Embed Size (px)

Citation preview

DISCLAIMER: This publication is intended for EDUCATIONAL purposes only. The information contained herein is subject to change with no notice, and while a great deal of care has been taken to provide accurate and current information, UBC, their affiliates, authors, editors and staff (collectively, the "UBC Group") makes no claims, representations, or warranties as to accuracy, completeness, usefulness or adequacy of any of the information contained herein. Under no circumstances shall the UBC Group be liable for any losses or damages whatsoever, whether in contract, tort or otherwise, from the use of, or reliance on, the information contained herein. Further, the general principles and conclusions presented in this text are subject to local, provincial, and federal laws and regulations, court cases, and any revisions of the same. This publication is sold for educational purposes only and is not intended to provide, and does not constitute, legal, accounting, or other professional advice. Professional advice should be consulted regarding every specific circumstance before acting on the information presented in these materials. © Copyright: 2011 by the UBC Real Estate Division, Sauder School of Business, The University of British Columbia. Printed in Canada. ALL RIGHTS RESERVED. No part of this work covered by the copyright hereon may be reproduced, transcribed, modified, distributed, republished, or used in any form or by any means – graphic, electronic, or mechanical, including photocopying, recording, taping, web distribution, or used in any information storage and retrieval system – without the prior written permission of the publisher.

4.1

Learning Objectives

After studying this chapter, a student should be able to:

# explain the purpose and content of the generalaccounting records kept by a business;

# describe the form and content of financialstatements and the accounting principles thatguide their preparation;

# journalize transactions, post and trial balancethem and formulate financial statements; and

# understand the relationship between the balancesheet and income statement.

INTRODUCTION TO

FINANCIAL STATEMENTS

Introduction

Financial statements contain information that may be important in negotiating a sale or in evaluating a business'sperformance. In this chapter and the next, we will examine the accounting concepts and terminology needed to interpretfinancial statements.

There are several reasons why this knowledge is important:

First, the Real Estate Services Act requires certain financial statements to be made available when a business is sold.

Second, if you have a proper understanding of the financial and profit generating aspects of the business, you will be ableto determine its market value.

Third, financial statements and accounting records are required by a brokerage for its own purposes and, in particular,for the requirements of dealing with trust funds. We will review the specific requirements of the Real Estate ServicesAct, Rules and Bylaws, and provide an introduction to financial statements and accounting concepts.

General Records

Importance and Need for Proper Accounting Control Over Brokerage Transactions

Let's review the obligations imposed by the Real Estate Services Act and Rules with regard to a brokerage's own records.Rule 8-1 provides:

(1) A brokerage must keep such financial records in connection with its business as are necessary toensure the appropriate and timely accounting of all transactions relating to real estate servicesprovided by the brokerage and its related licensees.

As we saw in Chapter 2, the Rules clearly state what records must be kept by a brokerage for transactions relating tobusiness and trust accounts (Rules 8-2 and 8-3 respectively). The Rules make a distinction between general brokerageaccounts and trust accounts, with the latter being subject to even more strict obligations, including separate specific trustledgers to be made accounting for transactions concerning the brokerage’s trust account. The Rules set out the specificobligations on brokerages to ensure proper books and accounts are kept.

©Copyright: 2011 by the UBC Real Estate Division

Chapter 4

4.2

Regulation 75/61, section 4.01 under the repealed Real Estate Act Regulations gave the following requirement:

Every person who applies for a licence under the Act . . . shall . . . have an appropriate knowledge ofthe books of account required in the operation of a real estate business.

Although this is no longer made explicit in the legislation, it should generally be assumed to still apply, as therequirements with respect to financial accounting on brokerages are equally extensive under the new Real Estate ServicesAct as they have ever been. Accordingly licensees should have a firm grasp of what is required of them under the newregulatory framework.

The discussion of accounting records will begin with a review of general business records.

Cash and Bank Records

As for any business, accurate and timely recording of all cash and banking transactions is a must. Depending on the sizeof the business operation, the records may range from simple handwritten accounts to a full scale computerized system.As a general rule, all cash and cheques received should be deposited in full and on a prompt basis. The deposit bookis a useful starting point for any cash record. Take care to keep personal transactions completely divorced from yourbrokerage business. The brokerage bank accounts, therefore, should be reserved strictly for business purposes.

Expenditures on behalf of the brokerage should always be made by cheque. The paid cheques and the supporting invoicesor statements provide a good record of the nature of the transaction and proof of its payment. Sometimes cash must beused to pay for incidental items; in this situation, you should still take care to keep receipts as a record of the payment.Many businesses find a petty cash fund useful for this purpose. The use of the fund should be limited to businesspurposes and not be seen as a convenient source of "pocket money."

A bookkeeper can readily prepare a summary of the banking transactions using a record known variously as a journal,cash book, synoptic, or book of original entry. No matter what form the record takes, the purpose is the same. Thejournal provides:

C a complete record of cash receipts and disbursements (cheques);C a breakdown of expenses paid for;C a way to keep a running record of the bank balance; andC a convenient summary for recording transactions in the accounts.

Payroll Records

Whenever a payroll is prepared, it is necessary to keep accurate records for both accounting and tax reporting purposes.A detailed record must be kept for each employee so that proper deductions for income tax, Canada Pension, andEmployment Insurance may be made. The government publishes deduction tables to assist in making these calculations.Only when all the necessary deductions have been determined can the actual paycheque be prepared. The details of thecheques could be entered in the journal just described or kept in a separate payroll journal if the size of the businesswarrants it.

Payroll deductions are due to Canada Revenue Agency by the fifteenth of the following month and payment can be madedirectly at the bank. Each employer must obtain an account number from Canada Revenue Agency to facilitate thisprocess. It is also necessary to report earnings and deductions for each employee for the calendar year on forms knownas T-4s. The T-4 forms have to be completed by the end of February of the following year.

©Copyright: 2011 by the UBC Real Estate Division

Introduction to Financial Statements

4.3

General Ledgers and Financial Statements

From the banking and payroll records an accountant or bookkeeper can summarize the financial activities into generalledger accounts. The general ledger is the group of accounts used to keep a separate record for each item found in thefinancial statements. In other words, the general ledger contains an account for each asset, liability, owner equity,revenue, and expense. Subject to adjustments necessary to properly match revenues and expenses, it is possible toprepare the actual financial statements for the business from this information. Appendix 1 shows a suggested chart ofaccounts which could be used for a real estate brokerage.

Trust Accounts

Review Sections 25 to 30 of the Real Estate Services Act and the discussion of Trust Accounts in Chapter 2.

The obligations that these sections impose on the brokerage are easily complied with as long as all funds received arepromptly deposited into the trust account and payments to the conveyancer or the brokerage itself are not madeprematurely.

A separate record sheet for each client is required. This record should completely describe the nature of the property,the amount of funds received, the names of the parties involved, and the commissions payable on the transactions. Rule8-1(2) of the Rules refers to the specific provisions.

At any time, the total of funds held in trust must always equal the total of the client accounts. This will be the case aslong as all trust funds received and credited to a client are deposited in the trust account and all payments on behalf ofa client are withdrawn from the trust bank account.

Examination of Records: Licence Applications

Several provisions in the Real Estate Services Act, Rules and Council Bylaws pertain to the records and accounts of abrokerage. Real estate brokers should be aware of the following sections.

C Section 86(2)(f) (and Rule 7-6) provides for the examination of books of a brokerage by the Real Estate Councilwithout restriction and further prohibits the withholding of information.

C Section 37(3) provides for an inquiry or audit by the Council during which Council can enter the premises ofthe brokerage, inspect and copy files, as well as require licensees (or directors and shareholders of a real estatebrokerage who are not licensees) to meet with investigators and answer inquiries.

C Section 38 allows the Council to apply to Court for an order to impound the books and records of a brokeragewhere there are reasonable grounds to believe a licensee has committed professional misconduct.

C Real Estate Council Bylaw 4-5(2) requires an application for a brokerage licence to be accompanied by afinancial statement in a form approved by the Superintendent which has been verified by the statutory declarationof the proposed managing broker or a certificate issued by a chartered accountant or certified general accountant.

A real estate broker is therefore charged with the responsibility of keeping records in such a way that he or she canreadily distinguish the brokerage's transactions from those transactions which affect his or her clients or other parties.

Each of these parties or separate financial units over which the brokerage exercises some degree of control must beaccounted for as a separate entity. To conform with legal requirements as well as to measure the progress of each entity,separate records must be kept.

©Copyright: 2011 by the UBC Real Estate Division

Chapter 4

4.4

Because these transactions (i.e., the exchange of assets, obligations, or services) involve dollar amounts, they are usuallyreferred to as financial transactions. The way in which the accountant communicates this financial information is throughthe process of accounting. Accounting is the language of business and, like any other language, it has its own specialvocabulary and its own special way of communicating information. Financial statements are an accountant's way ofcommunicating.

Form and Content of Financial Statements

Accounting

Accounting is the systematic recording, reporting and analysis of financial transactions. It is the medium through whichan entity records, summarizes, classifies and communicates its activities and transactions for a given period of time. Thisinformation is important as it aids in planning and controlling routine operations, making special decisions, andformulating overall policies and long-range plans.

Nature and Function of Financial Statements

Financial statements may be considered to be the end result of the recording, summarizing, and classifying of theaccounting process. They represent the medium through which information about business transactions that occurredover a certain period of time (usually one year) are communicated to interested parties.

Financial statements provide quantitative information about a particular entity which is intended to be useful in makingeconomic decisions. These economic decisions usually involve making rational choices among alternative courses ofaction. However, not all of the information that is needed will be contained in the financial statements.

Financial reporting should meet the following objectives:

C Financial reporting should provide information that is useful to present and potential investors and creditors andother users in making rational investment, credit, and similar decisions.

C Financial reporting should provide information to help present and potential investors, creditors, and other usersin assessing the amounts, timing, and uncertainty of prospective cash receipts from dividends or interest, andthe proceeds from the sale, redemption, or maturity of securities or loans.

C Financial reporting should provide information about the economic resources of an enterprise, the claims to thoseresources (obligations of the enterprise to transfer resources to other entities and owners' equity), and the effectsof transactions, events, and circumstances that change resources and claims on those resources.

Financial statements are compiled in accordance with Generally Accepted Accounting Principles, described below. In,Canada, the primary course of generally accepted accounting principles is the Accounting Handbook issued by theCanadian Institute of Chartered Accountants.

Generally Accepted Accounting Principles

To understand and interpret financial statements, familiarity with generally accepted accounting principles is important.Generally accepted accounting principles refer to the rules and guidelines followed in preparing financial statements andinclude the following principles.

With effect from January 1, 2011, there will be two different sets of generally accepted accounting principles in use inCanada. Public companies will be required to report in compliance with the International Financial Reporting Standards(IFRS). Private companies will be able to choose whether their financial statements will comply with the InternationalFinancial Reporting Standards or the Canadian Accounting Standards for Private Enterprises (ASPEs). Most private

©Copyright: 2011 by the UBC Real Estate Division

Introduction to Financial Statements

4.5

companies will elect to comply with the ASPEs which are less onerous because there will be insufficient benefit incompliance with IFRS to offset the higher costs incurred. This chapter assumes that the brokerage will elect to complywith the ASPEs.

Cost Principle

Commonly referred to as the historical cost principle, this principle holds that when a business enterprise acquires anasset, the asset's historical cost (the amount of consideration given up for the asset) is the appropriate amount to recordin the financial statements of the enterprise. While this seems obvious, it should be pointed out that at times an enterprisemay acquire an asset for an amount that is greater or less than the asset's fair market value on the date of the transaction.To conform to the cost principle, it is not appropriate to record the asset at what might be considered its fair marketvalue; the asset should be record at what the enterprise paid for it.

Revenue Recognition Principle

Revenue is usually the amount received or receivable by an entity for the provision of goods or services. The revenuerecognition principle holds that revenue should be recognized by an enterprise when it is earned, not necessarily whencash is received. This is referred to as the accrual basis of accounting as opposed to the cash basis. For example, underthe accrual method of accounting, a real estate representative would record the commission earned from the sale of ahouse on their accounting records when the "subject clauses" were removed from the contract of purchase and sale, eventhough the money for the commission would not be received until the completion date. On the other hand, the cash basiswould not allow the commission to be recorded until the cash was actually received. The accrual basis of accountingis more common and will be used throughout the chapter. Revenue then, is considered to be earned when title to goodshas passed from the seller to the purchaser. In the case of a service enterprise, revenue is earned when the services arerendered.

Matching Principle

This principle holds that expenses directly associated with particular revenues should be recognized in the same periodin which the revenue is recognized. Other expenses should be recognized in the period in which the goods or servicesare consumed. In other words, insurance costs covering a calendar year should be recognized each month and not allin the month in which the insurance begins or the month in which the premium is paid. Costs which benefit more thanone month should, to the extent practical, be recognized over the period benefited by the costs. As with the revenueprinciple, the matching principle requires the accrual basis of accounting be used for maintaining records of the entity;that is, expenses are recorded when incurred, which is not necessarily when they are paid.

Materiality Principle

During the course of any year, expenses such as the purchase of stationery or cleaning supplies may be incurred whichhave a relatively low cost but are used up over a period of several months. The effort involved to allocate these costsover the several months that they are used would exceed any conceivable benefit achieved by such an allocation. Indetermining whether any allocation is significant enough to make, one should consider if it is likely to impact anydecisions or judgements made by the users of the financial statements. If the cost is below that threshold, it should beexpensed when the stationery or supplies are acquired and not spread over the months in which they are used.Conversely, where a large cost (such as insurance) is incurred which benefits the entire year, the cost should be allocatedin accordance with the matching principle.

Objectivity Principle

The objectivity principle holds that all accounting information should be reported on objectively determined and verifiabledata. This principle is closely aligned with the cost principle, in that the best way to determine objectivity in accountingtransactions is the amount of consideration given up at the date of the transaction. If accounting information is recordedon a cost basis, this information could, if required, be certified by an independent party (such as an auditor, if an auditwas performed).

©Copyright: 2011 by the UBC Real Estate Division

Chapter 4

4.6

Consistency Principle

Accounting recognizes that alternatives exist in the recording of transactions, and in certain cases generally acceptedaccounting principles allow the same transaction to be recorded in more than one way.

The consistency principle holds that once a business enterprise adopts one generally accepted accounting principle froma number of alternatives, the enterprise should follow that principle in the ensuing years. This does not mean that abusiness enterprise is prohibited from changing from one generally accepted accounting principle to another that is moreappropriate. However, if a business enterprise were to do this on a continuous basis, it would render the financialstatements virtually meaningless since users would not be able to assess performance from one year to the next. Changesin accounting principles should be made only where the change will result in more relevant information being providedto the users of the financial statements.

Fiscal Year

All taxpayers compute their income and tax liability for taxation years. Individuals use the calendar year as their taxationyear. Corporations report their income on the basis of a "fiscal period" that may be different from the calendar year.Self-employed individuals, partners and professional corporations must report their income on a calendar year basis.

Corporations may initially choose any fiscal period, but then must consistently report income for tax purposes on thatbasis. No taxation year may be longer than 53 weeks, and a change of year end may be made only with the approvalof the Minister of National Revenue. There are certain circumstances where a corporation's taxation year may bedeemed to end; for example, an amalgamation is deemed to cause the end of a taxation year.

Double-Entry Bookkeeping System

Accounting is concerned with the recording of business transactions. This requires the analysis of each individualeconomic event of a business which can be measured objectively in terms of dollars.

The double-entry bookkeeping system which underlies the accounting process recognizes the dual nature of each financialtransaction – that is, each transaction affects at least two different financial statement items (accounts). The nature ofthe transaction must be examined in order to determine how it should be recorded. For example, the acquisition of anautomobile (an asset) might either decrease another asset (cash), or increase a liability (bank loan payable).

This double-entry system gives rise to the accounting equation which is expressed as:

Assets = Liabilities + Owners' Equity

Assets are items of value that are owned by the entity, whereas liabilities represent the dollar value of the claims thatcreditors have over the entity. Owners' equity represents the amount of money that the owners have invested in the entity.

You should also note that the accounting equation is the basic formula for the balance sheet. The equation not only showsthe different assets owned by the entity, but it also shows the proportional contribution of the assets by the creditors andowners. The balance sheet is discussed in detail in a later section.

Accounts

Accounts are the device used in a bookkeeping system to accumulate changes resulting from business transactions;therefore transactions affecting similar assets or liabilities will be summarized in one account. The way in which the twosides of offsetting transactions are recorded is through the use of two types of entries: debits and credits. Eachtransaction will be recorded by offsetting debit and credit entries in the accounts which are affected by the transaction.Debits are used to record increases in asset accounts, and decreases in liability accounts and owners' equity accounts.Credits are used to record decreases in asset accounts and increases in liability accounts and owners' equity accounts.

©Copyright: 2011 by the UBC Real Estate Division

Introduction to Financial Statements

4.7

In addition to asset accounts, liability accounts, and owners' equity accounts, there are also two other types of accounts:revenue accounts and expense accounts. Revenue accounts record the price of goods sold and services rendered tocustomers, while expense accounts record the cost of goods and services used. Increases in revenue accounts arerecorded using credits, and increases in expense accounts are recorded using debits.

To summarize:Type of account Increases Decreases

Assets Debits Credits

Liabilities Credits Debits

Owners' equity Credits Debits

Revenues Credits Debits

Expenses Debits Credits

Appendix 1 lists common examples of the different types of accounts used by real estate brokerages.

Review of Journalizing, Posting, and Trial Balancing

Journalizing

The first step in the accounting process is to record the economic event in a journal, referred to as journalizing. Thisjournal entry designates, in the journal, the accounts that are affected by the economic event. Since the objective of thisstep is to record, in one place, the essence of each business transaction, the following elements must be entered into thejournal:

C the date of the transaction (not the date of entry);C a source code (to enable the accountant to trace any entry back to the source transaction);C the names of the accounts affected; andC the amounts by which each account is increased or decreased.

Illustration 1

For example, two individuals form a partnership to buy houses and rent them. After an agreement is made as to thedivision of profits and responsibilities of each partner, the partners must then invest some of their own money or assetsinto the partnership. On January 1, 2010, Mr. Adams invests $80,000 cash and Mr. Brock invests $20,000 in cash aswell as an office building which he paid $30,000 for in 1999, but as of January 1, 2010 had a fair market value of$60,000 (i.e., this is what the partnership would have had to pay for that particular office building on that date). It wasestimated that the office building would last an additional 10 years and at the end of this period could be sold for $10,000scrap value (salvage value). The journal entry to record this transaction on the books of the partnership would be:

January 1, 2010

Cash 100,000Office building 60,000

Adam - capital 80,000Brock - capital 80,000

Note that it is not necessary to include a heading, "debit", before cash and office building and a heading, "credit", beforeAdam ) capital and Brock ) capital. Accounts that are debited are listed first and are placed closest to the left columnwhereas the accounts that are credited are indented to the right. Notice also that the total dollar amount of the debitsmust always equal the total dollar amount of the credits.

©Copyright: 2011 by the UBC Real Estate Division

Chapter 4

4.8

Title of Account

Debits are recordedon this side

Credits are recordedon this side

Figure 1Sample T-Account

Cash Adam - Capital

1/1/10 100,000 1/1/10 80,000

Office Buildings Brock - Capital

1/1/10 60,000 1/1/10 80,000

Figure 2Posting

Adjusting Journal Entries

At the end of each accounting period it is necessary to prepare adjusting journal entries. The matching principle dictatesthat assets that benefit the enterprise for more than one accounting period may not be expended in one period (unless theircost is immaterial). Since an asset may have been purchased in a previous fiscal year, accountants must remember that,when compiling financial statements, an adjusting entry must be made to record the portion of expense applicable to thecurrent period. For example, if a business enterprise purchases a two year insurance policy for $1,200 at the end of thefirst year, half or $600 would be expensed as the portion applicable to the current period.

Posting

As can be seen in the illustration just given, when there are numerous transactions it would be difficult to determine theamounts in each account by reference to the journal entries. The next step in the accounting process is to summarize allof the transactions which affect each individual account. This step is referred to as posting. The transactions aretransferred from the journal into T-accounts. The T-account is a form of writing the account by placing the title of theaccount at the top, and drawing a vertical line beneath it in the form of a "T". Journal entries which are debits arerecorded on the left hand side of the line, and journal entries which are credits are recorded on the right hand side of theline. Once all the journal entries have been posted to T-accounts, all of the transactions affecting any particular accountare recorded together in one T-account. T-accounts display the same information which was recorded by date in thejournal and reorganizes it to be presented by account.

To continue with the illustration, four different accounts are affected by the transaction of January 1, 2010. These arecash, office building, Adam ) capital, and Brock ) capital, shown in Figure 2.

This transaction can also be used to show how the balance sheet equation works, as shown in Figure 3.

©Copyright: 2011 by the UBC Real Estate Division

Introduction to Financial Statements

4.9

ASSETS = LIABILITIES + OWNERS' EQUITY1/1/10 Cash $100,000 Adam - Capital $80,000

OfficeBldg. 60,000 Brock - Capital 80,000

$160,000 $160,000

Figure 3Balance Sheet Equation

The office building is recorded at its fair market value as of January 1, 2010 (i.e., this is what the partnership would havehad to pay for that particular office building on that date). From the point of view of the partnership, it is consideredthat the office building was acquired from Mr. Brock on January 1, 2010 for its fair market value. On December 31,2010 if the partnership were to prepare financial statements, and on this date the fair market value of the office buildingis $100,000, it would not mean that the partnership could record the office building at $100,000. Nor does it mean thatMr. Brock's equity in the partnership has increased by $40,000. In essence, on January 1, 2010 Mr. Brock transferredhis rights on the office building to the partnership.

Trial Balance

The posting step in the accounting process is followed by preparation of a trial balance. The purpose of preparing a trialbalance is to isolate any errors that might have taken place in journalizing and posting and facilitate the preparation offinancial statements. In the preparation of the trial balance, the sum of the debit column and the sum of the credit columnof each T-account are calculated, and the lesser of these two sums is subtracted from the greater sum. The differenceis the balance for that T-account at the end of the financial period. For example, if the sum of the debit column is greaterthan the sum of the credit column, then the sum of the credit column is subtracted from the sum of the debit column, andthe account will have a debit balance. Similarly, if the sum of the credit column is greater than the sum of the debitcolumn, the account will have a credit balance.

Once the balance is calculated for each account, the account names are listed in a trial balance, and their debit or creditbalances are placed in the debit and credit columns respectively. Because of the offsetting nature of the journal entries,the sum of the debit column for all accounts in the trial balance must be equal to the sum of the credit column for allaccounts. If the totals of the two columns are not equal, then there has been an error in either the journalizing or postingsteps which must be corrected.

Illustration 2

The following detailed example itemizes the activities of the initial partnership over the fiscal year which endsDecember 31. Remember to consider the entry previously discussed in Illustration 1. Rather than including the date,numbers are used at the end of each transaction description so that you can follow the posting process more easily.

Transactions:

C On January 15, 2010 the partnership purchased office supplies of $800 on credit. At December 31, aninventory count revealed $250 of office supplies left (2) and (12).

C On January 18, they purchased a house and land in Coquitlam for $160,000. It was determined that the fair marketvalue of the house was $120,000 and the lot was $80,000. The partnership was able to purchase the house at areduced price because the vendors had already purchased another house in Surrey and were unable to keep up themortgage payments on both houses. The partnership paid for this house by paying down $50,000 cash and takingout a mortgage of $110,000 at 12% per annum, compounded monthly and due January 18, 2023 (3).

©Copyright: 2011 by the UBC Real Estate Division

Chapter 4

4.10

(1) Cash 100,000Office Building 60,000

Adam - capital 80,000Brock - capital 80,000

(2) Office Supplies 800Accounts Payable 800

(3) Rental property - house 96,000Land 64,000

Cash 50,000Mortgage 110,000

C It was estimated that the house would last 16 years more and at the end of this time would have no scrap value.

C On January 30, the supplies purchased on credit were paid for (4).

C On February 1, the house was rented to Harvey Treefall for $1,500 per month. Terms of the lease were that$500 had to be paid as security deposit with each month's rent payable on the first of each month. Mr. Treefallpaid $2,000 in cash for the month of February (5).

C Throughout 2010, Mr. Treefall paid his rent on time except for the months of November and December becausehe was laid off and was unable to meet his rental payments. Mr. Treefall was a good tenant and the partnershipfelt that he would be able to find employment in January 2011 when the economy improved (11).

C Utilities expenses for the year on the office building amount to $3,500 which was paid for in cash (6).

C During the year the partnership found it necessary to hire some part-time employees for a total of $12,000. Asof December 31, $2,000 of this was not yet paid to the employees (7).

C On February 1, the partnership took out a three year insurance policy on the office building for $3,600. Thisamount was paid on February 1 (8).

C Property taxes for 2010 on the office building and the rental property amounted to a total of $2,400 of which$2,000 was paid on June 30 and $400 was still unpaid at December 31 (9).

C Interest expense for the year on the mortgage amounted to $12,100. A total of $13,000 was paid to themortgage company during 2005 (10). In 2010, it was estimated that $3,000 would be paid off the principal ofthe mortgage. All amounts were paid on time to the mortgage company during 2010.

Illustration of Journalizing

The journal entries to record the above transactions follow.

In this entry the total cost of the house and land is $160,000, which is less than its fair market value (FMV). In orderto comply with the cost and objectivity principles, the house and land must be recorded at cost to the partnership. Thereis no breakdown of how much of the cost is attributable to the land and how much is attributable to the house. Since theFMV of the house and land are known, these amounts are used to allocate the partnership's cost. The FMV of the houseis 60% of the total FMV of both the house and land; therefore, 60% of the total cost is allocated to the house (60% of

©Copyright: 2011 by the UBC Real Estate Division

Introduction to Financial Statements

4.11

(4) Accounts Payable 800Cash 800

(5) Cash 2,000Rental revenue 1,500Security deposit 500

(6) Utilities expense 3,500Cash 3,500

(7) Wages expense 12,000Cash 10,000Wages payable 2,000

(8) Prepaid insurance 3,600Cash 3,600

(9) Property tax expense 2,400Cash 2,000Property taxes payable 400

Similar to entry (7)

(10) Interest expense 12,100Mortgage payable 900

Cash 13,000

(11) Cash 12,000Rental revenue 12,000

$160,000 = $96,000). The FMV of the land is 40% of the total FMV and $64,000 (40% of $160,000) would beallocated to the land.

It is necessary to separate the house and land since the house is depreciable and the land is not. Depreciation can be takenonly on the house ) not on the land.

The employees rendered service to the partnership in 2010 in the amount of $12,000. Although only $10,000 was paidin cash as at the end of the fiscal year, the 2010 wages expense is $12,000 and not $10,000 (in accordance with thematching principle which is based on the accrual basis of accounting).

This amount, like Entry (2), is put into an asset account, not an expense account. An adjusting entry will have to bemade at the end of the fiscal year to record the amount that has been consumed during 2010 (in accordance with thematching principle).

©Copyright: 2011 by the UBC Real Estate Division

Chapter 4

4.12

(12) Office supplies expense 550Office supplies 550

(13) Rent receivable 3,000Rental revenue 3,000

(14) Insurance expense 1,100Prepaid insurance 1,100

(15) Depreciation expense 10,500Accumulated depreciation:

Office building 5,000Accumulated depreciation:

Rental property 5,500

In practice, Entries (6), (7), (10), and (11) would not be made in the manner illustrated, since these transactions tookplace over the year, and an entry would be made each month. The method used was adopted solely in the interests ofsimplification.

In Entries (5) and (11), remember that Mr. Treefall has paid only nine months' rent in 2010 and he should have paideleven months'. This entry records $12,000 (eight months' rent from March to October). Entry (5) records rentreceived from Mr. Treefall for the first month of his tenancy ) February.

Illustration of Adjusting Entries

In Entry (2), when the office supplies were purchased, an asset account was debited. At the end of the year the inventoryrevealed that $550 worth of the supplies were used ($800 purchased less $250 left at the end of the year); thus anadjusting entry must be made to record this.

This entry records rent earned by the partnership for November and December but not yet paid for by Mr. Treefall. Itis necessary to conform to the revenue principle as well as the accrual basis of accounting.

When the insurance policy was paid on February 1, it was for a three year term. Each 12 months the insurance expenseused up would be $1,200 (one-third of $3,600). However, in 2010 only 11 months have elapsed since the purchase ofthe insurance policy; therefore, it is appropriate to record as an expense only 11/12 of the annual amount.

Depreciation can be calculated several ways. However, this discussion will focus on the straight line method.

Under the straight line method, an estimate is made at the time an asset is purchased (its acquisition date) of how manyyears the asset will be of economic benefit to the enterprise (the asset's economic life). In other words, for how manyyears will the asset be beneficial to the enterprise in contributing to revenue? An estimate is also made for the amountthat can be realized from the sale of the asset at the end of its useful life (referred to as the salvage value of the asset).Since the enterprise may expect to recover some of the cost of the asset when it is resold, it would be illogical to expenseall of the original cost of the asset since not all of its cost will be consumed by the business enterprise. The economic

©Copyright: 2011 by the UBC Real Estate Division

Original Cost & Salvage ValueEstimated Life

60,000 & 10,00010 years

Original Cost & Salvage ValueEstimated Life

96,000 & 016 years

Introduction to Financial Statements

4.13

life of a building is determined through consultation with experts who can estimate how long a building will last,considering the use to which it is put.

The depreciation expense is then computed by subtracting the estimated salvage value from the cost of the asset anddividing the remaining amount by the estimated number of years the asset will be of use. (Note that it is possible forthe estimated salvage value to be zero.) This figure will be the amount of depreciation expense that will be recorded eachyear as long as the asset is being used to generate revenues.

For this example, the office building's depreciation is arrived at in the following manner:

= Yearly Depreciation

= $ 5,000 per year

For the rental property, depreciation expense is calculated as follows:

= Yearly Depreciation

= $ 6,000 per year

However, the rental property was only put to use to generate revenues for 11 months in 2010; thus, 11/12 × $6,000= $5,500, the depreciation expense recorded for 2010.

The Accumulated Depreciation account which is used in the above journal entry to record the depreciation of an assetis a separate type of account, known as a contra asset account. This accumulated depreciation contra account is shownseparately on the financial statements and serves to offset its related asset account (refer to Figure 7). By using a contraaccount, decreases in the book value of an asset due to depreciation can be accumulated with credit entries, and the creditbalance in this account will show the total amount of depreciation in the asset to date. The reason for accumulatingdepreciation separately in a contra account rather than deducting it directly from the asset account is that doing this allowsusers to identify the original book value of the asset and the cumulative amount of depreciation claimed with respect tothat asset.

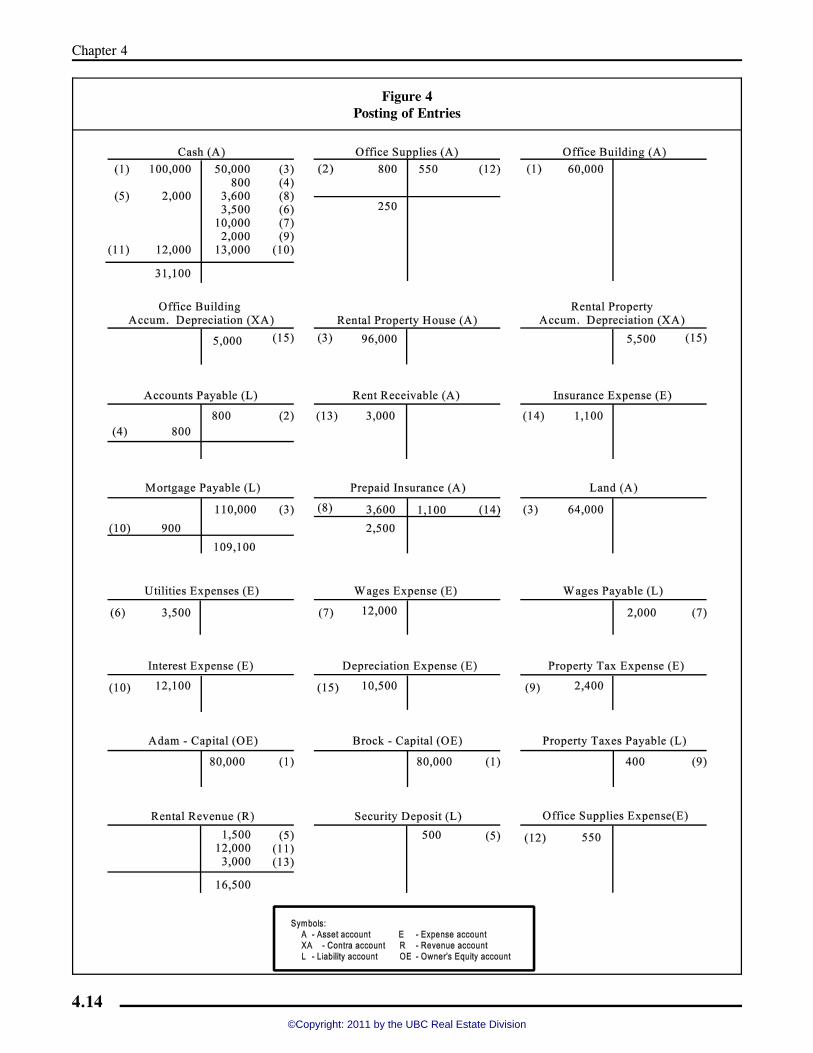

Illustration of Posting

Figure 4 illustrates the posting of the above entries into T-accounts.

Illustration of Trial Balance

After the entries have been posted, a trial balance is taken. Each account will first be totalled as illustrated in Figure 4and then a trial balance will be prepared as shown in Figure 5.

From the trial balance, the financial statements: balance sheet, income statement, and statement of changes in financialposition can be prepared. The first two are discussed in this chapter; the final statement is discussed in the next chapter.

©Copyright: 2011 by the UBC Real Estate Division

Chapter 4

4.14

Figure 4Posting of Entries

©Copyright: 2011 by the UBC Real Estate Division

Introduction to Financial Statements

4.15

DEBIT CREDIT

Cash $ 31,100 $Office supplies 250Office building 60,000

accumulated depreciation 5,000Rental property 96,000

accumulated depreciation 5,500Accounts payable 0Rent receivable 3,000Mortgage payable 109,100Land 64,000Security deposit 500Wages payable 2,000Property taxes payable 400Prepaid insurance 2,500Adam - capital 80,000Brock - capital 80,000Utilities expense 3,500Wages expense 12,000Interest expense 12,100Depreciation expense 10,500Insurance expense 1,100Property tax expense 2,400Office supplies expense 550Rental revenue 16,500

$ 299,000 $ 299,000

Figure 5Adam and Brock Partnership

Trial BalanceAs at December 31, 2010

The Financial Statements

Information about business transactions is communicated to external users through the medium of three financialstatements. The financial statements are the:

C income statement;C balance sheet (or statement of financial position); andC statement of cash flows.

The format of these statements is slightly different depending on the type of business enterprise. Some of thesedifferences include the following:

C The income statement of a partnership and proprietorship would not contain an expense account called incometax expense, whereas it would be included in a corporation's income statement.

C The owners' equity accounts of a sole proprietorship and partnership would be placed in one account on thebalance sheet; the account name would be the name of the proprietor or each partner. In a corporation, theowners' equity accounts are split into two separate accounts: the share capital account and the retained earningsaccount.

©Copyright: 2011 by the UBC Real Estate Division

Chapter 4

4.16

The Operating Statement (Revenue or Income Statement)

The Operating Statement is a listing of the revenue and expenses of an entity enterprise for a particular period of time,usually one year. This is different from the Balance Sheet, which shows the assets, liabilities, and owners' equity at aparticular date. The operating statement may be for any period of time ) for one month, a quarter, six months, or ayear. It would not usually be drawn up for a period exceeding one year. The operating statement can be seen as amotion picture covering a period of time. The general format of the operating statement is:

Revenue ! Expenses = Surplus (or Deficit)

Fiscal Year

Financial statements are compiled for a business enterprise at least once a year on the enterprise's fiscal year end. Thisfiscal year is a period of twelve months chosen by the business as the accounting period. It is not necessary that the fiscalyear end be the calendar year end. All business enterprises are free to choose whatever date they wish, but oncespecified, cannot change it at will.

Income Statement: Revenue and Expenses

Expenses may be defined as the cost of assets consumed in order to produce revenue. When the total revenues for aparticular period exceed the total expenses from that period, the difference is referred to as net income. When the reverseis true (total expenses for the period are greater than total revenues for that period) the difference is referred to as netloss.

The amount of the net income or net loss is closed off to the owners' equity account in the balance sheet. In the case ofa proprietorship, net income would increase the capital account of the proprietor or partners whereas a net loss wouldreduce these accounts. In a corporation, the net income or net loss is closed off to the retained earnings account. Thisthen serves as the connecting link between the income statement and the balance sheet. For example if, at the start ofthe period, the owners' equity account contained $100,000 and the enterprise suffered a loss of $15,000, the owners'equity account would now contain $85,000. If instead of a loss of $15,000 there was net income of $15,000, the owners'equity account would then be $115,000.

Some of the more common types of revenue include the following.

C Sales revenue is revenue realized from the sale of goods.C Service revenue is revenue realized from the rendering of services such as the services rendered by a physician

or accountant.C Interest revenue is revenue realized from lending money or placing money in a bank account.C Rental revenue is revenue realized from the renting or leasing of space the business owns.

Some of the more common types of expenses include the following:

C Cost of Goods Sold: In a business enterprise that derives its revenue through the sale of goods, the cost of goodssold would include the cost to the enterprise of purchasing or manufacturing the goods offered for sale. Thistype of account would not be present in a service enterprise.

This amount is calculated by a simple formula:

Beginning Inventory+ Purchases! Ending Inventory= Cost of Goods Sold (COGS)

©Copyright: 2011 by the UBC Real Estate Division

Introduction to Financial Statements

4.17

Rental revenue $ 16,500Expenses:

Utilities $ 3,500Wages 12,000Interest 12,100Depreciation 10,500Insurance 1,100Property Taxes 2,400Office supplies 550 42,150

Net Income (loss) ($ 25,650)

Figure 6Adam and Brock Partnership

Income StatementAs at December 31, 2010

When a business enterprise acquires goods for resale it does not expense them until they are actually sold. Totreat the cost of these goods as an expense to the enterprise before they are sold would violate the matchingprinciple. Hence, the cost of goods sold account is necessary in order to determine what the cost of theenterprise's revenues is for a given period of time.

C Interest expense is the cost of using borrowed money.

C Depreciation expense is the method used to allocate the cost of assets over a period of time.

Figure 6 illustrates the Income Statement for Adam and Brock Partnership.

The Balance Sheet (or Statement of Financial Position)

A balance sheet (also known as the statement of financial position or the statement of assets and liabilities) is a listingof the assets, liabilities, and owners' equity of a business enterprise at a specific date. It is analogous to the listing ofan inventory at a specific time.

On one hand, the balance sheet shows the assets of the enterprise ) the items of value owned by the enterprise ) and,on the other hand, it shows how these assets have been financed. An entity acquires assets either by borrowing themoney from creditors (debt financing) or by using the money provided by the owners for the enterprise (equity).Therefore, there are two sources of financing for the acquisition of assets – creditors and owners. The liabilities of anentity are the items of value owed by the enterprise. The liabilities represent the equity that the creditors have in theenterprise, whereas owners’ equity is, as the name implies, the equity that the owners have in the entity. It follows then,that the total of the assets of an entity must equal a total of its sources of capital.

As you have learned, the relationship between these three elements is expressed by the balance sheet equation:

Assets = Liabilities + Owners' Equity

Another way of looking at the balance sheet is to think that when a business acquires assets, it does so either byborrowing the money from creditors or by using the money provided by the owners of the enterprise. Therefore, thereare two sources of financing assets: creditors and owners. It follows, then, that the total of the assets of a businessenterprise must equal the total of its sources of capital.

©Copyright: 2011 by the UBC Real Estate Division

Chapter 4

4.18

Balance Sheet Classifications

Apart from a listing of the assets, liabilities, and owners' equity in the balance sheet, accountants also attempt to classifyassets and liabilities.

Current Assets: Current assets are those assets that will either be converted into cash, sold, or consumed within oneyear or the normal operating cycle of the business, whichever is longer. Current assets are listed in order of liquidity(the items that are most readily converted into cash would be listed first). Examples of current assets include cash,marketable securities, accounts receivable, rent receivable, inventories, and prepaid expenses.

C Marketable securities are temporary investments of a business enterprise in the securities of another entity. Inorder for this type of investment to be classified as a current asset, it must meet two criteria:- the investment must be readily convertible into cash; and- management must not intend to keep the investment for more than one year.If the market value of temporary investments is readily available (as, for example, would be the case if theinvestment was traded on an exchange), the investment should be revalued to market value each time thatfinancial statements are prepared with the revaluation gain or loss being treated as revenue or expense.

C Accounts receivable are amounts due from customers for the sale of goods or rendering of services for whichcash has not been received.

C Inventories include items that are held for resale to customers and supplies used in the business.

C Prepaid expenses represent services or rights to services for which cash has been paid but the services have notyet been consumed.

Non-Current (Fixed) Assets: Non-current assets are those that will not be sold or consumed within one year or thenormal operating cycle of the business. These include investments that management has no intention of selling withina year as well as property, plant, and equipment.

The assets included under the caption property, plant, and equipment are those assets from which benefit or use can bederived over more than one accounting period. Because the benefits from these assets last more than one accountingperiod, the matching principle dictates that we cannot charge off in one year the cost of these assets. We must allocatethe cost of these assets over the period they will benefit the firm. This allocation is accomplished by recording thedepreciation adjusting entry.

A point of caution is required here for those who have had some experience with the tax system of depreciation, knownas capital cost allowance. While the subject of income tax is covered in another chapter, it is important to realize thatthe Income Tax Act only governs how a tax return is computed. It does not dictate what method or amount ofdepreciation is to be recorded in the accounting records.

Current Liabilities: Current liabilities are those liabilities that the enterprise expects to pay off within a year. Examplesof current liabilities would include accounts payable, tenants' deposits, interest payable, property taxes payable, wagespayable, and income taxes payable.

C Accounts payable represent amounts owed by the business enterprise to suppliers of goods and/or services whichhave already been received but not yet paid for in cash.

C Property taxes payable are those taxes which have accrued but have not yet been paid in cash.

C Wages payable are wages owed to employees. Employees are not usually paid in advance. Usually businessesretain employees' wages until after a two week period of work has been done. These wages, for which anemployee has rendered service but has not yet been paid, will fall under this category.

©Copyright: 2011 by the UBC Real Estate Division

Introduction to Financial Statements

4.19

C As mentioned, income taxes payable would not be present on the financial statements of a partnership orproprietorship but would appear on the financial statements of a corporation. They represent the amount ofincome taxes owed.

C Tenants' deposits are amounts paid in advance by the tenants for security purposes. They represent a liabilityin the hands of the landlord since cash has been received for service not yet rendered.

Noncurrent (Long-term) Liabilities: Noncurrent liabilities are those liabilities that are not expected to be paid withinone year. The most common of these from a borrower's viewpoint would be mortgages payable ) the amount stillowing on the principal of the mortgage. It is important to note that the amount of the principal owing on the mortgagefor the following year is deducted from the noncurrent liabilities and is included in current liabilities. Also note that inthe Adam and Brock example, no adjusting journal entry was necessary to reflect the allocation of $3,000 from long termmortgage payable to the current portion of mortgage payable. This is an internal allocation, and will only appear on thebalance sheet.

Differences in Accounts of Various Types of Business Enterprises

As mentioned earlier, there are slight differences in the wording of the different types of accounts used by the threedifferent forms of business organization. Regardless of the type of business organization, assets and liabilities wouldbe the same.

However, differences as to the type of account take place in the owners' equity section. In a proprietorship, the equitysection would usually be entitled Joe Forsey ) capital. This account would reflect all of the investments made by theowner in the business, profits, and withdrawals.

For a partnership, the equity section would retain a capital account for each of the partners and, as for the proprietorship,investments, profits, and withdrawals made by each partner would be reflected in his or her capital account. In the caseof a corporation, the owners' equity is also referred to as shareholders' equity. In the shareholders' equity section thereare two major classifications. The first is referred to as share capital and represents the investment made by all of theshareholders of the corporation. The second part is known as retained earnings and represents the accumulation of netincome of the corporation from the time of its inception, less any withdrawals paid to the shareholders in the form ofdividends.

Figure 7 illustrates the Balance Sheet for Adam and Brock Partnership.

Reference to Figures 5 and 6 is required in order to construct a balance sheet for Adam and Brock Partnership. Allitems, except owners' equity, are transferred from Figure 5 onto the balance sheet (Figure 7). For a partnership, owners'equity (referred to as owners' capital) is the sum of all capital invested in the property plus net income minus net lossesminus cash withdrawals. Because this is an equal partnership, the net loss of $25,650 (see Figure 6) is shared equally.Thus, each partner's original capital of $80,000 is reduced by half of $25,650, or $12,825, resulting in capital for eachpartner of $67,175 (80,000 ! 12,825).

©Copyright: 2011 by the UBC Real Estate Division

Chapter 4

4.20

ASSETS

Current assets:Cash $ 31,100Rent receivable 3,000Prepaid insurance 2,500Office supplies 250

Total current assets $ 36,850

Noncurrent AssetsOffice building $ 60,000! less accumulated depreciation 5,000 55,000

Rental property 96,000! less accumulated depreciation 5,500 90,500Land 64,000

Total Noncurrent Assets 209,500Total Assets $ 246,350

LIABILITIES AND OWNERS' EQUITY

Current Liabilities:Wages payable $ 2,000Security deposit 500Property taxes payable 400Current portion of mortgage payable 3,000

Total Current Liabilities $ 5,900

Noncurrent Liabilities:Mortgage payable $ 109,100! less current portion 3,000

Total Noncurrent Liabilities 106,100Total Liabilities $ 112,000

Owners' Equity:Adam - capital $ 67,175Brock - capital 67,175 134,350

Total Liabilities and Owners' Equity $ 246,350

Figure 7Adam and Brock Partnership

Balance SheetAs at December 31, 2010

©Copyright: 2011 by the UBC Real Estate Division

Introduction to Financial Statements

4.21

Comparative Financial Statements

When you look at the annual reports of corporations, you will notice that more than one set of financial statements ispresented. These are referred to as comparative financial statements.

The accounting profession feels that the presentation of comparative financial statements enhances the usefulness of thestatements and brings out more clearly the nature and trends of current changes affecting the enterprise. What this typeof presentation emphasizes is the fact that statements for a series of periods are far more significant than those for a singleperiod and that the accounts for one period are only an installment in what is essentially a continuous history.

As you deal with the analysis of financial statements in the next chapter, you will see how it would be virtually impossibleto analyze financial statements if only one period were presented.

Explanatory Notes and Comments

Most sets of published financial statements include explanatory notes. These notes are an integral part of the financialstatements, whose purpose is to add clarity to the information conveyed. The notes indicate the actual accountingmethods used by the entity and disclose additional information to that which is presented in the three principal statements.A careful reading of the notes which are appended to the financial statements is necessary to obtain an understanding ofwhat is contained in the statements.

Limitations of Financial Statements

Reference was made earlier to the fact that the financial statements do not contain all of the information that is requiredfor users to make decisions. In addition to this, there are other limitations of financial statements:

C They are primarily quantitative in nature.C They are limited to individual business enterprises.C Some of the information contained in them is founded on estimates; for example, depreciation expense.C They are limited to past transactions; they report on what has already taken place;C They do not generally include increases in the market value of assets.

Conclusion

In this chapter we have introduced a number of accounting concepts and terms necessary for the proper interpretationand use of financial statements. While no detailed explanation of the accounting process has been given, most users offinancial statements can manage without extensive exposure to these procedures. The next chapter discusses cashbudgeting and the various methods used to analyze and interpret financial statements. It also provides information onaccounting and bookkeeping software packages.

©Copyright: 2011 by the UBC Real Estate Division

Chapter 4

4.22

APPENDIX 1Chart of Accounts (for a Corporation)

Balance Sheet Accounts

101 to 199 Asset Accounts 300 to 399 Owners' Equity Accounts101 General Bank Account 310 Common Stock104 Savings Account 330 Retained Earnings107 Trust Account 340 Dividends110 Temporary Investments 350 Income Summary114 Accounts Receivable117 Interest Receivable Income Statement Accounts120 Notes Receivable124 Representatives' Receivable 400 to 499 Revenue Accounts128 Prepaid Advertising 410 Residential Commissions130 Prepaid Insurance 420 Commercial Commissions132 Prepaid Rent 430 Referral Revenue140 Supplies Inventory 470 Appraisal Revenue145 Land 475 Miscellaneous150 Building 480 Interest151 Accumulated Depreciation - Building155 Automobiles 500 to 599 Expense Accounts156 Accumulated Depreciation - Automobiles 510 Commissions - Representatives160 Furniture & Fixtures 515 Commissions - Other Brokers161 Accumulated Depreciation - Furniture 520 M.L.S. Fees

& Fixtures 525 Referral fees165 Leasehold Improvements 530 Service fees166 Accumulated Amortization - Leasehold 535 Advertising

Improvements 540 Equipment Rental170 Franchise 550 Recruiting171 Accumulated Amortization - Franchise 555 Promotions175 Goodwill 560 Interest176 Accumulated Amortization - Goodwill 565 Maintenance

200 to 299 Liability Accounts 575 Property Taxes201 Bank Loans 580 Salaries & Wages210 Business Improvement Loans 585 Telephone215 Accounts Payable 590 Gas & Oil - Automobiles220 Interest Payable 595 Repair - Automobiles225 Salaries Payable 597 Utilities230 Employees' Withholding Payable 599 Income Taxes235 Client Trust Liability240 Commissions Payable245 M.L.S. Payable250 Other Brokers' Payable255 Bonus Payable260 Utilities Payable265 Property Taxes Payable270 Income Taxes Payable - Company

570 Office Supplies

Account numbers can be used to objectively identify accounts in order to avoid confusion between accounts with similarnames. Accounts are numbered within ranges to identify their types. For example, asset accounts are all numberedbetween 101 to 199 above. Note that this is not an exhaustive list.

©Copyright: 2011 by the UBC Real Estate Division