Embed Size (px)

Citation preview

Research & Market Intell igence

DEALER SENTIMENT INDEXSECOND QUARTER 2021

Research & Market Intell igence

Dealer Sentiment IndexS E C O N D Q U A R T E R 2 0 2 1A U n i q u e M a r k e t D r i v e s O p t i m i s m

BackgroundData for the Cox Automotive Dealer Sentiment Index (CADSI) is gathered via a quarterly online survey of franchised and independent auto dealers.

Dealer responses are weighted by dealership type and volume of sales to closely reflect the national dealer population. Data is used to calculate an index wherein a number over 50 indicates more dealers view conditions as strong or positive rather than weak or negative.

The Q2 2021 CADSI is based on 1,139 U.S. auto dealer respondents, comprising 589 franchised dealers and 550 independents. The survey was conducted from April 26 to May 10, 2021.

The next quarterly report will be released in September 2021. The CADSI was first published in Q3 2017.

2Dealer Sentiment Index Q2 2021

Key Takeaways

3Dealer Sentiment Index Q2 2021

Dealer sentiment in the second quarter of 2021 saw substantial growth year over year and compared to Q2 2019 with the overall current market index increasing to 67, well above the positive threshold of 50 in the Cox Automotive Dealer Sentiment Index (CADSI). More dealers in the U.S. now feel that the current market is strong compared to those who feel it is weak, another indication of the overall market recovery from the depths of Q2 2020.

Dealers are also optimistic about the market ahead. The 3-month market outlook index reading of 63 is an increase from last quarter and, importantly, equal to Q1 2020, the final pre-COVID-19 reading. Profits in Q2 are strong, dealers are reporting. The profit index in Q2 hit a record 59, while the price pressure index dropped to a record low 33, meaning a majority of dealers are feeling little pressure to lower prices.

“Driven by the unique circumstances of strong demand and low inventory, dealer sentiment

climbed to a record high in the spring,” said Cox Automotive Chief Economist Jonathan Smoke. “The first two quarters of 2021 are showing a strongly recovering market, balancing on a perfect mix of pent-up demand, rising prices, and low inventory.”

Consistent with current market trends, the new-vehicle inventory index decreased significantly to 13 in Q2, a substantial 31-point drop from last quarter and a record low. The used-vehicle inventory index saw similar movement from Q1 to Q2, falling to 21, also a record low, although equal to Q3 2020. Tight inventory was ranked as the top factor holding back business in Q2, and, when asked, 53% of dealers noted that Finding/Buying Inventory was their top priority in the quarter.

Unlike inventory, customer traffic showed a significant improvement in Q2, with the index increasing 28 points from the prior quarter and reaching a record-high 57. This reading indicates more dealers feel their customer

traffic is strong than feel it is weak, likely due to pent-up demand.

Despite tight inventory, vehicle sales have been healthy in 2021. The Q2 new-vehicle sales index of 65 was a record for Q2 and near the all-time high of 66. The used-vehicle sales index in Q2 reached 62, an all-time record high and the first time the overall used-vehicle sales index moved above 60.

The top 5 factors holding back business shifted notably in Q2 from Q1, with Limited Inventory jumping to the top spot with 64% of dealers citing it. Market Conditions rose to No. 2 at 34%. Business Impacts from COVID-19, meanwhile, fell to the No. 3 spot from No. 1. The Economy moved down to No. 4 while Expenses rose from No. 7 to No. 5, with 19% of dealers citing it as a factor holding back business. Notably, Political Climate fell to No. 6 from No. 5 in top factors list, a level equal to Q2 2020. Political Climate as a factor holding back business peaked at No. 3 in Q4 2020.

Dealer Sentiment IndexS E C O N D Q U A R T E R 2 0 2 1

Dealer Sentiment Index Q2 2021

Strong

Weak

4845 46

49 51 51

4448 49 48 47 49

20

56

49 49

67

54 55 54 55 5659

51 5054 56

5155

30

68

61 61

77

4642 43

4750 48

4247 48 46 46 47

17

53

46 45

63

Q2 2017 Q3 2017 Q4 2017 Q1 2018 Q2 2018 Q3 2018 Q4 2018 Q1 2019 Q2 2019 Q3 2019 Q4 2019 Q1 2020 Q2 2020 Q3 2020 Q4 2020 Q1 2021 Q2 2021

Overall Franchise Independent

Q1: How would you describe the current market for vehicles in the areas where you operate?

4

Note: Scale 1 - 100

Dealer Sentiment IndexS E C O N D Q U A R T E R 2 0 2 1

Dealer Sentiment Index Q2 2021

Strong

Weak

Q2: What do you expect the market for vehicles in your area to look like 3 months from now?

5

5552 53

70

56 57

49

63

5551 51

63

4550 48

596364

57 57

7369

61

54

62 6257

54

66

5760 58

6874

52 51 52

70

5255

47

63

5249 51

61

4046 44

5659

Q2 2017 Q3 2017 Q4 2017 Q1 2018 Q2 2018 Q3 2018 Q4 2018 Q1 2019 Q2 2019 Q3 2019 Q4 2019 Q1 2020 Q2 2020 Q3 2020 Q4 2020 Q1 2021 Q2 2021

Overall Franchise IndependentNote: Scale 1 - 100

Dealer Sentiment IndexS E C O N D Q U A R T E R 2 0 2 1

Dealer Sentiment Index Q2 2021

Strong

Weak

38 3734 35

40 41

33 35

4240 37 36

13

4441

29

57

43 4245 43 44 46

4138

45 4743 45

20

5552

46

72

36 3631 33

39 39

30 33

4137 35

32

11

4037

24

52

Q2 2017 Q3 2017 Q4 2017 Q1 2018 Q2 2018 Q3 2018 Q4 2018 Q1 2019 Q2 2019 Q3 2019 Q4 2019 Q1 2020 Q2 2020 Q3 2020 Q4 2020 Q1 2021 Q2 2021

Overall Franchise IndependentNote: Scale 1 - 100

Q3: How do you rate the customer traffic to your dealership over the past 3 months?

6

Dealer Sentiment IndexS E C O N D Q U A R T E R 2 0 2 1

Dealer Sentiment Index Q2 2021

Strong

Weak

Q4: How would you describe your profits over the past 3 months?

7

4441 41 41 43 42

38 3844 42 44

40

17

46 48

39

59

48 50 49 49 51 49 4943

51 52 51 51

25

6670

63

82

4338 38 38

41 4035 36

4238

4236

14

40 41

31

51

Q2 2017 Q3 2017 Q4 2017 Q1 2018 Q2 2018 Q3 2018 Q4 2018 Q1 2019 Q2 2019 Q3 2019 Q4 2019 Q1 2020 Q2 2020 Q3 2020 Q4 2020 Q1 2021 Q2 2021

Overall Franchise IndependentNote: Scale 1 - 100

Dealer Sentiment IndexS E C O N D Q U A R T E R 2 0 2 1

Dealer Sentiment Index Q2 2021

Easy

Difficult

Q5: How would you describe your ability to get credit to operate your business over the past 3 months?

8

5955 57

61 59 59 60 60 61 60 60 58

4651

54 5458

67 66 68 7065 67 69 68 67 66 65 65

5761 63 64 66

5652 54

58 57 57 57 58 59 59 58 57

4348

51 5155

Q2 2017 Q3 2017 Q4 2017 Q1 2018 Q2 2018 Q3 2018 Q4 2018 Q1 2019 Q2 2019 Q3 2019 Q4 2019 Q1 2020 Q2 2020 Q3 2020 Q4 2020 Q1 2021 Q2 2021

Overall Franchise IndependentNote: Scale 1 - 100

Dealer Sentiment IndexS E C O N D Q U A R T E R 2 0 2 1

Dealer Sentiment Index Q2 2021

Growing

Declining

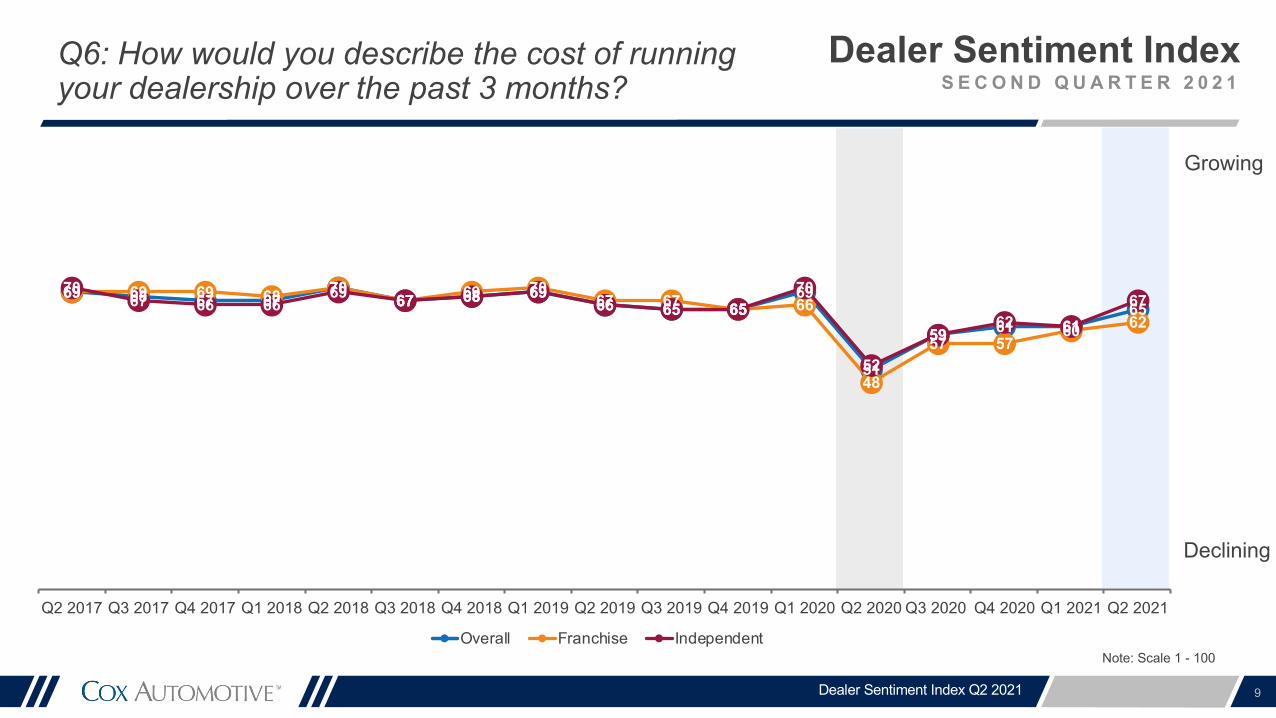

Q6: How would you describe the cost of running your dealership over the past 3 months?

9

69 68 67 6770

67 68 6966 65 65

69

51

59 61 6165

69 69 69 68 7067 69 70

67 67 65 66

48

57 5760 62

7067 66 66

69 67 68 6966 65 65

70

52

5962 61

67

Q2 2017 Q3 2017 Q4 2017 Q1 2018 Q2 2018 Q3 2018 Q4 2018 Q1 2019 Q2 2019 Q3 2019 Q4 2019 Q1 2020 Q2 2020 Q3 2020 Q4 2020 Q1 2021 Q2 2021

Overall Franchise IndependentNote: Scale 1 - 100

Dealer Sentiment IndexS E C O N D Q U A R T E R 2 0 2 1

Dealer Sentiment Index Q2 2021

Good

Poor

Q7: How would you describe the current new-vehicle sales environment?

10

57 5761

6559 60

5753 54 55 56 57

39

6166

6165

57 5761

6559 60

5753 54 55 56 57

39

6166

6165

Q2 2017 Q3 2017 Q4 2017 Q1 2018 Q2 2018 Q3 2018 Q4 2018 Q1 2019 Q2 2019 Q3 2019 Q4 2019 Q1 2020 Q2 2020 Q3 2020 Q4 2020 Q1 2021 Q2 2021

Overall FranchiseNote: Scale 1 - 100

Dealer Sentiment IndexS E C O N D Q U A R T E R 2 0 2 1

Dealer Sentiment Index Q2 2021

Q8: How would you describe the current new-vehicle inventory levels?

11

6762

68

6157 59 60

6461 59

56

41

29

4844

13

6762

68

6157 59 60

6461 59

56

41

29

4844

13

Q2 2017 Q3 2017 Q4 2017 Q1 2018 Q2 2018 Q3 2018 Q4 2018 Q1 2019 Q2 2019 Q3 2019 Q4 2019 Q1 2020 Q2 2020 Q3 2020 Q4 2020 Q1 2021 Q2 2021

Overall FranchiseNote: Scale 1 - 100

Growing

Declining

Dealer Sentiment IndexS E C O N D Q U A R T E R 2 0 2 1

Dealer Sentiment Index Q2 2021

Growing Strong

Declining Weak

Inventory/ProfitsQ4: How would you describe your profits over the past 3 months? Q8: How would you describe the current new-vehicle inventory levels?

12

Note: Scale 1 - 100

6762

68

6157 59 60

6461 59

56

41

29

4844

13

48 50 49 49 51 49 4943

51 52 51 51

25

6670

63

82

Q2 2017 Q3 2017 Q4 2017 Q1 2018 Q2 2018 Q3 2018 Q4 2018 Q1 2019 Q2 2019 Q3 2019 Q4 2019 Q1 2020 Q2 2020 Q3 2020 Q4 2020 Q1 2021 Q2 2021

New Vehicle Inventory Franchise Profits

Dealer Sentiment IndexS E C O N D Q U A R T E R 2 0 2 1

Dealer Sentiment Index Q2 2021

Q9: How would you describe the current new-vehicle inventory mix?

13

Note: Scale 1 - 100

Good

Poor

Note: New question introduced in Q2 2019

7572 73 73

64

42

53 54

33

7572 73 73

64

42

53 54

33

Q2 2017 Q3 2017 Q4 2017 Q1 2018 Q2 2018 Q3 2018 Q4 2018 Q1 2019 Q2 2019 Q3 2019 Q4 2019 Q1 2020 Q2 2020 Q3 2020 Q4 2020 Q1 2021 Q2 2021

Overall Franchise

Dealer Sentiment IndexS E C O N D Q U A R T E R 2 0 2 1

Dealer Sentiment Index Q2 2021

Large

Small

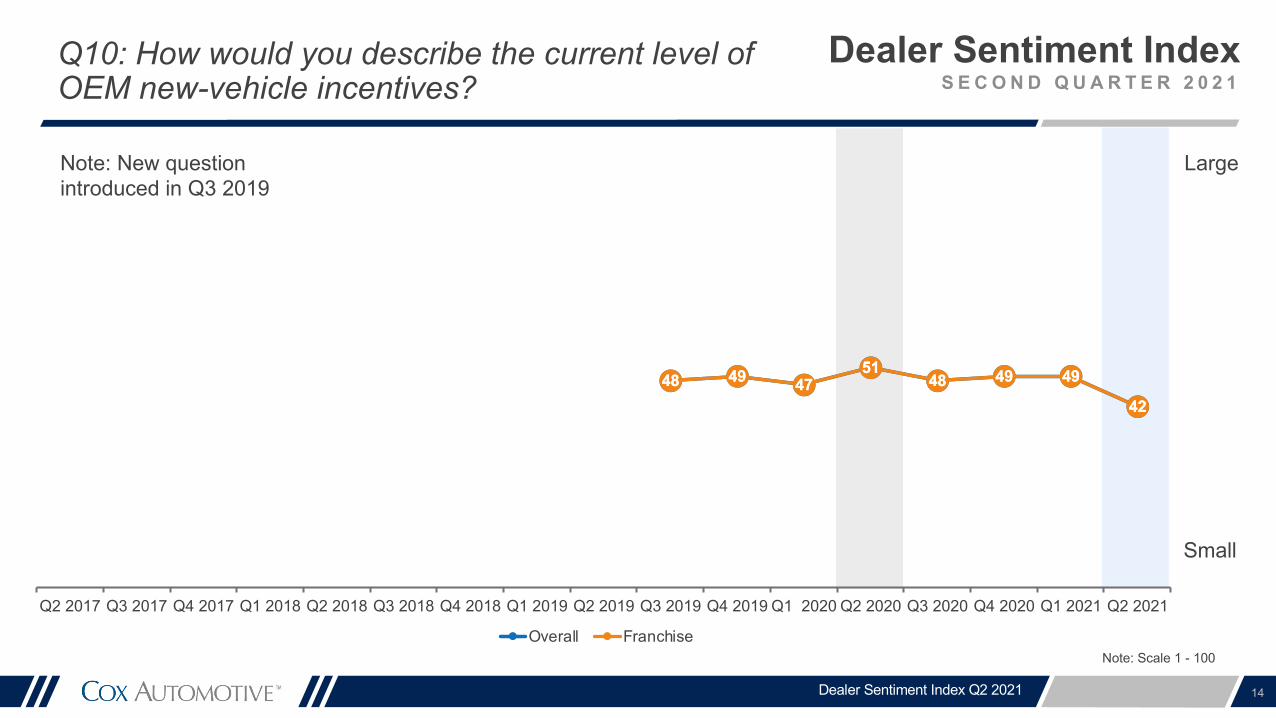

Q10: How would you describe the current level of OEM new-vehicle incentives?

14

48 49 4751

48 49 49

4248 49 47

5148 49 49

42

Q2 2017 Q3 2017 Q4 2017 Q1 2018 Q2 2018 Q3 2018 Q4 2018 Q1 2019 Q2 2019 Q3 2019 Q4 2019 Q1 2020 Q2 2020 Q3 2020 Q4 2020 Q1 2021 Q2 2021

Overall FranchiseNote: Scale 1 - 100

Note: New question introduced in Q3 2019

Dealer Sentiment IndexS E C O N D Q U A R T E R 2 0 2 1

Dealer Sentiment Index Q2 2021

Q11: How would you describe the current used-vehicle sales environment?

15

55 57 55 56 55 5751 53

56 55 53 53

26

5552

47

62

70 68 67 6972 72

68 6672 73

6672

43

77

68 66

77

5053 51 52 50 52

46 4851 49 49 47

20

47 47

40

56

Q2 2017 Q3 2017 Q4 2017 Q1 2018 Q2 2018 Q3 2018 Q4 2018 Q1 2019 Q2 2019 Q3 2019 Q4 2019 Q1 2020 Q2 2020 Q3 2020 Q4 2020 Q1 2021 Q2 2021

Overall Franchise IndependentNote: Scale 1 - 100

Good

Poor

Dealer Sentiment IndexS E C O N D Q U A R T E R 2 0 2 1

Dealer Sentiment Index Q2 2021

Growing

Declining

Q12: How would you describe the current used-vehicle inventory levels?

16

51 5359

49 48 4854

46 4753 53

31

21

41 41

21

55 55

6258

52 54

62

53 5458 59

43

28

4853

25

5053

58

45 46 4652

44 44

51 51

27

19

39 37

19

Q2 2017 Q3 2017 Q4 2017 Q1 2018 Q2 2018 Q3 2018 Q4 2018 Q1 2019 Q2 2019 Q3 2019 Q4 2019 Q1 2020 Q2 2020 Q3 2020 Q4 2020 Q1 2021 Q2 2021

Overall Franchise IndependentNote: Scale 1 - 100

Dealer Sentiment IndexS E C O N D Q U A R T E R 2 0 2 1

Dealer Sentiment Index Q2 2021

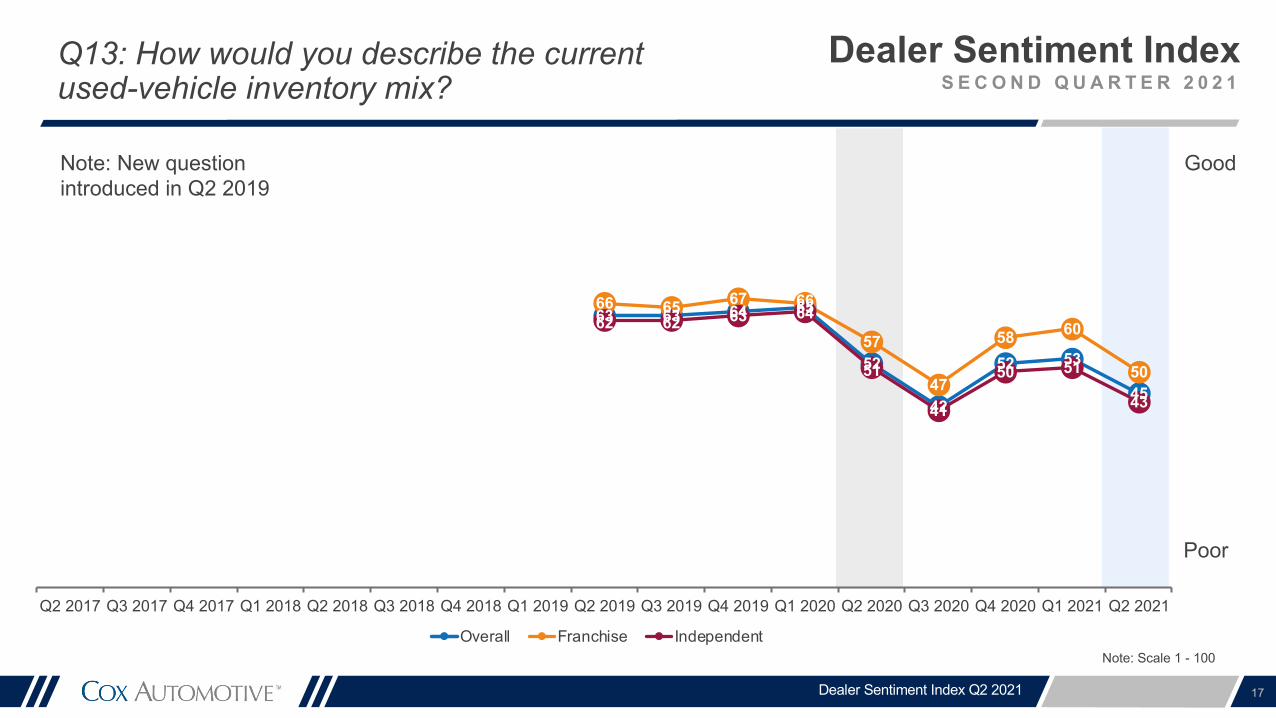

Q13: How would you describe the current used-vehicle inventory mix?

17

63 63 64 65

52

42

52 53

45

66 65 67 66

57

47

58 60

50

62 62 63 64

51

41

50 51

43

Q2 2017 Q3 2017 Q4 2017 Q1 2018 Q2 2018 Q3 2018 Q4 2018 Q1 2019 Q2 2019 Q3 2019 Q4 2019 Q1 2020 Q2 2020 Q3 2020 Q4 2020 Q1 2021 Q2 2021

Overall Franchise IndependentNote: Scale 1 - 100

Good

Poor

Note: New question introduced in Q2 2019

Dealer Sentiment IndexS E C O N D Q U A R T E R 2 0 2 1

Dealer Sentiment Index Q2 2021

More

Less

Q14: How much pressure do you feel to lower your prices?

18

Note: Scale 1 - 100

64 6367

62 64 6367

63 64 63 63 63

70

4551

57

33

65 67 6762

66 65 67 67 66 65 64 6669

37

4851

23

63 6267

62 63 6366

62 63 62 62 63

70

4852

58

37

Q2 2017 Q3 2017 Q4 2017 Q1 2018 Q2 2018 Q3 2018 Q4 2018 Q1 2019 Q2 2019 Q3 2019 Q4 2019 Q1 2020 Q2 2020 Q3 2020 Q4 2020 Q1 2021 Q2 2021

Overall Franchise Independent

Dealer Sentiment IndexS E C O N D Q U A R T E R 2 0 2 1

Dealer Sentiment Index Q2 2021

Growing

Declining

Q15: How would you describe your dealership's current staffing levels?

19

52 52 52 54 52 50 50 48 50 49 50 52

35

4347 46 47

56 55 5560

55 53 52 53 54 53 5459

35

5053 54

5050 51 51 52 51 49 49 47 49 48 49 50

3540

45 4346

Q2 2017 Q3 2017 Q4 2017 Q1 2018 Q2 2018 Q3 2018 Q4 2018 Q1 2019 Q2 2019 Q3 2019 Q4 2019 Q1 2020 Q2 2020 Q3 2020 Q4 2020 Q1 2021 Q2 2021

Overall Franchise IndependentNote: Scale 1 - 100

Dealer Sentiment IndexS E C O N D Q U A R T E R 2 0 2 1

Dealer Sentiment Index Q2 2021

Better

Worse

20

51

74

51

74

Q2 2017 Q3 2017 Q4 2017 Q1 2018 Q2 2018 Q3 2018 Q4 2018 Q1 2019 Q2 2019 Q3 2019 Q4 2019 Q1 2020 Q2 2020 Q3 2020 Q4 2020 Q1 2021 Q2 2021

Overall FranchiseNote: Scale 1 - 100

Note: New question introduced Q1 2021

Q16: How would you describe the current level of business in your fixed operation?

Dealer Sentiment IndexS E C O N D Q U A R T E R 2 0 2 1

Dealer Sentiment Index Q2 2021

Growing

Declining

21

72 7472 74

Q2 2017 Q3 2017 Q4 2017 Q1 2018 Q2 2018 Q3 2018 Q4 2018 Q1 2019 Q2 2019 Q3 2019 Q4 2019 Q1 2020 Q2 2020 Q3 2020 Q4 2020 Q1 2021 Q2 2021

Overall FranchiseNote: Scale 1 - 100

Note: New question introduced Q1 2021

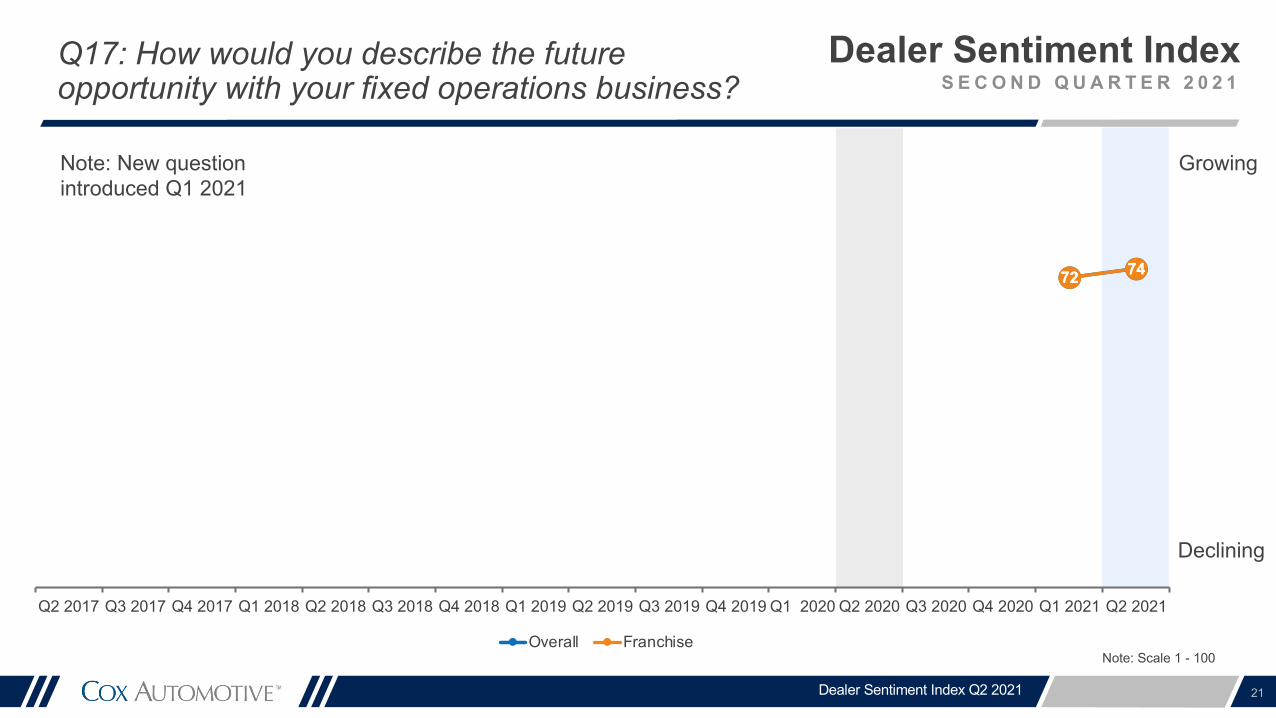

Q17: How would you describe the future opportunity with your fixed operations business?

Dealer Sentiment IndexS E C O N D Q U A R T E R 2 0 2 1

Dealer Sentiment Index Q2 2021

Strong

Weak

Q18: How would you describe the current U.S. economy?

22

55 55 57

23

4043 44

5455 5457

29

4853 51

6055 55 57

21

3740 42

52

Q2 2017 Q3 2017 Q4 2017 Q1 2018 Q2 2018 Q3 2018 Q4 2018 Q1 2019 Q2 2019 Q3 2019 Q4 2019 Q1 2020 Q2 2020 Q3 2020 Q4 2020 Q1 2021 Q2 2021

Overall Franchise IndependentNote: Scale 1 - 100

Note: New question introduced in Q3 2019

Dealer Sentiment IndexS E C O N D Q U A R T E R 2 0 2 1

Dealer Sentiment Index Q2 2021

Better

Worse

Q19: Compared to last year, how would you describe your EV sales?

23

515549

Q2 2017 Q3 2017 Q4 2017 Q1 2018 Q2 2018 Q3 2018 Q4 2018 Q1 2019 Q2 2019 Q3 2019 Q4 2019 Q1 2020 Q2 2020 Q3 2020 Q4 2020 Q1 2021 Q2 2021

Overall Franchise IndependentNote: Scale 1 - 100

(EV) Electric Vehicle

Note: New question introduced Q2 2021

Dealer Sentiment IndexS E C O N D Q U A R T E R 2 0 2 1

Dealer Sentiment Index Q2 2021

Growing

Declining

Q20: What do you expect the EV market in your area to look like 3 months from now?

24

555953

Q2 2017 Q3 2017 Q4 2017 Q1 2018 Q2 2018 Q3 2018 Q4 2018 Q1 2019 Q2 2019 Q3 2019 Q4 2019 Q1 2020 Q2 2020 Q3 2020 Q4 2020 Q1 2021 Q2 2021

Overall Franchise IndependentNote: Scale 1 - 100

Note: New question introduced Q2 2021

25

Factors Holding Back Your Business?

Significant decrease vs previous quarter

Significant increase vs previous quarter

Dealer Sentiment IndexS E C O N D Q U A R T E R 2 0 2 1

OVE

RA

LL R

AN

K

Q2 '21 Q1 ’21 Q2 '201 Limited Inventory 64% 43% 26%

2 Market Conditions 34% 38% 49%

3 Business Impacts From COVID-19/Coronavirus 28% 46% 75%

4 Economy 24% 42% 60%

5 Expenses 19% 21% 18%

6 Political Climate 18% 36% 22%

7 Competition 15% 20% 12%

8 Credit Availability for Consumers 14% 18% 22%

9 Consumer Confidence 8% 25% 42%

10 Staff Turnover 8% 7% 5%

11 Regulations 6% 9% 12%

12 Consumer Transparency in Pricing 4% 5% 5%

13 Tariffs on Imported Vehicles and Parts 4% 2% 2%

14 Credit Availability for Business 4% 6% 9%

15 Weather 3% 17% 5%

16 Interest Rates 3% 3% 2%

17 OEM Mandates/Restrictions 3% 2% 2%

Dealer Sentiment Index Q2 2021

Q2 ‘1933%40%

N/A

N/A

29%N/A

35%

31%

13%

12%

7%

12%

4%

6%N/A

16%

4%

26

Factors Holding Back Your Business?

Significant decrease vs previous quarter

Significant increase vs previous quarter

OVE

RA

LL R

AN

K

Q2 '21 Q1 ’21 Q2 '2018 Dealership Systems/Tools 3% 2% 2%

19 Lack of Consumer Incentives From My OEM 2% 3% 3%

20 Technology to Support Sales 2% 2% 3%

21 Technology to Support Operations 2% 2% 1%

22 OEM Priorities 2% 2% 2%

23 Too Much Retail Inventory 1% 2% 6%

Dealer Sentiment Index Q2 2021

Dealer Sentiment IndexS E C O N D Q U A R T E R 2 0 2 1

Q2 ‘195%N/A

N/A

N/A

N/A

7%

27

Factors Holding Back Your Business?

Significant decrease vs previous quarter

Significant increase vs previous quarter

Q2 '21 Q1 ’21 Q2 '201 Limited Inventory 67% 41% 15%

2 Business Impacts From COVID-19/Coronavirus 25% 42% 72%

3 Market Conditions 24% 31% 45%

4 Political Climate 19% 38% 23%

5 Economy 19% 36% 53%

6 Staff Turnover 14% 10% 9%

7 Expenses 11% 10% 13%

8 OEM Mandates/Restrictions 10% 7% 8%

9 Lack of Consumer Incentives From My OEM 10% 13% 12%

10 Competition 8% 18% 10%

11 OEM Priorities 8% 7% 7%

12 Consumer Confidence 8% 25% 38%

13 Credit Availability for Consumers 6% 9% 8%

14 Regulations 6% 7% 14%

15 Weather 4% 20% 6%

16 Tariffs on Imported Vehicles and Parts 4% 3% 2%

17 Dealership Systems/Tools 3% 2% 1%

FRA

NC

HIS

ED D

EALE

RS

Dealer Sentiment Index Q2 2021

Dealer Sentiment IndexS E C O N D Q U A R T E R 2 0 2 1

Q2 ‘1919%

N/A

39%

N/A

N/A

25%

21%

17%N/A

37%N/A

22%

23%

4%N/A

6%

7%

28

Factors Holding Back Your Business?

Significant decrease vs previous quarter

Significant increase vs previous quarter

Q2 '21 Q1 ’21 Q2 '2018 Interest Rates 3% 2% 2%

19 Consumer Transparency in Pricing 2% 4% 3%

20 Technology to Support Operations 2% 1% 1%

21 Credit Availability for Business 2% 1% 2%

22 Technology to Support Sales 1% 2% 2%

23 Too Much Retail Inventory 1% 0% 4%

FRA

NC

HIS

ED D

EALE

RS

Dealer Sentiment Index Q2 2021

Dealer Sentiment IndexS E C O N D Q U A R T E R 2 0 2 1

Q2 ‘1926%

12%N/A

1%N/A

6%

29

Factors Holding Back Your Business?

Significant decrease vs previous quarter

Significant increase vs previous quarter

Q2 '21 Q1 ’21 Q2 '201 Limited Inventory 63% 43% 29%

2 Market Conditions 38% 40% 50%

3 Business Impacts From COVID-19/Coronavirus 29% 48% 76%

4 Economy 25% 44% 62%

5 Expenses 21% 25% 20%

6 Political Climate 17% 36% 22%

7 Competition 17% 21% 13%

8 Credit Availability for Consumers 16% 21% 27%

9 Consumer Confidence 9% 26% 43%

10 Staff Turnover 7% 6% 4%

11 Regulations 6% 10% 11%

12 Credit Availability for Business 5% 7% 11%

13 Consumer Transparency in Pricing 5% 6% 6%

14 Tariffs on Imported Vehicles and Parts 4% 1% 3%IND

EPEN

DEN

T D

EALE

RS

Dealer Sentiment Index Q2 2021

Dealer Sentiment IndexS E C O N D Q U A R T E R 2 0 2 1

Q2 ‘1938%

40%

N/A

N/A

31%

N/A

34%

33%

11%

7%

8%

7%

13%

4%

30

Factors Holding Back Your Business?

Significant decrease vs previous quarter

Significant increase vs previous quarter

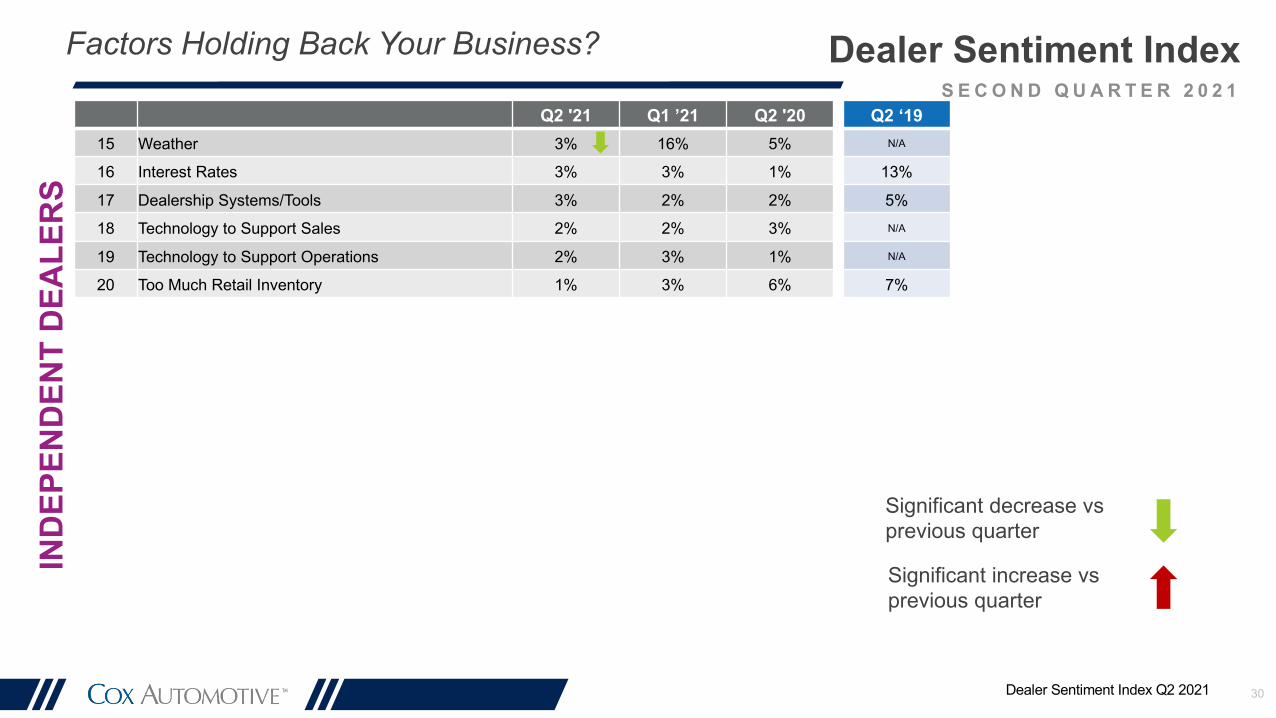

Q2 '21 Q1 ’21 Q2 '2015 Weather 3% 16% 5%

16 Interest Rates 3% 3% 1%

17 Dealership Systems/Tools 3% 2% 2%

18 Technology to Support Sales 2% 2% 3%

19 Technology to Support Operations 2% 3% 1%

20 Too Much Retail Inventory 1% 3% 6%

IND

EPEN

DEN

T D

EALE

RS

Dealer Sentiment Index Q2 2021

Dealer Sentiment IndexS E C O N D Q U A R T E R 2 0 2 1

Q2 ‘19N/A

13%

5%N/A

N/A

7%

The Business Impact of COVID-19

31Dealer Sentiment Index Q2 2021

Dealer Sentiment IndexS E C O N D Q U A R T E R 2 0 2 1

Dealer Sentiment Index Q2 2021

Strong

Weak

4845 46

49 51 51

4448 49 48 47 49

20

56

49 49

67

54 55 54 55 5659

51 5054 56

5155

30

68

61 61

77

4642 43

4750 48

4247 48 46 46 47

17

53

46 45

63

Q2 2017 Q3 2017 Q4 2017 Q1 2018 Q2 2018 Q3 2018 Q4 2018 Q1 2019 Q2 2019 Q3 2019 Q4 2019 Q1 2020 Q2 2020 Q3 2020 Q4 2020 Q1 2021 Q2 2021

Overall Franchise Independent

Q1: How would you describe the current market for vehicles in the areas where you operate?

32

Note: Scale 1 - 100

Dealer Sentiment IndexS E C O N D Q U A R T E R 2 0 2 1

Dealer Sentiment Index Q2 2021

Strong

Weak

Q2: What do you expect the market for vehicles in your area to look like 3 months from now?

33

5552 53

70

56 57

49

63

5551 51

63

4550 48

596364

57 57

7369

61

54

62 6257

54

66

5760 58

6874

52 51 52

70

5255

47

63

5249 51

61

4046 44

5659

Q2 2017 Q3 2017 Q4 2017 Q1 2018 Q2 2018 Q3 2018 Q4 2018 Q1 2019 Q2 2019 Q3 2019 Q4 2019 Q1 2020 Q2 2020 Q3 2020 Q4 2020 Q1 2021 Q2 2021

Overall Franchise IndependentNote: Scale 1 - 100

Dealer Sentiment IndexS E C O N D Q U A R T E R 2 0 2 1

Dealer Sentiment Index Q2 2021 34

Top Priorities at This Time

Overall Franchised (A) Independent (B) High Tax States (A)

All Other States (B)

Q2 2021 Q1 2021 Q2 2021 Q1 2021 Q2 2021 Q1 2021 Q2 2021 Q1 2021 Q2 2021 Q1 2021

Finding/Buying inventory 53% 34% 44% 20% 55% A 38% A 46% 27% 54% 35% A

Staying in business in general 14% 23% 5% 9% 17% A 28% A 16% 29% B 13% 22%

Retaining customers 7% 8% 13% B 16% B 5% 5% 3% 7% 8% A 8%

Improving efficiency in general 6% 10% 10% B 18% B 5% 7% 6% 8% 6% 10%

Improving Sales and Service solutions 5% 9% 8% B 10% 4% 8% 12% B 10% 4% 8%

Reducing expenses by cutting unnecessary costs 4% 6% 3% 5% 5% 6% 4% 10% B 4% 5%

Gaining market share 4% 7% 9% B 16% B 2% 4% 2% 5% 4% 8%

Retaining employees 3% 3% 5% B 5% B 2% 2% 3% 3% 3% 3%

Selling the dealership* 1% N/A 0% N/A 2% N/A 1% N/A 1% N/A

Acquiring other storefronts* 1% N/A 0% N/A 1% N/A 1% N/A 1% N/A

Other 2% 1% 3% 1% 2% 1% 6% B 1% 2% 1%

A/B indicates significant difference between groups at the 95% confidence level

GREEN: Significant increase from prior quarterRED: Significant decrease from prior quarter*option added in Q2 2021

Dealer Sentiment IndexS E C O N D Q U A R T E R 2 0 2 1

Dealer Sentiment Index Q2 2021 35

Regional View – Index Scores (Franchised Dealers)

Question Answer North-east

Mid-west South West

Current Market Strong/Weak 76 78 78 74

Market Next 3 Months Strong/Weak 71 72 77 77

Customer Traffic Strong/Weak 69 77 73 67

Profits Strong/Weak 79 86 84 76

Dealer Credit Easy/Difficult 62 65 68 67

Costs Growing/Declining 61 62 59 66

New Vehicle Sales Good/Poor 67 61 69 64

New Vehicle Inventory Growing/Declining 14 10 14 16

New Vehicle Inventory Mix Good/Poor 38 28 34 35Note: Scale 1 – 100GREEN: Significant increase from prior quarterRED: Significant decrease from prior quarter

Dealer Sentiment IndexS E C O N D Q U A R T E R 2 0 2 1

Dealer Sentiment Index Q2 2021 36

Regional View – Index Scores (Franchised Dealers)

Question Answer North-east

Mid-west South West

Used Vehicle Sales Good/Poor 78 77 77 75

Used Vehicle Inventory Growing/Declining 29 21 27 24

Used Vehicle Inventory Mix Good/Poor 55 48 48 46

Price Pressure More/Less 24 20 23 26

Staffing Growing/Declining 53 51 49 51

OEM incentives Large/Small 42 43 43 41

Economy Strong/Weak 60 61 59 62

Current Fixed Operations Better/Worse 71 75 74 75

Future Fixed Operations Growing/Declining 74 70 79 73

Current BEV Sales Better/Worse 58 56 49 59

Future BEV Sales Growing/Declining 64 59 53 63

Note: Scale 1 – 100GREEN: Significant increase from prior quarterRED: Significant decrease from prior quarter

37

Contact Information:

Dara HailesManager, Public RelationsCox [email protected]

Mark SchirmerDirector, Public RelationsCox [email protected]

Dealer Sentiment IndexS E C O N D Q U A R T E R 2 0 2 1

37Dealer Sentiment Index Q2 2021