Embed Size (px)

Citation preview

December 2008 I t P t ti Investor Presentation

December 2008 Investor Presentation

Introduction to CHK

● #1 producer of U.S. natural gas– 3Q’08 natural gas production of 2,138 mmcf/day; ~3.5% of U.S. production; 2009E

2 214mmcf/day and 2010E 2 515 mmcf/day2,214mmcf/day and 2010E 2,515 mmcf/day● #1 driller in U.S.

– ~130 operated rigs currently, on the way down to ~110-115 operated rigs until gas markets rebalance, ~85 non-operated rigs, ~15 info only rigs; collector of ~12% of all daily drilling information generated in the U S (~20% in our areas of interest)information generated in the U.S. (~20% in our areas of interest)

● #1 large-cap production growth– Increased production by 23% in ’07 to 2.0 bcfe/day; projecting increase of 17% in ’08 to 2.3

bcfe/day and increases of 5-10% in ’09 and 10-15% in ’10 to 2.4 and 2.7 bcfe/day, respectivelyrespectively

● #1 large-cap proved reserve growth– 12.1 tcfe estimated proved reserves at 9/30/08; targeting 12.0-12.5 tcfe of proved reserves

by 12/08, 13.5-14.0 tcfe by 12/09, and 15-16 tcfe by 12/10● #1 gas resource play● #1 gas resource play

– 55 tcfe of risked unproved reserve potential; >10-year drilling inventory of 35,500 net drilling locations

● #1 inventory of U.S. onshore leasehold and 3-D seismic– 15 0 mm net acres of U S onshore leasehold and 20 8 mm acres of 3-D seismic data

215.0 mm net acres of U.S. onshore leasehold and 20.8 mm acres of 3 D seismic data

Data above incorporates:• Information as of 9/30/08 - Pro forma for Marcellus Shale JV with StatoilHydro in 4Q’08• CHK’s Outlook as of 12/7/08• Risk disclosure regarding unproved reserve estimates appears on page 34

December 2008 Investor Presentation

Financial Highlights

● $22.2 billion enterprise value– $9.1 billion equity value, $10.8 billion net long-term debt, plus $0.5 billion preferred stock and

$1.8 billion working capital deficit● Strong profitability

– 2009E: ebitda $5.2 billion, operating cash flow $4.8 billion, net income to common $1.6 billion● Well hedged

– 71% of 4Q’08, 74% of 2009 and 48% of 2010 production hedged at average prices of $9.00, $8.48 and $9.81 per mcfe, respectively $ p , p y

● Innovative joint venture arrangements– CHK/PXP in Haynesville Shale: $3.3 billion for 20% interest– CHK/BP in Fayetteville Shale: $1.9 billion for 25% interest– CHK/STO in Marcellus Shale: $3.4 billion for 32.5% interest

● Prudent balance sheet● Prudent balance sheet– Net debt to cap ratio of 43% at 9/30/08; anticipating ~40% by 12/08 and ~34% by 12/09– Staggered maturities with low fixed rates; first maturity in November 2012– Strong asset and cash flow coverage of debt

● Anticipating substantial balance sheet improvement– Substantial asset growth cash generation and earnings set to meaningfully deleverage CHK by YE’09 – Substantial asset growth, cash generation and earnings set to meaningfully deleverage CHK by YE 09 – Since July 2008, CHK reduced drilling and leasehold and producing property acquisition capex by

~$10.0 billion, or ~58%● Great value to investors

– 2009E multiples: 1.9x operating cash flow, 4.3x ebitda, 5.6x P/E ratioTrading at steepest discount to estimated net asset value per share & lowest earnings multiples ever

3– Trading at steepest discount to estimated net asset value per share & lowest earnings multiples ever

Data above incorporates:• CHK’s Outlook as of 12/7/08 • Pro forma for Marcellus Shale JV with StatoilHydro and conversion of $765 million of senior notes for $24 million common shares in 4Q’08• Reconciliations to GAAP measures appear on page 23• Summary of hedging positions appear on page 26• An assumed common stock price of $15.00, NYMEX prices of $7.00/mcf and $70.00/bbl and excludes effects of FAS 133 (unrealized hedging gain or loss)

December 2008 Investor Presentation

Financial and Operational Update –Proactive Cash Flow Managementg

● CHK continues to proactively adapt to changing market conditions● Reduced 2009 and 2010 capital spending plans on 12/7/08 to

achie e a cash ne tral b dget o er the ne t t o ears that does not achieve a cash neutral budget over the next two years that does not depend on future asset sales– Further reduced drilling budget by $2.9 billion, or 31%, and leasehold and

acquisition budget by $2.2 billion, or 78%, relative to 11/3/08 Outlook– Have reduced spending plans four times in the last four months in response Have reduced spending plans four times in the last four months in response

to lower natural gas and oil prices and turbulent financial marketsSince July 2008, CHK has reduced its 2009 and 2010 spending plans for drilling, leasehold & producing property acquisitions by ~$10 billion, or 58%CHK operated rig count has decreased from 158 rigs in 8/08 to 130 rigs currently and will be further reduced to 110-115 rigs in early 1Q’09, when approximately half of its rigs paid fully or partially paid for by its JV partners

– Now targeting production growth of 5-10% in 2009 and 10-15% in 2010● Planning to build up to $4 billion in additional cash resources by

year-end 2010 through further asset monetizationsVPP d/ l f d i g ti– VPPs and/or sales of producing properties

– Leasehold sales or JVs– Midstream system sales or equity partner investments

4

December 2008 Investor Presentation

Financial and Operational Update –Asset Monetizations on the Horizon

● In discussions to sell CHK’s fourth VPP on properties in the Anadarko and Arkoma Basins

100 bcfe of proved reserves– ~100 bcfe of proved reserves– Current net production of ~55 mmcfe/day– ~$450 million in cash proceeds, or $4.50/mcfe– Working to close by year-end 2008

● Intend to market CHK’s fifth VPP on all or a portion of South TX ● Intend to market CHK s fifth VPP on all or a portion of South TX producing properties– Received multiple bids for entire asset package, but believe a VPP

transaction will yield a better value proposition– ~80 bcfe of proved reserves– Current net production of ~70 mmcfe/day– ~$450 million in cash proceeds, or $5.60/mcfe– Working to close in 1Q’09

● In discussions with multiple parties for either a minority investment in CHK’s midstream operations or the p rchase of a portion of in CHK’s midstream operations or the purchase of a portion of existing systems in 1Q’09

5

December 2008 Investor Presentation

Financial and Operational Update –Hedge Protection and Cost Advantagesg g

● Restructured hedge positions substantially protects 2009 cash flow– ~76% of anticipated 2009 natural gas production hedged through swaps

and collars with a floor of $8 20 per mcfeand collars with a floor of $8.20 per mcfe– Only 12% of anticipated production hedged through swaps with knock out

provisions, much of which is concentrated in 4Q’09● Anticipating substantially lower drillbit finding and development

costs for CHK in 2009 through:g– Joint venture drilling carries– 10-20% lower oilfield service costs– Continued operational excellence

● Targeting ~2.5 tcfe of proved reserve additions in 2009 from ~$3 billion of net drilling capital, which would imply a production replacement rate of >250% and a cost of ~$1.20/mcfe– Includes the benefit of drilling carries in CHK’s three shale JVs, with

~1.1 tcfe of proved reserve additions from $500 million in net drilling capital at a cost of ~$0 45/mcfecapital at a cost of $0.45/mcfe

6

December 2008 Investor Presentation

Financial and Operational Update –Liquidity and Filings with the SECq y g

● CHK has ample current and projected financial liquidity– ~$1.5 billion in cash and cash equivalents on hand in early December ’08– Targeting ~$2 billion in cash and cash equivalents by year-end 2008 if Targeting $2 billion in cash and cash equivalents by year end 2008 if

successful in completing CHK’s fourth VPP– Managing business to a cash neutral budget that is not dependent on future

asset sales● On 11/26/08, CHK filed registration statements and distribution

g g t ith th SEC i d t t b d fi i l agency agreements with the SEC in order to create broad financial flexibility for an uncertain economic and commodity market environment over the next few quarters– We underestimated how the market would assess the purpose, implication,

timing and magnitude of our filings; we made a mistakeg g g ;– In response, we have terminated our distribution agency agreement with

three securities firms and have amended our acquisition shelf registration statement on Form S-4 to reduce common shares registered from 50 million to 25 million

● In 4Q’08 CHK converted $765 million of convertible senior notes for ● In 4Q 08, CHK converted $765 million of convertible senior notes for ~24 million common shares– At face value of convertible senior notes, effective issue price of

~$32 per share– After considering the elimination of existing dilution potential in the notes,

effective issue price of >$40 per share(1)

7effective issue price of >$40 per share(1)

1) Assumes common stock price >$75 per share at maturity of convertible senior notes

CHK’s Distinctive Business Strategy

December 2008 Investor Presentation

We’re Good at Anticipating Opportunities & Challengesg

● CHK recognized earlier than most that higher oil and natural gas prices, combined with better drilling and completion technology, would potentially make unconventional gas resource plays highly economicgas resource plays highly economic

● Since ’98, Chesapeake’s business strategy has been to:– Grow through an aggressive unconventional resource discovery and leasing program followed

by large-scale drilling programs– Recognize and mitigate risks throughout our business– Recognize and mitigate risks throughout our business– Maintain a balanced capital structure with long-term debt maturities

● Today, Chesapeake is well positioned for the future:– Won the great early 21st century land grab and built the nation’s top gas resource base– Developed world-class technical capabilities in unconventional resources and discovered Developed world class technical capabilities in unconventional resources and discovered

multiple new plays – Achieved substantial operating scale and vertical integration including the nation’s 6th largest

drilling rig fleet, related service businesses and a large midstream gathering and processing operationB ilt f l d di ti ti t i l t lt th b bli CHK t – Built a successful and distinctive entrepreneurial corporate culture, thereby enabling CHK to have what it believes is the most talented, motivated and productive workforce in the industry

Expanded employee base over 13-fold over the last ten years to 7,600– In 2008, CHK has monetized producing assets and undeveloped leasehold that had a cost

basis of ~$3 billion for $11.7 billion in cash and drilling carries for a profit of ~$8.7 billion9

g p

Now moving to advance present value forward through asset monetizations via VPP’s and promoted partnerships

December 2008 Investor Presentation

CHK’s Business Model

● Chesapeake’s large and diversified production base and leasehold inventory offers multiple monetization and value offers multiple monetization and value creation alternatives– Volumetric production payments (VPPs)– Leasehold joint ventures– High-grading property sales– Hedging to secure strong profit margins

Invest inHigh Quality

Leasehold

Apply Cutting-EdgeGeoscience

Technology to DiscoverNew Plays

– Hedging to secure strong profit margins● Chesapeake’s diversified, vertically-integrated

“natural gas manufacturing machine” is well positioned for future growth– Industry-leading leasehold acquisition

programprogram– 7,600 total employees, including 1,800

geoscience, engineering and operations department employees

– The nation’s most active drilling program with 130 operated rigs including 83 rigs in

Harvest Value by SellingProducing Properties and/or

Proven Leasehold

DrillAggressivelyto IncreaseProductionwith 130 operated rigs, including 83 rigs in

CHK’s own rig fleet– Large midstream gathering and processing

operations– Compression operations and manufacturing

and through EverydayProductionof Mcfe’s

and ConvertLeaseholdto ProvedReserves

10

Asset Overview

CHK drilling a Barnett Shale well near downtown Fort Worth, Texas

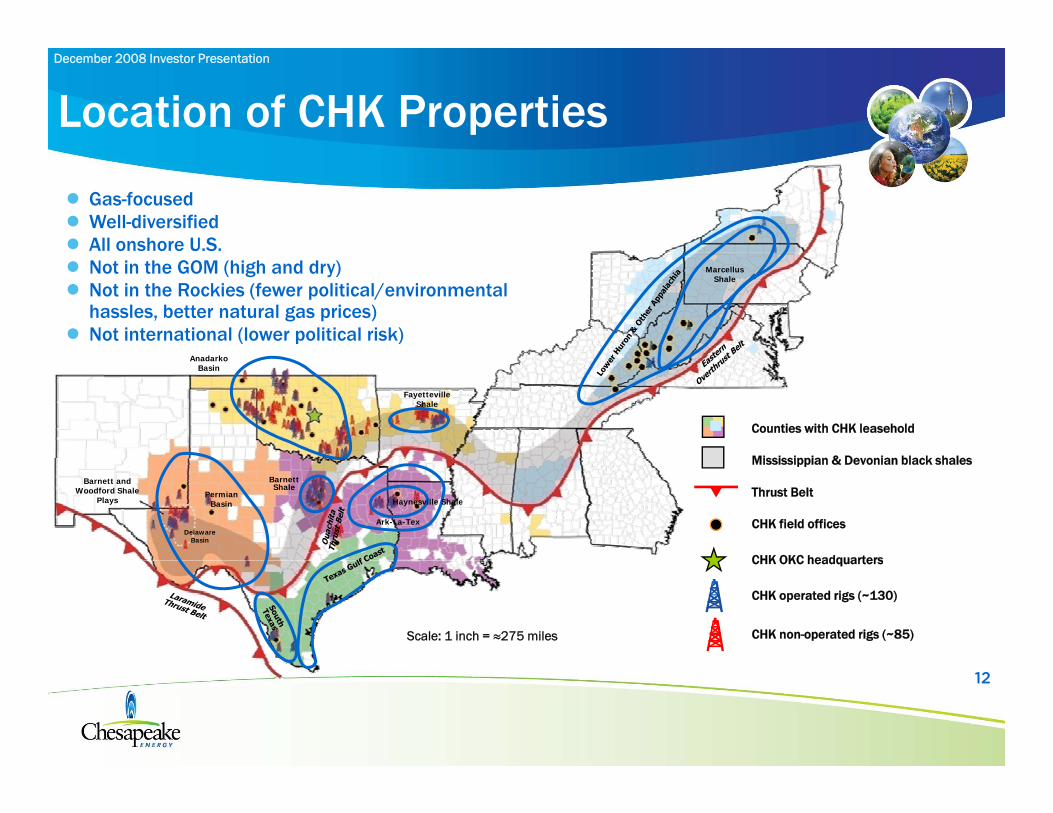

December 2008 Investor Presentation

Location of CHK Properties

● Gas-focused● Well-diversified● All onshore U.S.● Not in the GOM (high and dry)● Not in the Rockies (fewer political/environmental

hassles, better natural gas prices)● Not international (lower political risk)

d k

Marcellus Shale

Counties with CHK leasehold

Mississippian & Devonian black shales

AnadarkoBasin

FayettevilleShale

CHK field offices

Thrust Belt

CHK OKC headquarters

Mississippian & Devonian black shalesBarnettShale

PermianBasin

DelawareBasin

Barnett and Woodford Shale

Plays Haynesville Shale

Ark-La-Tex

Scale: 1 inch = ≈275 miles

CHK OKC headquarters

CHK operated rigs (~130)

CHK non-operated rigs (~85)

12

December 2008 Investor Presentation

America’s #1 Gas Resource Base

● CHK is well positioned for long-term fi bl h

Net Acreage15.0 million acres

Drillsites~35,500 net drillsites

profitable growth

● Largest combined inventories of leasehold and 3-D seismic data in the industry

● 2 3 bcfe of daily production 92% gas

4.65,500

10 4● 2.3 bcfe of daily production, 92% gas

● 12.1 tcfe of proved reserves, 93% gas

● 54.6 tcfe of risked unproved reserves– 168 tcfe of unrisked unproved reserves Proved Undeveloped Risked Unproved

10.4 30,000

p

● 15.0 million net acres of leasehold

● 20.8 million acres of 3-D seismic data

● >10-year inventory of ~35,500 net drillsites

pReserves

4.1 tcfe

pReserves54.6 tcfe

0.9 5.2

Conventional gas resource

Unconventional gas resource3.2 49.4

13

• As of 9/30/08 - Pro forma for recent Marcellus Shale JV with StatoilHydro • Risk disclosure regarding unproved reserve estimates appears on page 34

December 2008 Investor Presentation

CHK’s Drilling Inventory

Total ProvedEst. Risked Est. Avg. Total Risked and Risked Unrisked Current

CHK CHK Drilling Net Reserves Proved Unproved Unproved Unproved DailyIndustry Net Density Undrilled Per Well Reserves Reserves Reserves Reserves Production

Play Area Position (1) Acreage (Acres) Wells (bcfe) (bcfe) (bcfe) (bcfe) (bcfe) (mmcfe)

Conventional Gas Resource

Southern Oklahoma #1 345,000 120 600 2.20 740 900 1,640 3,300 155South Texas #3 130,000 80 350 2.00 430 400 830 1,700 125Mountain Front #1 140 000 320 100 5 00 220 300 520 1 100 70Mountain Front #1 140,000 320 100 5.00 220 300 520 1,100 70Other Conventional Top 3 3,985,000 Various 4,450 Various 2,320 3,600 5,920 19,500 455Conventional Sub-total 4,600,000 5,500 3,710 5,200 8,910 25,600 805

Unconventional Gas ResourceHaynesville Shale #1 480,000 80 3,000 6.50 200 14,400 14,600 29,000 50Marcellus Shale #1 1,200,000 80 3,700 3.75 30 11,600 11,630 46,200 15Marcellus Shale #1 1,200,000 80 3,700 3.75 30 11,600 11,630 46,200 15Fort Worth Barnett Shale #2 315,000 60 3,000 2.65 2,810 5,200 8,010 6,900 560Fayetteville Shale (Core Area) #2 415,000 80 3,700 2.20 535 6,600 7,135 8,900 145Sahara #1 970,000 70 7,400 0.55 1,125 2,800 3,925 4,600 225Colony, Granite & Atoka Washes #1 333,000 120 1,100 3.25 1,065 2,300 3,365 4,200 200Deep Haley #1 500,000 320 300 6.00 270 1,200 1,470 6,400 85Other Unconventional Top 3 6,187,000 Various 7,800 Various 2,310 5,300 7,610 36,000 250Unconventional Sub-total 10,400,000 30,000 8,345 49,400 57,745 142,200 1,530

Total 15,000,000 35,500 12,055 54,600 66,655 167,800 2,335

14

• As of 9/30/08 - Pro forma for recent Marcellus Shale JV with StatoilHydro • Risk disclosure regarding unproved reserve estimates appears on page 34

December 2008 Investor Presentation

CHK was the Largest U.S. Natural Gas Producer in 3Q’08

Daily U.S. Natural Gas Production (a,b) 2007 2007

3Q'08 3Q'08 Reported U.S. Proved U.S U.S. Rigsvs. 2Q'08 vs. 3Q'07 Net Proved Gas Gas Reserve RP Drilling on

C ( ) Ti k 3Q'08 2Q'08 3Q'07 % Ch g % Ch g Reserves R ki g R ti (d) 11/28/08 ( )Company (c) Ticker 3Q'08 2Q'08 3Q'07 % Change % Change Reserves Ranking Ratio (d) 11/28/08 (e)

Chesapeake CHK 2,138 2,143 1,851 (0.2%) 15.5% 10,137 4 13 130BP BP 2,094 2,140 2,186 (2.1%) (4.2%) 15,375 1 20 27ConocoPhillips COP 2,073 2,132 2,335 (2.8%) (11.2%) 12,634 3 17 48Devon DVN 2,006 1,939 1,784 3.5% 12.4% 7,143 7 10 81Anadarko APC 1,994 1,869 1,637 6.7% 21.8% 8,504 6 12 44Anadarko APC 1,994 1,869 1,637 6.7% 21.8% 8,504 6 12 44XTO XTO 1,949 1,795 1,561 8.6% 24.9% 9,441 5 13 85EnCana ECA 1,674 1,629 1,387 2.8% 20.7% 6,008 8 10 51Chevron CVX 1,431 1,588 1,695 (9.9%) (15.6%) 3,226 11 6 12EOG EOG 1,196 1,139 997 5.0% 20.0% 4,220 9 10 57ExxonMobil XOM 1,167 1,274 1,414 (8.4%) (17.5%) 13,172 2 31 14Willi WMB 1 096 1 110 926 (1 3%) 18 4% 4 143 10 10 33Williams WMB 1,096 1,110 926 (1.3%) 18.4% 4,143 10 10 33Shell RDS 942 1,096 1,131 (14.1%) (16.7%) 2,468 15 7 20El Paso EP 664 707 693 (6.1%) (4.2%) 3,100 12 13 28Apache APA 636 759 764 (16.2%) (16.8%) 2,699 13 12 16Occidental OXY 570 602 604 (5.3%) (5.6%) 2,672 14 13 13Southwestern SWN 569 487 317 16.8% 79.5% 1,450 19 7 28Newfield NFX 488 480 510 1.7% (4.3%) 1,810 18 10 29Questar STR 439 393 317 11.7% 38.5% 1,868 16 12 27Marathon MRO 426 431 464 (1.2%) (8.2%) 1,007 20 6 17Noble NBL 384 402 404 (4.5%) (5.0%) 1,840 17 13 11

Totals / Average 23,936 24,115 22,977 -0.8% 7.1% 112,918 12 771

15(a) Based on company reports(b) In mmcf/day(c) Independents in blue, majors in black, pipelines in green(d) Based on annualized 3Q’08 production(e) Source: Smith International Survey (operated rig count)

December 2008 Investor Presentation

What’s New in the Haynesville Shale?

● CHK’s largest discovery and expected to become the largest U.S. natural gas fieldPl 3 5 illi i NW

100 Miles

● Play encompasses a ~3.5 million acre area in NW Louisiana and E. TX

● CHK is the largest leasehold owner in the core area of the play, ~700,000 gross acres, ~480,000 net acres (after PXP 20 %) or ~20% of the playnet acres (after PXP 20 %), or ~20% of the play

● Planning to ramp from 14 rigs currently, up to ~35 by YE’09

● 9/30/08 net production of ~50 mmcfe/day (~65 mmcfe gross)

90 M

iles

mmcfe gross)● Based on drilling results by CHK, an EUR range of

4.5–8.5 bcfe per well for the Core Area is reasonable with mid-point of 6.5 bcfe

● ~3,000 potential net risked wells in inventory to CHK HorizontalP d i W ll

, p ydevelop 14 tcfe of risked unproved reserves – Currently have 130 bcfe of PUD reserves

Area Within Outline = 3.5 Million Acres

Horizontal RigsChesapeake

Horizontal RigsIndustry

HaynesvillePenetrations

CHK Acreage

Producing Wells

Industry HorizontalProducing Wells

16

Note: Risk disclosure regarding unproved reserve estimates appears on page 34

December 2008 Investor Presentation

What’s New in the Barnett Shale?

● CHK is the second-largest producer, most active driller and largest leasehold owner in the Core and 82 Miles gTier 1 sweet spots of Tarrant, Johnson and western Dallas counties

● 9/30/08 net production of ~560 mmcfe/day is up ~37% YTD

● Have improved drilling efficiency and reduced avg. days to drill from 30-35 days to 15-20 days

● Planning to operate an average of ~26 rigs in 2009 to further develop ~315,000 net acres of leasehold,

Core &Tier 1Outline

67 M

iles

p , ,of which ~280,000 net acres are located in the prime Core and Tier 1 areas

● Industry leading urban-drilling expertise has become a significant competitive advantageCHK Acreage

● ~3,000 potential net risked wells in inventory to develop ~0.8 tcfe of PUD and 5.2 tcfe of risked unproved reserves

CHK Rigs

17

Note: Risk disclosure regarding unproved reserve estimates appears on page 34

December 2008 Investor Presentation

What’s New in the Fayetteville Shale?

● Planning to operate an average of ~20 rigs in 2009 to further develop ~415,000

t f l h ld net acres of leasehold ● 9/30/08 net production of ~145

mmcfe/day is up ~46% YTD● ~3,700 potential net risked wells in

inventory to develop = ~7.1 tcfe of PUD y pand risked unproved reserves– ~9 tcfe of PUD and unrisked unproved

reserves● Closed sale of 25% interest in ~540,000

net acres and ~180 mmcfe/day of / yproduction to BP for $1.9 billion ($1.1 billion in cash, $800MM in carry) in September 2008

● Secured firm transportation capacity of 375 mmcf/day and an option on 125

Chesapeake Rigs

Industry Rigs

Fayetteville Penetrations

CHK Acreage

CHK Producing Wells

Industry Producing Wells

375 mmcf/day and an option on 125 mmcf/day on the Fayetteville Express pipeline that will be built and operated by Kinder Morgan and Energy Transfer– Late 2010/early 2011 completion

● CHK is the second-largest producer in the Fayetteville Shale and second-largest leasehold owner in the Core area of the play

18

Note: Risk disclosure regarding unproved reserve estimates appears on page 34

December 2008 Investor Presentation

What’s New in the Marcellus Shale?

● CHK is a top-3 producer and the largest

CHK Rigs

CHK Acreage

leasehold owner in the Marcellus Shale play● Currently operating ~3 rigs to further develop

~1.2 million net acres of leasehold and plan to operate up to 15 rigs by YE’09

● 9/30/08 net production of ~15 mmcfe/day is up ~300% YTD

● CHK sold a 32.5% interest in CHK’s Marcellus Shale assets in Appalachia to StatoilHydro for $3 375 billion$3.375 billion– CHK received $1.25 billion in cash at closing and

will collect a further $2.125 billion from 2009 to 2012 to fund 75% of CHK’s 67.5% share of drilling and completion expenditures

– Transaction closed on 11/24/08

19

Note: Risk disclosure regarding unproved reserve estimates appears on page 34

Financial Overview

December 2008 Investor Presentation

Strong Cash Margins andSteady Debt Levels per Mcfe

$8 50 $9.00 $9.50

Net cash marginP f d di id d

y p

3Q’08 Averages(per mcfe)

$6.00 $6.50 $7.00 $7.50 $8.00 $8.50 Preferred dividends

Interest expense G&AProduction taxProduction expenseLong term debt/mcfe of proved reserves

3Q’08 net cash

Realized price: $8.38

(1)

(2)

$3 00 $3.50 $4.00 $4.50 $5.00 $5.50 $

$ /

mcf

e

3Q 08 net cashmargin: $6.18

$0.50 $1.00 $1.50 $2.00 $2.50 $3.00

Production expense: $1.12

Production tax: $0.41

Preferred dividends: $0.03Interest expense: $0.26G&A: $0.38

$0.00

1999 2000 2001 2002 2003 2004 2005 2006 2007 1Q08 2Q08 3Q08

Total cash costs = $2 20

Sr. UnsecuredRating B3/B B2/B B1/B+ B1/B+ Ba3/BB- Ba3/BB- Ba2/BB Ba2/BB Ba3/BB

Ba3/BB

21Total cash costs = $2.20

(1) Excludes unrealized gains/losses on interest rate derivatives(2) Excludes non-cash stock based compensation

December 2008 Investor Presentation

Senior Note Maturity Schedule@ 9/30/08

$3,600

$4,000

Total Senior Notes: $10.1 billion

/ /

$2 400

$2,800

$3,200Average Rate: 5.6%Average Maturity: 8.3 years

$2,526(1)

$3,323(1)

$1,600

$2,000

$2,400

$ in

MM

$1 270

$400

$800

$1,200$864

$600

$1,051(1)

$1,270

$500Bank credit

facility matures November 2012

$0

$400

'08 '09 '10 '11 '12 '13 '14 '15 '16 '17 '18 '19 '20

(1) Recognizes earliest investor put option as maturity and pro forma for conversion of $765 illi f tibl i t f 24 illi h i 4Q’08

Rate:7.625% 6.375%

6.625%6.875%

7.5%7.0%

6 25%6 5%

2.75% 6.875%7.5%6.25%2.5%

7.25%2.25%

November 2012

22$765 million of convertible senior notes for 24 million common shares in 4Q’08 6.25%6.5%

Staggered long term debt maturity structure with no senior notes due for five years; cash flow of >$30 billion likely before first payment

December 2008 Investor Presentation

2009 Financial Projections at Various Natural Gas Prices

($ in millions; oil at $70.00 NYMEX) $5.00 $6.00 $7.00 $8.00 $9.00

O/G revenue (unhedged) @ 880 bcfe(1) $4,338 $5,050 $5,761 $6,473 $7,185

H d i ff t(2) 1 660 1 266 1 015 566 135

As of 12/7/08 Outlook

Hedging effect(2) 1,660 1,266 1,015 566 135

Marketing and other (@ $0.15/mcfe) 132 132 132 132 132

Production taxes 5% (217) (252) (288) (324) (359)

LOE (@ $1.15/mcfe) (1,012) (1,012) (1,012) (1,012) (1,012)

G&A (@ $0.46/mcfe)(3) (405) (405) (405) (405) (405)

Ebitda 4,496 4,779 5,203 5,430 5,676

Interest (@ $0.43/mcfe) (374) (374) (374) (374) (374)

Operating cash flow(2)(3)(4) 4,122 4,405 4,829 5,056 5,302

Oil and gas depreciation (@ $2.25/mcfe) (1,980) (1,980) (1,980) (1,980) (1,980)

Depreciation of other assets (@ $0 22/mcfe) (194) (194) (194) (194) (194) Depreciation of other assets (@ $0.22/mcfe) (194) (194) (194) (194) (194)

Income taxes (38.5% rate) (750) (859) (1,022) (1,110) (1,205)

Net income to common(1) $1,198 $1,372 $1,633 $1,772 $1,923

Net income to common per fully diluted shares $1.98 $2.27 $2.70 $2.93 $3.18

Net debt/ebitda(5) 2.4 2.3 2.1 2.0 1.9

Debt to book capitalization ratio 34% 34% 34% 33% 33%

Ebitda/fixed charges (including pfd. dividends)(6) 7.6 8.1 8.8 9.2 9.6

MEV/operating cash flow(7) 2.2x 2.1x 1.9x 1.8x 1.7x

EV/ebitda(8) 5.0x 4.7x 4.3x 4.1x 3.9x

PE ratio(9) 7 6x 6 6x 5 6x 5 1x 4 7x23

PE ratio 7.6x 6.6x 5.6x 5.1x 4.7x(1) Before effects of FAS 133 (unrealized hedging gain or loss)(2) Includes the non-cash effect of CNR hedges(3) Includes charges related to stock based compensation(4) Before changes in assets and liabilities(5) Net debt = long-term debt less cash(6) Fixed charges ($590mm) = interest expense of $566 million plus dividends of $24 million(7) MEV (Market Equity Value) = $9.1 billion ($15.00/share x 607 mm fully diluted shares as of 09/30/08; pro forma for conversion of $765 million of convertible senior notes for 24 million shares in 4Q’08)(8) EV (Enterprise Value) = $22.2 billion (Market Equity Value, plus $10.8 billion of net long-term debt plus $0.5 billion preferred stock treated as debt and $1.8 billion working capital deficit)(9) Assuming a common stock price of $15.00/share

December 2008 Investor Presentation

2010 Financial Projections at Various Natural Gas Prices

($ in millions; oil at $80.00 NYMEX) $5.00 $6.00 $7.00 $8.00 $9.00

O/G revenue (unhedged) @ 996 bcfe(1) $5,005 $5,811 $6,618 $7,424 $8,230

Hedging effect(2) 767 941 1 331 930 504

As of 12/7/08 Outlook

Hedging effect 767 941 1,331 930 504

Marketing and other (@ $0.15/mcfe) 149 149 149 149 149

Production taxes 5% (258) (299) (341) (382) (424)

LOE (@ $1.20/mcfe) (1,195) (1,195) (1,195) (1,195) (1,195)

G&A (@ $0.46/mcfe)(3) (458) (458) (458) (458) (458)

Ebitda 4,010 4,949 6,104 6,468 6,806

Interest (@ $0.38/mcfe) (374) (374) (374) (374) (374)

Operating cash flow(2)(3)(4) 3,636 4,575 5,730 6,094 6,432

Oil and gas depreciation (@ $2.20/mcfe) (2,191) (2,191) (2,191) (2,191) (2,191)

Depreciation of other assets (@ $0 22/mcfe) (219) (219) (219) (219) (219) Depreciation of other assets (@ $0.22/mcfe) (219) (219) (219) (219) (219)

Income taxes (38.5% rate) (472) (833) (1,278) (1,418) (1,548)

Net income to common(1) $754 $1,332 $2,042 $2,266 $2,474

Net income to common per fully diluted shares $1.23 $2.17 $3.33 $3.69 $4.03

Net debt/ebitda(5) 2.7 2.2 1.8 1.7 1.6

Debt to book capitalization ratio 27% 27% 26% 26% 26%

Ebitda/fixed charges (including pfd. Dividends)(6) 6.8 8.4 10.4 11.0 11.6 MEV/operating cash flow(7) 2.5x 2.0x 1.6x 1.5x 1.4x

EV/ebitda(8) 5.6x 4.5x 3.6x 3.4x 3.3x

PE ti (9) 12 2 6 9 4 5 4 1 3 724

PE ratio(9) 12.2x 6.9x 4.5x 4.1x 3.7x(1) Before effects of FAS 133 (unrealized hedging gain or loss)(2) Includes the non-cash effect of CNR hedges(3) Includes charges related to stock based compensation(4) Before changes in assets and liabilities(5) Net debt = long-term debt less cash(6) Fixed charges ($588mm) = interest expense of $566 million plus dividends of $22 million(7) MEV (Market Equity Value) = $9.1 billion ($15.00/share x 607 mm fully diluted shares as of 09/30/08; pro forma for conversion of $765 million of convertible senior notes for 24 million shares in 4Q’08)(8) EV (Enterprise Value) = $22.2 billion (Market Equity Value, plus $10.8 billion of net long-term debt, plus $0.5 billion preferred stock treated as debt and $1.8 billion working capital deficit)(9) Assuming a common stock price of $15.00/share

December 2008 Investor Presentation

Cash Resource Plan 4Q’08 - ’10(1)

Net Cash Resources ($ in millions) Total

Operating cash flow(1)(2) $1,250 - $1,300 $4,800 - $5,100 $5,700 - $6,100 $11,750 - $12,500Leasehold and producing properties transactions Sales 1,400 - 1,450 500 - 1,000 500 - 1,000 2,400 - 3,450 Volumetric Production Payments 425 - 475 900 - 1 000 450 - 500 1 775 - 1 975

Q4'08E 2010E2009E

Volumetric Production Payments 425 475 900 1,000 450 500 1,775 1,975 Acquisitions (900 - 1,000) (300 - 350) (250 - 300) (1,450 - 1,650) Net leasehold and producing properties transactions 925 - 925 1,100 - 1,650 700 - 1,200 2,725 - 3,775Debt and equity offerings - - - -Midstream debt and equity financings 460 500 - 600 500 - 600 1,460 - 1,660Proceeds from investments and other - - - -

Total: $2,635 - $2,685 $6,400 - $7,350 $6,900 - $7,900 $15,935 - $17,935

Net Cash Uses ($ in millions)Drilling $1,400 - $1,500 $2,800 - $3,100 $3,500 - $3,800 $7,700 - $8,400Geologic and geophysical 75 100 - 125 100 - 125 275 - 325Midstream infrastructure and compression 300 - 325 500 - 600 500 - 600 1,300 - 1,525Other PP&E 100 - 150 200 - 250 200 - 250 500 - 650Dividends, capitalized interest, etc. 150 - 200 500 - 600 500 - 600 1,150 - 1,400Cash income taxes 300 - 325 250 - 275 100 - 200 650 - 800Total: $2 325 $2 575 $4 350 $4 950 $4 900 $5 575 $11 575 $13 100Total: $2,325 - $2,575 $4,350 - $4,950 $4,900 - $5,575 $11,575 - $13,100

Net Cash Change $110 - 310 $2,050 - 2,400 $2,000 - 2,325 $4,360 - 4,835

$3.5 billion revolving credit facility ($ in millions)Beginning balance, net of cash on hand $1,500 $1,290 ($935)Potential change ($210) ($2,225) ($2,165)Ending balance, net of cash on hand $1,290 ($935) ($3,100)

Production (bcfe per day) 2.25 2.41 2.73

Proved reserves(3) (tcfe) 12.25 13.75 15.5Proved reserves per fully diluted share (mcfe) 20.7 22.7 25.3YOY % change in proved reserves per FD share 15% 10% 11%

Debt to Capitalization 40% 34% 26%

Long-term debt, net of cash on hand ($ in millions)(4) $11,870 $9,645 $7,480

25

(1) From Outlook as of 12/7/08 and assumes NYMEX prices of $6.95/mcf and $63.91/bbl in 4Q’08 and $7.00-$8.00/mcf, $70/bbl and $80/bbl in 2009 and 2010, respectively

(2) Before changes to asset and liabilities. Reconciliations to GAAP measures appear on pages 23-24(3) Under existing SEC proved reserve definitions – likely to increase by up to 5 tcfe per year beginning 12/31/09(4) Pro forma for conversion of $765 million of convertible senior notes for 24 million shares in 4Q’08

Long-term debt per mcfe of proved reserves $0.97 $0.70 $0.48

December 2008 Investor Presentation

Successful Hedging Reduces Risk andHelps Secure Attractive Cash Marginsp g

CHK’s natural gas and oil hedge positions for 4Q’08-2010(1)(2)

Natural Gas Collars(5) % HedgedNYMEX Avg. Floor Price

4Q 2008 Total 14% $7.75 $9.322009 Total 38% $7 36 $9 06

Nymex Avg. Ceiling PriceNatural Gas Swaps(3)(4) % Hedged

NYMEX Avg. Price

4Q 2008 Total 60% $9.09

2009 Total 37% $9 10

GOilOil GNYMEX Strip Prices @ 12/5/08

(6)NYMEX

2009 Total 38% $7.36 $9.062010 Total 3% $7.71 $11.46

2009 Total 37% $9.10

2010 Total 46% $9.58

Gas

$ 7 07$ 65 12

Oil

4Q 20082009201020112012

$ 6.94$ 6.17$ 7.25$ 7.51$ 7.50

$ 77.92$ 48.76$ 59.78$ 67.18$ 71.97

5 Y A

Oil GasOil(6) % Hedged

4Q 2008 Total 43%

2009 Total 48%

2010 Total 37%

Avg. Price

$90.25

$78.09

$81.19

$ 7.07$ 65.125-Year Average$

26(1) Excludes written calls(2) Includes CNR derivative liabilities assumed at MTM value upon closing. Assumes approximately the midpoint of company

production forecast for each item and includes hedging positions as of 12/7/2008(3) Includes positions with knockout provisions for 12% of 2009 at knockout prices of $5.75 - $6.75 and for 35% of 2010 production

at knockout prices of $5.45 - $7.40/mcf(4) Does not include calls written with average premiums of $0.74 at average strike prices of $10.37 in 4Q’08, $0.63 and $11.40 in

2009 and $0.72 and $10.77 in 2010(5) Includes three-way collars(6) Includes cap-swaps and knockout swaps

Summaryy

December 2008 Investor Presentation

CHK = Great Value

($ in millions, except per share data) $5.00 $6.00 $7.00 $8.00 $9.00

September 30, 2008 - Pro FormaNAV @ various NYMEX gas prices(1)

Average NYMEX Natural Gas Prices

Proved reserves 15,600$ 19,800$ 23,900$ 28,100$ 32,300$ Unproved reserves(2) 5,500 10,900 21,800 32,700 43,700 Value of CHK hedges(3) 3,500 3,300 3,600 2,600 1,600 Value of CNR hedges - - (100) (100) (100) Other assets(4) 4,500 4,500 4,500 4,500 4,500 PXP, BP and STO future drilling cost receivables 4,525 4,525 4,525 4,525 4,525 Less: long-term debt (net of cash equivalents) (10,800) (10,800) (10,800) (10,800) (10,800) Less: preferred stock (when not dilutive) (500) (300) - - - Less net working capital (1,800) (1,800) (1,800) (1,800) (1,800)

Shareholder value 20,525$ 30,125$ 45,625$ 59,725$ 73,925$

Fully diluted common shares (in millions)(5) 607 614 620 620 620

NAV per share 33.81$ 49.06$ 73.59$ 96.33$ 119.23$ p

Potential % upside(5) 125% 227% 391% 542% 695%

Asset value to long-term debt 2.9x 3.8x 5.2x 6.5x 7.8x

Leasehold Transaction Implied Values UndrilledAcres Net

Plays to CHK

Implied Shale Leasehold Value

($ in billions)

Implied Shale Leasehold

Value/AcreGasOil

4Q 2008 $ 6 94$ 77 92

Oil GasNYMEX Strip Prices @ 12/5/08

Marcellus Shale 1,200,000 $5,800 $7.0Haynesville Shale 480,000 $15,000 $7.2Fayetteville Shale 415,000 $12,500 $5.2Fort Worth Barnett Shale Core & Tier 1 280,000 $17,500 $4.9All other plays 13,225,000 $1,000 $13.2Total 15,600,000 $2,402 $37.5

$ 7.07$ 65.12

4Q 20082009201020112012

$ 6.94$ 6.17$ 7.25$ 7.51$ 7.50

$ 77.92$ 48.76$ 59.78$ 67.18$ 71.97

5-Year Average

28(1) NYMEX natural gas price scenarios and NYMEX oil price held constant at $100.66 per bbl - Pro forma for

recent Marcellus Shale JV with StatoilHydro; $1.25 billion in cash received at closing(2) 55 tcfe of unproved reserves valued from $0.10-$0.80/mcfe(3) As of Outlook issued on 12/7/08(4) Buildings, drilling rigs, midstream gas assets at net book value and investments at market value(5) Based on common stock price of $15.00 per share – Pro forma for conversion of $765 million of convertible

senior notes for 24 million shares in 4Q’08

December 2008 Investor Presentation

Why Buy CHK?

● Gas Focus– Purest play in U.S. natural gas; largest producer of U.S. natural gas

● GrowthGrowth– Total production growth of 23% in ’07; projecting increases of 17% in ’08, 5-10% in ’09 and

10-15% in ’10 ● Sustainability

– 55 tcfe of proved and risked unproved reserves; >10-year drilling backlog of ~35,500 net drillsites across multiple gas resource playsdrillsites across multiple gas resource plays

● Value– Trade at a substantial discount to estimated NAV

● Diversified Risk– Uniquely focused business strategy; well-diversified, all-onshore U.S. asset base

● Security● Security– Strong asset value to debt coverage; substantial cash flow generation capabilities

● Hedging– Successful track record of locking in margins and investment returns during past five years

● Balance Sheet– Balanced structure; long-term assets financed with staggered long-term debt maturities; greatly

expanded equity base; substantial deleveraging possible through asset monetization program over the next two years

● Income– Pay a $0.30 annual common stock dividend

29

• Reflects CHK’s Outlook as of 12/7/08 • Risk disclosure regarding unproved reserve estimates appears on page 34

y

Appendixpp

December 2008 Investor Presentation

Natural Gas Advantages

● CLEAN:– Carbon-light structure represents a key advantage for America’s

g f tenergy futureNatural gas is a simple molecule that contains only one carbon atom and four hydrogen atoms

– Natural gas is by far the cleanest-burning hydrocarbon on the planetEmits half the CO2 of coal, contains low levels of nitrogen and sulfur dioxide 2 gand near zero levels of mercury or particulate emissions

– Drilling for natural gas leaves a small footprintPad drilling, for example, is a great new innovation to further reduce surface impact

● AFFORDABLE:● AFFORDABLE:– Natural gas prices are roughly 60% of the BTU equivalent price of oil– Developing LNG market worldwide helps reduce gas price volatility in

the U.S.– In 2007 the cost of heating homes with natural gas per BTU was less In 2007, the cost of heating homes with natural gas per BTU was less

than half that of electricity– Compressed natural gas (CNG) is ~$1.14 per gallon in Oklahoma and

if you had a home fueling unit your price would be between $0.80 –$0.95 per gallon

31

December 2008 Investor Presentation

Natural Gas Advantages

● ABUNDANT:– Latest Colorado School of Mines Potential Gas Committee study

estimate shows potential gas reserves of 1,525 tcf in the U.S. –a 75-year supply!

This new projection, coupled with Canadian projections, gives North America over 120 years of supply

– Recent shale discoveries change everything we know about natural Recent shale discoveries change everything we know about natural gas supply in the U.S. and the world

Higher natural gas prices combined with better drilling and completion technology has made a whole new class of assets economic to drillThousands of acres have opened up for new drilling activity and future production growthproduction growth

● AMERICAN:– Natural gas is produced in 32 of 50 states

benefits of greater production and use are very widespread

32

December 2008 Investor Presentation

Corporate Information

Chesapeake Headquarters6100 N. Western Avenue

Contacts:

Jeffrey L. Mobley, CFAOklahoma City, OK 73118Web site: www.chk.com

Senior Vice President –Investor Relations and Research(405) [email protected]

C St k NYSE CHK

Marcus C. RowlandExecutive Vice President andChief Financial Officer

Common Stock – NYSE: CHK

Other Publicly Traded Securities CUSIP Ticker7.5% Senior Notes Due 2013 #165167BC0 CHK137.5% Senior Notes Due 2014 #165167BG1 CHK147.0% Senior Notes Due 2014 #165167BJ5 CHKA14 Chief Financial Officer

(405) [email protected]

6.875% Senior Notes Due 2016 #165167BE6 CHK166.375% Senior Notes Due 2015 #165167BL0 CHKJ156.625% Senior Notes Due 2016 #165167BN6 CHKJ166.50% Senior Notes Due 2017 #165167BS5 CHK176.25% Senior Notes Due 2018 #165167BQ9 CHK186.875% Senior Notes Due 2020 #165167BV0 CHK202 75% C ti t C tibl S i N t D 2035 #165167BW6 CHK352.75% Contingent Convertible Senior Notes Due 2035 #165167BW6 CHK357.625% Senior Notes Due 2013 #165167BY2 CHKJ136.25% Senior Notes Due 2017 #027393390 N/A2.50% Contingent Convertible Senior Notes Due 2037 #165167BZ9/165167CA3 CHK37/CHK37A7.25% Senior Notes Due 2018 #165167CC9 CHK18A2.25% Contingent Convertible Senior Notes Due 2038 #165167CB1 CHK38

33

(1) ISIN #

December 2008 Investor Presentation

Certain Reserve & Production Information

● The Securities and Exchange Commission has generally permitted oil and gas companies, in their filings with the SEC, to disclose only proved reserves that a company has demonstrated by actual production or conclusive formation tests to be economically and legally producible under existing p y g y p geconomic and operating conditions. We use the terms “unproved” reserves, including both “risked” and “unrisked” unproved reserves, reserve “potential” or “upside”, “ultimate recovery” and other descriptions of volumes of reserves potentially recoverable through additional drilling or recovery techniques that the SEC’s guidelines may prohibit us from including in filings with the SEC. To estimate unproved reserves the company uses a probability-weighted statistical approach to estimate estimate unproved reserves, the company uses a probability weighted statistical approach to estimate the potential number of drillsites and potential unproved reserves associated with such drillsites. These estimates are by their nature more speculative than estimates of proved reserves and accordingly are subject to substantially greater risk of being actually realized by the company. The company's methodology for estimating "unproved" reserves is different from the methodology and guidelines used by the Society of Petroleum Engineers for estimating "probable" and "possible" guidelines used by the Society of Petroleum Engineers for estimating probable and possible reserves.

● Our production forecasts are dependent upon many assumptions, including estimates of production decline rates from existing wells and the outcome of future drilling activity. Also, our internal estimates of reserves, particularly those in our recent acquisitions where we may have limited review

f d t i ith th ti b bj t t i i d b diff t f th of data or experience with the properties, may be subject to revision and may be different from those estimates by our external reservoir engineers at year end. Although we believe the expectations, estimates and forecasts reflected in these and other forward-looking statements are reasonable, we can give no assurance they will prove to have been correct. They can be affected by inaccurate assumptions and data or by known or unknown risks and uncertainties.

34

December 2008 Investor Presentation

Forward-Looking Statements

● This presentation includes include “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. Forward-looking statements give our current expectations or forecasts of future events. They include estimates of future natural gas and oil reserves, expected natural gas and oil production andfuture expenses assumptions regarding future natural gas and oil prices planned asset sales budgeted capital expenditures future expenses, assumptions regarding future natural gas and oil prices, planned asset sales, budgeted capital expenditures for drilling and acquisitions of leasehold and producing property, and other anticipated cash outflows, as well as statementsconcerning anticipated cash flow and liquidity, business strategy and other plans and objectives for future operations. Disclosures concerning the fair value of derivative contracts and their estimated contribution to our future results of operations are based upon market information as of a specific date. These market prices are subject to significant volatility.

● Factors that could cause actual results to differ materially from expected results are described in “Risk Factors” in the y pProspectus Supplement we filed with the U.S. Securities and Exchange Commission on November 26, 2008. These risk factors include the volatility of natural gas and oil prices; the limitations our level of indebtedness may have on our financial flexibility; unanticipated adverse effects the current financial crisis may have on our business and financial condition; the availability ofcapital on an economic basis, including through planned asset monetization transactions, to fund reserve replacement costs; our ability to replace reserves and sustain production; our ability to compete effectively against strong independent natural gas and oil companies and majors; uncertainties inherent in estimating quantities of natural gas and oil reserves and projecting future rates of production and the amount and timing of development expenditures; uncertainties in evaluating natural gas andoil reserves of acquired properties and associated potential liabilities; possible unsuccessful exploration and development drilling; declines in the values of our natural gas and oil properties resulting in ceiling test write-downs; lower prices realized on natural gas and oil sales and collateral required to secure hedging liabilities resulting from our commodity price risk management activities; the negative impact lower natural gas and oil prices could have on our ability to borrow; drilling andoperating risks, including potential environmental liabilities; production interruptions that could adversely affect our cash flow; and pending or future litigation Our production forecasts are dependent upon many assumptions including estimates of and pending or future litigation. Our production forecasts are dependent upon many assumptions, including estimates of production decline rates from existing wells and the outcome of future drilling activity. Although we believe the expectations and forecasts reflected in these and other forward-looking statements are reasonable, we can give no assurance they will prove to have been correct. They can be affected by inaccurate assumptions or by known or unknown risks and uncertainties.

● We caution you not to place undue reliance on our forward-looking statements, which speak only as of the date of this presentation and we undertake no obligation to update this information

35presentation, and we undertake no obligation to update this information.