Embed Size (px)

Citation preview

© 2013 Deloitte LLP. All rights reserved.

April 2013

Parameters of Competition for a Turkish International Financial CentreTom Shave

© 2013 Deloitte LLP. All rights reserved.

International Financial CentreParameters of Competition

2

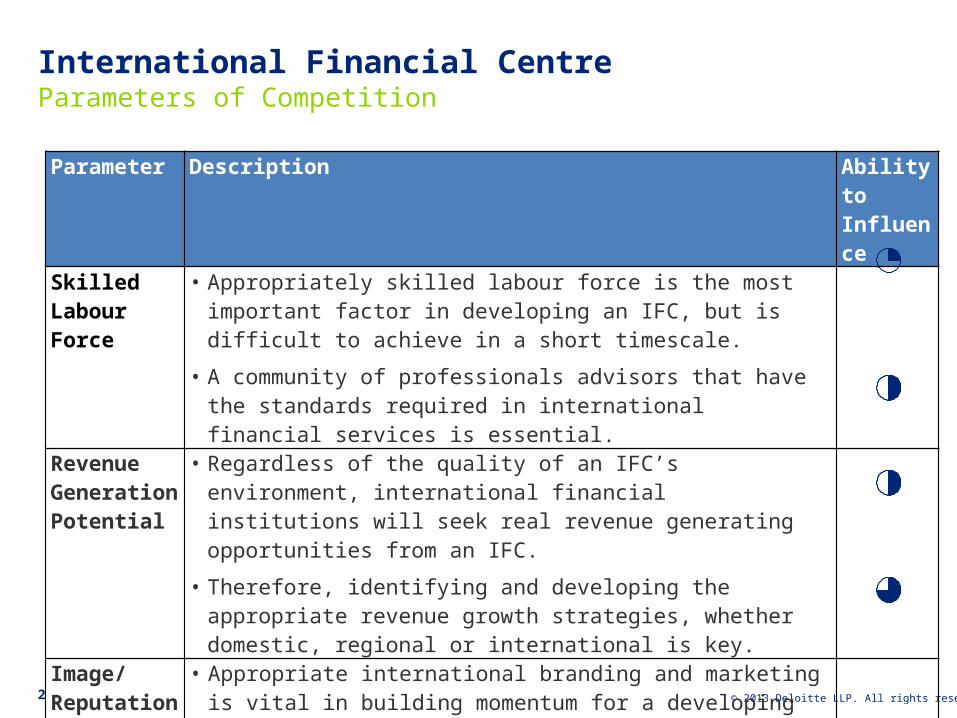

Parameter Description Ability to Influence

Skilled Labour Force

• Appropriately skilled labour force is the most important factor in developing an IFC, but is difficult to achieve in a short timescale.

• A community of professionals advisors that have the standards required in international financial services is essential.

Revenue Generation Potential

• Regardless of the quality of an IFC’s environment, international financial institutions will seek real revenue generating opportunities from an IFC.

• Therefore, identifying and developing the appropriate revenue growth strategies, whether domestic, regional or international is key.

Image/ Reputation

• Appropriate international branding and marketing is vital in building momentum for a developing IFC.

Legal environment

• A reliable, flexible and efficient legal system is a critical component for any successful IFC.

• As a general rule of thumb common law (based on case law) rather than civil law is more flexible in dealing with the demands of a dynamic financial services industry.

© 2013 Deloitte LLP. All rights reserved.

International Financial CentreParameters of Competition

3

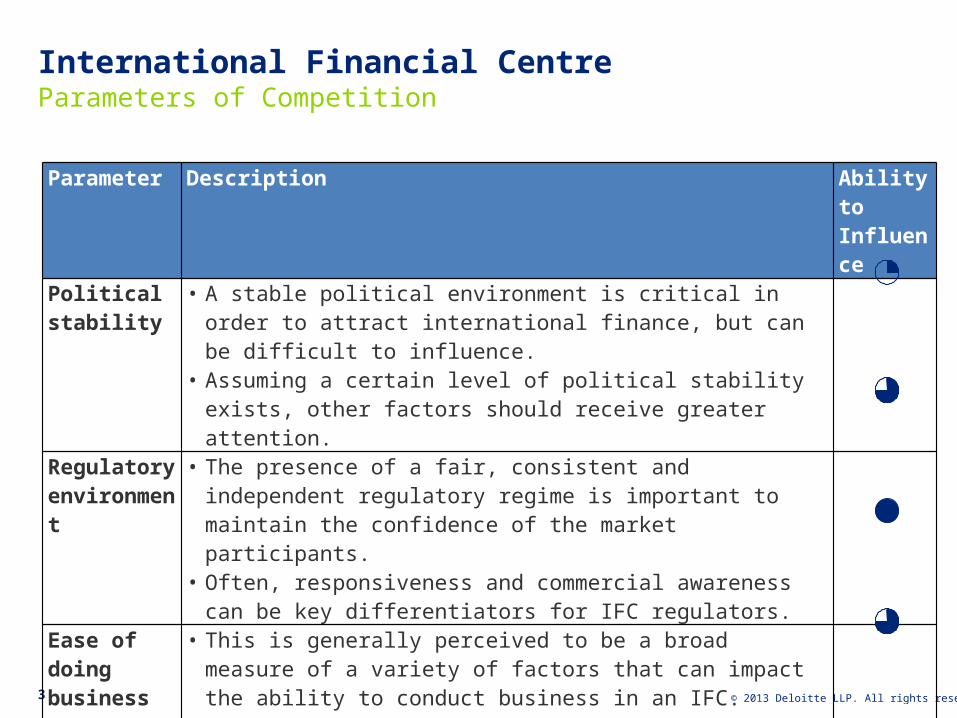

Parameter Description Ability to Influence

Political stability

• A stable political environment is critical in order to attract international finance, but can be difficult to influence.

• Assuming a certain level of political stability exists, other factors should receive greater attention.

Regulatory environment

• The presence of a fair, consistent and independent regulatory regime is important to maintain the confidence of the market participants.

• Often, responsiveness and commercial awareness can be key differentiators for IFC regulators.

Ease of doing business

• This is generally perceived to be a broad measure of a variety of factors that can impact the ability to conduct business in an IFC.

• It can include administrative burdens for establishing businesses, labour freedoms, clarity of business rules and corruption.

Fiscal environment

• An attractive fiscal regime remains a desirable feature for IFCs, even despite the recent focus on international tax policy.

• This is not the same as zero, or abnormally low, tax.

© 2013 Deloitte LLP. All rights reserved.

International Financial CentreParameters of Competition

4

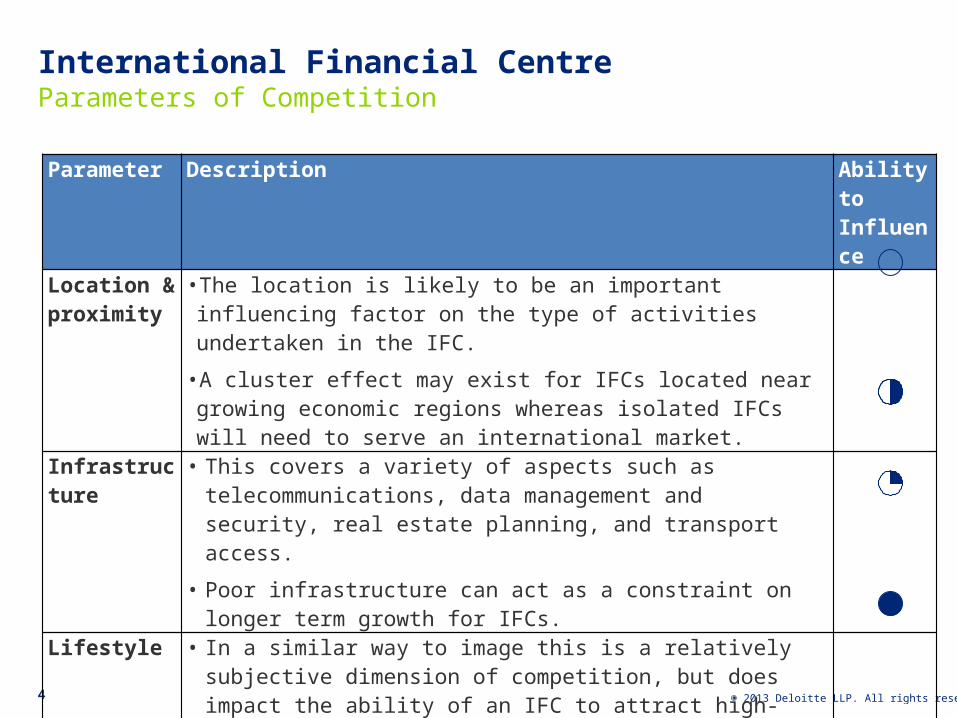

Parameter Description Ability to Influence

Location & proximity

•The location is likely to be an important influencing factor on the type of activities undertaken in the IFC.

•A cluster effect may exist for IFCs located near growing economic regions whereas isolated IFCs will need to serve an international market.

Infrastructure • This covers a variety of aspects such as telecommunications, data management and security, real estate planning, and transport access.

• Poor infrastructure can act as a constraint on longer term growth for IFCs.

Lifestyle • In a similar way to image this is a relatively subjective dimension of competition, but does impact the ability of an IFC to attract high-calibre financial services professionals.

Cost of doing business

• Given the current economic climate the operating costs for financial institutions, including real estate and labour, can impact location decisions.

• However, generally more developed IFCs have higher costs so a competitive advantage can be gained for some emerging IFCs.

© 2013 Deloitte LLP. All rights reserved.

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited (“DTTL”), a UK private company limited by guarantee, and its network of member firms, each of which is a legally separate and independent entity. Please see www.deloitte.co.uk/about for a detailed description of the legal structure of DTTL and its member firms.

Deloitte LLP is the United Kingdom member firm of DTTL.

This publication has been written in general terms and therefore cannot be relied on to cover specific situations; application of the principles set out will depend upon the particular circumstances involved and we recommend that you obtain professional advice before acting or refraining from acting on any of the contents of this publication. Deloitte LLP would be pleased to advise readers on how to apply the principles set out in this publication to their specific circumstances. Deloitte LLP accepts no duty of care or liability for any loss occasioned to any person acting or refraining from action as a result of any material in this publication.

Deloitte LLP is a limited liability partnership registered in England and Wales with registered number OC303675 and its registered office at 2 New Street Square, London EC4A 3BZ, United Kingdom. Tel: +44 (0) 20 7936 3000 Fax: +44 (0) 20 7583 1198.

© 2013 Deloitte LLP. All rights reserved.

Member of Deloitte Touche Tohmatsu Limited5