Embed Size (px)

Citation preview

Disclaimer

I, Durgesh Kumar Kabra by means of this information is not rendering any professional advice or

service whatsoever

I have taken reasonable care to ensure that the information provided is accurate. Every effort has

been made to avoid errors or omissions in this NEWSLETTER. Inspite of this, errors may creep in.

Any mistake, error or discrepancy noted maybe brought to our notice which shall be taken care of

in our next edition.

I take no legal responsibility for any consequential incidents that may arise from errors or

omissions contained in this information

This is prepared based on the information available with DMKH at the time of preparing the

same, which is subject to changes that may directly or indirectly impact the information

provided. It is suggested that to avoid any doubt the reader should cross- check all the facts, law and

contents of the book with original Government Publication or notification.

I am under no obligation whatsoever to update or revise this information provided herein

This information provided is for intended recipient for knowledge and guidance purpose only

Neither me nor any person associated with me is responsible for any loss due to the informationprovided here. I recommend you to seek more clarity depending upon your businessrequirements

1

COMPLIANCE CHART JUNE 2021

The Business entity such as Proprietary Concerns/Partnership Firms/ LLP/ AOP/HUF/ Companies, etc. has to follow various statutory compliances monthly/quarterly/half-yearly/annually, as the case may be. For the benefit of all and timely compliances related to various laws applicable to be followed for the month of JUNE (MAY Commitments) are listed below:

Important Due date for Direct Tax and Statutory Compliance

SR. NO

Form to be filed

For the Period

Due date Who should file?

1 Challan No. ITNS-281

May 2021

07.06.2021 Payment of TDS/TCS deducted /collected in May 2021.

2 Electronic Challan cum Return (ECR) (PF)

May 2021

15.06.2021 E-payment of Provident Fund

3 ESI Challan May 2021

15.06.2021 ESI payment

4 Form No. 3BB May 2021

15.06.2021 Due date for furnishing statement in Form no. 3BB by a stock exchange in respect of transactions in which client codes been modified after registering in the system for the month of May, 2021

5 PT Payment FY 2021-22

20.06.2021 Professional tax payment for the financial year 2021-22. (Karnataka). Due date differs from one state to another

6 Pan and Aadhar linking

– 30.06.2021 Personals who have not linked their Aadhar with PAN Card

7 Payment of Tax under Vivad se Viswas Scheme

– 30.06.2021 Personals who have disputes related to income tax

8 Form SFT Return

FY 2020-21

30.06.2021 Tax payers who are required to file form 61 A

2

9 Payment of Advance Tax

First Quarter of FY 2021-22

15.06.2021 Personals who required to pay Advance Tax

Important Due date for Indirect Tax and Statutory Compliance`

SL NO

Form to be filed

For the Period

Due date Who should file?

1 GSTR 7 May 2021 10.06.2021 GSTR 7 is a return to be filed by the persons who is required to deduct TDS (Tax deducted at source) under GST

2 GSTR 8 May 2021 10.06.2021 GSTR-8 is a return to be filed by the e-commerce operators who are required to deduct TCS (Tax collected at source) under GST

3 GSTR 1 May 2021 11.06.2021 Taxpayers having an aggregate turnover of more than Rs. 1.50 Crores or opted to file Monthly Return

4 GSTR 1 IFF (QRMP)

May 2021 11.06.2021 GST return for the taxpayers who opted for QRMP scheme (Optional)

5 GSTR 6 May 2021 13.06.2021 Input Service Distributors 6 GSTR 5

& 5A May 2021 20.06.2021 Non-Resident Taxpayers and ODIAR services

provider

7 GSTR 3B May 2021 20.06.2021 The due date for GSTR-3B having an Annual Turnover of more than 5 Crores

8 GST Challan

For all Quarterly filers

25.06.2021 GST Challan Payment if no sufficient ITC for April (for all Quarterly Filers)

The month of June 2021 is crucial for the due dates for various compliances under Goods and Service Act, Income Tax Act, Companies Act and LLP Act. Filing the above mentioned forms on or before the due dates will save the Taxpayers from hefty penalties.

3

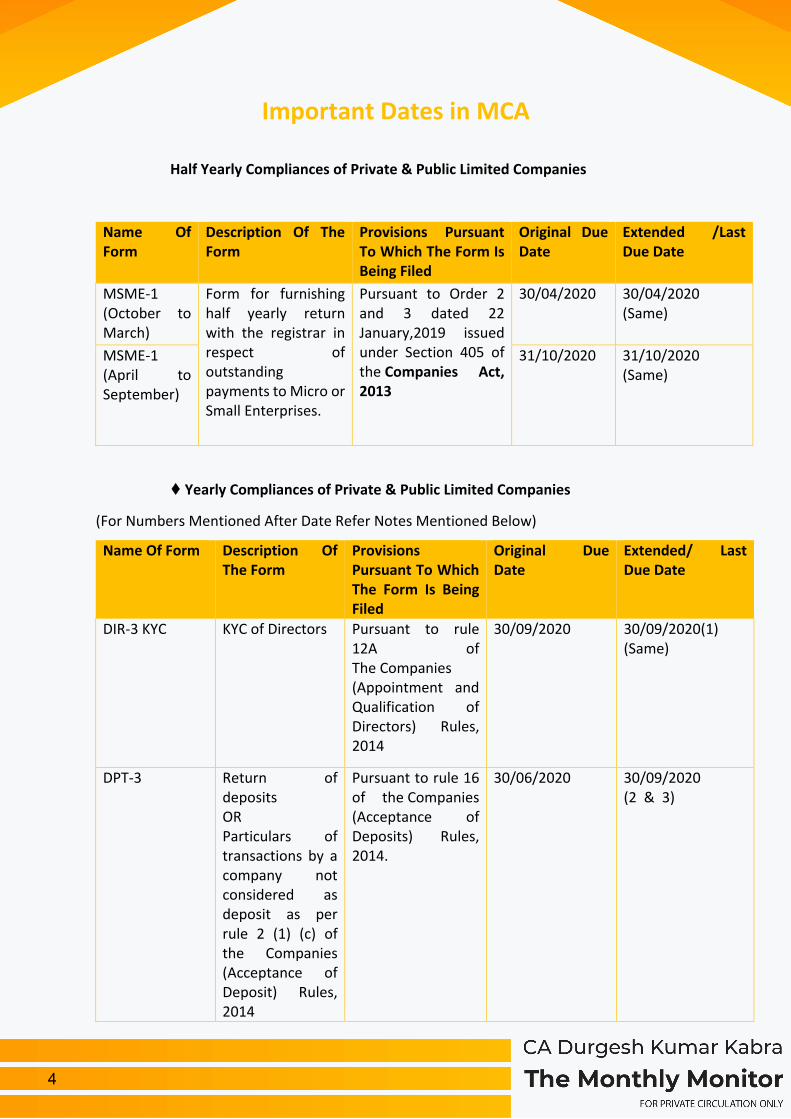

Important Dates in MCA

Half Yearly Compliances of Private & Public Limited Companies

Name Of Form

Description Of The Form

Provisions Pursuant To Which The Form Is Being Filed

Original Due Date

Extended /Last Due Date

MSME-1 (October to March)

Form for furnishing half yearly return with the registrar in respect of outstanding payments to Micro or Small Enterprises.

Pursuant to Order 2 and 3 dated 22 January,2019 issued under Section 405 of the Companies Act, 2013

30/04/2020 30/04/2020 (Same)

MSME-1 (April to September)

31/10/2020 31/10/2020 (Same)

♦ Yearly Compliances of Private & Public Limited Companies

(For Numbers Mentioned After Date Refer Notes Mentioned Below)

Name Of Form Description Of The Form

Provisions Pursuant To Which The Form Is Being Filed

Original Due Date

Extended/ Last Due Date

DIR-3 KYC KYC of Directors Pursuant to rule 12A of The Companies (Appointment and Qualification of Directors) Rules, 2014

30/09/2020 30/09/2020(1) (Same)

DPT-3 Return of deposits OR Particulars of transactions by a company not considered as deposit as per rule 2 (1) (c) of the Companies (Acceptance of Deposit) Rules, 2014

Pursuant to rule 16 of the Companies (Acceptance of Deposits) Rules, 2014.

30/06/2020 30/09/2020 (2 & 3)

4

OR Return of Deposit and Particulars of transactions by a company not considered as deposit.

BEN-2 Return to the Registrar in respect of declaration under section 90

Pursuant to section 90(4) of The Companies Act, 2013 and rule 4 and rule 8 of the Companies (Significant Beneficial Owners) Rules, 2018.

31/03/2020 30/09/2020 (2 & 3)

AOC-4 (FOR FY-2019-20)

Form for filing financial statement and other documents with the Registrar

Pursuant to section 137 of the Companies Act, 2013 sub-rule (1) of Rule 12 of Companies (Accounts) Rules, 2014

Within 30 Days From Conclusion Of AGM

29/10/2020 (In Most Of The Cases) (In Case where AGM Date is 30/09/2020)

AOC-4 CFS Form for filing consolidated financial statements and other Documents with the Registrar.

Pursuant to section 137 of the Companies Act, 2013 and Rule 12 of the Companies (Accounts) Rules, 2014

Within 30 Days From Conclusion Of AGM

29/10/2020 (In Most Of The Cases) (In Case where AGM Date is 30/09/2020)

AOC-4 XBRL (FOR FY-2019-20)

Form for filing XBRL document in respect of financial statement and other documents with the Registrar

Pursuant to section 137 of the Companies Act, 2013 and rule 12(2) of the Companies (Accounts) Rules,2014

Within 30 Days From Conclusion Of AGM

29/10/2020 (In Most Of The Cases) (In Case where AGM Date is 30/09/2020) (In case CFS is Applicable to such companies than XML of CFS shall be attached in Form AOC-4 XBRL)

5

FORM MR-3 (FOR FY- 2019-20)

Submission of Secretarial Audit Report along with the Board Report when: Its total Paid- up capital is equal to or crosses Rs.50 crore or Its annual turnover is equal to or exceeds Rs 250 crore.

Section 204 of Companies Act, 2013 to be read with Rule 9 of The companies (Appointment and Remuneration Personnel) Rules, 2014.

To Be Submitted Along With Board Report As An Attachment In AOC-4 (XBRL).

To Be Submitted Along With Board Report As An Attachment In AOC-4 (XBRL).

MGT-7 Annual Return Pursuant to sub-Section(1) of section 92 of the Companies Act, 2013 and sub-rule (1) of rule 11ofthe Companies(Management andAdministration)Rules, 2014.

Within 60 Days From Conclusion Of AGM

28/11/2020 (In Most Of The Cases) (In Case where AGM Date is 30/09/2020)

MGT-8 Certificate By A Company Secretary In Practice In case of a listed company or a company having paid up share capital of Ten Crore rupees or more or turnover of Fifty Crore rupees or More.

Pursuant to section 92(2) of the Companies Act, 2013 and rule 11(2) of Companies (Management and Administration) Rules, 2014.

To Be Submitted To ROC as an Attachment of Form MGT-7.

To Be Submitted To ROC as an Attachment of Form MGT-7.

6

MGT-14 To Be Filed By Public Company After Passing Resolution Of Approval Of Financial Statements And Board Report In Board Meeting.

Pursuant to section 117& 179 of the Companies Act, 2013.

Within 30 Days From Passing Of Board Resolution

Within 30 Days From Passing Of Board Resolution. (2 & 3)

ADT-1 (IF APPLICABLE FOR THE SAID YEAR)

Notice to the Registrar by company for appointment of Auditor

Pursuant to section 139 of the Companies Act, 2013 and Rule 4(2) of the Companies (Audit and Auditors) Rules, 2014.

Within 15 Days From Conclusion Of AGM (In Case AGM where Date is 30/09/2020)

14/10/2020 (Same)

CRA-2 Form of intimation of appointment of cost auditor by the company to Central Government

Pursuant to section 148(3) of Companies Act, 2013 and rule 6 (2) & 6 (3A) of the Companies (cost records and audit) Rules, 2014.

Within a period of 30 days of the Board meeting in which such appointment is made or within 180 days of the commencement of the financial year, whichever is earlier.

Within a period of 30 days of the Board meeting in which such appointment is made or within 180 days of the commencement of the financial year, whichever is earlier. (Same)

CRA-4 Form for filing Cost Audit Report with the Central Government

Pursuant to section 148(6) of Companies Act, 2013 and rule 6(6) of the Companies (cost records and audit) Rules, 2014

Within 30 Days From Receipt Of Cost Audit Report

Within 30 Days From Receipt Of Cost Audit Report (Same)

PAS-6 Form for Reconciliation of Share Capital Audit Report on half yearly basis.

Pursuant to rule 9A(8) of the Companies (Prospectus and Allotment of Securities) Rules, 2014.

The form is to be filed half yearly and within 60 days from the date of deployment of form on Website of MCA.

The form is to be filed half yearly and within 60 days from the date deployment of form on Website of MCA. (Same) (4)

7

Note:

(Due Dates Of Forms Are Extended Pursuant To The Below Mentioned Circulars)

Pursuant to update by Ministry of Corporate Affairs dated 31st March, 2020 & Pursuant to General Circular No. 11 dated 24th March, 2020 & General Circular No. 12 dated 30th March 2020.

The following measures have been implemented for:

o ➡Disqualified/ Deactivated DIN: DIN holders of DINs marked as ‘Deactivated’ due to non-filing of DIR-3KYC/DIR-3 KYC-Web are encouraged to become compliant once again without any filing fee of INR 5000/- but by Filling Form DIR-3KYC/DIR-3 KYC-Web before 30th September,2020.

General Circular No. 12 dated 30th March 2020

List of Forms-CFSS, 2020 & LLP Modified Settlement Scheme 2020

General Circular No. 16/2019 dated 28th November, 2019 regarding Form PAS-6.

♦ Compliances to Newly Incorporated Companies

(For Numbers Mentioned After date refer Notes Mentioned Below)

Name Of Form

Description Of The Form

Provisions Pursuant To Which The Form Is Being Filed

Original Due Date

Extended/Last Due Date

INC-20A Declaration for commencement of business

Pursuant to Section 10A(1)(a) of the Companies Act, 2013 and Rule 23A of the Companies (Incorporation) Rules, 2014.

Within 180 Days Of Incorporation

Within 360 Days Of Incorporation {180+180 (Extended Due To Covid-19)} (5)

ADT-1 Notice to the Registrar by company for appointment of auditor

Pursuant to section 139 of the Companies Act,2013 and Rule 4(2) of the Companies (Audit and Auditors) Rules, 2014.

Within 15 Days Of Appointment Of 1st Auditor.

Within 15 Days Of Appointment Of 1st Auditor.

Note:

(Due Dates Of Forms Are Extended Pursuant To The Below Mentioned Circulars)

5 Point no. 6 of General Circular No. 11 dated 24th March, 2020

8

♦ Yearly Compliances for Limited Liability Partnerships

(For Numbers Mentioned After date refer Notes Mentioned Below)

Name Of Form

Description Of The Form

Provisions Pursuant To Which The Form Is Being Filed

Original Due Date

Extended/Last Due Date

LLP-11 Annual Return of Limited Liability Partnership (LLP)

Pursuant to rule 25(1) of Limited Liability Partnership Rules, 2009.

30/05/2020 30/09/2020 (6 & 7)

LLP-8 Statement of Account & Solvency

Pursuant to rule 24 of Limited Liability Partnership Rules, 2009.

30/10/2020 30/10/2020 (Same)

Note:

(Due Dates Of Forms Are Extended Pursuant To The Below Mentioned Circulars)

UPDATES IN CORPORATE LAWS

Relaxation on levy of additional fees in filing certain forms under CA, 2013 and LLP Act, 2008 Circular dated May 03, 2021 MCA has provided relaxation on levy of additional fees for filing of certain forms (other than the charge related forms) having due dates between April 01, 2021andMay 31, 2021.These form scan now be filed upto July 31, 2021without levy of additional fees

Relaxation of time for filing Charge Forms under Companies Act, 2013 Circular dated May 03, 2021 The Ministry has also notified that the period between April 01, 2021andMay 31, 2021shall not be reckoned for the purpose of counting the number of days under section 77 & 78 of the Act for the charge related forms i.e CHG-1 and CHG-9 filed by the company or the charge holder. The said relaxation would also apply in such cases, where the date of creation or modification of charge is before 1st April 2021 but the timeline for such form had not expired under Section 77 as on 1st April 2021.

Relaxation w.r.t. gap between two Board Meetings

9

Circular dated May 03, 2021 The MCA vide another circular dated May 03, 2021, extended the interval of 120 days for holding Board meetings as provided in section 173 of the Companies Act, 2013 by a period of 60 days i.e effectively the gap between 2 board meetings may extend to 180 days instead of 120 days. The relaxation has been provided for the board meetings to be held in the 1stquarter ending June 30, 2021 and 2ndquarter ending September 30, 2021.

CSR Expenditure (Section 135 of the Companies Act. 2013)

Amount to be contributed as specified under Companies Act, 2013?

Section 135 provides that the companies, which are mandatorily required to spend towards CSR, shall spend at least 2% of their Average Net Profit (Calculated under section 198, and shall be exclusive of such sums as provided under CSR rules) of the preceding 3 Financial Years. However, if 3 FY are not completed since incorporation then average of profit earned during such period.

Set off if more than 2% contributed?

If a Company spends more than 2% in any FY then such excess can be set off in the immediate next 3 FY against the amount required to be contributed under Section 135 of the Companies Act, 2013 in the Succeeding years.

If not contributed or amount remains unspent other than in case of ongoing projects?

Failure to spend shall be explained by the Board in its Report under Section 134, and transfer such unspent amount, within 6 months of the end of FY, to a fund specified under Schedule VII.

Amount remain unspent in case of ongoing project?

“Ongoing Project” means a multi-year project undertaken by a Company in fulfillment of its CSR obligation having timelines not exceeding three years excluding the financial year in which it was commenced, and shall include such project that was initially not approved as a multi-year project but whose duration has been extended beyond one year by the board based on reasonable justification.”

Amount remain unspent on account of Multi-Year project shall be transferred to the “UNSPENT CSR ACCOUNT” within 30 days form the end of Financial year, and which can be spend within 3 FY.

If amount remain unspent even after aforementioned 3 FY, then such amount shall be transferred to the fund as specified under Schedule VII within a period of 30 days from the end of 3rd FY.

10

Administrative Overheads?

“Administrative overheads” means the expenses incurred by the company for general management and administration of Corporate Social Responsibility functions in the company but shall not include the expenses directly incurred for the designing, implementation, monitoring, and evaluation of a particular Corporate Social Responsibility project or programme.”

Administrative overheads shall not exceed 5% of the Total CSR amount for the Financial Year.

Creation and acquisition of Capital Assets?

Yes, a Company can spend CSR amount for the above assets, but such asset shall be held by:

(a) a company established under section 8 of the Act, or a Registered Public Trust or Registered Society, having charitable objects and CSR Registration Number under sub-rule (2) of rule 4; or

(b) Beneficiaries of the said CSR project, in the form of self-help groups, collectives, entities; or

(c) a public authority:

Deduction under Income Tax Act?

Section 37 of the Income Tax Act, 1961 categorically refuses to provide any deduction of the amount spent as CSR under Section 135 of the Companies Act, 2013.

However, if amount spent under CSR falls under section 30-36 of the Income Tax Act, 1961 then such expenditure shall be allowed to be deducted.

Social Security relief to dependents of Workers Passed away due to Covid-19

The Ministry of Labour and Employment has announced social security reliefs to the dependents of the workers who passed away due to Covid.

The enhanced social security is sought to be provide without any additional financial burden to the employers.

1. Employees State Insurance Act 1948 (E S I C): –

At present for the insured person under ESIC, after death or disablement of the insured person due to employment injury, a pension equivalent to 90% of the average daily wage drawn by the insured person is available to the spouse and widowed mother for life long and

11

for children till they attain the age of 25 years. For the female child the benefit is available till her marriage.

Amendment –

To support the families of the insured person under the ESIC scheme, all dependent family members of insured person who have been REGISTERED in the online portal of ESIC prior to their diagnosis of COVID disease and subsequent death due to the Covid disease, will be entitled to receive the same benefits and in the same scale as received by the dependents of insured person who die as a result of employment injury subject to following conditions,

– The insured person must have been REGISTERED on the ESIC portal at least THREE MONTHS PRIOR to the diagnosis of Covid disease resulting in death.

– The insured person must have been employed for wages and contributions for at least 78 days should have been paid or payable in respect of deceased insured person during a period of one year immediately preceding the diagnosis of Covid disease resulting in death.

The insured person who fulfils the eligibility conditions and have died due to Covid disease their dependents will be entitled to receive the MONTHLY PENSION equivalent to 90% of the average daily wage of the insured person during their life.

The scheme will be effective for a period of TWO years with effect from 24/03/2020.

2. Employees Provident Fund & Miscellaneous Provisions Act 1948 (EPF): –

Under the Employees Deposit Linked Insurance Scheme, all surviving family members of the deceased employee of this scheme are eligible to minimum benefit of Rs.2.5 lakhs and maximum Rs.6 lakhs provided the deceased employee was in employment for a continuous period of 12 months in same establishment preceding his death.

Amendment –

– The amount of maximum benefit under Employees Deposit Linked Insurance Scheme (EDLI) increase from Rupees Six Lakhs to Rupees Seven Lakhs to the family members of the deceased employee.

– Minimum assurance benefit of Rupees 2.5 Lakhs to the eligible family members of the deceased employee who was a member for a continuous period of 12 months in one or more establishments preceding his death in place of existing provision of continuous employment in the same establishment for 12 months.

It will benefit the contractual / casual workers who were losing out on benefits due to the condition of one year in one establishment.

– Restoration of provision of minimum Rs.2.5 Lakhs compensation retrospectively with effect from 15th February 2020 for THREE years.

12

Updates in Direct Tax (Income Tax) Laws Launch of new e-filing Portal of the Income Tax Department - Non-availability of e-filing services from 01.06.2021 to 06.06.2021 The Income Tax Department is going to launch its new e-filing portal www.incometax.gov.in on 7th June, 2021. The new e-filing portal (www.incometax.gov.in) is aimed at providing taxpayer convenience and a modern, seamless experience to taxpayers: • New taxpayer friendly portal integrated with immediate processing of Income Tax Returns (ITRs) to issue quick refunds to taxpayers; • All interactions and uploads or pending actions will be displayed on a single dashboard for follow-up action by taxpayer; • Free of cost ITR preparation software available online and offline with interactive questions to help taxpayers fill ITR even without any tax knowledge, with prefilling, for minimizing data entry effort; • New call center for taxpayer assistance for immediate answers to taxpayer queries with FAQs, Tutorials, Videos and Chabot/live agent; • All key portal functions on desktop will be available on Mobile App which will be enabled subsequently for full anytime access on mobile network; • New online tax payment system on new portal will be enabled subsequently with multiple new payment options using net banking, UPI, Credit Card and RTGS/NEFT from any account of taxpayer in any bank, for easy payment of taxes. In preparation for this launch and for migration activities, the existing portal of the Department at www.incometaxindiaefiling.gov.in would not be available to taxpayers as well as other external stakeholders for a brief period of 6 days i.e. from 1st June, 2021 to 6th June, 2021. In order to avoid any inconvenience to taxpayers, the Department will not fix any compliance dates during this period. Further, directions have been issued to fix hearing of cases or compliances only from 10th June, 2021 onwards, to give taxpayers time to respond on the new system. If, any hearing or compliance which requires submissions online has been scheduled during this period, the same will be preponed or adjourned and the work items would be rescheduled after this period. The Department has also intimated external entities including Banks, MCA, GSTN, DPIIT, CBIC, GeM, DGFT who avail services of PAN verification etc. about the non-availability of the services and to request them to make arrangements to ensure that their customers/stakeholders are apprised, so that any relevant activity can be completed prior to or after the blackout period. Taxpayers are encouraged to complete all their urgent tasks involving any submission, upload or downloads before 1st June, 2021 to avoid any difficulty during the blackout period. The Department requests the patience of all taxpayers and other stakeholders during the switch over to the new e-filing portal and the subsequent initial period while they get familiarized with the new system. This is another initiative by CBDT towards providing ease of compliance to its taxpayers and other stakeholders.

13

Extension of Time for Intimation of Aadhaar and Certain Other Time Limits In view of the COVID-19 pandemic, certain time limits specified under the various tax and Benami laws have been extended by the Taxation and Other Laws (Relaxation and Amendment of Certain Provisions) Act, 2020 and subsequent notifications issued under this Act. The extended last date for intimating Aadhaar number under the Income-tax Act, 1961 (the Act) for the purposes of linking Aadhaar with PAN is 31st March, 2021. Representations have been received from taxpayers that the last date for intimating the Aadhaar number may further be extended in the wake of the on-going COVID-19 pandemic. Keeping in view the difficulties faced by the taxpayers, the Central Government has issued notification today extending the last date for the intimation of Aadhaar number and linking thereof with PAN to 30th June, 2021. The said notification also extended time-limits for issue of notice under section 148 of the Act, passing of consequential order for direction issued by the Dispute Resolution Panel (DRP) and processing of equalisation levy statements to 30th April, 2021.

Income Tax Refund: A Fiduciary Duty Owed by Department to Assessee Sections 237 and 239 of the Income Tax Act, 1961 deals with the procedure of the refund of the excess income tax paid by the assessee to the revenue department. Section 239 provides for the limitation period of one year within which the assessee should claim his income tax refund. However, this provision is omitted by the 2019 amendment to the Income Tax Act. Now, it creates a diplomatic situation to claim for the refund of the income tax, as from now there is no limitation period available for claiming of such refund. Thus, it gives liberty to the taxpayer to claim his refunds of 10, 20 years back. The Income tax refund usually happens in three situations namely:

a. Self-Assessment b. Tax Deducted at Source (TDS) c. Advance Tax

At present, the procedure of auto calculation is followed as the Income Tax Return (ITR) of the assessee is filed online. The system will auto calculate the refund due to the assessee and an intimation will be send to the taxpayer under Section 143 of the Income Tax Act. This whole procedure is done online after the filing of ITR within the time period prescribed and there is no need on the part of the assessee to claim income tax return on her own. In addition to this, if the assessee is claiming for the refund of previous years he has to file an application for the condonation of delay before the Assessing Officer (AO) under section 5 of the Limitation Act. If the application of the assessee is rejected by the AO, he can file an appeal under Section 260A to the High Court within 120 days of the order of Assessing Officer (AO).

14

However, this appeal will stand maintainable in the High Court if it involves the substantial question of law, otherwise it will get rejected prima facie by the High Court. Thus, the assessee in the case of income tax refund has to frame his case in such a way to make his appeal maintainable in the High Court, if the same is rejected by the AO. Apart from this remedy, there is one more remedy available to the taxpayer. In 2015, a circular was passed by the CBDT with the subject: “Condonation of delay in filing refund claim and claim of carry forward of losses under Section 119(2)(b) of the Income Tax Act.” In this circular the conditions for the condonation and the procedure to be followed is prescribed. These guidelines and conditions are mentioned below: If the amount of claim is upto 50 Lakhs the power of acceptance/rejection of such application will be vested with Principle Commissioner of Income Tax/ Commissioners of Income Tax. If the amount of claim exceeds 50 lakhs such application shall be considered by the board. The limitation period of 6 years from the end of assessment is given under the circular. Thus, an assessee claiming for income tax refund should file such application within the period of 6 years. In Tata Limited Capital 21 case the Supreme Court had discussed in detail the moral and the legal obligations on the part of Income tax department to make the refund of the excess amount due to the taxpayer, along with the interest. The court held that when the collection by the department is illegal there is a corresponding obligation on the part of the revenue to make the refund of such exceeding tax paid by the assessee. Note:

a. Sec. 237: As per this provision if the assessee is able to satisfy the Assessing Officer that the tax which has been paid by him in the previous year exceeds the tax amount which he is actually liable to pay under the Income Tax Act, he shall be given the refund as per the processing of the revenue department.

b. Sec 143: Under this provision, the assessee will receive an intimation from the tax department in case it has been found that any refund is due to the assessee.

c. Sec.119(2)(b): This provision deals with the exemption and grants the power to the Income Tax Authority that in case of un avoidable hardships they can pass any special order which would solve the purpose of such enactment.

15

Updates in Indirect Tax (GST) Laws Availment of ITC for April, May & June, 2021 in June 2021 return In 43rd Meeting of the GST Council, dated 28th May 2021 there is one major relief relating to COVID 19 is provided i.e Cumulative application of rule 36(4) for availing ITC for tax periods April, May and June, 2021 in the return for the period June, 2021. What is the meaning of Cumulative application of rule 36(4) for availing ITC for tax periods April, May and June, 2021 in the return for the period June, 2021? Before understanding this relaxation, we should know about Rule 36(4) which provides Maximum ITC that can be taken in return period is ITC which is reflected in GSTR 2B relating to that return period plus 5% i.e. If Rs. 100000 is reflected in Jan 2B then maximum ITC will be Rs. 105000 in January month. Now even if recipient has actual GST on invoice basis Rs. 200000, he can take only Rs. 105000 and next 95000 will be available when supplier will upload return which results into blocking of money for few months. Now as per relaxation provided we need not to see April 21 and May 21 GSTR 2B, we can take Credit as per Invoice basis that is by ignoring rule 36(4). Now when we come in June month we need to take all three months GSTR 2B plus 5% that can be maximum cumulative ITC for April, May and June Month. Now suppose after totalling of ITC in GSTR 2B for three months comes to Rs. 500000 and we have taken rs. 400000 already in April and May month then max ITC that can be taken in June month is Rs. (500000 plus 5%) -Rs. 400000 I. E Rs. 125000. In case if we have already taken rs. 600000 in two months then in June 21 we need to reverse Rs. 600000-525000 = Rs. 75000. In case of any query you can be reached at [email protected]

GST Applicability on Branded Cereals India had been agriculture based economy and the sector has significant contribution in GDP as well in terms of generation of employment. Monsoon has always played a crucial role in the health of economy in any financial year. However, being the core sector for the human needs and survival, the intention of the government has always been to provide the relief in the taxation, at least to the raw agriculture products and activities. In India, different kind of cereals i.e. wheat, rice, millet, barley, ragi etc are being produced. These raw agriculture products are subject to various processes before they reach to consumer for consumption. Primary processing involves several different processes, designed to clean, sort and remove the inedible fractions from the grains. Primary processing of cereals includes cleaning, grading, hulling, milling, pounding, grinding, tempering, parboiling, soaking, drying, sieving. As far as the raw agriculture products are concerned, they were never subject to any kind of direct or indirect taxes. However, for the processed cereals, the exemption as granted in the

16

VAT regime whether the same was sold as branded or unbranded or under any registered name or otherwise. In the present article, we will examine the liability of GST on the supply of processed cereals. As we know, the cereals have been sold in two different manners, where in first condition; these are sold in loose and does not bear any trade name or brand name. For example, one can go and purchase one kg. rice in loose from some grocery shop. There cannot be any GST liability on supply of such unbranded and loose cereals. In today’s consumer oriented market, many suppliers are involved in selling of the cereals under their registered brand name or trade name in unit containers. The association of the brand with product develops the trust to the consumer, which is based on the reputation of the brand name/trade name owner. This trust is in form of quality of the product, where the consumer links the same with the reputation of brand and purchase the product. Vide Notification number 1/2017-Central Tax (Rate) dated 28.06.2017; the cereals have been kept under Schedule-1 with total tax rate of 5% (2.5% CGST + 2.5 % SGST). The relevant entries of the notification is reproduced –

45 10 All goods i.e. cereals, put up in unit container and bearing a registered brand name

46 1001 Wheat and meslin put up in unit container and bearing a registered brand name

47 1002 Rye put up in unit container and bearing a registered brand name 48 1003 Barley put up in unit container and bearing a registered brand name 49 1004 Oats put up in unit container and bearing a registered brand name 50 1005 Maize (corn) put up in unit container and bearing a registered brand

name 51 1006 Rice put up in unit container and bearing a registered brand name 52 1007 Grain sorghum put up in unit container and bearing a registered

brand name 53 1008 Buckwheat, millet and canary seed; other cereals such as Jawar,

Bajra, Ragi] put up in unit container and bearing a registered brand name

Further in notification number 2/2017-Central Tax (rate), the exemption has been extended to the goods covered in chapter 10 on fulfilling of certain conditions-

65 1001 Wheat and meslin [other than those put up in unit container and bearing a registered brand name]

66 1002 Rye [other than those put up in unit container and bearing a registered brand name]

67 1003 Barley [other than those put up in unit container and bearing a registered brand name]

17

68 1004 Oats [other than those put up in unit container and bearing a registered brand name]

69 1005 Maize (corn) [other than those put up in unit container and bearing a registered brand name]

70 1006 Rice [other than those put up in unit container and bearing a registered brand name]

71 1007 Grain sorghum [other than those put up in unit container and bearing a registered brand name]

72 1008 Buckwheat, millet and canary seed; other cereals such as Jawar, Bajra, Ragi] [other than those put up in unit container and bearing a registered brand name]

Amendments in exemptions from GST on donation of covid relief materials With the second wave of the ongoing pandemic, Government of India has taken remarkable steps on the war footing basis to make the life-saving materials available in the country from across the globe with the continuous support of all the Ministries and their respective departments and the Corporate houses, Charitable Organisation, NGOs, etc. Unlike the first wave where even the basic materials were not available like masks, sanitizers, PPE kits, etc., in the current second wave India is equipped with all these, however, with the requirement of life saving materials, adequate and timely steps have been taken to import these materials like oxygen cylinders, oxygen concentrators, vaccines, etc. From the perspective of taxation, exemptions from taxation have been given by the CBIC from Customs duty, Health Cess and IGST on many such items. Few notifications have been regarding the exemption which has been dealt below along-with the procedural requirement. It is important to note that exemptions have been given on import of only those items whose availability are not in adequate quantity in India, therefore, one may find masks, sanitizers, PPE kits, oximeter, thermometer, Test kit, etc. not been exempted from these taxes. Customs duty and health cess exemption Notification No. 27/2021–Customs New Delhi, the 20th April, 2021: The notification exempts Customs duty &/or Health Cess and is applicable till 31st October, 2021. The same is applicable on following goods: Remdesivir Active Pharmaceutical Ingredients; Beta Cyclodextrin (SBEBCD) used in manufacture of Remdesivir, subject to the condition that the importer follows the procedure set out in the Customs (Import of Goods at Concessional Rate of Duty) Rules, 2017; Injection Remdesivir. Notification No. 28/2021–Customs dated 24th April, 2021 further amended vide Notification No. 31/2021–Customs dated 31st May, 2021: The notification exempts Customs duty &/or Health Cess and is applicable till 31st July, 2021 which has been further

18

extended till 31st August, 2021 as per the decision taken in 43rd GST Council Meeting. The same is applicable on following goods:

S.No. Chapter, heading, sub-heading or tariff item

Description

(1) (2) (3) 1. 9019 20, 9804 Oxygen concentrator including flow meter, regulator,

connectors and tubings. [Important Note: For commercial use 9804, For personal use (Courier/FPO) 9804]

2. 2804 40 Medical Oxygen 3. 8421 39 Vacuum Pressure Swing Absorption (VPSA) and Pressure Swing

Absorption (PSA) oxygen plants, Cryogenic oxygen Air Separation Units (ASUs) producing liquid/gaseous oxygen.

4. 7311 Oxygen canister. 5. 9018 Oxygen filling systems. 6. 7311 Oxygen storage tanks 7. 9018 Oxygen generator 8. 7311 ISO containers for Shipping Oxygen 9. 7311, 8418 or 8419 Cryogenic road transport tanks for Oxygen

10. 7311, 8418 or 8419 Oxygen cylinders including cryogenic cylinders and tanks

11.

Any Chapter

Parts of goods at S.No.1 and 3 to 10 above, used in the manufacture of equipment related to the production, transportation, distribution or storage of Oxygen, subject to the condition that the importer follows the procedure set out in the Customs (Import of Goods at Concessional Rate of Duty) Rules, 2017.

12. 9019 Any other device from which oxygen can be generated 13. 9018 or 9019 Ventilators, including ventilator with compressors; all

accessories and tubing’s; humidifiers; viral filters (should be able to function as high flow device and come with nasal cannula).

14. 9018 High flow nasal cannula device with all attachments; nasal cannula for use with the device.

15. 6506 99 00 Helmets for use with non-invasive ventilation. 16. 9019 Non-invasive ventilation or nasal masks for ICU ventilators.

17. 9019 Non-invasive ventilation nasal masks for ICU ventilators. 18. 3002 COVID-19 vaccine.

19

19. 29 or 30 Amphotericin B. [Note: The medicine Amphotericin B required for treatment of Black Fungus has been decided to be included in the exemption list in 43rd GST Council Meeting on 28th May, 2021. Basis which the same has been inserted as Sl. No. 19 vide Notification No. 31/2021-Customs dated 31st May, 2021.]

IGST Exemption Notification No. 30/2021-Customs New Delhi, the 1st May, 2021: The notification reduced the rate of tax of IGST to 12% on Oxygen concentrator, imported for personal use and is applicable till 30th June, 2021. It is worthwhile to note that the levy of GST on import for personal use when received as gift is challenged before the Hon’ble High Courts of Delhi as well as Bombay wherein the former has held that the imposition of IGST on the import of oxygen concentrators as gift for personal use is unconstitutional in the case of Gurcharan Singh vs UOI which was challenged primarily on the grounds of Article 14 and 21 of the Constitution of India and in order to bring a parity with the commercial purpose where the Government has already given adhoc exemption. Ad hoc Exemption Order No. 4/2021-Customs dated 3rd May, 2021 read with Instruction No. 09/2021-Customs dated 3rd May, 2021: The notification exempts IGST and is applicable till 30th June, 2021. It is pertinent to note that the exemption order shall apply to all the consignments pending clearance from Customs as on date of issue of order, i.e., the 3rd May, 2021. It is important to note that as per the decision taken in 43rd GST Council Meeting held on 28th May, 2021, the said adhoc exemption has been further extended till 31st August, 2021 vide Ad hoc Exemption Order No. 5/2021-Customs dated 31st May, 2021. The same is applicable on goods covered under the said mentioned below subject to the conditions of approval from Nodal Authority appointed in States and its usage: Notification No. 27/2021-Customs, dated the 20th April, 2021 Notification No. 28/2021-Customs, dated the 24th April, 2021

Checklist for GSTR-9 (Due Date – 31st December of next F.Y.) Before going to file the GSTR-9 annual return, we should have several data ready with us to provide in the annual return. 1. List of tax invoices (Taxable, Exempted & Non- GST Supplies) issued during the period in Excel which is matched with total sales of the tally and turnover declared in the audited financial statements. 2. List of tax invoices (Taxable, Exempted & Non- GST Supplies) reflected in GSTR-1. Details of monthly total outward supplies reflected in GSTR-1

20

3. Details of monthly total outward supplies (Taxable, Exempted & Non- GST Supplies) reflected in GSTR-3b 4. Reconciliation of E-Way bill data with the tax invoices (Taxable, Exempted & Non- GST Supplies) issued during the period GSTIN state wise 5. Points 1, 2, 3 and 4 must be matched with each other if there is any discrepancy then reasons must be identifiable. 6. List of Invoices on which RCM was applicable and considered in Financial Statements. 7. List of Invoices on which RCM was paid during the year. 8. Points 6 and 7 must be matched with each other if there is any discrepancy then reasons must be identifiable. 9. Reconciliation of advances received and GST paid for Services. 10. List of debit/credit notes issued during the period and reconciliation of the same with books of 11. In case company has the different units/branch all over India, then the stock transfer between units/branches also to be reconciled with the books. 12. Reconciliation discount given to the customer with purpose and recheck if the same under GST act allowed or not. 13. List of Invoices in specified format on which ITC has been claimed which is matched with the tally and the audited financial statements (Specified format attached herewith). 14. Details of monthly ITC claimed in GSTR-3b 15. Ensure all the input credit taken bills are uploaded by the suppliers and it is reflecting in the GSTR-2A. 16. Points 13, 14 and 15 must be matched with each other if there is any discrepancy then reasons must be Identifiable. 17. Ensure all the availed credits are eligible as per the act and the ineligible credits, common credits are reversed & accounted properly. 18. Check and ensure input credit taken on supplier invoices paid within 180 days, if not the same input to be reversed along with interest @18% p.a. 19. All the credit taken on TRAN-1 credit reflecting in the GST portal

21

20. List of Amendments of outward supplies made in GSTR-1 and GSTR-3B till the month of September following the end of financial year. 21. List of Amendments of Inward supplies made in GSTR-3B till the month of September following the end of financial year. 22. Calculate the Tax Liability due to amendments and make DRC-3 for the payment along with interest @18% p.a. 23. Details of GST refund / demands during the year. 24. List of Goods/ Capital goods transferred to the Job Worker. 25. List of supplies received from composition tax payers 26. List of goods sent on approval basis but not returned. 27. List of HSN wise summary of outward supplies. 28. List of HSN wise summary of inward supplies. 29. File by attaching the DSC of the Tax Payer.

Highlights of 43rd GST Council meeting Recommendations of 43rd GST Council meeting COVID-19 related medical goods including Amphotericin B for free distribution given full exemption from IGST upto 31.08.2021 Custom duty exemption also given to Amphotericin B Amnesty Scheme to provide relief to taxpayers regarding late fee for pending returns; late fee also rationalised for future tax periods Simplification of Annual Return for Financial Year 2020-21 Posted On: 28 MAY 2021 The 43rd GST Council met under the Chairmanship of Union Finance & Corporate Affairs Minister Smt. Nirmala Sitharaman through video conferencing here today. The meeting was also attended by Union Minister of State for Finance & Corporate Affairs Shri Anurag Thakur besides Finance Ministers of States & UTs and senior officers of the Ministry of Finance & States/ UTs. The GST Council has made the following recommendations relating to changes in GST rates on supply of goods and services and changes related to GST law and procedure: COVID-19 RELIEF As a COVID-19 relief measure, a number of specified COVID-19 related goods such as medical oxygen, oxygen concentrators and other oxygen storage and transportation equipment, certain diagnostic markers test kits and COVID-19 vaccines, etc., have been recommended for

22

full exemption from IGST, even if imported on payment basis, for donating to the government or on recommendation of state authority to any relief agency. This exemption shall be valid upto 31.08.2021. Hitherto, IGST exemption was applicable only when these goods were imported “free of cost” for free distribution. The same will also be extended till 31.8.2021. It may be mentioned that these goods are already exempted from Basic Customs duty. Further in view of rising Black Fungus cases, the above exemption from IGST has been extended to Amphotericin B. Further relief in individual item of COVID-19 after Group of Ministers (GoM) submits report on 8th June 2021 As regards individual items, it was decided to constitute a Group of Ministers (GoM) to go into the need for further relief to COVID-19 related individual items immediately. The GOM shall give its report by 08.06.2021. OTHER RELIEFS ON GOODS

a. To support the LympahticFilarisis (an endemic) elimination programme being conducted in collaboration with WHO, the GST rate on Diethylcarbamazine (DEC) tablets has been recommended for reduction to 5% (from 12%).

b. Certain clarifications/clarificatory amendments have been recommended in relation to GST rates. Major ones are, – Liveability of IGST on repair value of goods re-imported after repairs GST rate of 12% to apply on parts of sprinklers/ drip irrigation systems falling under tariff heading 8424 (nozzle/laterals) to apply even if these goods are sold separately.

SERVICES

a. To clarify those services supplied to an educational institution including anganwadi(which provide pre-school education also), by way of serving of food including mid- day meals under any midday meals scheme, sponsored by Government is exempt from levy of GST irrespective of funding of such supplies from government grants or corporate donations.

b. To clarify these services provided by way of examination including entrance examination, where fee is charged for such examinations, by National Board of Examination (NBE), or similar Central or State Educational Boards, and input services relating thereto are exempt from GST.

c. To make appropriate changes in the relevant notification for an explicit provision to make it clear that land owner promoters could utilize credit of GST charged to them by developer promoters in respect of such apartments that are subsequently sold by the land promoter and on which GST is paid. The developer promoter shall be allowed to pay GST relating to such apartments any time before or at the time of issuance of completion certificate.

d. To extend the same dispensation as provided to MRO units of aviation sector to MRO units of ships/vessels so as to provide level playing field to domestic shipping MROs vis a vis foreign MROs and accordingly, –

e. GST on MRO services in respect of ships/vessels shall be reduced to 5% (from 18%). f. PoS of B2B supply of MRO Services in respect of ships/ vessels would be location of

recipient of service

23

g. To clarify that supply of service by way of milling of wheat/paddy into flour (fortified with minerals etc. by millers or otherwise )/rice to Government/ local authority etc.for distribution of such flour or rice under PDS is exempt from GST if the value of goods in such composite supply does not exceed 25%. Otherwise, such services would attract GST at the rate of 5% if supplied to any person registered in GST, including a person registered for payment of TDS.

h. To clarify that GST is payable on annuity payments received as deferred payment for construction of road. Benefit of the exemption is for such annuities which are paid for the service by way of access to a road or a bridge.

i. To clarify those services supplied to a Government Entity by way of construction of a rope-way attract GST at the rate of 18%.

j. To clarify that services supplied by Govt. to its undertaking/PSU by way of guaranteeing loans taken by such entity from banks and financial institutions is exempt from GST.

COVID-19 related relief measures for taxpayers: In addition to the relief measures already provided to the taxpayers vide the notifications issued on 01.05.2021, the following further relaxations are being provided to the taxpayers: A. For small taxpayers (aggregate turnover upto Rs. 5 crore)

a. March & April 2021 tax periods: i. NIL rate of interest for first 15 days from the due date of furnishing the

return in FORM GSTR-3B or filing of PMT-06 Challan, reduced rate of 9% thereafter for further 45 days and 30 days for March,2021 and April, 2021 respectively.

ii. Waiver of late fee for delay in furnishing return in FORM GSTR-3B for the tax periods March / QE March, 2021 and April 2021 for 60 days and 45 days respectively, from the due date of furnishing FORM GSTR-3B.

iii. NIL rate of interest for first 15 days from the due date of furnishing the statement in CMP-08 by composition dealers for QE March 2021, and reduced rate of 9% thereafter for further 45 days.

b. For May 2021 tax period: i. NIL rate of interest for first 15 days from the due date of furnishing the

return in FORM GSTR-3B or filing of PMT-06 Challan, and reduced rate of 9% thereafter for further 15 days.

ii. Waiver of late fee for delay in furnishing returns in FORM GSTR-3B for taxpayers filing monthly returns for 30 days from the due date of furnishing FORM GSTR-3B.

B. For large taxpayers (aggregate turnover more than Rs. 5 crore) i. A lower rate of interest @ 9% for first 15 days after the due date of

filing return in FORM GSTR-3B for the tax period May, 2021. ii. Waiver of late fee for delay in furnishing returns in FORM GSTR-3B for

the tax period May, 2021 for 15 days from the due date of furnishing FORM GSTR-3B.

24

C. Certain other COVID-19 related relaxations to be provided, such as 1. Extension of due date of filing GSTR-1/ IFF for the month of May 2021 by 15 days. 2. Extension of due date of filing GSTR-4 for FY 2020-21 to 31.07.2021. 3. Extension of due date of filing ITC-04 for QE March 2021 to 30.06.2021. 4. Cumulative application of rule 36(4) for availing ITC for tax periods April, May and

June, 2021 in the return for the period June, 2021. 5. Allowing filing of returns by companies using Electronic Verification Code (EVC),

instead of Digital Signature Certificate (DSC) till 31.08.2021.

D. Relaxations under section 168A of the CGST Act: Time limit for completion of various actions, by any authority or by any person, under the GST Act, which falls during the period from 15th April, 2021 to 29th June, 2021, to be extended up to 30th June, 2021, subject to some exceptions.

[Wherever the timelines for actions have been extended by the Hon’ble Supreme Court, the same would apply] 4. Simplification of Annual Return for Financial Year 2020-21:

a. Amendments in section 35 and 44 of CGST Act made through Finance Act, 2021 to be notified. This would ease the compliance requirement in furnishing reconciliation statement in FORM GSTR-9C, as taxpayers would be able to self-certify the reconciliation statement, instead of getting it certified by chartered accountants. This change will apply for Annual Return for FY 2020-21.

b. The filing of annual return in FORM GSTR-9 / 9A for FY 2020-21 to be optional for taxpayers having aggregate annual turnover up to Rs 2 Crore;

c. The reconciliation statement in FORM GSTR-9C for the FY 2020-21 will be required to be filed by taxpayers with annual aggregate turnover above Rs 5 Crore.

d. Retrospective amendment in section 50 of the CGST Act with effect from 01.07.2017, providing for payment of interest on net cash basis, to be notified at the earliest.

Latest Updates in SEBI

Off-market transfer of securities by FPI

1. The Finance Act, 2021 provides tax Incentives for relocating foreign funds to International Financial Services Centre (IFSC) in order to make the IFSC in GIFT City a global financial hub.

2. In view of the above objective and to further facilitate such ‘relocation’, it has been decided that a FPI (‘original fund ‘or its wholly owned special purpose vehicle) may approach its DDP for approval of a one-

3. Time ‘off-market’ transfer of its securities to the ‘resultant fund’. The terms ‘original fund’, ‘relocation’ and ‘resultant fund’ will have the same meaning as assigned to them under the Finance Act, 2021.

4. The DDP after appropriate due diligence may accord its approval for a one-time ‘off-market’ transfer of securities for such relocation.

25

5. Relocation request will imply that the FPI has deemed to have applied for surrender of its registration and the DDP may be guided by the guidelines pertaining to surrender of FPI registration.

6. The ‘off-market’ transfer shall be allowed without prejudice to any provisions of tax laws and FEMA.

7. Para 3, Part C of SEBI Circular No. IMD/FPI&C/CIR/P/2019/124 dated November 05, 2019 stands modified to the extent of para 2 above.

8. DDPs and Custodians are requested to bring the contents of this circular to the notice of their clients.

9. The circular is issued in exercise of powers conferred under Section 11(1) of the Securities and Exchange Board of India Act, 1992.

10. A copy of this circular is available at the web page “Circulars” on our website 11. www.sebi.gov.in

Relaxation in compliance with requirements pertaining to AIFs and VCFs

1. SEBI in receipt of representation from AIF Industry, requesting extension of timelines for various regulatory filings and compliances for AIFs and VCFs, due to ongoing second wave of the CoVID-19 pandemic and restrictions imposed by various state governments.

2. After consideration, it has been decided to extend the due dates for regulatory filings by AIFs and VCFs, during the period ending March 2021toJuly2021 as prescribed under SEBI (Alternative Investment Funds) Regulations, 2012 and circulars issued there under. AIFs and VCFs may submit regulatory filings for the aforesaid periods, as applicable, on or before September 30, 2021.

3. This Circular is issued in exercise of powers conferred under Section 11(1) of the Securities and Exchange Board of India Act, 1992, to protect the interest of investors in securities and to promote the development of, and to regulate the securities market. This Circular shall come into force with immediate effect.

4. This Circular is available on SEBI website at www.sebi.gov.in under the categories “Legal Framework” and under the drop down “Circulars” and "Info for -Alternative Investment Funds”.

Format of compliance report on Corporate Governance by Listed Entities

1. As per the provisions of Regulation 27(2) of Securities and Exchange Board of India (Listing Obligations and Disclosure Requirements) Regulations, 2015 (“Listing Regulations”), a listed entity is required to submit a quarterly compliance report on corporate governance in the format specified by the Board from time to time to recognised Stock Exchange(s).

26

2. The format for compliance report on Corporate Governance by listed entities has been specified, as per the following annexures, vide Circular No. CIR/CFD/CMD/5/2015 dated September 24, 2015 and modified vide Circular No. SEBI/HO/CFD/CMD1/CIR/P/2019/78 dated July 16, 2019. Annex -I-on quarterly basis; Annex -II-at the end of a financial year Annex -III-at the end of 6 months from the close of financial year.

3. In order to bring about transparency and to strengthen the disclosures around loans/ guarantees/comfort letters/ security provided by the listed entity, directly or indirectly to promoter/ promoter group entities or any other entity controlled by them, it has been decided to mandate such disclosures on a half yearly basis, in the Compliance Report on Corporate Governance. The format of disclosure in this regard is specified vide Annex –IV of the said report and shall be effective from financial year2021-22.

4. Accordingly the format for compliance report on Corporate Governance shall be as under:

Annex -I-on quarterly basis; Annex -II-at the end of a financial year Annex -III-at the end of 6 months from the close of financial year. Annex-IV-on a half yearly basis (w.e.f. first half year of the FY 21-22)

5. This circular supersedes the aforementioned SEBI Circulars dated September 24, 2015 and July 16, 2019.

6. The Stock Exchanges are advised to bring the provisions of this Circular to the notice of listed entities and also disseminate the same on their websites.

7. This Circular is issued in exercise of the powers conferred under Section 11(1)of the Securities and Exchange Board of India Act, 1992 read with Regulation 101of the Securities and Exchange Board of India (Listing Obligations and Disclosure Requirements) Regulations, 2015.

Disclosure of the following only w.r.t schemes which are subscribed by the investor:

A. Risk-o-meter of the scheme and the benchmark along with the performance disclosure of the scheme vis-à-vis benchmark and B. Details of the portfolio

1. SEBI, vide circular no. SEBI/HO/IMD/IMD-II DOF3/P/CIR/2021/555 dated April 29,

2021, specified disclosures with regard to disclosure of (a) risk-o-meter of the scheme and the benchmark along with the performance disclosure of the scheme vis-à-vis benchmark and (b) details of portfolio, which were applicable from June 01, 2021.

27

2. Based on the representation received from AMFI, it has been decided to extend the implementation date of the provisions of the aforesaid circular to September 1, 2021.

3. This circular is issued in exercise of the powers conferred under Section 11 (1) of the Securities and Exchange Board of India Act 1992, read with the provision of Regulation 77 of SEBI (Mutual Funds) Regulation, 1996 to protect the interests of investors in securities and to promote the development of, and to regulate the securities market.

28

29

CA DURGESH KUMAR KABRAChartered Accountant

Address :-803-804, Ashok Heights, Nicco Circle, Near BhutaSchool,Old Nagardas Road, Gundavali, Andheri East,Mumbai - 400069

PHONE : 022-26824800 / 4900

MOBILE : +91 9869015418

EMAIL : [email protected] [email protected]

Follow me on :

![· co co 40 Illiö % t J O O o o o co o o o co o o IJ o o co +0 a o O O O o . 0) 00 oo co E co co o O co co O co co co co co co o 00 co co o u] co CO](https://img.dokumen.tips/doc/110x75/5b810bdc7f8b9a7b6f8b79f2/-co-co-40-illioe-t-j-o-o-o-o-o-co-o-o-o-co-o-o-ij-o-o-co-0-a-o-o-o-o-o-0.jpg)