Embed Size (px)

Citation preview

Discounted Cash Flow Valuation Model Water Infrastructure Assets

Introduction – Logan City

• Logan City situated in the heart of South East Queensland

• 63 suburbs • More than 300,000 people • Fifth largest local government area (by population)

in Australia • Third largest budget • Covers 957 square kilometres

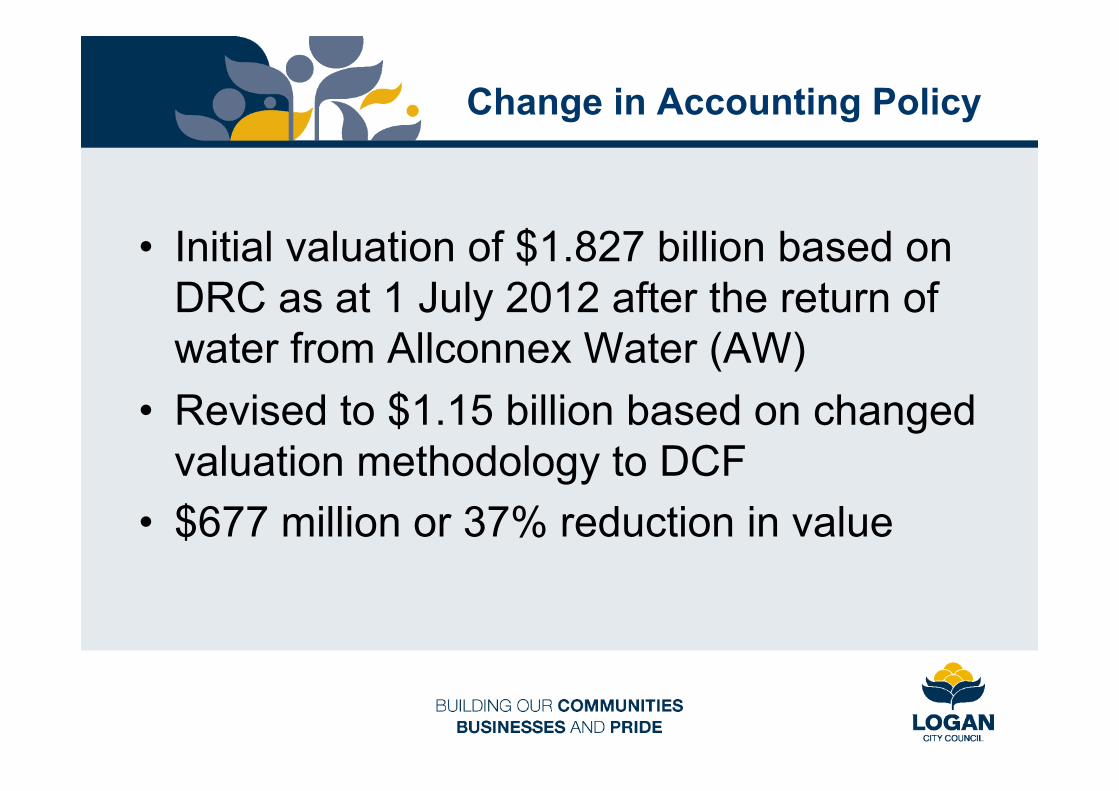

Change in Accounting Policy

• During 2013/2014 Logan City Council (LCC) worked with QAO, QTC & Deloittes to change the valuation methodology of its Water Infrastructure Assets

• We moved from Depreciated Replacement Cost (DRC) to Discounted Cash Flow (DCF)

Change in Accounting Policy

• Initial valuation of $1.827 billion based on

DRC as at 1 July 2012 after the return of water from Allconnex Water (AW)

• Revised to $1.15 billion based on changed valuation methodology to DCF

• $677 million or 37% reduction in value

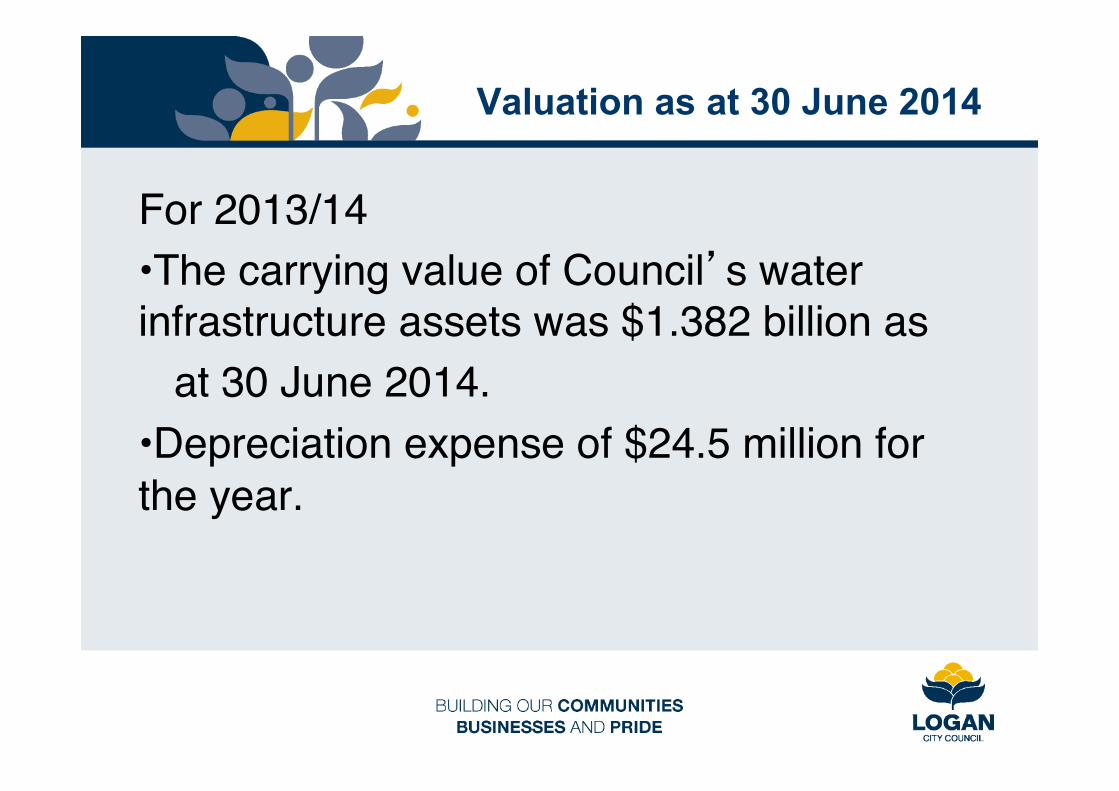

Valuation as at 30 June 2014

For 2013/14"• The carrying value of Council’s water infrastructure assets was $1.382 billion as" at 30 June 2014."• Depreciation expense of $24.5 million for the year.

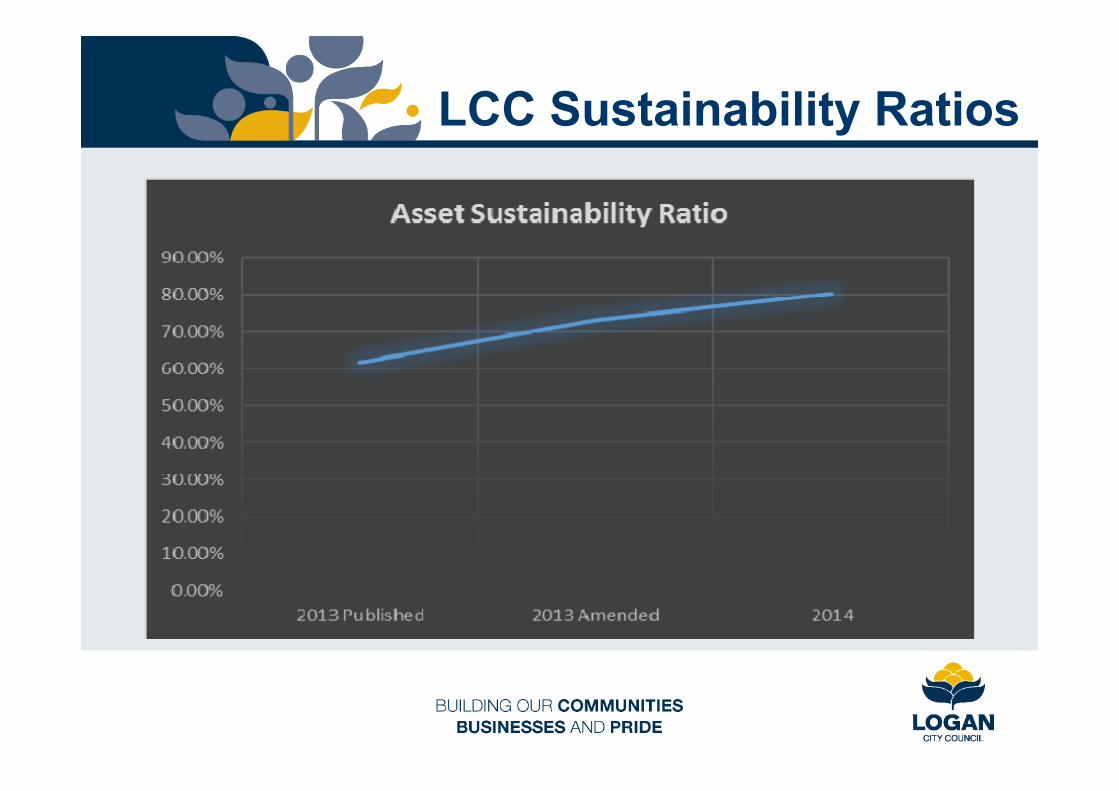

LCC Sustainability Ratios

LCC Sustainability Ratios

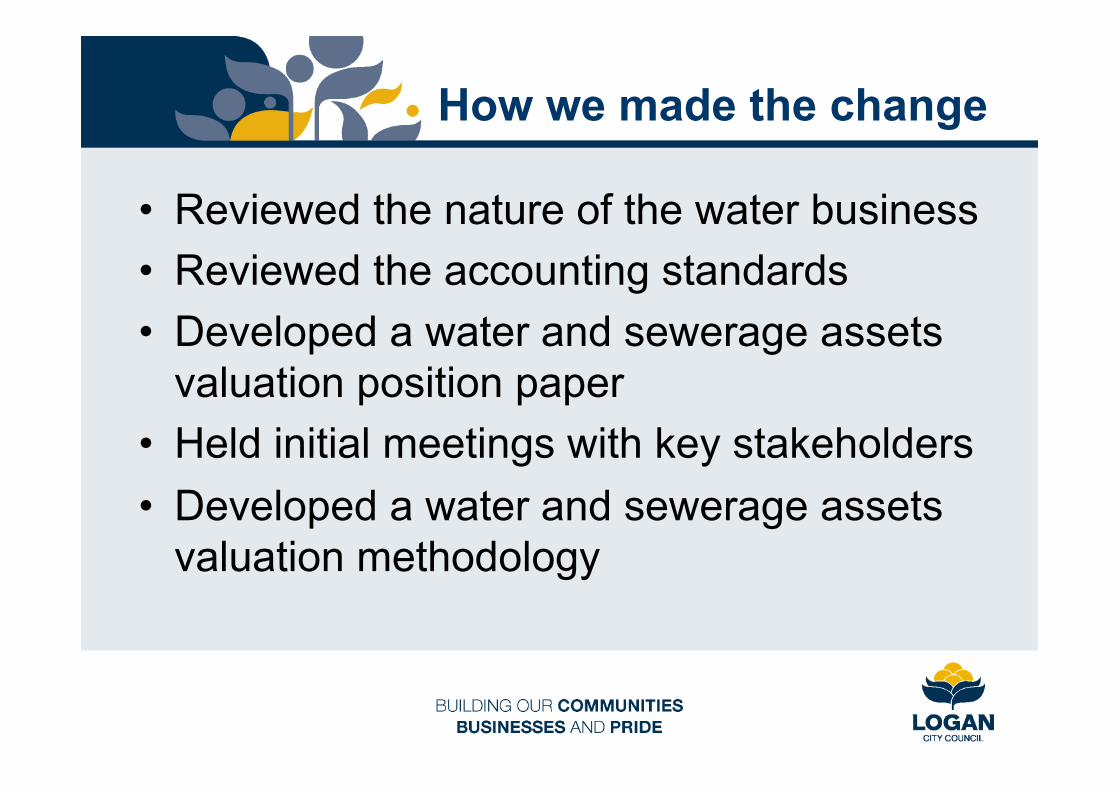

How we made the change

• Reviewed the nature of the water business • Reviewed the accounting standards • Developed a water and sewerage assets

valuation position paper • Held initial meetings with key stakeholders • Developed a water and sewerage assets

valuation methodology

How we made the change

• Made changes to Council’s Revaluation of Non- Current Assets Policy

• Refined our 10 year water business financial model

• Established a DCF valuation model • Input 10 year financial model information

into DCF valuation tool

How we made the change

• Reviewed DCF model results for reasonableness

• Reviewed impact on financial statements –change in accounting policy

• Prepared final valuation work papers for audit

Consequence of change

• A reduction in depreciation • Move from operating deficit to surplus • An improvement in our asset sustainability

ratios • Alignment of valuation approach with other

water service providers in South East Queensland which are subject to the QCA Regulatory Framework ie QUU, Unitywater and SEQWater.

Consequence of change Con’t

• An opportunity to smooth asset valuations on a year by year basis by using future cashflows of the business

• An alignment of pricing and depreciation methodologies

Where to from here

But we can’t stand still as: • Spending on renewals changes each year (impact on asset sustainability ratio) • Asset base increase yearly (donated assets, assets constructed and annual revaluations) • Still a large value of assets under DRC valuation methodology

Where to from here

• LCC now has a focus on Stormwater Drainage Assets to review: Ø The componentisation of assets Ø The use of new technology as modern

equivalent (pipe relining) Ø The assets estimated useful lives

• Early indications are that the overall life of the stormwater drainage assets may be extended.

Where to from here

• Continued improvement in asset management systems to refine identification of renewals spending

• Continued use of prudency and efficiency principles in the development of the capital program