Embed Size (px)

Citation preview

DOCUMENT RESUME

ED 364 776 CE 065 426

TITLE Accounting Principles 30G. Interim Guide.INSTITUTION Manitoba Dept. of Education and Training,

Winnipeg.REPORT NO ISBN-0-7711-1135-5PUB DATE 93NOTE 83p.; For a related guide, see CE 065 427.PUB TYPE Guides Classroom Use Teaching Guides (For

Teacher) (052)

EDRS PRICE MF01/PC04 Plus Postage.DESCRIPTORS *Accounting; Bookkeeping; *Business Education;

Classroom Techniques; Course Content; EducationalResources; Employment Potential; Foreign Countries;High Schools; Job Skills; Learning Activities; LessonPlans; Student Evaluation; Teaching Methods; Units ofStudy

IDENTIFIERS Manitoba

ABSTRACTThis curriculum guide was developed for a

senior-level introductory accounting course for students in highschools in Manitoba. The course introduces Canadian accountingprinciples and practices; it applies Generally Accepted AccountingPrinciples (GAAP) to introductory financial accounting. The guideincludes the following components: (1) an employability skillsprofile; (2) recommended program patterns for business educationcourses; (3) rationale for the program; (4) evaluation methods; (5)

time allotments; (6) goals and objectives; and (7) five units ofstudy. The units cover these topics: basic concepts, the cycle,controlling cash, merchandise accounting, and payroll. Units consistof a goal, objectives, and teaching methods keyed to the objectives.Two appendixes list Generally Accepted Accounting Principles andexplain the Goods and Services Tax. A bibliography listing 18 textsand a source for materials completes the guide. (KC)

***********************************************************************

Reproductions supplied by EDRS are the best that can be madefrom the orienal document.

***********************************************************************

1993AuAccounting Principles 30G

U.S DEPARTMENT OF EDUCATIONOnco ol Educahonat Research and Improvement

EDUCATIONAL RESOURCES INFORMATIONCENTER (ERIC)

El Frus document has been reproduced asreceived from the person or orgenrztiOnoogrnahng el

fl Monor changes have been made 10 .rnprovereproduChon quality

"PERMISSION TO REPRODUCE THISMATERIAL HAS BEEN GRANTED BY

Romts Owe. or opauons stated $n Ih.s docurnen1 do not neCessenly represent offic.alOE RI posd,on or MSc,/

TO THE EDUCATIONAL RESOURCESINFORMATION CENTER (ERICI."

Interim Guide

1993

Accounting Principles 30G

Interim Guide

*ManitobaEducationand Training l )

ISBN 0-7711-1135-5

4

ACCOUNTING PRINCIPLES 30G

This guide replaces, in part, the Accounting 202 and 302 guides of 1982, andbecomes effective September, 1993. The contents have been developed as part ofthe review of the Business Education cluster of courses which are affected bycomputer technology.

ACKNOWLEDGEMENTS

Members of the Business Education Steering Committee are

Gayle Halliwell (Chair)Lord Selkirk School Division No. 11

John ProudfootSt. James-Assiniboia School Division No. 2

Iris OverbyInterlake School Division No. 21

Lily BudzakWinnipeg School Division No. 1

Bill VandurmeSt. Vital School Division No. 6

Ben ZajacRiver East School Division No. 9

Roy Watt, ConsultantGoewan Personnel Services

Kathy Brough, Office Systems ManagerManitoba Telephone System

Edith LyonManitoba Business Education Teachers' Association

Ken HardyRed River Community College

ACCOUNTING PRINCIPLES

Members of the Accounting Working Party are

Andre Favreau (Writer)Fort Garry School Division No. 5

Dawn HicksSt. James-Assiniboia School Division No. 2

Sharon WilsonSeven Oaks School Division No. 10

Ken HardyRed River Community College

Tony Boron, CGABoeing Canada

Consultants to committees are

Marcel Daeninck (until 1992)Business Education ConsultantManitoba Education and Training

Tom PrinsBusiness Education ConsultantManitoba Education and Training

H. Marshall DraperCoordinator, Technology and ScienceManitoba Education and Training

ACCOUNTING PRINCIPLES

6

so

CONTENTS

Employability Skills Profile 1

Recommended Program Patterns 2

Rationale 3

Evaluation 4

Time Allotments 5

Goals and Objectives 5

Accounting Principles 30G 13

Basic Concepts 15The Cycle 22Controlling Cash 42Merchandise Accounting 55Payroll 65

Accounting Appendix 71

Bibliography 75

ACCOUNTING PRINCIPLES"7i

EM

PLO

YA

BIL

ITY

SK

ILLS

PR

OF

ILE

: The

Crit

ical

Ski

lls R

equi

red

of th

e C

anad

ian

Wor

kfor

ce

Aca

dem

ic S

kills

Tho

se s

kills

whi

ch p

rovi

de th

e ba

sic

foun

datio

nto

get

, to

keep

, and

to p

rogr

ess

on a

job

and

toac

hiev

e th

e be

st r

esul

ts.

Can

adia

n em

ploy

ers

need

peo

ple

who

are

abl

eto C

omm

unic

ate

Und

erst

and

and

spea

k th

e la

ngua

ges

in w

hich

busi

ness

is c

ondu

cted

List

en to

und

erst

and

and

lear

nR

ead,

com

preh

end,

and

use

writ

ten

mat

e-ria

ls, i

nclu

ding

gra

phs,

cha

rts,

and

dis

play

sW

rite

effe

ctiv

ely

in th

e la

ngua

ges

in w

hich

busi

ness

is c

ondu

cted

Thi

nk Thi

nk c

ritic

ally

and

act

logi

cally

to e

valu

ate

situ

atio

ns, s

olve

pro

blem

s, a

nd m

ake

deci

sion

sU

nder

stan

d an

d so

lve

prob

lem

s in

volv

ing

mat

hem

atic

s an

d us

e th

e re

sults

Use

tech

nolo

gy, i

nstr

umen

ts, t

ools

and

info

rmat

ion

syst

ems

effe

ctiv

ely

Acc

ess

and

appl

y sp

ecia

lized

kno

wle

dge

from

vario

us fi

elds

, e.g

., sk

illed

trad

es, t

echn

olog

y,ph

ysic

al s

cien

ces,

art

s an

d so

cial

sci

ence

s

Lear

nC

ontin

ue to

lear

n fo

r lif

e

Per

sona

l Man

agem

ent S

kills

The

com

bina

tion

of s

kills

, atti

tude

s an

dbe

havi

ours

req

uire

d to

get

, to

keep

, and

to p

ro-

gres

s on

a jo

b an

d to

ach

ieve

the

best

res

ults

.

Can

adia

n em

ploy

ers

need

peo

ple

who

dem

on-

stra

te

Pos

itive

Atti

tude

s an

d B

ehav

iour

sS

elf-

este

em a

nd c

onfid

ence

Hon

esty

, int

egrit

y, a

nd p

erso

nal e

thic

sA

pos

itive

atti

tude

tow

ard

lear

ning

, gro

wth

,an

d pe

rson

al h

ealth

Initi

ativ

e, e

nerg

y, a

nd p

ersi

sten

ce to

get

the

job

done

Res

pons

ibili

tyA

bilit

y to

set

goa

ls a

nd p

riorit

ies

in w

ork

and

pers

onal

life

Abi

lity

to p

lan

and

man

age

time,

mon

ey, a

ndot

her

reso

urce

s to

ach

ieve

goa

lsA

ccou

ntab

ility

for

actio

ns ta

ken

Ada

ptab

ility

Pos

itive

atti

tude

s to

war

d ch

ange

Rec

ogni

tion

of a

nd r

espe

ct fo

r pe

ople

'sdi

vers

ity a

nd in

divi

dual

diff

eren

ces

The

abi

lity

to id

entif

y an

d su

gges

t new

idea

sto

get

the

job

done

crea

tivity

Tea

mw

ork

Ski

lls

Tho

se s

kills

nee

ded

to w

ork

with

oth

ers

on a

job

and

to a

chie

ve th

e be

st r

esul

ts.

Can

adia

n em

ploy

ers

need

peo

ple

who

are

abl

eto W

ork

with

Oth

ers

Und

erst

and

and

cont

ribut

eto

the

orga

niza

tion'

s go

als

Und

erst

and

and

wor

k w

ithin

the

cultu

re o

fth

e gr

oup

Pla

n an

d ra

ke d

ecis

ions

with

oth

ers

and

supp

ort t

he o

utco

mes

Res

pect

the

thou

ghts

and

opi

nion

s of

oth

ers

in th

e gr

oup

Exe

rcis

e "g

ive

and

take

" to

ach

ieve

gro

upre

sults

See

k a

team

app

roac

h as

app

ropr

iate

Lead

whe

n ap

prop

riate

, mob

ilizi

ng th

e gr

oup

for

high

per

form

ance

The

re is

a g

row

ing

conc

ern

that

man

y yo

ung

peop

ledo

not

see

the

dire

ct r

elev

ance

of w

hat t

hey

are

lear

ning

in s

choo

l to

thei

r ne

eds

in la

ter

life.

The

Con

fere

nce

Boa

rd o

f Can

ada

has

iden

tifie

d th

ecr

itica

l ski

lls, q

ualit

ies,

and

abi

litie

s th

at s

tude

nts

will

requ

ire to

mak

e a

succ

essf

ul tr

ansi

tion

from

sch

ool

to w

ork.

The

se s

kills

are

dev

elop

ed th

roug

h a

varie

tyof

life

exp

erie

nces

pro

vide

d by

par

ents

, int

egra

ted

educ

atio

nal a

ppro

ache

s in

sch

ools

, pos

t-se

cond

ary

inst

itutio

ns, a

ctio

ns th

at s

uppo

rt s

kiN

dev

elop

men

ton

the

fob,

and

form

al a

nd in

form

al o

ppor

tuni

ties

for

upda

ting

skill

s th

roug

hout

life

.

9

RECOMMENDED PROGRAM PATTERNS

This flowchart is meant to provide schools with a recommended sequence of studiesfor tne new Business Education courses. While the prerequisite to any course is at thediscretion of the school, the skill development as shown in the flowchart isrecommended. However, it is left to schools to schedule courses and to advisestudents based upon the educational readiness of individual students.

Exploration of General Business 20G/25G*

Business I OG/ I SG* Retailing 20S

IntroductoryKeyboardingI SG

AdvancedKeyboarding2SG

ComputerApplications20G

WordProcessing30G

Business Principles 30GShorthand andTranscription 30SPromotions 30SRelations in Business 30S

AutomatedOffice40S

AdvancedWord Processing4S S

* Under development

SoftwareApplications30S

Economics 40GLaw 40GShorthand andTranscription 40SManagement 40S

Marketing Practicum 40S

Seminarin Business40S

AccountingPrinciples30G

AccountingSystems

405

ACCOUNTING PRINCIPLES 2

RATIONALE

Accounting Principles 30G introduces Canadian accounting principles and practices.It is designed as a full and autonomous course. Completion of Accounting Principles30G is also recommended prior to study of Accounting Systems 405. Throughout thecourse, Generally Accepted Accounting Principles (GAAP) are monitored and followed.The consistent application of GAAP gives owners, managers, investors, and analystsconfidence that financial statements are prepared in accordance with a set ofrecognized standards.

Accounting Principles 30G is recommended for all students. On a personal level,knowledge of accounting is essential for banking, investing and saving, and forpolitica and consumer decisions. Students considering entrepreneurial pursuits willbenefit from this course. Business terms and practices are introduced as theaccounting cycle is studied.

For those Senior Years students who plan post secondary studies, AccountingPrinciples 30G may be part of career exploration in such areas as professionalaccounting, management and business studies, statistics, and computers.

Many students will use accounting knowledge and skills in entry-level occupations inboth small and large businesses. For those who become independent businessowners and professional people, knowledge and experience with accounting principlesand practices are essential. In Accounting Principles 30G, simple financial statementsare prepared and analyzed in both a service and a merchandising business.

The course is designed as a study of GAAP as they apply in introductory financialaccounting. The application of these principles and practices to computer accountingsoftware is the main thrust of Accounting Systems 40S. Consequently, no computerapplication is recommended for Accounting Principles 30G.

Accounting Principles 30G serves as the introduction to Accounting Systems 40S.The Generally Accepted Accounting Principles introduced and applied are built uponin the second course. Mastery of all objectives of Accounting Principles 30G isrecommended for success in all future accounting programs and courses.

ACCOUNTING PRINCIPLES 3

EVALUATION

Accounting Principles 30G is a study of GAAP as they apply to introductoryaccounting. Understanding and appreciation of GAAP, analyses of the effects ofbusiness decisions, the recording of transactions, and the preparation of reports andfinancial statements are all important facets of the course. Learning in each aspectshould be evaluated.

Formative tests are to be held throughout the term in order to provide importantfeedback to both the students and teacher. These formative tests may be the basisfor

further instruction by the teacheradditional study of concepts by studentssupplementary student practice in recording entries and preparation and analysesof reports and financial statements

It is recommended that tests be administered frequently. Students will appreciate theopportunity to discuss the dates of tests and the scheme for student evaluation nearthe beginning of the course.

Many teachers choose also to test knowledge of specific material on a unit-by-unitbasis. Understanding and application of principles may then be evaluated with testsand assignments held less frequently at the end of large blocks of work.

Guidelines for Evaluation

Unit 1 Basic Concepts 10%

Unit 2 The Accounting Cycle 40%

Unit 3 Controlling Cash 10%

Unit 4 Merchandise Accounting 30%

Unit 5 Payroll 10%

100%

ACCOUNTING PRINCIPLES 4

TIME ALLOTMENTS

Accounting Principles 30G is a full-credit course that has been developed by ManitobaEducation and Training, for general purposes. It represents 110-120 hours ofinstruction.

The following guidelines for time allotments are recommended

UNITS HOURS

. Basic concepts 10

2. The accounting cycle 45 50

3. Controlling cash 15

4. Merchandise accounting 30 35

5. Payroll 10 15

110 120

GOALS AND OBJECTIVES

To introduce students to basic accounting principlesTo have students complete the accounting cycleTo teach students the principles of cash receipts controlTo have students complete the accounting cycle of a merchandising businessTo have students record all the entries of payroll accounting

Objectives

UNIT 1: BASIC CONCEPTS

Beginning the Accounting System

Students should be able to

explain the need for and the purpose of financial records and accounting systemsdescribe and use the basic accounting principles of starting an accounting system

ACCOUNTING PRINCIPLES 3 5

Accounting Equation

Students should be able to

classify assets, liabilities, and owner's equityclassify as an asset or a liability each item from a random list of assets andliabilitiescalculate the tot& assets and the total liabilitiesdetermine the owner's equitydetermine, when given two elements, the missing element in the fundamentalaccounting equation

Financial Statements

Students should be able to

construct balance sheets for small businessesinterpret and analyze simple balance sheets from given data and managementcasesidentify, analyze and record increases and decreases in the fundamental elements(assets, liabilities, owner's equity, revenue and expenses) resuiting from businesstransactionssummarize the results of changes to the fundamental elements by preparingbalance sheets and income statements

General Ledger Accounts

Students should be able to

explain the need for and the purpose of ledger accountsexplain the relationship of each ledger account to the accounting equationapply the principles of debit and credit to the balance sheet accountsuse T-accounts to show increases and decreases in asset, liability aid owner'sequity accountsapply the principles of debit and credit to the income statement accountsuse T-accounts to show increases and decreases in revenue and expenseaccounts

Generally Accepted Accounting Principles

Students should be able to

define what is meant by GAAPsexplain the revenue recognition GAAP

ACCOUNTING PRINCIPLES 6

e

explain the expense recognition GAAPexplain the matching GAAP

UNIT 2: THE CYCLE

Source Documents

Students should be able to

explain the importance of and the need for source documentsidentify source documentsprepare source documentsuse calculators to check the mathematical accuracy of source documentsanalyze the debit and credit parts of business transactions from given sourcedocuments

Journal Entries

Students should be able to

explain the need for and the importance of a journalrecord journal entries resulting from business transactionsfollow appropriate checking and correcting procedures for preparing accountingproofs to the journal

Ledger

Students should be able to

explain the need for and the importance of the ledgerprepare a chart of accountsstate the purpose of each ledger accountpost journal entries into the appropriate ledger accounts with cross references foreach entryfollow appropriate checking and correcting procedures for preparing accountingproofs for a ledger account balance

Trial Balance

Students should be able to

explain the need for and the importance of the trial balanceprepare a trial balance

ACCOUNTING PRINCIPLES 71 5

follow appropriate procedures for locating and correcting errors in the trial balanceclassify the types of accounts in the trial balance and name the normal side ofeach account balance

Worksheet

Students should be able to

explain the need for and the purposes of a worksheetprepare a six-column worksheet

Financial Statements

Students should be able to

explain the need for and the purpose of an income statement and a balance sheetprepare income statements from information in six-column worksheetsprepare balance sheets in account and report forms from information in six-columnworksheetsanalyze the performance and financial position of businesses from incomestatements and balance sheets

Closing Accounts

Students should be able to

explain the Cost GAAPexplain and calculate what is meant as the cost of an assetexplain the need for and the purpose of closing the ledgerrecord closing entries in the journalprepare journal entries to close revenue accountsprepare journal entries to close expense accountsprepare journal entries to transfer net income or net loss to the capital accountprepare a journal entry to transfer the drawing account to the capital accountpost closing entries to the ledger accountsprepare a post-closing trial balance

/- 6

ACCOUNTING PRINCIPLES

* UNIT 3: CONTROLLING CASH

Cash Receipts

Students should be able to

identify, explain and apply the accounting principles of cash receipts control, i.e.,objectivity and revenueprepare daily cash proofsprepare a cash receipts journal (record from source documents, total and rule)post from the cash receipts journal

Cash Payments

Students should be able to

identify, explain and apply the accounting principles of cash disbursements(payments) controlprepare daily proofsprepare a cash payments journal (record from source documents, total and rulepost from the cash payments journal

Petty Cash

Students should be able to

explain the need for a petty cash fund and petty cash vouchersrecord the establishment of a petty cash fund'record the entries needed to maintain a petty cash bookrecord the entry needed to replenish the fund

Bank Reconciliation

Students should be able to

explain the purposes of a bank reconciliationidentify the sources of information required for the preparation of a bankreconciliationprepare a bank reconciliation

ACCOUNTING PRINCIPLES 9

Cash Account and Cheque Book Adjustments

Students should be able to

explain the need for entries to adjust the cash account and the cheque stubbalancerecord the entries to adjust the cash accountadjust/correct the cheque stub balance

UMT 4: MERCHANDISE ACCOUNTING

Merchandising Business

Students should be able to

define merchandising businessidentify and explain how a merchandising business differs from a service businessidentify the special accounts for a merchandising businessidentify the special journals for a merchandising business

Sales Journal

Students should be able to

identify the need for and the purpose of a sales journalrecord the sales of merchandise in the sales journaltotal and rule the sales journal

Accounts Receivable Ledger

Students should be able to

identify the need for and the purpose of the accounts receivable ledgeropen an accounts receivable ledgerpost from the sales journalidentify the need for credit memorandarecord the sales returns and .dlowancespost sales returns and allowances

ACCOUNTING PRINCIPLES 10

Purchases Journal

Students should be able to

identify the need for and the purpose of a purchases journaltotal and rule the purchases journal

Accounts Payable

Students should be able to

identify the need for an accounts payable ledgeropen an accounts payable ledgerpost from the purchases journalrecord and post transportation-in costsidentify the need for a debit memorecord purchases returns and allowancespost purchases returns and allowances

UNIT 5: PAYROLL

Payroll Accounting

Students should be able to

explain the need for and the components of a payroll systemcompute gross earningsdetermine payroll deductionscalculate net payidentify the need for and the purpose of the payroll registerprepare a payroll registerrecord the journal entries for the payroll informationrecord the journal entries for the payment of the payroll to the employeesrecord the journal entries for payments of amounts owed to other agencies

ACCOUNTING PRINCIPLES 1 1

ACCOUNTINGPRINCIPLES 30G

UNIT 1: BASIC CONCEPTS

GOAL: To introduce students to basic accounting principles.

OBJECTIVES METHODS

1.0 Beginning the Accounting System

Students should be able to

1.1 explain the need for andthe purpose of financialrecords and accountingsystems

L.le the textbook as well as pertinentexamples, e.g., family, school records,corporations, to illustrate howimportant it is to maintain accuraterecords of the money flowing into andout of an organization. Maintain aclass discussion about the type ofinformation that any business wouldneed in order to make intelligentdecisions regarding the handling of itsmoney. Use the questions in theintroductory chapter of the textbookfor further discussion and practice.

Illustrate the calculation of the netfinancial worth of an individual byusing the following example

1.2 describe and use the basicaccounting principles ofstarting an accountingsystem

Financial Worth of a HighSchool Student

Money in pocket $ 7.23Cash in bank 235.00Clothes 450.00CD player 350.00CD collection 170.00Sailboard 1350.00

$2562.23

ACCOUNTING PRINCIPLES 15

UNIT 1: BASIC CONCEPTS (CONT.) (

OBJECTIVES1

METHODS

Use the same example to introducethe idea of deducting what thestudent owes to accurately determinethe financial net worth.Example: The student in the aboveexercise still owes $800.00 on hissailboard. To calculate his netfinancial worth we must subtract whathe owes from what he owns

OWNS OWES = NET FINANCIAL i,

WORTH OF AN INDIVIDUAL

The textbook may contain casestudies or questions that could beused to reinforce this concept(Transparency Master 1).

2.0 Accounting Equation

Students should be able to

2.1 classify assets, liabilitiesand owner's equity

2.2 classify as an asset or aliability each item from arandom list of assets andliabilities

i

,

The above basic accounting equationmay be used to discuss the termsassets (what an organization owns),liabilities (what an organization owes)and owner's equity (financial worth ofthe organization). Formulate theFundamental Accounting Equation

ASSETS = LIABILITIES +OWNER'S EQUITY

A variety of methods, such asflashcards, board work, write-onslides, etc., may be used to drill thestudents on the classification of assetsand liabilities (Transparency Master 2).

ACCOUNTING PRINCIPLES

e

16

UNIT 1: BASIC CONCEPTS (CONT.)

OBJECTIVES METHODS

2.3 calculate the total assetsand the total liabilities

2.4 determine the owner'sequity

2.5 determine, when given twoelements, the missingelement in the fundamentalaccounting equation

Use teacher-generated examples toillustrate the calculation of total assetsand total liabilities. Students shouldcalculate each from other teacher-generated or textbook questions.

Have the student determine whichelement is missing from theaccounting equation using textbook-or teacher-generated questions. Alsohave the student calculate the value ofthe missing element when givenvalues for the other two elements(Transparency Master 3).

3.0 Financial Statements

Students should be able to

3.1 construct balance sheetsfor small businesses

Explain the importance of preparingbeginning balance sheets for allbusinesses. Use the textbook toillustrate the balance sheet(Transparency Master 4).

The ledger of T-account balance sheetshould be used at this stage.Demonstrate in a step-by-step methodhow to prepare a balance sheet.Emphasize that the ledger form ofbalance sheet has a left side and aright side which correspond to theaccounting equation (A =L + OE) andthat these two sides must be equal,thus the name balance sheet.

41) ACCOUNTING PRINCIPLES 17

UNIT 1: BASIC CONCEPTS (CONT.)

OBJECTIVES METHOD

3.2

3.3

interpret and analyzesimple balance sheets fromgiven data andmanagement cases

identify, analyze and recordincreases and decreases inthe fundamental elements(assets, liabilities, owner'sequity and expenses)resulting from businesstransactions

Illustrate, using an example from thetext, how each balance sheet isanalyzed using the simple questionsWHO What is the name of thecompany?WHAT What is the name of theform?WHEN What is the date of thebalance sheet?Also have students identify the BODYof the balance sheet and the totals ofthe assets, liabilities, and owner'sequity.

Using the fundamental accountingequation and the balance sheet,illustrate how the assets, liabilities,and owner's equity are increased ordecreased when they are debited orcredited. A simple chart can be usedto illustrate these concepts

DR CRAssets +

Liabilities

Owner's Equity

Prepare a transparencyPrinciples of Debit andit in the discussion of(Transparency Master

Assets

Liabilities +

OE +

of the BasicCredit and use

these principles5).

ACCOUNTING PRINCIPLES 18

1

UNIT 1: BASIC CONCEPTS (CONT.)

OBJECTIVES METHODSi

Have students prepare balance sheetsin correct format using the textbookexamples.

3.4 summarize the results ofchanges to thefundamental elements bypreparing balance sheetsand income statements

4.0 General Ledger Accounts

Students should be able to

4.1 explain the need for andthe purpose of ledgeraccounts

4.2 explain the relationship ofeach ledger account to theaccounting equation

4.3 apply the principles of debitand credit to the balancesheet accounts

Explain why ledger accounts lead to amore efficient method of handlingtransactions. Illustrate what ledgeraccounts look like and howtransactions are recorded in them byusing the ledger accountstransparency or a teacher-generatedillustration (Transparency Master 6).

Illustrate this concept further by givingthe students simplified examples toanalyze. They should be able toidentify which accounts are involvedand, using the principles of credit anddebit, analyze how they will beaffected by each trapsaction.

ACCOUNTING PRINCIPLES 19

UNIT 1: BASIC CONCEPTS (CONT.)

OBJECTIVES METHODS

4.4 use T-accounts to showincreases and decreases inasset, liability and owner'sequity accounts

4.5 apply the principles of debitand credit to the incomestatement accounts

4.6 use T-accounts to showincreases and decreases inrevenue and expenseaccounts

Illustrate the concepts and proceduresof recording changes in asset, liability,and owner's equity accounts by usingsimulated account forms called T-accounts. Demonstrate the use of theT-accounts using the chalkboard ortransparencies (Transparency Masters7-1 0).

Have students analyze transactionsand identify the accounts to bedebited and credited. Apply theprinciples of debit and credit to theincome statement accounts.

Perform a simiiar demonstration forthe revenue and expense accountsand have students do examples andquestions from the text (TransparencyMasters 11 and 12).

ACCOUNTING PRINCIPLES

"u20

UNIT 1: BASIC CONCEPTS (CONT.)

OBJECTIVES METHODS

5.0 Generally Accepted AccountingPrinciples

Students should be able to

5.1 define what is meant by Explain the need for GAAPs. HaveGAAPs students write the definitions for each

of the GAAPs. Use questions from5.2 explain the revenue the textbook or workbook to further

recognition GAAP illustrate the GAAPs and their place inaccounting.

5.3 explain the expenserecognition GAAP See Appendix I for a complete listing

of the GAAPs and their definitions.5.4 explain the matching GAAP

NOTE: For the purpose of simplicity, the concept of the GST will be introducedunder merchandise accounting. Teachers interested in teaching the GSTat this point may refer to Appendix II.

ACCOUNTING PRINCIPLES 21

UNIT 2: THE CYCLE

GOAL: To have students complete the accounting cycle.

OBJECTIVES METHODS

1.0 Source Documents

Students should be able to

1.1 explain the importance of Illustrate the importance of sourceand the need for source documents by explaining the functiondocuments of each

To initiate the accounting cycleTo provide the accountant withinformation needed for makingaccounting entriesTo act as a basic proof if records arequestionedTo provide additional information notrecorded in accounting records.

1.2 identify source documents Illustrate the current types of sourcedocuments by using visual aids suchas overhead transparencies, actualsource documents or textbookexamples.

1.3 prepare source documents Prepare cheques and receipts andhave students do the same.

1.4 use calculators to check Have students check the accuracy ofthe mathematical accuracy several examples of sourceof source documents documents. Emphasize the

importance of this procedure.

1.5 analyze the debit and credit Using several examples of sourceparts of business documents, have students analyze thetransactions from given documents in terms of accounts to besource documents debited and credited.

ACCOUNTING PRINCIPLES 22

UNIT 2: THE CYCLE (CONT.)

OBJECTIVES METHODS

2.0 Journal Entries

Students should be able to

2.1 explain the need for andthe importance of a journal

2.2 record journal entriesresulting from businesstransactions

Use the following as some of the keypoints that should be stressed whenexplaining the importance of thejournal

The need for chronological recordingof business transactions to presentthe daily history of the businessThe need for more completeinformationThe need for an effective means oflocating errorsThe need for a system of providingevidence of the transactions ifsource documents are lost

Discuss the relationship betweensource documents and journal entries.

Use familiar transactions fromproblems completed in the previoussections.

Explain the journal entry in terms ofchanges in the accounting equationand the ledger. Have students analyzeseveral transactions. Use of ananalysis sheet such as the one foundin Transparency Master 13 mightprove useful before the studentsrecord the journal entry. Provideseveral examples of journal entrieseither on the chalkboard or theoverhead for illustrative purposes.

0 ACCOUNTING PRINCIPLES 23

UNIT 2: THE CYCLE (CONT.)

OBJECTIVES METHODS

2.3 follow appropriate checkingand correcting proceduresfor preparing accountingproofs to the journal

Emphasize in these examples that thejournal entry is very important. Stressthe sequence of recording the entries.A list of procedures and sequencesuch as the one that follows may beused

Note the date of the sourcedocumentRecord debit account title at thedate marginRecord the amount in the debitcolumn (left column)Record credit account title a halfinch from the date marginRecord the amount in the creditcolumn (right column)Record the explanation of thetransaction

Students will learn this concept onlythrough practice. It is recommendedthat several questions from thetextbook be used to develop andreinforce journalizing skills.

Use a calculator to check the accuracyof the equality of the debit and creditcolumns in the general journal.

,

ACCOUNTING PRINCIPLES 24

UNIT 2: THE CYCLE (CONT.)

OBJECTIVES METHODS

3.0 Ledger

Students should be able to

3.1 explain the need for and The purposes of the ledger could bethe importance of theledger

discussed using the following

To sort the journal entries intoaccountsTo summarize the effect oftransactions on accountsTo show in one place the totalamount of each accountTo supply account balances toprepare an up-to-date balance sheetand income statement

3.2 prepare a chart of accounts Explain that the chart of accountsoutlines the order of the accounts inthe ledger. This procedure makes iteasy to locate on the financial reportsand also serves as a guide injournalizing by identifying the accounttitles to be used when recordingtransactions.

CHART OF ACCOUNTS

Assets 101-199Liabilities 201-299Owner's Equity 301-399Revenue 401-499Expenses 501-599

3.3 state the purpose of each Discuss and give an example for eachledger account type of ledger account.

_

ACCOUNTING PRINCIPLES 25

UNIT 2: THE CYCLE (CONT.)

OBJECTIVES METHODS

3.4 post journal entries to the Demonstrate the posting procedureappropriate ledger accounts using the chalkboard and/or overheadwith cross references for projector. Be sure to stress neat andeach entry accurate work. A list of posting

procedures could be prepared ordictated to assist students in theirwork

Locate the ledger account for thefirst debit in the journal entryEnter the date of the journal entry inthe Date column on the debit side ofthe ledgerEnter an explanation, if needed, forthe entryEnter the journal initial and the pagenumber in the Post ReferencecolumnEnter the debit amount in the Debitmoney columnCalculate the balance of each ledgeraccount after an entry is postedEnter the account number in thePost Reference column of the journalto show that the information hasbeen postedLocate the ledger account for thenext entry. If the next entry is acredit, apply the procedure on thecredit side of the account

Demonstrate the steps in balancingeach account (foot debit column, footcredit column, subtract the smallercolumn from the larger) using thesame examples. Have students workthe textbook questions dealing withthis procedure.

ACCOUNTING PRINCIPLES 26

32

UNIT 2: THE CYCLE (CONT.)

OBJECTIVES METHODS

3.5 follow appropriate checkingand correcting proceduresfor preparing accountingproofs for a ledger accountbalance

Use calculators to check themathematical accuracy and record thebalance of each account on the side oforigin the same side as that onwhich it shows in the accountingequation

Assets = DR balanceLiabilities = CR balanceOwner's Equity = CR balanceRevenue = CR balanceExpense = DR balance

4.0 Trial Balance

Students should be able to

4.1 explain the need for andthe importance of the trialbalance

Discuss the purposes of the trialbalance

To prove that the ledger is inbalanceIt serves as a step to finding theprofit or loss of the business

Emphasize that each entry of the trialbalance is a double entry containingone or more debits and credits andthat in the end, the total debits andthe total credits should be equal if allof the journalizing was done correctly.

111 ACCOUNTING PRINCIPLES

1 3

27

UNIT 2: THE CYCLE (CONT.)

OBJECTIVES METHODS

4.2 prepare a trial balance Demonstrate the preparation of a trialbalance using a teacher-preparedexample. As you work through theexample, have students write thebasic steps for preparing a trialbalance

Write the headingEnter each ledger account in the trialbalanceRule a single line across bothcolumns (signifying that all amountsabove the line are to be totalled)Add each amount columnRule a double line across the amountcolumns (signifying that the workabove the double line is completeand correct)

Emphasize that even though the trialbalance does balance, this is only aproof of the debits and credits notof the accounting soundness of theentries.

Have students work on the questionsin the textbook that deal with the trialbalance.

ACCOUNTING PRINCIPLES 28

UNIT 2: THE CYCLE (CONT.) 1

OBJECTIVES METHODS

4.3 follow appropriateprocedures for locating andcorrecting errors in the trialbalance

Discuss the types of errors that arecommonly made when preparing trialbalances. Explain how these errorscan be located and corrected. A chartof sources of posting errors and achart of methods of location andcorrection of errors may be used toassist students.

Sources of posting errors

Entire transaction not postedEither the debit or credit part of atransaction not postedPosting to the correct side but to thewrong accountCalculating balance incorrectlyTransposing figures

ACCOUNTING PRINCIPLES

35

29

UNIT 2: THE CYCLE (CONT.)

OBJECTIVES METHODS

4.4 classify the types ofaccounts in the trialbalance and name thenormal side of eachaccount balance

Location and correction of errors

Re-add both sides of the trialbalanceFind the difference betweer thetotals of the trial balance columns.Check in the ledger to determine ifthe amount of the difference is anaccount balance omitted from thetrial balanceDivide the amount of the differencebetween the two totals of the trialbalance by two. Check theaccounts to see if the amount hasbeen recorded on the wrong sideDivide the amount of the differencebetween the two totals of the trialbalance by nine. If the difference isdivisible by nine, check fortransposition of numbersCompare the balances on the trialbalance with balances in ledgeraccountsCheck the pencil footings and theaccount balance in the ledgerVerify the posting of each item inthe journal

ACCOUNTING PRINCIPLES

3G

30

UNIT 2: THE CYCLE (CONT.)

OBJECTIVES METHODS

5.0 Worksheet

Students should be able to

5.1 explain the need for andthe purposes of aworksheet

.

Explain the functions that a worksheetserves in the preparation of thefinancial statements. Use thefollowing as a guide

A sorting device (convenient meansof sorting accounts into differentclassifications; income statementcolumns and balance sheet columns)Calcuiating device (calculating netincome or loss)Source of data for closing entries(when the temporary accounts areclosed and their balances transferredto the summary account, thegrouping of these accounts in theincome statement columns of theworksheet help in the process)Device for making adjusting entries(this function will become moreapplicable when looking at a ten-column worksheet covered in thesection dealing with completion ofthe accounting cycle)

ACCOUNTING PRINCIPLES

0 7

31

UNIT 2: THE CYCLE (CONT.)

OBJECTIVES METHODS

5.2 prepare a six-columnworksheet

Explain and discuss the reasons forusing the worksheet

Aids in preparing the financialstatementProvides for organization ofaccounting dataShows the total picture ofaccounting information

Emphasize the fact that the worksheetshows the whole picture in one place:trial balance, net income, data for theincome statement, and data for thebalance sheet.

Develop the first worksheet through astep-by-step class presentation. Havestudents complete the sameworksheet in their notebooks.

Emphasize that the worksheet is aworking paper that may be prepared inpencil. Also emphasize the step-by-step approach in preparing the six-column worksheet. Use the followingsteps in worksheet preparation

Write the main headingRecord the trial balanceExtend each item from the trialbalance to the proper statementcolumnDetermine and record net income inthe income statement debit columnRecord net income in the balancesheet credit columnRule double lines

ACCOUN1.1IG PRINCIPLES 32 411)

UNIT 2: THE CYCLE (CONT.)

OBJECTIVES METHODS

6.0 Financial Statements

Students should be able to

6.1 explain the need for andthe purpose of an incomestatement and a balancesheet

6.2 prepare income statementsfrom information in six-column worksheets

Discuss the overall purpose offinancial statements

Provision of financial informationabout the business to owners,management, creditors andgovernment

Discuss the main purpose of eachstatement

Income Statement to showoperating results for a business over aperiod of time

Balance Sheet to present thefinancial position of a business at aspecific date.

Instruct the students to accordion-foldthe worksheet between each pair ofcolumns. This places the data in theincome statement columns close tothe account titles when preparing theincome statement.

Develop the income statement througha step-by-step class presentation(Transparency Master 14).

Have students prepare the sameincome statement in their notebooks.

110 ACCOUNTING PRINCIPLES 33

UNIT 2: THE CYCLE (CONT.)

OBJECTIVES METHODS

6.3

6.4

prepare balance sheets inaccount and report formsfrom information in six-column worksheets

analyze the performanceand financial position ofbusinesses from incomestatements and balancesheets

Emphasize that all the informationneeded to prepare the incomestatement is available from the twoincome statement columns on theworksheet.

Demonstrate the preparation of abalance sheet using the aboveteaching method, introducing thereport format.

Have students prepare the samebalance sheet forms in theirnotebooks.

Be sure to emphasize that all of therequired data is readily available fromthe worksheet in the two balancesheet columns. Emphasize also thatmethodical, ar:curate work isnecessary to complete the financialstatements in good form.

Discuss the questions that areanswered by financial statements

What does the business own?What debts does the business owe?Is net income increasing/decreasing?Should selling prices beincreased/decreased?Should more money be invested in thebusiness?

ACCOUNTING PRINCIPLES

4 0

34

UNIT 2: THE CYCLE (CONT.)

OBJECTIVES METHODS

7.0 Closing Accounts

Students should be able to

7.1 explain the Cost GAAP See Appendix I.

7.2 explain and calculate whatis meant as the cost of anasset

7.3 explain the need for and Have students refer to previouslythe purpose of closing theledger

completed ledgers and balance sheets,prepared from the information in theledger. Ask the students to comparethe balance of the capital account inthe general ledger with the reportedfinal capital balance in the balancesheet and to note the differencebetween the recorded amounts.

The purpose of closing entries shouldbe discussed

To transfer the net income or thenet loss for a period of time to thecapital account so that the owner'sequity is accurately reported andshown each fiscal periodTo assist in the preparation of theincome statement

ACCOUNTING PRINCIPLES 35

UNIT 2: THE CYCLE (CONT.)

OBJECTIVES METHODS

7.4 record closing entries in thejournal

I

0 To close all open accounts 1

1

containing elements of revenue and 1

expenses so that all such accountsare balanced, closed and "emptied"for the period for a fresh start in the I

subsequent accounting period 1

1

I

Explain how closing entries will update '

the balance of the capital account inthe general ledger.

I

Emphasize the importance of preparing I

the ledger for the next accountingperiod by clearing the revenueaccounts and the expense accounts oftheir balances.

Provide students with a ledger that isready to close.

Use a ledger prepared by students inworking through the accounting cyclefrom opening entries to thepreparation of financial statements.

Teach the meaning of "closed"account by demonstrating when anaccount is closed and how it is closedby preparing and posting a journalentry.

ACCOUNTING PRINCIPLES

4'436

,UNIT 2: THE CYCLE (CONT.)

)

OBJECTIVES METHODS

Present the use of the new account,revenue and expense summary,showing how this account is used as a"clearing account" and how itsummarizes the net income or net lossand thus allows only one net amountto be transferred to capital rather thanall the individual balances in therevenue and the expense accounts.

7.5 prepare journal entries to Have students follow the teacher'sclose revenue accounts step-by-step demonstration to close

the revenue accounts to the revenueand expense summary Account with ajournal entry posted immediately.

Have students complete the samestep-by-step work at their desks.

7.6 prepare journal entries to Have students work with theclose expense accounts instructor step-by-step to close the

expense accounts into the R & Esummary account with the journalentries posted immediately.

7.7 prepare journal entries to Determine the net income or net losstransfer net income or net in the R & E summary account. Closeloss to the capital account the R & E summary account to the

capital account with the journal entryposted immediately.

ACCOUNTING PRINCIPLES 37

UNIT 2: THE CYCLE (CONT.)

OBJECTIVES METHODS

Demonstrate each of the steps in theclosing procedure by showing thefollowing

The information for each closingentry being taken from theworksheetThe closing entry being made in thejournalThe effect of posting the closingentries to the ledger accounts

Demonstrate, using a step-by-stepprocedure with student involvement,how each and all of the accounts willappear after closing.

ACCOUNTING PRINCIPLES . 38

UNIT 2: THE CYCLE (CONT.)

OBJECTIVES METHODS

7.8 prepare a journal entry totransfer the drawingaccount to the capitalaccount

Emphasize that the major steps inpreparing the closing entries are asfollows

Prepare a closing entry for allaccounts with credit balancesshown in the income statementcredit amount column of theworksheetPrepare a closing entry for allaccounts with debit balances shownin the income statement debitamount column of the worksheetPrepare a closing entry to record thenet income (or net loss) in thecapital account and to close the R &E summary account

Demonstrate using a step-by-stepapproach with student involvement.Transfer the drawing account to thecapital account with the journal entryposted immediately.

ACCOUNTING PRINCIPLES 39

4 5

UNIT 2: THE CYCLE (CONT.)

OBJECTIVES METHODS

7.9 post closing entries to theledger accounts

Use a chart similar to the following toillustrate the steps used to closerevenue and expense accounts

Revenue ExpenseAccounts Accounts

Step 1 Step 2

CR balances DR balancestransferred transferred

to CR side of to DR sideR & E Summary of R & E

Summary

R & E Summary

Step 1 Step 2

Balance Balance ofof Expense Revenue

Account Accounts(Step 3)transfer

to Capital

Capital Account Step 3net profit

ACCOUNTING PRINCIPLES

4 6

40

UNIT 2: THE CYCLE (CONT.)

OBJECTIVES METHODS

7.10 prepare a post-closing trialbalance

Discuss the purpose of a post-closingtrial balance: to determine if theledger is in balance before therecording of the transactions for thenext fiscal period.

Use a step-by-step approach withstudent involvement, to prepare thepost-closing trial balance. Point outthat the accounts appearing on thepost-closing trial balance arepermanent accounts. Show that theaccounts listed on the post-closingtrial balance and their balances are thesame as those appearing on thebalance sheet.

ACCOUNTING PRINCIPLES 41

UNIT 3: CONTROLLING CASH

GOAL: To teach students the principles of cash receipts control.

OBJECTIVES METHODS

1.0 Cash Receipts

Students should be able to

1.1 identify, explain and apply Identify and explain the following needthe accounting principles ofcash receipts control, i.e.,objectivity and revenue

and purposes to control cash receipts

To control theft, fraud and errorsmade by people within the businessTo provide a more efficient use ofemployee time

Emphasize and discuss the principlesof internal control of cash receipts

Deposit all cash dailySeparate the tasks of recording andhandling cash receivedCreate serially numbered sourcedocuments for cash receivedPrepare a daily cash proofUse periodic auditsPrepare bank reconciliationstatements

1.2 prepare daily cash proofsIllustrate and emphasize the procedurefor preparing daily cash proofs.

ACCOUNTING PRINCIPLES 42

UNIT 3: CONTROLLING CASH (CONT.)

OBJECTIVES METHODS

1.3 prepare a cash receiptsjournal (record from sourcedocuments, total and rule)

Illustrate and discuss the repetitivedebit entries for a series of entries toCash in the General journal. Callattention to the need to post the Cashentries several times from the generaljournal to the ledger.

Explain the need for a more efficientway to record cash receipts and topost the total cash received once atthe end of the month.

List and explain the source documentsfor cash receipts: cash register tapes,sales slips, cheques, money orders.

Demonstrate, using the overhead orthe chalkboard, how to journalize cashreceipts in the cash receipts journal.

Emphasize these concepts

The space saved by using a cashreceipts journal (CRJ)The convenience provided by therulings in the CRJ

ACCOUNTING PRINCIPLES 43

UNIT 3: CONTROLLING CASH (CONT.)

OBJECTIVES METHODS

1.4 post from the cash receiptsjournal

Demonstrate the procedure fortotalling and ruling the CRJ.

Emphasize the importance of

Totalling and checking the arithmeticaccuracy of the single moneycolumnRetention of the double-entrysystem in the CRJ

THE SINGLE TOTAL OF THE CASH,DEBIT, AGREES WITH THE TOTAL OFTHE TOTAL OF THE INDIVIDUALCREDIT ENTRIES.

ACCOUNTING PRINCIPLES 44

UNIT 3: CONTROLLING CASH (CONT.)

OBJECTIVES METHODS

2.0 Cash Payments

Students should be able to

2.1 identify, explain and applythe accounting principles ofcash disbursements(payments) control

2.2 prepare daily proofs

Identify and explain the same needsand purposes listed to control cashreceipts.

Stress the importance of the principlesof internal control of cash payments

Verify and approve all invoices forpaymentsMake all payments of materialamounts by chequeUse a petty cash fundUse only serially numbered chequesfor full accountabilityCancel all supporting documentspaid by cashDivide the responsibility of handlingcheques and for recording paymentsPrepare daily cash proofs of cashbalance

ACCOUNTING PRINCIPLES 45

UNIT 3: CONTROLLING CASH (CONT.)

OBJECTIVES METHODS

2.3 prepare a cash paymentsjournal (record from sourcedocuments, total and rule)

Illustrate and discuss the repetitivecredit entries to Cash in the generaljournal.

Call attention to the need to post theCash Credit entries several times fromthe general journal entries to theledger.

Explain the need for a more efficientway to record cash payments and topost the total cash paid once at theend of the month.

Stress the following prock,oures

Verifying and approving invoicesIssuing chequesCancelling bills paidMailing signed chequesPreparing cheque records

Emphasize the following during therecording of cash payments

Reason for disbursing cashMethod of recording transactions forcheque stubs in cash paymentsjournal

Prepare a cash payments journal onthe chalkboard or on an overheadtransparency.

Use a step-by-step approach duringthe recording of cash payments.

ACCOUNTING PRINCIPLES

546

UNIT 3: CONTROLLING CASH (CONT.)

OBJECTIVES METHODS

2.4 post from the cashpayments journal

Stress and demonstrate a step-by-stepprocedure for

Posting of debit entriesTotalling and ruling amount columnPosting total cash payments

411) ACCOUNTING PRINCIPLES

5:3

47

UNIT 3: CONTROLLING CASH (CONT.)

OBJECTIVES METHODS

3.0 Petty Cash

Students should be able to

3.1 explain the need for a pettycash fund and petty cashvouchers

3.2 record the establishment ofa petty cash fund

Discuss the purposes of the pettycash fund

To take care of small cash paymentsTo avoid the time and the cost ofmaking small payments by cheque

Discuss and explain the format andthe purpose of petty cash vouchers.Show examples of petty cashvouchers.

Emphasize the following

The issuing of a cheque to establishthe petty cash fundThe recording of the amount of thepetty cash fund in the petty cashbookThe purpose and/or use of a pettycash box or drawer

Use examples of pages from a pettycash book to illustrate this topic.

ACCOUNTING PRINCIPLES

5,1*

48

UNIT 3: CONTROLLING CASH (CONT.)

OBJECTIVES METHODS

3.3 record the entries neededto maintain a petty cashbook

3.4 record the entry needed toreplenish the fund

Emphasize the `,.ollowing points

Format of a typical petty cash bookFormat of a petty cash voucherProcedure for transferringinformation given on a voucher tothe petty cash book

Use'a step-by-step approach toillustrate how to enter information inthe petty cash book.

Emphasize the following

The procedure for totalling andruling the petty cash fund columnsin the petty cash book to determinethe cash paid out and the cash onhandVerification of the total of the cashon hand with the total of the cashcolumn in the petty cash bookIssuance of a cheque to replenishthe petty cash fund to its originalamountRecording the transaction ofreplenishing the petty cash fund inthe appropriate journal and in thepetty cash book

ACCOUNTING PRINCIPLES 49

UNIT 3: CONTROLLING CASH (CONT.)

OBJECTIVES METHODS

4.0 Bank Reconciliation

Students should be able to

4.1 explain the purposes of abank reconciliation

Review and/or teach the procedure foropening accounts in banks or otherfinancial institutions

Preparation of deposits and depositslipsProcessing of deposits by financialinstitutionsProcedure for writing cheques andrecording information on chequestubs

Emphasize that a bank reconciliation isan integral part of any business'soverall system for the effective controlof cash.

Stress the importance of the cashcontrol aspect as well as the methodof preparing a bank reconciliationstatement.

Discuss the principles of usingchequing accounts as a part of anybusiness's system for control of itsasset, cash.

ACCOUNTING PRINCIPLES 50

UNIT 3: CONTROLLING CASH (CONT.)

OBJECTIVES METHODS

The financial institution is acustodian of the funds of thebusinessThe funds of a business on depositwith a financial institution representa debt (liability) owning by thefinancial institution to the businessThe debt on the records of thefinancial institution increases eachtime the business makes depositsand this debt decreases each timethe business writes cheques on thefinancial institutionThe amount of indebtedness of thefinancial institution to the businessappears as an asset reflected by theCash account maintained in therecords of the businessTwo independent records of Cashare kept to control it. Therefore, anidentical figure for Cash shouldappear in both sets of books

Discuss the need to prepare astatement to correct anyerrors/discrepancies existing betweenthe two sets of records.

Compare a copy of the financialinstitution's record (monthlystatement) with the records of thebusiness (the chequebook and theledger account for Cash).

ACCOUNTING PRINCIPLES

5

51

UNIT 3: CONTROLLING CASH (CONT.)

OBJECTIVES METHODS

4.2

4.3

identify the sources ofinformation required for thepreparation of a bankreconciliation

prepare a bankreconciliation

Explain how to analyze a monthlybank statement and the formsenclosed with the statement.

Discuss the significance ofoutstanding cheques, cancelledcheques, deposits in transit,dishonoured cheques, bankmemoranda, service charges, errors,and certified cheques.

Analyze a problem by checking andcomparing a monthly bank statementagainst the information in thechequebook record for the business.Explain that this is a sorting process.

Emphasize the following

The purpose and the format of amonthly bank statementThe procedure of verifying the cashaccount balance with thechequebook balanceThe purpose of the bankreconciliation statement

Use the standard reconciliation formfound on the reverse side of bankstatements or two-column journalpaper.

ACCOUNTING PRINCIPLES

552

,..._UNIT 3: CONTROLLING CASH (CONT.)

OBJECTIVES METHODS

Demonstrate the preparation of thereconciliation statement.Point out that the reconciliationstatement must show a reconciliationof the cash balance: the adjustedbank balance must agree with theadjusted chequebook balance as at thedate of reconciliation.

5.0

-

Cash Account and Cheque BookAdjustment

Students should be able to

5.1 explain the need for entriesto adjust the cash accountand the cheque stubbalance

Explain the purpose of the adjustingentries to be made following thecompletion of the reconciliationstatement

To bring the balance of the latestchequebook record into agreementwith the adjusted cash balance onthe reconciliation statementTo update the cash account in theledger by journalizing and postingthe adjusting entries.

IIIACCOUNTING PRINCIPLES

5053

UNIT 3 CONTROLLING CASH (CONT.)

OBJECTIVES METHODS

5.2

5.3

record the entries to adjustthe cash account

adjust/correct the chequestub balance

Emphasize that the source of theseentries is in the section of thereconciliation statement thatreconciles the cash balance of thebusiness and not of the bank.

Demonstrate the method ofadjusting/correcting the chequebook(cheque stub balance).

NOTE: See Appendix II for more information concerning taxes related to salesand purchases.

ACCOUNTING PRINCIPLES

G

54

UNIT 4: MERCHANDISE ACCOUNTING

GOAL: To have students complete the accounting cycle of a merchandisingbusiness.

OBJECTIVES METHODS

1.0 Merchandising Business

Students should be able to

1.1 define merchandising The definition of the termbusiness merchandising business is a business

that buys and resells goods or onethat buys finished goods and sellsthem at a profit.

1.2 identify and explain how a The differentiation comes from themerchandising businessdiffers from a servicebusiness

fact that

A merchandising business obtains itsrevenue from selling goodsA service business obtains itsrevenue from selling services

1.3 identify the special Identify and discuss the specialaccounts for a accounts for merchandisingmerchandising business businesses

Inventory (Beginning)PurchasesTransportation-InPurchases Returns and AllowancesPurchases DiscountsInventory (Ending)

Explain the relationship of the specialmerchandising account by using amathematical example.

ACCOUNTING PRINCIPLES 55

UNIT 4: MERCHANDISE ACCOUNTING (CONT.)

OBJECTIVES METHODS

Prepare a diagram to illustrate theconcept of cost of goods sold.Develop a poster/overheadtransparency of the diagram. Usevisual aids to explain the Cost ofGoods concept (Transparency Master15).

Identify and discuss the followingspecial accounts: Sales, Sales Returnsand Allowances, Sales Discounts.Explain the relationship of the aboveaccounts by using a mathematicalexample and the following net salesequation

Sales (Sales Returns and Allowances+ Sales Discounts) = Net Sales(Transparency Masters 16 and 17).

ACCOUNTING PRINCIPLES

6`'4

56

UNIT 4: MERCHANDISE ACCOUNTING (CONT.)

OBJECTIVES METHODS

1.4 identify the special journalsfor a merchandisingbusiness

Prepare a transparency to identify anddiscuss the special journals used by atypical merchandising firm.

Identify and discuss the basicprinciples involved with all specialjournals

Types of special journals aredetermined by the scope and natureof the operations of a businessenterpriseSpecial journals are needed only forthe types of transactions that occurfrequentlyEach special journal is designed torecord a series of similar types oftransactionsSpecial journals should be costeffective, resulting in a saving oftime and space

Discuss the advantages of usingspecial journals

Permits better division of workReduces the number of postingsReduces detail and amount of spacerequired to record transactionsDecreases opportunities for errorsMakes it easier to analyze andretrieve data

ACCOUNTING PRINCIPLES

63

57

UNIT 4: MERCHANDISE ACCOUNTING (CONT.)

OBJECTIVES METHODS

2.0 Sales Journal

Students should be able to

2.1 identify the need for andthe purpose of a salesjournal

2.2 record the sales ofmerchandise in the salesjournal

,

Discuss the need for a special journalto record credit sales of the invoicesfor each monthly accounting period.Demonstrate the repetitive nature ofcredit sales, especially for amerchandising business, to point outthe advantages of using a specialsales journal.

Definition: Sales journal is used torecord credit sales (and cash sales) bydesignated categories, e.g., foods, drygoods, hardware.

Point out that in accounting practicethe sales journal may have manydifferent forms and names.

The design of the sales journalacknowledges the specific type ofrevenue-making transactions (sales).

Discuss and analyze sourcedocuments sales invoices.

Have students analyze the salesinvoices in the form of a double entry.

Demonstrate the recording of entriesin the sales journal and have studentsprepare the same entries.

ACCOUNTING PRINCIPLES 58

4)

1

UNIT 4: MERCHANDISE ACCOUNTING (CONT.)

OBJECTIVES METHODS

2.3 total and rule the salesjournal

Demonstrate, using a step-by-stepapproach, the totalling, ruling andcross-balancing of the sales journaland have students perform the sameprocedure.

Definition: Cross-balancing the salesjournal page determines if the total ofthe debit columns equals the total ofthe credit columns.

3.0 Accounts Receivable Ledger

3.1 identify the need for andthe purpose of theaccounts receivable ledger

3.2 open an accountsreceivable ledger

Discuss the purposes of the accountsreceivable ledger

Contain customer's accountsProvide for division of labourProvide accounting controlPrevent overcrowding of the generalledger

Demonstrate the opening of theaccounts in the accounts receivableledger and have students perform thesame procedure.

Emphasize the following

The logical order of customers in theaccounts receivable ledgerSpecial information about customers(names and addresses, credit limits)

41) ACCOUNTING PRINCIPLES

6'059

UNIT 4: MERCHANDISE ACCOUNTING (CONT.)

OBJECTIVES METHODS

3.3 post from the sales journal Discuss and explain information aboutpostings

Posting as a controlling functionPosting daily ' the accountsreceivable ledger because of needfor current balancesPosting monthly to the accountsreceivable account in the generalledger when results of businessoperation are determined andfinancial statements are prepared

Demonstrate and have students postfrom the sales journal.

3.4 identify the need for credit Explain the need for and the purposememoranda of credit memoranda. Show examples

of credit memoranda.

Definition: Credit memorandum is aspecial statement granting a reductionin the invoice price of damaged/returned goods or shortage of goods.

Analyze the credit memorandum.

3.5 record the sales returns and Record the sales return; andallowances allowances in the appropriate journal

according to your particular text.

Discuss and have studentsdemonstrate the debit and creditentries.

ACCOUNTING PRINCIPLES

6

60

UNIT 4: MERCHANDISE ACCOUNTING (CONT.)

OBJECTIVES METHODS

3.6 post sales returns andallowances

Demonstrate the posting procedure.

Emphasize that there is a doubleposting

To the controlling AccountsReceivable account in the generalledgerTo the individual customer's accountin the accounts receivable ledger

4.0 Purchases Journal

Students should be able to

4.1 identify the need for andthe purpose of a purchasesjournal

Discuss the need for a special journalto record credit purchases. Havestudents identify, from examples, theneed for a purchases journal to listchronologically all credit purchases.Demonstrate the repetitive nature ofcredit purchases, especially for amerchandising business, to point outthe advantages of using a specialpurchases journal.

111 ACCOUNTING PRINCIPLES

6"i

61

UNIT 4: MERCHANDISE ACCOUNTING (CONT.)

OBJECTIVES METHODS

4.2 total and rule the purchasesjournal

Explain that in accounting practice thepurchases journal may have manydifferent forms and names. Thedesign of the purchases journal isdependant upon the types of purchasetransactions. The teacher may alsointroduce the multi-column purchasesjournal for all purchases on credit.

Demonstrate and have studentsprepare the recording of entries in thepurchases journal.

Demonstrate, using a step-by-stepapproach, the totalling and ruling ofthe purchases journal and havestudents perform the same procedure.

Explain and demonstrate theprocedure for cross-balancing thepurchases journal. Discuss theimportance of obtaining a cross-balance before the totals are posted tothe general ledger.

Cross-balancing a journal pagedetermines if the total of the debitcolumns equals the total of the creditcolumns.

ACCOUNTING PRINCIPLESLI

62

UNIT 4: MERCHANDISE ACCOUNTING (CONT.)

OBJECTIVES METHODS

5.0 Accounts Payable

Students should be able to

5.1 identify the need for an Discuss the purposes of the accountsaccounts payable ledger payable ledger.

Contains creditor's accountsProvides for division of labourProvides for accounting controlPrevents overcrowding of thegeneral ledgerProvides information pertinent torotating the schedule of payments

5.2 open an accounts payable Demonstrate the opening of anledger accounts payable ledger. Have

students perform the same procedure.

Emphasize

The alphabetical order of creditors inthe accounts payable ledgerThe special information aboutcreditors

5.3 post from the purchases Emphasize posting as a controllingjournal function: posting daily to the

accounts payable ledger because ofthe need for current balances andposting monthly to the accountspayable control account in the generalledger when results of businessoperations are determined andfinancial statements are prepared.

Demonstrate and have students postfrom the purchases journal.

ACCOUNTING PRINCIPLES 63

UNIT 4: MERCHANDISE ACCOUNTING (CONT.)

OBJECTIVES METHODS

5.4 record and post Discuss the relationship oftransportation-in costs transportation-in costs to the cost of

merchandise. Emphasize that thetransportation-in costs must be addedto the purchase cost to obtain thecost of goods delivered.

Demonstrate the recording oftransportation-in the appropriatejournal and have students perform thesame procedure.

Discuss and demonstrate the postingof transportation-in costs to thegeneral ledger and to the accountspayable ledger and have studentsperform the same procedure.

5.5 identify the need for a debit Discuss the source document, debitmemo memorandum, for purchases returns

and allowances.

5.6 record purchases returnsand allowances

5.7 post purchases returns and Emphasize the posting to theallowances Accounts Payable control account in

the general ledger and to the individualcreditor's account in the accountspayable ledger.

ACCOUNTING PRINCIPLES

7 0

64

UNIT 5: PAYROLL

GOAL: To have students record all the entries of payroll accounting.

OBJECTIVES METHODS

1.0 Payroll Accounting

Students should be able to

1.1 explain the need for and Explain the need to organize anthe components of a efficient payroll accounting system topayroll system control varicus payroll systems and to

maintain adequate payroll records asrequired by law.

Discuss the components of a payrollsystem

Procedures for timekeeping andcomputing earningsCalculating deductions from grossearningsRecording the payrollMaintaining payroll recordsDisbursing payments to employees,governments and other agencies

1.2 compute gross earnings Discuss the responsibility of theemployee to acquire a SIN and theresponsibility of the employer to havethe new employee complete a TD1 tax

,

form. Explain that the TD1 form is anauthorization form to deduct thecorrect rate of income tax.

Show examples of the related SIN andTD1 forms.

ACCOUNTING PRINCIPLES

71

65

UNIT 5: PAYROLL (CONT.)

OBJECTIVES METHODS

Discuss how common salary/wageplans determine the gross earnings ofemployees. Discuss various types ofsalary/wage plans: hourly-rate plan,salary plan, commission plan, piece-rate plan and combination of plans.

Explain factors that affect theemployee's hours of work and wages

Contract of employmentAgreement between an employerand a union (if applicable)Government legislation

Point out and discuss the reason fortimekeeping. The record of hoursworked may be in the form of a timecard for employees paid by the hourand an attendance record foremployees paid on a salary basis.

Reason for Timekeeping: Law requiresan employer to keep a complete recordof the hours worked by an employee.

Demonstrate the computation of grossearnings for various salary/wage plansand discuss the concept of grossearnings.

ACCOUNTING PRINCIPLES 66

UNIT 5: PAYROLL (CONT.)

OBJECTIVES METHODS

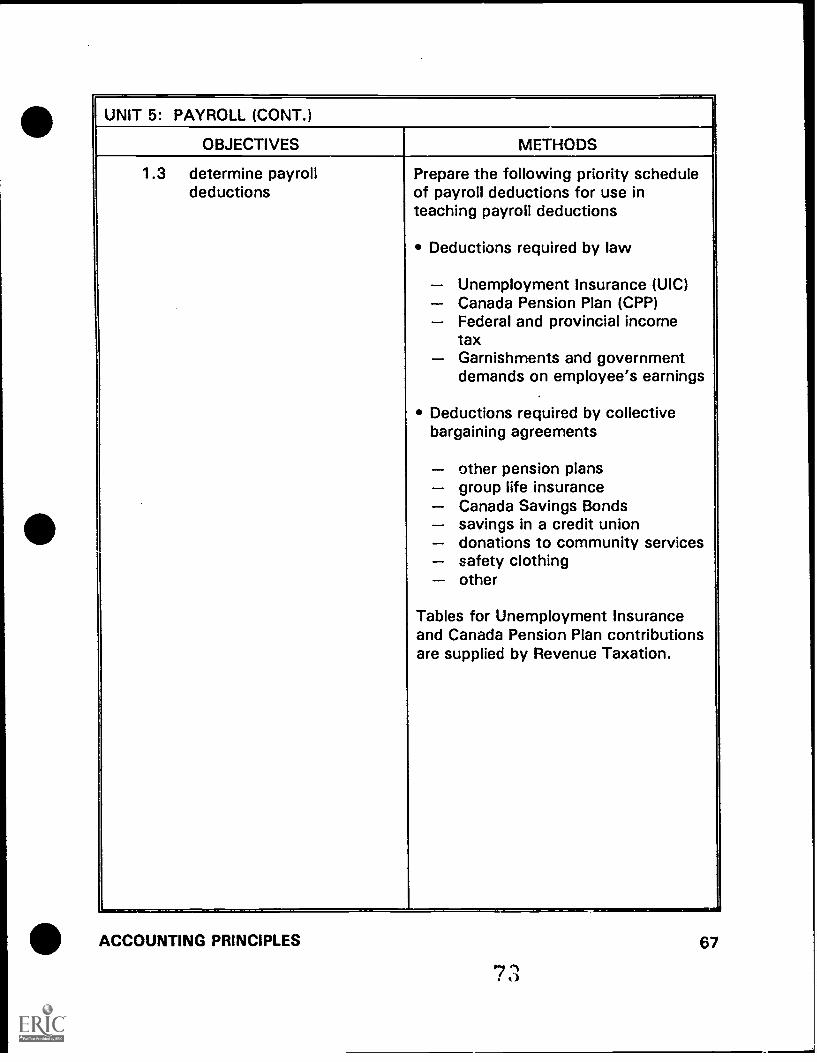

1.3 determine payrolldeductions

Prepare the following priority scheduleof payroll deductions for use inteaching payroll deductions

Deductions required by law

Unemployment Insurance (UIC)Canada Pension Plan (CPP)Federal and provincial incometaxGarnishments and governmentdemands on employee's earnings

Deductions required by collectivebargaining agreements

other pension plansgroup life insuranceCanada Savings Bondssavings in a credit uniondonations to community servicessafety clothingother

Tables for Unemployment Insuranceand Canada Pension Plan contributionsare supplied by Revenue Taxation.

ACCOUNTING PRINCIPLES

7 3

67

UNIT 5: PAYROLL (CONT.)

OBJECTIVES METHODS

1.4 calculate net pay Have students calculate severalexamples of the employee's net pay.

The textbook that you are usingshould have problems that can beused for this purpose.

1 .5 identify the need for and Explain the three steps in recordingthe purpose of the payrollregister

the payroll

Preparation of payroll summarypayroll registerPreparation of summary of details of

1 each employee's earningsemployee's individual earnings

,

record1

Journalizing and posting the payrollto update the general ledgeraccounts affected by the payroll

1.6 prepare a payroll register Explain the importance of the payrollregister in preparing a summary of allthe payroll data in one place.

Discuss the following facts

Payroll registers are prepared foreach payroll planPayroll registers vary in format anddesign from company to companyContent of a payroll registergenerally contains the names andidentification numbers of employees,details of employee's gross earningsand deductions and calculations ofemployee's net pay

ACCOUNTING PRINCIPLES

7c;

68

UNIT 5: PAYROLL (CONT.)

OBJECTIVES METHODS

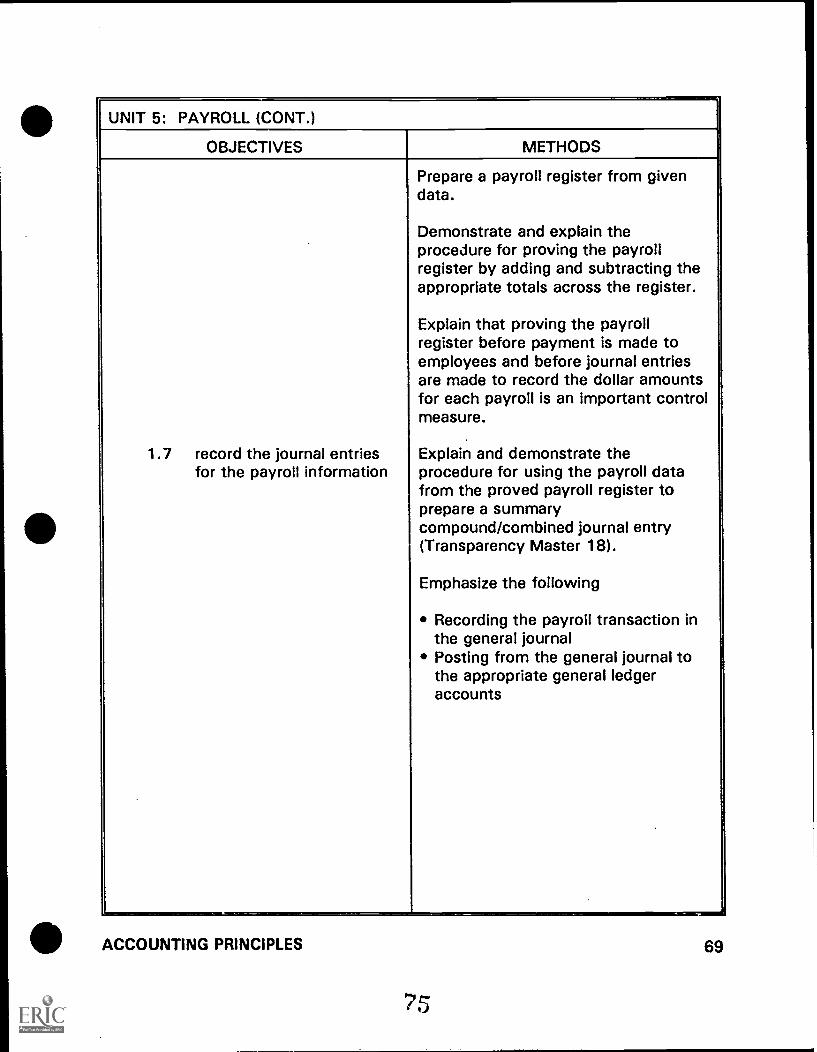

1.7 record the journal entriesfor the payroll information

Prepare a payroll register from givendata.

Demonstrate and explain theprocedure for proving the payrollregister by adding and subtracting theappropriate totals across the register.

Explain that proving the payrollregister before payment is made toemployees and before journal entriesare made to record the dollar amountsfor each payroll is an important controlmeasure.

Explain and demonstrate theprocedure for using the payroll datafrom the proved payroll register toprepare a summarycompound/combined journal entry(Transparency Master 18).

Emphasize the following

Recording the payroll transaction inthe general journalPosting from the general journal tothe appropriate general ledgeraccounts

-,ACCOUNTING PRINCIPLES

5

69

UNIT 5: PAYROLL (CONT.)

OBJECTIVES METHODS

1.8

1.9

record the journal entriesfor the payment of thepayroll to the employees

record the journal entriesfor payments of amountsowed to other agencies

Discuss and demonstrate the entry incash payments journal.

Discuss and demonstrate the entries inthe cash payments journal.

ACCOUNTING PRINCIPLES

7G

70

ACCOUNTING APPENDIX

APPENDIX I

GAAPs: Generally Accepted Accounting Principles

These GAAPs are presented together in this appendix. They should be introduced atappropriate times during the course.

The Business Entity Concept the accounting for a business should be keptseparate from the owners of the business or from any other business. Alltransactions and financial statements must reflect the financial position of thebusiness alone.

The Going Concern Concept the business in question is going to continue tooperate until notice has been given to the contrary. This concept generally comesinto consideration in the value of the assets.