Embed Size (px)

Citation preview

Bureau of Agricultural Economics, Canberra

A BAE submission to the IAC

Project 41341

WHEAT MARKETING AND ASSISTANCE

Australian Government Publishing Service Canberra 1987

0 Commonwealth of Australia

This work is copyright. As permitted under the Copyright Act - which allows fair dealings for the purpose of study, research, criticism or review - selected passages, tables or diagrams may be reproduced provided that due acknowledgment is made. However, the entire document or major sections may not be reproduced by any process without written permission. Copyright is the responsibility of the Director Publishing and Marketing, AGPS. Inquiries should be directed to the Manager, AGPS Press, Australian Government Publishing Service, GPO Box 84, Canberra ACT 2601.

ISSN 0814-9445 ISBN 0 644 06805 1

The inquiry into the wheat industry by the Industries Assistance Commission is an initial step in considering the wheat marketing arrangements to apply after June 1989, when the provisions of the current Wheat Marketing Act 1984 expire. The Commission is required to report by 26 February 1988, soon after the reporting date of the Royal Commission into Grain Storage, Handling and Transport to which the Bureau submitted evidence in April 1987.

The Bureau's submission concentrates on aspects of wheat marketing, both domestic and export, and assistance, in particular market support arrangements. Thus, the submission is broad ranging but does not include analysis of the distribution system, which was the subject of the Bureau's recently published Occasional Paper, Institutional Arrangements in the Wheat Distribution System.

The preparation of this submission was carried out under the general direction of Roger Rose by Rhonda Treadwell, Graham Love, Paul Gavel, Peter Gillard, Meng Chang, Mike Hinchy and Peter Sniekers of the Crop Marketing and Outlook Branch.

ROBERT BAIN Director

Bureau of Agricultural Economics Canberra ACT

August 1987

iii

CONTENTS

Summary and Recommendations

1. Introduction

1.1 Background 1.2 Scope and aims of the submission 1.3 Current marketing and payment arrangements 1.4 The distribution system 1.5 Industry outlook 1.6 Farm incomes

2. Wheat Payment Arrangements

2.1 Implications of revenue pooling 2.2 Implications of cost pooling 2.3 Evaluation of current payment system

3. Domestic Wheat Marketing

3.1 Characteristics of the domestic wheat market 3.2 Analysis of current marketing arrangements 3.3 Arguments against competition 3.4 Effects of introducing competition

4. Export Marketing

4.1 The international wheat market 4.2 Arguments for the current arrangements 4.3 Effects of competitive exporting 4.4 Implications of change in wheat marketing and distribution

5. Assistance

5.1 Underwriting 5.2 Research funding 5.3 Alternative policies

Appendix A: Estimation of Permit Wheat Price Range and Savings

References

Figures

1 Australian wheat production, exports and closing stocks

2 Farm income of family farms

3 Real farm business debt

4 Australian Wheat Board domestic wheat sales

5 Sales and price of industrial wheat

Tables

1 Australian wheat production, domestic sales and exports

2 Wheat and other crops industry: financial performance measures, by state and all broadacre industries for Australia

3 Domestic off-farm marketing costs

4 Illustrative financing costs for various wheat categories

5 Advance payments

6 Off-farm liquid assets, wheat and other crops

7 Alternative wheat payment arrangements

8 Domestic and export use of wheat

9 National flour usage

10 Wheat exports as a proportion of world trade

11 Relative unit returns to wheat exports, by market group

A1 Savings to Victorian permit wheat buyers

A2 Savings to New South Wales permit wheat buyers

A3 Savings to Victorian growers from selling permit wheat

A4 Savings to New South Wales growers from selling permit wheat

WHEAT MARKETING AND ASSISTANCE

SUMMARY AND RECOMMENDATIONS

On 30 June 1989 the current (eighth) wheat marketing scheme is scheduled to expire, having been enacted in late October 1984 for the five years commencing with the 1984-85 season. As previously, the Commonwealth Government has instructed the Industries Assistance Commission to inquire into and report on assistance and marketing arrangements as they relate to the Australian wheat industry, as a basis on which to consider whether to extend or change the scheme.

Scrutiny of the current marketing arrangements leads to the conclusion that the current scheme has four primary objectives: equity, efficiency, the provision of price insurance and assistance through government underwriting, and the maintenance of a controlled marketing environment. The aim of this submission is to evaluate the marketing and assistance arrangements in terms of efficiency.

Wheat marketing is controlled by the Australian Wheat Board. The Board is the sole receiver and marketing agent for all wheat exported and for most wheat sold in Australia (that is, for all wheat other than that sold under permit or by authorisation). Concurrent with the Commission inquiry, a Royal Commission is inquiring into the storage, handling and transport of grain with the aim of recommending how to achieve an efficient distribution system. Following a major study, the Bureau has put forward three options for improving the distribution system. Two of these options involve the adoption of a competitive distribution system which would lead to substantial improvements in efficiency in grain distribution. This report addresses the marketing and assistance arrangements not covered in that study .

Industry situation

During the 1980s a decline in wheat import demand, together with US and EC support policies, resulted in falling wheat prices and an accumulation of wheat stocks in the United States and elsewhere. As a result of these falling prices Australian production of wheat has declined from the record 22 Mt in 1983-84 to around 16 Mt in 1985-86 and 1986-87. Despite this fall, the volume of exports reached a peak of 16 Mt in the latter two years due to the sale of large wheat stocks. Over the next few years it is probable that the Australian wheat industry will have an annual output below 14 Mt, exports of 11-12 Mt, a guaranteed minimum price for Australian standard white (ASW) wheat of less than $135/t, and an average net return to growers of around $95/t. In the medium term, as long as world stocks remain high relative to use, low wheat prices are likely to persist, and a further decline in wheat production from the 1987 level will be experienced in Australia. In the longer term a price recovery is possible as unprotected producers voluntarily lower production and the European and US governments restrain production due to the high and rising costs of their support policies.

Incomes of wheat farms have fallen consistently since 1983-84 to an estimated average of zero in 1986-87. While depreciation of the Australian dollar has, in the recent past, shielded growers to some extent from the sharp decline in world wheat prices, rising costs of marketing, inputs and interest have had an adverse effect on incomes. In the short term, wheat and

other crop farmers face great financial pressures due to declining farm incomes and land values coupled with rising debt levels and interest costs.

Payment and charpinp arrangements

The pooling of revenues and costs is a tradition of marketing arrangements for Australian wheat. Pooling is applied over time, location and quality. Pooling of revenues results in wheat growers being paid the average return from the sale of the season's wheat within the category delivered. Pooling over time spreads the risk of price fluctuations over the selling period for the crop. Such pooling will lead to inefficiency only if the selling period is very long - as it is under the current pooling arrangements .

Although different prices have been allowed for six categories of wheat since 1984, payments are still averaged across broad quality ranges within these categories. For example, growers of around 70 per cent of Australia's wheat crop are paid the pooled price for ASW wheat, although a number of selling categories are distinguished within this class. Pooling across such broad quality ranges discourages production of higher quality, higher priced wheat in favour of lower quality, higher yielding wheats. This problem has been recognised by the Australian Wheat Board, which is planning to introduce several payment categories for ASW wheat of differing quality, based on protein content. For the fullest transmission of price signals to growers, the quality categories for payment should be the same as those for sale.

Costs are pooled at the national, state or regional level; costs are pooled across classes of wheat, areas of production, and markets, and over the period of time that marketing costs are incurred on each year's crop. Pooling of costs eliminates incentives to minimise costs, as the charges paid by growers do not correspond to the costs of their own actions. As the Bureau's recent study of wheat distribution concluded, widespread pooling of distribution costs should be discontinued. This conclusion is equally applicable to the national pooling of the Wheat Board's marketing and finance costs. Charges for marketing a grower's wheat should be, as far as is practicable, the actual costs incurred.

The elimination of pooling would improve the signals reaching growers on the actual market returns from their wheat and the costs of distributing and marketing it. This would result in growers adjusting their production decisions in accordance with changes in the market and would give incentives for the minimisation of costs to those who have control over these costs.

A major problem with the current system of advance payments is that it forces on all growers the same borrowing regimen, despite differences in their cash flow requirements and variations in opportunity costs of grower funds. The deferred payment options under the current arrangements offer some flexibility in borrowing, but only in relation to timing. Current arrangements dictate that the grower - who may not in fact need to borrow the amount of the advance payment - must incur the loss of any difference between the Wheat Board's borrowing costs and the return on the grower's own investment of funds. A voluntary advance payment system would give growers more control of their finances by offering choices on both the timing and the amount of the advance payment. (Such a scheme would, however, incur higher administrative costs than the current system.)

Advance payment to growers provides them with a borrowing subsidy. This provision of relatively cheap funds to wheat growers will result in the misallocation of funds in the economy from investments with higher or less risky returns.

When growers deliver wheat to the Wheat Board, that wheat does not assume a value immediately but has some likely future sales value. Accordingly, while growers should be able to use this asset as collateral for borrowings, they should not expect to be paid the sale value of the wheat immediately. A procedure which would overcome the above problems would be to issue, on delivery, negotiable certificates detailing the quality and quantity of the wheat, and subsequently to pay growers after the sales have been made. The certificates should be freely negotiable and usable as collateral for borrowings by the grower.

Domestic marketing

With an average of 2.2 Mt of sales a year, the domestic market is small in relation to exports, which are about 14-15 Mt a year. Since 1939, domestic marketing of wheat has been controlled by the Wheat Board. Domestic wheat prices are set administratively on the basis of the Board's export price quotes. In addition, all buyers of wheat for human consumption are charged $16/t to cover the Board's cost of servicing this market. This flat per-tonne margin leads to cross subsidisation between millers and provides no incentive for an individual miller to minimise the cost of services. A competitive market would overcome these problems by allowing the price mechanism to determine the value of services and wheat prices.

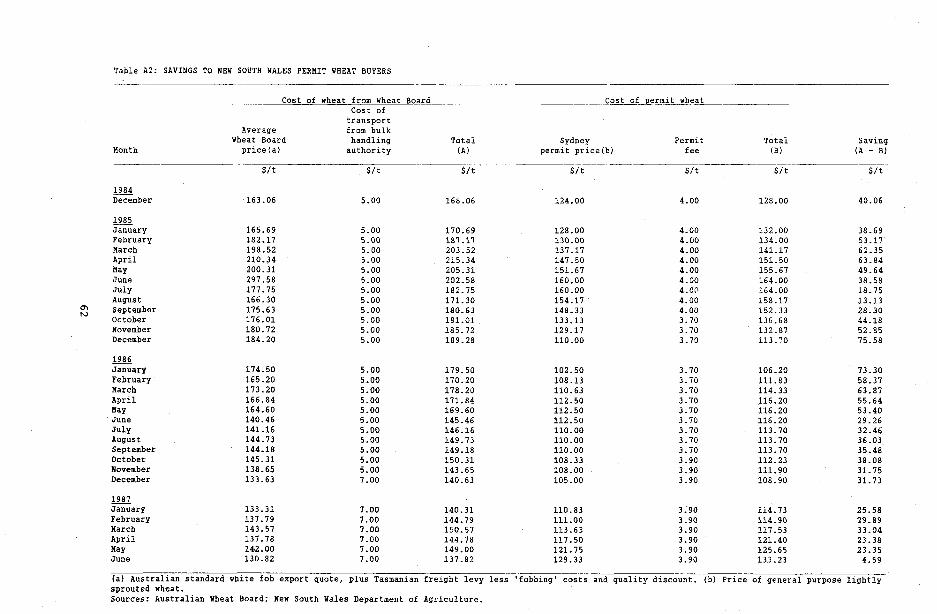

Current legislation allows, under permit, private trade in feed wheat, and around three-quarters of feed wheat is now sold in this way. It has been estimated in the present study that, through permit trading, growers and buyers have gained significant savings, mainly from the avoidance of unnecessary handling, transport and administration costs.

Arguments advanced in favour of monopoly control of domestic marketing appear unjustified. Since production and consumption of wheat are dispersed, it is unlikely that there are significant economies of scale in the domestic marketing of wheat. Long term sales contracts could be used to guarantee to millers the continuity of supply they require; this continuity is not dependent on the existence of a central marketing authority. Grain hygiene could be maintained after the introduction of competition in domestic marketing and distribution through a system of licencing and inspection of country storages , together with the incentives provided by the price mechanism.

The operation of a competitive domestic market would be similar to that of the existing markets for livestock and some other grains, which operate effectively without compulsory acquisition of the products or compulsory centralised marketing. Allowing competition in domestic marketing would result in a better distribution system, capable of adapting to changing market circumstances. Widespread revenue and cost pooling would not survive in a competitive market; growers would receive the correct market signals concerning their wheat and would pay according to the services used, leading to more efficient production decisions.

Competition in domestic marketing offers the prospect of real benefits to wheat growers and users through reduced marketing and distribution costs and improved grower awareness of the market values of wheat qualities. The

distribution of these gains between growers, merchants, manufacturers and consumers will depend on their relative market power and the responsiveness of supply and demand to price. As has been the case in permit trading of feed wheat, growers are likely to appropriate a smaller share of these gains than buyers. Nevertheless, with the option of delivery to the Wheat Board pool, growers would certainly do no worse than under the current arrangements, and would be likely to reap some benefits.

All wheat sold on the domestic market is subject to the Tasmanian freight levy, which is designed to cover the Board's costs in shipping wheat from selected mainland ports to Tasmania. There appears to be little economic justification for this subsidy, or for its being paid by wheat growers and users rather than by all taxpayers.

Export marketing

The Wheat Board has total control of the export marketing of all Australian wheat, and sells directly to governments or their agents as well as to international grain traders. As most of Australia's wheat is exported, the method of export marketing is crucial. In exporting, unlike domestic marketing, it cannot be decided on the available information whether the present Wheat Board monopoly or competitive export marketing would achieve the higher net return for Australia's wheat exports.

Of the arguments advanced in favour of monopoly control of export marketing of Australia's wheat crop, none presents a real advantage over a competitive marketing system. For example, if there are substantial economies of scale in international marketing, these could be realised in a competitive environment, as indeed they are being realised by international grain traders. There is little evidence of the Wheat Board using market power to increase returns to growers. Grain hygiene could be maintained without centralised control of distribution and export marketing, though it is unclear whether the costs of pest control would in that case be higher. On the other hand, competitive marketing has the advantage of providing effective incentives for good performance, whereas the current arrangements can be expected only to discourage poor performance, through the Wheat Board's public accountability requirements. Without a competitive tendering process the efficiency of the Wheat Board cannot be gauged nor ensured. Increased use of open, unrestricted tenders would give an added incentive for the efficient marketing of wheat.

If competition were allowed in export marketing, one effect would be that the potential savings from allowing competition in distribution and domestic marketing would be fully realised, by fostering a more competitive environment in every aspect of wheat marketing and distribution. If the Board were to retain its export monopoly, these potential savings could still be achieved provided that the Board were required to use competitive tenders to acquire the distribution services. With competition in wheat marketing (both domestic and export) the distortionary practice of widespread pooling of costs and revenues could not survive. Consequently, growers would have more accurate information on market returns for their wheat, which would lead to more efficient production decisions and facilitate adjustments to changing market circumstances.

Assistance

Price underwriting is the main form of assistance to the wheat industry. Under this scheme the Government guarantees early payment of a minimum price

t o wheat producers. There are several r i s k s tha t are o f concern t o wheat growers, tha t o f income f luc tua t ion being o f prime importance. Underwriting reduces the r i s k o f price var ia t ions over t ime but i s no t e f f e c t i v e i n reducing the r i s k o f income f luc tua t ions from other causes, and can i n f ac t increase such f luc tua t ions . This i s true whether the underwriting scheme i s financed by government o r growers.

The problem i s tha t the underwriting o f wheat prices may cause resources t o be diverted t o wheat growing, espec ia l ly i n times o f low pr ices . There are other measures which curren t ly ac t t o reduce t he r i s k o f income f luc tua t ions t o wheat growers. The Export Finance Insurance Corporation addresses the p o s s i b i l i t y o f imperfections i n t he insurance market by o f f e r i n g addi t ional insurance against de fau l t by overseas c red i t buyers o f wheat. This scheme would s t i l l be avai lable i f marketing o f wheat were open t o competit ion.

The current provisions o f the Rural Adjustment Scheme make assis tance avai lable t o po t en t i a l l y v iab le farmers who would face bankruptcy i f forced t o r e l y on commercial lenders . Such a pol icy a t tacks the most fundamental problem tha t a r i s e s i f (as i s the case) r i s k markets are incomplete. Furthermore, un l ike underwriting, assis tance under the scheme i s avai lable when and where i t i s most needed. Given the l e ve l o f funding, it i s o f b e n e f i t only a t the margin. F ina l ly , s ince the scheme appl ies uniformly across i ndus t r i e s , it w i l l no t d i s t o r t resource a l loca t ion as s e l ec t i v e underwriting can.

Currently the Commonwealth Government funds wheat research t o the same amount as growers contr ibute . Total research funding by growers and the Commonwealth Government a t present amounts t o l e s s than 0.5 per cent o f the wheat indus t ry ' s gross value o f production, which i s l e s s than the l e v e l s f o r the wool and l i ves tock i ndus t r i e s . Funding f o r wheat research could be increased subs tan t ia l ly t o achieve alignment wi th these o ther broadacre i ndus t r i e s .

Recommendations

In t h i s submission i t has been demonstrated tha t there i s scope for i n e f f i c i e n c y i n the current marketing arrangements. Growers may n o t , i n consequence, be receiving the highest returns f o r t h e i r wheat, and the arrangements are no t s u f f i c i e n t l y f l e x i b l e t o f a c i l i t a t e adequate adjustment t o changing market circumstances. Changes t o the current arrangements are necessary t o encourage the highest l e ve l o f e f f i c i e n c y i n wheat marketing, d i s t r i bu t i on and production.

Marketing arrangements

Competition i n the domestic marketing and d i s t r i bu t i on o f wheat should be allowed, as t h i s would o f f e r rea l savings and r e s u l t i n a system be t t e r able t o adapt quickly t o changing market circumstances. The Tasmanian f r e igh t subsidy and l e v y on growers should be stopped, as it d i s t o r t s the pat tern o f wheat use .

The Wheat Board's monopoly control over export marketing should be re ta ined , s ince it i s not proven tha t allowing competit ion would r e s u l t i n ne t b e n e f i t s . To increase the e f f i c i e n c y and f l e x i b i l i t y o f wheat marketing t he Board should, however, be required t o make a number o f changes t o i t s operations. The Board should:

- increase the use of open, unrestricted competitive tenders for wheat designated for resale through international grain traders;

- accept Australian wheat for sale from anyone in the domestic market;

- use an open, competitive tendering process to obtain distribution services;

- restrict pooling of revenues, by closing annual pools at the start of the next season and increasing the number of grades for payment;

- discontinue cost pooling, for both distribution and marketing costs, wherever practicable; and

- replace the current payment system with a scheme whereby growers would be given on delivery a certificate detailing the quality and quantity of their wheat; these certificates should be freely negotiable and acceptable as collateral for borrowings.

Assistance

The level of assistance to the wheat industry should be approximately equal to that for other broadacre industries, to avoid misallocation of resources within the broadacre sector. If underwriting is retained, the underwritten price should be based on gross market returns, so that marketing costs are not underwritten. If competition is allowed in domestic and/or export marketing, a deficiency payment scheme operated by a government agency (not the Wheat Board) should be used.

Underwriting should, however, be discontinued, as it is not effective in reducing income risk and can cause resources to be misallocated, particularly within the broadacre industries. If underwriting is discontinued, assistance through wheat research funding should be increased to a level similar to that provided to other broadacre industries. With competition in domestic marketing, the method of col l ec ting growers ' research levies would need to be changed to either collection by end users in the domestic market and by the Wheat Board on export sales, or collection by all merchants including the Board.

1. INTRODUCTION

The current (eighth) five-year wheat marketing scheme, enacted in late October 1984, is scheduled to expire on 30 June 1989. As was done for earlier plans, the Commonwealth Government has instructed the Industries Assistance Commission to inquire into and report on assistance and marketing arrangements for the Australian wheat industry in preparation for enacting the ninth such scheme.

The terms of reference for the inquiry again call for a report on the nature, extent and duration of any assistance that should be accorded to the wheat industry, for the five years commencing with the 1989-90 season. In particular, the Commission has been instructed to report on the effects that the agricultural support policies of major wheat producing countries have had on international wheat markets and the Australian wheat industry. In doing so, the Commission is to determine whether changes occurring within the industry will be of sufficient magnitude and duration as to warrant adjustment to government policies affecting the Australian wheat industry. If adjustment is deemed necessary, the Commission is to recommend the rate at which it should occur, taking into account the industry's capacity to adjust in the current economic climate.

1.1 Background -

The broad objectives of the wheat marketing arrangements have changed little over the years, but the emphasis placed on each objective has varied. Since the sixth scheme greater effort has been made to relate domestic prices to export market prices. A deliberate shift occurred in the seventh scheme, when greater emphasis was placed on reducing risk through guaranteeing minimum prices rather than maintaining price stability. All modifications to the marketing arrangements have occurred within a centrally controlled marketing system, operated by the Australian Wheat Board. The Board has identified its own main objective as the development of an efficient marketing framework and the maximisation of returns to growers (Australian Wheat Board 1986a).

Miller and White (1980) have referred to a confusion of objectives, and Watson (1984) has noted that this confusion is likely to persist because of the different attitudes of those affected by policy outcomes. The objectives behind each wheat marketing scheme have never been precisely specified. As a result, the nature of the underlying purposes is open to interpretation.

The Bureau of Agricultural Economics (1983) summarised the underlying objectives of previous wheat schemes as equity, stabilisation and the provision of assistance. However, it was noted that these objectives were losing some of their relevance due to increased dependence on the export market, increased variability in export prices and an increasing awareness of the inefficiencies associated with controlled marketing. From an examination of the institutional arrangements specified in the Wheat Marketing Act 1984, the main objectives of the current scheme can be interpreted as equity, the provision of price insurance and government assistance through public underwriting, the efficient marketing of Australian wheat and the maintenance of a controlled marketing environment.

1.2 Scope and Aims of the Submission

The principal aim of this submission is to evaluate the marketing and assistance arrangements, in terms of their adaptability to changing market conditions and their efficiency in relation both to obtaining the highest net return and to providing the correct market signals to growers. Four key aspects of the current wheat marketing and assistance arrangements are examined, namely the payment arrangements, domestic marketing, export marketing and assistance.

The first aspect addressed (section 2) is the arrangements by which growers receive payment and are charged marketing and distribution costs for wheat delivered to the Australian Wheat Board. In this connection the first question to be examined is whether the current practice of pooling payments and costs reduces efficiency. Second, the current arrangement of advance payments is evaluated in regard to efficiency and ease of adjustment to changing market circumstances.

In section 3, domestic marketing arrangements are evaluated. The current arrangements are compared with a competitive marketing system as regards their effect on efficiency of marketing and returns to growers.

The third aspect, examined in section 4, is export marketing. In the highly competitive world wheat market, efficient and effective export marketing is essential. Changes have occurred in the market that are highly unfavourable for Australia. The question addressed in section 4 is how to maximise returns to growers from export wheat. The importance of removing self-imposed impediments to performance is critical. The questions of how to position the Wheat Board in the market and to organise export marketing of wheat in order as to maximise returns to Australian growers are examined. The effects of alternative arrangements in the distribution system and domestic marketing are also considered.

The provision of government assistance to wheat growers is the final aspect addressed. The effect of assistance on efficiency in the wheat industry and the Australian economy generally is examined, with particular attention to the appropriateness of providing such assistance in the present forms, namely through underwriting of grower returns and research funding.

1.3 Current Marketing and Payment Arrangements

The acquisition and marketing of Australian wheat is at present governed by the Wheat Marketing Act 1984, which applies to the seasons 1984-85 to 1988-89 inclusive. In Australia, wheat marketing is controlled by a statutory authority, the Australian Wheat Board. Under Commonwealth and complementary state legislation, the Board is the sole receiver and marketing agent for most wheat sold in Australia, and for all wheat exported. Delivery of wheat to the Board is made by delivering to an authorised receiver, which is the bulk handling authority in each state.

Costs and revenues arising from marketing wheat are pooled - most distribution costs on a state basis, and marketing costs and revenue on a national basis. Growers receive an averaged payment for the wheat they deliver, but (since 1984-85) with different rates of payment for Australian standard white (ASW) and five other categories.

The Commonwealth Government underwrites growers' returns through a guaranteed minimum price. Here again, unlike previous wheat marketing arrangements, the Wheat Marketing Act 1984 provides different minimum payments for ASW and other categories of wheat, whereas previously all wheat was underwritten to ASW value only. The ASW category - into which typically about 70 per cent of national receivals are accepted - is the benchmark from which differentials for other wheats are calculated (Australian Wheat Board 1986b). The ASW guaranteed minimum price is calculated as 95 per cent of the average of the ASW gross pool return for the current season and the two lowest of the previous three seasons, less the Wheat Board's costs. Since the guaranteed minimum price is calculated net of Wheat Board costs, it also tends to underwrite these costs.

For the 1986-87 season, six categories have been identified for payment purposes. They are prime hard (Al), hard (A2), ASW (B), general purpose 1 - lightweight (C), general purpose 2 - weather-damaged (D) and feed wheat (E). Within the A1 and A2 categories, various grades are defined in terms of protein level, between which there are further price differentials. Varietal dockages are applied within the Al, A2 and B categories to discourage the production of certain wheat varieties. Discounts are levied on deliveries that are weather damaged and/or contaminated by foreign materials.

The preliminary guaranteed minimum price for each of the six categories is determined around August. The forecast pool return net of Wheat Board costs is used in this preliminary calculation. Final guaranteed minimum prices are calculated in the following February when better information on likely market returns becomes available.

Growers receive an advance payment, in two instalments. The first (interim) advance is 90 per cent of the preliminary guaranteed minimum price for the category of wheat delivered, less storage, handling and transport costs. This payment is usually made within three weeks of wheat delivery to the bulk handling authority. Most growers receive their second (final) advance payment in March. The sum of the interim and final advance payments is the final guaranteed minimum price. Where the realised net return from wheat sales exceeds the sum of the advance payments the balance is distributed to growers in a series of subsequent payments.

Quality differences among grades within each wheat category are reflected in second, rather than first, payments. That is, every grower who delivers wheat of a certain category receives the same first payment (except for any receival dockages). Second payments, however, include adjustments made to the final guaranteed minimum prices resulting from quality differences among grades within the categories.

Three deferred payment options were also introduced in 1984-85:

. Under the first option, 35 per cent of the interim advance and 100 per cent of the final advance payment are deferred until 21 April, whereupon these amounts are paid with interest at the Australian Savings Bond rate.

. The second option is the same as the first, except that the deferral date is 21 August.

. The third option is for the final advance to be deferred until 21 August, when it is paid with interest at the Australian Savings Bond rate.

A deferred delivery option is also available, whereby growers can obtain interest on the advance payments at the Australian Savings Bond rate for deferring delivery of wheat for a period of 2-14 weeks following a 'prescribed date' for a particular silo. The prescribed date is based on a five-year average opening date for the silo.

As a proportion of total production, domestic sales of wheat produced within Australia have been declining for the past forty years. Australia has thus become more dependent on export markets for the disposal of its wheat crop (table 1). Sales of wheat on both the domestic and export markets are controlled by the Australian Wheat Board. For pricing purposes, current legislation differentiates domestic wheat sold for human consumption from that sold for industrial use and for stock feed. All domestic wheat prices are either set administratively or are at least subject to some degree of administrative oversight and control. The prices of wheat sold for human consumption are determined quarterly on the basis of the Board's export price quotes (see below) plus a fixed margin to cover the costs of services. Prices for industrial and stock feed wheat are set by the Board on the basis of its daily export price quotations, and are subject to the agreement of the Australian Agricultural Council.

Certain arrangements presently exist for growers to sell directly to buyers on the domestic market. The most flexible of these arrangements is the permit scheme for stock feed wheat. This scheme allows private trade in stock feed wheat under permits issued by the Wheat Board. The wheat is subject to only minimal administrative control and does not enter the

Table 1: AUSTRALIAN WHEAT PRODUCTION, DOMESTIC SALES AND EXPORTS(a)

Domestic sales Domestic Total as a proportion

Year Production sales Exports sales of total sales

(a) Domestic sales for 1984-85 and subsequent years include permit sales of stock feed wheat. (b) 1 December to 30 September; previous years ended 30 November, and subsequent years ended 30 September. (p) Provisional. Source: BAE (1986a, 1987a).

Board's pool. Thus, its price is not directly underwritten by the Commonwealth Government.

On the export marketing side, the Board employs a number of selling strategies which include direct sale to governments, sale to government agents or marketing authorities, sale through grain trading companies, and sale to the Commonwealth Government so that it can meet its food aid obligations. The Board sets price quotations for Australian wheat for export on each working day. These price quotes are set according to the commercial judgment of the Board, taking into consideration the world supply-demand situation as reflected in the prices offered by competing exporters, particularly the United States. Essentially, the Board bases its quoted price on that of competing US wheat, and may adjust this price to allow for such factors as exchange rates and ocean freight rates (Perkins, Sniekers and Geldard 1984). Since 1985 the presence on the market of increasingly significant quantities of subsidised wheat has had the result that often the published quote is not indicative of prices realised in many of Australia's markets.

1.4 The Distribution Svstem

Concurrent with the Commission inquiry into marketing and assistance to the wheat industry there is a Royal Commission into Grain Storage, Handling and Transport. The Bureau has recently published a report on the grain distribution system (Spriggs, Geldard, Gerardi and Treadwell 1987). The following is a summary of the main findings of that report.

In Australia the wheat distribution system is characterised by statutory monopolies established and protected from competition by Commonwealth and state legislation. These monopolies comprise the Australian Wheat Board, and bulk handling and rail authorities in each wheat exporting state. The Board receives wheat through the bulk handling authorities, which are its licensed receivers, and growers must deliver to a bulk handling authority all their wheat except that sold directly to a buyer under permit or by authorisation. A grower does not necessarily have to deliver wheat to the bulk handling authority in the same state as the wheat is grown.

The relationship between the licensed receivers and the Board is set out in the Grain Storage and Handling Agreement. This specifies the bulk handling services required by the Board from each bulk handling authority and the payment arrangements for these services. The current agreement differs from previous agreements in being more performance oriented, providing for rewards and penalties for good and poor performance.

Most wheat is transported by the rail authorities. Though rail has a cost advantage over road for long distance haulage of bulk products, in the case of wheat there are other factors which have contributed to the dominant position of rail transport. These include the lack of road receival facilities at ports (in New South Wales, for example) and legislative restrictions (as in Queensland, Victoria and Western Australia, though not interstate). With the exception of Westrail, the rail authorities are protected from competition with other railways. There are no restrictions on road transport of wheat in South Australia, which has the shortest average distance for transporting wheat and the largest proportion of wheat transported to ports by road.

Wheat is shipped from twenty ports. Each port is controlled by a statutory public authority whose role and functions are detailed in state legislation. A considerable number of these ports cannot completely load large ships, with the result that some ships have to load at two or more ports.

The current institutional arrangements governing wheat distribution have given rise to several efficiency problems. Inefficiencies in the wheat distribution system may occur due to the mixing of social (non-commercial) and efficiency goals, the inadequacy of incentives for good economic performance in the current institutional arrangements, and the fact that the organisations providing distributing services have a state rather than a national perspective. The Bureau proposed three basic options for changing the institutional arrangements to overcome these problems (Spriggs et al. 1987).

The first option was to remove non-commercial objectives and to improve incentives for efficiency in the existing statutory monopolies. Additional legislative amendments were proposed to eliminate conflict of interest on authority boards, to increase the accountability of the authorities and to improve co-ordination in the grain distribution system. It was concluded that competition would encourage increased efficiency; thus, the second option was to introduce competition to the existing statutory monopolies as well as making the changes included in the first option. The third option was to privatise the bulk handling authorities, in addition to the changes involved in the first two options.

These three broad policy options represent an ascending order of change to institutional arrangements in the grain distribution industry. In examining the marketing and assistance arrangements in the wheat industry it will be necessary to consider them in relation not only to the current institutional arrangements in the distribution system but also in relation to possible changes in the distribution system following the Royal Commission into Grain Storage, Handling and Transport.

1.5 Industrv Outlook

During the 1980s there has been a persistent imbalance between world wheat production and demand, with a consequent accumulation of stocks, particularly in the United States, the European Community and Canada. This imbalance has resulted from a decline in wheat import demand together with the persistence in the United States and Europe of support policies which have divorced the prices paid to farmers for wheat from the price realised for the same wheat on the world market. As a consequence, world wheat prices have fallen markedly (Love 1987a). The result has been falling real farm incomes in the non-subsidising export countries and, in the case of Australia, the triggering of temporary price support under the government's guaranteed minimum price arrangements. This price support, while assisting growers, has covered only part of the decline in average net returns experienced by growers from 1985-86 to 1986-87.

From the peak of almost 13 million ha in 1983-84, the area planted to wheat in Australia has declined by 13 per cent to just over 11.2 million ha in 1986-87, and is estimated to have declined further to around 9.4 million ha in 1987-88 (BAE 1987a). To date, the effect of this decline in area (and consequently in production) on export sales has been cushioned by sales from the large wheat stocks accumulated from the large 1983-84 and 1984-85

harvests (figure 1). While production has fallen, exports have risen, reaching a record 16 Mt in 1985-86.

The full effect on exports of the production decline will become apparent from the 1987-88 season. Stocks at the end of 1986-87 are expected to be close to minimum carryover levels, and exports in 1987-88 will be almost exclusively of wheat produced in that year. With 1987-88 production forecast at about 13 Kt, 1987-88 exports could be around 11 Mt, or about 28 per cent lower than in 1986-87.

The prospects for the Australian wheat industry over the next few years are for production to remain below 14 Kt, exports to be 11-12 Mt, the ASW guaranteed minimum price to be under $135/t, and average net return to growers to be in the region $90/t to $100/t. This situation will lead to a further swing away from wheat production into livestock enterprises, and a further decline of wheat as a contributor to exports and national income.

While world stock levels remain high relative to use, low wheat prices are likely to persist in the medium term and a further decline in wheat production will be experienced in Australia. In the current low price period, however, some of the adjustments required to bring world wheat supply and demand into balance are occurring. The high and rising costs of US and EC price support policies are encouraging these countries to restrain production. Low prices are gradually building a recovery in world wheat import demand and reducing the incentive of countries to use the export market for the disposal of occasional surpluses as they strive for self- sufficiency (Love 1987b). For a traditional wheat producer such as Australia, survival through the current market recession and ability to take advantage of any future market recovery will depend on removing any self- imposed impediments to efficient wheat production, distribution and marketing.

Figure 1: AUSTRALIAN WHEAT PRODUCTION, EXPORTS AND CLOSING STOCKS 25-

Production

20-

B...

15-

1°-

+c--- .. Exports C---,-----C-- ----_. a... S.

.S* .. ... .. .S.. . S..

S..

. S . . . Closing stocks

5-

Mt

Minimum closing stocks - a . . . . . . . ....... . .... .. . - ----

I I I l 1983 1984 1985 1986 1987 - 84 -85 -86 -87(~) -88(f)

(f) Forecast. (p) Preliminary. Source: BAE (1987a).

1.6 Farm Incomes

The challenge involved in maintaining a viable wheat industry becomes obvious when recent data on wheat farm income and debt are examined. Falling cereal prices and rising farm input prices and off-farm marketing costs have resulted in estimated average incomes of wheat and other crop farms falling to zero in 1986-87 (see figure 2 and revised 1986-87 projections in table 2). Negative farm incomes have become increasingly prevalent over the past few years, with 55 per cent of wheat and other crop farms having negative farm incomes in 1985-86 compared with only 15 per cent in 1979-80. However, a quarter of wheat and other crop farms still had farm incomes in excess of $20 000 in 1985-86 (Hall and Backhouse 1987). The average contribution of wheat and other crop farms fell from 58 per cent in 1983-84 to 48 per cent in 1985-86 (BAE 1987b). Simultaneously the importance of other crops increased substantially, to 26 per cent, with livestock receipts rising slightly to 18 per cent.

While depreciation of the Australian dollar has, in the recent past, shielded growers to some extent from the sharp decline in world wheat prices, rising interest costs have had an adverse effect on incomes. This rise has been due to both rising interest rates and the increased debt of many farms. Interest costs of wheat and other crop farms represented 18 per cent of their total cash costs in 1985-86 - double the 1977-78 share.

The rise in farm debt has been due to an increased demand for working capital, particularly after the 1977-78 and 1982-83 droughts, and the need for capital to expand farm operations by acquiring both new machinery and land. During the late 1970s and early 1980s wheat and other crop farms increased their debt while expanding their operations when land values were relatively high, and rising, and cropping incomes were good. The result is that, since 1977-78, this group of farms has experienced the fastest rate of increase in real average farm debt of any broadacre industry (figure 3). In 1985-86 the average debt of wheat and other crop farms was $127 000, and 12.5 per cent of these farms had debts in excess of $294 000. (However, in the same year, a quarter of wheat and other crop farms had no debt.) The average debt of these farms rose again in 1986-87 to $137 000, whereas the average debt for all broadacre farms remained around the 1985-86 level of $80 000.

In 1986-87, land prices in general were below the long term trend, largely because of high interest rates and the poor prospects of cropping activities. Consequently, farmers in the cropping sector, who have considerable debt and limited cash flow, are experiencing a marked reduction in their ability to service debt and a fall in their level of equity. This is illustrated by the relatively high proportion of wheat and other crop farms which are estimated to be financially 'at risk': 19 per cent, in 1985-86, compared with only 5 per cent of all farms surveyed by the Bureau. (A farm is classified as 'at risk' if its equity ratio is less than 70 per cent and if its cash margin - that is, total cash receipts less cash costs, repayment of one-eighth of outstanding debt and a family living allowance equal to the adult pastoral award wage - is negative.)

Some wheat farmers are responding to their declining level of returns by switching to livestock, and wherever possible by reducing costs and reorganising their financial commitments. In the short term, wheat and other crop farms face great financial pressures due to declining farm incomes and land values coupled with rising debt levels and interest costs.

Figure 2: FARM INCOME OF FAMILY FARMS

601 1988-87 dollars

I Figure 3: REAL FARM BUSINESS DEBT

Table 2: WHEAT AND OTHER CROPS INDUSTRY: FINANCIAL PERFORMANCE MEASURES, BY STATE AND ALL BROADACRE INDUSTRIES FOR AUSTRALIA Average per farm

New South Wales Victoria Queensland Western Australia . Unit 1985-86 (p) 1986-87 (2) 1985-86 (p) 1986-87 (2) 1985-86 (p) 1986-87k) 1985-86 (P) 1986-87 ( 2 ) Item

Components of investment returns Total cash receipts $ 175 240 (15) 170 000 94 580 (16) 115 600 107 350 (9) 91 000 168 570 (12) 208 800 Total cash costs $ 171 690 (21) 180 300 66 380 (11) 70 900 85 610 (12) 97 500 132 400 (11) 142 300 Farm cash operating surplus $ 3 540 (ns) -10 300 28 200 (35) 44 700 21 740 (45) -6 500 36 170 (30) 66 400

Buildup in trading stocks S 3 920 (65) 2 100 3 200 (31) 700 3 050 (51) 2 400 3 450 (34) 1 800 Depreciation $ 31 010 (12) 32 700 25 490 (11) 25 600 20 600 (8) 21 700 35 670 (10) 38 600 Operator and family labour $ 22 230 (10) 23 300 20 110 (13) 21 100 20 560 (7) 21 600 20 990 (8) 22 000 Return to capital and management S -45 180 (37) -64 200 -14 200 (44) -1 300 -16 370 (53) -47 400 -17 050 (62) 7 600

Return adjusted to full equity S Capital appreciation $ Full equity return, incl. capital appreciation S

Rate of return, excl. capital appreciation %

Rate of return, incl. capital appreciation %

Real rate of return, incl. capital appreciation %

Other financial items Farm capital at 30 June Fare business debt (a) Farm liquid assets (a)

Components pf farm income on family farms Total cash receipts $ Total cash costs $ Farm cash operating surplus $

197 210 (14) 191 600 94 580 (16) 115 600 106 570 (9) 192 990 (20) 202 400 66 380 (11) 70 900 83 390 (13) 4 220 (ns) -10 700 28 200 (35) 44 700 23 180 (36)

Buildup in trading stocks Depreciation

Farm income Farm income per work-year of family labour

Off-farm income

-25 810 (75) -44 700 5 910 (ns) 19 800 5 850 (ns)

(continued below)

Table 2 (continued)

south Australia Australia All broadacre 1985-86 (p) 1986-87 ( 2 ) 1985-86 (p) 1986-87(z) 1985-86(p) 1986-87 ( 2 )

Components of investment returns Total cash costs $ 101 420 (14) 118 900 129 420 (6) 138 800 102 590 (3) 111 200 Total cash recelpts $ 65 160 (13) 71 000 105 700 (9 ) 113 900 80 310 (4) 83 300 Farm cash operating surplus $ 36 260 (19) 47 800 23 720 (24) 25 000 22 280 (9) 27 900

Bulldup In tradlng stocks S 780 (ns) 1 l00 2 970 (25) 1 600 4 660 (25) 3 300 Depreczation $ 23 320 (14) 24 500 27 030 (5) 28 400 16 800 ( 3 ) 16 600 Operator and famlly labour $ 18 220 (12) 19 100 20 530 (5) 21 500 18 040 ( 2 ) 18 900 Return to capltal and management $ -4 500 (ns) 5 300 -20 870 (24) -23 300 -7 910 (22) -4 300

Return adjusted to full equity $ 6 100 (ns) 18 000 -1 490 (ns) 2 300 4 4 1 0 (31) 11 000 Capital appreciation $ -86 780 (16) 2 000 -90 650 (13) -22 500 -41 170 (8) 0 Full equlty return, incl. capital appreciation $ -80 690 (18) 19 900 -92 140 (12) -20 200 -36 760 (9) 11 000

Rate of return, excl. capital appreciation % 0.8 (ns) 2.7 -0.2 (ns) 0.3 0.6 (31) 1.6

W Rate of return, 4 incl. capital appreciation % -10.6 (13) 3.0 -12.0 (10) -3.0 -5.1 (9) 1.6

Real rate of return, incl. capital appreciation

Other financial items Farm capital at 30 June Farm business debt (a) Farm liquid assets(a1

Components of farm income on family farms Total cash receipts $ 111 450 (14) 130 500 135 200 (6) 145 600 107 730 (3) 114 600 Total cash costs $ 72 310 (12) 77 100 110 210 ( 9 ) 117 900 83 700 (4) 86 100 Farm cash operating surplus $ 39 140 (20) 53 500 24 990 (23) 27 800 24 030 ( 9 ) 28 500

Buildup in trading stocks Depreciation

Farm income Farm income per work-year of family labour

Off-farm income

(a) At 30 June. (p) Preliminary survey estimates. (2) Projected survey estimates. na Not available. ns Not supplied. Note: Figures in parentheses are relative standard errors, expressed as percentages of the estimates. A guide to interpreting these is included in 'Survey definitions and procedures' (BAE 1987b), as are explanations of other items. Source: BAE farm survey.

2. WHEAT PAYMENT ARRANGEKENTS

It is important not only that the payment system should give a quick and accurate indication of market prices, but also that the actual costs of marketing and distributing wheat should be apparent to growers. It is, after all, the growers who pay these costs and thus have the incentive to minimise them. Marketing and distribution costs have become substantial in relation to wheat growers' returns. In the five years up to and including 1985-86, these costs (from the bulk handling authority silo to port) averaged 25 per cent of total gross returns to wheat growers (table 3).

The interest cost of borrowings by the Wheat Board is the third largest component of domestic off-farm wheat marketing costs, and in the same five- year period averaged 28 per cent of total wheat marketing costs, or 7 per cent of growersf returns (table 3). Over this period, interest costs increased by around 40 per cent, due mainly to rising interest rates and increases in the carryover of wheat by the Wheat Board. The question must be asked whether the payment system can be improved.

In evaluating the current payment system, several aspects need to be addressed. The first aspect examined here is the widespread, traditional practice of pooling revenues and costs - a practice which is considered by many growers as equitable. This pooling occurs over time, location and quality. Cost pooling occurs at the national, state or regional levels and is applied across classes of wheat, among different areas of production, and over the period of time that the costs of marketing each year's crop are incurred. Revenue pooling occurs at the national level and is applied within

Table 3: DOMESTIC OFF-FARM WHEAT MARKETING COSTS

Item 1981-82 1982-83 1983-84(a) 1984-85(a) 1985-86(a)

S/t S/t S/t S/t S/t Handling and storage costs 12.84 12.93 15.17 15.63 14.98

Freight to terminal ports 14.93 14.15 18.08 16.28 13.61

AWB interest and bank charges 12.17 6.84 11.43 15.30 17.00(s)

AWB administration and depreciation 0.87 1.54 0.81 1.38 1.88

Marketing and .promotion 0.18 0.47 0.17 0.17 0.62

Wheat research levy 0.20 0.25 0.40 0.40 0.45

Total 41.19 36.18 46.06 49.16 48.54

Gross pool return 163.14 187.15 166.91 183.20 176.87

(a) Incomplete. Further costs may be incurred until the pool is finalised. (S) Estimated by the BAE. Sources: Australian Wheat Board (1986a); BAE (1986a).

classes of wheat, across markets for wheat, and over the period of disposal of a wheat crop.

Pooling is not always an inefficient practice, and will be present to some extent under any circumstances. When the administrative costs of separating costs or revenues become larger than the benefits of doing so, pooling of these costs or returns is efficient. In a competitive market, the price mechanism will ensure that costs or revenues will be pooled only to the point where the benefits of further disaggregation do not exceed the costs of that disaggregation. It is doubtful whether this is true of the widespread pooling of costs and revenues which is still practiced in Australian wheat marketing and distribution.

Second, the method of payment needs to be evaluated in terms of the accuracy and timeliness of market signals it gives to growers and the flexibility it provides for adjusting to changing market conditions.

It is worth noting that these aspects of the payment arrangements are quite distinct from the issue of underwriting assistance (which will be examined in section 5). Although this assistance is, for convenience, included by the Wheat Board within its payment arrangements, it is not a return from the market and could be paid separately from the Wheat Board returns to growers.

2.1 Im~lications of Revenue Pooling

Pooling of revenues results in all Australian wheat growers being paid the average return from the sale of wheat of the delivered category. In spite of this distinction of categories, these payments are still made across fairly broad quality ranges. These averages are across all markets (local and export) and over the time taken to dispose of a year's deliveries. In this subsection, the distribution of net returns and risk among growers resulting from revenue pooling arrangements under the current wheat marketing plan is discussed.

(a) Quality

If the number of classes of payment provided to growers - termed the degree of payment segregation - is sufficient so that there will be premiums and discounts to growers corresponding to all the premiums and discounts paid for quality differences by the buyers, cross subsidisation among growers on the basis of quality will be minimised. It might be asked whether this degree of segregation would entail additional costs in physically segregating wheat categories. Wheat is physically segregated to a larger extent than the current number of paymetit categories, due to natural segregation by region as well as administered segregation. Thus, further payment segregation would be possible without additional segregation costs.

Under the present Wheat Marketing Act, growers of around 70 per cent of Australia's wheat crop are paid the pooled price for Australian standard white (ASW), although there is a number of selling categories within the ASW category. A considerable degree of payment cross subsidisation therefore occurs among growers of ASW quality wheat. The only quality signals that ASW wheat growers currently receive are from varietal dockages (which discourage the production of certain varieties) and discounts levied on deliveries that are weather-damaged or contaminated by foreign materials. Because the number of ASW selling categories is larger than the number of ASW payment

categories, distorted incentives are being provided to growers. In particular, growers do not receive the correct price incentives for the production of grain with qualities demanded by the market. This can lead to insufficient production of these grains.

If there is inadequate payment segregation, then within a particular pool category, producers of high quality wheats will in effect subsidise producers of lower quality wheats (assuming that there is a premium for quality in the marketplace). The existence of such cross subsidisation may discourage production of higher quality wheats within the ASW category, if producers have control over quality and especially if there is a production tradeoff between quality and yield. This problem has been recognised by the Wheat Board, which announced early in 1987 that payments for ASW quality wheat would be segregated by protein content.

The Australian Wheat Board (1987a) has proposed that the payment variation for ASW wheat should be $3/t for each percentage point of protein between 9.5 per cent and 11.5 per cent protein, and $2/t for each percentage point of protein outside that range. The size of the proposed differentials indicates that significant cross subsidisation has occurred hitherto. It remains to be seen whether the differentials suggested far the Board's pilot scheme will be beneficial.

(b) Time

The full payment to the grower, which may not be completed until several years after delivery, is based on returns from the sale of a wheat crop not at a particular point in time (such as the time of delivery to a bulk handling authority), but over a period of years. Thus, pooled returns to growers do not specifically reflect returns during the year in which the particular grower's wheat was grown or delivered. A peculiarity of the current pooling system is that each year's production (pool) is kept quite separate even though its sale may not be finalised for several years, and sales for more than one season's crop are made concurrently. Revenue within each year's pool is averaged not only across broad quality ranges and across all markets but over the time taken to sell that year's crop.

There seems little difference in principle between pooling revenue from a crop over the time taken to sell that crop, and pooling revenues between crops. Significant distortions and delays to market signals result from pooling over a long selling period; as wheat is an annual crop, if pooling of returns were confined within each crop year there would be a less distortionary effect on production decisions.

A reduction in the time taken for each wheat pool to be finalised could thus reduce distortions of market signals. This could be achieved through a system whereby each pool buys out the previous year's pool at the expected returns. In October 1986 the Wheat Board offered growers an immediate discounted payment ('cash out' option) for their remaining equity in the 1984-85 pool. After seven months, only 23 per cent of the 1984-85 pool had been cashed out under this option. The low proportion of growers accepting this offer indicates some of the problems of such a scheme. For example, growers have little information on which to judge whether the Board's estimate of the remaining equity is a true reflection of expected returns for the wheat remaining in the pool. Also, as discount rates differ between growers, some growers may have lower discount rates than that used by the Wheat Board and hence would not accept the discounted value. A simpler alternative would be to use normal accounting procedures and close the pool

at the end of the year by valuing the stock and transferring the inventory to the next year's pool.

Growers delivering to the Wheat Board have no control over the marketing of their particular crop and are forced to accept the pooling of the risk due to price fluctuations. In contrast, growers in an unregulated market, such as the US market, retain significant choice as to when their wheat is marketed. Growers initially bear the risk of market price fluctuations when they decide to produce wheat. A grower may seek to mitigate this risk, for example by hedging on che futures market. In Australia the risk of market fluctuations over time is spread over all participants in the pool, regardless of their risk preferences.

In summary, the current practice of pooling revenue across broad quality ranges and over a long selling period is distorting and delaying market price signals to growers. Such pooling should be limited, as discussed above, and revenue should be disaggregated where the benefits of doing so exceed the costs. However, under current marketing arrangements, there is little incentive to restrict pooling. For example, in attempting to further disaggregate revenue the Wheat Board could face resistance from growers who would be required to pay any additional administrative cost. On the other hand, the benefits of disaggregating revenue - that is, the improved market signals leading to more efficient production decisions - may not be immediately clear to growers or to the Wheat Board.

2.2 Implications of Cost Poolin9

(a) Pooline of distribution costs

Costs of distribution (storage, handling and transport) are pooled across location, quality and time, and have been pooled on a state basis since 1978-79. These costs are pooled across all categories and grades of wheat regardless of the costs associated with segregating or handling any individual quality of wheat. No account is taken of the differences in efficiency that exist among silos at different locations or in the operating, maintenance and capital costs of the silos.

Spriggs et al. (1987) concluded that the pooling of distribution charges on a state basis necessarily gives rise to cross subsidies which translate into incorrect price signals. Because the charges levied on growers do not vary between delivery points, there is no incentive for growers to deliver to the cheapest point and thus to reduce distribution costs. The end result is a cross subsidy from low cost users to high cost users, and higher total costs than necessary.

Distribution charges are pooled over time, with no adjustments for the timing of wheat deliveries. This, combined with the early returns of the current payment system, results in the rational choice by growers to deliver at harvest, which leads to long queues at receival points, peak load problems, distorted decisions regarding on-farm storage, and possibly overcapitalisation in delivery facilities. To reduce carrying costs and to minimise peak load problems at delivery, the system of cost pooling would have to be altered.

Since the charges paid by growers do not necessarily reflect the costs incurred by each individual, the pooling of distribution charges favours some growers at the expense of others and eliminates the incentive to

minimise costs. If charges were related more closely to costs, growers, bulk handling authorities, rail authorities and the Wheat Board would have more effective incentives to minimise the costs of wheat distribution. As discussed in Spriggs et al. (1987), widespread cost pooling would not occur in a competitive market. Under current arrangements, however, there is little pressure to abandon cost pooling, and indeed growers have in the past exerted pressure to continue it.

(b) pool in^ of marketine costs

The Wheat Board's marketing costs are paid equally (per tonne) by all wheat growers. They include interest costs (of financing advance payments), marketing and promotional expenses, insurance on export credit sales and other finance operations, and general administration fees including labour charges and sundry items. As shown in table 3, interest costs are by far the largest component of the Board's marketing costs.

The Wheat Board's marketing costs are pooled on a national basis and over all wheat delivered - that is, over all qualities of wheat, even though the costs associated with marketing different qualities may vary. For example, although some grades may be sold more quickly than others, the interest cost is averaged over all grades so that growers who supply grades which are sold quickly have to contribute to the financing costs of other, unsold grades. Financing costs will also differ for each quality category, since they earn different advance payments. As is shown in table 4, if all categories were sold at the same time, growers who delivered feed wheat could be subsidising those who delivered higher value wheat such as ASW or prime hard (by helping to finance their higher advance payments). On the other hand, if prime hard wheat were sold more quickly than feed wheat the subsidy could be the other way. The result of such pooling is that generally the grower is given an incorrect signal, which in turn may lead to the distortion of production decisions.

As long as wheat from all growers is supplied equally to all importers of Australian wheat, all growers should contribute equally to the costs of marketing their wheat in all these markets. This pooling of marketing costs across all markets may result in inadequate incentives to minimise costs, particularly if growers are unaware of the cost differences among markets. Finally, because these costs are pooled over the time taken to sell the wheat crop, the risks associated with the costs of marketing wheat during the entire disposal period of a particular year's pool are equally borne by all wheat deliveries in that year.

Like the pooling of distribution costs and that of revenue across wheat qualities, the pooling of marketing costs (particularly across wheat qualities and over long periods of time) leads to incorrect signals to growers, which in turn encourage inappropriate decisions regarding the level of wheat production.

2.3 Evaluation of Current Payment System

The current payment system has been developed in an attempt to improve market signals and the timeliness of payments to wheat growers by increasing the advance payment (table 5). On the other hand, wheat payment arrangements characterised by a high advance payment invariably encourage growers to deliver their wheat to bulk handling authorities as soon as it is harvested. This in itself would not result in inefficient delivery decisions. However,

Table 4: ILLUSTRATIVE FINANCING COSTS FOR VARIOUS WHEAT CATEGORIES

Cost relative Guaranteed Monthly Total to Australian minimum Storage interest financing standard

Category price period rate(a) cost white

$/t months % $/t $/t

1984-85 Prime hard 155.35 6 0.833 7.77 +O .50 ASW(b) 145.35 6 0.833 7.27 Feed 100.35 6 0.833 5.02 -2.25

Prime hard 155.35 3 0.833 3.88 -3.39 ASW 145.35 6 0.833 7.27 Feed 100.35 9 0.833 7.53 +0.26

1985-86 Prime hard 174.87 6 1.042 10.93 +1.56 ASW(b) 149.87 6 1.042 9.37 Feed 114.87 6 1.042 7.18 -2.19

Prime hard 174.87 3 1.042 5.46 -3.91 ASW 149.87 6 1.042 9.37 Feed 114.87 9 1.042 10.77 +l. 40

1986-87 Prime hard 157.62 6 0.833 7.88 ASW(b) 139.83 6 0.833 6.99 Feed 105.77 6 0.833 5.29 -1.70

Prime hard 157.62 3 0.833 3.94 -3.05 ASW 139.83 6 0.833 6.99 Feed 105.77 9 0.833 7.93 +O .94

(a) Based on BAE estimate of average Australian Wheat Board borrowing costs. (b) Australian standard white. Source: Australian Wheat Board (198713).

as the costs incurred by early delivery over a short period are pooled across all growers, there is no incentive for individual growers to minimise these costs. Because storage and handling costs are pooled, growers do not know the full cost consequences of delivery at different times. Also, because interest costs of meeting the advance payments are pooled, all growers pay the average financing cost even though their delivery times differ. The deferred delivery option is an attempt to circumvent this problem by reimbursing the interest. It is repaid at the Australian Savings Bond rate, which in 1985-86 was higher than the Wheat Board's average interest rate and thus more than repaid the growers.

(a) The finance effects

A problem with the current system is that it forces on all growers the same borrowing regimen despite differences in cash flow requirements and variations in opportunity costs of growers' funds. Ideally an efficient

Table 5: ADVANCE PAYMENTS

Borrowings Total Advance Receival Advance by AWB for payment to on total

Season by AWB (a) payment (b) advance (c) grower (d) payment

1969 -70 9 755 40.42 394 43.85 92 1970-71 6 936 40.42 280 46.82 8 6 1971-72 7 666 40.42 310 48.75 83 1972-73 5 439 40.40 220 49.54 82 1973-74 11 200 44.09 494 104.36 42 1974-75 10 705 44.09 472 104.94 42 1975-76 11 258 55.12 621 95.98 5 7 1976-77 10 933 66.00 722 79.45 83 1977 -78 8 540 66.00 564 88.25 7 5 1978-79 17 456 75.00 1 309 129.55 58 1979-80 15 327 114.71 1 758 154.55 74 1980-81 10 059 131.92 1 327 147.42 89 1981-82 15 547 141.55 2 201 149.92 94 1982-83 7 887 141.32 1 115 178.30 79 1983-84(p) 21 111 150.00 3 167 154.50(s) 97 1984-85(p) 17 546 145.35 2 550 166.35 (S) 8 7 1985-86(s) 15 085 149.87 2 261 157.37(s) 95 1986-87(s) 15 140 139.83 2 117 139.83(e) 100

(a) Receival of all wheat. (b) For ASW wheat or equivalent. (c) Receival multiplied by ASW advance (which accounts for about 70 per cent of receival). (d) ASW basis for states other than Western Australia; prior to deductions for distribution services, wheat tax and levies. (e) Estimate based on assumption of no further payments. (p) Preliminary. (S) Estimated by BAE. Source: Australian Wheat Board (1986a); BAE (1986a, 1987a); Australian Wheat Board.

payment system should give a quick indication of market returns and should give growers control over their financing arrangements, so that they can adjust their borrowings to suit their particular circumstances. The deferred payment options offered under the current arrangements do address this need, but only partially. Growers still have very limited options in terms of the timing and the amount of borrowings.

Under current arrangements, growers compulsorily receive an advance payment and pay interest on that payment until the wheat is sold. It must be asked, first, whether all growers require this finance; second, (if so) whether they could obtain it more cheaply than the Wheat Board; and, finally, whether they require only a part of it, or require it for a shorter period. In other words, is any part of the present interest cost unavoidable?

On average, the Wheat Board can obtain finance at a lower rate of interest than can an individual grower. In 1985-86 growers faced an average interest rate of around 18-19 per cent (Reserve Bank of Australia 1987), whereas the average rate on Wheat Board borrowings was about 12.5 per cent. This difference is due to several factors. One of these is only transitory.

In 1985-86 Australian interest rates were well above rates in many other countries. The Board was able to take advantage of this difference, and borrowed largely overseas. However, this difference in rates is now declining; moreover, some individual growers can also borrow overseas. The other main reason for the Board's ability to secure funds at a relatively low rate of interest derives from its very high credit rating, which arises from government underwriting (see section 5).

Although growers may on average face higher borrowing costs than the Wheat Board, some growers may have access to cheaper alternative funds. The off-farm liquid assets of farmers are a readily accessible source of funds that could be used if an advance payment were not available. On average, off-farm liquid assets per wheat farm were lower than the advance payment in 1985, except in Queensland (table 6). Nevertheless, at 30 June in 1985 and 1986 about 24 per cent of wheat growers surveyed by the Bureau had liquid assets in excess of their advance payments. (Allowing for sampling error, there is a 2 in 3 chance that the true value for this figure was between 20 per cent and 28 per cent.) These particular wheat growers, who received up to 20 per cent of the total advance payments, may not have required this advance. In addition, many wheat growers may not need to borrow the full amount of the advance payment.

The Bureau's survey data indicate that, at 30 June in 1985 and 1986, the ratios of the state average amounts of liquid assets to the state average advance payments ranged from 28 per cent in Western Australia to 116 per cent in Queensland (table 6). Cash flow of course varies throughout the year; this comparison, however, was made at a time of generally low liquidity following planting. The rates of return that growers received on

Table 6: OFF-FARM LIQUID ASSETS, WHEAT AND OTHER CROPS, AT 30 JUNE 1985 Average per farm

I tem

New South Queens- Western South Wales Victoria land Australia Australia Australia

Trading bank deposits 4 425 2 949 5 142 2 113 480 3 219 Savings bank deposits 2 177 3 185 1 610 6 633 8 549 3 982 Interest bearing deposits 18 979 6 687 48 971 25 942 8 059 18 960 Debentures, bonds 771 10 582 145 1712 1 511 3 257 Other financial institutional deposits 2 668 1 663 6 275 658 1 847 2 367 Company shares 15 17 128 1 110 2 060 495 Total equalisation deposits 18 244 460 676 0 226 Other 108 1 279 8 2 0 8 366 1 507

Total liquid assets 29 161 26 606 62 813 38 844 30 872 34 013

First advance 46 665 38 402 54 324 138 230 49 777

Source: BAE farm surveys.

most types of liquid assets would have been lower than the Wheat Board interest rate (table 6 and Reserve Bank of Australia 1987). Thus, growers might have been better off if they had used these assets in place of all or part of the advance payment, had those options been available.

The advance payment is a system whereby credit is forced upon the wheat grower. Whether or not growers require the Wheat Board to borrow on their behalf, current arrangements dictate that growers still have to incur the loss of any difference between the Board's interest rate and the return on money they themselves invest. On average, growers may benefit from the Board's borrowing activities, but, as shown above, some may not.

In table 7 a number of alternative payment arrangements are presented with their key features and associated benefits and costs. This list is by no means exhaustive; it includes mainly those options that have been proposed by grower or industry groups.

From the standpoint of giving growers more control over their own finances, a better alternative to the current system would be to offer an advance payment as an option, with a choice as to the timing and amount as well as whether an advance is taken or not. The cost of offering growers more control over their borrowing requirements may well include higher Wheat Board administration costs, which would be passed back to growers. The benefits of offering a more flexible system would need to be weighed against the costs of operating the system.

(b) The subsidv effect

Another aspect of the current payment arrangements which needs to be addressed is the appropriateness, from a national viewpoint, of making funds available to wheat growers at concessional interest rates. As noted above, a major reason why the Wheat Board can offer relatively low interest rates to growers is its high credit rating, due in part to government underwriting. This amounts to a subsidy on funds for wheat growers. The rationale for such a subsidy is questionable, in view of the recent deregulation of the Australian capital market, the availability to eligible farmers of interest rate subsidies through the Rural Adjustment Scheme and the distorting effect that such subsidies have on the allocation of funds in Australia.

Subsidising funds to wheat growers will increase their use of funds at the expense of those investments whose returns are higher or less risky than those of wheat growers but lower or more risky than the Wheat Board can offer. Thus, funds will not be directed to where the highest return is available. On efficiency grounds, provision of this subsidy is undesirable. Whether there are more appropriate methods of assisting the wheat industry is discussed in section 5.

To avoid this misallocation yet provide wheat growers with a quick market signal, the preferred arrangement would be for the Board to issue negotiable certificates to growers on delivery of their wheat. The certificates would detail the quality and quantity of wheat delivered. Certificates would be freely negotiable and usable as collateral for borrowings by the grower. On receipt of returns from sale of the wheat the Board would redeem the certificate. Such a system should not increase the administrative cost of the Board but would allow growers full control over their finances. Also, because the certificates would have a market value, they would give growers a quick indication of the market return on their crops.

Table 7: ALTERNATIVE WHEAT PAYMENT ARRANGEMENTS

Policy option Benefits Costs

1. Current svstem

(a) Advance pavment

. High advance payment . Improved cash flow . Large interest cost

. Cost and revenue to growers . Distortion of market pooling signals

. Cross subsidies