Embed Size (px)

Citation preview

DISCERNING TRENDS IN COMMODITY PRICES

WorkshoponCommoditySuperCycles– BankofCanada(Ottawa)April27‐28,2015

1DiscerningTrendsinCommodityPrices

DimitriDimitropoulosandAdonisYatchew

Motivation Commoditypricesaredrivenbyacomplexityofforces: depletionanddiscovery innovationandobsolescence competitionandstrategicbehaviour geopoliticsandconflict growth,developmentandbusinesscycles.

Ourdeparturepoint‐‐ pricetrendsarefundamentallynonparametric.

Thispaperappliesnonparametricmethodstopricedataon11commodities‐‐ 3hydrocarbonsand8metals‐‐ fortheperiod1900‐2014.

DiscerningTrendsinCommodityPrices 2

Nonparametric Modeling of TrendWedrawonthreeideasinthenonparametrics literaturetoconstructandestimateparsimoniousmodels:

1. ThePartialLinearModel

2. Cross‐Validation

3. ShapeSimilarity

DiscerningTrendsinCommodityPrices 3

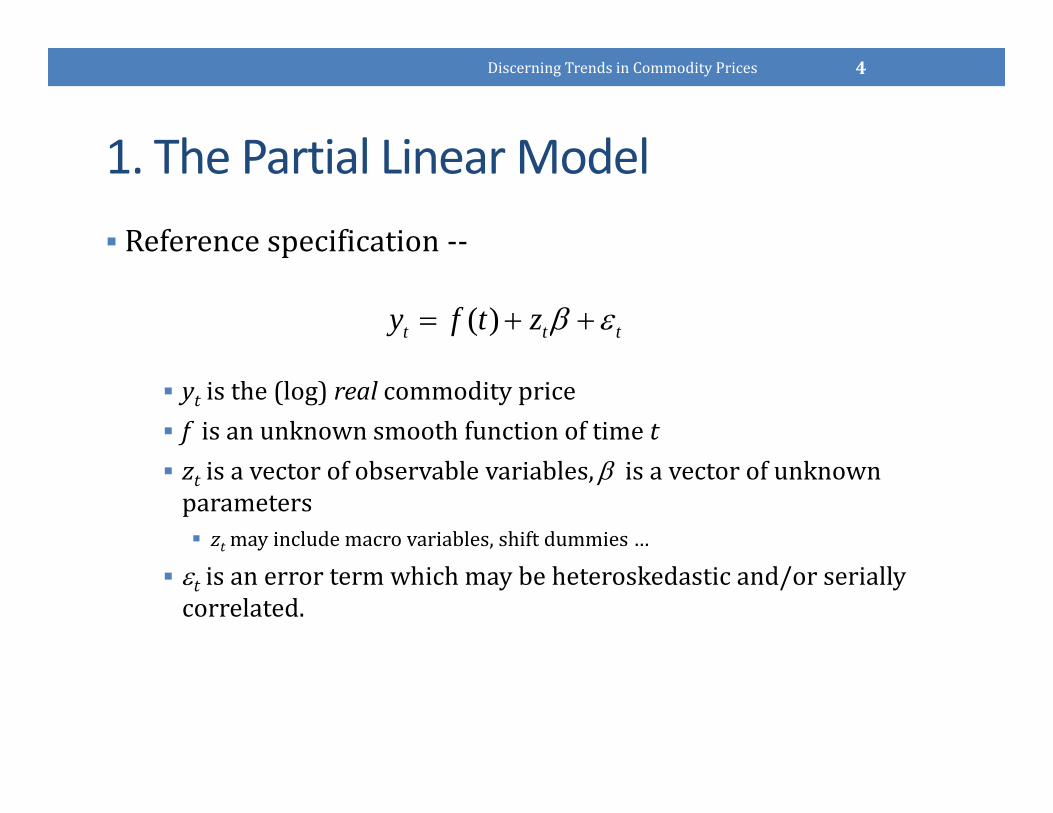

1. The Partial Linear Model Referencespecification‐‐

yt isthe(log)real commodityprice f isanunknownsmoothfunctionoftimet zt isavectorofobservablevariables, isavectorofunknownparameters ztmayincludemacrovariables,shiftdummies…

t isanerrortermwhichmaybeheteroskedasticand/orseriallycorrelated.

DiscerningTrendsinCommodityPrices 4

( )t t ty f t z

2. Cross‐Validation Considerapurenonparametrictrendmodel yt f(t) t.Nonparametricestimators‘smooth’thedata. Howdoesoneselectanappropriatedegreeofsmoothing?

Over‐smoothing Under‐smoothing

Minimizingthemeansquareerrorbychoosingthesmoothingparameterλwillnotwork– oneobtainsaperfectfit. Solution?Cross‐validation.

DiscerningTrendsinCommodityPrices 5

Year

log

pric

e

1900 1920 1940 1960 1980 2000

2.5

3.0

3.5

4.0

4.5

5.0

Oil

Yearlo

g pr

ice

1900 1920 1940 1960 1980 2000

2.5

3.0

3.5

4.0

4.5

5.0

Oil

21

1

ˆ ,T

tTt

y f t

2. Cross‐Validation in iid Setting Intheiid setting,cross‐validationpermitsoptimalselectionofthesmoothingparameterλ. Fixλ andforeacht,estimatef(t)whileomitting thet‐thobservation. Repeattheprocessoveragridofvaluesofλ. Selectthevalueofλthatminimizesmeansquarederror:

Essentially,determinationofthedegreeofsmoothingisbasedontheabilitytopredict‘outofsample’.

DiscerningTrendsinCommodityPrices 6

21

1

ˆmin .,t

T

tTt

fC y tV

2. Cross‐Validation in AR Setting Nearbyobservationsarenotstatisticallyindependent. Omittingindividual observationswillleadtoover‐fitting.

Solution?OmitobservationsinaneighborhoodN(t)ofeachpoint:

DiscerningTrendsinCommodityPrices 7

21

1mi ˆ ,n .N

T

tT tt

fCV ty

x

y

0.0 0.2 0.4 0.6 0.8 1.0

-0.1

0.0

0.1

0.2

0.3

True FunctionOver-fittingOptimal Smoothing

3. Shape Similarity

DiscerningTrendsinCommodityPrices 8

Year

log

pric

e

1900 1920 1940 1960 1980 2000

3.0

3.2

3.4

3.6

3.8

4.0

4.2

4.4

Coal

Year

log

pric

e

1900 1920 1940 1960 1980 2000

2.5

3.0

3.5

4.0

4.5

5.0

Oil

Model Features1. Ourparsimoniousspecificationbalancesflexibility

andprecision:i. Nonparametriccomponentallowsflexibleidentificationoftrend.ii. But,apurenonparametricmodelwherezvariablesarealsotreated

nonparametricallyissubjectto‘curseofdimensionality’.iii. Macroeconomiceffectsarearguablyamenabletoparametricmodeling,

e.g.,mightexpectunemploymenttohavemonotoneeffectoncopperprices.Shiftvariables,whichcapture‘regimechange’maybeincludedinthezvector.

2. Cross‐validationallowsdata‐drivendeterminationofsmoothnessparameter.

3. Toolsavailableforassessing/testingshapesimilarityoftrends.

DiscerningTrendsinCommodityPrices 9

( )t t ty f t z

Model Estimation ‐consistentestimatesofthecoefficientsonthez’s canbeobtainedbyregressingthe‘detrended’priceonthe‘detrended’parametricvariables

Sincetheresidualsarelikelyheteroskedasticandseriallycorrelated,wereportNewey‐Weststandarderrors,adaptedtothecurrentsetting.

Afterremovingtheestimatedparametriceffects,thetrendeffectcanbeestimatedbyperformingnonparametricregressiononthemodel

Asymptoticconfidencebandscanbeconstructedaroundtheestimateofnonparametricfunctiontogaugeprecisionofestimatedtrend.

DiscerningTrendsinCommodityPrices 10

[ | ] [ | ] .t t t t ty E y t z E z t

n

ˆ .t t ty z f t

Endogeneity Issues Inestimatingtheparametriceffects,wehaveastandardregressionmodeloftheform

where

However,inmodelingoilprices,ormoregenerallyhydrocarbonprices,certainmacroeconomicvariables(e.g.,unemployment)arelikelytobecorrelatedwiththeresidual.

Inthesecasesweapplyinstrumentalvariableestimationtothepartiallinearmodel.

DiscerningTrendsinCommodityPrices 11

* *t t ty z

* *[ | ] and [ | ]t t t t t ty y E y t z z E z t

Data Pricesof11commodities:3hydrocarbons(oil,naturalgas,coal)and8metals(copper,nickel,zinc,iron,tin,silver,lead,aluminium)fortheperiod1901to2014.

MainsourceisManthy (1978),fromwhichweobtainthecommoditypriceseriesandthewholesalepriceindexpriorto1973.

Additionalsourcesareusedtoupdatethedatato2014. Thepriceseriesforoil,naturalgasandcoalareaugmentedusingpricespublishedbytheUSEnergyInformationAdministration(EIA).

Formetalsprices,theUSGeologicalSurveyHistoricalStatisticsforMineralandMaterialCommoditiesintheUnitedStates isusedtocompletethetimeseriesto2012,andLMEpricesthroughto2014.

ThewholesalepriceindexisupdatedusingtheProducerPriceIndex(Commodities) aspublishedbytheU.S.BureauofLaborStatistics.

DiscerningTrendsinCommodityPrices 12

Data Macroeconomicvariablesareincludedtocontrolforshorttermbusinesscycledynamicsandlongertermeconomicgrowthtrends; growthrateoftheGrossDomesticProduct(GDP)of20OECDcountriesaswellas6developingcountries. Source:MaddisonProject'sStatisticsonWorldPopulationandGDP1‐2010,updatedto2014usingWorldBank'sWorldDevelopmentIndicatorsdatabase.

USunemploymentrateseriesconstructedfromLesbergott (‘57)fortheperiod1900‐42,andfromtheBureauofLaborStatisticsthroughto2014.

UKunemploymentrateseriesconstructedfromDenmanandMcDonald(‘96)fortheperiod1900‐70,andfromtheOfficeofNationalStatisticsthroughto2014.

Indicatorvariablesforeventsthatareexpectedtohaveinfluencedcommodityprices,e.g.,OPECactionsin1973,U.S.Federalminingandenvironmentallegislationinthelate1960s.

DiscerningTrendsinCommodityPrices 13

Hotelling and His Descendants

HotellingRuletellsusthattherealpriceofanexhaustibleresourceshouldbetrendingupwardinthelongrun.

However,suchpredictionsaretypicallyrejectedbydata,aspricesareoftenobservedtofall,atleastovercertainperiodsoftime.

Inattemptstorationalizethisphenomenon,variousauthorshaveproposedextensionsofthebasicframeworktoallowforU‐shapedtrends,oscillatorytrends,structuralbreaks….

DiscerningTrendsinCommodityPrices 14

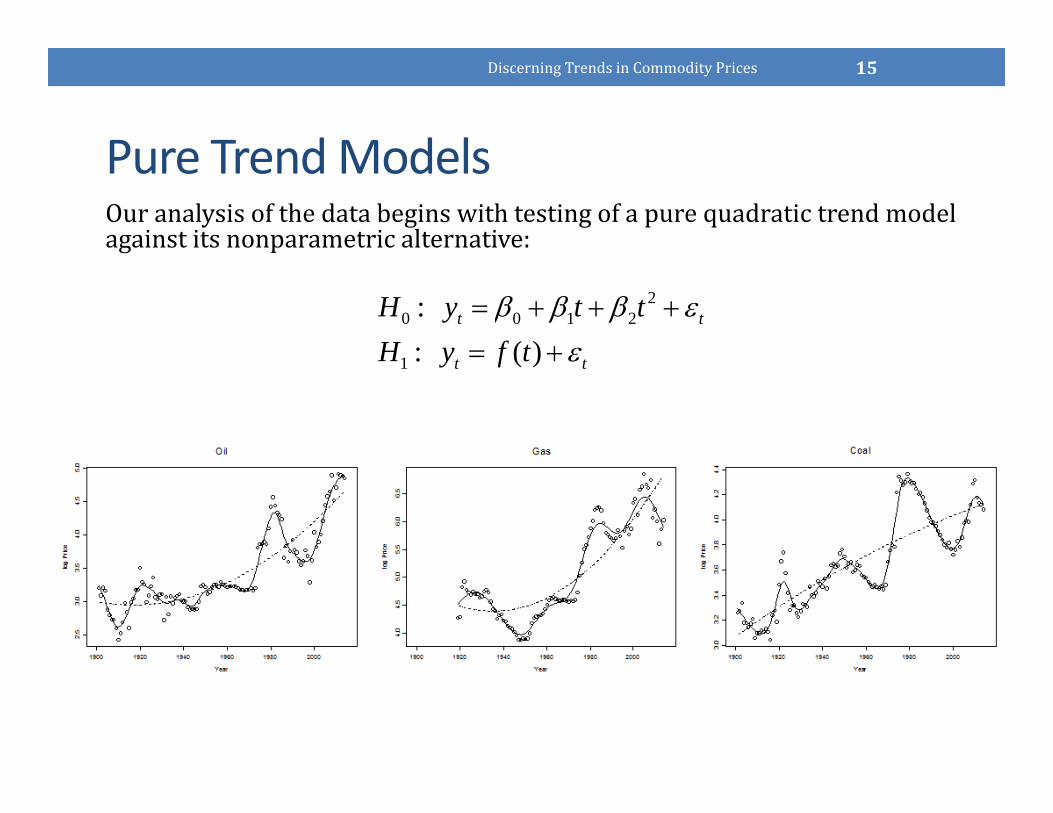

Pure Trend ModelsOuranalysisofthedatabeginswithtestingofapurequadratictrendmodelagainstitsnonparametricalternative:

V15.8 V10.6 V27.2

DiscerningTrendsinCommodityPrices 15

20 0 1 2

1

: : ( )

t t

t t

H y t tH y f t

DiscerningTrendsinCommodityPrices 16

Pure Trend Models Inmostcasesthequadratictrendmodelisrejectedinfavourofthenonparametricversion,theexceptionsbeingzinc,leadandaluminum.

Casualinspectionsuggestsdegreeofshapesimilarityamongvariousgroups:(i)hydrocarbons,(ii)copper‐nickel,(iii)iron‐tin.

Aluminumisonlycommoditythatdisplaysastrongseculardownwardtrend.

Weconsidermoreformallywhethercertaincommoditiesbearshapesimilarityintheirlongertermtrendsbycomparingindividualtrendsagainstapooledestimate,togetherwithits95%uniformconfidenceband.

DiscerningTrendsinCommodityPrices 17

Pure Trend Models ‐‐ Shape Similarity

Boththeoilandgastrendestimatesliewithinthepooleduniformbandformostofthedataperiod.

Beginningaround2009,theindividualpricetrendsdiverge‐‐ U.S.naturalgaspricesplummetfirst,asaresultofthefracking revolution,whileoilpricesremainhighuntillate2014,atwhichtimetheyalsoplunge.

DiscerningTrendsinCommodityPrices 18

YearPool

1920 1940 1960 1980 2000

-2-1

01

23

OilGasPooledUniform Conf Band

Oil and Gas -- Uniform Confidence Band

Pure Trend Models ‐‐ Shape Similarity

Bothoilandcoaltrendsfollowgenerallysimilarpaths,althoughtherearesomedifferencesintiming.

Formostofthe1901‐2014period,oilandcoaltrendsgenerallyliewithinthe95%uniformconfidenceboundsofthepooledtrendestimate.

DiscerningTrendsinCommodityPrices 19

YearPool

1900 1920 1940 1960 1980 2000

-2-1

01

23

OilcoalPooledUniform Conf Band

Oil and Coal -- Uniform Confidence Band

Pure Trend Models ‐‐ Shape Similarity

Metalspricesexhibitconsiderablevolatility,buttheestimatedtrendcurvesforcopperandnickel,andironandtin,showadegreeofsimilarity.

Inbothcases,theuniformboundsofthepooledestimatecapturetheindividualtrendpathsforeachofthemetalspairs.

DiscerningTrendsinCommodityPrices 20

Inclusion of Macro Variables

Wenowincorporateparametriceffectsintoourmodels,andestimatethepartiallinearmodeloftheform:

Smoothnessparametersaredeterminedthroughcross‐validation.

DiscerningTrendsinCommodityPrices 21

( )t t ty f t z

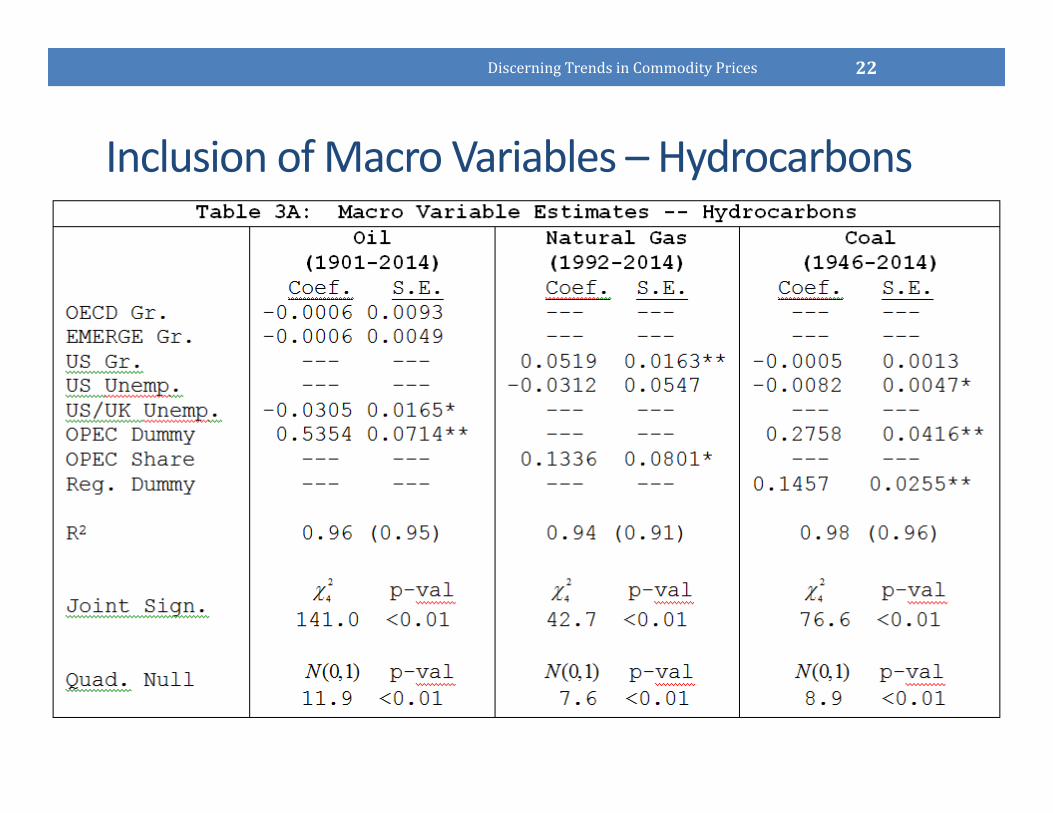

Inclusion of Macro Variables – Hydrocarbons

DiscerningTrendsinCommodityPrices 22

Inclusion of Macro Variables – Hydrocarbons

Theseexhibitstrongjointsignificanceinthemodelsforallthreefuels.

Theirinclusionwouldappeartohaveamodestimpactontotalexplanatorypower.Thereasonisthatinthepurenonparametricmodel,thetrendvariableispickingupmacroeffects.Inthepartiallinearmodel,theroleoftrenddeclinessignificantly.

Foroilprices, NeitherOECDnoremergingeconomiesgrowthrateshaveasignificantimpact. TheaverageUS/UKunemploymentrateismarginallysignificant. ThechangeinstrategicbehaviourbyOPECbeginninginlate1973isestimatedtoincreaseoilprices,onaverage,inexcessof50%.

DiscerningTrendsinCommodityPrices 23

Inclusion of Macro Variables – Hydrocarbons Fornaturalgasprices, Asthesemarketsareprimarilycontinental.WeuseU.S.pricesandthereforeU.S.growthandunemploymentrates.

Wefocusonpost1992data,asthismarketwentthroughaperiodofpriceconstraintsforinter‐statetradeuntiltheearly1990’s.(Estimatesfor1919‐2014areavailable.)

U.S.growthisastronglysignificantdriverofcontinentalnaturalgasprices,whileU.S.unemploymentisnot.

NotethatanOPECdummywouldnotbeidentified,sointhiscaseweincludetheOPECmarketshare‐‐ whichissignificantatthe10%level.

Forcoalprices, WeuseU.S.growthandunemploymentrates. Wefocusonthepost‐warperiod,1946‐2014. U.S.economicgrowthisnotasignificantfactorinexplainingthepriceseries,butunemploymentismarginallysignificantwithanegativeimpactonprices.

TheOPECeffectislargeandstronglysignificant,increasingcoalpricesinexcessof25%onaveragerelativetotrend.

The“RegulatoryDummy”‐‐ whichcapturestheimpactsofcoalminesafetylegislationpassedin1969,andtheamendmentstotheCleanAirActin1970‐‐isstronglystatisticallysignificant,increasingcoalpricesbyanestimated15%.

DiscerningTrendsinCommodityPrices 24

Inclusion of Macro Variables –Metals

DiscerningTrendsinCommodityPrices 25

Inclusion of Macro Variables –Metals Thereissubstantialvariationinthedata‐drivensmoothingparameter,leadingtoconsiderablevariationinthegoodness‐of‐fitacrossmodels.

Theparametricvariables– OECDandemergingeconomygrowthrates,andtheUS/UKunemploymentrate– arejointlysignificantin5outof8metals.

OECDgrowthratesaresignificantinthecopperandleadequations,whilegrowthinemergingeconomiesisstatisticallyinsignificantinallmodels.

Theunemploymentrateissignificantinexplainingcopper,iron,lead,tin,silverandzincprices.

DiscerningTrendsinCommodityPrices 26

Goodness of FitPureTrendModel PartialLinearModel

Total

Oil 1901‐2014 0.950 0.960 0.774 0.488

NaturalGas 1992‐2014 0.910 0.940 0.753 0.112

Coal 1946‐2014 0.960 0.980 0.497 0.640

Copper 1901‐2014 0.770 0.810 0.640 0.357

Nickel 1901‐2014 0.830 0.830 0.824 0.012

Zinc 1901‐2014 0.230 0.260 0.177 0.252

Iron 1901‐2014 0.920 0.930 0.867 0.403

Tin 1901‐2014 0.800 0.830 0.748 0.066

Silver 1901‐2014 0.900 0.910 0.870 0.029

Lead 1901‐2014 0.420 0.490 0.356 0.079

Aluminium 1901‐2014 0.930 0.930 0.922 0.006

DiscerningTrendsinCommodityPrices 27

Relationship to the Literatures

Deterministictrendmodels

Super‐cycles,spectralanalysis

Stochastictrendmodels

DiscerningTrendsinCommodityPrices 28

Concluding Comments Trendsarefunctionsofunknownshape– hencenonparametrictechniquesareuseful.

Estimationoftrendfunctioncanbeguidedbytheabilityoftheestimatortopredictoutofsample(cross‐validation).

Commoditytrendsmaydisplayshapesimilarity,atleastovercertainperiodsoftime.Thiscanimproveprecisionofestimationandanticipationofcertainscenarios.

DiscerningTrendsinCommodityPrices 29

Hydrocarbon Shape Similarity• Considerthehydrocarbontriad.From1946to2008thecorrelationsofthe(log)priceofoilwithgasandcoalare97%and98%respectively.

• Thengasandcoalpricesturndown.

• Perhapstherecentdropinoilpricesisnotentirelysurprising.

DiscerningTrendsinCommodityPrices 30

Year

YCoa

l

1960 1980 2000

3.6

3.8

4.0

4.2

4.4

Coal

Year

YG

as

1960 1980 2000

4.0

4.5

5.0

5.5

6.0

6.5

Gas

Year

YO

il

1960 1980 2000

3.0

3.5

4.0

4.5

Oil