Embed Size (px)

Citation preview

Modern Economy, 2018, 9, 907-923 http://www.scirp.org/journal/me

ISSN Online: 2152-7261 ISSN Print: 2152-7245

DOI: 10.4236/me.2018.95058 May 11, 2018 907 Modern Economy

Determinants of Foreign Direct Investment in the Nigerian Telecommunication Sector

O. Arawomo*, J. F. Apanisile

Department of Economics, Obafemi Awolowo University, Ile-Ife, Nigeria

Abstract This paper investigated the key determinants of FDI in the Nigerian tele-communication sector. The study made use of data from 1986 to 2014. An-nual data on infrastructure, government expenditure, trade openness and market size, were sourced from the World Development Indicators (WDI) of the World Bank. FDI flow into telecommunication sector, foreign exchange rate, interest rate and inflation, were sourced from Central Bank of Nigeria Statistical Bulletin. Data were analyzed using graphs, t-test and Autoregressive Distributed Lag (ARDL). The results showed that the key determinants of FDI in the sector are market size and trade openness (t = 5.75 to 9.05; p < 0.05) on positive side, as well as Inflation and real interest rate (t = −0.05 to −4.03; p < 0.05) on negative side. The study therefore concludes that the key determi-nants of FDI flow into the Nigerian telecommunication sector are market size, trade openness, government expenditure, inflation and interest rate.

Keywords Determinants of FDI, Expenditure, Trade

1. Introduction

Foreign Direct Investment (FDI) has emerged as the most important source of external resource flows to developing countries over the years and has become an integral part in the formation of capital in these countries. Therefore, at-tempts have been made by Nigerian authorities to try to attract FDI via various reforms. The reforms included the deregulation of the economy, the new indus-trial policy of 1989, the establishment of the Nigeria Investment Promotion Commission (NIPC) in early 1990s, and the signing of Bilateral Investment Treaties (BITs) in the late 1990s. The benefits of foreign direct investment in-clude promoting economic growth, technology transfer and job-creation in the

How to cite this paper: Arawomo, O. and Apanisile, J.F. (2018) Determinants of Foreign Direct Investment in the Nigerian Telecommunication Sector. Modern Econ-omy, 9, 907-923. https://doi.org/10.4236/me.2018.95058 Received: March 23, 2018 Accepted: May 8, 2018 Published: May 11, 2018 Copyright © 2018 by authors and Scientific Research Publishing Inc. This work is licensed under the Creative Commons Attribution International License (CC BY 4.0). http://creativecommons.org/licenses/by/4.0/

Open Access

O. Arawomo, J. F. Apanisile

DOI: 10.4236/me.2018.95058 908 Modern Economy

local economies. Also, FDI can serve to integrate domestic markets into the global economic system far more effectively than could have been achieved only by traditional trade flows.

FDI flow into Nigerian economy has increased over the years from $6 billion in 2009 to $7.03 billion in 2013. The percentage share of telecommunication sector to total FDI increased from 0.9% in 1986 to 2.3% in 1990. Among 1999 to 2006, its share decreased to 1.7% and it increased to 24% between 2007 and 2013 (CBN, 2014). In order to attract more FDI, there is need to improve on the fac-tors that can influence the inflow of FDI into the host country. Many studies have been conducted on the factors responsible for inward FDI into a host country. Pfeffermann and Madarassy [1] identified the size of the domestic market, inflation, exchange rate volatility, interest rate and macroeconomic poli-cies as critical variables that determines foreign direct investment in developing countries. According to Iyela [2], corruption increases the cost of doing business and as such foreign investors would prefer to invest in countries with lower rates of corruption. Meanwhile, Ezeanyeji and Ifebi [3] found out that stable political environment, improved infrastructural facilities, policy consistency and stabi-lized exchange rate are fundamental in attracting FDI to an economy. Most of these studies on determinant of FDI did not place emphasis on a specific sector and very few made use of indicators or measurements for these factors. The fac-tors that influence FDI flow varies per sector, a factor that is of great importance to a foreign investor in a sector may be less important to the other in another sector. Hence, the need is to investigate these factors for specific sectors.

Among foreign investments, telecommunication is one of most strategic in-dustries of national economic control. This is because telecommunication covers many other industrial sectors including the sectors of manufacture, entertain-ment and communication. Foreign investment is not merely a provider and im-provement of local telecommunication equipments. The banking and finance sector is reaping the benefits of deregulation of telecommunication as this has created more opportunities for investment. Also, foreign investments in the tel-ecommunication subsector have contributed to the creation of job in the econ-omy. As a result of these great benefits derived from this sector, there is need to attract FDI flow to the sector.

Several factors have been identified in literature to determine the inflow of FDI into telecommunication sector. These includes, market size, per capita in-come, competition, infrastructure, trade openness, political instability, employ-ment and skill level, technology diffusion and knowledge transfer and linkages, exchange rate rules and regulations, resource endowment, among others [4] [5] [6] [7]. According to these studies some of these factors have impacted nega-tively on the inflow of FDI while some factors have impacted FDI positively. However, most of these studies considered a few factors for investigation which could have resulted in the neglect of some other important factors. Based on this, there is need to do more thorough study in this area. This paper will there-

O. Arawomo, J. F. Apanisile

DOI: 10.4236/me.2018.95058 909 Modern Economy

fore investigate the determinants of FDI in the Nigerian telecommunication sector.

2. Review of Empirical Literature

Generally speaking there is a wide range of variables that can influence a foreign investors to invest in a certain location but the truth is not all of them have equal degree of importance to each foreign investor, therefore it is wise to note that some of these determinants may have more weight to one foreign investor and less to the other at a certain period of time. Several studies have articulated em-pirically the determinants of foreign direct investment in a country, some of which buttressed on FDI at national level and others on FDI in a specific sector.

Pfeffermann and Madarassy [1] identified the size of the domestic market, in-flation, exchange rate volatility, interest rate and macroeconomic policies as critical variables that determines foreign direct investment in developing econ-omies. Their findings indicate that the size of the domestic market and capacity utilization are positively related to foreign direct investment, an unstable ex-change rate also creates foreign exchange risk and uncertain investment climate. Whereas, inflation and volatile exchange rates have negative effects on foreign investment while high and rising inflation rates heighten fears of rising costs of imported capital goods and inputs. However, Demirhan and Masca [8] used the cross-sectional data of 38 developing countries for the period of 2000 to 2004 to examine the determinants of FDI in developing countries. They used econome-tric model and found that per capita income, growth rate, existence of main tel-ephone lines, and trade openness have significant positive impact on FDI in-flows. Similarly, inflation rate and tax rate also significantly attract FDI, with negative sign. On the other hand, they analyzed that risk and labour cost is in-significant to FDI inflows in developing countries.

The study by Elijah [9] employed an econometric model to regress FDI on exogenous variables that include human capital, real exchange rate, annual infla-tion and openness of the Kenya economy. The author found that economic openness and human capital affect FDI inflows positively in the short-run. But inflation and real exchange were negatively related to FDI inflows in the short-run and long-run respectively. A similar econometric model of FDI was used by Fuat and Ekrem [10] to examine location related factors that influence FDI inflows into the Turkish economy. They discovered that the size of the host country’s market, infrastructure (proxied by share of transportation, energy and communication expenditures in GDP) and the openness of the economy (as measured by the ratio of exports to imports) are positively related to FDI in-flows. The results further revealed that both exchange rate instability and eco-nomic instability (measured by interest rate) have negative effects on FDI.

Aqeel and Nishat [11] empirically identified the variables of FDI growth in Pakistan for the period of 1961 to 2003. They used co-integration along with er-ror correction techniques for identifying factors which influence level of FDI.

O. Arawomo, J. F. Apanisile

DOI: 10.4236/me.2018.95058 910 Modern Economy

The results had shown that corporate tax rate, import tariffs, exchange rate, de-valuation of rupee and liberalization measures had positive and significant rela-tionship with FDI. Similarly, Zaman et al. [5] empirically investigated the eco-nomic determinants of FDI in Pakistan for the period from 1971-2003. He found that unit labour cost, inflation, market size, and trade balance revealed their sig-nificant impact, while service sector showed its insignificant contribution to-wards FDI.

Anyanwu [12] in his study on the determinant of FDI inflows to Africa con-cluded that there is a positive relationship between market size and FDI inflows, openness to trade has a positive impact on FDI inflows, higher financial devel-opment has negative effect on FDI inflows, high government consumption ex-penditure attracts FDI inflows to Africa, higher FDI goes where international remittances also goes in Africa, agglomeration has a strong positive impact on FDI inflows to Africa, natural resource endowment and exploitation (especially for oil) attracts huge FDI into Africa, East and Southern African sub-regions appear positively disposed to obtain higher levels of inward FDI. Rojid et al. [13] notes that natural resources, market size, labour cost, human capital, corporate tax and political instability are significant factors in attracting FDI to Africa. Meanwhile, Asiedu [14], using a panel data for 22 countries in Sub-Saharan Africa (SSA) over the period 1984-2000, find that countries that are endowed with natural resources or have large markets attract more FDI. In addition, good infrastructure, an educated labor force, macroeconomic stability, openness to FDI, an efficient legal system, less corruption and political stability promote in-ward FDI.

In Nigeria, a large number of empirical works have been carried out on FDI determinants. Using time series econometric technique on annual data of Nige-ria, Soumyananda [15] examined the effect of the country’s natural resource ex-port, along with openness, market size and macroeconomic risk variables like inflation and foreign exchange rate on FDI inflow during 1970-2006. The study supports earlier literature except market size in case of Nigeria. Generally, the market size is considered as the major determining factor for FDI. It might be true for other country but not in Nigeria during 1970-2006. The study suggests that the endowment of natural resources, macroeconomic risk factors and policy variable like openness are significant determinants of FDI inflow to Nigeria. The findings suggest that the bulk of FDI inflow to Nigeria can be explained by re-source-seeking FDI. Consequently, Akenbor and Tennyson [16] empirically analyzed the impact of natural assets, market size, infrastructure, human capital, investment policies, population health, reliability of legal system, corruption, and political risk on FDI in Nigeria during the period of 1999-2012, and also to determine the factor with the strongest and weakest impact. It was gathered in the study that market size, natural assets, infrastructure, domestic credit, ex-change rate, legal system and population health of the country have a positive relationship with FDI; while corruption, human capital development, political

O. Arawomo, J. F. Apanisile

DOI: 10.4236/me.2018.95058 911 Modern Economy

risk and trade openness have a negative relationship with FDI. Donwa, Mgbame and Ezeani [17] examined the determinants of FDI flows

into oil and gas sector in Nigeria. The study adopted a desk based library me-thod where the knowledge gained from various literature as well as empirical studies reviewed form the basis for conclusion and recommendations. They concluded that the major determinants of Foreign Direct Investment flows into oil and gas sector in Nigeria are Domestic Market size, Trade openness, Infla-tion, Exchange rate and economic policies and necessary measures should be provided to combat inflation and exchange rate variability as these factors dis-courages FDI flow and in turn affects economic growth.

Keith [4] researched on FDI and telecommunication in India, he established that market size, level of support of infrastructure, education level of work force, economy’s level of openness and poor governance in form of high levels of gov-ernment debt are the most important factors that will determine inflow of FDI into Indian telecommunication sector. He established that Foreign direct in-vestment in the Indian telecommunications sector would likely increase further if limits on investment were removed, regulations were clarified and the physical infrastructure was improved. Meanwhile, Sandeep and Surender [7] did a similar study and chose increase in trade, employment and skill level, technology diffu-sion and knowledge transfer and linkages and spillover of domestic firm to be the determinant factors. They find that a stable, transparent and non-discriminatory regulatory system is the best way to attract more foreign investment in India.

In the study of FDI flow into Pakistan telecommunication sector, Qaiser [6] identified political stability, fluctuation in GDP and rules and regulations. He found that there is negative association between political risk instability in Pa-kistan and inflow of FDI and a positive correlation between inflow of FDI and fluctuation in economic growth. Whereas Shumaila et al. [5] considered market size, competition, literacy rate, foreign trade and per capita income and con-cluded that all these factors are positively related to FDI.

3. Methodology 3.1. Model Specification

In an attempt to analyze the relationship between foreign direct investment in telecommunication and its determinant, this study used the OLI-paradigm (ownership, internalization and location) as a guide. However, the key determi-nant in decision making process to invest abroad is location advantages of the host country which is of paramount concern for this objective. These location advantages (determinants of FDI flow) includes market size, inflation, exchange rate, infrastructure, political stability, portfolio diversification, resource location, differential rate of return, foreign exchange reserves, internalization, openness, government policy, political stability, tax policies, regulatory environment, infla-tion, industrial organization, the level of external indebtedness, foreign exchange rate, among others.

O. Arawomo, J. F. Apanisile

DOI: 10.4236/me.2018.95058 912 Modern Economy

This study selected some of the determinants noted by Soumyananda [15] and Anyanwu [12]. These studies were selected because they considered a wide range of factors for investigation. Soumyananda [15] examined the effect of the coun-try’s natural resource export, along with openness, market size and macroeco-nomic risk variables like inflation and foreign exchange rate on FDI inflow. The model is specified thus;

0 1 2 3

4 5

FDI marksize exchrate inf rate openness natresources

t tβ β β ββ β

= + + +

+ + (3.1)

where FDI represents foreign direct investment, β0 is Constant, marksize is market size, exchratet is the exchange rate, infratet is inflation rate, openness is the degree of openness and natresources is natural resources.

Anyanwu [12] identified first lag of FDI (FDI-1), urban population (Urban-Pop), GDP per capital (GDPPC), openness, financial development (Financial-dev), inflation, exchange rate, infrastructure, government consumption expend-iture, remittances, political rights, oil exporters and regions as the determi-nants of FDI in African countries. The model is presented below;

( ) ( ) ( )( ) ( ) ( )( ) ( ) ( )

0 1 2 3

4 5 6

7 8 9

10

FDI Urban Pop GDPPC Openness

Financialdev Inflation Exchange Rate

Infrastructure Govcons exp Re tan

Politica

ijt ijt ijt ijt

ijt ijt ijt

ijt ijt ijt

L

mit ces

β β β β

β β β

β β β

β

= + + +

+ + +

+ + +

+ ( ) ( ) ( )( )

11 12l Rights 1 Oilexporters

Regionsijt ijt ijt

ijtijt

FDIβ αβ

ψ ε

+ − +

+ +

(3.2)

This study will select the factors incorporated from the above studies as the possible factors that determine FDI inflow into the Nigerian telecommunication sector. Some of these factors such as natural resources, political rights, regions, and financial development would be ignored in this study due to unavailability of data.

The model for this study is specified using ARDL model because it allows for the model to take a sufficient number of lags to capture the data generating process in a general-to-specific modeling framework [19];

( )FDIT INFR ,OPN , MSZ ,FEX ,GEXP , INTR , INFLt t t t t t t tf= (3.3)

The model expresses foreign direct investment in telecommunication(FDIT) as a function of infrastructure (INFR), trade openness (OPN), market size (MSZ), foreign exchange rate (FEX), government expenditure (GEXP), interest rate (INTR) and inflation (INFL).

From Equation (3.3), the hypothesized relationship between foreign direct in-vestment in Nigerian telecommunication sector and its determinant is expressed in a linear form thus;

0 1 2 3 4

5 6 7

FDIT INFR OPN MSZ FEX GEXP INTR INFL

t t t t

t t t t

α α α α αα α α µ

= + + + +

+ + + + (3.4)

where α0 … α7 are parameter estimates and µ is the error term.

O. Arawomo, J. F. Apanisile

DOI: 10.4236/me.2018.95058 913 Modern Economy

To illustrate the ARDL modelling approach, Equation (3.4) will further be ex-pressed as;

01 1 1 1

1 1 1 1

1 1 2 1 3

ln FDIT INFR OPN ln MSZ FEX

GEXP INTR INFL ln FDIT

INFR OPN ln MSK

q q q q

j t i l t l k t i m t ii i i i

q q q q

r t i s t i n t i u t ii i i i

t t t

α β γ ϕ λ

η π φ ξ

δ δ δ

− − − −= = = =

− − − −= = = =

− − −

∆ = + ∆ + ∆ + ∆ + ∆

+ ∆ + ∆ + ∆ + ∆

+ + +

∑ ∑ ∑ ∑

∑ ∑ ∑ ∑

1 4 1 5 1

6 1 7 1 8 1

FEX GEXP INTR INFL ln FDIT

t t

t t t t

δ δδ δ δ ε

− −

− − −

+ +

+ + + +

(3.5)

The terms with the summation signs in Equation (3.5) represent the Error Correction Model (ECM) dynamics. The coefficients iδ are the long run mul-tipliers corresponding to long run relationship and ln is the natural log operator.

0α and tε represent the constant and the white noise respectively while , , , , , , ,j l k m r s n uβ γ φ λ η π ϕ ξ represents the short run effects. Δ is the first differ-

ence operator while q is the lag length for the ECM. Equation (3.5) is therefore estimated to obtain the relationship between FDIT and the explanatory va-riables.

3.2. Sources of Data

This study made use of secondary data. The data for the variables are annual in nature from 1986-2014. Data for infrastructure, trade openness, market size and government expenditure, would be sourced from the World Development Indi-cators (WDI) of the World Bank (2015); FDI flow into telecommunication sec-tor, foreign exchange rate, interest rate and inflation, would be sourced from Central Bank of Nigeria Statistical Bulletin (2015).

3.3. Estimation Techniques

The Autoregressive Distributed Lag (ARDL) model will be used to achieve the objective of this study. The ARDL approach to cointegration which was intro-duced originally by Pesaran and Shin [18] was employed here to examine the re-lationship between foreign direct investment in Nigerian telecommunication sector and its determinant. The ARDL model does not require all variables to be I(1) as the Johansen framework and it is still applicable if we have I(0) and I(1) variables in our set. It also allows for the model to take a sufficient number lags to capture the data generating process in a general-to-specific modelling frame-work [19].

To test whether the lagged levels of the variables in the equation are statisti-cally significant or not, the calculated F-statistics is compared with the critical value tabulated by Pesaran et al. [20]. If the F-statistics is above the upper critical value, the null hypothesis of no long run can be rejected, irrespective of the or-ders of integration for the time series. Otherwise, if the statistics fall below the lower critical values, then the null hypothesis cannot be rejected.

Once the long run relationship or co-integration has been established, the second stage of testing involves the estimation of the long run coefficients which

O. Arawomo, J. F. Apanisile

DOI: 10.4236/me.2018.95058 914 Modern Economy

represents the optimum order of the variables. This can be done using selection criteria like Akaike’s Information Criteria (AIC), Schwartz-Bayesian Criteria (SBC), Hannan Quinn Information Criteria (HQIC) and R-bar Square Criteria. However, the most consistent lag length chosen by the criterion will be used. Then the associated error correction is derived in order to calculate the adjust-ment coefficients of the error correction term. Therefore, the short run effects are captured by the coefficients of the first differenced variables in the ECM model.

Having done this, there is also the need to perform a series of diagnostic tests on the stochastic properties established in the model. This is because the exis-tence of a long run relationship does not necessarily imply that the estimated coefficients are stable [21]. This therefore, involves testing of the residuals (ho-moskedasticity, serial correlation, functional form and normality), as well as sta-bility tests such as the Cumulative Sum of recursive residuals (CUSUM) and cumulative sum of squares of recursive residuals (CUSUMsq) to ensure that the estimated model is statistically robust.

4. Empirical Results 4.1. Descriptive Statistics of Data Series

All data series used in the study covers the period from 1986 to 2014. Table 1 shows the descriptive statistics of the annual data series used in the analysis. The skewness and kurtosis statistics are particularly of great importance since they were used in the computation of Jarque-Bera statistic, which was used in testing for the normality or asymptotic property of a particular series. It is observed that the values of mean and median are close. This indicates that the data are distri-buted symmetrically [22]. The Jarque-Bera statistics significantly accept the normal distribution for all variables, indicating normality of their conditional distributions.

4.2. Unit Root Tests

Time series data are characterized to be either stationary or non stationary. However, regressing a stationary time series variable on a non stationary time series variable or a non stationary variable on a non stationary variable will re-sult to a spurious regression. Unit root tests such as the Augmented Dickey Ful-ler (ADF) test and Philips-Perron (PP) test were carried out to ascertain if the variables are stationary or not. In conducting the unit root test, the variables can be I(0), I(1) or I(2). However, auto regressive distributed lag (ARDL) technique does not accommodate I(2) variables. This is because the bound test is based on the assumption that the variables are either I(0) or I(1).

It is observed in Table 2 that using ADF test variables logmsz and infl are I(1) series. dinfra, rintr, opn, infl and fex are significant at levels while logfdi is nei-ther significant at I(0) nor I(1). PP test reveals that all other variables are signifi-cant at I(0) except logfdit, logmsz and infl which are significant at I(1).

O. Arawomo, J. F. Apanisile

DOI: 10.4236/me.2018.95058 915 Modern Economy

Table 1. Descriptive statistics of data series.

(a)

LOGFDIT LOGMSZ RINTR INFL

Mean 21.13594 6.516062 −0.628649 20.82815

Median 20.52518 6.343662 2.767927 12.21701

Maximum 25.17303 7.001282 25.28227 72.83550

Minimum 18.14097 6.203019 −43.57266 5.382224

Std. Dev 1.888953 0.273519 18.20473 19.34185

Skewness 0.382659 0.614375 −0.819032 1.427361

Kurtosis 2.330839 1.658278 3.169784 3.579496

Jarque-Bera 1.248799 3.999634 3.277100 10.25302

Probability 0.535583 0.135360 0.194262 0.005937

Sum 612.9422 188.9658 −18.23083 604.0164

Sum Sq. Dev 99.90798 2.094748 9279.537 10475.00

Observations 29 29 29 29

(b)

INFRA FEX GEXP OPN

Mean 0.482854 109.8392 8.780584 22.31429

Median 0.373598 89.65000 8.200050 21.49798

Maximum 1.177806 272.3700 17.94384 36.48173

Minimum 0.102674 49.73417 4.833249 10.40073

Std. Dev 0.278451 60.43724 3.135207 7.574603

Skewness 1.063896 1.692839 1.057334 0.461189

Kurtosis 3.083853 4.716055 3.722030 2.280494

Jarque-Bera 5.479223 17.40925 6.033386 1.653568

Probability 0.064595 0.000166 0.048963 0.437454

Sum 14.00276 3185.337 254.6369 647.1144

Sum Sq. Dev 2.170982 102274.5 275.2266 1606.489

Observation 29 29 29 29

Source: Author’s Computation from EViews 9 (2017).

4.3. Determinants of Foreign Direct Investment in the Nigerian Telecommunication Sector

The aim of this study is to investigate the determinants of FDI in the Nigerian telecommunication sector over the study period, the ARDL approach was em-ployed in achieving this objective. There is need to determine the optimal lag structure in the ARDL models, followed by the bounds test to show if the va-riables are cointegrated.

The lag order selection is determined using the Akaike Criterion (AIC), Schwartz Bayesian Criterion (BIC) and Hannan-Quinn Criterion (HQC). As

O. Arawomo, J. F. Apanisile

DOI: 10.4236/me.2018.95058 916 Modern Economy

Table 2. Unit root tests.

Augmented Dickey-Fuller (ADF) Test Philips-Perron (PP) Test

Variable Level 1st Difference Status Level 1st Difference Status

logfdit −1.019524 (0.7301)

−2.506344 (0.3224)

−1.433259 (0.5517)

−12.35701*** (0.0000)

I(1)

logmsz 0.594886 (0.9870)

−5.235247*** (0.0013)

I(1) 0.538953 (0.9851)

−5.217091*** (0.0013)

I(1)

fex −3.733436***

(0.0090) I(0)

−3.833681*** (0.0071)

I(0)

dinfra −3.383578**

(0.0207) I(0)

−3.383578** (0.0207)

I(0)

infl −2.510853 (0.1237)

−3.435291* (0.0712)

I(1) −2.598355 (0.1052)

−5.767097 (0.0004)

I(1)

rintr −5.308931***

(0.0002) I(0)

−5.308896*** (0.0002)

I(0)

opn −3.243412**

(0.0279) I(0)

−3.154872** (0.0338)

I(0)

gexp −3.373271**

(0.0208) I(0)

−3.426223** (0.0185)

I(0)

Source: Author’s Computation from EViews 9 (2017). Note: *, ** and *** denotes significance at 10%, 5% and 1% levels respectively.

shown in Table 3, the AIC, BIC and HQC suggested three lags and as such any of the criteria can be used since they all chose the same lag length.

The bounds test results are presented in Table 4. The F-statistic approximate-ly fell above the upper critical bound at 10%, 5% and 1% level of significance. The F-statistic also fell above the lower critical bound at 10%, 5% and 1% level of significance. The results therefore indicated that there existed a long run rela-tionship among the variables.

4.4. Analysis of the Determinants of Foreign Direct Investment in the Nigerian Telecommunication Sector

The result of the long run and short run relationship among the variables is pre-sented in Table 5. In the long run, the coefficient of market size (5.09) showed that it has positive significant relationship with FDI in telecommunication. This implies that a unit increase in market size would increase FDI flow into tele-communication by 5.09%. Likewise in the short run the current year value of market size had a positive and significant effect on FDI in telecommunication with a coefficient value of 3.92. A unit increase in market size would increase FDI flow into telecommunication by 3.92%. Also, its last two years value had a positive but insignificant impact on FDI in telecommunication. Therefore, it can be concluded that market size is a major factor that can attract FDI flow into the Nigerian telecommunication sector. This positive effect of market size as ex-pected is consistent with studies by Asiedu [14]; Soumyanada [15] and Qaiser

O. Arawomo, J. F. Apanisile

DOI: 10.4236/me.2018.95058 917 Modern Economy

Table 3. Lag length selection criteria.

Lag LogL LR FPE AIC SC HQ

0 −478.857 NA 11363110 38.94856 39.3386 39.05674

1 −375.179 132.7077 622491.7 35.77433 39.28469 36.74795

2 −217.829 100.7039* 2948.781* 28.30634 34.93702 30.14541

3 5061.736 0 NA −388.9389* −379.1879* −386.2344*

Source: Author’s Computation from EViews 9 (2017). Note: * denotes lag order selection by the criterion. LR: sequential modified LR test statistic (each test at 5% level); FPE: Final Prediction Error; AIC: Akaike Information Criterion; SC: Schwarz Information Criterion; HQ: Hannan-Quinn Information Criterion. Table 4. ARDL bounds test.

Model F-statiatic No. of Regressors (K)

f (logmkz, dinfra, fex, gexp, opn, infl, rintr) 16.57586 7

Critical value bounds

Significance I(0) Bound I(1) Bound

10% 2.03 3.13

5% 2.32 3.5

1% 2.96 4.26

Source: Author’s Computation from EViews 9 (2017).

[6] which reported that market size has a positive and significant relationship with FDI. Theoretically, the investment incentive for market seeking FDI such as telecom firms who seek to expand their market presence by increasing their pe-netration in local markets is the market size.

Similarly, in the long run, trade openness has a positive and significant effect on FDI in telecommunication with coefficient value of 0.12 at 1% significant lev-el. This implies that a unit increase in trade openness would increase FDI flow into telecommunication by 12%. This also applies in the short run where the current year value of trade openness had positive but insignificant impact on FDI in telecommunication while its last one year value is negatively related to FDI. From this result a deduction can be made that trade openness is positively related to the inflow of FDI in telecommunication sector. This is supported by Anyanwu [12] and Sandeep and Surender [7] that the more open an economy is, the greater the FDI it can attract. Also, the gravity model applied to trade, in its simplest form [23] states that the volume of trade between any two countries is positively correlated with the economic volumes of the exporter and importer countries.

Likewise, the coefficient of infrastructure is positive (0.10) but insignificant in the long run. This implies that one percent increase in infrastructure does not have significant impact on FDI in telecommunication. Also, in the short run the current year value of infrastructure had positive (0.61) and insignificant impact on FDI flow in telecommunication. Meanwhile its last one year value had a

O. Arawomo, J. F. Apanisile

DOI: 10.4236/me.2018.95058 918 Modern Economy

Table 5. (a) Long run and (b) short run relationships.

(a)

Long Run Coefficients

Variable Coefficient t-Statistic Prob.

LOGMSZ 5.08705 9.054031*** 0.0008

DINFR 0.099051 0.114501 0.9144

FEX −0.000204 −0.13285 0.9007

GEXP −0.074958 −1.43759 0.2239

OPN 0.117488 5.745742*** 0.0045

INFL −0.051712 −3.61493** 0.0225

RINTR −0.062692 −4.02929** 0.0157

C −12.547069 −3.11259** 0.0358

(b)

Short Run Coefficient

Variable Coefficient t-Statistic Prob.

D(LOGRFDI(−1)) −0.358012 −4.29152** 0.0127

D(LOGRFDI(−2)) −0.923824 −12.3211*** 0.0002

D(LOGMSZ) 3.916468 4.336566** 0.0123

D(LOGMSZ(−1)) 2.560737 1.902323 0.1299

D(DINFR) 0.614838 1.41994 0.2286

D(DINFR(−1)) 2.017467 3.736869** 0.0202

D(FEX) −0.000162 −0.13317 0.9005

D(GEXP) 0.054205 1.84342 0.139

D(GEXP(−1)) 0.135455 3.610545** 0.0225

D(OPN) 0.013376 1.06752 0.3459

D(OPN(−1)) −0.022726 −2.21049* 0.0916

D(INFL) −0.033872 −4.19254** 0.0138

D(INFL(−1)) 0.010541 2.782017** 0.0497

D(RINTR) −0.024514 −5.53679*** 0.0052

ECT(−1) −0.796752 −6.91415*** 0.0023

R2 = 0.998706 Adjusted R2 = 0.991913 F-statistic = 147.0178

Prob (F-statistic) = 0.000100

Source: Author’s Computation from EViews 9 (2017). Note: *,** and *** denotes significance at 10%, 5% and 1% levels respectively.

positive and significant impact on FDI in telecommunication. Overall, it can be deduced that an increase in infrastructure does not necessarily imply an increase in FDI flow into the Nigerian telecommunication sector. This contradicts the

O. Arawomo, J. F. Apanisile

DOI: 10.4236/me.2018.95058 919 Modern Economy

view of Keith [4]; Asiedu [14] and Akenbor and Tennyson [16] which reported that infrastructure promote inward FDI. The contrary result from this study can be traced to the nature of the sector (telecommunication). Infrastructures in Ni-geria have improved over the years but this may not be significant in attracting FDI into telecommunication sector as most of the infrastructures needed in the sector are made available by foreign investors.

Table 5 indicates that the inflation has a negative and significant impact on FDI in telecommunication in the long run with coefficient value of −0.05. This implies that a unit increase in inflation would decrease FDI flow into telecom-munication by 5%. Also, in the short run there exists a negative and significant relationship between the current year value of inflation and FDI in telecommu-nication. The coefficient value of inflation (−0.03) implies that a unit increase in inflation would decrease FDI in telecommunication by 3%. However, its last one year value had a positive effect on FDI flow into the sector. Therefore, increase in inflation would discourage the flow of FDI into the Nigerian telecommunica-tion sector which is in conformity to the study of Elijah [9]. This is also sup-ported by Fisher equation which explains that when inflation is low, the nominal interest rate is also low. Therefore, financial cost on FDI is low, and rate of re-turn on investment is high.

Furthermore, the coefficient value of government expenditure (−0.07) in the long run showed that it had negative and insignificant effect on FDI in tele-communication. This implies that government expenditure is unimportant in attracting FDI in the long run. However, in the short run the current year value of government expenditure had a positive but insignificant impact on FDI in telecommunication. Meanwhile its last one year value had a positive and signifi-cant impact with coefficient value of 0.14, implying that an increase in govern-ment expenditure will increase FDI flow into the sector by 14%. Therefore it can be concluded that government expenditure is vital in attracting FDI into tele-communication sector. The finding is supported by Anyanwu [12]. The Keyne-sian theory posited that there exists a multiplier effect of a change in expenditure on the national income. Hence an increase in the government expenditure would lead to increased employment and investment which would improve ag-gregate output.

In addition, the coefficient values and p-values of foreign exchange rate in-dicates that it had negative and insignificant impact on FDI flow into telecom-munication both in the long and short run. This implies that foreign exchange rate is not an important determinant of FDI flow into the Nigerian telecommu-nication sector. A possible reason for this result is that the exchange rate effects of third countries come through correlations that affect location choice of risk averse firms, which invest in countries whose exchange rates are negatively cor-related to other exchange rates as a way of diversifying FDI [20]. This finding contradicts some studies [11] [24] which concludes that foreign exchange rate is essential in attracting FDI into an economy as increase in exchange rate would

O. Arawomo, J. F. Apanisile

DOI: 10.4236/me.2018.95058 920 Modern Economy

increase FDI inflow. Consequently, Table 5 showed that interest rate had a negative and significant

impact on FDI in telecommunication in the long run with coefficient value of −0.06 at 1% significant level. This implies that a unit increase in interest rate would decrease FDI flow into telecommunication by 6%. Similarly, in the short run there exists a negative and significant relationship between current year val-ue of interest rate and FDI inflow. The coefficient value of interest rate was −0.02, implying that an increase in interest rate would decrease FDI inflow by 2%. Therefore it can be reported that the higher the interest rate of Nigeria, the less attractive its telecommunication sector would be to FDI inflow. From Fisher equation, when inflation is low, the nominal interest rate is also low. Therefore, financial cost on FDI is low, and rate of return on investment is high. This also agrees with study by Fuat and Ekrem [10].

The Error Correction Term (ECT) for this cointegrating relationship was negative as expected (−0.80) and significant which showed that about 80% of short run deviations would be corrected for annually. Also from the ARDL re-gression result, the various tests (R2, Adjusted R2, F-statistic, and p-value) of sig-nificance on the model showed good result. The R2 of 0.998 indicated high ex-planatory power of the independent variables. The adjusted R2 value of the mod-el also supported this fact. F-statistic which measures the overall significance of the model suggests that all estimated regression model is statistically significant. This is indicated by the F-statistic (147.0178) and p-value (0.000100).

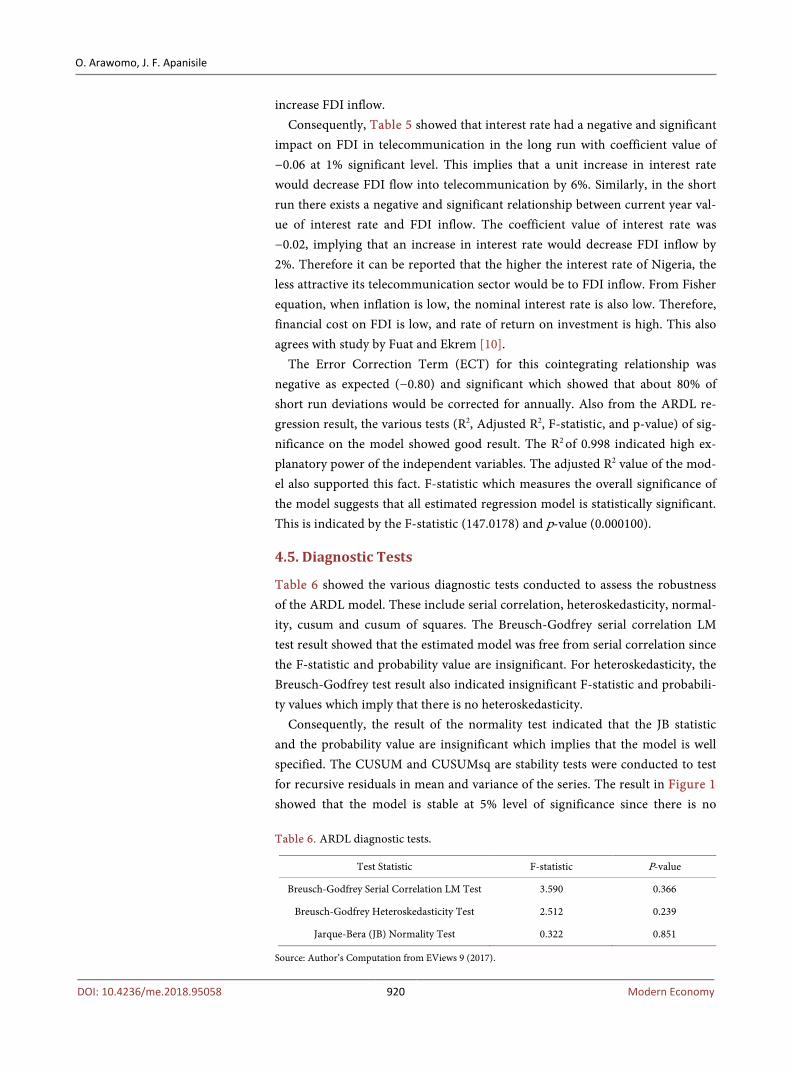

4.5. Diagnostic Tests

Table 6 showed the various diagnostic tests conducted to assess the robustness of the ARDL model. These include serial correlation, heteroskedasticity, normal-ity, cusum and cusum of squares. The Breusch-Godfrey serial correlation LM test result showed that the estimated model was free from serial correlation since the F-statistic and probability value are insignificant. For heteroskedasticity, the Breusch-Godfrey test result also indicated insignificant F-statistic and probabili-ty values which imply that there is no heteroskedasticity.

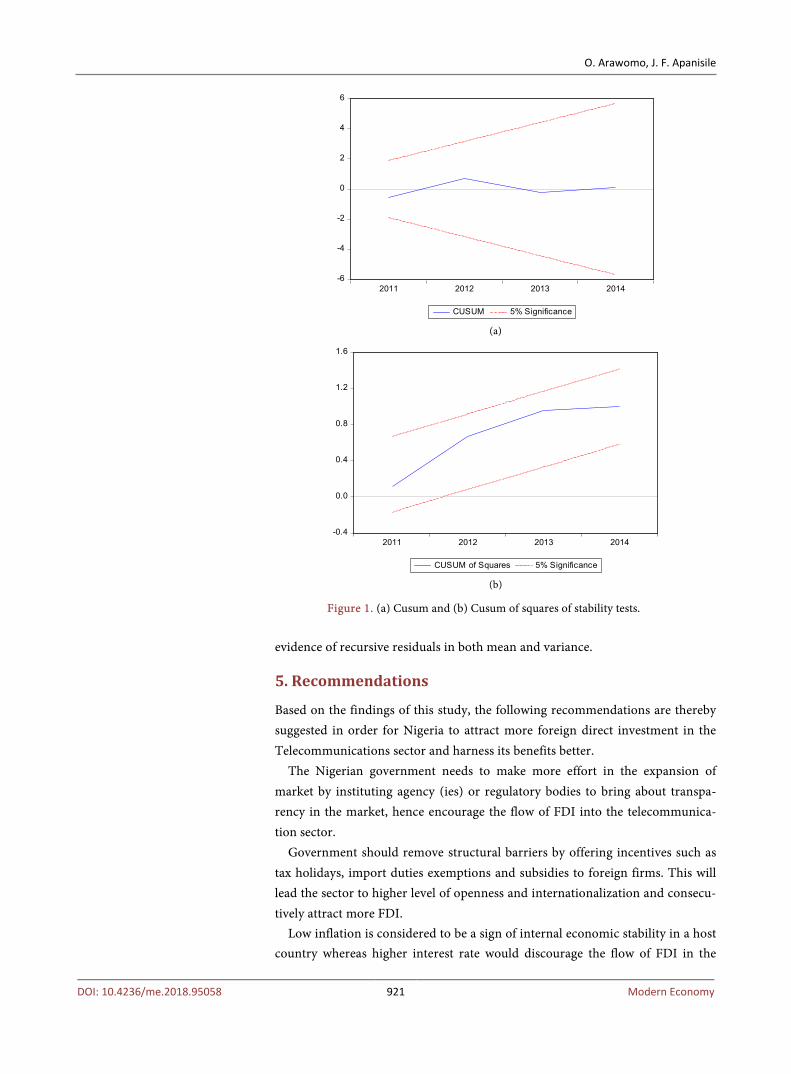

Consequently, the result of the normality test indicated that the JB statistic and the probability value are insignificant which implies that the model is well specified. The CUSUM and CUSUMsq are stability tests were conducted to test for recursive residuals in mean and variance of the series. The result in Figure 1 showed that the model is stable at 5% level of significance since there is no Table 6. ARDL diagnostic tests.

Test Statistic F-statistic P-value

Breusch-Godfrey Serial Correlation LM Test 3.590 0.366

Breusch-Godfrey Heteroskedasticity Test 2.512 0.239

Jarque-Bera (JB) Normality Test 0.322 0.851

Source: Author’s Computation from EViews 9 (2017).

O. Arawomo, J. F. Apanisile

DOI: 10.4236/me.2018.95058 921 Modern Economy

(a)

(b)

Figure 1. (a) Cusum and (b) Cusum of squares of stability tests. evidence of recursive residuals in both mean and variance.

5. Recommendations

Based on the findings of this study, the following recommendations are thereby suggested in order for Nigeria to attract more foreign direct investment in the Telecommunications sector and harness its benefits better.

The Nigerian government needs to make more effort in the expansion of market by instituting agency (ies) or regulatory bodies to bring about transpa-rency in the market, hence encourage the flow of FDI into the telecommunica-tion sector.

Government should remove structural barriers by offering incentives such as tax holidays, import duties exemptions and subsidies to foreign firms. This will lead the sector to higher level of openness and internationalization and consecu-tively attract more FDI.

Low inflation is considered to be a sign of internal economic stability in a host country whereas higher interest rate would discourage the flow of FDI in the

-6

-4

-2

0

2

4

6

2011 2012 2013 2014

CUSUM 5% Significance

-0.4

0.0

0.4

0.8

1.2

1.6

2011 2012 2013 2014

CUSUM of Squares 5% Significance

O. Arawomo, J. F. Apanisile

DOI: 10.4236/me.2018.95058 922 Modern Economy

telecom sector. Therefore, government should improve on the close monitoring of these macroeconomic stability indicators by balancing the budget and re-stricting the money supply so as to put them under control.

More government expenditure should be channeled towards creation of in-vestment friendly and enabling environment for foreign investors. This includes addressing the issue of insecurity in the country, giving of incentives and reduc-ing the bureaucracy associated with starting a business.

6. Conclusion

Having investigated the determinants of FDI in the Nigerian telecommunication sector, this study revealed a number of factors that can attract or discourage the flow of FDI into the sector. These factors include, market size, trade openness, inflation, interest rate and government expenditure. Ultimately, the study found that market size, trade openness and government expenditure had a positive and significant effect on FDI flow into the sector while inflation and interest rate had negative and significant relationship with FDI flow in the sector. However, in-frastructure had a positive but insignificant effect on FDI flow while foreign ex-change rate had a negative and insignificant effect on FDI, making these factors less important in attracting FDI into the sector. The study therefore concludes that the key determinants of FDI flow into the sector are market size, trade openness, government expenditure, inflation and interest rate.

References [1] Pfeffermann, G.P. and Madarassy, A. (1992) Trends in Private Investment in De-

veloping Countries. International Finance Corporation Discussion, 16.

[2] Iyela, A. (2009) The Trend of Foreign Direct Investment in Nigeria: Problems and the Way out. Journal of the National Association for Science, Humanities and Edu-cation Research, 7, 15-25.

[3] Ezeanyeji, C.I. and Ifebi, O.L. (2016) Impact of Foreign Direct Investment on Sec-toral Performance in the Nigerian Economy: A Study of Telecommunications Sec-tor. International Journal of Humanities Social Sciences and Education, 3, 57-75.

[4] Green, K. (2005) Foreign Direct Investment in the Indian Telecommunications Sector. MPRA Paper No. 18099.

[5] Zaman, K. and Shumaila, H. (2006) Economic Determinants of Foreign Direct In-vestment in Pakistan. Journal of Humanities and Social Sciences, 181-192.

[6] Qasier, M. (2010) Foreign Direct Investment in Pakistan Telecom Sector: School of Management, Blekinge Institute of Technology.

[7] Sandeep, B. and Surender, K. (2013) Fdi’s in India—A Study of Telecommunication Industry. International Journal of Advanced Research in Management and Social Sciences, 2.

[8] Demirhan, E. and Masca, M. (2008) Determinants of Foreign Direct Investment Flows to Developing Countries: A Cross-Sectional Analysis. Prague Economic Pa-pers, 4, 356-369. https://doi.org/10.18267/j.pep.337

[9] Elijah, O.K. (2006) Determinants of Foreign Direct Investment in Kenya. Institute African de Development Economiqueet de Planification Publication, Dakar.

O. Arawomo, J. F. Apanisile

DOI: 10.4236/me.2018.95058 923 Modern Economy

[10] Fuat, E. and Ekrem, T. (2002) Locational Determinants of Determinants of Foreign Direct Investment in an Emerging Market Economy: Evidence from Turkey. Mul-tinational Business Review, 10.

[11] Aqeel, A. and Nishat, M. (2005) The Determinants of Foreign Direct Investment in Pakistan. 20th Annual PSDE Conference, Islamabad.

[12] Anyanwu, J.C. (2011) Determinants of Foreign Direct Investment inflows to Africa, 1980-2007. Working Paper Series No. 136, African Development Bank, Tunis.

[13] Rojid, S., Sectanah, B., Ramessur, S.T. and Sannassee, V. (2005) Determinants of FDI; Lessons from African Economics. University of Maauritius.

[14] Asiedu, L. (2006) Foreign Direct Investment in Africa: The Role of Natural Re-sources, Market Size, Government Policy, Institutions and Political Instability. United Nations University. https://doi.org/10.1111/j.1467-9701.2006.00758.x

[15] Soumyananda, D. (2009) Factors Attracting FDI to Nigeria: An Empirical Investiga-tion. Madras School of Economics India.

[16] Akenbor, C.O. and Tennyson, O. (2014) Determinants of Foreign Direct Invest-ment in a Democratic Society: The Nigeria Experience. The Business & Manage-ment Review, 4, 282-294.

[17] Donwa, P.A., Mgbame, C.O. and Ezeani, B.O. (2015) Foreign Direct Investment (FDI) Flows into Oil and GasSector in Nigeria. IJMDD, 2, 287-295.

[18] Pesaran, M.H. and Shin, Y. (1995) Autoregressive Distributed Lag Modelling Ap-proach to Cointegration Analysis. DAE Working Paper Series No. 9514, Depart-ment of Economics, University of Cambridge, Cambridge.

[19] Banerjee, A. (1993) Co-Integration, Error Correction, and the Econometric Analysis of Non-Stationary Data. Oxford University Press, Oxford. https://doi.org/10.1093/0198288107.001.0001

[20] Pesaran, M.H., Shin, Y. and Smith, R.J. (2001) Bounds Testing Approaches to the Analysis of Level Relationships. Journal of Applied Econometrics, 16, 289-326. https://doi.org/10.1002/jae.616

[21] Bahmani-Oskooee, M. and Brooks, T.J. (1999) Bilatera J-Curve between US and Her Trading Partners. Weltwirtschaftliches Archive, 135, 156-165.

[22] Karmel, H. and Polasek, M. (1980) Applied Statistics for Economist, Carlton Victo-ria, Pitman.

[23] Tinbergen, J. (1962) Shaping the World Economy: Suggestions for an International Economic Policy. Twentieth Century Fund, New York.

[24] Eiteman, D.K., Stonehill, A.I. and Moffett, M.H. (2010) Multinational Business Finance. 12th Edition, Pearson Prentice Hall, Boston.