Embed Size (px)

Citation preview

Design Choices and Equity Implications

of Community Shared Solar

Gabe Chan, University of Minnesota

Project Team: Matt Grimley, Ben Ihde, Isaac Evans, Poulomi Mazumder,

Elizabeth Arnold, Jacob Herbers, Maureen Hoffman, Jordan Morgan, Nick

Neuman, Ryan Streitz

USAEE/IAEE North American Conference

November 12-15, 2017

2

Will energy and environmental policies

make the world more or less fair?

Will considering fairness make energy

and environmental policies more or less

effective and politically durable?

Agenda

• Distributional impacts of solar deployment

• The community shared solar model

• Research methods

• Preliminary results

3

DISTRIBUTIONAL IMPACTS OF

SOLAR DEPLOYMENT

4

Energy expenditures as a fraction of income: the “Energy Burden”

5

6

7Borenstein (2017), JAERE

Fra

ction o

f C

usto

mers

by Incom

e G

roup

CA Residential Solar Adoption vs. Income Distribution

Federal energy subsidies are much more regressive than other tax credits

8Borenstein and Davis (2016), TPE

Building Equity in Solar Programs

• Obama’s 2016 “Clean Energy Savings for All Americans

Initiative”

o Property-Assessed Clean Energy (PACE)

o Low Income Housing Energy Assistance Program

(LIHEAP) for efficiency and renewables

o Solar Training Network

o Community Solar Challenge

• State programs

• Private sector efforts

o Solar City(?)9

COMMUNITY SHARED SOLAR

10

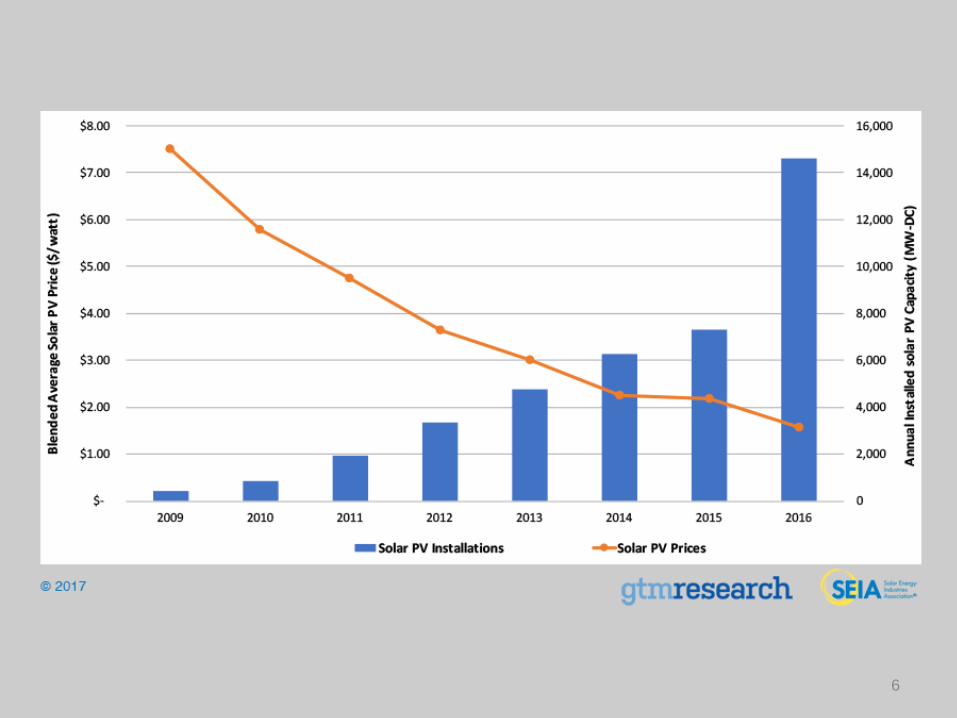

Community Shared Solar (CSS)

11

CSS Policy Diffusion

12Source: Stanton, NRRI 2016

13SEPA (2015)

14ILSR (2017)

15ILSR (2017)

16

Opening Up the Solar Market?

17NREL (2014)

CSS Design Elements

• Ownership Model

18

CSS Ownership Models

19

CSS Design Elements

• Ownership Model

• Subscription Model

o Pay up front; leasing

o Pay as you go; bill crediting

• System and site selection

o Project design; investment partners

o Rate design

• Enrollment and outreach

• Program management

20

Opportunities

Scale economies

Could open up access to

finance (flexible ownership)

Eased siting constraints;

siting opportunities

Eased participation

constraints: no building

ownership, roof space,

maintenance, etc.

Challenges

Requires greater institutional

support, coordination

Increased financing

requirements (scale)

Pushes 3rd-party owned DER

challenges further

Participation constraints may

be too low: no “community”

Other Considerations

How distributed? Who participates? Who pays?

Key Uncertainties

• CSS programs are designed to lower barriers:

o Scale lowers cost

o No requirement for on-site deployment

o No requirement for ownership

o Alternative source of finance can compensate

participants based on economics

• Solar remains a capital-intensive investment

o Will community solar programs replicate the

distributional impacts of rooftop solar?

22

METHODS

23

Analytic Approach

• State Program Design

o How have different states addressed the distributional

impacts of CSS programs?

o Comparative case studies of 6 mandated state

programs: focus on MN Xcel’s program (165 MW)

• MN Utility Program Evaluation

o How do different utility program design options affect

costs and access to subscribers?

o Financial analysis of ~50 CSS programs in MN

24

PRELIMINARY RESULTS:

STATE MANDATED PROGRAMS

25

State Program Design

• States are deploying a variety of policies to increase

access to low/moderate income (LMI) households:

o LMI carveouts/mandates

o Financial incentives (tariff “adders”)

o Grant funding and loans for specific projects

• What is working?

26

State Program Design

27

California

(PG&E, SDG&E,

SCE)

Colorado

(Xcel, Black

Hills)

Maryland

(CSEGS Pilot)

Massachusetts

(NRG)

Minnesota

(Xcel)

New York

(NY-SUN)

CSS Capacity

(MW)22 30 0 99 165 3

CSS Planned

Capacity

(MW)

0 >20 53 0 604 794

Carve Out

20% for "most

disadvantaged";

10% for MASH

5% carve-out

10% carve-out;

30% to projects

in LMI areas

-- --

Carve-outs in

Phase I, then

removed

Tariff AdderUnder

consideration-- --

SREC-II and

SREC transfer

Under

consideration--

Grant

Funding

CSI: 10%

directed to LMI

until 2021

$1.2 mil to GRID

AlternativesSpecial Fund

MA Solar Loan

Program--

LMI CSS eligible

for several large

grants ($1.2 bil)

Other

Strategies

Subscription

goals,

certification,

capacity limits

0-down financing -- Anchor offtakers

Anchor

subscribers

(Minneapolis)

--

Siz

eL

MI P

rog

ram

s

State Program Design: Key Takeaways

• Carve-outs may not improve equity

o CO program’s carve-out remains under-subscribed

o Even at 0-cost, LMI subscriptions have been low

• Favorable tariffs crowd-out residential participation

o MN program’s favorable tariff has created large supply, but limited residential participation

• Risk drives subscriber screening by 3rd party developers

o Where 3rd parties develop CSS projects, credit screens and long contracts favor stable customers

• Grant funding has attracted LMI participation but doesn’t scale 28

The Community in Community Solar?

29

• Minnesota’s Xcel CSS program has many restrictions to

localize benefits – but no direct residential requirements:

o Minimum 5 subscribers

o No subscriber with >40% of output or a subscription

more than 120% of past consumption

o Gardens up to 1 MW (disputed interpretation)

• Are these efforts working?

Distributional Impacts Remain Skewed

PRELIMINARY RESULTS:

MN CSS PROGRAMS

31

Who Offers Community Solar in

Minnesota?

Municipal Utilities:

Moorhead Public

Service

Investor Owned

Utilities

Minnesota Power

(Allete)

Xcel Energy

Co-Ops:

Arrowhead

Beltrami

Connexus

Cooperative L&P

Crow Wing

Itasca

Kandiyohi

Lake Region

McLeod

Meeker

People’s Energy

Redwood

Runestone

South Central

Stearns

Steele-Waseca

Tri-County

Wright-Hennepin

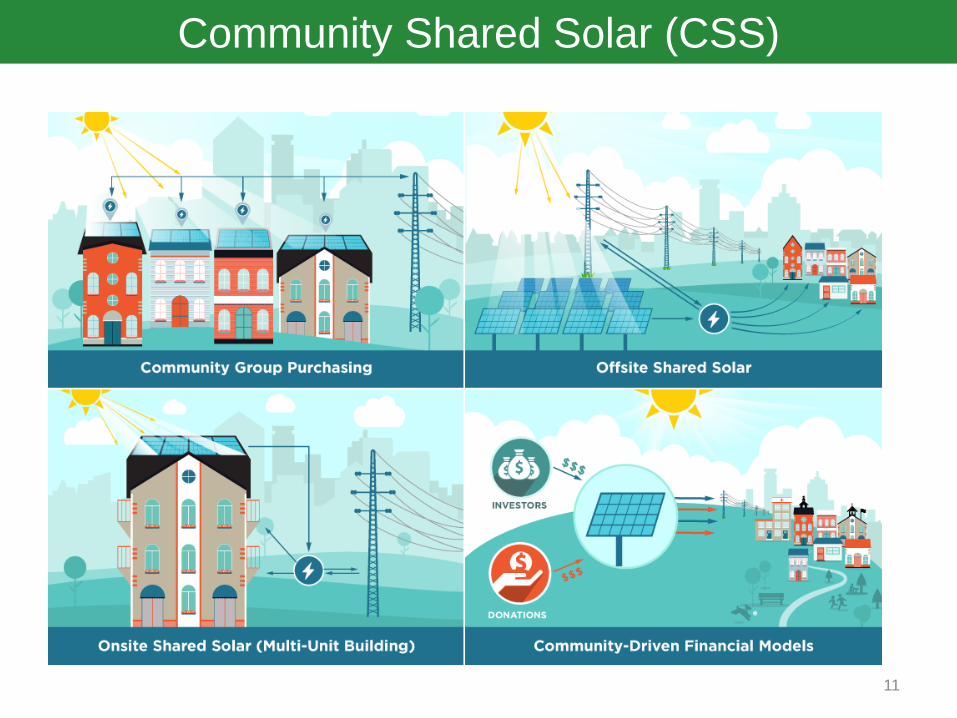

MN Utility Program Evaluation

33

0

2

4

6

8

10

12

14

16

50 - 45 45 - 40 40 - 35 35 - 30 30 - 25 25 - 20 20 - 15 15 - 10 10 - 5 5 - 0 +0 - +5

Nu

mb

er o

f C

SS C

on

trac

ts

Subscription NPV ($/W)

PAYG PUF/LL

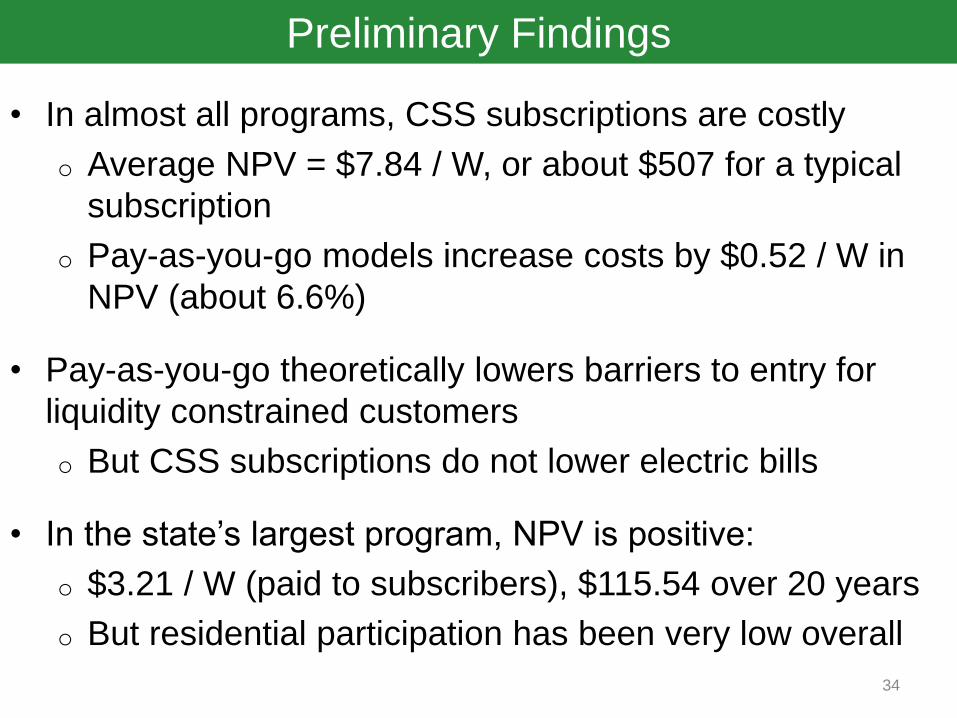

Preliminary Findings

• In almost all programs, CSS subscriptions are costly

o Average NPV = $7.84 / W, or about $507 for a typical

subscription

o Pay-as-you-go models increase costs by $0.52 / W in

NPV (about 6.6%)

• Pay-as-you-go theoretically lowers barriers to entry for

liquidity constrained customers

o But CSS subscriptions do not lower electric bills

• In the state’s largest program, NPV is positive:

o $3.21 / W (paid to subscribers), $115.54 over 20 years

o But residential participation has been very low overall

34

Next Steps

• Evaluate LMI-targeted programs as state programs roll out

o Explore other, “experimental” policy design options

• Explore the potential of 3rd party intermediaries to open up

CSS subscription markets

• Tie policy design measures to more immediate outcome

metrics

o Subscriptions by income group

o Subscription benefits

35

What does community solar look like in MN?

• Fills the divide between rooftop (0-100kW) and utility-

scale solar (50-100MW)

• Currently contributes 24% of solar power in Minnesota,

with tens of MW coming online each month

– First 1MW panel of community solar went online in

December, 2016

![Implications of Lexical Choices in Translating Novels as Literary … · 2015-12-11 · Jamal Mohamed Giaber trans-kom 8 [2] (2015): 415-445 Implications of Lexical Choices in Translating](https://img.dokumen.tips/doc/110x75/5e6dfdaa14ab2c0b5f4b6849/implications-of-lexical-choices-in-translating-novels-as-literary-2015-12-11-jamal.jpg)