Embed Size (px)

Citation preview

Delivering in an Evolving Market

Alan Chirgwin Vice President Marketing – Iron Ore14 May 2015

Disclaimer

Forward-looking statementsThis release contains forward-looking statements, including statements regarding: trends in commodity prices and currency exchange rates; demand for commodities; plans, strategies and objectives of management; closure or divestment of certain operations or facilities (including associated costs); anticipated production or construction commencement dates; capital costs and scheduling; operating costs and shortages of materials and skilled employees; anticipated productive lives of projects, mines and facilities; provisions and contingent liabilities; tax and regulatory developments. Forward-looking statements can be identified by the use of terminology such as ‘intend’, ‘aim’, ‘project’, ‘anticipate’, ‘estimate’, ‘plan’, ‘believe’, ‘expect’, ‘may’, ‘should’, ‘will’, ‘continue’, ‘annualised’ or similar words. These statements discuss future expectations concerning the results of operations or financial condition, or provide other forward-looking statements. These forward-looking statements are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results to differ materially from those expressed in the statements contained in this release. Readers are cautioned not to put undue reliance on forward-looking statements. For example, our future revenues from our operations, projects or mines described in this release will be based, in part, upon the market price of the minerals, metals or petroleum produced, which may vary significantly from current levels. These variations, if materially adverse, may affect the timing or the feasibility of the development of a particular project, the expansion of certain facilities or mines, or the continuation of existing operations.Other factors that may affect the actual construction or production commencement dates, costs or production output and anticipated lives of operations, mines or facilities include our ability to profitably produce and transport the minerals, petroleum and/or metals extracted to applicable markets; the impact of foreign currency exchange rates on the market prices of the minerals, petroleum or metals we produce; activities of government authorities in some of the countries where we are exploring or developing these projects, facilities or mines, including increases in taxes, changes in environmental and other regulations and political uncertainty; labour unrest; and other factors identified in the risk factors discussed in BHP Billiton’s filings with the U.S. Securities and Exchange Commission (the “SEC”) (including in Annual Reports on Form 20-F) which are available on the SEC’s website at www.sec.gov.Except as required by applicable regulations or by law, the Group does not undertake any obligation to publicly update or review any forward-looking statements, whether as a result of new information or future events.

Non-IFRS financial information BHP Billiton results are reported under International Financial Reporting Standards (IFRS) including Underlying EBIT and Underlying EBITDA which are used to measure segment performance. This release may also include certain non-IFRS measures including Underlying attributable profit, Underlying basic earnings per share, Underlying EBITDA interest coverage, Adjusted effective tax rate, Underlying EBIT margin, Underlying EBITDA margin, Underlying return on capital, Free cash flow, Net debt and Net operating assets. These measures are used internally by management to assess the performance of our business, make decisions on the allocation of our resources and assess operational management. Non-IFRS measures have not been subject to audit or review and should not be considered as an indication of or alternative to an IFRS measure of profitability, financial performance or liquidity.

No offer of securitiesNothing in this presentation should be construed as either an offer to sell or a solicitation of an offer to buy or sell BHP Billiton securities in any jurisdiction, or be treated or relied upon as a recommendation or advice by BHP Billiton.

Reliance on third-party informationThe views expressed in this release contain information that has been derived from publicly available sources that have not been independently verified. No representation or warranty is made as to the accuracy, completeness or reliability of the information. This release should not be relied upon as a recommendation or forecast by BHP Billiton.

Slide 2Alan Chirgwin, Vice President Marketing - Iron Ore, 14 May 2015

Summary of content

Slide 3

Market Overview: Structural Changes

Adjusting to a Changing Environment

Platforms success: transparent, liquid and efficient market

Alan Chirgwin, Vice President Marketing - Iron Ore, 14 May 2015

China steel demand facing short-term headwinds

• Domestic steel demand is facing temporary headwinds

– property market downturn

– manufacturing activity slowdown

– weak machinery demand in line with low investment in manufacturing

– softening of consumption of home appliances and automobile

– traders de-stocking

China apparent steel demand1 growth(YoY, %)

1. Apparent steel demand = crude steel production + imports – exports.Source: BHP Billiton; NBS; Mysteel.

Slide 4

-8

-6

-4

-2

0

2

4

6

8

10

12

CY11 CY12 CY13 CY14 Q1CY15

Alan Chirgwin, Vice President Marketing - Iron Ore, 14 May 2015

China steel production has recently increased its focus on exports

• China has been a steel net exporter since 2005

• Steel exports increased in CY14, as Chinese mills tries to mitigate the temporary domestic demand weakness

• Steel exports remained high in Q1CY15

• Steel exports are expected to remain high in the long term due to China cost competitiveness and more overseas investment

Production declines on weak domestic demand(million tonnes of crude steel)

Slide 5

500

550

600

650

700

750

800

850

CY11 CY12 CY13 CY14 1QCY15

Domestic sales Exports

annualised

Source: BHP Billiton; NBS.

Alan Chirgwin, Vice President Marketing - Iron Ore, 14 May 2015

Despite short-term volatility, China steel stock per capita has large upside potential

• Despite an expected moderation in the rate of demand growth, upside still exists for the Chinese steel industry

• Short-term demand could be subject to investment cyclicality affecting incremental stock addition

• Over the long-term, China will need more steel for sustainable economic growth

• We expect China’s crude steel production to peak at 1 to 1.1 billion tonnes in the mid-2020s and plateau through to 2030

0

2

4

6

8

10

12

2000 2010 2015f 2020f 2030f

China US

Source: BHP Billiton; IHS Global Insight; worldsteel.1. Accumulation of steel stock is calculated from apparent steel consumption, net of trade in steel containing goods and net of steel out of use (scrapped).

Substantial growth in Chinese steel stock(finished steel per capita1, t)

Slide 6Alan Chirgwin, Vice President Marketing - Iron Ore, 14 May 2015

Our increase in volume, for value, has resulted in no growth in our market position

Alan Chirgwin, Vice President Marketing - Iron Ore, 14 May 2015 Slide 7

• BHP Billiton has maintained its share of iron ore exports through a disciplined program of investment

• We approved our last major investment at WAIO in 2011

• Since then we have focused on productivity

– capacity utilisation, driving more volume through existing infrastructure

– reducing external expenditure through lower demand, better rates and insourcing services

– driving efficiencies and optimising functional support to enable people productivity

• Our productivity focus has resulted in volume growth above the original capital investment

Source: Wood Mackenzie 2015.1. All iron ore products including lump, fines, pellet feed and pellets, 100%.2. Share of exports in 2014. BHP Billiton data excludes Samarco.

2008-2014 CAGR Share of exports2

Rest of World 10% 31%

Vale 3% 21%

Rio Tinto Pilbara 8% 20%

BHP Billiton WAIO 11% 17%

Fortescue 46% 11%

Total 10% 100%

Total iron ore export growth1

0

20

40

60

80

100

2000

2002

2004

2006

2008

2010

2012

2014

Share of iron ore exports1

(%)

WAIO

Rio Tinto

Vale

FMG

Rest of World

Displacement of China’s high cost domestic production by seaborne supply

Slide 8

40

60

80

100

120

140

160

180

200

20

40

60

80

100

Apr-11 Apr-12 Apr-13 Apr-14 Apr-15

Private mine operation ratePlatts 62% Fe fines CFR China price

Operation rate of Chinese private iron ore mines vs. spot iron ore price(%)

1. Private mine only, excludes SOE production.Source: SMM Survey; Platts.

(US$/dmt)

Alan Chirgwin, Vice President Marketing - Iron Ore, 14 May 2015

• Chinese high cost mines displaced as low cost seaborne supply entered the market

– primarily due to economic factors

– more displacement expected to take place in 2015

– displacement rate expected to slow as SOEs account for a higher portion of total production

1

High-cost seaborne production also displaced

Source: GTIS; China Customs.1. Data basis CY2015 guidance

Slide 9

10

20

30

40

50

60

70

80

90

100

Australia Brazil South Africa Others

Seaborne iron ore imports to China(%)

Alan Chirgwin, Vice President Marketing - Iron Ore, 14 May 2015

The iron ore cost curve expected to flatten further over time

Alan Chirgwin, Vice President Marketing - Iron Ore, 14 May 2015

• Global contestable iron ore demand growth is expected to moderate

• Seaborne supply growth is expected to continue exceeding demand growth over the medium term

• We expect to retain a favourable position on the cost curve

– underpinned by quality of our resource base and further productivity gains

Source: BHP Billiton internal estimates; Cost curve from Macquarie Research, April 2015.1. Demand refers to contestable demand. Future supply growth refers to BHP Billiton estimates of incremental supply from the majors only.

2011 2012 2013 2014 2015 2016

Cumulativesupply growth¹

Cumulativedemand growth¹

Growth in low-cost supply expected to outpace demand…(62% Fe, Mtpa, dry) Supply growth > demand

…leading to a flatter cost curve(CIF China equivalent basis, US$/t, nominal)

CY15

Cumulative volume(Mt)

BHP

CY13

Slide 10

Summary of Content

Slide 11

Market Overview: Structural Changes

Adjusting to a Changing Environment

Platforms success: transparent, liquid and efficient market

Alan Chirgwin, Vice President Marketing - Iron Ore, 14 May 2015

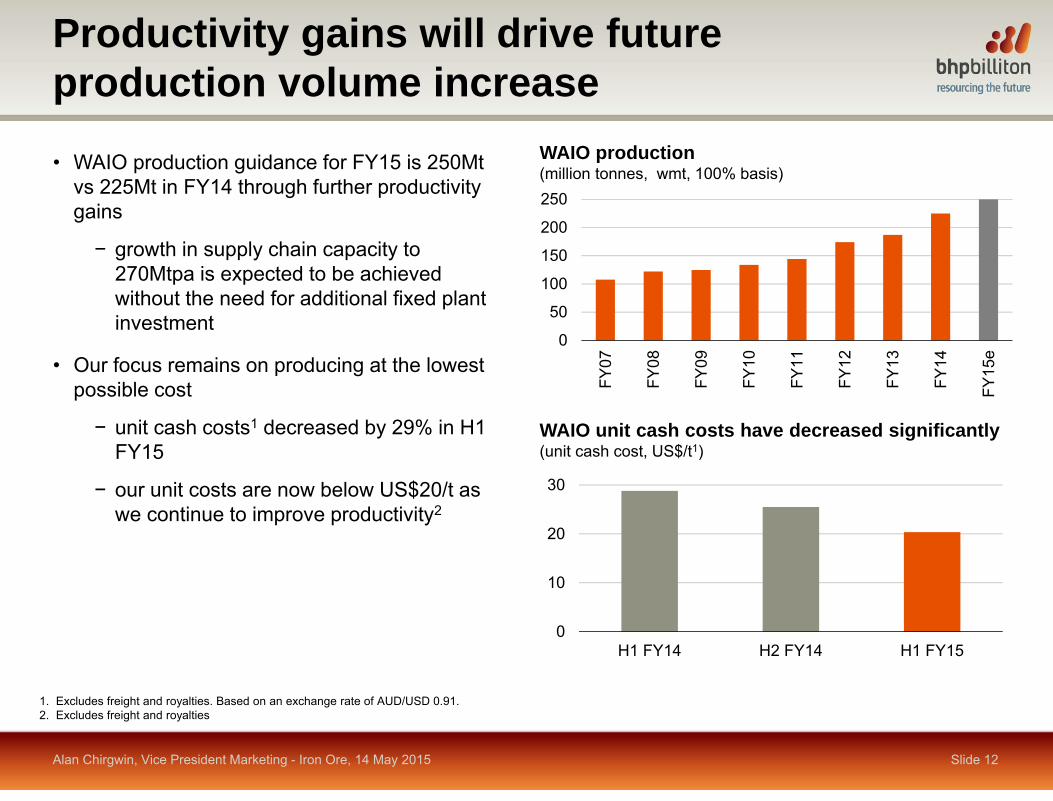

Productivity gains will drive future production volume increase

• WAIO production guidance for FY15 is 250Mt vs 225Mt in FY14 through further productivity gains

− growth in supply chain capacity to 270Mtpa is expected to be achieved without the need for additional fixed plant investment

• Our focus remains on producing at the lowest possible cost

− unit cash costs1 decreased by 29% in H1 FY15

− our unit costs are now below US$20/t as we continue to improve productivity2

Slide 12Alan Chirgwin, Vice President Marketing - Iron Ore, 14 May 2015

1. Excludes freight and royalties. Based on an exchange rate of AUD/USD 0.91.2. Excludes freight and royalties

WAIO unit cash costs have decreased significantly(unit cash cost, US$/t1)

0

10

20

30

H1 FY14 H2 FY14 H1 FY15

WAIO production(million tonnes, wmt, 100% basis)

0

50

100

150

200

250

FY07

FY08

FY09

FY10

FY11

FY12

FY13

FY14

FY15

e

Chinese mills increasingly value stable, high quality ore

• China is following the global trend towards larger blast furnaces

• This trend is driven by economic factors as well as environmental considerations

• High quality raw materials lower emissions

Blast capacity by furnace sizes (%)

Slide 13

% 0

% 20

% 40

% 60

% 80

2010 2014Source: Mysteel; BHP Billiton, External1. Calculated based on data from: 6th International congress on the Science and Technology of Ironmaking (2012), Progress and Perspective of Iron Making in China, Sha Yongzhi et al5th Chinese sintering flue gas DeSOx and DeNOx technology conference (2015), Research and Application on synchronized technologies of multiple pollutant removal in sintering flue gas, Xining Lu

Sinter De-SOx capacity1

(%)

*

*J/K/T refers to Japan, Korea and Taiwan.

m3m3

% 0

% 20

% 40

% 60

% 80

% 100

2009 2010 2011 2012 2013 2014 J/K/T<1000 1000-1999 2000-2999 >3000 m3m3

Alan Chirgwin, Vice President Marketing - Iron Ore, 14 May 2015

Newman Blend Lump is the direct charge choice of the future

Slide 14

Note: 1. Lump does not go through high temperature agglomeration processes that oxidise S to SOx gases. Sulphur content is also very low (NBLL YEJ14 = 0.02%S). Secondary fines contributes to sinter plant emissions.Source: BHP Billiton

• Newman Blend Lump (NBL) generates very low SOx emissions1)

– a benchmark for chemical quality and in-furnace performance

– low in chloride, alkalis and trace impurities

– an increasingly attractive product as gas cleaning costs increase

dust

SOx

dioxinNOx

metals

CO2

Environmental maturity curve:

Increasing complexity and cost to remove

Lump is the only true direct charge

Lump Fines Concentrate

PelletSinter

Sintering Pelletising

Blast Furnace

China

JKT, Europe

Increasing Maturity

Alan Chirgwin, Vice President Marketing - Iron Ore, 14 May 2015

Summary of Content

Slide 15

Market Overview: Structural Changes

Adjusting to a Changing Environment

Platforms success: transparent, liquid and efficient market

Alan Chirgwin, Vice President Marketing - Iron Ore, 14 May 2015

Platform sales doubled from CY13 to CY14

Slide 16

Spot transactions via globalORE and COREX(kt)

Source: globalORE; CBMX.

14,647

30,575

62,026

CY12 CY13 CY14

Members on globalORE(#)

73

113 115

CY12 CY13 CY14

+424%

191

243263

CY12 CY13 CY14

Members on COREX(#)

+58% +38%

Alan Chirgwin, Vice President Marketing - Iron Ore, 14 May 2015

Spot transactions and platform sales are informing price indices

Slide 17

Reported iron ore 62% Fe fines spot transactions* vs. Indexes (US cents/dmtu)

50

70

90

110

130

150

170

190

210

230

250

Jan-12 Apr-12 Jun-12 Sep-12 Dec-12 Mar-13 Jun-13 Sep-13 Dec-13 Mar-14 Jun-14 Sep-14 Dec-14 Mar-15

Platts 62% Fe Index TSI 62% Fe 2.0% Al2O3 Fines IndexMB 62% Fe Fines Index Argus 62% Fe Fines IndexCOREX 61.5% Fines Index Platts reported Fines spot transactionsCOREX Fines globalORE Fines

Note: include spot transactions with Fe grade range from 60% to 63.5%. CBMX launched since May.08, 2012, and globalORE launched since May.30, 2012.Source: Plstts; globalORE; CBMX; TSI; MB; CISA.

Alan Chirgwin, Vice President Marketing - Iron Ore, 14 May 2015

Summary

Alan Chirgwin, Vice President Marketing - Iron Ore, 14 May 2015

• China steel demand facing short term headwinds, mainly due to weak property market

• Long-term upside remains for steel industry, evidenced by low steel stocks per capita

• China’s net exports reached record highs in 2014, as mills focus on external markets to mitigate domestic weakness

• Low-cost seaborne supply, mainly from Australia has displaced higher cost production, Chinese and seaborne alike

• The iron ore cost curve will continue to flatten, the degree to which is dependent on the industry’s ability to debottleneck and further reduce costs

• BHP Billiton’s iron ore continues to deliver on volume commitments through productivity gains, driving greater value for shareholders

• Rising transaction volume on trading platforms highlight their success at driving market transparency, liquidity and efficiency

Slide 18

![Evolving libraries delivering new experience 102514[2]](https://img.dokumen.tips/doc/110x75/557d60d5d8b42abf3d8b513f/evolving-libraries-delivering-new-experience-1025142.jpg)