Embed Size (px)

Citation preview

Don’t be anxious, smile.

What is Taxation?

• It is the inherent power by which the sovereign state imposes financial burden upon persons and property as a means of raising revenues in order to defray the necessary expenses of the government (Tax Digest by Crescencio Co Untian, 2002).

• Taxation is the imposition of financial charges or other levies, upon a taxpayer (an individual or legal entity) by a state such that failure to pay is punishable by law.

It is a mode by which government make exactions for revenue in order to support their existence and carry out their legitimate objectives (Tax Law and Jurisprudence by Justice Vitug, 2000).

It is the most pervasive and the strongest of all the powers of the government. Taxes are the lifeblood of the government, without which, it cannot subsist.

What is Taxation?

History of Taxation

• The first known system of taxation was in Ancient Egypt around 3000 BC - 2800 BC in the first dynasty of the Old Kingdom.

• In Biblical times, tax is already prevalent. According to Genesis 47:24:

•

• "But when the crop comes in, give a fifth of it to Pharaoh. The other four-fifths you may keep as seed

for the fields and as food for yourselves and your households and your children".

• Earliest taxes in Rome are called as portoria were customs duties on imports and exports

• Augustus Caesar introduced the inheritance tax to provide retirement funds for the military. The tax was five percent on all inheritances except gifts to children and spouses .

• In England, taxes were first used as emergency measures.

History of TaxationHistory of Taxation

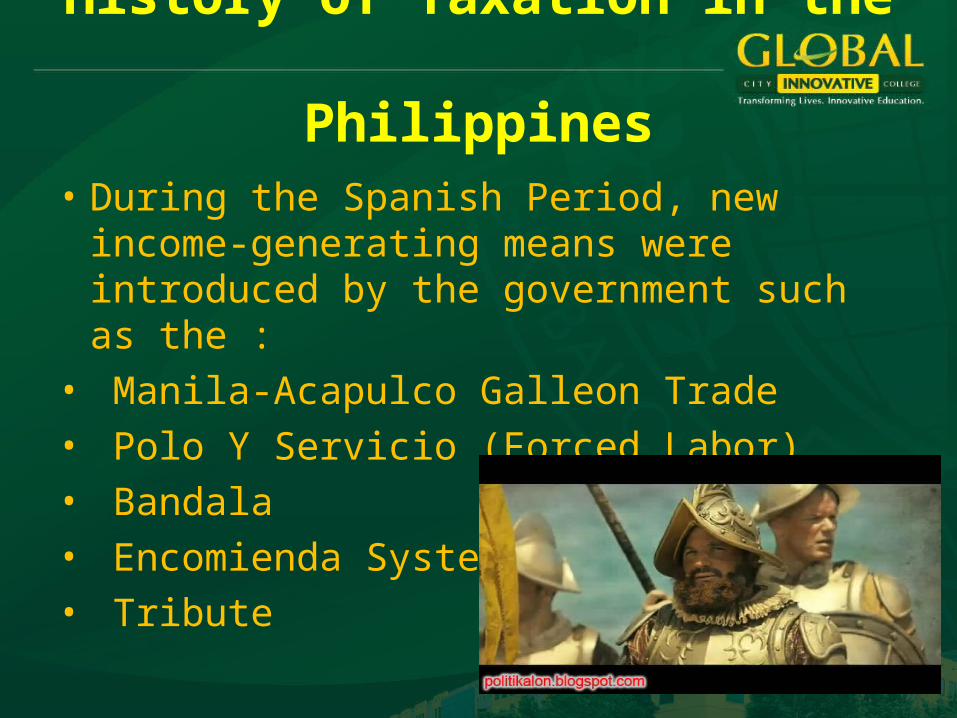

History of Taxation in the Philippines

• The pre-colonial society, being communitarian, did not have taxes.

History of Taxation in the Philippines

• During the Spanish Period, new income-generating means were introduced by the government such as the :

• Manila-Acapulco Galleon Trade• Polo Y Servicio (Forced Labor)• Bandala• Encomienda System• Tribute

Manila-Acapulco Galleon Trade was the main source of income for the colony during its early years.

The Galleon trade brought silver from Nueva Castilla and silk from China by way of Manila.

History of Taxation in the Philippines

Polo Y Servicio is the forced labor for 40 days, of men ranging from 16 to 60 years of age who were obligated to give personal services to community projects. One could be exempted from the polo by paying a fee called falla (which was worth one and a half real).

Bandala is one of the taxes collected from the Filipinos. It comes from the Tagalog word mandala, which is a round stock of rice stalks to be threshed.

History of Taxation in the Philippines

Encomienda are large tracts of land given to a person as reward for a meritorious act. The encomenderos were given full authority to manage the encomienda by collecting tribute from the inhabitants and govern people living on it.

Tribute was the residence tax during the Spanish times. It may be paid in cash or kind, partly, or wholly.

But in 1884, the tribute was replaced by the cedula personal or personal identity paper, equivalent to the present community tax certificate.

History of Taxation in the Philippines

That in the 19th century, the “cedula” served as an identification card that had to be carried at all times. A person who could not present his or her cedula to a guardia civil could then be detained for being “indocumentado”.

Andres Bonifacio and other Katipuneros tore their cedulas in August 1896, signaling the start of the Philippine Revolution.

Did you know?

The Development of the Community Tax• The cédula was imposed by the Americans on

January 1, 1940, when Commonwealth Act No. 465 went into effect, mandating the imposition of a base residence tax of fifty centavos and an additional tax of one peso based on factors such as income and real estate holdings.

• The payment of this tax would merit the issue of a residence certificate. Corporations were also subject to the residence tax.

A sample cedula in the 1920s.

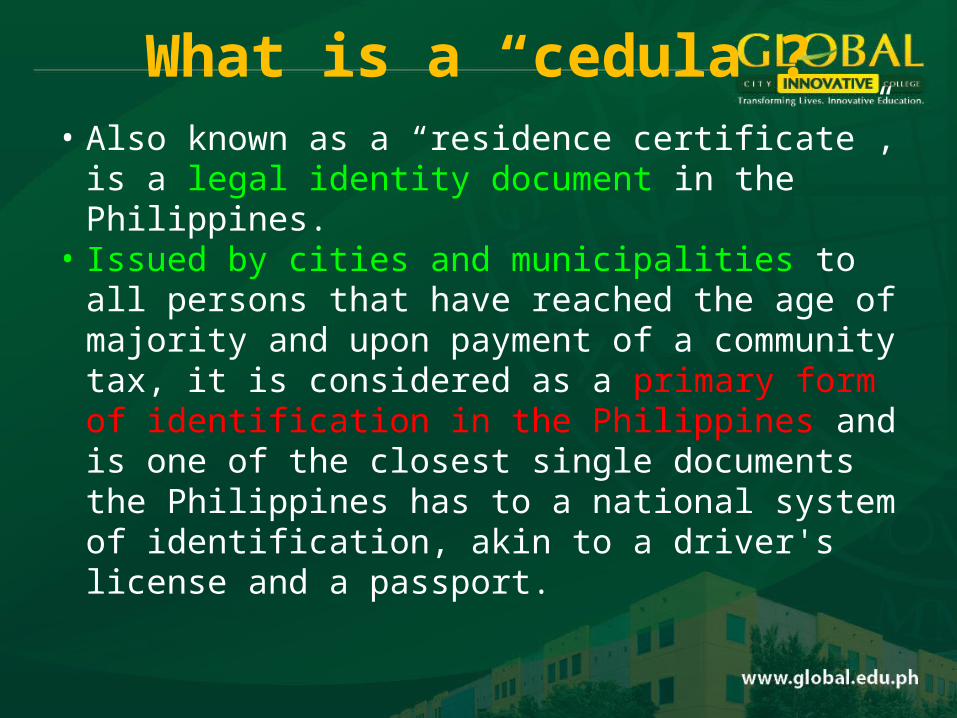

What is a “cedula”?• Also known as a “residence certificate”, is a

legal identity document in the Philippines. • Issued by cities and municipalities to all

persons that have reached the age of majority and upon payment of a community tax, it is considered as a primary form of identification in the Philippines and is one of the closest single documents the Philippines has to a national system of identification, akin to a driver's license and a passport.

A person is required to present a cedula when he or she acknowledges a document before a notary public; takes an oath of office upon election or appointment to a government position; receives a license, certificate or permit from a public authority; pays a tax or fee; receives money from a public fund; transacts official business; or receives salary from a person or corporation.

Why is “cedula” important?

Taxation has four main purposes or effects:

1. Revenue2. Redistribution3. Repricing4. Representation

The Four R’s of Taxation

RevenueThe taxes raise money to spend on armies, roads, schools and hospitals, and on more indirect government functions like market regulation or legal systems.

The Four R’s of Taxation

RedistributionThis refers to the transferring wealth from the richer sections of society to poorer sections.

RepricingTaxes are levied to address externalities; for example, tobacco is taxed to discourage smoking, and a carbon tax discourages use of carbon-based fuels.

The Four R’s of Taxation

RepresentationAs what goes with the slogan "no taxation without representation" , it implies that: rulers tax citizens, and citizens demand accountability from their rulers as the other part of this bargain.

What is a “cedula”?

The main purpose of taxation is to accumulate funds for the functioning of the government machineries. No government in the world can run its administrative office without funds and it has no such system incorporated in itself to generate profit from its functioning.

The government’s ability to serve the people depends upon the taxes that are collected. Taxes are indispensable in the government operation and without it, the government will be paralyzed.

Why Tax?

Tax law in the Philippines covers national and local taxes. National taxes refer to national internal revenue taxes imposed and collected by the national government through the Bureau of Internal Revenue (BIR) and local taxes refer to those imposed and collected by the local government. The 1987 Philippine Constitution sets limitations on the exercise of the power to tax. The rule of taxation shall be uniform and equitable. The Congress shall evolve a progressive system of taxation. (Article VI, Section 28, Paragraph 1).

The Philippine Tax System

Tax evasion happens when there is fraud through pretension and the use of other illegal devices to lessen one’s taxes, there is tax evasion, under-declaration of income, and non-declaration of income and other items subject to tax, Under-appraisal of goods subject to tariff , and over-declaration of deductions

What is Tax Evasion?

The Congress may, by law, authorize the President to fix within specified limits, and subject to such limitations and restrictions as it may impose, tariff rates, import and export quotas, tonnage and wharfage dues, and other duties or imposts within the framework of the national development program of the Government (Article VI, Section 28, Paragraph 2).

The Branches of Government vis-à-vis the Tax Law

The President shall have the power to veto any particular item or items in an appropriation,revenue, or tariff bill, but the veto shall not affect the item or items to which he does not object (Article VI, Section 27, Paragraph 2).

The Supreme Court has the power to: review, revise, reverse, modify, or affirm on appeal or certiorari, as the law or the Rules of Court may provide, final judgments and orders of lower courts in “all cases involving the legality of any tax, impost, assessment, or toll, or any penalty imposed in relation thereto” (Article VIII, Section 5, Paragraph 2b).

The Branches vis-à-vis the Tax Law

A) Personal, capitation or poll taxesThese are taxes of fixed amount

upon residents or persons of a certain class without regard to their property or business

B) Property taxes1. Real Property Tax - an annual tax that may be imposed by a province or city or a municipality on real property such as land, building, machinery and other improvements affixed or attached to real property.

The Forms of Taxes Imposed on Persons and Property

2. Estate Tax (Inheritance Tax) - a tax on the right of transmitting property at the time of death and on the privilege that a person is given in controlling to a certain extent the disposition of his property to take effect upon death.

3. Gift or Donor’s Tax - a tax on the privilege of transmitting one’s property or property rights to another or others without adequate and full valuable consideration.

The Forms of Taxes Imposed on Persons and Property

4. Capital Gains Tax - tax imposed on the sale or exchange of property . Those imposed are presumed to have been realized by the seller for the sale, exchange or other disposition of real property located in the Philippines, classified as capital assets.

C. Income Taxes - Taxes imposed on the income of the taxpayers from whatever sources it is derived. Tax on all yearly profits arising form property, possessions, trades or offices.

The Forms of Taxes Imposed on Persons and Property

D. Excise or License Taxes - Taxes imposed on the privilege, occupation or business not falling within the classification of poll taxes or property taxes. These are imposed on alcohol products; on tobacco products; on petroleum products like lubricating oils, grease, processed gas etc; on mineral products such as coal and coke and quarry resources; on miscellaneous articles such as automobiles.

The Forms of Taxes Imposed on Persons and Property

Under these lies two other taxes:1.Documentary Stamp Tax - a tax imposed upon documents, instruments, loan agreements and papers and upon acceptance of assignments, sales and transfers of obligation and etc.

2. Value added tax- is imposed on any person who, in the course of trade or business sells, barters, exchanges, leases, goods or properties, renders services, or engages in similar transactions.

The Branches of Government vis-à-vis the Tax Law

1. Individualsa. Resident Citizenb. Non-resident Citizenc. Resident Aliensd. Non-resident Aliens

2. Corporationsa. Domestic Corporationsb. Foreign Corporations

3. Estate under judicial settlement

4. Trusts irrevocable both as to the trust property and as to the income.

Who Should Pay Taxes?

The Constitution expressly grants tax exemption on certain entities/institutions such as: 1. Charitable institutions, churches, parsonages or convents appurtenant thereto, mosques, and nonprofit cemeteries and all lands, buildings and improvements actually, directly and exclusively used for religious, charitable or educational purposes (Article VI, Section 28, Paragraph 3).

Who (or What) are those exempted in paying taxes?

Who (or What) are those exempted in paying taxes?2. Non-stock non-profit educational institutions used actually, directly, and exclusively for educational purposes. (Article XVI, Section 4 (3)).

Exempted to tax as stated in the Article 283 of Rules and Regulations Implementing Local Government Code of 1991 (RA 7160):

• Local water districts• Cooperatives duly registered under RA 6938, otherwise known as the Cooperative Code of the Philippines• Non-stock and non-profit hospitals and educational institutions• Printer and/or publisher of books or other reading materials prescribed by DECS (now DepEd) as school texts or references, insofar as receipts from the printing and / or publishing thereof are concerned.

Top Celebrity Taxpayers in 2010

![4000 Essential English Words - Internet Archive · 2016. 11. 17. · anxious [gerj/cjas] adj. When a person is anxious, they worry that something bad will happen.-»She was anxious](https://img.dokumen.tips/doc/110x75/60b31605db2bec2604179ede/4000-essential-english-words-internet-archive-2016-11-17-anxious-gerjcjas.jpg)