Embed Size (px)

Citation preview

Debt Relief, Institutions and Growth in Poor Countries

Andrea F. PresbiteroE–mail: [email protected]

Homepage: www.dea.unian.it/presbitero/

1Universita Politecnica delle Marche

2Money and Finance Research group (MoFiR)

IMF – Research Department — Washington DC, March 27, 2009

AF Presbitero (Univpm) Debt, Institutions & Growth International Monetary Fund 1 / 32

Book project

Introduction

The presentation deals with external (and domestic) debt in poor countries.

It is based on two chapters of the book “Debt Relief Initiatives: PolicyDesign and Outcomes” (Arnone and Presbitero), forthcoming in theAshgate’s Global Finance series in 2009.

The book is an ex-post evaluation of the HIPC Initiative aimed at drawinguseful suggestions for debt reduction programs.

We recognize the great efforts made by the World Bank and the IMF andthe importance of the results achieved. However, we stress:

1 the potential sources of future distress, related to a rising domesticdebt in many HIPCs,

2 the critical role of institutions in shaping debt relief effectiveness(country specific approach),

3 the monitoring of the progresses in poverty reduction and economicgrowth (it is probably to soon to draw conclusions)

AF Presbitero (Univpm) Debt, Institutions & Growth International Monetary Fund 2 / 32

Book project

The book: “Debt Relief Initiatives: Policy Design and Outcomes”

1 The Building Blocks

The IMF-WB HIPC Initiative: Description and IssuesExternal Debt Sustainability: Theory and Approaches

2 HIPC/LIC and Macroeconomic Management

Money and Interest Rates: The Missing Link of Fiscal AdjustmentDomestic Debt in Developing Countries and in HIPCsDomestic Debt and Debt Sustainability

3 Macroeconomic Performance, Poverty and Social Indicators

External Debt and Growth: Mixed EvidenceAn Empirical ApplicationAn Ex-post Evaluation of Debt Relief

4 From HIPCs to the Least Income Countries Initiative and beyond.

A Comprehensive Approach to Debt SustainabilityThe Role of Institutions: Governance ConditionalityCoordination Issues, Responsible Lending and Vulture FundsSuggestions for Debt Relief Programs

AF Presbitero (Univpm) Debt, Institutions & Growth International Monetary Fund 3 / 32

Book project

1 Book project

2 The Debt-Growth Nexus in Poor Countries: A ReassessmentAim and related literatureData and MethodologyResultsConclusions

3 Debt Relief Effectiveness and Institution BuildingAim and related literatureThe determinants of debt reliefThe outcomesConclusions

AF Presbitero (Univpm) Debt, Institutions & Growth International Monetary Fund 4 / 32

The Debt-Growth Nexus in Poor Countries: A Reassessment Aim and related literature

Aim and motivations

The large costs of debt relief programs require sound evidence on the growtheffect of debt reduction.

Recent research raised some concerns on high debt being a real constraint toeconomic growth and social expenditures in poor countries.

The paper directly investigates the role played by institutions and policies inthe debt-growth nexus, building on the hypothesis that this relationshipcould differ according to countries’ specific characteristics (Cordella et al2005).

AF Presbitero (Univpm) Debt, Institutions & Growth International Monetary Fund 5 / 32

The Debt-Growth Nexus in Poor Countries: A Reassessment Aim and related literature

Theoretical underpinnings

The rationale for a negative correlation between external debt and economicgrowth is related to:

1 debt overhang (Krugman 1988; Sachs 1989; Koeda 2008 explicitly forLICs), even if:

net positive resource transfers reduce the disincentive effect ofdebt (Bird and Milne 2003) andweak economic institutions and infrastructure represent the majorhindrance to investment in HIPCs (Arslanalp and Henry 2006)

2 macroeconomic uncertainty which generates a misallocation ofresources (short-termism and “waiting” option) and reduce theefficiency and productivity of capital.

3 disincentive on investments in human capital and on the government’swillingness to adopt structural reforms (Sachs 2002, Vamvakidis 2007).

AF Presbitero (Univpm) Debt, Institutions & Growth International Monetary Fund 6 / 32

The Debt-Growth Nexus in Poor Countries: A Reassessment Aim and related literature

Empirical evidence

The evidence on debt overhang (Elbadawi et al 1997; Pattillo et al 2002,2004; Clements et al 2003) lacks robustness (Moss and Chiang 2003;Chauvin and Kraay 2005): the main issue to deal with is the direction ofcausality (Easterly 2001 and Lane 2004).

Debt irrelevance above a certain (country-specific) debt threshold(Cordella et al 2005).

The negative relationship between debt and growth could be driven byomitted time invariant country characteristics (Imbs and Ranciere 2008).

The paper controls for a time variant institutional indicator, interacting itwith debt indicators in order to find out a possible source of heterogeneity.

AF Presbitero (Univpm) Debt, Institutions & Growth International Monetary Fund 7 / 32

The Debt-Growth Nexus in Poor Countries: A Reassessment Data and Methodology

The dataset

The dataset covers 114 low- and middle-income countries over the period1980–2004. The main sources are the WDI, the GDF and the WEO.

External debt is measured in net present value terms (Dikhanov 2004) as aratio over GDP or exports (denominators are filtered to reduce reversecausality (Easterly 2001; Cordella et al 2005)).

The quality of policies and institutions is measured by the Country Policyand Institutional Assessments (CPIA) indicator (results comparable to theWorld Bank-IMF DSF country-specific debt burden thresholds).

Data are averaged over non-overlapping five years periods.

AF Presbitero (Univpm) Debt, Institutions & Growth International Monetary Fund 8 / 32

The Debt-Growth Nexus in Poor Countries: A Reassessment Data and Methodology

Methodology

The dynamic growth model is estimated with the two-step System-GMMadopting the Windmeijer’s (2005) finite-sample correction:

GROWTHi,t = αGDPi,t−1 + Xi,tβ′ + δ1DEBTi,t + δ2DEBT 2

i,t + ηi + τt + εi,t

where DEBT is alternatively the ratio of the NPV of external debt over(filtered) GDP or exports, X is a vector of controls including investment,population growth, schooling, openness, the variability of inflation, andterms of trade; ηi are country-specific time invariant effects (six regionaldummies); τt are times fixed effects.

This basic setup is augmented including:

1 the institutional indicator (CPIA, continuous or categorical),2 interacting the debt indicators with the institutional one.

AF Presbitero (Univpm) Debt, Institutions & Growth International Monetary Fund 9 / 32

The Debt-Growth Nexus in Poor Countries: A Reassessment Results

External Debt, GDP Growth and Level, by Institutional Quality

Institutions NPV Real pc Real Aid/GDP Obs.(CPIA index) Debt/GDP GDP growth GDP pc

Weak 62.80 -0.04 959 10.30 120Medium 49.23 1.77 1,222 10.75 125Strong 35.47 2.83 2,347 4.67 133

Whole sample 48.70 1.57 1,534 8.48 378

Institutions matter

the negative correlation between external debt and economic growth could bedriven by the role played by institutions and policies, which are associated with alower external debt and higher growth rates.

AF Presbitero (Univpm) Debt, Institutions & Growth International Monetary Fund 10 / 32

The Debt-Growth Nexus in Poor Countries: A Reassessment Results

NPV of PPG External Debt over GDP, Two-Step System–GMM

Dep. Var.: GROWTH (1) (2) (3) (4) (5) (6)

(DEBT/GDP) 2.415** 1.583 1.931* -0.027 0.035 4.605**[1.232] [1.659] [1.098] [0.465] [0.470] [2.099]

(DEBT/GDP)2 -0.487*** -0.310 -0.664**[0.170] [0.222] [0.276]

CPIA 1.112*** 3.630***[0.315] [1.164]

(DEBT/GDP) × CPIA -0.690**[0.306]

Good CPIA (0,1) 7.613*** 16.493***[2.011] [5.889]

(DEBT/GDP) × Good CPIA -1.649*** -7.002**[0.537] [3.234]

(DEBT/GDP)2 × Good CPIA 0.760*[0.430]

Omitted categories: Weak CPIA and (DEBT/GDP) × Weak CPIA

Medium CPIA (0,1) 5.484***[1.996]

Strong CPIA (0,1) 8.031***[2.217]

(DEBT/GDP) × Medium CPIA -1.189**[0.505]

(DEBT/GDP) × Strong CPIA -1.616***[0.574]

Observations 378 378 378 378 378 378Number of countries 110 110 110 110 110 110

AF Presbitero (Univpm) Debt, Institutions & Growth International Monetary Fund 11 / 32

The Debt-Growth Nexus in Poor Countries: A Reassessment Results

Results

The debt-growth relationship follows a debt Laffer curve (col 1), whosemaximum is in correspondence of a ratio of NPV of external debt over GDPequals to 11 (very similar to the ones estimated by Pattillo et al (2002) andCordella et al (2005)).

The inclusion of the CPIA index (col 2) makes the relationship between debtand growth no more significant.

The marginal impact of external debt to economic growth is positive whenthe CPIA index is low and turns negative for larger values (col 3).

Large debts impinge on economic growth in countries with medium andstrong policies (col 5).

Institutions matter for the debt-growth nexus

The debt Laffer curve looses significance when policies are taken into account,suggesting that institutional quality could be a common determinant of both lowgrowth and high debt.

AF Presbitero (Univpm) Debt, Institutions & Growth International Monetary Fund 12 / 32

The Debt-Growth Nexus in Poor Countries: A Reassessment Results

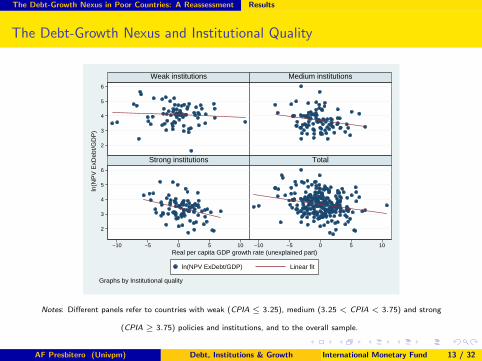

The Debt-Growth Nexus and Institutional Quality

2

3

4

5

6

2

3

4

5

6

−10 −5 0 5 10 −10 −5 0 5 10

Weak institutions Medium institutions

Strong institutions Total

ln(NPV ExDebt/GDP) Linear fit

ln(N

PV

ExD

ebt/G

DP

)

Real per capita GDP growth rate (unexplained part)

Graphs by Institutional quality

Notes: Different panels refer to countries with weak (CPIA ≤ 3.25), medium (3.25 < CPIA < 3.75) and strong

(CPIA ≥ 3.75) policies and institutions, and to the overall sample.

AF Presbitero (Univpm) Debt, Institutions & Growth International Monetary Fund 13 / 32

The Debt-Growth Nexus in Poor Countries: A Reassessment Results

The economic impact of debt on growth

A reduction in the ratio of the NPV of external debt over GDP from 60 to20 per cent is associated with an increase in the GDP growth rate of 1.06(1.42) in countries with medium (strong) institutions.

The effect is almost nil and statistically not significant in countries with aweak institutional framework.

In those countries, economic growth is likely to be constrained by otherfactors, and positive net resource transfers (aid flows as a share of GDP aremore than twice larger than in countries with strong institutions) could helpreduce the crowding out of public investment (Cordella et al 2005).

AF Presbitero (Univpm) Debt, Institutions & Growth International Monetary Fund 14 / 32

The Debt-Growth Nexus in Poor Countries: A Reassessment Results

Robustness

Partial correlation between debt and growth depends on the choice betweencontemporaneous, initial or lagged debt ratios (Depetris Chauvin and Kraay2005).

Reverse causality is addressed taking lagged debt ratios instead ofcontemporaneous ones and results are broadly consistent.

Results are generally robust to:

1 nominal external debt (scaled by GDP or exports).2 a reduction in the number of instruments (Roodman 2007).3 changes in the set of control variables, including M2, secondary

education, income classification, a dummy for HIPCs, and the ratios oftotal debt service and official aid over GDP.

AF Presbitero (Univpm) Debt, Institutions & Growth International Monetary Fund 15 / 32

The Debt-Growth Nexus in Poor Countries: A Reassessment Results

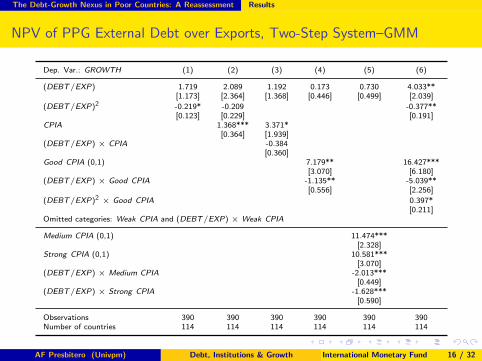

NPV of PPG External Debt over Exports, Two-Step System–GMM

Dep. Var.: GROWTH (1) (2) (3) (4) (5) (6)

(DEBT/EXP) 1.719 2.089 1.192 0.173 0.730 4.033**[1.173] [2.364] [1.368] [0.446] [0.499] [2.039]

(DEBT/EXP)2 -0.219* -0.209 -0.377**[0.123] [0.229] [0.191]

CPIA 1.368*** 3.371*[0.364] [1.939]

(DEBT/EXP) × CPIA -0.384[0.360]

Good CPIA (0,1) 7.179** 16.427***[3.070] [6.180]

(DEBT/EXP) × Good CPIA -1.135** -5.039**[0.556] [2.256]

(DEBT/EXP)2 × Good CPIA 0.397*[0.211]

Omitted categories: Weak CPIA and (DEBT/EXP) × Weak CPIA

Medium CPIA (0,1) 11.474***[2.328]

Strong CPIA (0,1) 10.581***[3.070]

(DEBT/EXP) × Medium CPIA -2.013***[0.449]

(DEBT/EXP) × Strong CPIA -1.628***[0.590]

Observations 390 390 390 390 390 390Number of countries 114 114 114 114 114 114

AF Presbitero (Univpm) Debt, Institutions & Growth International Monetary Fund 16 / 32

The Debt-Growth Nexus in Poor Countries: A Reassessment Conclusions

Main result and its policy implications

Institutions matter. Debt relief is likely to be effective only in countrieswith sound institutions (Dessy and Vencatachellum 2007; Harrabi et al2007).

Debt relief policies should avoid one-size-fits-all programs and be tailored tocountry-specific characteristics, as already done in the DSF.

Debt cancelation conditional upon an actual improvements in institutionalquality (governance conditionality) could act as a strong incentive forrecipients to strengthen institutions and policies (Collier 2007).

This analysis has many limitations and has to be complemented with thedirect assessment of debt relief effectiveness.

Finally, debt relief could be motivated by other considerations (i.e. odiousdebt, a signalling–endorsement effect).

AF Presbitero (Univpm) Debt, Institutions & Growth International Monetary Fund 17 / 32

Debt Relief Effectiveness and Institution Building Aim and related literature

Aim of the paper

$100 billion in debt relief granted by donors to LIC between 1989 and 2003had a very limited effect on public spending, investment and growth(Depetris Chauvin and Kraay 2005).

This paper moves from the conclusion of the previous one and aims at:

1 identify the determinants of debt relief,2 directly assessing the effectiveness of debt relief on different

macroeconomic outcomes.

The focus in on institutions and policies to evaluate whether donors arerewarding institution building and to what extent debt relief is associatedwith subsequent improvements in the institutional framework.

AF Presbitero (Univpm) Debt, Institutions & Growth International Monetary Fund 18 / 32

Debt Relief Effectiveness and Institution Building Aim and related literature

The rationale for debt relief

Debt overhang and crowding out are two arguments in favor of debt relief(but the empirical evidence is inconclusive (Rajan 2005)).

However, debt relief could not necessarily trigger growth and developmentbecause:

1 debt relief curse: aid dependence could undermine institutional quality(Knack 2001; Moss et al 2006; and, in contrast, Kanbur 2000),

2 debt relief has a minimal impact on HIPCs’ net resource transfers(Arslanalp and Henry 2006),

3 large external debt might be a signal of a high (and stable over time)discount rate against the future (Easterly 2002).

Multilateral debt relief could partially overcome these problems and debtrelief would become more effective with time (learning by doing).

AF Presbitero (Univpm) Debt, Institutions & Growth International Monetary Fund 19 / 32

Debt Relief Effectiveness and Institution Building The determinants of debt relief

Model and data

Debt relief consists in (1) the selection of eligible countries and (2) thechoice of the amount of debt reduction (Freytag and Pehnelt 2009).

The determinants of debt relief are estimated using a two-step model a laHeckman where:

1 in the selection equation, the probability of receiving debt relief isfunction of the past debt relief, aid inflows, real GDP per capita, debtservice, the NPV of external debt, CPIA, a dummy for HIPCs, and thestatus of former colony;

2 in the outcome equation the amount of debt relief is function of pastlevels of aid, total debt service, external debt and CPIA.

The dataset covers 62 developing countries over the period 1988-2007 andmerges WDI data with other datasets on debt relief (Depetris Chauvin andKraay 2005), external (Dikhanov 2004) and domestic debt (Abbas 2007),and institutions (CPIA, WGI).

AF Presbitero (Univpm) Debt, Institutions & Growth International Monetary Fund 20 / 32

Debt Relief Effectiveness and Institution Building The determinants of debt relief

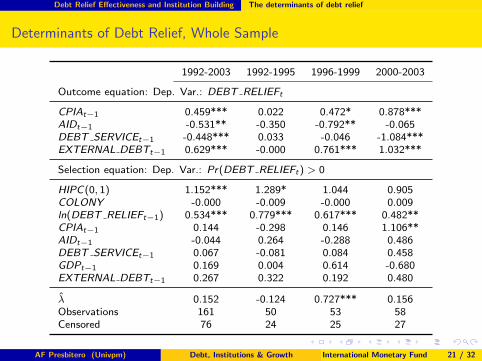

Determinants of Debt Relief, Whole Sample

1992-2003 1992-1995 1996-1999 2000-2003

Outcome equation: Dep. Var.: DEBT RELIEFt

CPIAt−1 0.459*** 0.022 0.472* 0.878***AIDt−1 -0.531** -0.350 -0.792** -0.065DEBT SERVICEt−1 -0.448*** 0.033 -0.046 -1.084***EXTERNAL DEBTt−1 0.629*** -0.000 0.761*** 1.032***

Selection equation: Dep. Var.: Pr(DEBT RELIEFt) > 0

HIPC(0, 1) 1.152*** 1.289* 1.044 0.905COLONY -0.000 -0.009 -0.000 0.009ln(DEBT RELIEFt−1) 0.534*** 0.779*** 0.617*** 0.482**CPIAt−1 0.144 -0.298 0.146 1.106**AIDt−1 -0.044 0.264 -0.288 0.486DEBT SERVICEt−1 0.067 -0.081 0.084 0.458GDPt−1 0.169 0.004 0.614 -0.680EXTERNAL DEBTt−1 0.267 0.322 0.192 0.480

λ 0.152 -0.124 0.727*** 0.156Observations 161 50 53 58Censored 76 24 25 27

AF Presbitero (Univpm) Debt, Institutions & Growth International Monetary Fund 21 / 32

Debt Relief Effectiveness and Institution Building The determinants of debt relief

Results

1 Debt relief is path dependent (Michaelowa 2003).

2 Donors grant debt relief to countries which are most in need and with lowrepayment capacity.

3 In correspondence of the HIPC Initiative, donors changed behavior, choosingthe eligible countries and the amount of debt relief on the basis of the qualityof policies and institutions, rewarding the countries with better governance

4 The increased influence of the IMF and the World Bank is partially divertingdonors’ decisions from political considerations (Dollar and Levin 2006).

5 Results are similar for the sub-sample of HIPCs and hold even using the WGI.

AF Presbitero (Univpm) Debt, Institutions & Growth International Monetary Fund 22 / 32

Debt Relief Effectiveness and Institution Building The outcomes

Debt relief delivered: an assessment

Given its cost, debt relief deserves a careful scrutiny about its effectiveness.

On aggregate, the HIPC Initiative and the MDRI have been successful inrelaxing the budget balance and increasing poverty reduction expenditures.

However, the situation at country level is heterogeneous, with countries thatstill face harsh financing constraints and have limited poverty-reducingexpenditures.

More resources and poverty reduction expenditures are not necessarilycorrelated with improvements in the welfare of the poor (Gomanee et al2005; Weiss 2008) and HIPCs are still far away from the achievements of theMDGs (Unctad 2006)

Expectations should be realistic: Tanzania, Ghana and Uganda need around15% of GDP in external financing to fund the MDGs (Sachs et al 2004),while debt relief counts for less than 3%.

AF Presbitero (Univpm) Debt, Institutions & Growth International Monetary Fund 23 / 32

Debt Relief Effectiveness and Institution Building The outcomes

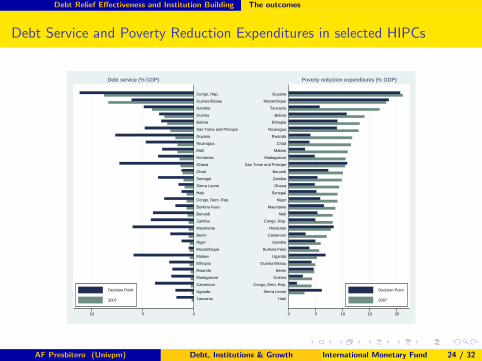

Debt Service and Poverty Reduction Expenditures in selected HIPCs

0510

Tanzania

Uganda

Cameroon

Madagascar

Rwanda

Ethiopia

Malawi

Mozambique

Niger

Benin

Mauritania

Zambia

Burundi

Burkina Faso

Congo, Dem. Rep.

Haiti

Sierra Leone

Senegal

Chad

Ghana

Honduras

Mali

Nicaragua

Guyana

Sao Tome and Principe

Bolivia

Guinea

Gambia

Guinea Bissau

Congo, Rep.

Debt service (% GDP)

Decision Point

2007

0 5 10 15 20

Haiti

Sierra Leone

Congo, Dem. Rep.

Guinea

Benin

Guinea Bissau

Uganda

Burkina Faso

Gambia

Cameroon

Honduras

Congo, Rep.

Mali

Mauritania

Niger

Senegal

Ghana

Zambia

Burundi

Sao Tome and Principe

Madagascar

Malawi

Chad

Rwanda

Nicaragua

Ethiopia

Bolivia

Tanzania

Mozambique

Guyana

Poverty reduction expenditures (% GDP)

Decision Point

2007

AF Presbitero (Univpm) Debt, Institutions & Growth International Monetary Fund 24 / 32

Debt Relief Effectiveness and Institution Building The outcomes

Previous studies

In general, results are rather disappointing: there is weak evidencesupporting a positive impact on public and social spending, investment andgrowth rates (Depetris Chauvin and Kraay 2005; Johansson 2008; Cuaresmaand Vincelette 2008).

Focusing on Africa and considering the role of institutions provide betterresults: in countries with good (or improving) institutional quality, debtreduction is associated with an increase in the the share of country’sexpenditures allocated either to public education or health (Dessy andVencatachellum 2007) and in the credit to the private sector (Harrabi et al2007).

AF Presbitero (Univpm) Debt, Institutions & Growth International Monetary Fund 25 / 32

Debt Relief Effectiveness and Institution Building The outcomes

Empirical strategy

The main hypothesis to test would be the actual impact of debt relief onpoverty reduction, but this is not possible at this stage.

Debt relief effectiveness is assessed indirectly, focusing on differentmacroeconomic indicators (Y ) which are related to economic development:

1 real per capita GDP growth,2 the investment rate,3 foreign direct investments over GDP,4 domestic debt over GDP5 the quality of policies and institutions

Empirically, data are averaged over four non-overlapping five years periods(1988-91; 1992-95; 1996-99; 2000-03; 2004-07) and the following equationis estimated with the within-group estimator:

Yi,t − Yi,t−1 = α + β · DEBT RELIEFt−1 + γDt + εi,t

AF Presbitero (Univpm) Debt, Institutions & Growth International Monetary Fund 26 / 32

Debt Relief Effectiveness and Institution Building The outcomes

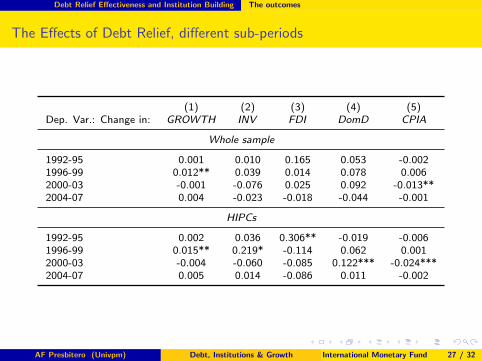

The Effects of Debt Relief, different sub-periods

(1) (2) (3) (4) (5)Dep. Var.: Change in: GROWTH INV FDI DomD CPIA

Whole sample

1992-95 0.001 0.010 0.165 0.053 -0.0021996-99 0.012** 0.039 0.014 0.078 0.0062000-03 -0.001 -0.076 0.025 0.092 -0.013**2004-07 0.004 -0.023 -0.018 -0.044 -0.001

HIPCs

1992-95 0.002 0.036 0.306** -0.019 -0.0061996-99 0.015** 0.219* -0.114 0.062 0.0012000-03 -0.004 -0.060 -0.085 0.122*** -0.024***2004-07 0.005 0.014 -0.086 0.011 -0.002

AF Presbitero (Univpm) Debt, Institutions & Growth International Monetary Fund 27 / 32

Debt Relief Effectiveness and Institution Building The outcomes

Debt Relief and the Subsequent Institutional Framework, WGI

BDI

BENBFA

BOLCAF

CIV

CMRCOG

COM

ERI

ETHGHA

GINGMB

GNBGUY

HND

HTI

KGZ

LBR

MDGMLI

MOZ

MRT

MWI NER

NICNPL

RWASDN

SEN

SLE

SOMSTPTCD

TGOTZA

UGA

ZAR

ZMB BDI BEN

BFA

BOLCAF

CIV

CMRCOGCOM

ERI

ETH

GHA

GINGMBGNBGUY

HNDHTI

KGZ

LBR

MDG

MLI MOZ

MRT

MWINER

NIC

NPL

RWA

SDNSEN SLE

SOMSTP

TCDTGO

TZA

UGA ZARZMB

−1

−.5

0.5

0 20 40 60 0 20 40 60

2000−2003 2004−2007

Cha

nge

betw

een

t and

t−1

Debt relief at time t−1

Corruption index

BDIBEN

BFABOL

CAFCIV

CMRCOGCOM

ERI

ETH

GHAGIN

GMB

GNB

GUY

HND

HTI

KGZ

LBR

MDG

MLIMOZ

MRT

MWI NER

NICNPL

RWA

SDNSEN

SLE

SOM

STPTCD

TGO

TZAUGA

ZAR

ZMB

BDI

BEN

BFA

BOL

CAF

CIV

CMRCOG

COM

ERI

ETHGHA

GINGMB

GNBGUY

HNDHTI

KGZ

LBR

MDGMLI MOZ

MRT

MWI

NER NIC

NPL

RWA

SDNSEN

SLE

SOM

STP

TCDTGO

TZAUGA ZAR

ZMB

−.5

0.5

0 20 40 60 0 20 40 60

2000−2003 2004−2007

Cha

nge

betw

een

t and

t−1

Debt relief at time t−1

Rule of law index

BDI

BEN

BFA

BOL

CAF CIV

CMRCOG

COM

ERIETH

GHA

GIN

GMB

GNB

GUYHND

HTIKGZLBR MDG

MLI MOZMRT

MWI

NER

NIC

NPL

RWA

SDNSENSLESOM

STPTCD

TGO

TZA

UGA

ZARZMB

BDI

BENBFABOL

CAFCIV

CMRCOGCOM

ERI

ETH

GHAGIN

GMB

GNB

GUY

HNDHTI

KGZ

LBR

MDG MLI MOZ

MRT

MWINER NIC

NPL

RWA

SDNSEN

SLE

SOM STPTCD

TGO TZA

UGA

ZARZMB

−.5

0.5

1

0 20 40 60 0 20 40 60

2000−2003 2004−2007

Cha

nge

betw

een

t and

t−1

Debt relief at time t−1

Voice and accountability index

BDI BEN

BFA

BOLCAF

CIV

CMR

COGCOMERI

ETHGHAGIN

GMBGNB

GUYHND

HTIKGZ

LBRMDGMLI

MOZMRTMWI

NERNIC

NPL

RWASDN

SEN

SLE

SOMSTPTCD

TGO

TZA

UGAZARZMB

BDI

BENBFA

BOL

CAF

CIV

CMR

COG

COMERI

ETHGHA

GINGMB GNBGUYHNDHTI

KGZ

LBRMDG

MLI MOZ

MRT

MWI

NER

NIC

NPL

RWA

SDNSEN

SLE

SOMSTP

TCD

TGO

TZAUGA ZARZMB

−1

−.5

0.5

0 20 40 60 0 20 40 60

2000−2003 2004−2007

Cha

nge

betw

een

t and

t−1

Debt relief at time t−1

Government effectiveness index

BDIBEN

BFA BOL

CAF

CIV

CMRCOG

COM

ERI ETH

GHAGIN

GMB

GNB

GUY

HNDHTI

KGZ

LBR MDGMLI

MOZ

MRTMWI

NER

NIC

NPL

RWA

SDNSEN

SLE

SOM

STPTCD

TGO

TZA UGA

ZAR ZMB

BDI

BEN

BFA

BOL

CAF

CIV

CMRCOGCOMERI

ETH

GHA

GINGMB

GNBGUYHND

HTI

KGZ

LBR

MDG MLIMOZ

MRT

MWI

NERNIC

NPL

RWA

SDNSEN

SLE

SOM

STPTCD

TGO

TZAUGA

ZAR

ZMB

−1

01

0 20 40 60 0 20 40 60

2000−2003 2004−2007

Cha

nge

betw

een

t and

t−1

Debt relief at time t−1

Political stability index

BDI

BEN

BFA

BOLCAF CIV

CMRCOGCOM

ERI

ETH

GHA

GIN

GMB

GNB GUYHND

HTIKGZ

LBR

MDG

MLI

MOZMRT

MWI

NER

NICNPL

RWASDN

SEN

SLE

SOM

STPTCD

TGO

TZA UGA

ZAR

ZMB

BDIBEN

BFA

BOL

CAF

CIV

CMRCOGCOM

ERI

ETHGHA

GINGMB GNBGUYHNDHTI

KGZ

LBRMDG

MLIMOZMRTMWI

NERNICNPL

RWASDN

SEN

SLE

SOMSTPTCDTGO

TZAUGA

ZAR

ZMB

−1

−.5

0.5

1

0 20 40 60 0 20 40 60

2000−2003 2004−2007

Cha

nge

betw

een

t and

t−1

Debt relief at time t−1

Regulatory quality index

AF Presbitero (Univpm) Debt, Institutions & Growth International Monetary Fund 28 / 32

Debt Relief Effectiveness and Institution Building The outcomes

Results

1 On the whole, debt relief seems to be ineffective, but this is due to timeheterogeneity.

2 Since the end of the nineties, debt relief is associated with increasingdomestic financing and worsening governance in HIPCs.

3 The lack of significance of any shift from external to internal financing inthe last period could be due to poor data availability, while the lack ofevidence of a debt relief curse could be a signal of an increased effectivenessof debt relief in institution building.

4 From 2000 onwards there is no evidence of debt relief triggering economicgrowth (debt overhang).

5 There is no evidence of debt relief (1) having a differentiated impactaccording to institutional quality and (2) being less effective the larger theamount of foreign aid because of the increased management effort requiredto local bureaucrats and of a sort of aid fatigue.

AF Presbitero (Univpm) Debt, Institutions & Growth International Monetary Fund 29 / 32

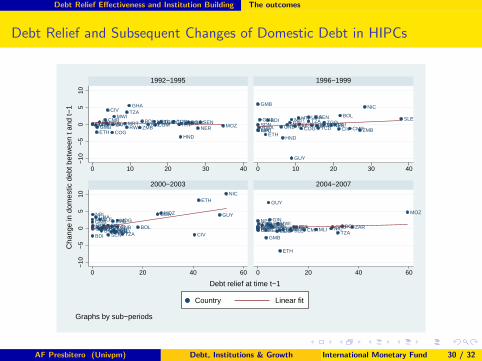

Debt Relief Effectiveness and Institution Building The outcomes

Debt Relief and Subsequent Changes of Domestic Debt in HIPCs

BDI BENBFABOLCAF

CIV

CMR

COG

COMETH

GHA

GINGMBGNB GUY

HND

HTIMDGMLI

MOZMRTMWI

NERNICNPL RWASDN SENSLE TCDTGO

TZA

UGAZARZMB

BDIBENBFA

BOL

CAF CIV CMRCOGCOM

ETH

GHA GIN

GMB

GNB

GUY

HND

HTIMDG MLIMOZ

MRT

MWINER

NIC

NPLRWASDN

SEN SLE

TCDTGOTZA

UGA

ZMB

BDIBENBFA

BOLCAF

CIVCMRCOG

COM

ETH

GHA

GINGMB

GNB

GUY

HNDHTIMDG

MLI

MOZ

MRT

MWI

NER

NIC

NPL

RWASDN

SEN

SLE

TCDTGOTZA

UGAZMB

BDIBEN BFA BOL

CAF CIV CMRCOGCOM

ETH

GHA

GIN

GMB

GNB

GUY

HNDHTI MDG MLI

MOZ

MWINER NIC

NPLSDN

SEN SLETCDTGO

TZAUGA ZARZMB

−10

−5

05

10−

10−

50

510

0 10 20 30 40 0 10 20 30 40

0 20 40 60 0 20 40 60

1992−1995 1996−1999

2000−2003 2004−2007

Country Linear fit

Cha

nge

in d

omes

tic d

ebt b

etw

een

t and

t−1

Debt relief at time t−1

Graphs by sub−periods

AF Presbitero (Univpm) Debt, Institutions & Growth International Monetary Fund 30 / 32

Debt Relief Effectiveness and Institution Building The outcomes

Debt relief and domestic debt (Arnone and Presbitero 2007)

The rising domestic debt in many HIPCs may be an unintended consequenceof the HIPC Initiative.

The program was successful in bringing inflation under control but largeprimary deficits persisted and kept deteriorating through the nineties.

The lack of access to international capital markets and of adequate inflowsof concessional loans are forcing many HIPCs to recur do domestic marketsto tap their financing gap.

The shift from external to domestic financing is likely to undermine theoverall public debt sustainability and is particularly costly, leading to thecrowding out of private sector investment (Christensen 2005; by contrast,Harrabi et al (2007) show that debt relief enhance credit to private sector).

Some of the countries which have low (or declining) poverty reductionexpenditures are also the ones with high or rising domestic debt.

AF Presbitero (Univpm) Debt, Institutions & Growth International Monetary Fund 31 / 32

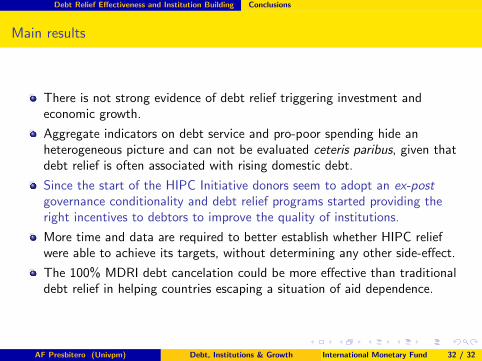

Debt Relief Effectiveness and Institution Building Conclusions

Main results

There is not strong evidence of debt relief triggering investment andeconomic growth.

Aggregate indicators on debt service and pro-poor spending hide anheterogeneous picture and can not be evaluated ceteris paribus, given thatdebt relief is often associated with rising domestic debt.

Since the start of the HIPC Initiative donors seem to adopt an ex-postgovernance conditionality and debt relief programs started providing theright incentives to debtors to improve the quality of institutions.

More time and data are required to better establish whether HIPC reliefwere able to achieve its targets, without determining any other side-effect.

The 100% MDRI debt cancelation could be more effective than traditionaldebt relief in helping countries escaping a situation of aid dependence.

AF Presbitero (Univpm) Debt, Institutions & Growth International Monetary Fund 32 / 32