Embed Size (px)

Citation preview

Doing business abroad - Legal aspects from

the EU/German perspective

Thomas Hoffmann, Assoc. Prof., Dr. iur., LL.M.,

Tallinn Law School, Rechtsanwalt (DE) bnt attorneys in CEE

Overview

• Contracts with foreign partners

• Applicable law to contracts

• Product liability and Producer’s liability

• Dispute settlement

• Setting up shop abroad/joint ventures

• Taxes

All about Contracts (1)

• Realistic approach to language skills of both parties

(age?)

• Offers, requests: Buyer’s language

• E-mails, calls, negotiations: whatever works – as

long as it works!

• Agreements: both have to understand everything

• A good translation is cheaper than a bad agreement!

All about Contracts (2)

• If something looks to good to be true, it is [usually]

not true.

• „If you need an answer today, the answer is no.“

• The „one million flies“-rule: this may be a good

agreement for others, but not for you.

• Do not wrestle with dinos, but:

• Read the agreement!

• General conditions may in certain cases be void.

All about Contracts (3)

• Contracts as the basis of a successful

business partnership – main purpose is

clarification, not base for future disputes!

• Documentation in writing

• E-mails

• Common understanding

5 / xx

All about Contracts (4)

• „Private autonomy“…

• … and its limits: General Business Terms

• Dispensable law mandatory law

• Consumer law law between enterprises

• „Special“ contracts: service dimension of law

6 / xx

7

All about Contracts (5)

Case study 1

• A British company sends an order for 1500 electronicdevices to an Estonian company. The Estonian companyreceives the order. Before he is able to send anacceptance, the British party revokes its order by fax. Nevertheless, the Estonian company sends a messageaccepting the order, relying on § 18 II VÕS, according towhich an offeror is bound by his offer. The British partner refers to the the “postal rule”, according to which anoffer can be revoked at any time up until the acceptanceis dispatched.

• Is there are binding contract?

All about Contracts (6)

Case study 2

An Estonian enterprise sells wooden furniture

to a German furniture store.

In the store‘s business conditions liability for

intent and gross negligence is excluded.

The store does not control the furniture on

arrival. After a month a defect is detected and

the store demands remedy.

What if the defect was invisible?

What if the seller knows about the defect?

8

Product liability (1)

Claimed compensation:

• Not for the defect of the product itself, but

for damages caused by that product

• In general: Not intermediate seller, but

producer should be held liable

• But: No contract between final user and

producer

9 / xx

Product liability (2)

• Approach therefore: Tortious liability

• What may be the tortious action?

1. Constructional defect

2. Fabrication defect

3. Instruction defect

4. Product supervision defect

10

Product liability (3)

• Differentiate:

– Product liability (ProdHaftG)

– Producer’s liability (Sec. 823 I BGB)

11

Product liability (4)

• Product liability:

Implementation of EU directive 85/374

• Regulated in separate act,

“Produkthaftungsgesetz”

(ProdHaftG, Product liability act)

12

Product liability (5)

• Sec 1 par 1: Liability for all integrity damages

• Sec 1 par 1 cont’d: “ (…) item of property is of a type ordinarily intended for private use or consumption”

• Strict liability (no exculpation clause)

13

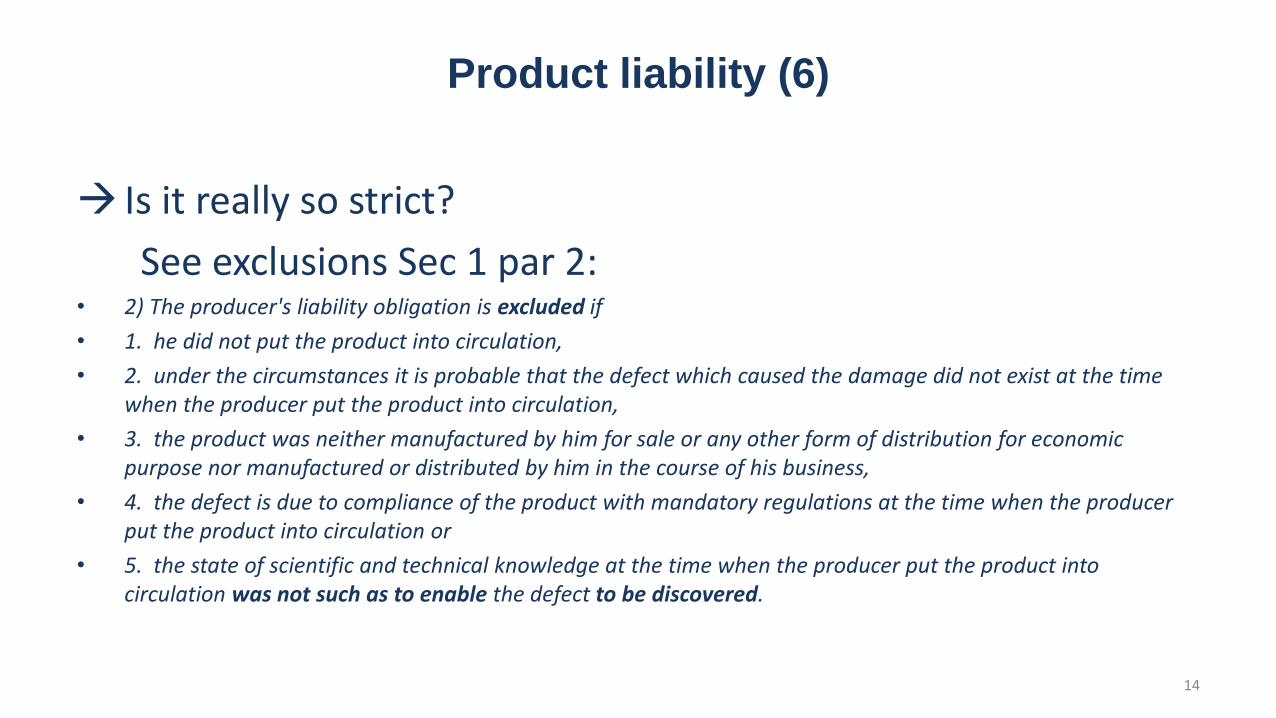

Product liability (6)

Is it really so strict?

See exclusions Sec 1 par 2: • 2) The producer's liability obligation is excluded if

• 1. he did not put the product into circulation,

• 2. under the circumstances it is probable that the defect which caused the damage did not exist at the time when the producer put the product into circulation,

• 3. the product was neither manufactured by him for sale or any other form of distribution for economic purpose nor manufactured or distributed by him in the course of his business,

• 4. the defect is due to compliance of the product with mandatory regulations at the time when the producer put the product into circulation or

• 5. the state of scientific and technical knowledge at the time when the producer put the product into circulation was not such as to enable the defect to be discovered.

14

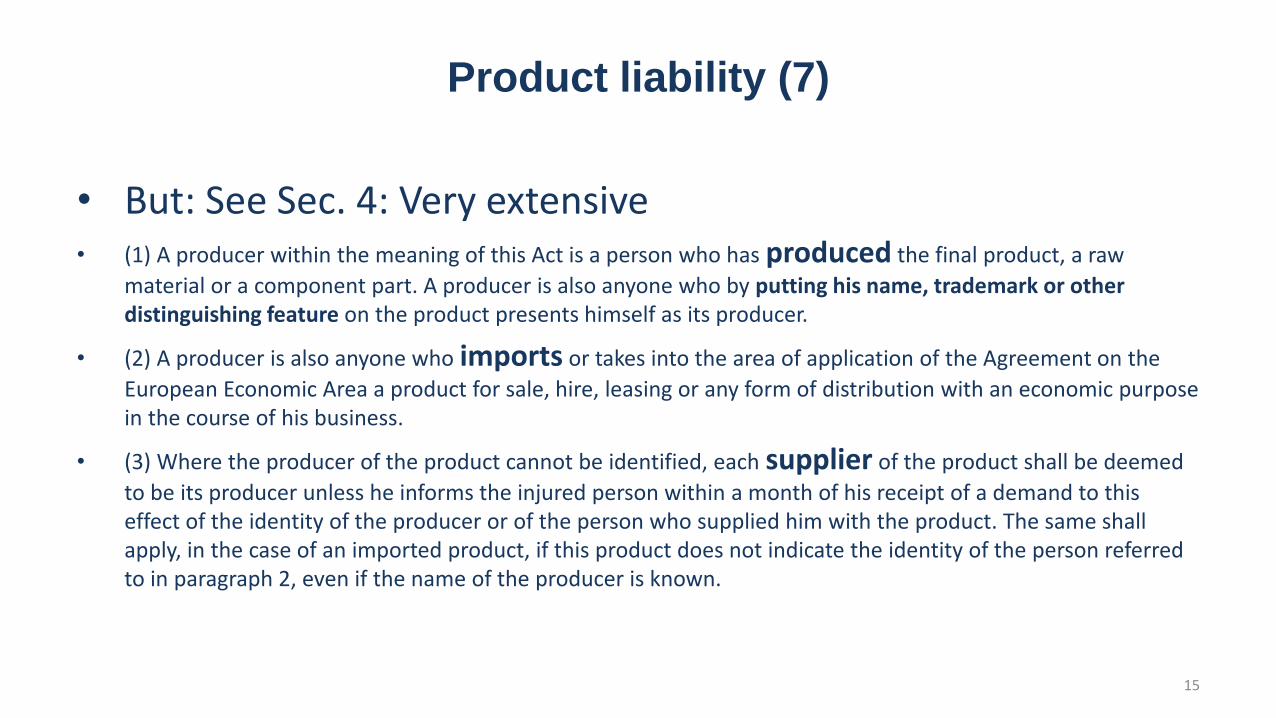

Product liability (7)

• But: See Sec. 4: Very extensive• (1) A producer within the meaning of this Act is a person who has produced the final product, a raw

material or a component part. A producer is also anyone who by putting his name, trademark or other distinguishing feature on the product presents himself as its producer.

• (2) A producer is also anyone who imports or takes into the area of application of the Agreement on the

European Economic Area a product for sale, hire, leasing or any form of distribution with an economic purpose in the course of his business.

• (3) Where the producer of the product cannot be identified, each supplier of the product shall be deemed

to be its producer unless he informs the injured person within a month of his receipt of a demand to this effect of the identity of the producer or of the person who supplied him with the product. The same shall apply, in the case of an imported product, if this product does not indicate the identity of the person referred to in paragraph 2, even if the name of the producer is known.

15

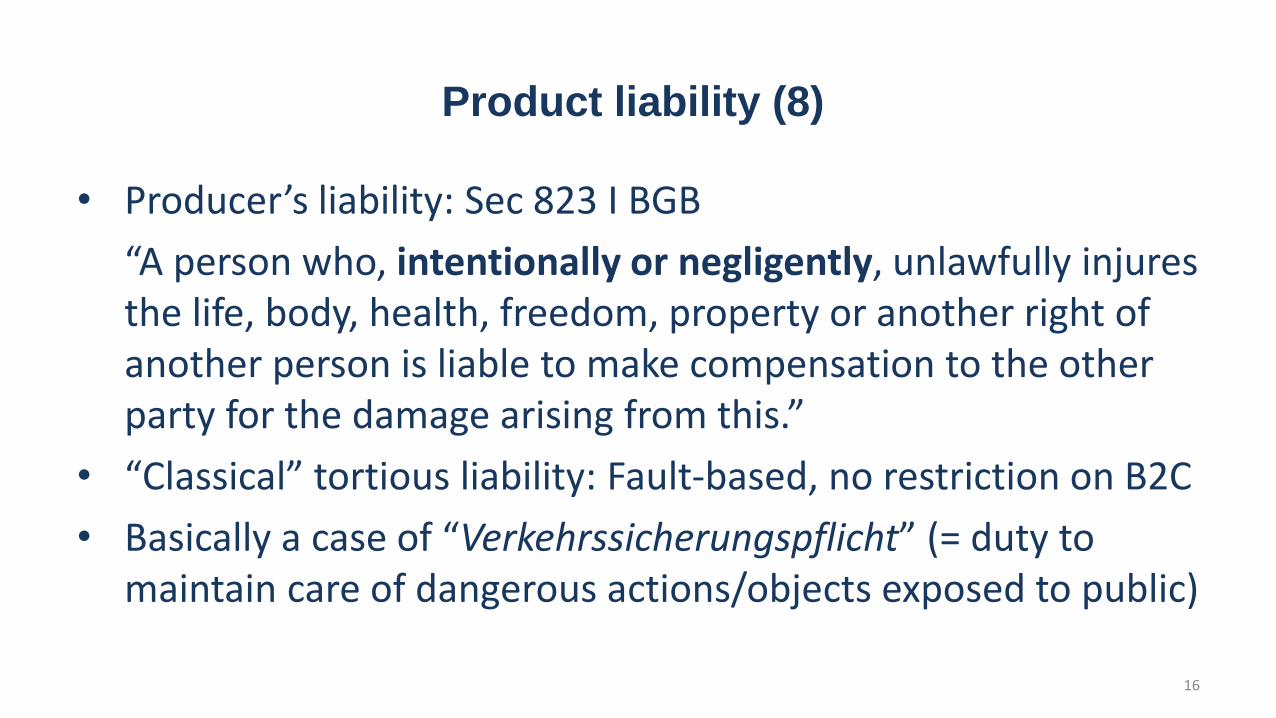

Product liability (8)

• Producer’s liability: Sec 823 I BGB

“A person who, intentionally or negligently, unlawfully injures the life, body, health, freedom, property or another right of another person is liable to make compensation to the other party for the damage arising from this.”

• “Classical” tortious liability: Fault-based, no restriction on B2C

• Basically a case of “Verkehrssicherungspflicht” (= duty to maintain care of dangerous actions/objects exposed to public)

16

Product liability (9)

• Liable: Only producer, not importer/supplier

• Exculpation possible, but fault assumed (reversal of proof in contrast to wording of sec. 823 I BGB!)

17

Product liability (10)

Product Liability:

ProdHaftG

• Prod.+Supplier

• B+C may claim

• Strict Liability(but see exceptions)

• Max/Min. liability

• Limitation: 3 years from awareness 18

Producer’s Liab.:

Sec. 823 I BGB

• Only Producer

• Only consumer(if prop. damage)

• Fault-based Liab.

• unlimited amount

• Limitation: 3 y. from damage

Dispute resolution (1)

What to do in cases of a dispute?

– Reminder

– Order for payment (Maksekäsumenetlus)

• Local court at debtor’s seat, enforceable title

• https://www.just.ee/et/eesmargid-tegevused/maksekasumenetlus-ja-e-toimik

– Legal action

• Below EUR 5.000:

• Costs: to be borne by the defeated party19 / xx

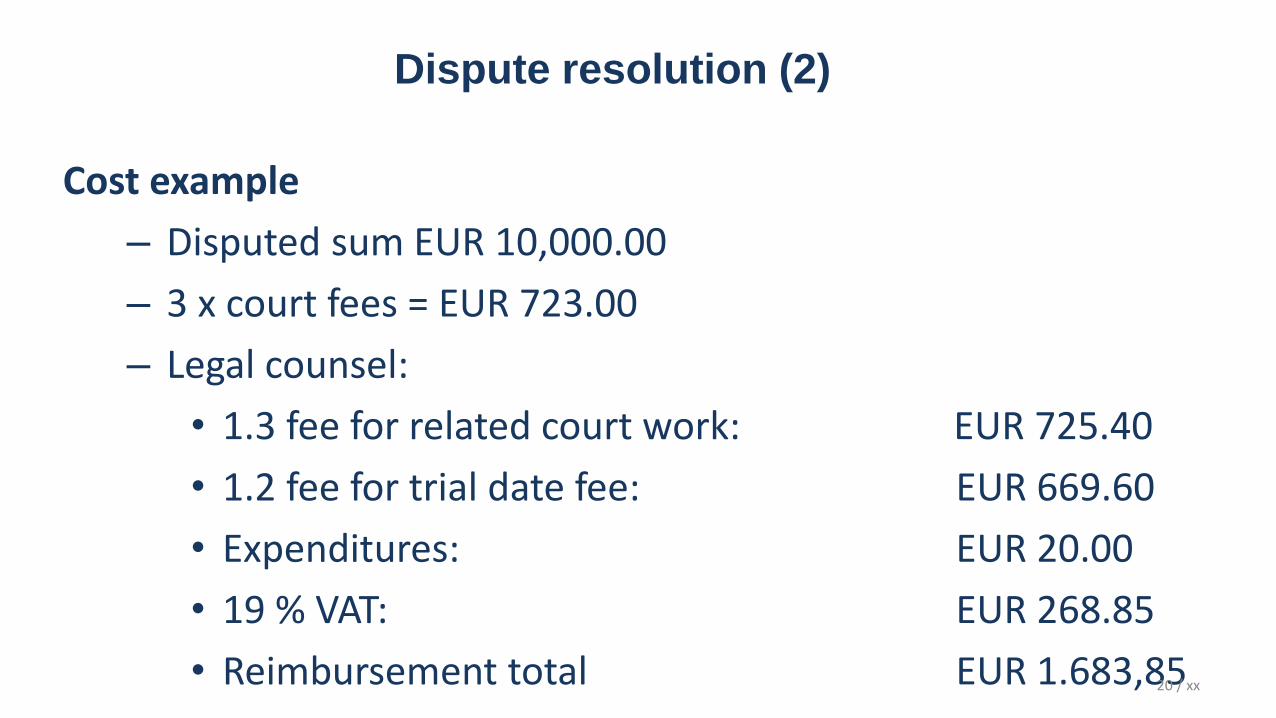

Dispute resolution (2)

Cost example

– Disputed sum EUR 10,000.00

– 3 x court fees = EUR 723.00

– Legal counsel:

• 1.3 fee for related court work: EUR 725.40

• 1.2 fee for trial date fee: EUR 669.60

• Expenditures: EUR 20.00

• 19 % VAT: EUR 268.85

• Reimbursement total EUR 1.683,8520 / xx

Dispute resolution (3)

Alternative Dispute Resolution

• Agreeing on an arbitral tribunal

– Neutrality

– Effectiveness

– Speed of decisions

• Disputes with Consumers

– Coming soon: Online dispute resolution

– Advantage: low costs, matters of publicity

21 / xx

Joint Venture – Contractual Arrangements

Attention when entering into a Company with a

partner/partners!

• The beginning of joint project is the correct time for setting

basic contractual arrangements!

• Avoid 50/50 deadlock-situations!

• Review contracts when new parties are going to enter!

• There is strict mandatory liability of directors and (in some

situations) shareholders under German law – independent

from the individual contribution!

Setting up shop

• No permanent representation necessary

• Different forms of doing business in

Germany:

– (independent sales agent)

– simple (tax) registration (= dependent branch)

– registered („independent“) branch

establishment

– subsidiary company (e.g. GmbH)

23

Branch establishment vs. Subsidiary company

Forms of doing business in Germany

• independent sales agent

• simple (tax) registration (= dependend branch)

• necessary if a taxable „permanent establishment“ is established

on the Territory of Germany (e.g. by way of stock holding, long-

term services)

• Registered („independent“) branch establishment

• registration of OÜ in German commercial register

• tax registration

• in fact not independent but part of the origin legal entity

• set-up by notarial deed and according registration in commercial

reg.

• Subsidiary company (e.g. GmbH)

• legally independent from mother company

Made in Germany

• German Federal Court (1973): „From a ‚German product‘ it must be

expected that it is produced by a German company in Germany. The

essential worth of the product must be based on a German service.

• High Court Stuttgart (1995): „Made in Germany is misleading if most of

the main parts have been bought from abroad. If some parts have been

bought from abroad the product may still labled as „Made in Germany“ if

the services which are relevant for the worth of the product are performed

in Germany.

Relevant Criteria are:

• relevant production in Germany

• signficant added value by assembling in Germany

• significant finishing in Germany

• ECJ (1985): Restrictions only possible in consideration of the free

movement of goods

Claim Management / Securities

Securities

• Preliminary Control of Contract Partners

• GmbH, UG (= Mini GmbH), GbR

• Prepayment

• Retention of title

• simple form (title passes when payment is completed)

• prolonged retention (allows buyer to already sell the goods; instead

the claims of the buyer against its own customers serve as security)

• extended retention (secures not only payment claims for the specific

soled goods but also other claims; e.g. in case of permanent trade)

• „processing clause“ if semi-finished products are sold for the

purpose of finishing (under German law the title of ownership

mandatorily passes by way of processing/finishing).

• Guaranty / Bank Guaranty (attention: guaranty can be „Garantie“ or

„Bürgschaft“)

Seite 27

Labour Law (1)

• Form for employment contract:

- Generally no special form required

- Contract period longer than 1 month: Written

form

• Minimum content in that case: see § 2

NachwG

• Reminder: Standard business terms must

meet legal standards, otherwise ineffective

Seite 28

Kündigungsschutzgesetz

(act on protection against dismissal)

• Applicability:

• Minimum number of employees: 6

• Employee-employer relationship: more than 6 months

• „Kündigungsschutzklage“ has to be raised within three

weeks after receipt of letter of dismissal

• Scope of protection:

Dismissal must be socially justifiable, not justified

meaning of reasons are not based in the „person or

behaviour of the employee or urgent company-related

requirements“ (the latter being „dringende betriebliche

Erfordernisse“ in German) which can not be combined

with the continuation of the employment.

Labour Law (2)

Seite 29

Working hours

The daily hours of work for employees should in generall

not exceed 8 hours, 3 ArbZG

Deviating provisions are possible in the collective

agreement or in an operational and service agreement

based on a collective agreement

Special regulations for:

Night and shift work, § 6 ArbZG

Sundays and holidays, §§ 9 ff. ArbZG

Extraordinary situations, §§ 14 ff. ArbZG

Labour Law (3)

Seite 30

Holidays

Holiday must be granted at least 24 working days p.a.

(calculated on a 6-day week),§ 3 BUrlG

The employee is fully entitled for payed leave as soon as

the employment relationship lasts 6 months, § 4 BUrlG

If an employee falls ill during the holidays, the time of

incapacity for work is not taken off as vacation, § 9 BUrlG

When timing the holiday, the personal preferences of the

employee must be considered, unless they preclude

urgent operational interests of the company or preferences

of other workers who deserve priority from a social point of

view, § 7 BUrlG

Labour Law (4)

Seite 31

Part-time work

Part-time work is regulated in the part-time and temporary

employment act (TzBfG, Teilzeitbefristungsgesetz), which

aims to promote part-time work and to draw up clear rules on

part-time

An employee is part-time employed if his regular workweek

is shorter than that of a comparable full-time employee,§ 2

Basically, a fixed-term contract 1 is only possible if a valid

reason is given for the limitation,§ 14 para. TzBfG

Exceptionally, a limitation is possible also without objective

reason, but in that case only up to a total duration of two

years (i.e. taking into account three extensions),§ 14 Abs. 2

TzBfG

Labour Law (5)

Seite 32

Minor employment („450 €-jobs“)

Minor employment is an employment relationship, in which

the remuneration does not exceed a certain limit or which

lasts only briefly

The income threshold is currently 450 euros per month

Where a person has two or more mini-jobs and the

remuneration thereof is more than the income limit, none of

these is seen as minijob

Advantages: Almost no taxes, possibility to be exempted of

all insureances (netto=almost brutto)

Besides, for part-time employees the same labor law

regulations apply as for 'normal' employees

Labour Law (6)

Seite 33

Minimum salary

Since 1 January 2019 Germany has a minimum wage of

9.19 EUR

After 1 January 2020: 9,35 Euro

Binds all employers – having established their business in

Germany or abroad – as far as they employ employees

performing their work in Germany

There are exceptions for interns, honorary activities etc.

The minimum wage is a gross wage per hour (brutto) and

has to be paid out directly (no set-off etc.)

When calculating the minimum wage special attention has

to be paid to details, e.g. which allowances or fringe

benefits may be included in the calculation

Labour Law (7)

Seite 34

Labour costs

(Lohn- und Lohnnebenkosten)

Primary labor costs (Lohnkosten) are the sum of all wage-

related expenses, which are paid in a given period from the

employer or to the employee

Secondary labour costs (Lohnnebenkosten) are costs that

are added to the actual salary of the employeem but are

also paid for by the employer

Employers' social contributions

Cost of vocational education and training

Other expenses

Labour Law (8)

Seite 35

Compulsory social insurance

The social insurance is a compulsory insurance, imposed

by the Social Security Codes (SGB)

Elements: Health insurance:§ 5 SGB V und§ 2 KVLG 1989

Long-term care insurance (Pflegeversicherung):§§ 20 f. SGB XI

Pension insurance:§§ 1 f. SGB VI und§ 1 ALG

Insurance against unemployment:§ 25 ff.SGB III

Accident insurance:§ 2 SGB VII

Persons which have to be insured: all employees, farmers, craftsmen and publicists and artists,

Handicapped persons,

Recipients of unemployment benefit I or II, the transitional allowance or certain

other Compensation Benefits

Persons who were previously in a statutory health insurance and do not have

private health insurance (eg returners from abroad)

Labour Law (9)

Labour Law (10)

• In principle: legal provisions of the EU

member state in which the worker is

employed apply

• Exception: posting within the EU

• expected stay abroad is not

more than 24 months

• labour contract in the country of

origin

36

Labour Law (11)

Posting of Workers

Notification

• Specific form has to be issued to the customs in

German language

Confirmation

• complying with the minimum conditions of

minimum wages

posting of workers

37

Labour Law (12)

Documentation duties

– beginning

– end

– and aggregate hours of the workers’ daily assignments

– Documentation to be set up not later than seven days

– in German language

Keep following documents present:

– employment contract

– time sheets

– pay slips and

– proof of payment of wages

38

Seite 39

Continued payment in case of illness

In case of illness the employee is entitled to continued

payment of wages for a period of up to 6 weeks (regulated

in Entgeltfortzahlungsgesetz, FZG)

The amount depends on the regular agreed remuneration

of the employee

Conditions:

Inability to work due to illness

Employee falls ill without proper fault

The employment must have existed at least four weeks

After 6 weeks, sick pay is regulated in§ 44 ff. SGB V (health

insurance is covering sick leave)

Labour Law (13)

Seite 40

Maternity protection

The act on the protection of working mothers (MutterschutzG)

provides special protection against dismissal

The dismissal of a woman during pregnancy and until the expiry

of four weeks after giving birth is not permitted,§ 9 MuSchG

The MuSchG also protects expectant mothers by special

employment prohibitions for certain activities which may be

dangerous to them

Note: In a job interview, a potential female employee is not

obliged to disclose details of a possible pregnancy; if explicitly

asked, the applicant is not obliged to tell the truth

Labour Law (14)

Seite 41

Income tax

The income tax is a community tax, which is levied on the

income of individuals (natural persons)

Income tax is due on both on the world income of

individuals resident or ordinarily resident in Germany

(unlimited income tax liability,§ 1 para. 1 sentence 1

EStG), as well as on the domestic income (§ 49 Income

Tax Act) of persons who are neither resident nor ordinarily

resident in Germany (limited income tax liability, § 1,

para. 4 EStG)

The actual income tax to be paid depends on the taxable

income and the individual tax rate

Seite 42

NB: Nothing in these presentations should be interpretedas legal advice and/or the opinion of TalTech, Tallinn Law Schoolor bnt attorneys in CEE. It is intended as presentation of theauthor’s personal general impressions only. The informationpresented may not reflect most current legal developments. Youshould accept legal advice only from alicensed legal professional with whom you have an attorney-client relationship.

TALTECH UNIVERSITYEhitajate tee 5, 19086 Tallinn, Tel + 372 620 2002 (E-R 8.30–17.00)

taltech.ee