Embed Size (px)

Citation preview

DPA SECRETS

REVEALED

THE NEWEST AND HOTTEST

LOAN PROGRAM AVAILABLE

USING THE DPA STRATEGY

1

WHAT IS DPA?

Stands for “Down Payment Assistance”

Is an UNOFFICIAL TERM that is NO LONGER USED in Real

Estate

Used to Be a “One-Stop” Shop for Getting Both POF

(Proof of Funds) and Partial Transactional Funds for Your

Property Down Payment

Government Regulators Began Cracking Down on These

Organizations

Now the SMART Investor Has to Use 2 Different Places to

Pull Off This Process

Company for Proof of Funds or Letter of Credit

Company for Partial Transactional or “Wet” Funds

2

A LITTLE BIT ABOUT DPA…

Financial Structure

80% ConventionalLoan

20% Seller Carry

3

IN ORDER FOR THIS TO WORK…

20%+

EQUITY

Mortgage

Lien(s) Less Than 80%

4

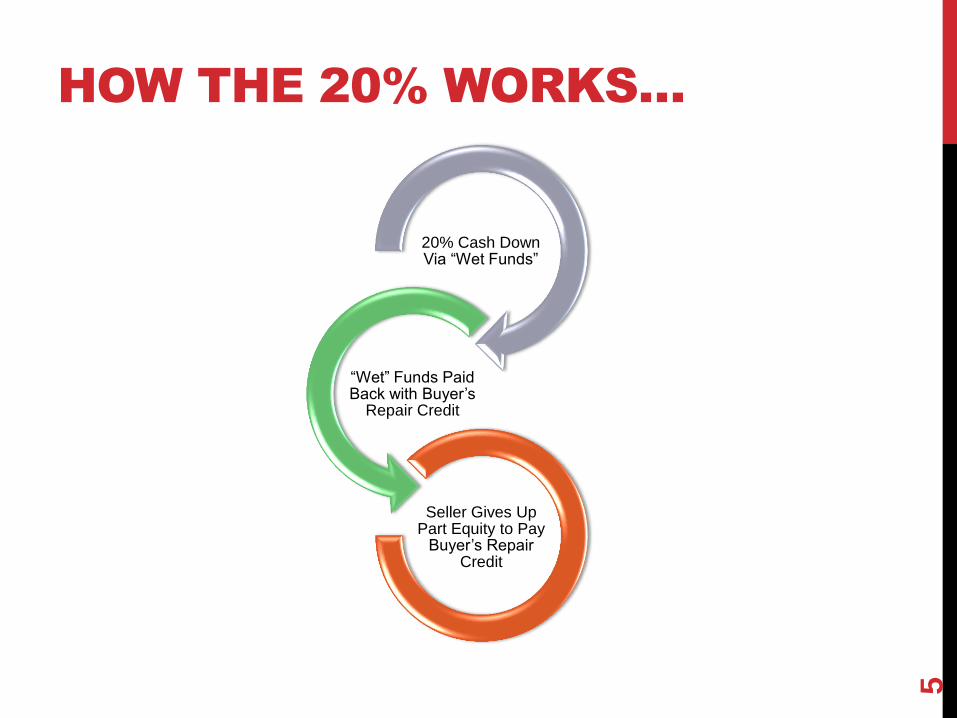

HOW THE 20% WORKS…

20% Cash Down Via “Wet Funds”

“Wet” Funds Paid Back with Buyer’s

Repair Credit

Seller Gives Up Part Equity to Pay

Buyer’s Repair Credit

5

RULES…

Seller MUST Have At Least the 20% in Equity

Lender CANNOT Know That You Are Using Partial Seller

Carry Back or Doing a Private Mortgage Contract on the

Back End

Transactional or “Wet” Funds are NOT a Loan; Funds GO

IN and Are PAID BACK in the SAME ESCROW CLOSING

DAY

Buyer’s Repair Credit Pays Back the “Wet” Funds

Through Escrow Instructions; This Comes OUT of the

Proceeds of Equity that the Seller Would NORMALLY Be

Getting in the Form of a Check After Closing

6

SELLER CARRY RULES…

Terms Can Be ANYTHING As Long As You BOTH Agree to

the Terms

Private Mortgage Contract Goes Into Place BEFORE You

Close Escrow

Seller Takes a 2nd Position and MAY Place a Lien on the

Property AFTER Escrow Close; This DOES NOT Hinder the

1st Position Loan in ANY WAY Nor Can the 1st Position

Lienholder Do Anything About Terminating Your Mortgage

If They Find Out

If You Stop Making Payments on the Seller-Carry 2nd

Position, the Property DOES NOT Go Into Foreclosure!

7

8

LOANS UNDER $1 MILLION

Loan SIZE is Under $1 Million

LTV is 60%

This Means Purchase Price is BELOW $1.67 Million

No Occupancy Requirements

Seller Can Hold 30% on a Privately Held 2nd

12% - 14% Interest Only Loan

1-3 Year Term

1 – 6 Points to the Lender; 2 Points to the Money broker

No Prepayment Penalty

Will Offer Rehab Money

LOANS OVER $1 MILLION

Loan SIZE is Over $1 Million

LTV is 60%

This Means Purchase Price is At or Above $1.67 Million

No Occupancy Requirements

Seller Can Hold 30% on a Privately Held 2nd

12% Interest Only

3 Year Term

2 Points to the Lender; 2 Points to the Money Broker

No Prepayment Penalty

Will Offer Rehab Money

THE 60/30/10

10

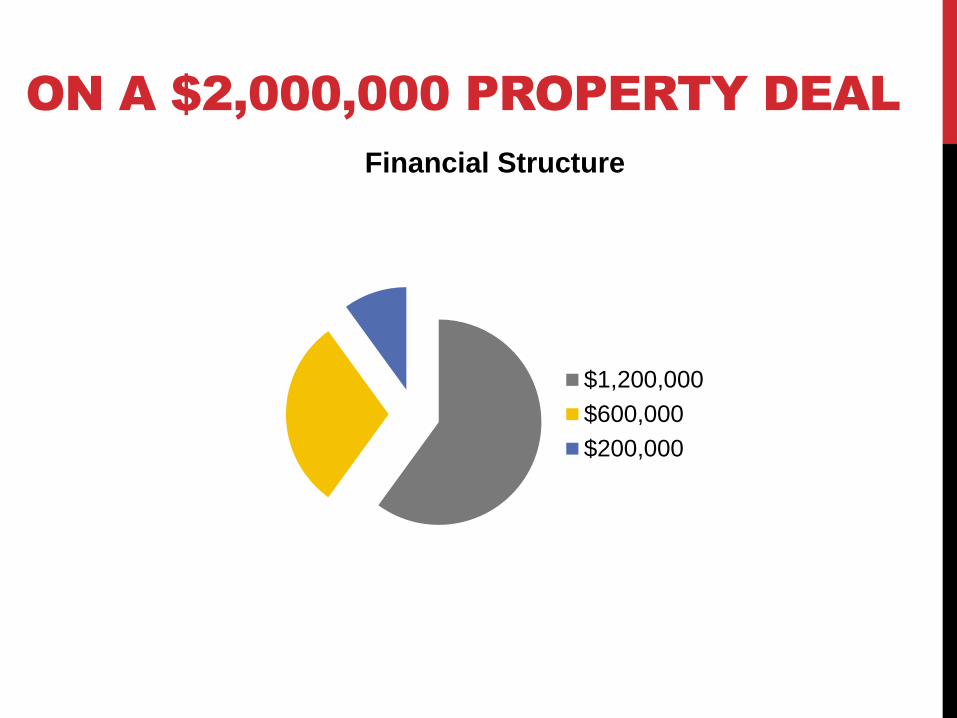

ON A $2,000,000 PROPERTY DEAL

Financial Structure

1stPosition

SellerCarry

WetFunds

Seller MUST Have 40%

in Equity to Make This

Deal Work!

ON A $2,000,000 PROPERTY DEAL

Financial Structure

$1,200,000

$600,000

$200,000

BUYER’S REPAIR CREDIT

$100,000 per $1,000,000 in Asking Price

Add 7% - 10% for Fees Making It About $110,000 per

$1,000,000 in Asking Price

Easier to Get in a Buyer’s Repair Credit than up to 30% of

the Purchase Price

13

STRUCTURE

Lender Will Know ONLY About the 30% Seller 2nd Position

Private Loan

Lender WILL NOT Know About the Additional 10%

Lender Needs to Believe that 10% of the Deal was YOUR

CASH DOWN PAYMENT

Additional 10% Will Be a Private Mortgage 3rd Position

with the Seller

Buyer’s Repair Credit will Cover Partial Transactional

Funding of the 10%

14

VERIFIABLE FUNDS

Make Sure You KNOW Where the “Verifiable” Funds are

Coming From (Which Bank?)

Make Sure This Coincides With Where the Partial

Transactional Funder Will Be Sending the Funds From

Most POF and Wet Funders Use Larger Banks

15

HOW TO DEAL

WITH

FINANCIALS

Real POF

Balance with Other “Non-Verifiable” Assets

Must Add Up to Amount Being Borrowed

Some Lenders Require Amount Being Borrowed

(or “Loan Size”) + 5%

BASIC PREMISE

Total Purchase Price is $2,000,000

Down Payment is 20% or $400,000

Loan Size is $1,600,000

Financials Have to Match the $1,600,000

Some Lenders Require the Additional 5% or

$80,000 Totaling $1,680,000

SCENARIO

Proof of Funds (or POF) to Total HALF or $840,000

“Non-Verifiable” to Total the Other HALF

BREAK DOWN

Cash in Bank Accounts

Stocks

Bonds

Real Estate

Anything with a Paper Trail

“VERIFIABLE”

Stamp Collection

Sports Memorabilia

Antiques

Jewelry

Furniture

Coin Collection

Etc.

“NON-VERIFIABLE”

Stock in a Private Company

• Can Be Verifiable & Non-Verifiable

• Can Be Stock in YOUR Company

• Stock Can Be Designated to Have ANY

“Reasonable” Value

• Intellectual Properties Have Value Including:

• Software

• Copyrighted Materials: Books, Drawings, Pictures

• Trademarks

• Patents

“VERIFIABLE &

NON-VERIFIABLE”

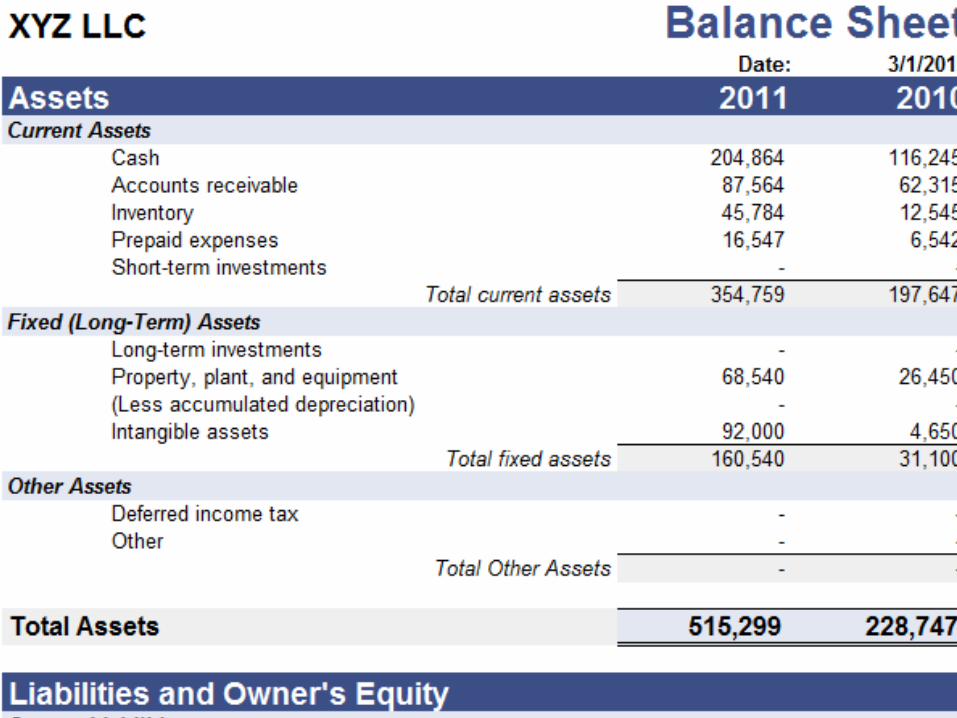

• Balance Sheet

• Business & Personal

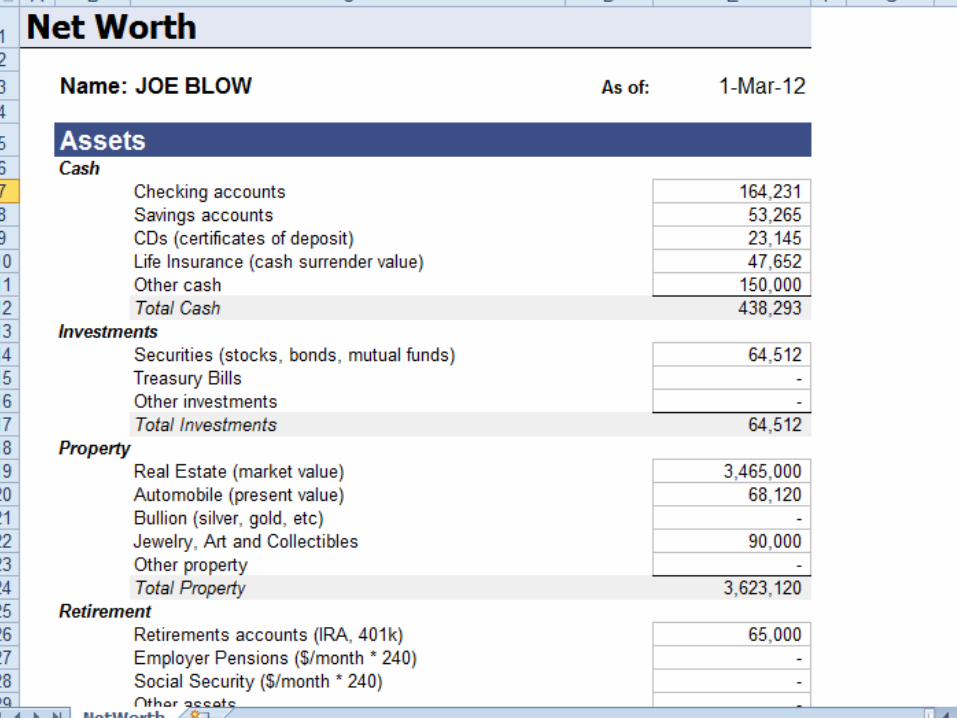

• Net Worth Sheet

• Business & Personal

• Company Sales Projections

• Usually 3 – 5 Years

• Cash Flow Statement

• Currently Functioning Companies

SOME FINANCIAL DOCUMENTS…

24

25

26

27

28

29

30