Embed Size (px)

DESCRIPTION

Developing Marginal Cost-Based Rates. Kelly Eakin Senior Vice President Christensen Associates Energy Consulting APPA Business and Financial Conference Austin, TX September 25, 2007. Objectives of Presentation. - PowerPoint PPT Presentation

Citation preview

Developing MarginalCost-Based Rates

Kelly EakinSenior Vice President

Christensen Associates Energy Consulting

APPA Business and Financial ConferenceAustin, TX

September 25, 2007

September 2007 2 CA Energy Consulting

Objectives of Presentation

Provide a framework to evaluate social gains from marginal cost pricing and address the challenge of fixed cost recovery

Identify key determinants to marginal cost pricing gains

Look for ways to incorporate pricing efficiency principles into cost of service analysis

September 2007 3 CA Energy Consulting

Business Objectives

Revenue Sufficiency

Maximizing stakeholder value

September 2007 4 CA Energy Consulting

Outline

Economics Basics The Regulatory Dilemma Incorporating Marginal Cost Pricing

Principles into Cost of Service Analysis A Simple Stylized Example Conclusions

September 2007 5 CA Energy Consulting

Economics Basics

September 2007 6 CA Energy Consulting

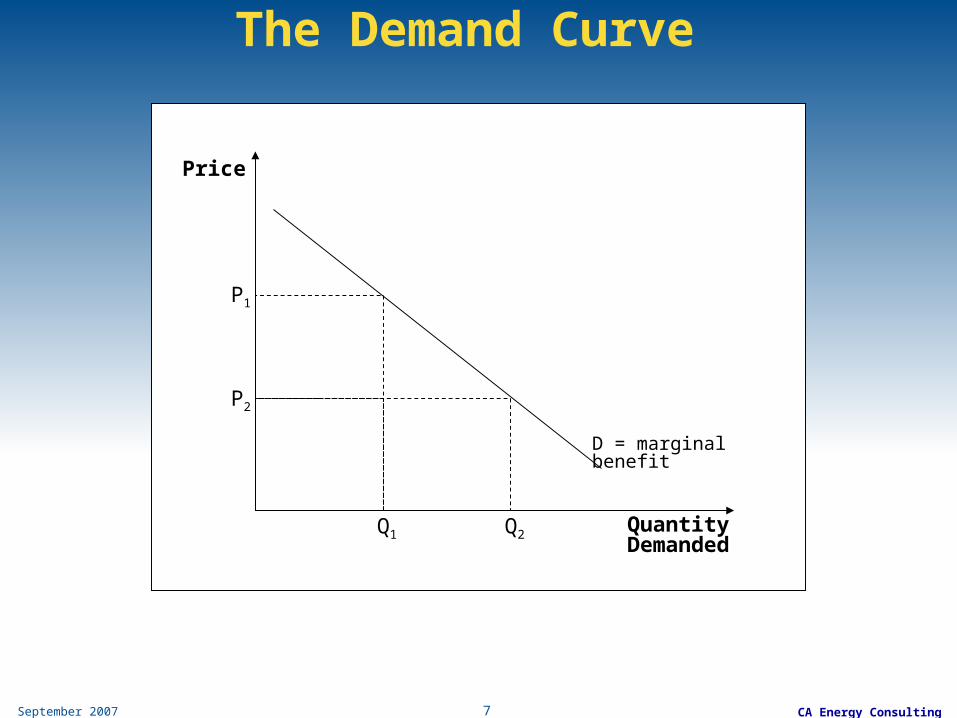

Demand

Consumers are willing to pay for a good because it brings them some benefit or satisfaction

As more of a good is consumed, the additional or marginal benefit decreases (law of diminishing returns)

Consequently, the consumer’s willingness to pay for another unit of a good decreases as consumption increases

Law of Demand: Consumers will buy more of a good a lower prices, other things the same

Price Elasticity of Demand: — A measure of customer price responsiveness

— εD = % change in quantity demanded ÷ % change in price

September 2007 7 CA Energy Consulting

The Demand Curve

Price

QuantityDemanded

D = marginal benefit

P1

P2

Q1 Q2

September 2007 8 CA Energy Consulting

Costs

Costs reflect the “supply side” of a market For goods to come to market, a supplier

needs to expect at least to recover (variable) costs

September 2007 9 CA Energy Consulting

Cost Measures (1)

Total Costs— Variable Cost – costs associated with the

inputs that change as production levels change— Fixed Cost – costs that remain the same

regardless of the production level, sometimes called “sunk costs” (e.g., capital costs)

— Total Cost = Variable Cost + Fixed Cost or TC=VC+FC

September 2007 10 CA Energy Consulting

Cost Measures (2)

Average Cost Concepts— Average Variable Cost (AVC)

• Variable cost per unit of output: AVC=TVC/Q— Average Fixed Cost (AFC)

• Fixed cost per unit of output: AFC/Q• AFC decreases as output increases (spreading out the

overhead)— Average Total Cost (ATC)

• Cost per unit of output: • ATC = TC/Q• ATC = AVC +AFC

The utility industry term “average embedded cost” corresponds closely to the economic term average total cost

September 2007 11 CA Energy Consulting

Cost Measures (3)

Marginal Cost (MC)— Marginal cost measures how cost changes as

an additional unit of output is produced— MC = ∆TC/∆Q = ∆TVC/∆Q — Marginal cost is the supply schedule for a

competitive profit-maximizing firm— A supply schedule is more ambiguous if there

is a lack of competition or the firm is not a profit maximizer

September 2007 12 CA Energy Consulting

Cost Measures (4)

Fixed Costs— Common cost—overhead costs that occurs

regardless of product lines offered, production levels or customer classes served

— Class-specific fixed cost—costs that do not vary with production levels but that are avoidable if a customer class is not served

— Product-specific fixed cost—costs that do not vary with production levels but that are avoidable if a product line is not produced

— Fixed cost recovery can introduce price distortion and resulting social value loss (called economic inefficiency)

September 2007 13 CA Energy Consulting

Cost Measures (5)

Incremental Cost (ICi)— Incremental cost indicates the additional cost of

adding a product line or serving another customer class

— Subtle differences from marginal cost• Discrete change instead of incremental change

• May involve some product/class specific fixed (but avoidable) costs

• ICi = TC – TC without Qi = TC – TC(~ Qi)

Average Incremental Cost (AICi)— AICi = ICi/Qi

— Important concept in investigating cross-subsidies

September 2007 14 CA Energy Consulting

Cost Concepts (6)

Finally, pulling in some cost of service concepts— Attributable costs (or directly assigned costs) are those

costs that can be assigned as “caused” by serving a customer class• Variable costs • Class-specific fixed costs• Product-specific fixed costs for products serving only one

customer class— Non-attributable costs—those costs that occur

regardless of whether a particular customer class is served• Common costs• Product-specific fixed costs for products serving all customer

classes

September 2007 15 CA Energy Consulting

Cross-Subsidization

Charging some more than attributable cost so that others pay less than their attributable cost

Different criteria for cross-subsidization— Price vs. Average Total Cost— Price vs. Average Variable Cost— Price vs. Marginal Cost— Price vs. Average Incremental Cost

Cross-subsidization involves — Inefficiency— Fairness issue

September 2007 16 CA Energy Consulting

Cross-Subsidization

Pi < AICi — Revenue from class less than its incremental cost— Serving the class adds to the overhead contribution required from

other classes— Other classes would pay less if this class were not served— The class is receiving a cross-subsidy from other classes

Pi = AICi — Revenue just covers incremental cost but class makes no

contribution to overhead— No impact on other classes— No cross-subsidy

Pi > AICi — Revenue from class more than its incremental cost— the class makes a contribution to overhead— Other classes would pay more if this class were not served— No cross-subsidy

September 2007 17 CA Energy Consulting

Economic Efficiency

Economic efficiency occurs when resources are used in a way that generates the greatest economic value

Price = Marginal Cost is the efficiency condition— P > MC too little produced; additional value would

exceed additional cost— P < MC too much produced; additional cost of last

unit more than offsets additional value— P=MC maximum net benefit; no way to reallocate

resources to increase economic value

September 2007 18 CA Energy Consulting

The Efficiency of Competition

P

q

Firm

ATCMC

P

Q = nq

D = MB

S = MC

Industry

September 2007 19 CA Energy Consulting

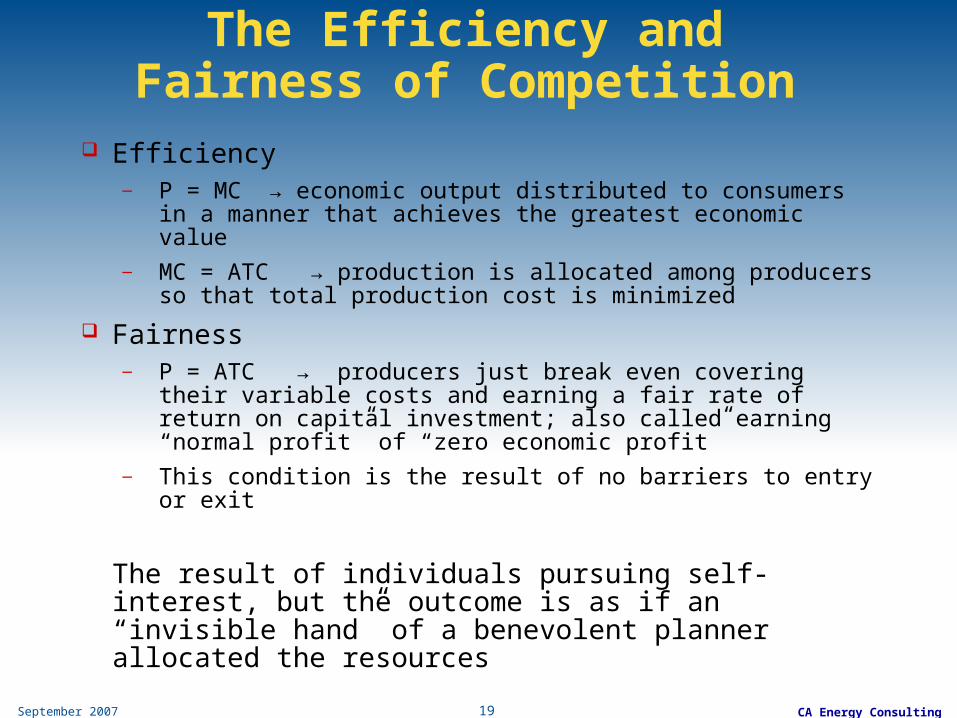

The Efficiency and Fairness of Competition

Efficiency— P = MC → economic output distributed to consumers in a

manner that achieves the greatest economic value— MC = ATC → production is allocated among producers so that

total production cost is minimized

Fairness— P = ATC → producers just break even covering their variable

costs and earning a fair rate of return on capital investment; also called earning “normal profit” of “zero economic profit”

— This condition is the result of no barriers to entry or exit

The result of individuals pursuing self-interest, but the outcome is as if an “invisible hand” of a benevolent planner allocated the resources

September 2007 20 CA Energy Consulting

The Invisible Hand

September 2007 21 CA Energy Consulting

The Regulatory Dilemma

September 2007 22 CA Energy Consulting

Alas, competition and efficiency may not prevail

Industry might not be competitive— Barriers to entry— Large economies of scale

Firms might not be profit-maximizers— Public power has stakeholders rather than shareholders— Other non-profit organizations have objectives other

than maximizing profit Revenue adequacy still a requirement, but

efficiency may not be a result

September 2007 23 CA Energy Consulting

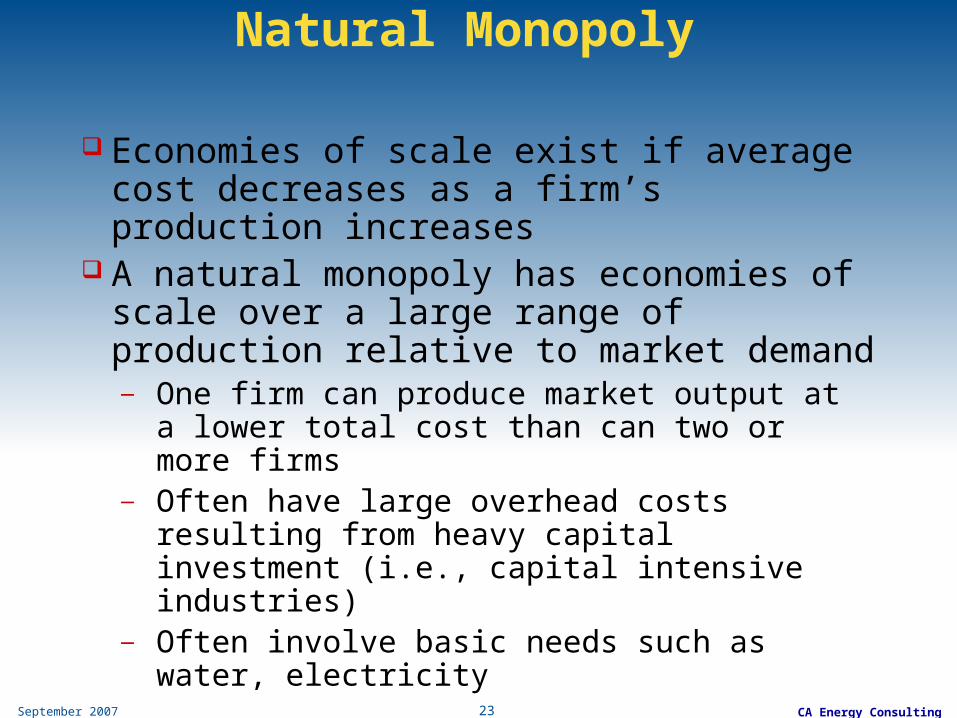

Natural Monopoly

Economies of scale exist if average cost decreases as a firm’s production increases

A natural monopoly has economies of scale over a large range of production relative to market demand— One firm can produce market output at a lower

total cost than can two or more firms— Often have large overhead costs resulting from

heavy capital investment (i.e., capital intensive industries)

— Often involve basic needs such as water, electricity

September 2007 24 CA Energy Consulting

Natural Monopoly

$

Q

ATC

MCD

September 2007 25 CA Energy Consulting

Rationale for Regulation

Promoting competition is inefficient in a natural monopoly situation— Instead rate regulation is the policy

prescription— Called public utility regulation— Trying to achieve competitive-type (invisible

hand) outcomes via regulation

September 2007 26 CA Energy Consulting

The Not-So Invisible Hand of Regulation

Intervenor Discovery

File Case

Company Presents

Witnesses

Staff & Intervenors

Prefile Testimony

Company Files Rebuttal

Cross Examination on Rebuttal

Submission of Briefs

Commission Decision

Commission Order

Staff & Intervenors

Present Witnesses

>>

>

>

“Cost-of-Service” Study

September 2007 27 CA Energy Consulting

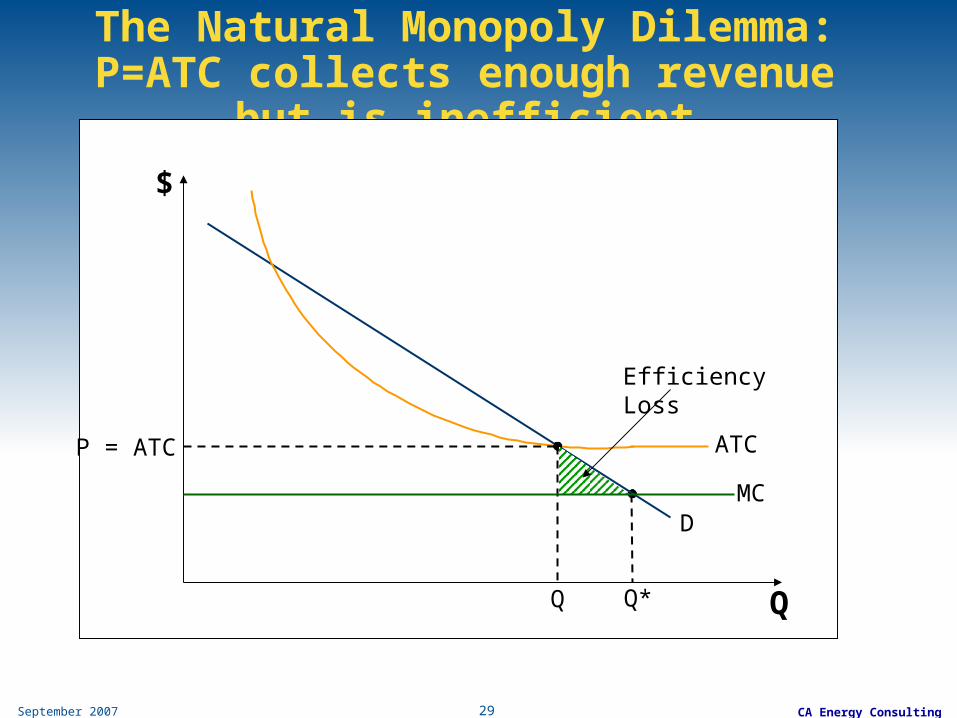

The Natural Monopoly Dilemma

A natural monopoly presents the regulator with a dilemma— Left unregulated, the monopolist could charge

high prices resulting in inefficiency and a transfer of wealth from customers to the monopolist

— Setting P=MC results in efficiency but insufficient revenues

— Set P=ATC collects sufficient revenues but is inefficient

— Issue becomes more complex with multiple products and customer classes

September 2007 28 CA Energy Consulting

The Natural Monopoly Dilemma: P=MC is efficient but revenue inadequate

$

Q

ATC

MCD

ATC

P

Q*

Losses

September 2007 29 CA Energy Consulting

The Natural Monopoly Dilemma: P=ATC collects enough revenue but is inefficient

$

Q

ATC

MCD

P = ATC

Q*Q

Efficiency Loss

September 2007 30 CA Energy Consulting

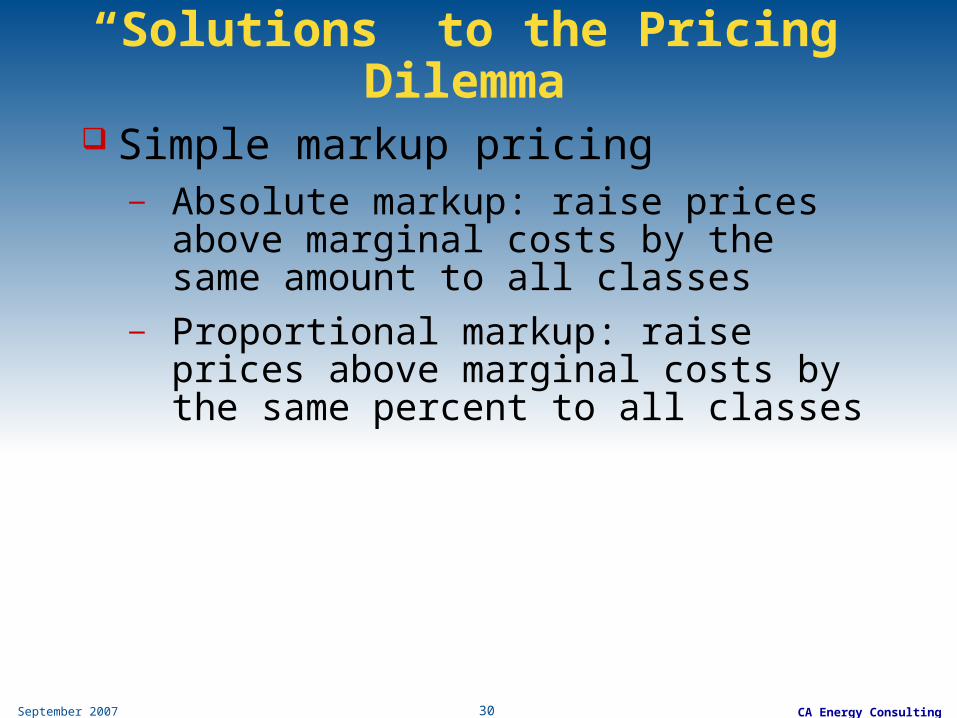

“Solutions” to the Pricing Dilemma

Simple markup pricing— Absolute markup: raise prices above marginal

costs by the same amount to all classes — Proportional markup: raise prices above

marginal costs by the same percent to all classes

September 2007 31 CA Energy Consulting

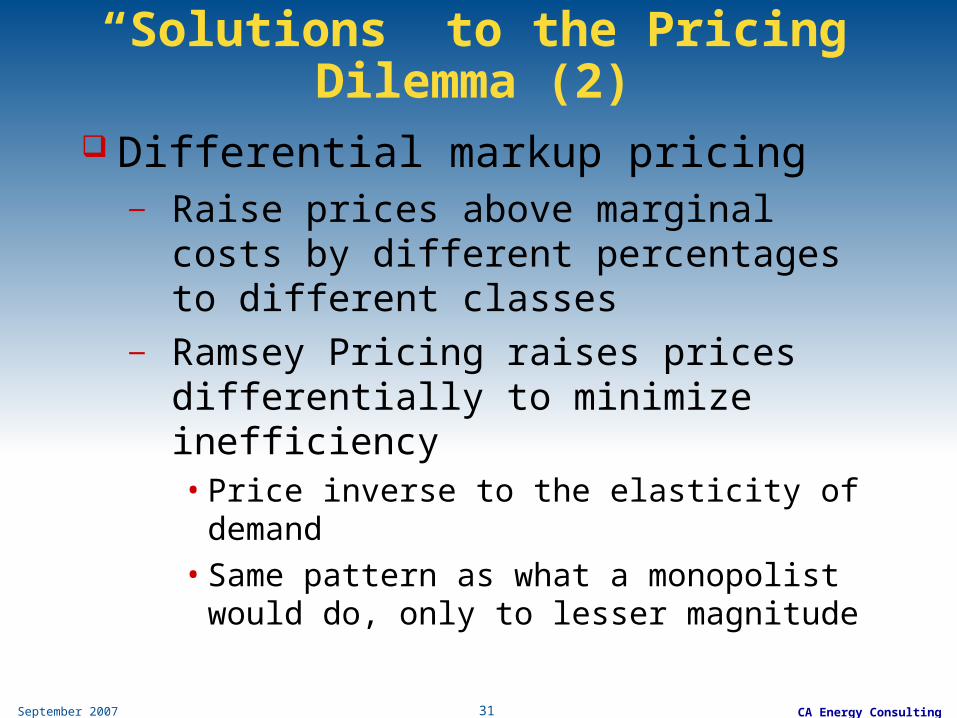

“Solutions” to the Pricing Dilemma (2)

Differential markup pricing — Raise prices above marginal costs by different

percentages to different classes— Ramsey Pricing raises prices differentially to

minimize inefficiency• Price inverse to the elasticity of demand

• Same pattern as what a monopolist would do, only to lesser magnitude

September 2007 32 CA Energy Consulting

“Solutions” to the Pricing Dilemma (3)

Non-linear pricing— Collect some fixed costs via a non-volumetric

charge (i.e., not per kWh or per kW)— If all fixed costs were collected non-

volumetrically, then per unit charge could be set at marginal cost

September 2007 33 CA Energy Consulting

Incorporating Marginal Cost Pricing Principles into Cost of Service Analysis Cost

of Service Basics

September 2007 34 CA Energy Consulting

Why investigate cost of service?

Improve understanding of the business Help with rate design Requirement for rate case

September 2007 35 CA Energy Consulting

Basic Steps for a Traditional Cost of Service Study

Determine the Overall Revenue Requirement Establish the customer classes Attribute the attributable costs Allocate the non-attributable costs Set rates to achieve the revenue requirements

September 2007 36 CA Energy Consulting

A Modified Approach: Marginal Cost-Based Cost of Service

Determine the Overall Revenue Requirement Establish the customer classes Attribute the attributable costs Set preliminary prices at marginal costs Conduct preliminary cross-subsidy analysis Mark up prices to subsidized classes to eliminate

cross-subsidies Calculate revenue insufficiency Mark up prices to all classes to achieve revenue

requirement Introduce revenue-neutral non-linear pricing to

improve pricing efficiency

September 2007 37 CA Energy Consulting

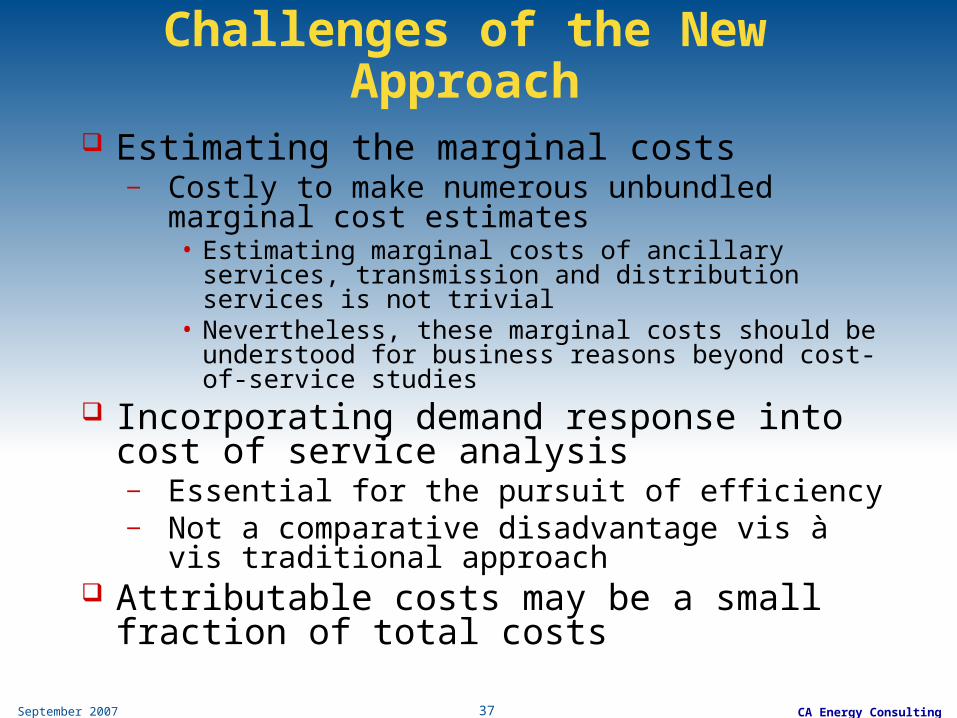

Challenges of the New Approach

Estimating the marginal costs— Costly to make numerous unbundled marginal cost

estimates• Estimating marginal costs of ancillary services, transmission

and distribution services is not trivial• Nevertheless, these marginal costs should be understood for

business reasons beyond cost-of-service studies Incorporating demand response into cost of service

analysis— Essential for the pursuit of efficiency— Not a comparative disadvantage vis à vis traditional

approach Attributable costs may be a small fraction of total

costs

September 2007 38 CA Energy Consulting

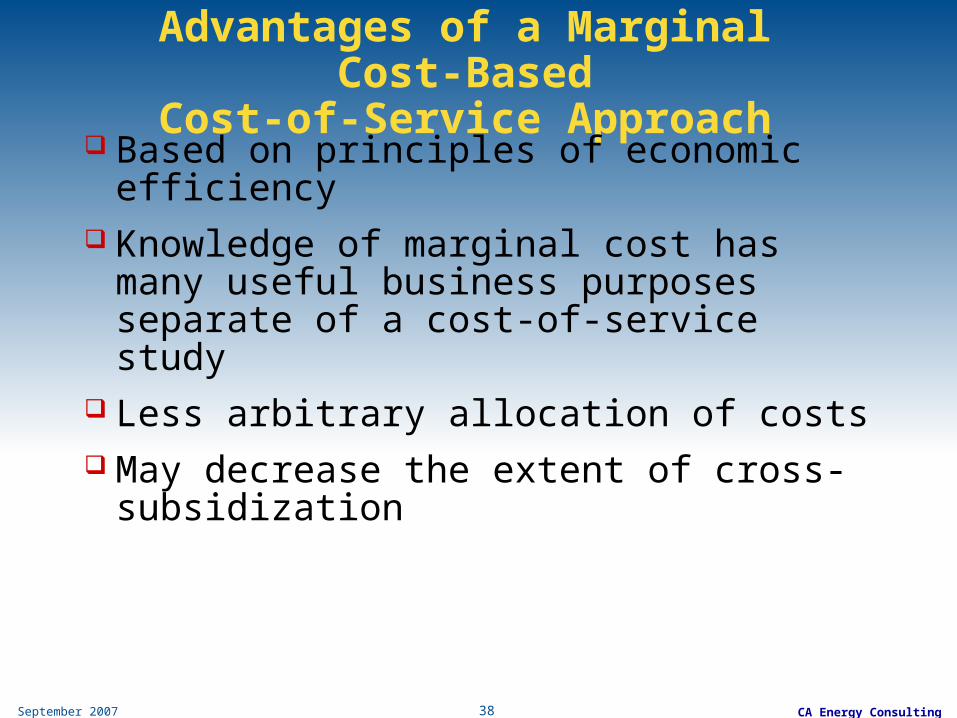

Advantages of a Marginal Cost-BasedCost-of-Service Approach

Based on principles of economic efficiency Knowledge of marginal cost has many

useful business purposes separate of a cost-of-service study

Less arbitrary allocation of costs May decrease the extent of cross-

subsidization

September 2007 39 CA Energy Consulting

Simple Stylized Example

September 2007 40 CA Energy Consulting

Three Customer Classes

Customers Additional

Sites

Average Customer Annual Usage (kWH)

Residential 1,000,000 0 10,000

Commercial 50,000 10,000 100,000

Industrial 1,000 0 1,000,000

September 2007 41 CA Energy Consulting

Marginal Costs(Assuming constant marginal cost)

Customers(annual)

AdditionalSites (annual)

Energy($/kWH)

Residential $ 100 $ - $ 0.10

Commercial $ 1,000 $ 500 $ 0.06

Industrial $ 5,000 $ - $ 0.04

September 2007 42 CA Energy Consulting

Cost Structure(Millions)

Fixed Costs

Customer Cost

Extra Site Costs

Energy Cost TOTAL

Common Cost $ 400 $ - $ - $ - $ 400

Residential $ 80 $ 100 $ - $1,000 $1,180

Commercial $ 15 $ 50 $ 5 $ 300 $ 370

Industrial $ 5 $ 5 $ - $ 40 $ 50

TOTAL $ 500 $ 155 $ 5 $1,340 $2,000

September 2007 43 CA Energy Consulting

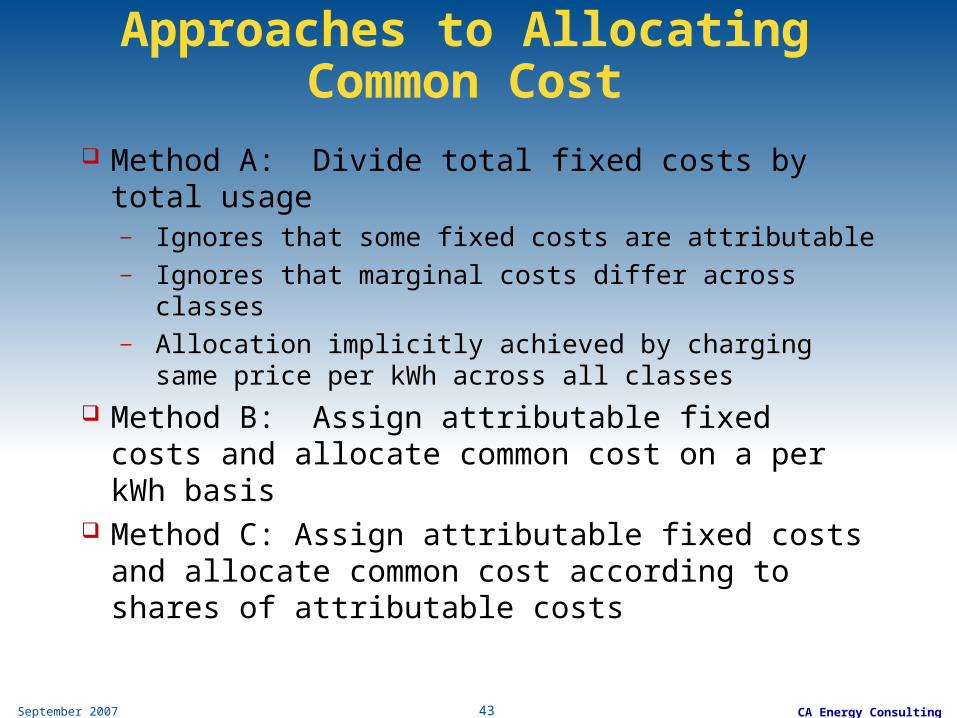

Approaches to Allocating Common Cost

Method A: Divide total fixed costs by total usage— Ignores that some fixed costs are attributable— Ignores that marginal costs differ across classes— Allocation implicitly achieved by charging same price

per kWh across all classes Method B: Assign attributable fixed costs and

allocate common cost on a per kWh basis Method C: Assign attributable fixed costs and

allocate common cost according to shares of attributable costs

September 2007 44 CA Energy Consulting

Alternative Allocations of Common Cost

Method A Method B Method C

Residential $ 70 $ 250 $ 295

Commercial $ 255 $ 125 $ 93

Industrial $ 75 $ 25 $ 13

TOTAL $ 400 $ 400 $ 400

September 2007 45 CA Energy Consulting

Cost Recovery Through Energy Pricing Only

($/kWh)

Method A Method B Method C

Residential $ 0.125 $ 0.143 $ 0.148

Commercial $ 0.125 $ 0.099 $ 0.093

Industrial $ 0.125 $ 0.075 $ 0.063

September 2007 46 CA Energy Consulting

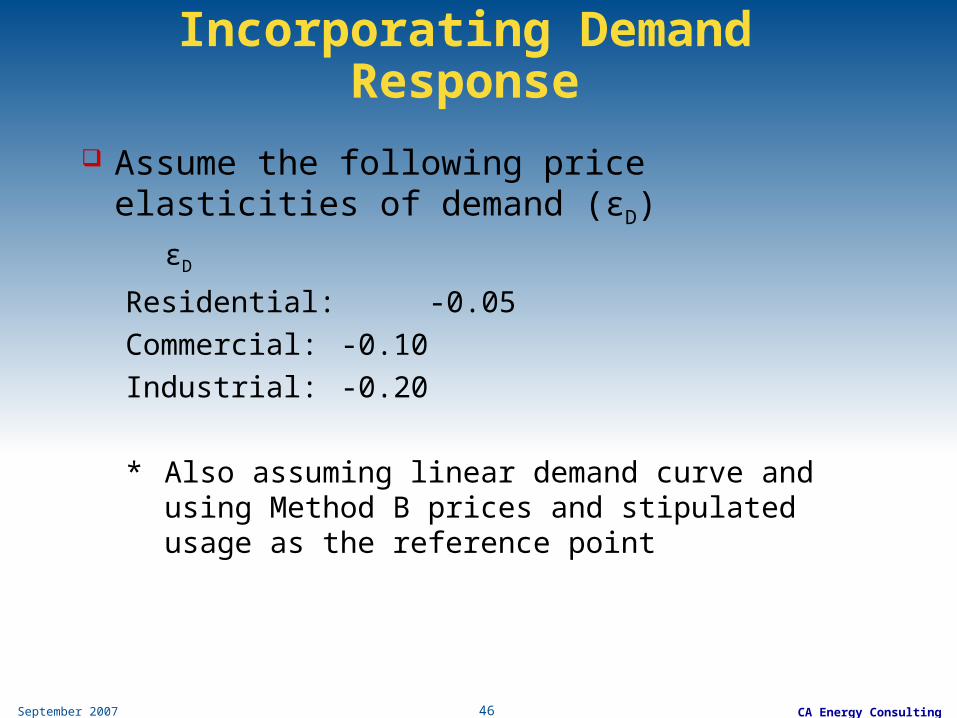

Incorporating Demand Response

Assume the following price elasticities of demand (εD)

εD

Residential: -0.05

Commercial: -0.10

Industrial: -0.20

* Also assuming linear demand curve and using Method B prices and stipulated usage as the reference point

September 2007 47 CA Energy Consulting

Recall the Efficiency Loss Triangle from Pricing Away from Marginal Cost

$

Q

ATC

MCD

P = ATC

Q*Q

Efficiency Loss

September 2007 48 CA Energy Consulting

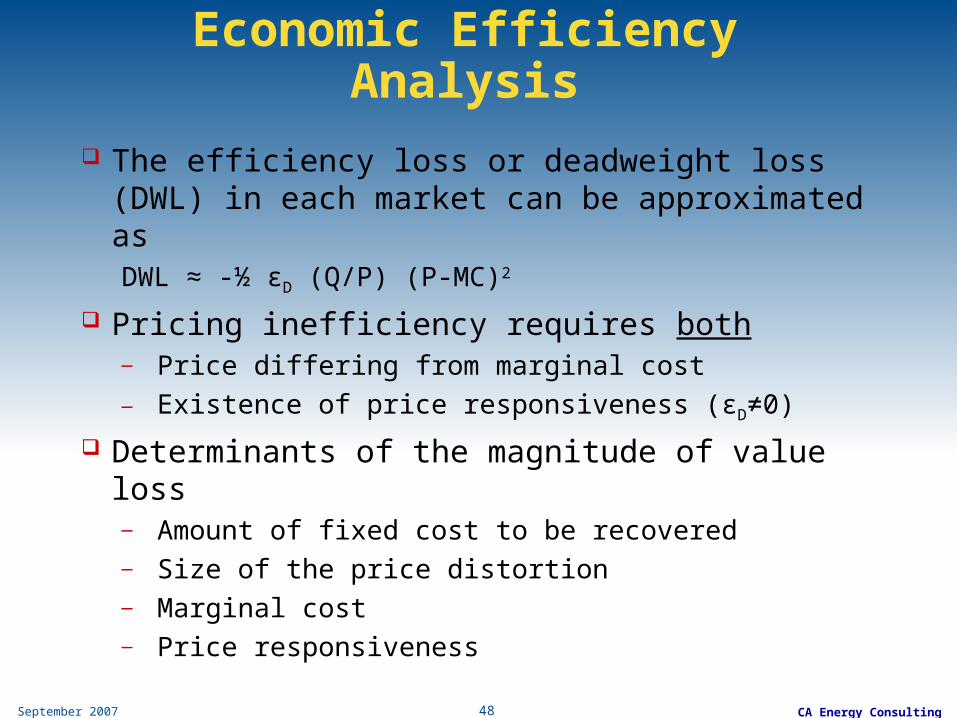

Economic Efficiency Analysis

The efficiency loss or deadweight loss (DWL) in each market can be approximated asDWL ≈ -½ εD (Q/P) (P-MC)2

Pricing inefficiency requires both— Price differing from marginal cost— Existence of price responsiveness (εD≠0)

Determinants of the magnitude of value loss— Amount of fixed cost to be recovered— Size of the price distortion— Marginal cost— Price responsiveness

September 2007 49 CA Energy Consulting

Efficiency Loss from Markup Pricing(Millions)

Method A Method B Method C

Residential $ 1.09 $ 3.23 $ 3.94

Commercial $ 10.67 $ 3.84 $ 2.67

Industrial $ 9.63 $ 1.63 $ 0.68

TOTAL $ 21.40 $ 8.71 $ 7.29

September 2007 50 CA Energy Consulting

Efficiency Loss as a Percentage of Class Revenue

Method A Method B Method C

Residential 0.09% 0.23% 0.27%

Commercial 1.71% 0.78% 0.58%

Industrial 7.71% 2.18% 1.08%

TOTAL 1.07% 0.44% 0.36%

September 2007 51 CA Energy Consulting

Non-linear Marginal Cost PricesMonthly Customer Charge

Monthly Additional Site Charge

Energy Charge ($/kWh)

Residential

Method A $ 20.83 $ 0.10

Method B $ 35.83 $ 0.10

Method C $ 39.58 $ 0.10

Commercial

Method A $ 533.33 $ 41.67 $ 0.06

Method B $ 316.67 $ 41.67 $ 0.06

Method C $ 262.50 $ 41.67 $ 0.06

Industrial

Method A $ 7,083.33 $ 0.04

Method B $ 2,916.67 $ 0.04

Method C $ 1,875.00 $ 0.04

September 2007 52 CA Energy Consulting

Non-linear Marginal Cost Prices

The price schedules listed in the preceding table are all economically efficient

The fixed charges are rolled into the customer charge

The customer charge may be too steep to for some customers within a class

— For those classes can reduce the customer charge and increase the energy charge

— Use the marginal cost pricing as starting point for adjustment

— Inefficiency introduced by raising the energy charge might not be great for very inelastic demand

September 2007 53 CA Energy Consulting

Conclusions

September 2007 54 CA Energy Consulting

Foundation of a Foundation

Cost of Service analysis provides a necessary foundation for a rate case or rate setting

Marginal cost pricing principles provide a foundation for the COS foundation

— Structurally sound: revenue recovery without cross-subsidies

— Level: achieve competitive-type efficiency— Earthquake proof: framework that allows easy and

appropriate response to competitive threats and other market dynamics

September 2007 55 CA Energy Consulting

Summary

Marginal cost pricing principles and cost-of-service objectives are compatible

Simultaneous pursuit of revenue sufficiency and maximum stakeholder value

Recovery of fixed cost is the big challenge Recovery of fixed cost via fixed charges the most

efficient High fixed charges may not be feasible for some

customer classes

September 2007 56 CA Energy Consulting

Summary

Being diligent on figuring out all variable costs reduces the fixed cost recovery burden

Getting prices aligned with marginal cost is more important for classes with greater price responsiveness, which also tend to be the competitive at-risk customers

Foundation of a Foundation