Embed Size (px)

Citation preview

Volume 21 Issue 4 Article 2

1976

Determination of the Useful Life of a Taxpayer's Asset for Determination of the Useful Life of a Taxpayer's Asset for

Purposes of the Federal Income Tax Deduction for Depreciation Purposes of the Federal Income Tax Deduction for Depreciation

Using Statistical Methods to Analyze the Facts and Using Statistical Methods to Analyze the Facts and

Circumstances Circumstances

Robert E. Anthony

Follow this and additional works at: https://digitalcommons.law.villanova.edu/vlr

Part of the Accounting Law Commons, and the Tax Law Commons

Recommended Citation Recommended Citation Robert E. Anthony, Determination of the Useful Life of a Taxpayer's Asset for Purposes of the Federal Income Tax Deduction for Depreciation Using Statistical Methods to Analyze the Facts and Circumstances, 21 Vill. L. Rev. 674 (1976). Available at: https://digitalcommons.law.villanova.edu/vlr/vol21/iss4/2

This Comment is brought to you for free and open access by Villanova University Charles Widger School of Law Digital Repository. It has been accepted for inclusion in Villanova Law Review by an authorized editor of Villanova University Charles Widger School of Law Digital Repository.

[VOL. 21

COMMENTS

DETERMINATION OF THE USEFUL LIFE OF A TAXPAYER'SASSET FOR PURPOSES OF THE FEDERAL INCOME TAX

DEDUCTION FOR DEPRECIATION USING STATISTI-CAL METHODS TO ANALYZE THE FACTS

AND CIRCUMSTANCES

I. INTRODUCTION

Section 167 of the Internal Revenue Code of 1954 provides, interalia, that "[t]here shall be allowed as a depreciation deduction a reason-able allowance for the exhaustion, wear and tear . . .of property used in[a] trade or business, or . . . held for the production of income."' Inorder to depreciate an asset, a taxpayer must determine, among otherthings,2 the period" over which the depreciation is to be taken - the lifeof the asset.3 For tax purposes, however, the important period is notthe maximum period for which an asset could physically be used, but itsuseful life - the period for which the asset may reasonably be expectedto be used in the taxpayer's business.4 Treasury regulations to Section

1. INT. REV. CODE OF 1954, § 167(a).2. The taxpayer must also determine the adjusted basis of the asset, its salvage

value, and the depreciation method which he will use. Treas. Reg. § 1.167(a)-1 (1972).3. J. FREELAND & R. STEPHENS, FUNDAMENTALS OF FEDERAL INCOME TAXATION

690-93 (1972); M. GORDON & G. SHILLINGLAW, ACCOUNTING: A MANAGEMENTAPPROACH 321 (4th ed. 1969); C. MOORE & R. JAEDICKE, MANAGERIAL ACCOUNTING47 (2d ed. 1967) ; cf. United States v. Ludey, 274 U.S. 295, 300 (1927).

4. Section 1.167(a)-1 (b) of the Treasury Regulations provides in pertinent part:[T]he estimated useful life of an asset is not necessarily the useful life inherentin the asset but is the period over which the asset may reasonably be expectedto be useful to the taxpayer in his trade or business or in the production ofhis income.

Treas. Reg. § 1.167(a)-l(b) (1972).See Massey Motors, Inc. v. United States, 364 U.S. 92 (1960). In Massey,

the Court was concerned with the useful lives of automobiles which were held byan automobile rental company for an average of only 15 months before beingreplaced. The Court concluded that the statutory term "useful life" referred to theperiod for which an asset may reasonably be expected to be employed in the tax-payer's business, not its full economic life. Id. at 107; accord, Kerr-Cochran, Inc.,30 T.C. 69, 78-79 (1958) (cost of a warehouse built on leased land should be depre-ciated over its useful life instead of over the original 5 year term of the lease sinceit was reasonably certain that the lease would be renewed); Caflisch Lumber Co.,20 B.T.A. 1223, 1227 (1930) (the railroad right of way of a spur line onto timberlands should be depreciated over its useful life, which will end when timbering opera-tions on the land are completed); Gordon Lubricating Co., 24 CCH Tax Ct. Mem.697, 717-18 (1965) (the useful lives of depreciable assets useful only under a contractwhich the taxpayer had with Gulf Oil Corporation were not necessarily limited to theoriginal term of the contract but will depend on the probability of future renewals ofthat contract).

(674)

1

Anthony: Determination of the Useful Life of a Taxpayer's Asset for Purpos

Published by Villanova University Charles Widger School of Law Digital Repository, 1976

1975-1976] COMMENTS 675

167 set forth some of the factors that can be considered in determiningthis period:

(1) wear and tear and decay or decline from natural causes,

(2) the normal progress of the art, economic changes, inventions,and current developments within the industry and the taxpayer'strade or business,

(3) the climatic and other local conditions peculiar to the taxpayer'strade or business, and

(4) the taxpayer's policy as to repairs, renewals, and replacements. 5

In determining the useful lives of assets a taxpayer has a choice:he can use the Class Life Asset Depreciation Range System,6 or he canarrive at the useful lives of his assets on the basis of the facts and circum-stances which are applicable to his particular assets, without dependingupon published guidelines. 7 The taxpayer who chooses this latter coursewill often be faced with a determination of great complexity for whichhe will need professional assistance. Even though such assistance may inmany cases demand the expertise of attorneys and accountants who havespecialized in this area, the average practitioner may be exposed to sucha problem at some time. Unfortunately, the available literature tends totreat this area in one of two ways: either so superficially as to be of littleassistance, or in such great detail as to be beyond the practitioner's needs.

5. Treas. Reg. § 1.167(a)-l(b) (1972).6. The Asset Depreciation Range System, which applies to certain property

put in service after December 31, 1970, Treas. Reg. § 1.167(a)-l1 (1973), and theClass Life System, which applies to certain property put in service before January 1,,1971, Treas. Reg. § 1.167(a)-12 (1973), allow the taxpayer to group his assets under-various classifications for which useful lives have been established through the IRS's.experience with the industry. For general discussions of these systems, see J. LYON,DEPRECIATION: ADR SYSTEM FOR PosT-1970 PROPERTY (Tax Management Portfolio.No. 255-2nd 1973); J. LYON, DEPRECIATION: CLASS LIFE SYSTEM FOR PRE-1971PROPERTY (Tax Management Portfolio No. 295 1973); Rev. Proc. 72-10, 1972-1CuM. BULL. 721.

Even if a taxpayer is not eligible for or chooses not to use the aforementionedisystems, he can base his estimates of useful life on the published guidelines (see note 5and accompanying text supra), taking the position that these guidelines are repre-sentative of the experience of others in his industry. J. LYON, A. BARTLETT, & H.HOLMES, DEPRECIATION - BASIS, USEFUL LIFE, SALVAGE A-33 (Tax ManagementPortfolio No. 62-4th 1974) [hereinafter cited as LYON]. Section 1.167(a)-i(b) ofthe Treasury Regulations allows such a reliance on experience in the industry, statingin pertinent part:

If the taxpayer's experience is inadequate, the general experience in the in-dustry may be used until such time as the taxpayer's own experience forms anadequate basis for making the determination.

Treas. Reg. § 1.167(a)-l(b) (1972).7. Section 1.167(a)-i(b) of the Treasury Regulations provides in pertinent part:

This period [the estimated useful life of an asset] shall be determined by reference-to his [the taxpayer's] experience with similar property taking into accountpresent conditions and probable future developments.

Treas. Reg. § 1.167(a)-1(b) (1972); see LYON, supra note 6, at A-27; INTERNAL.REVENUE SERVICE, TAX INFORMATION ON DEPRECIATION 3 (Publication No. 534, 1975)..

2

Villanova Law Review, Vol. 21, Iss. 4 [1976], Art. 2

https://digitalcommons.law.villanova.edu/vlr/vol21/iss4/2

VILLANOVA LAW REVIEW

This comment will attempt to strike a middle course, providing thepractitioner with enough information so that he can appreciate the majorproblems and pitfalls inherent in the determination of an asset's usefullife, yet avoiding the legal idiosyncrasies which are of interest only to theexpert tax attorney or accountant.

II. SCOPE OF THE TAXPAYER'S BURDEN OF PROOF

In considering the various methods of computing an asset's usefullife, it is helpful to keep in mind the amount and detail of factual datanecessary to support the taxpayer's depreciation deduction. Although thetaxpayer has the burden of establishing the reasonableness of a deduction,8

the Internal Revenue Service (IRS), in an effort to eliminate contro-versies involving an insubstantial amount of tax revenue, 9 promulgatedRevenue Ruling 90.10 This ruling announced the policy that claimeddepreciation deductions would be challenged only if the examining revenueemployee concludes that there was a clear and convincing basis for achange in the deduction." Concurrently, the IRS promulgated RevenueRuling 91,12 which sets forth the factors to be considered in applying the

policy of Revenue Ruling 90.l Among the factors to be considered were

whether the rates utilized by the taxpayer were fair and reasonable, 14

whether the method used by the taxpayer had been consistently applied, 15

and whether any proposed adjustments were substantial. 18

8. Treas. Reg. § 1.167(b)-O(a) (1956).9. 4 J. MERTENS, LAW OF FEDERAL INCOME TAXATION § 23.04a (rev. ed. 1973)

[hereinafter cited as MERTENS].10. Rev. Rul. 90, 1953-1 CuM. BULL. 43.11. Id. Revenue Ruling 90 provides in pertinent part:[I]t shall be the policy of the Service not to disturb depreciation deductions, andrevenue employees shall propose adjustments in the depreciation deduction onlywhere there is a clear and convincing basis for a change.

Id. This policy has also been incorporated into the regulations to Section 167which provide that "[glenerally, depreciation deductions so claimed will be changedonly where there is a clear and convincing basis for a change." Treas. Reg. §1.167(b)-0(a) (1956).

12. Rev. Rul. 91, 1953-1 Cum. BULL. 44.13. Id. Revenue Ruling 91 provides in pertinent part:

Among the factors which should be given careful consideration in order togive full force and effect to the announced policy are the following:

(a) Whether depreciation rates used by the taxpayer are fair and reason-able under the circumstances;

(b) Whether the taxpayer has followed a consistent practice in arriving atthe amount of the depreciation deductions;

(c) Whether in considering all factors, including reasonable tolerances, anyadjustments proposed are substantial.

In the establishment of the depreciation rates for a taxpayer, careful con-sideration shall be given to facts and arguments presented by the taxpayer withrespect to obsolescence, as well as to the repair and maintenance policy of thetaxpayer.

Id.14. Id. (a).15. Id. (b).16. Id. (c).

[VOL. 21

3

Anthony: Determination of the Useful Life of a Taxpayer's Asset for Purpos

Published by Villanova University Charles Widger School of Law Digital Repository, 1976

1975-1976]

Questions arise as to what is a "clear and convincing basis for achange"'17 and how large a proposed adjustment must be before it is"substantial."' s Unfortunately, there are no clear answers to these ques-tions.1' The determinations would appear to be largely within the dis-cretion20 of the Commissioner, who can apply the policy of RevenueRuling 9021 and 9122 as broadly or as narrowly as he deems warrantedby the facts of a particular case.2 3

After the examiner has determined that a basis for a change exists,the taxpayer will be called in. If the examiner and a taxpayer cannotreach an agreement 24 and if the change proposed by the examiner is"material," a valuation engineer can be consulted.25 These engineers, whoare employees of the IRS Engineering and Valuation Branch, are expertswho render technical assistance to revenue agents in examining taxpayers'returns and preparing court cases. 26 Although the findings of the engi-neers are not conclusive, their testimony has been accorded considerableweight by the IRS and the courts,27 which hear the matter if the IRSand the taxpayer cannot reach an agreement.

In a trial, a taxpayer will also be at a disadvantage because theCommissioner's rulings are supported by a presumption of correctness,with the taxpayer bearing the burden of proving that the Commissioner'sdetermination is incorrect.28 With sufficient evidence, however, a taxpayer

17. Treas. Reg. § 1.167(b)-O(a) (1956); see note 11 and accompanying text supra.18. Rev. Rul. 91, 1953-1 Cum. BULL. 44.19. MERTENS, supra note 9, § 23.04a; Parker, How the IRS Engineering and

Valuation Branch Works; Its Policies on Depreciation, 10 J. TAx. 69 (1959).20. MERTENS, supra note 9, § 23.04a.21. See note 11 and accompanying text supra.22. See notes 12-16 and accompanying text supra.23. Parker, supra note 19, at 69-70. Compare cases cited in note 28 infra with

cases cited in note 29 infra. Revenue Procedure 57-18 stated that if the requirementsof Revenue Rulings 90 and 91 are met at any particular time, an adjustment will bemade despite the fact that a depreciation deduction was claimed in a previous returnand was accepted without change upon examination. Rev. Proc. 57-18, 1957-1 CuM.BULL. 748, 749.

24. Treas. Reg. § 1.167(d)-i (1960).25. Rev. Rul. 90, 1953-1 CuM. BULL. 43. An engineer is consulted only upon the

revenue agent's request. Parker, supra note 19, at 69. A taxpayer, however, cannothave his case reviewed by an IRS engineer unless the agent agrees. Id.

26. Parker, supra note 19, at 70.27. Englert, Subjective Tests for "Useful Life" and "Salvage Value" Cause

Difficult Problems of Proof, 16 J. TAX. 214, 216 (1962). In A.A. Gallagher Warehous-ing Corp., 24 CCH Tax Ct. Mem. 38, 45 (1965), the engineer's report was the primaryevidence before the court. The taxpayer did not question the engineer's qualifications,methods, or accuracy and the court stated that "[c]onsequently, the recommendationscontained in the report are entitled to considerable weight as the opinions of qualifiedappraisers." Id. at 45. But see notes 30-33 and accompanying text infra.

28. Welch v. Helvering, 290 U.S. 111, 115 (1933); Biggs v. Commissioner, 440F.2d 1, 4-5 (6th Cir. 1971) (taxpayer failed to meet his burden of coming forwardwith evidence to show that a determination of tax deficiencies was erroneous becausein many instances his only supporting evidence was the statement that, "[i]f I deductedit, it was for business"); Imeson v. Commissioner, 73-2 CCH TAX CT. REP. 9775(9th Cir. 1973) (although the 7-year useful life ascribed by the Commissioner to

COMMENTS

4

Villanova Law Review, Vol. 21, Iss. 4 [1976], Art. 2

https://digitalcommons.law.villanova.edu/vlr/vol21/iss4/2

678 VILLANOVA LAW REVIEW [VOL. 21

can establish the reasonableness of his depreciation deduction.29 In oneparticularly noteworthy case,30 although the Commissioner's determina-tion resulted from a study of the taxpayer's records made by an IRSvaluation engineer,8 ' the taxpayer's computation, based upon a study byits own experts,3 2 was upheld, partly because the taxpayer's method wasbased upon more intimate knowledge of the depreciated assets.3 3 Thedecision was particularly noteworthy because the testimony of IRS valua-tion engineers had carried such great weight in the past. 4

taxpayer's business vehicles was, in the court's view, longer than was readily justifiedby common experience, the court allowed that determination to stand because the tax-payer did not offer proof to establish her position) ; Pensacola Greyhound Racing, Inc.,32 CCH Tax Ct. Mem. 1064, 1070 .(1973) (taxpayer failed to introduce evidencesupporting his determination of the useful lives of his property and therefore failedto carry his burden of proof and place in doubt the Commissioner's presumption ofcorrectness); Ralph E. Schumaker, 29 CCH TAX CT. MEM. 1315, 1317 (1970), aff'd,451 F.2d 1349 (6th Cir. 1972) (taxpayer offered no evidence other than his owntestimony to substantiate the useful lives of his property and therefore did not over-come the presumption of correctness of the Commissioner's determination) ; Easterv. Commissioner, 338 F.2d 968, 969 (4th. Cir. 1964), cert. denied, 381 U.S. 912 (1965)(neither the government nor the taxpayer produced evidence to support their deter-minations and since the Commissioner's 'determination is presumptively correct andthe burden is upon the taxpayer to prove otherwise, the court indicated that it had nochoice but to affirm the Commissioner's determination).

29. Northern Natural Gas Co. v. O'Malley, 277 F.2d 128, 137 (8th Cir. 1960)(the taxpayer offered voluminous and specific evidence, expert and otherwise, con-sisting of statistical estimates of its natural gas reserves, to establish that its de-termination of the proper rate of depreciation was correct and the Commissioner'swas erroneous) ; Vegetable Farms, Inc. v. Commissioner, 191 F.2d 677 (9th Cir.1951) (the court rejected the Commissioner's determination which was based uponspeculation as unsupported and clearly erroneous in the face of taxpayer's two wit-nesses who supported the taxpayer's position); Geuder, Paeschke & Frey Co. v.Commissioner, 41 F.2d 308, 310-11 (7th Cir. 1930) (the legal presumption that theCommissioner's determination is prima facie correct was overcome by the testimonyof officers of taxpayer who had been closely associated with the business for 30years); Cumberland Glass Mfg. Co. v. United States, 44 F.2d 455, 461-62 (Ct. Cl.1930) (the taxpayer's depreciation deduction was sustained because it was deter-mined by company officials who had many years of experience and an accurate andtechnical knowledge of the property - its actual use and operation in the plant, age,cost, and probable useful life, and the current cost of repairs and replacements);Laura Massaglia, 33 T.C. 379, 388 (1959), aff'd, 286 F.2d 258 (10th Cir. 1961) (theCommissioner offered no testimony as to the remaining useful lives of the taxpayer'sproperty, but attempted to rest solely upon the presumption of correctness and wasoverturned by the court which accepted the testimony of the taxpayer's expert wit-nesses) ; Herbert Shainberg, 33 T.C. 241, 254 (1959) (taxpayer's position was upheldwhen the Commissioner offered no justification for a change and taxpayer presentedseveral witnesses who were very familiar with the business).

30. Portland Gen. Elec. Co. v. United States, 189 F. Supp. 290 (D. Ore. 1960),aff'd, 310 F.2d 877 (9th Cir. 1962).

31. 189 F. Supp. at 294-95.32. Id. at 294 & n.6.33. Id. at 300.34. Englert, supra note 27, at 216. See also note 27, supra. In A.A. Gallagner

Warehousing Corp., 24 CCH Tax Ct. Mem. 38, 45 (1965), the IRS engineer'smethods and accuracy were not questioned, whereas in Portland, the taxpayer con-tended that its experts were more qualified due to their experience. Portland Gen.Elec. Co. v. United States, 189 F. Supp. 290, 294 n.6 (1960), aff'd, 310 F.2d 877,(9th Cir. 1962).

5

Anthony: Determination of the Useful Life of a Taxpayer's Asset for Purpos

Published by Villanova University Charles Widger School of Law Digital Repository, 1976

1975-1976]

Although the amount and detail of evidence necessary for a taxpayerto overcome the Commissioner's presumption of correctness will varyfrom case to case, one available standard for measuring the evidencenecessary to support a verdict for the taxpayer is the "reasonable approxi-mation rule." To meet the burden under this standard, a taxpayer mustshow that his determination is a reasonable approximation of the amountthat fairly may be included in the accounts of any year.a5

III. METHODS OF DETERMINING USEFUL LIVEs

Depending upon the nature of the information available to him, ataxpayer can utilize one of several methods in determining the usefullives of his assets on the basis of the particular facts and circumstancesapplicable to them. The taxpayer can use a statistical method to studyhis past experience with similar assets, or, if the taxpayer is aware ofparticular facts which distinguish an asset from other similar assets, suchunique circumstances will control that asset's useful life. 86 For example,the normal physical life of a railroad spur line would be irrelevant if it wasbuilt to serve a timbering operation which will be exhausted at a particulartime, after which the line would be useless. In such a case, althoughthe spur line would normally last longer, the unique knowledge that theeconomic usefulness of the line is limited by the completion of the timber-ing operation will limit the useful life of the spur line to that period.37

If the taxpayer chooses a statistical method to determine the usefullife of an asset, two of the available approaches are the turnover method8"and the analysis of survivor curves.8 9 While these approaches are basedupon past experience, 40 the taxpayer can adjust his results if, in his in-formed judgment, present conditions suggest that future experience withthat particular asset will produce a useful life different from that arrivedat by analysis of the past experience.4 1

35. The Supreme Court proposed such a rule for the substantiation of a tax-payer's reasonable allowance to cover obsolescence of tangible property. Burnet v.United States, 282 U.S. 648, 654-55 (1931). Subsequently, the Ninth Circuit indicatedthat such a standard would be appropriate to measure the taxpayer's burden ofproof in establishing the useful life of property for the purpose of a depreciationdeduction. Western Terminal Co. v. United States,'412 F.2d 826, 827 (9th Cir. 1969).

36. LYON, supra note 6, at A-33.37. Caflisch Lumber Co., 20 B.T.A. 1223 (1930).38. See notes 42-58 and accompanying text infra.39. For a discussion of the definition and computation of a survivor curve, see

notes 59-83 and accompanying text infra.40. LY N, supra note 6, at A-34.41. Revenue Ruling 91 provides in pertinent part:

In the establishment of the depreciation rates for a taxpayer, careful consider-ation shall be given to facts and arguments presented by the taxpayer with respectto obsolescence, as well as to the repair and maintenance policy of the taxpayer.

Rev. Rul. 91, 1953-1 Cum. BULL. 44 (1953). Revenue Ruling 90 states also that"[tihe determination of the amount of the deduction is largely a matter about whichthere may be reasonable differences of informed judgment." Rev. Rul. 90, 1953-1 CuM.BULL. 43 (1953). See also A. MARSTON, R. WINFREY, & J. HEMPSTEAD, ENGINEERING

VALUATION AND DEPRECIATION 139 (2d ed. 1953) [hereinafter cited as MARSTON].

COMMENTS

6

Villanova Law Review, Vol. 21, Iss. 4 [1976], Art. 2

https://digitalcommons.law.villanova.edu/vlr/vol21/iss4/2

VILLANOVA LAW REVIEW

A. Turnover Method

The turnover method42 is a statistical approach based upon the theorythat an asset's useful life can be measured by the time it takes the unitsof the asset in service 43 to "turn-over" - the period which passes beforethe units of that asset that were being used by the taxpayer in his businessat a particular time are completely retired from service.44 In order tocompute the useful life of a particular asset by use of the turnover method,the taxpayer must have available a record of both the number of assets inservice at the end of each year and the number of assets retired on a yearlybasis.45 The age of the assets at retirement is not needed, however. 46

Three procedures may be employed to determine the turnover period.The simple example of a company which keeps a constant supply of90,000 units of a particular asset in service at all times will be used toillustrate these procedures. Each year 10,000 units are retired and 10,000new units are put into service to replace them. To use the first procedure,a record of the cumulative additions and retirements47 must be compiled(Table 1, Columns 4 and 6) and plotted on a graph (Chart 1, Line a -cumulative additions and Line b - cumulative retirements). The turnoverperiod is the horizontal distance between the two lines48 - in this case9 years. To use the second procedure, the yearly balance of the unitsof the asset in service must be compiled (Table 1, Column 2) and plotted(Chart 2, Line a) and the number of retirements accumulated backward 49

42. MARSTON, supra note 41, at 167-69. See also COMMITTEE ON ENGINEERING,DEPRECIATION AND VALUATION OF THE NATIONAL ASSOCIATION OF REGULATORYUTILITY COMMISSIONS, PUBLIC UTILITY DEPRECIATION PRACTICES 138-42 (1968)(published by the National Association of Regulatory Utility Commissions, 3327ICC Building, P.O. Box 684, Washington, D.C. 20044) [hereinafter cited as NARUC].

43. An asset is first put "in service" when it is formally entered onto the com-pany's financial records, usually when it is purchased and first used in the manufac-turing process. The asset is removed from service when the accounting departmentretires the asset on the books, usually when it has become obsolete, destroyed byaccident, or worn out. The service life of the asset is the time span between thosetwo points in time. MARSTON, supra note 41, at 139-42.

44. NARUC, supra note 42, at 138.45. Id.; see MARSTON, supra note 41, at 167. In order to use this method, the

taxpayer would have to have information available for a period of time at leastequal to the turnover period. For example, if the taxpayer had 100 units of an assetin service in 1965 and he retired 10 units per year, he would have to have recordsfrom 1965 to 1975 in order to determine that the turnover period equals 10 years. Id.

46. Id.; see NARUC, supra note 42, at 138.47. The cumulative additions and retirements are the accumulated totals of the

yearly additions (Table 1, Column 3) and yearly retirements (Table 1, Column 5).48. MARSTON, supra note 41, at 167. Usually this distance is measured between

the most recent dates plotted on the graph so as to take into account, as much aspossible, any changes which might influence the rate of retirement. Id.

49. This total is the number of retirements which have occurred in the past,accumulated on a yearly basis beginning with the most recent year and accumulatingbackward into past years, year by year (Table 1, Column 7). Records need only tobe available in the past for a length of time equal to the turnover period - in thisexample 9 years, January 1, 1967 to January 1, 1976.

[VOL. 21

7

Anthony: Determination of the Useful Life of a Taxpayer's Asset for Purpos

Published by Villanova University Charles Widger School of Law Digital Repository, 1976

1975-1976]

must be compiled (Table 1, Column 7) and plotted (Chart 2, Line b).The turnover period is the number of years - the distance on the hori-zontal axis - between the point from which the retirements are accumu-lated (January 1, 1976) and the point at which the two lines intersect50

(Chart 2, Point c - January 1, 1967) - in this case 9 years. To usethe third procedure, the yearly balance of the asset must again be compiledand plotted (Chart 3, Line a) and the number of additions accumulatedbackward 5' must be compiled (Table 1, Column 8) and plotted (Chart 3,Line b). The turnover period is the number of years between the pointfrom which the additions were accumulated (January 1, 1976) and thepoint at which the lines intersected 52 (Chart 3, Point c - January 1,1976) - in this case, again, 9 years.

Unfortunately, the turnover period calculated by the use of these pro-cedures will equal the average useful life of the asset only if the balanceof that asset in use is stable and not increasing or decreasing.55 A simpleexample will illustrate the problem. Assume that the taxpayer's businessis expanding and he wishes to increase the number of units of the asset inservice. Therefore, he retires 5,000 units of the asset each year and adds10,000 units. Using the three procedures, the following results are ob-tained: Procedure I - cumulative additions (Table 2, Column 2; Chart 1,Line a'), cumulative retirements (Table 2, Column 3; Chart 1, Line b').As even a visual inspection will indicate, there is no constant horizontaldistance between the lines; the useful life has been distorted by the con-stant additions of assets in excess of retirement. Procedure II - yearlybalance (Table 2, Column 1; Chart 2, Line a'), backward accumulatedretirements (Table 2, Column 5; Chart 2, Line bl) - the turnover periodis 22 years (January 1, 1976 to January 1, 1954). Procedure III -

yearly balance (Table 2, Column 1; Chart 3, Line a'), backwardaccumulated additions (Table 2, Column 4; Chart 3, Line b') - theturnover period is approximately 14.7 years (January 1, 1976 to Point d).

Because of this inequality in the results, the turnover period must beadjusted to compensate for the growth. 4 This adjustment and a morecomplicated adjustment for the "mortality dispersion" - the manner inwhich the actual useful lives of the individual assets vary from the averagelife of the group of assets - must be made in order to approximate theaverage useful life. To make these adjustments an appropriate survivor

50. MASTON, supra note 41, at 167.51. See note 49 supra. This total is calculated in the same manner as retirements

accumulated backward.52. MARSTON, supra note 41, at 168.53. Id. Such a stable balance in the asset account of a going concern would be

very rare. Id.54. Id. To make this adjustment a constant rate of growth must be assumed, an

assumption which will adversely affect the estimation of the average useful life ofthe asset if the rate of growth varies. Because the growth rate is rarely stable, theadjusted turnover period must be regarded as merely an approximation of the averageservice life. Id.

COMMENTS

8

Villanova Law Review, Vol. 21, Iss. 4 [1976], Art. 2

https://digitalcommons.law.villanova.edu/vlr/vol21/iss4/2

VILLANOVA LAW REVIEW

curve55 must be assumed for the property. 6 This assumption is based uponstudies concerning similar assets and upon informed judgment.5 7 Oncean appropriate survivor curve has been arrived at, the adjustment canbe made upon the basis of graphs constructed by statistical experts whichplot the proper adjustments to be made for the standard survivor curvesat various rates of growth. 8 Needless to say, such adjustments are beyondthe competence of all but experienced valuation engineers and statisticalexperts.

B. Survivor Curves

A second statistical approach to determining the useful life of anasset is to generate a survivor curve for the particular asset59 and thento analyze that curve to determine the asset's useful life.60 A survivorcurve is a curve which indicates the percentage of some particular type ofasset which is still in service from the time when that asset is first putin service until the time when the last unit is retired (maximum age).61Table 3 and Chart 4 provide examples of survivor curves. 62 There areseveral methods of generating survivor curves, three of which will beexamined in this section.

1. The Retirement Rate MethodThe Retirement Rate Method 63 requires the use of extensive informa-

tion concerning the asset of which the useful life is being determined.6 4

To generate a retirement rate survivor curve, the number of units putin service each year and the number and age of units retired each year

55. For a discussion of the definition and computation of a survivor curve, seenotes 59-83 and accompanying text infra.

56. NARUC, supra note 42, at 142.57. Id.58. Id. at 139-42; MARSTON, supra note 41, at 153-54.59. See notes 63-75 and accompanying text infra.60. MARSTON, supra note 41, at 142-63. For a discussion of the analysis of sur-

vivor curves, see notes 76-78 and accompanying text infra. This second statisticalapproach, which is also called the "actuarial method," is preferred to the turnovermethod. Id. at 169; see note 54 supra. The turnover method, however, may be theonly method possible when the ages of retired assets cannot be determined. Id.Although the turnover method is still used in some instances (the IRS valuationengineer used it unsuccessfully in Portland Gen. Elec. v. United States, 189 F. Supp.290, 295 & n. 7 (1960); see notes 30-33 and accompanying text supra), its use hasdeclined as the use of more accurate and sophisticated methods gains precedence.NARUC, supra note 42, at 138.

61. MARSTON, supra note 41, at 147. So that various survivor curves can becompared, the horizontal axis is often expressed in terms of percentage of averageservice life instead of in terms of years. Id. at 147, 149-53.

62. Id. at 146-47. The format of the tables and charts used as examples in theremainder of this article are based on the format of the tables and figures in MARSTON,supra note 41, at 146, 147, 150, 151, 156, 157, 158, 160, 162.

63. Id. at 154-55. Of the three actuarial methods (Retirement Rate, OriginalGroup, and Individual Unit) the Retirement Rate Method is considered to be the bestby far because it is based upon the analysis of the data on all property in serviceduring recent years. Id. at 154.

64. Id. at 154, 167.

[VOL. 21

9

Anthony: Determination of the Useful Life of a Taxpayer's Asset for Purpos

Published by Villanova University Charles Widger School of Law Digital Repository, 1976

1975-19761

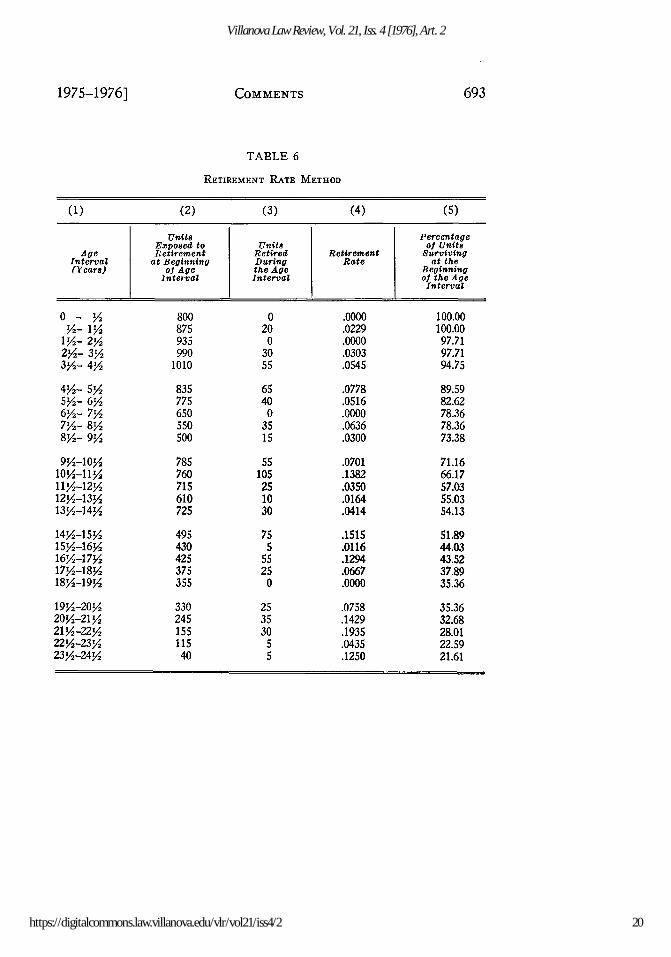

(Tables 4 & 5) are correlated over a limited time span6" to determine therate at which the asset is retired at various ages. The following steps66 areinvolved in making this correlation (based on the sample data in Tables4 & 5):

1. For some recent time span (in this case January 1, 1970 to January1, 1975) determine how many of the units originally put in service arestill functioning as of the first day of January of each year (Table 4) andconsequently, how many of those units were retired during each of theyears 1970 through 1974 (Table 5).

2. Determine the number of units of various ages which were "ex-posed to retirement" during the time span under consideration, i.e., howmany 1-year-old units, 2-year-old units, etc., were in service and thereforeremained to be retired. This is done by adding the numbers in Table 4in a "stair-step manner." For example, to calculate the number of 10% -11% (average age 11) year-old units that were exposed to retirement,add 10 (in 1974, units installed in 1963 were an average of 11 years old),125 (in 1973, units installed in 1962 were an average of 11 years old),125 (1961 to 1972), 400 (1960 to 1971), and 100 (1959 to 1970) whichequals 760 (Table 6, Column 2, age interval 10% - 11%). Repeat thiscalculation for each age interval (Table 6, Column 2).

3. Determine the number of units of various ages which were re-tired during the time span under consideration, i.e., how many 1-year-oldunits were retired, how many 2-year-old units were retired, and so forth.This is done by adding the numbers in Table 5 in a stair-step manner.For example, to calculate the number of units which were retired whenthey were between 10% and 11Y years old (average age 11 years), add0 (none of the units which were put in service in 1959 were retired in1970 when they were 11 years old) + 50 + 50 + 5 + 0 = 105 (Table 6,Column 3, age interval 10% - 11%). Repeat this calculation for each ageinterval (Table 6 Column 3).

4. For each age interval divide the units retired (Table 6, Column 3)by the units exposed to retirement (Table 6, Column 2) to determinewhat percentage of the units exposed to retirement were actually retired(Table 6, Column 4).

5. Using the rate of retirement figures calculated in step 4, deter-mine what percentage of the original number of units put in service werestill surviving at the beginning of each age interval. This is done bymultiplying the retirement rate (Table 6, Column 4) by the percentageof units surviving at the beginning of each age interval (Table 6, Column5) and subtracting the result from the percentage of the total units which

65. Id. at 154. The time span which is chosen should be a recent period of normalbusiness activity which will give reliable data indicative of present policies andstandards. The period should be long enough, however, so that retirement rates willaverage out over the normal ups and downs of the business cycle. Id.

66. Id. at 154-55.

COMMENTS

10

Villanova Law Review, Vol. 21, Iss. 4 [1976], Art. 2

https://digitalcommons.law.villanova.edu/vlr/vol21/iss4/2

VILLANOVA LAW REVIEW

were surviving at the beginning of the interval (Table 6, Column 5). Theresult is the percentage of units surviving at the beginning of the nextinterval. The first few calculations would be done as follows:

Interval: 0 -Retirement rate: .0000% surviving at the beginning of the age interval: 100.00100.00 - (100.00 x .0000) = 100.00

Interval: % - 1%Retirement rate: .02297 surviving at the beginning of the age interval: 100.00100.00 - (100.00 x .0229) = 97.71

Interval: 1% - 2%Retirement rate: .00007 surviving at the beginning of the age interval: 97.7197.71 - (97.71 x .0000) = 97.71

Interval: 2% - 3 %Retirement rate: .0303% surviving at the beginning of the age interval: 97.7197.71 - (97.71 x .0303) = 94.75

6. Plot the survivor curve using the age intervals (Table 6, Column1) on the horizontal axis and the percentage of units surviving at thebeginning of the age intervals (Table 6, Column 5) on the vertical axis.

2. The Original Group Method

The Original Group Method67 of generating a survivor curve requiresthat records of the retirements of the units of an asset put in service duringeach year be available68 - that is, the records of the retirements of theunits put in service in 1950 (the 1950 original group), the records ofthe 1951 group, the 1952 group, and so forth. For example (Table 7),a record was kept of the number of units of an asset surviving each yearout of a particular group of 1000 units put in service in 1950. The per-centage surviving (Table 7, Column 4) is calculated by determining whatpercentage of the original 1000 units are in service as of January 1 ofeach subsequent year, until they were all retired in 1975.69 The survivorcurve is plotted by using the Average Age (Table 7, Column 2) as thehorizontal axis and the Percentage Surviving (Table 7, Column 4) as thevertical axis. This method is useful in comparing the trends in the retire-ments of groups of assets which were put in service at different times.70

67. Id. at 155, 159-61.68. Id. at 159, 167.69. Id. at 159.70. Id. Differences in performance between groups may be due to changed de-

signs, improved maintenance, conditions of usage, etc. Id.

[VOL. 21684

11

Anthony: Determination of the Useful Life of a Taxpayer's Asset for Purpos

Published by Villanova University Charles Widger School of Law Digital Repository, 1976

1975-1976]

3. The Individual Unit Method

In order to use the Individual Unit Method,71 records must be avail-able showing the ages of the assets that are retired (Table 8, Column 1)and how many units were retired at various ages7 2 (Table 8, Column 3).To calculate the percentage of the total retirements which occurred duringeach age interval (Table 8, Column 4), the number of units which wereretired in each interval (Table 8, Column 3) is divided by the totalnumber of units retired during the entire period for which records werekept (Total, Table 8, Column 3). From these figures the percentagesurviving at the beginning of each interval (Table 8, Column 5) can becalculated by subtracting from the percentage surviving at the beginningof each interval the percentage of total retirements that occurred duringthat particular age interval (Table 8, Column 4) which equals the per-centage surviving at the beginning of the next interval. Example (fromTable 8) :

% - 1Y 100.00- 2.68

1% - 2% 97.32- 0.00

2%-3% 97.32- 4.03

3%-4% 93.29

As in the other methods,7 3 the survivor curve can be plotted fromthe percentage surviving at the beginning of each age interval (Table 8,Column 5) .

The Individual Unit Method is not a recommended method althoughit may be the only method which can be used if the available data islimited.74 If the assets have been in service for a relatively short periodof time, this method can be misleading because the average useful life so

71. Id. at 161-64.72. Id. at 161, 167.73. See text accompanying note 61 supra.74. The retirement rate method is based upon an analysis of all the property in

service during a period of years and in order to use it the taxpayer must have avail-able extensive records showing the number of units put in service each year and thenumber and ages of units retired each year. MARSTON, supra note 41, at 154, 167;see text accompanying notes 64 & 65 supra. The original group method uses only thedata concerning the retirements of a group of units put in service in one particularyear. MARSTON, supra note 41, at 154; see text accompanying note 68 supra. Theindividual unit method uses only data of units which have been retired. MARSTON,supra note 41, at 154; see text accompanying note 72 supra. In order to use the turn-over methods, ages of retired units are not necessary and only annual additions andretirements need be available. MARSTON, supra note 41, at 167; see text accompanyingnotes 45 & 46 supra.

COMMENTS

12

Villanova Law Review, Vol. 21, Iss. 4 [1976], Art. 2

https://digitalcommons.law.villanova.edu/vlr/vol21/iss4/2

VILLANOVA LAW REVIEW

calculated will equal the average life of the assets retired. Thus, thecalculation ignores the possibility that there may be a substantial numberof units which have long service lives and, thus, have not entered into thecalculations. 75 An example will serve to illustrate the problem. If unitsof an asset were first put in service in 1960 and the Individual Unit Methodwas used to calculate data from which to generate a survivor curve in1975, the results in Table 9, Column 5 would be obtained. However, ifa substantial number of units had lives longer than 15 years, theywould not have been retired as of 1975 and could only be included in thedata at some point in the future. Thus, if a calculation were to be madein 1985, the results in Column 7 would be obtained and a longer averageuseful life would be calculated from the survivor curve

4. Computation of the Average Useful Life

Having generated a survivor curve for an asset by one of the afore-mentioned methods, the taxpayer can determine the average useful life ofthat asset by measuring the area enclosed between the curve and the twoaxes. 76 This area is measured in units of "%-years. ' '77 Thus, the averageuseful life of the remaining units in service can be determined by dividingthe area enclosed under that portion of the curve to the right of the pointindicating the age of the asset by the percentage of units in service atthat time.78 For example, during the first age interval (0 - %), 100%of the units are in service (Table 3, Column 2), and the area remainingunder the curve to the right of the point representing that age intervalis the entire area between the curve and the two axes. This area equals1,249.98%-years (Table 3, Column 3). Applying the aforementionedrule, the useful life would be determined by dividing 1,249.98%-years by100% with a result of 12.4998 years or approximately 12% years. Thisis the average useful life of all the units when first put in service. Foranother example, 14% years later (age interval 14% - 15%), 27.68%of the units were still in service (Table 3, Column 2) and the area underthe curve to the right of 14% equals 94.57%-years (Table 3, Column 3).94.57%-years divided by 27.68% equals 3.42 years, which is the averageuseful life of the units remaining in service.

The application of one of the three methods of generating a survivorcurve usually results in a rough curve79 or a stub curve.80 Since the

75. MARSTON, supra note 41, at 163.76. MARSTON, supra note 41, at 148, 164. This area would be determined mathe-

matically using calculus.77. In plotting a survivor curve (Chart 4), time is measured on the horizontal

axis and the percentage of property surviving in service is measured on the vertical axis.78. MARSTON, supra note 41, at 148-49.79. For examples of rough curves obtained by applying tne tnree methods, see id.

at 161 (Fig. 7.5). Irregular curves can result because the time period used was tooshort or the number of units involved was too small. Id. at 164.

80. Id. at 164. A stub curve - one that does not reach the horizontal axis - isa likely result when using the Retirement Rate and Original Group Methods sincethe data generated often does not extend to the point where the percentage of units

[VOL. 21

13

Anthony: Determination of the Useful Life of a Taxpayer's Asset for Purpos

Published by Villanova University Charles Widger School of Law Digital Repository, 1976

1975-1976]

average useful life of the asset cannot be determined without a complete,smooth survivor curve,"' it is necessary to complete and smooth the roughcurve using sophisticated statistical methods, 8 2 a detailed analysis of whichis beyond the scope of this article.

Although the statistical methods have their disadvantages in that thesophisticated techniques involved demand the skill of an expert, theiradoption appears to indicate a trend as more industries develop experienceand compile standard families of survivor curves corresponding to thepeculiar characteristics of their assets.88

IV. CONCLUSION

It is obvious that the depreciation deduction is a vitally important one,particularly in businesses with a large investment in depreciable capitalassets. As was observed in one commentary:

Surely . . . there are few areas in income taxation where carefulattention to detail can be so well rewarded. The shorter the usefullives that can be successfully defended before the Revenue Service,the larger the depreciation allowances and the greater the financialbenefit from savings or deferment of taxes. At the same time, careful-ness or indifference in claiming or continuing useful lives that cannotbe defended is one of the quickest ways to build up substantial taxdeficiencies to be paid with interest.8 4

Robert E. Anthony

surviving at the beginning of the last interval correlated equals zero (Table 6,Column 5). Id.

81. See note 76 and accompanying text supra. The most probable average usefullife is indicated by a smooth survivor curve because such a curve is likely to resultfrom reliable, abundant data. MARSTON, supra note 41, at 164. Also, events whichwould tend to cause sharp changes in the curve are unlikely to occur frequently. Id.

82. There are several methods of extending and smoothing survivor curves, threeof which will be discussed. If a stub curve is relatively smooth and extends belowapproximately 40% surviving, it can often be extended by eye by an experiencedexpert. MARSTON, supra note 31, at 164. Another way of smoothing curves is bymatching the curve to standard curves generated by statisticians. Id. at 165-67. Inmany large industries, standard curves which are known to be representatives ofthe shapes of curves which are likely to be encountered within the industry have beencompiled. Id. at 167. A group of curves known as the "Iowa type curves" - a groupof 18 curves which have been found to approximate many survivor curves - havealso been developed and can be used in matching. Id. at 153-54; LYON, supra note 6,at A-34.

The last method of smoothing and extending survivor curves is known asstatistical curve fitting and involves complicated mathematical procedures. MARSTON,supra note 41, at 165.

83. MARSTON, supra note 41, at 153, 165. One example of the recognition by theIRS of the trend toward statistical methods was the issuance of Revenue Ruling67-378 which prescribed the standard mortality dispersion table - a statistical com-pilation of average useful lives of assets - to be used as the basis for determiningthe amount of retirements in mass accounts subject to investment credit recapture.Rev. Rul. 67-378, 1967-2 CUM. BULL. 45-46 (1967).

84. LYON, supra note 6, at A-33.

COMMENTS

14

Villanova Law Review, Vol. 21, Iss. 4 [1976], Art. 2

https://digitalcommons.law.villanova.edu/vlr/vol21/iss4/2

VILLANOVA LAW REVIEW

TABLE 1

(1) (2) (3) (4) (5) (6) (7) (8)

10 G

Tu .a *'

ta is a taA

1950 90,0001951 90,000 10,0001952 90,000 10,0001953 90,000 10,0001954 90,000 10,0001955 90,000 10,0001956 90,000 10,0001957 90,000 10,0001958 90,000 10,0001959 90,000 10,0001960 90,000 10,0001961 90,000 10,0001962 90,000 10,0001963 90,000 10,0001964 90,000 10,0001965 90,000 10,0001966 90,000 10,0001967 90,000 10,0001968 90,000 10,0001969 90,000 10,0001970 90,000 10,0001971 90,000 10,0001972 90,000 10,0001973 90,000 10,0001974 90,000 10,0001975 90,000 10,0001976 90,000 10,000

10,000 10,00020,000 10,00030,000 10,00040,000 10,00050,000 10,00060,000 10,00070,000 10,00080,000 10,00090,000 10,000

100,000 10,000110,000 10,000120,000 10,000130,000 10,000140,000 10,000150,000 10,000160,000 10,000170,000 10,000180,000 10,000190,000 10,000200,000 10,000210,000 10,000220,000 10,000230,000 10,000240,000 10,000250,000 10,000260,000 10,000

Company founded Jan. 1, 1950 with a beginning balance of 90,000 units of the asset.

[VOL. 21

10,00020,00030,00040,00050,00060,00070,00080,00090,000

100,000110,000120,000130,000140,000150,000160,000170,000180,000190,000200,000210,000220,000230,000240,000250,000260,000

250,000240,000230,000220,000210,000200,000190,000180,000170,000160,000150,000140,000130,000120,000110,000100,000

90,00080,00070,00060,00050,00040,00030,00020,00010,000

0

250,000240,000230,000220,000210,000200,000190,000180,000170,000160,000150,000140,000130,000120,000110,000100,00090,00080,00070,00060,00050,00040,00030,00020,00010,000

0

15

Anthony: Determination of the Useful Life of a Taxpayer's Asset for Purpos

Published by Villanova University Charles Widger School of Law Digital Repository, 1976

1975-1976] COMMENTS

TABLE 2

(1) (2) (3) (4) (5)

Jan. 1 of Units of Additions RetirementsFollowing Asset in Cumulative Cumulative Accumulated Accumulated

Year Service Additions Retirements from Present from PresentBackward Backward

90,00095,000

100,000105,000110,000115,000120,000125,000130,000135,000140,000145,000150,000155,000160,000165,000170,000175,000180,000185,000190,000195,000200,000205,000210,000215,000220,000

10,00020,00030,00040,00050,00060,00070,00080,00090,000

100,000110,000120,000130,000140,000150,000160,000170,000180,000190,000200,000210,000220,000230,000240,000250,000260,000

5,00010,00015,00020,00025,00030,00035,00040,00045,00050,00055,00060,00065,00070,00075,00080,00085,00090,00095,000

100,000105,000110,000115,000120,000125,000130,000

250,000240,000230,000220,000210,000200,000190,000180,000170,000160,000150,000140,000130,000120,000110,000100,000

90,00080,00070,00060,00050,00040,00030,00020,00010,000

0

125,000120,000115,000110,000105,000100,000

95,00090,00085,00080,00075,00070,00065,00060,00055,00050,00045,00040,00035,00030,00025,00020,00015,00010,000

5,0000

16

Villanova Law Review, Vol. 21, Iss. 4 [1976], Art. 2

https://digitalcommons.law.villanova.edu/vlr/vol21/iss4/2

VILLANOVA LAW REVIEW

TABLE 3

Col. (1) (2) (3) (4) (5)

Remaining ExpectancyPercent Area Under Expectancy of Survivors

Surviving at Survivor of Survivors at BeginningAge Beginning of Curve to at Beginning of Age

Intervals Age Intervals Right of of Age Interval(%) Beginning of Interval (Percentage

Age Interval (17ears) of Average(%-Years) Life)

100.00100.00100.0099.9299.59

98.8397.4595.1391.2184.94

76.1165.4354.2343.8134.92

27.6821.8517.0713.10

9.78

7.044.853.161.931.08

0.540.230.080.020.00

1,249.981,199.981,099.981,000.02

900.26

801.05702.91606.62513.45425.38

344.85274.08214.25165.23125.87

94.5769.8050.3435.2623.82

15.419.465.462.911.41

0.600.210.060.010.00

690 [VOL. 21

0 - %Y/2- I1V

1 - 2%2V2- 3Y3 - 4V

4V - 5Y5Y- 6V6Y- 77Y- 8%8Y- 9Y

9%2-10%10 -1111 -12%12Y2-1313 -14

14 -1515 -1616 -1717 -1818 -19

19 -2020 -21Y21 -2222 -2323Y-241

24 -2525V-26Y26 -2727 -2828 -29$

12.5012.0011.0010.019.04

8.117.216.385.635.01

4.534.193.953.773.60

3.423.192.952.692.44

2.191.951.731.511.31

1.110.910.750.500.00

100.0096.0088.0080.0772.32

64.8457.7051.0145.0340.06

36.2533.5131.6130.1728.84

27.3325.5623.5921.5319.48

17.5115.6113.8212.0810.44

8.897.486.004.000.00

17

Anthony: Determination of the Useful Life of a Taxpayer's Asset for Purpos

Published by Villanova University Charles Widger School of Law Digital Repository, 1976

1975-1976] COMMENTS 691

TABLE 4

Units Units Remaining in Service at the Beginning of YearYear Installed

DuringYear 1970 1971 1972 1973 1974 1975

1950 100 50 50 45 45 40 351951 135 130 130 130 100 70 701952 25 20 20 20 10 10 101953 75 60 55 55 55 55 551954 200 100 100 75 75 75 601955 150 150 100 100 75 75 751956 300 200 175 150 150 150 1251957 25 20 20 20 20 15 151958 70 70 65 65 60 60 601959 175 100 100 100 90 90 901960 500 450 I 400 350 350 350 3501961 150 125 125 I 125 75 75 751962 200 150 135 130 1 125 120 1001963 15 15 15 15 10 I 10 101964 90 90 70 70 70 70 701965 175 165 160 160 160 155 1501966 200 175 160 155 155 155 1401967 225 200 200 175 150 150 1501968 275 275 275 260 250 220 2001969 100 100 100 100 90 85 851970 300 --- 300 290 290 285 2851971 125 - 125 125 125 1251972 150 -- - - 150 145 1451973 200 ---- 200 1951974 25 ... ...- 251975 ----...

3985 2645 2755 2715 2680 2785 2690

18

Villanova Law Review, Vol. 21, Iss. 4 [1976], Art. 2

https://digitalcommons.law.villanova.edu/vlr/vol21/iss4/2

692 VILLANOVA LAW REVIEW [VOL. 21

TABLE 5

Units Units Retired During The Calendar YearYear Installed

During 1970 1971 1972 1973 1974Year

1950 100 - 5 -- 5 51951 135 - 30 30 ----

1952 25 _ 10 --

1953 75 5 - - - -1954 200 - 25 -- 151955 150 50 - 25 - -

1956 300 25 25 - - 251957 25 -- -___ 5 ----1958 70 5 5 ...1959 175 - - 10 ..

1960 500 50 [ 50 --

1961 150 - - [ 50 ...-.1962 200 15 5 5 j 5 201963 15 -... 5 ..1964 90 20 .. --

1965 175 5 . 5 51966 200 15 5 ..... 151967 225 25 25 ...1968 275 15 10 30 201969 100 - 10 5 --1970 300 10 _5 __1971 125 .....- -..

1972 150 --.- 5 ----1973 200 ----..... 51974 25 --- ----

1975 ..........

3985 190 165 185 95 110

19

Anthony: Determination of the Useful Life of a Taxpayer's Asset for Purpos

Published by Villanova University Charles Widger School of Law Digital Repository, 1976

1975-1976]

TABLE 6

RETIREMENT RATE METHOD

(1) (2) (3) (4) (5)

Units PercentageEaposed to Units of Units

Age Ketirement Retired Retirement SurvivingInterval at Beginning During Rate at the(Years) of Age the Age Beginning

lnterval Interval of the AgeInterval

I/2- 2Y

2Y2- 3V3Y- 4Y

4Y2- 5/5Y- 6%6%2- 7Y7Y- 8%8Y- 9

9 -1010 -1111 -12

12%-13Y13 -14

14 -1515 -1616 -1717 -1818 -19

19 -2020V-21 Y21 r-22Y222Y-23/23 -24

.0000

.0229

.0000

.0303

.0545

.0778

.0516.0000.0636.0300

.0701.1382.0350.0164.0414

.1515

.0116

.1294

.0667

.0000

.0758

.1429

.1935

.0435

.1250

100.00100.00

97.7197.7194.75

89.5982.6278.3678.3673.38

71.1666.1757.0355.0354.13

51.8944.0343.5237.8935.36

35.3632.6828.0122.5921.61

COMMENTS

20

Villanova Law Review, Vol. 21, Iss. 4 [1976], Art. 2

https://digitalcommons.law.villanova.edu/vlr/vol21/iss4/2

VILLANOVA LAW REVIEW

TABLE 7

ORIGINAL GROUP METHOD

[VOL. 21

(1) (2) (3) (4)

Average Units of PercentageAge of Original of Original

Survivors 1000 GroupYear (as of 1/1 Surviving Surviving

of Year in (as of 1/1 (as of 1/1ol 1) of Year in of Ycar in

0 o. 1) Ooi. 1)

1950 0 1000 100.001951 V 1000 100.001953 1 , 995 99.501954 22 990 99.001955 3Y2 960 96.00

1956 4Y2 920 92.001957 5 2 875 87.501958 62 840 84.001959 7 2 800 80.001960 8Y, 750 75.00

1961 92 705 70.501962 102 640 64.001963 11% 585 58.501964 122 500 50.001965 13%, 450 45.00

1966 14Y, 405 40.501967 15y/ 380 38.001968 16V2 360 36.001969 17%2 310 31.001970 18y2 290 29.00

1971 192 275 27.501972 202 200 20.001973 21V 135 13.501974 22Y 60 6.001975 23Y, 0 0.00

21

Anthony: Determination of the Useful Life of a Taxpayer's Asset for Purpos

Published by Villanova University Charles Widger School of Law Digital Repository, 1976

1975-1976] COMMENTS

TABLE 8

INDIVIDUAL UNIT METHOD

(1) (2) (3) (4) (5)

Age Interval Units Percentage PercentageAverage Age During Retired of Total Surviving

of Units which the at the Retirements at the

Retired Retirements Average Age Retired Beginning(Years) Occurred and During During the of Age

(Years) the Interval Age Interval Interval(Units) (%) (%)

0- Y

1%- 2%/2Y/- 3%3Y2- 4%

4Y2- 5/Y5Y2- 6Y26Y2- 7%7%- 828Y2- 92

9/2-10/2

10-11%11-12%12Y2-13Y/13Y2-14Y2

14V2-15/215Y2-16Y216Y2-17/217Y2-18V2182-192

19Y2-20/2202-21/,21Y2-22222Y2-23Y223Y2-24Y2

100.00100.0097.3297.3293.29

85.9177.1971.8271.8267.12

65.1157.7343.6440.2838.94

34.9124.8424.1716.7913.43

13.4310.07

5.371.340.67

0.00

7.3814.09

3.361.344.03

10.070.677.383.360.00

3.364.704.030.670.67

22

Villanova Law Review, Vol. 21, Iss. 4 [1976], Art. 2

https://digitalcommons.law.villanova.edu/vlr/vol21/iss4/2

VILLANOVA LAW REVIEW

TABLE 9

(1) (2) (3) (4) (5) (6) (7)

Units % of Total % of TotalRetired Retirements Retirements

Average Age During (up to 1975) % (up to 1985) %Age Interval Age Retired Surviving Retired Surviving

Interval During Age During AgeInterval Interval

0.000.000.431.302.613.042.835.43

10.8714.7824.3515.22

7.833.914.133.27

100.00100.00100.0099.5798.2795.6692.6289.7984.3673.4958.7134.3619.1411.317.403.27

460 units retired as of 1975

560 units retired as of 1985

696 [VOL. 21

0.000.000.361.072.142.502.324.468.93

12.1420.0012.50

6.433.213.392.68

0 - Y2/2 - IV2

1 V- 2V22Y- 3%23,- 4%4V- 5Y5%- 6%V6Y%- 7%7%- 8%8%- 9%V9V-10%

10%-11%11V-12%12%2-13Y13%,-14Y14%2-15Y

15V-16%16V-17%17V-18%181-19Y19%-20%203-21%21Y%-22%22Y-23123Y-24%24%-25%

100.00100.00100.00

99.6498.5796.4393.9391.6187.1578.2266.0846.0833.5827.1523.9420.55

17.8715.3713.0510.37

5.733.231.80.91.36.18

23

Anthony: Determination of the Useful Life of a Taxpayer's Asset for Purpos

Published by Villanova University Charles Widger School of Law Digital Repository, 1976

1975-1976]

CHART ONE

31-

26- --- ,gz _

200

110-

16o0 , ,

10 1 /" "

Il/c

120 -I

h-4

30-

20-10111051 I / L '43 6 1 'bSW 17 '69 t l 7 '7 j-

COMMENTS

24

Villanova Law Review, Vol. 21, Iss. 4 [1976], Art. 2

https://digitalcommons.law.villanova.edu/vlr/vol21/iss4/2

VILLANOVA LAW REVIEW

CqIART Two

----- ----- - - - -

420-

40d - "-

00-, r -

Cw . I ...I A

S I i I I I'

10 ;, ,f v &zI/;"yY 7 M 53T-S

[VOL. 21

25

Anthony: Determination of the Useful Life of a Taxpayer's Asset for Purpos

Published by Villanova University Charles Widger School of Law Digital Repository, 1976

1975-1976]

CHART THREE

565e1

1•114-4 X

70------

3D0

I --

Vn3 7Y 731 i/ 7 of a WI P1 W IV J7 bI $i vi . r xl

I , 3 q1 S I 'f 7 U 13 Y3I~ Lf lb /1 10 If~~ V X. 23 IV 2f

COMMENTS

26

Villanova Law Review, Vol. 21, Iss. 4 [1976], Art. 2

https://digitalcommons.law.villanova.edu/vlr/vol21/iss4/2

VILLANOVA LAW REVIEW

CHART FOUR

I5 !-

- --- - - - - -

30-

25 ---

iS--

/ - - - - . -.

0 I 2 3 I f 0 P. a 1 I I' I$ is 17 M I f 1 0 1 ;3 2' , i. f

IV-b lo h lo kp 4o0. io eb 40 o 4o im iii.vo P1 if,. io ; ;1o

[VOL. 21

CI".(

27

Anthony: Determination of the Useful Life of a Taxpayer's Asset for Purpos

Published by Villanova University Charles Widger School of Law Digital Repository, 1976