Embed Size (px)

Citation preview

Delivering sustainable solutions in a more competitive world

Review of Packaging Deposits System for the UK Final Report December 2008 www.erm.com

Defra

Review of Packaging Deposits System for the UK

December 2008

Reference 0088452

Prepared by: Simon Gandy, Jonna Fry and Jackie Downes

For and on behalf of Environmental Resources Management Approved by: Simon Aumonier Signed: Position: Partner Date: 11th December 2008

This report has been prepared by Environmental Resources Management the trading name of Environmental Resources Management Limited, with all reasonable skill, care and diligence within the terms of the Contract with the client, incorporating our General Terms and Conditions of Business and taking account of the resources devoted to it by agreement with the client. We disclaim any responsibility to the client and others in respect of any matters outside the scope of the above. This report is confidential to the client and we accept no responsibility of whatsoever nature to third parties to whom this report, or any part thereof, is made known. Any such party relies on the report at their own risk.

CONTENTS

EXECUTIVE SUMMARY I

1 INTRODUCTION 1

1.1 BACKGROUND TO THE PROJECT 1 1.2 OBJECTIVES OF THIS PROJECT 1 1.3 ERM’S APPROACH 2 1.4 STRUCTURE OF THIS REPORT 3

2 FEATURES OF BEVERAGE CONTAINER DEPOSIT SYSTEMS 4

2.1 INTRODUCTION 4 2.2 TYPICAL SCOPE OF A BEVERAGE DEPOSIT SYSTEM 5 2.3 PARTIES INVOLVED IN DEPOSIT SYSTEMS 6 2.4 MANDATORY VERSUS VOLUNTARY DEPOSIT SYSTEMS 8 2.5 LABELLING CONTAINERS 8 2.6 TYPICAL BEVERAGE CONTAINER COLLECTION MECHANISMS 9 2.7 SORTING, BULKING AND RECYCLING/RECOVERING OF CONTAINERS 10 2.8 ASSURING SECURITY AND PREVENTING FRAUD 11 2.9 POTENTIAL HEALTH AND SAFETY IMPLICATIONS OF DEPOSIT SYSTEMS 12 2.10 POTENTIAL CROSS BOUNDARY ISSUES AND SINGLE MARKET IMPLICATIONS 13 2.11 COSTS AND INCOME STREAMS 14 2.12 VALUE OF THE DEPOSIT 15 2.13 TYPICAL CONTAINER RETURN RATES IN DEPOSIT SYSTEMS 17 2.14 IMPACTS OF DEPOSIT SCHEMES 17 2.15 THE ROLE OF REVERSE VENDING MACHINES (RVMS) 18 2.16 THE ROLE OF THE CLEARING HOUSE 22 2.17 SUMMARY – ADVANTAGES AND DISADVANTAGES OF DEPOSITS SYSTEMS 22

3 THE CURRENT UK SYSTEM 24

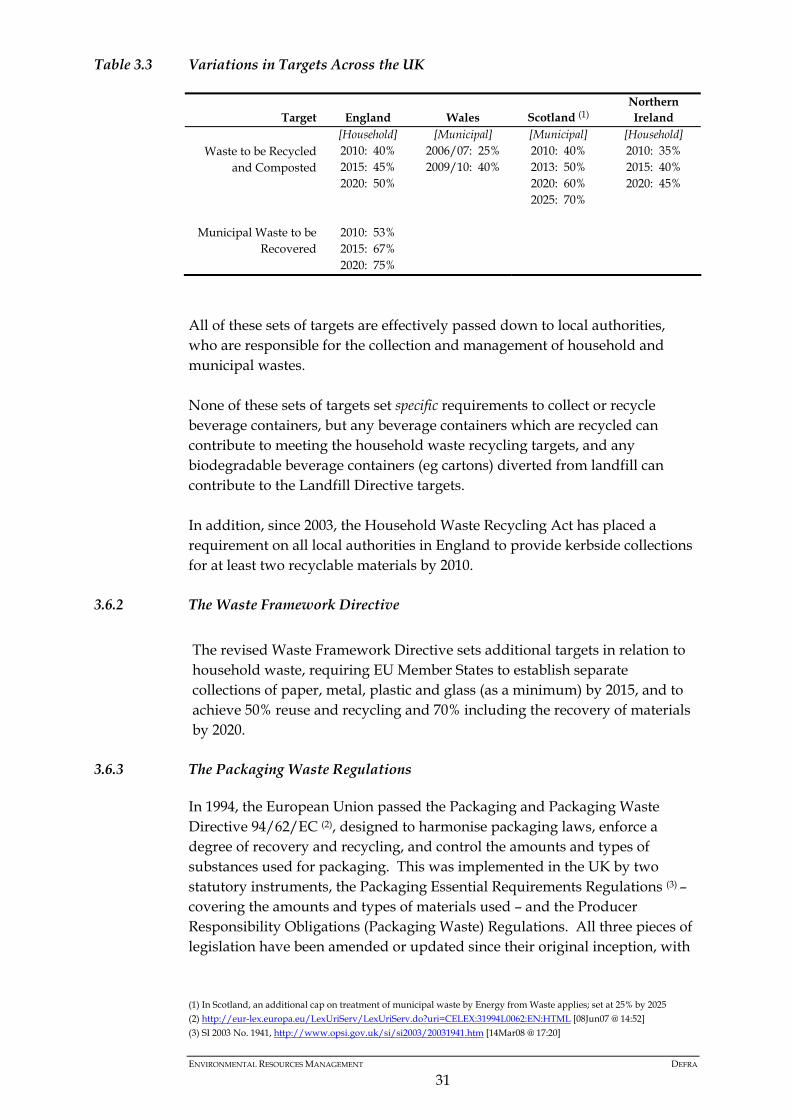

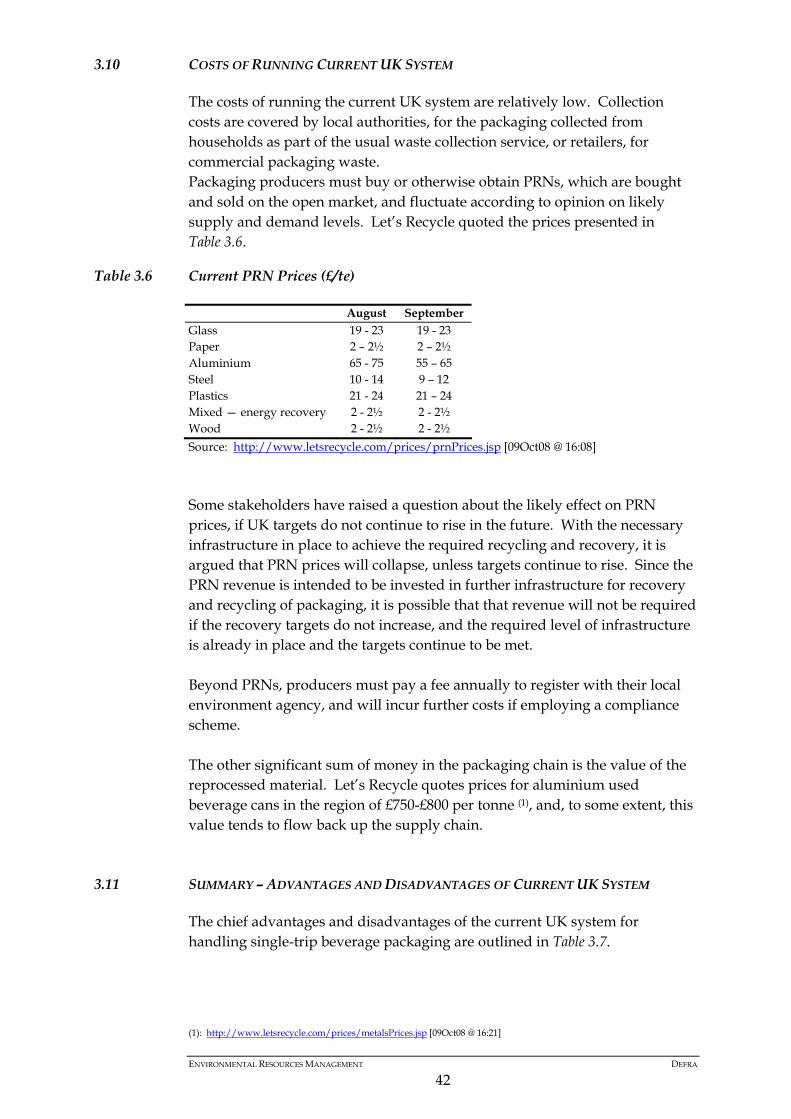

3.1 INTRODUCTION 24 3.2 TYPES OF BEVERAGE PACKAGING IN THE UK 24 3.3 THE UK BEVERAGE SECTOR 25 3.4 SINGLE USE BEVERAGE CONTAINERS IN WASTE 27 3.5 THE UK PACKAGING SUPPLY CHAIN 30 3.6 RELEVANT LEGISLATIVE AND NATIONAL TARGETS 30 3.7 THE UK’S PACKAGING WASTE RECYCLING PERFORMANCE 36 3.8 VOLUNTARY SCHEMES IN THE UK 37 3.9 SCOTTISH PROPOSALS FOR A DEPOSIT SYSTEM 41 3.10 COSTS OF RUNNING CURRENT UK SYSTEM 42 3.11 SUMMARY – ADVANTAGES AND DISADVANTAGES OF CURRENT UK SYSTEM 42

4 HOW DEPOSIT SYSTEMS COULD WORK IN THE UK 45

4.1 SCOPE OF A POTENTIAL SYSTEM 45

4.2 HOW THE SYSTEM MIGHT WORK 49 4.3 IMPACT ON THE UK’S CURRENT PACKAGING WASTE SYSTEM 51 4.4 POSSIBLE ECONOMIC COSTS OF A DEPOSIT SYSTEM 55 4.5 LEGAL CONSIDERATIONS 55 4.6 ALTERNATIVE OPTIONS FOR INCREASING RECYCLING RATES 57

5 CONCLUSIONS AND RECOMMENDATIONS 63

5.1 ALTERNATIVE SUGGESTIONS TO ACHIEVE INCREASED RECYCLING 65 5.2 SUMMARY 67

ANNEXES

ANNEX A REVIEW OF MEMBER STATE EXPERIENCE

A1 DENMARK A2 GERMANY A3 SWEDEN A4 NETHERLANDS

ANNEX B LIST OF CONTRIBUTING STAKEHOLDER ORGANISATIONS

ENVIRONMENTAL RESOURCES MANAGEMENT DEFRA

I

EXECUTIVE SUMMARY

Defra commissioned a report on deposit schemes in 2004, and its basic findings suggested that a deposit system would be problematic. However, there has recently been renewed interest in the possible use of deposit systems and the use of reverse vending as a collection method for beverage containers. In this report, again commissioned by Defra, Environmental Resources Management Limited (ERM) looks at features of packaging deposit systems and the role they might play in increasing recovery and recycling of single-use drink containers (plastic, aluminium and glass) in the UK. ERM’s method for this study involved extensive consultation with industry stakeholders in the UK, as well as reviewing deposit systems in four other EU Member States. Detailed tables reporting how those countries’ systems work are provided in Annex A, and a list of all stakeholders in provided in Annex B.

How Beverage Deposit Systems Work

Chapter 2 provides a description of the typical features of beverage deposit systems, based upon the findings from the review of circumstances in other EU Member States. The basic principle of deposit systems on beverage packaging is that supermarkets, kiosks, etc, on purchasing beverage products from a bottler or importer, pay an additional fee on the packaging in the form of a deposit. The fee is generally determined by the packaging material and the container size, and is indicated via a label on the packaging. On purchasing the beverage product in store, the consumer will pay the additional fee to the retailer and the fee is then reimbursed when the consumer returns the empty packaging. This encourages a high return rate and allows beverage packaging to be collected and returned for reuse or recycling. The chapter goes on to consider the range of decisions governing the deposit system that need to be made. These include deciding which materials and packs are covered, how labelling will be handled, how security can be assured and fraud prevented, how to deal with potential cross border issues, the value of the deposits and fees, and the role of the clearing house. Some general learnings from the other EU Member States are presented in Box 1.

The Current UK System

Chapter 3 describes the current UK system, in terms of the beverage packaging market, and arrangements for collecting and recycling single-use beverage containers. The UK Packaging Regulations place obligations on parties throughout the packaging production chain, starting with the manufacturers of the packaging materials, through to the pack/fillers and retailers. In addition, importers are made responsible for the packaging they bring into the country.

ENVIRONMENTAL RESOURCES MANAGEMENT DEFRA

II

Box 1 Some General Learnings from European Deposit Systems

• Implementation All national systems reviewed are mandatory rather than voluntary.

• Wide Ranging The deposit schemes in other EU Member States typically involve many parties along the packaging supply chain:

- producers/importers

- retailers

- consumers

- logistics/waste management companies

- centralised body

- monitoring/enforcement body

• Products None of the reviewed deposit schemes has milk in their scope.

• Collection Split between retailers and RVMs. Typically, split is initially 80:20, but reverses to 20:80 over a number of years, as RVMs are rolled out.

• Deposit Value Details vary, but the typical range of deposit values is 10p-30p.

• Container Return Rates The other EU Member States (that report figures) are seeing return rates of >80%.

• Labelling As the schemes are all mandatory, a labelling system is used to indicate on which containers a deposit is due. National barcodes reduce the chances of cross-border issues.

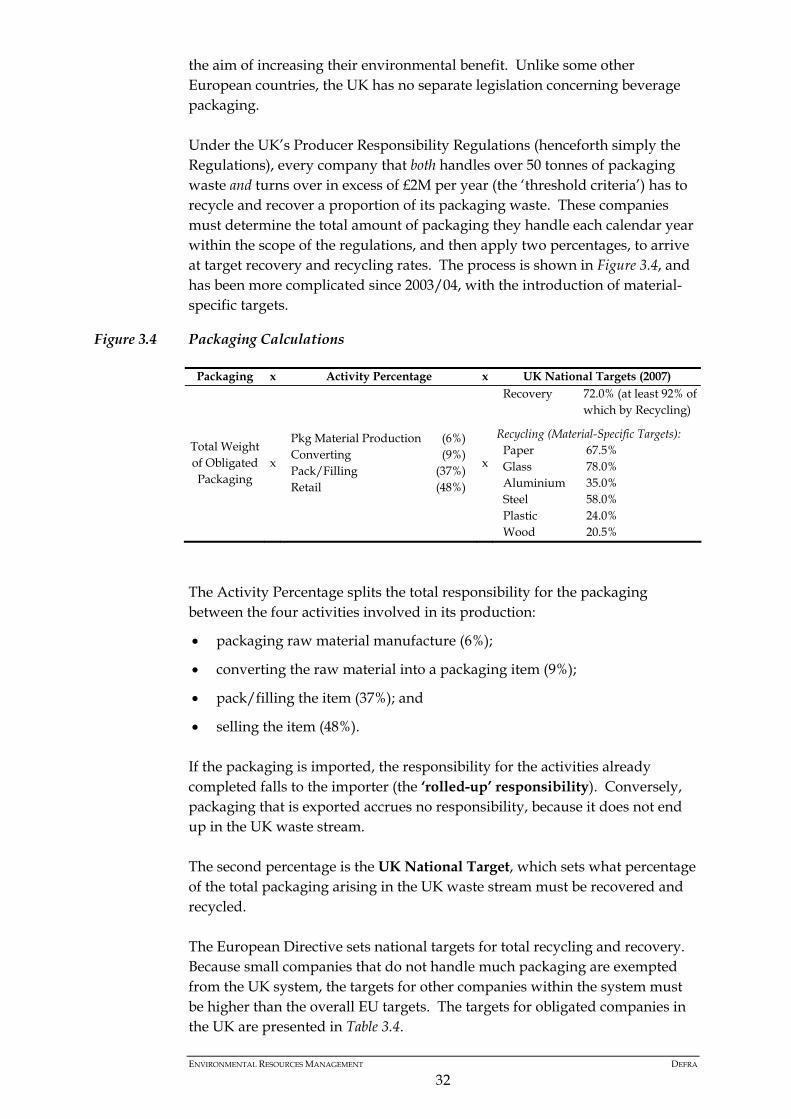

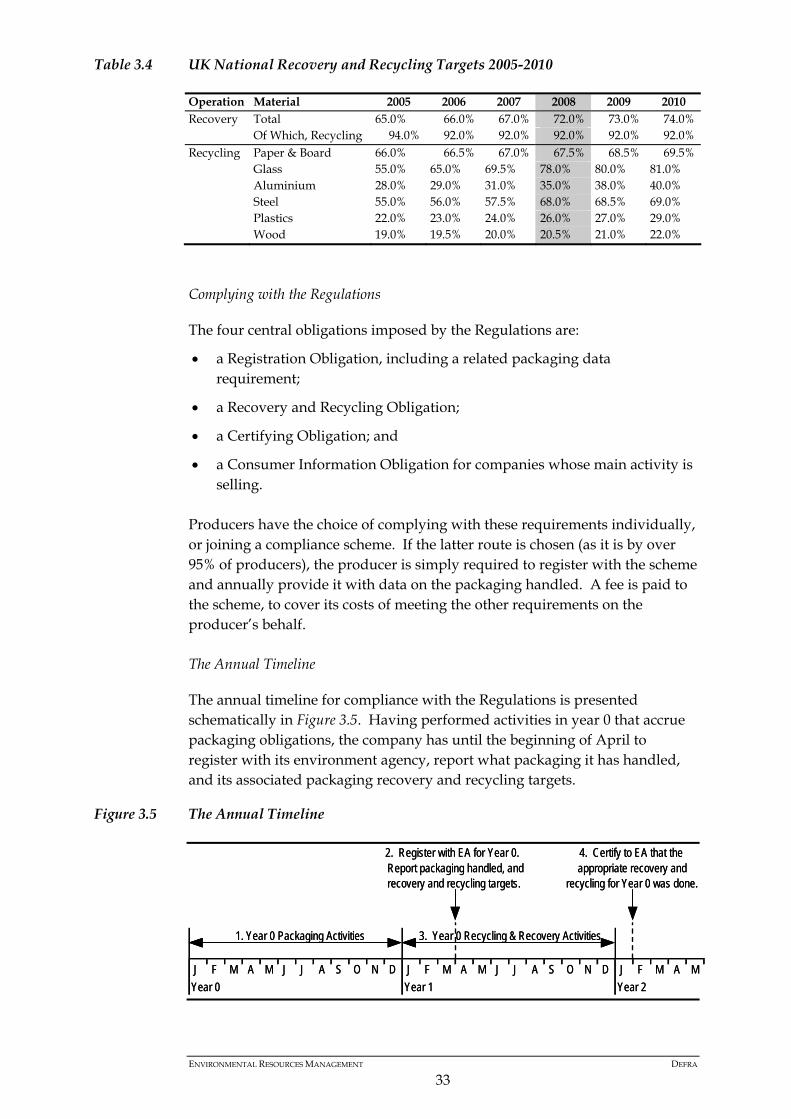

Each obligated company must acquire evidence (in the form of packaging recovery notes, PRNs) over the course of the year that their packaging recycling and recovery obligations have been fulfilled. PRNs are traded on an open market like shares, and are subject to the same rises and falls in value, depending on supply and demand. The revenue from PRNs is meant to be reinvested into the reprocessing industry, to fund the commissioning of further equipment, so that increasing targets can be met. If PRN targets fail to increase, many stakeholders believe their price will collapse. The majority of packaging waste from households is collected by local authorities as part of their regular collection rounds, either as source-separated dry recyclables or mixed up with the residual waste. The council arranges for the bulking of the recyclable materials, where possible, and onward supply to reprocessing companies. The current UK system is relatively efficient at collecting and recycling beverage packaging waste, inasmuch as it is handled together with other similar packaging and non-packaging (notably newspapers and magazines) recyclable waste. There are two distinct challenges that persist for the UK recycling infrastructure. The first is to increase the coverage (in terms of both geography and materials accepted) of the source-separated kerbside collections, so that all residents have the same opportunities to divert their waste from landfill. The second is to find a way to encourage all those who have the infrastructure to make full use of it. The UK has seen significant growth in the collection and recycling of packaging waste since the introduction of the Regulations in 1998. However, performance on the overall recovery rate continues to lag behind other EU

ENVIRONMENTAL RESOURCES MANAGEMENT DEFRA

III

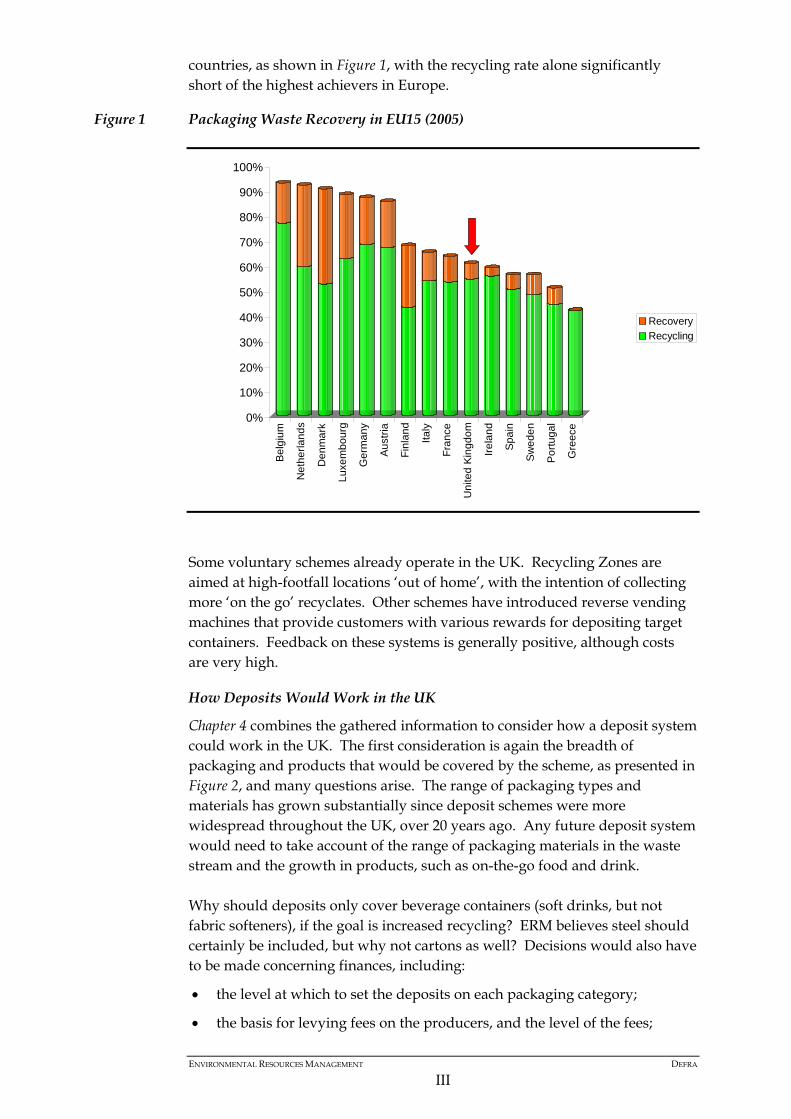

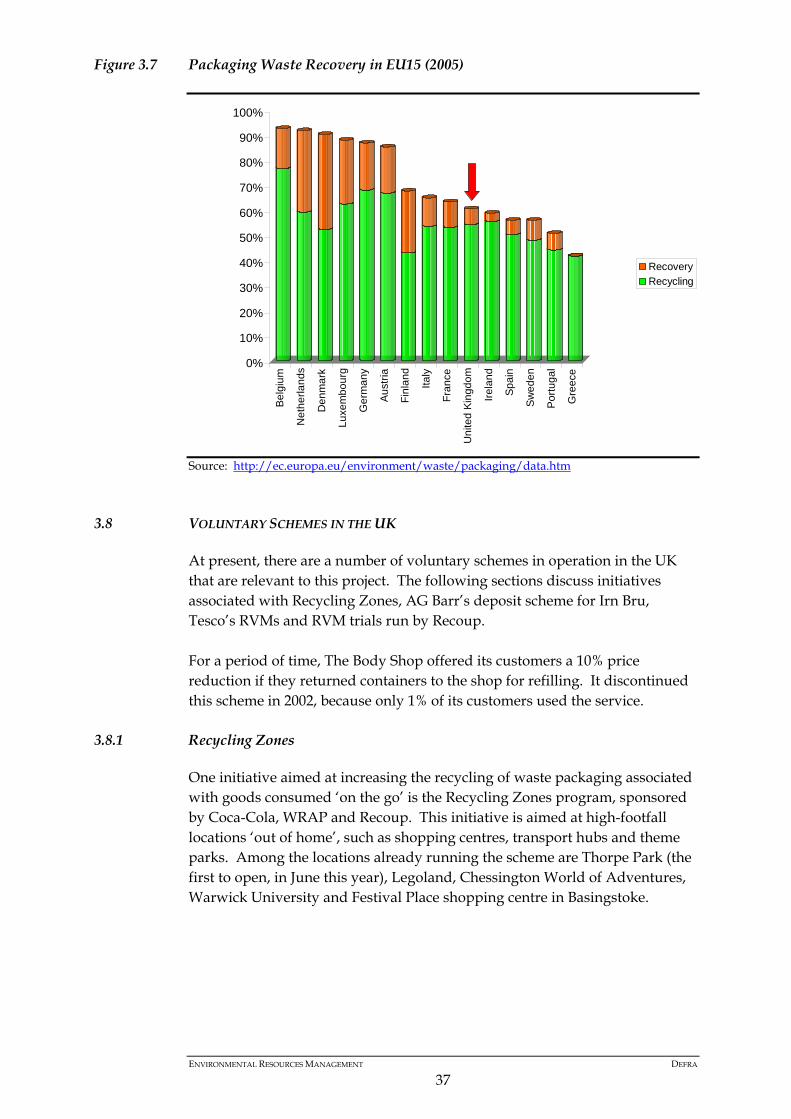

countries, as shown in Figure 1, with the recycling rate alone significantly short of the highest achievers in Europe.

Figure 1 Packaging Waste Recovery in EU15 (2005)

Some voluntary schemes already operate in the UK. Recycling Zones are aimed at high-footfall locations ‘out of home’, with the intention of collecting more ‘on the go’ recyclates. Other schemes have introduced reverse vending machines that provide customers with various rewards for depositing target containers. Feedback on these systems is generally positive, although costs are very high.

How Deposits Would Work in the UK

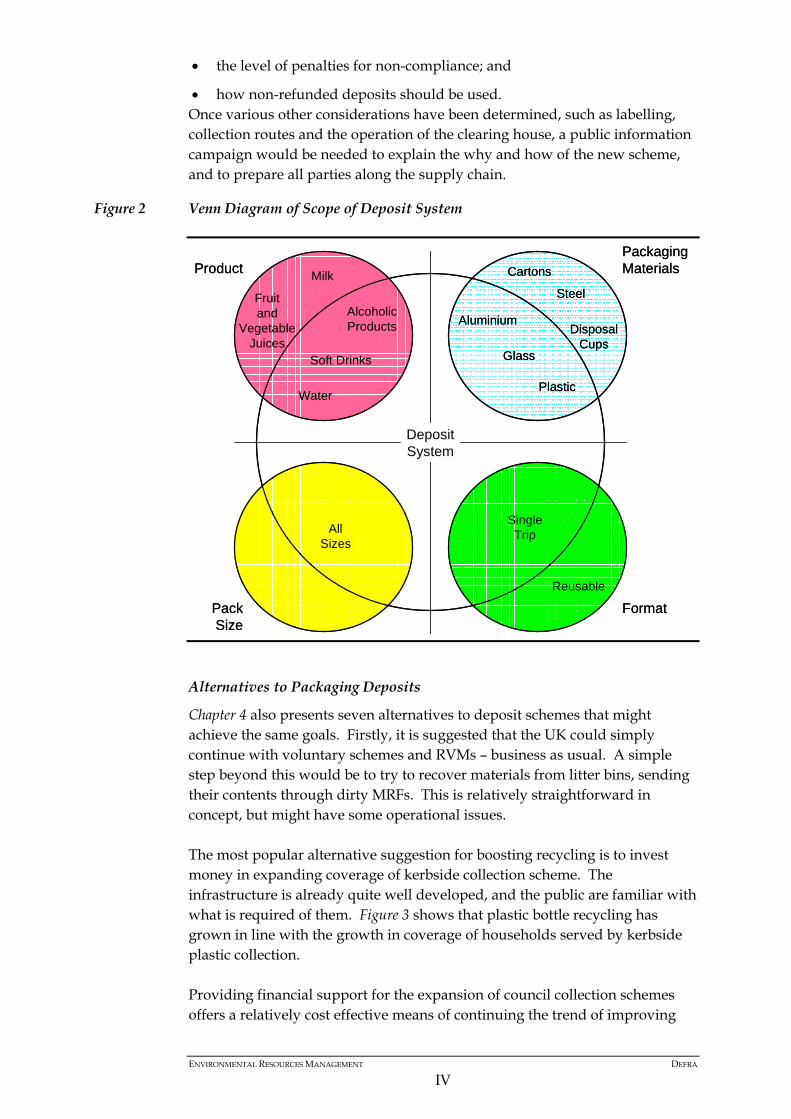

Chapter 4 combines the gathered information to consider how a deposit system could work in the UK. The first consideration is again the breadth of packaging and products that would be covered by the scheme, as presented in Figure 2, and many questions arise. The range of packaging types and materials has grown substantially since deposit schemes were more widespread throughout the UK, over 20 years ago. Any future deposit system would need to take account of the range of packaging materials in the waste stream and the growth in products, such as on-the-go food and drink. Why should deposits only cover beverage containers (soft drinks, but not fabric softeners), if the goal is increased recycling? ERM believes steel should certainly be included, but why not cartons as well? Decisions would also have to be made concerning finances, including:

• the level at which to set the deposits on each packaging category;

• the basis for levying fees on the producers, and the level of the fees;

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Belg

ium

Net

herla

nds

Den

mar

k

Luxe

mbo

urg

Ger

man

y

Aust

ria

Finl

and

Italy

Fran

ce

Uni

ted

King

dom

Irela

nd

Spai

n

Swed

en

Portu

gal

Gre

ece

RecoveryRecycling

ENVIRONMENTAL RESOURCES MANAGEMENT DEFRA

IV

• the level of penalties for non-compliance; and

• how non-refunded deposits should be used. Once various other considerations have been determined, such as labelling, collection routes and the operation of the clearing house, a public information campaign would be needed to explain the why and how of the new scheme, and to prepare all parties along the supply chain.

Figure 2 Venn Diagram of Scope of Deposit System

Alternatives to Packaging Deposits

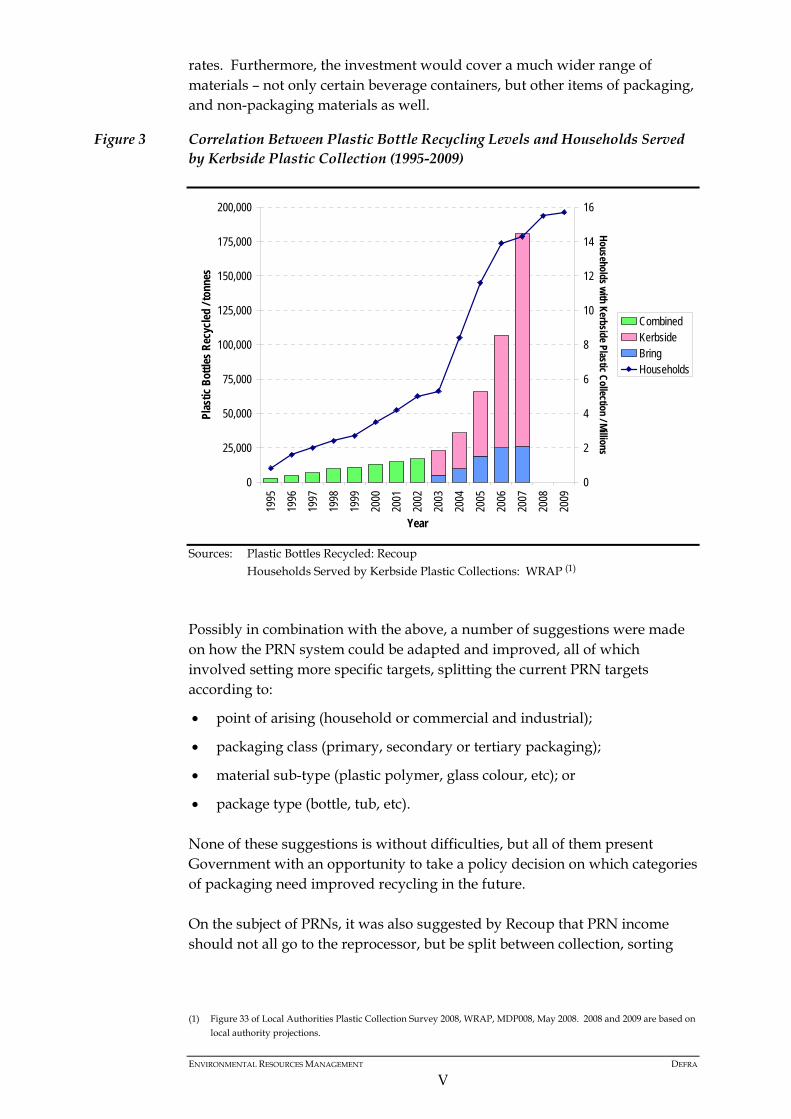

Chapter 4 also presents seven alternatives to deposit schemes that might achieve the same goals. Firstly, it is suggested that the UK could simply continue with voluntary schemes and RVMs – business as usual. A simple step beyond this would be to try to recover materials from litter bins, sending their contents through dirty MRFs. This is relatively straightforward in concept, but might have some operational issues. The most popular alternative suggestion for boosting recycling is to invest money in expanding coverage of kerbside collection scheme. The infrastructure is already quite well developed, and the public are familiar with what is required of them. Figure 3 shows that plastic bottle recycling has grown in line with the growth in coverage of households served by kerbside plastic collection. Providing financial support for the expansion of council collection schemes offers a relatively cost effective means of continuing the trend of improving

PackagingMaterials

Format

Product

PackSize

Cartons

Steel

Aluminium

Glass

DisposalCups

Plastic

SingleTrip

Reusable

AllSizes

AlcoholicProducts

Soft Drinks

Water

Milk

Fruitand

VegetableJuices

DepositSystem

PackagingMaterials

Format

Product

PackSize

Cartons

Steel

Aluminium

Glass

DisposalCups

Plastic

SingleTrip

Reusable

AllSizes

AlcoholicProducts

Soft Drinks

Water

Milk

Fruitand

VegetableJuices

DepositSystem

ENVIRONMENTAL RESOURCES MANAGEMENT DEFRA

V

rates. Furthermore, the investment would cover a much wider range of materials – not only certain beverage containers, but other items of packaging, and non-packaging materials as well.

Figure 3 Correlation Between Plastic Bottle Recycling Levels and Households Served by Kerbside Plastic Collection (1995-2009)

Sources: Plastic Bottles Recycled: Recoup Households Served by Kerbside Plastic Collections: WRAP (1)

Possibly in combination with the above, a number of suggestions were made on how the PRN system could be adapted and improved, all of which involved setting more specific targets, splitting the current PRN targets according to:

• point of arising (household or commercial and industrial);

• packaging class (primary, secondary or tertiary packaging);

• material sub-type (plastic polymer, glass colour, etc); or

• package type (bottle, tub, etc). None of these suggestions is without difficulties, but all of them present Government with an opportunity to take a policy decision on which categories of packaging need improved recycling in the future. On the subject of PRNs, it was also suggested by Recoup that PRN income should not all go to the reprocessor, but be split between collection, sorting

(1) Figure 33 of Local Authorities Plastic Collection Survey 2008, WRAP, MDP008, May 2008. 2008 and 2009 are based on

local authority projections.

0

25,000

50,000

75,000

100,000

125,000

150,000

175,000

200,000

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

Year

Plas

tic B

ottle

s Rec

ycled

/ ton

nes

0

2

4

6

8

10

12

14

16

Households with Kerbside Plastic Collection / Millions

CombinedKerbsideBringHouseholds

ENVIRONMENTAL RESOURCES MANAGEMENT DEFRA

VI

and reprocessing, since, for plastics in particular, it is not the reprocessing capacity that is the bottle neck, but collection and sorting. The most radical alternative raised by stakeholders involved changing the metric by which the targets are set from weight, which is obvious and easy to measure, to carbon, which is arguably a much better indicator of environmental impact. The reasons behind this change are relatively clear, but the general opinion is that the science is not yet well enough developed.

Conclusions

In Chapter 5, ERM provides our conclusions. Defra originally presented a series of key questions that the study should address, and the results are as follows:

Would a deposit system lead to increased collection and/or improve the quality of the materials collected?

Yes. The general consensus is that a deposit system would increase the total tonnages of materials collected, although a significant amount of the deposited packaging would be cannibalised from existing collection schemes. However, a deposit scheme may also capture some of the hard to reach materials – particularly ‘on the go’ food and drink packaging. There was less agreement about whether or not there would be a concurrent improvement in the quality of materials collected.

What role might reverse-vending play in a deposit scheme or as an alternative? Could reverse vending alone provide a similar or better outcome?

Reverse Vending Machines (RVMs) would play an important role in any deposit scheme, freeing retailers, to some extent, from the burdens of redeeming deposits. RVM trials in the UK have proved popular with the public, and RVMs in shopping areas could divert recyclates from waste bins. Whether RVMs would reduce littering is disputed.

What would be the likely effect on local authority collections/existing collection mechanisms?

There was widespread agreement that the introduction of deposits would have a detrimental effect on existing collection mechanisms in general, and council kerbside collections in particular. Deposits on only a proportion of packaging materials may add to the householder confusion over the varying scope of local authority services, which has been widely reported by stakeholders, and this may be a disincentive to participation. The deposit scheme would divert a significant amount of packaging waste from the kerbside schemes, and that may have a knock-on effect on other materials currently collected at kerbside.

What are the pre-conditions for success of a deposit scheme? Box 2.2 provides details on some of the things that need to be in place before a deposit scheme can be launched. In brief: the centralised body would need to have been established; all the producers and importers must have registered and labelled their products, and paid the associated fees; the retailers must have some form of collection system in place;

ENVIRONMENTAL RESOURCES MANAGEMENT DEFRA

VII

hauliers and reprocessors must be set to receive the returned packaging through the new channels; and consumers must be informed about the new system.

What are the likely costs (including administrative and operational costs)? Are there likely to be less costly alternatives to increasing recycling?

Although this question was included in the brief, it was also recognised by Defra that an economic study of deposits was outside the terms of reference. To give one general ballpark assessment of costs, the German deposit scheme acknowledged that compulsory deposits cost around three times as much per container as household-based collection systems.

What information is there on industry evidence on deposit schemes? To ERM’s knowledge, there are no deposit schemes in the UK currently handling single-trip packaging, with the exception of voluntary schemes run at events such as music festivals. Tesco reports that their voluntary RVMs, awarding loyalty points for returned packaging, have been well received by customers, but are very expensive.

What information - if any - is there on the effects of deposits schemes on littering? ERM has found little hard evidence that deposit schemes reduce littering. One exception is a recent nature clean-up lead by the Danish Society for Nature Conservation, which collected 154 389 cans, of which only 7989 (5%) were deposit-bearing cans. The rest were foreign cans that were not part of the Danish scheme.

Would certain drinks categories, producers or packaging systems be discriminated against or favoured by a deposit scheme?

Possibly to some extent. General stakeholder opinion was that, unless the deposit scheme is introduced uniformly over all packaging systems, manufacturers might change their choice of packaging to get around the rules. However, experience from other European countries is that this has rarely occurred. Opinion was that consumer preferences had a significantly higher influence on packaging material choice than whether the material was part of a deposit scheme or not.

Would this have any effect on the market for containers which can be refilled (or the likelihood of such a market taking off)?

ERM has found no evidence that introducing deposits for single-trip containers might increase the market for refillable containers. On the contrary, evidence from the other European countries shows that the use of refillable beverage packaging is in decline, for other reasons.

Are the conclusions on benefits and disadvantages different for each material? Might deposit schemes encourage packaging producers to substitute one material for another?

ERM considers that the benefits and disadvantages of a deposit scheme are the same for each material. However, as noted above, unless the scheme is introduced uniformly across all materials, some market distortion is likely.

ENVIRONMENTAL RESOURCES MANAGEMENT DEFRA

VIII

ERM would make the following closing comments on the study.

• It is not disputed that a deposit scheme would increase recycling, but alternative schemes could achieve the same or better results at a lower cost.

• Deposits could be seen to impose an additional cost to householders who are not easily able to participate.

• It is likely that the majority of materials collected through a deposit scheme would be diverted from the existing household collection schemes, rather than being new material that is not currently collected.

• Deposits would require the development of a new tranche of infrastructure to collect and store the packaging at retailers, while reducing the usage of the existing kerbside collection infrastructure.

• Deposits may make a contribution to reducing litter, but, for ‘on the go’ packaging, it is thought that the major impact would be to divert packaging from waste bins to recycling bins.

• A deposit scheme would have to be carefully designed, in order not to fall foul of legal requirements to be proportionate and non-discriminatory, and in order not to encourage producers to change their choice of packaging material.

If Defra decided against introducing a deposit scheme, there are alternatives that might achieve the same goal of increasing recycling and recovery of packaging waste. ERM makes two specific suggestions on this matter:

• Further funds could be invested in kerbside collection infrastructure. Households are increasingly familiar with these schemes, and much of the infrastructure required is already in place.

• Those funds could be provided, at least in part, by changes to the PRN system. Of the suggestions listed, splitting targets according to primary, secondary and tertiary packaging might be the least problematic.

Finally, voluntary schemes at large events have proved highly effective in combating littering of the cups on which deposits had been placed, and could be further encouraged. ERM December 2008

ENVIRONMENTAL RESOURCES MANAGEMENT DEFRA

1

1 INTRODUCTION

Environmental Resources Management Limited (ERM) was commissioned by Defra to carry out a desk-based study on deposit schemes and reverse vending machines for single-use beverage containers. This report looks at the features of packaging deposit systems and the role that they might play in increasing recovery and recycling of single-use drink containers (plastic, aluminium and glass) in the UK.

1.1 BACKGROUND TO THE PROJECT

Defra commissioned a report on deposit schemes in 2004. Its basic findings suggested that a deposit system would be problematic. However, there has been renewed interest in the possible use of deposit systems and the use of reverse vending as a collection method for beverage containers. In particular, the Campaign to Protect Rural England (CPRE) supports the introduction of a deposit system as a means to reduce litter. CPRE has recently launched a campaign with this aim in mind. At the same time, it is thought that a deposit system on one-way drinks packaging could improve the separate collection of the containers, making the waste material more attractive to recyclers and reprocessors. Reprocessors have voiced their concerns about the levels of material contamination in local authority kerbside-collected recyclables and reverse vending machines could help to address this problem.

1.2 OBJECTIVES OF THIS PROJECT

With this background in mind, this project aims to consider how a deposit system and reverse vending machines could work to increase the recycling and recovery of single use beverage containers (plastic, aluminium and glass). It also considers the impact such a system would have on litter arisings. The original scope of the project did not include:

• an evaluation of the use of deposits for returnable/refillable containers;

• single use beverage containers manufactured from materials other than plastic, aluminium and glass (eg cartons); or

• a detailed cost comparison of different options for increasing the collection and recycling of single use beverage containers.

However, in carrying out the work, these issues have arisen, and been addressed to a certain extent. They are commented upon where appropriate.

ENVIRONMENTAL RESOURCES MANAGEMENT DEFRA

2

An overall aim of the project was to address the key questions shown in Box 1.1 as posed by Defra’s project team.

Box 1.1 Key Questions to be Addressed in this Study

1.3 ERM’S APPROACH

In evaluating packaging deposit schemes and their possible introduction in the UK, ERM has consulted with a number of key stakeholders, including representatives of the:

• packaging manufacturing sector, including the Packaging Federation, Alupro, British Glass and Nampak;

• government organisations, including BERR, the Advisory Committee on Packaging (ACP) and the Environment Agency;

• the Waste & Resources Action Programme (WRAP);

• Non-Governmental Organisations (NGOs), including the Campaign for the Protection for Rural England (CPRE) and Friends of the Earth (FoE);

• packaging recycling or environmental organisations, including Incpen, Valpak, Recoup and Novelis;

• the Local Authority Recycling Advisory Committee (LARAC); and

• retail and beverage supply sector, including Tesco, M&S, the Association of Convenience Stores (ACS), the British Soft Drinks Association (BSDA) and the British Beer and Pub Association (BBPA).

• Would a deposit system lead to increased collection and/or improve the quality of the materials collected?

• What role might reverse-vending play in a deposit scheme or as an alternative? Could reverse vending alone provide a similar or better outcome?

• What would be the likely effect on local authority collections/existing collection mechanisms?

• What are the pre-conditions for success of a deposit scheme?

• What are the likely costs (including administrative and operational costs)? Are there likely to be less costly alternatives to increasing recycling?

• What information is there on industry evidence on deposit schemes?

• What information - if any - is there on the effects of deposits schemes on littering?

• Would certain drinks categories, producers or packaging systems be discriminated against or favoured by a deposit scheme?

• Would this have any effect on the market for containers which can be refilled (or the likelihood of such a market taking off)?

• Are the conclusions on benefits and disadvantages different for each material? Might deposit schemes encourage packaging producers to substitute one material for another?

ENVIRONMENTAL RESOURCES MANAGEMENT DEFRA

3

We have also reviewed the existing packaging deposit systems in Germany, the Netherlands, Sweden and Denmark. A full list of stakeholders consulted in provided in Annex B.

1.4 STRUCTURE OF THIS REPORT

This report contains the following chapters:

Chapter 2 provides a description of typical features of deposit systems;

Chapter 3 provides a description of the features of the UK’s existing systems for collecting and recycling single-use beverage containers;

Chapter 4 provides an assessment of how deposit systems could work in the UK;

Chapter 5 provides our conclusions in relation to the key questions in Box 1.1 This report also containers two annexes:

Annex A Country reports for Denmark, Germany, the Netherlands and Sweden.

Annex B List of Stakeholders Consulted.

ENVIRONMENTAL RESOURCES MANAGEMENT DEFRA

4

2 FEATURES OF BEVERAGE CONTAINER DEPOSIT SYSTEMS

2.1 INTRODUCTION

This section outlines the features of a deposit system, to allow comparison with the UK’s existing system for collecting and recycling single use beverage containers, reviewed in Chapter 3. In order to understand the features of packaging deposit systems, ERM has reviewed existing systems in Denmark, Germany, Sweden and the Netherlands. Additional information has been obtained through discussions with key stakeholders. The basic principle of deposit systems on beverage packaging is that supermarkets, kiosks, etc, on purchasing beverage products from a bottler or importer, pay an additional fee on the packaging in the form of a deposit. The fee is generally determined by the packaging material and the container size, and is indicated via a label on the packaging. On purchasing the beverage product in store, the consumer will pay the additional fee to the retailer and the fee is then reimbursed when the consumer returns the empty packaging. This encourages a high return rate and allows beverage packaging to be collected and returned for reuse or recycling. In developing a deposit system, a number of issues have to be considered and a range of decisions governing the system need to be made. The following sections address these issues. Section 2.2 Typical Scope of a Beverage Deposit System

Section 2.3 Parties Involved in Deposit Systems

Section 2.4 Mandatory versus Voluntary Deposit Systems

Section 2.5 Labelling Containers

Section 2.6 Typical Beverage Container Collection Mechanisms

Section 2.7 Sorting, Bulking and Recycling/Recovering of Containers

Section 2.8 Assuring Security and Preventing Fraud

Section 2.9 Potential Health and Safety Implications of Deposit Systems

Section 2.10 Potential Cross Boundary Issues and Single Market Implications

Section 2.11 Costs and Income Streams

Section 2.12 Value of the Deposit

Section 2.13 Typical Container Return Rates in Deposit Systems

Section 2.14 Impacts of Deposit Schemes

Section 2.15 The Role of Reverse Vending Machines

Section 2.16 The Role of the Clearing House

Section 2.17 Summary – Advantages and Disadvantages of Deposits Systems

ENVIRONMENTAL RESOURCES MANAGEMENT DEFRA

5

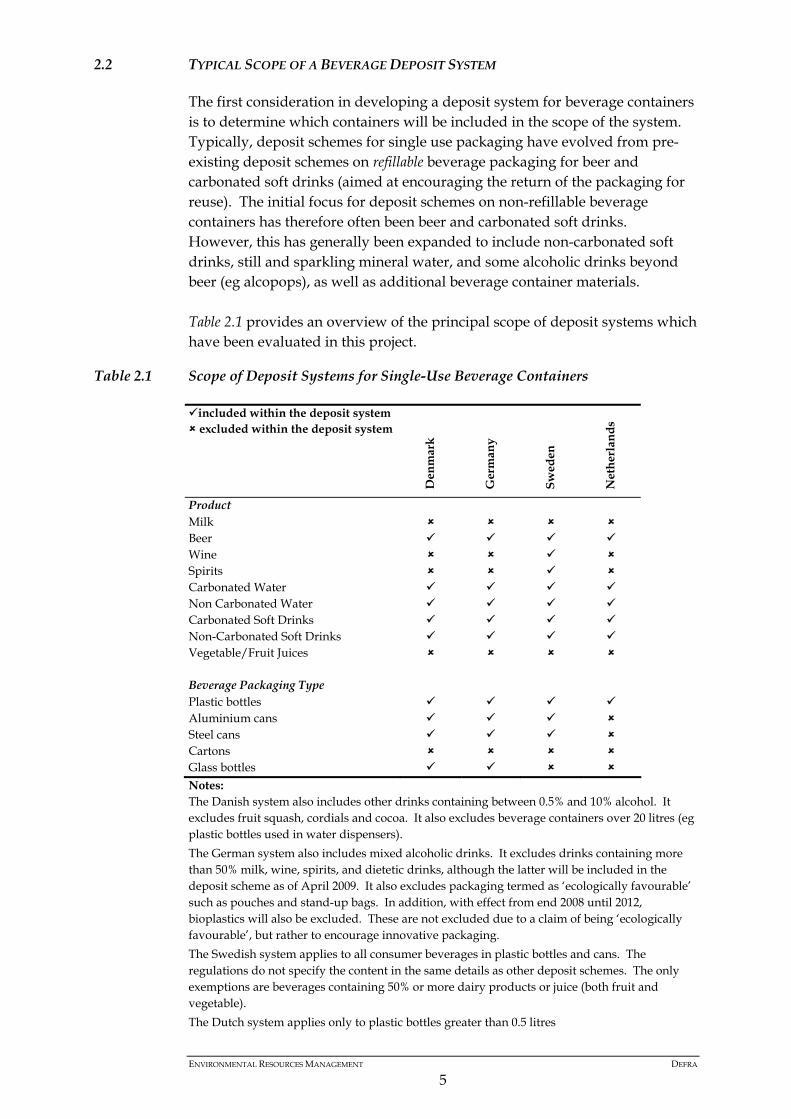

2.2 TYPICAL SCOPE OF A BEVERAGE DEPOSIT SYSTEM

The first consideration in developing a deposit system for beverage containers is to determine which containers will be included in the scope of the system. Typically, deposit schemes for single use packaging have evolved from pre-existing deposit schemes on refillable beverage packaging for beer and carbonated soft drinks (aimed at encouraging the return of the packaging for reuse). The initial focus for deposit schemes on non-refillable beverage containers has therefore often been beer and carbonated soft drinks. However, this has generally been expanded to include non-carbonated soft drinks, still and sparkling mineral water, and some alcoholic drinks beyond beer (eg alcopops), as well as additional beverage container materials. Table 2.1 provides an overview of the principal scope of deposit systems which have been evaluated in this project.

Table 2.1 Scope of Deposit Systems for Single-Use Beverage Containers

included within the deposit system excluded within the deposit system

Den

mar

k

Ger

man

y

Swed

en

Net

herl

ands

Product Milk Beer Wine Spirits Carbonated Water Non Carbonated Water Carbonated Soft Drinks Non-Carbonated Soft Drinks Vegetable/Fruit Juices Beverage Packaging Type Plastic bottles Aluminium cans Steel cans Cartons Glass bottles Notes: The Danish system also includes other drinks containing between 0.5% and 10% alcohol. It excludes fruit squash, cordials and cocoa. It also excludes beverage containers over 20 litres (eg plastic bottles used in water dispensers). The German system also includes mixed alcoholic drinks. It excludes drinks containing more than 50% milk, wine, spirits, and dietetic drinks, although the latter will be included in the deposit scheme as of April 2009. It also excludes packaging termed as ‘ecologically favourable’ such as pouches and stand-up bags. In addition, with effect from end 2008 until 2012, bioplastics will also be excluded. These are not excluded due to a claim of being ‘ecologically favourable’, but rather to encourage innovative packaging. The Swedish system applies to all consumer beverages in plastic bottles and cans. The regulations do not specify the content in the same details as other deposit schemes. The only exemptions are beverages containing 50% or more dairy products or juice (both fruit and vegetable). The Dutch system applies only to plastic bottles greater than 0.5 litres

ENVIRONMENTAL RESOURCES MANAGEMENT DEFRA

6

With regard to the scope of the packaging deposit systems in these countries, the main points are summarised below.

• None of the single-use deposit systems apply to milk (although there are still some non-deposit return schemes for reusable milk bottles in the UK). The main reason for excluding milk is that returned milk containers pose particular health and safety concerns. Other reasons for the exclusion of milk containers appear to be: - milk is considered to be a staple food in many countries, and

increasing the sale price of milk by applying a deposit is not considered acceptable;

- milk is not generally sold as a beverage to be consumed ‘on the go’, and milk containers are not generally littered; and

- in some countries, milk is generally sold in cartons which, due to their shape, pose specific problems in current reverse vending machines.

Similar arguments apply to vegetable or fruit juices.

• The scope of the current deposit system in Germany is based primarily on ‘ecologically unfavourable’ non-refillable containers. The term ‘ecologically unfavourable’ was defined in a life cycle assessment study commissioned by the Federal Environment Agency.

The legal framework for the current German deposit system was initially defined in 2003, but the system faced a number of legal difficulties and industry challenges, and changes were introduced in 2005 in response to rulings from the European Court of Justice. One impact of these was the removal of the legal basis for the individual solutions (also known as ‘island solutions’) where retailers took back only the containers sold in store, by specifying particular bottle shapes. Retailers operating these independent solutions avoided the cost of participating in clearing systems. An unfortunate consequence of this approach was that these retailers often stopped selling cans due to their generic shape.

• Single-use glass bottles account for a very small volume of the beverages sold in Sweden (~ 0.5%). As a consequence, the Swedish deposit system has not been expanded to include single-use glass packaging. However, deposits do apply to returnable glass bottles, which have a significant market share especially for beer.

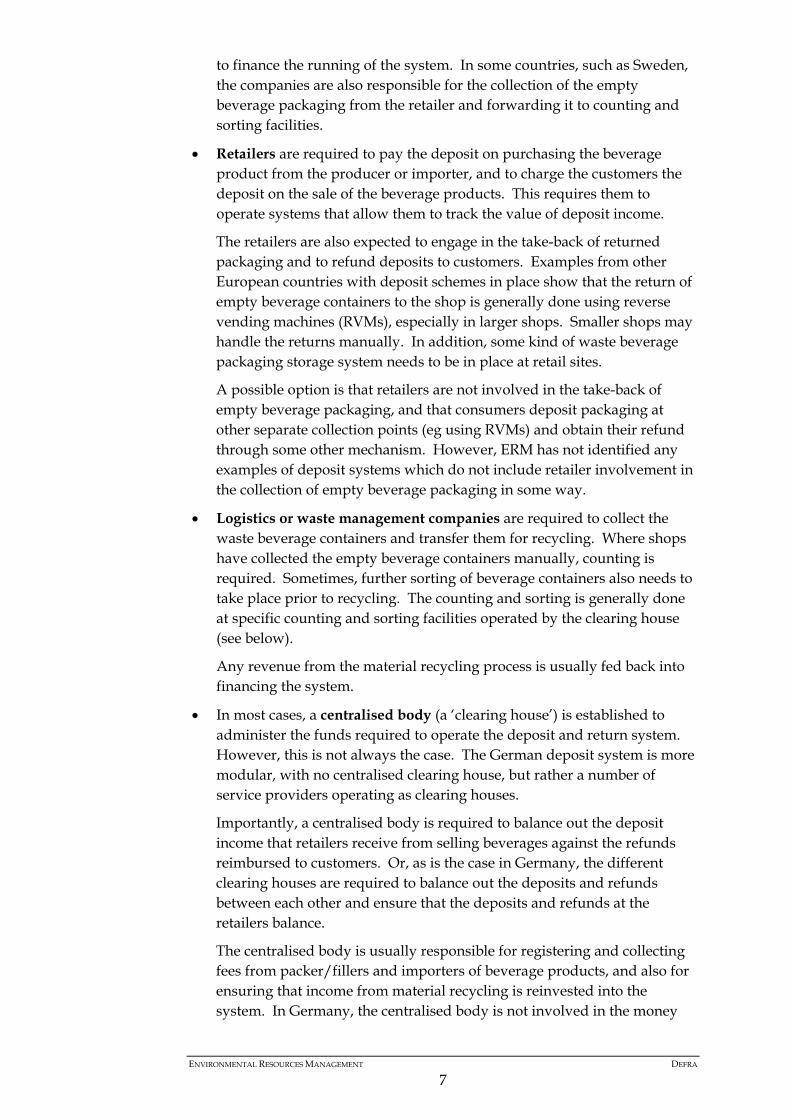

2.3 PARTIES INVOLVED IN DEPOSIT SYSTEMS

Although the most visible parties in a packaging deposit system are retailers and consumers, a range of players have to be involved to ensure a deposit system works effectively. The exact roles of these players need to be clearly defined and agreed. The typical roles are summarised below.

• Companies which bottle beverage products and companies which import packaged products have to ensure that a deposit is applied to their products and that the beverage packaging is appropriately labelled. These companies are required to register and pay into a centralised fund

ENVIRONMENTAL RESOURCES MANAGEMENT DEFRA

7

to finance the running of the system. In some countries, such as Sweden, the companies are also responsible for the collection of the empty beverage packaging from the retailer and forwarding it to counting and sorting facilities.

• Retailers are required to pay the deposit on purchasing the beverage product from the producer or importer, and to charge the customers the deposit on the sale of the beverage products. This requires them to operate systems that allow them to track the value of deposit income.

The retailers are also expected to engage in the take-back of returned packaging and to refund deposits to customers. Examples from other European countries with deposit schemes in place show that the return of empty beverage containers to the shop is generally done using reverse vending machines (RVMs), especially in larger shops. Smaller shops may handle the returns manually. In addition, some kind of waste beverage packaging storage system needs to be in place at retail sites.

A possible option is that retailers are not involved in the take-back of empty beverage packaging, and that consumers deposit packaging at other separate collection points (eg using RVMs) and obtain their refund through some other mechanism. However, ERM has not identified any examples of deposit systems which do not include retailer involvement in the collection of empty beverage packaging in some way.

• Logistics or waste management companies are required to collect the waste beverage containers and transfer them for recycling. Where shops have collected the empty beverage containers manually, counting is required. Sometimes, further sorting of beverage containers also needs to take place prior to recycling. The counting and sorting is generally done at specific counting and sorting facilities operated by the clearing house (see below).

Any revenue from the material recycling process is usually fed back into financing the system.

• In most cases, a centralised body (a ‘clearing house’) is established to administer the funds required to operate the deposit and return system. However, this is not always the case. The German deposit system is more modular, with no centralised clearing house, but rather a number of service providers operating as clearing houses.

Importantly, a centralised body is required to balance out the deposit income that retailers receive from selling beverages against the refunds reimbursed to customers. Or, as is the case in Germany, the different clearing houses are required to balance out the deposits and refunds between each other and ensure that the deposits and refunds at the retailers balance.

The centralised body is usually responsible for registering and collecting fees from packer/fillers and importers of beverage products, and also for ensuring that income from material recycling is reinvested into the system. In Germany, the centralised body is not involved in the money

ENVIRONMENTAL RESOURCES MANAGEMENT DEFRA

8

flows. Instead, its main responsibilities include the management of the deposit label, the provision of the master database, and the IT interface.

• Consumer involvement is key and mandatory, inasmuch as consumers are required to pay the deposit value in addition to the product purchase price, and must return the empty beverage container in order to obtain the refund. If the deposit level is too low and the consumer is not sufficiently incentivised to return the empty beverage container, the return rate will be low and the deposit system has in effect failed.

• A monitoring or enforcement body is required to ensure that the system is not subject to fraudulent behaviour or claims by any player in the deposit system. In reality, this is done by various parties, including the organisation administering the system, the ‘inland revenue’, clearing houses, etc. Also, some government department generally is in charge of monitoring/auditing the organisation administering the system.

As empty beverage containers (new and waste) are effectively assigned a financial value over and above their inherent material value (eg scrap value for aluminium can), monitoring and enforcement procedures need to be in place to prevent fraudulent claims of deposit values.

It is important that the system also protects the full range of players including: - consumers, to ensure that deposits are repaid; - retailers, to ensure that they can reclaim any deposits repaid ‘over and

above’ the value of the deposits which they have collected; and - packer/fillers, to protect those who are legitimately funding the

systems against potential free-riders who may attempt to operate outside the system.

2.4 MANDATORY VERSUS VOLUNTARY DEPOSIT SYSTEMS

A further design consideration for deposit schemes for beverage containers is whether they are operated as mandatory or voluntary systems. The European schemes reviewed by ERM are all national schemes and are all mandatory. This is principally seen to be necessary to avoid market distortion towards those who might otherwise not voluntarily participate. If two soft drinks firms are competing for business, one selling products with deposits on their packaging, and the other deposit-free, the consumer will see the cheaper price for the latter and, other things being equal, choose their product in preference.

2.5 LABELLING CONTAINERS

Mandatory packaging deposit systems require all packaging within the scope of the system to be labelled. The label is required to meet two functions, as follows.

1. To provide the consumer with information that the beverage product is part of the deposit scheme and the value of the deposit required to be paid.

ENVIRONMENTAL RESOURCES MANAGEMENT DEFRA

9

2. To verify the packaging is part of the valid deposit system. The label needs to be designed or applied in such a manner as to limit fraud.

Labels are applied, in the case of cans, during the printing of the can or, if self-adhesive labels are used, during the filling process, and, in the case of bottles, during the filling process, when the label is applied. The packer/filler or importer is required to pay a charge to the centralised body or bodies when the product enters the market, and charge the deposit to the retailer purchasing the beverage product. The label is one means of indicating that the packaging is part of the official deposit system and the appropriate charge has been paid to the centralised body. In those countries operating deposit systems (and, in particular, those relying on RVMs as a collection method), part of the labelling information is generally a bar code specific to the country of sale and the product. This helps ensure a deposit is not refunded on a container which was purchased in another country where an initial deposit has not been paid. In Denmark and Germany, there are strict guidelines and procedures for those buying and applying the labelling ink. The countries have introduced security codes using a special ink combination in order to eliminate fraud from the copying of barcodes. The ability to use the ink and labels is only afforded to those parties which have paid the necessary fees into the central system.

2.6 TYPICAL BEVERAGE CONTAINER COLLECTION MECHANISMS

The initial collection of used single-use beverage containers is linked to the refund of the deposit. As a result, the mechanisms for returning containers are generally linked to retailers who are selling beverage products. Collection of single use beverage containers usually involves either:

• reverse vending machines (RVMs); and/or

• retailers manually collecting and storing containers. RVMs accept waste beverage containers and provide a means of deposit refund (generally in the form of a refund ticket to be redeemed in store; no purchase is generally required). Their use reduces the need for manual handling of returned beverage containers, and the technology is available in a range of different styles and levels of sophistication. Because the use of RVMs has implications for this and several subsequent sections of this chapter, they are dealt with separately in Section 2.15. Even if RVMs are employed in the deposit systems, manual collection systems are typically also required, if only to offer a ‘back up’ when the RVMs are not functioning, or are not equipped to take the full range of containers covered by the system.

ENVIRONMENTAL RESOURCES MANAGEMENT DEFRA

10

For beverage containers accepted manually, retail staff need to be able to recognise deposit labels, inspect the packaging to ensure it is still intact, and refund the value of the deposit. The deposit is refunded directly at the store. The initial point of collection triggers the repayment of the deposit to the consumer. In many RVMs, in order to avoid duplicate fraudulent claims for the deposit value, beverage container such as cans and plastic bottles are punctured or crushed, or subsequently crushed in a compactor. If manually collected, the waste beverage containers are generally counted at a counting facility. Prior to transport of the containers to that facility, the storage of returned containers needs to ensure that the containers are not damaged and must be secure, to avoid theft and subsequent duplicate claims of the refund value.

2.7 SORTING, BULKING AND RECYCLING/RECOVERING OF CONTAINERS

Once collected by the retailer or the RVM, the containers must be sorted, bulked and sent for reprocessing. Box 2.1 summarises the beverage container collection method for plastic bottles in the Netherlands. Similar collection methods apply in the other countries assessed.

Box 2.1 Plastic Bottle Collection Methods in the Netherlands

The requirements at the sorting facilities determine the initial sorting required at the retailers. Most sorting facilities use automated high speed sorting machines handling up to 500 containers per minute and able to sort co-mingled plastic bottles, cans and glass (although generally no more than 20% glass, to avoid breakage). Glass bottles may be sorted separately at the retailers due to the specific requirements for their storage (glass bottles are generally stored in rigid containers (eg pallet boxes) whereas plastic bottles and cans are stored in plastic bags). Some collection and storage methods at retailers will result in a little additional sorting. For example, in Denmark and Sweden, the material fractions (plastic, cans, glass) are generally sorted in the RVM or manually, and arrive at the sorting facility in separate bags. In addition, in Sweden a number of retailers have separate RVMs for plastic bottles and cans, as combi-RVMs are significantly more expensive. In Germany, the empty beverage containers generally arrive at the sorting and counting facility as co-mingled containers. Manual sorting of containers can result in single stream materials ready for counting. However, if the retailer

In the Netherlands, waste plastic bottles are bulked up following initial collection. Each retailer is provided with plastic bags and security tags/closures for the bags. The full and sealed bags are subsequently transported to one of three centralised sorting and checking facilities. At these facilities, further checks are made to confirm the returned containers are valid (ie the container is part of the deposit scheme) and retailers are provided with a confirmation report on the exact value of the deposits for which they receive reimbursement from the centralised body.

ENVIRONMENTAL RESOURCES MANAGEMENT DEFRA

11

has little storage space, or the RVM is small, different containers may be collected together, and require sorting downstream, before they can be sent to reprocessing. To optimise the recycling of containers (and therefore their value), the sorting process needs to make distinctions:

1. between the three main types of containers listed; and

2. between additional sorting characteristics outlined in Table 2.2. In some cases, this may not be easily achieved (eg glass containers which are covered with complete labels/sleeves).

Table 2.2 Optimal Sorting Requirements

Main Types of Containers Additional Individual Characteristics Polymer bottles Polymer type Colour (clear, white, green, etc) Glass bottles Colour (clear, green, brown) Cans Metal type

2.8 ASSURING SECURITY AND PREVENTING FRAUD

The packaging label provides some security against any initial fraud, but additional procedures need to be in place to prevent fraudulent deposit claims, both before and after the packaging item is used. Once the packaging has been produced and the deposit label has been applied, the packaging assumes a value equal to that deposit (and the value of the deposit might well exceed the value of the packaging itself). If the deposit label is applied prior to the packing/filling operation, the deposit value will effectively be assumed by the empty packaging. Any logistics operation may need tighter security arrangements to prevent theft of empty packaging (eg warehousing), as deposit refunds could potentially be ‘reclaimed’ without having been paid in the first place. At the other end of the packaging life cycle, it is necessary to ensure that the deposit on the packaging is only claimed once. As previously mentioned, retailers and RVMs are the main routes to obtain a deposit refund, and they store collected containers prior to movement to either sorting or recycling facilities. As a result, procedures need to be in place to prevent these containers being subject to duplicate fraudulent refunds. An intact container can potentially be stolen and have its deposit claimed again at any point after its initial collection, until it is recycled/reprocessed, so secure arrangements have to be made along the waste supply chain. Duplicate claims on containers returned via RVMs can be prevented by crushing returned containers. For glass bottles or manual take-back, retailers need to keep the waste beverage containers secured until they reach the counting facility.

ENVIRONMENTAL RESOURCES MANAGEMENT DEFRA

12

As the UK is an island, the potential for fraud is less than many other countries, as, with the exception of the Irish border, cross-border movement of containers is less straightforward and much more costly. If a system were to operate in the UK, RVM manufacturers have suggested that a system using the existing barcode to identify a product manufactured or imported into the UK would suffice. Potential fraud in the UK would most likely be confined to small scale photocopying or production of fake barcodes, labels and deposit vouchers (Consumer Fraud). It is far less likely that large scale fake container manufacture (Industrial Fraud) would be an issue; it would need to be on a large scale, and would require bulk loads of containers to be deposited and placed into the RVMs, which would be relatively easy to detect in most locations. The RVMs can also include security systems to identify repeat containers and bar codes of the same type, with automatic alerts to the retail outlet. Direct discussions with representatives of the organisations administering the deposit schemes in Denmark and Sweden suggest that fraud is not a major issue in these countries. It is generally detected and dealt with swiftly through improvements to the RVMs or the system itself. Examples of fraud include:

• copying of the barcode and applying to non-deposit bearing containers;

• purchase of beverage products abroad and selling in shops (eg corner shops); and

• customers or shop staff feeding containers through twice.

2.9 POTENTIAL HEALTH AND SAFETY IMPLICATIONS OF DEPOSIT SYSTEMS

There is a range of anecdotal information regarding the H&S implications of accepting waste beverage containers at retail sites. This includes concerns regarding the safe storage of glass containers, the return of containers containing residual beverages and odour issues associated with empty packaging. On a more practical note, retailers need to implement appropriate and safe storage to minimise any risk of material spillage. Furthermore, for glass bottles in particular, moving large numbers of the containers around the store could give rise to a manual handling risk to the retailer, although no more of a risk than the receipt and movement of products for sale. While all of these points seem reasonable, the different national deposit systems have generally addressed these and ERM has been unable to find any statistical data that lends support to health and safety concerns over and above the general handling of beverage containers. It should be possible to

ENVIRONMENTAL RESOURCES MANAGEMENT DEFRA

13

mitigate all of the identified concerns by undertaking an appropriate risk assessment. Health and safety is the main reason for milk and juice not generally being part of the deposit schemes, due to concerns over odours and potential health issues with any remaining beverage in returned containers. Depending on the frequency of collection, the waste beverage containers may be stored at the retailers for some time, potentially in the vicinity of food products sold in store.

2.10 POTENTIAL CROSS BOUNDARY ISSUES AND SINGLE MARKET IMPLICATIONS

Deposit systems in Germany, Sweden, the Netherlands and Denmark have all had to consider how to handle consumer imports of packaged beverages and also the implications of beverage containers being returned into the deposit system from outside the national boundaries. The deposit systems are national systems and therefore beverages sold within the respective countries are required to bear a deposit and the consumer is entitled to a refund. Beverages purchased by the consumer in other countries do not form part of the deposit schemes. To align with the emphasis of increasing recycling rates, some of the deposit schemes allow for the RVMs to accept non-deposit bearing beverage containers, but, of course, no deposit is returned. A specific issue of the cross-border sales between Germany and Denmark is that German retailers near the Danish border are authorised through an exemption by the local government in Schleswig Holstein to sell drinks to Scandinavian consumers without charging the German deposit. This is not the case for other border areas in Germany. The Scandinavian consumers must complete an export declaration confirming their intention to export the beverages purchased to their home countries on the same day. The declaration does not contain a statement preventing these customers from returning empty beverage containers to the border shops. German retailers have suggested that the Danish deposit is applied to beverages sold to Danish consumers in German border shops, but this involves a number of practical issues (eg control of the Danish deposit label in Germany, what shops should be included, collection in Germany) that are considered unworkable by the Danish deposit system. ERM was unable to determine any particular barrier of deposits systems that would be worse for foreign suppliers compared with new national suppliers. There does not seem to be any difference in joining a scheme whether you are a national brewery, a foreign brewery, an importer or whatever. The only possible barrier would be that new companies have to learn about the system, and that might be easier if you are national, owing to personal experience and language issues.

ENVIRONMENTAL RESOURCES MANAGEMENT DEFRA

14

2.11 COSTS AND INCOME STREAMS

The main activities associated with running a packaging deposit and collection system that incur costs are listed below.

• administrative and data functions;

• administration of money flow;

• labelling procedures;

• security and fraud prevention;

• public awareness raising;

• packaging collection systems (eg RVMs);

• movement of waste packaging; and

• reprocessing of waste packaging (although this is not peculiar to deposit systems).

There are also additional costs associated with the time and resources spent:

• monitoring and regulating the system;

• reviewing the effectiveness of the system, and

• agreeing the scope and value of deposits paid. In order to meet these costs, income is generated from three principal routes, as follows.

1. Fees charged to industry – typically on packer/fillers and importers who place beverage containers on the market. Charges are usually made in proportion to the number of beverage products placed on the market.

2. Deposits which are charged but not redeemed, because the packaging is not returned by the consumer.

3. Value of the waste material collected. In running a successful deposit system, it is important that the income generated ‘matches’ the costs incurred as closely as possible, as most deposit systems run as ‘not for profit’ systems. However, determining the costs and revenues of operating a ‘cost neutral’ deposit system are challenging for a number of reasons, including:

• the number of packer/fillers and importers of beverages is subject to change and hence the income received from these parties will fluctuate;

• the volumes and types of containers placed on the market are subject to market fluctuations (eg seasonal variations, market trends, general economic influences) and hence the income received from packer/fillers and un-redeemed deposits will also fluctuate;

• the value of the deposit will influence container return rates and therefore the total value of unredeemed deposits (see below);

ENVIRONMENTAL RESOURCES MANAGEMENT DEFRA

15

• return rates have a direct effect on the costs associated with collecting, movement and recycling of containers, but the return rate is difficult to predict, particularly during the initial operation of a deposit system; and

• the value of collected materials will fluctuate according to recycling markets.

For these reasons, the centralised body is usually responsible for ensuring the fair allocation of costs between industry players and the monitoring of system costs. This has resulted in changes to the deposit value in some systems. The deposit systems reviewed in this project have all been in existence for some time. In particular, those in Sweden and Denmark are well-established systems that have evolved from existing deposit systems for refillable containers. Box 2.2 provides some thoughts on the aspects associated with establishing a new deposit system in a country where no existing system is in operation.

Box 2.2 What Needs to be In Place Before Launching a Deposit System?

2.12 VALUE OF THE DEPOSIT

In most countries, the value of the deposit varies according to the type and/or size of container. Table 2.3 provides an overview of the deposits charged according to the different container types in the countries reviewed in this project. The figures show the value both in national currency but also an indication of the value in UK sterling.

Introducing a deposit system from ‘scratch’ requires careful planning. Some of the main implications of establishing a new system are summarised below.

• All producers and importers will need to label their products and pay into the centralised fund and the centralised body would need to have been established. Otherwise safeguards would need to be put in place to: - avoid producers operating outside the system having an unfair market advantage (the purchase price of their goods would be lower than those within the system). - reduce consumer confusion (eg some drinks would include a deposit; others would not).

• Labelling procedures and associated security arrangements would need to be in place.

• The beverage container collection infrastructure would need to be in place to allow consumers to return beverage containers following product purchase. Once a deposit is charged, the return mechanism needs to be available. This would require up front investment in collection infrastructure (eg RVMs or collection sites) and prior notification of retailers.

• The deposit refund system would need to be clearly established, to ensure all retailers understand the procedures for charging and reimbursing deposits.

• A consumer education campaign would be required to ensure they understand the system.

• Arrangements for sorting and recycling of containers would need to be in place.

ENVIRONMENTAL RESOURCES MANAGEMENT DEFRA

16

Table 2.3 Value of Deposits on Beverage Containers (†)

Country Plastic Bottles Aluminium Cans Glass Bottles Denmark < 1 litre DKK 1.00

(~11 pence) 0.5 litre DKK 1.50 (~16 pence) ≥ 1 litre DKK 3.00 (~32 pence)

< 1 litre DKK 1.00 (~11 pence) ≥ 1 litre DKK 3.00 (~32 pence)

< 1 litre DKK 1.00 (~11 pence) ≥ 1 litre DKK 3.00 (~32 pence)

Germany* 0.1 to 3.0 litres 25 Euro cents (~20 pence)

0.1 to 3.0 litres 25 Euro cents (~20 pence)

0.1 to 3.0 litres 25 Euro cents (~20 pence)

Sweden ≤ 1 litre SEK 1.00 (~ 12 pence) > 1 litre SEK 2.00 (~ 25 pence)

All sizes SEK 0.50 (~ 6 pence)

N/A

Netherlands ≥ 0.5 litre 25 Euro cents (~20 pence)

N/A Specific sizes 25 Euro cents (~20 pence)

(*) The German deposit system originally distinguished between sizes of container. In 2005, the deposit value was standardised to 25 Euro cents for all container sizes.

(†) Exchange rates used: £1 = DKK 9.4249 = SEK 8.0487 = €1.2631 A number of issues need to be considered when setting the value of the deposit for beverage containers.

• The value of the deposit has to provide a sufficient incentive to encourage consumers to return containers. Higher deposit values generally result in higher collection rates for beverage containers.

• However, a deposit which is higher than the cost of manufacturing empty packaging may encourage fraud by encouraging production of new containers simply to attempt to obtain a deposit refund.

• The value of the deposit relative to the value of the product may have unexpected consequences. For example, the retail value of some low cost soft drinks may be lower than the value of the deposit, which may discourage consumers from purchasing the product. Conversely, the relatively high value of some products (eg champagne) to their deposit may mean that the consumers of such products are unlikely to be incentivised into returning the container.

• The value of deposits needs to be set such that it is not seen as artificially increasing the cost of beverages, or hiding a product price increase. This could impact on general inflation figures and have wider economic consequences.

ENVIRONMENTAL RESOURCES MANAGEMENT DEFRA

17

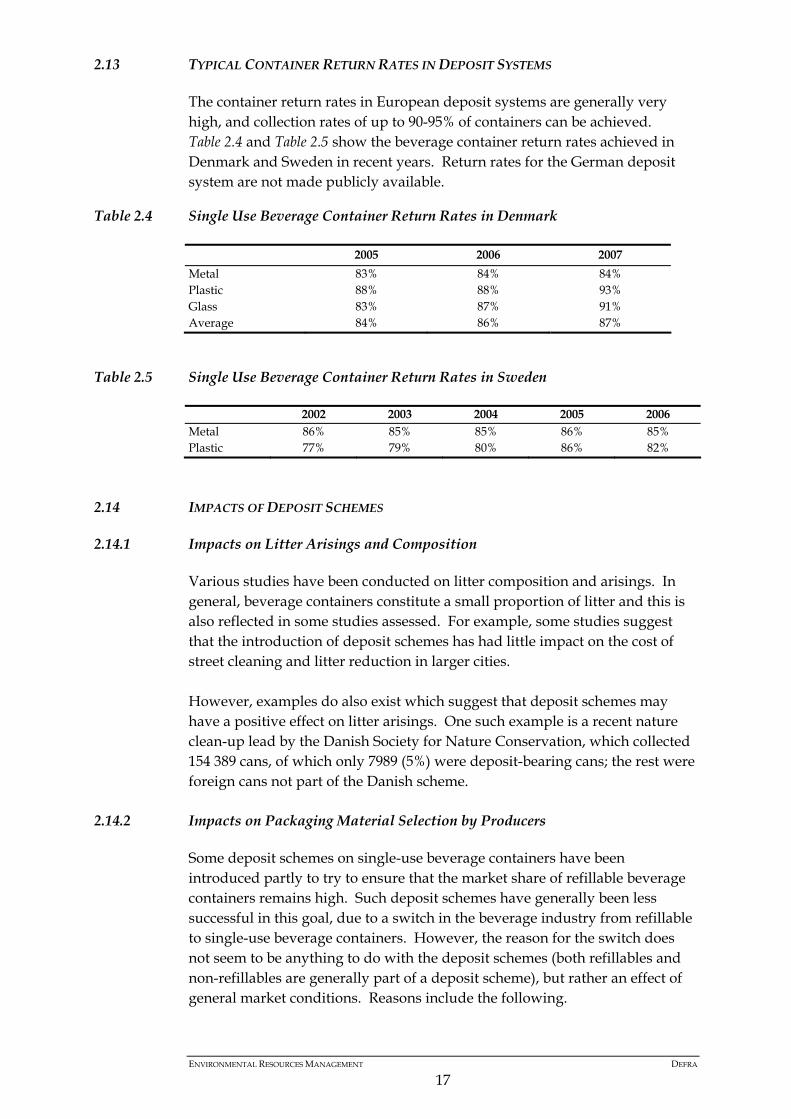

2.13 TYPICAL CONTAINER RETURN RATES IN DEPOSIT SYSTEMS

The container return rates in European deposit systems are generally very high, and collection rates of up to 90-95% of containers can be achieved. Table 2.4 and Table 2.5 show the beverage container return rates achieved in Denmark and Sweden in recent years. Return rates for the German deposit system are not made publicly available.

Table 2.4 Single Use Beverage Container Return Rates in Denmark

2005 2006 2007 Metal 83% 84% 84% Plastic 88% 88% 93% Glass 83% 87% 91% Average 84% 86% 87%

Table 2.5 Single Use Beverage Container Return Rates in Sweden

2002 2003 2004 2005 2006 Metal 86% 85% 85% 86% 85% Plastic 77% 79% 80% 86% 82%

2.14 IMPACTS OF DEPOSIT SCHEMES

2.14.1 Impacts on Litter Arisings and Composition

Various studies have been conducted on litter composition and arisings. In general, beverage containers constitute a small proportion of litter and this is also reflected in some studies assessed. For example, some studies suggest that the introduction of deposit schemes has had little impact on the cost of street cleaning and litter reduction in larger cities. However, examples do also exist which suggest that deposit schemes may have a positive effect on litter arisings. One such example is a recent nature clean-up lead by the Danish Society for Nature Conservation, which collected 154 389 cans, of which only 7989 (5%) were deposit-bearing cans; the rest were foreign cans not part of the Danish scheme.

2.14.2 Impacts on Packaging Material Selection by Producers

Some deposit schemes on single-use beverage containers have been introduced partly to try to ensure that the market share of refillable beverage containers remains high. Such deposit schemes have generally been less successful in this goal, due to a switch in the beverage industry from refillable to single-use beverage containers. However, the reason for the switch does not seem to be anything to do with the deposit schemes (both refillables and non-refillables are generally part of a deposit scheme), but rather an effect of general market conditions. Reasons include the following.

ENVIRONMENTAL RESOURCES MANAGEMENT DEFRA

18

• Practicality and cost: refillables, although also part of the deposit and refund scheme, are generally collected by the breweries themselves. By switching to non-refillables, the task of collection and sorting is taken over by the deposit scheme.

• Space saving at the production location: washing facilities are not required in a bottling plant for single-use beverage containers.

• Hygiene issues: with reference to the above, these are eliminated.

• Marketing: a refillable bottle looks less attractive in the eyes of the consumer with its scuffs and marks.

With regard to the selection of beverage container materials, and, more specifically, the substitution of beverage containers that are not part of a deposit scheme, the overriding issue seems to be consumer acceptance rather than avoiding the deposit. However, such examples do exist; one producer in Sweden switched to a bottle made from a plastic that was not part of the deposit scheme. This was addressed in a later amendment to the legislation, with the expansion of the plastics covered. In Denmark, the scheme has been expanded recently to include non-carbonated drinks. This could potentially lead to some substitution of packaging for such beverages (eg still water) into other containers that are not part of the deposit scheme (eg pouches, cartons) in order to avoid the imposition of a deposit on the product. However, no examples of this have yet been seen.

2.15 THE ROLE OF REVERSE VENDING MACHINES (RVMS)

2.15.1 Introduction

The majority of RVMs are similar in both design and function. Machines will accept an identified range of containers (limited only by the demand for the material, the size and capacity of the machine and the aperture shape and size). Containers which have been deposited will then either be stored, or compacted and shredded within the machine before collection. Storage capacities are dependant on the overall size of machine (or, in the case of ‘hole in the wall’ machines, the size of the room behind). As an example, a 2.6m2 footprint unit for up to two waste streams (based on a Tomra T-83 HCp Dual Cabinet RVM) has a capacity of up to 7000 cans (0.35 litre), or 11 000 PET bottles (0.5 litre), or 300 glass bottles (crushed). RVMs vary in size, from small units for just one material type to banks of several machines capable of accepting a wide range of materials. RVMs are generally located either within a store (often in the front foyer), or at the front entrance to a supermarket (in similar locations to cash dispenser machines). The retailer will chose a location which is intended to draw the

ENVIRONMENTAL RESOURCES MANAGEMENT DEFRA

19

consumer into the store to make a purchase. Facilities are also in place in smaller shopping areas (eg district centres, service stations / garages, 24-hour shops, etc). Ideally, consumers should be able to return participating containers to all established points of purchase and be reimbursed the deposit value.

Figure 2.1 Examples of Reverse Vending Machines

In some cases, RVMs are integrated into a larger recycling facility, which also is used for containers and materials without a deposit. The RVMs themselves may also be configured to accept items which are not part of the deposit scheme. The most common materials accepted by RVMs are aluminium and steel cans, plastic bottles (in the main PET) and glass bottles. Cardboard containers and beverage cartons are also accepted in some cases, but this is not widespread, as there are more potential hygiene/odour concerns with these materials (such as milk packaging), and it is harder to handle cartons so that the barcode can be read. Plastic vending cups and even crisp packets (1) are collected in some locations (the latter being driven by litter problems rather than any value in the material). Containers can be returned to both automated (eg an RVM) and manual (eg a simple identified container) collection points. Once a deposit scheme has been in operation for some time, most containers are taken by consumers to automated collection points. In Germany, when the deposit system was first introduced, the majority of containers (roughly 80%) were returned to retailers, with only 20% via RVMs. After 5-6 years of operation, this pattern has switched, with approximately 80% of the containers now being returned to RVMs and 20% to retail outlets. A similar pattern is noted in other countries with well developed deposit systems.

(1) Sawtry Community College, Peterborough as reported by Peterborough Today, accessed from

http://www.peterboroughtoday.co.uk/news/RECYCLING-The-vending-machine-that.998768.jp, October 2008.

ENVIRONMENTAL RESOURCES MANAGEMENT DEFRA

20

Where manual systems are used, an additional counting stage is required. This is usually reflected by a lower deposit value for containers.

2.15.2 Identifying Containers

The vast majority of RVMs will identify a container by reading its barcode. This will either be the existing barcode on the packaging, or an additional ‘national’ barcode which has been added where there is a high potential for cross border movement of products from one country to another. The RVM will identify the barcode on a database before accepting the container. Using a barcode technology means that additional containers can easily be added to the deposit scheme and the barcode database updated. Most systems use a database in excess of 100 000 barcodes. Some machines will include additional technologies to identify the container; most comprising of a camera system which will recognise the shape and/or an additional identification marking on the container. This is particularly the case where the potential for fraud and cross border movement of containers is a major concern (such as the schemes in Denmark and Germany). These systems are more complex and expensive. Any rejected materials will be ejected from the machine unless the machine has been programmed to accept the container but not issue any refund. The deposit is refunded once the container has been successfully identified.

2.15.3 Refund of Deposits

Most machines refund a voucher or ticket deposit, which is then taken to the store checkout to be redeemed for cash or used as part payment for purchases. This encourages the consumer to enter the store and spend, which is cited as one of the benefits of a RVM system to the retail industry (though see also Section 3.8.3). Some machines refund cash directly, although this is generally recognised as a more expensive method (this is because the machines require more maintenance and there are inherent security risks associated with handling, loading and storing cash). Some systems offer alternative rewards (such as loyalty card points). These are not strictly ‘deposit’ schemes, as no initial charge was made. Such schemes generally accept a wider range of recyclable materials including paper, cardboard and plastic bags.

2.15.4 Performance and Key Facts - RVM Deposit Schemes

Sweden - Returpack

The Swedish system is currently in operation for aluminium cans, small and large PET bottles. Containers can be returned to both manual and automated locations in retail centres. Across the country there are:

• 10 000 points of return, of which 6500 are RVMs.

ENVIRONMENTAL RESOURCES MANAGEMENT DEFRA

21

This is a mandatory system; all containers sold in the sizes specified by the legislation are part of the deposit scheme. Return rates of 85% for metal cans and 82% for plastic bottles were reported for 2006. Denmark – Dansk Retursystem

The Danish system covers glass bottles, plastic bottles and drinks cans, both single use and refillable, and is a mandatory system. There are more than 7000 sales locations (supermarkets, grocery shops, kiosks, restaurants, cafes, hotels, catering, and other outlets) registered with Dansk Retursystem as sellers of beverages in deposit-bearing containers. There are in the region of 2500 RVMs located within these outlets. Return rates of 84% for cans, 93% for plastic bottles, and 91% for glass bottles were reported for 2007. Germany – Deutsche Pfandsystem

The German system covers glass bottles, plastic bottles and drinks cans, both single use and refillable, and is a mandatory system. There are near to 100 000 points of sale selling beverages in single use packaging and in the region of 21 000 RVMs supporting the deposit system. Return rates for the German system are not made publicly available. The Netherlands – Stichtling Verpakkingen Nederland

The Dutch system covers plastic bottles and refillable glass bottles, and is a mandatory system.

2.15.5 Cost and funding of RVMs

In Europe, RVMs are generally purchased by the retailer (whereas, in the US, retailers mostly lease machines). Financial support is provided to the shops in several of the countries assessed, in the form of a handling allowance/subsidy. The allowance is paid per container and varies according to container type, in-store equipment (ie whether the shop has RVMs, compactors). These subsidies are provided to stores in order to optimise the ‘bottle room’ with regard to equipment and lay-out and to further the efficiency of the whole collection chain. In Sweden, the allowance being paid to shops with RVMs is higher than that paid to shops without, in order to encourage shops to install RVMs. In Denmark, it is the opposite, with shops with RVMs and compactors receiving the smallest allowance, and shops without the largest allowance, in order to reflect the actual cost to the retailer more accurately. The fees paid by producers and importers cover the handling allowance. The handling fee is administered by the central organisation.

ENVIRONMENTAL RESOURCES MANAGEMENT DEFRA

22

Other financial support may also be available. For example, in Denmark, part of the logistics fee paid by producers and importers is used to improve efficiency in shops through financial support to optimise ‘bottle room’ layout, equipment, etc. The outright purchase cost of RVMs ranges from just a few thousand GBP for a small machine, suitable for a service station or convenience shop, through to £20 000 and above for high volume machines which can accept in the region of 3000 containers per day (1). A premium is paid for machines which can separate fractions of clear and coloured materials (eg coloured PET and glass bottles). In Germany for example, the 21 000 RVMs have been installed at an average cost of about £11 000 each. Additional costs may be incurred by the retailer, particularly where larger machines are installed and some building work is required to fix equipment to the wall, or alter the entrance or other designated area of the store to take account of the deposit location.

2.16 THE ROLE OF THE CLEARING HOUSE

The role of the clearing house is to administer the deposit and control the flow of refund money within the deposit system. Importantly, the clearing house is required to balance out the deposit income that retailers receive from selling beverages against the refunds reimbursed to customers. This involves managing the IT systems linked to the RVMs in the stores and the counting machines at counting and sorting facilities. In some countries (eg Sweden and Denmark), the role of the clearing house is held by the organisation administering the national system. This means that acting as a clearing house is only one of the roles held by the organisation. Other roles may include: registering and collecting fees from producers and importers; registering retailers; administering fees; management of the deposit label; monitoring fraud; collection of empty beverage containers from stores; operating the counting and sorting facilities; and running public awareness campaigns. In Germany, the centralised body is not involved in the flow of money. Instead, its main responsibilities include the management of the deposit label, the provision of the master database, and the IT interface.

2.17 SUMMARY – ADVANTAGES AND DISADVANTAGES OF DEPOSITS SYSTEMS

Table 2.6 summarises the advantages and disadvantages of deposit systems.

(1) This information, which applies to RVMs in general, was provided during an interview with Wolfgang Ringel, Vice

President TOMRA Systems, October 2008

ENVIRONMENTAL RESOURCES MANAGEMENT DEFRA

23

Table 2.6 Advantages and Disadvantages of Deposit Systems

Advantages Disadvantages Increased return rates Most countries without deposit schemes do not reach the same return rates for single use beverage containers as those achieved in countries with deposit schemes. The countries that are covered in this study (and that report their figures) all exceed 80% return rates, and a number of material return rates exceed 90%.

Costs Evidence from the national deposit schemes in other European countries show that introducing a deposit scheme has cost implications to producers and importers, and retailers. A presentation (1) from Deutsche Pfandsystem GmbH (the German deposit system for disposal drinks packaging) concluded that compulsory deposits cost around three times as much per container as household-based collections.