Embed Size (px)

DESCRIPTION

Diagnose Mittestand (von Sparkasse)

Citation preview

Informationen zum Deutschen Sparkassen- und Giroverband erhal-ten Sie unter 030 20225-0 oderauf unserer Website www.dsgv.de.

Diagnose Mittelstand 2012

German SMEs – stable even in difficult times

S Finanzgruppe Deutscher Sparkassen- und Giroverband

Three out of four enterprises in Germany trust the Savings Banks Finance Group as their financial services provider. In Germany, giving advice to and providing finance for small and medium-sized enterprises is the core of the business policy of savings banks and Landesbanken. To achieve this goal, they use their strengths: their precise knowledge of their customers and their personal circumstances as well as their full coverage of all of Ger-many’s regions.

Diagnose Mittelstand 2012 is the eleventh annual analysis conducted by the Deutscher Sparkassen- und Giroverband, providing representative data on the current status and the future prospects of small and medium-sized enterprises in Germany.

Diagnose Mittelstand 2010 Titel

Key Findings of the Diagnose Mittelstand 2012

4

Key Findings of the Diagnose Mittelstand 2012

Diagnose Mittelstand is an annual analysis of the most important segment of the German economy: the so-called SMEs, i.e. small and medium-sized enterprises. The analysis is based on two pillars:

– Firstly, a data analysis of the extensive collection of balance sheets of the savings banks’ business custom-ers;

– Secondly, a survey conducted among experts to col-lect the views of the savings banks’ customer account managers with regard to the current business perfor-mance of small and medium-sized enterprises.

In each of the years up to and including 2009, the analy-sis of balance sheet data covered a total of up to 230,000 year-end financial statements of business clients of sa vings banks and Landesbanken. For 2010, for which approx. 112,000 balance sheets are already available, the trends of the SME’s key ratios were extrapolated for this most recent financial year.

This year’s Diagnose Mittelstand analyses the trends observed among SMEs against the background of their long-term development, bearing in mind the structural changes and the economic ups and downs in the past ten years. This analysis shows how difficult the environment

5

has been for SMEs at times. However, SMEs have also bene fited in this period from the much stronger competi-tiveness of the German economy, and SMEs have even proven to be a key contributor to this development. SMEs have not been instrumental in deepening recessions and aggravating the crisis in recent years; instead, they have proven to be a stabilising factor for the country – even in difficult times.

In the past few years, the SMEs’ level of employment, capacity utilisation and profitability have improved con-siderably. While the deep recession in the winter of 2008-2009 left its traces in some of the key ratios, the SMEs’ overall performance has remained remarkably robust and stable.

In the period under review, the equity ratio has steadily increased. The median for the entire SME segment increased from 12.8 percent in 2008 to 15.1 percent in 2009 and now 18.3 percent as a trend extrapolated for the fiscal year 2010. This upward trend applies to enterprises of all sizes and segments – in manufacturing, crafts, trade and construction. While the ratios are lower for SMEs than for large-scale companies which have also achieved improvements, the ratios of SMEs have been rising at a faster pace.

0 5 2010 15 25 30 35

200820092010

27.729.6

30.3

12.815.1

18.3

16.919.5

9.3

21.4

6.9

12.1

€0 to €1 million Small enterprises

Equity Ratio of Enterprises, 2008 to 2010 median values, as a percentage, by turnover volume category

€1 to €50 million Medium-sized enterprises

€0 to €50 million SMEs

> €50 millionLarge-scale companies

6

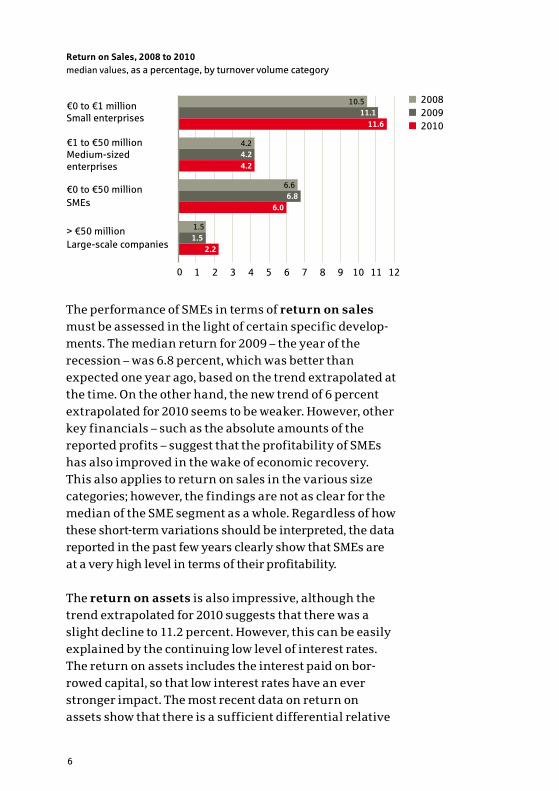

The performance of SMEs in terms of return on sales must be assessed in the light of certain specific develop-ments. The median return for 2009 – the year of the recession – was 6.8 percent, which was better than expected one year ago, based on the trend extrapolated at the time. On the other hand, the new trend of 6 percent extrapolated for 2010 seems to be weaker. However, other key financials – such as the absolute amounts of the reported profits – suggest that the profitability of SMEs has also improved in the wake of economic recovery. This also applies to return on sales in the various size ca tegories; however, the findings are not as clear for the median of the SME segment as a whole. Regardless of how these short-term variations should be interpreted, the data reported in the past few years clearly show that SMEs are at a very high level in terms of their profitability.

The return on assets is also impressive, although the trend extrapolated for 2010 suggests that there was a slight decline to 11.2 percent. However, this can be easily explained by the continuing low level of interest rates. The return on assets includes the interest paid on bor-rowed capital, so that low interest rates have an ever stronger impact. The most recent data on return on assets show that there is a sufficient differential relative

€0 to €1 million Small enterprises

0 1 2 3 4 5 6 7 8 9 10 11 12

Return on Sales, 2008 to 2010median values, as a percentage, by turnover volume category

200820092010

1.51.5

2.2

6.66.8

6.0

4.24.24.2

10.511.1

11.6

€1 to €50 million Medium-sized enterprises

€0 to €50 million SMEs

> €50 millionLarge-scale companies

7

to the interest rates of risk-free investments such as Ger-man sovereign bonds.

The personnel expenses ratio – calculated at 19.1 per-cent in 2010 – remains virtually unchanged. This figure is the result of two opposite trends: on the one hand, the much higher per-capita productivity due to the economic recovery and the return to longer regular working hours; and on the other hand, a return to somewhat more dynamic pay rises.

To ensure that the description of the situation of SMEs is as up-to-date as possible, despite the inevitable delays in the presentation and analysis of the balance sheets, the analysis of balance sheet data for the Diagnose Mittel-stand is traditionally supplemented by a survey of experts, which makes it possible to cover the latest developments.

In November 2011, all the savings banks were asked to answer seven questions on five issues; the questions were addressed specifically to the managers responsible for corporate banking business. As in previous years, the return rate once again reached an extremely high level (81 percent). This makes it possible to provide a nearly nation-wide, representative account of the status of

0 5 10 15 20

Return on Assets, 2008 to 2010median values, as a percentage, by turnover volume category

200820092010

5.75.1

6.3

13.112.1

11.2

11.711.010.8

14.813.3

11.9

€0 to €1 million Small enterprises

€1 to €50 million Medium-sized enterprises

€0 to €50 million SMEs

> €50 millionLarge-scale companies

8

Germany’s SMEs as of the end of 2011. The results are detailed enough to break them down into Germany’s var-ious federal states.

Despite the gloomier economic prospects and the consi-derable uncertainty created in the wake of the govern-ment debt crisis, the corporate account experts of the savings banks continue to paint a robust picture of Ger-many’s SMEs. More than 50 percent of the respondents believe that their business clients are in a better posi-tion than in the previous year, while nearly all of the remaining respondents have not found any change. Only slightly more than 2 percent have observed a deteriora-tion.

The improvement of the capital base, already known from the long-term trend, seems to have continued at the end of 2011. This is corroborated by the ratio of positive reports (more than 58 percent) to negative reports (only 3.5 percent).

In addition, savings banks reported that the volumes of originated investment finance continued to increase in autumn 2011 although the increase was not as signifi-cant as in the previous year. However, the balance of “more” and “less” continues to be positive.

€0 to €1 million Small enterprises

0 5 2010 15 25

Personnel Expenses Ratio, 2008 to 2010 median values, as a percentage, by turnover volume category

200820092010

€1 to €50 million Medium-sized enterprises

€0 to €50 million SMEs

> €50 millionLarge-scale companies

13.314.714.7

18.418.919.1

20.422.222.2

16.515.8

13.6

9

Replacement investments are still the principal invest-ment purpose. However, expansion investments, which have been reported in the survey at a rate of 35 percent, are now cited more frequently. This accelerated capacity expansion is strong evidence of the fact Germany’s SMEs continue to be optimistic – despite the public finance crisis.

Expectations are similarly positive when it comes to the employment prospects in the various regions. Nearly 27 percent of the respondents expect that their SME cli-ents will continue to build up employment in 2012. The savings banks that expect employment losses in their regions (not even 5 percent) are clearly a minority.

The “special question” asked in this year’s survey of experts was what percentage of the savings banks’ busi-ness customers had become much more cautious in response to the financial market turbulences and to the government debt crisis. A total of 70 percent of the sav-ings banks found such a change in less than one out of five customers, while 45 percent of the savings banks stated that not even one out of ten business customers showed such changes.

In response to the question of how this change in beha-viour manifested itself in this sub-group, savings banks cited reluctance to invest, more cautious employment planning and higher levels of liquidity as predominant patterns of behaviour. Overall, the fact that SMEs are not greatly affected demonstrates that SMEs continue to go about their business steadily and largely unscathed. In the current situation, SMEs have once again proven to be solid as a rock in turbulent waters and have helped to sta-bilise the macroeconomic situation.

Diagnose Mittelstand 2012 as well as many supplemen-tary tables can be downloaded as PDF files by visiting our website at www.dsgv.de/en and clicking on the head-ings “Facts” – “Publications” – “Diagnose Mittelstand”.

http://www.dsgv.de/en/facts/publications.html

Imprint

Published by:Deutscher Sparkassen- und GiroverbandCharlottenstrasse 47 D-10117 BerlinGermany

Phone +49-30-20225-0Fax +49-30-20225-250www.dsgv.de

Unit responsible for this publicationCommunications and Media

DataMarket Service, Economics and Financial Markets

TextEconomics and Financial Markets