Embed Size (px)

Citation preview

The audio portion of the conference may be accessed via the telephone or by using your computer's speakers. Please refer to the instructions emailed to registrants for additional information. If you have any questions, please contact Customer Service at 1-800-926-7926 ext. 1.

NOTE: If you are seeking CPE credit, you must listen via your computer — phone listening is no longer permitted.

Contribution Default Remedies for LLCs and Partnerships: Tax Consequences of Dilution, Set‐Offs and Constructive Loans

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

THURSDAY, SEPTEMBER 6, 2018

Presenting a live 90‐minute webinar with interactive Q&A

Professor Bradley T. Borden, Professor of Law, Brooklyn Law School, Brooklyn, N.Y.

Anthony L. Minervini, Senior Manager, Ernst & Young, New York

Tips for Optimal Quality

Sound QualityIf you are listening via your computer speakers, please note that the quality of your sound will vary depending on the speed and quality of your internet connection.

If the sound quality is not satisfactory, you may listen via the phone: dial 1-866-570-7602 and enter your PIN when prompted. Otherwise, please send us a chat or e-mail [email protected] immediately so we can address the problem.

If you dialed in and have any difficulties during the call, press *0 for assistance.

NOTE: If you are seeking CPE credit, you must listen via your computer — phone listening is no longer permitted.

Viewing QualityTo maximize your screen, press the F11 key on your keyboard. To exit full screen, press the F11 key again.

FOR LIVE EVENT ONLY

Continuing Education Credits

In order for us to process your continuing education credit, you must confirm your participation in this webinar by completing and submitting the Attendance Affirmation/Evaluation after the webinar.

A link to the Attendance Affirmation/Evaluation will be in the thank you email that you will receive immediately following the program.

For CPE credits, attendees must participate until the end of the Q&A session and respond to five prompts during the program plus a single verification code. In addition, you must confirm your participation by completing and submitting an Attendance Affirmation/Evaluation after the webinar.

For additional information about continuing education, call us at 1-800-926-7926 ext. 2.

FOR LIVE EVENT ONLY

Program Materials

If you have not printed the conference materials for this program, please complete the following steps:

• Click on the ^ symbol next to “Conference Materials” in the middle of the left-hand column on your screen.

• Click on the tab labeled “Handouts” that appears, and there you will see a PDF of the slides for today's program.

• Double click on the PDF and a separate page will open.

• Print the slides by clicking on the printer icon.

FOR LIVE EVENT ONLY

Contribution‐Default Remedies of LLCs and Partnerships

Bradley T. BordenBrooklyn Law School

Anthony L. MinerviniErnst & Young LLP

Background

• LLC and partnership agreements often include contribution obligations

• Initial contributions• Additional contributions

• Contributions are important• Fund entity operations• Determine interests in entity• Determine voting rights• Determine rights to distributions

6

Contribution‐Default Remedies

• Entity agreements typically provide remedies against members who fail to meet contribution obligations

• Remedies typically would only apply to obligations to make additional contributions

7

Reasons for Contribution‐Default Remedies

• Preserve established interest alignments• Limit ownership interests of one or more members for regulatory purposes

• E.g., Foreign‐controlled entity may lose favorable tax‐reporting status

• Prevent erosion of membership interests and voting rights

• Disincentivize default• Share cost in downturn

8

Legal Effect of Default Remedies

• Dilution as sole remedy• Operating agreement provided dilution as a remedy

• Percentage interests based upon capital contributions• No provision in operating agreement or statute for damages to compel defaulting member to make contribution

• Only remedy against defaulting member is dilution

• Canyon Creek Development, LLC v. Fox, 46 Kan.App.2d 370 (2011)

9

Member Liable for Additional Contribution

• Damages as remedy• Operating agreement provided loss of 50% of interest for contribution default within 45 days, loss of remainder of interest after 180 days

• Operating agreement included Rights and Remedies clause:• Provision in Agreement in addition to other remedies under law, statute, ordinance, or otherwise

• State statute:• Member is obligated to an LLC to perform any promise to contribute cash

• Defaulting member liable under the preservation‐of‐remedies clause

• Vinton v. Grayson, ____ A.3d ____ (Super. Ct. Del. 2018)

10

Contribution Default in Loss Situation

• Canyon Creek and Vinton were both loss situations• Would case arise in gain situation?

• Interest in entities with negative value does not have positive value

• Interest‐dilution is not a penalty or remedy in loss situations

• Presentation focuses on economic effect of defaulting and default remedies of entities with value

• Entities could be losing value, but still have value• Entities could be operating at loss but be increasing in value• Non‐defaulting members or entity accept interest‐dilution as remedy

• Interest is of equal or greater value than damages?

11

Types of Dilution Remedies

• Natural Dilution• Dilution determined solely by reference to dilution denominators

• Punitive Dilution• Non‐contributing member’s interest dilutes by more than the amount determined using the dilution denominators

• Contributing member’s interest increases by more than the amount determined using the dilution denominators

• Unless provided otherwise, assume entity distributes in accordance with members’ percentage interests

12

Dilution Denominators

• Contribution‐Denominated Interests—Canyon Creek• Percentage interests determined in reference to contributions•

• Historical‐Value‐Denominated Interests•

• Market‐Value‐Denominated Interests•

. .

13

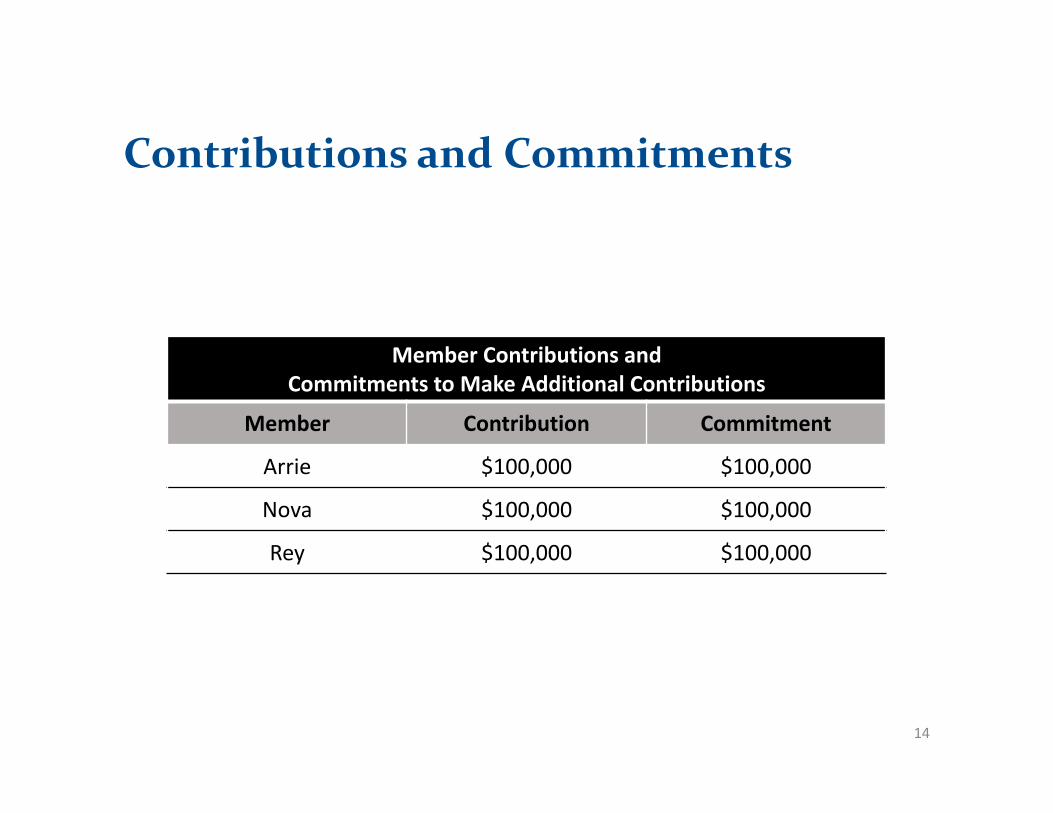

Contributions and Commitments

Member Contributions and Commitments to Make Additional Contributions

Member Contribution Commitment

Arrie $100,000 $100,000

Nova $100,000 $100,000

Rey $100,000 $100,000

14

Capital Call

• Members make initial contributions• LLC calls for each member to contribute $100,000• Arrie and Nova each contribute $100,000• Rey defaults—makes no additional contribution

15

Contribution‐Denominated Natural Dilution—Non‐Defaulting Members Pay Own Commitments

Effect of Disproportionate Additional Contribution on Total Contributions

Member InitialContribution

Initial Percentage Interests

Additional Contribution

Total Contribution

Percent of Total

Arrie $100,000 33.33% $100,000 $200,000 40%

Nova $100,000 33.33% $100,000 $200,000 40%

Rey $100,000 33.33% $0 $100,000 20%

Total $300,000 $200,000 $500,000

16

Capital Call—Contributing Members Cover Default Amount

• Members make initial contribution• LLC calls for each member to contribute $100,000• Arrie and Nova each contribute $100,000• Rey defaults—makes no additional contribution• Arrie and Nova cover default by each contributing an additional $50,000

17

Contribution‐Denominated Natural Dilution—Non‐Defaulting Members Cover Default Shortfall

Natural Dilution of Disproportionate Additional Contribution—Members Cover Default Shortfall

Member InitialContribution

Initial Percentage Interests

Additional Contribution

Total Contribution

Percent of Total

Arrie $100,000 33.33% $150,000 $250,000 41.67%

Nova $100,000 33.33% $150,000 $250,000 41.67%

Rey $100,000 33.33% $0 $100,000 16.67%

Total $300,000 $300,000 $600,000

18

Punitive Dilution

• Example• Amount actually contributed to cover the default amount deemed to be 200% of amount actually paid to cover default

• 200% is a contribution multiplier

20

Punitive Dilution with Contribution Multiplier

Punitive Dilution of Disproportionate Additional Contribution—Members Cover Default Shortfall

Member InitialContribution

Initial Percentage Interests

Actual Additional Contribution

Deemed Additional Contribution

Total Contribution

Percent of Total

Arrie $100,000 33.33% $150,000 $50,000 $300,000 42.86%

Nova $100,000 33.33% $150,000 $50,000 $300,000 42.86%

Rey $100,000 33.33% $0 $0 $100,000 14.28%

Total $300,000 $300,000 $100,000 $700,000

21

Tax Questions

• Is a contribution merely a contribution, even if there is a punitive dilution?

• Contributions are tax‐free under § 721• Is there a taxable capital shift?

22

Effect of Punitive Dilution

Member Percent of Total, Natural Dilution

Percent of Total, Punitive Dilution

Change Caused by Punitive Dilution

Arrie 41.67% 42.86% +1.19Nova 41.67% 42.86% +1.19Rey 16.67% 14.28% ‐2.39

Capital‐Shift Basics

• Capital Shift • A member’s right to existing capital shifts to another member

• Right to existing capital = amount a member would receive if entity liquidated

23

Example of Capital Shift Resulting from Punitive Dilution

• Assumptions• Entity assets are worth $300,000 at time of capital call• Entity assets are worth $600,000 immediately after call

• Notice that as a result of the punitive dilution, Rey goes from having a right in $100,000 of the entity’s assets to having only $85,680, so a capital shift occurred.

24

Example of Capital Shift Resulting from Punitive Dilution

MemberPercentage Interest

Before Call

Value of Right to Capital Before Call

Percentage Interest After Call

Value of Right to Capital After Call

Arrie 33.33% $100,000 42.86% $257,160Nova 33.33% $100,000 42.86% $257,160Rey 33.33% $100,000 14.28% $85,680

Possible Tax Outcome—Disregard Capital Shift

• Dilution is Non‐Recognition Event• Non‐taxable bargain purchase for contributing member?

• Members have not negotiated value at time of shift• Parties’ actions may suggest divergent assessments of value• Dilution method was determined at formation

• No loss/deduction for defaulting member• Future allocations reflect new percentage interests• Gain/loss recognized on liquidating distributions

• Contributing members recognize long‐term capital gain• Defaulting members recognize long‐term capital loss

• If distributions are in accordance with interests, not in accordance with capital account balances, can allocations have economic effect?

25

Tax Outcomes—Treat Capital Shift as Bargain Purchase

26

Tax Outcomes Disregarding Capital Shift

Member Basis—InitialContribution

Actual Additional Contribution

§ 722 Basis Following

Contributions

Percent of Total

Share of $600,000

Distribution

Gain/(Loss)on

Distribution

Arrie $100,000 $150,000 $250,000 42.86% $257,160 $7,160Nova $100,000 $150,000 $250,000 42.86% $257,160 $7,160Rey $100,000 $0 $100,000 14.28% $85,680 ($14,320)Total $300,000 $300,000 $600,000 $600,000

Possible Tax Outcome—Recognize Capital Shift

• Under what theory does value shift from defaulting member to contributing member?

• Sale of interest• Defaulting member transfers interest for no consideration• Contributing member acquires interest as a bargain• Contributing member takes share of defaulting member’s capital account• Effect of § 754 election?

• Payment of punitive damages• Defaulting member transfers interest as damages• Contributing member receives punitive damages• What is the flow of cash? Deemed distribution, payment, and contribution?• If transfer of property, does defaulting member recognize gain (or loss) on

transfer?• Abandoned property?

• Defaulting member walks away from forfeited interest• Contributing member obtains a windfall

• Different tax theories affect timing and character of gain/loss recognized and effect on capital accounts and inside basis

27

Tax Treatment Possible Tax Outcomes

Taxing the Capital Shift Resulting from Punitive Dilution

Defaulting Member Contributing Member

Sale of Interests § 741 capital loss?Capital gain?What about bargain purchase?§ 743 adjustment?

Payment of Damages Deduction or capital expenditure?Gain recognized on transfer? Ordinary income

Abandoned Property § 165 ordinary loss? Ordinary income windfall?

28

Tax Outcomes—Treat Capital Shift as Recognition Event

29

Tax Outcomes Recognizing Capital Shift

Member Basis—InitialContribution

Actual Additional Contribution

Tax Result of Capital

Shift

Adjusted Basis

Following Shift

Share of $600,000

Distribution

Gain/(Loss)on

Distribution

Arrie $100,000 $150,000 $7,160 $257,160 $257,160 $0Nova $100,000 $150,000 $7,160 $257,160 $257,160 $0Rey $100,000 $0 ($14,320) $85,680 $85,680 $0Total $300,000 $300,000 $600,000 $600,000

Historical‐Value Denominated Dilutions

• Use capital accounts to determine effect of disproportionate contribution

• Capital account maintenance• Increases

• Contributions• Allocations of income and gain

• Decreases• Allocations of deductions and losses• Distributions

• Assumption:• Entity has $60,000 of losses prior to allocation

30

Historical‐Value‐Denominated Natural Dilution

31

Historical‐Value‐Denominated Interest Computation

Member InitialContribution

Initial Percentage Interests

Share of Loss

Additional Contribution

Balance After Additional Contribution

Percent of Total

Arrie $100,000 33.33% ($20,000) $150,000 $230,000 42.59%Nova $100,000 33.33% ($20,000) $150,000 $230,000 42.59%Rey $100,000 33.33% ($20,000) $0 $80,000 14.81%Total $300,000 ($60,000) $300,000 $540,000

Contribution‐Denominated Dilution vs. Historical‐Value‐Denominated Dilution

• Effect of using contribution‐denominated dilution instead of historical‐value‐denominated dilution

• Dilution denominator affects amount of dilution

32

Effect of Contribution Denominator—Natural Dilution

Member Percent of Total, Contribution

Percent of Total, Historical‐Value

Change Caused by Denominator

Arrie 41.67% 42.59% ‐0.92Nova 41.67% 42.59% ‐0.92Rey 16.67% 14.81% +1.86

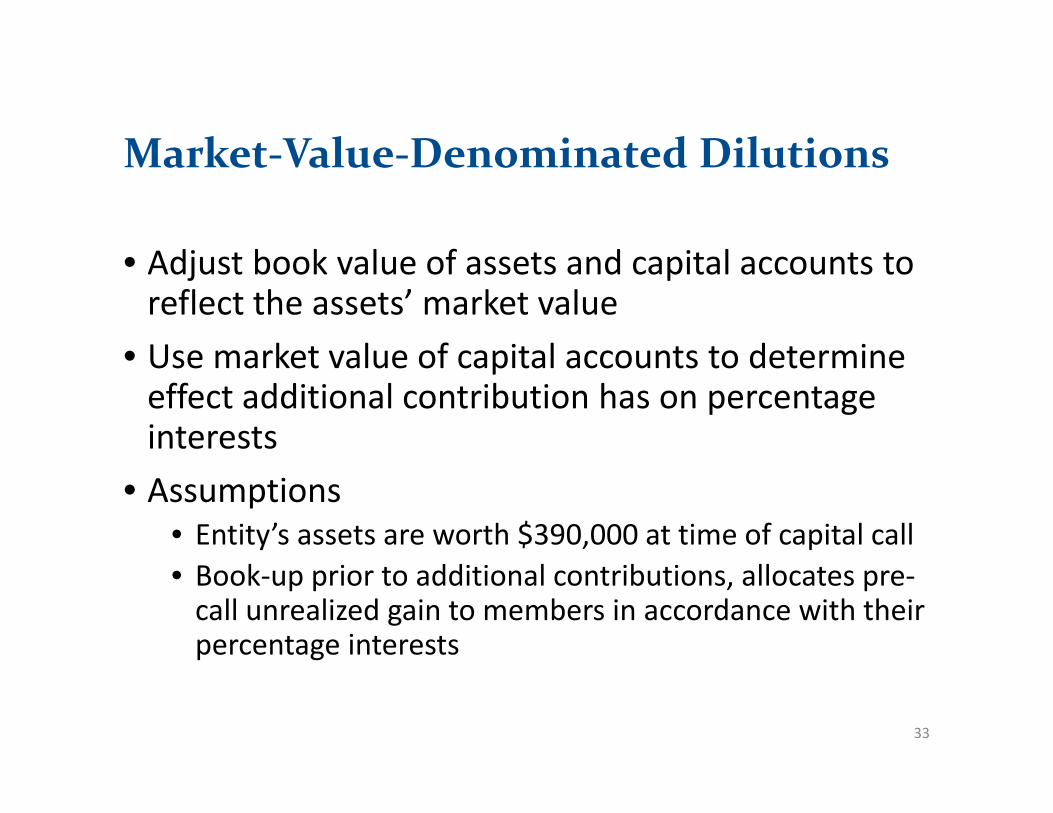

Market‐Value‐Denominated Dilutions

• Adjust book value of assets and capital accounts to reflect the assets’ market value

• Use market value of capital accounts to determine effect additional contribution has on percentage interests

• Assumptions • Entity’s assets are worth $390,000 at time of capital call• Book‐up prior to additional contributions, allocates pre‐call unrealized gain to members in accordance with their percentage interests

33

Market‐Value‐Denominated Natural Dilution

34

Historical‐Value‐Denominated Interest Computation

Member InitialContribution

Initial Percentage Interests

Share of Book‐Up

Additional Contribution

Balance After Additional Contribution

Percent of Total

Arrie $100,000 33.33% $30,000 $150,000 $280,000 40.58%Nova $100,000 33.33% $30,000 $150,000 $280,000 40.58%Rey $100,000 33.33% $30,000 $0 $130,000 18.84%Total $300,000 $300,000 $690,000

Contribution‐Denominated Dilution vs. Market‐Value‐Denominated Dilution

• Effect of use contribution‐denominated dilution instead of market‐value‐denominated dilution

• Does using contribution‐denominated dilution cause a taxable capital shift?

35

Effect of Dilution Denominator—Natural Dilution

Member Percent of Total, Contribution

Percent of Total, Market‐Value

Change Caused by Denominator

Arrie 41.67% 40.58% +1.09Nova 41.67% 40.58% +1.09Rey 16.67% 18.84% ‐2.18

Effect of Dilution‐Computation Method

• Using contribution‐denominated dilution• Appears to create a capital shift• Tax result of capital shift should be the same as tax result of punitive dilution

• Challenges to taxing capital shift• What is fair market value?• If default is discretionary, the members would appear to disagree about the value of the entity’s assets

• Does IRS want to be in the business of valuing assets to determine tax treatment of dilution resulting from contribution defaults?

36

Capital Lock‐In vs. Capital Shift

• Capital Lock‐In• Members’ rights in entity assets lock in at time of additional contribution

• Book‐up helps establish members’ rights in entity assets• Members’ rights in pre‐call assets tied to pre‐call percentage interests

• Post‐contribution allocations based upon new percentage interests

• Lock‐in creates a distribution waterfall• Pre‐call value distributed in accordance with pre‐call percentage interests

• Post‐call value distributed in accordance with post‐call percentage interests

38

Example of Capital Lock‐In

• Members retain rights to pre‐call value and additional contributions

• Allocations of future profits are based upon post‐call percentage interests

39

Capital Lock‐In

Member Pre‐Call Value

Pre‐Call Percentage Interests

Additional Contribution

Post‐Call Value

Percentage Interest in

Future Profit

Arrie $130,000 33.33% $150,000 $280,000 40.58%Nova $130,000 33.33% $150,000 $280,000 40.58%Rey $130,000 33.33% $0 $130,000 18.84%Total $390,000 $690,000

Distribution Scenario with Capital Lock‐In

• Waterfall• First, to the members in amounts equal to their pre‐call interests in the value of the entity’s assets

• Second, to the members to return their additional contributions

• Third, to the members in accordance with their post‐call percentage interests

• Example: Entity has $720,000 to distribute two years after capital call

40

Application of Capital Lock‐In Waterfall

41

Distribution with Pre‐Call Lock‐In and Post‐Call Allocation According to New Percentage Interests

Arrie Nova Rey Total

Pre‐Call Interest 33.33% 33.33% 33.33%

Pre‐Call Value $130,000 $130,000 $130,000 $390,000

Additional Contribution $150,000 $150,000 $300,000

Post‐Call Interest 40.58% 40.58% 18.84%

Post‐Call Profit $12,174 $12,174 $5,652 $30,000

Total $292,174 $292,174 $135,652 $720,000

Observations of Capital Lock‐In

• Capital lock‐in prevents capital shifts• Minimizes tax ambiguity

• Affects defaulting member to a lesser extent• Minimizes the deterrent effect of default remedy

42

Dilution‐Preventing Remedies

• Goal• Ensure that some or all members’ percentage interests remain unchanged

• General types of dilution‐preventing remedies• Member‐to‐member constructive loan• Crossover member‐to‐member loan• Member‐to‐entity constructive loan

43

Member‐to‐Member constructive loan

• Entity agreement creates loan• Loan is a contribution‐default remedy• Loan is constructive—not entered into between members per se

• Defaulting member is deemed to borrow from contributing member

• Defaulting member deemed to make contribution• Distributions to defaulting member are used to repay member‐to‐member loan

• Defaulting member’s interest is security for loan• “Lending” member does not get priority distribution from entity

• Loan is to member, not entity

44

Tax and Financial Aspects of Member‐to‐Member Loan

• Return on loan may be less than return on contribution• Usury laws may cap amount of interest chargeable

• Effect of security interest if defaulting member goes into bankruptcy

• Will lending member be a secured creditor?• Does state law allow and recognize the loan?

• Interest income to lending member, instead of income allocated from entity

• Defaulting member’s interest deduction subject to interest rules

• Foreclosure• Sale for debt‐forgiveness consideration

45

Crossover Member‐to‐Member Loan

• Member‐to‐member loan• Loan “crosses over” and becomes a contribution from the lending member, if defaulting member does not cure

• What is the structure of the crossover?• Constructive cash contribution

• Distribution to defaulting member• Repayment of loan• Contribution by lending member

• Constructive note contribution• Lending member contributes note• Entity distributes note to defaulting member

• Disguised sale of partnership interest• Could IRS and courts disregard the stated form of transaction?

46

Tax and Financial Aspects of Crossover Member‐to‐Member Loan

• Effect of contribution• Natural or punitive dilution?• Taxable capital shift?

• Effect of loan forgiveness• COD to defaulting member?• Gain = liability relief – basis of forfeited interests?

47

Member‐to‐Entity Constructive Loan

• Contributing member covers defaulting member’s contribution shortfall

• Contributing member’s transfer of proceeds to entity is deemed to be a loan from the member to the entity

• Loan should give lending member distribution priority

• What are the terms of the loan?• Does contributing member forfeit return by making loan?

• Loan could convert to contribution48