Embed Size (px)

Citation preview

DEVELOPMENT OF A MARINE

ENERGY ROADMAP FOR PANAMA

Masters of Mechanical Engineering with

Renewable Energy Individual Project

By: Chris Matthew

31st of March, 2016

i

PERSONAL STATEMENT

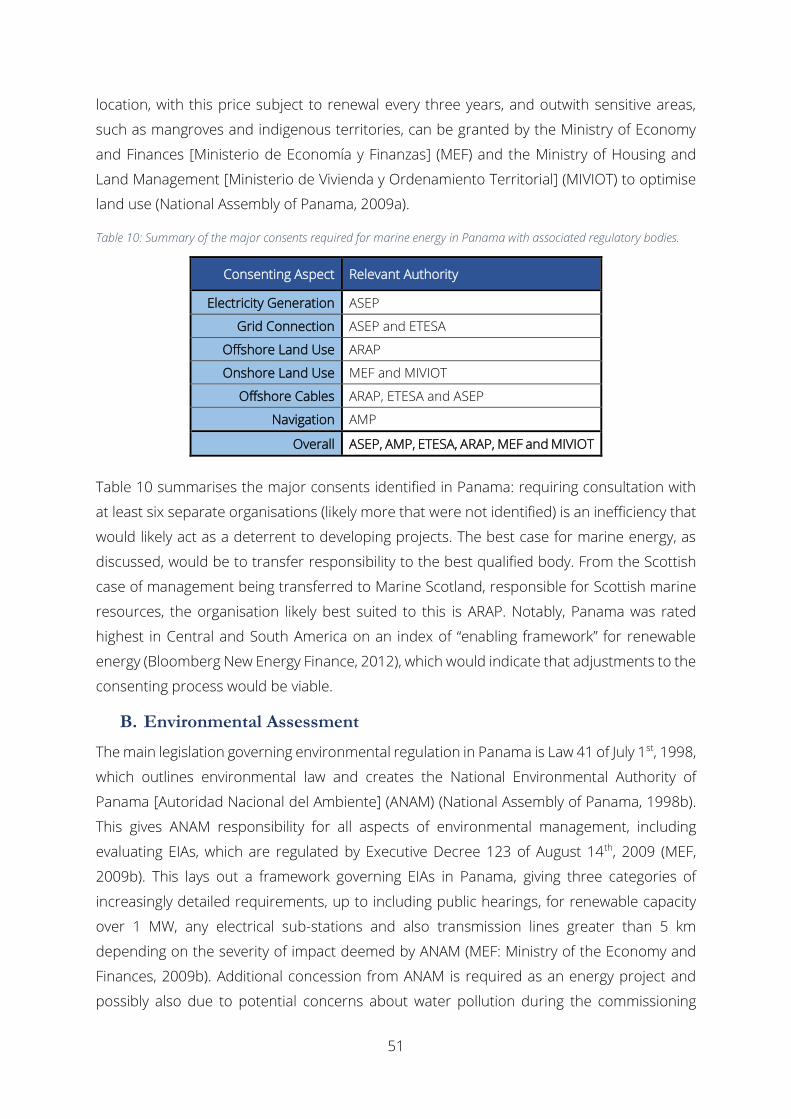

The Panamanian government recently begun an investigation into the potential of marine

energy locally. Commissioned by the UK Commonwealth Foreign Office, the Energy Policy,

Economics and Innovation department of the Institute for Energy Systems has focused on

developing a more detailed picture of the potential for marine energy in Panama. This led to

the project description being provided by Henry Jeffrey, the project supervisor along with

Laura Finlay. The outline, along with guidance from the project supervisors, provided the

basic structure of the report in terms of major aspects addressed; namely resource,

technology, infrastructure and supply chain, financial mechanisms and legislation and

regulation.

From this, my work progressed by personal investigation and collation of information for each

of the above aspects in sequence. Weekly meetings with Henry and Laura provided feedback

and, initially, direction, but the review of literature and final recommendations which

constitutes the main body of this report were conducted independently. Given my lack of

prior experience of the marine energy sector, guidance was more pronounced initially, but

subsided as the project progressed with my knowledge and understanding.

Progress in this way was steady, although a lack of fluency in Spanish was problematic at

times whilst investigating Panama, with limited information being available online in English.

I found the only other major difficulty was condensing work down: in my case several months-

of investigation yielded a significant amount of writing, not all of which was relevant to the

final report. In any case, all research was beneficial developing a more comprehensive

understanding of the sector overall which hopefully has been conveyed within.

Thank you for taking the time to read my report.

31st of March, 2016

Date

Signed

(Chris Matthew)

ii

SUMMARY

DEVELOPMENT OF A MARINE ENERGY ROADMAP FOR PANAMA

By Chris Matthew

31st of March, 2016

In this report, a roadmap for marine energy is developed for Panama, to present marine

energy as a yet-unconsidered form of electricity generation and inform strategic decision-

making. Increasing demand for diversified renewable energy in Panama is demonstrated

alongside description of the vast potential energy available in the oceans. The roadmap

structure is then presented as suitable for assessment of Panama: analysis of other

roadmaps and two decision-making tools, PESTLE and the analytic hierarchy process led to

choice of a high-level, PESTLE-style analysis with alternative subheadings given the example

of other marine energy roadmaps.

An understanding of the marine energy sector globally was then developed in terms of

resource, technology, infrastructure and supply chain, finances and legislation and regulation.

This is used to assess Panama relative to these factors, allowing determination of strengths

of and gaps in the local marine energy landscape. Analysis both globally and locally in Panama

is conducted for each subheading, followed by brief discussion of the findings.

Based on this, recommendations are made with respect to what steps would be necessary

for both deployment and development scenarios for marine energy. Certain aspects are

found to be eminently suitable for marine energy, such as the ocean thermal energy

conversion (OTEC) resource, tidal barrage supply chain, infrastructure associated with the

Panama Canal and success with existing wind and solar laws. However, other aspects are

identified as requiring development, including: further investigation of the tidal range and

OTEC resource, development of infrastructure and expansion outwith the canal,

implementing appropriate financial mechanisms and developing a marine spatial plan, a

“one-stop-shop” consenting process and a strategic environmental assessment for OTEC.

These major recommendations are presented graphically to form the main conclusions of

the report.

iii

TABLE OF CONTENTS

1. INTRODUCTION .......................................................................................................................... 1

1.1. Project Motivation ............................................................................................................. 1

1.2. Project Outline ................................................................................................................... 4

2. LITERATURE REVIEW .................................................................................................................. 6

2.1. Technology Roadmaps ..................................................................................................... 6

2.2. Renewable Energy Roadmaps ........................................................................................ 7

2.3. Marine Energy Roadmaps ............................................................................................... 8

2.4. Decision Making Comparison ......................................................................................... 9

2.4.1. PESTLE Analysis Outline ................................................................................... 9

2.4.2. Analytic Hierarchy Process Outline ............................................................. 10

2.4.3. Comparison of Analytic Hierarchy Process and PESTLE ........................ 11

3. METHODOLOGY ...................................................................................................................... 12

4. RESULTS AND DISCUSSION .................................................................................................. 14

4.1. Marine Energy Resource................................................................................................ 14

4.1.1. Resource Case Studies................................................................................... 14

4.1.2. Resource in Panama ....................................................................................... 18

4.1.3. Discussion ......................................................................................................... 23

4.2. Technology, Infrastructure and Supply Chain .......................................................... 24

4.2.1. Available Technology ...................................................................................... 25

4.2.2. Infrastructure and Supply Chain Requirements ...................................... 29

4.2.3. Infrastructure and Supply Chain in Panama ............................................. 31

4.2.4. Discussion ......................................................................................................... 36

4.3. Financial Mechanisms .................................................................................................... 37

4.3.1. The Need for Financial Mechanisms in Renewable Energy ................... 37

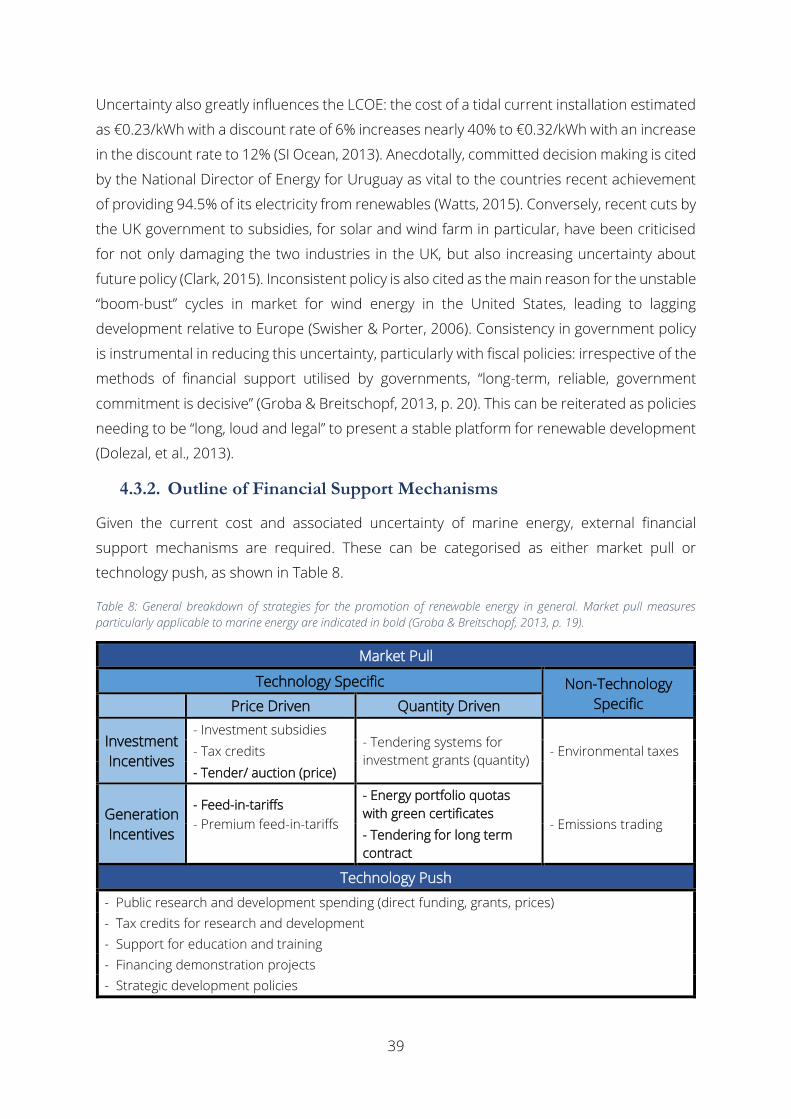

4.3.2. Outline of Financial Support Mechanisms ................................................ 39

4.3.3. Financial Mechanisms in Panama ............................................................... 43

4.3.4. Discussion ......................................................................................................... 45

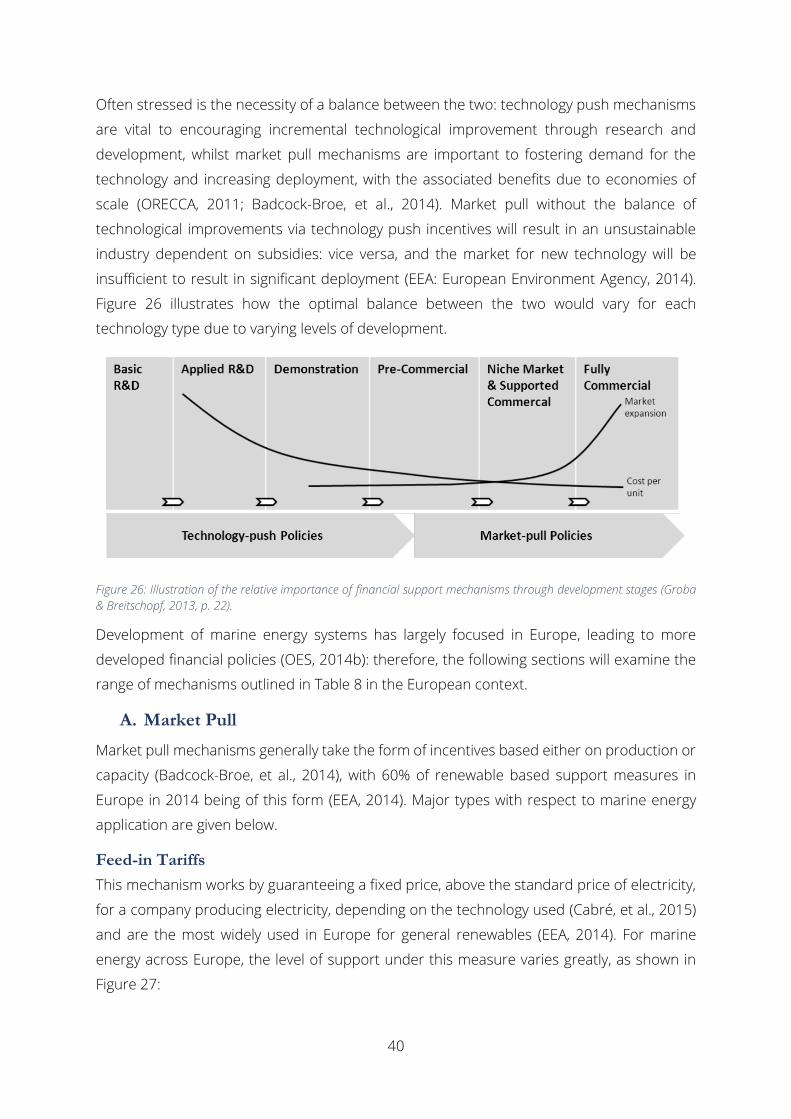

iv

4.4. Legislation and Regulation ............................................................................................ 46

4.4.1. Marine Energy Legislation and Regulation ................................................ 46

4.4.2. Legislation and Regulation in Panama ....................................................... 50

4.4.3. Discussion ......................................................................................................... 53

5. RECOMMENDATIONS ............................................................................................................. 54

5.1. Deployment Scenario ..................................................................................................... 55

5.2. Development Scenario ................................................................................................... 56

6. CONCLUSIONS ........................................................................................................................ 58

REFERENCES ...................................................................................................................................... 60

v

GLOSSARY

AHP : Analytic hierarchy process

AMP : National Marine Authority of Panama [La Autoridad Marítima de

Panamá]

ANAM : National Environment Authority [Autoridad Nacional del Ambiente]

ARAP : Authority on the Aquatic Resources of Panama [Autoridad de los

Recursos Acuáticos de Panamá]

ASEP : National Authority of Public Services [Autoridad Nacional de los

Servicios Publicos]

EEA : European Environment Agency

EIA : Environmental impact assessment

EMEC : European Marine Energy Centre

ETESA : Electricity Transmission Company of Panama [Empresa de Transmisión

Eléctrica, S.A]

FiT : Feed-in-tariff

GIS : Geographic information system

IRENA : International Renewable Energy Agency

LCOE : Levelised cost of electricity

MEF : Ministry of Economy and Finances [Ministerio de Economía y Finanzas]

MHK : Marine hydro-kinetic

MIVIOT : Ministry of Housing and Land Management [Ministerio de Vivienda y

Ordenamiento Territorial]

MSP : Marine spatial plan

NCRE : Non-conventional renewable energy

OES : Ocean Energy Systems

ORECCA : Off-shore Renewable Energy Conversion platforms – Coordination

Action

OTEC : Ocean thermal energy conversion

ROC : Renewable Obligation Certificate

SEA : Strategic environmental assessment

TEC : Tidal energy converter

WEC : Wave energy converter

1

1. INTRODUCTION

1.1. Project Motivation

Panamanian per capita electricity demand has nearly quadrupled since 1971, its population

grew from 1.5 million to 3.8 million over the same period (World Bank, 2015) and electrical

generation capacity increased from 560 MW in 1980 (Energy Information Agency, 2015) to

2,746 MW in May 2015 (Gómez, 2015). This growth is expected to continue, with the

Panamanian National Energy Secretariat [Secretaría Nacional de Energía] estimating

electrical energy consumption will increase from approximately 9,000 GWh in 2015 to 12,000

GWh in 2025, with peak demand roughly doubling to 2,900 MW (National Energy Secretariat ,

2009). As such, there is a clear need in Panama for new electricity generating capacity to

meet this increasing demand.

Existing capacity has been split largely between hydropower and fossil fuels, with

hydroelectric decreasing from 80% of installed capacity in 1996 (National Energy Secretariat ,

2009) to 52% in May 2015 (Gómez, 2015). This dependency on just two main sources of

electricity has been problematic, with the de-rated capacity margin (a metric used to assess

security of supply) falling to 0% in 2010 (National Competitiveness Centre, 2015) and

emergency electricity rationing enforced in 2013 due to a period of drought restricting

hydroelectric capacity (Kriel, 2013). Although as much as 3,040 MW of further potential

hydropower development has been identified (National Energy Secretariat , 2009), this or the

construction of additional fossil fuel plants will only mitigate the underlying problem of

ensuring security and robustness of supply, as Panama has no indigenous fossil fuels (World

Energy Council, 2013a),

Although the causal relation between economic growth and electrical consumption has been

debated (Payne, 2010; Ozturk, 2010), it is apparent that shortages of electricity supply will

negatively affect development. Given the over-reliance on just two sources it is clear that

diversification is the best option, with it generally agreed that diversification and import

dependency contribute positively and negatively respectively towards energy security

(Lesbirel, 2004; Li, 2005; Sovacool & Mukherjee, 2011). Development of local renewable

energy sources will both increase diversity in the electricity supply and also reduces import

dependency. This has already been recognised by the Panamanian government, with goals

of combatting climate change, reducing emissions and diversifying supply outlined in

legislation such as Executive Decree No. 36 of 2007 (National Assembly of Panama, 2007)

and Law No. 45 of 2004 (National Assembly of Panama, 2004).

2

Specific laws have already led to deployment of significant renewable capacity in Panama.

This includes 337 MW of onshore wind (Lewis & Behar, 2015) and 66 MW of solar power

(ETESA: Electricity Transmission Company of Panama, 2014). However, even with these

indications of moving away from traditional capacity, consideration thus far in Panama has

been solely of these two technologies. The most recent National Energy Plan [Plan Nacional

de Energía] for 2009-2023 mentions marine energy as at a “frankly experimental stage” which

will “not contribute measurably to national future energy” (National Energy Secretariat , 2009,

pp. 87, Author's Translation). Despite this, Panama already displays promising suitability for

marine energy technology: possessing 2,500 km of coastline adjacent to both the Pacific

Ocean and Caribbean Sea (Central Intelligence Agency, 2013) and having a strong vested

interest in the oceans, with marine sectors generating roughly 20% of GDP (Ibañez, 2014).

Oceans contain energy in numerous ways, including gravitational potential, kinetic, chemical

and thermal energy. Useful energy that can be converted into electricity can be broken down

into waves, tidal range, tidal currents, open ocean currents, thermal energy differentials and

osmotic potential (Lewis & Estefen, 2011). Of these, technological maturity varies greatly.

Tidal barrage is the most mature, with megawatt scale capacity deployed in 1968 (Bernshtein,

1972). Ocean current, by comparison, remains at a conceptual stage pending improvements

in turbine technology to utilise slower flow rates (Bedard, et al., 2010). In this report, the focus

will be on wave, tidal current, tidal range and ocean thermal energy conversion (OTEC).

Osmotic power and ocean currents are omitted as both sectors are considered too

immature to make an understanding of factors, such as available resource and technology

requirements, too uncertain; rendering further analysis unreliable (Mofor, et al., 2014).

Estimates of the globally available marine energy resource vary considerably, but all concur

that for each of the four types above the potential is significant. One estimate puts the

theoretical potential for all technologies at as high as 7,400 EJ/year (2,055,555 TWh/year)

(Lewis & Estefen, 2011), as much as 15 times greater than global primary energy

consumption in 2013 (Energy Information Agency, 2015). Shown in Figure 1, waves are

estimated to contain 29,000 TWh/year globally, largely confined to latitudes of 30-60° (Mørk,

et al., 2010). OTEC estimates includes 55,000 TWh/year (Lockheed Martin, 2012), with the

complementary distribution at latitudes of less than 30° shown in Figure 2. Energy estimates

for tidal current and tidal range are highly dependent on local topography and other factors,

making global energy estimates problematic, but consideration of both sources gave a total

of 7,800 TWh/year (OES: Ocean Energy Systems, 2011). Distribution of the M2 tidal range (the

principal semidiurnal component) is shown in Figure 3 to indicate the distribution of

significant resource.

3

Figure 1: Global wave power depiction (Cornett, 2008).

Figure 2: Global average temperature difference between 20-1000m water depths (Vega, 2014, p. 20).

Tidal Range (cm)

0

70 35 105 140

Figure 3: Global map of the M2 tidal constituent (OES, 2011).

4

1.2. Project Outline

Given the enormous potential of marine energy and the clear demand for diversified

electricity, marine energy should be given due consideration. Technology or sectoral

roadmapping is widely used in the renewable energy industry as “A future based strategic

planning device” (Winebrake, 2003, p. 1) and is an excellent tool for assessing the potential

for marine energy in Panama. This represents the main aim of this project: to use the

roadmap structure to create a strategic proposal for the potential development and

commercialisation of the marine energy sector in Panama.

This report first examines existing roadmaps in the Literature Review (p. 6); starting with their

general structure, before analysing specific renewable energy and marine energy examples

to determine common features and how to best structure analysis. Two decision making

tools are discussed and compared in detail:

PESTLE: an open ended analysis of the Political, Economic, Social, Technological,

Legal and Environmental aspects.

Analytic Hierarchy Process (AHP): a systematic method of analysing complex

decisions with multiple solutions.

The PESTLE approach was then determined, in the Methodology (p. 12), to be more

appropriate given the nature of the project. However, given the barriers and strategies

outlined in existing marine energy roadmaps, an alternative framework described below was

determined to be more appropriate. The main body of the report is dedicated to the Results

and Discussion (p. 14), where the global case best suited to facilitating marine energy is

determined and compared to conditions in Panama for the following subheadings:

1. Resource, which entails four case studies, one for each energy source, from countries

with some of the most significant resource globally to compare with the Panamanian

example.

2. Technology, infrastructure and supply chain, where examination of current

technology allows understanding of infrastructural and supply chain requirements:

from this Panamanian suitability for developing or deploying each technology is

discussed.

3. Financial Mechanisms, in terms of mechanisms to encourage marine energy, are

outlined and compared to existing general renewable energy measures in Panama.

4. Legislation and regulation for marine energy is considered, leading to identification of

key barriers and how best to reduce these in Panama.

5

From this understanding of the critical factors influencing the marine energy sector both

globally and in Panama, a strategic plan to be outlined as described in the Recommendations

(p. 54). This is based on two scenarios: one, more passive approach, involving deployment of

technologies improved and developed elsewhere globally and the other, more proactive

approach, involving the development of technology locally. The suitability of the existing

landscape in Panama is discussed, with the measures which would need to be enacted

summarised graphically. This enhanced understanding of the potential for marine energy

locally, as well as the steps (and importantly an indication of the level of investment required)

which best facilitate its development, allows for better informed decision making in Panama

regarding developing electricity generation capacity.

6

2. LITERATURE REVIEW

2.1. Technology Roadmaps

Technology roadmaps were formally developed by Motorola in the 1970s, initially for product

planning at a company level (Willard & McClees, 1987). A roadmap can be summarised as “A

future based strategic planning device that outlines the goals, barriers, strategies necessary

for achieving a given vision of technological advancement and market penetrations”

(Winebrake, 2003, p. 1). Generally, roadmaps consider three key points (Amer & Daim, 2010):

1. Determining a vision in terms of targets and goals;

2. Determining the current state of affairs relative to this;

3. Outlining what steps would be necessary to implement the stated vision.

This provides an extended outlook, which identifies critical factors and allows better informed

investment in developing technology (Bray & Garcia, 1997). They also provide a vital tool for

maximising the effectiveness of innovation via systematic analysis of the technology or sector

(Rinne, 2004).

Flexibility in terms of the process and overall structure allows roadmaps to be developed for

a wide range of focuses and scales, from the level of individual companies to globally (Phaal,

et al., 2004). One review identified more than 2,000 public domain roadmaps (Phaal, 2011),

ranging from exploration of the solar system (NASA, 2006) to the medical applications of

nanotechnology (Hartwig, 2006). Roadmap structures vary massively, depending on the

application, context and desired outcomes in terms of planning (Kappel, 2001), but at the

broadest level one review categorised roadmaps as of two main types: “entity level”, which

generally focus on broader scales and themes, and “attribute level”, which examine specific,

quantifiable factors (Kajikawa, et al., 2008). Given the quantitative requirements of “attribute

level” roadmaps, they were observed to occur more for established, mature sectors (Kajikawa,

et al., 2008). Additionally, for all roadmaps some form of multi-layered graphical plan

connecting the technology with market opportunities was also included (Carvalho, et al.,

2012), as shown in Figure 4:

7

Figure 4: Generic technology roadmap architecture (Carvalho, et al., 2012, p. 1419).

Although a flexible and adaptable roadmap structure allows application to a wide variety of

subjects, the lack of a “template” is cited as one reason for difficulty in execution on an

ongoing basis (Phaal, et al., 2004). Similarly, given the predictive and time dependent nature

of roadmaps, keeping them up-to-date with current events as they affect the underlying

assumptions becomes problematic (Lee & Park, 2005). Despite this, the process of creating

a roadmap can be more useful than the finished product, via the dialogue, investigation and

understanding developed (Grossman, 2004).

2.2. Renewable Energy Roadmaps

Roadmaps focusing specifically on renewable energy share the same breadth of format as

general roadmaps. They can be classified as one of three levels: at a national scale, with focus

on energy security, policy and dependence; at a sectoral scale, with focus on common needs,

barriers to development and overall risks; or at an organisational scale, to evaluate and

prioritise research and development towards stated goals (Amer & Daim, 2010). The

European Renewable Energy Council renewable energy roadmap for member states is an

example of the former, providing consumption targets along with plans for increasing the

share of individual technologies (European Renewable Energy Council, 2002). Sector level

roadmaps are generally developed by consortia of companies, research laboratories or

government departments (Amer & Daim, 2010). An example of this type is the Canadian wind

technology roadmap, which helped develop a consensus on key issues and provided

recommendations following from several workshops involving the government, industry and

academia (Natural Resources Canada, 2009). Finally, a roadmap for the hydrogen fuel cells is

an example of an organisational roadmap, making key recommendations for investment

decisions for the Canadian Institute for Fuel Cell Innovation (Sparrow & Whittaker, 2005).

8

Analysis of this classification determined that national level roadmaps were closer to the

“entity level” type, with longer term forecasts befitting to the greater level of uncertainty.

Organisational roadmaps were closer to the “attribute level” end of the spectrum, given the

definite specifications and requirements available, with this type also occurring more

frequently for mature technologies such as wind (Amer & Daim, 2010).

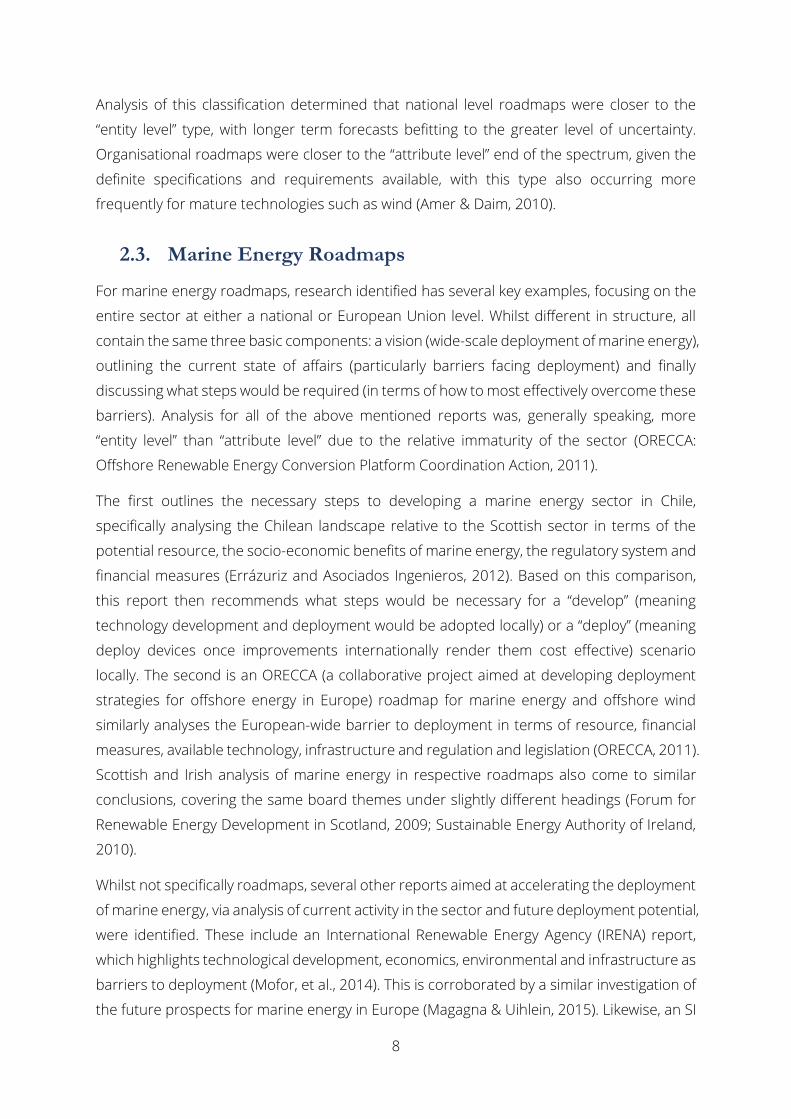

2.3. Marine Energy Roadmaps

For marine energy roadmaps, research identified has several key examples, focusing on the

entire sector at either a national or European Union level. Whilst different in structure, all

contain the same three basic components: a vision (wide-scale deployment of marine energy),

outlining the current state of affairs (particularly barriers facing deployment) and finally

discussing what steps would be required (in terms of how to most effectively overcome these

barriers). Analysis for all of the above mentioned reports was, generally speaking, more

“entity level” than “attribute level” due to the relative immaturity of the sector (ORECCA:

Offshore Renewable Energy Conversion Platform Coordination Action, 2011).

The first outlines the necessary steps to developing a marine energy sector in Chile,

specifically analysing the Chilean landscape relative to the Scottish sector in terms of the

potential resource, the socio-economic benefits of marine energy, the regulatory system and

financial measures (Errázuriz and Asociados Ingenieros, 2012). Based on this comparison,

this report then recommends what steps would be necessary for a “develop” (meaning

technology development and deployment would be adopted locally) or a “deploy” (meaning

deploy devices once improvements internationally render them cost effective) scenario

locally. The second is an ORECCA (a collaborative project aimed at developing deployment

strategies for offshore energy in Europe) roadmap for marine energy and offshore wind

similarly analyses the European-wide barrier to deployment in terms of resource, financial

measures, available technology, infrastructure and regulation and legislation (ORECCA, 2011).

Scottish and Irish analysis of marine energy in respective roadmaps also come to similar

conclusions, covering the same board themes under slightly different headings (Forum for

Renewable Energy Development in Scotland, 2009; Sustainable Energy Authority of Ireland,

2010).

Whilst not specifically roadmaps, several other reports aimed at accelerating the deployment

of marine energy, via analysis of current activity in the sector and future deployment potential,

were identified. These include an International Renewable Energy Agency (IRENA) report,

which highlights technological development, economics, environmental and infrastructure as

barriers to deployment (Mofor, et al., 2014). This is corroborated by a similar investigation of

the future prospects for marine energy in Europe (Magagna & Uihlein, 2015). Likewise, an SI

9

Ocean report (another project towards a common strategy for wave and tidal current

deployment) determined that the major risks affecting deployment are financial,

technological, consenting and infrastructural (Badcock-Broe, et al., 2014). These major

subheadings identified in existing marine energy roadmaps and other reports will be

discussed subsequently in the Methodology to determine the most suitable structure.

2.4. Decision Making Comparison

A major feature of all these roadmaps is the collation information to improve the

effectiveness of decision making. Again, flexibility can be seen as a strength of the loose

structure, allowing incorporation of other management practices such as SWOT analysis, the

Delphi method, quality function deployment, PESTLE analysis and AHP (Amer & Daim, 2010).

In the context of this project and of marine energy in Panama though, not all techniques

would be equally applicable. For example the Delphi technique functions by collating

assessments from experts of the field in question (Hsu & Sandford, 2007) and quality

function deployment was developed towards product refinement at a company level rather

than considering the potential for an entire industry (Govers, 1996). Following

recommendations from both the project supervisors and the project examiner, PESTLE

analysis and AHP are compared here to determine which would be more suitable in

conjunction with the sectoral-scale roadmap structure.

2.4.1. PESTLE Analysis Outline

PESTLE analysis, which stands for “Political, Economic, Social, Technological, Legal and

Environmental”, is where an option is assessed individually in the stated terms (Havas, 2012).

This involves some form of investigation to identify relevant factors and then an assessment

to determine the impact and implications of the findings (Team FME, 2013). A selection of

factors, which could be considered for each section, is shown in Table 1:

Table 1: Non-exhaustive list of generic factors for consideration in a PESTLE analysis (Kolios & Read, 2013) (Team FME,

2013).

Political Government stability, bureaucracy issues, taxation and “green” targets

Economic Financing, technology push and market pull mechanisms

Social Public perceptions, education, demographics and support

Technological Rate of development, deployment, industry standards and supply

chain

Legal Regulatory bodies, consenting process and grid connection

Environmental Environmental impact, legislation, agencies and CO2 abatement

10

PESTLE analysis is widely used in the general analysis of renewable energy: examples include

for risk identification for the tidal industry in the UK (Kolios & Read, 2013), the development

of renewable energy in Malawi (Zalengera, et al., 2014) and analysing the progress of

renewable energy in the most recent EU member states (Patlitzianas & Karagounis, 2011).

Generally speaking, PESTLE analysis is used as “generic orientation tool” (Team FME, 2013, p.

11) to analyse the situation, rather than making absolute conclusions or deciding between

given options.

2.4.2. Analytic Hierarchy Process Outline

AHP is a multi-criteria decision making tool that operates quantitatively not by giving an

absolute answer, but by assessing options relative to each other (Brunelli, 2015). The main

steps are shown below (Saaty, 2008):

1. Definition of the problem and determination of type of answer sought;

2. Structure the decision hierarchy, as shown in Figure 5: with the top being the ultimate

aim and intermediate levels indicating assessment criteria, with the available options

given at the bottom;

Figure 5: Example of a simple AHP for selecting a job based on the main criteria of flexibility, opportunity, security,

reputation and salary (Saaty, 2008, p. 87).

3. Construct pairwise comparison matrices to evaluate each assessment criteria relative

to each other, giving weightings for each;

4. Assessment of each decision which feeds back into the previously determined

weightings to determine the best choice.

11

This process becomes increasingly complex given greater numbers of criteria and options

available (Brunelli, 2015), and so a wide variety of software is available to simplify the AHP

decision making process. Foremost is Expert Choice, developed by the creator of AHP,

Thomas Saaty (Ishizaka & Labib, 2009).

Similarly to PESTLE analysis, AHP is also widely used in the assessment of renewable energy,

including: the assessment of renewable energy alternatives for Istanbul (Kaya & Kahraman,

2010), the prioritisation of risks to tidal energy projects in the UK (Kolios, et al., 2013) and the

ranking of renewable technologies available to implement in Spain (Cristobal, 2011). In these

cases, the assessment was of discrete solutions to a given problem, with absolute solutions.

2.4.3. Comparison of Analytic Hierarchy Process and PESTLE

The main difference between the two methods is that AHP allows the user to decide between

a finite number of discrete and similar solutions whereas PESTLE follows an open-ended

methodology that allows for a more qualitative approach. This is evidenced by the literature

reviewed: AHP decision making tends to be between individual technologies (Kaya &

Kahraman, 2010; Cristobal, 2011) rather than assessment of the potential of a sector (Kolios

& Read, 2013; Zalengera, et al., 2014); the latter being more similar to the purpose of this

project.

In the case of marine energy in Panama, the conclusions drawn are unlikely to be as

completely clear-cut as deciding between which technology type would be best suited for all-

out development and deployment, as the progression of a new electricity generating

technology in a country will be more nuanced than a simple “yes or no” decision. Given the

definition of a roadmap as a tool that “outlines the goals, barriers, strategies necessary for

achieving a given vision of technological advancement and market penetrations” (Winebrake,

2003, p. 1), this report is not aimed to make an absolute judgement on the possibility of

deployment of marine energy but to develop the possibilities and potential for the industry.

Given the inherent uncertainty and immense range of factors influencing the future of an

entire sector, the flexible approach afforded by PESTLE would be more appropriate than a

deterministic, absolute one such as AHP.

12

3. METHODOLOGY

Investigation of general technology roadmaps indicates that as marine energy is a relatively

immature sector it is better suited to an “entity level” analysis given the lack of more specific

“attribute level” information. Review of renewable energy specific roadmaps, particularly at

the sectoral scale, showed that emphasis would be best placed on common needs and

barriers to deployment. This was further corroborated by sectoral marine energy roadmaps

and other reports: generally all focused on identifying barriers to deployment and discussing

how best to remove or reduce these to maximise development and deployment. As such, for

this type of national scale analysis of the marine energy sector in Panama, it can be

determined that a general “entity level” analysis of factors influencing marine energy is more

appropriate, rather than the specific attributes governing it.

PESTLE was determined to be a better suited decision making tool in the case of marine

energy in Panama, however, given the range of issues addressed in other marine energy

roadmaps, a modified structure to PESTLE is more appropriate. Otherwise, crucial

components of successful marine energy sector may be neglected, such as the available

resource and infrastructure requirements. To address the major factors affecting the

development of marine energy in Panama, a PESTLE-style methodology will be used, but with

the following subheadings adapted from marine energy roadmaps. In each case, a review of

the wide range of literature describing the “best practice” for encouraging marine energy

development will be compared to the existing Panamanian landscape.

1. Resource: Focus on developing an understanding of how the characteristics of an

ocean, in terms of wave behaviour, tidal velocities, tidal range and temperature

difference, can be considered significant in terms of energy potential. This is then

be used to assess available information about the potential of each energy type

in Panama.

2. Technology, Infrastructure and Supply Chain: Examination of the current

development of technology of all types will better consideration of the

infrastructure and supply chain requirements across the sector and individually

for specific technologies. This will then determine the adequacy of the existing

landscape for technology development or deployment, so highlighting necessary

areas for development.

3. Financial Mechanisms: Analyse the array of financial support mechanisms best

suited to maximising development and deployment of marine energy; whether by

creating a favourable market via “market pull” or encouraging technological

13

improvements via “technology push”. This is then compared to existing energy

financial mechanisms in place in Panama.

4. Legislation and Regulation: How marine energy fits into existing energy legislation

and regulation, renewable or otherwise; particularly how to expedite the process,

thereby reducing it as a barrier to development. The Panamanian legislative and

regulative outlook will then be analysed to determine which steps would best

encourage marine energy.

Following this investigation of “best practice” and comparison with the case of Panama,

recommendations will be made via two scenarios, similarly to the marine energy

roadmap for Chile (Errázuriz and Asociados Ingenieros, 2012). First is a “deployment”

scenario, which involves delaying deployment of marine energy devices or systems until

global improvements in technology render them cost effective. Although more passive,

this still entails ensuring that the marine energy landscape, with respect to the identified

factors above, is optimised for marine energy deployment. The second of these scenarios

is “development”: namely, taking the active approach of investment in local technology

development, rather than waiting for cost reductions to occur elsewhere. Given that a

graphical plan was identified as a common feature of roadmaps, these steps described

will also be summarised graphically to represent the key recommendations of the project.

14

4. RESULTS AND DISCUSSION

4.1. Marine Energy Resource

This section examines the marine energy resource for wave, tidal current, tidal range and

OTEC in Chile, UK, South Korea and the US respectively, which have all been recognised

globally for their resource. The case in Panama is then examined to determine the relative

significance of the local resource.

4.1.1. Resource Case Studies

A. Wave Energy in Chile

Casual observation of the global wave energy map in Figure 1 (p. 3), confirms that Chile is

“one of the most suitable places in the world for the generation of electrical power from wave

energy” (Monárdez, et al., 2008, p. 8; Errázuriz and Asociados Ingenieros, 2012). Due to this,

several detailed studies have been carried out, foremost of which is summarised in Figure 6

(Monárdez, et al., 2008), in addition to another study (Garrad Hassan, 2009). The wave power

is shown to vary from an annual average of 20-120 kW/m depending on the latitude.

Figure 6: Results of the two main studies of wave energy in Chile (Errázuriz and Asociados Ingenieros, 2012, p. 23).

Chile also displays favourable seasonable variability: shown in Figure 7, which demonstrates

that the available resource remains significant year round, save for in the north. For the

majority of the sites shown in Figure 6 the P90% (the percentage of the time the given power

15

is exceeded, in this case 90%) was always above 10 kW/m, as well as optimum capacity factors

ranging from 50-60%, among the highest in the world (Monárdez, et al., 2008).

Figure 7: Monthly distribution of wave power for the Northern, Central and Southern Chile at a depth of 25m (Monárdez,

et al., 2008, p. 4).

B. Tidal Current in the United Kingdom

The UK is recognised as possessing one of the most significant tidal current resources in the

world (Renewable UK, 2013), with peak mean tidal velocities of 3.8m/s at Kyle Rhea (Black &

Veatch, 2011). Final energy estimates however are sensitive to assumptions required, due to

the lack of large scale generating capacity on which to base energy extraction models (Black

& Veatch, 2005): estimates shown in Table 2 vary by up to three times. Classification of

significant tidal flow also varies: for device cut-in speeds between 0.7 m/s (Crown Estate, 2013)

and 1.5 m/s (Black & Veatch, 2005), with current greater than 2.5 m/s considered necessary

to generate significant energy (Lewis, et al., 2015).

Table 2: List of studies regarding the available energy from tidal current in UK waters.

Study Extractable Resource

European Commission (1996) 30.8 TWh/y

Black & Veatch (2005) 18 TWh/y (±30%)

Black & Veatch (2011) 29 TWh/y (-45%/ +30%)

Crown Estate (2013) 20.9 TWh/y

16

Tidal current resource is usually constrained by coastal topography, occurring most

commonly around features such as narrow straights, headlands and estuaries (Lewis &

Estefen, 2011). This is evidenced by up to 80% of the potential in the UK occurring in just ten

sites (Black & Veatch, 2005); depicted in Figure 8.

Figure 8: Depiction of the location of major tidal current sites across the UK (Crown Estate, 2012, p. 9)

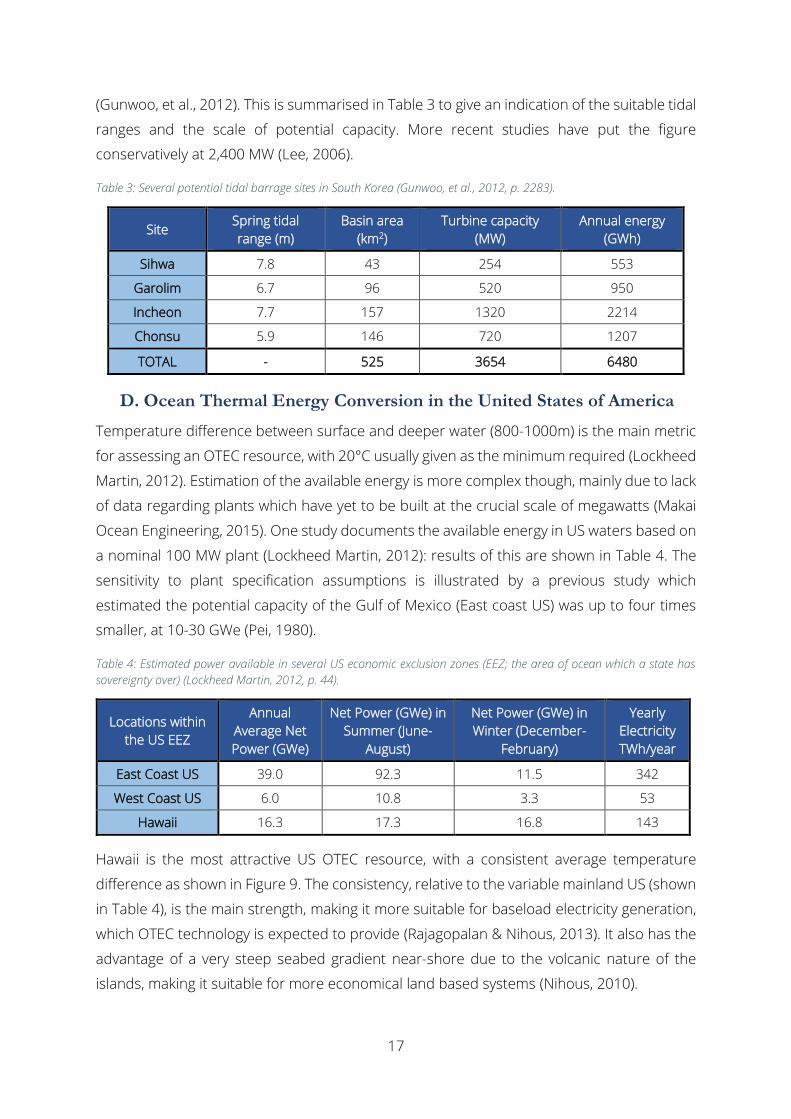

C. Tidal Range in South Korea

Similarly, tidal range energy estimates are dictated by local topography, being dependent on

the available volume of water in addition to the tidal range, making national-scale

assessments less common; instead usually taking the form of site feasibility studies (Tousif &

Taslim, 2011). The irregular coastline and high tidal range brought on by the enclosed Yellow

Sea makes the Western coast of South Korea one of the most promising locations in the

world for tidal range energy (Gunwoo, et al., 2012). As such, numerous feasibility studies have

been conducted since the 1930s: the largest of which, conducted by the Korean Ocean

Research and Development Institute in 1978, identified a total of 6,500 MW across 10 sites

17

(Gunwoo, et al., 2012). This is summarised in Table 3 to give an indication of the suitable tidal

ranges and the scale of potential capacity. More recent studies have put the figure

conservatively at 2,400 MW (Lee, 2006).

Table 3: Several potential tidal barrage sites in South Korea (Gunwoo, et al., 2012, p. 2283).

Site Spring tidal

range (m)

Basin area

(km2)

Turbine capacity

(MW)

Annual energy

(GWh)

Sihwa 7.8 43 254 553

Garolim 6.7 96 520 950

Incheon 7.7 157 1320 2214

Chonsu 5.9 146 720 1207

TOTAL - 525 3654 6480

D. Ocean Thermal Energy Conversion in the United States of America

Temperature difference between surface and deeper water (800-1000m) is the main metric

for assessing an OTEC resource, with 20°C usually given as the minimum required (Lockheed

Martin, 2012). Estimation of the available energy is more complex though, mainly due to lack

of data regarding plants which have yet to be built at the crucial scale of megawatts (Makai

Ocean Engineering, 2015). One study documents the available energy in US waters based on

a nominal 100 MW plant (Lockheed Martin, 2012): results of this are shown in Table 4. The

sensitivity to plant specification assumptions is illustrated by a previous study which

estimated the potential capacity of the Gulf of Mexico (East coast US) was up to four times

smaller, at 10-30 GWe (Pei, 1980).

Table 4: Estimated power available in several US economic exclusion zones (EEZ; the area of ocean which a state has

sovereignty over) (Lockheed Martin, 2012, p. 44).

Locations within

the US EEZ

Annual

Average Net

Power (GWe)

Net Power (GWe) in

Summer (June-

August)

Net Power (GWe) in

Winter (December-

February)

Yearly

Electricity

TWh/year

East Coast US 39.0 92.3 11.5 342

West Coast US 6.0 10.8 3.3 53

Hawaii 16.3 17.3 16.8 143

Hawaii is the most attractive US OTEC resource, with a consistent average temperature

difference as shown in Figure 9. The consistency, relative to the variable mainland US (shown

in Table 4), is the main strength, making it more suitable for baseload electricity generation,

which OTEC technology is expected to provide (Rajagopalan & Nihous, 2013). It also has the

advantage of a very steep seabed gradient near-shore due to the volcanic nature of the

islands, making it suitable for more economical land based systems (Nihous, 2010).

18

Figure 9: Average annual temperature difference between 20m and 1000m depths around Hawaii between July 2007

and June 2009 (Nihous, 2010, p. 4).

4.1.2. Resource in Panama

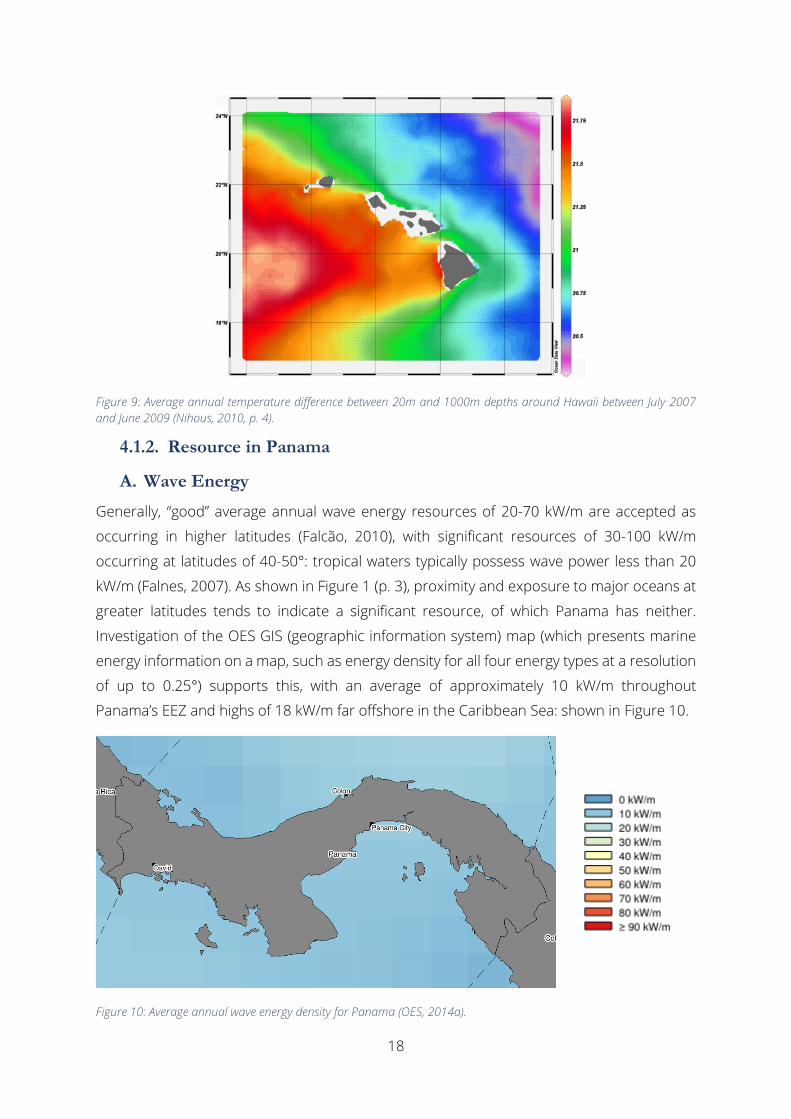

A. Wave Energy

Generally, “good” average annual wave energy resources of 20-70 kW/m are accepted as

occurring in higher latitudes (Falcão, 2010), with significant resources of 30-100 kW/m

occurring at latitudes of 40-50°: tropical waters typically possess wave power less than 20

kW/m (Falnes, 2007). As shown in Figure 1 (p. 3), proximity and exposure to major oceans at

greater latitudes tends to indicate a significant resource, of which Panama has neither.

Investigation of the OES GIS (geographic information system) map (which presents marine

energy information on a map, such as energy density for all four energy types at a resolution

of up to 0.25°) supports this, with an average of approximately 10 kW/m throughout

Panama’s EEZ and highs of 18 kW/m far offshore in the Caribbean Sea: shown in Figure 10.

Figure 10: Average annual wave energy density for Panama (OES, 2014a).

19

Data was also obtained from Stephen Barstow (co-author of the paper which produced

Figure 1; p. 3) of Fugro OCEANOR, a company specialising in environmental monitoring (Fugro

OCEANOR, 2012), which details half-hourly wave data over the course of 2012 for 7°N, 80°W.

This corroborates information given OES GIS map, indicating an average power output of 9.0

kW/m and a P90% of just 3.5 kW/m. As such, relative to the annual averages of 20-120 kW/m

and the P90% of at least 10 kW/m found in Chile, the available wave resource in Panama is

unlikely to warrant attention.

B. Tidal Current

A trial version of the UK Hydrographic Office Total Tide program was obtained from Pisys

Marine, an Aberdeenshire based distributor of marine geographic information systems (Pisys

Marine, 2015). This program contains information on tidal current measurements at selected

ports and over 3,000 points worldwide (UK Hydrographic Office, 2014): there were however

no information points present on either the Caribbean or Pacific coasts of Panama, despite

being one of the busiest shipping routes in the world (American Association of Port

Authorities, 2014). Even though there is a notable tide on the Pacific coast, lack of tidal

current data for the entrance to the Panama Canal at Balboa suggest a lack of any significant

tidal current, especially at the velocities greater than 2.5 m/s which are deemed significant

enough to warrant electricity generation (Lewis, et al., 2015). On the Caribbean coast, tidal

ranges (discussed in detail in the subsequent paragraphs) are minimal, averaging

approximately 0.5m (UK Hydrographic Office, 2014), making it unlikely that there are any tidal

currents at all.

C. Tidal Range

Typically tidal barrage systems are deemed to require a head of at least 5 m to be

economically feasible (Kempener & Neumann, 2014a). However, other tidal barrage systems,

namely tidal lagoons, are generally deemed to require less head than barrages, with 4 m

deemed the minimum criteria in two studies (Crown Estate, 2013; Kempener & Neumann,

2014a).

Observation of the OES GIS map reveals that Panama possesses a notable tidal range (Figure

11), albeit only on the Pacific coast, with a maximum of approximately 5m given in the Gulf

of Panama (OES, 2014a). This was corroborated with Total Tide, which gave averages of less

than 0.5m on the Caribbean coast and an average range of between 3-5m on the Pacific side,

depending on the port (UK Hydrographic Office, 2014). Of the 16 available ports with tidal

range data, Balboa and Rio Chepo, both located in the northernmost aspect of the Gulf of

Panama, were found to possess the greatest average tidal range of 4.7m and 4.6m

respectively: attributable to the favourable basin formed by the Gulf of Panama.

20

Figure 11: Depiction of the maximum calculated tidal ranges for Panama (OES, 2014a).

D. Ocean Thermal Energy Conversion

OTEC is the most immediately obvious potential marine energy source in Panama given its

equatorial proximity: it is widely acknowledged that the OTEC resource is confined between

the Tropics of Cancer and Capricorn (Lewis & Estefen, 2011; Lockheed Martin, 2012; Vega,

2014) . No investigation has been found published exclusively for the Panamanian resource

but information can be extrapolated from two global studies. Firstly, observation of the OES

GIS map shows that Panama has definite potential, with mean annual temperature

differences of up to 25°C, shown in Figure 12 (OES, 2014a). The white areas in this figure

show either where the water depth does not extend to 1,000 m or the temperature

difference is <20°C, which does miss out potential resource in slightly shallower waters

(Lockheed Martin, 2012).

Figure 12: Mean annual temperature difference between 20-1,000 m depth for Panama (OES, 2014a).

Water temperature difference

21

A second, more comprehensive, OTEC resource study carried out by Lockheed Martin

describes Panama in passing as representing an “attractive OTEC resource” (Lockheed Martin,

2012, p. 36). This study includes shallower water resources due to cold water temperature

taken from a depth which maximises annual power by balancing increased pump power

requirements with the increased efficiency from deeper, colder water (see Section 4.2.1 for

description of the technology), as opposed to the OES GIS map which simply assumes the

temperature difference between 20m and 1000m water depths. The findings of this study

are also presented as a GIS Map in the form of the Marine Hydro-Kinetic (MHK) Atlas (US

Department of Energy, 2013): the temperature difference for this is shown in Figure 13. Of

note is the discrepancy in terms of minimum distance to shore on either coasts compared

to the OES Map in Figure 12; due to the inclusion of the shallower water resource.

Figure 13: Mean annual temperature difference for surface water and a depth chosen to maximise power output (US

Department of Energy, 2013).

In addition to a slightly greater temperature difference, the Caribbean coast of Panama has

the advantage of lower seasonal variability between the summer and winter months as

(Figure 14). As OTEC is most commonly assumed to function as baseload plants (Lockheed

Martin, 2012; Vega, 2014), the Caribbean coast would likely be better suited. Furthermore,

the resource on the Caribbean coast is generally closer to shore than on the Pacific as shown

in Figure 15, significantly as the cost of a 10 km underwater power cable is estimated at 10%

of total capital costs for a nominal 50 MW plant (Vega, 2010).

22

Figure 14: Depiction of the seasonal variation in power (given in MW): summer (June-July-August) on the left and winter

(December-January-February) on the right (US Department of Energy, 2013).

Figure 15: Bathymetry around Panama, with 1000m contour highlighted in red (National Centers for Environmental

Information, 2016).

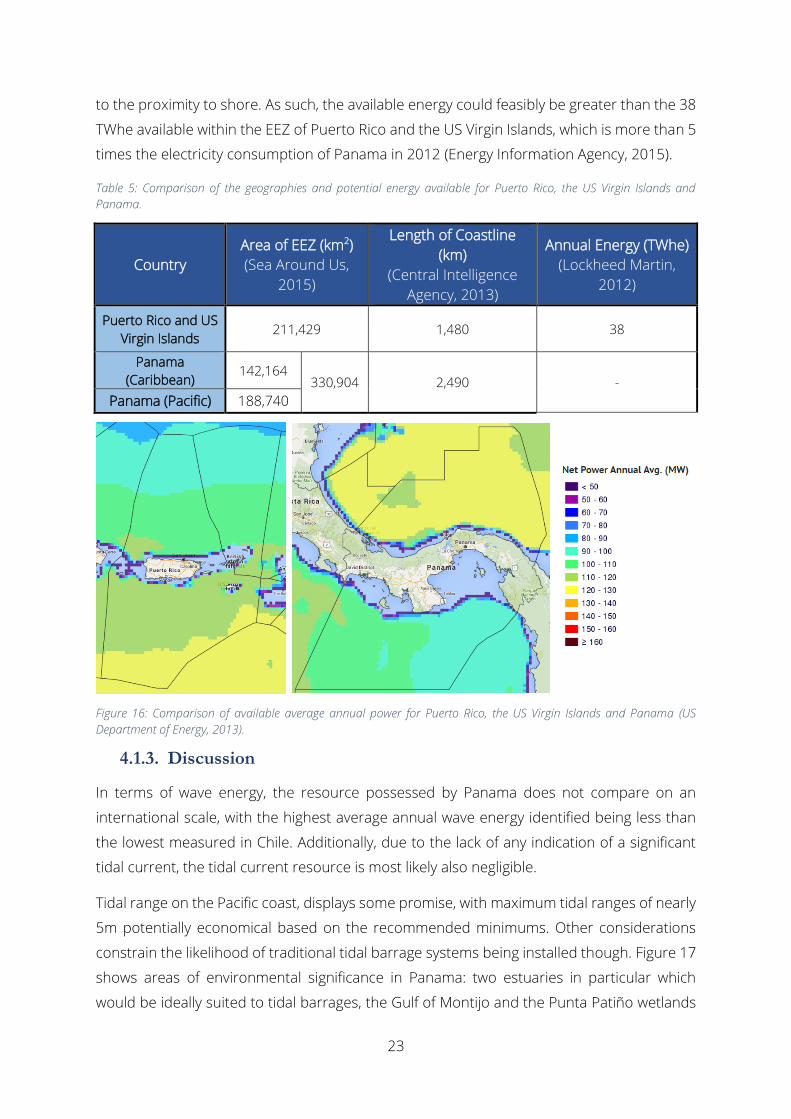

Although mentioning Panama in passing, the Lockheed Martin study does not describe the

resource in any detail: a comparison with Puerto Rico and the US Virgin Islands can however

be made to give an indication of the resource. Table 5 shows that the areas of the Economic

Exclusion Zones (EEZ) for both are the same order of magnitude, with Panama’s half again as

large. Visual comparison of the average annual available power (Figure 16 ) shows them to

be again roughly equivalent, with Panama possesing a possibly greater resource due to the

larger area of yellow (120 - 130 MW) in the Caribbean sea. Panama also possesses a longer

length of coastline, which would likely make the technically extractable resource higher due

23

to the proximity to shore. As such, the available energy could feasibly be greater than the 38

TWhe available within the EEZ of Puerto Rico and the US Virgin Islands, which is more than 5

times the electricity consumption of Panama in 2012 (Energy Information Agency, 2015).

Table 5: Comparison of the geographies and potential energy available for Puerto Rico, the US Virgin Islands and

Panama.

Country

Area of EEZ (km2)

(Sea Around Us,

2015)

Length of Coastline

(km)

(Central Intelligence

Agency, 2013)

Annual Energy (TWhe)

(Lockheed Martin,

2012)

Puerto Rico and US

Virgin Islands 211,429 1,480 38

Panama

(Caribbean) 142,164

330,904 2,490 -

Panama (Pacific) 188,740

Figure 16: Comparison of available average annual power for Puerto Rico, the US Virgin Islands and Panama (US

Department of Energy, 2013).

4.1.3. Discussion

In terms of wave energy, the resource possessed by Panama does not compare on an

international scale, with the highest average annual wave energy identified being less than

the lowest measured in Chile. Additionally, due to the lack of any indication of a significant

tidal current, the tidal current resource is most likely also negligible.

Tidal range on the Pacific coast, displays some promise, with maximum tidal ranges of nearly

5m potentially economical based on the recommended minimums. Other considerations

constrain the likelihood of traditional tidal barrage systems being installed though. Figure 17

shows areas of environmental significance in Panama: two estuaries in particular which

would be ideally suited to tidal barrages, the Gulf of Montijo and the Punta Patiño wetlands

24

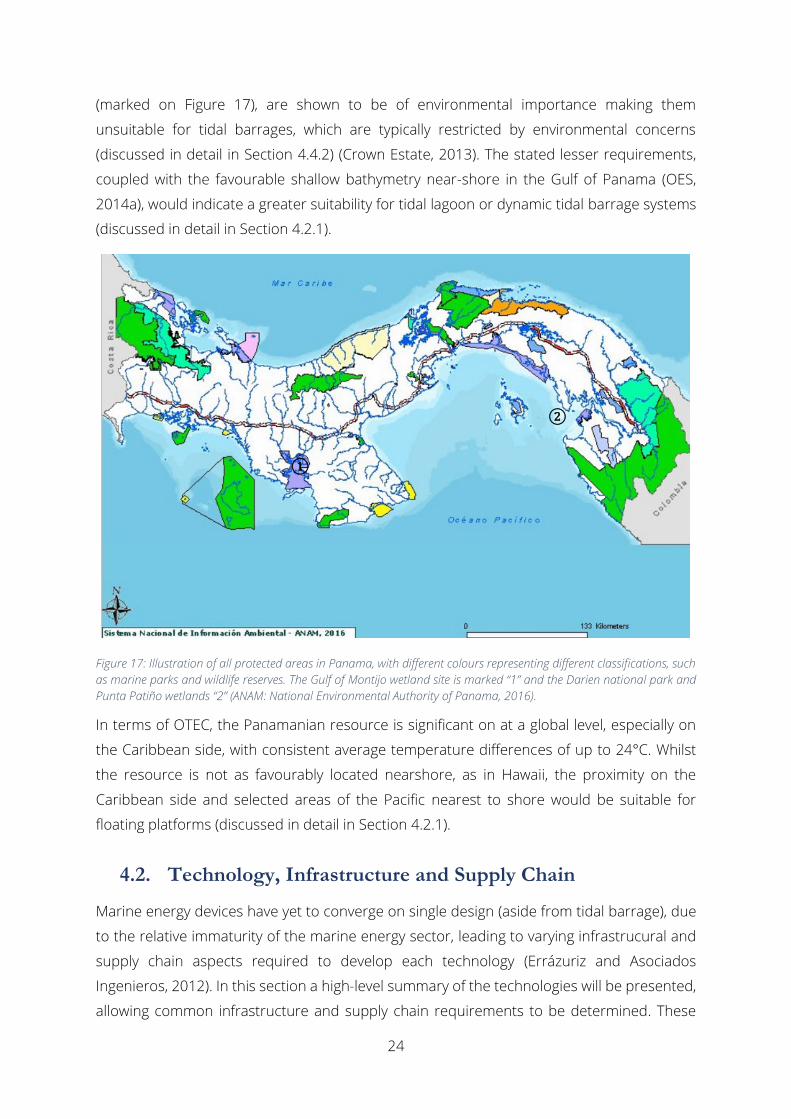

(marked on Figure 17), are shown to be of environmental importance making them

unsuitable for tidal barrages, which are typically restricted by environmental concerns

(discussed in detail in Section 4.4.2) (Crown Estate, 2013). The stated lesser requirements,

coupled with the favourable shallow bathymetry near-shore in the Gulf of Panama (OES,

2014a), would indicate a greater suitability for tidal lagoon or dynamic tidal barrage systems

(discussed in detail in Section 4.2.1).

Figure 17: Illustration of all protected areas in Panama, with different colours representing different classifications, such

as marine parks and wildlife reserves. The Gulf of Montijo wetland site is marked “1” and the Darien national park and

Punta Patiño wetlands “2” (ANAM: National Environmental Authority of Panama, 2016).

In terms of OTEC, the Panamanian resource is significant on at a global level, especially on

the Caribbean side, with consistent average temperature differences of up to 24°C. Whilst

the resource is not as favourably located nearshore, as in Hawaii, the proximity on the

Caribbean side and selected areas of the Pacific nearest to shore would be suitable for

floating platforms (discussed in detail in Section 4.2.1).

4.2. Technology, Infrastructure and Supply Chain

Marine energy devices have yet to converge on single design (aside from tidal barrage), due

to the relative immaturity of the marine energy sector, leading to varying infrastrucural and

supply chain aspects required to develop each technology (Errázuriz and Asociados

Ingenieros, 2012). In this section a high-level summary of the technologies will be presented,

allowing common infrastructure and supply chain requirements to be determined. These

①

②

25

contributing factors are used to examine the infrastructure and supply chain in Panama to

develop an understanding of and make recommendations on the current suitability for the

presented technologies.

4.2.1. Available Technology

A. Wave Energy

Of the four sectors, wave energy converters (WEC) exist in the greatest variety, with

numerous studies existing that classify and catalogue more than 50 designs (Drew, et al.,

2009; Khan & Bhuyan, 2009; Errázuriz and Asociados Ingenieros, 2012; US Department of

Energy, 2013). The lack of convergence on a single design stems from the numerous ways in

which energy can be extracted, wheteher the dvice is onshore, near-shore or offshore and

the type of power take-off system used to convert the motion of waves into electricity

(Errázuriz and Asociados Ingenieros, 2012). Examples of several major types are shown in

Figure 18, with one classification system shown in Figure 19. Development of WECs has been

focused for the most part in European nations, with test centres such as the European

Marine Energy Centre (EMEC) in Orkney facilitating this (Lewis & Estefen, 2011). Perhaps one

of the best-known WECs, the 750 kW Pelamis P2 attenuator device (as shown in Figure 18),

was tested there in 2010 (Yemm, et al., 2012).

Figure 18: Major types of WECs (Thresher, et al., 2012, pp. 9-16).

26

Figure 19: Depiction of the ways in which WECs differ (Lewis & Estefen, 2011, p. 905).

B. Tidal Current

Similarly to WECs, tidal energy converters (TEC) come in a wide range of types and again there

is a wide variety of literature classifying this (Khan, et al., 2009; EMEC, 2011; Lewis & Estefen,

2011). Major types of devices are shown in Figure 20; several other unique types also exist,

such as Archimedes screws and tidal kites (Harris, 2013). Devices also differ in other ways,

such as the mooring (devices can be floating or mounted on the seabed), power take-off

equipment (most use some form of generator but some, such as the oscillating hydrofoil, use

pressurised fluids) and so on, as shown in Figure 21 (Khan, et al., 2009).

Figure 20: Primary types of TECs (Thresher, et al., 2012, pp. 9-18).

27

Figure 21: Depiction of the major ways in which tidal current devices differ (Mofor, et al., 2014, p. 20).

Although these can be classified in as many as ten different ways, horizontal or vertical axis

designs have emerged as the most popular, with 58 out of 76 surveyed devices being either

of these types (Khan, et al., 2009). One of the most significant devices is the 1.2 MW SeaGen

device, located in Strangford Lough, Ireland, and installed in 2008 as the first grid-connected

commercial scale turbine the in the UK (Jha, 2008), consisting of twin 600 kW, 16m diameter

rotors mounted on a single pylon on the seabed (RE News, 2016).

C. Tidal Barrage

Tidal barrage technology “represents the oldest and most mature of all the ocean power

technologies” (Khan & Bhuyan, 2009, p. 9), with one of the oldest plants being the 1.7 MW

Kislaya plant in Russia, commissioned in 1968 (Bernshtein, 1972). Systems generally use bi-

directional low-head bulb turbines, with the generator enclosed within, in conjunction with a

civil works to generate sufficient head; usually across an estuary to minimise the length of

barrage required (Clark, 2007).

Figure 22: Image of the lake Sihwa tidal range plant in South Korea (Gunwoo, et al., 2012, p. 2283).

28

The largest tidal barrage in the world is the 254 MW Lake Sihwa plant in South Korea shown

in Figure 22 (Bae, et al., 2010), previously mentioned in Section 4.1.1. This and the 240 MW

La Rance plant in France represent more than 95% of total installed tidal range capacity in

the world (Mofor, et al., 2014). Proposed configurations which have not been developed

include utilising a tidal lagoon, which operates similarly to traditional barrages only enclosing

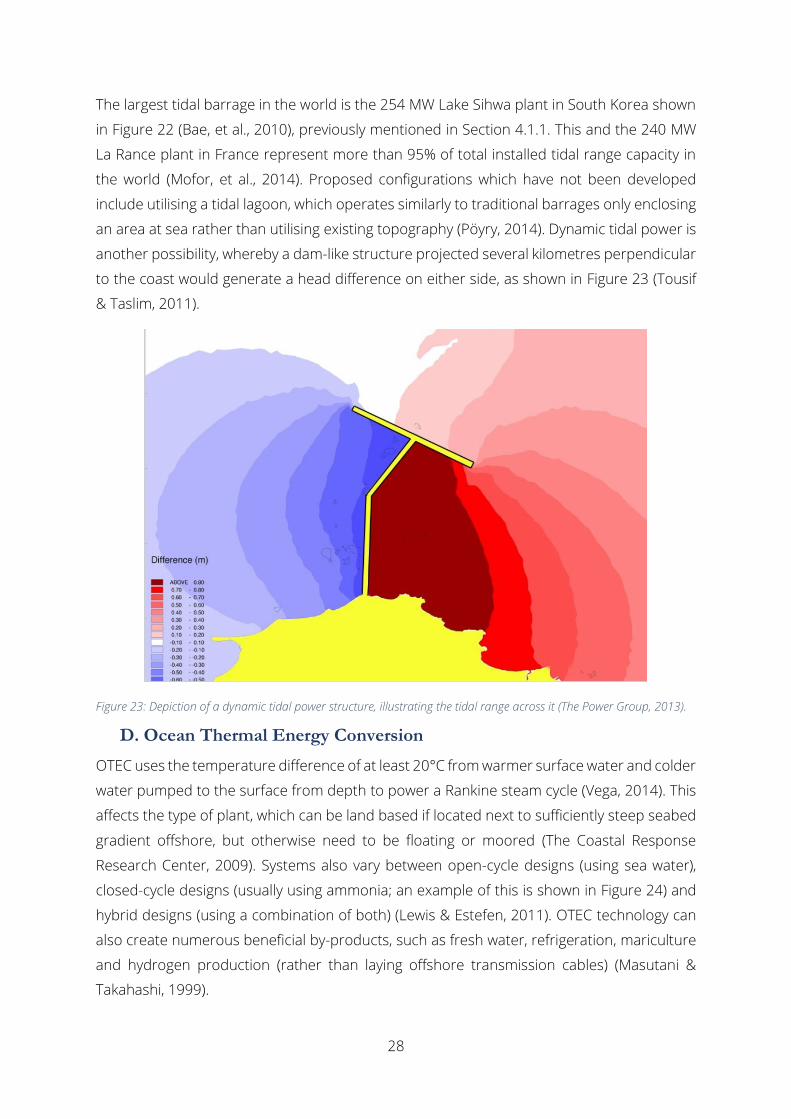

an area at sea rather than utilising existing topography (Pöyry, 2014). Dynamic tidal power is

another possibility, whereby a dam-like structure projected several kilometres perpendicular

to the coast would generate a head difference on either side, as shown in Figure 23 (Tousif

& Taslim, 2011).

Figure 23: Depiction of a dynamic tidal power structure, illustrating the tidal range across it (The Power Group, 2013).

D. Ocean Thermal Energy Conversion

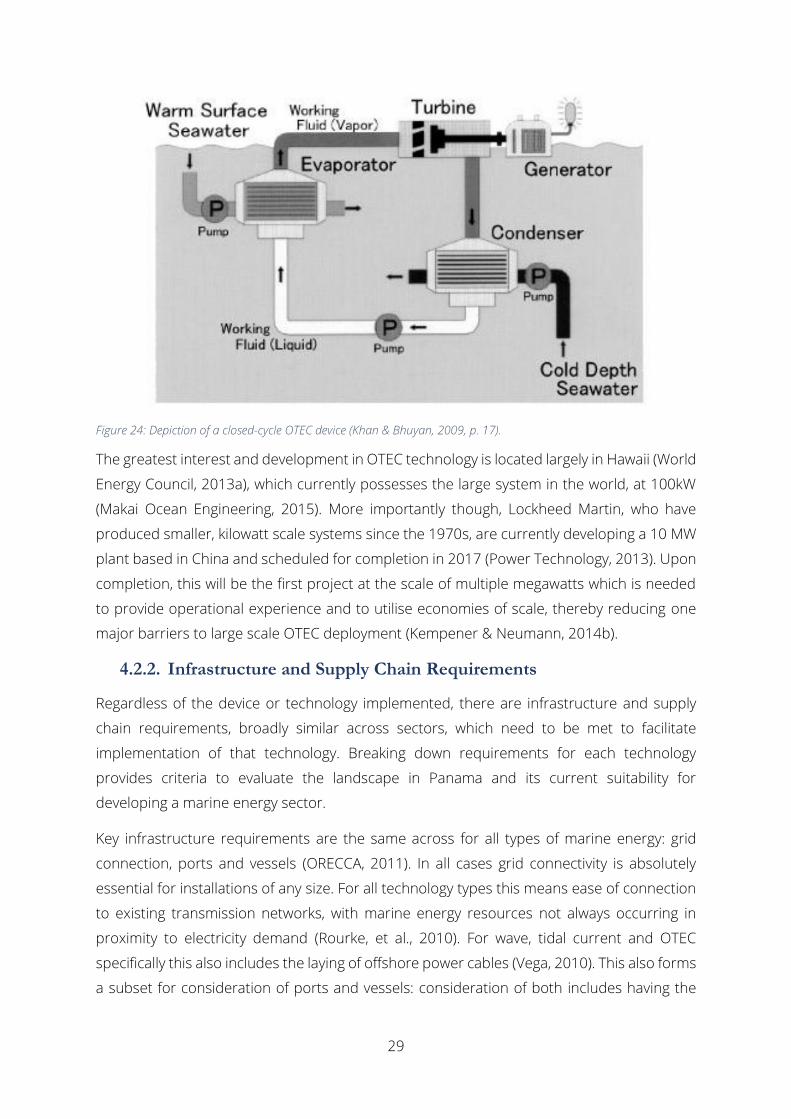

OTEC uses the temperature difference of at least 20°C from warmer surface water and colder

water pumped to the surface from depth to power a Rankine steam cycle (Vega, 2014). This

affects the type of plant, which can be land based if located next to sufficiently steep seabed

gradient offshore, but otherwise need to be floating or moored (The Coastal Response

Research Center, 2009). Systems also vary between open-cycle designs (using sea water),

closed-cycle designs (usually using ammonia; an example of this is shown in Figure 24) and

hybrid designs (using a combination of both) (Lewis & Estefen, 2011). OTEC technology can

also create numerous beneficial by-products, such as fresh water, refrigeration, mariculture

and hydrogen production (rather than laying offshore transmission cables) (Masutani &

Takahashi, 1999).

29

Figure 24: Depiction of a closed-cycle OTEC device (Khan & Bhuyan, 2009, p. 17).

The greatest interest and development in OTEC technology is located largely in Hawaii (World

Energy Council, 2013a), which currently possesses the large system in the world, at 100kW

(Makai Ocean Engineering, 2015). More importantly though, Lockheed Martin, who have

produced smaller, kilowatt scale systems since the 1970s, are currently developing a 10 MW

plant based in China and scheduled for completion in 2017 (Power Technology, 2013). Upon

completion, this will be the first project at the scale of multiple megawatts which is needed

to provide operational experience and to utilise economies of scale, thereby reducing one

major barriers to large scale OTEC deployment (Kempener & Neumann, 2014b).

4.2.2. Infrastructure and Supply Chain Requirements

Regardless of the device or technology implemented, there are infrastructure and supply

chain requirements, broadly similar across sectors, which need to be met to facilitate

implementation of that technology. Breaking down requirements for each technology

provides criteria to evaluate the landscape in Panama and its current suitability for

developing a marine energy sector.

Key infrastructure requirements are the same across for all types of marine energy: grid

connection, ports and vessels (ORECCA, 2011). In all cases grid connectivity is absolutely

essential for installations of any size. For all technology types this means ease of connection

to existing transmission networks, with marine energy resources not always occurring in

proximity to electricity demand (Rourke, et al., 2010). For wave, tidal current and OTEC

specifically this also includes the laying of offshore power cables (Vega, 2010). This also forms

a subset for consideration of ports and vessels: consideration of both includes having the

30

capacity and capability to deal with the installation, commissioning and maintenance of

devices, both on and offshore (Errázuriz and Asociados Ingenieros, 2012).

From examining classifications of supply chain requirements for each technology type,

common factors can be identified. For wave and tidal current, this includes steel, concrete,

moorings and expertise (Errázuriz and Asociados Ingenieros, 2012). Certain devices may

have specific requirements, such as hydraulics or alternative power take-off systems, but due

to the extensive variety of devices and therefore requirements, only the above are

investigated. For tidal barrage, the major sectors are materials (largely concrete and other

aggregates), turbines, vessels and skills (Department of Energy and Climate Change, 2010).

Lastly, several OTEC requirements are broadly similar to other sectors, with moorings, steel

and concrete (particularly in the construction of an offshore platform) as for wave and tidal

current (The Coastal Response Research Center, 2009). Comparing other OTEC aspects, such

as the cold water pipe, to other industries would be largely redundant due to a lack of

projects of a relevant scale, as stated in previous sections. Substantial research and

development is needed before properly understanding the complete supply chain demands

of OTEC (The Coastal Response Research Center, 2009).

Rather than exhaustively examining each supply chain requirement individually, only the

aspects shared by all technology types will be examined in detail: namely steel, concrete and

general expertise. Other requirements, such as turbines, steam cycle equipment and the

cold water pipe will be briefly discussed separately. Specific details of quantitative

requirements for each supply chain aspect are scarce, due to the relative immaturity of the

sector (ORECCA, 2011), so the following paragraphs will briefly outline each: detailed analysis

will be carried out subsequently with respect to Panama.

Concrete and Aggregates: Important for all sectors, in especially high volumes for

constructing embankments for tidal range (Department of Energy and Climate Change,

2010) as well as for moorings and the actual structure of the device for the other sectors

(Court, 2008; The Coastal Response Research Center, 2009).

Steel: For wave, tidal current and OTEC this includes for the supports, anchors or

platforms of devices and in the case of wave and tidal current, the devices themselves can

be fabricated from steel (Court, 2008). Less crucial for tidal barrage, where the structure

consists mainly of civil works (Clark, 2007).

General Expertise: As the most general category, it includes personnel to assess, make

decisions, implement and manage projects in all aspects (Errázuriz and Asociados

Ingenieros, 2012).

31

Other Supply Chain Requirements: Two main types of turbines are also required: for tidal

range these are low head bulb turbines (Department of Energy and Climate Change, 2010)

and for tidal current horizontal axis devices, the most common as discussed, the device is

made up largely of turbine and nacelle assemblies (Court, 2008). OTEC also requires other

aspects unique to this type, such as the offshore platform and steam cycle equipment,

including pumps, turbines and heat exchangers (The Coastal Response Research Center,

2009).

4.2.3. Infrastructure and Supply Chain in Panama

Having outlined the general infrastructure and supply chain requirements relevant to each

sector, this section will assess the existing landscape in Panama for suitability of marine

energy deployment or development. Despite the difficulty in assessing maritime capacity

particularly, due to the myriad of often conflicting aspects, especially for a relative immature

sector like marine energy (Wells & McConnell, 2011), this will help to determine what steps,

if any, would need to be taken to best foster marine energy locally.

A. Infrastructure

Ports

In 2013, the Panamanian ports of Balboa and Colón (the Pacific and Caribbean entrances to

the canal respectively) were the second and third busiest ports in Central and South America

in terms of twenty-foot equivalent units (a volumetric term used to assess shipping capacity);

equivalent to 57% of overall Central American volume in the same year (American Association

of Port Authorities, 2014). However, outwith these and excluding Cristobal and Manzanillo

International Terminal, which are both immediately adjacent to Colón, the next largest port

in the country, Almirante, in the Western Bocas Del Toro province, experienced slightly less

than 0.6% the percentage of container volume traffic in 2013 relative to Balboa (American

Association of Port Authorities, 2014). Applying the conditions that any port constructing or

installing marine energy devices (in this case specifically wave or tidal current devices)

requires at least 100m of quay, a minimum 6m of water depth and a 200 tonne capacity or

greater crane (Wells & McConnell, 2011), the only suitable ports are those located at the

Caribbean and Pacific entrances to the canal (Sea Rates, 2010). As such, outwith of the two

hubs at either end of the Panama Canal, there is a lack of port infrastructure suitable for

marine energy. This is not necessarily completely inimical though: analysis of port

requirements for offshore wind categorises them as suitable for manufacturing, construction

or operations and maintenance, with the latter having lesser requirements (Bard &

Thalemann, 2011). Although ports other than those around the canal might be unsuitable

for deploying devices, they could still be sufficiently developed to service existing devices.

32

Developing the capacity of ports to meet the requirements identified above for marine

energy would also be beneficial to Panama’s economy in the long term, as determined in

Ireland, with synergies benefiting other sectors (Wells & McConnell, 2011). The National

Marine Authority of Panama’s [La Autoridad Marítima de Panamá] (AMP) Strategic Marine

Plan [La Estrategia Marítima Nacional] already includes commitment to development of

Panama’s ports: although the focus is on those close to the Panama Canal, as the major

economic hubs, it does state commitment to improving and expanding other existing ports,

as well as constructing new ones (AMP, 2008). This commitment to expansion is also

reiterated in Law 56 of 2008, which governs ports and marine facilities (National Assembly of

Panama, 2008). Although this would largely focus on shipping and logistics capacity, this

capacity has been stated to be analogous to marine energy (ORECCA, 2011) and so would

still be beneficial.

Vessels

In 2014, Panama possessed the largest merchant navy in the world, with 214 million gross

register tonnage (GRT: equivalent to 100 cubic feet) for vessels over 100 GRT, representing

20% of the global total (Department for Transport, 2015). However this gives a false

impression: the majority are not based in Panama, but taking advantage of “open registries”

to avoid local maritime regulations whilst having no other ties with the country (BBC News,

2014).

The country does possess a developing auxiliary maritime services industry, which includes

repair and servicing of vessels and offshore platforms. Analysis of the sector in Panama

determined it was still relatively immature: beginning significant development only in 2000

with the transfer of ownership of the canal to the Panamanian government and with less

than a quarter of ships currently transiting the canal utilising local auxiliary services (Ibañez,

2014). Despite this, strong synergies between this sector and marine energy (Bard &

Thalemann, 2011) would indicate suitability for adaption to deploying and servicing marine

energy devices.

Fishing is also a large contributor to the Panamanian economy, as the second largest export

after bananas (Food and Agriculture Organization of the United Nations, 2007). The most

recent UN Food and Agriculture Organization “Fishery and Aquaculture Profile”, whilst now

likely outdated, identified 260 vessels 15-22m long with tonnages of up to 150 GRT, as well

as 666 “industrial” vessels with a capacity greater than 10 GRT (Food and Agriculture

Organization of the United Nations, 2007). The report also highlights a general decline in the

fishing industry at the time of writing: similarly to the situation in Scotland, which has

prompted interaction with the industry to determine the likelihood of fishing vessels

diversifying into servicing the offshore renewable energy industry (Sea Energy, 2014).

33

Anecdotally, in Ireland, fourteen fishing boats have already been contracted to supply

offshore wind and tidal projects (News Letter, 2014). As such, Panama’s fishing fleet could

also be an opportunity in terms of being repurposed to meet the supply chain needs of a

marine energy industry.

Grid Connectivity

In terms of offshore grid connection for energy generation, research failed to identify any

notable examples in Panama. As an illustration, in the entire Americas, only 30 MW of

offshore wind (the only other technology requiring similar grid connection) capacity currently

exists under construction (Alstom, 2015), relative to 5.4GW of capacity installed globally in

2012 (World Energy Council, 2013a). Supply chain capacity to connect offshore marine

energy devices is unlikely to currently exist in Panama. If an offshore wind sector were to

develop in Panama this would carry significant synergies for marine energy; otherwise

operations and maintenance vessels have been identified as well suited to adaptation for

this type of role (ORECCA, 2011).

In terms of grid infrastructure onshore, the current Panamanian transmission network is

shown in Figure 25. Existing infrastructure follows population centres and generating

capacity, with more than half the population living in the corridor between Colón and Panama

City alongside the canal (National Institute of Statistics and Census [Instituto Nacional de

Estadística y Censo], 2010). This is linked to the cluster of hydroelectric stations in the

Western, mountainous region of the country where the majority of installed hydroelectric

capacity is located (National Energy Secretariat , 2009). This connection is inadequate to meet

demand near the canal and so expansion is planned as shown, with further development

alongside existing lines under consideration (Lewis & Behar, 2015). Aside from the existing

230kV and dual 115kV lines established to Changuinola in the East and Colón at the entrance

to the canal respectively, any large scale power generation on the Caribbean side would

require significantly more investment in transmission lines to connect to the existing

infrastructure. With the grid considerably closer to the sea on the Pacific side, it makes

connecting marine energy systems more feasible and cost effective here. This

notwithstanding, the evidence of planned grid development does indicate that expansion is

feasible if the resource was deemed significant.

34

Figure 25: Current electricity grid of Panama: hydroelectric power stations are denoted as blue triangles and thermal

capacity as red squares (ETESA, 2014, p. 65).

B. Supply Chain

Concrete and Aggregate

A direct comparison to the scale of work required by a tidal barrage system exists in the

soon-to-be completed US$5.25 billion Panama Canal expansion project, with the new Pacific

access channel alone requiring the excavation of 50 million cubic meters of material (Canal

de Panamá, 2014). This makes it of the same scale in terms of estimated volume of aggregate,

if not larger, than a proposed 3.6 GW tidal lagoon project in the Severn estuary described in

a feasibility study (Department of Energy and Climate Change, 2010). The project also

requires the construction of four dams totalling 5.2 km to raise the new channel 9m above

the adjacent lake (Mejia, et al., 2011); again on a comparable scale to the 9km, 30m tall Lake

Sihwa barrage in Korea (Bae, et al., 2010).

Panama’s existing electrical generation capacity also reinforces this suitability, given the

similarities between the high volumes of civil engineering works required for both tidal

barrage and hydroelectric projects: with more than half of its current capacity being

hydroelectric and plans for nearly double this to be constructed (National Energy Secretariat ,

2009). As such, given the multi-billion dollar scale of work carried out in Panama and the

expertise developed, it is likely one of the places better suited in the world to the high

demand of civil engineering works for tidal barrage specifically. Given this, it is unlikely that

the demands of the other marine energy sectors would be problematic relatively.

35

Steel

There is no for iron ore production in Panama: in 2014 imports of iron and steel in all forms

totalled US$400 million, making it the largest net importer in Central America (UN Comtrade,

2014). In terms of apparent use (deliveries and imports minus exports) of finished steel

product, Panama ranked more modestly as third in Central America with roughly 800,000

tonnes in 2014 (World Steel Association, 2015).

There is a lack of local economic large scale steel production capacity. The new gates for the