Embed Size (px)

Citation preview

Wealth Management Education Series

Discover the World of Insurance

1

Wealth Management Education Series

Discover the World

of Insurance Managing your wealth well is like tending

a beautiful formal garden – you need to

start with good soil and a good set of tools.

Just as good soil has the proper fertility

to nourish a plant, the right foundation

in fi nancial literacy should empower you

to cultivate a successful investment and

protection portfolio. Discover the World

of Insurance is part of our fi nancial

education series to help educate you on

the fundamentals of investing and fi nancial

protection as you tend to your very own

fi nancial garden.

2

What is Insurance?

Insurance can provide you with fi nancial protection. It can help you maintain your lifestyle in the event of serious illness or accident. It can enable your loved ones to pay their expenses if you can no longer provide for them. It can shield you from losses if you experience an unexpected event like a fi re or theft.

You can also use insurance to plan for large expenses that you are anticipating later in life such as your children’s education or your retirement. Some insurance plans are even designed to help you meet your fi nancial goals.

Most insurance plans are basically agreements between you and the insurer. You pay the insurer a fee for assuming your fi nancial risk (premium). If a certain event occurs (insured event), then the insurer pays you an agreed amount of money (sum assured or benefi t).

In short, insurance can protect you from the things that worry you most.

3

What is Insurance?

How can Insurance help you?

We live in an uncertain world in which we must constantly adapt to diffi cult situations. Medical advances and improved healthcare are helping us live longer.

You may fi nd yourself asking:

What if I die too soon? How will my family survive with food, medical, education and other living expenses?

What if I live a long life? Have I saved enough to live a comfortable life and pay my bills after I retire?

What if I have an unexpected problem? How will I cope with the costs and continue my lifestyle if a serious accident causes my expenses to increase?

If you have these or other concerns, insurance can help protect you, and the people and things that are dear to you, from fi nancial hardship.

Dying too soon Living a long life Unexpected problems

Traditional Life Insurance• Whole of Life • Endowment• Universal

Health• Disability Income Protection• Total Permanent Disability• Critical Illness Trauma• Medical Expenses • Terminal Illness

Investment-Linked Life Insurance

General Personal• Consumer Credit • Home Contents• Unemployment • Motor Vehicle• Helper • Travel • Golf • Pet

Term Life Insurance• Mortgage

Repayment• Accidental Death

General Commercial• Liability • Property • Employee Benefi t • Commercial Auto • Business Interruption• Worker’s Compensation

Insurance Can Help

Annuity

4

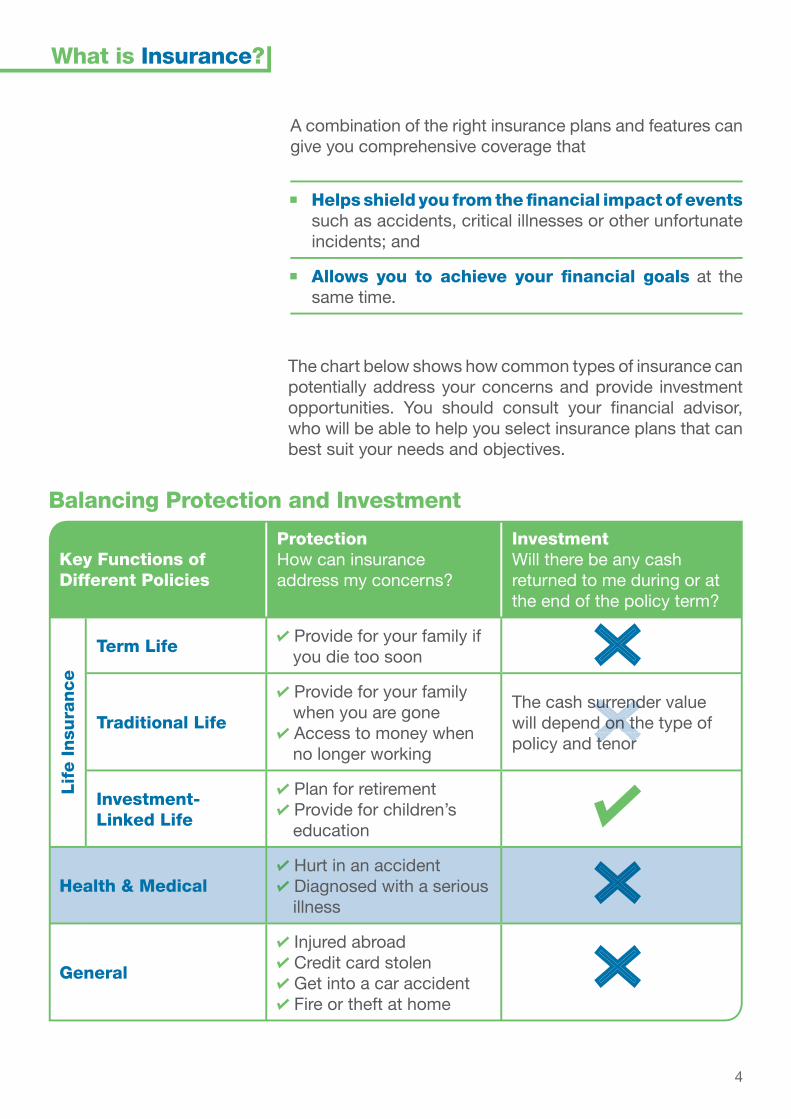

A combination of the right insurance plans and features can give you comprehensive coverage that

Helps shield you from the fi nancial impact of events such as accidents, critical illnesses or other unfortunate incidents; and

Allows you to achieve your fi nancial goals at the same time.

Balancing Protection and Investment

Key Functions of Different Policies

ProtectionHow can insurance address my concerns?

InvestmentWill there be any cash returned to me during or at the end of the policy term?

Lif

e I

nsu

ran

ce

Term Life Provide for your family if you die too soon

Traditional Life

Provide for your family when you are gone Access to money when no longer working

The cash surrender value will depend on the type of policy and tenor

Investment-Linked Life

Plan for retirement Provide for children’s education

Health & Medical Hurt in an accident Diagnosed with a serious illness

General

Injured abroad Credit card stolen Get into a car accident Fire or theft at home

urrenon t

surrendd on thtenor

The chart below shows how common types of insurance can potentially address your concerns and provide investment opportunities. You should consult your fi nancial advisor, who will be able to help you select insurance plans that can best suit your needs and objectives.

What is Insurance?

5

Life Insurance

I am only looking for protection against life’s unexpected events.”

6

There are different types of life insurance plans. The one that is right for you depends on your needs.

Term Life Insurance plans are the most straightforward – they payout only when the insured event occurs (ie. death).

Traditional Life Insurance plans payout when an insured event occurs (ie. death) but they also include a savings or investment component that allows part of your premium to grow over time and provide you with a return (if any) on your investment.

Investment-Linked Plans have a primary objective of maximizing investment returns but they also provide some insurance protection.

Life insurance policies may also have add-on plans, which extend your insurance coverage for situations such as serious injury or illness. Some add-on plans are free while others you need to pay for. The section on Health and Medical Insurance discusses common add-on plans and additional policies that can help compliment your life insurance coverage. Some common add-ons are as follows:

Life Insurance

Mortgage Repayment Insurance

This type of insurance is sometimes included with Term Life Insurance plans. It pays off your mortgage if you pass away so that your mortgage payments do not become a burden on your family. The sum assured for Mortgage Repayment Insurance can decrease each year by a set amount, or in line with the amount that you owe on your mortgage.

Accidental Death Insurance

Accidental Death Insurance is an add-on that may pay your family an increased benefi t if your death is caused by an accident covered under the policy. Some plans pay out extra benefi ts for specifi c accidents, such as if you die while travelling on public transportation.

7

I want to make sure my family is protected when I am no longer here to do so.”

Term Life Insurance1

8

Key Benefi ts… Affordability Premiums are lower than Investment-Linked Plans as no investment component is included.

Security These plans provide fi nancial assistance when your loved ones (and in some cases you) need it most.

Tax These plans may provide certain tax advantages in some countries.

Points to consider… Premiums

For Term Life Insurance plans, premiums are generally fi xed for the term of the plan. However, for some plans, the premiums may be subject to change.

Payment Interval Premiums are usually payable at regular points in the policy term. However, “limited

pay” and “single premium” plans offer you the option of paying your premiums over a shorter time or making a one-time premium payment.

Coverage Period The policy term may be set to a specifi c number of years or to a certain age. Prerequisites

Most life insurance products cannot be bought until the insurer decides you are eligible and agrees to underwrite the risks of the plan as a result of your personal circumstances which may require you to provide medical records or undergo a health check. <see “Glossary” on page 27 > Insurers might offer a “Guaranteed Issue” policy without a detailed review process, but they will not cover pre-existing medical conditions.

Issuer Risk The insurer must pay out the sum assured or accumulated cash value under the life

insurance policy. But, if the insurer faces fi nancial diffi culty then they may not make the payments.

Term Life Insurance

These plans are generally considered in the market to be the most affordable life insurance coverage. If you were to pass away, they protect your family when they would be most vulnerable. The sum assured can stay the same or it can increase by a fi xed amount or percentage each year. Such plans do not have an investment component, so you are not exposed to investment returns (or investment losses) if the policy expires before the insured event occurs.

Some Term Life Insurance policies allow for all or part of the premium to be returned to you if the insured event does not occur during the term of the policy.

Countries differ on the tax insurance benefi ts. Check with a tax advisor to understand how your insurance plan will be taxed.

9

My main objective is to seek protection against unexpected life events.”

Traditional Life Insurance

2

10

Whole of Life (permanent protection)

A Whole of Life plan provides cover for your entire life – it never runs out. Upon death, the sum assured is paid to your benefi ciaries. These policies invest part of your premium, which provides an accumulated cash value (if any) that you can withdraw or borrow against.

Endowment (limited time protection)

Like other life insurance plans, an Endowment plan makes a payout to your benefi ciaries if you die while covered. However, it also pays the sum assured to you on its maturity date if you are still living. These plans have higher premiums than other Traditional Life Insurance plans, but may be good tools to help you prepare for large future expenses, such as your children’s education or retirement.

Universal Life A Universal Life plan generally consists of two components: (i) life insurance and (ii) a cash account. The life insurance portion of a Universal Life plan is actually an annual renewable Term Life Insurance policy (see page 8). The cash account builds up every year and earns a return at either a guaranteed rate or at the current rate, whichever is higher.

Annuity An Annuity gives you a regular stream of payments or a lump sum payment in the future, usually at your expected retirement age. Please note that such payments are not guaranteed by the insurance provider. You must make regular premium payments or a lump sum payment to your insurer up front. An Annuity is usually offered as part of a Traditional Life Insurance or Investment-Linked Plan.

Traditional Life Insurance

Traditional Life Insurance policies include an investment component, which may allow you to achieve fi nancial objectives while at the same time protecting you. While the premiums for Traditional Life Insurance policies are higher than Term Life Insurance, these plans potentially build up a cash value that you can withdraw or borrow against. Your accumulated cash value (if any) usually depends on how long you hold the policy. However, the exact calculation is set by the terms of the policy you purchase. <see “Glossary” on page 27 “Accumulated cash value” >

Some common types of Traditional Life Insurance are Whole of Life, Endowment, Universal Life and Annuity policies. Depending on your exact protection and investment objectives, you can pick the type of policy that is right for you.

11

Key Benefi ts… Cost predictability Premiums are generally fi xed for the duration of these policies so you will know how much the insurance will cost you each year. However, for some plans the premiums may be subject to change.

Tax These plans may provide certain tax advantage in some countries.

Legacy planning Benefi ciaries receive a payout as long as premiums are paid or there is suffi cient value left to keep the policy in force.

Access to CashThese policies may build up a cash value, which you may be able to borrow against or withdraw from the policy.

Cash value returned If you wish, you can stop paying your policy premiums and receive the cash value (if any) that has been accumulated in the policy.

Cash Value put to workYou can use the cash value of the policy to transform the policy into a Paid-Up insurance policy, which means that you do not pay any additional premiums but the benefi t of the policy is reduced to refl ect that. <see “Glossary” on page 27 “Paid-Up insurance” >

Traditional Life Insurance

12

Points to consider…

Coverage Period Life insurance cover is provided as long as the policy remains active. Whole of

Life, Universal Life, and Annuity plans generally cover you until the end of your life. Endowment plans generally provide coverage for a set number of years, such as 10, 15, 20 or 25 years.

Customisable Add-on Plans may also be available, giving you useful coverage for other events

such as serious illness or injury. (see page 19)

Cash Access You may borrow against the cash value (if any) of your policy at the current loan rate.

You can also surrender the policy, which means that you no longer pay premiums and the accumulated cash value is returned to you. But note that if you surrender your policy early you will be charged high termination fees, and dividends will generally be less than if the policy remained in force.

Issuer Risk The insurer must pay out the sum assured or accumulated cash value under the life

insurance policy. But, if the insurer faces fi nancial diffi culty then they might not make the payments.

Market Risk The value of your investment may drop if the broader stock or bond market goes

down. It may also drop in response to common market risk factors, such as stock prices, interest rates, foreign exchange rates, and commodity prices.

Sovereign Risk Your investment returns may be affected by the political and economic events in the

country where the investment is made. For example, an issuer of a bond investment may be forced to make payments in the local currency of the issuer’s country instead of the original currency of the investment.

Foreign Exchange Risk Some of your investments may be made in a foreign currency, which can change

in value when compared against your home currency. These foreign exchange movements may reduce or wipe out your investment returns.

Traditional Life Insurance

13

Life InsuranceInvestment-Linked Plans

3 My main objective is to seek investment returns but I would also like some protection against unexpected life events.”

14

Policy Features Options

Premium Single lump sum premium or Regular premiums

Choice of Underlying Investments

Insurer’s in-house investment funds Third-party investment funds Closed-end investment funds (single premium only)

<see “Glossary” on page 27 “Closed-end investment funds” >

If your motivation for getting life insurance is geared more towards investment, then Investment-Linked Plans (ILP) may be what you are looking for. These policies combine investment and protection, to help you achieve your fi nancial goals while providing cover at the same time. Premiums are used to buy (i) life insurance protection and (ii) investment units in professionally managed investment-linked funds, which may be managed by the insurer or external fund managers.

Policies do not provide guaranteed cash values because the value of ILPs depends on the price and performance of the underlying fund units and in some cases, the value could be zero. Fees and expenses for ILPs are paid out of the premium or the sale of purchased units.

Investment-Linked Plans

Key Features of Investment-Linked Plans

15

Key Benefi ts… FlexibilityILPs offer you fl exibility to:-(i) top-up contributions on a regular basis or

whenever you wish;(ii) withdraw from certain funds; or(iii) switch investments among different funds.

Regular-premium ILPs also allow you to vary your level of coverage or to pay premiums for short periods. However, charges usually apply if you choose these options.

DiversityILPs let you choose from a range of funds managed by professional fund managers, allowing you to diversify your investments and your risk.

SecurityOnce you buy an ILP, your insurance coverage is guaranteed for the duration of the plan, even if your health declines.

Points to consider…Investment-Linked Plans can help grow your money but they can also expose you to investment risks. In some cases, the value of your Investment-Linked Plan may be zero.

Issuer Risk The insurer must pay out the sum assured or accumulated cash value under the life

insurance policy. But, if the insurer faces fi nancial diffi culty then they might not make the payments.

Market Risk The value of your investment may drop if the broader stock or bond market goes

down. It may also drop in response to common market risk factors, such as stock prices, interest rates, foreign exchange rates, and commodity prices.

Sovereign risk Your investment returns may be affected by the political and economic events in the

country where the investment is made. For example, an issuer of a bond investment may be forced to make payments in the local currency of the issuer’s country instead of the original currency of the investment.

Foreign Exchange Risk Some of your investments may be made in a foreign currency, which can change

in value when compared against your home currency. These foreign exchange movements may reduce or wipe out your investment returns.

Investment-Linked Plans

16

Which type of Life Insurance policy is right for me?

The chart below summarises the differences between the various types of common life insurance policies. Your fi nancial advisor can help you better understand the specifi c differences between the plans and recommend a policy that best suits your needs.

Types of Life Insurance

Term Life

Whole Life

Universal Life

Endowment Plan

Investment-Linked Plans

Death Benefi t

Flexible Payments

Guaranteed Cash Value

Depends on the underlying investment

Tax Advantages

Maturity Value

Optional for selected plans

Optional for selected plans

alsele

l fted

Comparison of Life Insurance Policies

Life Insurance

17

Life Insurance

Types of Policy Features

Explanation

Non-Participating Whole Life versus Participating Whole Life

Both offer fi xed premiums through the policy term. But they differ in their Cash Values:

Most• Non-Participating plans set a schedule of fi xed cash value at the start of the policy which you receive upon policy anniversaries until the maturity date. Participating• plans pay you ‘dividends’, which means you get a share of the insurer’s profi ts. These ‘dividends’ may or may not be guaranteed, and can:- offset premiums;- earn interest;- increase insurance coverage; or- be withdrawn as cash.

Limited Pay Allows you to pay premiums for a set number of years or up to certain age, while providing cover for the entire policy term.

Premiums are generally higher given the shorter period for premium payment.

Single Premium Whole of Life plans where you pay the premium in a single lump sum payment with no further payment required.

These policies have immediate cash and loan values, which can be signifi cant but may decrease overtime.

Each insurance policy may also offer different features, some of which are described below

How else do insurance policies differ from each other?

Common Policy Features and What They Mean

18

Health and Medical Insurance

If I become seriously sick or injured, I want to know that I have fi nancial protection.”

In their simplest forms, these plans provide cover for a wide range of unforeseen personal events such as a serious illness or accident. It should be noted that some events may be excluded from certain plans. You can purchase these plans on their own or together with life insurance to expand your coverage.

Health and Medical Insurance plans do not have an investment component. Some plans do, however, allow for all or part of the premium to be returned to you if you do not make any claims during the policy term.

19

Common Health and Medical Insurance Policies and their Key Features

Types of Policies Key Features

Total & Permanent Disability

Pays benefi t if you become disabled (e.g. loss of limbs, blindness) or are unable to return to work due to illness or injury.

Commonly available as an add-on to other life insurance policies.

Pre-existing medical conditions or hazardous occupations may disqualify coverage.

Disability Income Protection

Adds to your income if you are unable to work due to a disability from an illness or accident.

Benefi ts are usually paid monthly so that you can maintain your standard of living and continue to pay your expenses.

Can be tailored to meet your employment situation.

Critical / Trauma Pays benefi ts if you are diagnosed with a specifi ed major illness or if you suffer a serious injury, such as severe burns or loss of sight or hearing.

Available as an add-on to other plans or stand-alone cover.

Premiums tend to be 3-4 times higher than standard Term Life Insurance.

Terminal Illness Offered as an add-on to life insurance or Critical Illness Insurance.

Allows the policy to pay you the benefi t if you have less than 6 or 12 months to live.

The benefi t is usually capped at a certain amount.

Medical Expenses Covers the costs of hospitalisation, surgery, or medical treatment.

Limits may apply to the amount of expenses that are reimbursed.

The specifi c features of any plan will be determined by the insurance plan terms and conditions as provided by the insurance provider and such features may not be consistent with the contents of the table above.

Health and Medical Insurance

20

Key Benefi ts… Diversity There is a wide range of products available that cover serious illness and injury so you can tailor your insurance plans to meet your needs.

Affordability Premiums are lower than Traditional Life Insurance because the policy does not usually cover death or include an investment component.

Security These plans provide fi nancial assistance when you need it most. They give you a fi nancial safety net when government or employer benefi ts and personal savings may be inadequate.

Tax These plans may provide certain tax advantages in some countries.

Countries differ on tax treatment of insurance plans. Check with a tax advisor to understand how your insurance plan will be taxed.

Points to consider…

Cost For regular premium plans, premiums generally (i) increase every year at each policy anniversary; (ii) increase every fi ve years; or (iii) average out over the policy term.

Payment Interval Premiums are usually payable at regular points in the policy term. But “limited pay”

plans enable you to pay your premiums over a shorter time.

Coverage Period The policy term may be set to a specifi c number of years or to a certain age.

Customisable Many products also allow several types of protection to be combined into one policy

and can extend coverage to several people at the same time.

Prerequisites Most Health and Medical Insurance plans cannot be bought until the insurer decides

you are eligible and agrees to underwrite the risk of a plan as a result of a review of your personal circumstances which may require you to provide medical records or undergo a health check. <see “Glossary” on page 27> Insurers might offer a “Guaranteed Issue” policy (usually in relation to accidents only) without a detailed review process, but they will not cover pre-existing medical conditions.

Health and Medical Insurance

21

General Insurance

I don’t want to worry about being inconvenienced when things go wrong.”

22

Common Personal General Insurance Plans and their Key Features

Types of Policies Key Features

Home and Contents Covers your place of residence or home that you lease to someone else.

Reimburses cost of repairs and third-party claims for damages due to accidents.

Contents insurance covers theft or damage to contents of insured property; usually as an add-on to the main policy.

Motor Vehicle Covers loss or damage arising from use of your car or other motor vehicle (e.g. injury, property damage, and medical payments)(i) Property insurance covers damage to or theft

of car; and(ii) Third-party liability insurance covers you

against claims from others.

Travel Covers loss incurred during travel (e.g. cancellation, delayed departures, loss of baggage, theft, medical expenses, and accidental death).

Available options include:-(i) Single trip or annual policies; and(ii) Personal or family member cover.

Certain hazardous locations, activities or medical conditions may disqualify you from coverage (e.g. skydiving or motor racing).

1 Personal General InsurancePersonal General Insurance plans protect you against losses arising from various non-life events, for example, damage, theft, fi re, natural disasters, or other emergencies. There is no cash value to be returned at the end of the coverage period. General Insurance plans may be renewed annually at the insurer’s discretion.

Personal General Insurance

23

Types of Policies Key Features

Consumer Credit Insurance (or Payment Protection Insurance)

Repays loans in the event of death due to accident, disability or job loss.

Covers wide variety of consumer loans (e.g. auto loans, credit card debt, and personal loans).

Redundancy/ Unemployment Insurance

Directly pays specifi ed companies that you owe money to (eg. credit card debt or personal loans).

Maximum period of payment ranges from 12-24 months.

May also provide regular income during policy period.

Coverage depends on terms of the policy.

Golf Insurance Covers accidental loss or damage to golf equipment and personal effects while golfi ng.

May even cover entertainment expenses following a “hole-in-one”.

Domestic Helper Insurance Provides comprehensive coverage for a domestic helper employed in your home.

Protects against legal liabilities should helper or third party suffer injuries in the course of his or her work.

Pet Insurance Covers veterinary costs when your pet is ill or injured.

Some policies also include benefi ts in event of pet’s theft or death.

The specifi c features of any plan will be determined by the insurance plan terms and conditions as provided by the insurance provider and such features may not be consistent with the contents of the table above.

Personal General Insurance

24

Common Commercial General Insurance Plans and their Key Features

Types of Policies Key Features

General Liability Covers your business for personal injuries or property damage that you cause other people or businesses (e.g. a customer getting injured in your store).

Includes the cost of defending and resolving those lawsuits.

Errors and Omissions Liability (“E&O”)

Covers mistakes that cause injury to other people or businesses. (e.g. damages from an insurance agent forgetting to fi le a policy application or a notary fi lling out a notarization incorrectly).

Malpractice or Professional Liability

Available for doctors, dentists, accountants, real estate agents, architects, and other professionals.

Covers losses if a professional causes injury by acting in a way other members of his profession would not (e.g. a doctor making a mistake that other doctors in his specialty would not have made).

Pays the professional’s defence costs and any judgment or settlement.

Commercial General Insurance

I rely on the smooth running of my business to serve my customers and support my employees. I want to keep it safe from certain events.”

2 Commercial General InsuranceJust like individuals, businesses need to protect themselves against risks or they could face serious fi nancial problems. Commercial General Insurance plans protect businesses from many different types of risks. For example, malpractice or product liability plans protect your business from lawsuits. Business interruption and property insurance can cover losses from fi re, fl ooding, or other natural disasters. General Insurance plans may be renewed annually, at the insurer’s discretion.

25

Types of Policies Key Features

Directors’ and Offi cers’ Liability Insurance

Bought by corporations and non-profi t organisations to cover the costs of lawsuits against their directors and offi cers.

Property Pays for losses and damage to real or personal property (e.g. fi re damage in your offi ce).

You can insure your: Offi ce including furniture, contents and fi xtures;• Commercial property building; Equipment • (e.g. computers and machinery); and Cargo/Inventory (e.g. items shipped by air, sea or land).

Commercial Auto Covers the cars, vans, trucks and trailers used in your business.

Pays if your vehicles are damaged or stolen or if the driver injures a person or property.

Worker’s Compensation Covers you for your employee’s on-the-job injuries.

In some countries, businesses with employees are required to carry some type of workers’ compensation insurance.

Business Interruption Covers the cash fl ow and profi t that is affected by an interruption to your business.

For example, if key manufacturing machinery is damaged by fl oods, the income that is lost due to the two-month interruption to the production schedule may be covered.

Employee Benefi t Covers health, dental, disability expenses, and life insurance for employees and the company’s directors or owners.

The specifi c features of any plan will be determined by the insurance plan terms and conditions as provided by the insurance provider and such features may not be consistent with the contents of the table above.

Commercial General Insurance

26

Key Benefi ts… Financial security and peace of mindThese policies provide fi nancial protection against unexpected events so you can continue to live your life and run your business with limited consequences.

AffordabilityPremiums are generally more affordable as there is no investment component.

Tax These plans may provide certain tax advantages in some countries.

Broad range of coverageDespite their lower premiums, these policies may still provide a signifi cant amount of cover, especially for third-party liability claims.

Security These policies may function as a fi nancial safety net, allowing you to potentially avoid out-of-pocket costs.

CustomisableMany products allow several types of protection to be combined into one policy.

Countries differ on tax treatment of insurance plans. Check with a tax advisor to understand how your insurance plan will be taxed.

General Insurance

Points to consider…

Payment Intervals Premiums are typically paid once a year. They may increase on renewal or be raised

by the insurer if you make a large number of claims. If you do not make any claims in the preceding year, then you may receive a “no claims discount”.

Coverage Period Policy terms usually last one year.

Prerequisites Underwriting <see “Glossary” on page 27> is usually required and the insurer will

assess your eligibility for cover based on potential risk factors.

No Cash Value These policies do not carry a cash value.

27

Glossary of Insurance Terms

Benefi t Payout from the plan if the event that you have insured against occurs. This is also known as “sum assured”.

Accumulated cash value

Some insurance policies have an accumulated cash value. This is the balance that is left in your insurance policy after policy related expenses are paid and interest is calculated. You may borrow against the accumulated cash value (if any) without affecting your insurance coverage. If you cancel the policy, you may take out the accumulated cash value (if any), although you may need to pay penalties.

Claim Request for the insurer to pay out the sum assured as agreed in the policy.

Closed-end funds These investment funds issue only a fi xed number of shares, and do not issue new shares even if investor demand grows. Share purchases take place in the secondary market and prices are determined by investor demand. Shares of these funds are often traded at a premium or discount compared to the fund’s net asset value. Further, such funds usually do not allow investors to redeem prior to a stated maturity date.

Deductible/Excess First portion of claim amount that the insured must pay. The insurer will pay out the remainder up to the claim limit.

Dividends/Bonuses

Some plans, such as Traditional Life Insurance plans offer an annual bonus payment that may be withdrawn at your discretion. Dividends and bonuses usually take time to become available and if cashed early they may not be worth their full value.

Paid-Up insurance This feature is only available for Whole of Life plans. When you have accumulated enough cash value from your premium payments, you can stop paying your premiums for a time and keep your life insurance coverage.

Policy Another name for your insurance plan.

Policy term Length of time the insurance plan is in effect.

Premium Fee that you pay to the insurer. Premiums may be regular or one-off.

Add-on Add-on plans (sometimes known as riders) extend the cover of your insurance plan. Some add-on plans are available free-of-charge and are a good way to help you gain more protection.

Underwriting Way to determine the eligibility of the person to be insured. Commonly determined through health check ups, personal background checks, and previous claims history.

28

Important Legal Information

In Brunei Darussalam, Standard Chartered Bank (“SCB”) is registered as a branch officeand is licensed and regulated by Authoriti Monetari Brunei Darussalam.

This document contains material and information from sources that we believe are reliable. The general products we describe are not suitable for everyone. We provide this document for general information and educational purposes only and emphasize that you should not use this information as the basis for making any decisions to purchase an insurance plan. We can change the opinions we hold without notice.

This document is not an offer, solicitation or invitation to purchase any insurance products and services. If you are in doubt about any of the contents, you should seek independent professional advice.

You may not copy any part of this document in any manner without SCB’s written permission.

GW

M03

/201

2

How can we help you further?Do you have a question on what you have just read? Would you like to have a further discussion on this subject?

Contact your Relationship Manager, or any of our Standard Chartered Bank locations closest to you for more information.

AsiaBangladesh standardchartered.com/bd+880 2 8957272 or+880 2 8961151

Bruneistandardchartered.com/bn+673 265 8000

Chinastandardchartered.com.cn800 820 8088

Hong Kongstandardchartered.com.hk+852 2886 8868 or +852 2886 8888

Indiastandardchartered.co.in3940 4444 or 6601 4444

Indonesiastandardchartered.com/id+62 21 57 9999 88 or 68000

Japanstandardchartered.co.jp0120 989 802 or +81 3 4360 8888

Koreascfirstbank.com1577 7744

Malaysiastandardchartered.com.my1300 888 888

Nepalstandardchartered.com/np+977 1 478 2333

Pakistanstandardchartered.com/pk111 002 002 or 0800 44 444

Singaporestandardchartered.com.sg1800 747 7000

Sri Lanka standardchartered.com/lk+94 11 2480 480

Taiwanstandardchartered.com.tw02 40580088

Thailandstandardchartered.co.th1595

Vietnamstandardchartered.com/vn+84 8 3 911 0000

Middle EastBahrain standardchartered.com/bh+973 17 531 532 or 80001 802

Jordanstandardchartered.com/jo+ 962 6565 8011

Lebanonstandardchartered.com/lb/en+961 390 1212

Omanstandardchartered.com/om+968 2477 3535

Qatarstandardchartered.com/qa+974 4465 8555

UAEstandardchartered.ae600 5222 88

AfricaBotswana standardchartered.com/bw361 5800

Kenyastandardchartered.com/ke+254 20 329 3900 or 722 203666 or 733 335511

Ghanastandardchartered.com/gh0302 740100

Nigeria standardchartered.com/ng+234 1 270 4611-4

Tanzania standardchartered.com/tz022 2164 999

Uganda standardchartered.com/ug041 4340077

Zambia standardchartered.com/zm998 or 0977 999 990

Zimbabwe standardchartered.com/zw/en+2634 758078 or 79

EuropeGermanystandardchartered.de069 770 750 444

Bahrain

Germany

KenyaUganda

Jordan

Lebanon

Ghana

IndiaOmanQatar

UAE

Nigeria

Brunei

Taiwan

ChinaKorea

Hong Kong

Malaysia

Thailand

Singapore

Japan

Indonesia

Vietnam

Bangladesh

Botswana

Tanzania

Pakistan

Nepal

Sri Lanka

Zambia

Zimbabwe