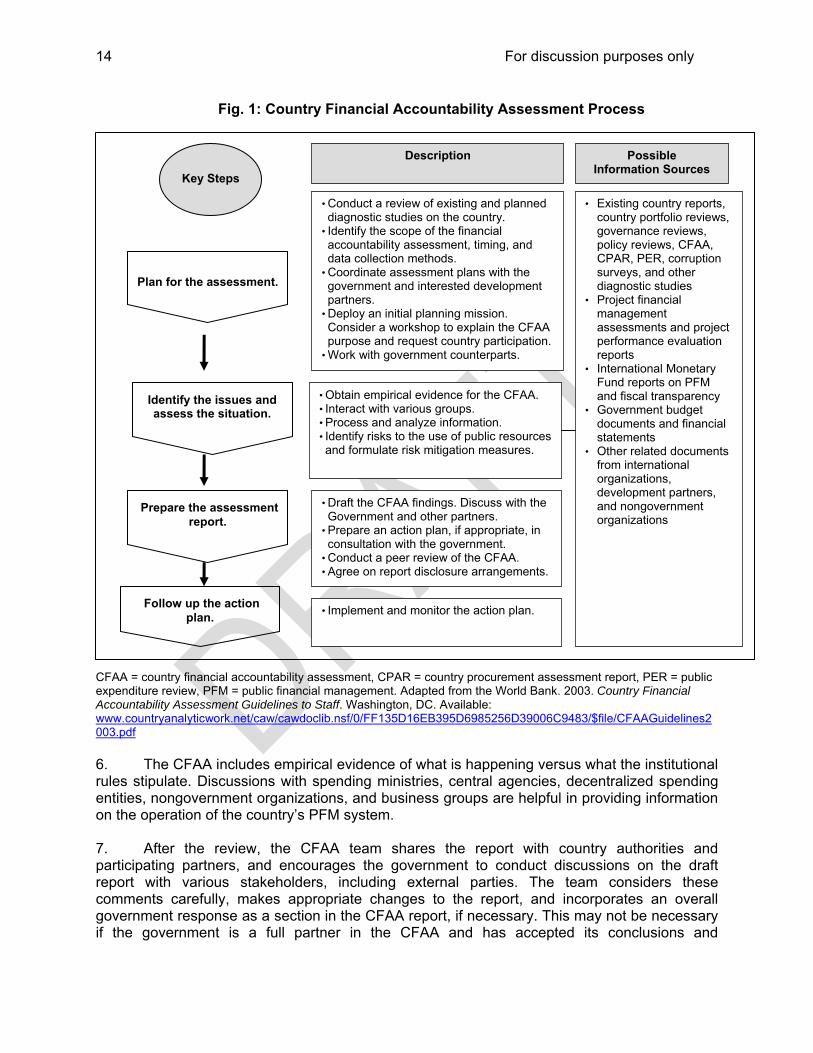

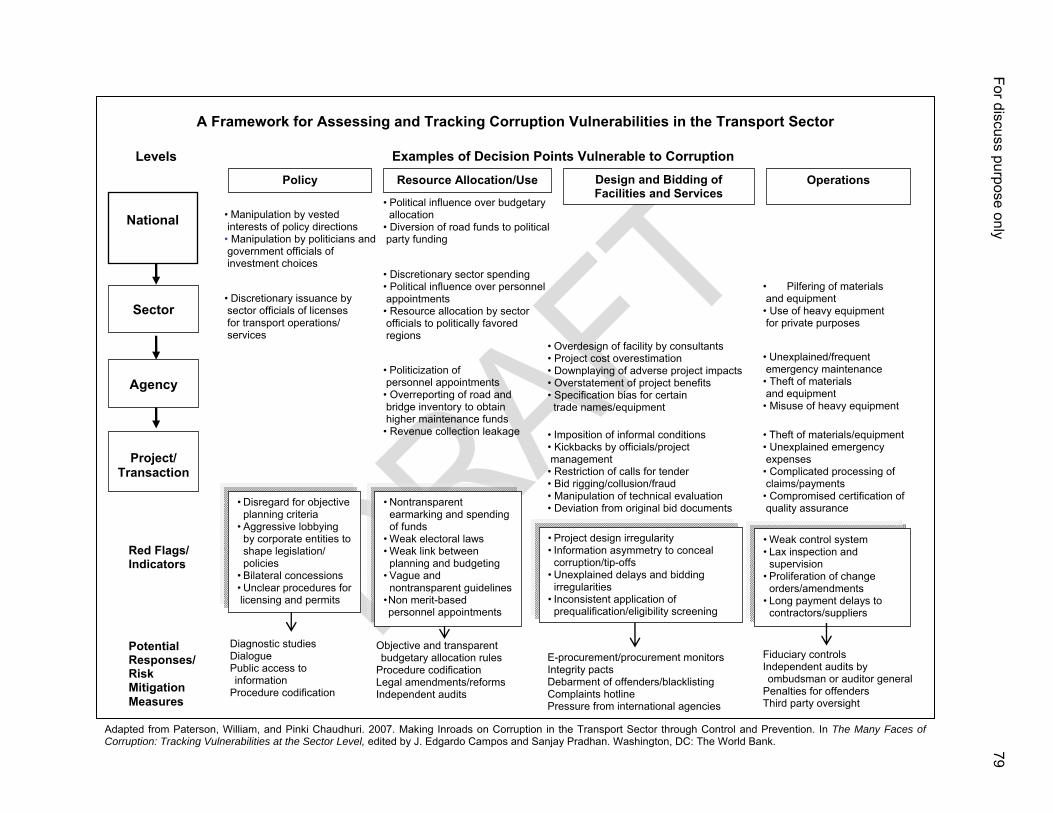

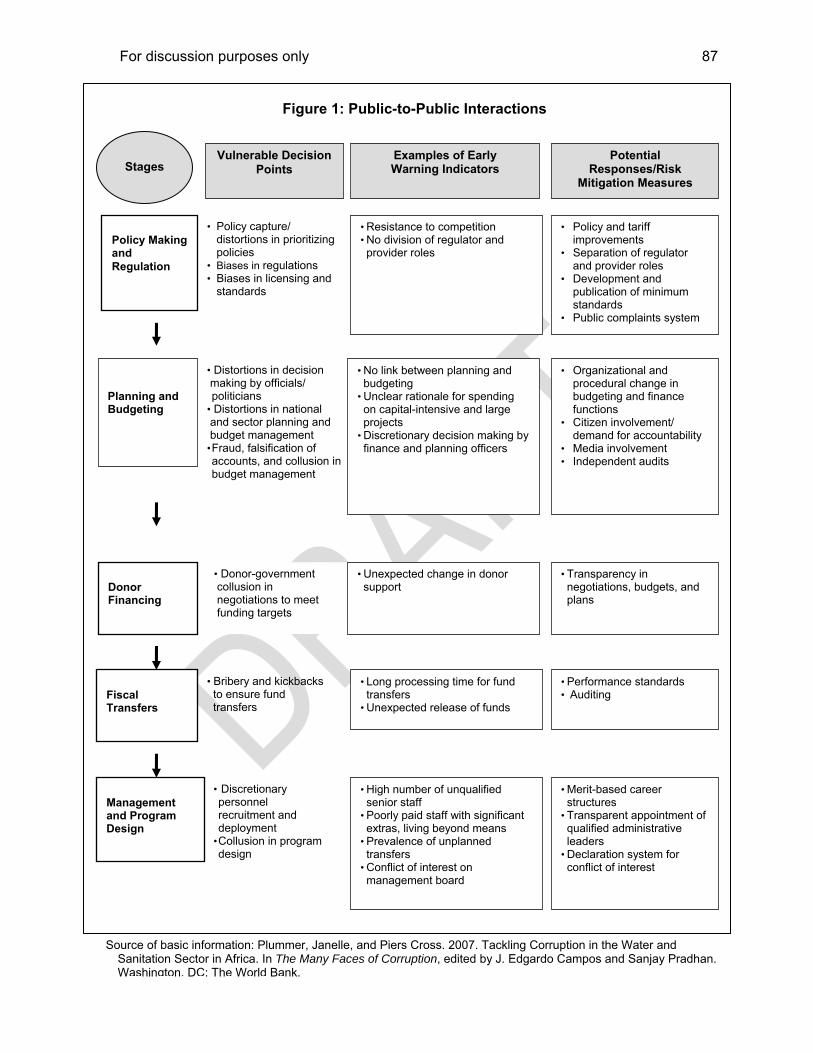

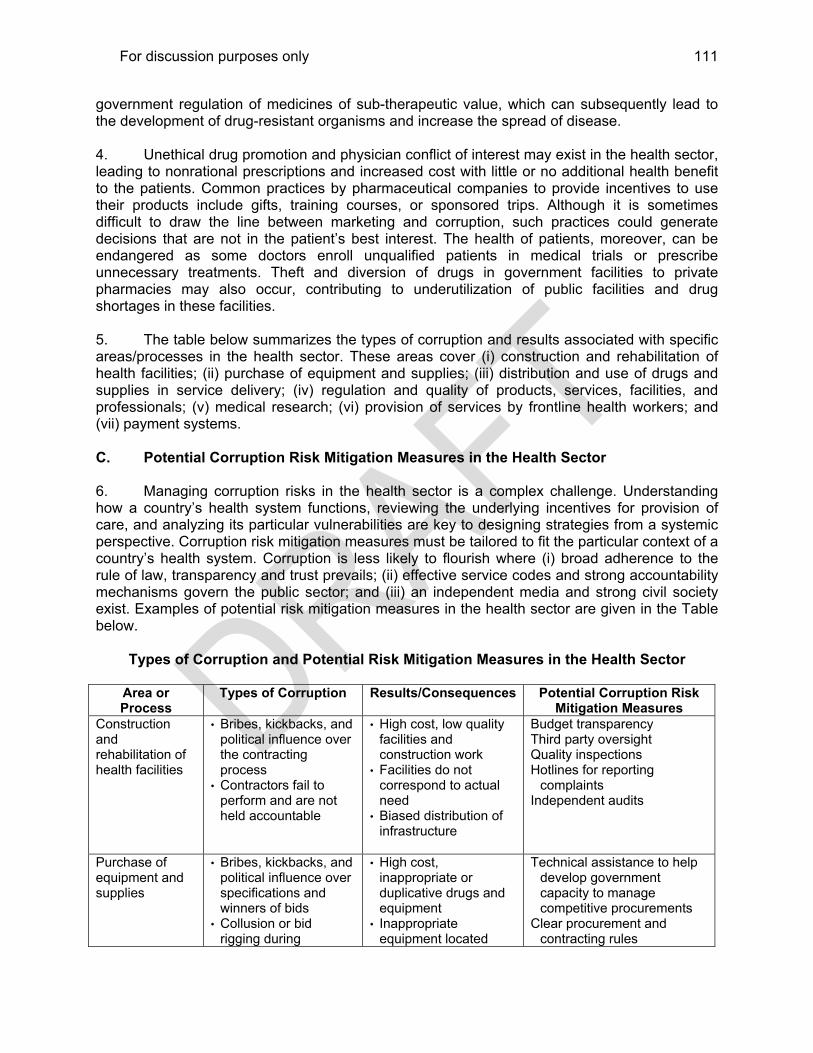

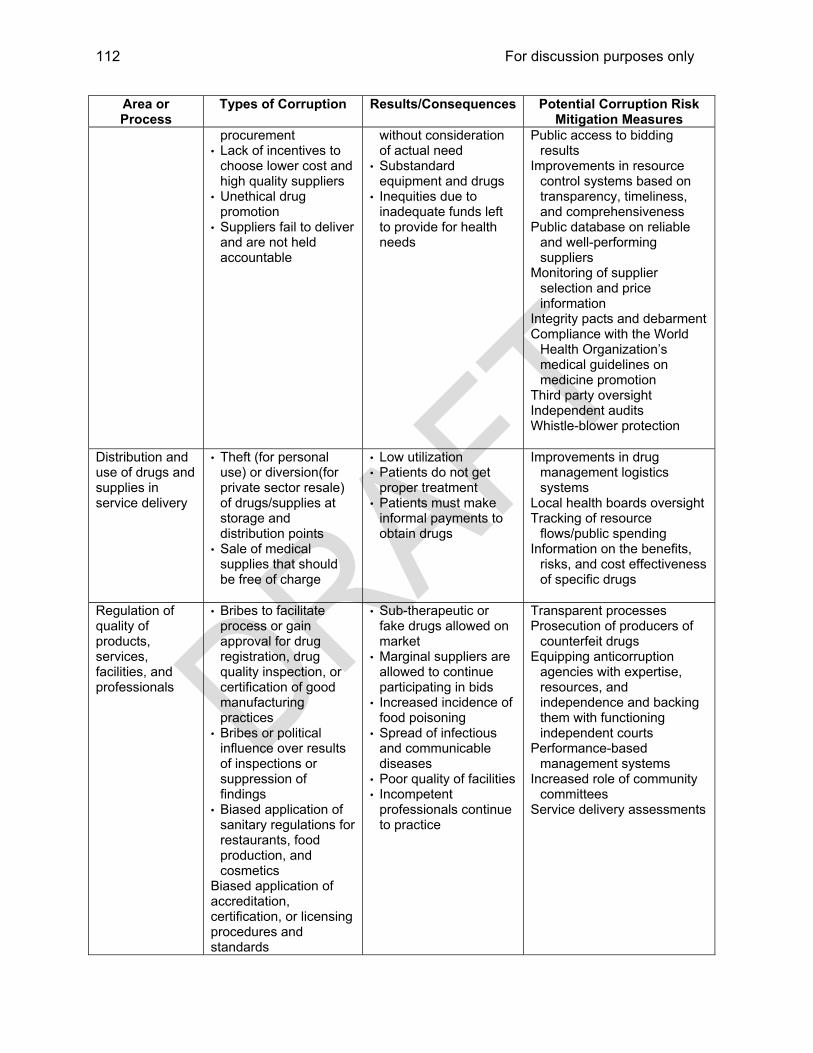

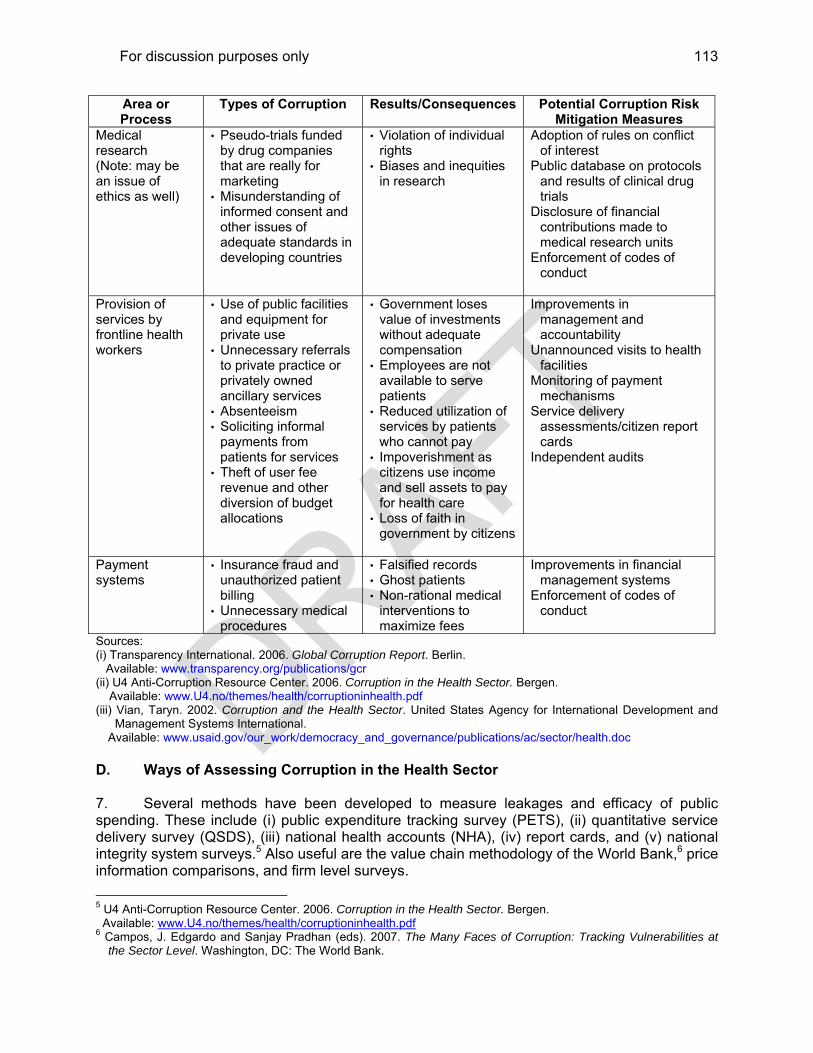

This Sourcebook does not necessarily reflect the views and policies of the Asian Development Bank or its board of governors or the governments they represent. ADB does not guarantee the accuracy of the data included in this publication and accepts no responsibility for any consequence of their use. Use of the term “country” does not imply any judgment by the authors or ADB as to the legal or other status of any territorial entity.

The Sourcebook will be finalized after pilot-testing. ADB would welcome any feedback from practicioners on the usefulness of the tools. Please provide comments to [email protected].

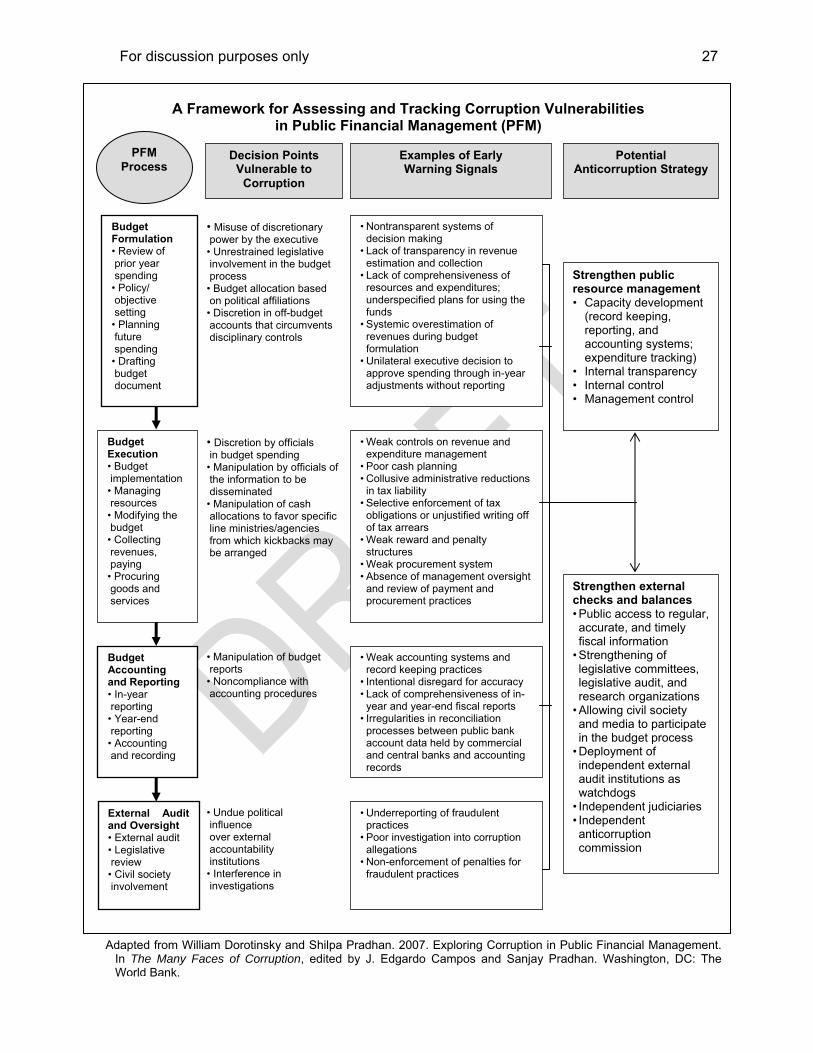

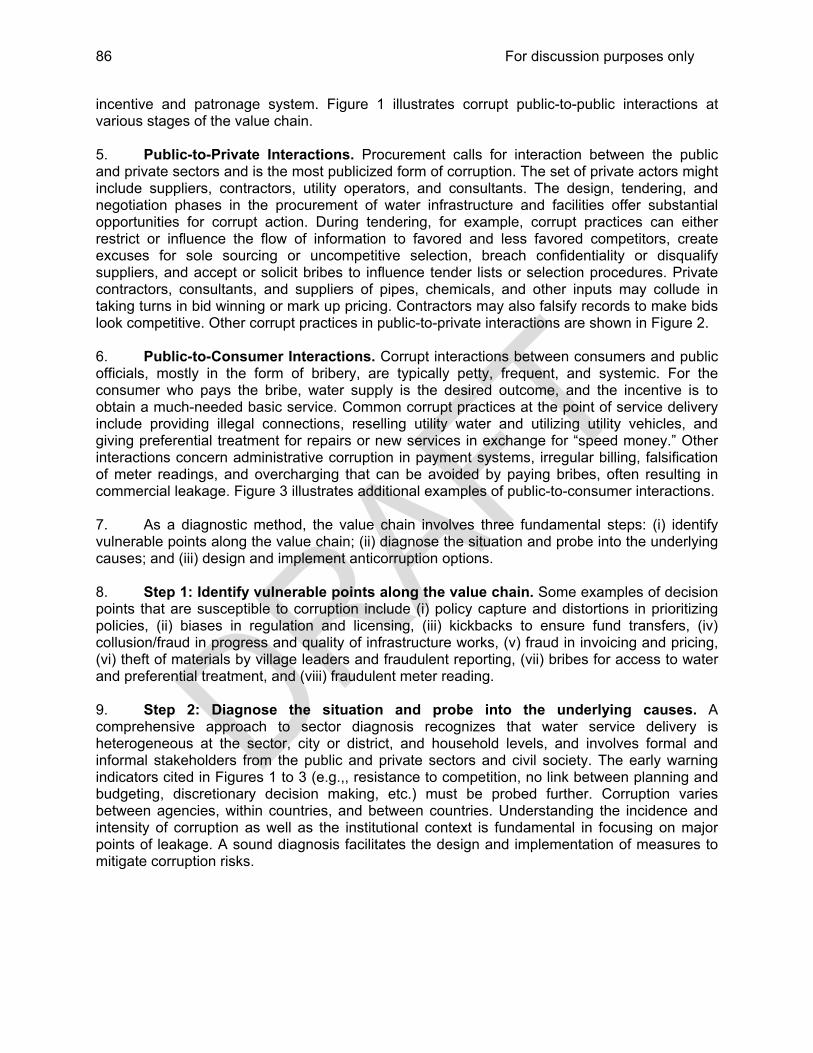

For discussion purposes only

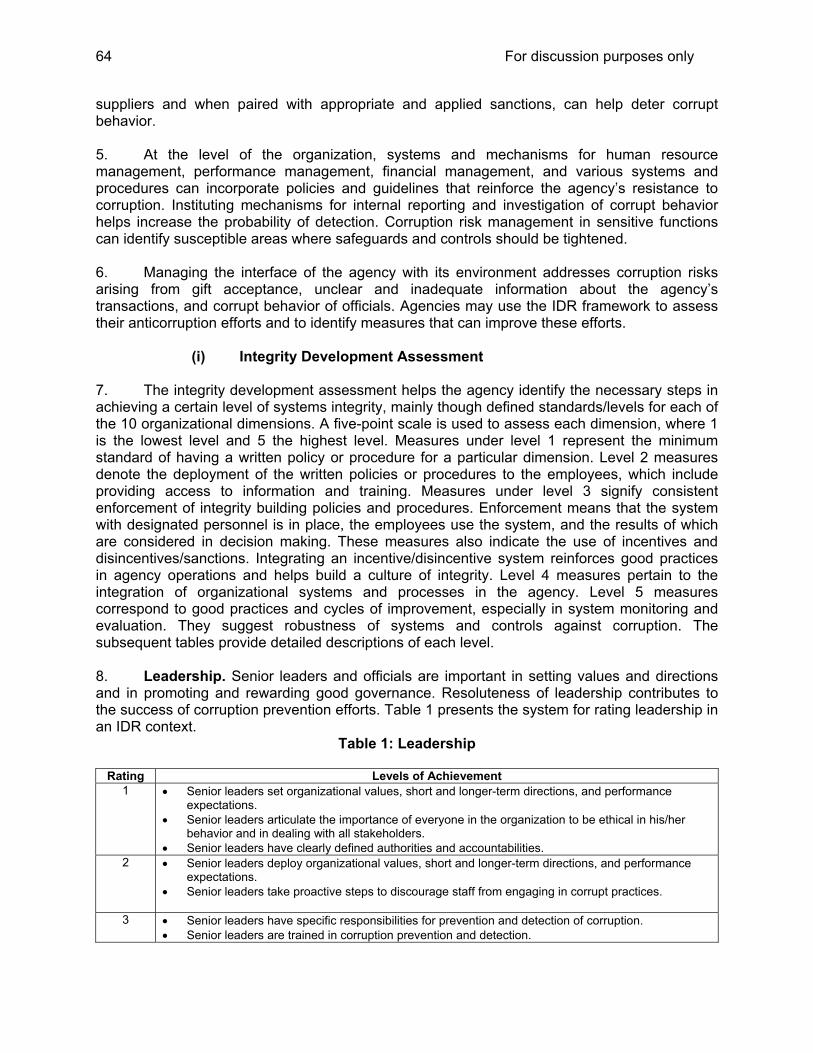

2

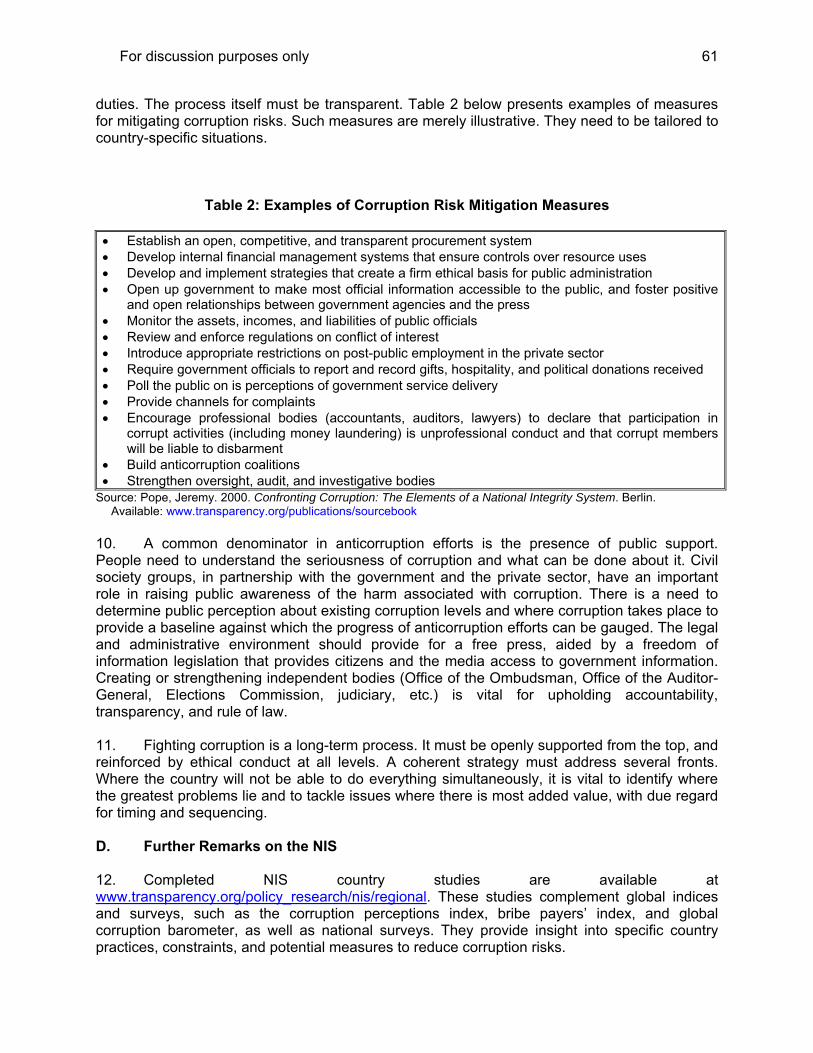

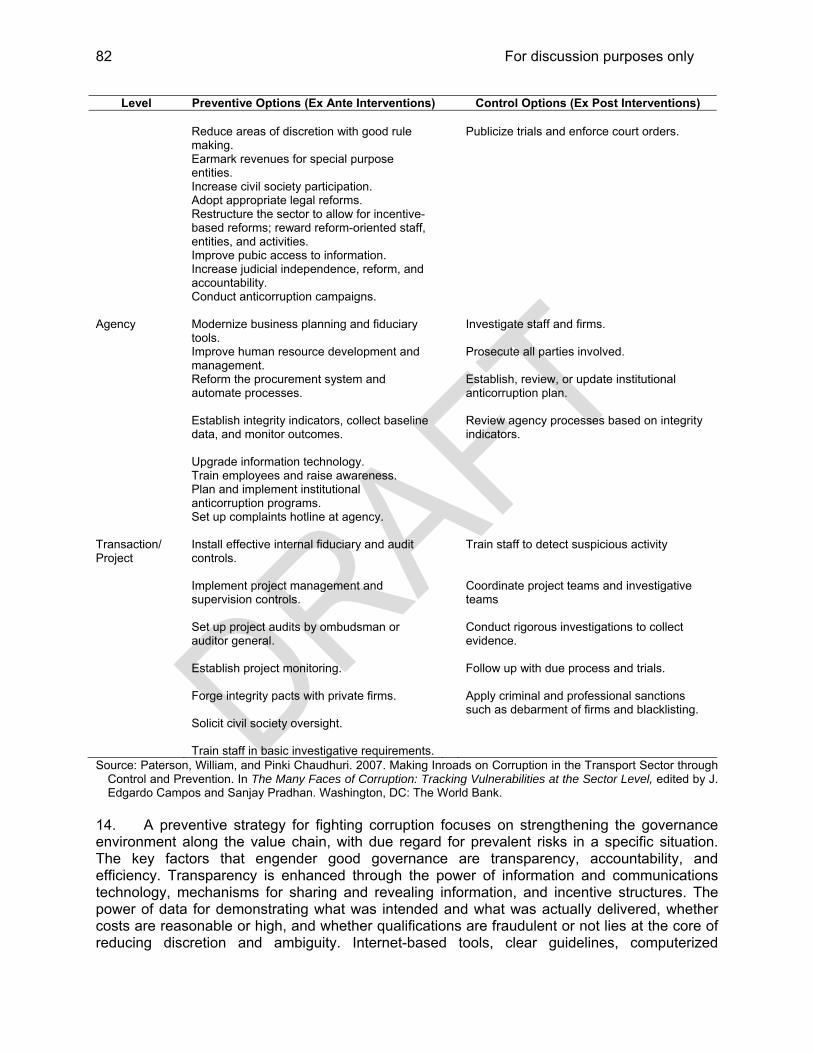

Acknowledgments

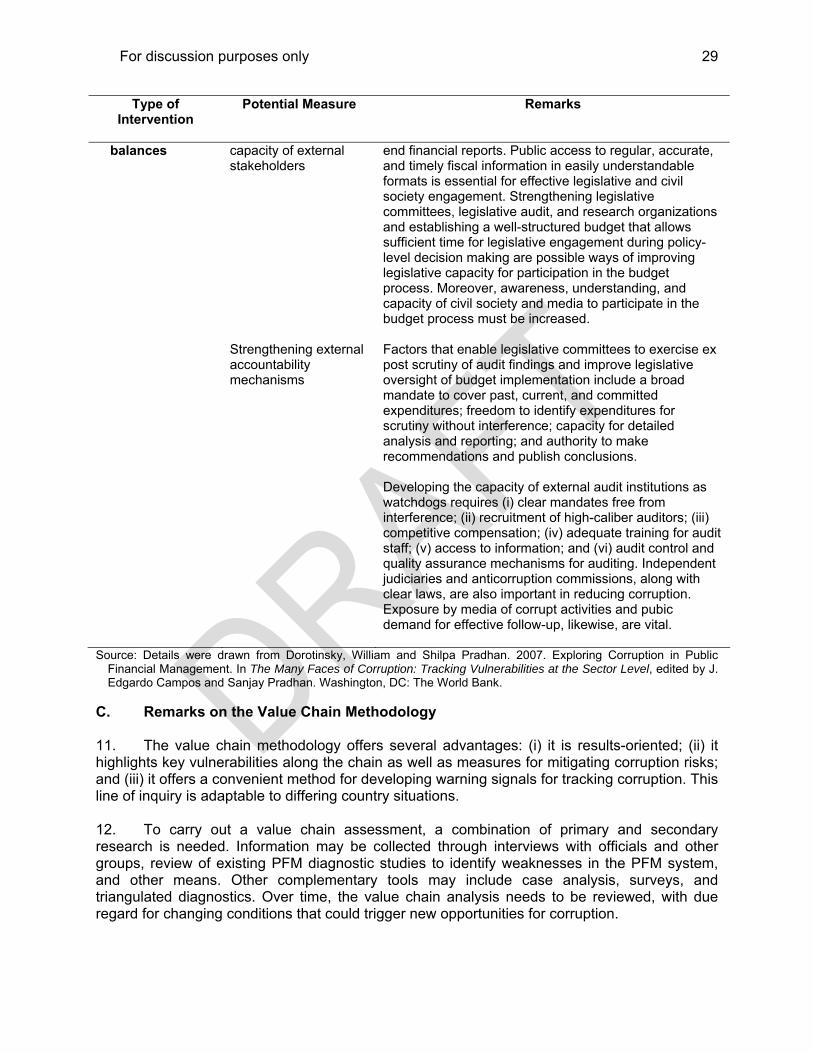

The Sourcebook: Diagnostics to Help Prepare Governance Risk Assessments (the Sourcebook) draws heavily from governance diagnostics that various development partners and organizations developed. It is intended to complement the Guidelines for Implementation of ADB’s Second Governance and Anticorruption Action Plan (GACAP II). The Sourcebook offers a compilation of existing governance tools and analytical frameworks to inform and help, where appropriate, the preparation of risk assessments/risk management plans required under GACAP II. Awareness of existing tools and diagnostic studies is expected to facilitate the work of staff and consultants in reviewing what could be useful for governance risk assessments and in determining analytical gaps that they still need to address. The Sourcebook covers the three priority themes of GACAP II─public financial management, public procurement, and combating corruption.

Special acknowledgment goes to the World Bank whose substantial and diverse contributions to governance diagnostics cut across the thematic spectrum of GACAP II. In particular, the value chain analysis introduced in the World Bank publication The Many Faces of Corruption: Tracking Vulnerabilities at the Sector Level (J. Edgardo Campos and Sanjay Pradhan (eds.), Poverty Reduction and Economic Management, World Bank, 2007) provides useful tools for systematically identifying corruption vulnerabilities at the sector level.

Sincere thanks go to the Public Expenditure and Financial Accountability (PEFA) Secretariat for its PEFA performance measurement tool, and the Organisation for Economic Co-operation and Development, for its procurement assessment methodology and other related governance studies. Similarly, recognition is given to Transparency International’s national integrity systems diagnostics and to the integrity development review of the Development Academy of the Philippines, which are useful in assessing existing safeguards against corruption at the national and agency levels, respectively. Other valuable contributions to the Sourcebook came from the U4 Anti-Corruption Resource Center and from authors working on similar concerns.

Sandra Nicoll, principal governance specialist of ADB, managed the preparation of the Sourcebook. Brenda M. Katon, ADB consultant, researched and identified relevant governance diagnostics; and reviewed, synthesized, and prepared the summaries in this Sourcebook.

The Sourcebook benefited from the review of various ADB staff: Kathleen Moktan, director of the Governance and Capacity Development Division; Hans van Rijn, governance specialist; and members of ADB’s Governance Community of Practice. J. Edgardo Campos of the World Bank also provided feedback. These valuable contributions are gratefully acknowledged.

For discussion purposes only

3

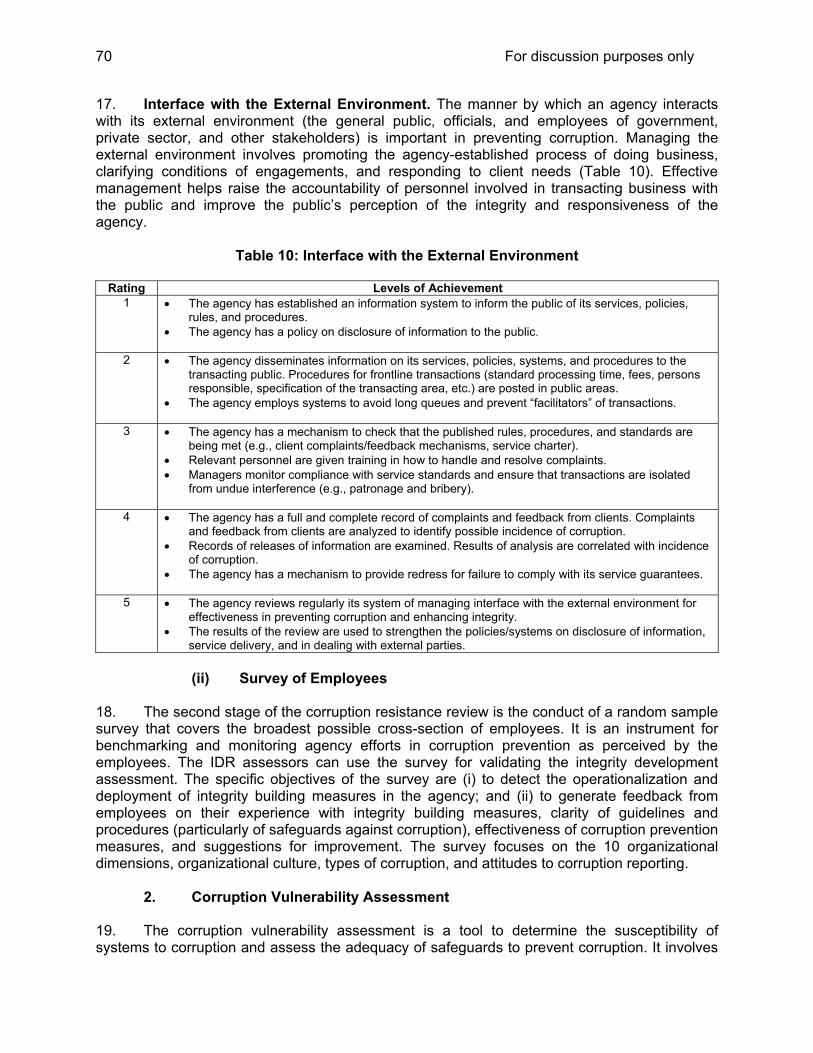

Table of Contents

SECTION 1

Overview of Diagnostic Tools 4

SECTION 2

Public Financial Management 12

SECTION 3

Public Procurement 30

SECTION 4

Combating Corruption

57

For discussion purposes only

4

SECTION 1 – OVERVIEW OF DIAGNOSTIC TOOLS

For discussion purposes only

5

BACKGROUND 1. The Guidelines for Implementing ADB’s Second Governance and Anticorruption Action Plan (GACAP II) were approved in May 2008. The Guidelines describe the process for implementing GACAP II, and the requirement in the Country Partnership Strategy (CPS) Guidelines1 that CPSs are informed by risk assessments (RAs) and risk management plans (RMPs) for national/subnational government systems in which ADB is engaged, and priority sectors for ADB operations. 2. The Sourcebook: Diagnostics to Help Prepare Governance Risk Assessments (the Sourcebook) has three objectives. It aims to (i) complement the GACAP II Guidelines by offering a compilation of diagnostic tools and analytical frameworks to inform and assist, where appropriate, the preparation of RAs and RMPs required under GACAP II; (ii) present summaries of existing tools for assessing governance systems at various levels to provide a quick overview of these tools and frameworks; and (iii) heighten awareness of available diagnostic studies that could serve as inputs to staff and consultants in making professional judgments of what could usefully inform a risk assessment. Gaps in available analysis can be determined and subsequently addressed when undertaking RAs/RMPs. The Sourcebook is not intended to provide definitive guidelines for conducting RAs/RMPs. Such guidance can be found in the GACAP II Guidelines.2 3. The Sourcebook focuses on the three governance thematic priorities under GACAP II: (i) public financial management (PFM), (ii) public procurement, and (iii) combating corruption through preventive, enforcement, and investigative measures.3 These themes apply to national/subnational levels of government and to ADB priority sectors in developing member countries. The Sourcebook provides information on (i) existing diagnostic studies by development partners, and (ii) analytical frameworks for undertaking risk assessments.

TYPES OF ASSESSMENTS

4. Governance diagnostics are systematic activities to collect data, evidence, and perceptions. They provide information to both government and development partners on (i) the strengths and weaknesses of governance systems, (ii) the risks to which funds channeled through these systems may be exposed, (iii) possible directions and priorities for improving governance systems, and (iv) key issues for dialogue with the government and other stakeholders. 5. Broadly, diagnostic assessments may fall into self-assessment and external assessment. Self-assessment entails a reflective and systematic review by a country/sector/agency of its own governance systems and processes. This type of assessment normally has checklists and indicators to make measurement consistent and comparable. It has a potential for building local capacity by investing in and drawing on local know-how, and for fostering ownership.4 It is also strategic in terms of taking steps to move from a diagnostic 1 ADB. 2007. Country Partnership Strategy Guidelines. Manila.

Available: www.adb.org/documents/Guidelines/CPS-guidelines.pdf 2 ADB. 2008. Guidelines for Implementing ADB’s Second Governance and Anticorruption Action Plan (GACAP II).

Manila. Available: www.adb.org/Documents/Guidelines/GACAP-II-Guidelines.pdf 3 ADB. Second Governance and Anticorruption Action Plan. Manila.

Available: www.adb.org/Documents/Policies/Governance/GACAP-II.pdf 4 Rakner, Lise, and Vibeke Wang. 2007. Governance Assessments and the Paris Declaration. Paper presented

during the United Nations Development Programme seminar in Bergen. September. Available: www.undp.org/oslocentre/docs07/BergenSeminar.pdf

For discussion purposes only

6

assessment to the design and implementation of appropriate strategies and programs. Self-assessments, however, may have a potential for bias and may be constrained by insufficient diagnostic capacity. A validation process involving external assessors could contribute to credibility and transparency, and to an agreement on assigned scores and priorities.5 External assessments generally tend to offer greater room for objectivity and analytical rigor. Dialogue between an assessment team and a recipient government provides opportunities for ministries and agencies to communicate, uncover sources of difficulties, and begin working together. Triggering this internal dialogue is an important output of external assessments. 6. Multiple tools are valuable in diagnosis because they uncover different perspectives. The diagnostic exercise can be carried out in a phased manner: (i) analyze broad trends through existing indicators, (ii) identify areas of vulnerability and assess risks, and (iii) prioritize activities in particular sectors or levels of government.

METHODOLOGIES FOR GOVERNANCE DIAGNOSTIC 7. Surveys and interviews may be conducted for both external assessments and self-assessments. Surveys are used in generating sector/subsector diagnosis, as seen in public expenditure tracking surveys, quantitative service delivery surveys, report cards, and investment climate surveys. In the integrity development review, surveys are used to obtain feedback on safeguards against corruption, along with interviews/focus group discussions to assess integrity development. Triangulated diagnostics that involve various key informants (citizens, firms, public officials, etc.) offer multidimensional perspectives and facilitate validation of assessment findings. 8. Aggregate analysis supports a big picture perspective (country and cross-country). It covers the World Bank's worldwide governance indicators, which consist of (i) voice and accountability, (ii) political stability and absence of violence, (iii) government effectiveness, (iv) regulatory quality, (v) rule of law, and (vi) control of corruption.6 It also includes the corruption perceptions index and global corruption barometer of the Transparency International (www.transparency.org), and the global integrity report of the Global Integrity (www.globalintegrity.org). The high level of aggregation of the indices tends to make assessment rather abstract. Nevertheless, the data can serve as a first cut on areas where further analysis is required. Also useful is country profiling that brings together available findings from various diagnostics (www.business-anti-corruption.com/normal.asp?pageid=6).

PUBLIC FINANCIAL MANAGEMENT DIAGNOSTICS 9. Table 1 presents the key strengths and limitations of PFM diagnostic tools described in Section 2: (i) Country Financial Accountability Assessment (CFAA); (ii) Public Expenditure and Financial Accountability (PEFA) Performance Measurement; and (iii) Framework for Assessing and Tracking Corruption Vulnerabilities in Public Financial Management.

5 Public Expenditure and Financial Accountability Working Group. 2005. Supporting Better Country Public Financial

Management Systems. Washington, DC. Available: www.pefa.org 6 Kaufmann, Daniel, Aart Kraay, and Massimo Mastruzzi. 2008. Governance Matters VII. Washington, DC: World

Bank Institute. Available: www.worldbank.org/wbi/governance

For discussion purposes only

7

Table 1: Diagnostic Tools in Public Financial Management

Diagnostic Tool Key Features Country Financial Accountability Assessment or CFAA (World Bank)

• Designed to provide information about the financial management environment in which funds may be disbursed

• Assesses risks to the achievement of a country’s development objectives posed by gaps or weaknesses in public financial management (PFM) arrangements

• Covers (i) budget formulation, (ii) budget execution, (iii) reporting and auditing, and (iv) external scrutiny of public finances

• Provides recommendations and action plans • Informs the design and implementation of a capacity development program • Does not examine the risk that funds will not be well spent; not an audit that

tracks spending • Does not assess the level of sovereign risk (the risk that donor funds might not

be repaid at all or might not be repaid on time)

Public Expenditure and Financial Accountability Performance Measurement (PEFA)

• Looks into six core dimensions: (i) credibility of the budget; (ii) comprehensiveness and transparency; (iii) policy-based budgeting; (iv) predictability and control in budget execution; (v) accounting, recording, and reporting; and (vi) external scrutiny and audit

• Uses information from fiscal and expenditure policy analysis to assess the extent to which the PFM system constitutes an enabling factor for achieving planned budgetary outcomes, such as (i) aggregate fiscal discipline, (ii) strategic resource allocation, and (iii) efficient service delivery

• Primarily a statement of current performance with indicators (benchmarking) • Does not include action plans • Its set of indicators, however, could provide a common platform for dialogue

between government and development partners regarding the current PFM performance, recent progress, and development of an action plan

• The government may carry out an initial self-assessment, development partners and the government may undertake the process jointly, or the government may just provide information

• Does not assess fiduciary risk (e.g., funds are not used for their intended purposes). However, it can be an input to a separate fiduciary risk assessment.

Framework for Assessing and Tracking Corruption Vulnerabilities in Public Financial Management (World Bank)

• Uses a value chain methodology to understanding corruption in PFM, mainly by assessing and tracking vulnerabilities along the chain of budget formulation, budget execution, budget accounting and reporting, and external audit and oversight

• Identifies early warning signals and potential anticorruption strategies • Updating is needed over time, with due regard for changing conditions and new

opportunities for corruption PEFA = public expenditure and financial accountability Sources: (i) World Bank. 2003. Country Financial Accountability Assessment Guidelines to Staff. Washington, DC. Available:

www.countryanalyticwork.net/caw/cawdoclib.nsf/0/FF135D16EB395D6985256D39006C9483/$file/CFAAGuidelines2003.pdf

(ii) Public Expenditure and Financial Accountability Program. 2005. Public Financial Management Performance Measurement Framework. Washington, DC. Available: www.pefa.org

(iii) Allen, Richard, Salvatore Schiavo-Campo, and Thomas Columkill Garrity. 2004. Assessing and Reforming Public Financial Management. Washington, DC: The World Bank. Available: http://go.worldbank.org/T7WH97YN00

(iv) Dorotinsky, William, and Shilpa Pradhan. 2007. Exploring Corruption in Public Financial Management. In The Many Faces of Corruption, edited by J. Edgardo Campos and Sandjay Pradhan. Washington, DC: The World Bank.

For discussion purposes only

8

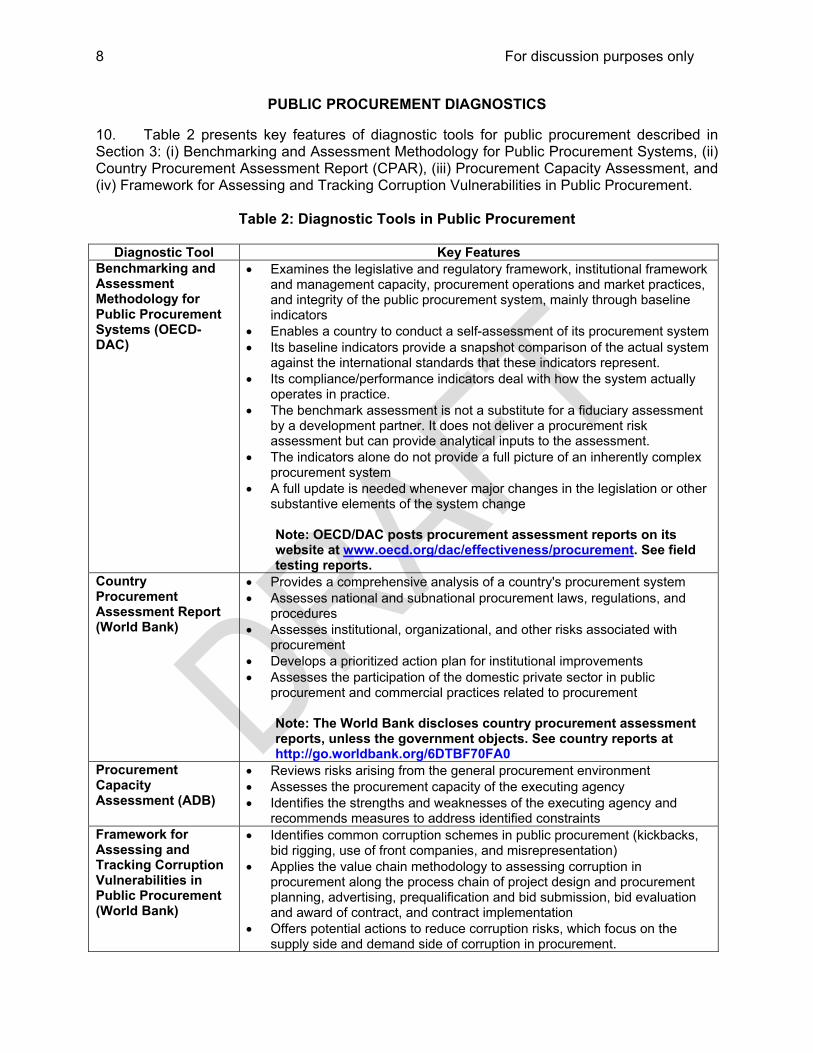

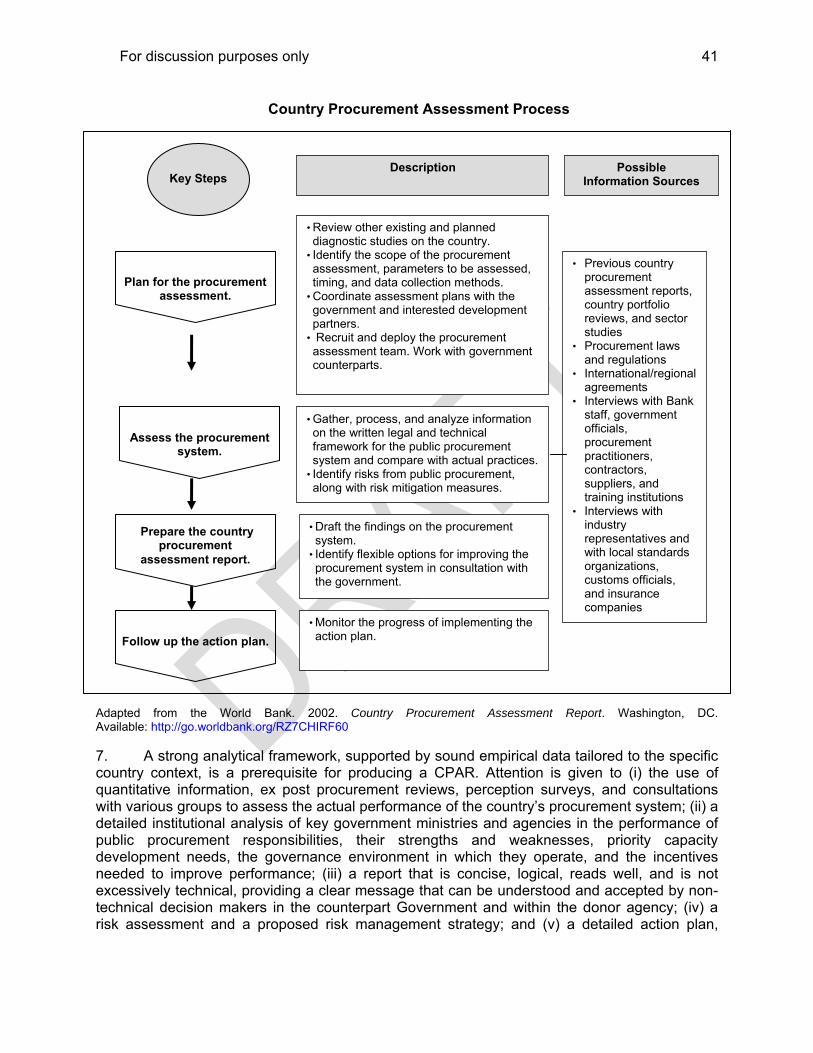

PUBLIC PROCUREMENT DIAGNOSTICS 10. Table 2 presents key features of diagnostic tools for public procurement described in Section 3: (i) Benchmarking and Assessment Methodology for Public Procurement Systems, (ii) Country Procurement Assessment Report (CPAR), (iii) Procurement Capacity Assessment, and (iv) Framework for Assessing and Tracking Corruption Vulnerabilities in Public Procurement.

Table 2: Diagnostic Tools in Public Procurement

Diagnostic Tool Key Features Benchmarking and Assessment Methodology for Public Procurement Systems (OECD-DAC)

• Examines the legislative and regulatory framework, institutional framework and management capacity, procurement operations and market practices, and integrity of the public procurement system, mainly through baseline indicators

• Enables a country to conduct a self-assessment of its procurement system • Its baseline indicators provide a snapshot comparison of the actual system

against the international standards that these indicators represent. • Its compliance/performance indicators deal with how the system actually

operates in practice. • The benchmark assessment is not a substitute for a fiduciary assessment

by a development partner. It does not deliver a procurement risk assessment but can provide analytical inputs to the assessment.

• The indicators alone do not provide a full picture of an inherently complex procurement system

• A full update is needed whenever major changes in the legislation or other substantive elements of the system change

Note: OECD/DAC posts procurement assessment reports on its website at www.oecd.org/dac/effectiveness/procurement. See field testing reports.

Country Procurement Assessment Report (World Bank)

• Provides a comprehensive analysis of a country's procurement system • Assesses national and subnational procurement laws, regulations, and

procedures • Assesses institutional, organizational, and other risks associated with

procurement • Develops a prioritized action plan for institutional improvements • Assesses the participation of the domestic private sector in public

procurement and commercial practices related to procurement

Note: The World Bank discloses country procurement assessment reports, unless the government objects. See country reports at http://go.worldbank.org/6DTBF70FA0

Procurement Capacity Assessment (ADB)

• Reviews risks arising from the general procurement environment • Assesses the procurement capacity of the executing agency • Identifies the strengths and weaknesses of the executing agency and

recommends measures to address identified constraints Framework for Assessing and Tracking Corruption Vulnerabilities in Public Procurement (World Bank)

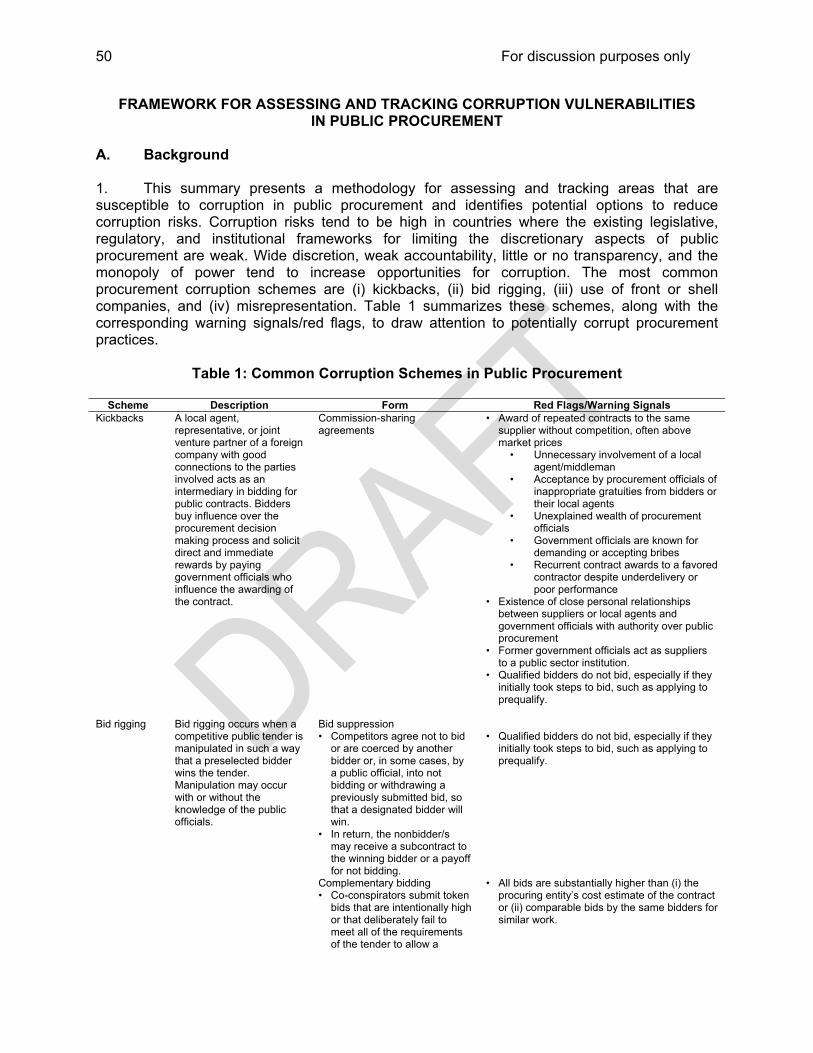

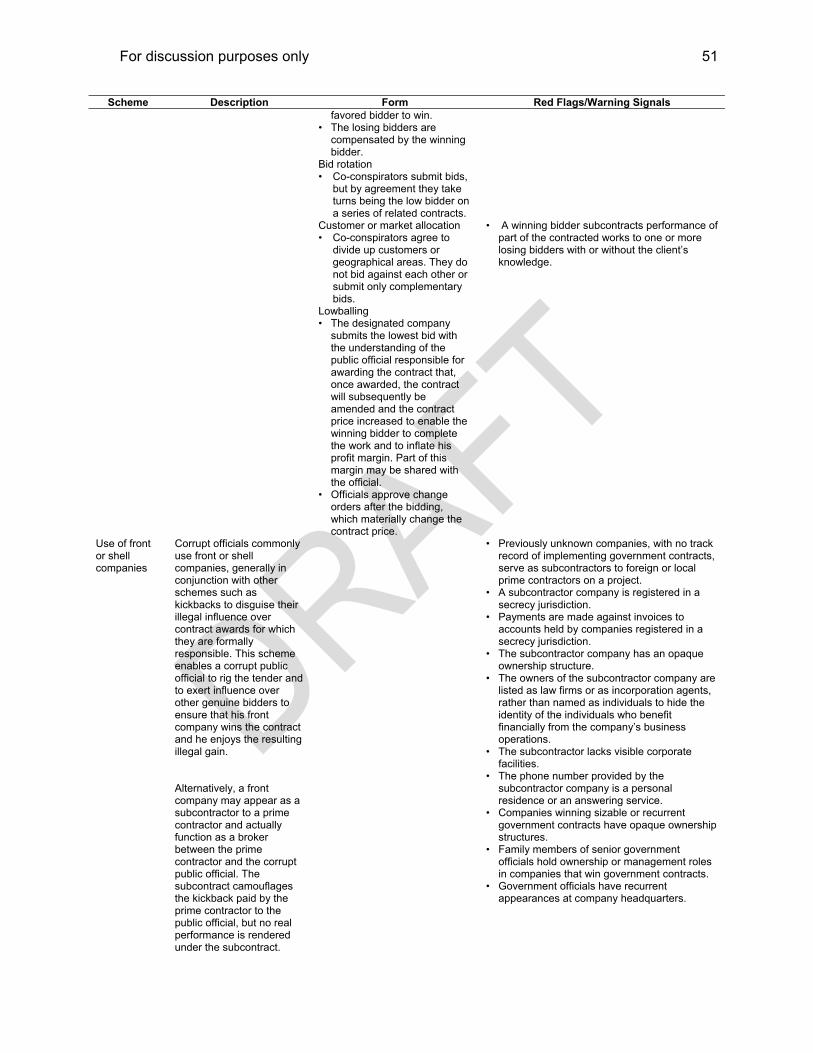

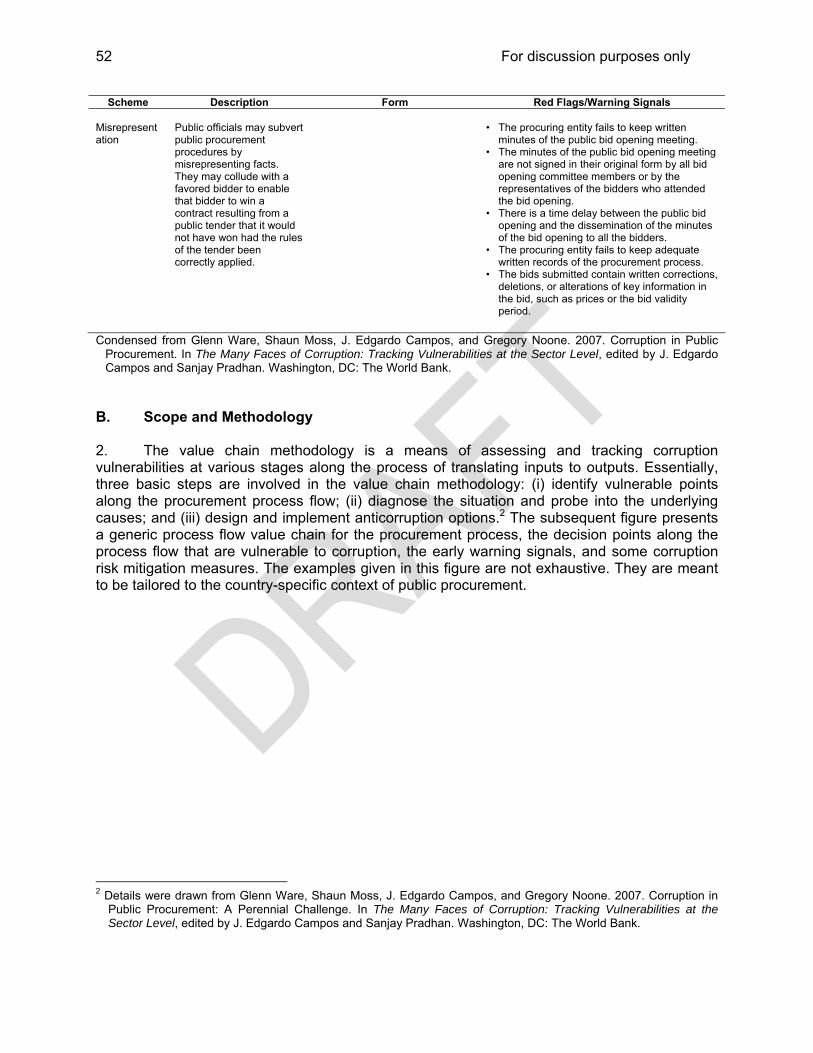

• Identifies common corruption schemes in public procurement (kickbacks, bid rigging, use of front companies, and misrepresentation)

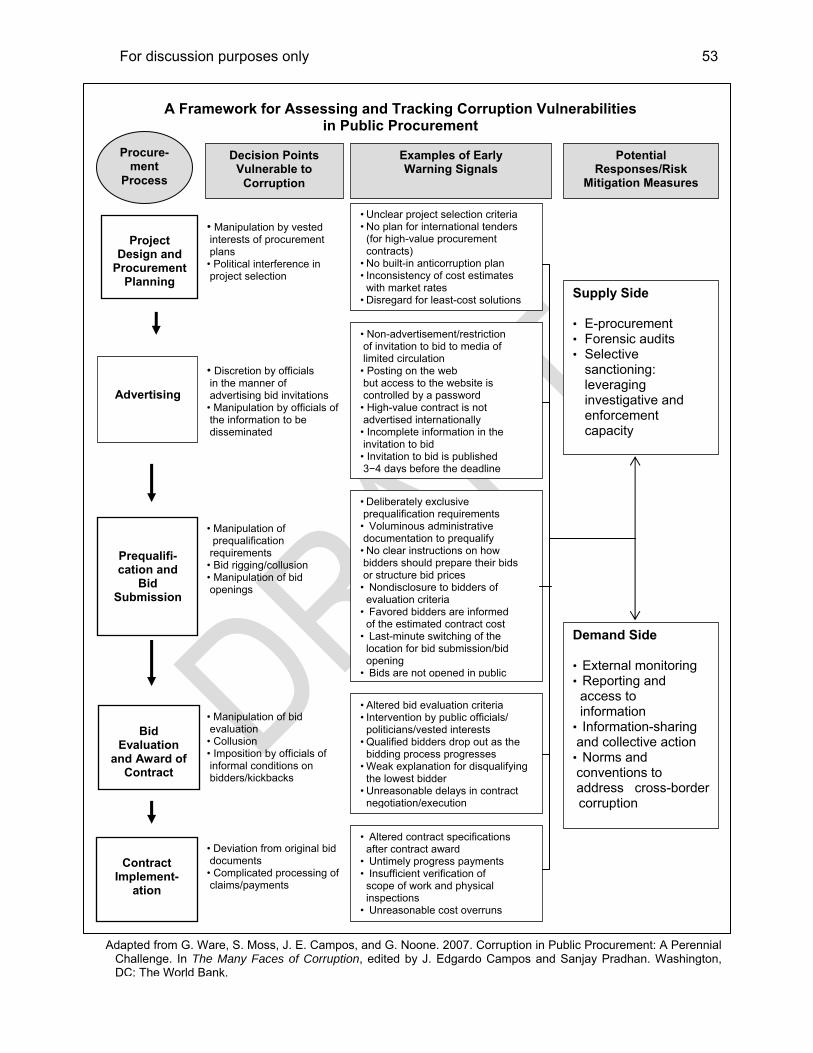

• Applies the value chain methodology to assessing corruption in procurement along the process chain of project design and procurement planning, advertising, prequalification and bid submission, bid evaluation and award of contract, and contract implementation

• Offers potential actions to reduce corruption risks, which focus on the supply side and demand side of corruption in procurement.

For discussion purposes only

9

ADB = Asian Development Bank, OECD–DAC = Organisation for Economic Co-operation and Development –Development Assistance Committee Sources: (i) Organisation for Economic Co-operation and Development. 2006. Methodology for Assessment of National

Procurement Systems. Version 4. Paris. Available: www.oecd.org/dataoecd/1/36/37130136.pdf (ii) OECD/DAC. 2007. Pilot Exercise Progress Reports. Paris. Available: www.oecd.org/dac/effectiveness/procurement (iii) World Bank. 2002. Country Procurement Assessment Report. Washington, DC. Available:

www.countryanalyticwork.net/caw/cawdoclib.nsf/vewMainProductToolkits/0F42E09A92F63AAD85256C5E005EB0EA/$file/preparation+of+CPAR.pdf and http://go.worldbank.org/RZ7CHIRF60

(iv) ADB. 2007. Procurement Capacity Assessment: Executing Agency. Manila. Available: http://mms.adb.org/test/capacity-assessment-guide.pdf (v) Ware, Glenn, Shaun Moss, J. Edgardo Campos, and Gregory Noone. 2007. Corruption in Public Procurement: A

Perennial Challenge. In The Many Faces of Corruption, edited by J. Edgardo Campos and Sandjay Pradhan. Washington, DC: The World Bank.

ANTICORRUPTION DIAGNOSTICS

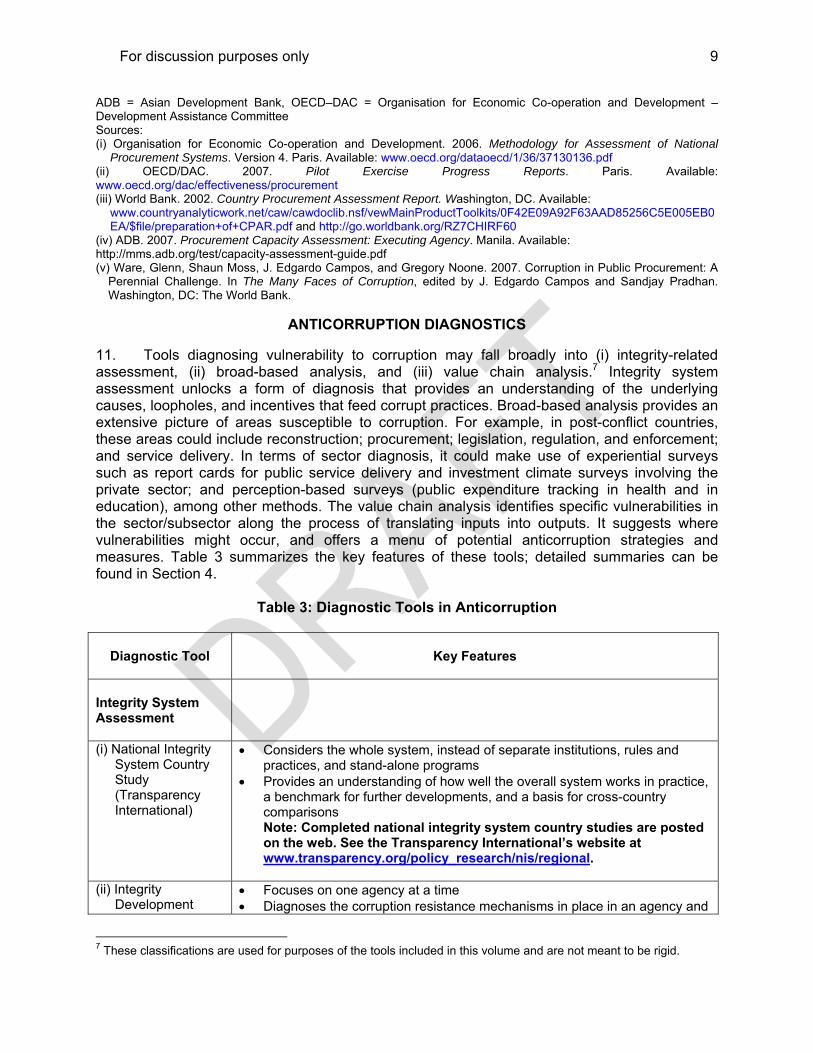

11. Tools diagnosing vulnerability to corruption may fall broadly into (i) integrity-related assessment, (ii) broad-based analysis, and (iii) value chain analysis.7 Integrity system assessment unlocks a form of diagnosis that provides an understanding of the underlying causes, loopholes, and incentives that feed corrupt practices. Broad-based analysis provides an extensive picture of areas susceptible to corruption. For example, in post-conflict countries, these areas could include reconstruction; procurement; legislation, regulation, and enforcement; and service delivery. In terms of sector diagnosis, it could make use of experiential surveys such as report cards for public service delivery and investment climate surveys involving the private sector; and perception-based surveys (public expenditure tracking in health and in education), among other methods. The value chain analysis identifies specific vulnerabilities in the sector/subsector along the process of translating inputs into outputs. It suggests where vulnerabilities might occur, and offers a menu of potential anticorruption strategies and measures. Table 3 summarizes the key features of these tools; detailed summaries can be found in Section 4.

Table 3: Diagnostic Tools in Anticorruption

Diagnostic Tool

Key Features

Integrity System Assessment

(i) National Integrity System Country Study (Transparency International)

• Considers the whole system, instead of separate institutions, rules and practices, and stand-alone programs

• Provides an understanding of how well the overall system works in practice, a benchmark for further developments, and a basis for cross-country comparisons Note: Completed national integrity system country studies are posted on the web. See the Transparency International’s website at www.transparency.org/policy_research/nis/regional.

(ii) Integrity Development

• Focuses on one agency at a time • Diagnoses the corruption resistance mechanisms in place in an agency and

7 These classifications are used for purposes of the tools included in this volume and are not meant to be rigid.

For discussion purposes only

10

Diagnostic Tool

Key Features

Review (Development Academy of the Philippines)

assesses its vulnerabilities to corruption • Provides a corruption prevention and integrity enhancement plan • Multi-method approach • Detailed checklists • Top management support and commitment of the agency are vital

Country Self-Assessment/Stock-taking: Anticorruption (ADB/OECD)

• Provides a comprehensive overview of the country’s existing legal and institutional framework to enhance transparency in the public sector, combat bribery and promote integrity in business operations, and facilitate public involvement in anticorruption efforts

• Helps identify emerging trends and remaining challenges to combating corruption

Note: Completed country reports are posted on the web. See www.oecd.org/corruption/asiapacific.

Value Chain Methodology (World Bank)

• Focuses on results that a sector or process seeks to achieve • Provides a structured picture of vulnerable decision points • Points to key vulnerabilities and remedial measures that could mitigate

corruption risks • Offers a mechanism for developing warning signals/indicators for tracking

the incidence of corruption • Adaptable to various sector/subsector situations • Changes in institutional actors and sector structures can give rise to new

corruption opportunities and risks; initial findings need to be revisited and updated.

ADB = Asian Development Bank, OECD = Organisation for Economic Co-operation and Development. Sources: (i) Transparency International. Various years. National Integrity Systems Country Studies. Berlin.

Available: www.transparency.org/policy_research/nis/regional (ii) Pope, Jeremy. 2000. Confronting Corruption: The Elements of a National Integrity System. Berlin: Transparency

International. Available: www.transparency.org/policy_research/nis (iii) Development Academy of the Philippines. 2007. Pursuing Reforms through Integrity Development. Manila. (iv) ADB/OECD Anti-Corruption Initiative for Asia and the Pacific. 2003. Action Plan Stocktaking Exercise. (v) Campos, J. Edgardo, and Sanjay Pradhan (eds.). 2007. The Many Faces of Corruption: Tracking Vulnerabilities at

the Sector Level. Washington, DC: The World Bank. (vi) U4 Anti-Corruption Resource Center. Various sector and thematic assessments. Bergen. Available:

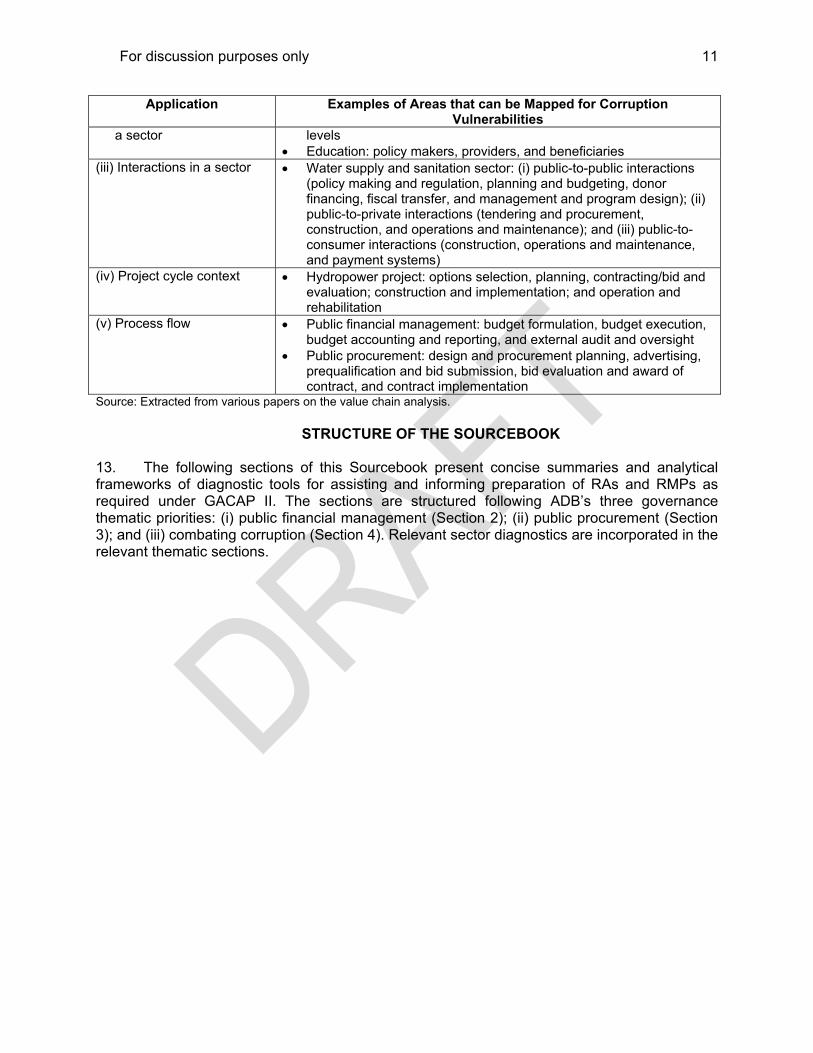

www.u4.no/themes 12. As shown in Table 4, the value chain methodology has a number of applications that can fit specific situations.

Table 4: Various Applications of the Value Chain Methodology

Application

Examples of Areas that can be Mapped for Corruption Vulnerabilities

(i) Sector/subsector context: sequential stages

• Electricity sector: generation, transmission, and distribution • Pharmaceuticals as a subset of the health sector: manufacturing,

registration, drug selection, procurement, distribution, and prescription and dispensing

(ii) Levels of operation within • Transport sector: national, sector, agency, and project/transaction

For discussion purposes only

11

Application

Examples of Areas that can be Mapped for Corruption Vulnerabilities

a sector

levels • Education: policy makers, providers, and beneficiaries

(iii) Interactions in a sector

• Water supply and sanitation sector: (i) public-to-public interactions (policy making and regulation, planning and budgeting, donor financing, fiscal transfer, and management and program design); (ii) public-to-private interactions (tendering and procurement, construction, and operations and maintenance); and (iii) public-to-consumer interactions (construction, operations and maintenance, and payment systems)

(iv) Project cycle context

• Hydropower project: options selection, planning, contracting/bid and evaluation; construction and implementation; and operation and rehabilitation

(v) Process flow

• Public financial management: budget formulation, budget execution, budget accounting and reporting, and external audit and oversight

• Public procurement: design and procurement planning, advertising, prequalification and bid submission, bid evaluation and award of contract, and contract implementation

Source: Extracted from various papers on the value chain analysis.

STRUCTURE OF THE SOURCEBOOK

13. The following sections of this Sourcebook present concise summaries and analytical frameworks of diagnostic tools for assisting and informing preparation of RAs and RMPs as required under GACAP II. The sections are structured following ADB’s three governance thematic priorities: (i) public financial management (Section 2); (ii) public procurement (Section 3); and (iii) combating corruption (Section 4). Relevant sector diagnostics are incorporated in the relevant thematic sections.

For discussion purposes only

12

SECTION 2

PUBLIC FINANCIAL MANAGEMENT

Country Financial Accountability Assessment Methodology

13

Public Expenditure and Financial Accountability Performance Measurement

17

Framework for Assessing and Tracking Corruption Vulnerabilities in Public Financial Management

25

For discussion purposes only

13

COUNTRY FINANCIAL ACCOUNTABILITY ASSESSMENT METHODOLOGY

A. Background

1. The World Bank’s country financial accountability assessment (CFAA) is a diagnostic tool designed to enhance knowledge of a country’s public financial management (PFM) and accountability arrangements. The CFAA (i) provides information on the state and performance of PFM systems; (ii) assesses risks to the achievement of a country’s development objectives posed by gaps or weaknesses in PFM arrangements; (iii) pinpoints priorities for action; and (iv) informs the design and implementation of capacity building programs.1 B. Scope and Methodology

2. The CFAA addresses the overall quality of a country’s PFM, covering budget development, budget execution and monitoring, reporting and auditing, and external scrutiny of public finances. Government ownership and leadership of the CFAA process, along with open and transparent processes, are vital to ensure that the product is responsive to the country’s development priorities and is positioned in a broader governance context. With the move toward greater use of country PFM systems rather than separate “ring-fenced” systems, the CFAA will increasingly support loan portfolio management and inform decisions on the scope and depth of financial management assessments of implementing entities for individual projects, financial reporting and auditing requirements for the portfolio, and approaches to the supervision of financial aspects of the portfolio. 3. The scope of work to be carried out in each CFAA is determined by the knowledge required. This, in turn, depends on (i) the availability of relevant information on PFM, (ii) the planned resource transfer pattern (including lending volumes, instruments to be used, and the sector and institutional focus of the program), (iii) the views of the government, and (iv) agreements reached with development partners. The scope and level of coverage of the CFAA considers the country’s size, stage of development, and relationship with development partners. 4. Risk Assessment. The CFAA incorporates an assessment of risks to funds that are managed through the PFM system. In particular, the key aspects of risks that are analyzed include (i) non-spending of funds for the purposes set out in the budget, which could indicate unrealistic budgets, inadequate internal controls to allocate funds and adhere to budget limits, and lack of commitment to fiscal discipline; (ii) noncoverage by the budget of significant government activities, which could indicate a risk that budget support from the donor might be diverted to off-budget activities for which there is little transparency; (iii) insufficiency of reliable and timely information on budget execution; and (iv) inconsistency between practices and rules. The risk assessment in the CFAA informs the overall assessment of fiduciary risk to donor funds. 5. CFAA Process. The key steps in the CFAA process are summarized in the subsequent figure.

1 World Bank. 2003. Country Financial Accountability Assessment Guidelines to Staff. Washington, DC. Available:

www.countryanalyticwork.net/caw/cawdoclib.nsf/0/FF135D16EB395D6985256D39006C9483/$file/CFAAGuidelines2003.pdf

For discussion purposes only

14

CFAA = country financial accountability assessment, CPAR = country procurement assessment report, PER = public expenditure review, PFM = public financial management. Adapted from the World Bank. 2003. Country Financial Accountability Assessment Guidelines to Staff. Washington, DC. Available: www.countryanalyticwork.net/caw/cawdoclib.nsf/0/FF135D16EB395D6985256D39006C9483/$file/CFAAGuidelines2003.pdf 6. The CFAA includes empirical evidence of what is happening versus what the institutional rules stipulate. Discussions with spending ministries, central agencies, decentralized spending entities, nongovernment organizations, and business groups are helpful in providing information on the operation of the country’s PFM system. 7. After the review, the CFAA team shares the report with country authorities and participating partners, and encourages the government to conduct discussions on the draft report with various stakeholders, including external parties. The team considers these comments carefully, makes appropriate changes to the report, and incorporates an overall government response as a section in the CFAA report, if necessary. This may not be necessary if the government is a full partner in the CFAA and has accepted its conclusions and

Fig. 1: Country Financial Accountability Assessment Process

• Draft the CFAA findings. Discuss with the Government and other partners.

• Prepare an action plan, if appropriate, in consultation with the government.

• Conduct a peer review of the CFAA. • Agree on report disclosure arrangements.

• Existing country reports, country portfolio reviews, governance reviews, policy reviews, CFAA, CPAR, PER, corruption surveys, and other diagnostic studies

• Project financial management assessments and project performance evaluation reports

• International Monetary Fund reports on PFM and fiscal transparency

• Government budget documents and financial statements

• Other related documents from international organizations, development partners, and nongovernment organizations

• Conduct a review of existing and planned diagnostic studies on the country.

• Identify the scope of the financial accountability assessment, timing, and data collection methods.

• Coordinate assessment plans with the government and interested development partners.

• Deploy an initial planning mission. Consider a workshop to explain the CFAA purpose and request country participation.

• Work with government counterparts.

Description

PossibleInformation Sources

Key Steps

• Obtain empirical evidence for the CFAA. • Interact with various groups. • Process and analyze information. • Identify risks to the use of public resources and formulate risk mitigation measures.

• Implement and monitor the action plan.

Follow up the action plan.

Prepare the assessment report.

Identify the issues and assess the situation.

Plan for the assessment.

For discussion purposes only

15

recommendations. The government is given an opportunity to reflect in its comments any disagreement between the CFAA team and the government. The team discusses and agrees on disclosure arrangements with the government.2 The CFAAs are not disclosed without the government’s agreement. The country may request that the risk assessment not be made public, or the country director may advise that such disclosure is not appropriate. In such cases, the CFAA team prepares the risk assessment as a separate document. 8. The CFAA action plan focuses on key issues and desired outcomes that are tailored to the country’s needs, and considers existing reform programs agreed among the country and development partners. Recommendations are prioritized and their impact clearly linked to an improved PFM. They may also be classified into short, medium, and long term. The action plan estimates any requirements for technical assistance, capacity development, and financial support. In principle, the government is responsible for coordinating action plans and follow-up work, but a development partner may sometimes need to initiate this action. C. Examples of Risks from PFM

9. Table 1 presents illustrative risks to help the reader understand potential risks from PFM systems. These risks, along with the proposed actions, were drawn from completed CFAA reports of the World Bank. The proposed actions were tailored to country-specific conditions.

Table 1: Examples of Risks and Proposed Actions

Risks Proposed Actions Time Frame for Action

Unpredictable budget execution is likely to severely limit financial accountability.

Implement the accountable financial management framework agreed with the International Monetary Fund to meet essential fiscal transparency standards.

Short to medium term

Administrative and financial weaknesses of the Office of the Auditor General are likely to impede effective scrutiny of public funds.

Provide adequate autonomy and resources. Formulate and implement an institutional development plan for strengthening the Office of the Auditor General, including an external audit work program, risk-based audit practices, organizational structure, and human resources strategy.

Short to medium term

Legislative oversight has been fairly effective but long breaks in the accountability cycle could lead to accumulation of backlog of pending audit reports and undermine the accountability chain.

Build awareness, information sharing, and technical capacity of the review committees in the legislature to improve scrutiny. Amend relevant practices to clear backlogs and allow greater access to the findings of the Public Accounts Committee (PAC). Improve PAC oversight by legislative debate and formal government response on its reports.

Short term

2 The CFAAs appear on the country analytic work website hosted by the World Bank as part of the harmonization

agenda development, subject to government permission on access by different users. Available: www.countryanalyticwork.net

For discussion purposes only

16

Weak internal controls could lead to diversion of project funds to unauthorized or unintended uses.

Develop selection criteria and parameters for selection of project managers/coordinators based on technical and managerial competence.

Short term

Enforce a policy about the placement of accounts staff in development projects (e.g., only competent and properly trained staff are placed in development projects; transfers will not be made on an ad hoc basis; and proper hand over and continuity will be assured).

Short term

Harmonize the country’s reporting system to one reporting system that satisfies the requirements of the government and development partners.

Medium term

Source: World Bank. Various years and countries. Country Financial Accountability Assessment. Washington, DC. Available: www.countryanalyticwork.net/ D. Remarks on the CFAA

10. The CFAA is a diagnostic tool for PFM and accountability. It does not provide a pass/fail assessment of a country’s PFM system or define minimum standards for system capabilities and performance. Its main concern is whether or not donor funds are spent on authorized/intended purposes, as expressed in the country’s budget. Moreover, it does not examine developmental risk—the risk that donor funds, as part of the budget flowing through the country’s PFM system, will not be well spent. It does not aim to assess the quality of public spending and the level of financial or sovereign risk (e.g., the risk that donor funds might not be repaid at all or might not be repaid on time). 11. The CFAA typically focuses on national governments. However, it may evaluate the PFM systems of a subnational government that receives direct lending or manages a substantial portion of public expenditures from the national budget. Whether the CFAA can evaluate PFM at the subnational level depends not only on the availability of adequate time and resources but also on the size and capacity of subnational governments. Some subnational governments may have adequate capacity to provide the necessary information on PFM systems and actual revenues and expenditures. Others may lack that capacity. 12. In some countries, nongovernmental organizations (NGOs) may carry out service delivery, and may receive substantial transfers from the national budget. A CFAA is unlikely to be able to analyze the PFM systems of numerous small NGOs. However, where the flow of budget funds to NGOs is significant, the CFAA at a minimum indicates the type and scale of NGO activity. In some cases, it may be possible to obtain some assessment of the quality of NGO financial management through reviews of donor projects involving particular NGOs. 13. In some countries, public enterprises may have a significant impact on the national budget, either through cash subsidies or capital injections received from the budget, or in certain cases, dividends paid to the budget from profitable operations. At a minimum, the CFAA describes the size of the public enterprise sector, its relationship with the national budget, and the general arrangements for government oversight of public enterprise finances. Where public enterprises are significant, the CFAA reviews the extent to which the PFM system provides for performance accountability and transparency. Where guarantees of private enterprise debt may pose a significant fiscal risk, the CFAA discusses them in the risk section.

For discussion purposes only

17

PUBLIC EXPENDITURE AND FINANCIAL ACCOUNTABILITY PERFORMANCE MEASUREMENT

A. Background

1. This diagnostic tool assesses the performance of public financial management (PFM) systems, processes, and institutions over time. It was developed by the public expenditure and financial accountability (PEFA) partners,1 in collaboration with the Organisation for Economic Co-operation and Development/Development Assistance Committee (OECD/DAC) Joint Venture on PFM. The main objective is to provide an objective, internationally comparable framework for assessing a country’s PFM system. Information on the PFM weaknesses, in turn, facilitates identification of risks arising from these weaknesses. 2. The PEFA framework, which became operational in 2005, was a response to a number of problems associated with earlier PFM diagnostic tools. These pertained to (i) transactions costs, where many diagnostic instruments placed considerable burden on country governments; (ii) the need for standardizing the assessment of PFM systems, mainly because earlier tools were developed for different purposes and were being applied in different ways; (iii) increasing the coverage of PFM assessments; and (iv) weak government ownership, particularly when PFM assessments were conducted with limited government involvement.2 B. Scope and Methodology 3. The PEFA performance measurement framework focuses on six core dimensions: (i) budget credibility, (ii) comprehensiveness and transparency, (iii) policy-based budgeting, (iv) predictability and control in budget execution, (v) accounting, recording, and reporting, and (vi) external scrutiny and audit (see subsequent Figure). 4. Measuring the performance of these core dimensions involves 31 high-level PFM indicators that focus on the central government, including the related oversight institutions (see Table 1). Operations of other levels of general government and of public enterprises are considered in the performance indicator (PI) set only to the extent they impact the performance of the national PFM system and its linkages to national fiscal policy (refer to PI-8, PI-9, and PI-23). The PIs fall under four categories: (i) PFM system out-turns, which capture the immediate results of the PFM system in terms of actual expenditures and revenues by comparing them to the original approved budget, as well as level of and changes in expenditure arrears; (ii) crosscutting features, which highlight the comprehensiveness and transparency of the PFM system across the entire budget cycle; (iii) budget cycle, which focuses on the performance of the key systems, processes, and institutions within the budget cycle of the central government; and (iv) donor practices, which account for elements of donor practices that impact the performance of the country’s PFM system.3 1 The PEFA is a multi-agency partnership program sponsored by the World Bank, the European Commission, the

International Monetary Fund, the United Kingdom’s Department for International Development, the French Ministry of Foreign Affairs, the Royal Norwegian Ministry of Foreign Affairs, the Swiss State Secretariat for Economic Affairs, and the Strategic Partnership with Africa.

2 Allen, Richard, Salvatore Schiavo-Campo, and Thomas Columkill Garrity. 2004. Assessing and Reforming Public Financial Management: A New Approach. Washington, DC: The World Bank. Available: http://go.worldbank.org/T7WH97YN00

3 In March 2008, the PEFA secretariat came out with draft guidelines for application of the PEFA performance measurement framework at subnational government level, mainly to ensure appropriate and consistent application of the indicators and a sound basis for interpreting the findings. This draft is available at www.pefa.org.

For discussion purposes only

18

Source: PEFA. 2005. Public Financial Management Performance Measurement Framework. Washington, DC. Available: www.pefa.org 5. Each indicator seeks to measure performance of a key PFM element against a scale of A to D, where the highest possible score of A implies that the core element meets the relevant objective.4 The indicators focus mainly on the basic qualities of a PFM system, based on existing good international practices. The discussion of each of the indicators distinguishes 4 For details on the scoring system, please refer to PEFA. 2005. Public Financial Management Performance

Measurement Framework. Washington, DC. Available: www.pefa.org

Framework for Public Financial Management Performance Measurement

Extent to which the existing PFM system supports the achievement of aggregate fiscal discipline, strategic resource allocation, and efficient service delivery

Type of Assessment Provided by the Performance Measurement Framework

Analytical Features

Extent to which PFM systems, processes, and institutions meet the core dimensions of PFM performance

Measurement of the operational performance of the key elements of the PFM system

PFM (public financial management) system support for budgetary outcomes • Aggregate fiscal discipline • Strategic resource allocation • Efficient service delivery

Core dimensions of an open and orderly PFM system • Credibility of the budget • Comprehensiveness and transparency

• Policy-based budgeting • Predictability and control in budget execution

• Accounting, recording, and reporting

• External scrutiny and audit

Indicator-led analysis of the core dimensions of PFM performance

For discussion purposes only

19

between the assessment of the present situation (the indicator-led analysis) and a description of the reform measures being introduced to address the identified weaknesses. This is to avoid confusion between what the situation is and what is happening in terms of reforms.

Table 1: Indicator Set for Public Financial Management Performance

Performance Indicator (PI)

Number Indicator Remarks/Description

A. PUBLIC FINANCIAL MANAGEMENT (PFM) OUT-TURNS: Credibility of the Budget

PI-1 Aggregate expenditure out-turn compared to original approved budget

The implementation of the budgeted expenditure is important in supporting the delivery of public services for the year, as expressed in policy statements, output commitments, and work plans.

PI-2 Composition of expenditure out-turn compared to original approved budget

Where the composition of expenditure varies considerably from the original budget, the budget will not be a useful statement of policy intent.

PI-3 Aggregate revenue out-turn compared to original approved budget

A comparison of budgeted and actual revenue provides an overall indication of the quality of revenue forecasting. However, external shocks may occur that could not have been forecast and do not reflect inadequacies in administration. These should be explained in the narrative.

PI-4 Stock and monitoring of expenditure payment arrears

This indicator is concerned with measuring the extent to which there is a stock of arrears, and the extent to which the systemic problem is being brought under control. Also important is the assessment of the existence and completeness of data on arrears, without which no assessment can be made.

B. KEY CROSSCUTTING ISSUES: Comprehensiveness and Transparency

PI-5 Classification of the budget

This indicator assesses the classification system used for formulation, execution, and reporting of the central government’s budget. A robust classification system allows the tracking of spending on the following dimensions: administrative unit, economic, functional, and program.

PI-6 Comprehensiveness of information included in budget documentation

Annual budget documentation, as submitted to the legislature for scrutiny and approval, should allow a complete picture of central government fiscal forecasts, budget proposals, and out-turn of previous years. It should include information on (i) macroeconomic assumptions; (ii) fiscal deficit; (iii) deficit financing; (iv) debt stock; (v) financial assets; (vi) prior year’s budget out-turn; (vii) current year’s budget; (viii) summarized budget data for both revenue and expenditure; and (ix) explanation of the budget implications of new policy initiatives, with estimates of the budgetary impact of all major revenue policy changes and/or some major changes to expenditure programs.

PI-7 Extent of unreported government operations

Annual budget estimates, in-year execution reports, year-end financial statements, and other fiscal reports for the public should cover all budgetary and extra-budgetary activities of central government to allow a complete picture of central government revenue, expenditures across all categories, and financing.

PI-8 Transparency of inter-governmental fiscal relations

Given the increasing tendency for primary service delivery to be managed at subnational government levels, correct interpretation of sectoral resource allocation and actual spending effort require tracking of expenditure information at all levels of government according to sectoral categories. The dimensions to be assessed include (i) transparent and rules-based systems in the horizontal allocation among subnational governments of unconditional and conditional

For discussion purposes only

20

Performance Indicator (PI)

Number Indicator Remarks/Description

transfers from central government; (ii) timeliness of reliable information on subnational governments on their allocations from central government for the coming year; and (iii) extent to which consolidated fiscal data (at least on revenue and expenditure) is collected and reported for general government according to sectoral categories.

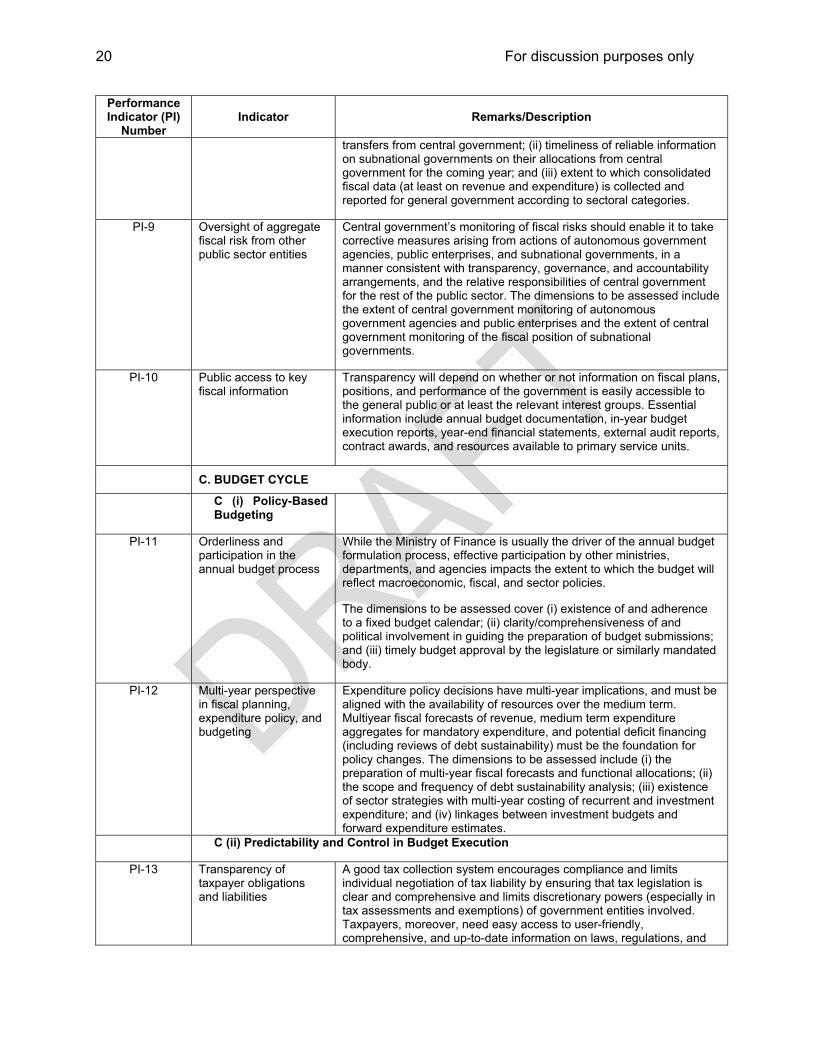

PI-9 Oversight of aggregate fiscal risk from other public sector entities

Central government’s monitoring of fiscal risks should enable it to take corrective measures arising from actions of autonomous government agencies, public enterprises, and subnational governments, in a manner consistent with transparency, governance, and accountability arrangements, and the relative responsibilities of central government for the rest of the public sector. The dimensions to be assessed include the extent of central government monitoring of autonomous government agencies and public enterprises and the extent of central government monitoring of the fiscal position of subnational governments.

PI-10 Public access to key fiscal information

Transparency will depend on whether or not information on fiscal plans, positions, and performance of the government is easily accessible to the general public or at least the relevant interest groups. Essential information include annual budget documentation, in-year budget execution reports, year-end financial statements, external audit reports, contract awards, and resources available to primary service units.

C. BUDGET CYCLE

C (i) Policy-Based Budgeting

PI-11 Orderliness and participation in the annual budget process

While the Ministry of Finance is usually the driver of the annual budget formulation process, effective participation by other ministries, departments, and agencies impacts the extent to which the budget will reflect macroeconomic, fiscal, and sector policies. The dimensions to be assessed cover (i) existence of and adherence to a fixed budget calendar; (ii) clarity/comprehensiveness of and political involvement in guiding the preparation of budget submissions; and (iii) timely budget approval by the legislature or similarly mandated body.

PI-12 Multi-year perspective in fiscal planning, expenditure policy, and budgeting

Expenditure policy decisions have multi-year implications, and must be aligned with the availability of resources over the medium term. Multiyear fiscal forecasts of revenue, medium term expenditure aggregates for mandatory expenditure, and potential deficit financing (including reviews of debt sustainability) must be the foundation for policy changes. The dimensions to be assessed include (i) the preparation of multi-year fiscal forecasts and functional allocations; (ii) the scope and frequency of debt sustainability analysis; (iii) existence of sector strategies with multi-year costing of recurrent and investment expenditure; and (iv) linkages between investment budgets and forward expenditure estimates.

C (ii) Predictability and Control in Budget Execution

PI-13 Transparency of taxpayer obligations and liabilities

A good tax collection system encourages compliance and limits individual negotiation of tax liability by ensuring that tax legislation is clear and comprehensive and limits discretionary powers (especially in tax assessments and exemptions) of government entities involved. Taxpayers, moreover, need easy access to user-friendly, comprehensive, and up-to-date information on laws, regulations, and

For discussion purposes only

21

Performance Indicator (PI)

Number Indicator Remarks/Description

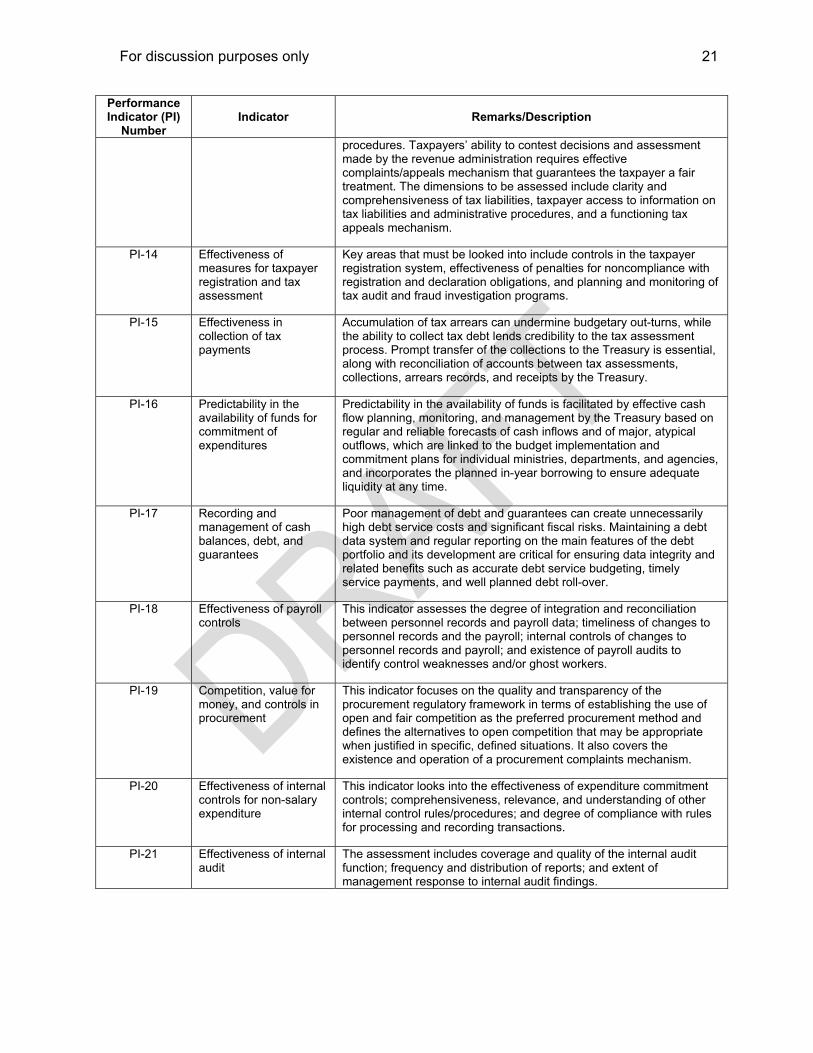

procedures. Taxpayers’ ability to contest decisions and assessment made by the revenue administration requires effective complaints/appeals mechanism that guarantees the taxpayer a fair treatment. The dimensions to be assessed include clarity and comprehensiveness of tax liabilities, taxpayer access to information on tax liabilities and administrative procedures, and a functioning tax appeals mechanism.

PI-14 Effectiveness of measures for taxpayer registration and tax assessment

Key areas that must be looked into include controls in the taxpayer registration system, effectiveness of penalties for noncompliance with registration and declaration obligations, and planning and monitoring of tax audit and fraud investigation programs.

PI-15 Effectiveness in collection of tax payments

Accumulation of tax arrears can undermine budgetary out-turns, while the ability to collect tax debt lends credibility to the tax assessment process. Prompt transfer of the collections to the Treasury is essential, along with reconciliation of accounts between tax assessments, collections, arrears records, and receipts by the Treasury.

PI-16 Predictability in the availability of funds for commitment of expenditures

Predictability in the availability of funds is facilitated by effective cash flow planning, monitoring, and management by the Treasury based on regular and reliable forecasts of cash inflows and of major, atypical outflows, which are linked to the budget implementation and commitment plans for individual ministries, departments, and agencies, and incorporates the planned in-year borrowing to ensure adequate liquidity at any time.

PI-17 Recording and management of cash balances, debt, and guarantees

Poor management of debt and guarantees can create unnecessarily high debt service costs and significant fiscal risks. Maintaining a debt data system and regular reporting on the main features of the debt portfolio and its development are critical for ensuring data integrity and related benefits such as accurate debt service budgeting, timely service payments, and well planned debt roll-over.

PI-18 Effectiveness of payroll controls

This indicator assesses the degree of integration and reconciliation between personnel records and payroll data; timeliness of changes to personnel records and the payroll; internal controls of changes to personnel records and payroll; and existence of payroll audits to identify control weaknesses and/or ghost workers.

PI-19 Competition, value for money, and controls in procurement

This indicator focuses on the quality and transparency of the procurement regulatory framework in terms of establishing the use of open and fair competition as the preferred procurement method and defines the alternatives to open competition that may be appropriate when justified in specific, defined situations. It also covers the existence and operation of a procurement complaints mechanism.

PI-20 Effectiveness of internal controls for non-salary expenditure

This indicator looks into the effectiveness of expenditure commitment controls; comprehensiveness, relevance, and understanding of other internal control rules/procedures; and degree of compliance with rules for processing and recording transactions.

PI-21 Effectiveness of internal audit

The assessment includes coverage and quality of the internal audit function; frequency and distribution of reports; and extent of management response to internal audit findings.

For discussion purposes only

22

C (iii) Accounting, Recording, and Reporting

PI-22 Timeliness and regularity of accounts reconciliation

Reliable reporting of financial information requires constant checking and verification of the recording practices of accountants. Important aspects cover regularity of bank reconciliations and regularity of reconciliation and clearance of suspense accounts and advances.

PI-23 Availability of information on resources received by service delivery units

This indicator assesses the collection and processing of information to demonstrate the resources that were actually received (in cash and kind) by the most common frontline service delivery units in relation to the overall resources made available to the sector, irrespective of which level of government is responsible for the operation and funding of those units.

PI-24 Quality and timeliness of in-year budget reports

This assesses the scope of reports in terms of coverage and compatibility with budget estimates, timeliness of the issuance of reports, and quality of information.

PI-25 Quality and timeliness of annual financial statements

This indicator looks into the completeness of the financial statements, timeliness of submission of the financial statements, and accounting standards used.

C (iv) External Scrutiny and Audit PI-26 Scope, nature, and

follow up of external audit

This indicator centers on the scope/nature of audit performed, timeliness of submission of audit reports to the legislature, and evidence of follow up on audit recommendations.

PI-27 Legislative scrutiny of the annual budget law

This focuses on the scope of the legislature’s scrutiny; extent to which the legislature’s procedures are well established and respected; adequacy of time for the legislature to respond to budget proposals; and rules for in-year amendments to the budget without ex-ante approval by the legislature.

PI-28 Legislative scrutiny of external budget reports

This indicator covers the timeliness of examination of audit reports by the legislature; extent of hearings on key findings undertaken by the legislature; and issuance of recommended actions by the legislature and implementation by the executive.

D. DONOR PRACTICES D-1 Predictability of direct

budget support This indicator centers on the annual deviation of actual budget support from the forecast provided by the donor agencies and in-year timeliness of donor disbursements.

D-2 Financial information provided by donors for budgeting and reporting on project and program aid

This looks into the completeness and timeliness of budget estimates by donors for project support and frequency and coverage of reporting by donors on actual donor flows for project support.

D-3 Proportion of aid that is managed by use of national procedures

This indicator probes into the overall proportion of aid funds to central government that are managed through national procedures. The requirement that national authorities use different (donor-specific) procedures for the management of aid funds diverts capacity away from managing the national systems.

Source: Condensed from PEFA. 2005. Public Financial Management Performance Measurement Framework. Washington, DC. Available: www.pefa.org

6. PFM Performance Report. The PFM performance report is a concise document, not exceeding 35 pages. It aims to provide a comprehensive and integrated assessment of PFM performance of a country based on an indicator-led analysis. Country reports may be downloaded from www.pefa.org.

For discussion purposes only

23

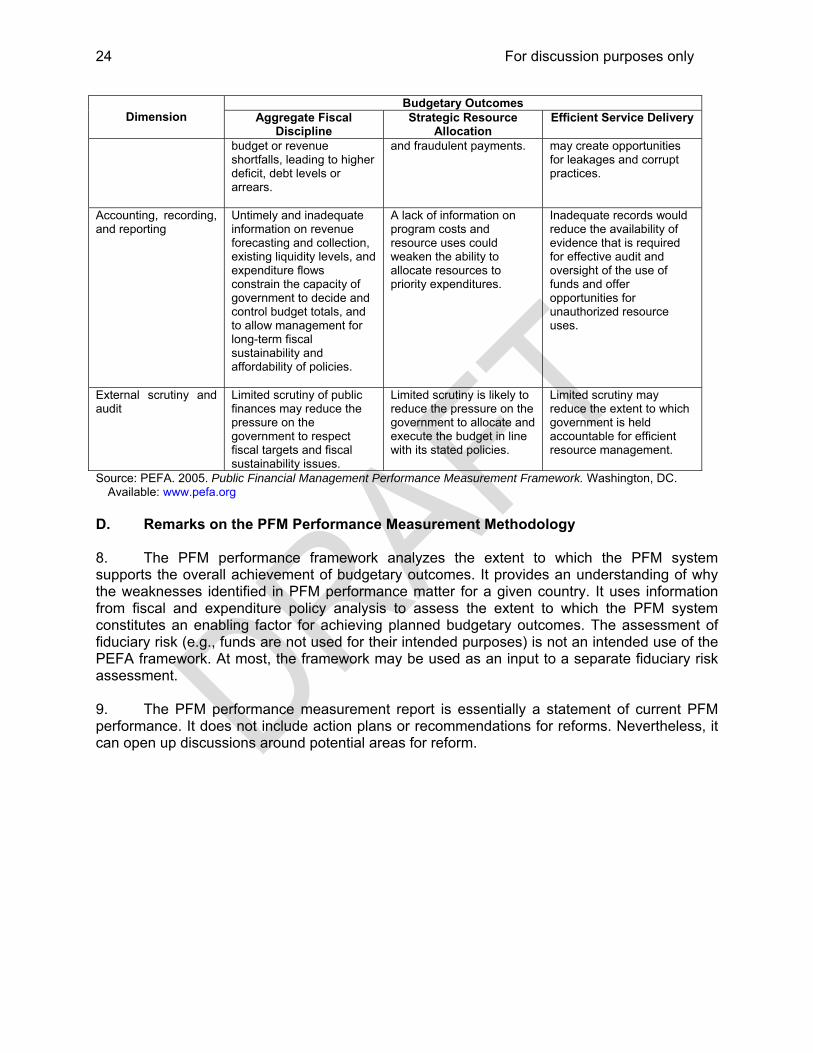

C. Illustrative Links between the PFM System and Budgetary Outcomes 7. Table 2 provides examples of links between the PFM system dimensions and budgetary outcomes. It shows how poor PFM performance affects aggregate fiscal discipline, strategic resource allocation, and service delivery.

Table 2: Links between the PFM System Dimensions and Budgetary Outcomes

Budgetary Outcomes Dimension Aggregate Fiscal

Discipline Strategic Resource

Allocation Efficient Service Delivery

Budget credibility An unrealistic budget is likely to overshoot the deficit target or increase the level of arrears. This can arise from over optimistic revenue forecasts, under budgeting of non-discretionary expenditures, and revenue leakages.

A non-credible budget may lead to shortfalls in funding priority expenditures.

Noncompliance with the budget may lead to shifts across expenditure categories, reflecting personal preferences rather than efficiency of service delivery.

Comprehensiveness and transparency

Activities that take place without reference to the fiscal targets are likely to increase the risk of unsustainable liabilities for the government.

Extra-budgetary funds could undermine the efficiency of strategic planning against government priorities. Lack of transparency limits the capacity of the legislature, media, and civil society to assess the extent to which the government is implementing policy priorities.

Lack of comprehensiveness is likely to increase waste of resources and decrease the provision of services. It may also facilitate patronage and corrupt practices by limiting the scrutiny of operations, expenditures, and procurement processes not integrated in budget management and reporting.

Policy-based budgeting

Limited integration of medium-term implications of fiscal decisions (spending and revenue decisions, approval of guarantees and entitlement programs, etc.) in the budget process can lead to unsustainable policies.

The lack of a medium-term perspective could undermine allocation decisions. The costs of a new policy initiative may be systematically underestimated.

The lack of multi-year perspective may contribute to inadequate planning of the recurrent costs of investment decisions and of the funding for multi-year procurement.

Predictability and control in budget execution

Poor synchronization of cash inflows, liquidity, and outflows may weaken fiscal management. Weak control arrangements may allow expenditures in excess of

Disorderly budget execution could lead to unplanned reallocations and reduce resource availability for priorities. Weak control arrangements may allow unauthorized expenditures

Lack of predictability in resource flows undermines the ability of front-line service delivery units to plan and use those resources in a timely and efficient manner. Inadequate controls of payrolls, procurement, and expenditure processes

For discussion purposes only

24

Budgetary Outcomes Dimension Aggregate Fiscal

Discipline Strategic Resource

Allocation Efficient Service Delivery

budget or revenue shortfalls, leading to higher deficit, debt levels or arrears.

and fraudulent payments. may create opportunities for leakages and corrupt practices.

Accounting, recording, and reporting

Untimely and inadequate information on revenue forecasting and collection, existing liquidity levels, and expenditure flows constrain the capacity of government to decide and control budget totals, and to allow management for long-term fiscal sustainability and affordability of policies.

A lack of information on program costs and resource uses could weaken the ability to allocate resources to priority expenditures.

Inadequate records would reduce the availability of evidence that is required for effective audit and oversight of the use of funds and offer opportunities for unauthorized resource uses.

External scrutiny and audit

Limited scrutiny of public finances may reduce the pressure on the government to respect fiscal targets and fiscal sustainability issues.

Limited scrutiny is likely to reduce the pressure on the government to allocate and execute the budget in line with its stated policies.

Limited scrutiny may reduce the extent to which government is held accountable for efficient resource management.

Source: PEFA. 2005. Public Financial Management Performance Measurement Framework. Washington, DC. Available: www.pefa.org

D. Remarks on the PFM Performance Measurement Methodology 8. The PFM performance framework analyzes the extent to which the PFM system supports the overall achievement of budgetary outcomes. It provides an understanding of why the weaknesses identified in PFM performance matter for a given country. It uses information from fiscal and expenditure policy analysis to assess the extent to which the PFM system constitutes an enabling factor for achieving planned budgetary outcomes. The assessment of fiduciary risk (e.g., funds are not used for their intended purposes) is not an intended use of the PEFA framework. At most, the framework may be used as an input to a separate fiduciary risk assessment. 9. The PFM performance measurement report is essentially a statement of current PFM performance. It does not include action plans or recommendations for reforms. Nevertheless, it can open up discussions around potential areas for reform.

For discussion purposes only

25

FRAMEWORK FOR ASSESSING AND TRACKING CORRUPTION VULNERABILITIES IN PUBLIC FINANCIAL MANAGEMENT

A. Background 1. This summary provides a framework for understanding corruption in relation to public financial management (PFM), for assessing vulnerabilities to corruption, and for designing options to mitigate corruption risks. Systemic factors that increase the risk of corruption generally include (i) weak capacity, (ii) inadequate internal controls, (iii) limited transparency, (iv) poor management control and oversight, and (v) weak external accountability in public spending. Corruption in PFM diverts scarce resources away from public purposes, undermines the ability of governments to achieve their development agenda, directly affects spending on priority sectors, and can have an adverse impact on growth. B. Scope and Methodology 2. The value chain methodology is a means of assessing and tracking corruption vulnerabilities at various stages along the process of translating inputs to outputs. In PFM, the four generic stages are (i) budget formulation, (ii) budget execution, (iii) accounting and reporting, and (iv) external audit and oversight. The prevailing balance of interest, incentives, and institutional norms affects all stages of the PFM process. 3. Budget formulation takes place in a political, policy, regulatory, and institutional context. The executive has a major role in drafting the budget and presenting the budget proposal to the legislature. The extent of legislative involvement depends on the constitutional nature of the state itself. The constitutional form of government defines the legislative power to amend the budget, the veto power of the president, and the power of the legislature to override the budget. Legislatures in presidential systems are designed to perform a more significant role in budget formulation than those in parliamentary systems, where the executive by definition commands the majority in the parliament. Legislative influence over the budget is affected by the electoral system and the number and nature of political parties (strong parties, coalition governments). Corruption during budget formulation is primarily grand or political corruption and is influenced by the distribution of budgetary powers between the executive and the legislature. 4. The budget execution process varies across countries but it generally covers cash management, procurement, and revenue management. Cash management includes (i) the commitment stage, when purchase orders are placed or contracts signed; (ii) the verification stage, when the spending agencies confirm the delivery of the goods and check the bill; (iii) payment authorization, in which a public accountant allows the payment; and (iv) the payment stage, when the bill is paid by cash, check, or electronic transfers. Budget execution is the most fertile ground for corrupt activities because resources actually flow and assets change hands during this stage. 5. Accurate, timely, and transparent record keeping, accounting, and reporting of revenue and expenditure information is essential for enforcing accountability in the budget process. Although budget accounting and reporting do not generally offer direct opportunities for corruption, corruption during the budget execution stage is often detected through strong accounting and reporting systems. Intentional disregard for accuracy and comprehensiveness can obscure fraudulent activity, impede auditing, and restrict management control and oversight.

For discussion purposes only

26

6. External audit and oversight are important in promoting fiscal responsibility. Corruption is possible in the face of undue political influence over external accountability institutions that leads to underreporting of fraudulent practices and inadequate investigation into corruption allegations. Civil society, including the media, can help uphold accountability in the PFM process. 7. The subsequent figure illustrates a generic application of the value chain methodology by summarizing the PFM stages, the decision points along the process flow that are vulnerable to corruption, the early warning signals, and potential anticorruption strategies. The examples given in this Figure are not exhaustive. They must be tailored subsequently to the country-specific PFM context. Essentially, three basic steps are involved in the value chain methodology: (i) identify vulnerable points along the PFM process flow; (ii) diagnose the situation and probe into the underlying causes; and (iii) design and implement anticorruption options.1 8. Step 1: Identify vulnerable points along the PFM process. Functioning PFM systems are part of good governance. In this regard, the public expenditure and financial accountability (PEFA) assessment tool is a possible take-off point for identifying weaknesses in management control and oversight, internal transparency, and internal control. PEFA indicators do not directly measure corruption in PFM but they pinpoint flaws in public resource management. Some examples of decision points that are susceptible to corruption include (i) misuse of discretionary power by the executive, (ii) unrestrained legislative involvement in the budget process, (iii) discretion in off-budget accounts that circumvents disciplinary controls, (iv) manipulation of cash allocations to favor specific groups, (v) manipulation of budget reports, (vi) noncompliance with accounting procedures, (vii) political influence over external accountability institutions; and (viii) external interference in investigations of fraudulent practices. 9. Step 2: Diagnose the situation and probe into the underlying causes. When using the value chain methodology, it is important to distinguish between corruption, and a range of institutional weaknesses that foster inefficiency. For example, weak capacity could be responsible for poor budget formulation and external audit, rather than corruption. Early warning signals at various stages of the PFM process, as enumerated in the subsequent Figure, need to be probed further. A review of the decision making process, case analysis of incident cases, and triangulated diagnostics are necessary before drawing any conclusion. The response to the situation will differ depending on the underlying cause. 10. Step 3: Design and implement anticorruption options. Reducing the risk of corruption in PFM calls for the creation of robust public finance systems, which are open to internal and external scrutiny and which minimize opportunities for corruption and maximize detection and remediation. A two-pronged strategy may consist of: (i) strengthening public resource management, and (ii) strengthening external checks and balances. The Table below provides details. A useful guide to sequencing PFM reforms in low-capacity settings is the

1 Details were drawn from Dorotinsky, William and Shilpa Pradhan. 2007. Exploring Corruption in Public Financial

Management. In The Many Faces of Corruption: Tracking Vulnerabilities at the Sector Level, edited by J. Edgardo Campos and Sanjay Pradhan. Washington, DC: The World Bank.

For discussion purposes only

27

Budget Formulation • Review of prior year spending • Policy/ objective setting • Planning future spending • Drafting budget document

Decision Points Vulnerable to

Corruption

A Framework for Assessing and Tracking Corruption Vulnerabilities in Public Financial Management (PFM)

• Weak controls on revenue and expenditure management

• Poor cash planning • Collusive administrative reductions

in tax liability • Selective enforcement of tax

obligations or unjustified writing off of tax arrears

• Weak reward and penalty structures

• Weak procurement system • Absence of management oversight

and review of payment and procurement practices

Strengthen public resource management • Capacity development

(record keeping, reporting, and accounting systems; expenditure tracking)

• Internal transparency • Internal control • Management control

• Nontransparent systems of decision making

• Lack of transparency in revenue estimation and collection

• Lack of comprehensiveness of resources and expenditures; underspecified plans for using the funds

• Systemic overestimation of revenues during budget formulation

• Unilateral executive decision to approve spending through in-year adjustments without reporting

Budget Accounting and Reporting • In-year reporting • Year-end reporting • Accounting and recording

External Audit and Oversight • External audit • Legislative review • Civil society involvement

Examples of EarlyWarning Signals

PotentialAnticorruption Strategy

• Misuse of discretionary power by the executive • Unrestrained legislative involvement in the budget process • Budget allocation based on political affiliations • Discretion in off-budget accounts that circumvents disciplinary controls

PFM Process

• Underreporting of fraudulent practices

• Poor investigation into corruption allegations

• Non-enforcement of penalties for fraudulent practices

Budget Execution • Budget implementation • Managing resources • Modifying the budget • Collecting revenues, paying • Procuring goods and services

• Weak accounting systems and record keeping practices

• Intentional disregard for accuracy • Lack of comprehensiveness of in-

year and year-end fiscal reports • Irregularities in reconciliation

processes between public bank account data held by commercial and central banks and accounting records

Strengthen external checks and balances • Public access to regular, accurate, and timely fiscal information

• Strengthening of legislative committees, legislative audit, and research organizations

• Allowing civil society and media to participate in the budget process

• Deployment of independent external audit institutions as watchdogs

• Independent judiciaries • Independent anticorruption commission

Adapted from William Dorotinsky and Shilpa Pradhan. 2007. Exploring Corruption in Public Financial Management. In The Many Faces of Corruption, edited by J. Edgardo Campos and Sanjay Pradhan. Washington, DC: The World Bank.

• Discretion by officials in budget spending • Manipulation by officials of the information to be disseminated • Manipulation of cash allocations to favor specific line ministries/agencies from which kickbacks may be arranged

• Manipulation of budget reports • Noncompliance with accounting procedures

• Undue political influence over external accountability institutions • Interference in investigations

For discussion purposes only

28

platform approach, wherein each platform focuses on an improved outcome. The entry point should focus on the weakest link and build on the improved outcome to strengthen other PFM dimensions. For example, in developing countries with overall PFM weaknesses, strengthening capacity and internal controls could come before increasing transparency and accountability.

Potential Corruption Risk Mitigation Measures in Public Finance Management

Type of Intervention

Potential Measure Remarks

(i) Strengthening

public resource management

Capacity development Activities that strengthen the capacity of PFM systems include hiring qualified staff; implementing competitive wage levels; training existing and new staff on budget issues and ethical conduct; implementing a robust classification system that allows tracking of expenditures; improving budget and process comprehensiveness; and progressively implementing a more purpose-oriented budget.

Internal transparency Improving internal transparency should aim to increase frequency of in-year fiscal reports, accuracy of fiscal reports, timeliness and accuracy of year-end fiscal reports, comprehensiveness of accounting and reporting, user-friendliness of report formats, and timely report dissemination.

Internal control Internal control refers to procedures to streamline processes and prevent or detect improper use of funds. Typical activities include formally recorded transaction approvals, authorizations, verifications, reconciliations, reviews of performance, security of assets, segregation of duties, and information control systems. Others cover measures for taxpayer registration and tax assessment, payroll controls, internal controls for non-salary expenditure, procedures for timely and regular accounts reconciliation, clearly defined and simple audit standards, increased authority for internal audit bodies, strengthened payroll audits, and automated payment systems.

Management control and oversight

An initial step in reducing potential corruption is management oversight of budgeted expenditure, deviations from the approved budget for expenditures and revenues, expenditure payment arrears, or aggregate fiscal risk from public sector entities. Possible activities include (i) detection of fraudulent practices and responding to fraud; (ii) instituting procedures to follow up on audit findings and recommendations; (iii) strengthening planning and monitoring of tax, expenditure and payroll audit, and fraud investigation programs; and (iv) implementing procedures to hold fraudulent behavior to account.

(ii) Strengthening checks and

Increasing external transparency and

Transparency of budget information includes access to budgetary documents, in-year financial reports, and year-

For discussion purposes only

29

Type of Intervention

Potential Measure Remarks

balances capacity of external stakeholders