Embed Size (px)

Citation preview

6 February 2014

Divya Reddy

Director, Global Energy & Natural Resources

202-903-0017

Global CO2 Policy Challenges and lessons learned

Prepared for The Gasification Technologies Council

Eurasia Group overview:

Founded in 1998, Eurasia Group has offices in New York, Washington, DC,

London, and Tokyo.

Eurasia Group provides consulting and advisory services to corporations,

financial institutions, and government organizations

50+ full-time country and sector experts who are political scientists

Global network of several hundred in-country experts worldwide

1

Prepared for The Gasification Technologies Council

Global Climate Change Policy

I. Multilateral negotiations

II. United States

III. European Emissions Trading System

IV. China

2

Prepared for The Gasification Technologies Council

I: MULTILATERAL NEGOTIATIONS

3

Prepared for The Gasification Technologies Council

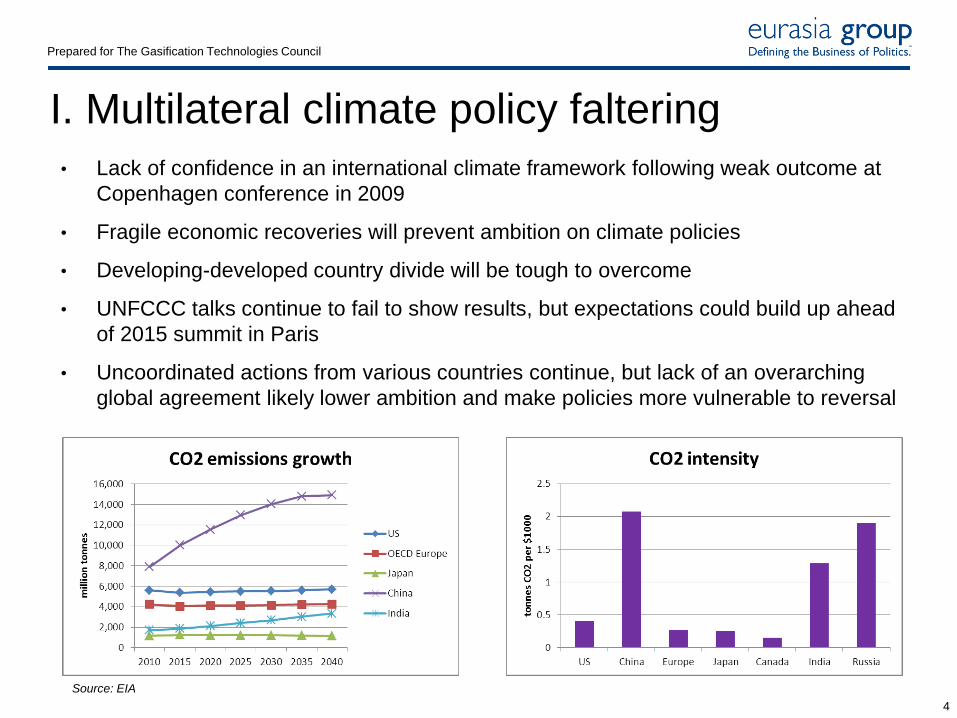

I. Multilateral climate policy faltering

4

• Lack of confidence in an international climate framework following weak outcome at

Copenhagen conference in 2009

• Fragile economic recoveries will prevent ambition on climate policies

• Developing-developed country divide will be tough to overcome

• UNFCCC talks continue to fail to show results, but expectations could build up ahead

of 2015 summit in Paris

• Uncoordinated actions from various countries continue, but lack of an overarching

global agreement likely lower ambition and make policies more vulnerable to reversal

Source: EIA

Prepared for The Gasification Technologies Council

II. UNITED STATES

5

Prepared for The Gasification Technologies Council

Second-term Obama climate policy centered on power

sector regulations

6

• Key component is GHG performance

standards for power plants (New Source

Performance Standards), though standards

for existing plants likely to be modest due

to power reliability concerns

• Stated timeline :

• September 2012: NSPS proposal for new

power plants

• June 2014: NSPS draft rule for existing

power plants

• June 2015: Finalize NSPS for existing plants

• NSPS for new plants to be aggressive and

costly for coal, even though new draft rule

will issue separate standards for coal and

gas plants

Prepared for The Gasification Technologies Council

III: EU EMISSIONS TRADING SCHEME

7

Prepared for The Gasification Technologies Council

EU ETS design overview • Who’s covered: Power and industrial facilities; airlines

• Emissions reduction target: 20% reduction from 1990

levels by 2020

• Basic mechanics:

• Introduce a fixed number of emissions allowances into the market

each year

• Obligated facilities have targets that they can meet by buying

allowances or cutting emissions and selling allowances

• Three phases:

• Phase I (2005-2007)—pilot phase

• Phase II (2008-2012)—Kyoto phase

• Phase III (2013-2020)—current phase 8

Prepared for The Gasification Technologies Council

EU emissions in decline since 1990

9

Source: European Commission

Prepared for The Gasification Technologies Council

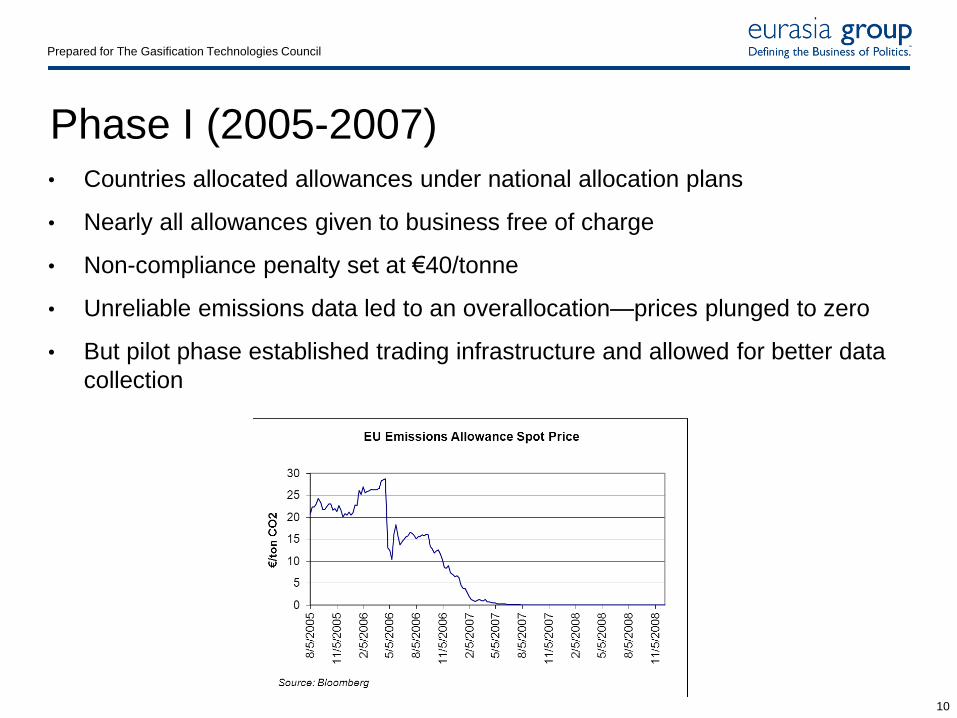

Phase I (2005-2007) • Countries allocated allowances under national allocation plans

• Nearly all allowances given to business free of charge

• Non-compliance penalty set at €40/tonne

• Unreliable emissions data led to an overallocation—prices plunged to zero

• But pilot phase established trading infrastructure and allowed for better data

collection

10

Prepared for The Gasification Technologies Council

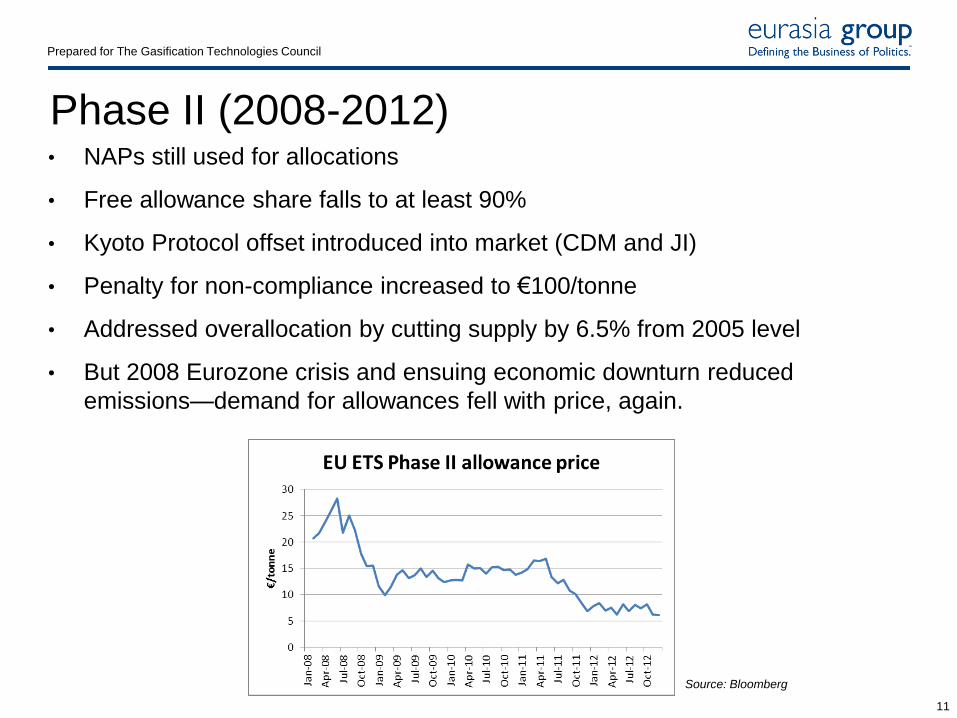

Phase II (2008-2012) • NAPs still used for allocations

• Free allowance share falls to at least 90%

• Kyoto Protocol offset introduced into market (CDM and JI)

• Penalty for non-compliance increased to €100/tonne

• Addressed overallocation by cutting supply by 6.5% from 2005 level

• But 2008 Eurozone crisis and ensuing economic downturn reduced

emissions—demand for allowances fell with price, again.

11

Source: Bloomberg

Prepared for The Gasification Technologies Council

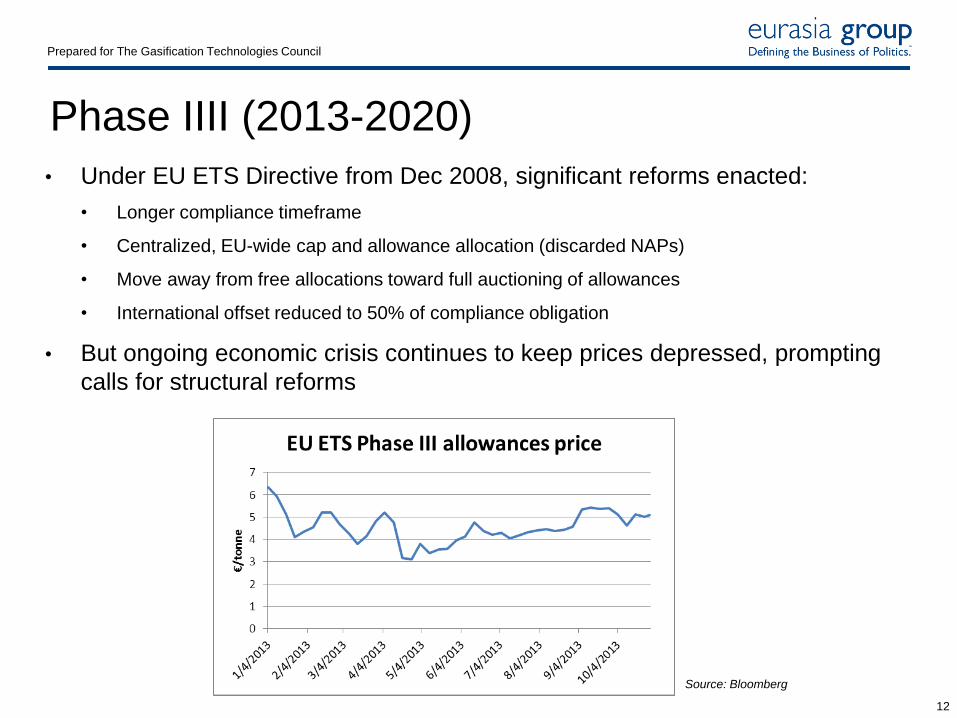

Phase IIII (2013-2020)

• Under EU ETS Directive from Dec 2008, significant reforms enacted:

• Longer compliance timeframe

• Centralized, EU-wide cap and allowance allocation (discarded NAPs)

• Move away from free allocations toward full auctioning of allowances

• International offset reduced to 50% of compliance obligation

• But ongoing economic crisis continues to keep prices depressed, prompting

calls for structural reforms

12

Source: Bloomberg

Prepared for The Gasification Technologies Council

EU ETS in practice: Challenges • Price fluctuations: Data deficiencies and changes in economic outlook created major price swings

• Government intervention: The low carbon price has prompted efforts to intervene in the market to

prop up prices

• Carbon leakage: As energy-intensive industrial facilities see free allocations phased out, concerns

over carbon leakage will grow and could prompt renewed calls for a border carbon price for imports

• Energy costs: The issue of Europe losing competitiveness in manufacturing is becoming more

salient, and the ETS is in the crosshairs as a contributing factor

• Fuel mix: Disadvantages coal in the fuel mix, but keeps coal in the game if prices are low; fuel-

switching to renewables requires higher prices

• Political support: Various member states hold different positions, challenging agreement on reforms

• Member-state policy: Some countries like the UK and France have considered separate carbon

policies, challenging compliance

• International linkages: Given limited schemes outside of EU and unique considerations for each

program, linkages will prove challenges (Australia)

• Eurozone crisis: In addition to sending prices lower, the crisis has tested political backing for the

program and raised competitiveness concerns

• Emissions reductions: Given low price and other challenges, not clear how much of a motivating

factor the ETS has been

• Trading fraud: Incidents of tax fraud and stolen credits arose in 2010

13

Prepared for The Gasification Technologies Council

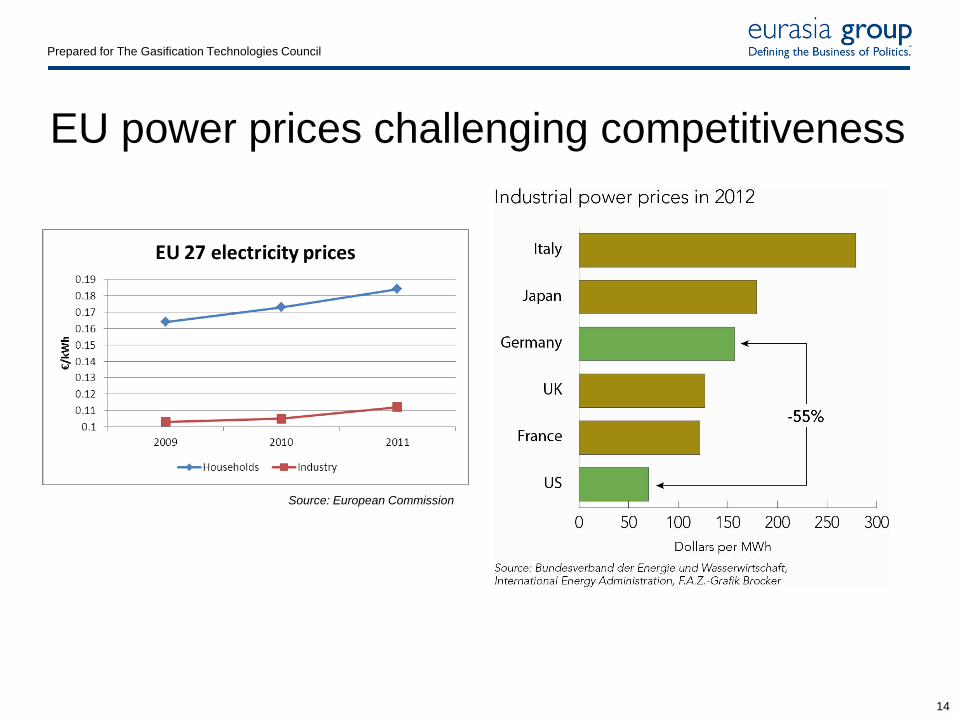

EU power prices challenging competitiveness

14

Source: European Commission

Prepared for The Gasification Technologies Council

ETS reforms

• Short-term fix: Backloading

• Longer-term fixes: Structural reform; post-2020 targets

• Backloading plan picks up steam

• Initial vote in April failed

• Revisions to water down—delays auctioning 900 million

allowances in 2013-2015 and reintroduce them in 2016-17

• Passed in European Parliament on 3 July

• Next step is passage in European Council—German position key

• Structural reforms more challenging

• Proposal for 40% reduction from 1990 levels by 2030

• 2030 targets will not be finalized until 2015

15

Prepared for The Gasification Technologies Council

Lessons learned

• Commodity created by government decree will be exposed to government intervention

risk—program changes will cause price volatility and challenge predictability

• Short compliance phases limit predictability for longer term corporate decision making

• Accurate emissions data is key to ensuring adequate supply to meet targets and

create a robust market

• Robust oversight required to avoid trading fraud that distorts the market for companies

trading for compliance purposes

• Free allocations can create windfalls for some companies whose allocation exceeds

their emissions

• Economic fluctuations that are not baked into emissions caps could send prices low

enough to fail to incentivize emissions reduction behaviors and investments

• Utilities were better placed to trade on data compared to industrial companies

• Although they lower compliance costs, offsets can prevent companies from

undertaking mitigation, especially if offset prices are low

16

Prepared for The Gasification Technologies Council

III: CHINA

17

Prepared for The Gasification Technologies Council

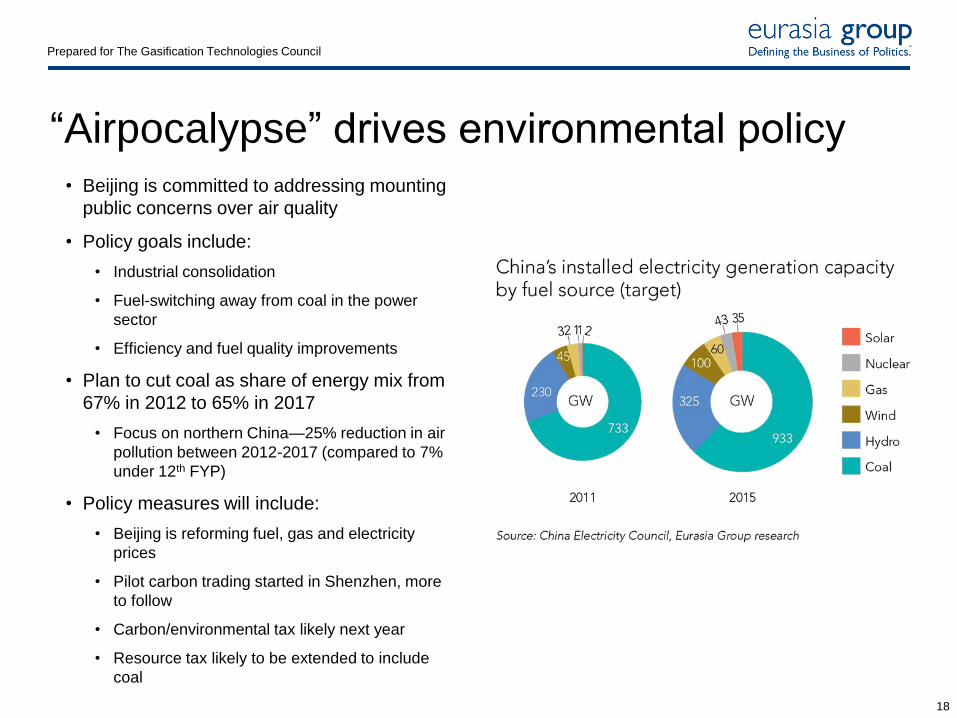

“Airpocalypse” drives environmental policy • Beijing is committed to addressing mounting

public concerns over air quality

• Policy goals include:

• Industrial consolidation

• Fuel-switching away from coal in the power

sector

• Efficiency and fuel quality improvements

• Plan to cut coal as share of energy mix from

67% in 2012 to 65% in 2017

• Focus on northern China—25% reduction in air

pollution between 2012-2017 (compared to 7%

under 12th FYP)

• Policy measures will include:

• Beijing is reforming fuel, gas and electricity

prices

• Pilot carbon trading started in Shenzhen, more

to follow

• Carbon/environmental tax likely next year

• Resource tax likely to be extended to include

coal

18

Prepared for The Gasification Technologies Council

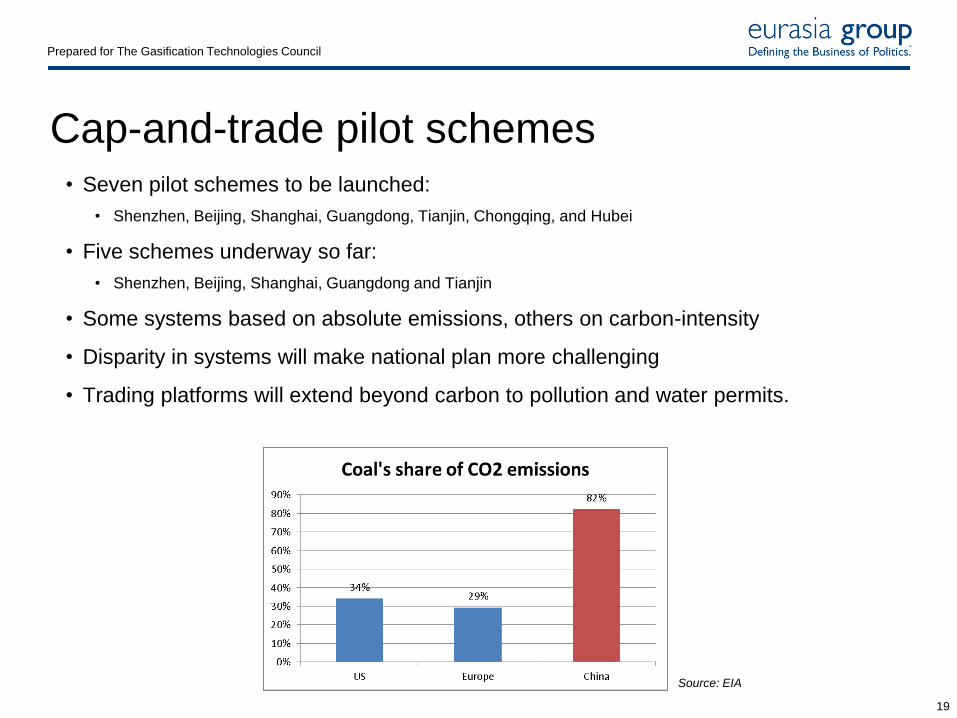

Cap-and-trade pilot schemes • Seven pilot schemes to be launched:

• Shenzhen, Beijing, Shanghai, Guangdong, Tianjin, Chongqing, and Hubei

• Five schemes underway so far:

• Shenzhen, Beijing, Shanghai, Guangdong and Tianjin

• Some systems based on absolute emissions, others on carbon-intensity

• Disparity in systems will make national plan more challenging

• Trading platforms will extend beyond carbon to pollution and water permits.

19

Source: EIA

Eurasia Group is the world’s leading global political risk research and consulting firm. This presentation

is intended solely for internal use by the recipient and is based on the opinions of Eurasia Group

analysts and various in-country specialists. This presentation is not intended to serve as investment

advice, and it makes no representations concerning the credit worthiness of any company. This

presentation does not constitute an offer, or an invitation to offer, or a recommendation to enter into any

transaction. Eurasia Group maintains no affiliations with government or political parties.

© 2013 Eurasia Group | www.eurasiagroup.net

Executive office

149 Fifth Avenue, 15th floor

New York, NY 10010

Washington office

1818 N Street NW, 7th floor

Washington, DC 20036

London office

30-31 Great Sutton Street, 1st floor

London EC1V 0NA

United Kingdom

20