Embed Size (px)

Citation preview

Denbury.com | NYSE: DNR

Corporate Presentation June 2014

Click to edit Master title style

Denbury.com | NYSE: DNR

Click to edit title style

2

The data contained in this presentation that are not historical facts are forward-looking statements that involve a number of risks and

uncertainties. Such statements may relate to, among other things: long-term strategy; anticipated levels of future dividends and rate of

dividend growth; forecasts of capital expenditures, drilling activity and development activities; timing of carbon dioxide (CO2) injections

and initial production response to such tertiary flooding projects; estimated timing of pipeline construction or completion or the cost

thereof; dates of completion of to-be-constructed industrial plants and their first date of capture of anthropogenic CO2; estimates of costs,

forecasted production rates or peak production rates and the growth thereof; estimates of hydrocarbon reserve quantities and values,

CO2 reserves, helium reserves, future hydrocarbon prices or assumptions; future cash flows or uses of cash, availability of capital or

borrowing capacity; rates of return and overall economics; estimates of potential or recoverable reserves and anticipated production

growth rates in our CO2 models; estimated production and capital expenditures for full-year 2014 and periods beyond; and availability and

cost of equipment and services. These forward-looking statements are generally accompanied by words such as “estimated”,

“preliminary”, “projected”, “potential”, “anticipated”, “forecasted”, “expected”, “assume” or other words that convey the uncertainty of future

events or outcomes. These statements are based on management’s current plans and assumptions and are subject to a number of risks

and uncertainties as further outlined in our most recent Form 10-K and Form 10-Q filed with the SEC. Therefore, actual results may differ

materially from the expectations, estimates or assumptions expressed in or implied by any forward-looking statement herein made by or

on behalf of the Company.

Cautionary Note to U.S. Investors – Current SEC rules regarding oil and gas reserve information allow oil and gas companies to disclose

in filings with the SEC not only proved reserves, but also probable and possible reserves that meet the SEC’s definitions of such terms.

We disclose only proved reserves in our filings with the SEC. Denbury’s proved reserves as of December 31, 2013 were estimated by

DeGolyer & MacNaughton, an independent petroleum engineering firm. In this presentation, we make reference to probable and possible

reserves, some of which have been estimated by our independent engineers and some of which have been estimated by Denbury’s

internal staff of engineers. In this presentation, we also refer to estimates of original oil in place, resource or reserves “potential”, barrels

recoverable, or other descriptions of volumes potentially recoverable, which in addition to reserves generally classifiable as probable and

possible (2P and 3P reserves), include estimates of reserves that do not rise to the standards for possible reserves, and which SEC

guidelines strictly prohibit us from including in filings with the SEC. These estimates, as well as the estimates of probable and possible

reserves, are by their nature more speculative than estimates of proved reserves and are subject to greater uncertainties, and accordingly

the likelihood of recovering those reserves is subject to substantially greater risk.

About Forward-Looking Statements

Click to edit Master title style

Denbury.com | NYSE: DNR

Click to edit title style A Different Kind of Oil Company

3

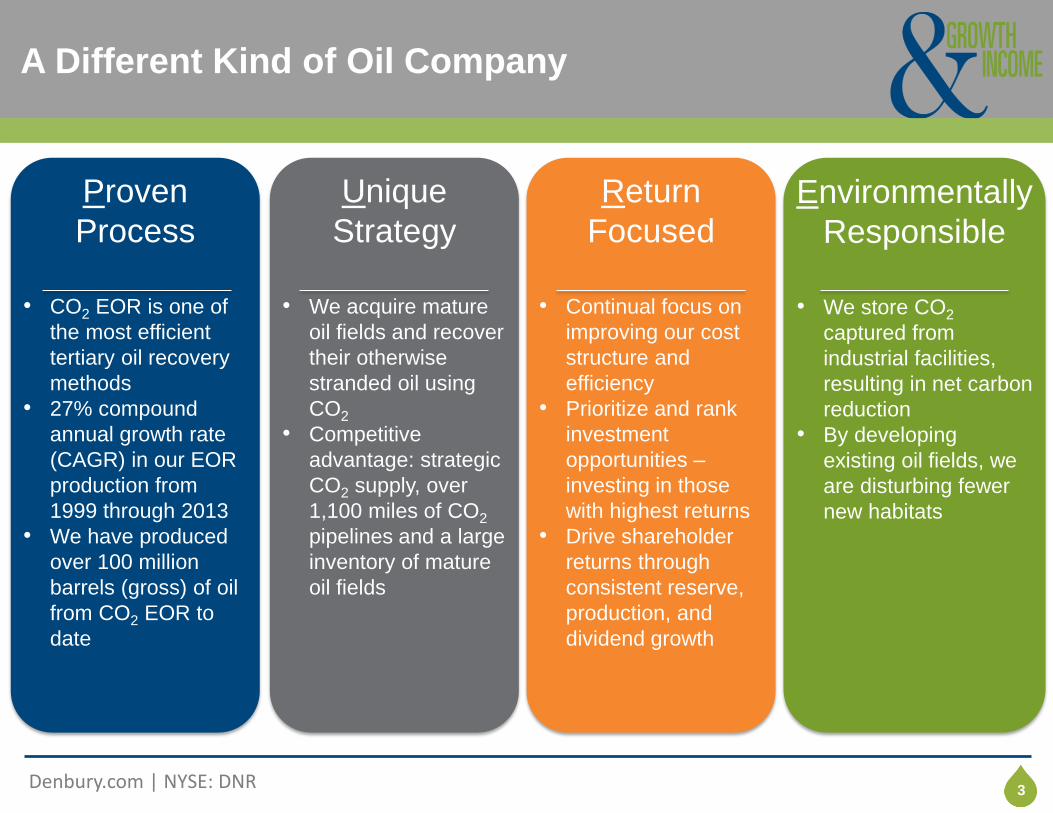

Proven

Process

• CO2 EOR is one of

the most efficient

tertiary oil recovery

methods

• 27% compound

annual growth rate

(CAGR) in our EOR

production from

1999 through 2013

• We have produced

over 100 million

barrels (gross) of oil

from CO2 EOR to

date

Unique

Strategy

• We acquire mature

oil fields and recover

their otherwise

stranded oil using

CO2

• Competitive

advantage: strategic

CO2 supply, over

1,100 miles of CO2

pipelines and a large

inventory of mature

oil fields

Return

Focused

• Continual focus on

improving our cost

structure and

efficiency

• Prioritize and rank

investment

opportunities –

investing in those

with highest returns

• Drive shareholder

returns through

consistent reserve,

production, and

dividend growth

Environmentally

Responsible

• We store CO2

captured from

industrial facilities,

resulting in net carbon

reduction

• By developing

existing oil fields, we

are disturbing fewer

new habitats

Click to edit Master title style

Denbury.com | NYSE: DNR

Click to edit title style Total Return Focus

4

Growth Income

● Estimated 4%-8% organic

production growth through 2020

● Large portfolio of lower-risk,

long-lived assets

● Balanced and disciplined

approach

● Capital flexibility

● Supplement with acquisitions

● Estimated dividend yield(1) of

1.5% for 2014 and 3.3% for 2015

● Stability and sustainability are

key:

Target funding capital

expenditures and dividends

within cash flow

Maintain a healthy balance

sheet

(1) Based on $16.78 share price and $0.25 expected annualized dividend rate in 2014 and $0.55 (mid-point of guidance) expected dividend rate in 2015.

Click to edit Master title style

Denbury.com | NYSE: DNR

Click to edit title style Denbury at a Glance

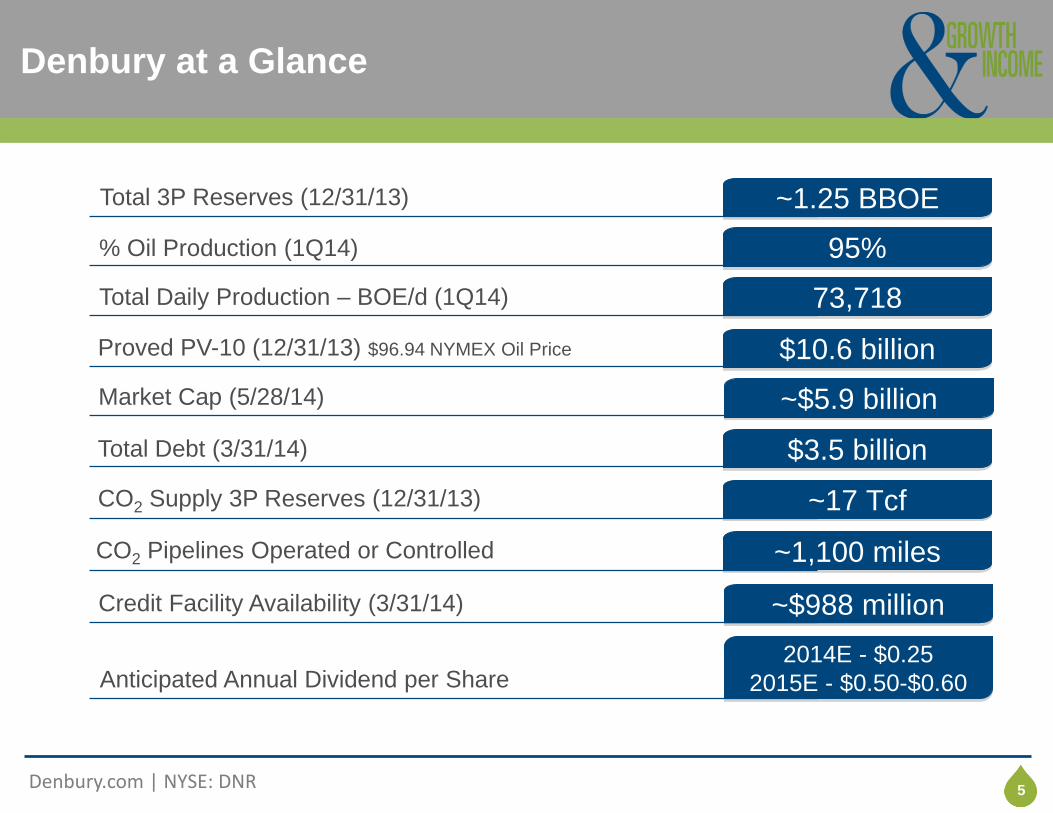

5

~$5.9 billion

73,718

$10.6 billion

~17 Tcf

~1,100 miles

Market Cap (5/28/14)

Total Daily Production – BOE/d (1Q14)

Proved PV-10 (12/31/13) $96.94 NYMEX Oil Price

CO2 Supply 3P Reserves (12/31/13)

CO2 Pipelines Operated or Controlled

~1.25 BBOE

95%

Total 3P Reserves (12/31/13)

% Oil Production (1Q14)

$3.5 billion Total Debt (3/31/14)

~$988 million Credit Facility Availability (3/31/14)

2014E - $0.25

2015E - $0.50-$0.60 Anticipated Annual Dividend per Share

Click to edit Master title style

Denbury.com | NYSE: DNR

Click to edit title style What is CO2 EOR & How Much Oil Does it Recover?

6

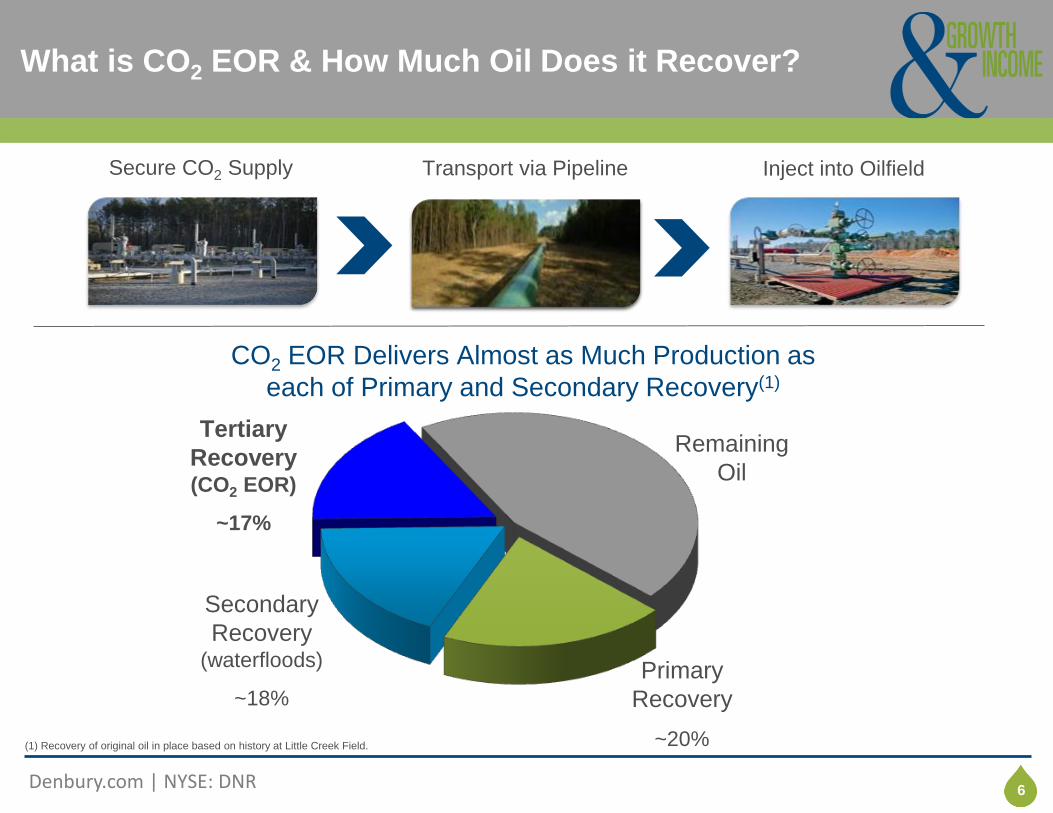

Secure CO2 Supply Transport via Pipeline Inject into Oilfield

CO2 EOR Delivers Almost as Much Production as

each of Primary and Secondary Recovery(1)

Secondary

Recovery (waterfloods)

~18%

Tertiary

Recovery (CO2 EOR)

~17%

Remaining

Oil

Primary

Recovery

~20% (1) Recovery of original oil in place based on history at Little Creek Field.

Click to edit Master title style

Denbury.com | NYSE: DNR

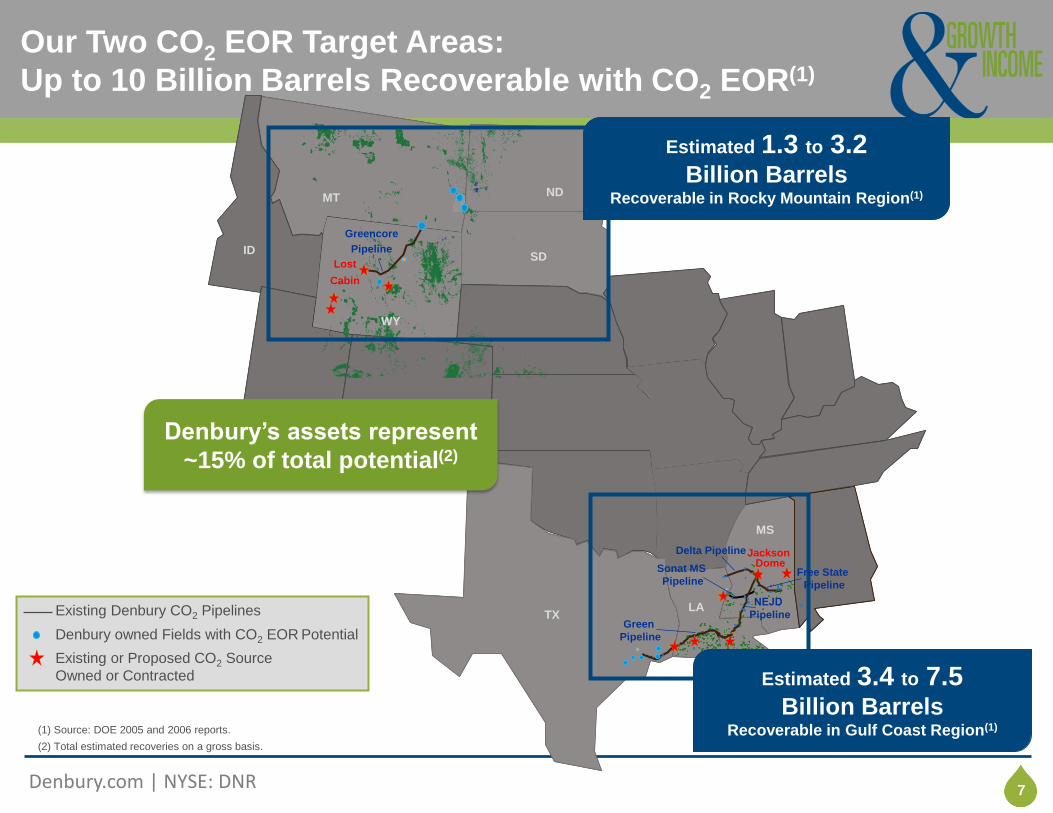

Click to edit title style Our Two CO2 EOR Target Areas:

Up to 10 Billion Barrels Recoverable with CO2 EOR(1)

7 7

Existing or Proposed CO2 Source

Owned or Contracted

Existing Denbury CO2 Pipelines

Denbury owned Fields with CO2 EOR Potential Green

Pipeline

Jackson Dome

Delta Pipeline

Sonat MS

Pipeline

ND

SD Lost

Cabin

ID

MT

WY

TX LA

MS

Greencore

Pipeline

Estimated 3.4 to 7.5 Billion Barrels

Recoverable in Gulf Coast Region(1) (1) Source: DOE 2005 and 2006 reports.

(2) Total estimated recoveries on a gross basis.

Estimated 1.3 to 3.2 Billion Barrels

Recoverable in Rocky Mountain Region(1)

Free State

Pipeline

Denbury’s assets represent

~15% of total potential(2)

Click to edit Master title style

Denbury.com | NYSE: DNR

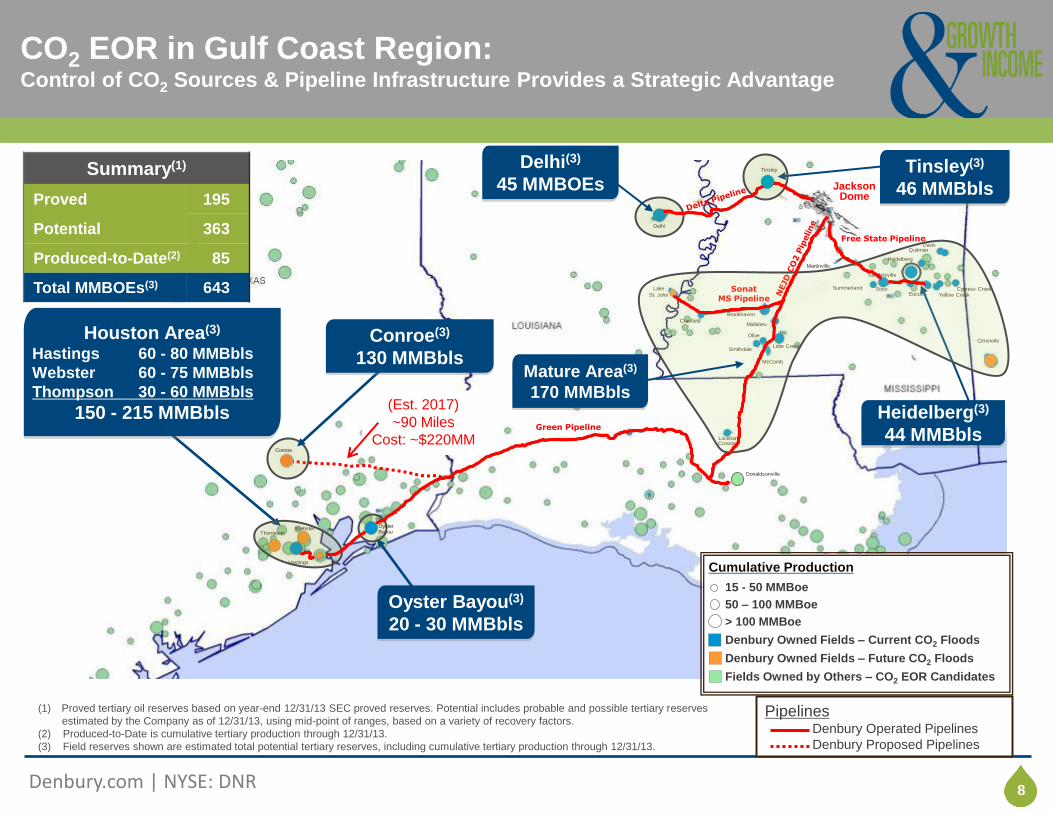

Click to edit title style CO2 EOR in Gulf Coast Region: Control of CO2 Sources & Pipeline Infrastructure Provides a Strategic Advantage

8

(1) Proved tertiary oil reserves based on year-end 12/31/13 SEC proved reserves. Potential includes probable and possible tertiary reserves

estimated by the Company as of 12/31/13, using mid-point of ranges, based on a variety of recovery factors.

(2) Produced-to-Date is cumulative tertiary production through 12/31/13.

(3) Field reserves shown are estimated total potential tertiary reserves, including cumulative tertiary production through 12/31/13.

Jackson Dome

Sonat MS Pipeline

Green Pipeline

Citronelle

(2)

Tinsley

Free State Pipeline

Martinville

Davis Quitman

Heidelberg

Summerland Soso

Sandersville

Eucutta Yellow Creek Cypress Creek

Brookhaven

Mallalieu

Little Creek

Olive

Smithdale

McComb

Donaldsonville

Delhi

Lake

St. John

Cranfield

Lockhart Crossing

Hastings

Conroe

Oyster Bayou

Delhi(3)

45 MMBOEs Tinsley(3)

46 MMBbls

Mature Area(3)

170 MMBbls

Oyster Bayou(3)

20 - 30 MMBbls

Conroe(3)

130 MMBbls

Summary(1)

Proved 195

Potential 363

Produced-to-Date(2) 85

Total MMBOEs(3) 643

15 - 50 MMBoe

50 – 100 MMBoe

> 100 MMBoe

Denbury Owned Fields – Current CO2 Floods

Denbury Owned Fields – Future CO2 Floods

Fields Owned by Others – CO2 EOR Candidates

Cumulative Production

Thompson

Heidelberg(3)

44 MMBbls

Houston Area(3)

Hastings 60 - 80 MMBbls

Webster 60 - 75 MMBbls

Thompson 30 - 60 MMBbls

150 - 215 MMBbls

Webster

(Est. 2017)

~90 Miles

Cost: ~$220MM

Pipelines Denbury Operated Pipelines

Denbury Proposed Pipelines

Click to edit Master title style

Denbury.com | NYSE: DNR

Click to edit title style CO2 EOR in Rocky Mountain Region: Control of CO2 Sources & Pipeline Infrastructure Provides a Strategic Advantage

9

MONTANA

NORTH DAKOTA

SOUTH DAKOTA

WYOMING

Elk Basin

Shute Creek

(XOM)

Lost Cabin

(COP)

DGC Beulah

Riley Ridge

(DNR)

Greencore Pipeline

232 Miles

Bell Creek(4)

40 - 50 MMBbls

Cedar Creek Anticline Area

260 - 290 MMBbls

Grieve Field(4)

6 MMBbls Existing CO2

Pipeline

CO2 Sources

(1) Proved tertiary oil reserves based on year-end 12/31/13 SEC proved reserves. Potential includes probable and possible tertiary reserves estimated by

the Company as of 12/31/13, using approximate mid-points of ranges, based on a variety of recovery factors.

(2) Produced-to-Date is cumulative tertiary production through 12/31/13.

(3) Reported on a gross working interest or 8/8th’s basis, except for overriding royalty interest in LaBarge Field.

(4) Field reserves shown are estimated total potential tertiary reserves, including cumulative tertiary production through 12/31/13.

Existing or Proposed CO2 Source

Owned or Contracted

Hartzog Draw(4)

20 - 30 MMBbls

Summary(1)

Proved 34

Potential 317

Produced-to-Date(2) <1

Total MMBbls 351

(Est. 2019-2020)

~250 Miles

Cost: ~$500MM

Interconnect

(Completed 1Q14)

(Est. 2021)

~130 Miles

Cost: ~$225MM

LaBarge Area

399 BCF Nat Gas

13 BCF Helium

3.3 TCF CO2(3)

Pipelines Denbury Pipelines

Denbury Proposed Pipelines

Pipelines Owned by Others

15 - 50 MMBoe

50 – 100 MMBoe

> 100 MMBoe

Denbury Owned Fields – Current CO2 Floods

Denbury Owned Fields – Future CO2 Floods

Fields Owned by Others – CO2 EOR Candidates

Cumulative Production

Click to edit Master title style

Denbury.com | NYSE: DNR

Click to edit title style

(1) Based on year-end 2012 and 2013 SEC reported proved reserves.

(2) Based on internal estimates, refer to slide 2 for full disclosure relative to forward-looking statements.

More than a Billion Barrels of Oil Potential

10

0

250

500

750

1,000

1,250

1,500

12/31/12Proved

Reserves

12/31/13 Proved

Reserves

+ CO2 EORPotential

+ OtherPotential

Total Potential

MM

BO

E

.....

.....

.....

80%

Oil

90%

Oil 54%

Oil

83%

Oil

100%

Oil

(2) (2)

1,250

409

102

468

680

(1) (1)

=

Click to edit Master title style

Denbury.com | NYSE: DNR

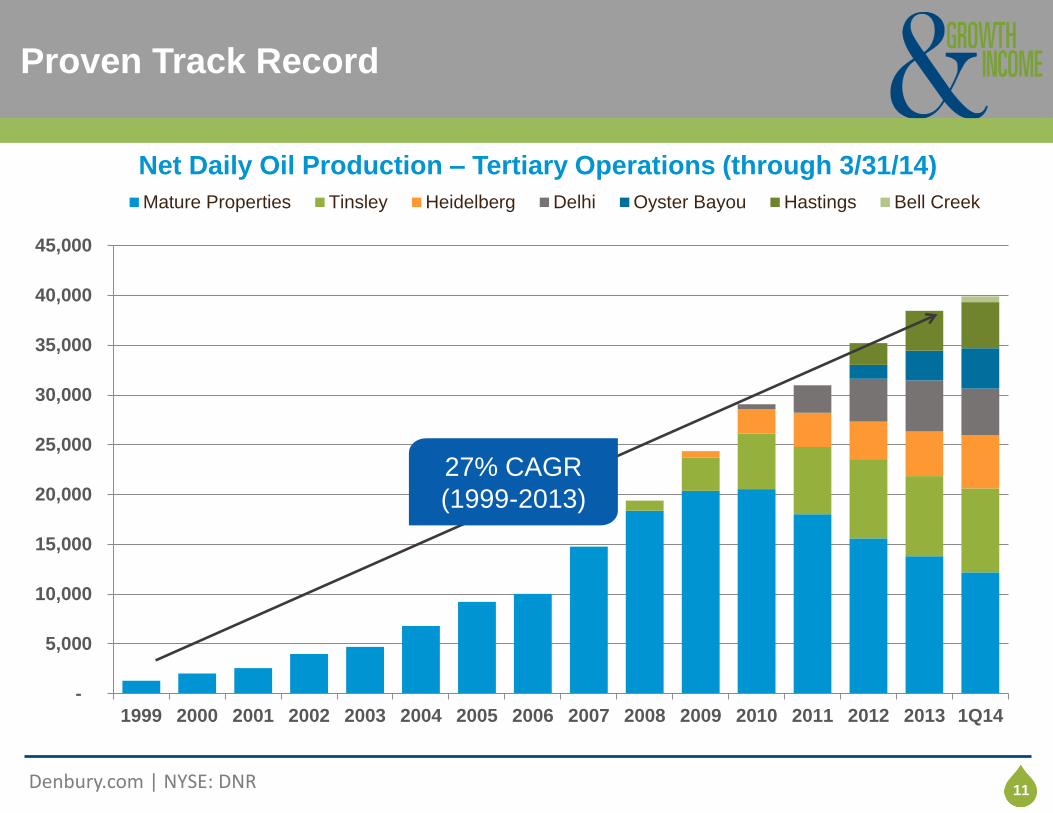

Click to edit title style Proven Track Record

11

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 1Q14

Mature Properties Tinsley Heidelberg Delhi Oyster Bayou Hastings Bell Creek

Net Daily Oil Production – Tertiary Operations (through 3/31/14)

27% CAGR

(1999-2013)

Click to edit Master title style

Denbury.com | NYSE: DNR

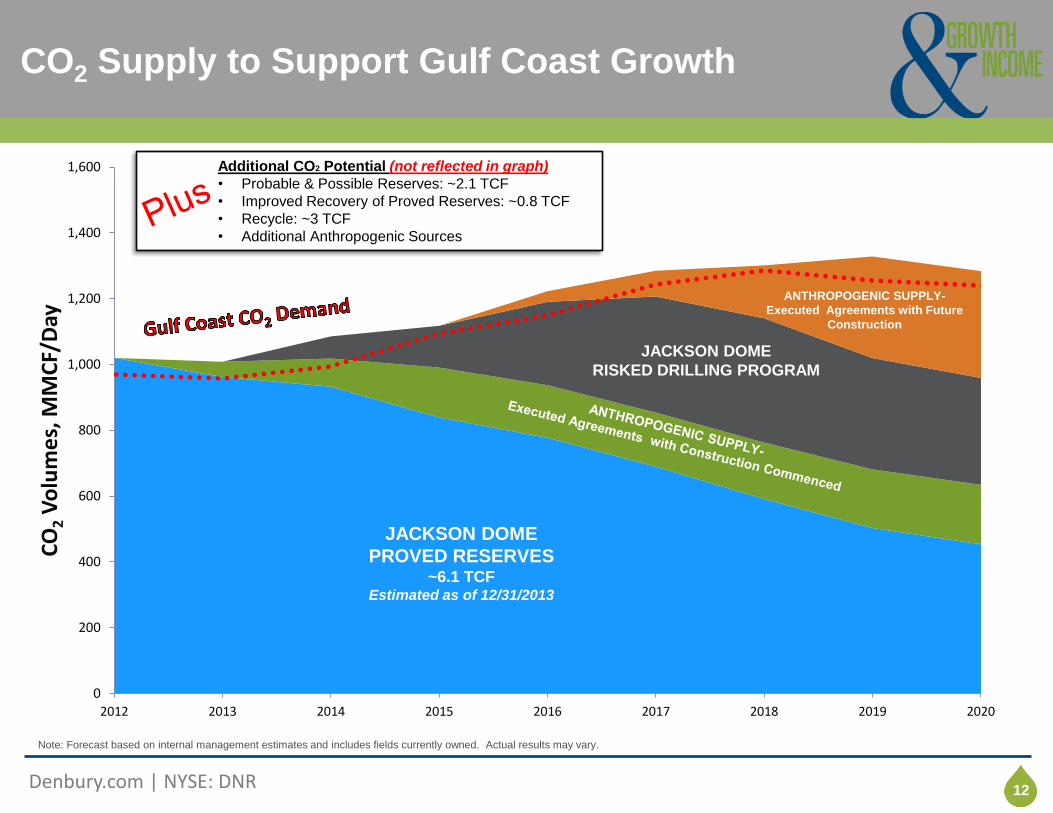

Click to edit title style CO2 Supply to Support Gulf Coast Growth

12

0

200

400

600

800

1,000

1,200

1,400

1,600

2012 2013 2014 2015 2016 2017 2018 2019 2020

CO

2 V

olu

me

s, M

MC

F/D

ay ANTHROPOGENIC SUPPLY-

Executed Agreements with Future

Construction

JACKSON DOME

RISKED DRILLING PROGRAM

JACKSON DOME

PROVED RESERVES ~6.1 TCF

Estimated as of 12/31/2013

Additional CO2 Potential (not reflected in graph)

• Probable & Possible Reserves: ~2.1 TCF

• Improved Recovery of Proved Reserves: ~0.8 TCF

• Recycle: ~3 TCF

• Additional Anthropogenic Sources

Note: Forecast based on internal management estimates and includes fields currently owned. Actual results may vary.

Click to edit Master title style

Denbury.com | NYSE: DNR

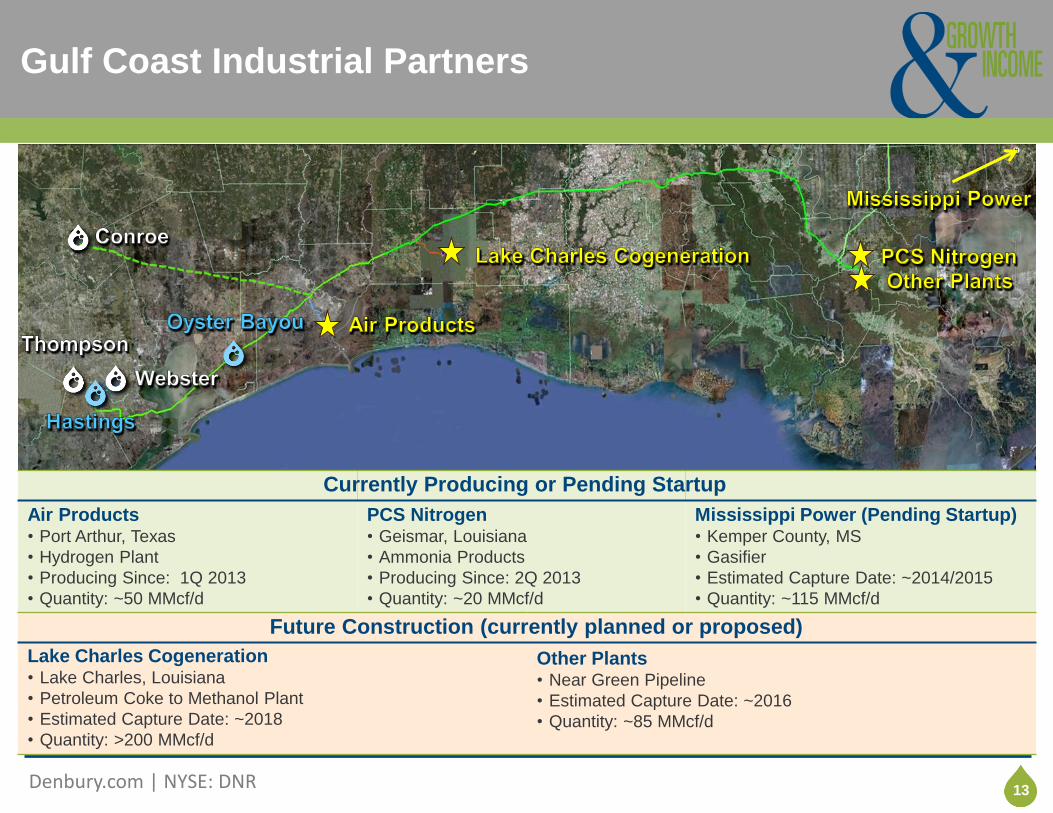

Click to edit title style Gulf Coast Industrial Partners

13 13

Air Products • Port Arthur, Texas

• Hydrogen Plant

• Producing Since: 1Q 2013

• Quantity: ~50 MMcf/d

PCS Nitrogen • Geismar, Louisiana

• Ammonia Products

• Producing Since: 2Q 2013

• Quantity: ~20 MMcf/d

Mississippi Power (Pending Startup) • Kemper County, MS

• Gasifier

• Estimated Capture Date: ~2014/2015

• Quantity: ~115 MMcf/d

Lake Charles Cogeneration

• Lake Charles, Louisiana

• Petroleum Coke to Methanol Plant

• Estimated Capture Date: ~2018

• Quantity: >200 MMcf/d

Other Plants • Near Green Pipeline

• Estimated Capture Date: ~2016

• Quantity: ~85 MMcf/d

Currently Producing or Pending Startup

Future Construction (currently planned or proposed)

Click to edit Master title style

Denbury.com | NYSE: DNR

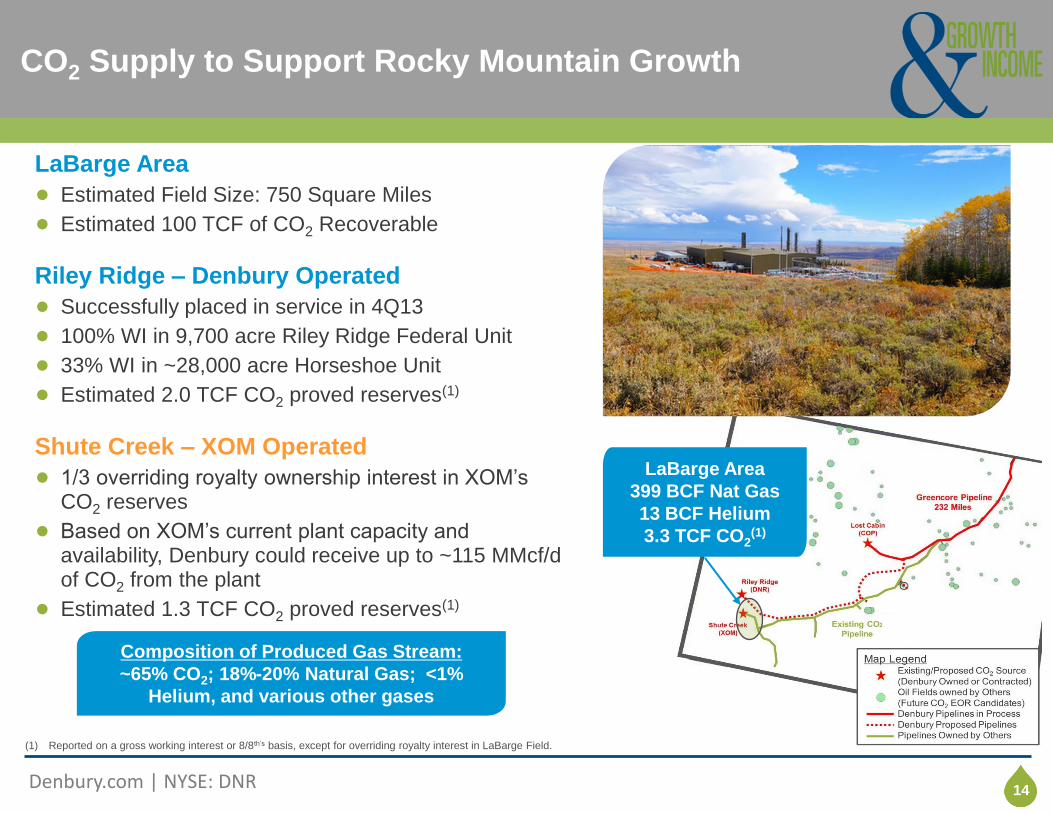

Click to edit title style CO2 Supply to Support Rocky Mountain Growth

14

LaBarge Area

● Estimated Field Size: 750 Square Miles

● Estimated 100 TCF of CO2 Recoverable

Riley Ridge – Denbury Operated

● Successfully placed in service in 4Q13

● 100% WI in 9,700 acre Riley Ridge Federal Unit

● 33% WI in ~28,000 acre Horseshoe Unit

● Estimated 2.0 TCF CO2 proved reserves(1)

Shute Creek – XOM Operated

● 1/3 overriding royalty ownership interest in XOM’s CO2 reserves

● Based on XOM’s current plant capacity and availability, Denbury could receive up to ~115 MMcf/d of CO2 from the plant

● Estimated 1.3 TCF CO2 proved reserves(1)

LaBarge Area

399 BCF Nat Gas

13 BCF Helium

3.3 TCF CO2(1)

Composition of Produced Gas Stream:

~65% CO2; 18%-20% Natural Gas; <1%

Helium, and various other gases

(1) Reported on a gross working interest or 8/8th’s basis, except for overriding royalty interest in LaBarge Field.

Click to edit Master title style

Denbury.com | NYSE: DNR

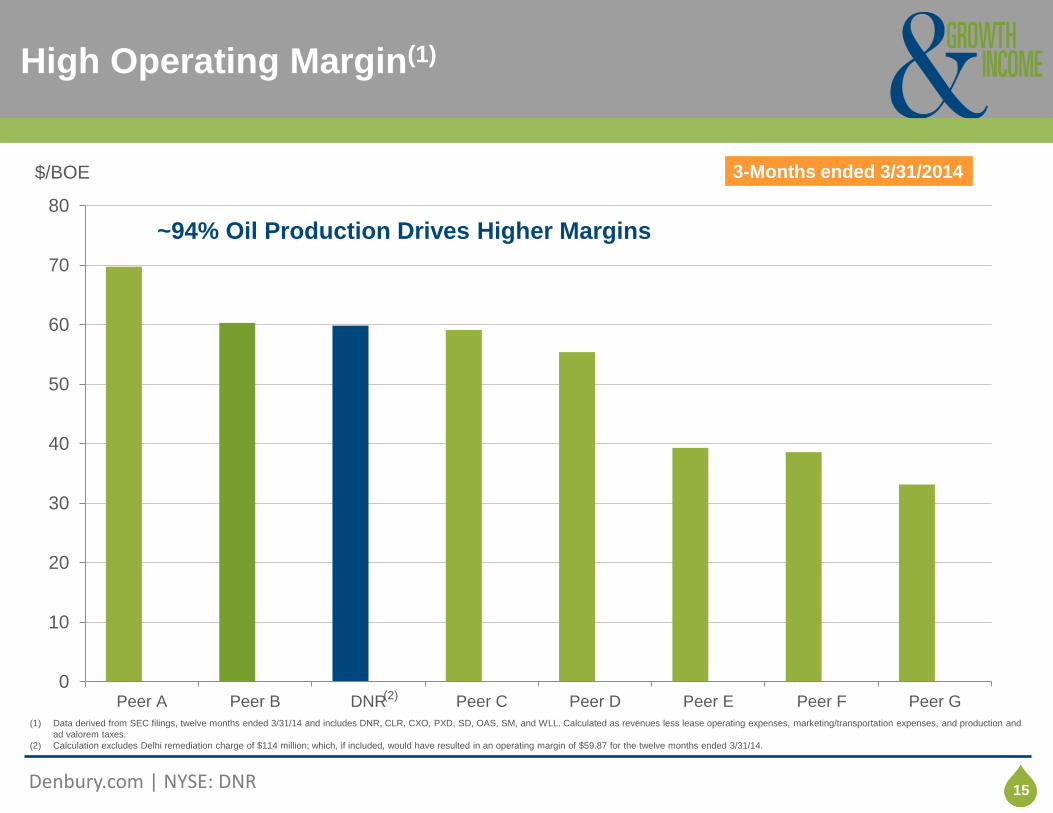

Click to edit title style High Operating Margin(1)

15

0

10

20

30

40

50

60

70

80

Peer A Peer B DNR Peer C Peer D Peer E Peer F Peer G

$/BOE

~94% Oil Production Drives Higher Margins

3-Months ended 3/31/2014

(2) 1

5 (1) Data derived from SEC filings, twelve months ended 3/31/14 and includes DNR, CLR, CXO, PXD, SD, OAS, SM, and WLL. Calculated as revenues less lease operating expenses, marketing/transportation expenses, and production and

ad valorem taxes.

(2) Calculation excludes Delhi remediation charge of $114 million; which, if included, would have resulted in an operating margin of $59.87 for the twelve months ended 3/31/14.

Click to edit Master title style

Denbury.com | NYSE: DNR

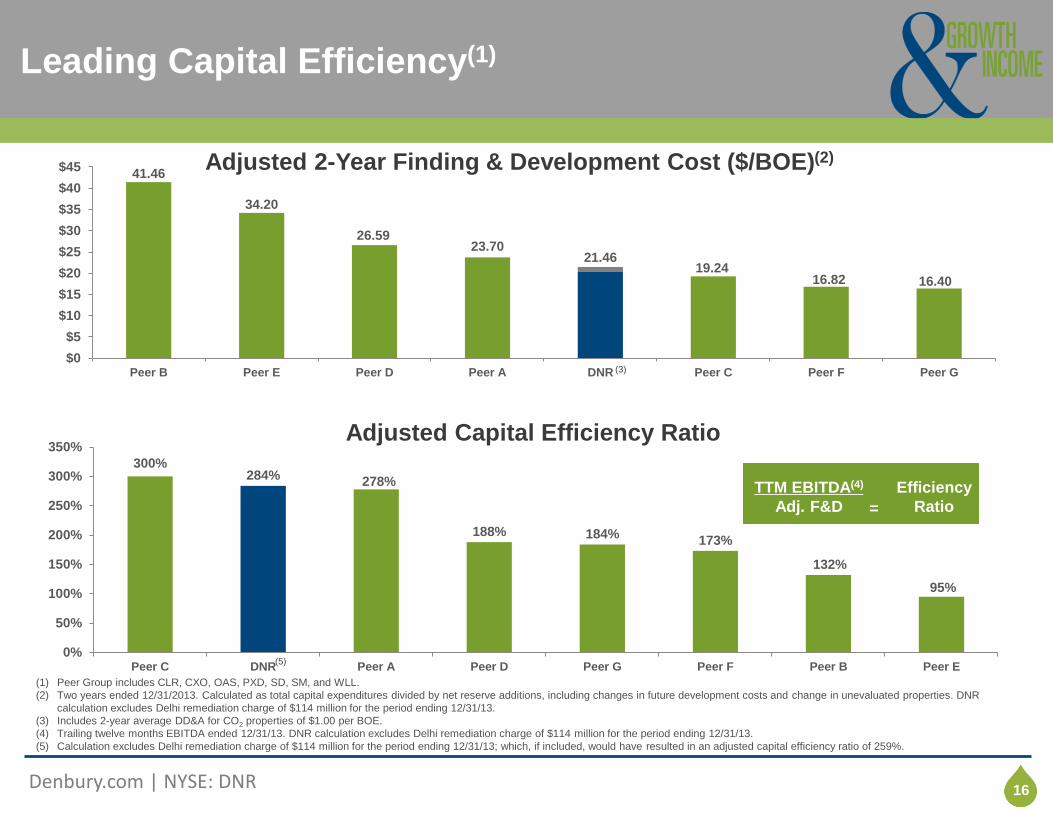

Click to edit title style Leading Capital Efficiency(1)

16

16 16

(1) Peer Group includes CLR, CXO, OAS, PXD, SD, SM, and WLL.

(2) Two years ended 12/31/2013. Calculated as total capital expenditures divided by net reserve additions, including changes in future development costs and change in unevaluated properties. DNR

calculation excludes Delhi remediation charge of $114 million for the period ending 12/31/13.

(3) Includes 2-year average DD&A for CO2 properties of $1.00 per BOE.

(4) Trailing twelve months EBITDA ended 12/31/13. DNR calculation excludes Delhi remediation charge of $114 million for the period ending 12/31/13.

(5) Calculation excludes Delhi remediation charge of $114 million for the period ending 12/31/13; which, if included, would have resulted in an adjusted capital efficiency ratio of 259%.

300% 284% 278%

188% 184% 173%

132%

95%

0%

50%

100%

150%

200%

250%

300%

350%

Peer C DNR Peer A Peer D Peer G Peer F Peer B Peer E

Adjusted Capital Efficiency Ratio

41.46

34.20

26.59 23.70

21.46 19.24

16.82 16.40

$0

$5

$10

$15

$20

$25

$30

$35

$40

$45

Peer B Peer E Peer D Peer A DNR Peer C Peer F Peer G

Adjusted 2-Year Finding & Development Cost ($/BOE)(2)

(3)

TTM EBITDA(4)

Adj. F&D

Efficiency

Ratio =

(5)

Click to edit Master title style

Denbury.com | NYSE: DNR

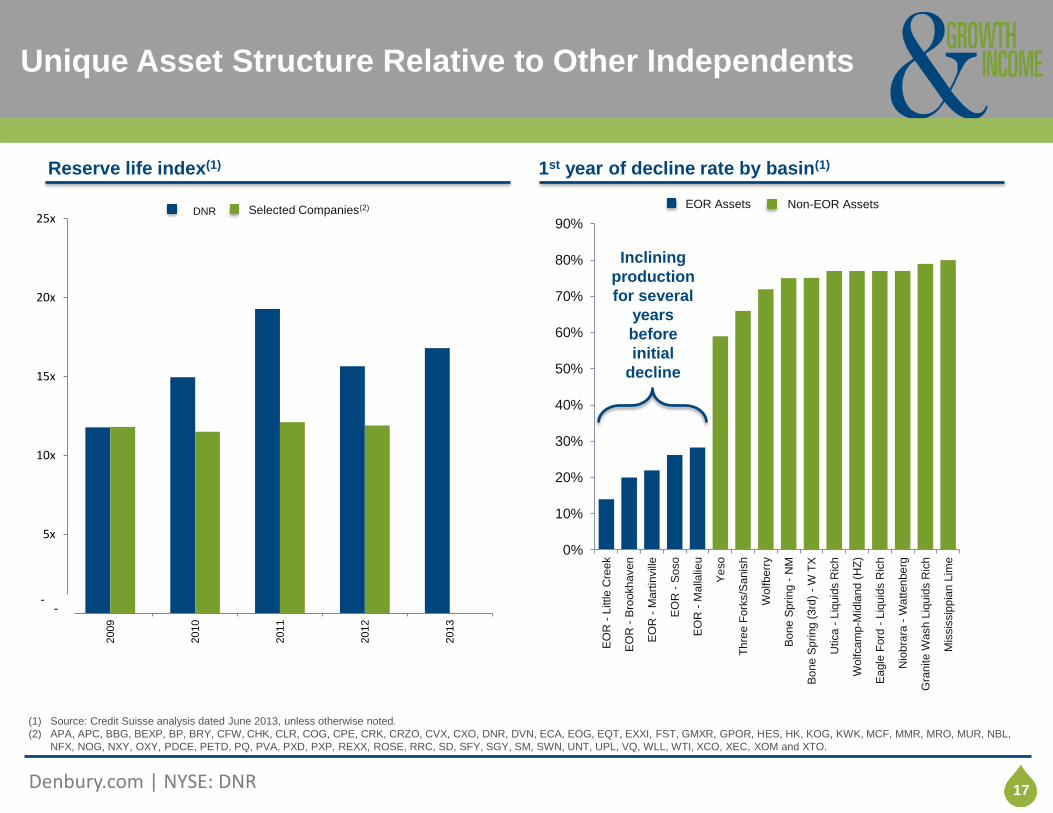

Click to edit title style Unique Asset Structure Relative to Other Independents

17

(1) Source: Credit Suisse analysis dated June 2013, unless otherwise noted.

(2) APA, APC, BBG, BEXP, BP, BRY, CFW, CHK, CLR, COG, CPE, CRK, CRZO, CVX, CXO, DNR, DVN, ECA, EOG, EQT, EXXI, FST, GMXR, GPOR, HES, HK, KOG, KWK, MCF, MMR, MRO, MUR, NBL,

NFX, NOG, NXY, OXY, PDCE, PETD, PQ, PVA, PXD, PXP, REXX, ROSE, RRC, SD, SFY, SGY, SM, SWN, UNT, UPL, VQ, WLL, WTI, XCO, XEC, XOM and XTO.

Reserve life index(1) 1st year of decline rate by basin(1)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

EO

R -

Little C

reek

EO

R -

Bro

okh

aven

EO

R -

Ma

rtin

vill

e

EO

R -

Soso

EO

R -

Ma

llalie

u

Ye

so

Th

ree F

ork

s/S

anis

h

Wolfberr

y

Bo

ne S

pring

- N

M

Bo

ne S

pring

(3rd

) -

W T

X

Utica -

Liq

uid

s R

ich

Wolfcam

p-M

idla

nd (

HZ

)

Ea

gle

Ford

- L

iquid

s R

ich

Nio

bra

ra -

Wa

tten

be

rg

Gra

nite W

ash L

iquid

s R

ich

Mis

sis

sip

pia

n L

ime

EOR Assets Non-EOR Assets

Inclining

production

for several

years

before

initial

decline

DNR Selected Companies(2)

x

5x

10x

15x

20x

25x

2009

2010

2011

2012

2013

- -

Click to edit Master title style

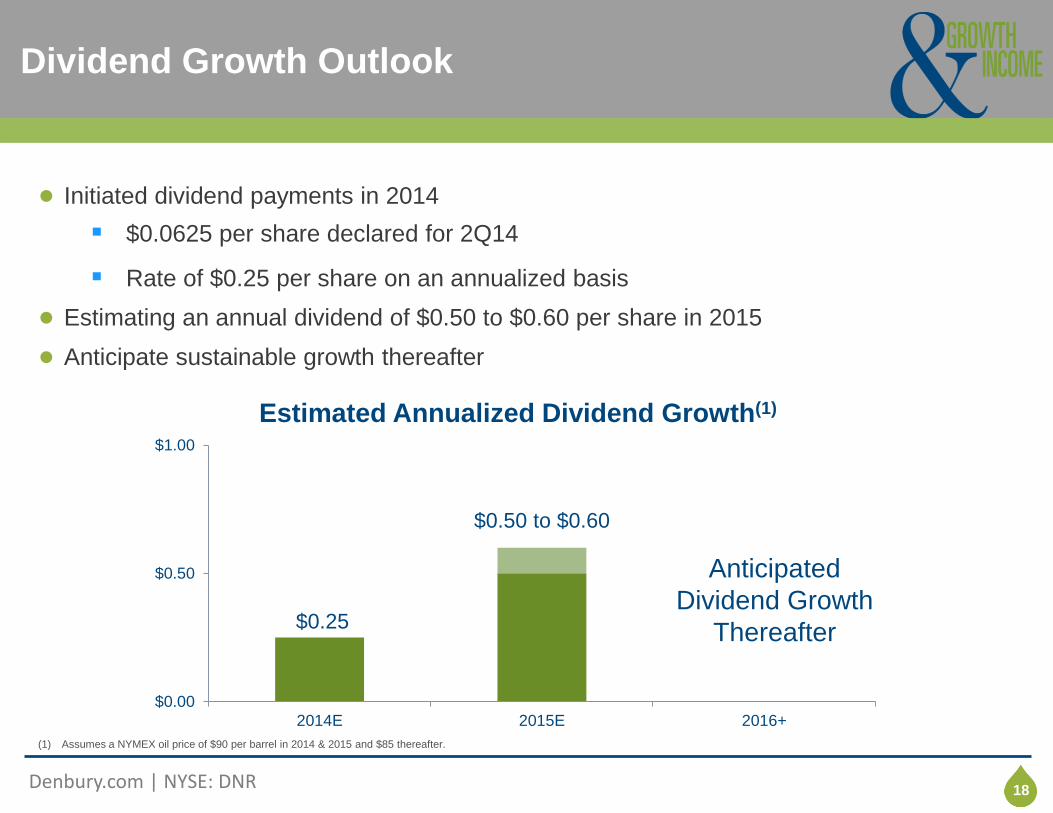

Denbury.com | NYSE: DNR

Click to edit title style Dividend Growth Outlook

18

● Initiated dividend payments in 2014

$0.0625 per share declared for 2Q14

Rate of $0.25 per share on an annualized basis

● Estimating an annual dividend of $0.50 to $0.60 per share in 2015

● Anticipate sustainable growth thereafter

$0.25

$0.50 to $0.60

$0.00

$0.50

$1.00

2014E 2015E 2016+

Estimated Annualized Dividend Growth(1)

Anticipated

Dividend Growth

Thereafter

(1) Assumes a NYMEX oil price of $90 per barrel in 2014 & 2015 and $85 thereafter.

Click to edit Master title style

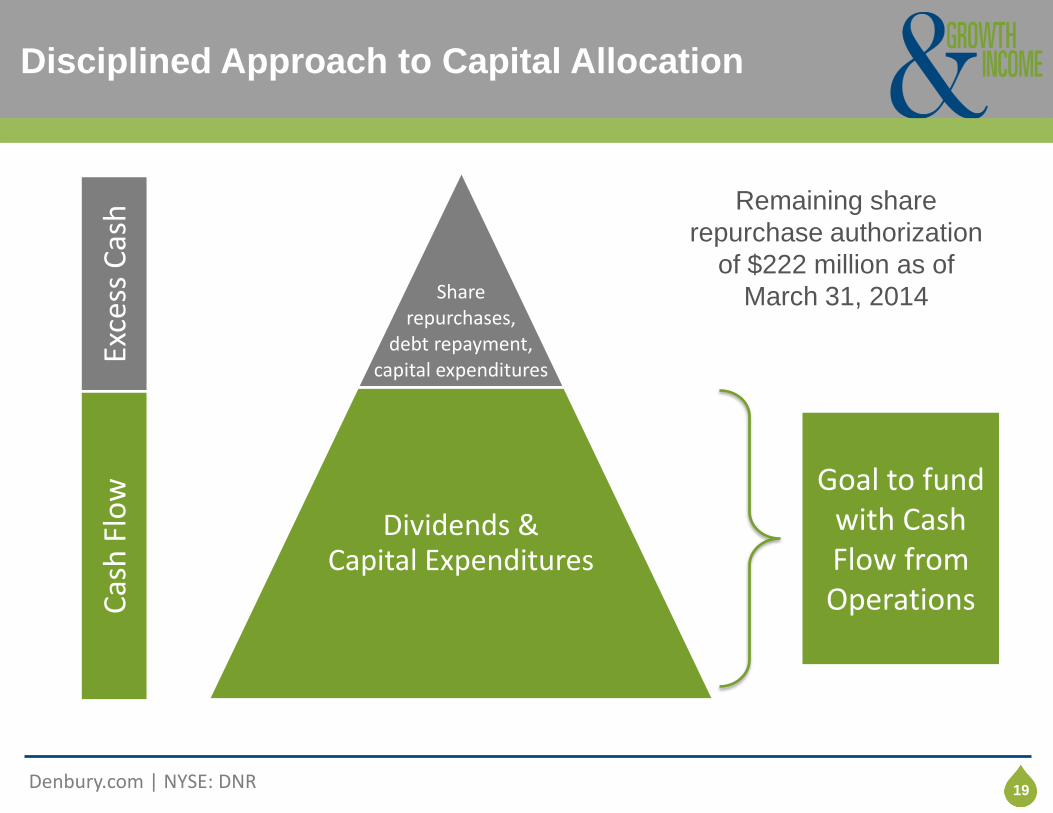

Denbury.com | NYSE: DNR

Click to edit title style Disciplined Approach to Capital Allocation

19

Share

repurchases, debt repayment,

capital expenditures

Dividends & Capital Expenditures

Cas

h F

low

Ex

cess

Cas

h

Goal to fund with Cash Flow from Operations

Remaining share

repurchase authorization

of $222 million as of

March 31, 2014

Click to edit Master title style

Denbury.com | NYSE: DNR

Click to edit title style

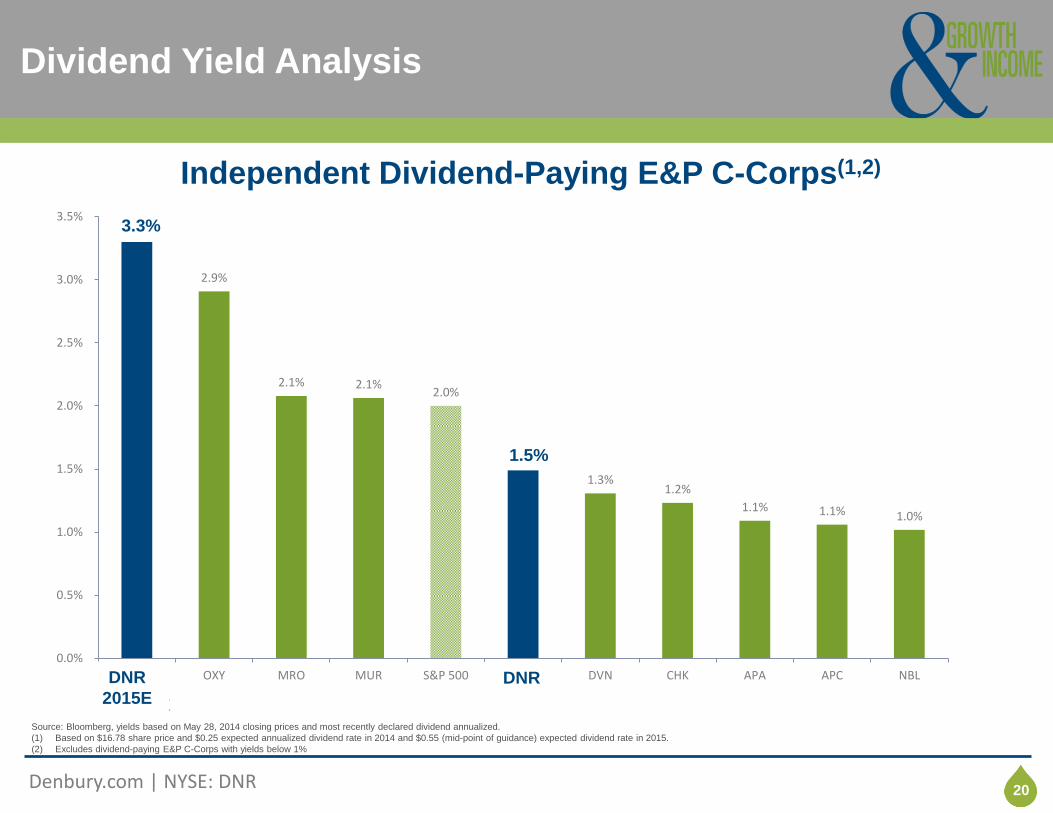

3.3%

2.9%

2.1% 2.1% 2.0%

1.5%

1.3% 1.2%

1.1% 1.1% 1.0%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

DNR 2015 OXY MRO MUR S&P 500 DNR DVN CHK APA APC NBL

Dividend Yield Analysis

20

Independent Dividend-Paying E&P C-Corps(1,2)

Source: Bloomberg, yields based on May 28, 2014 closing prices and most recently declared dividend annualized.

(1) Based on $16.78 share price and $0.25 expected annualized dividend rate in 2014 and $0.55 (mid-point of guidance) expected dividend rate in 2015.

(2) Excludes dividend-paying E&P C-Corps with yields below 1%

DNR

2015E

1.5%

3.3%

DNR

2015E

DNR

Click to edit Master title style

Denbury.com | NYSE: DNR

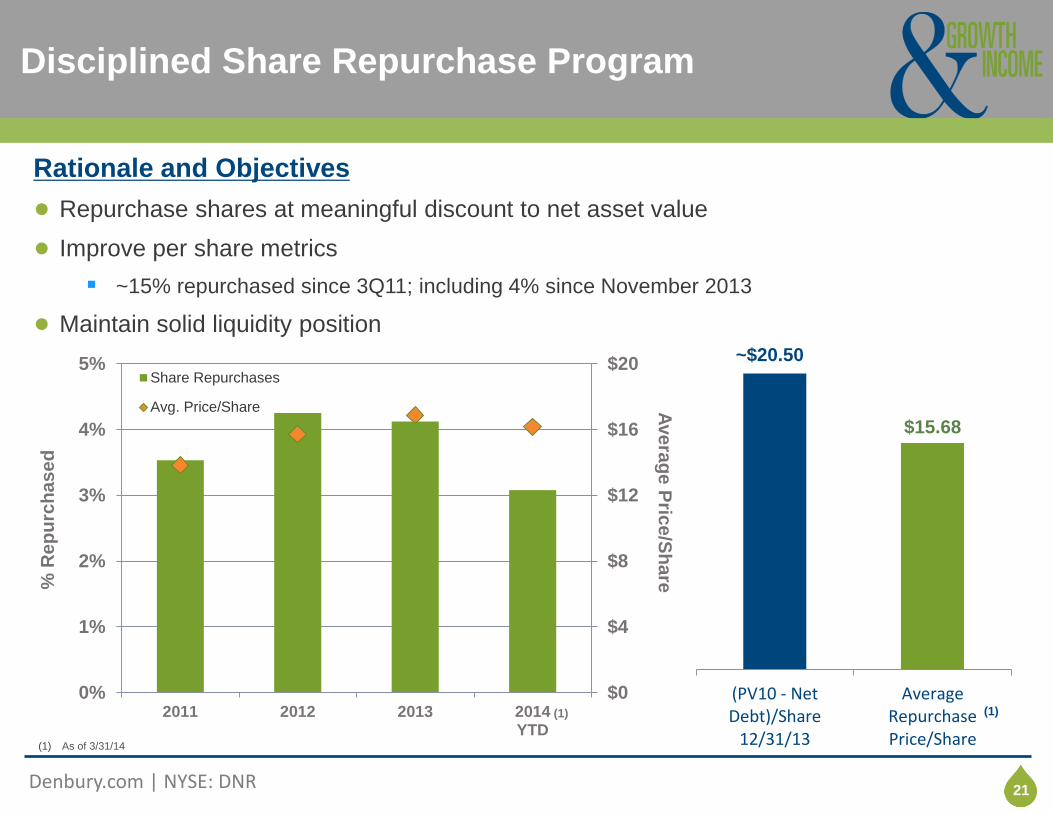

Click to edit title style Disciplined Share Repurchase Program

21

$15.68

(PV10 - NetDebt)/Share

12/31/13

AverageRepurchasePrice/Share

~$20.50

(1) As of 3/31/14

$0

$4

$8

$12

$16

$20

0%

1%

2%

3%

4%

5%

2011 2012 2013 2014YTD

Ave

rag

e P

rice

/Sh

are

% R

ep

urc

ha

se

d

Share Repurchases

Avg. Price/Share

(1) (1)

Rationale and Objectives

● Repurchase shares at meaningful discount to net asset value

● Improve per share metrics

~15% repurchased since 3Q11; including 4% since November 2013

● Maintain solid liquidity position

Click to edit Master title style

Denbury.com | NYSE: DNR

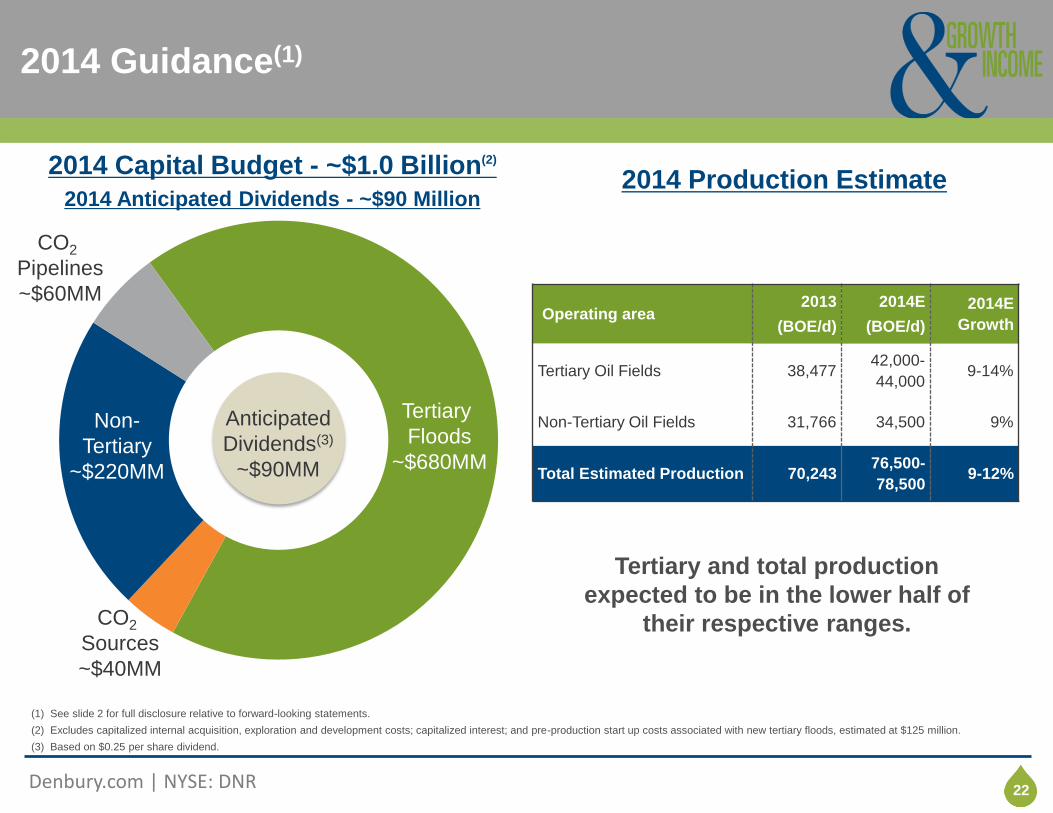

Click to edit title style 2014 Guidance(1)

22

Operating area 2013

(BOE/d)

2014E

(BOE/d)

2014E

Growth

Tertiary Oil Fields 38,477 42,000-

44,000 9-14%

Non-Tertiary Oil Fields 31,766 34,500 9%

Total Estimated Production 70,243 76,500-

78,500 9-12%

2014 Production Estimate

(1) See slide 2 for full disclosure relative to forward-looking statements.

(2) Excludes capitalized internal acquisition, exploration and development costs; capitalized interest; and pre-production start up costs associated with new tertiary floods, estimated at $125 million.

(3) Based on $0.25 per share dividend.

Tertiary

Floods

~$680MM

Non-

Tertiary

~$220MM

2014 Capital Budget - ~$1.0 Billion(2)

2014 Anticipated Dividends - ~$90 Million

CO2

Pipelines

~$60MM

CO2

Sources

~$40MM

Anticipated

Dividends(3)

~$90MM

Tertiary and total production

expected to be in the lower half of

their respective ranges.

Click to edit Master title style

Denbury.com | NYSE: DNR

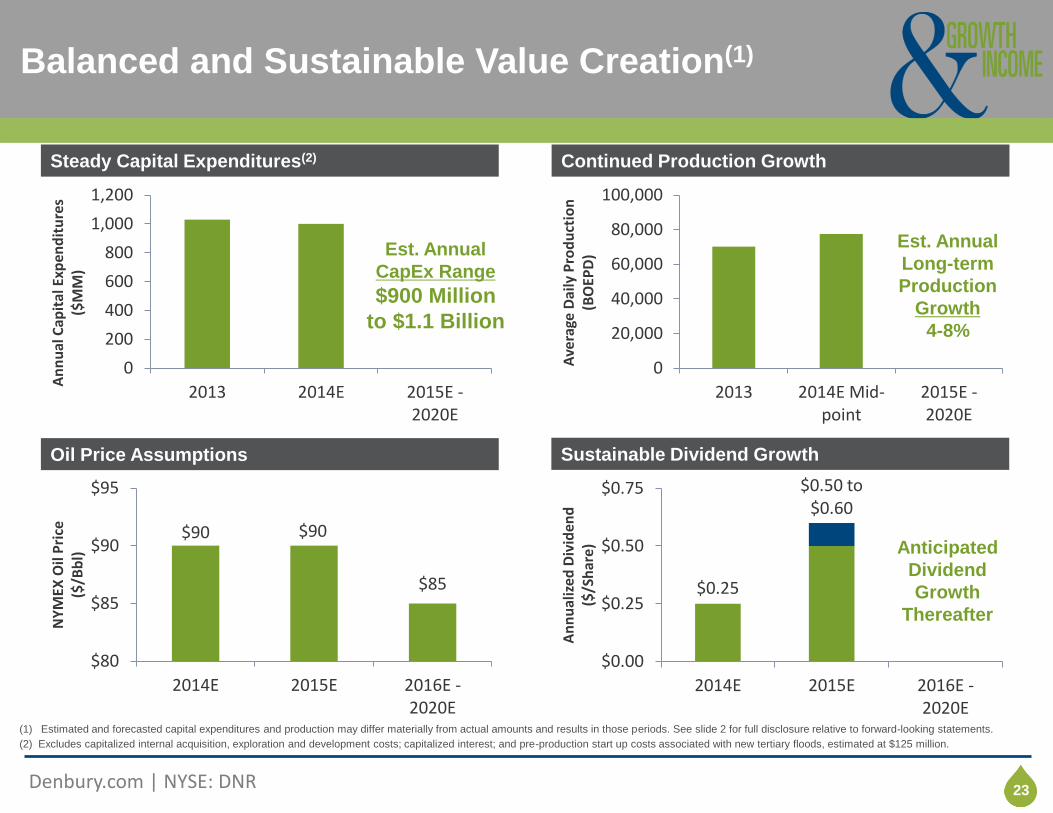

Click to edit title style Balanced and Sustainable Value Creation(1)

23

0

20,000

40,000

60,000

80,000

100,000

2013 2014E Mid-point

2015E -2020E

Ave

rage

Dai

ly P

rod

uct

ion

(B

OEP

D)

Continued Production Growth

Est. Annual

Long-term

Production

Growth

4-8%

0

200

400

600

800

1,000

1,200

2013 2014E 2015E -2020E

An

nu

al C

apit

al E

xpen

dit

ure

s ($

MM

)

Steady Capital Expenditures(2)

Est. Annual

CapEx Range

$900 Million

to $1.1 Billion

$0.25

$0.50 to $0.60

$0.00

$0.25

$0.50

$0.75

2014E 2015E 2016E -2020E

An

nu

aliz

ed D

ivid

end

($

/Sh

are)

Sustainable Dividend Growth

Anticipated

Dividend

Growth

Thereafter

(1) Estimated and forecasted capital expenditures and production may differ materially from actual amounts and results in those periods. See slide 2 for full disclosure relative to forward-looking statements.

(2) Excludes capitalized internal acquisition, exploration and development costs; capitalized interest; and pre-production start up costs associated with new tertiary floods, estimated at $125 million.

Oil Price Assumptions

$90 $90

$85

$80

$85

$90

$95

2014E 2015E 2016E -2020E

NY

MEX

Oil

Pri

ce

($/B

bl)

Click to edit Master title style

Denbury.com | NYSE: DNR

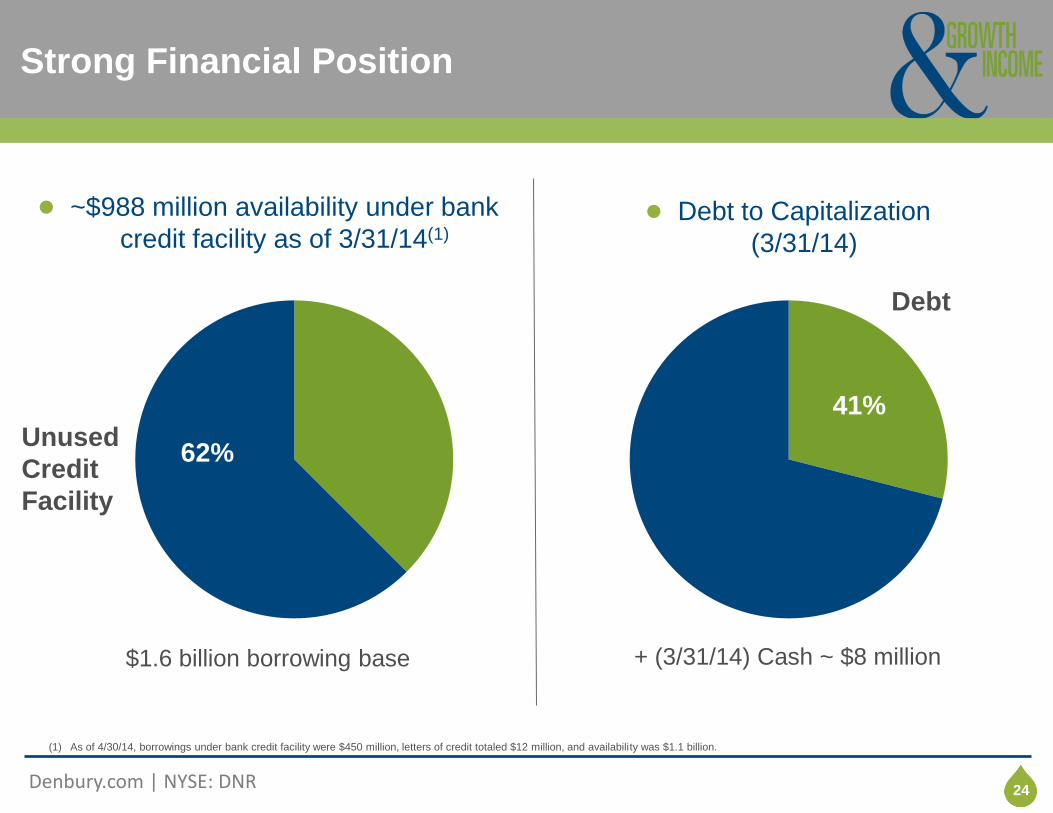

Click to edit title style Strong Financial Position

24

62%

● ~$988 million availability under bank

credit facility as of 3/31/14(1) ● Debt to Capitalization

(3/31/14)

38%

Debt

+ (3/31/14) Cash ~ $8 million

41%

(1) As of 4/30/14, borrowings under bank credit facility were $450 million, letters of credit totaled $12 million, and availability was $1.1 billion.

$1.6 billion borrowing base

Unused

Credit

Facility

Click to edit Master title style

Denbury.com | NYSE: DNR

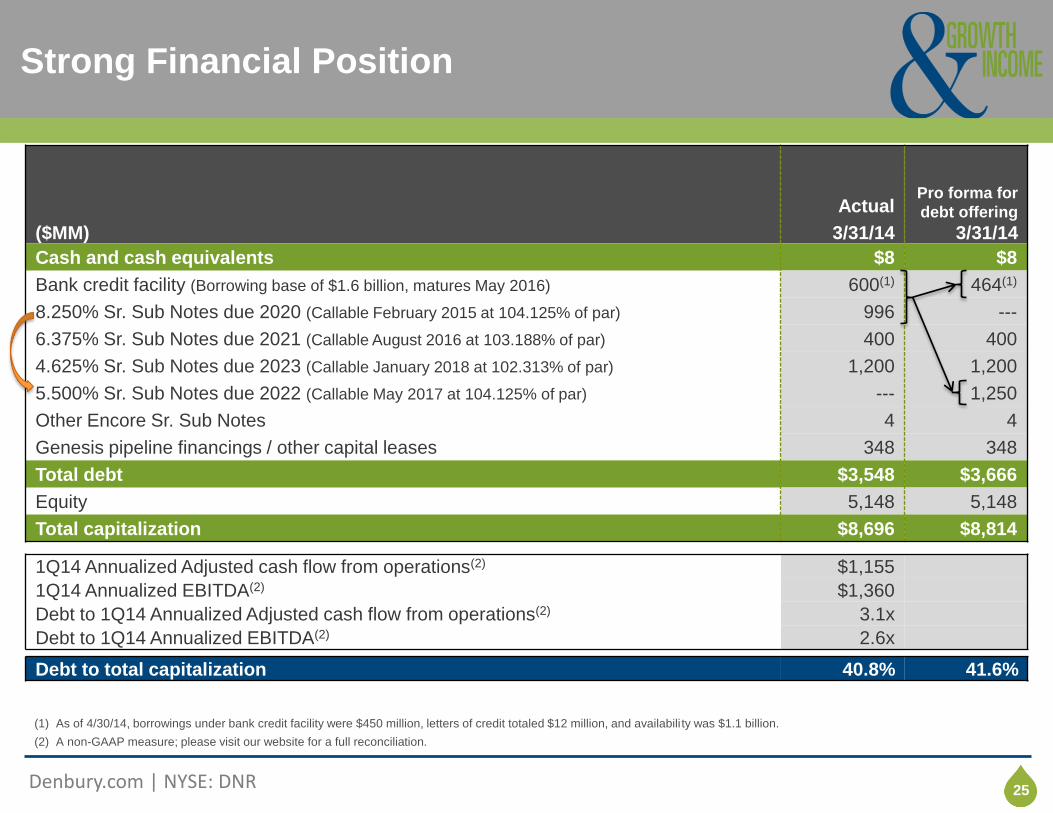

Click to edit title style Strong Financial Position

25

($MM)

Actual

3/31/14

Pro forma for

debt offering

3/31/14

Cash and cash equivalents $8 $8

Bank credit facility (Borrowing base of $1.6 billion, matures May 2016) 600(1) 464(1)

8.250% Sr. Sub Notes due 2020 (Callable February 2015 at 104.125% of par) 996 ---

6.375% Sr. Sub Notes due 2021 (Callable August 2016 at 103.188% of par) 400 400

4.625% Sr. Sub Notes due 2023 (Callable January 2018 at 102.313% of par) 1,200 1,200

5.500% Sr. Sub Notes due 2022 (Callable May 2017 at 104.125% of par) --- 1,250

Other Encore Sr. Sub Notes 4 4

Genesis pipeline financings / other capital leases 348 348

Total debt $3,548 $3,666

Equity 5,148 5,148

Total capitalization $8,696 $8,814

1Q14 Annualized Adjusted cash flow from operations(2) $1,155

1Q14 Annualized EBITDA(2) $1,360

Debt to 1Q14 Annualized Adjusted cash flow from operations(2) 3.1x

Debt to 1Q14 Annualized EBITDA(2) 2.6x

Debt to total capitalization 40.8% 41.6%

(1) As of 4/30/14, borrowings under bank credit facility were $450 million, letters of credit totaled $12 million, and availabili ty was $1.1 billion.

(2) A non-GAAP measure; please visit our website for a full reconciliation.

Click to edit Master title style

Denbury.com | NYSE: DNR

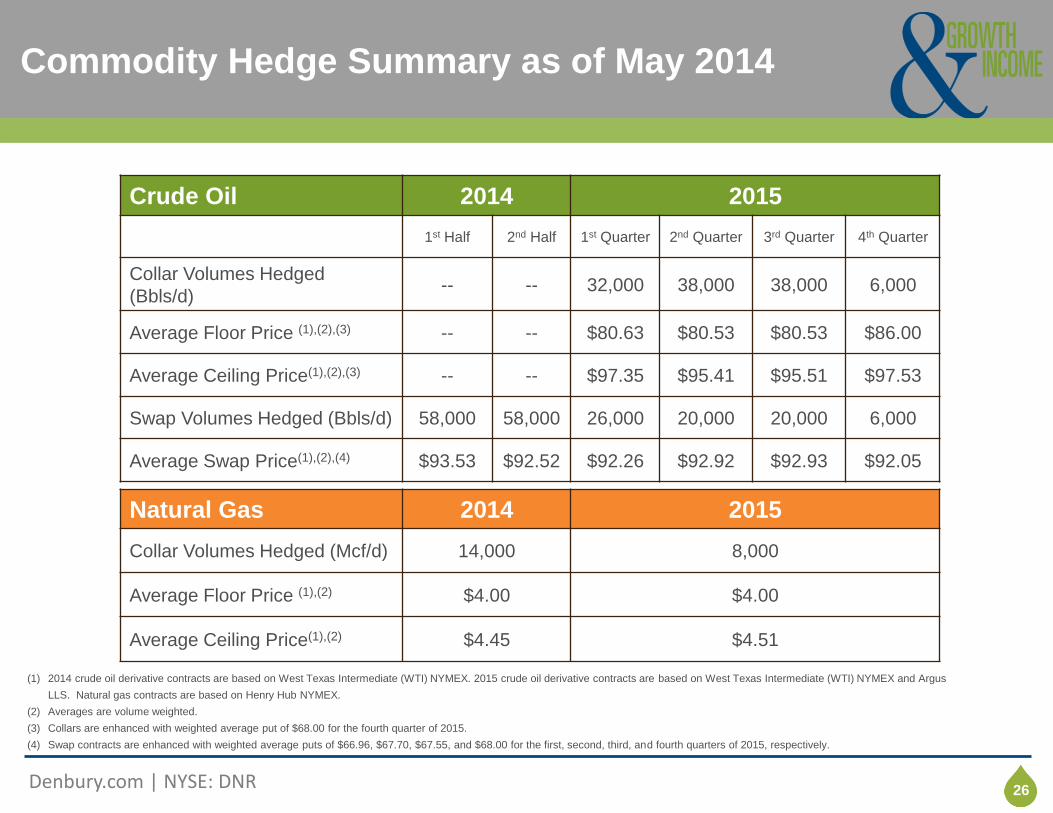

Click to edit title style Commodity Hedge Summary as of May 2014

26

Natural Gas 2014 2015

Collar Volumes Hedged (Mcf/d) 14,000 8,000

Average Floor Price (1),(2) $4.00 $4.00

Average Ceiling Price(1),(2) $4.45 $4.51

Crude Oil 2014 2015

1st Half 2nd Half 1st Quarter 2nd Quarter 3rd Quarter 4th Quarter

Collar Volumes Hedged

(Bbls/d) -- -- 32,000 38,000 38,000 6,000

Average Floor Price (1),(2),(3) -- -- $80.63 $80.53 $80.53 $86.00

Average Ceiling Price(1),(2),(3) -- -- $97.35 $95.41 $95.51 $97.53

Swap Volumes Hedged (Bbls/d) 58,000 58,000 26,000 20,000 20,000 6,000

Average Swap Price(1),(2),(4) $93.53 $92.52 $92.26 $92.92 $92.93 $92.05

(1) 2014 crude oil derivative contracts are based on West Texas Intermediate (WTI) NYMEX. 2015 crude oil derivative contracts are based on West Texas Intermediate (WTI) NYMEX and Argus

LLS. Natural gas contracts are based on Henry Hub NYMEX.

(2) Averages are volume weighted.

(3) Collars are enhanced with weighted average put of $68.00 for the fourth quarter of 2015.

(4) Swap contracts are enhanced with weighted average puts of $66.96, $67.70, $67.55, and $68.00 for the first, second, third, and fourth quarters of 2015, respectively.

Click to edit Master title style

Denbury.com | NYSE: DNR

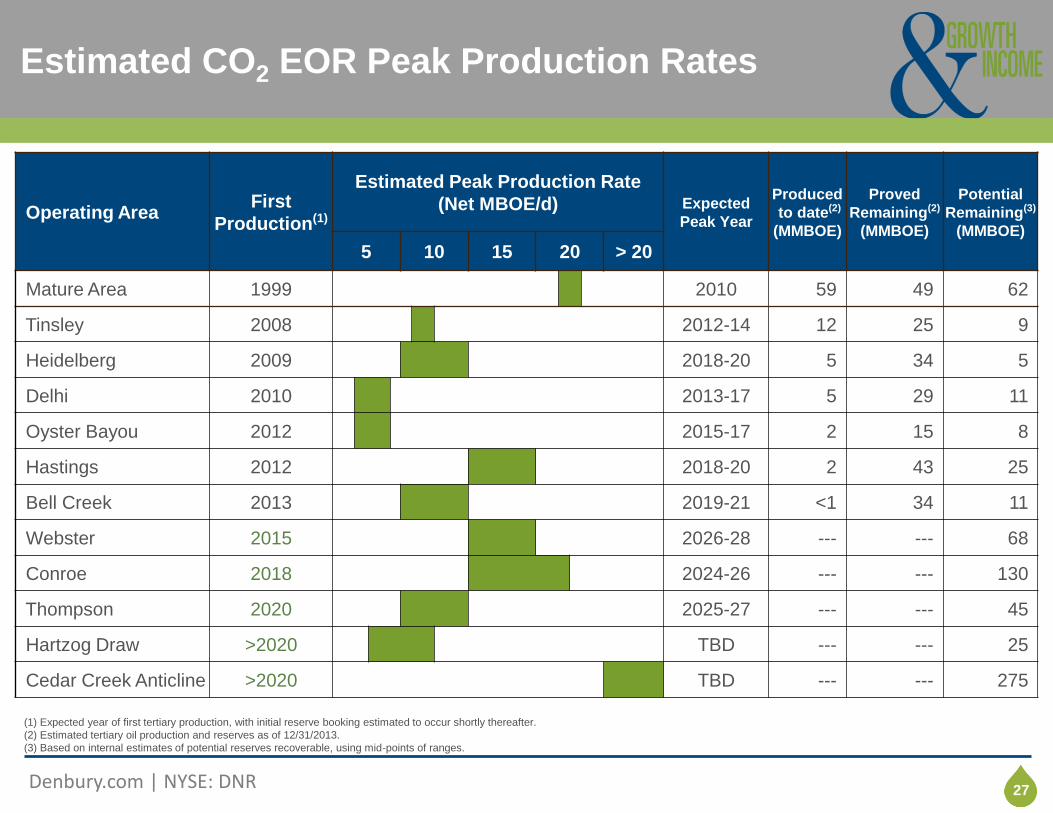

Click to edit title style Estimated CO2 EOR Peak Production Rates

27

Operating Area First

Production(1)

Estimated Peak Production Rate

(Net MBOE/d) Expected

Peak Year

Produced

to date(2)

(MMBOE)

Proved

Remaining(2)

(MMBOE)

Potential

Remaining(3)

(MMBOE)

5 10 15 20 > 20

Mature Area 1999 2010 59 49 62

Tinsley 2008 2012-14 12 25 9

Heidelberg 2009 2018-20 5 34 5

Delhi 2010 2013-17 5 29 11

Oyster Bayou 2012 2015-17 2 15 8

Hastings 2012 2018-20 2 43 25

Bell Creek 2013 2019-21 <1 34 11

Webster 2015 2026-28 --- --- 68

Conroe 2018 2024-26 --- --- 130

Thompson 2020 2025-27 --- --- 45

Hartzog Draw >2020 TBD --- --- 25

Cedar Creek Anticline >2020 TBD --- --- 275

(1) Expected year of first tertiary production, with initial reserve booking estimated to occur shortly thereafter.

(2) Estimated tertiary oil production and reserves as of 12/31/2013.

(3) Based on internal estimates of potential reserves recoverable, using mid-points of ranges.

Click to edit Master title style

Denbury.com | NYSE: DNR

Click to edit title style IN SUMMARY: Value Driven

28

● Focused on delivering value through consistent growth in production,

reserves, and dividends

● Strategic advantage in CO2 EOR supports lower-risk, long-term growth

outlook and substantial free cash flow generation

● High operating margin and capital efficiency

● Funding capex and dividends with cash flow, strong oil hedging

program and disciplined share repurchase program

Leading Growth & Income, CO2 EOR Company in the US

Click to edit Master title style

Denbury.com | NYSE: DNR

Click to edit title style Corporate Information

29

Corporate Headquarters

Denbury Resources Inc.

5320 Legacy Drive

Plano, Texas 75024

Ph: (972) 673-2000

denbury.com

Contact Information Jack Collins

Executive Director, Finance and Investor Relations

(972) 673-2028

Ross Campbell

Manager, Investor Relations

(972) 673-2825

Lauren Power

Financial Analyst, Investor Relations

(972) 673-2433

Appendix

Click to edit Master title style

Denbury.com | NYSE: DNR

Click to edit title style Why is CO2 EOR our core focus?

31

● High Confidence of Oil Target

Over 100 million barrels (gross) produced by Denbury to date

Net upward adjustments to reserves to date

● CO2 Flooding Recovers Oil (CO2 ♥’s Crude Oil)

First commercial CO2 EOR flood started production in 1972

Over 1.5 billion barrels produced to date in the US(1)

Current estimated production in the US is >280 MBbls/d(2)

● A Very Repeatable Process with a lot of Running Room

Up to 10 Billion Barrels Recoverable with CO2 EOR in our two operating areas(3)

Over 900 Million Barrels (net) of 3P CO2 EOR reserves in our portfolio today

(1) Oil & Gas Journal, Dec. 7, 2009.

(2) Oil & Gas Journal, July 2, 2012.

(3) Source: DOE 2005 and 2006 reports.

Click to edit Master title style

Denbury.com | NYSE: DNR

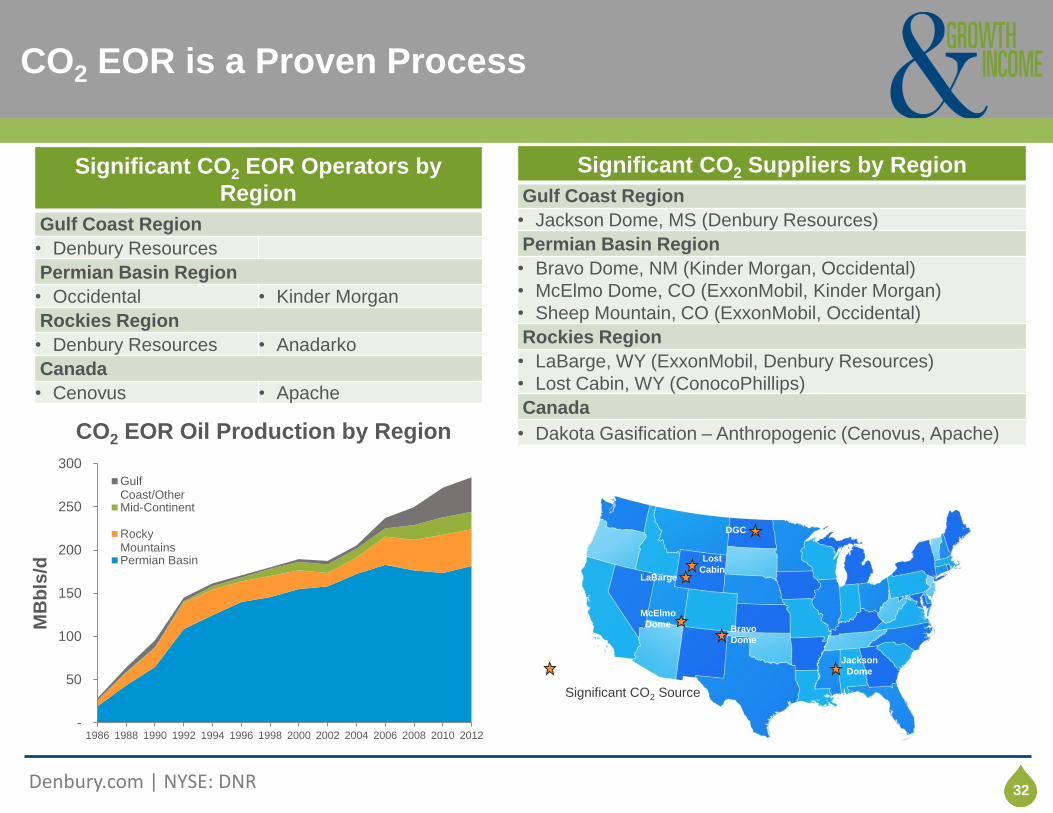

Click to edit title style CO2 EOR is a Proven Process

32

Significant CO2 Suppliers by Region

Gulf Coast Region

• Jackson Dome, MS (Denbury Resources)

Permian Basin Region

• Bravo Dome, NM (Kinder Morgan, Occidental)

• McElmo Dome, CO (ExxonMobil, Kinder Morgan)

• Sheep Mountain, CO (ExxonMobil, Occidental)

Rockies Region

• LaBarge, WY (ExxonMobil, Denbury Resources)

• Lost Cabin, WY (ConocoPhillips)

Canada

• Dakota Gasification – Anthropogenic (Cenovus, Apache)

Significant CO2 EOR Operators by

Region

Gulf Coast Region

• Denbury Resources

Permian Basin Region

• Occidental • Kinder Morgan

Rockies Region

• Denbury Resources • Anadarko

Canada

• Cenovus • Apache

Jackson

Dome

Bravo

Dome

LaBarge

Lost

Cabin

DGC

McElmo

Dome

Significant CO2 Source

-

50

100

150

200

250

300

1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012

MB

bls

/d

CO2 EOR Oil Production by Region

GulfCoast/OtherMid-Continent

RockyMountainsPermian Basin

Click to edit Master title style

Denbury.com | NYSE: DNR

Click to edit title style CO2 Operations: Oil Recovery Process

33

CO2 PIPELINE - from Jackson Dome

CO2 moves through formation mixing with oil droplets, expanding them and moving them to producing wells.

INJECTION WELL - Injects

CO2 in dense phase

PRODUCTION WELLS

Produce oil, water and CO2 (CO2 is recycled)

Model for Oil Recovery Using CO2 is +/- 17%

of Original Oil in Place (Based on Little Creek)

Primary recovery = +/- 20%

Secondary recovery (waterfloods) = +/- 18%

Tertiary (CO2) = +/- 17%

Oil Formation

Click to edit Master title style

Denbury.com | NYSE: DNR

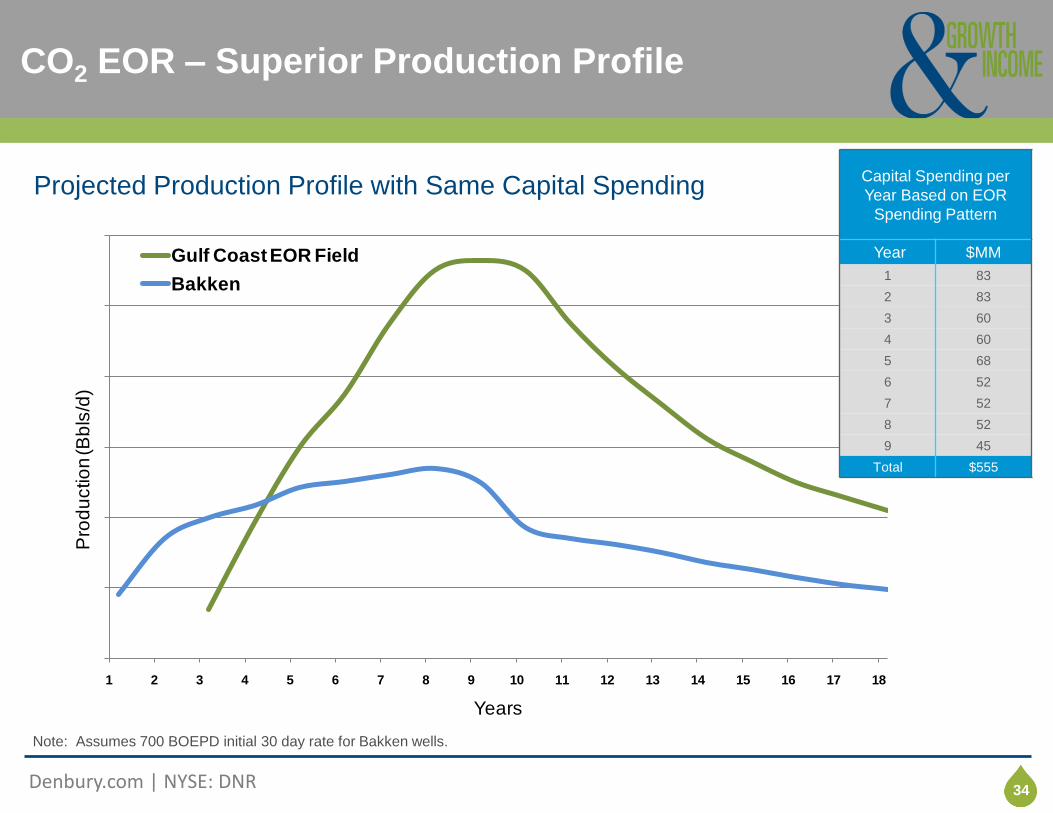

Click to edit title style CO2 EOR – Superior Production Profile

34

0

2,000

4,000

6,000

8,000

10,000

12,000

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18

Pro

du

ctio

n (B

bls

/d)

Years

Gulf Coast EOR Field

Bakken

Projected Production Profile with Same Capital Spending Capital Spending per

Year Based on EOR

Spending Pattern

Year $MM

1 83

2 83

3 60

4 60

5 68

6 52

7 52

8 52

9 45

Total $555

Note: Assumes 700 BOEPD initial 30 day rate for Bakken wells.

Click to edit Master title style

Denbury.com | NYSE: DNR

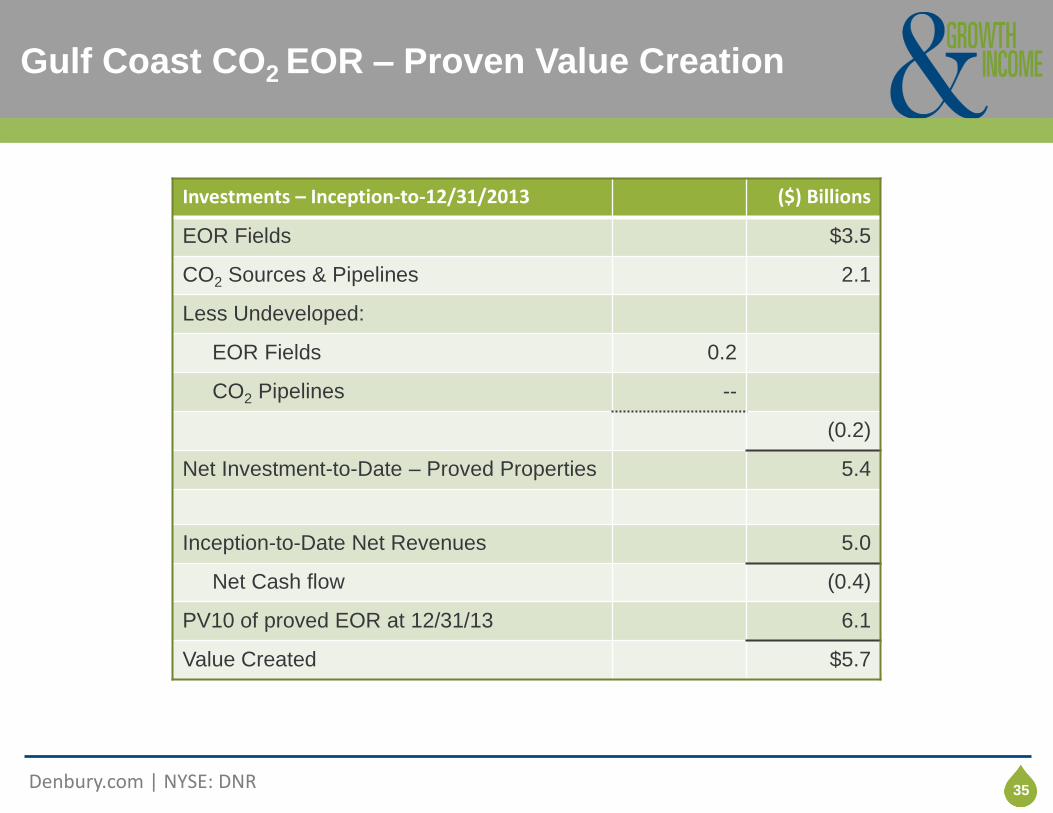

Click to edit title style Gulf Coast CO2 EOR – Proven Value Creation

35

Investments – Inception-to-12/31/2013 ($) Billions

EOR Fields $3.5

CO2 Sources & Pipelines 2.1

Less Undeveloped:

EOR Fields 0.2

CO2 Pipelines --

(0.2)

Net Investment-to-Date – Proved Properties 5.4

Inception-to-Date Net Revenues 5.0

Net Cash flow (0.4)

PV10 of proved EOR at 12/31/13 6.1

Value Created $5.7

Click to edit Master title style

Denbury.com | NYSE: DNR

Click to edit title style

● Successfully plugged source of leak & surface remediation completed(2)

● Restored CO2 injection outside impacted area and isolated impacted area with

water curtain injection wells

(1) As of March 31, 2014, we had recorded $114 million of expenses related to the remediation of Delhi Field. This estimate is subject to change.

(2) Based on currently known remediation requirements.

Status Update

● Performing additional reviews of P&A wells

● Continuing to strengthen internal P&A criteria

● Dedicated staff to investigate, implement and monitor

● ~$200 MM budgeted for P&A’s over next 5 years across all CO2 EOR fields

~$50 MM budgeted for P&A’s in 2014

P&A Initiatives Taken

Delhi Field(1)

Click to edit Master title style

Denbury.com | NYSE: DNR

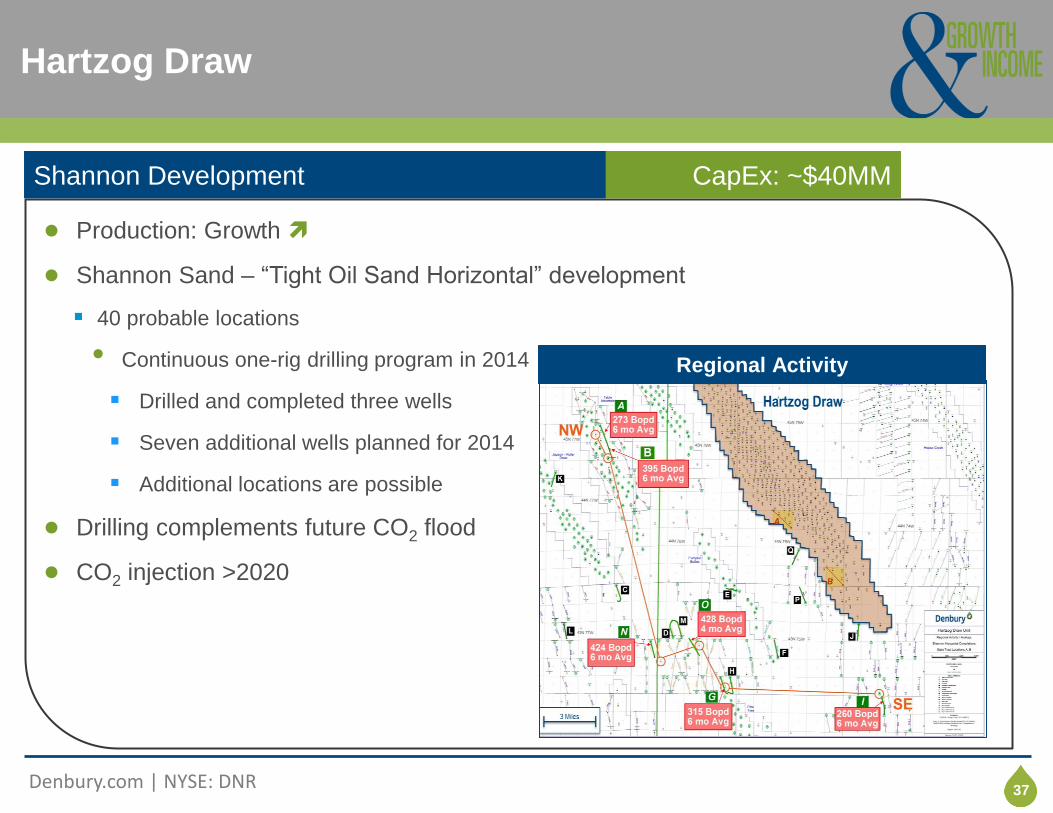

Click to edit title style Hartzog Draw

37

● Production: Growth

● Shannon Sand – “Tight Oil Sand Horizontal” development

40 probable locations

• Continuous one-rig drilling program in 2014

Drilled and completed three wells

Seven additional wells planned for 2014

Additional locations are possible

● Drilling complements future CO2 flood

● CO2 injection >2020

Shannon Development CapEx: ~$40MM

Regional Activity

Click to edit Master title style

Denbury.com | NYSE: DNR

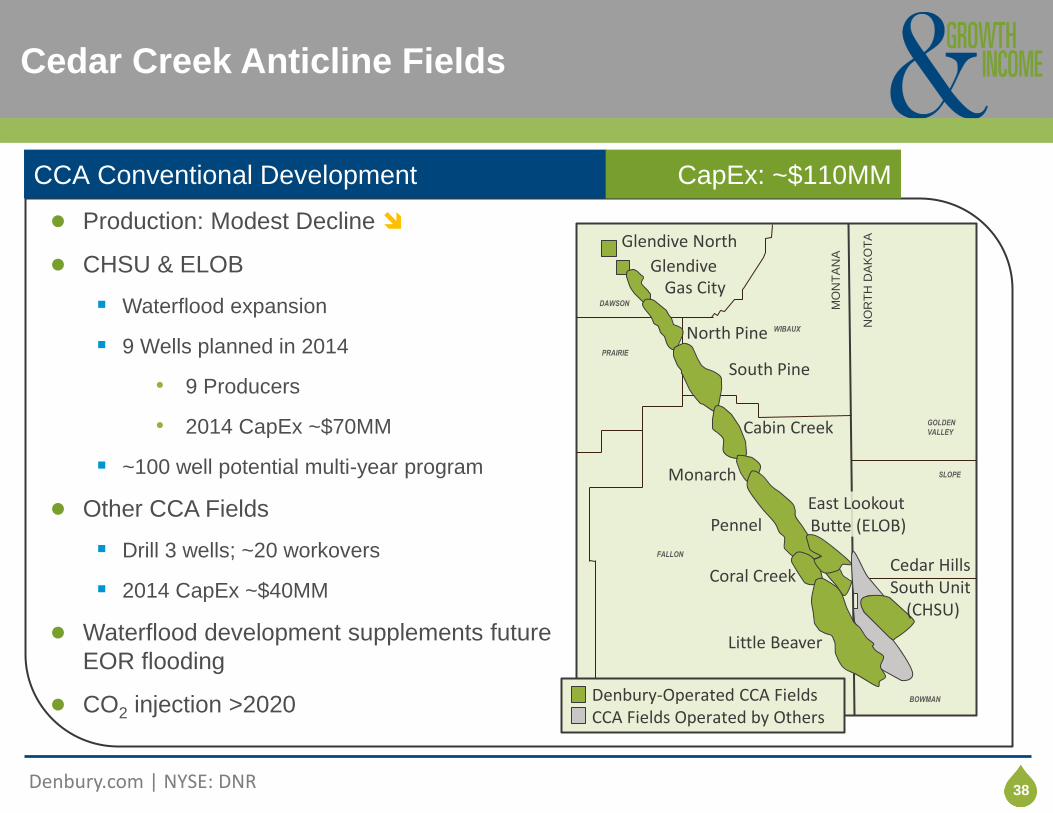

Click to edit title style Cedar Creek Anticline Fields

38

MO

NT

AN

A

NO

RT

H D

AK

OT

A

DAWSON

PRAIRIE

WIBAUX

GOLDEN

VALLEY

FALLON

SLOPE

BOWMAN

Glendive North

Glendive Gas City

North Pine

South Pine

Cabin Creek

Monarch

Pennel

Coral Creek

Little Beaver

East Lookout Butte (ELOB)

Denbury-Operated CCA Fields CCA Fields Operated by Others

Cedar Hills South Unit

(CHSU)

● Production: Modest Decline

● CHSU & ELOB

Waterflood expansion

9 Wells planned in 2014

• 9 Producers

• 2014 CapEx ~$70MM

~100 well potential multi-year program

● Other CCA Fields

Drill 3 wells; ~20 workovers

2014 CapEx ~$40MM

● Waterflood development supplements future

EOR flooding

● CO2 injection >2020

CCA Conventional Development CapEx: ~$110MM

Click to edit Master title style

Denbury.com | NYSE: DNR

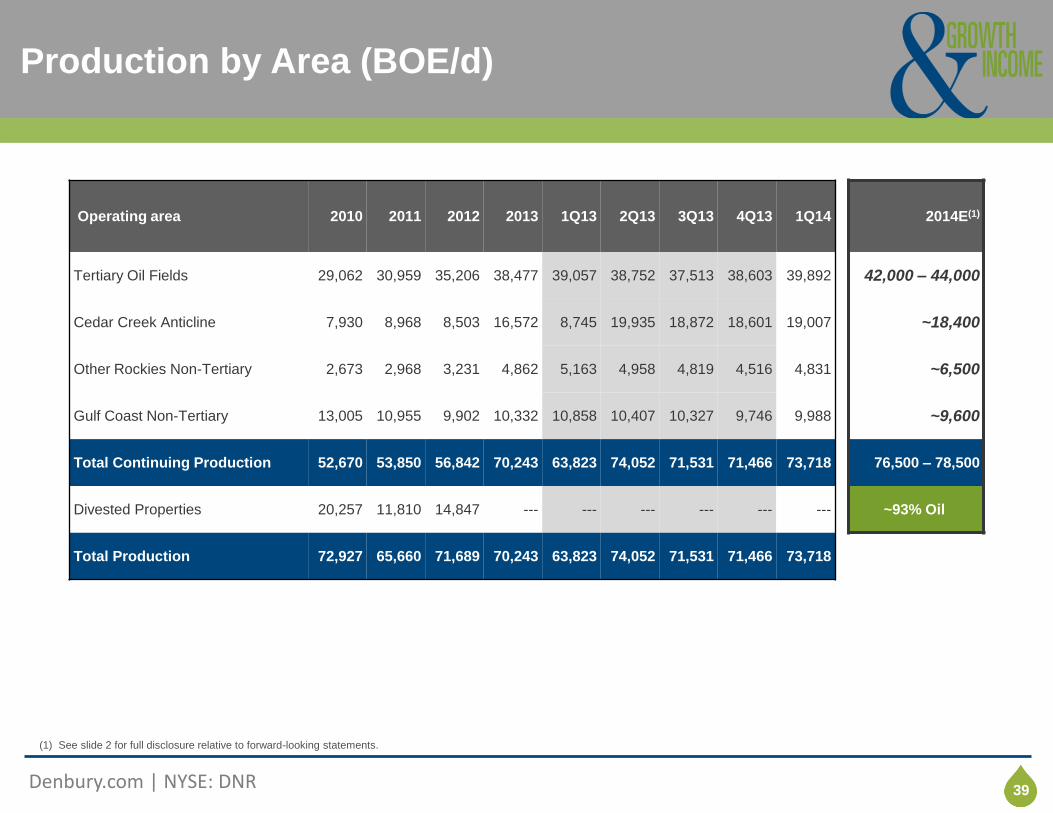

Click to edit title style Production by Area (BOE/d)

39

(1) See slide 2 for full disclosure relative to forward-looking statements.

Operating area 2010 2011 2012 2013 1Q13 2Q13 3Q13 4Q13 1Q14 2014E(1)

Tertiary Oil Fields 29,062 30,959 35,206 38,477 39,057 38,752 37,513 38,603 39,892 42,000 – 44,000

Cedar Creek Anticline 7,930 8,968 8,503 16,572 8,745 19,935 18,872 18,601 19,007 ~18,400

Other Rockies Non-Tertiary 2,673 2,968 3,231 4,862 5,163 4,958 4,819 4,516 4,831 ~6,500

Gulf Coast Non-Tertiary 13,005 10,955 9,902 10,332 10,858 10,407 10,327 9,746 9,988 ~9,600

Total Continuing Production 52,670 53,850 56,842 70,243 63,823 74,052 71,531 71,466 73,718 76,500 – 78,500

Divested Properties 20,257 11,810 14,847 --- --- --- --- --- --- ~93% Oil

Total Production 72,927 65,660 71,689 70,243 63,823 74,052 71,531 71,466 73,718

Click to edit Master title style

Denbury.com | NYSE: DNR

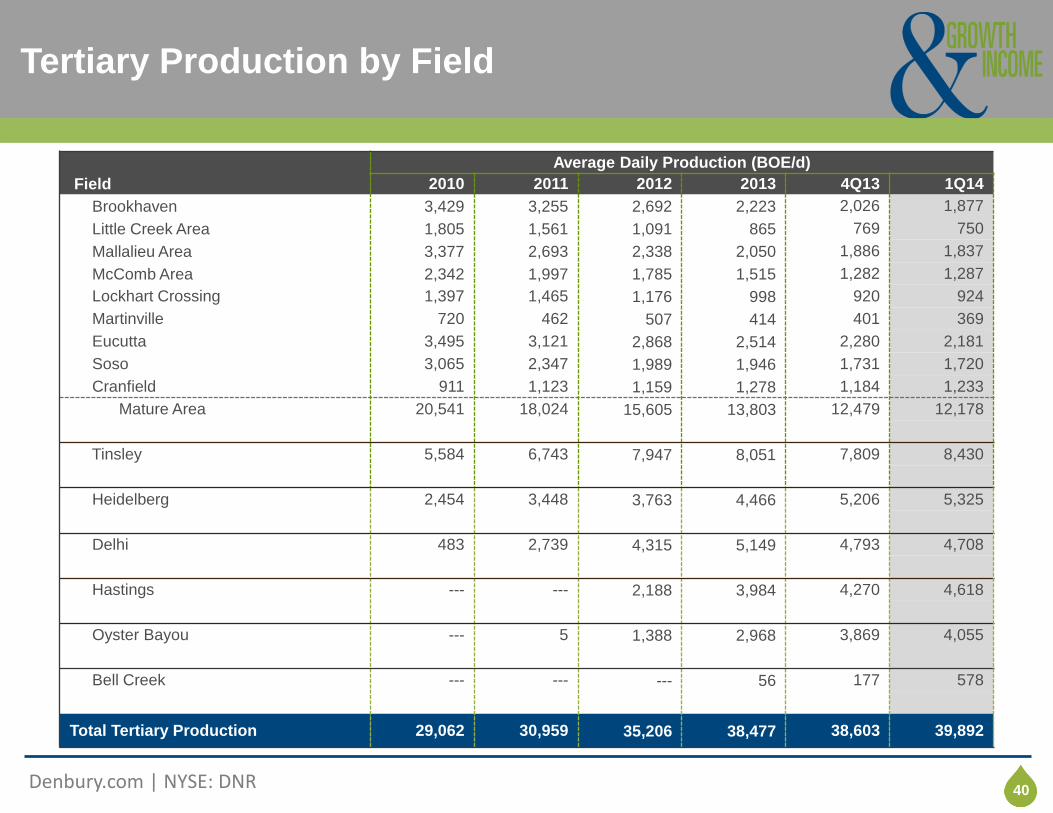

Click to edit title style Tertiary Production by Field

40

Average Daily Production (BOE/d)

Field 2010 2011 2012 2013 4Q13 1Q14

Brookhaven 3,429 3,255 2,692 2,223 2,026 1,877

Little Creek Area 1,805 1,561 1,091 865 769 750

Mallalieu Area 3,377 2,693 2,338 2,050 1,886 1,837

McComb Area 2,342 1,997 1,785 1,515 1,282 1,287

Lockhart Crossing 1,397 1,465 1,176 998 920 924

Martinville 720 462 507 414 401 369

Eucutta 3,495 3,121 2,868 2,514 2,280 2,181

Soso 3,065 2,347 1,989 1,946 1,731 1,720

Cranfield 911 1,123 1,159 1,278 1,184 1,233

Mature Area 20,541 18,024 15,605 13,803 12,479 12,178

Tinsley 5,584 6,743 7,947 8,051 7,809 8,430

Heidelberg 2,454 3,448 3,763 4,466 5,206 5,325

Delhi 483 2,739 4,315 5,149 4,793 4,708

Hastings --- --- 2,188 3,984 4,270 4,618

Oyster Bayou --- 5 1,388 2,968 3,869 4,055

Bell Creek --- --- --- 56 177 578

Total Tertiary Production 29,062 30,959 35,206 38,477 38,603 39,892

Click to edit Master title style

Denbury.com | NYSE: DNR

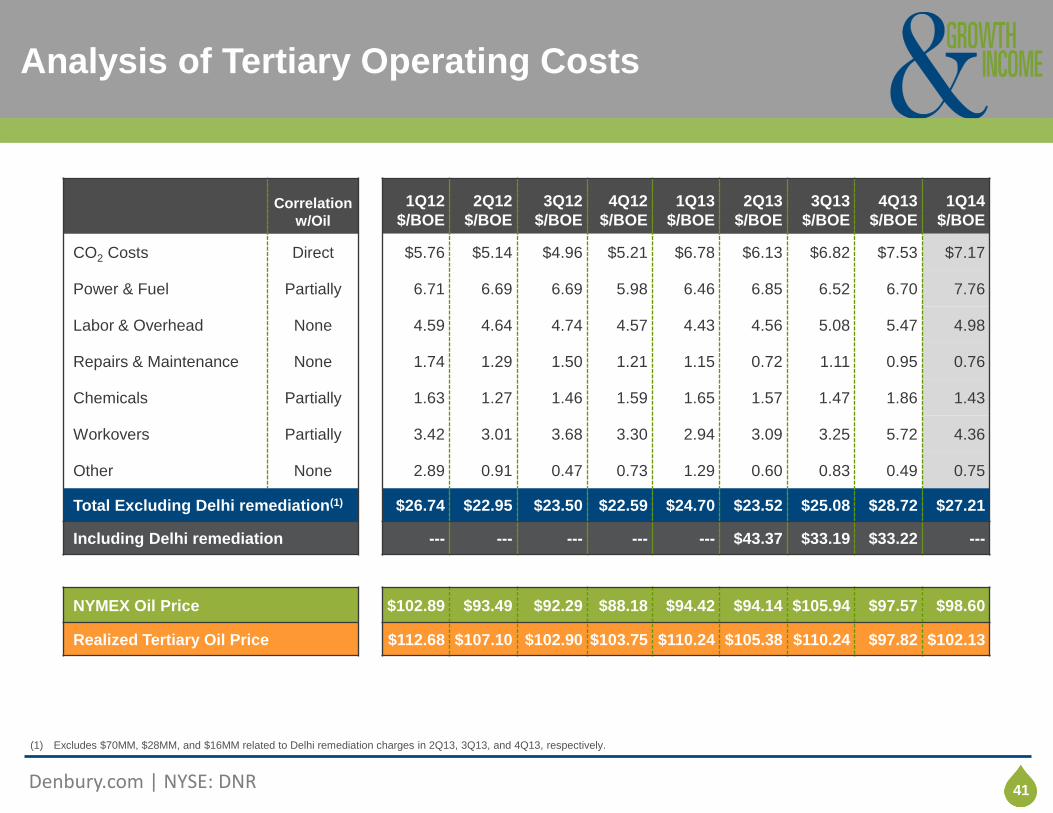

Click to edit title style Analysis of Tertiary Operating Costs

41

Correlation

w/Oil

1Q12

$/BOE

2Q12

$/BOE

3Q12

$/BOE

4Q12

$/BOE

1Q13

$/BOE

2Q13

$/BOE

3Q13

$/BOE

4Q13

$/BOE

1Q14

$/BOE

CO2 Costs Direct $5.76 $5.14 $4.96 $5.21 $6.78 $6.13 $6.82 $7.53 $7.17

Power & Fuel Partially 6.71 6.69 6.69 5.98 6.46 6.85 6.52 6.70 7.76

Labor & Overhead None 4.59 4.64 4.74 4.57 4.43 4.56 5.08 5.47 4.98

Repairs & Maintenance None 1.74 1.29 1.50 1.21 1.15 0.72 1.11 0.95 0.76

Chemicals Partially 1.63 1.27 1.46 1.59 1.65 1.57 1.47 1.86 1.43

Workovers Partially 3.42 3.01 3.68 3.30 2.94 3.09 3.25 5.72 4.36

Other None 2.89 0.91 0.47 0.73 1.29 0.60 0.83 0.49 0.75

Total Excluding Delhi remediation(1) $26.74 $22.95 $23.50 $22.59 $24.70 $23.52 $25.08 $28.72 $27.21

Including Delhi remediation --- --- --- --- --- $43.37 $33.19 $33.22 ---

NYMEX Oil Price $102.89 $93.49 $92.29 $88.18 $94.42 $94.14 $105.94 $97.57 $98.60

Realized Tertiary Oil Price $112.68 $107.10 $102.90 $103.75 $110.24 $105.38 $110.24 $97.82 $102.13

(1) Excludes $70MM, $28MM, and $16MM related to Delhi remediation charges in 2Q13, 3Q13, and 4Q13, respectively.

Click to edit Master title style

Denbury.com | NYSE: DNR

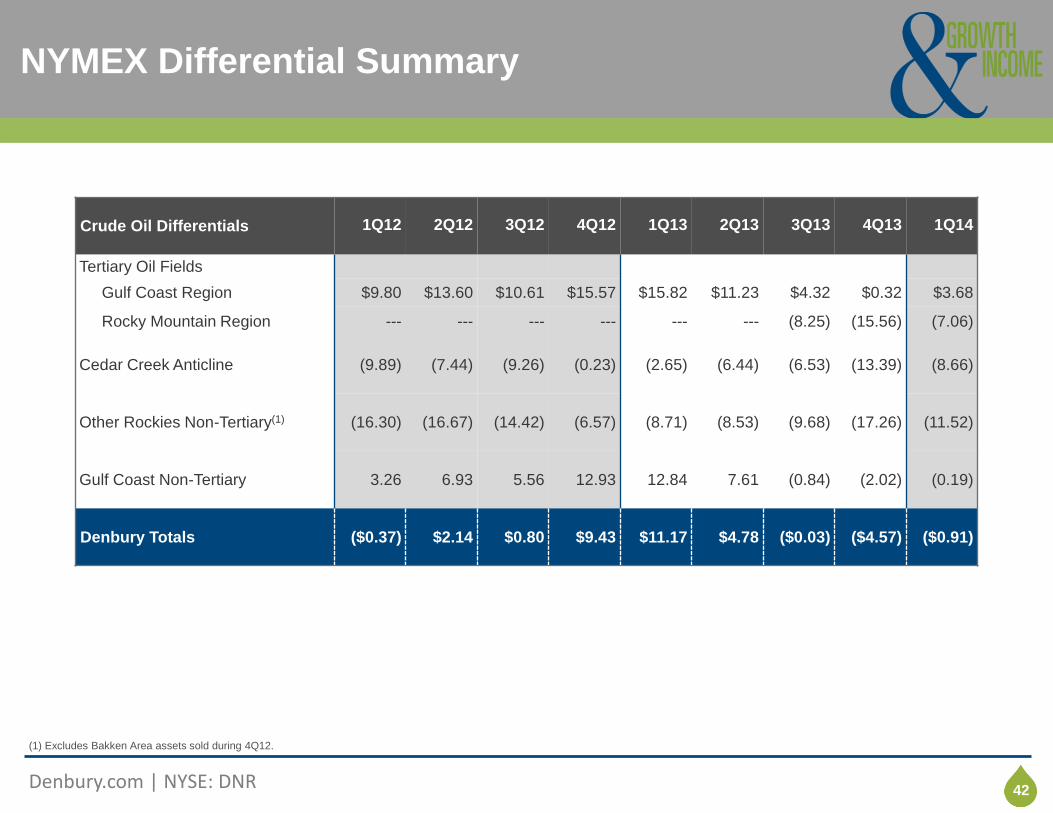

Click to edit title style NYMEX Differential Summary

42

(1) Excludes Bakken Area assets sold during 4Q12.

Crude Oil Differentials 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14

Tertiary Oil Fields

Gulf Coast Region $9.80 $13.60 $10.61 $15.57 $15.82 $11.23 $4.32 $0.32 $3.68

Rocky Mountain Region --- --- --- --- --- --- (8.25) (15.56) (7.06)

Cedar Creek Anticline (9.89) (7.44) (9.26) (0.23) (2.65) (6.44) (6.53) (13.39) (8.66)

Other Rockies Non-Tertiary(1) (16.30) (16.67) (14.42) (6.57) (8.71) (8.53) (9.68) (17.26) (11.52)

Gulf Coast Non-Tertiary 3.26 6.93 5.56 12.93 12.84 7.61 (0.84) (2.02) (0.19)

Denbury Totals ($0.37) $2.14 $0.80 $9.43 $11.17 $4.78 ($0.03) ($4.57) ($0.91)

Click to edit Master title style

Denbury.com | NYSE: DNR

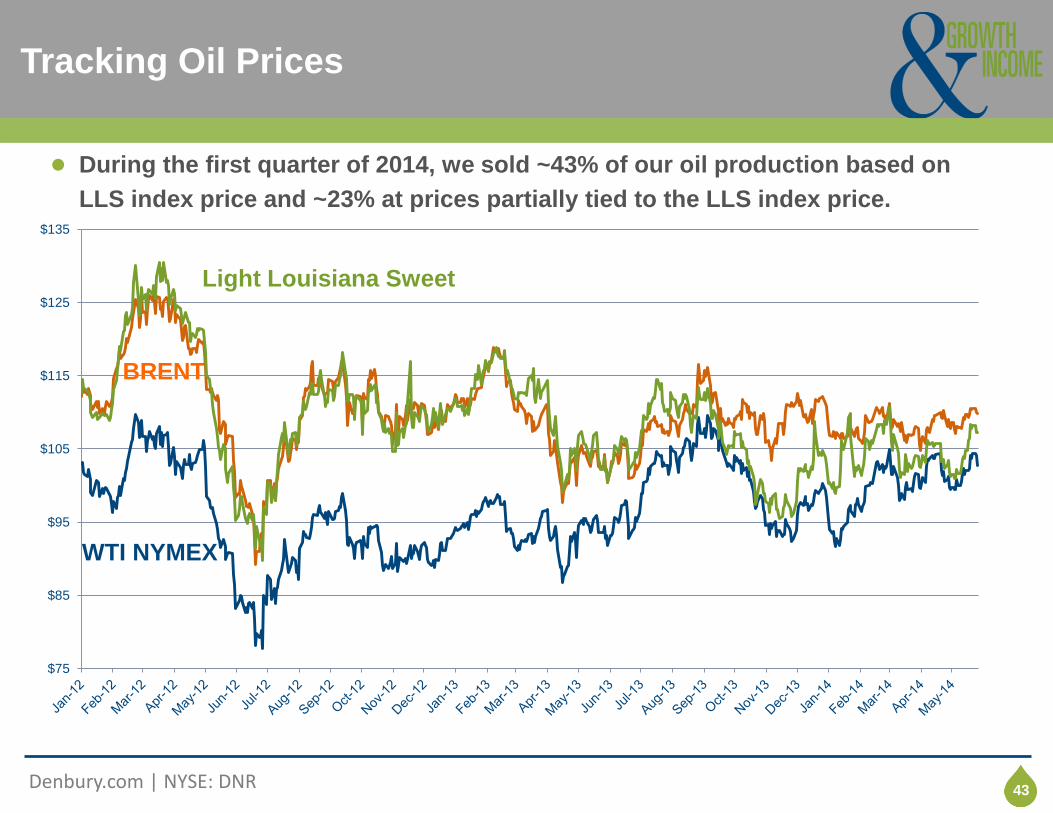

Click to edit title style Tracking Oil Prices

43

Light Louisiana Sweet

WTI NYMEX

BRENT

● During the first quarter of 2014, we sold ~43% of our oil production based on

LLS index price and ~23% at prices partially tied to the LLS index price.

$75

$85

$95

$105

$115

$125

$135

Click to edit Master title style

Denbury.com | NYSE: DNR

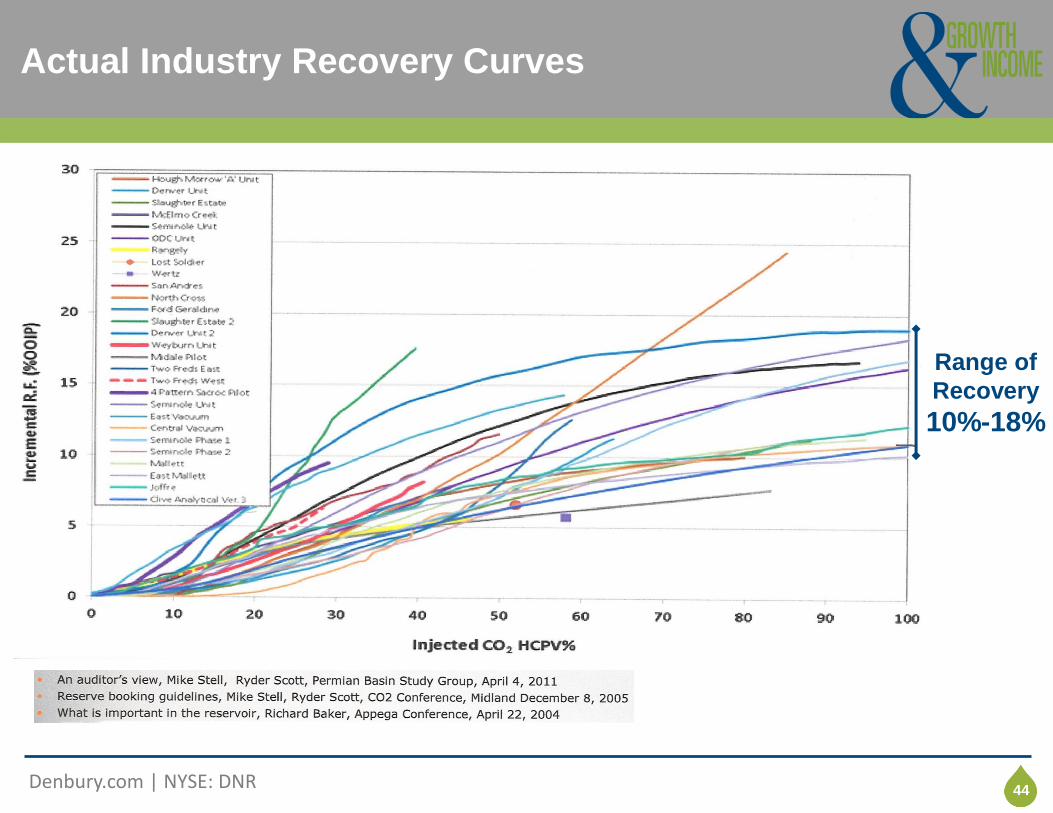

Click to edit title style Actual Industry Recovery Curves

44

Range of

Recovery

10%-18%

Click to edit Master title style

Denbury.com | NYSE: DNR

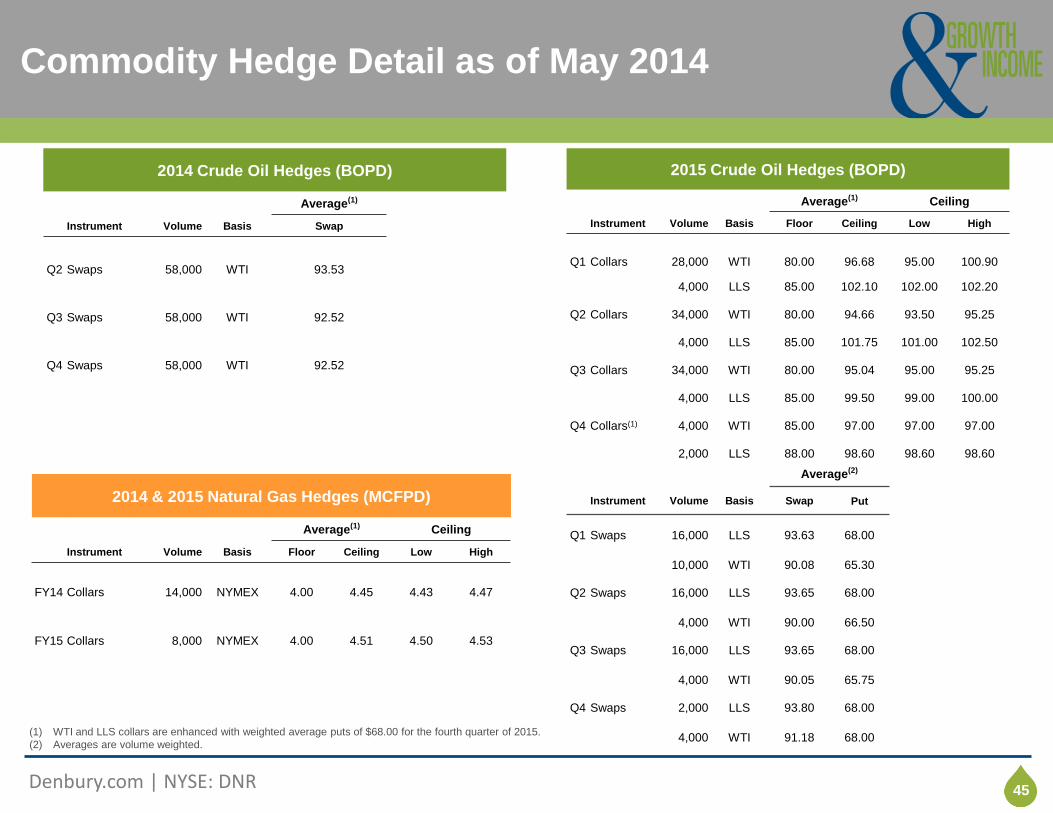

Click to edit title style Commodity Hedge Detail as of May 2014

45

(1) WTI and LLS collars are enhanced with weighted average puts of $68.00 for the fourth quarter of 2015.

(2) Averages are volume weighted.

2014 & 2015 Natural Gas Hedges (MCFPD)

Average(1) Ceiling

Instrument Volume Basis Floor Ceiling Low High

FY14 Collars

14,000 NYMEX 4.00 4.45 4.43 4.47

FY15 Collars 8,000 NYMEX 4.00 4.51 4.50 4.53

2015 Crude Oil Hedges (BOPD)

Average(1) Ceiling

Instrument Volume Basis Floor Ceiling Low High

Q1 Collars

28,000 WTI 80.00 96.68 95.00 100.90

4,000 LLS 85.00 102.10 102.00 102.20

Q2 Collars 34,000 WTI 80.00 94.66 93.50 95.25

4,000 LLS 85.00 101.75 101.00 102.50

Q3 Collars 34,000 WTI 80.00 95.04 95.00 95.25

4,000 LLS 85.00 99.50 99.00 100.00

Q4 Collars(1) 4,000 WTI 85.00 97.00 97.00 97.00

2,000 LLS 88.00 98.60 98.60 98.60

Average(2)

Instrument Volume Basis Swap Put

Q1 Swaps 16,000 LLS 93.63 68.00

10,000 WTI 90.08 65.30

Q2 Swaps 16,000 LLS 93.65 68.00

4,000 WTI 90.00 66.50

Q3 Swaps 16,000 LLS 93.65 68.00

4,000 WTI 90.05 65.75

Q4 Swaps 2,000 LLS 93.80 68.00

4,000 WTI 91.18 68.00

2014 Crude Oil Hedges (BOPD)

Average(1)

Instrument Volume Basis Swap

Q2 Swaps 58,000 WTI 93.53

Q3 Swaps 58,000 WTI 92.52

Q4 Swaps 58,000 WTI 92.52

Click to edit Master title style

Denbury.com | NYSE: DNR

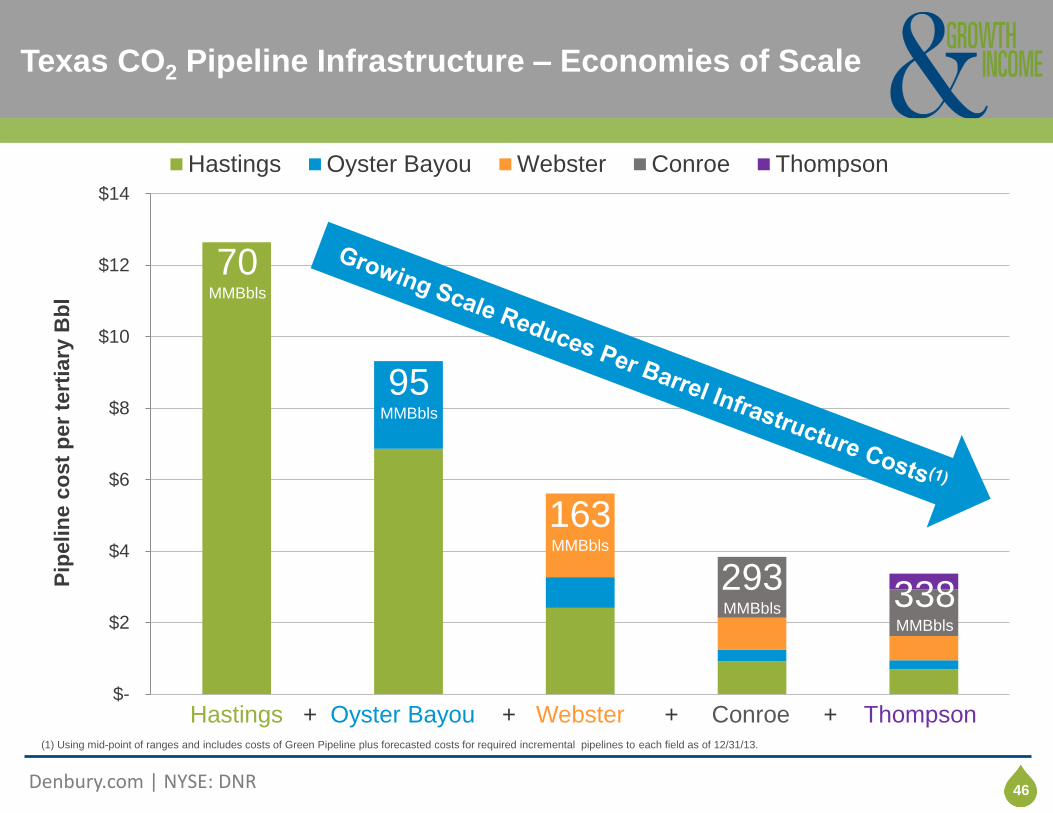

Click to edit title style Texas CO2 Pipeline Infrastructure – Economies of Scale

46

$-

$2

$4

$6

$8

$10

$12

$14

Pip

elin

e c

ost

per

tert

iary

Bb

l

Hastings Oyster Bayou Webster Conroe Thompson

Hastings + Oyster Bayou + Webster + Conroe + Thompson

70 MMBbls

95 MMBbls

163 MMBbls

293 MMBbls 338

MMBbls

(1) Using mid-point of ranges and includes costs of Green Pipeline plus forecasted costs for required incremental pipelines to each field as of 12/31/13.

Click to edit Master title style

Denbury.com | NYSE: DNR

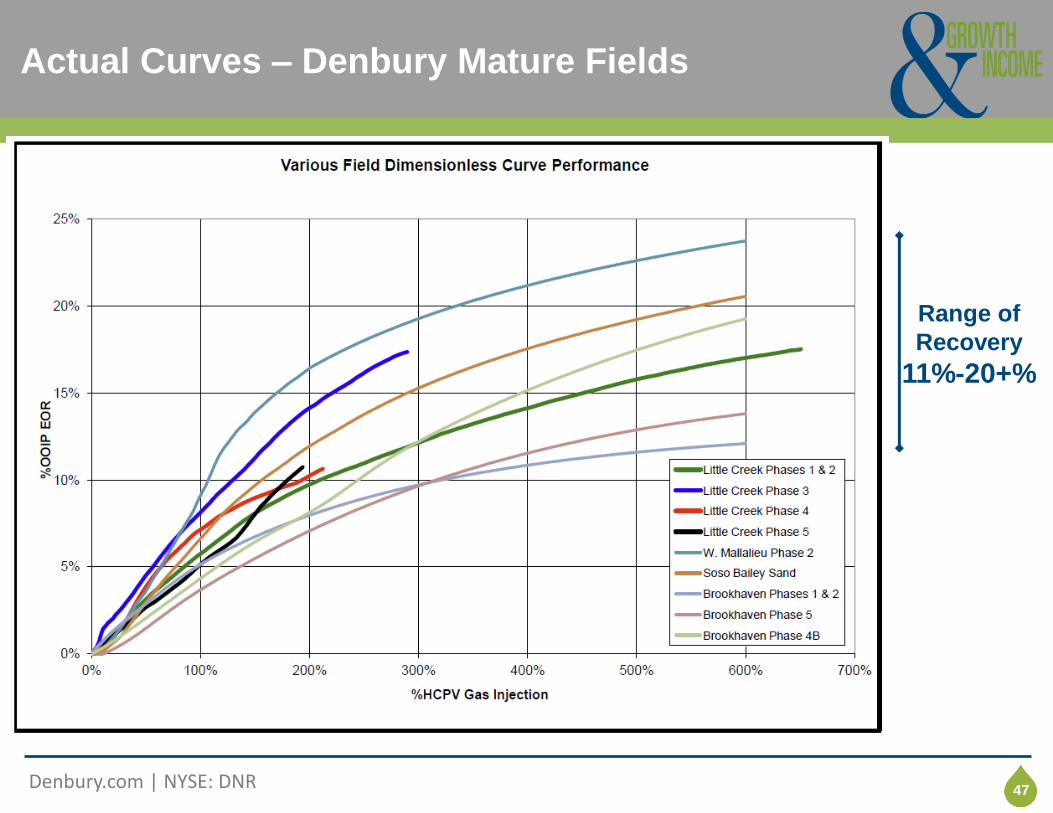

Click to edit title style Actual Curves – Denbury Mature Fields

47

Range of

Recovery

11%-20+%