Embed Size (px)

DESCRIPTION

Basically Derivative is important class of financial instrument which centrals to today's financial markets and trade markets. It offers wide range of risk protection and involve in innovative investment strategies.

Citation preview

DERIVATIVE MARKET

GROUP - 4

1. Introduction to Derivatives2. Currency Future3. Currency Option4. Interest Rate Swap5. Currency Swap6. Credit Default Swap7. Credit Linked Note

AGENDA

The derivatives market is the financial market for derivatives, financial instruments like futures or options, which are derived from other forms of assets.

What are derivative markets ?

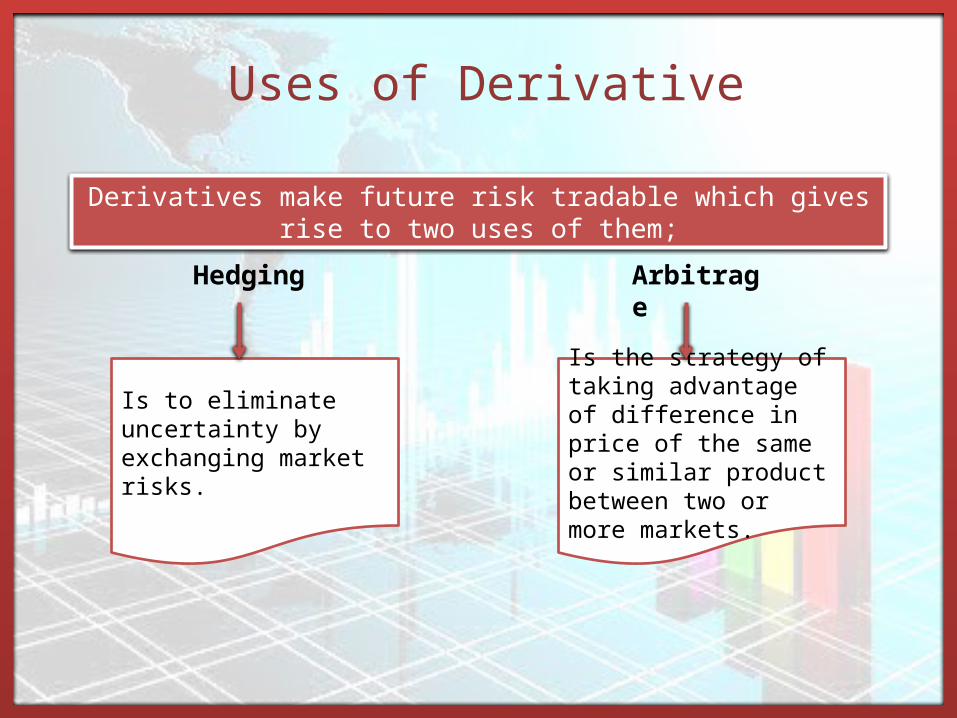

Uses of Derivative

Derivatives make future risk tradable which gives rise to two uses of them;

Is to eliminate uncertainty by exchanging market risks.

Is the strategy of taking advantage of difference in price of the same or similar product between two or more markets.

Hedging Arbitrage

Types of derivatives Instrument

futuresoptionsIRSCurren

cy SwapCDS’sCLN’s

A futures contract is a standardized contract, traded on an exchange, to buyor sell a certain underlying asset or an instrument at a certain date in thefuture, at a specified price. When the underlying is an exchange rate, the contract is termed a “currency futures contract”. In other words, it is a contract to exchange one currency for another currency at a specified date and a specified rate in the future.

Who is eligible to trade in currency

derivatives ?

Foreign Institutional

Investors (FII)

Currency futures

Does the national economy of India need currency future ?

Every business exposed to foreign exchange risk needs to have a facility

to hedge against such risk.

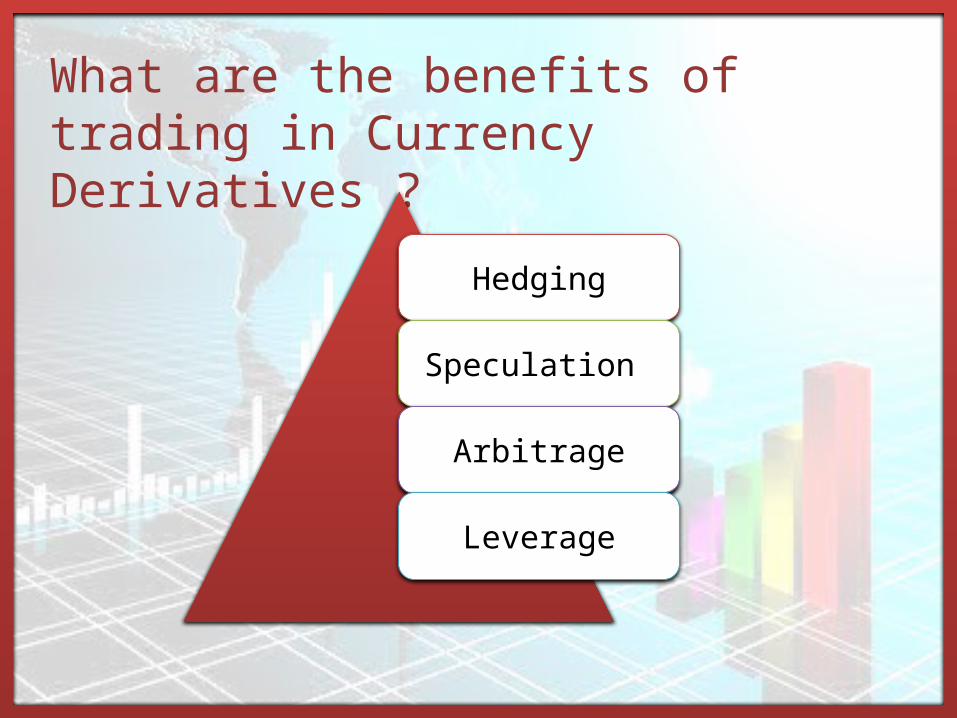

What are the benefits of trading in Currency Derivatives ?

Hedging

Speculation

Arbitrage

Leverage

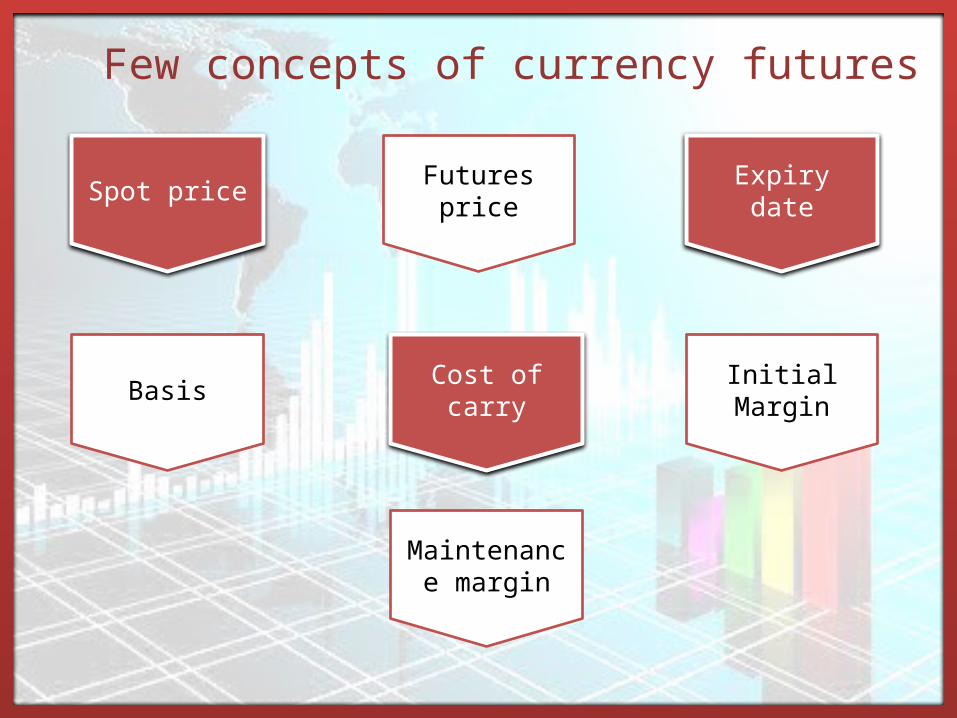

Spot price Expiry dateFutures price

Basis Cost of carry Initial Margin

Maintenance margin

Few concepts of currency futures

FUTURES PAYOFFS

Payoff for the buyer of the currency

Payoff for seller of futures

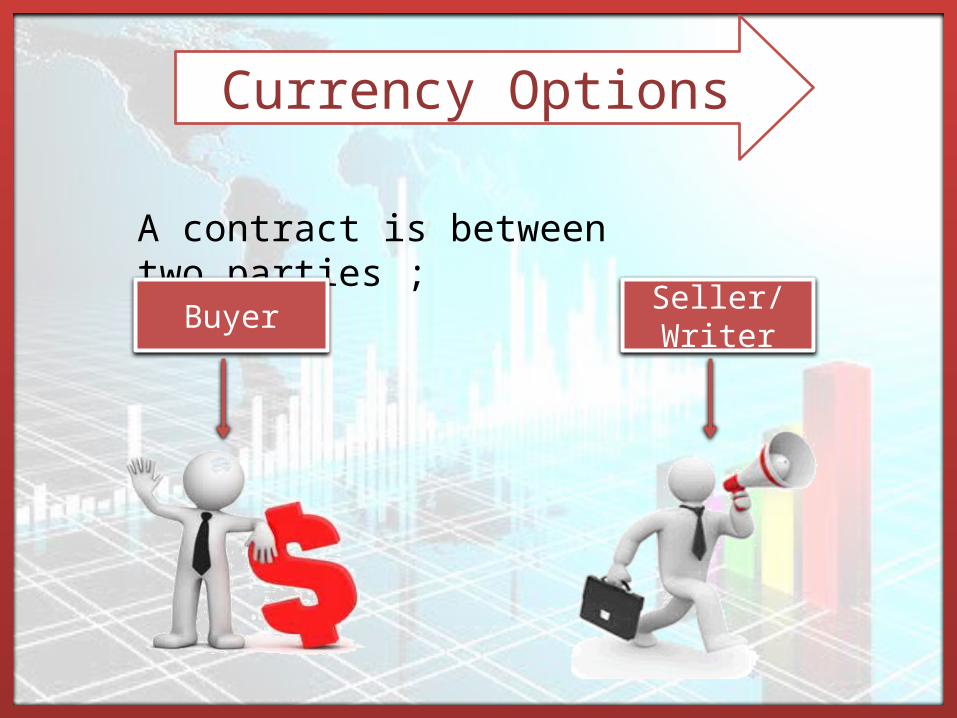

Currency Options

A contract is between two parties ;

Buyer Seller/Writer

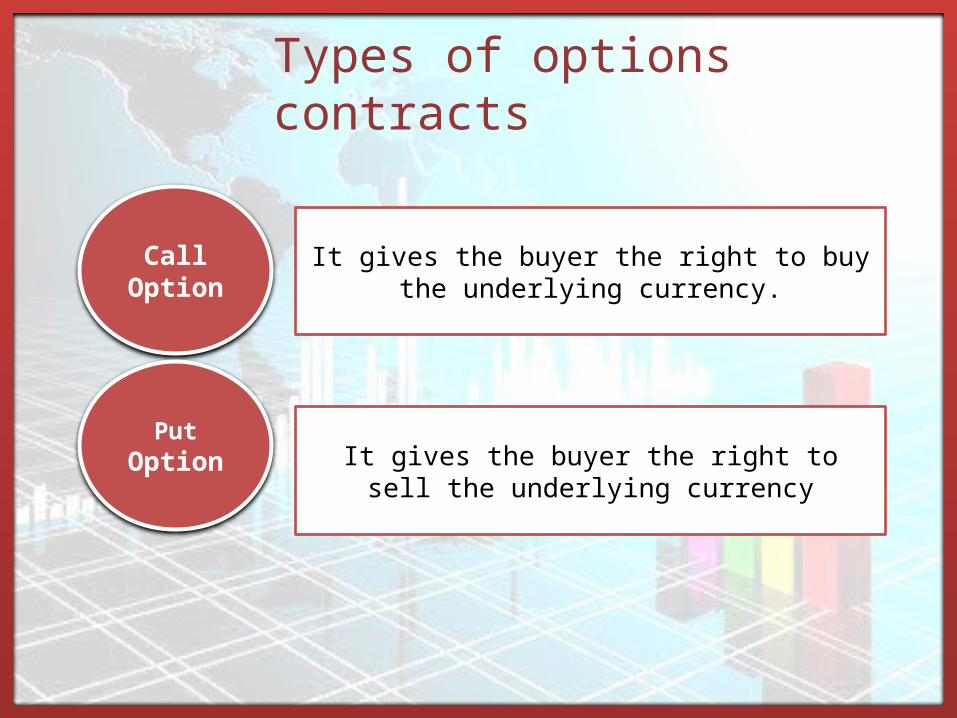

Types of options contracts

Call Option

Put Option

It gives the buyer the right to buy the underlying currency.

It gives the buyer the right to sell the underlying currency

In a foreign exchange transaction, one currency is bought, while another is simultaneously sold. An option to buy US dollars against the Indian

Rs(USD Call) is an option to sell IND Rs.against the US dollar (Rs. Put). In every foreign exchange transaction, one currency is purchased and another currency is sold. Consequently, every currency option is both a call and a

put.

Importers

Exporters

Buy/CallSell/put

Buy/Put Sell/Call

Conti…

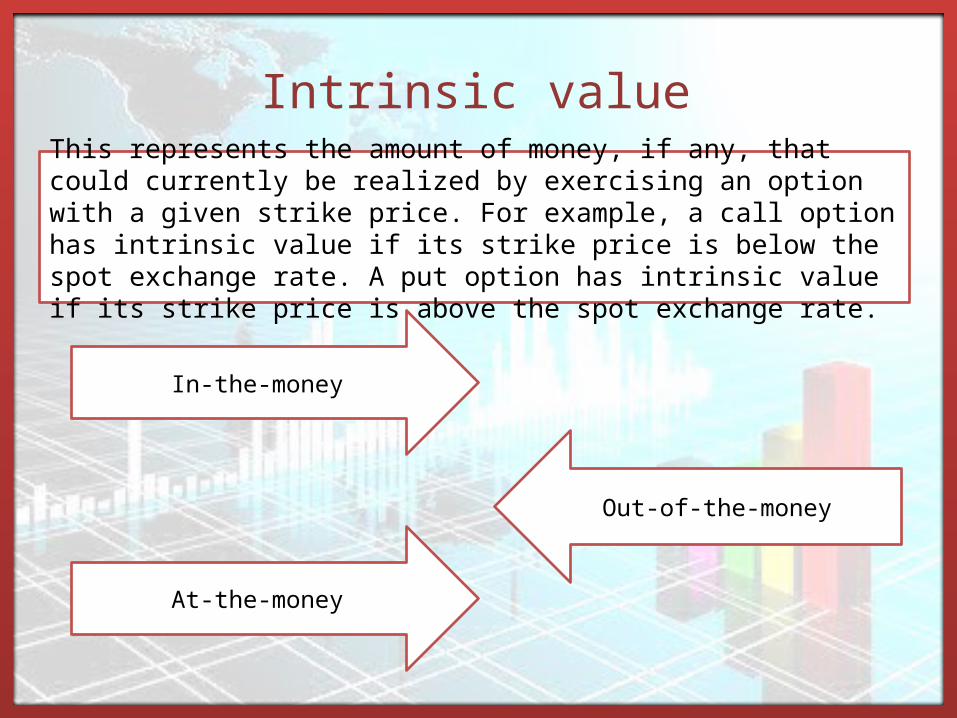

Intrinsic value

This represents the amount of money, if any, that could currently be realized by exercising an option with a given strike price. For example, a call option has intrinsic value if its strike price is below the spot exchange rate. A put option has intrinsic value if its strike price is above the spot exchange rate.

In-the-money

Out-of-the-money

At-the-money

Strategies using options1. Buy Call

Strategy Payoffs When to use

Bullish: Buy call option

Profit: when USD/INR goes up and option exercisedLoss: when USD/INR does not go up and option expires unexercised

Very bullish on USD

2. Sell or put

Strategy Payoffs When to use

Bullish: Sell put option

Profit: when USD/INR does not go down and option expires unexercisedLoss: when USD/INR goes down and option is exercised

Not bearish on USD

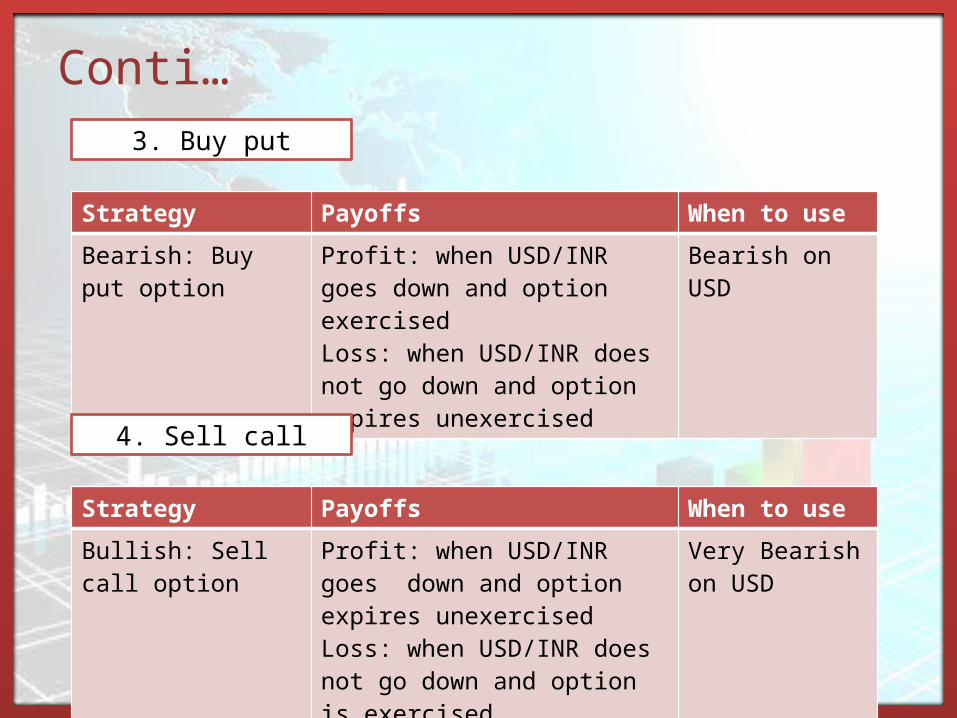

3. Buy put

Strategy Payoffs When to use

Bearish: Buy put option

Profit: when USD/INR goes down and option exercisedLoss: when USD/INR does not go down and option expires unexercised

Bearish on USD

4. Sell call

Strategy Payoffs When to use

Bullish: Sell call option

Profit: when USD/INR goes down and option expires unexercisedLoss: when USD/INR does not go down and option is exercised

Very Bearish on USD

Conti…

Swaps

Swaps are private agreements between two parties to exchange cash flows in the future according to a prearranged formula. The two commonly used

swaps are:

Interest Rate Swap

Currency Swap

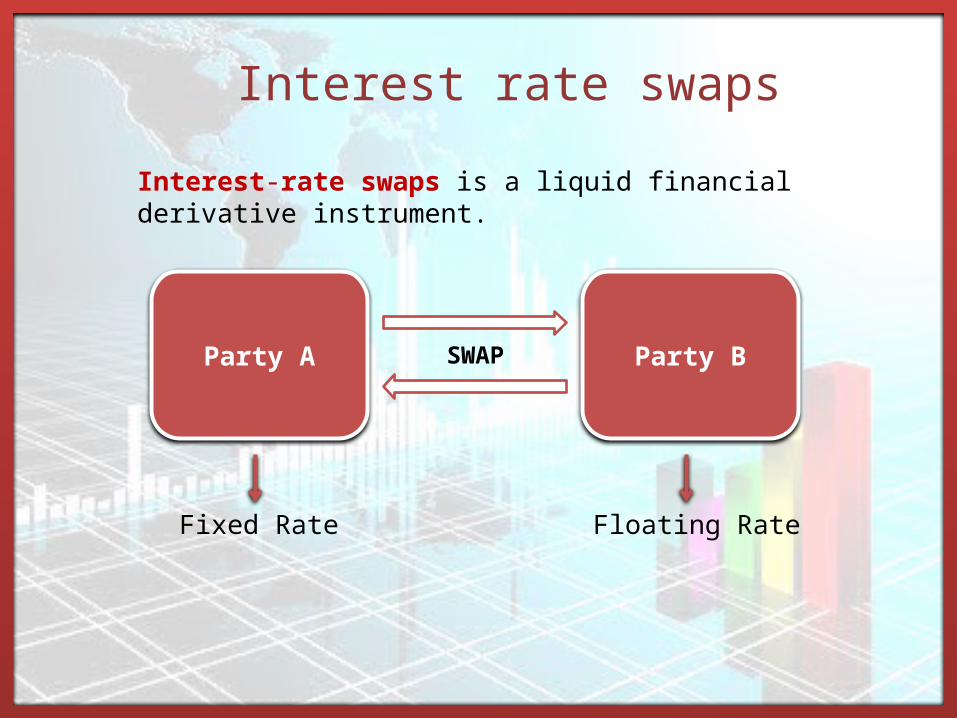

Interest rate swaps

Interest-rate swaps is a liquid financial derivative instrument.

Party A Party B

Fixed Rate Floating Rate

SWAP

Video

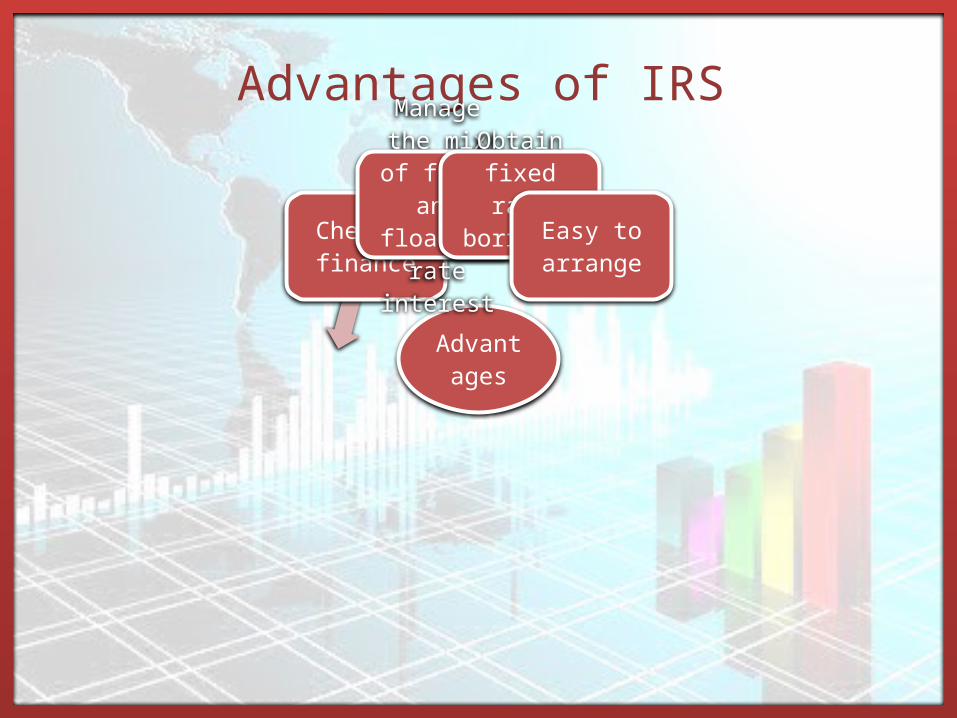

Advantages of IRS

Advantages

Cheaper finance

Manage the mix of fixed and floating rate interest

Obtain fixed rate

borrowingEasy to arrange

DISADVANTAGES OF IRS

Disadvantages

Single currencyMarket risk

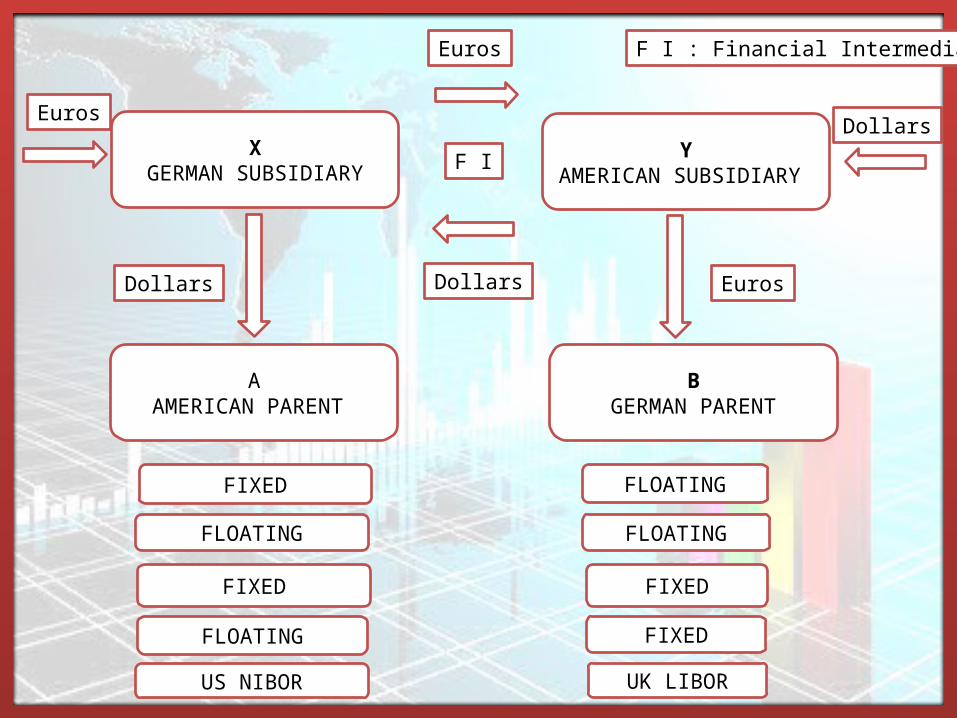

Currency Swap

Currency Swap is a contract to exchange cash flows in one currency (Euro) for cash flows

in another currency (Dollar) over a fixed period of time at predetermined exchange &

interest rates.

XGERMAN SUBSIDIARY

BGERMAN PARENT

YAMERICAN SUBSIDIARY

AAMERICAN PARENT

Euros

Euros

Dollars

DollarsDollars Euros

FIXED

FLOATING

FIXED

FLOATING FIXED

FIXED

FLOATING

FLOATING

US NIBOR UK LIBOR

F I

F I : Financial Intermediary

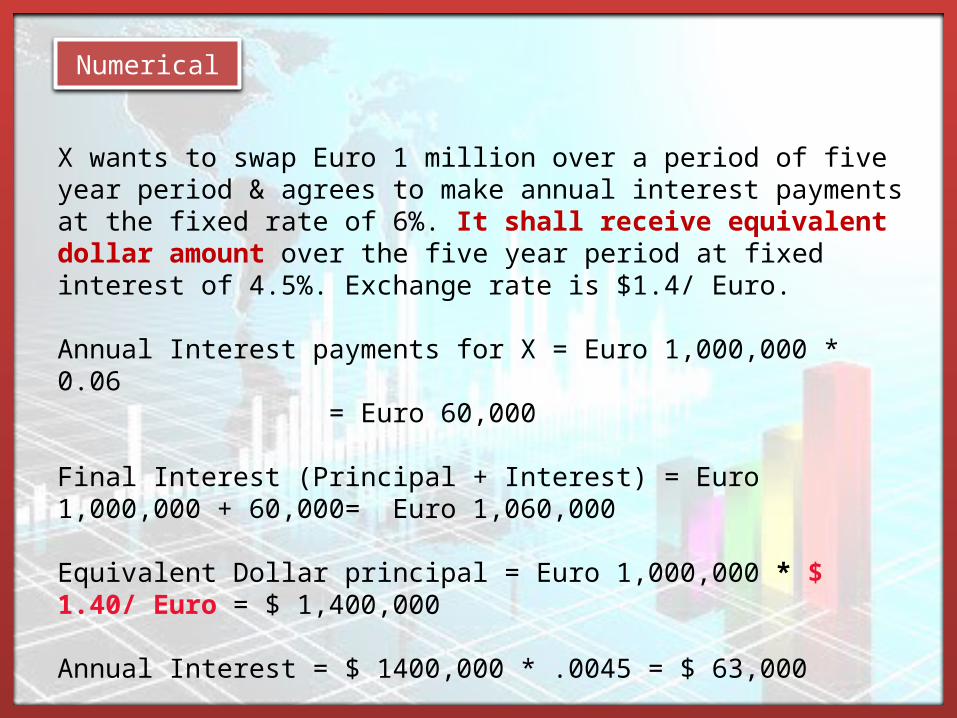

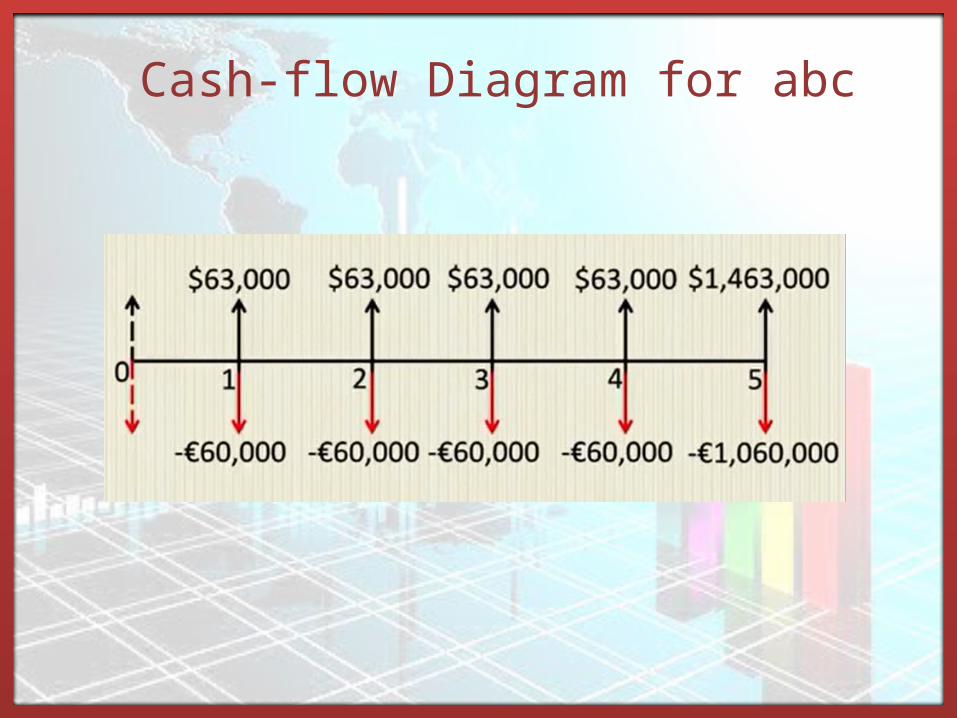

X wants to swap Euro 1 million over a period of five year period & agrees to make annual interest payments at the fixed rate of 6%. It shall receive equivalent dollar amount over the five year period at fixed interest of 4.5%. Exchange rate is $1.4/ Euro.

Annual Interest payments for X = Euro 1,000,000 * 0.06 = Euro 60,000

Final Interest (Principal + Interest) = Euro 1,000,000 + 60,000= Euro 1,060,000

Equivalent Dollar principal = Euro 1,000,000 * $ 1.40/ Euro = $ 1,400,000

Annual Interest = $ 1400,000 * .0045 = $ 63,000

Final Receipt = $63,000 + $ 1,400,000 = $ 1,463,000

Numerical

Cash-flow Diagram for abc

In case after entering into swap agreement a company wants to exit the swap, they can exit by settling the contract orderly using the process of unwinding.

Unwinding :

Requires discounting both the cash flows at the new interest rates that exist at the time of unwinding

NPV in one currency is converted to other currency with the new exchange rate to determine settlement amount.

UNWINDING SWAP

Interest on 3 year Euro Cash-flow = 7%Interest on 3 year $ Cash-flow = 4%New Exchange Rate = $ 1.35/ Euro

NPV of $ Cash Inflows discounted at 4% = $1,419,425.54

NPV of Euro Cash Outflows discounted at 7% = Euro -973,756.84

PV of Euro Cash Outflows in $ = Euro -973,756.84 * $1.35/ Euro = $ 1,314,571.73

Thus, Settlement amount = $1,419,425.54 - $ 1,314,571.73 = $104,853.91

Numerical

Credit default swaps allow one party to "buy" protection from another party for losses that might be incurred as a result of default by a specified reference credit (or credits).

Credit Default Swaps

Example

Suppose Bank A buys a bond which issued by a Steel Company. To hedge the default of Steel Company:Bank A buys a credit default swap from Insurance Company C.Bank A pays a fixed periodic payments to C, in exchange for default protection.

Exhibit

Steel companyReference Asset

Bank A BuyerInsurance Company CSeller

Premium Fee

Credit Event

Contingent payment on

Credit Risk

A credit-linked note (CLN) is essentially a funded CDS, which transfers credit risk from the note issuer to the investor.

Credit Linked Note

·If no event : issuer repays investor scheduled principal + interest (no need for protection any more)·If credit event : issuer can withhold interest and if necessary part of principalFrom protection buyer : equivalent to issue normal bond + buy credit protection(Par value of note = max payout on the CDS)From protection seller : knowing max amount to pay BUT bears credit risk of the issuer

Exhibit

THANKYOU