Embed Size (px)

Citation preview

INFRASTRUCTURE AND PROJECT FINANCE

CREDIT OPINION9 June 2016

Update

RATINGSDelek & Avner (Tamar Bond) Ltd.

Domicile Israel

Long Term Rating Baa3

Type Senior Secured - FgnCurr

Outlook Stable

Please see the ratings section at the end of this reportfor more information.The ratings and outlook shownreflect information as of the publication date.

Contact

Tomas O'Loughlin 44-20-7772-1798Senior Credit [email protected]

Douglas Segars 44-20-7772-1584Associate [email protected]

CLIENT SERVICES

Americas 1-212-553-1653

Asia Pacific 852-3551-3077

Japan 81-3-5408-4100

EMEA 44-20-7772-5454

Delek & Avner (Tamar Bond) Ltd.Annual Update

Summary Rating RationaleThe Baa3 ratings reflect: (1) low gas reserves risk, (2) favourable demand dynamics, (3) thestrategic importance of the Tamar gas field to Israel, (4) a diversified pool of long term gasoff-takers, anchored by a 15 year take-or-pay contract with the Israel Electric CorporationLimited (IEC, Baa3, stable), (5) flexibility in contracted off-take arrangements from 2019,(6) our expectation that Tamar will face competition from other Israeli gas fields, but notbefore 2020, (7) that the Project is located in a region and country exhibiting significantgeopolitical risk, (8) a lack of covenants binding the operator to the Project and (9) fewercreditor protections than many other rated projects.

Exhibit 1

Tamar Gas Field - Overview

Source: Netherland, Sewell & Associates, Inc, Lummus Consultants, Issuer

Credit Strengths

» Substantial gas reserves

» Strategic importance of the Tamar gas field for Israel

» Long term off-take agreements with Israel's significant gas users

» No viable alternative supply until the Leviathan field is developed

Credit Challenges

» Flexibility in off-take agreements from 2019

» Geopolitical event risk

MOODY'S INVESTORS SERVICE INFRASTRUCTURE AND PROJECT FINANCE

This publication does not announce a credit rating action. For any credit ratings referenced in this publication, please see the ratings tab on the issuer/entity page onwww.moodys.com for the most updated credit rating action information and rating history.

2 9 June 2016 Delek & Avner (Tamar Bond) Ltd.: Annual Update

Rating OutlookThe stable outlook reflects our expectation that gas sales from Tamar will meet or exceed our base case forecasts over the term of thefinancing.

Factors that Could Lead to an Upgrade

» Increased certainty around long-term revenue assumptions, either via (1) buyer commitments to maintain minimum take or payvolumes at current forecast levels for the duration of the financing or (2) the Sponsors entering into material new gas sale andpurchase agreements for the period post 2020.

Factors that Could Lead to a Downgrade

» Key off-takers exercising their option to reduce minimum take-or-pay volumes that are not replaced with alternative equivalentarrangements.

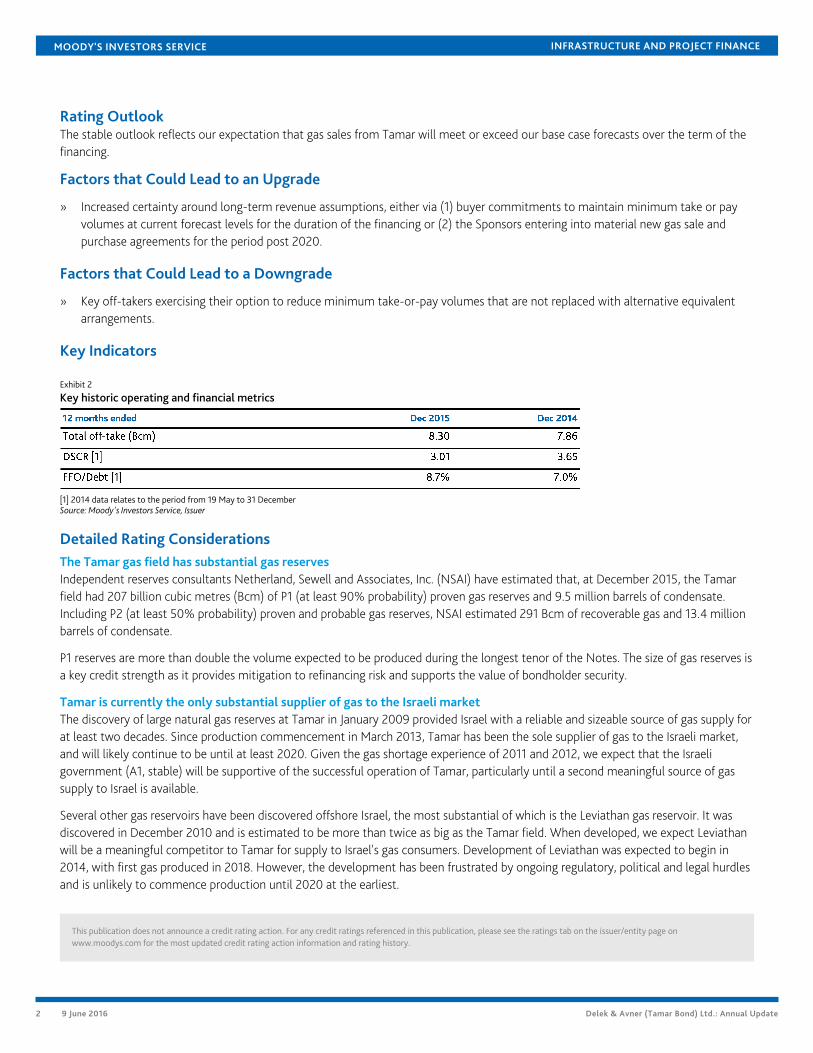

Key Indicators

Exhibit 2

Key historic operating and financial metrics

[1] 2014 data relates to the period from 19 May to 31 DecemberSource: Moody's Investors Service, Issuer

Detailed Rating ConsiderationsThe Tamar gas field has substantial gas reservesIndependent reserves consultants Netherland, Sewell and Associates, Inc. (NSAI) have estimated that, at December 2015, the Tamarfield had 207 billion cubic metres (Bcm) of P1 (at least 90% probability) proven gas reserves and 9.5 million barrels of condensate.Including P2 (at least 50% probability) proven and probable gas reserves, NSAI estimated 291 Bcm of recoverable gas and 13.4 millionbarrels of condensate.

P1 reserves are more than double the volume expected to be produced during the longest tenor of the Notes. The size of gas reserves isa key credit strength as it provides mitigation to refinancing risk and supports the value of bondholder security.

Tamar is currently the only substantial supplier of gas to the Israeli marketThe discovery of large natural gas reserves at Tamar in January 2009 provided Israel with a reliable and sizeable source of gas supply forat least two decades. Since production commencement in March 2013, Tamar has been the sole supplier of gas to the Israeli market,and will likely continue to be until at least 2020. Given the gas shortage experience of 2011 and 2012, we expect that the Israeligovernment (A1, stable) will be supportive of the successful operation of Tamar, particularly until a second meaningful source of gassupply to Israel is available.

Several other gas reservoirs have been discovered offshore Israel, the most substantial of which is the Leviathan gas reservoir. It wasdiscovered in December 2010 and is estimated to be more than twice as big as the Tamar field. When developed, we expect Leviathanwill be a meaningful competitor to Tamar for supply to Israel's gas consumers. Development of Leviathan was expected to begin in2014, with first gas produced in 2018. However, the development has been frustrated by ongoing regulatory, political and legal hurdlesand is unlikely to commence production until 2020 at the earliest.

MOODY'S INVESTORS SERVICE INFRASTRUCTURE AND PROJECT FINANCE

3 9 June 2016 Delek & Avner (Tamar Bond) Ltd.: Annual Update

Limited, but good, operating historyNoble Energy, Inc (Baa3 negative) operates the Tamar gas field. Since first gas sales in March 2013, production levels have beenconsistently in line with or above base case projections. In 2015 8.31 Bcm was produced, marginally above the base case of 8.25 Bcm.

The Project benefits from favourable demand dynamics but, post 2020, competition for supply and flexibility in off-takeagreements could reduce cash flow predictabilityIn its 2014 report, Economic Model Ltd (EML), the market consultant, forecasted that demand growth will continue to be driven byelectricity and cogeneration demand stemming from population growth, economic growth and increasing living standards. EML alsoexpected that the availability of natural gas will promote further demand, including the conversion of coal fired generation to use gas,electrification of Israel's railway system, increased water desalination, gas usage for transportation and the development of methanebased chemical and petrochemical industries.

While the market consultant's assumptions regarding electricity and cogeneration demand growth appear reasonable, we believe thereis less certainty around the timing and quantum of drivers of demand from as yet unestablished sources. If such demand eventuates,significant expansion of pipeline and production capacity would be required.

The Sponsors have entered into long-term gas sale and purchase agreements (GSPAs) with all of Israel's significant gas users. The mostsignificant off-take agreement is with Israel's state owned electricity utility, IEC, which is expected to account for around half of salesvolumes. In 2015 the GSPA with IEC was amended to reflect the partial exercise of IEC's option to increase quantities of gas it willpurchase from Tamar in the period from 2020. Recently, the Minister for National Infrastructure, Energy and Water instructed IEC toreduce coal fired generation by 15%, which is expected to be replaced with gas fired generation.

GSPAs covering the Project's entire expected production volumes through 2018 have been signed with 30 customers. The GSPAs arelong term in nature (typically 15 to 17 years) and stipulate minimum take or pay quantities of gas, with defined pricing mechanisms.

However, the GSPAs typically include a clause allowing minimum take-or-pay volumes to be reduced in the period between 2018and 2020. These volume reduction options coincide with the anticipated production start date of the Leviathan gas field. The Israeligovernment's desire is to have a second source of gas to the Israeli market to improve security of supply and increase competition. Theflexibility within off-take agreements allows Tamar's customers to contract some of their gas requirements with the Leviathan partners.

Although the market consultant forecasts that gas demand will outstrip the combined output from Tamar and Leviathan, theuncertainty around future demand and supply dynamics means the project is subject to a degree of revenue risk.

The IEC GSPA also has a gas price reset mechanism in 2021 (when the price may be reset to a prevailing market price subject to amaximum 25% change) and in 2024 (maximum 10% change), introducing further revenue uncertainty. Other GSPAs do not have suchprice reset mechanism and benefit from floor prices.

The project is resilient to low global hydrocarbon pricesThe average price of gas sold by the project has fallen marginally (by about 5% in Q4 2015 compared with Q4 2014). The pricing in asmall portion of gas sales contracts is linked to the price of Brent crude. The impact of lower pricing under these contracts was largelymitigated by i) the existence of floor prices in the oil linked contracts and ii) the off-setting impact of the pricing mechanism in the IECGSPA, which is linked to US CPI.

Liquidity AnalysisThe financing does not utilise the amortising payment structure typical of rated project financings. Instead, the debt profile involvesfive bullet payments that each account for 20% of total debt. Bullet structures potentially introduce a degree of refinancing risk and/or act as a liquidity strain at bullet maturity dates, as compared with amortising structures. To mitigate the risks associated with suchsignificant repayment requirements, the structure includes two reserving mechanisms; (1) a $100 million Debt Payment Fund that maybe used for debt service but must be fully funded prior to distributions being made; and (2) a Principal Reserve Fund cash lock up forbetween 12 and 18 months prior to each bullet repayment date. These reserves are expected to be generally sufficient to meet interestand principal payments from internal cash flows. To the extent that there are deficits we would expect amounts to be relatively smalland refinancing risk low.

MOODY'S INVESTORS SERVICE INFRASTRUCTURE AND PROJECT FINANCE

4 9 June 2016 Delek & Avner (Tamar Bond) Ltd.: Annual Update

Exhibit 3

In our base case, with the reserving mechanisms, the Issuer would be able to meet debt service from internal cash generation

Source: Moody's Investors Service, Issuer

The first series of $400 million bonds becomes due in December 2016. As of May 2016, the Issuer had approximately $345 millioncash and expect that the Issuer will have sufficient cash resources to meet this payment.

ProfileDelek & Avner (Tamar Bond) Ltd (the Issuer) is a financing vehicle owned by affiliates of Delek Group Ltd (the Sponsors). The Sponsorsown an aggregate 31.25% beneficial interest in the Tamar gas field (Tamar), an operating deepwater gas field in the East Mediterraneanoffshore Israel.

The Tamar reservoir was discovered in January 2009. It had, at December 2015, 207 billion cubic metres (Bcm) of proven (P1) gasreserves. Tamar has a demonstrated track record of successful operational performance since gas production commenced in March2013.

In May 2014 the Issuer raised $2 billion senior secured bonds (the Notes) in five series of $400 million each, due in December 2016,December 2018, December 2020, December 2023 and December 2025, respectively. Concurrently, the Issuer loaned the proceedsto the Sponsors. The Sponsor Loans are secured by a first priority fixed pledge of 90.4% of each Sponsor's Working Interest (theCollateral) and recourse against the Sponsors in connection with the Sponsor Loans will be (subject to certain exceptions) limited tothe Collateral pledged by each Sponsor.

Delek Group Ltd (unrated) is an Israeli integrated energy group listed on the Tel Aviv Stock Exchange.

MOODY'S INVESTORS SERVICE INFRASTRUCTURE AND PROJECT FINANCE

5 9 June 2016 Delek & Avner (Tamar Bond) Ltd.: Annual Update

Rating Methodology and Scorecard FactorsThe Project's rating falls within the scope of Moody's Generic Project Finance Methodology, published in December 2010. Please seethe Credit Policy page on www.moodys.com for a copy of the methodology.

Exhibit 4

Tamar Bond Rating Factors

[1] Rating from grid denotes a scorecard output and is not a Moody's published rating.Source: Moody's Investors Service

Ratings

Exhibit 5Category Moody's RatingDELEK & AVNER (TAMAR BOND) LTD.

Outlook StableSenior Secured Baa3

Source: Moody's Investors Service

MOODY'S INVESTORS SERVICE INFRASTRUCTURE AND PROJECT FINANCE

6 9 June 2016 Delek & Avner (Tamar Bond) Ltd.: Annual Update

© 2016 Moody's Corporation, Moody's Investors Service, Inc., Moody's Analytics, Inc. and/or their licensors and affiliates (collectively, "MOODY'S"). All rights reserved.

CREDIT RATINGS ISSUED BY MOODY'S INVESTORS SERVICE, INC. AND ITS RATINGS AFFILIATES ("MIS") ARE MOODY'S CURRENT OPINIONS OF THE RELATIVE FUTURE CREDITRISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES, AND CREDIT RATINGS AND RESEARCH PUBLICATIONS PUBLISHED BY MOODY'S ("MOODY'SPUBLICATIONS") MAY INCLUDE MOODY'S CURRENT OPINIONS OF THE RELATIVE FUTURE CREDIT RISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKESECURITIES. MOODY'S DEFINES CREDIT RISK AS THE RISK THAT AN ENTITY MAY NOT MEET ITS CONTRACTUAL, FINANCIAL OBLIGATIONS AS THEY COME DUE AND ANYESTIMATED FINANCIAL LOSS IN THE EVENT OF DEFAULT. CREDIT RATINGS DO NOT ADDRESS ANY OTHER RISK, INCLUDING BUT NOT LIMITED TO: LIQUIDITY RISK, MARKETVALUE RISK, OR PRICE VOLATILITY. CREDIT RATINGS AND MOODY'S OPINIONS INCLUDED IN MOODY'S PUBLICATIONS ARE NOT STATEMENTS OF CURRENT OR HISTORICALFACT. MOODY'S PUBLICATIONS MAY ALSO INCLUDE QUANTITATIVE MODEL-BASED ESTIMATES OF CREDIT RISK AND RELATED OPINIONS OR COMMENTARY PUBLISHEDBY MOODY'S ANALYTICS, INC. CREDIT RATINGS AND MOODY'S PUBLICATIONS DO NOT CONSTITUTE OR PROVIDE INVESTMENT OR FINANCIAL ADVICE, AND CREDITRATINGS AND MOODY'S PUBLICATIONS ARE NOT AND DO NOT PROVIDE RECOMMENDATIONS TO PURCHASE, SELL, OR HOLD PARTICULAR SECURITIES. NEITHER CREDITRATINGS NOR MOODY'S PUBLICATIONS COMMENT ON THE SUITABILITY OF AN INVESTMENT FOR ANY PARTICULAR INVESTOR. MOODY'S ISSUES ITS CREDIT RATINGSAND PUBLISHES MOODY'S PUBLICATIONS WITH THE EXPECTATION AND UNDERSTANDING THAT EACH INVESTOR WILL, WITH DUE CARE, MAKE ITS OWN STUDY ANDEVALUATION OF EACH SECURITY THAT IS UNDER CONSIDERATION FOR PURCHASE, HOLDING, OR SALE.

MOODY'S CREDIT RATINGS AND MOODY'S PUBLICATIONS ARE NOT INTENDED FOR USE BY RETAIL INVESTORS AND IT WOULD BE RECKLESS AND INAPPROPRIATE FORRETAIL INVESTORS TO USE MOODY'S CREDIT RATINGS OR MOODY'S PUBLICATIONS WHEN MAKING AN INVESTMENT DECISION. IF IN DOUBT YOU SHOULD CONTACTYOUR FINANCIAL OR OTHER PROFESSIONAL ADVISER. ALL INFORMATION CONTAINED HEREIN IS PROTECTED BY LAW, INCLUDING BUT NOT LIMITED TO, COPYRIGHT LAW,AND NONE OF SUCH INFORMATION MAY BE COPIED OR OTHERWISE REPRODUCED, REPACKAGED, FURTHER TRANSMITTED, TRANSFERRED, DISSEMINATED, REDISTRIBUTEDOR RESOLD, OR STORED FOR SUBSEQUENT USE FOR ANY SUCH PURPOSE, IN WHOLE OR IN PART, IN ANY FORM OR MANNER OR BY ANY MEANS WHATSOEVER, BY ANYPERSON WITHOUT MOODY'S PRIOR WRITTEN CONSENT.

All information contained herein is obtained by MOODY'S from sources believed by it to be accurate and reliable. Because of the possibility of human or mechanical error as wellas other factors, however, all information contained herein is provided "AS IS" without warranty of any kind. MOODY'S adopts all necessary measures so that the information ituses in assigning a credit rating is of sufficient quality and from sources MOODY'S considers to be reliable including, when appropriate, independent third-party sources. However,MOODY'S is not an auditor and cannot in every instance independently verify or validate information received in the rating process or in preparing the Moody's Publications.

To the extent permitted by law, MOODY'S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability to any person or entity for anyindirect, special, consequential, or incidental losses or damages whatsoever arising from or in connection with the information contained herein or the use of or inability to use anysuch information, even if MOODY'S or any of its directors, officers, employees, agents, representatives, licensors or suppliers is advised in advance of the possibility of such losses ordamages, including but not limited to: (a) any loss of present or prospective profits or (b) any loss or damage arising where the relevant financial instrument is not the subject of aparticular credit rating assigned by MOODY'S.

To the extent permitted by law, MOODY'S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability for any direct or compensatorylosses or damages caused to any person or entity, including but not limited to by any negligence (but excluding fraud, willful misconduct or any other type of liability that, for theavoidance of doubt, by law cannot be excluded) on the part of, or any contingency within or beyond the control of, MOODY'S or any of its directors, officers, employees, agents,representatives, licensors or suppliers, arising from or in connection with the information contained herein or the use of or inability to use any such information.

NO WARRANTY, EXPRESS OR IMPLIED, AS TO THE ACCURACY, TIMELINESS, COMPLETENESS, MERCHANTABILITY OR FITNESS FOR ANY PARTICULAR PURPOSE OF ANY SUCHRATING OR OTHER OPINION OR INFORMATION IS GIVEN OR MADE BY MOODY'S IN ANY FORM OR MANNER WHATSOEVER.

Moody's Investors Service, Inc., a wholly-owned credit rating agency subsidiary of Moody's Corporation ("MCO"), hereby discloses that most issuers of debt securities (includingcorporate and municipal bonds, debentures, notes and commercial paper) and preferred stock rated by Moody's Investors Service, Inc. have, prior to assignment of any rating,agreed to pay to Moody's Investors Service, Inc. for appraisal and rating services rendered by it fees ranging from $1,500 to approximately $2,500,000. MCO and MIS also maintainpolicies and procedures to address the independence of MIS's ratings and rating processes. Information regarding certain affiliations that may exist between directors of MCO andrated entities, and between entities who hold ratings from MIS and have also publicly reported to the SEC an ownership interest in MCO of more than 5%, is posted annually atwww.moodys.com under the heading "Investor Relations — Corporate Governance — Director and Shareholder Affiliation Policy."

Additional terms for Australia only: Any publication into Australia of this document is pursuant to the Australian Financial Services License of MOODY'S affiliate, Moody's InvestorsService Pty Limited ABN 61 003 399 657AFSL 336969 and/or Moody's Analytics Australia Pty Ltd ABN 94 105 136 972 AFSL 383569 (as applicable). This document is intendedto be provided only to "wholesale clients" within the meaning of section 761G of the Corporations Act 2001. By continuing to access this document from within Australia, yourepresent to MOODY'S that you are, or are accessing the document as a representative of, a "wholesale client" and that neither you nor the entity you represent will directly orindirectly disseminate this document or its contents to "retail clients" within the meaning of section 761G of the Corporations Act 2001. MOODY'S credit rating is an opinion asto the creditworthiness of a debt obligation of the issuer, not on the equity securities of the issuer or any form of security that is available to retail investors. It would be recklessand inappropriate for retail investors to use MOODY'S credit ratings or publications when making an investment decision. If in doubt you should contact your financial or otherprofessional adviser.

Additional terms for Japan only: Moody's Japan K.K. ("MJKK") is a wholly-owned credit rating agency subsidiary of Moody's Group Japan G.K., which is wholly-owned by Moody'sOverseas Holdings Inc., a wholly-owned subsidiary of MCO. Moody's SF Japan K.K. ("MSFJ") is a wholly-owned credit rating agency subsidiary of MJKK. MSFJ is not a NationallyRecognized Statistical Rating Organization ("NRSRO"). Therefore, credit ratings assigned by MSFJ are Non-NRSRO Credit Ratings. Non-NRSRO Credit Ratings are assigned by anentity that is not a NRSRO and, consequently, the rated obligation will not qualify for certain types of treatment under U.S. laws. MJKK and MSFJ are credit rating agencies registeredwith the Japan Financial Services Agency and their registration numbers are FSA Commissioner (Ratings) No. 2 and 3 respectively.

MJKK or MSFJ (as applicable) hereby disclose that most issuers of debt securities (including corporate and municipal bonds, debentures, notes and commercial paper) and preferredstock rated by MJKK or MSFJ (as applicable) have, prior to assignment of any rating, agreed to pay to MJKK or MSFJ (as applicable) for appraisal and rating services rendered by it feesranging from JPY200,000 to approximately JPY350,000,000.

MJKK and MSFJ also maintain policies and procedures to address Japanese regulatory requirements.

REPORT NUMBER 1026983