Embed Size (px)

Citation preview

1

Directors’ Report Dear Shareholders, On behalf of the Board of Directors, the report on the performance of the Company for the first quarter ended 31st March, 2015 is presented below: Operations The parent company has made net profit of RO 1.2 m (2014: 1.4 m) on revenue of RO 85 m (2014: 94 m)and the consolidated net profit is RO 1.3 m (2014: RO 1.4 m) on revenue of RO 90m (2014: RO 98 m). We are pleased to inform that the company has received the commencement order for the ROP General Hospital Project. Further to our previous disclosure, the period of the Off Plot Delivery Contract (ODC) of North Oman has been extended for a further seven months commencing 1st September 2015. The Ras Al Hadd Airport project has been completed and the substantial completion certificate is awaited. Further, we have been awarded projects worth RO 46 Million during this quarter. As part of the company’s efforts to appoint the Omani cadre in managerial positions, Mr. Sulaiman Ahmed Ali Al Busaidi, a well –qualified and experienced cadre, has been appointed in the post of the Chief Internal Auditor. Outlook The Directors have the pleasure to inform you that the parent company continues to maintain an order book position in the range of over RO 690 million. We are expecting award of some more projects, which are already tendered. On Record We are elated and share in the joy of the nation on the return of His Majesty Sultan Qaboos bin Said to his beloved Sultanate and wish him good health, wellbeing and a long life. We are grateful to the Government and various Ministries for their support and for providing opportunities for the private sector to participate in the development of Oman’s economy. The Board would also like to thank our esteemed clients, Banks and Financial Institutions Consultants, Suppliers, Service Providers and Shareholders for their generous cooperation and continued support and the employees and management of the company for their commitment and dedication. Salim Said Hamad Al Fannah Al Araimi Chairman

Galfar Engineering & Contracting SAOG & Subsidiaries

Consolidated Statement of Financial Position As at 31st March, 2015 Amount in RO '000s

Notes Mar, 2015 Mar, 2014 Mar, 2015 Mar, 2014ASSETSNon-current AssetsProperty, plant and equipment 3 88,157 105,825 101,317 117,056 Intangible assets 4 1,048 1,422 22,233 7,017 Investment in subsidiaries 5 4,496 2,090 - - Investment in associates 6 8,706 8,706 4,738 6,254 Investment available for sale 125 125 145 145 Retentions receivables 9 31,335 34,382 31,360 34,382

133,867 152,550 159,793 164,854 Current AssetsInventories 7 18,598 34,982 19,426 35,791 Contract work in progress 8 68,782 57,451 71,286 59,190 Contract and trade receivables 9 223,532 206,654 235,048 211,288 Advances, prepayments and other receivables 10 27,882 22,245 25,254 25,811 Deposits with bank 11 1,293 3,508 1,296 3,551 Cash and bank balances 12 1,575 2,024 3,499 3,477

341,662 326,864 355,809 339,108 Total Assets 475,529 479,414 515,602 503,962 EQUITY AND LIABILITIES EquityShare capital 13 41,522 37,747 41,522 37,747 Share premium 14 18,337 23,370 18,337 23,370 Statutory reserve 15 13,840 12,582 14,093 12,772 Foreign currency translation reserve 16 - - (1,832) (1,403) Rretained earning 30,767 29,708 30,685 30,710 Non controlling inetrest - - 964 992 Total Equity 104,466 103,407 103,769 104,188 Non-current LiabilitiesTerm loans 18 68,667 47,079 76,318 47,899 Employees' end of service benefits 22 11,486 11,232 11,668 11,394 Advance payables 23 20,380 8,390 23,863 11,315 Deferred tax liability 24 5,743 6,679 6,342 7,109

106,276 73,380 118,191 77,717 Current LiabilitiesTerm loans -current portion 18 33,316 26,884 34,479 27,399 Short term loans 19 37,500 29,800 42,584 29,800 Bank borrowings 20 58,433 99,269 60,099 100,912 Trade payables 21 80,840 90,028 90,761 99,133 Other payables and provisions 23 54,080 55,062 62,371 61,437 Provision for taxation 24 618 1,584 3,348 3,376

264,787 302,627 293,642 322,057 Total Liabilities 371,063 376,007 411,833 399,774 Total Equity and Liabilities 475,529 479,414 515,602 503,962

Net Assets per share (RO) 32 0.252 0.274 0.248 0.273

The attached notes 1 to 34 form part of these consolidated financial statements.

Consolidated Parent Company

Galfar Engineering & Contracting SAOG & Subsidiaries

Consolidated Statement of Comprehensive IncomeFor the three months period ended 31st March, 2015 Amount in RO '000s

Notes Q1, 2015 Q1, 2014 Q1, 2015 Q1, 2014

Contract income 84,578 93,543 85,381 95,054

Sales and services income 25 786 724 4,414 3,321

Total revenue 85,364 94,267 89,795 98,375

Other income 26 601 377 574 399

Cost of contracts and sales 27 (79,433) (87,718) (83,016) (90,837)

Gross Profit 6,532 6,926 7,353 7,937

General and administrative expenses 28 (2,652) (2,854) (3,057) (3,351)

Profit / (loss) from operations 3,880 4,072 4,296 4,586

Financing costs, net 30 (2,452) (2,482) (2,681) (2,556)

Share in loss of associates 6 - - (71) (217)

Profit / (loss) before tax 1,428 1,590 1,544 1,813

Income tax expense 24 (175) (187) (269) (407)

1,253 1,403 1,275 1,406

Profit attributable to:

Equity shareholders of parent company 1,253 1,403 1,264 1,400

Non-controlling interests 11 6

1,253 1,403 1,275 1,406

Basic earnings per share 31 0.003 0.004 0.003 0.004

The attached notes 1 to 34 form part of these consolidated financial statements.

Consolidated

Profit / (loss) for the period

Parent Company

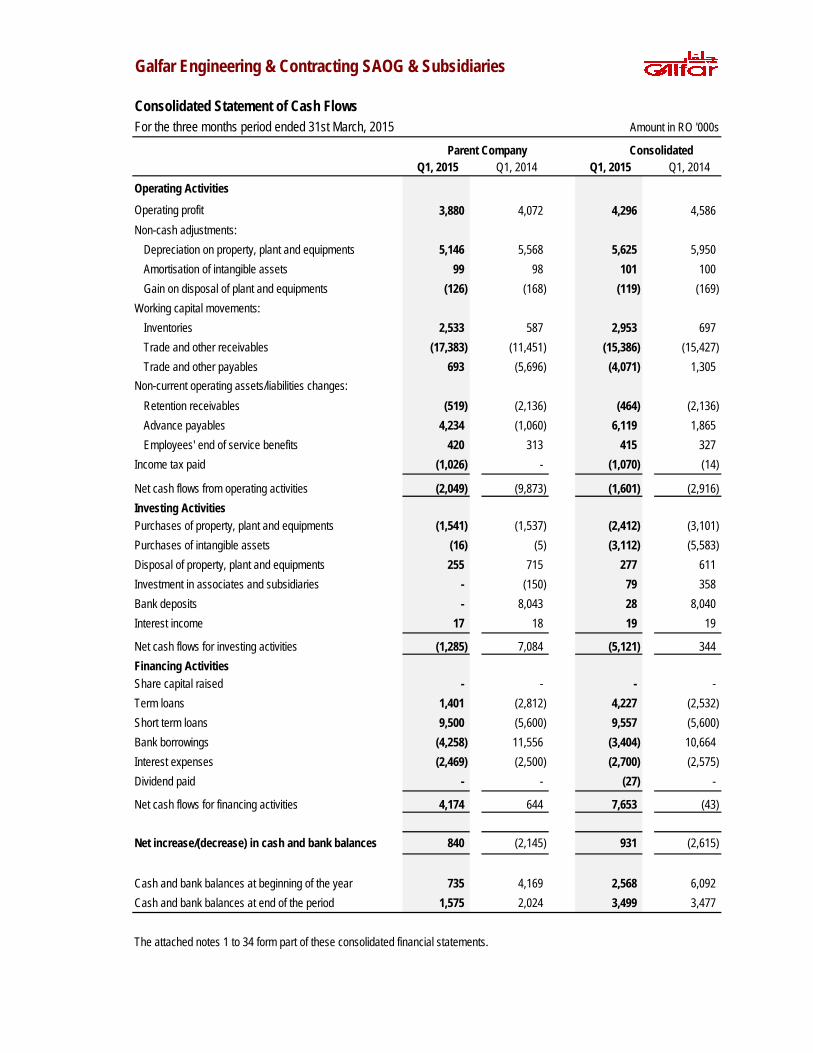

Galfar Engineering & Contracting SAOG & Subsidiaries

Consolidated Statement of Cash FlowsFor the three months period ended 31st March, 2015 Amount in RO '000s

Q1, 2015 Q1, 2014 Q1, 2015 Q1, 2014

Operating Activities

3,880 4,072 4,296 4,586 Non-cash adjustments:

Depreciation on property, plant and equipments 5,146 5,568 5,625 5,950 Amortisation of intangible assets 99 98 101 100 Gain on disposal of plant and equipments (126) (168) (119) (169)

Working capital movements:Inventories 2,533 587 2,953 697 Trade and other receivables (17,383) (11,451) (15,386) (15,427) Trade and other payables 693 (5,696) (4,071) 1,305

Retention receivables (519) (2,136) (464) (2,136) Advance payables 4,234 (1,060) 6,119 1,865 Employees' end of service benefits 420 313 415 327

Income tax paid (1,026) - (1,070) (14)

Net cash flows from operating activities (2,049) (9,873) (1,601) (2,916) Investing ActivitiesPurchases of property, plant and equipments (1,541) (1,537) (2,412) (3,101) Purchases of intangible assets (16) (5) (3,112) (5,583) Disposal of property, plant and equipments 255 715 277 611 Investment in associates and subsidiaries - (150) 79 358 Bank deposits - 8,043 28 8,040 Interest income 17 18 19 19

Net cash flows for investing activities (1,285) 7,084 (5,121) 344 Financing ActivitiesShare capital raised - - - - Term loans 1,401 (2,812) 4,227 (2,532) Short term loans 9,500 (5,600) 9,557 (5,600) Bank borrowings (4,258) 11,556 (3,404) 10,664 Interest expenses (2,469) (2,500) (2,700) (2,575) Dividend paid - - (27) -

Net cash flows for financing activities 4,174 644 7,653 (43)

Net increase/(decrease) in cash and bank balances 840 (2,145) 931 (2,615)

Cash and bank balances at beginning of the year 735 4,169 2,568 6,092 Cash and bank balances at end of the period 1,575 2,024 3,499 3,477

The attached notes 1 to 34 form part of these consolidated financial statements.

Parent Company Consolidated

Operating profit

Non-current operating assets/liabilities changes:

Galfar Engineering & Contracting SAOG & Subsidiaries

Statement of Changes in Equity -Parent CompanyFor the three months period ended 31st March, 2015 Amount in RO '000s

Share Capital Share Premium Statutory Reserve

Foreign Currency

Translation

Retained Earnings Total Grand

Total

Balance as at 1st January, 2015 37,747 23,370 12,582 29,514 103,213

Net comprehensive income for the period - - - 1,253 1,253

Transfer to statutory reserve - (1,258) 1,258 - -

Stock dividend 3,775 (3,775) - - -

Balance as at 31st March, 2015 41,522 18,337 13,840 30,767 104,466

Statement of Changes in Equity -Consolidated For the three months period ended 31st March, 2015Balance as at 1st January, 2015 37,747 23,370 12,835 (1,859) 29,421 101,514 980 102,494

Net comprehensive income for the period - - - - 1,264 1,264 11 1,275

Transfer to statutory reserve - (1,258) 1,258 - - - - -

Foreign currency translation reserve - - - 27 - 27 - 27

Stock dividend 3,775 (3,775) - - - - - -

Dividend paid - - - - - - (27) (27)

Balance as at 31st March, 2015 41,522 18,337 14,093 (1,832) 30,685 102,805 964 103,769

Attributable to equity holders of the parent companyNon

controlling interest

Galfar Engineering & Contracting SAOG & Subsidiaries

Notes to Consolidated Financial StatementsAs at 31st March, 2015

1. Activities

Galfar Engineering and Contracting SAOG (“the parent company”) is an Omani joint stock company registered under the Commercial Companies Law ofthe Sultanate of Oman and listed in Muscat Security Exchange.

The principal activities of Galfar Engineering and Contracting SAOG and its subsidiaries (“the group”) are road, bridge and airport construction, oil andgas including EPC works, civil and mechanical construction, public health engineering, electrical, plumbing and maintenance contracts and BOTprojects.

2. Significant Accounting Policies

Basis of preparationThese consolidated financial statements are prepared on the historical cost basis, as modified by the revaluation of derivative financial instruments atfair value through statement of comprehensive income , available-for-sale financial assets that have been measured at fair value and in accordance withInternational Financial Reporting Standards (IFRS), the requirements of the Commercial Companies Law of the Sultanate of Oman, 1974 (as amended)and comply with the disclosure requirements set out in the ‘Rules and Guidelines on Disclosure by issuer of Securities and Insider Trading’ issued by theCapital Market Authority (CMA) of the Sultanate of Oman.

The preparation of the consolidated financial statements requires management to make judgments, estimates and assumptions that affect thereported amount of financial assets and liabilities at the date of the financial statements and the resultant provisions and changes in fair value for theyear. Such estimates are necessarily based on assumptions about several factors involving varying, and possibly significant, degrees of judgment anduncertainty and actual results may differ from management’s estimates resulting in future changes in estimated assets and liabilities. The assumptionsconcerning the key sources of estimation uncertainty at the reporting date are set out in note 38.

These consolidated financial statements have been presented in Rial Omani which is the functional and reporting currency for these consolidatedfinancial statements and all values are rounded to nearest thousand (RO '000) except when otherwise indicated.

Change in accounting policy and disclosuresThe accounting policies are consistent with those used in the previous financial year.

Accounting PoliciesThe significant accounting policies adopted by the group are as follows:

Basis of consolidationThe consolidated financial statements comprise those of Galfar Engineering and Contracting SAOG, its subsidiaries and its associates as at closing ofeach period. A subsidiary is a company in which the parent company owns, directly or indirectly more than half of the voting power.

The subsidiary is consolidated from the date on which control is transferred to the group and ceases to be consolidated from the date on which control istransferred out of the group.

The financial statements of the subsidiary are prepared for the same reporting period as the parent company using consistent accounting policies.Adjustments are made to bring into line any dissimilar accounting policies which may exist.

All intercompany balances, income and expenses, unrealised gains and losses and dividends resulting from intra-group transactions are eliminated.

A change in the ownership interest of a subsidiary, without a change of control, is accounted for as an equity transaction.

Losses are attributed to the non-controlling interest even if that results in a deficit balance.

Galfar Engineering & Contracting SAOG & Subsidiaries

Notes to Consolidated Financial StatementsAs at 31st March, 2015

Investments in associatesThe group’s investments in its associates are accounted for under the equity method of accounting. In the parent company's separate financialstatements, the investment in an associate is carried at cost less impairment. An associate is an entity in which the group has significant influence andwhich is neither a subsidiary nor a joint venture.

Under the equity method, the investment in the associate is carried in the statement of financial position at cost plus post- acquisition changes in thegroup’s share of net assets of the associate. Goodwill relating to an associate is included in the carrying amount of the investment. After application ofthe equity method, the group determines whether it is necessary to recognise any additional impairment loss with respect to the group’s net investmentin the associate. The statement of comprehensive income reflects the share of the results of operations of the associate. Where there has been achange recognised directly in the equity of the associate, the group recognises its share of any changes and discloses this, when applicable, in thestatement of changes in equity. Profits and losses resulting from transactions between the group and the associate are eliminated to the extent of theinterest in the associate.

Property, plant and equipment All items of property, plant and equipment held for the use of group’s activities are recorded at cost less accumulated depreciation and any identifiedimpairment loss. Land is not depreciated. Such cost includes the cost of replacing part of the property, plant and equipment and borrowing costs forlong-term construction projects if the recognition criteria are met. When significant parts of property, plant and equipment are required to be replaced atintervals, the group recognises such parts as individual assets with specific useful lives and depreciation, respectively. Likewise, when a majorinspection is performed, its cost is recognised in the carrying amount of the plant and equipment as a replacement if the recognition criteria are satisfied.All other repair and maintenance costs are recognised in the statement of comprehensive income as incurred.

Depreciation is charged so as to write off the cost of property, plant and equipment over their estimated useful lives, using the straight line method, onthe following bases:

Buildings and camps over 15 & 4 yearsPlant and machinery over 7 & 10 years Motor vehicles and heavy equipment over 7 & 10 yearsFurniture and equipment over 6 yearsComputers and software over 5 yearsProject equipment and tools over 6 years

Items costing less than RO 100 are expensed out in the year of purchase.

The assets’ residual values, useful lives and methods of depreciation are reviewed at each financial year end. Where the carrying value of an asset isgreater than its estimated recoverable amount, it is written down immediately to its recoverable amount.

An item of property, plant and equipment and any significant part initially recognised is derecognised upon disposal or when no future economic benefitsare expected from its use or disposal. Any gain or loss arising on derecognition of the asset, calculated as the difference between the net disposalproceeds and the carrying amount of the asset is recognised in the statement of comprehensive income when the asset is derecognised.

Capital work in progress Properties in the course of construction for production, rental or administrative purposes, or for purposes not yet determined, are carried at cost, lessany recognised impairment loss. Depreciation of these assets, on the same basis as other property assets, commences when the assets are ready fortheir intended use.

Intangible assets Computer software:Computer software costs that are directly associated with identifiable and unique software products and have probable economic benefits exceeding the costs beyond one year are recognised as an intangible asset. Direct costs include staff costs of the software development team and an appropriateportion of relevant overheads. Computer software costs recognised as an asset are amortised using the straight-line method over the estimated usefullife of five years.

Galfar Engineering & Contracting SAOG & Subsidiaries

Notes to Consolidated Financial StatementsAs at 31st March, 2015

Concessionaire rights:Concessionaire rights arising from Design, Build, Finance, Operate and Transfer (DBFOT) road projects are shown at historical cost. These have a finiteuseful life and are carried at cost less accumulated amortisation. Amortisation is calculated using the straight-line method to allocate the cost ofintangible assets over their estimated lease period and is recognised in the statement of comprehensive income.

Available-for-sale investments Available-for-sale investments are initially recognised at cost, which includes transaction costs, and are, in general, subsequently carried atfair value. Available-for-sale equity investments that do not have a quoted market price in an active market, and for which other methods of reasonablyestimating fair value are inappropriate, are measured at cost, as reduced by allowances for estimated impairment. Changes in fair value arereported as other comprehensive income.

An assessment is made at each reporting date to determine whether there is objective evidence that an investment may be impaired. If such evidenceexists, any impairment loss (being the difference between cost and fair value, less any impairment loss previously recognised) is removed from othercomprehensive income and recognised in the income statement.

Inventories Inventories are stated at the lower of cost and net realisable value. Cost comprises purchase price and all direct costs incurred in bringing theinventories to their present location and condition. Cost is calculated using the weighted average method. Net realisable value represents the estimated selling price less all estimated costs to be incurred in marketing, selling and distribution. Provision is made where necessary for obsolete, slow movingand defective items.

Financial instruments Financial assets and financial liabilities are recognised on the group’s statement of financial position when the group becomes a party to the contractualprovisions of the instrument.

The principal financial assets are trade and other receivables, term deposits, available for sale investments and cash and bank balances. The principal financial liabilities are trade payables, liabilities against finance leases, term loans, bank borrowings and overdrafts.

Derivative financial instruments Derivatives are initially recognised at cost on the date a derivative contract is entered into and are subsequently remeasured at their fair value. Changes in the fair value of derivative instruments are recognised immediately in the statement of comprehensive income.

Trade and other receivablesTrade receivables are amounts due from customers for billing in the ordinary course of business for construction contracts. If collection is expected in one year or less (or in the normal operating cycle of the business if longer), they are classified as current assets. If not, they are presented as non-current assets.

A provision for impairment of trade receivables is established when there is objective evidence that the Group will not be able to collect all amounts due according to the original terms of receivables. The amount of the provision is the difference between the asset’s carrying amount and the present value of estimated future cash flows, discounted at the original effective interest rate.

Term depositsTerm deposits are carried on the statement of financial position at their principal amount.

Cash and cash equivalentsFor the purpose of the cash flows statement, the group considers cash on hand and bank balances with a maturity of less than three months from thedate of placement as cash and cash equivalents.

Trade and other payables Trade payables are obligations to pay for goods or services that have been acquired in the ordinary course of business from suppliers. Accountspayable are classified as current liabilities if payment is due within one year or less (or in the normal operating cycle of the business if longer). If not, they are presented as non-current liabilities.

Galfar Engineering & Contracting SAOG & Subsidiaries

Notes to Consolidated Financial StatementsAs at 31st March, 2015

Interest-bearing loans and borrowingsBorrowings are recognised initially at fair value, net of transaction costs incurred. Borrowings are classified as current liabilities unless the company hasan unconditional right to defer settlement of the liability for at least 12 months after the reporting date.

Borrowing costsBorrowing costs directly attributable to the acquisition, construction or production of an asset that necessarily takes a substantial period of time to getready for its intended use or sale are capitalised as part of the cost of the respective assets untill such time as the assets are substantially ready for theirintended use. All other borrowing costs are expensed in the period they occur. Borrowing costs consist of interest and other costs that an entity incurs inconnection with the borrowing of funds.

OffsettingFinancial assets and financial liabilities are offset and the net amount reported in the statement of financial position only when there is a legallyenforceable right to set off the recognised amounts and the group intends to either settle on a net basis, or to realise the asset and settle the liabilitysimultaneously.

ProvisionsProvisions for environmental restoration, restructuring costs and legal claims are recognised when: the group has a present legal or constructiveobligation as a result of past events; it is probable that an outflow of resources will be required to settle the obligation; and the amount has been reliablyestimated. Restructuring provisions comprise lease termination penalties and employee termination payments. Provisions are not recognised for futureoperating losses.

Where there are a number of similar obligations, the likelihood that an outflow will be required in settlement is determined by considering the class ofobligations as a whole. A provision is recognised even if the likelihood of an outflow with respect to any one item included in the same class ofobligations may be small.

Provisions are measured at the present value of the expenditures expected to be required to settle the obligation and the risks specific to the obligation.

Provision for employees’ benefits Termination benefits for Omani employees are contributed in accordance with the terms of the Social Securities Law of 1991.

End of service benefits are accrued in accordance with the terms of employment of the group's employees at the reporting date, having regard to therequirements of the applicable labour laws of the countries in which the group operates and in accordance with IAS 19. Employee entitlements to annualleave and leave passage are recognised when they accrue to employees and an accrual is made for the estimated liability arising as a result of servicesrendered by employees up to the reporting date. These accruals are included in current liabilities, while that relating to end of service benefits isdisclosed as a non-current liability.

Dividend on ordinary sharesDividends on ordinary shares are recognised as a liability and deducted from equity when they are approved by the company’s shareholders.

Taxation Current income taxTaxation is provided based on relevant laws of the respective countries in which the group operates. Current income tax assets and liabilities for the

Deferred taxationDeferred tax is provided using the liability method on temporary differences at the reporting date between the tax bases of assets and liabilities and theircarrying amounts for financial reporting purposes. Deferred income tax assets and liabilities are measured at the tax rates that are expected to apply tothe period when the asset is realised or the liability is settled, based on laws that have been enacted at the reporting date.

Deferred income tax assets are recognised for all deductible temporary differences and carry-forward of unused tax assets and unused tax losses to theextent that it is probable that taxable profit will be available against which the deductible temporary differences and the carry-forward of unused taxassets and unused tax losses can be utilised.

Galfar Engineering & Contracting SAOG & Subsidiaries

Notes to Consolidated Financial StatementsAs at 31st March, 2015

Contract revenue and profit recognition A construction contract is defined by IAS 11 as a contract specifically negotiated for the construction of an asset.

When the outcome of a construction contract cannot be estimated reliably, contract revenue is recognised only to the extent of contract costs incurredthat are likely to be recoverable. When the outcome of a construction contract can be estimated reliably and it is probable that the contract will beprofitable, contract revenue is recognised over the period of the contract. When it is probable that total contract costs will exceed total contract revenue,the expected loss is recognised as an expense immediately. Contract revenue corresponds to the initial amount of revenue agreed in the contract andany variations in contract work, claims and incentive payments to the extent that it is probable that they will result in revenue, and they can be reliablymeasured.

A variation is included in contract revenue when:(a) it is probable that the customer will approve the variation and the amount of revenue arising from the variation; and (b) the amounts of revenue can be reliably measured.

Claims are included in contract revenue only when:(a) negotiations have reached an advanced stage such that it is probable that the customer will accept the claim; and (b) the amount that it is probable will be accepted by the customer can be measured reliably.

Incentive payments are included in contract revenue when:(a) the contract is sufficiently advanced that it is probable that the specified performance standards will be met or exceeded; and (b) the amount of the incentive payment can be measured reliably.

The company uses the ‘percentage of completion method’ to determine the appropriate amount to recognise in a given period. The stage of completionis measured by reference to the contract costs incurred up to the reporting date as a percentage of total estimated costs for each contract. Costsincurred in the year in connection with future activity on a contract are excluded from contract costs in determining the stage of completion. They arepresented as inventories, prepayments or other assets, depending on their nature.

Contract work in progressWork in progress on long term contracts is calculated at cost plus attributable profit, to the extent that this is reasonably certain after making provision forcontingencies, less any losses foreseen in bringing contracts to completion and less amounts received and receivable as progress payments. These aredisclosed as 'Due from customers on contracts'. Cost for this purpose includes direct labour, direct expenses and an appropriate allocation ofoverheads. For any contracts where receipts plus receivables exceed the book value of work done, the excess is included as ' Due to customers oncontracts' in accounts payable and accruals.

Sales and service incomeRevenue from sales of goods is recognised when the significant risks and rewards of ownership of the goods have passed to the buyer and the amountof revenue can be measured reliably.

Revenue from rendering of services is recognised when the outcome of the transaction can be estimated reliably, by reference to the stage ofcompletion of the transaction at the reporting date.Contract costsContract costs include costs that relate directly to the specific contract and costs that are attributable to contract activity in general and can be allocatedto the contract. Costs that relate directly to a specific contract comprise: site labour costs (including site supervision); costs of materials used inconstruction; depreciation of equipment used on the contract; costs of design, and technical assistance that is directly related to the contract.

The Group’s contracts are typically negotiated for the construction of a single asset or a group of assets which are closely interrelated or interdependentin terms of their design, technology and function. In certain circumstances, the percentage of completion method is applied to the separately identifiablecomponents of a single contract or to a group of contracts together in order to reflect the substance of a contract or a group of contracts.

Contract costs are recognised as expenses in the period in which they are incurred.

When it is probable that total contract costs will exceed total contract revenue, the expected loss is recognised as an expense immediately.

Galfar Engineering & Contracting SAOG & Subsidiaries

Notes to Consolidated Financial StatementsAs at 31st March, 2015

Interest incomeInterest revenue is recognised as the interest accrues.

Dividend incomeDividend income is recognised when the right to receive the dividend is established.

Directors’ remuneration The Parent Company follows the Commercial Companies Law 1974 (as amended), and other latest relevant directives issued by CMA, in regard todetermination of the amount to be paid as Directors’ remuneration. Directors’ remuneration is charged to the statement of comprehensive income in thesucceding year to which they relate after its approval in AGM.

Share capitalOrdinary shares are classified as equity. Incremental costs directly attributable to the issue of new ordinary shares are shown in equity as a deduction,net of tax, from the proceeds.Where any group company purchases the company’s equity share capital (treasury shares), the consideration paid, including any directly attributableincremental costs (net of income taxes) is deducted from equity attributable to the company’s equity holders until the shares are cancelled or reissued.Where such ordinary shares are subsequently reissued, any consideration received, net of any directly attributable incremental transaction costs and therelated income tax effects, is included in equity attributable to the company’s equity holders.

Foreign currency translationEach entity in the group determines its own functional currency and items included in the financial statements of each entity are measured using thatfunctional currency. Items included in the financial statements of the company are measured and presented in Rials Omani being the currency of theprimary economic environment in which the parent company operates.

Transactions in foreign currencies are initially recorded in the functional currency rate ruling at the date of the transaction. Monetary assets and liabilitiesdenominated in foreign currencies are retranslated at the functional currency rate of exchange ruling at the reporting date. All differences are taken tothe statement of comprehensive income. Non-monetary items that are measured in terms of historical cost in a foreign currency are translated using theexchange rates as at the dates of the initial transactions. Non-monetary items measured at fair value in a foreign currency are translated using theexchange rates at the date when the fair value was determined.

Notes to Consolidated Financial StatementsAs at 31st March, 2015

3. Property, plant and equipment - Parent Company Amount in RO '000s

Particulars Land Building & Camps

Plant & Machinery

Motor Vehicles & Equipment

Furniture & Equipments

Project Equipment

& Tools

Capital Work-in- Progress Total

Costs

At 1st January 2015 1,278 32,348 122,030 69,982 8,156 9,089 16 242,899 Additions 25 627 646 76 22 145 1,541 Disposals - - (323) (783) - - - (1,106) Transfers - - At 31st March, 2015 1,278 32,373 122,334 69,845 8,232 9,111 161 243,334

Depreciation

At 1st January 2015 - 19,400 73,742 44,825 6,603 6,438 - 151,008 Charge for the period - 415 2,729 1,603 138 261 - 5,146 Disposals - - (288) (689) - - - (977) Transfers - - At 31st March, 2015 - 19,815 76,183 45,739 6,741 6,699 - 155,177

Net book valueAt 31st March, 2015 1,278 12,558 46,151 24,106 1,491 2,412 161 88,157

At 31st March, 2014 1,278 13,380 56,452 29,557 1,760 3,274 124 105,825

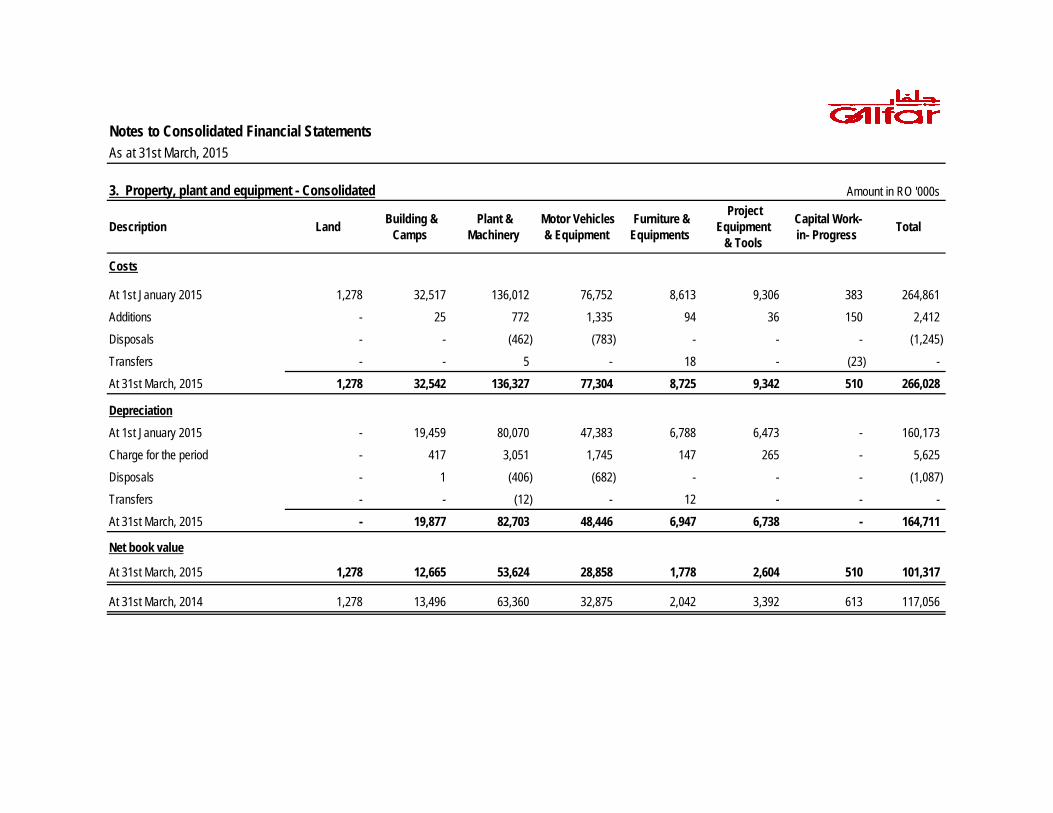

Notes to Consolidated Financial StatementsAs at 31st March, 2015

3. Property, plant and equipment - Consolidated Amount in RO '000s

Description Land Building & Camps

Plant & Machinery

Motor Vehicles & Equipment

Furniture & Equipments

Project Equipment

& Tools

Capital Work-in- Progress Total

Costs

At 1st January 2015 1,278 32,517 136,012 76,752 8,613 9,306 383 264,861

Additions - 25 772 1,335 94 36 150 2,412

Disposals - - (462) (783) - - - (1,245)

Transfers - - 5 - 18 - (23) -

At 31st March, 2015 1,278 32,542 136,327 77,304 8,725 9,342 510 266,028

DepreciationAt 1st January 2015 - 19,459 80,070 47,383 6,788 6,473 - 160,173

Charge for the period - 417 3,051 1,745 147 265 - 5,625

Disposals - 1 (406) (682) - - - (1,087)

Transfers - - (12) - 12 - - -

At 31st March, 2015 - 19,877 82,703 48,446 6,947 6,738 - 164,711

Net book value

At 31st March, 2015 1,278 12,665 53,624 28,858 1,778 2,604 510 101,317

At 31st March, 2014 1,278 13,496 63,360 32,875 2,042 3,392 613 117,056

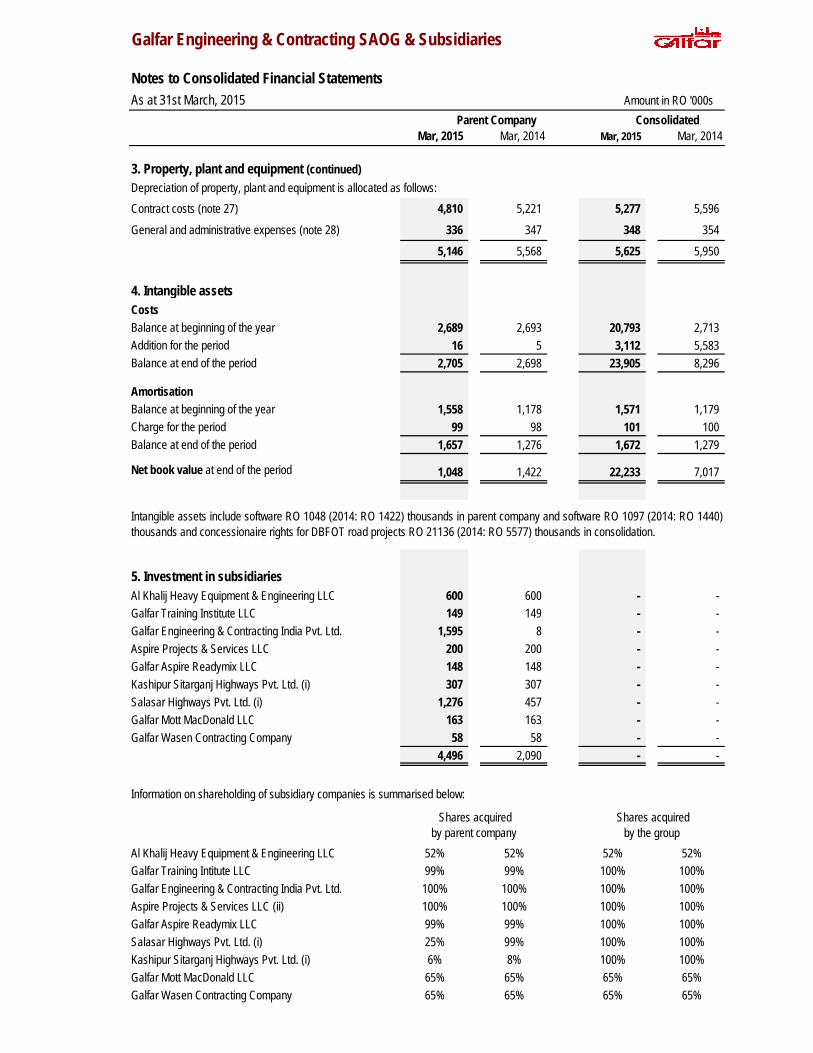

Galfar Engineering & Contracting SAOG & Subsidiaries

Notes to Consolidated Financial StatementsAs at 31st March, 2015 Amount in RO '000s

Mar, 2015 Mar, 2014 Mar, 2015 Mar, 2014

3. Property, plant and equipment (continued)Depreciation of property, plant and equipment is allocated as follows:Contract costs (note 27) 4,810 5,221 5,277 5,596

General and administrative expenses (note 28) 336 347 348 354

5,146 5,568 5,625 5,950

4. Intangible assetsCostsBalance at beginning of the year 2,689 2,693 20,793 2,713 Addition for the period 16 5 3,112 5,583 Balance at end of the period 2,705 2,698 23,905 8,296

AmortisationBalance at beginning of the year 1,558 1,178 1,571 1,179 Charge for the period 99 98 101 100 Balance at end of the period 1,657 1,276 1,672 1,279

Net book value at end of the period 1,048 1,422 22,233 7,017

5. Investment in subsidiariesAl Khalij Heavy Equipment & Engineering LLC 600 600 - - Galfar Training Institute LLC 149 149 - - Galfar Engineering & Contracting India Pvt. Ltd. 1,595 8 - - Aspire Projects & Services LLC 200 200 - - Galfar Aspire Readymix LLC 148 148 - - Kashipur Sitarganj Highways Pvt. Ltd. (i) 307 307 - - Salasar Highways Pvt. Ltd. (i) 1,276 457 - - Galfar Mott MacDonald LLC 163 163 - - Galfar Wasen Contracting Company 58 58 - -

4,496 2,090 - -

Information on shareholding of subsidiary companies is summarised below:

Al Khalij Heavy Equipment & Engineering LLC 52% 52% 52% 52%Galfar Training Intitute LLC 99% 99% 100% 100%Galfar Engineering & Contracting India Pvt. Ltd. 100% 100% 100% 100%Aspire Projects & Services LLC (ii) 100% 100% 100% 100%Galfar Aspire Readymix LLC 99% 99% 100% 100%Salasar Highways Pvt. Ltd. (i) 25% 99% 100% 100%Kashipur Sitarganj Highways Pvt. Ltd. (i) 6% 8% 100% 100%Galfar Mott MacDonald LLC 65% 65% 65% 65%Galfar Wasen Contracting Company 65% 65% 65% 65%

Parent Company Consolidated

Intangible assets include software RO 1048 (2014: RO 1422) thousands in parent company and software RO 1097 (2014: RO 1440)thousands and concessionaire rights for DBFOT road projects RO 21136 (2014: RO 5577) thousands in consolidation.

Shares acquired by parent company

Shares acquired by the group

Galfar Engineering & Contracting SAOG & Subsidiaries

Notes to Consolidated Financial StatementsAs at 31st March, 2015 Amount in RO '000s

Mar, 2015 Mar, 2014 Mar, 2015 Mar, 2014 Parent Company Consolidated

6. Investment in associatesGalfar Engineering & Contracting Kuwait KSC (GEC) (i) 5,323 5,323 2,525 3,069 Mahakaleswar Tollways Pvt. Ltd. (MTPL) (ii) 2,255 2,255 (828) (539) Shree Jagannath Expressway Pvt. Ltd. (SJEPL) (ii) 739 739 1,396 1,566 Ghaziabad Aligarh Expressway Pvt. Ltd. (GAEPL) (ii) 344 344 2,101 2,044 International Water Treatment LLC (IWT) (iii) 45 45 (456) 114

8,706 8,706 4,738 6,254

Information on shareholding of associate companies is summarised below:

Galfar Engineering & Contracting Kuwait KSC (i) 26% 26% 26% 26%Mahakaleswar Tollways Pvt. Ltd. (MTPL) (ii) 26% 26% 26% 26%Shree Jagannath Expressway Pvt. Ltd. (SJEPL) (ii) 6% 6% 26% 26%Ghaziabad Aligarh Expressway Pvt. Ltd. (GAEPL) (ii) 2% 2% 26% 26%International Water Treatment LLC (iii) 30% 30% 30% 30%

The following table illustrates summarised information of the group’s investment in its associates:

Share of associate’s statement of financial position:Current assets 9,365 13,181 Non-current assets 56,207 45,547 Current liabilities (10,663) (13,191)

Non-current liabilities (50,171) (39,283) Net assets and carrying amount of the investment 4,738 6,254

Share of associate’s statement of income:Revenue 4,420 5,078 Costs of revenue 4,491 5,295 Loss for the period (71) (217)

7. InventoriesMaterials and consumables 20,383 35,433 21,237 36,268 Allowance for non-moving inventories (1,785) (451) (1,811) (477)

18,598 34,982 19,426 35,791

8. Contract work in progress

68,782 57,451 71,286 59,190

605 1,742 6,963 5,806

Shares acquired by parent company

Shares acquired by the group

Loss for the period comprises of MTPL, India RO -113 (Year 2014: RO -132) thousands, GEC, Kuwait RO 42 (Year 2014: RO -169)thousands and IWT, Oman RO 0 (Year 2014: RO 84) thousands.

Work-in-progress on long term contracts at cost plus attributable profit considered as receivablesTo customers under construction contracts recorded as billings in excess of work done (note 23)

Galfar Engineering & Contracting SAOG & Subsidiaries

Notes to Consolidated Financial StatementsAs at 31st March, 2015 Amount in RO '000s

Mar, 2015 Mar, 2014 Mar, 2015 Mar, 2014 Parent Company Consolidated

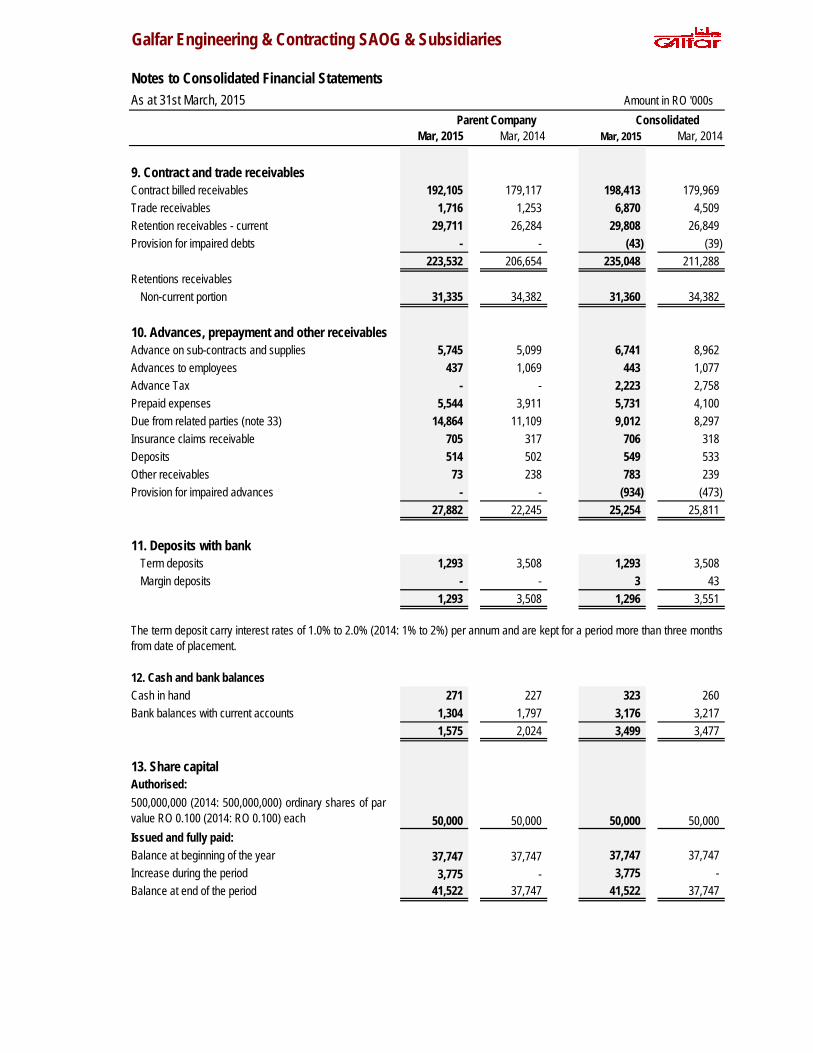

9. Contract and trade receivablesContract billed receivables 192,105 179,117 198,413 179,969 Trade receivables 1,716 1,253 6,870 4,509 Retention receivables - current 29,711 26,284 29,808 26,849 Provision for impaired debts - - (43) (39)

223,532 206,654 235,048 211,288 Retentions receivables

Non-current portion 31,335 34,382 31,360 34,382

10. Advances, prepayment and other receivablesAdvance on sub-contracts and supplies 5,745 5,099 6,741 8,962 Advances to employees 437 1,069 443 1,077 Advance Tax - - 2,223 2,758 Prepaid expenses 5,544 3,911 5,731 4,100 Due from related parties (note 33) 14,864 11,109 9,012 8,297 Insurance claims receivable 705 317 706 318 Deposits 514 502 549 533 Other receivables 73 238 783 239 Provision for impaired advances - - (934) (473)

27,882 22,245 25,254 25,811

11. Deposits with bankTerm deposits 1,293 3,508 1,293 3,508 Margin deposits - - 3 43

1,293 3,508 1,296 3,551

12. Cash and bank balancesCash in hand 271 227 323 260 Bank balances with current accounts 1,304 1,797 3,176 3,217

1,575 2,024 3,499 3,477

13. Share capitalAuthorised:

50,000 50,000 50,000 50,000 Issued and fully paid:Balance at beginning of the year 37,747 37,747 37,747 37,747 Increase during the period 3,775 - 3,775 - Balance at end of the period 41,522 37,747 41,522 37,747

The term deposit carry interest rates of 1.0% to 2.0% (2014: 1% to 2%) per annum and are kept for a period more than three monthsfrom date of placement.

500,000,000 (2014: 500,000,000) ordinary shares of parvalue RO 0.100 (2014: RO 0.100) each

Galfar Engineering & Contracting SAOG & Subsidiaries

Notes to Consolidated Financial StatementsAs at 31st March, 2015 Amount in RO '000s

Mar, 2015 Mar, 2014 Mar, 2015 Mar, 2014 Parent Company Consolidated

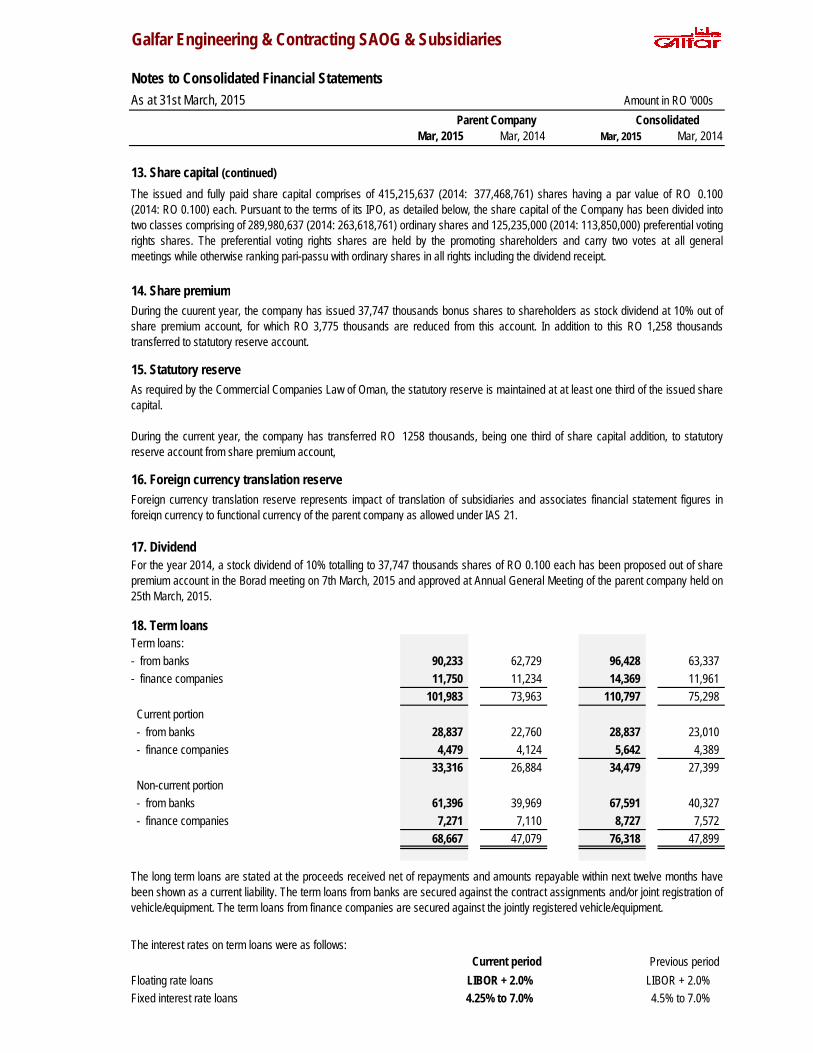

13. Share capital (continued)

14. Share premium

15. Statutory reserve

16. Foreign currency translation reserve

17. Dividend

18. Term loansTerm loans: - from banks 90,233 62,729 96,428 63,337 - finance companies 11,750 11,234 14,369 11,961

101,983 73,963 110,797 75,298 Current portion - from banks 28,837 22,760 28,837 23,010 - finance companies 4,479 4,124 5,642 4,389

33,316 26,884 34,479 27,399 Non-current portion - from banks 61,396 39,969 67,591 40,327 - finance companies 7,271 7,110 8,727 7,572

68,667 47,079 76,318 47,899

The interest rates on term loans were as follows:

Floating rate loans LIBOR + 2.0% LIBOR + 2.0%Fixed interest rate loans 4.25% to 7.0% 4.5% to 7.0%

The issued and fully paid share capital comprises of 415,215,637 (2014: 377,468,761) shares having a par value of RO 0.100(2014: RO 0.100) each. Pursuant to the terms of its IPO, as detailed below, the share capital of the Company has been divided intotwo classes comprising of 289,980,637 (2014: 263,618,761) ordinary shares and 125,235,000 (2014: 113,850,000) preferential votingrights shares. The preferential voting rights shares are held by the promoting shareholders and carry two votes at all generalmeetings while otherwise ranking pari-passu with ordinary shares in all rights including the dividend receipt.

During the cuurent year, the company has issued 37,747 thousands bonus shares to shareholders as stock dividend at 10% out ofshare premium account, for which RO 3,775 thousands are reduced from this account. In addition to this RO 1,258 thousandstransferred to statutory reserve account.

As required by the Commercial Companies Law of Oman, the statutory reserve is maintained at at least one third of the issued sharecapital.

During the current year, the company has transferred RO 1258 thousands, being one third of share capital addition, to statutoryreserve account from share premium account,

Foreign currency translation reserve represents impact of translation of subsidiaries and associates financial statement figures inforeign currency to functional currency of the parent company as allowed under IAS 21.

For the year 2014, a stock dividend of 10% totalling to 37,747 thousands shares of RO 0.100 each has been proposed out of sharepremium account in the Borad meeting on 7th March, 2015 and approved at Annual General Meeting of the parent company held on25th March, 2015.

The long term loans are stated at the proceeds received net of repayments and amounts repayable within next twelve months havebeen shown as a current liability. The term loans from banks are secured against the contract assignments and/or joint registration ofvehicle/equipment. The term loans from finance companies are secured against the jointly registered vehicle/equipment.

Current period Previous period

Galfar Engineering & Contracting SAOG & Subsidiaries

Notes to Consolidated Financial StatementsAs at 31st March, 2015 Amount in RO '000s

Mar, 2015 Mar, 2014 Mar, 2015 Mar, 2014 Parent Company Consolidated

19. Short term loans - from banks 37,500 29,800 42,584 29,800

20. Bank borrowings Bank overdrafts 9,059 22,861 10,725 24,504 Loan against trust receipts 42,988 54,558 42,988 54,558 Bills discounted 6,386 21,850 6,386 21,850

58,433 99,269 60,099 100,912

21. Trade payablesSundry creditors 44,828 56,315 53,856 64,191 Provision for purchases and sub-contracts 36,012 33,713 36,905 34,942

80,840 90,028 90,761 99,133

22. Employees’ end of service benefitsBalance at beginning of the year 11,066 10,919 11,253 11,067 Charge for the period 500 637 575 702 Paid during the period (80) (324) (160) (375) Balance at end of the year 11,486 11,232 11,668 11,394

23. Other payables and provisionsProvision for employees’ leave pay and passage 6,470 7,351 6,536 7,413 Creditors for capital purchases 816 2,534 816 2,534 Advance payables -current 30,955 25,014 31,062 25,102 Due to customers on contracts (note 8) 605 1,742 6,963 5,806 Retention on sub-contracts 1,907 1,847 2,071 1,928 Accrued expenses 10,988 9,888 12,846 10,076 Due to related parties (note 33) 1,430 2,164 1,897 2,535 Dividend payable - 3,775 - 3,775 Other payables 909 747 180 2,268

54,080 55,062 62,371 61,437 Advance payables

Non-current portion 20,380 8,390 23,863 11,315

Bank short term loans are repayable in one year and are secured against the contract assignments and/or joint registration ofvehicle/equipment. The interest rates on these loans vary between 4.0% to 4.5% (2014: 4.0% to 5.0%) per annum.

Bank borrowings are repayable on demand or within one year. The interest rates on bank borrowings vary between 4.0% to 5.5%(2014: 4.0% to 7.0%) per annum. Bank borrowings are secured against the contract assignments and/or joint registration ofvehicle/equipment.

Galfar Engineering & Contracting SAOG & Subsidiaries

Notes to Consolidated Financial StatementsAs at 31st March, 2015 Amount in RO '000s

Mar, 2015 Mar, 2014 Mar, 2015 Mar, 2014 Parent Company Consolidated

24. Taxation

Income tax expenseTax charge for the current period 460 407 554 603 Deferred tax charge for the period (296) (220) (296) (196) Tax charge of prior years 11 - 11 -

175 187 269 407

Provision for tax

Balance at beginning of the year 1,173 1,177 3,853 2,787 Charge during the period 471 407 565 603 Tax paid during the period (1,026) - (1,070) (14) Balance at end of the period 618 1,584 3,348 3,376

Deferred tax liability

Balance at beginning of the year 6,039 6,899 6,638 7,305 Charge during the period (296) (220) (296) (196) Balance at end of the period 5,743 6,679 6,342 7,109

25. Sales and services incomeSales and services 508 415 3,659 2,412 Hiring services 278 309 727 752 Training services - - 28 157

786 724 4,414 3,321

26. Other incomeGain on sale of assets 126 168 119 169 Dividend income 30 - - - Miscellaneous income 445 209 455 230

601 377 574 399

The parent company income tax assessment up to the year 2009 has been finalized by the taxation department. The incomeassessments of the subsidiaries are at various stages of completion. The management believes that any taxation for the unassessedyears will not be material to the financial position of the Group as at the reporting date. The status of tax provision is as follows:

Income tax is provided for parent company and Omani subsidiaries as per the provisions of the 'Law of Income Tax on Companies' inOman @ 12% of taxable profit after adjusting non-assessable and disallowable items and statutory exemption of RO 30,000. It isprovided for Indian subsidiary as per 'Income tax Act' in India @ 33% of taxable profit after adjusting non-admissible expenses anddepreciation difference.

Deferred income taxes are calculated on all temporary differences under the balance sheet liability method using a principal tax rateas per tax law of the respective country.

The net deferred tax liability and deferred tax charge/(release) in the comprehensive income statement are attributable to followingitems:

Galfar Engineering & Contracting SAOG & Subsidiaries

Notes to Consolidated Financial StatementsAs at 31st March, 2015 Amount in RO '000s

Mar, 2015 Mar, 2014 Mar, 2015 Mar, 2014 Parent Company Consolidated

27. Cost of contract and salesMaterials 24,830 28,737 25,777 29,431 Manpower costs (note 29) 23,132 25,428 24,076 26,342 Sub-contracting costs 15,060 14,897 15,116 14,733 Plant and equipments repair and maintenance 3,821 4,667 4,228 5,068 Plant and equipments hiring costs 1,259 1,356 1,417 1,587 Fuel expenses 3,187 3,751 3,549 4,092 Training expenses - - 21 63 Duties and taxes - - 52 125 Depreciation (note 3) 4,810 5,221 5,277 5,596 General and administrative expenses (note 28) 3,334 3,661 3,503 3,800

79,433 87,718 83,016 90,837

28. General and administrative expensesManpower costs (note 29) 1,241 1,404 1,456 1,628 Rent 1,065 1,134 1,133 1,181 Electricity and water charges 781 726 808 750 Insurance charges 776 961 868 1,020 Bank guarantee and other charges 445 529 489 537 Professional and legal charges 334 246 378 260 Communication expenses 254 271 276 290 Repairs and maintenance -others 182 147 183 153 Business promotion expenses 20 69 22 71 Traveling expenses 71 110 89 121 Printing and stationery 88 130 96 135 Tender fees 63 45 63 46 Directors expenses 74 200 74 200 Miscellaneous expenses 157 98 176 116 Depreciation and amortisation (note 3 and 4) 435 445 449 454 Debts and advances impaired - - - 189

5,986 6,515 6,560 7,151 Pertaining to cost of contract and sales 3,334 3,661 3,503 3,800

2,652 2,854 3,057 3,351 29. Manpower costsSalary and wages 17,732 19,027 18,291 19,843 Employees service benefits 2,939 3,232 3,083 3,357 Camp and catering expenses 2,488 3,102 2,592 3,206 Hired salary and wages 460 677 693 709 Staff incentives - - 89 36 Other expenses 754 794 784 819

24,373 26,832 25,532 27,970 Pertaining to cost of contract and sales 23,132 25,428 24,076 26,342 Pertaining to general and administration expenses 1,241 1,404 1,456 1,628

30. Financing costs, netInterest expense 2,469 2,500 2,700 2,575 Interest income (17) (18) (19) (19)

2,452 2,482 2,681 2,556

Galfar Engineering & Contracting SAOG & Subsidiaries

Notes to Consolidated Financial StatementsAs at 31st March, 2015 Amount in RO '000s

Mar, 2015 Mar, 2014 Mar, 2015 Mar, 2014 Parent Company Consolidated

31. Earnings per share

Profit for the year 1,253 1,403 1,264 1,400 Number of shares in '000 (note 13) 415,220 377,470 415,220 377,470 Basic earnings per share for the period (RO) 0.003 0.004 0.003 0.004

32. Net assets per share

Net assets 104,466 103,407 102,805 103,196 415,220 377,470 415,220 377,470

Net assets per share (RO) 0.252 0.274 0.248 0.273

33. Related party transactions

Contract income 1,641 726 4,805 2,924 Sales and services 503 533 511 1,032 Sale of property, plant and equipment - 1,065 - 1,065 Purchase of property, plant and equipment 41 84 41 84 Purchase of goods and services 3,343 4,397 3,343 4,463 Director's remuneration 74 200 74 200

Due from shareholders 237 158 237 158 Due from subsidiary and associate companies 10,041 8,076 4,188 5,540 Due from other related parties 4,586 2,875 4,587 2,875

14,864 11,109 9,012 8,573

Due to shareholders 156 182 156 182 Due to subsidiary and associate companies 149 494 616 864 Due to other related parties 1,125 1,488 1,125 1,489

1,430 2,164 1,897 2,535

34. Comparative amounts

The basic earnings per share is calculated by dividing the profit for the period attributable to the shareholders of the parent companyby the weighted average number of shares outstanding during the year as follows:

Net assets per share is calculated by dividing the equity attributable to shareholders of the parent company at the reporting date bythe number of shares outstanding as follows:

Number of shares in '000 (note 13)

Related parties comprise the directors and business entities in which they have the ability to control or exercise significant influencein financial and operating decisions. The group maintains significant balances with these related parties which arise in the normal course of business from commercialtransactions, and are entered into at terms and conditions which the management consider to be comparable with those adopted forarm’s length transactions with third parties.

The following is a summary of significant transactions with related parties which are included in the financial statements:

Balances of related parties recognised and disclosed in notes 10 and 23 respectively are as follows:

Certain of the corresponding figures of previous year have been reclassified in order to conform with the presentation for the currentyear. Such reclassifications do not affect previously reported profit or shareholder’s equity.