Embed Size (px)

Citation preview

8/12/2019 Definations Section Handout PDP 13 KTBA FE and ST on Services SUH

http://slidepdf.com/reader/full/definations-section-handout-pdp-13-ktba-fe-and-st-on-services-suh 1/23

General Concepts of Federal Excise and Sales Tax On Services in PakistanHandout PDP – 2013

Karachi Tax Bar Association Page 1

OUTPUT TAX

The Federal Excise Act, 2005/ Provincial OrdinancesThe Sales Tax Act, 1990- Section 2(20)

“Output tax”, in relation to a registered person, means -

(a) tax levied under this Act on a supply of goods, made by the person;(b) tax levied under the Federal Excise Act, 2005 in sales tax mode as a duty of excise on the manufacture or production of thegoods, or the rendering or providing of the services, by the person ;(c) Provincial sales tax levied on services rendered or provided by the person ;

The Sindh Sales Tax on Services Act 2011 Section 2(62)

Output Tax in relation to a registered person, means the tax levied under this Act on the services provided or rendered by the

person

The Punjab Sales Tax on Services Act 2012 NO Definition

The Khyber Pakhtunkhwa Finance Act 2013 NO Definition

PERSON

The Federal Excise Act, 2005/ Provincial OrdinancesThe Sales Tax Act, 1990 - Section 2(18)

The Sindh Sales Tax on Services Act 2011 Section 2(63)

The Punjab Sales Tax on Services Act 2012 Section 2(29)

The Khyber Pakhtunkhwa Finance Act 2013 Section 2(36)

“person” means -

(a) an individual;(b) an association of individuals or persons;(c) a company;

(d) Federal Government;(e) a Provincial Government;(f) a local authority or local government; or(g) a foreign government, a political subdivision of a foreign government, or public international organization

8/12/2019 Definations Section Handout PDP 13 KTBA FE and ST on Services SUH

http://slidepdf.com/reader/full/definations-section-handout-pdp-13-ktba-fe-and-st-on-services-suh 2/23

General Concepts of Federal Excise and Sales Tax On Services in PakistanHandout PDP – 2013

Karachi Tax Bar Association Page 2

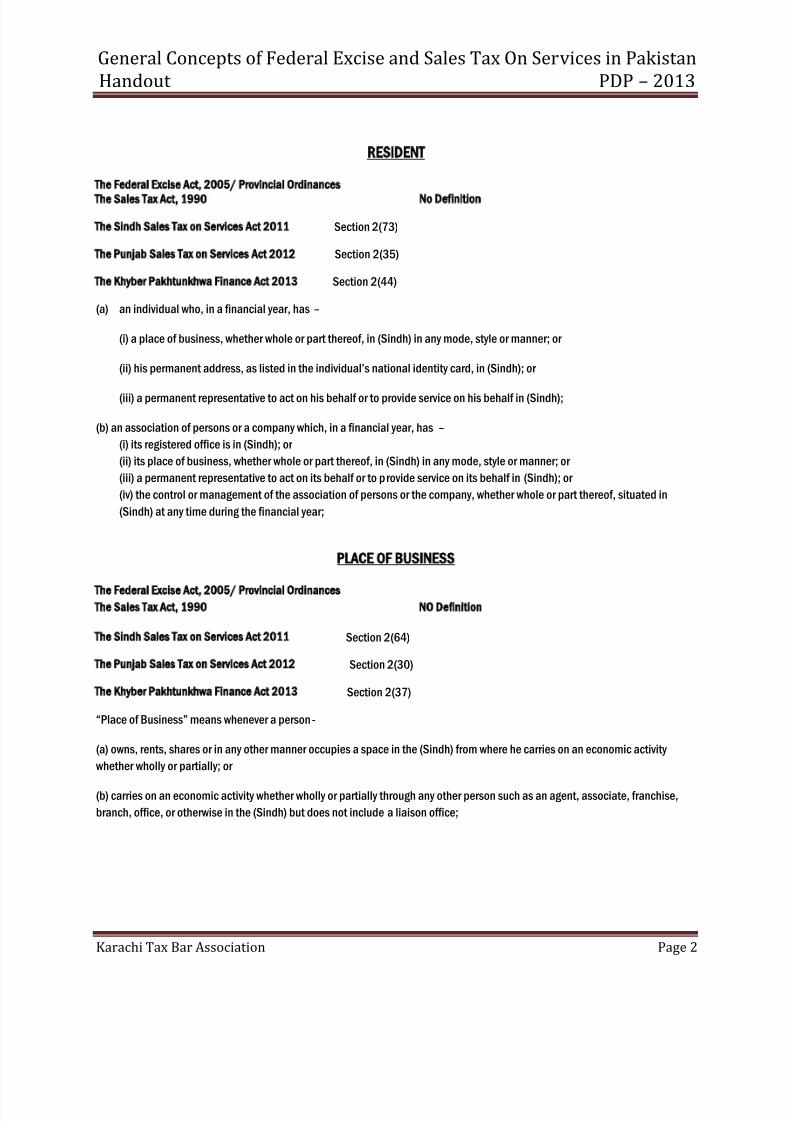

RESIDENT

The Federal Excise Act, 2005/ Provincial OrdinancesThe Sales Tax Act, 1990 No Definition

The Sindh Sales Tax on Services Act 2011 Section 2(73)

The Punjab Sales Tax on Services Act 2012 Section 2(35)

The Khyber Pakhtunkhwa Finance Act 2013 Section 2(44)

(a) an individual who, in a financial year, has –

(i) a place of business, whether whole or part thereof, in (Sindh) in any mode, style or manner; or

(ii)his permanent address, as listed in the individual’s national identity card, in (Sindh); or

(iii) a permanent representative to act on his behalf or to provide service on his behalf in (Sindh);

(b) an association of persons or a company which, in a financial year, has – (i) its registered office is in (Sindh); or(ii) its place of business, whether whole or part thereof, in (Sindh) in any mode, style or manner; or(iii) a permanent representative to act on its behalf or to provide service on its behalf in (Sindh); or(iv) the control or management of the association of persons or the company, whether whole or part thereof, situated in(Sindh) at any time during the financial year;

PLACE OF BUSINESS

The Federal Excise Act, 2005/ Provincial OrdinancesThe Sales Tax Act, 1990 NO Definition

The Sindh Sales Tax on Services Act 2011 Section 2(64)

The Punjab Sales Tax on Services Act 2012 Section 2(30)

The Khyber Pakhtunkhwa Finance Act 2013 Section 2(37)

“Place of Business” means whenever a person -

(a) owns, rents, shares or in any other manner occupies a space in the (Sindh) from where he carries on an economic activity whether wholly or partially; or

(b) carries on an economic activity whether wholly or partially through any other person such as an agent, associate, franchise,branch, office, or otherwise in the (Sindh) but does not include a liaison office;

8/12/2019 Definations Section Handout PDP 13 KTBA FE and ST on Services SUH

http://slidepdf.com/reader/full/definations-section-handout-pdp-13-ktba-fe-and-st-on-services-suh 3/23

General Concepts of Federal Excise and Sales Tax On Services in PakistanHandout PDP – 2013

Karachi Tax Bar Association Page 3

TAXABLE SERVICES

The Federal Excise Act, 2005/ Provincial Ordinances Section 3 of the FE Act and PST Ordinances

the FE Act

3(d) services provided in Pakistan including the services originated outside but rendered in Pakistan;”

Specified in first schedule to the FE Act

The PST Ordinances

Subject to the provisions of this ordinance there shall be charged, levied and paid a tax ……on taxable services rendered orprovided in the (Balochistan)

Specified in the Schedule

The Sindh Sales Tax on Services Act 2011 Section 3

The Punjab Sales Tax on Services Act 2012 Section 3

The Khyber Pakhtunkhwa Finance Act 2013 Part 3 chapter 1 Section 19

A taxable service is a service listed in the Second Schedule to this Act

Schedules of Taxable and Services

Services Excisable under the FE Act (First Schedule TABLE II)

S.No. Description of goods Heading/Sub-heading Number

Rate of Duty

(1) (2) (3) (4)1 Advertisement on closed circuit T.V. 9802.3000 16% of the charges2 Advertisement on cable T.V. network 9802.5000 16% of the charges2a Advertisements in news papers and periodicals (excluding

Classified advertisements), and on hoarding boards, poles Signsand sign boards

9802.4000and9802.9000

16% of the charges

3 Facilities for travel 98.03(a) Services provided or rendered in respect of travel by air ofpassenger within the

territorial jurisdiction of Pakistan

9803.1000 16% of the charges plusRs.20 per ticket

(b)Services provided or rendered in respect of travel by air ofpassengers embarking on international journey from Pakistan

(i)Economy and economy plus

(ii)Club, business and first class.

9803.1100

Rs.3,840

Rs.6,8404 Inland carriage of goods by air 9804.1000 16% of the charges

8/12/2019 Definations Section Handout PDP 13 KTBA FE and ST on Services SUH

http://slidepdf.com/reader/full/definations-section-handout-pdp-13-ktba-fe-and-st-on-services-suh 4/23

General Concepts of Federal Excise and Sales Tax On Services in PakistanHandout PDP – 2013

Karachi Tax Bar Association Page 4

5 Shipping agents 9805.1000 (i) Rs.200 per house-billof lading in case ofCommon carriers IntFreight ii) 16% of thecharges in other case

6 Telecommunication services 98.12 19.5 % of charges

7 ***]8 Services provided by banking companies, insurance companies

of the cooperative financing societies, modarabs, musharikas,leasing companies, foreign exchange dealers, mom-bankingfinancial institutions, Assets Management Companies and otherpersons dealing in any such services.

98.13 16% of the charges

9 ***]10 ***]11 Franchise services 9823.0000 10% of the charges12 ***]13 Services provided of rendered by stock brokers 9819.1000 16% of the charges

14 Services provided or rendered by port and terminal operators inrelation to imports excluding stevedoring services.

9819.9090 16% of the charges

Services Taxable under the PST Ordinances (Islamabad and Balochistan)

S.No. Description of goods(1) (2)1. Services provided or rendered by hotels, marriage halls, lawns, clubs and caterers

(a) Services provided or rendered by hotels[ ]

(c ) Services provided or rendered by clubs(d) Services provided or rendered by caterers

2 Advertisement TV and radio excluding advertisements(i) if sponsored by a Government Agency for health education(ii) if sponsored by Population Welfare Division relating to Sathi educational promotion campaign funded by USAID; and(iii) public service message if telecast on television by World Wildlife Funds for Nature of UNICEF

3 Services provided or rendered by persons authorized to transact business on behalf of others(a) Custom Agents(b) Ship chandlers(c) Stevedores(d) Courier Services

Services Taxable under The KPK Act(Second Schedule)

S.No. Description Classification Rate of Tax(1) (2) (3) (4)

1. Services provided or rendered by hotels, marriage halls, lawns, clubs andcaterers and services ancillary thereto.

98.01 16%

8/12/2019 Definations Section Handout PDP 13 KTBA FE and ST on Services SUH

http://slidepdf.com/reader/full/definations-section-handout-pdp-13-ktba-fe-and-st-on-services-suh 5/23

General Concepts of Federal Excise and Sales Tax On Services in PakistanHandout PDP – 2013

Karachi Tax Bar Association Page 5

2. Services provided or rendered for personal care by beauty parlors, beautyclinics, slimming clinics

98.10 16%

3. Services provided and rendered by laundries and dry cleaners. 98.11 16%4. Telecommunication Services 98.12 19.5%5 Services provided or rendered by persons

authorized to transact business on behalf of others:-i. Customs agents;ii. Ship chandlers;iii. Stevedores; andiv. Ship management service

98.05 16%

6 Advertisement on T.V and Radio, newspapers, periodicals and Magazinesexcluding advertisements.(i) if sponsored by a Government Agency(ii) financed out of funds provided under grant in-aid agreement; andConveying public service messages.

98.02 16%

7 Advertisement on close Circuit TV or Cable TV 9802.3000 16%8 Courier services. 98.08 16%9 Services provided or rendered in respect of insurance to a policy holder by

an insurer, including a re-insurer:-i. Goods insurance.ii. Fire insuranceiii. Theft insurance.iv. Marine insurance. Other insurance

98.13 16%

10 Services provided by banking companies or nonbanking financialinstitutions including but not limited to all non-interest based servicesprovided or rendered against a consideration in form of a fee orcommission or charges.

98.13 16%

11 Services provided or rendered by the Stockbrokers. 98.19 16%

Services Taxable under The Sindh Act (Second Schedule)

With reduced rates as per notification SRB.3-4/8 2013 dated July 01 2013

S.No. Description Tariff Heading Rate of Tax(1) (2) (3) (4)

1 Telecommunication Services 98.12 19.5%2 Services provided or rendered by hotels, restaurants, marriage halls,

lawns, clubs and caterers.98.01 16%

3 Advertisement on TV, radio, CCT, newspaper, cable, poles, billboards, web or internet

98.02 16%

4 Services provides by stevedores, ship management service, , customsagents, advertisement agents, ship chandlers, sponsorship services,business support servicesShipping agents and freight forwarding agents

98.05 16%

Rs.500 per bill oflading

5 Services provided or rendered by property developers or promoters fora) Development of purchased or leased land for conversion intoresidential or commercial plots.(b) Construction of residential or commercial units.

9807.0000 Rs.100 per squareyard for land and,Rs.50 per squarefeet for constructedarea.

8/12/2019 Definations Section Handout PDP 13 KTBA FE and ST on Services SUH

http://slidepdf.com/reader/full/definations-section-handout-pdp-13-ktba-fe-and-st-on-services-suh 6/23

General Concepts of Federal Excise and Sales Tax On Services in PakistanHandout PDP – 2013

Karachi Tax Bar Association Page 6

6 Courier services 9808.0000 16%7 Services provided or rendered by persons engaged in contractual

execution of work or furnishing supplies9809.0000 16%

8 Services provided or rendered for personal care by beauty parlors,beauty clinics, slimming clinics or centers and others

98.10 10

9 Services provided or rendered by banking companies, Insurancecompanies, cooperative financing societies, modarabas, musharikas,leasing companies, foreign exchange dealers, non-banking financialinstitutions and other persons dealing in any such services.

98.13 16%

10 Architects or town plannersContractors of buildings (i.e water supply, gas supply, electrical andmechanical works etc.)

98.14 16%16%

11 Services provided or rendered by professionals and consultants, etc.Legal practitioners and consultants Accountants and auditors.Management consultantsSoftware or IT based system development consultants Tax consultants

98.15

9815.20009815.30009815.40009815.6000

9815.9000

4416%16%

412 Services provided or rendered by specialized agenciesSecurity agencyMarket research agency

98.189818.10009818.3000

1016%

13 Services provided or rendered by specified personsor businessesStockbrokers and commodity brokersMoney exchangerSurveyorsOutdoor photographers and videographersManagement consultantsServices provided or rendered by port operators, airport operators,airport ground service providersand terminal operators

98.19

9819.10009819.20009819.50009819.70009819.9300

9819.9090

16%16%16%16%16%

16%

14 Service provided or rendered by specialized Workshops or undertakings. Auto workshops, including authorized service stationsWorkshops for industrial machinery, constructions

98.20

9820.10009820.2000

16%16%

15 Services provided or rendered in specified fieldsHealth care centre, gyms or physical fitness center, etcBody massage centerPedicure centre

98.21 9821.10009821.40009821.5000

16%44

16 Franchise services 9823.0000 1017 Construction services

Management services including fund and assets management services Airport services Tracking Services

Security alarm servicesServices provided by motels and guest housesEvent Management services including the services by eventphotographers, event videographer and the persons related to suchevent managementExhibition services.

98.24 416%

16%

16%16%16%16%16%

16%18 Public bonded warehouses 9828.0000 16%

8/12/2019 Definations Section Handout PDP 13 KTBA FE and ST on Services SUH

http://slidepdf.com/reader/full/definations-section-handout-pdp-13-ktba-fe-and-st-on-services-suh 7/23

General Concepts of Federal Excise and Sales Tax On Services in PakistanHandout PDP – 2013

Karachi Tax Bar Association Page 7

19 Labour and manpower supply services 9829.0000 16%

20 Services provided in the matter of manufacturingor processing for others on toll basis

9830.0000 16%

21 Race Club:

(a) Services of entry/admission

(b) Other services

9831.0000 (a) Rs.200

per entry ticket orentry pass(b) 16%]

Services Taxable under The Punjab Act (Second Schedule)

S.No. Description Classification Rate of Tax(1) (2) (3) (4)

1 Services provided by hotels, “motels, guest house, marriage halls, clubs andcaterers etc.

9801.0000 16%

2 Advertisement on television and radio, excluding advertisements – (a) sponsored by an agency of the Federal or ProvincialGovernment for health education;(b) financed out of funds provided by a Government under grant-in aidagreement; and(c) conveying public service message, if telecast on television by the WorldWide Fund for Nature (WWF) or United Nations Children’s Fund (UNICEF).

9802.1000and9802.2000

16%

3 Services provided by persons authorized to transact business on behalf ofothers – (a) customs agents;(b) ship chandlers; and(c) Stevedores.

9805.40009805.80009805.2000

16%

4 Courier services. 9808.0000 16%5 Advertisement on a cable television. 9802.5000 16%6 Telecommunication services 98.12 19.5%7 Services provided in respect of insurance to a policy holder by an insurer,

including a re-insurerGoods, fire, theft, marine and other insurance

98.13 16%

8 Services provided by Banking Companies or Non-Banking FinancialInstitutions including but not limited to all noninterest based servicesprovided against a consideration in form or a fee or commission or charge

98.13 16%

9 Services provided by the stock brokers. 9819.1000 16%10 Services provided by shipping agents 9805.1000 16%11 Services provided by Restaurants. 9801.2000 16%12 Advertisements on hoarding boards, pole signs and sign boards and on

closed circuit TV, Websites or internet9802.0000 16%

13 Franchise Service. 9823.0000 16%14 Construction services 9824.0000

and9814.2000

(i) Rs.100 per

square yard forlanddevelopmentand,(ii)Rs.50 persquare feet forbuildingconstruction.

15 Services provided by property developers and promoters (including allied 9807.0000 16%

8/12/2019 Definations Section Handout PDP 13 KTBA FE and ST on Services SUH

http://slidepdf.com/reader/full/definations-section-handout-pdp-13-ktba-fe-and-st-on-services-suh 8/23

General Concepts of Federal Excise and Sales Tax On Services in PakistanHandout PDP – 2013

Karachi Tax Bar Association Page 8

services) respective subheading 98.14

16 Services provided by persons engaged in contractual execution of work orfurnishing supplies.

9809.0000 16%

17 Services provided by a foreign exchange dealer or exchange company or

money changer/money exchanger

9813.9000

9819.2000

16%

18 Services provided for personal care by beauty parlors, clinics, sliming clinicsincluding cosmetic and plastic surgery by such parlors/clinics.

9810.00009848.00009847.00009821.40009821.5000

16%

19 Management consultancy services including fund and asset managementservices.

9815.40009826.0000

16%

20 Services provided by port operators (including airports and dry ports) andallied services provided at ports and services provided by terminal operatorsincluding services in respect of public bonded warehouses

9838.0000 16%

21 Freight forwarding agents. 9805.3000 Rs.400 per billof lading

22 Services provided by software or IT-based system development consultants. 9815.6000 16%23 Services provided by technical, scientific & engineering consultants. 9815.5000

9819.940016%

24 Services provided by other consultants 9815.9000 16%25 Services provided by tour operators (other than

Hajj and Umrah)9805.5100 16%

26 Manpower recruitment agents 9805.6000 16%27 Services provided by security agency. 9818.1000 16%28 Services provided in respect of mining of minerals, oil & gas including

related surveys and allied activities. ---------------16%

29 Services provided by advertising agents 9805.7000 16%30 Services provided by share transfer agents. 9805.9000 16%31 Services provided by business support services 9805.9200 16%

32 Services provided by property dealers. 9806.2000 16%33 Services provided by fashion designers. 9834.0000 16%34 Services provided by architects, town planners and interior decorators. 9814.1000

9814.900016%

35 Services provided in respect of rent-a-car 9819.3000 16%36 Services provided by car/automobile dealers. 9806.3000 16%37 Services provided in respect of manufacturing or processing on toll or job

basis (against processing charges).9868.0000 16%

EXEMPT SERVICES

The Federal Excise Act, 2005/ Provincial Ordinances Section 16- 3rd Schedule to the FE ActSales Tax Act, 1990

All services provided or rendered except such services as are specified in the First schedule shall be exempt from whole of exciseduty levied under section 3.

Provided that services specified in the third schedule shall be exempt from duty.

8/12/2019 Definations Section Handout PDP 13 KTBA FE and ST on Services SUH

http://slidepdf.com/reader/full/definations-section-handout-pdp-13-ktba-fe-and-st-on-services-suh 9/23

General Concepts of Federal Excise and Sales Tax On Services in PakistanHandout PDP – 2013

Karachi Tax Bar Association Page 9

The Sindh Sales Tax on Services Act 2011 Section 2(40)

An “exempt service” means a service which is exemp t from tax under Section 10

The Punjab Sales Tax on Services Act 2012 Section 2(20)

An “Exempt service” means a service which is exempt from the tax under Section 12

The Khyber Pakhtunkhwa Finance Act 2013 Section 2(25)

An “exempt service” means a service which is exempt from the tax under Section 28

All of above exemption sections are identical as below

10. Exemptions. — (1) Notwithstanding the provisions of section 8, the Board, may, with the approval of the Government andsubject to such conditions and restrictions as it may impose, by notification in the official Gazette:

(a) exempt any taxable service from the whole or any part of the tax chargeable under this Act;

(b) exempt any taxable service provided by a specific person or a class of persons from the whole or any part of the tax chargeableunder this Act;

(c) exempt any recipient of services or class of such recipients, including international organizations and institutions, from thepayment of the whole or any part of the tax payable under this Act; and

(d) exempt any person or class of persons from the whole or any part of the tax chargeable under this Act.

(2) The exemption under sub-section (1) may be allowed from any previous date specified in the notification issued under sub -section (1).

A comparative list of services exempted from FED or Sales tax under the FE Act, PST Ordinances, Sindh Act or Punjab Act.Presently there is no list of exempt services in KPK Act.

Tariff Heading FE Act /PST Sindh Act Punjab Act98.01 Services of restaurants and caters with

turnover does not exceeds Rs.3.6 M in afinancial year, and marriage hall andlawns less 800 square yards --Except- air-conditioned, in a premisesof club or hotel, franchise, have morethan one outlets, utility bills exceedsRs.40,000 in any month

9801.40009801.6000

Services of clubs whose initial fee formembership does not exceeds

8/12/2019 Definations Section Handout PDP 13 KTBA FE and ST on Services SUH

http://slidepdf.com/reader/full/definations-section-handout-pdp-13-ktba-fe-and-st-on-services-suh 10/23

General Concepts of Federal Excise and Sales Tax On Services in PakistanHandout PDP – 2013

Karachi Tax Bar Association Page 10

Rs.30,000 and monthly fee uptoRs.1,000.-Refundable security deposits andcontributions for the welfare of clubstaff

98.02 - Advertisements financed outof funds provided under grants-in-aid agreements.- Advertisement in newspaperand periodicals- Cable TV operators

- Advertisements financed out of fundsprovided under grants-in-aidagreements.- Advertisement in newspaper andperiodicals

Advertisement sponsored by anagency of the federal orprovincial government for healtheducation,financed out of funds providedby a government under grant-in-aid agreement andconveying public servicemessage, if telecasted ontelevision by the World Wide Fund(WWF) or United NationsChildren’s Fund (UNICEF).

98.03 International Journey by air forHajj passengers, diplomats andsupernumerary crew.

98.09 Persons engaged in contractualexecution of work or furnishing ofsupplies subject to certain conditions,including contracts with total valuedoes not exceeds Rs.50 M in a financialyear and value of services involve uptoRs.10 M.-printing of text books

Persons engaged in contractualexecution of work or furnishing ofsupplies subject to certainconditions, including contracts with total value does not exceedsRs.50 M.-Printing of books

98.10 Services of beauty parlors /clinics lessthan Rs.3.6 M in a financial year.

Services of beauty parlors /clinics less than Rs.3.6 M in afinancial year.Except- air-conditioned, in apremises of club or hotel,franchise, have more than oneoutlets, annual utility billsexceeds Rs.600,000

98.12 Telecom services ofinternational leased lines andinternet related services.

Telecom services of internationalleased lines and internet relatedservices with a monthly fee uptoRs.1,500.

Telecom services of internationalleased lines and internet relatedservice.

98.13 Banking companies and non-banking financial companies inrespect of Hajj and Umarah,cheque book, musharaka and

modarba financing, utility billscollection, cheque return, andamount of mark up or interest

Banking companies and non-bankingfinancial companies in respect of Hajjand Umarah, cheque book, musharakaand modarba financing, utility bills

collection.and amount of mark up or interest

amount of mark up or interest

98.13 Life, health, crop, live stock andmarine insurance for exports

Life, health, crop and marine insurancefor exports

Life, health, crop and marineinsurance for exports

98.15 Export of services of Software and ITbased system development consultants

98.23 Franchise services payable by vendors of the auto partsindustry

8/12/2019 Definations Section Handout PDP 13 KTBA FE and ST on Services SUH

http://slidepdf.com/reader/full/definations-section-handout-pdp-13-ktba-fe-and-st-on-services-suh 11/23

General Concepts of Federal Excise and Sales Tax On Services in PakistanHandout PDP – 2013

Karachi Tax Bar Association Page 11

98.24 Construction services related to – commercial or industrial projects doesnot exceed Rs.50 M with a componentof services less than Rs.10 M.- Projects of developing and promoting

of land into buildings which payreduced rate of tax.- construction and repair of roads,ports, airports, railway, terminals,bridges, Government building ect.-construction of EPZ, SEZs, diplomaticbuildings and organization exempt fromincome tax.-projects of private residential houses

Construction services related to– commercial or industrialprojects does not exceed Rs.50M.- Projects where tax paid by

developers and promoters.- Government civil works.-construction of industrial zones,diplomatic buildings andorganization exempt from incometax.-construction under internationaltenders-projects of private residentialhouses

TAXABLE SERVICES

The Federal Excise Act, 2005/ Provincial Ordinances Section 3 of the FE Act and PST Ordinances

the FE Act

3(d) services provided in Pakistan including the services originated outside but rendered in Pakistan;”

Specified in first schedule to the FE Act

The PST Ordinances

Subject to the provisions of this ordinance there shall be charged, levied and paid a tax ……on taxable s ervices rendered orprovided in the (Balochistan)

Specified in the Schedule

The Sindh Sales Tax on Services Act 2011 Section 3

The Punjab Sales Tax on Services Act 2012 Section 3

The Khyber Pakhtunkhwa Finance Act 2013 Part 3 chapter 1 Section 19

A taxable service is a service listed in the Second Schedule to this Act, which is provided:

(a) by a registered person from his registered office or place of business in (Sindh);(b) in the course of an economic activity, including in the commencement or termination of the activity.

Explanation: This sub-Section deals with services provided by registered persons, regardless of whether those services areprovided to resident persons or non-resident persons.

(2) A service that is not provided by a registered person shall be treated as a taxable service if the service is listed in the SecondSchedule to this Act and:

(a) is provided to a resident person;(b) by a non-resident person in the course of an economic activity, including in the commencement or termination of the activity.

8/12/2019 Definations Section Handout PDP 13 KTBA FE and ST on Services SUH

http://slidepdf.com/reader/full/definations-section-handout-pdp-13-ktba-fe-and-st-on-services-suh 12/23

General Concepts of Federal Excise and Sales Tax On Services in PakistanHandout PDP – 2013

Karachi Tax Bar Association Page 12

Explanation: This sub-Section deals with services provided by non-resident persons to resident persons whether or not said resident person is an end consumer of such services.

(3) For the purposes of sub-Section (2), where a person has a registered office or place of business in Sindh and another outsideSindh, the registered office or place of business in Sindh and that outside Sindh shall be treated as separate legal persons.

(4) The Board may, with the approval of the Government and by notification in the official Gazette, prescribe rules for determiningthe conditions under which a particular service or class of services will be considered to have been provided by a person from hisregistered office or place of business in Sindh.

Rules of Origin of Services and Reverse Charge in Certain Situations

Section 20 of the KPK ActSection 4 of the Punjab Act

4. Application of principles of origin and reverse charge in certain situations. – (1) Where a person is providing taxable services ina Province other than the Punjab but the recipient of such services is resident of the Punjab or is otherwise availing such servicesin the Punjab and has charged tax accordingly, the person providing such services shall pay the amount of tax so charged to theGovernment.

(2) Where the recipient of a taxable service is a person registered under the Act, he shall deduct the whole amount of tax inrespect of the service received and pay the same with the Government.

(3) Where a person is providing taxable services in more than one Province or territory in Pakistan including the Punjab, suchperson shall be liable to pay tax to the Government to the extent the tax is charged from a person resident in the Punjab or from aperson who is otherwise availing such services in the Punjab.

(4) Where rendering of a taxable service originates from the Punjab but terminates outside Pakistan, such person shall berequired to pay tax on such service to the Government.

(5) Where a taxable service originates from outside Pakistan but is received or terminates in the Punjab, the recipient of su ch

service shall be liable to pay the tax to the Government.

(6) The persons who are required to pay the tax to the Government in terms of sub-sections (1), (2), (3), (4) and (5) shall be l iableto registration for purposes of this Act and the rules.

(7) All questions or disputes relating to the application of the principle of origin given in this section shall be resolved in terms ofthe already recorded understanding between the Federal Government and the Provincial Governments on the implementation ofreformed General Sales Tax provided that pendency of any such question or dispute shall not absolve the concerned person fromhis obligation to deposit the tax. 6

(8) The provisions of this section shall apply notwithstanding any other provision of this Act or the rules and the Government mayspecify special procedure to regulate the provisions of this section

PERSON LIABLE TO PAY TAX

The Federal Excise Act, 2005/ Provincial Ordinances Section 3(5)(c ) The Sales Tax Act, 1990 Section 3 (3)

Section 3(5) (c ) of the FE Act

8/12/2019 Definations Section Handout PDP 13 KTBA FE and ST on Services SUH

http://slidepdf.com/reader/full/definations-section-handout-pdp-13-ktba-fe-and-st-on-services-suh 13/23

General Concepts of Federal Excise and Sales Tax On Services in PakistanHandout PDP – 2013

Karachi Tax Bar Association Page 13

(5) The liability to pay duty shall be–

c) in case of services provided or rendered in Pakistan of person providing or rendering of such services, provided where servicesare rendered by the person out of Pakistan, the recipient of such services in Pakistan shall be liable to pay Duty

Section 3(3)of the ST Act

(3) The liability to pay the tax shall be,--

(a) in the case of supply of goods, of the person making the supply, and

(3A) Notwithstanding anything contained in clause (a) sub-section (3), the Federal Government may, by a notification in theofficial Gazette, specify the goods in respect of which the liability to pay tax shall be of the person receiving the supply.

The Sindh Sales Tax on Services Act 2011 S ection 9

The Punjab Sales Tax on Services Act 2012 Section 11

The Khyber Pakhtunkhwa Finance Act 2013 Section 27

All above provisions are identical / similar

(1) Where a service is taxable by virtue of sub-Section (1) of Section 3, the liability to pay the tax shall be on the registered personproviding the service.

(2) Where a service is taxable by virtue of sub-Section (2) of Section 3, the liability to pay the tax shall be on the person receivingthe service.

(3) Notwithstanding anything contained in sub-Sections (1) and (2), the Board, with the approval of Government may, by anotification in the official Gazette, specify the services or class of services in respect of which the liability to pay tax shall be onthe person providing the taxable service, or the person receiving the taxable service or any other person.

(4) Nothing contained in sub-Sections (1) and (2) shall prevent the collection of tax from a different person if that person is madeseparately or jointly or severally liable for this tax under Section 18.

RATE OF TAXABLE SERVICES

The Federal Excise Act, 2005/ Provincial Ordinances Section 3 of FE Act and PST Ordinances The Sales Tax Act, 1990

Section 3 FE Act

at the rate of sixteen per cent ad valorem except the goods and services specified in the First Schedule, which shall be charged to

Federal excise duty as, and at the rates, set-forth therein.

Section 3 of PST Ordinances

Subject to the provisions of this Ordinance, there shall be charged, levied and paid a tax known as Sales Tax at the rate of sixteenper cent of the value of the taxable services rendered or provided in the Province of Balochistan.

The Sindh Sales Tax on Services Act 2011 Section 8 of the Sindh Act

8/12/2019 Definations Section Handout PDP 13 KTBA FE and ST on Services SUH

http://slidepdf.com/reader/full/definations-section-handout-pdp-13-ktba-fe-and-st-on-services-suh 14/23

General Concepts of Federal Excise and Sales Tax On Services in PakistanHandout PDP – 2013

Karachi Tax Bar Association Page 14

The Punjab Sales Tax on Services Act 2012 Section 10 of the Punjab Act

The Khyber Pakhtunkhwa Finance Act 2013 Section 26 of the KPK Act

All above provisions are identical/similar

(1) Subject to the provisions of this Act, there shall be charged, levied, collected and paid a tax on the value of a taxable serviceat the rate specified in the Second Schedule.

(2) Government may, on the recommendation of the Authority and subject to such conditions and restrictions as the Governmentmay impose, by notification in the official Gazette, declare that in respect of any taxable service provided by a registered personor a class of registered persons, the tax shall be charged, levied and collected at such higher, lower, fixed or specific rate asmaybe specified in the said notification.

VALUE OF TAXABLE SERVICES

The Federal Excise Act, 2005/ Provincial Ordinances Section 12(2) of FE Act the Sales Tax Act, 1990 Section 2(46) of ST Act

Section 12 (2) of FE Act

Where any services are liable to duty under this Act at a rate dependent on the charges therefore, the duty shall be paid on totalamount of charges for the services including the ancillary facilities or utilities, if any, irrespective whether such services havebeen rendered or provided on payment of charge or free of charge or on any confessional basis.

Section 2(46) of ST Act

(46) ‘value of supply’ means: --

(a) in respect of a taxable supply, the consideration in money including all Federal and Provincial duties and taxes, if any, whichthe supplier receives from the recipient for that supply but excluding the amount of tax:

Provided that –

(i) in case the consideration for a supply is in kind or is partly in kind and partly in money, the value of the supply shall mean theopen market price of the supply excluding the amount of tax;

(ii) in case the supplier and recipient are associated persons and the supply is made for no consideration or for a consideration which is lower than the open market price, the value of supply shall mean the open market price of the supply excluding theamount of tax; and

(b) in case of trade discounts, the discounted price excluding the amount of tax; provided the tax invoice shows the discountedprice and the related tax and the discount allowed is in conformity with the normal business practices;

(c) in case where for any special nature of transaction it is difficult to ascertain the value of a supply, the open market price;

(e) in case where there is sufficient reason to believe that the value of a supply has not been correctly declared in the invoice, the value determined by the Valuation Committee comprising representatives of trade and the

8/12/2019 Definations Section Handout PDP 13 KTBA FE and ST on Services SUH

http://slidepdf.com/reader/full/definations-section-handout-pdp-13-ktba-fe-and-st-on-services-suh 15/23

General Concepts of Federal Excise and Sales Tax On Services in PakistanHandout PDP – 2013

Karachi Tax Bar Association Page 15

Provided that, where the Board deems it necessary it may, by notification in the official Gazette, fix the value of any importedgoods or taxable supplies or class of supplies and for that purpose fix different values for different classes or description of sametype of imported goods or supplies:

Provided further that where the value at which import or supply is made is higher than the value fixed by the Board, the valu e of

goods shall, unless otherwise directed by the Board, be the value at which the import or supply is made;

The Sindh Sales Tax on Services Act 2011 Section 5

The Punjab Sales Tax on Services Act 2012 Section 7

The Khyber Pakhtunkhwa Finance Act 2013 Section 23

All above provisions are identical/similar

The value of a taxable service is:

(a) the consideration in money including all Federal and Provincial duties and taxes, if any, which the person providing a servicereceives from the recipient of the service but excluding the amount of sales tax under this Act:

Provided that –

(i) in case the consideration for a service is in kind or is partly in kind and partly in money, the value of the service shall mean theopen market price of the service as determined under Section 6 excluding the amount of sales tax under this Act; and

(ii) in case the person provides the service and the recipient of the service are associated persons and the service is suppl ied forno consideration or for a consideration which is lower than the price at which the person provides the service to other persons

who are not associated persons, the value of the service shall mean the price at which the service is provided to such otherpersons who are not associated persons excluding the amount of sales tax;

(iii) in case a person provides a service for no consideration or for a consideration is lower than the price at which such a service isprovided by other persons, the value of the service shall mean the open market price for such a service;

8/12/2019 Definations Section Handout PDP 13 KTBA FE and ST on Services SUH

http://slidepdf.com/reader/full/definations-section-handout-pdp-13-ktba-fe-and-st-on-services-suh 16/23

General Concepts of Federal Excise and Sales Tax On Services in PakistanHandout PDP – 2013

Karachi Tax Bar Association Page 16

INPUT TAX

The Federal Excise Act, 2005 / Provincial OrdinancesThe Sales Tax Act, 1990 Section 2(14)of the ST Act

“Input tax”, in relation to a registered person, means—

(a) tax levied under this Act on supply of goods to the person;(b) tax levied under this Act on the import of goods by the person;(c) in relation to goods or services acquired by the person, tax levied under the Federal Excise Act, 2005 in sales tax mode as aduty of excise on the manufacture or production of the goods, or the rendering or providing of the services;

(d) Provincial sales tax levied on services rendered or provided to the person;

(e) livied under the Sales Tax Act, 1990 as adapted in the State of Azad Jammu and Kashmir, on the supply of goods received bythe person;

The Sindh Sales Tax on Services Act 2011 Section 52

“Input tax”, in relation to a registered person, means, --

(a) tax levied under this Act on the services received by the person;(b) tax levied under the Sales Tax Act, 1990, on the goods imported by the person;(c) tax levied under the Sales Tax Act, 1990, on the goods or services received by the person; and(d) Provincial sales tax or Islamabad Capital Territory sales tax levied on the services received by the person:Provided that the Board may, by notification in the official Gazette, specify that any or all of the aforesaid tax shall not be treatedas input tax for the purposes of this Act subject to such conditions and limitations as the Board may specify in the notif ication;

The Punjab Sales Tax on Services Act 2012 – (n/a)

The Khyber Pakhtunkhwa Finance Act 2013 - (n/a)

8/12/2019 Definations Section Handout PDP 13 KTBA FE and ST on Services SUH

http://slidepdf.com/reader/full/definations-section-handout-pdp-13-ktba-fe-and-st-on-services-suh 17/23

General Concepts of Federal Excise and Sales Tax On Services in PakistanHandout PDP – 2013

Karachi Tax Bar Association Page 17

INPUT ADJUSTMENT / DETERMINATION OF TAX LIABILITY

The Federal Excise Act, 2005 /Provincial OrdinancesSales Tax Act, 1990 Section 7 of the ST Act

7. Determination of tax liability.-- (1) Subject to the provisions of section 8B, for the purpose of determining his tax liability inrespect of taxable supplies made during a tax period, a registered person shall, subject to the provisions of section 73, beentitled to deduct input tax paid or payable during the tax period for the purpose of taxable supplies made, or to be made, by himfrom the output tax that is due from him in respect of that tax period and to make such other adjustments as are specified insection 9:

Provided that where a registered person did not deduct input tax within the relevant period, he may claim such tax in the returnfor any of the six succeeding tax periods.

The Sindh Sales Tax on Services Act 2011 Section 15 – Rule 21

The Board may, subject to such conditions and restrictions as it may prescribe and with the approval of the Government, allowregistered persons to claim adjustments or deductions, including refunds arising as a result thereof, in respect of the sale taxpaid on or in respect of any taxable services or class of taxable services provided by them.

The Punjab Sales Tax on Services Act 2012

The Punjab Sales Tax on Services (Adjustment of Tax) Rules, 2012.

2. Determination of input tax .- (1) Subject to the provisions of the Act and the rules or notifications issued thereunder, aregistered person who holds a tax invoice for the purchase of goods or services used or consumed in providing of taxable servicesin his name, bearing his sales tax registration/NTN, shall be entitled to deduct or adjust input tax paid or payable during therelevant tax period.

The Khyber Pakhtunkhwa Finance Act 2013 Section 27

(1) The Authority may, subject to such conditions and restrictions as it may specify, allow registered persons to claim adjustmentsor deductions, including refunds arising as a result thereof, in respect of the tax paid under any other law on any account inrespect of any taxable service or goods or class of taxable services or goods provided by them.

(2) For the purposes of sub-Section (1), the Authority may adopt the principles or concepts laid down in such other law in respectof adjustments, deductions or refunds including zero-rating principle.

8/12/2019 Definations Section Handout PDP 13 KTBA FE and ST on Services SUH

http://slidepdf.com/reader/full/definations-section-handout-pdp-13-ktba-fe-and-st-on-services-suh 18/23

General Concepts of Federal Excise and Sales Tax On Services in PakistanHandout PDP – 2013

Karachi Tax Bar Association Page 18

(3) No adjustment or deduction of any tax payable under any other law shall be claimed by any person except in the manner andto the extent specified in the notification issued under sub-Section (1)

Input Tax Not Allowed

The Federal Excise Act, 2005 /Provincial OrdinancesSales Tax Act, 1990 Section 8 of the ST Act SRO.490 /2004

8. Tax credit not allowed .-- (1) Notwithstanding anything contained in this Act, a registered person shall not be entitled to reclaimor deduct input tax paid on--

(a) the goods or services used or to be used for any purpose other than for taxable supplies made or to be made by him;

(b) any other goods or services which the Federal Government may, by a notification in the official Gazette, specify;

(c) the goods under sub-section (5) of section 3;

(ca) the goods or services in respect of which sales tax has not been deposited in the Government treasury by the

(caa) purchases, in respect of which a discrepancy is indicated by CREST or input tax of which is not verifiable in the supply chain;

(d) fake invoices; and

(e) purchases made by such registered person, in case he fails to furnish the information required by the Board through anotification issued under sub-section (5) of section 26.

(2) If a registered person deals in taxable and non-taxable supplies, he can reclaim only such proportion of the input tax as isattributable to taxable supplies in such manner as may be specified by the Board.

(3) No person other than a registered person shall make any deduction or reclaim input tax in respect of taxable supplies made orto be made by him.

SRO. 490/2004

Following goods, acquired otherwise than as stock in trade, by a registered person, to be the goods in respect of which input taxshall not be claimed, namely:-

(a) vehicles falling in chapter 87 of the First Schedule to the Customs Act, 1969 (IV of 1969);

(b) food, beverages, garments, fabrics, etcetera and consumption on entertainment;

(c) gifts and give-aways;

(d) supply of electricity and gas to residential colonies of registered persons; and

(e) building materials including cement, bricks, paints, varnishes, distempers etc.;

(f) office equipment and machines (excluding electronic fiscal cash registers), furniture, structure, fixture and furnishingsexcluding those directly used in taxable activity;

(g) electrical and gas appliances, pipes, fittings excluding those directly used in taxable activity;

8/12/2019 Definations Section Handout PDP 13 KTBA FE and ST on Services SUH

http://slidepdf.com/reader/full/definations-section-handout-pdp-13-ktba-fe-and-st-on-services-suh 19/23

General Concepts of Federal Excise and Sales Tax On Services in PakistanHandout PDP – 2013

Karachi Tax Bar Association Page 19

(h) Wires, cables, ordinary electrical fittings and sanitary fittings, excluding those directly used in taxable

(i) crockery, cutlery, utensils etc., excluding those directly used in taxable activity.

Section 73 of the ST Act

73. Certain transactions not admissible. - (1) Notwithstanding anything contained in this Act or any other law for the time being inforce, payment of the amount for a transaction exceeding value of fifty thousand rupees, excluding payment against a utility bill,shall be made by a crossed cheque drawn on a bank or by crossed bank draft or crossed pay order or any other crossed bankinginstrument showing transfer of the amount of the sales tax invoice in favour of the supplier from the business bank account of thebuyer:

Provided that online transfer of payment from the business account of buyer to the business account of supplier as well aspayments through credit card shall be treated as transactions through the banking channel, subject to the condition that suchtransactions are verifiable from the bank statements of the respective buyer and the supplier.

(2) The buyer shall not be entitled to claim input tax credit, adjustment or deduction, or refund, repayment or draw-back or zero-rating of tax under this Act if payment for the amount is made otherwise than in the manner prescribed in sub-section (1),provided that payment in case of a transaction on credit is so transferred within one hundred and eighty days of issuance of thetax invoice.

(3) The amount transferred in terms of this section shall be deposited in the business bank account of the supplier, otherwise thesupplier shall not be entitled to claim input tax credit, adjustment or deduction, or refund, repayment or draw-back or zero-ratingof tax under this Act.

Explanation- For the purpose of this section, the term "business bank account" shall mean a bank account utilized by theregistered person for business transactions, declared to the Explanation- For the purpose of this section, the term "businessbank account" shall mean a bank account utilized by the registered person for business transactions, declared to theCommissioner in whose jurisdiction he is registered through Form STR 1 or change of particulars in registration database.

The Sindh Act (in addition to above) Rule 22

A registered person shall not be entitled to claim input tax adjustment in respect of:(i) capital goods not exclusively used in providing or rendering of services;(ii) fixed assets not exclusively used in providing or rendering of services;(iia) the following goods and services, acquired otherwise than as stock in trade, by a registered person:(iii) goods and services already in use on which sales tax is not paid, or, where paid, the input adjustment has been taken beforethe tax period July, 2011, or where the input related goods and services were purchased or acquired before the tax period July,2011;(iv) utilities bills not in the name of registered person unless evidence of consumption is produced in the matter of such claims;(viii) goods and services used or consumed in a service liable to a tax rate lesser than the 16% of the charges or to a specific rateof tax not based on value;(viiia) services liable to a tax rate lesser than 16% of the charges or to a specific rate of tax not based on value when used for

providing or rendering any service; and(ix) such goods or services as are notified by the SRB to be inadmissible for input tax adjustment.]

APPORTIONMENT OF INPUT TAX

The Federal Excise Act, 2005/ Provincial OrdinancesSales Tax Act, 1990 The Apportionment of Input Tax Rules (ST Rules)

The Sindh Sales Tax on Services Act 2011 (Sindh Rules)

8/12/2019 Definations Section Handout PDP 13 KTBA FE and ST on Services SUH

http://slidepdf.com/reader/full/definations-section-handout-pdp-13-ktba-fe-and-st-on-services-suh 20/23

General Concepts of Federal Excise and Sales Tax On Services in PakistanHandout PDP – 2013

Karachi Tax Bar Association Page 20

The Punjab Sales Tax on Services Act 2012 (Punjab Rules) The Khyber Pakhtunkhwa Finance Act 2013 (N/A)

No credit for non-taxable or exempt services.-

(1) The input tax paid on goods and services used in providing non-taxable or exempt services shall not be admissible.(2) In case an input is used in providing taxable services and also non-taxable or exempt services, the input tax shall beapportioned according to the following formula for availing of input tax adjustment/deduction, namely,-

Value of Taxable SuppliesAdjustable Input Tax = Value of Taxable and exempt X Total Input Tax

(or non taxable) Supplies

(3) The adjustments of input tax claimed under this rule by a registered person shall be subject to reconciliation and audit by theofficers of the Authority as and when needed under intimation to the registered person.

REFUND AND CARRY FORWARD OF TAX

The Federal Excise Act, 2005/ Provincial OrdinancesSales Tax Act, 1990 Section 10

(1) If the input tax paid by a registered person on taxable purchases made during a tax period exceeds the output tax on accountof zero rated local supplies or export made during that tax period, the excess amount of input tax shall be refunded to theregistered person not later than forty five days of filing of refund claim in such manner and subject to such conditions as theBoard may, by notification in the official Gazette specify:

Provided that in case of excess input tax against supplies other than zero rated or exports, such excess input tax may be carriedforward to the next tax period, along with the input tax as is not adjustable in terms of sub-Section (1) of Section 8B, and shall betreated as input tax for that period and the Board may, subject to such conditions and restrictions as it may impose, bynotification in the official Gazette, prescribe the procedure for refund of such excess input tax;

Provided further that the Board may, from such date and subject to such conditions and restrictions as it may impose, bynotification in the official Gazette, direct that refund of input tax against exports shall be paid along with duty drawback at therates notified in the said notification.

(2) If a registered person is liable to pay any tax, default surcharge or penalty payable under any law administered by the Board,the refund of input tax shall be made after adjustment of unpaid outstanding amount of tax or, as the case may, defaultsurcharge and penalty.

(3) Where there is reason to believe that a person has claimed input tax credit or refund which was not admissible to him, the

proceedings against him shall be completed within sixty days. For the purposes of enquiry or audit or investigation regardingadmissibility of the refund claim, the period of sixty days may be extended up to one hundred and twenty days by an officer notbelow the rank of an Additional Commissioner Inland Revenue and the Board may, for reasons to be recorded in written, extendthe aforesaid period which shall in no case exceed nine months

The Sindh Sales Tax on Services Act 2011 - Chapter V 23A Notification 30 June 2013

8/12/2019 Definations Section Handout PDP 13 KTBA FE and ST on Services SUH

http://slidepdf.com/reader/full/definations-section-handout-pdp-13-ktba-fe-and-st-on-services-suh 21/23

General Concepts of Federal Excise and Sales Tax On Services in PakistanHandout PDP – 2013

Karachi Tax Bar Association Page 21

Processing and sanction of claims for refund by a registered person will apply in following cases:-

(a) the amount of sales tax is erroneously or inadvertently deposited in excess of the amount due; and(b) the amount deposited by or recovered from the registered person is held not payable under the Act, as result of an order of acourt or an appellate forum.

The Punjab Sales Tax on Services Act 2012

The Khyber Pakhtunkhwa Finance Act 2013

ASSESSMENT OF TAX

The Federal Excise Act, 2005/ Provincial OrdinancesSales Tax Act, 1990- Section 11

11. Assessment of Tax and recovery of tax not levied or short- levied or erroneously refunded. -- (1) Where a person who isrequired to file a tax return fails to file the return for a tax period by the due date or pays an amount which, for somemiscalculation is less than the amount of tax actually payable, an Officer of Inland Revenue shall, after a notice to show cause tosuch person, make an order for assessment of tax, including imposition of penalty and default surcharge in accordance withsection 33 and 34:

Provided that where a person required to file a tax return files the return after the due date and pays the amount of tax payable inaccordance with the tax return along with default surcharge and penalty, the notice to show cause and the order of assessmentshall abate.

(2) Where a person has not paid the tax due on supplies made by him or has made short payment or has claimed input tax creditor refund which is not admissible under this Act for reasons other than those specified in sub-section (1), an Officer of InlandRevenue shall, after a notice to show cause to such person, make an order for assessment of tax actually payable by that personor determine the amount of tax credit or tax refund which he has unlawfully claimed and shall impose a penalty and chargedefault surcharge in accordance with section 33 and 34.

8/12/2019 Definations Section Handout PDP 13 KTBA FE and ST on Services SUH

http://slidepdf.com/reader/full/definations-section-handout-pdp-13-ktba-fe-and-st-on-services-suh 22/23

General Concepts of Federal Excise and Sales Tax On Services in PakistanHandout PDP – 2013

Karachi Tax Bar Association Page 22

(3) Where by reason of some collusion or a deliberate act any tax or charge has not been levied or made or has been short-leviedor has been erroneously refunded, the person liable to pay any amount of tax or charge or the amount of refund erroneously madeshall be served with a notice requiring him to show cause for payment of the amount specified in the notice.

(4) Where, by reason of any inadvertence, error or misconstruction, any tax or charge has not been levied or made or has beenshort-levied or has been erroneously refunded, the person liable to pay the amount of tax or charge or the amount of refunderroneously made shall be served with a notice requiring him to show cause for payment of the amount specified in the notice:

Provided that, where a tax or charge has not been levied under this sub-section, the amount of tax shall be recovered as taxfraction of the value of supply.

(5) No order under this section shall be made by an Officer of Inland Revenue unless a notice to show cause is given within fiveyears, of the relevant date, to the person in default specifying the grounds on which it is intended to proceed against him and theofficer of Sales Tax shall take into consideration the Provided that order under this section shall be made within one hundredand twenty days of issuance of show cause notice or within such extended period as the Commissioner may, for reasons to berecorded in writing, fix provided that such extended period shall in no case exceed ninety days:

Provided further that any period during which the proceedings are adjourned on account of a stay order or Alternative DisputeResolution proceedings or the time taken through adjournment by the petit ioner not exceeding sixty days shall be excluded fromthe computation of the period specified in the first proviso.

(6) Notwithstanding anything in sub-section (1), where a registered person fails to file a return, an officer of Inland Revenue notbelow the rank of Assistant Commissioner shall subject to such conditions as specified by the Federal Board of Revenue,determine the minimum tax liability of the registered person.

(7) For the purpose of this section, the expression "relevant date" means--

(a) the time of payment of tax or charge as provided under section 6; and

(b) in a case where tax or charge has been erroneously refunded, the date of its refund.

Section 14 of the FE Act

14. Recovery of unpaid duty or of erroneously refunded duty or arrears of duty, etc. —(1) Where any person has not levied or paid

any duty or has short levied or short paid such duty or where any amount of duty has been refunded erroneously, such person

shall be serviced with notice requiring him to show cause for payment of such duty provided that such notice shall be issued

within five years from the relevant date.

(2)The Officer of Inland Revenue, empowered in this behalf, shall after considering the objections of the person served with anotice to show cause under sub-section (1), determine the amount of duty payable by him and such person shall pay the amount

so determined along with default surcharge and penalty as specified by such officer under the provisions of this Act.

The Sindh Sales Tax on Services Act 2011 Section 23

(1) Where on the basis of any information acquired during an audit, inquiry, inspection or otherwise, an officer of the SRB, notbelow the rank of Assistant Commissioner SRB is of the opinion that a registered person has not paid the tax due on taxable

8/12/2019 Definations Section Handout PDP 13 KTBA FE and ST on Services SUH

http://slidepdf.com/reader/full/definations-section-handout-pdp-13-ktba-fe-and-st-on-services-suh 23/23