Embed Size (px)

Citation preview

Dealing with a DeficitKey challenges in dealing with a pension deficit in today’s economic climate

Pension Deficit Survey 2009

Special Report

Hewitt Associates Limited i Dealing with Pension Deficit Survey 2009

Contents

Executive Summary 1 About the Survey 2 Valuations and Increasing Deficits 3 Dealing with Increasing Deficits 5 Using Alternative Financing 9 Actions and Considerations for Alternative Financing 13

Hewitt Associates Limited 1 Dealing with Pension Deficit Survey 2009

Executive Summary

In early summer 2009 we surveyed employers and trustees in the UK on how pension deficits are being dealt with, capturing actions that are being taken, or being considered. We received 152 responses from a mixture of trustees and corporate sponsors of pension schemes. Increased Deficits An overwhelming number of our respondents (nearly 90%) anticipated higher scheme funding deficits at their next actuarial valuation. The increased deficits were expected to be caused by a combination of poor asset performance (major declines in the equity markets), increasing life expectancy and falling "real" discount rate assumptions (where funding is measured using gilt yields rather than corporate bond yields). Just over half of the respondents, both trustee and corporate, anticipated that these headline deficits would lead to higher contributions than the employer could reasonably afford. Tackling the Deficit Extending the length of the recovery plan was seen by both corporate (79%) and trustee (97%) respondents as the best action to take when considering the most affordable way of funding the expected increase in deficit. Other actions considered included: ■ Implementing liability reduction exercises, including closing the scheme to future accruals or changing early

retirement benefits (corporate 65%, trustee 63%). ■ Allowing for asset outperformance within the recovery plan (50% corporate, 36% trustee). ■ Use of alternative financing, including providing a parental company guarantee, granting the pension scheme a

charge over contingent assets, or using negative pledges to maintain covenant strength through the employer committing to not undertake certain actions without prior consultation with the trustees (38% corporate, 31% trustee).

■ Reduce the level of prudence included in technical provisions (26% corporate, 17% trustee). More detail on alternative financing Managing cashflows as a result of higher funding deficits was not the only reason identified for using alternative financing. Half of our respondents were already using some form of alternative financing. In the future over 80% of respondents anticipate using alternative financing for one reason or another. Currently, a parental guarantee is the most used alternative finance solution (34%) – more than all of the other types of alternative financing solutions combined. It is the least complex and least costly solution to implement, and it is often used to support a reduction in the PPF levy paid by the scheme. Placing charges over company assets, e.g. property is expected to be the preferred solution for those respondents looking to use alternative financing in the future. Use of a parental company guarantee is expected to continue. Whilst our experience is that use of escrow accounts are relatively uncommon, a significant number of our respondents (22%) expect to use this structure in the future. What is striking is the fact that respondents are anticipating using an increasingly varied range of solutions. This suggests that there is no "silver bullet" alternative financing solution, and the most appropriate solution will be specific to the circumstances of the scheme, the employer and the views of the Pensions Regulator. Where our respondents had considered using alternative financing, their main aims were:

■ Increasing the security of members' pension benefits; ■ Lowering the levies paid to the PPF; and ■ Lessening the cashflow strain on the employer either by replacing cash contributions, increasing the length of the

recovery plan, or allowing trustees to pursue a more aggressive investment strategy that would lower Technical Provisions.

Hewitt Associates Limited 2 Dealing with Pension Deficit Survey 2009

About the Survey

In early summer 2009 we surveyed employers and trustees in the UK on how pension deficits are being dealt with, looking to capture information on actions that are being taken, or being considered. The issue of pension deficits has taken on added significance as a result of the economic recession, which has seen many schemes suffer large deteriorations in their funding position. The survey received a total of 152 responses. The majority of respondents (59%) worked on the corporate side, with responsibility for dealing with the pension scheme in their capacities as members of Finance, Treasury, Pension, Tax and HR departments. However, it was not surprising to see a significant number (41%) of responses coming from trustee contacts. As many schemes experience worsening deficits, trustees will have a fiduciary duty to work with employers to put in place an appropriate funding strategy that will adequately address deficits and protect scheme members' benefits.

Responses

59%

41%

Trustee Corporates

Department

41%

29%

10%

14%

1%

5%

Trustee Finance Treasury HR Risk Pensions

Hewitt Associates Limited 3 Dealing with Pension Deficit Survey 2009

Valuations and Increasing Deficits

Larger deficits at the next valuation An overwhelming number of respondents (89%) anticipated larger scheme funding deficits at their next actuarial valuations. This is not surprising given the combination of: ■ Poor asset performance – for example, over the year to May 2009, the FTSE All Share Index fell some 27%. ■ Increasing life expectancy. ■ Falling "real" discount rate assumptions when the funding measure is linked to the movement in gilt, rather than

bond, yields. This increases the assessed value of liabilities. The chart below shows how the funding ratio of a typical pension scheme has changed over the last three years on a funding and accounting basis.

C h a rt o f fu n d in g le ve l fo r a typ ic a l s c h e m e o n a n a c c o u n tin g m e a s u re a n d a g ilts -b a s e d fu n d in g m e a s u re

6 0 %

6 5 %

7 0 %

7 5 %

8 0 %

8 5 %

9 0 %

9 5 %

1 0 0 %

1 0 5 %

1 1 0 %

31 M

ar 2

006

30 J

un 2

006

30 S

ep 2

006

31 D

ec 2

006

31 M

ar 2

007

30 J

un 2

007

30 S

ep 2

007

31 D

ec 2

007

31 M

ar 2

008

30 J

un 2

008

30 S

ep 2

008

31 D

ec 2

008

31 M

ar 2

009

30 J

un 2

009

Fu

nd

ing

lev

el

F un d in g m e asu re link e d to m o ve m e n ts in g ilts yie lds A c co u n ting m e as ure

Hewitt Associates Limited 4 Dealing with Pension Deficit Survey 2009

There was broadly a fifty-fifty split amongst all respondents when it came to deciding on whether the anticipated deficit increase would result in contributions higher than the employer could reasonably afford. It was interesting to observe that when assessed separately between trustee and employer respondents, opinion was still evenly split on whether the employer could afford the expected increased contributions, as shown by the charts below.

Trustee Responses Corporate Responses

Higher Contributions Than Employer could Reasonably Afford?

47% 53%

Yes No

Higher Contributions Than Employer could Reasonably Afford?

51%49%

Yes No

Assessing the level of contributions that an employer can afford in the long term is notoriously difficult. Issues to consider include the current strength of the employer's covenant, the long term financial outlook for the industry it is in, the level of competition within the industry, and the employer's expected future earnings. The strength of the covenant will vary from employer to employer and it is likely that those who felt their employer could reasonably afford higher contributions were connected to an employer with a strong covenant. Where contributions are expected to be higher than an employer can reasonably afford, trustees and the company will need to work collaboratively to put together an appropriate Recovery Plan. To bridge any gap that might exist between the two parties, alternative financing (discussed in more detail later in this report) could be used.

Hewitt Associates Limited 5 Dealing with Pension Deficit Survey 2009

Dealing with Increasing Deficits

Contributions With nearly all our respondents anticipating higher funding deficits, and correspondingly higher employer contributions, we next considered ways in which these contributions could be managed.

Contribution Reduction Options : Trustee

97%

17%

31%

36%

61%

0% 20% 40% 60% 80% 100% 120%

Reduce the level ofTechnical Provision

prudence

Use of alternative financing

Allow for additional assetoutperformance in the

Recovery Plan

Implement actions toreduce liabilities

Extend the length of theRecovery Plan

Contribution Reduction Options: Corporates

79%

65%

50%

26%

38%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

Reduce the level ofTechnical Provision

prudence

Use of alternative financing

Allow for additional assetoutperformance in the

Recovery Plan

Implement actions to reduceliabilities

Extend the length of theRecovery Plan

Extend the length of the Recovery Plan Amongst both corporate and trustee respondents, the most common action taken to keep deficit contributions to an affordable level is to extend the length of the Recovery Plan. This is consistent with statements which the Pension Regulator (tPR) has issued to trustees and employers on the impact of the economic downturn.

Hewitt Associates Limited 6 Dealing with Pension Deficit Survey 2009

The Pensions Regulator has indicated that it is possible to renegotiate previously agreed Recovery Plans, but expects any pain with regard to lower immediate contributions to be shared with other creditors. For new Recovery Plans sponsors and trustees should take into account all circumstances and have a clear explanation of why they have agreed a longer Recovery Plan, if this is what is decided. Additionally, tPR Regulator has indicated that there should be no reason for the pension deficit to "push an otherwise viable employer into insolvency." Furthermore, tPR also suggests that where there are "short-term" affordability issues, and where it has been agreed between trustees and employers to agree lower initial contributions to maintain the long term health of the employer, a back-end loaded plan may be more appropriate than a longer Recovery Plan. Whilst Recovery Plan extension is the most common option for both corporates and trustees, it is interesting to note that a higher proportion of corporates anticipated using other options, including liability reduction actions (see below) and allowing for additional asset outperformance in the Recovery Plan. Implement actions to reduce liabilities Implementing actions to reduce liabilities is the next most popular option for both trustees and employers. Almost two-thirds of both groups anticipate that this will be used to help reduce contribution requirements. There are a variety of different actions that can be employed to reduce the cost of benefits accruing in the future and/or reduce funding deficits. Many of these actions have the added benefit that they also reduce the level of volatility associated with pension contributions. The different actions include: ■ Closing a pension scheme to future accrual. Alternatively keeping the scheme open but modifying the level of

benefits provided in some way (e.g. by capping pensionable salary increases). ■ Undertaking an enhanced transfer value exercise, where the transfer value members are normally entitled to is

enhanced during a window of opportunity. ■ A benefit audit can sometimes reveal that certain benefits are being valued and/or paid which are in excess of that

required by the scheme rules, In addition, a data audit exercise can reveal that benefits are being valued and/or paid to members who no longer exist, or are no longer entitled to receive them. Depending upon the circumstances correcting this can lead to material savings.

Other actions such as a implementing a longevity swap or a pensioner buy-in are unlikely to improve the funding position of a scheme at present (albeit last year there were cases where a pensioner buy-in resulted in a funding level improvement). However, they will lead to a significant risk reduction in a scheme. The two graphs below illustrate the cost and risk reduction different benefit management actions can achieve for a particular pension scheme.

-10

-5

0

5

10

15

20

25

30

35

Close tofuture accrual

Cap pensionablesalary increases

ETVexercise

Pensionincrease

conversion

Dataclean

Benefitaudit

Early Retirementexercise

Longevity swap Pensionerbuy-in

Cash

flow r

educ

tion

(£M p

a)

Future servicePast service

0

10

20

30

40

50

60

70

80

Close tofuture accrual

Cap pensionablesalary increases

ETVexercise

Pensionincrease

conversion

Dataclean

Benefitaudit

Early Retirementexercise

Longevity swap Pensionerbuy-in

Risk Red

uctio

n - V

AR 9

5 (£M

)

Future servicePast service

Hewitt Associates Limited 7 Dealing with Pension Deficit Survey 2009

The level of cost and risk reduction that is achieved for the different benefit management actions will be situation specific. Issues for the employer to consider include: ■ What are the employee relation issues? ■ What is the accounting impact? This may be very different from the cashflow reduction achieved. ■ Is a cash injection required up-front to achieve greater savings in the long term? ■ Is the action complex and difficult to implement? Understanding the short term and long term implications of any liability reduction actions will be important for ensuring that the level of risk reduction justifies any costs involved. Trustees will need to consider what their responsibilities are with regard to any actions that are proposed to reduce liabilities, in light of general trust law and their duties under their Trust Deed and Rules. They will want to make sure that they consider any relevant guidance from tPR and other parties. In addition, it will be important to ensure that members are communicated with in a clear and appropriate way. Allow for additional asset outperformance in the Recovery Plan Whilst the Technical Provision target set by trustees must be prudent, the allowance for asset performance in the Recovery Plan need not – a Scheme Actuary can potentially certify a Recovery Plan that assumes a best estimate asset return. Typically a best estimate asset return will be significantly higher than the prudent discount rate used in calculating the Technical Provision liabilities. Depending upon the length of the recovery plan, and the best estimate asset return for a scheme compared to its discount rate, the use of a best estimate asset return compared to the liability discount rate can reduce annual deficit contributions by 50% or more. The survey shows that one-half of companies believe that there is scope to increase the allowance for additional asset outperformance in their recovery plan, and they intend to do so. Around one-third of trustees indicated that this is something they expect will be adopted at their next actuarial valuation. Use of alternative financing Alternative financing involves the use of non-cash funding and/or security to help manage cashflows. The asset or security that is provided can be contingent on the occurrence of specified events (e.g. employer insolvency or failure to achieve a pre-agreed scheme funding level). Alternative financing can be used on its own to replace cash contributions into a pension scheme. It can also be used to support some of the other actions that can be used to reduce deficit contributions. For example: ■ To support a lengthened or back-end loaded recovery plan. ■ To support an allowance for additional asset outperformance in the recovery plan by, for example, providing

additional funds should anticipated asset returns not materialise. ■ To allow a lower level of Technical Provisions to be set. The Pensions Regulator has indicated that where a longer recovery plan is considered appropriate pension scheme trustees are likely to look for alternative security, perhaps using contingent assets or other mechanisms. Our survey shows that the use of alternative financing to reduce deficits is anticipated by over one-third of companies (38%) and trustees (33%). Further information on alternative financing is given in the next section. Reduce the level of Technical Provision prudence The Pensions Regulator expects the Technical Provision target for a pension scheme to be appropriately prudent in light of the strength of the scheme sponsor(s).

Hewitt Associates Limited 8 Dealing with Pension Deficit Survey 2009

Trustees will therefore need to be sure that they can justify a reduction in a scheme's Technical Provision target before agreeing to do so. Possible reasons why trustees may be able to justify a reduction in Technical Provisions include: ■ The strength of covenant from the sponsor(s) supports a lower Technical Provision target (e.g. the covenant

improves as a result of, say, a parental company guarantee being provided. ■ There is more prudence in their Technical Provisions than they had first thought. This could, for example, be as a

result of a scheme experience investigation suggesting that certain demographic assumptions are more prudent than previously anticipated.

17% of trustees expect that the level of prudence within their Technical Provision target would be reduced at their next actuarial valuation. This is compared to 26% of company respondents who believed the same thing. The difference in numbers might be an indication of a likely source of future tension between companies and trustees.

Hewitt Associates Limited 9 Dealing with Pension Deficit Survey 2009

Using Alternative Financing

Different types of alternative financing The chart below shows the types of alternative financing that are currently being used (red bars) by respondents, and what type of alternative financing respondents anticipate using in the future (green bars).

1

0

1

3

5

3

6

10

9

34

6

8

17

15

21

22

20

34

33

14

0 10 20 30 40 50 60 70 80 90

Ring-fenced trade receivables

Use of intangibles (e.g. brand,licences)

Employer covenant insuranceproduct

Allocating Company property

Bank letter of credit

Payments tied to companysuccess

Escrow (including variants such assettlor trusts)

Negative pledges

Charge over assets

Parent/group guarantee

% of Respondants

Now Future

Alternative finance solutions include: ■ Parental guarantees: where the parent company of a corporate group guarantees some or all of the pension debt of

its subsidiaries; ■ Security/charge over assets: where trustees are granted a fixed or floating charge over a company's assets, e.g.

property; ■ Enhanced creditor status or subordination: where other creditors of the sponsoring employer have a subordinated

claim to the pension scheme in the event of the employer's insolvency; ■ Escrow accounts: a legal arrangement under which an asset is deposited in into safekeeping (e.g. a bank account)

under the trust of a neutral third party pending the satisfaction of a contractual contingency (e.g. regular funding contributions into the pension scheme) or condition (e.g. insolvency of the employer). If the condition is met, then the escrow agent will deliver the escrow assets to the party prescribed by the contract, the employer or the Trustees; and

■ Bank letter of credit: such that under pre-agreed circumstances, money can be drawn against the third party bank up to a specified amount (an alternative to this would be sponsor covenant insurance – the market for this type of cover is still immature).

Hewitt Associates Limited 10 Dealing with Pension Deficit Survey 2009

What is being used now? 50% of the 152 respondents to this survey currently use some form of alternative financing. This is expected to increase to over 80% in the future. Those who are using or are anticipating using alternative financing are not necessarily doing so to reduce contributions as a result of higher deficits. The use of a parent company guarantee is by far the most utilised alternative finance solution amongst respondents (34%). It is as common as all of the other types of alternative financing put together. This is not surprising as it is one of the least complex and costly solutions to implement. It has also been the favoured solution with regard to reducing the PPF levy – which has been the key driver for the use of alternative financing in the past. However, whilst a parent company guarantee can certainly be effective in helping to reduce the PPF levy, it is not always obvious how effective it would be in other situations. In this context it is important to consider the extent to which the guarantor is reliant upon its subsidiary guarantee. A useful indicator is the proportion of group/parent revenue or profits that originates from the subsidiary. In addition, it is important to consider where the assets of a business are held – by subsidiaries or the parent? A parental guarantee may not enhance scheme security if the parent is not much stronger than the scheme sponsors.

What is being considered for the future? Looking ahead, most of our respondents (52%) preferred a solution that granted the pension scheme a charge over company assets, including property. Other responses included; continued use of parental/group guarantees (34%); using escrow accounts, including variants (22%); payments tied to company success (21%); and increasing use of a banking letter of credit (15%). Assets which are charged to the pension scheme are usually unencumbered (i.e. they have no other creditor charge on them). Encumbered assets can be used, but this will reduce the value/reliance that the trustees can place on them. Examples of companies who have employed 'a charge over assets' solution include Tesco, Marks & Spencer, and Whitbread. The 52% of respondents who are thinking about placing charges over assets or transferring them into the pension scheme should be mindful about the following: ■ The asset's liquidity and the ease with which it can be realised into cash for the scheme; ■ The frequency with which the assets will be valued; ■ Where there is a long term strategy to wind-up the scheme or secure an annuity buy-in, consideration on whether

an insurance company is likely to accept the asset(s) as part of the insurance premium; and ■ The alternative financing solution considered by respondents will be based on their scheme's particular

circumstances, the unique pattern of the company's financial/asset base, the long-term de-risking strategy ear-marked for the scheme and any envisaged near term company re-structuring.

Other points of interest include: ■ A significant increase in the use of payments that are tied to the future success/profitability of a company is

anticipated. Such an approach can help address a situation where liquidity in a business may be limited at present, but is expected to improve in the future as the economy moves out of recession.

■ Negative pledges are also being used where no assets are available for a contingent asset solution. They are particularly useful if the covenant strength can be maintained by the company not doing something. For example, if a sponsoring employer has covenant strength, and is part of a large group of companies. If the trustees of its pension scheme do not want this strength/covenant to be passed to other companies in the Group (and diluted), they can ask for a negative pledge – i.e. the strength will not be diluted unless the trustees receive alternative protection. A negative pledge is usually about the trustees getting 'a seat at the table' rather than actually trying to restrict sensible company behaviour.

Hewitt Associates Limited 11 Dealing with Pension Deficit Survey 2009

■ A significant proportion of respondents are considering the use of bank letters of credit and employer covenant insurance products. Generally, we have found that at present these solutions are either not available or they are prohibitively expensive as a result of the credit crunch. In addition, some companies who have previously put a letter of credit in place are now looking to replace them with something else; due to the cost/difficulty of renewing them and the adverse impact they have on their borrowing facilities. However, respondents may be anticipating these solutions becoming more attractive in the future in a post credit crunch environment.

■ Other solutions which have had little or no application in the past (such as the use of company brand and other intangibles, and the application of trade receivables) are starting to be considered as companies and trustees search for assets on the corporate balance sheet which are either under-valued or under-utilised that can be used to help fund their pension scheme.

■ Respondents are anticipating using an increasingly varied range of solutions indicating that there isn't a single silver bullet that can deal with the different reasons for using alternative financing.

Why Alternative Financing? Whilst trustees will always prefer cash, many (including the Regulator) recognise that employers can face and, in some circumstances, are facing difficulties in the current economic environment to meet funding requirements of the pension scheme through cash alone. However, agreeing to put in place some form of additional security with the trustees, e.g. a charge over assets, can be a way to support the scheme without bankrupting the employer. Moreover, tPR has gone on record as saying that "the best outcome for scheme and employer is a viable sponsor that will continue to support the scheme". Where cash is tight, an alternative financing solution can be used to give pension schemes security against the risk that the employer will default on its pension contributions. All Respondents

0

5

3

7

8

8

11

20

1

7

12

13

19

23

33

33

3126

0 10 20 30 40 50 60 70 80

Capital Efficiency

Facilitate Corporate Restructuring

Avoid Unrecognisable Surplus

Use of Employer Related Assets

Take More Investment Risk

Avoid Trapped Surplus

Manage Cashflows

Reduce PPF Levy

Provide additional security formembers' benefits

% of Respondents

Now Future

The most popular reasons for using alternative financing now, or in the future, are to provide additional security for members' benefits (57%), reduce PPF levy contributions (55%) and to manage employer cashflow (46%). In the future managing cashflows along with PPF levy reduction are quoted as the most common reasons for using alternative financing. Providing additional security for members' benefits is not far behind (31%). However, it is interesting, but perhaps not surprising, to note that if the responses of corporates is considered in isolation managing cashflow (41%) was by far the most common reason cited for the use of alternative financing in the future.

Hewitt Associates Limited 12 Dealing with Pension Deficit Survey 2009

Other points of interest from the responses include: ■ Significantly more respondents are expecting to use alternative financing in the future (35%) than in the past (11%)

to avoid trapped surpluses or to reduce the risk of an unrecognisable surplus. If significantly higher cash contributions are being paid into a pension scheme as the result of a larger deficit, and asset values subsequently rebounded, there is a risk that surpluses will arise that either can't be physically accessed and/or recognised from an accounting perspective. Using some form of contingent asset that is only paid down into the scheme at a future point if the scheme is still in deficit can help avoid this issue.

■ A notable proportion of respondents (19%) expect to use alternative financing in the future to allow a more aggressive investment strategy to be agreed. Whilst the proportion of corporates anticipating this is higher (20%), a significant proportion of trustees (15%) also expect this. It is true that some schemes are currently investigating taking more investment risk (and increasing their equity exposure) as a potential way of closing their deficit over time. This may be considered to be attractive at present as equity markets are, arguably, considered low. Taking on additional investment risk may be a concern for trustees. Providing a contingent asset that will only pay out in the future if anticipated equity out-performance does not materialise can help address this concern.

■ Use of alternative financing to assist with capital reserving is only relevant for financial institutions such as banks and insurance companies. It is likely to have only applied to a small number of respondents. Where it does apply using alternative financing in this way can benefit financial services companies who must hold capital (using stress tests) for all risks associated with their business operations. If such institutions do not reserve for their pension schemes on a Pillar 2 basis but, instead, on a Pillar 1 basis (i.e. the lower of the accounting deficit or the net present value of the next five years worth of funding contributions), they could experience a net improvement in their overall capital position if they use alternative financing.

In summary, alternative financing and its application of contingent assets, is being used to deal with increasing deficits as follows: 1) To facilitate a riskier investment strategy that would see trustees investing in more return seeking assets. The

contingent asset would protect the scheme if assets did not achieve the anticipated excess returns. A higher discount rate could be applied in calculating technical provisions (liabilities) and, thus, resulting in a lower level of required funding; and

2) To support a "recovery plan" by providing collateral against the risk that the employer defaults on its obligation to

rectify a deficit or to give trustees added assurance where a longer or back-end loaded recovery plan (involving lower cash contributions in the earlier years) has been agreed.

Respondents should be careful about the "double-counting" effects of using contingent assets. The Pensions Regulator has indicated that if a contingent asset is supporting a back-end loaded recovery plan, it cannot generally support the scheme's Technical Provisions.

Hewitt Associates Limited 13 Dealing with Pension Deficit Survey 2009

Actions and Considerations for Alternative Financing

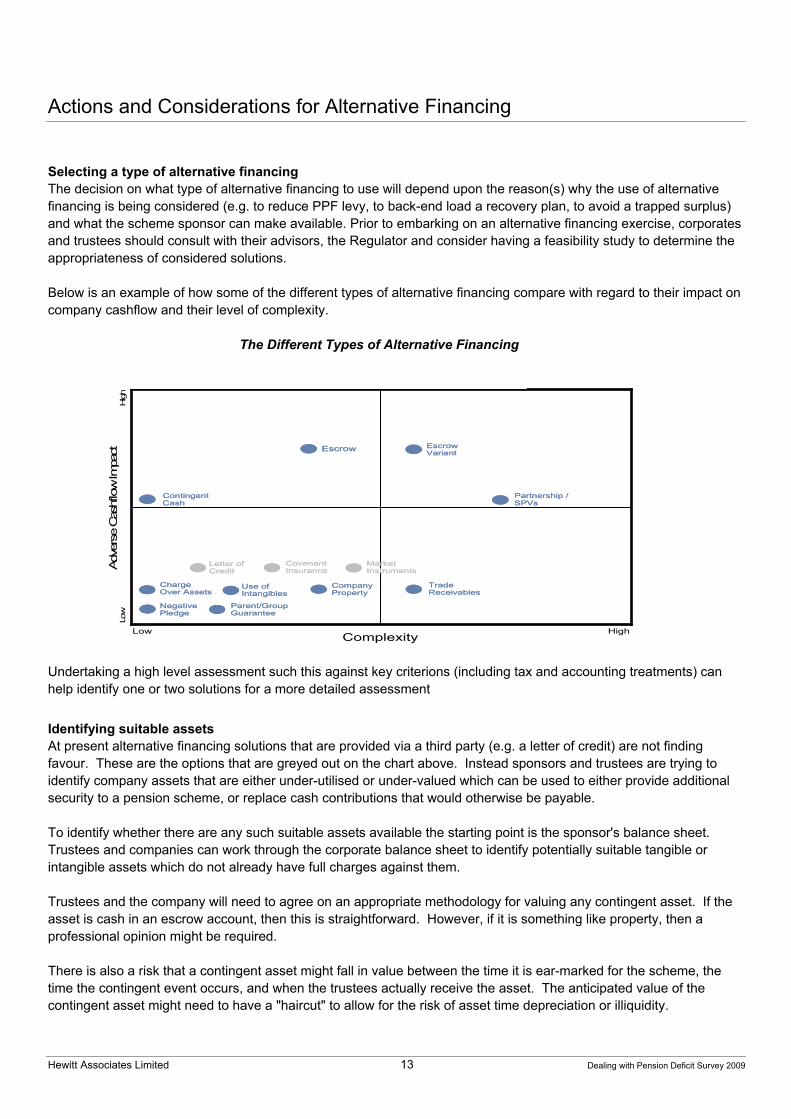

Selecting a type of alternative financing The decision on what type of alternative financing to use will depend upon the reason(s) why the use of alternative financing is being considered (e.g. to reduce PPF levy, to back-end load a recovery plan, to avoid a trapped surplus) and what the scheme sponsor can make available. Prior to embarking on an alternative financing exercise, corporates and trustees should consult with their advisors, the Regulator and consider having a feasibility study to determine the appropriateness of considered solutions. Below is an example of how some of the different types of alternative financing compare with regard to their impact on company cashflow and their level of complexity. The Different Types of Alternative Financing

Undertaking a high level assessment such this against key criterions (including tax and accounting treatments) can help identify one or two solutions for a more detailed assessment

Identifying suitable assets At present alternative financing solutions that are provided via a third party (e.g. a letter of credit) are not finding favour. These are the options that are greyed out on the chart above. Instead sponsors and trustees are trying to identify company assets that are either under-utilised or under-valued which can be used to either provide additional security to a pension scheme, or replace cash contributions that would otherwise be payable. To identify whether there are any such suitable assets available the starting point is the sponsor's balance sheet. Trustees and companies can work through the corporate balance sheet to identify potentially suitable tangible or intangible assets which do not already have full charges against them. Trustees and the company will need to agree on an appropriate methodology for valuing any contingent asset. If the asset is cash in an escrow account, then this is straightforward. However, if it is something like property, then a professional opinion might be required. There is also a risk that a contingent asset might fall in value between the time it is ear-marked for the scheme, the time the contingent event occurs, and when the trustees actually receive the asset. The anticipated value of the contingent asset might need to have a "haircut" to allow for the risk of asset time depreciation or illiquidity.

The Different Types Of Alternative Financing

Complexity

Adv

erse

Cas

hflow Im

pact EscrowEscrow Escrow

VariantEscrow Variant

Partnership /SPVsPartnership /SPVs

ContingentCashContingentCash

Letter of CreditLetter of Credit

Charge Over AssetsCharge Over Assets

NegativePledgeNegativePledge

Covenant InsuranceCovenant Insurance

Use of IntangiblesUse of Intangibles

Parent/Group GuaranteeParent/Group Guarantee

Market InstrumentsMarket Instruments

Company PropertyCompany Property

Trade ReceivablesTrade Receivables

Low High

Low

High

Hewitt Associates Limited 14 Dealing with Pension Deficit Survey 2009

Impact on Technical Provisions and Recovery Plans The use of alternative financing may allow a lower level of Technical Provisions to be agreed. This could be, for example, as a result of the trustees placing a higher value on the strength of employer covenant because of additional security they have been granted on employer insolvency. Alternatively (or in addition) the use of alternative financing can be used to support a recovery plan or replace cash contributions that would otherwise be due under a recovery plan.

The above charts show how non-cash funding and security can be used to manage cashflows and cash contributions: ■ The first chart shows how a physical asset, such as property, can replace cash in the first few years, allowing the

employer to defer cash contributions whilst it might have acute, short term liquidity issues; ■ The second chart shows where the company has offered the scheme security to facilitate a back-end loaded

Recovery Plan, enabling the management of the company cashflow; and ■ The final chart shows the cash flow contributions from the company into the scheme as a result of the use of a

contingent vehicle such as an escrow account. There are lower contributions into the scheme, with the remaining contributions going into the contingent vehicle.

Flexibility to substitute one type of alternative financing for another When preparing scheme funding documentation (Statement of Funding Principles and Recovery Plan) that include the use of alternative financing we recommend that the wording of these is flexible enough to allow one type of alternative financing to be replaced by another type of alternative financing "of equal value" in the future. The reason for this is circumstances can change and a particular type of alternative financing that worked in the past may no longer be appropriate in the future (for example, a letter of credit can no longer be obtained on reasonable terms, a company property needs to be sold). Introducing this flexibility at the outset means that the time and cost associated with fully revisiting funding arrangements can be avoided in the future. Implementation and ongoing monitoring The following should be considered when looking to implement an alternative financing solution: ■ Can the alternative financing solutions be structured such that it qualifies for PPF levy reduction? ■ Alternative financing solutions which involve the use of assets or property will require ongoing monitoring, including

asset revaluation and, sometimes, occasional liquidation to meet changes in scheme investment strategy (e.g. a pension buy-in exercise).

■ Alternative financing that involve the use of "contingent" assets will require agreement between trustees and employers on the timing of triggers, the length of time for "rectification" periods and agreement on the necessary actions which need taking should rectification periods lapse.

■ The employer might want to present a business case (as part of a feasibility study) to the trustees, identifying the size of the scheme deficit, the period over which any deficits will be rectified and the structure/value of the contingent asset to be used.

■ Trustees should receive advice around the legal, commercial and actuarial implications for any alternative financing solution proposed. This should include advice on assessing the strength of the employer covenant and determining the rationale and business case behind a proposed alternative finance solution.

0

2

4

6

8

10

12

14

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16Year

Def

icit

cont

ribut

ions

(£M

p.a

.)

Security provided to allow back end loading

0

2

4

6

8

10

12

14

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16Year

Def

icit

cont

ribut

ions

(£M

p.a

.) Physical asset replaces cashCash to scheme

0

2

4

6

8

10

12

14

1 2 3 4 5 6 7 8 9 10111213141516Year

Def

icit

cont

ribut

ions

(£M

p.a

.) Cash to contingent vehicleCash to scheme

Hewitt Associates Limited 15 Dealing with Pension Deficit Survey 2009

Alternative financing solutions can be complicated and trustees and companies will need to get comfortable with some of the complex mechanics of their operations (e.g. valuation, release and renewal, and analysis of security rights). As part of a due diligence or feasibility study on any solution, employers and trustees might want to consider the followings: ■ Clarity around objectives for why a particular solution is considered; ■ What other constraints / parameters are important? ■ Will a simple structure / vehicle suffice? ■ Ensure sufficient flexibility ■ Simple questions for trustees and corporate to ask themselves when buried in the complexities of the solution

include: ⎯ Why not cash now? ⎯ What is/are the event(s) that will trigger payments? ⎯ What will the scheme actually receive? ⎯ What are the risks? ⎯ How will I monitor this? ⎯ What else am I being asked to get this? ⎯ Is any other creditor's position improving?

Contact details To discuss the results of this survey please contact your usual Hewitt consultant or Dave Bush Michael Brewitt Email: [email protected] Email: [email protected] Tel: (0)1727 888 227 Tel: (0) 113 204 5585

SB18

90

About Hewitt Associates

Hewitt Associates (NYSE: HEW), a global human resources consulting and outsourcing company, helps leading organisations around the world anticipate and solve their most complex benefits, talent, and related financial challenges. With a history of exceptional client service since 1940, Hewitt has offices in over 40 countries and employs approximately 24,000 associates. For more information, please visit www.hewitt.com.

Nothing in this document should be treated as an authoritative statement of the law on an particular aspect or in any specific case. It should not be taken as financial advice and action should not be taken as a result of this document alone. Consultants will be pleased to answer questions on its contents but cannot give individual financial advice. Individuals are recommended to seek independent financial advice in respect of their own personal circumstances.

Hewitt Associates Limited is registered in England & Wales. Registered No: 4396810. Registered Office: 6 More London Place, London SE1 2DA.

Copyright @ 2009 Hewitt Associates Limited

www.hewitt.com/uk