Embed Size (px)

Citation preview

African Development Bank Group

Loan Accounting Division

Financial Control Department

Version : 2011

D e b t S e r v i c i n g H a n d b o o kD e b t S e r v i c i n g H a n d b o o k

B.P. 323 - 1002 Tunis Belvédère TunisiaTel.: (+216) 71 102 955Fax: (+216) 71 194 477Email: [email protected]: www.afdb.org

Loan Accounting Division

Financial Control Department

Version February 2011

Deb t Se r v i c i ng Handbook

African Development Bank Group

2

D e b t S e r v i c i n g H a n d b o o k - A f r i c a n D e v e l o p m e n t B a n k G r o u p

The Financial Controller’s Department is responsible

for administering the accounts of borrowers of the

African Development Bank Group1 (the Bank Group

or the ADB Group). The Loan Accounting Division

is responsible for billing and loan recovery matters,

and provides borrowers with services related to

loan accounting.

This Handbook is a resource intended primarily for

borrowers of the Bank Group, to assist in their

understanding of Bank Group policies and

procedures regarding the servicing of their debts

to the Bank Group.

This version supersedes all previous versions. It is

subject to periodic updates, to reflect changes in

the Bank Group’s product offerings and in the

related loan accounting, billing and recovery

procedures.

This Handbook is also available electronically on

the Bank Group website (http://www.afdb.org).

Foreword

1 The terms “The Bank Group” or “the ADB Group” refer to the African Development Bank (ADB), the African Development Fund (ADF) and the NigeriaTrust Fund (NTF). Where a discussion pertains specifically to one of these institutions, the institution is explicitly named.

3

ADBADFB.P.EUREURIBORGBPJIBARJPYLIBORMFIXMVLRNSGLNTFSVLRSFLRSFIXSGLUAUSD

African Development BankAfrican Development FundBasis pointEuroEuro Inter-Bank Offered RatesGreat Britain PoundJohannesburg Inter-Bank Offered RatesJapanese YenLondon Inter-Bank Offered RatesMulti-currency Fixed RateMulti-currency Variable RateNon sovereign guaranteed loansNigeria Trust FundSingle Currency Variable RateSingle Currency Floating RateSingle Currency Fixed RateSovereign guaranteed loansUnit of AccountUnited States Dollar

Acronyms

D e b t S e r v i c i n g H a n d b o o k - A f r i c a n D e v e l o p m e n t B a n k G r o u p

4

D e b t S e r v i c i n g H a n d b o o k - A f r i c a n D e v e l o p m e n t B a n k G r o u p

1. Introduction

1.1. The African Development Bank Group

1.2. Legal framework

2. Terms of Current ADB Lending Products

2.1 Loan maturity

2.2 Grace period

2.3 Currencies

2.4 Lending rate terms

2.5 Fees and commissions

2.6 Principal repayment terms

3. Terms of ADB Discontinued Lending Products

3.1 Variable rate loans

3.2 Multicurrency fixed rate loans

4. Terms of ADF Loans

4.1 ADF loans maturity, grace period and principal repayment terms

4.2 Currencies

4.3 Lending terms

5. Terms of NTF Loans

5.1 Maturity and grace period

5.2 Currencies

5.3 Lending terms

6. Debt Relief Initiatives

6.1 Highly Indebted Poor Countries (HIPC)

6.2 Multilateral Debt Relief Initiative

7. Loan Identification Number

7.1 Source of financing codes

Contents

6

6

7

8

8

8

8

9

11

12

13

13

14

15

15

17

20

21

21

21

21

23

23

24

25

25

5

7.2 Identification of financial product type

7.3 Loan numbering scheme

8. Billing Procedures

8.1 Methodology for calculating bills

8.2 Content of bill package and other available reports

9. Recovery Procedures

9.1 Order of payment application

9.2 Payments falling due on non-working days

9.3 Treatment of single currency payment

9.4 Treatment of shortfalls and excess payment

9.5 Incoming Payments Report

10. Arrears Management and Sanctions

10.1 Definition of arrears

10.2 Sanction policy of the Bank

10.3 Exemptions from sanctions

11. Cancellation Procedures

12. Prepayment Procedures

13. Reports Available to Borrowers

Bibliography

Annexes

Annex I: Statement of confirmed disbursements

Annex II: Loan status report

Annex III: Billing statements

Annex IV: Repayment statement

D e b t S e r v i c i n g H a n d b o o k - A f r i c a n D e v e l o p m e n t B a n k G r o u p

26

28

29

29

30

31

31

31

31

31

32

33

33

33

33

35

36

37

39

41

42

44

48

6

D e b t S e r v i c i n g H a n d b o o k - A f r i c a n D e v e l o p m e n t B a n k G r o u p

1.1. The African Development Bank Group

The primary objective of the African Development

Bank Group is to contribute to the sustainable

economic development and social progress of its

regional members, individually and jointly. This

objective is met by financing a broad range of

development projects and programs, primarily

through: (i) public sector loans (including policy-

based loans), private sector loans and equity

investments; and (ii) providing technical assistance

for institutional support projects and programs.

The African Development Bank Group comprises

the African Development Bank, the African

Development Fund and the Nigeria Trust Fund,

which are further described below.

Established in 1964, the AFRICAN DEVELOPMENT

BANK is a regional multilateral development bank owned

and supported by its current 77 member countries,

including 53 African and 24 non-African countries. As

members, the countries contribute to the capital of the

ADB. In addition to such contributed capital, the other

sources of funding include the following:

• Borrowings on the international capital

markets;

• Repayments from loans;

• Retained Earnings.

The AFRICAN DEVELOPMENT FUND is the main

concessionary window of the Bank Group. The

current membership of the ADF comprises 24

non-African State Participants, South Africa and

the African Development Bank. ADF provides

assistance to developing countries with low per

capita income through loans extended on more

favorable terms than the ADB as well as through

grants. The ADF is funded primarily through

periodic replenishments by the State Participants.

Replenishments to the Fund are usually made on

a three-year basis, unless State participants

decide otherwise.

The NIGERIA TRUST FUND, the third window in

the ADB Group, was established by the

government of Nigeria, with the objective of

providing development assistance to developing

countries with low per capita income through

loans extended on more concessionary terms

than the ADB. Although the ADF and NTF are

legally and financially distinct from the ADB, they

share the same staff, and their projects are subject

to the same standards as those of the ADB.

1. Introduction

7

1.2. Legal framework

1.2.1. General conditions

The standard conditions governing ADB and ADF

financial products are contained in the institutions’

General Conditions Applicable to Loan, Guarantee

and Grant Agreements and in the respective

operational guidelines. Similarly, conditions

governing NTF loans are contained in the NTF

operational guidelines. General Conditions are an

integral part of the loan agreements and cover

the following:

• Interest, commitment charges and other

charges computation

• Application of payments

• Repayment and prepayment provisions

• Currency provisions, including valuation of

currencies

• Withdrawal of proceeds

• Cancellation and suspension

• Acceleration to maturity

• Termination

• Various other legal provisions

1.2.2. Legal agreements

The main legal document for a financial lending

product offered by the Bank is an agreement

signed between the borrower and the Bank,

which sets out the terms and conditions of the

contract. When the Bank lends directly to a party

other than a member country, the Bank may also

enter into a guarantee agreement with the relevant

member country.

D e b t S e r v i c i n g H a n d b o o k - A f r i c a n D e v e l o p m e n t B a n k G r o u p

Figure 1: African Development Bank Group

The African Development Bank

(ADB)

The African Development Fund

(ADF)

The Nigeria TrustFund(NTF)

Commercial Terms Concessional Terms

8

D e b t S e r v i c i n g H a n d b o o k - A f r i c a n D e v e l o p m e n t B a n k G r o u p

The Bank’s range of products has evolved and

increased over the last decade, introducing

more flexibility and choice for the clients it serves.

These changes were driven by the need for the

Bank to be more responsive to its borrowers’ varied

and evolving needs. Changes include the

introduction of risk management products, allowing

clients to hedge against financial risks associated

with their ADB loans, and equity investments.

Guarantees and loan syndications were also added

to the menu allowing the Bank to play a catalytic

role in mobilizing capital to projects in the private

sector.

The Bank’s standard loans are categorized either

as Sovereign Guaranteed Loans (SGL) or

Non‐Sovereign Guaranteed Loans (NSGL). SGLs

are loans made to an eligible regional member

country (RMC) or to a public sector enterprise

supported by the full guarantee of the RMC in

whose territory the borrower is domiciled. NSGLs

are loans made either to public sector enterprises

without the existence of a sovereign guarantee or

to private sector enterprises.

This chapter presents the current ADB lending

terms.

2.1. Loan maturity

The African Development Bank provides long‐term

financing to its borrowers. SGLs have final maturities

of up to 20 years including a grace period of up to

5 years. NSGLs have final maturities of up to 15

years inclusive of the grace period.

2.2. Grace period

Grace periods are dependent on the specific

characteristics of the project and the time required

for its implementation but generally they should not

exceed 5 years. In exceptional cases, grace periods

longer than 5 years may be considered subject to

satisfactory justification of project requirements by

the borrower. The grace period starts from the date

of signature of the loan agreement.

2.3. Currencies

2.3.1. Currency of commitment

The Bank currently offers loans in US Dollars, Euro,

Japanese Yen and South African Rand (ZAR). The

Bank may also consider lending in other currencies

in which it funds itself efficiently and for which there

is sufficient demand.

2.3.2. Currency of disbursement

The Bank may execute disbursements in any

payment currency requested by the borrower. The

requested currency is purchased using the

exchange rate (spot rate) quoted by the selling bank

and the borrower’s obligation is recorded in the loan

currency. This currency purchase on behalf of the

borrower is free of charges.

2. Terms of current ADB lending products

2 The latest list of lending products is available on the Bank website: http://www.afdb.org/en/documents/financial-information/financial-products/

9

2.3.3. Currency of repayment

The loan principal, interest and any other fees are

payable in the currency of commitment. However,

currency conversion options are available and allow

borrowers to settle amounts due in any of the

following currencies: EUR, GBP, JPY and USD. The

borrower retains the exchange rate risk. Accordingly,

any shortfall or excess resulting from the application

of the single currency payment is for the borrower’s

account.

2.3.4. Local currency products

The Bank has broadened its scope to

accommodate the possibility of lending in local

currencies, and has developed a framework to

guide the provision of loans in Regional Member

Country (RMC) currencies.

2.4. Lending rate terms

2.4.1. Enhanced variable spread loans for sovereign guaranteed entities

In December 2009, the Bank introduced for

sovereign guaranteed entities the Enhanced Variable

Spread Loan (EVSL). Under the previously proposed

variable spread loan, the pricing comprised of the

Bank’s cost of borrowing and a lending spread (base

rate + funding margin + lending spread). Two

alternatives were offered to clients at loan approval:

they could either select a floating or fixed base rate.

With the new enhanced variable spread loan, the

pricing remains the same but offers a floating base

rate with a free embedded option to fix the base

rate on demand. This implies that over the life of

the loan, borrowers have the flexibility to fix the

interest rate on the cumulative disbursed and

outstanding amount at any time.

As presented in Table 1 below, the EVSL lending

rate has three components: a floating base rate that

can be fixed at borrower’s request; a funding margin;

and a lending spread.

The floating base rate is determined for each loan

currency with a reset frequency based on the Bank’s

selected reference interest rate in each market. The

Bank’s standard floating base rates are the 6‐month

Libor for USD and JPY; the 6‐month Euribor for

EUR; and the 3‐month Jibar for ZAR. Except for

the ZAR which resets quarterly on February 1st, May

1st , August 1st and November 1st , the other floating

rates reset semi-annually on February 1st and

August 1st.

D e b t S e r v i c i n g H a n d b o o k - A f r i c a n D e v e l o p m e n t B a n k G r o u p

Table 1: EVSL Lending Rate

a) Base Rate

Floating rate (6m Libor/Euribor, 3m Jibar)Can be fixed free of charge at the borrower’s request

b) Funding MarginBank’s cost of borrowing relative toLibor, Euribor, Jibar with semi-annual resets

c) Lending Spread Between 40 and 60 b.p.

d) Lending Rate (d)=(a)+(b)+(c)

10

D e b t S e r v i c i n g H a n d b o o k - A f r i c a n D e v e l o p m e n t B a n k G r o u p

If the borrower decides to fix the floating rate on

the cumulative disbursed and outstanding tranche,

the fixed base rate for that tranche is computed by

the Bank as the inter‐bank swap market rate

corresponding to the principal amortization

schedule. The Bank reserves the right to delay fixing

if the size of the tranche/disbursement is not large

enough to allow for a cost-effective fixing

transaction. In such cases, fixing would occur as

soon as an adequate disbursed amount, as

determined by the Bank, has been accumulated to

warrant the transaction and such amount should

be set out in the loan agreement.

The funding margin is currency specific. It is

calculated twice a year and applicable on February

1st and August 1st. It is the semester weighted

average of the spread between Libor/Euribor/Jibar

and the cost of the debt allocated to fund the single

currency floating rate loans portfolio.

The lending spread is subject to periodic review,

with changes applied prospectively only. The lending

spread has evolved overtime within a range of 40

to 60 basis points. Currently, sovereign-guaranteed

loans approved on or after January 1, 2011 carry

a lending spread of 60 basis points.

2.4.2. Fixed spread loan for sovereign guaranteed entities

Fixed Spread loans (FSL) were introduced in 2005

and offered borrowers a lending rate consisting of

a floating or fixed base rate and a fixed lending

spread that remains unchanged throughout the life

of the loan.

In January 2009, the Bank temporarily suspended,

for sovereign-guaranteed entities, the Fixed Spread

Loan product for new commitments by the

introduction of a funding margin. The objective of

this amendment was to ensure a full pass through

of the Bank’s borrowing costs to its clients, thereby

safeguarding its financial integrity and its ability to

remain a stable source of long term funding.

2.4.3. Fixed spread loan for non-sovereign guaranteed entities

Fixed Spread Loans (FSL) offer borrowers a lending

rate consisting of a floating rate (Libor/Euribor/Jibar)

and a specific fixed spread corresponding to the

project’s credit risk. The FSL includes the option to

fix the interest rate on demand while maintaining

the spread constant over the life of the loan.

Table 2: FSL Lending Rate for Sovereign-Guaranteed Entities

a) Base Rate

Floating rate (6m Libor/Euribor, 3m Jibar)

Fixed (specificinter-bank swapmarket rate)

b)Lending Spread

Bank’s standard lending spread

c) Lending Rate

(c)= (a)+(b)

11

2.5. Fees and commissions

2.5.1. Commitment fee

Commitment fees are intended to compensate the

Bank for the cost of giving borrowers the option to

draw down the funds during a predetermined period.

The commitment fee ranges from 0% to 1% per

annum for SGLs and for NSGLs it could be higher.

It is calculated on undisbursed loan balances and

starts accruing no later than 60 days after loan

signature.

The commitment fee has been removed since May

2005 for new commitments approved in favor of

sovereign-guaranteed entities. From January 1,

2011, the commitment fee is reintroduced for fast

disbursing policy-based loans which register

slippage in disbursements.

2.5.2. Fees specific to Non-Sovereign

Guaranteed loans

Appraisal fee

Appraisal fees partially or fully cover costs incurred

by the Bank in appraising new project proposals

and are payable even in cases where the project is

not approved.

Appraisal fees are payable no later than at the

signature of the loan agreement, or as agreed

among co-financiers in co‐financed projects.

Front end fee

The front‐end fee is designed to partially

compensate the Bank for the costs associated with

processing a loan request and preparation of the

documentation for loan approval. It is charged only

when the project is approved and it is not

reimbursed if the project is subsequently cancelled.

The front‐end fee is 1% of the loan amount. It is

payable before or at loan signature, however when

market and/or conditions warrant, the front end fee

may be paid up to thirty (30) days after loan

signature or as agreed among co-financiers in

co‐financed projects.

D e b t S e r v i c i n g H a n d b o o k - A f r i c a n D e v e l o p m e n t B a n k G r o u p

Table 3: FSL Lending Rate for Non-Sovereign Guaranteed Entities

a) BaseRate

Floating rate (6m Libor/Euribor, 3m Jibar)

Fixed (specificinter-bank swapmarket rate)

b)Lending Spread

Based on specific project risk

c) Lending Rate

(c)= (a)+(b)

12

D e b t S e r v i c i n g H a n d b o o k - A f r i c a n D e v e l o p m e n t B a n k G r o u p

Arrangement or Syndication fee

The arrangement or syndication fee is levied to pay

for the work and expenses of the arranger of the

syndication. This flat fee is paid by the borrower on

or before the date of signature of the loan

agreement. The level of this fee depends on the

complexity of the transaction in line with prevailing

market practices.

Loan administration fee

The loan administration fee is a flat fee levied to pay

for the work of the syndication Agent. The level and

payment frequency should be in line with prevailing

market practices.

Underwriting fee

Where ADB underwrites a portion of the B‐loan,

the borrower shall pay an underwriting fee to ADB.

The calculation details and payment date of this flat

fee should be stated in the loan agreement.

2.5.3. Fees specific to guarantees

Standby-fee

The standby-fee is charged on the undisbursed

portion of the underlying loan. This fee is in the

range of 0% to 1%.

Guarantee fee

This fee is similar to the lending spread on a Bank

loan. The guarantee fee comprises of the lending

spread that would have been charged if the Bank

had made a direct loan and a risk premium. The

risk premium reflects the risks associated with

particular guarantee structures.

2.6. Principal repayment terms

The Bank’s principal repayment terms provide for

the payment of equal installments of principal, after

the expiration of the grace period. Other principal

repayment terms such as bullet repayment and

step‐up or step‐down amortization of principal may

be considered subject to satisfactory justification

of project requirements by the borrower.

13

This section describes the terms and conditionsrelating to outstanding balances on ADB loan

products that have been withdrawn from the ADBmenu for new loan commitments.

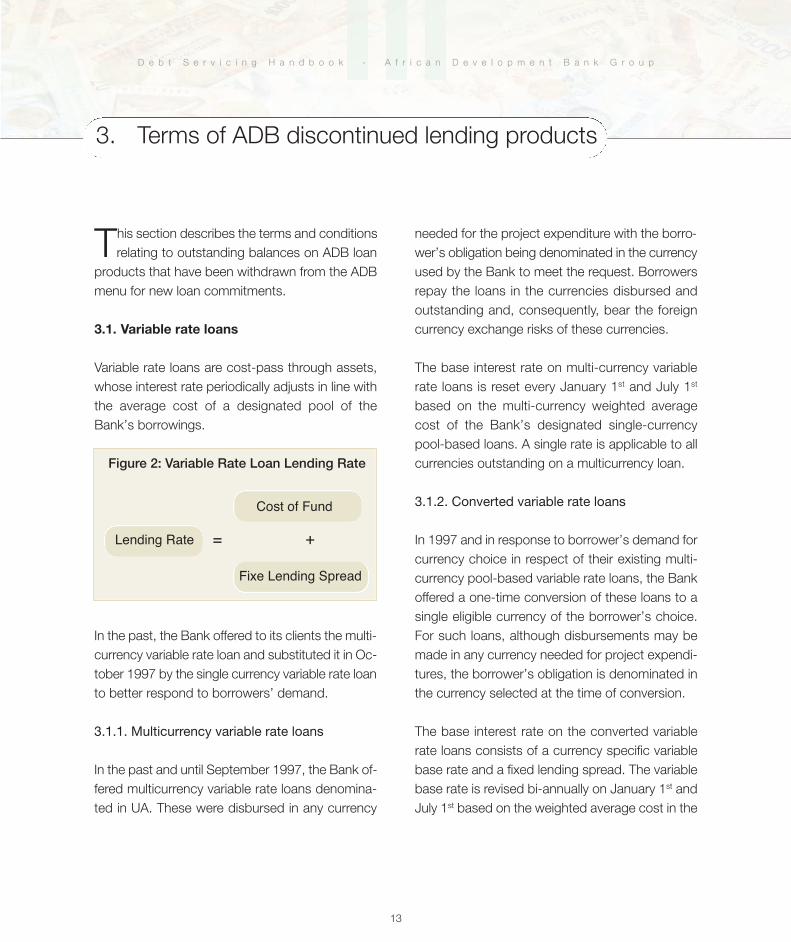

3.1. Variable rate loans

Variable rate loans are cost-pass through assets,whose interest rate periodically adjusts in line withthe average cost of a designated pool of theBank’s borrowings.

3. Terms of ADB discontinued lending products

D e b t S e r v i c i n g H a n d b o o k - A f r i c a n D e v e l o p m e n t B a n k G r o u p

=Lending Rate

In the past, the Bank offered to its clients the multi-currency variable rate loan and substituted it in Oc-tober 1997 by the single currency variable rate loanto better respond to borrowers’ demand.

3.1.1. Multicurrency variable rate loans

In the past and until September 1997, the Bank of-fered multicurrency variable rate loans denomina-ted in UA. These were disbursed in any currency

needed for the project expenditure with the borro-wer’s obligation being denominated in the currencyused by the Bank to meet the request. Borrowersrepay the loans in the currencies disbursed andoutstanding and, consequently, bear the foreigncurrency exchange risks of these currencies.

The base interest rate on multi-currency variablerate loans is reset every January 1st and July 1st

based on the multi-currency weighted averagecost of the Bank’s designated single-currencypool-based loans. A single rate is applicable to allcurrencies outstanding on a multicurrency loan.

3.1.2. Converted variable rate loans

In 1997 and in response to borrower’s demand forcurrency choice in respect of their existing multi-currency pool-based variable rate loans, the Bankoffered a one-time conversion of these loans to asingle eligible currency of the borrower’s choice.For such loans, although disbursements may bemade in any currency needed for project expendi-tures, the borrower’s obligation is denominated inthe currency selected at the time of conversion.

The base interest rate on the converted variablerate loans consists of a currency specific variablebase rate and a fixed lending spread. The variablebase rate is revised bi-annually on January 1st andJuly 1st based on the weighted average cost in the

+

Figure 2: Variable Rate Loan Lending Rate

Cost of Fund

Fixe Lending Spread

14

D e b t S e r v i c i n g H a n d b o o k - A f r i c a n D e v e l o p m e n t B a n k G r o u p

preceding semester of a designated single-cur-rency pool of the Bank’s borrowings.

3.1.3. Single currency variable rate loans

Effective October 1, 1997, the Bank Board of Di-rectors approved the introduction of single cur-rency loans in USD, JPY and EUR in response toits borrowers’ needs. The introduction of the ZARas loan currency was approved in 1998.

Loan disbursements can be transacted in anycurrency needed for project expenditures with theborrower’s obligation denominated in the cur-rency of loan commitment.

The base interest rate on the single currency va-riable rate loans is reset every January 1st and July1st based on the weighted average cost in the pre-

ceding semester of a designated single-currencypool of the Bank’s borrowings.

The single currency variable rate loan sufferedfrom the competition with other loan products thatprovide similar loan profiles at more competitivelevels. As a result and given the decreasing de-mand for this product, the Bank decided in De-cember 2009 to withdraw it from the menu ofinstruments offered to clients.

3.2. Multicurrency fixed rate loans

The Bank offered prior to July 1, 1990, the multi-currency fixed rate product. The rate is fixed forthe life of the loan at the time of approval and le-vied on the disbursed and outstanding currencybalances on the loan. A single rate is applicableto all currencies outstanding on the loan.

15

D e b t S e r v i c i n g H a n d b o o k - A f r i c a n D e v e l o p m e n t B a n k G r o u p

4. Terms of ADF loans

The African Development Fund (ADF) is the Bank

Group’s main concessional lending window.

ADF extends funds to the low income countries on

a concessional basis.

4.1. ADF loans maturity, grace period and principal repayment terms

ADF loans have final maturity of up to 50 years

including a 10-year grace period. For project loans,

principal amounts are amortized at an annual rate

of 1% of the cumulative disbursed amount for the

10 years following the grace period and 3% for the

remaining 30 years.

Where disbursements occur after the expiration of the

grace period, the annual amortization rate is adjusted

to ensure that 90% of the cumulative disbursed amount

of the loan is repaid over the last remaining 30 years.

The required adjustments are illustrated in Table 5.

Lines of credit extended by the Fund have final

maturity of up to 20 years including a 5-year grace

period and are repayable in equal installments.

Table 4: Example of amortization schedule

Life of the loan Amounts in UA

End of grace period - Cumulative disbursements 10,000 14,000 21,000 30,000

Year 11-20 (0.5% of cumulative disbursements per semester) 50 70 105 150

Year 21-50 (1.5% of cumulative disbursements per semester) 150 210 315 450

16

D e b t S e r v i c i n g H a n d b o o k - A f r i c a n D e v e l o p m e n t B a n k G r o u p

Table 5: Adjusted amortization – Disbursement after the grace period

Remaininginstallments

New disbursements

Cumulative disbursements

Repayments % of cumulativedisbursements

Cumulativerepayments

Outstandingbalance

Installment 1 20 10,000 50 0.50% 50 9,950Installment 2 19 10,000 50 0.50% 100 9,900Disbursement 4,000 14,000 100 13,900Installment 3 18 14,000 72 0.52% 172 13,828Installment 4 17 14,000 72 0.52% 244 13,756Installment 5 16 14,000 72 0.52% 317 13,683Installment 6 15 14,000 72 0.52% 389 13,611Installment 7 14 14,000 72 0.52% 461 13,539Installment 8 13 14,000 72 0.52% 533 13,467Disbursement 7,000 21,000 533 20,467Installment 9 12 21,000 131 0.62% 664 20,336Installment 10 11 21,000 131 0.62% 794 20,206Installment 11 10 21,000 131 0.62% 925 20,075Installment 12 9 21,000 131 0.62% 1,056 19,944Installment 13 8 21,000 131 0.62% 1,186 19,814Installment 14 7 21,000 131 0.62% 1,317 19,683Installment 15 6 21,000 131 0.62% 1,447 19,553Installment 16 5 21,000 131 0.62% 1,578 19,422Installment 17 4 21,000 131 0.62% 1,708 19,292Installment 18 3 21,000 131 0.62% 1,839 19,161Installment 19 2 21,000 131 0.62% 1,969 19,031Installment 20 1 21,000 131 0.62% 2,100 18,900Installment 21 60 21,000 315 1.50% 2,415 18,585Installment 22 59 21,000 315 1.50% 2,730 18,270Installment 23 58 21,000 315 1.50% 3,045 17,955Installment 24 57 21,000 315 1.50% 3,360 17,640Installment 25 56 21,000 315 1.50% 3,675 17,325Installment 26 55 21,000 315 1.50% 3,990 17,010Installment 27 54 21,000 315 1.50% 4,305 16,695Installment 28 53 21,000 315 1.50% 4,620 16,380Installment 29 52 21,000 315 1.50% 4,935 16,065Installment 30 51 21,000 315 1.50% 5,250 15,750Disbursement 9,000 30,000 5,250 24,750Installment 31 50 30,000 495 1.65% 5,745 24,255

17

disbursement currency chosen at negotiation or

in any currency used to purchase the payment

currency. This currency purchase on behalf of the

borrower is free of charges.

As soon as a disbursement is made, the

equivalent of the currency amount disbursed in

UA is debited to the loan account resulting in:

(i) a reduction in the undisbursed balance in

UA and

(ii) an increase in the outstanding currency

balance on the loan in the currency

selected by the borrower or in the currency

used by the Bank to meet the

disbursement request.

4.2. Currencies

4.2.1. Currency of commitment

ADF loans are denominated in Units of Account

(UA). For loans contracted after June 23, 2005,

borrowers have the option to select the currency

of disbursement (EUR, USD, JPY or GBP) at loan

signature.

4.2.2. Currency of disbursement

The Bank may execute disbursements in any

payment currency requested by the borrower.

The Bank purchases the requested currency using

the exchange rate (spot rate) quoted by the selling

bank and records the borrower’s obligation in the

D e b t S e r v i c i n g H a n d b o o k - A f r i c a n D e v e l o p m e n t B a n k G r o u p

18

D e b t S e r v i c i n g H a n d b o o k - A f r i c a n D e v e l o p m e n t B a n k G r o u p

Figure 3: Example of disbursement when no disbursement currency is selected and the Bank has USD liquidity3

1. Ministry of Finance requests a payment of

USD 1million

2. ADB pays tothe BeneficiaryUSD 1 million

5. ADB sends a bill in USD to Ministry of Finance

3. Loan Undisbursed Balance

decreases by UA 640,977.71UA/USD=1.5601

4. The Outstan-ding Balance increases byUSD 1 million

3 Exchange rates used are for illustrative purposes only. The rate for actual transactions would be the spot rate on the date of the transaction.

19

D e b t S e r v i c i n g H a n d b o o k - A f r i c a n D e v e l o p m e n t B a n k G r o u p

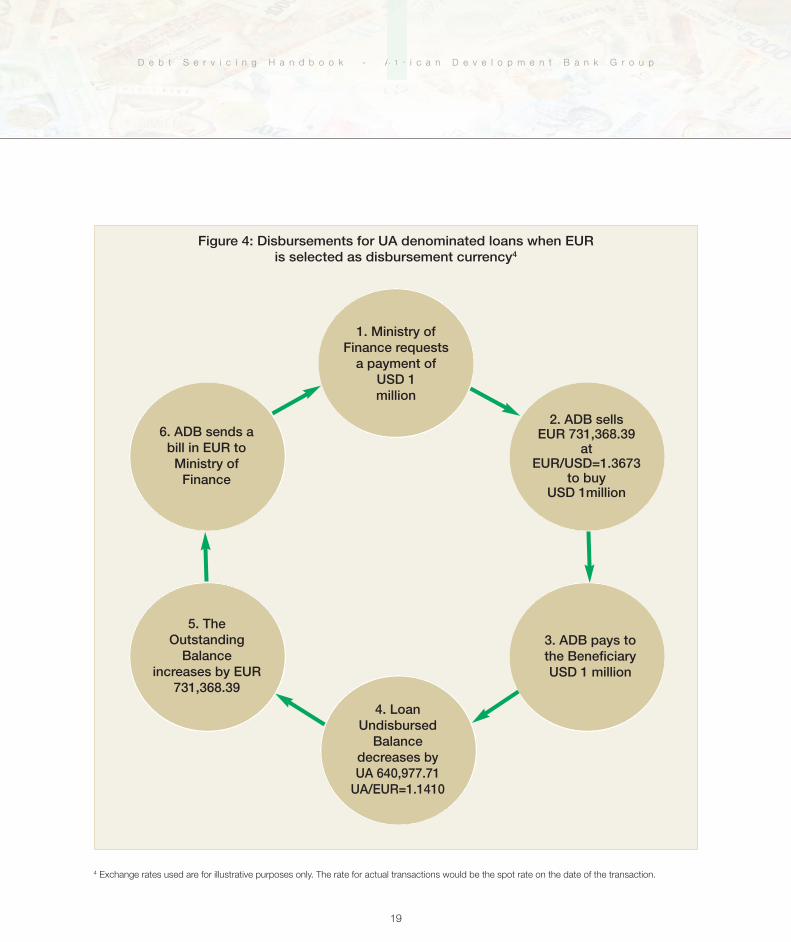

Figure 4: Disbursements for UA denominated loans when EUR is selected as disbursement currency4

1. Ministry of Finance requests a payment of

USD 1million

2. ADB sellsEUR 731,368.39

at EUR/USD=1.3673

to buyUSD 1million

3. ADB pays tothe BeneficiaryUSD 1 million

4. LoanUndisbursedBalance

decreases byUA 640,977.71UA/EUR=1.1410

5. The OutstandingBalance

increases by EUR731,368.39

6. ADB sends abill in EUR toMinistry of Finance

4 Exchange rates used are for illustrative purposes only. The rate for actual transactions would be the spot rate on the date of the transaction.

Figure 5: Lending terms under ADF window

20

D e b t S e r v i c i n g H a n d b o o k - A f r i c a n D e v e l o p m e n t B a n k G r o u p

4.2.3. Currency of repayment

Loan principal repayment and service charges are

billed and payable in the actual currencies

disbursed and outstanding. The commitment fee

is payable in USD. ADF provides currency

conversion options which allow borrowers to settle

amounts due in a single currency payment

denominated in any of the following currencies:

EUR, GBP, JPY and USD. The borrower’s

obligation remains in the loan currency and any

shortfall or excess resulting from the application

of the single currency payment is for the borrower’s

account.

4.3. Lending terms

No interest is charged on ADF loans. Only a service

charge of 75 basis points per annum is levied on the

disbursed and outstanding currency loan balance.

Loans approved after April 1, 1996 are subject to

a commitment charge of 0.5% per annum on the

undisbursed balance of the loan. Commitment

charges begin to accrue 120 days after the

signature of the loan agreement.

The table below summarizes the lending terms

under ADF window.

Maturity andPrincipal repayment

termsCurrency Grace Period Service Charge Commitment fee

Maturity Up to 50 years

Principal repayment:

• 1% of the

principal per

annum from the

11th to 20th year

• 3% of the

principal per

annum from the

21th to 50th year

Denominated inUA with the optionto select disbursementcurrency at loansignature (EUR,USD, JPY, or GBP)

Up to 10 years

0.75% per annumon disbursementand outstandingamount

0.50% per annumon undisbursedamount accruing120 days, startingat loan signaturedate

21

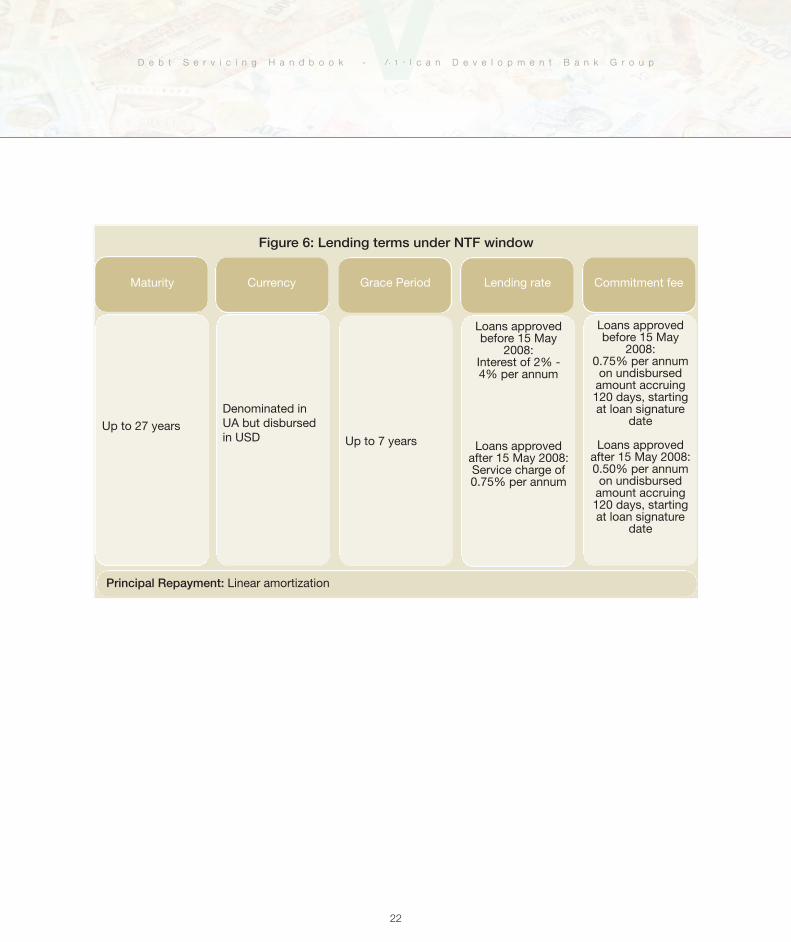

5.1. Maturity and grace period

NTF loans have final maturity of up to 27 years

including a grace period of up to 7 years.

5.2. Currencies

The Nigeria Trust Fund (NTF) extends loans

denominated in UA. Although loan disbursements may

be made in any payment currency requested, the

borrower’s obligation are denominated in US dollars.

5.3. Lending terms

Lending terms applicable to NTF loans were

revised on May 15, 2008.

For loans approved before May 15, 2008:

• The interest rate is fixed within a range of 2-

4% per annum, levied on the disbursed and

outstanding loan balance and payable in US

dollar.

• A commitment charge of 0.75% per annum

is levied on the undisbursed portion of each

signed loan, commencing 120 days after the

signature of the loan agreement.

For loans approved after May 15, 2008:

• No interest is charged. Only a service charge

of 75 basis points per annum is levied on the

disbursed and outstanding loan balance and

payable in US dollar.

• A commitment charge of 0.5% per annum

is levied on the undisbursed portion of each

signed loan, commencing 120 days after the

signature of the loan agreement.

NTF resources might be used to finance non-

sovereign guaranteed loans. Lending terms for

those loans would be the same as the ADB would

apply taking into consideration the Bank

Guidelines as well as the risk analysis of the

project.

5. Terms of NTF loans

D e b t S e r v i c i n g H a n d b o o k - A f r i c a n D e v e l o p m e n t B a n k G r o u p

22

D e b t S e r v i c i n g H a n d b o o k - A f r i c a n D e v e l o p m e n t B a n k G r o u p

Figure 6: Lending terms under NTF window

Maturity Currency Grace Period Lending rate Commitment fee

Up to 27 yearsDenominated inUA but disbursedin USD Up to 7 years

Loans approvedbefore 15 May

2008: Interest of 2% -4% per annum

Loans approvedafter 15 May 2008: Service charge of0.75% per annum

Loans approvedbefore 15 May

2008: 0.75% per annumon undisbursedamount accruing120 days, startingat loan signature

date

Loans approvedafter 15 May 2008: 0.50% per annumon undisbursedamount accruing120 days, startingat loan signature

date

Principal Repayment: Linear amortization

23

D e b t S e r v i c i n g H a n d b o o k - A f r i c a n D e v e l o p m e n t B a n k G r o u p

6.1. Highly Indebted Poor Countries (HIPC)

6.1.1. Overview

Created in September 1996, the Initiative for

Highly Indebted Poor Countries (HIPC) was

designed to reduce eligible countries’ debt burdens

to sustainable levels, subject to satisfactory policy

performance. The countries targeted under the

initiative were the poorest, most heavily indebted

countries that pursued certain programs of

adjustment and reforms.

The initiative was enhanced in 1999 as an outcome

of a comprehensive review by the International

Monetary Fund (IMF) and other institutions, including

public consultations. The Initiative’s debt-burden

thresholds were adjusted downward, which enabled

a broader group of countries to qualify for larger

volumes of debt relief.

HIPC countries, depending on their progress with

regard to certain macroeconomic criteria, fall in one

of the following statuses or categories5:

• Completion Point:

Countries reach completion point if they maintain

macroeconomic stability under a Poverty Reduction

and Growth Facility supported programs, carry out

key structural and social reforms and implement a

Poverty Reduction Strategy satisfactorily for one

year. Once a country reaches completion point, it

is entitled to full irrevocable debt relief.

• Decision Point:

In order to reach decision point, a country should

have a track record of macroeconomic stability,

have prepared an Interim Poverty Reduction

Strategy Paper, and cleared any outstanding

arrears. At decision point, countries begin to receive

interim HIPC debt relief on a provisional basis.

• Pre-Decision Point:

Countries at this stage have been assessed to meet

the income and indebtedness criteria at end-2004

and wish to avail themselves of the HIPC initiative.

6.1.2. Implementation modalities of HIPC

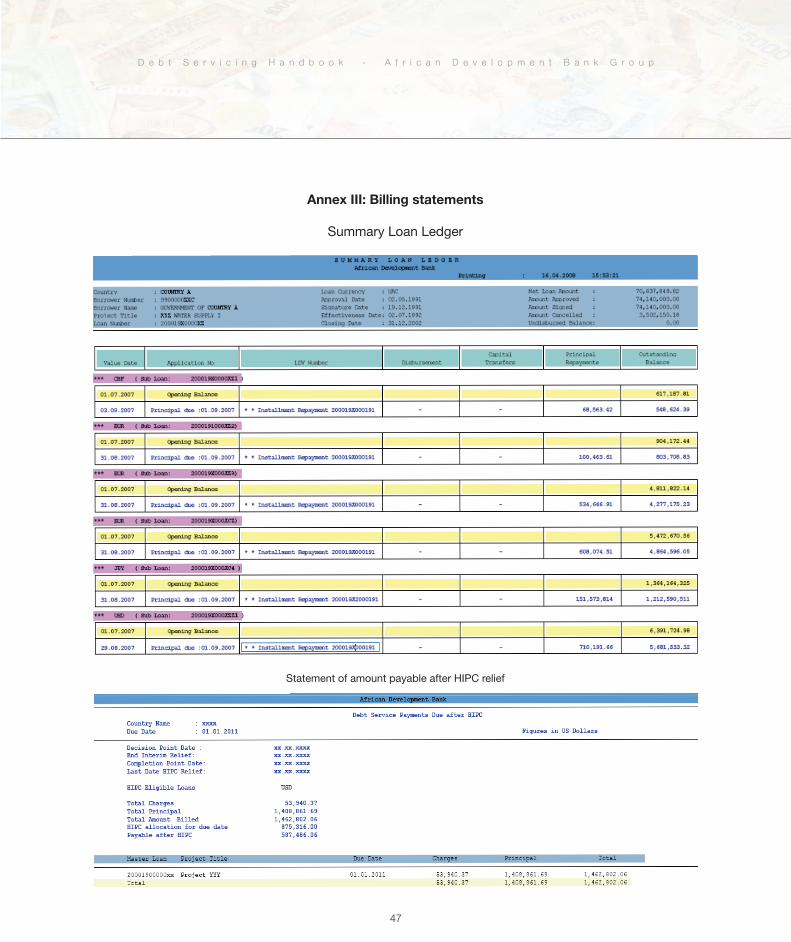

HIPC Debt Relief is delivered starting from decision

point and is applicable to the country’s Bank Group

portfolio on a pay-as-you-go basis as per the

schedule approved by the Board of Directors in the

decision point document.

At each due date, the debt service obligation of the

country is reduced by the amount of the relevant

HIPC allocation according to the HIPC schedule

approved by the Board.

The attainment of completion point status qualifies

a country for cancellation of its ADF eligible debt

under the Multilateral Debt Relief Initiative (MDRI).

HIPC allocation is discontinued for the ADF portfolio

while it continues to be delivered for the ADB and

6. Debt relief initiatives

5 HIPC statuses of Regional Member Countries are available in the Bank Group Annual Report: http://www.afdb.org/en/documents/publications/an-nual-report

NTF portfolios similarly to the allocation at decision

point.

6.2. Multilateral Debt Relief Initiative

6.2.1. Overview

In 2005, the G8 proposed that the African

Development Fund (ADF), the international

Development Association (IDA) and the International

Monetary Fund (IMF) cancel 100% of the eligible

debt of countries at completion date under the

enhanced HIPC initiative. This Multilateral Debt Relief

Initiative (MDRI) is aimed to further reduce the debts

of HIPCs and provide additional resources to help

them meet the Millennium Development Goals.

On April 19, 2006, the Boards of Directors of the

African Development Bank and African

Development Fund approved the ADF’s participation

in the MDRI. Accordingly, effective January 1, 2006,

Debt Relief under MDRI is to be provided by the

ADF once a country reaches the HIPC completion

point. ADB and NTF loans are not affected by the

initiative.

6.2.2. Modalities of MDRI implementation

Debt eligible for cancellation

The MDRI debt cancellation is applicable to the

outstanding balances, as of the implementation

date, of ADF loans which were disbursed and

outstanding as of December 31, 2004 (the cut-off

date). The MDRI implementation date is September

1, 2006 for countries that had reached completion

point prior to that date. For countries that reach

completion point after September 1, 2006, the

implementation date of MDRI is the completion

point date.

When MDRI is implemented for a country, the

delivery of ADF HIPC allocation is discontinued as

the eligible ADF loan balances are written-off.

Amount of Debt cancelled

The amount of individual loan balances that are

written off/cancelled under the MDRI from ADF

books is determined as follows:

• Cumulative disbursements as of the cut-off

date, less

• Related cumulative principal repayments as of

implementation date.

Amounts disbursed after the cut-off date are not

eligible for cancellation under the MDRI and remain

as obligations for the regional member countries

concerned. Consequently, bills for the residual loan

balances relating to such post cut-off

disbursements continue to be issued and are

expected to be fully serviced by the borrowing

member country.

24

D e b t S e r v i c i n g H a n d b o o k - A f r i c a n D e v e l o p m e n t B a n k G r o u p

25

D e b t S e r v i c i n g H a n d b o o k - A f r i c a n D e v e l o p m e n t B a n k G r o u p

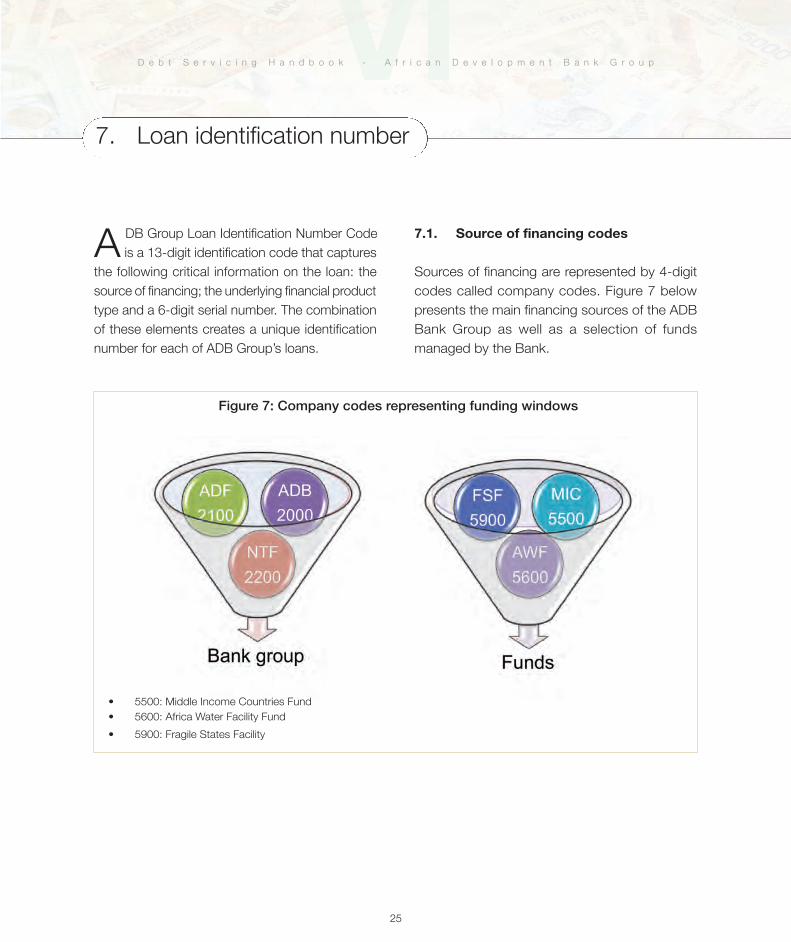

ADB Group Loan Identification Number Code

is a 13-digit identification code that captures

the following critical information on the loan: the

source of financing; the underlying financial product

type and a 6-digit serial number. The combination

of these elements creates a unique identification

number for each of ADB Group’s loans.

7.1. Source of financing codes

Sources of financing are represented by 4-digit

codes called company codes. Figure 7 below

presents the main financing sources of the ADB

Bank Group as well as a selection of funds

managed by the Bank.

7. Loan identification number

Figure 7: Company codes representing funding windows

• 5500: Middle Income Countries Fund

• 5600: Africa Water Facility Fund

• 5900: Fragile States Facility

26

D e b t S e r v i c i n g H a n d b o o k - A f r i c a n D e v e l o p m e n t B a n k G r o u p

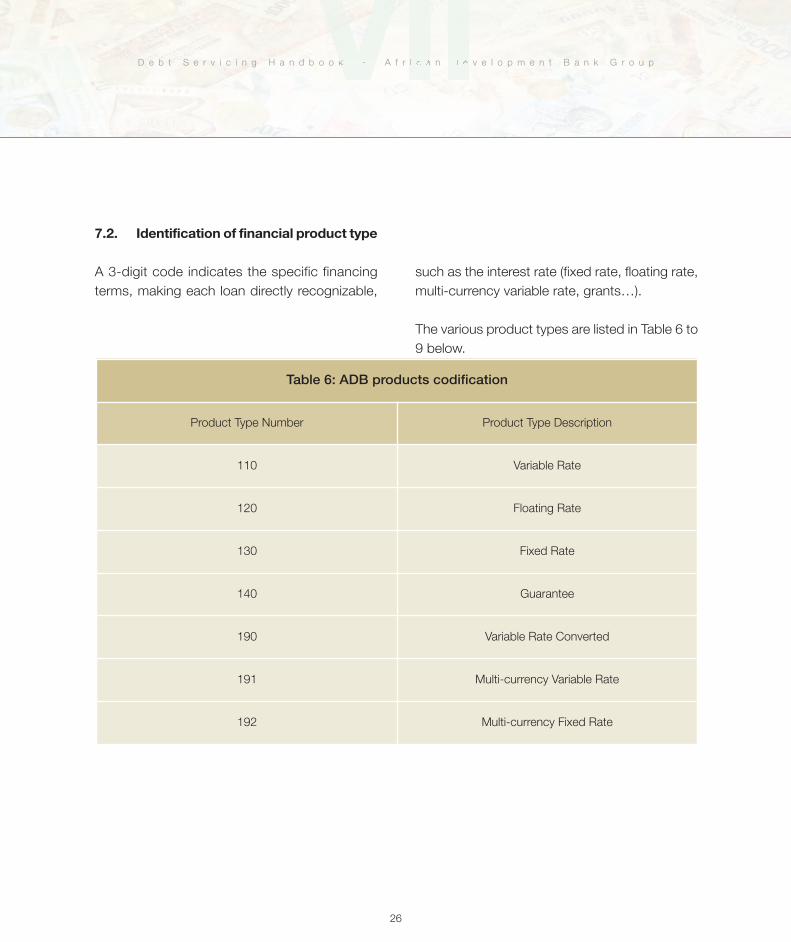

7.2. Identification of financial product type

A 3-digit code indicates the specific financing

terms, making each loan directly recognizable,

such as the interest rate (fixed rate, floating rate,

multi-currency variable rate, grants…).

The various product types are listed in Table 6 to

9 below.

Table 6: ADB products codification

Product Type Number Product Type Description

110 Variable Rate

120 Floating Rate

130 Fixed Rate

140 Guarantee

190 Variable Rate Converted

191 Multi-currency Variable Rate

192 Multi-currency Fixed Rate

27

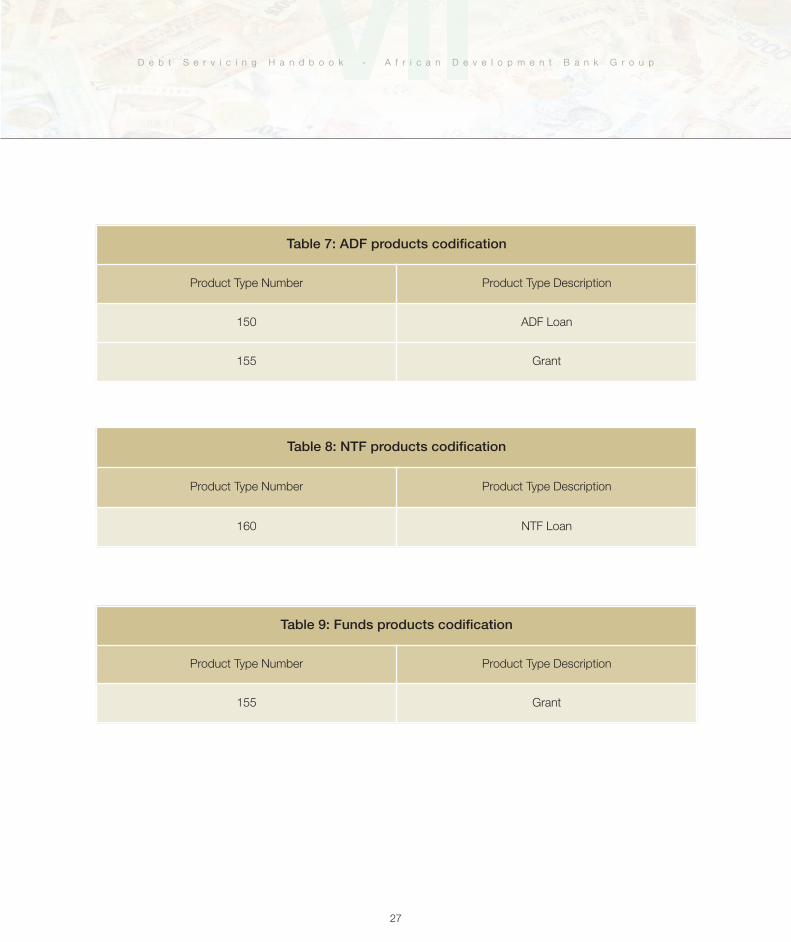

D e b t S e r v i c i n g H a n d b o o k - A f r i c a n D e v e l o p m e n t B a n k G r o u p

Table 7: ADF products codification

Product Type Number Product Type Description

150 ADF Loan

155 Grant

Table 8: NTF products codification

Product Type Number Product Type Description

160 NTF Loan

Table 9: Funds products codification

Product Type Number Product Type Description

155 Grant

Figure 9: Master and Sub Loans codification

Figure 8: Example of loan identification number

28

D e b t S e r v i c i n g H a n d b o o k - A f r i c a n D e v e l o p m e n t B a n k G r o u p

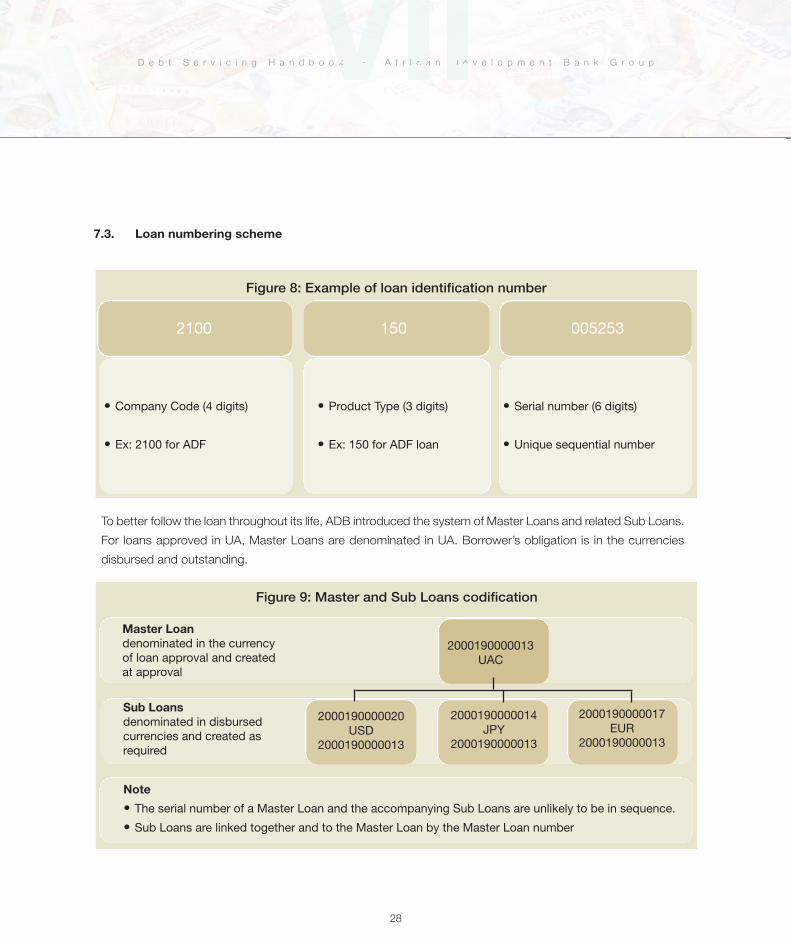

7.3. Loan numbering scheme

To better follow the loan throughout its life, ADB introduced the system of Master Loans and related Sub Loans.

For loans approved in UA, Master Loans are denominated in UA. Borrower’s obligation is in the currencies

disbursed and outstanding.

2100

• Company Code (4 digits)

• Ex: 2100 for ADF

150

• Product Type (3 digits)

• Ex: 150 for ADF loan

005253

• Serial number (6 digits)

• Unique sequential number

Master Loandenominated in the currency of loan approval and created at approval

Sub Loansdenominated in disbursed currencies and created as required

Note

• The serial number of a Master Loan and the accompanying Sub Loans are unlikely to be in sequence.

• Sub Loans are linked together and to the Master Loan by the Master Loan number

2000190000013UAC

2000190000014JPY

2000190000013

2000190000020USD

2000190000013

2000190000017EUR

2000190000013

29

Table des matières

8.1. Methodology for calculating bills

Sovereign-guaranteed loans are billed semi-

annually on the dates specified in the loan

agreement. The billing statements are prepared two

months before the semi-annual due date and sent

to borrowers six weeks before the due date. They

cover actual loan account movements for the six-

month period ending at the cut-off date, which is

two months before the due date of the bill as

illustrated in the table below.

If a billing period spans more than one interest rate

reset date, the rate is adjusted on the appropriate

date during the billing period in accordance with

rate fixing dates under the terms of the loan

agreement.

The last billing period of a loan is adjusted to cover

8-month period corresponding to the six months

interest period starting from the previous due date

plus the remaining two months.

Non-Sovereign-Guaranteed Loans are billed

according to the financial terms specified in the loan

agreement. Bills are usually issued every three or

six months without a cut-off period.

The other financial products offered by the Bank

are billed according to the applicable legal

documentation.

The main components of a bill are:

• Interest or Service charge based on the

outstanding currency balances over the billing

period;

• Commitment charge based on undisbursed

loan balances;

• Principal installment as specified in the loan

agreement.

8. Billing procedures

D e b t S e r v i c i n g H a n d b o o k - A f r i c a n D e v e l o p m e n t B a n k G r o u p

Due DateBilling Period

Cut-off DateApplicable Interest

Rate DateStart End

01-Aug-0801-Dec-07 31-Jan-08

31-May-0801-Aug-07

01-Feb-08 31-May-08 01-Feb-08

01-Feb-0901-Jun-08 31-Jul-08

30-Nov-0801-Feb-08

01-Aug-08 30-Nov-08 01-Aug-08

Table 10: Billing period and cut-off date

Table 11: Calculation of a bill

Component Formula

Interest and Service ChargeDisbursed & Outstanding (x) No. of days (x) Rate

360 or 365 Days*

Commitment ChargeUndisbursed Balance (x) No. of Days (x) Rate

360 or 365 Days*

PrincipalDisbursed & Outstanding - Arrears on Principal**

No of Remaining Installments

30

D e b t S e r v i c i n g H a n d b o o k - A f r i c a n D e v e l o p m e n t B a n k G r o u p

8.2. Content of bill package and other available reports

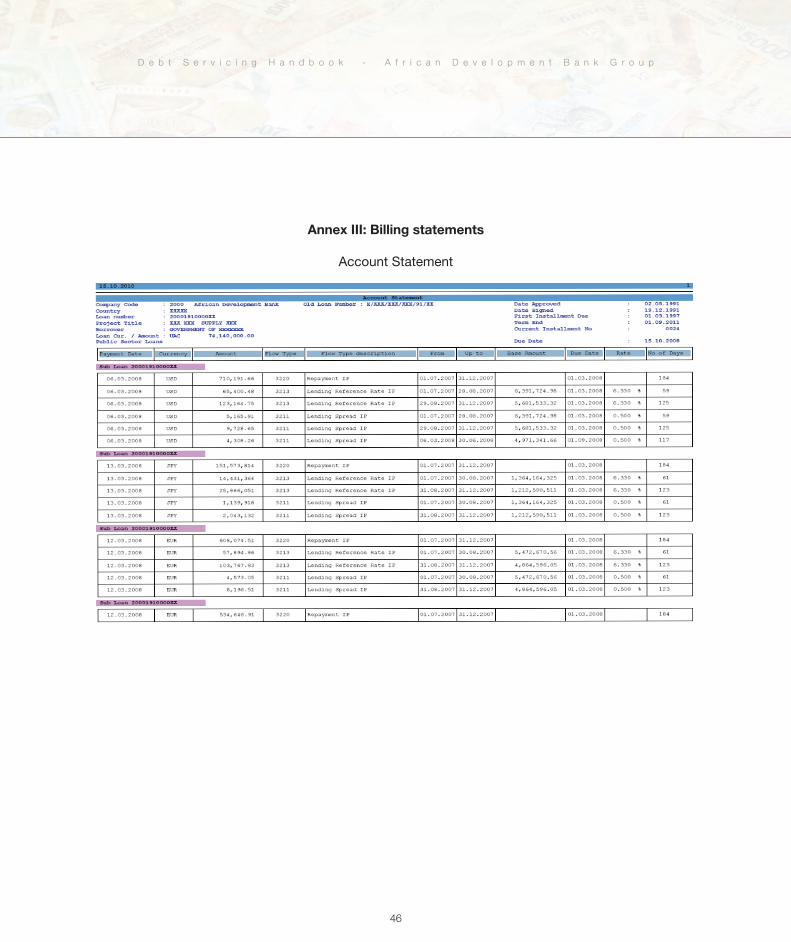

8.2.1. Billing package and repayment related information

The billing packages sent to borrowers (See Annex III)

provide the details of the amounts due on the given

due date. They include the following statements:

• Summary of Amounts due (Due by Currency);

• Statement of Single Currency Payment Option;

• Account Statement which provides detailed

computation;

• Summary Loan Ledger that reflects

movements on the loan;

• Amount payable after HIPC relief (if applicable).

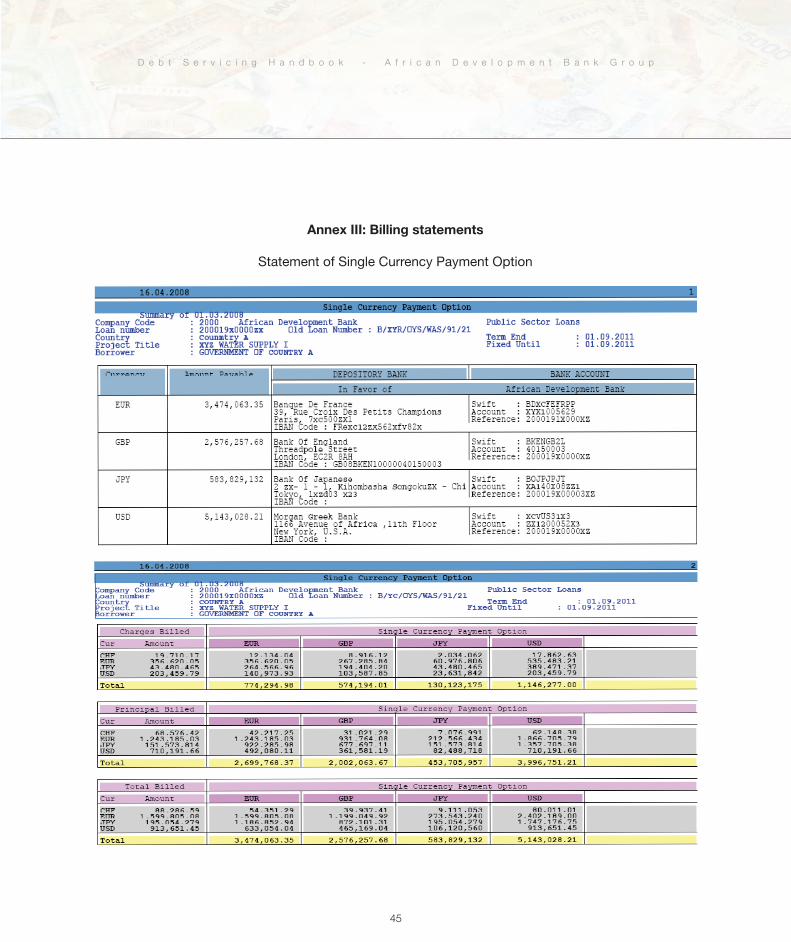

8.2.2. Single Currency Payment Option

Borrowers have the option to settle their debt

obligations in a single payment in any of the following

currencies: EUR, GBP, JPY, and USD. When this

option is exercised, the Bank acts as an agent of

the borrower to convert the payment received into

the required currencies. To facilitate the exercise of

this option, the single currency payment option

statement is included in the billing package.

Determination of Amount Payable under the Single Currency Payment Option

After calculating the amounts due in each loan

currency, estimates of the equivalent amounts in

each of the four currencies are determined using

the most recent exchange rates at billing date. The

rates used for conversion include a margin of

between 2 and 5 percent to cover possible

exchange rate fluctuations between billing and

settlement date.

Notwithstanding the above, shortfalls may occur in

the settlement process, due to adverse foreign

exchange rate movements. Such shortfalls remain

the responsibility of the borrower.

An illustrative Single Currency Payment Option

statement is presented at Annex III.

* Or any other interest calculation method specified in the loan agreement** Where principal billed is in arrears otherwise arrears do not feature

31

D e b t S e r v i c i n g H a n d b o o k - A f r i c a n D e v e l o p m e n t B a n k G r o u p

9.1. Order of payment application

Debt service payments are applied starting from

the oldest overdue to the most recent dues.

Within these categories, the funds received are

applied in the following order: commitment fees,

interest/service charge and principal.

9.2. Payments falling due on non-working days

If the due date falls on a non-working day for the

receiving bank, although interest and other charges

will continue to accrue on the outstanding loan

balance, no additional costs or penalties are

imposed on the borrower provided that payment

is received on the first working day thereafter. Other

business day conventions might be applied when

specified in the loan agreement.

9.3. Treatment of single currency payment

When a borrower exercises the single currency

payment option, the payment received is applied

first to amounts due in the currency of payment.

Any remaining funds are then used to purchase, on

behalf of the borrower, the other currencies due.

The Bank determines the loan currency equivalent

of the option currency received using market

exchange rates on the value date of the option

currency payment. These amounts are then applied

against bills as if payment had been received directly

from the borrower in the actual currencies due. Any

surplus or shortfalls arising from such transactions

are for the borrower’s account.

9.4. Treatment of shortfalls and excess payment

Shortfalls

A shortfall may arise due to either one of the

following reasons:

(i) the borrower exercises the single currency

payment option and makes payment in

accordance with the estimated amount

provided by the Bank at the time of billing, but

because of exchange rate fluctuations the

single currency payment is not sufficient to

purchase all currencies payable or

(ii) the borrower does not exercise the single

currency option but the amount received from

the borrower is not sufficient to cover the

amount billed.

Shortfalls are advised to borrowers and are due

immediately in case (ii). In case (i), payment is due

no later than the next due date. Shortfalls are

reported as arrears and continue to accrue

applicable interest when they relate to principal

amounts.

The Bank’s sanction policy provides for the

exemption from sanctions when the shortfall is due

to currency purchase transactions related to the

9. Recovery procedures

single currency payment option or when the unpaid

amount is less than UA 25,000.

Excess Payments

The Bank may hold excess funds for the borrower’s

account as a result of excess payments or following

currency purchases where foreign exchange rate

movements have been favorable to the borrower.

With the borrower’s consent, an excess payment

may be treated as follows:

• The excess may be held for the borrower’s

account and applied against the next bills or

capital subscriptions or against any other

obligation of the borrower.

• The excess may be refunded to the borrower.

9.5. Incoming Payments Report

The Application of Incoming Payments Report

(See Annex IV) is sent to borrowers following

receipt and application of their payments. This

report details the amounts received and how

they have been applied to charges and principal

for various loans. It also provides the amount of

excess payment that may arise.

32

D e b t S e r v i c i n g H a n d b o o k - A f r i c a n D e v e l o p m e n t B a n k G r o u p

33

D e b t S e r v i c i n g H a n d b o o k - A f r i c a n D e v e l o p m e n t B a n k G r o u p

10.1. Definition of arrears

Aloan is considered to be in arrears if payment

due is not received on the due date. If the

amount due remains fully or partially unpaid thirty

days after the due date, the Bank shall apply

sanctions to the borrower, in accordance with the

Sanctions Policy summarized below.

The Bank's financial ability to continue to promote

development depends on prompt servicing of

loans made by the Bank Group. Arrears may

ultimately impair the Bank's credit standing and

its ability to access resources for lending to

member countries on favorable terms. For these

reasons, the bank insists on settlement of invoices

when they fall due.

10.2. Sanction policy of the Bank

The policy relating to the recovery of arrears on

loans prescribes the rules and sanctions that are

applicable to borrowers and/or Guarantors in

default. The table 12 summarizes the sanctions

policy of the Bank Group.

Sanctions also automatically apply to a guarantor

fifteen (15) days from the date of application to the

borrower.

10.3. Exemptions from sanctions

Notwithstanding the above, sanctions may be wai-ved for a borrower in arrears under any of the fol-lowing circumstances:

• Technical assistance services financed from ADFresources allocated to the Technical AssistanceFund (TAF), particularly for pre-investmentstudies, institutional strengthening…;

• Training costs and scholarships;• Multinational projects and programs that shall

face only one sanction: prohibition from signingany new loan and/or guarantee agreements;

• Works and services concluded, supplies shippedor delivered prior to the date of application ofthe sanction involving suspension ofdisbursements. However, all relevantdisbursement requests must reach the BankGroup within a maximum of sixty days from thedate of application of the sanctions;

• Expenses payable to ADB/ADF with bilateralresources;

• Arrears whose cumulative amount does notexceed UA 25,000. The borrower is still howeverrequired to make immediate payment;

• Inadequate purchase of foreign exchange,incomplete transactions for foreign exchangepurchase, a billing error, amounts underinvestigation and payments returned bycommercial banks to borrowers.

10. Arrears management and sanctions

34

D e b t S e r v i c i n g H a n d b o o k - A f r i c a n D e v e l o p m e n t B a n k G r o u p

Table 12: Main Bank Group Sanctions

Trigger Sanction

Arrears of Over 30 days

Prohibition of the Borrower and/or Guarantor from signing any new Loanand/or Guarantee Agreement with the Bank Group.

Suspension of disbursements in respect of all Bank Group loans grantedto the Borrower and/or Guarantor.

Suspension of the granting of any new loans by the Bank Group to the

Borrower and/or Guarantor.

Application of the Cross-default sanction clause by virtue of which ADB

Group shall suspend in whole or in part the right of the Borrower or the Gua-

rantor to disbursement of Loan Funds because of a failure by the Borrower

or the Guarantor to perform any of its obligations under any Loan Agreement

or Guarantee Agreement concluded with ADB/ADF/NTF.

35

D e b t S e r v i c i n g H a n d b o o k - A f r i c a n D e v e l o p m e n t B a n k G r o u p

The borrower has unilateral right, by notice to the

Bank, to cancel without penalty any amount on

the loan not yet disbursed or the entire loan whether

or not the loan agreement has been signed except for

amounts for which the Bank Group has entered into a

special commitment. Cancellation by the borrower

takes effect at the latest sixty (60) days from the date

of receipt by the Bank of the cancellation request.

Similarly the Bank may, upon expiration of a three-

month notice period, cancel an amount of the loan.

The Bank may initiate a loan cancellation for any of the

following reasons:

• Renegotiated loan terms;

• Loan not signed after a period of 180 days from

approval date;

• No disbursements for over 2 years;

• Closing date expired;

• Project completed;

• Undisbursed balance below minimum threshold;

• Continuing suspension of disbursements;

• Mis-procurement;

For non-sovereign guaranteed operations, the criteria

for loans cancellation are defined in the loan agreement.

11. Cancellation procedures

Figure 10: Cancellation initiation and effective date

36

D e b t S e r v i c i n g H a n d b o o k - A f r i c a n D e v e l o p m e n t B a n k G r o u p

Article III of the General Conditions Applicable to

Loan and Guarantee Agreements provides for the

pre-payment of loans in advance of maturity.

Borrowers may prepay their loan at the expiration

of the prepayment notice period as provided for

in the loan agreement. In general, sovereign

guaranteed loans are subjected to a forty-five

days prepayment notice. Upon receipt of the

prepayment notice from the borrower, the Bank

calculates the amounts in principal and charges

that are due on the effective date of pre-payment.

Any undisbursed loan balance on the loan being

prepaid will be cancelled on the effective date of

prepayment. Other prepayment notice periods

may be specified in non-sovereign guaranteed

loan agreements.

A prepayment penalty that reflects the Bank’s

cost of re-deploying prepaid funds may be

applicable as provided for in the loan agreement.

12. Prepayment procedures

37

D e b t S e r v i c i n g H a n d b o o k - A f r i c a n D e v e l o p m e n t B a n k G r o u p

The Bank provides or makes available to

borrowers a set of reports for debt management

purposes. To facilitate and ensure the continuity of

such reporting, borrowers should promptly notify

the Bank of changes in their contact details.

In addition to the billing packages and payment

application reports, the Bank Group sends the

following reports to borrowers on a regular basis:

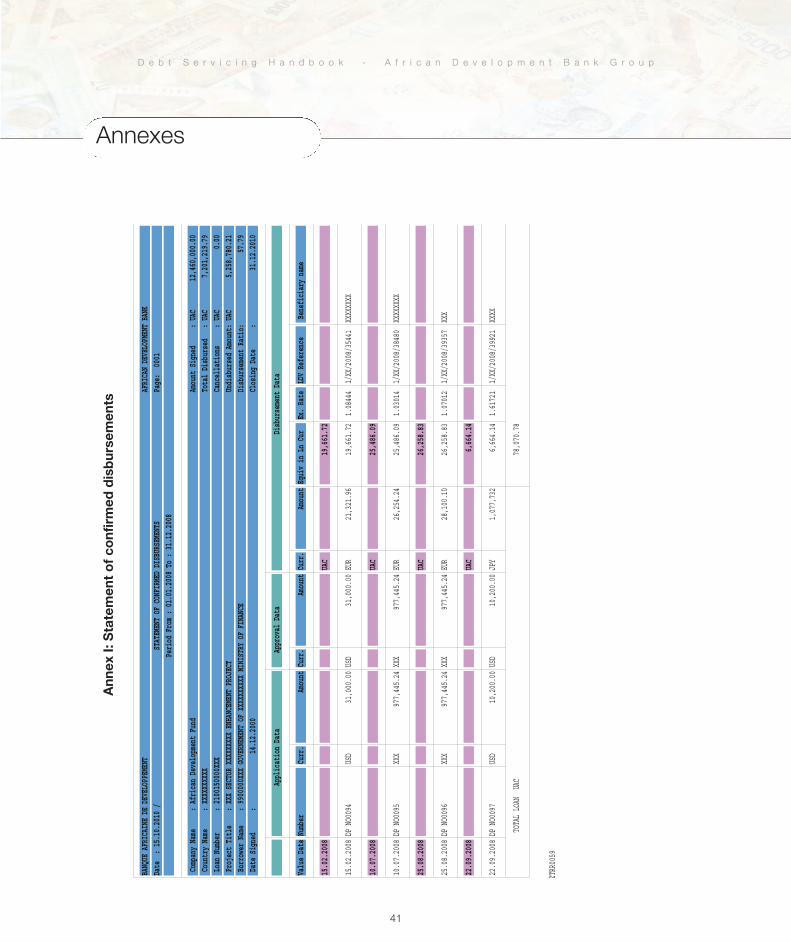

Statement of Confirmed Disbursements

The Statement of Confirmed Disbursements (See

Annex I) lists all disbursements made during the

month or any specified period. It also shows the

total disbursed in the loan currency, the undisbursed

balance on the loan as at the end of the specified

period and amounts cancelled, if any.

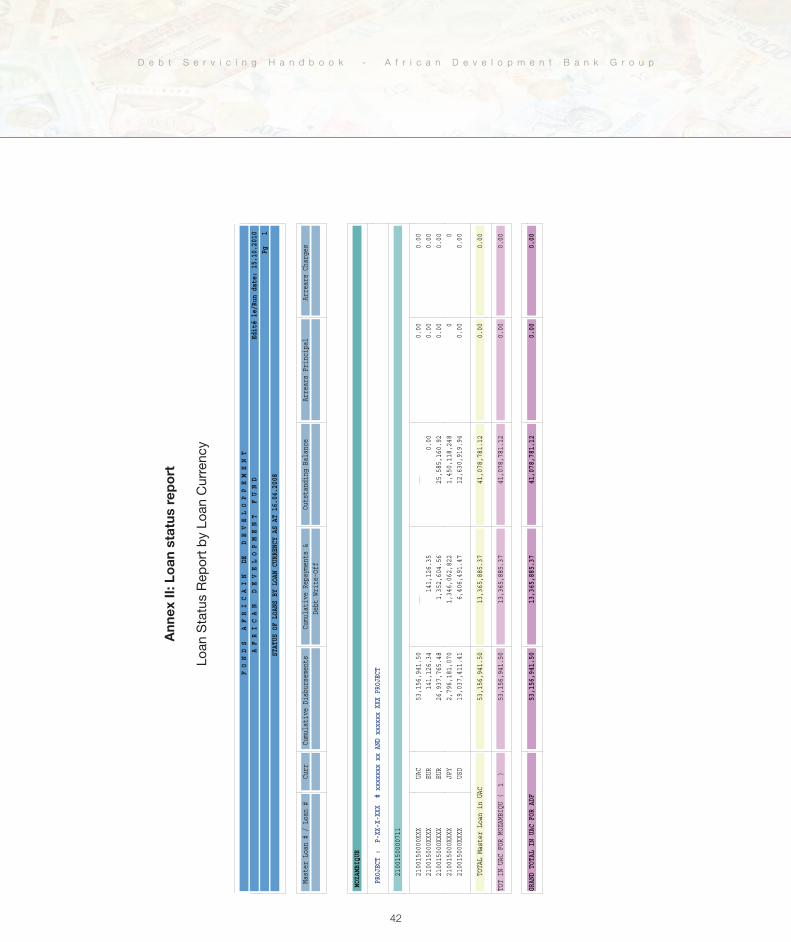

Loan Status Reports

The loan status reports (See Annex II) contain

information on the movements in borrowers’ loan

accounts as at a given date or for a specified period.

Generally, the following status reports are available:

• Loan Status report in loan currency as at a

particular date showing the cumulative

disbursements, repayments, the outstanding

loan balance and the arrears in principal and

charges when applicable.

• Loan Balance Confirmation report showing

cumulative disbursements, repayments in

principal and charges, and outstanding

balances as at a given date.

Planning-Related Information

This information is provided to borrowers and

executing agencies on demand and in accordance

with their specifications. Usually the information

required relates to consolidated basic loan data,

short and long range forecasts of debt service

payments and a summary of estimated debt service

payments.

13. Reports available to borrowers

38

D e b t S e r v i c i n g H a n d b o o k - A f r i c a n D e v e l o p m e n t B a n k G r o u p

Bibliography

39

D e b t S e r v i c i n g H a n d b o o k - A f r i c a n D e v e l o p m e n t B a n k G r o u p

Bibliography

General Conditions applicable to Loan, Guarantee and Grant Agreements of the

African Development Bank and the African Development Fund (February 2009)

ADB Loan Accounting, Billing and Recovery Handbook (April 1997)

Policy Relating to the Recovery of Arrears on Loans (May 1997)

Guidelines on Cancellation of ADB/ADF loans and grants (forthcoming – 2011)

Financial Products of the African Development Bank (June 2009)

Guidelines for Public Sector Loans (November 2000)

Enhancing Bank Support to Middle-Income Countries – Revised (February 2005)

Revised Financial Guidelines for Non-Sovereign Guaranteed Loans (February 2006)

Nigeria Trust Fund – Operational Guidelines (November 2008)

40

D e b t S e r v i c i n g H a n d b o o k - A f r i c a n D e v e l o p m e n t B a n k G r o u p

40

Annexes

41

D e b t S e r v i c i n g H a n d b o o k - A f r i c a n D e v e l o p m e n t B a n k G r o u p

AnnexesBANQUE AFRICAINE DE DEVELOPPEMENT

AFRICAN DEVELOPMENT BANK

Date : 15.10.2010 / STATEMENT OF CONFIRMED DISBURSEMENTS

Page: 0001

Period From : 01.01.2008 To : 31.12.2008

Company Name : African Development Fund

Amount Signed : UAC 12,460,000.00

Country Name : XXXXXXXXXX

Total Disbursed : UAC 7,201,219.79

Loan Number : 2100150000

XXX

Cancellations : UAC 0.00

Project Title :

XXX SECTOR XXXXXXXXX ENHANCEMENT PROJECT

Undisbursed Amount: UAC 5,258,780.21

Borrower Name : 9900000X

XX GOVERNEMENT OF XXXXXXXXXX

MINISTRY OF FINANCE

Disbursement Ratio: 57.79

Date Signed : 14.12.2000

Closing Date : 31.12.2010

Application Data

Approval Data

Disbursement Data

Value Date

Number

Curr.

Amount

Curr.

Amount

Curr.

Amount

Equiv in Ln Cur

Ex. Rate

LDV Reference

Beneficiary name

15.02.2008

UAC

19,661.72

15.02.2008

DP NO0094

USD

31,000.00

USD

31,000.00

EUR

21,321.96

19,661.72

1.08444

1/XX/2008/35441

XXXXXXXX

10.07.2008

UAC

25,486.09

10.07.2008

DP NO0095

XXX

977,445.24

XXX

977,445.24

EUR

26,254.24

25,486.09

1.03014

1/XX/2008/38480

XXXXXXXX

25.08.2008

UAC

26,258.83

25.08.2008

DP NO0096

XXX

977,445.24

XXX

977,445.24

EUR

28,100.10

26,258.83

1.07012

1/XX/2008/39357

XXX

22.09.2008

UAC

6,664.14

22.09.2008

DP NO0097

USD

10,200.00

USD

10,200.00

JPY

1,077,732

6,664.14

1.61721

1/XX/2008/39921

XXXX

TOTAL LOAN UAC

78,070.78

ZTRR0059

Ann

ex I:

Sta

tem

ent of co

nfirm

ed d

isbur

sem

ents

42

D e b t S e r v i c i n g H a n d b o o k - A f r i c a n D e v e l o p m e n t B a n k G r o u p

F O N D S A F R I C A I N DE D E V E L O P P E M E N T

A F R I C A N D E V E L O P M E N T F U N D

Edité le/Run date: 15.10.2010

Pg 1

STATUS OF LOANS BY LOAN CURRENCY AS AT 16.04.2008

Master Loan # / Loan #

Curr

Cumulative Disbursements

Cumulative Repayments &

Outstanding Balance

Arrears Principal

Arrears Charges

Debt Write-Off

MOZAMBIQUE

PROJECT : P-XX-X-XXX # xxxxxxx

xx AND xxxxxxXXXPROJECT

2100150000711

2100150000XXX

UAC

53,156,941.50

0.00

0.00

210015000XXXX

EUR

141,126.34

141,126.35

0.00

0.00

0.00

210015000X

XXX

EUR

26,937,765.48

1,352,604.56

25,585,160.92

0.00

0.00

210015000X

XXX

JPY

2,796,181,070

1,346,062,822

1,450,118,248

0

0

210015000X

XXX

USD

19,037,411.41

6,406,491.47

12,630,919.94

0.00

0.00

TOTAL Master Loan in UAC

53,156,941.50

13,365,885.37

41,078,781.12

0.00

0.00

TOT IN UAC FOR MOZAMBIQU ( 1 )

53,156,941.50

13,365,885.37

41,078,781.12

0.00

0.00

GRAND TOTAL IN UAC FOR ADF

53,156,941.50

13,365,885.37

41,078,781.12

0.00

0.00

Ann

ex II

: Loan

sta

tus re

port

Loan

Sta

tus

Rep

ort b

y Lo

an C

urre

ncy

43

D e b t S e r v i c i n g H a n d b o o k - A f r i c a n D e v e l o p m e n t B a n k G r o u p

Ann

ex II

: Loan

sta

tus re

port

Loan

Bal

ance

Con

firm

atio

n

44

D e b t S e r v i c i n g H a n d b o o k - A f r i c a n D e v e l o p m e n t B a n k G r o u p

Ann

ex II

I: Billin

g sta

tem

ents

Sta

tem

ent of

Bill

s D

ue b

y C

urre

ncy

45

D e b t S e r v i c i n g H a n d b o o k - A f r i c a n D e v e l o p m e n t B a n k G r o u p

Annex III: Billing statements

Statement of Single Currency Payment Option

46

D e b t S e r v i c i n g H a n d b o o k - A f r i c a n D e v e l o p m e n t B a n k G r o u p

Annex III: Billing statements

Account Statement

47

D e b t S e r v i c i n g H a n d b o o k - A f r i c a n D e v e l o p m e n t B a n k G r o u p

Statement of amount payable after HIPC relief

Annex III: Billing statements

Summary Loan Ledger

48

D e b t S e r v i c i n g H a n d b o o k - A f r i c a n D e v e l o p m e n t B a n k G r o u p

Annex IV: Repayment statement

Application of Incoming Payments Report

www.afdb.org

© 2

011

- AfD

B -

Des

ign,

Ext

erna

l Rel

atio

ns a

nd C

omm

unic

atio

n U

nit//J

KT

](https://img.dokumen.tips/doc/110x75/6203a3e2da24ad121e4bc066/handbook-of-statistics-on-central-government-debt596-kb.jpg)