Embed Size (px)

Citation preview

DIRECTORS’ REPORT 2015

1

The directors hereby present their report for the year ended 30 June 2015.

DIRECTORS The names and details of directors in office at the date of this report are:

Professor Diana Horvath AO MB BS, FRACMA, FAFPHM, FACHSE

Chair (Resigned 21/5/2015) Teaching position at the Medical School at USyd Director, Lifehouse RPAH

Professor Robert Lusby AM MD, MB BS, FRCS, FRACS Deputy Chair (Until 21/5/15) Chair (From 22/5/15) Head of the University of Sydney Clinical School at Concord Hospital Associate Dean of the Faculty of Medicine (Till 31/12/2014)

Professor David J Handelsman MB BS FRACP PhD Secretary to Board Director, ANZAC Research Institute Associate Dean (Research Strategy), Sydney Medical School, University of Sydney. Sub-Dean Research (Concord), Concord Medical School, University of Sydney. Head, Department of Andrology, Concord Hospital Dr Teresa Anderson B App Science (Speech Therapy), PhD Chief Executive, Sydney Local Health District

Dr Tim Sinclair PhD (Bus. Admin), M. Health Services Management,

B.App.Sc (Health Information Management) General Manager of Concord Repatriation General Hospital, Sydney Local Health District. He is also a Director on the ANZAC Health and Medical Research Foundation and an Advisory Board Member of the Australian Institute of Health Services Management.

Professor Bruce Robinson AM MB BS FRACP FAICD

(Resigned 21/5/2015) Dean, Faculty of Medicine, University of Sydney

Professor Ben Freedman OAM MBBS, BSc (Med), PhD, FRACP, FACC

(Alternate Director for Prof Bruce Robinson) (Resigned 21/5/2015)

Professor of Cardiology at Concord Hospital. Head of the Vascular Biology Group of The Anzac Research Institute. Director on the following Boards: Heart Research Institute, Bosch Institute, Asbestos Diseases Research Foundation, Centre for Vascular Research, Microsearch Foundation, Sydney Burns Foundation, and the Heart Foundation of Australia Research Committee, Fellow of the American College of Cardiology (FACC), the European Society of Cardiology (FESC), and the Cardiac Society of Australia and New Zealand (FCSANZ).

Professor Arthur Conigrave MD PhD FRACP (Alternate Director for

Prof Bruce Robinson) (Resigned 21/5/2015)

Professor, School of Molecular Bioscience, University of Sydney Associate Dean (Finance & Administration) and Deputy Dean, Sydney Medical School Endocrinologist, Royal Prince Alfred Hospital

DIRECTORS’ REPORT

Mr Paul Levins BA

President Intellectual Ventures Honorary Associate of the University of Sydney Graduate School of Government. Independent Director of auDA (Australia’s .au domain)

Ms Kerry Hogan-Ross BA LLB

Director, ANZAC Research Institute. Mediator at Kerry Hogan-Ross Mediations

Dr Katherine Moore B.App.Sc.(Occ Therapy); M.App.Sc.(Occ Therapy);

PhD (Health Services Management)

Director of Clinical Governance in the Sydney Local Health District. Holds numerous roles within the profession of occupational therapy including president of the NSW Occupational Therapy Association, member of the university accreditation panel, and as a previous member of the overseas qualifications assessment committee and a Practitioner member from New South Wales.

Dr Ilona Cunningham M.B.B.S., Fellowship of The Royal Australasian

College of Physicians, Fellowship in Haematology

Senior Staff Specialist, Head of Department, Department of Haematology- Concord Repatriation General Hospital

Mr George Elias B.Comm., Dip. FP., CPA(FPS), SSA, MFAA Credit Adviser

TM, CERTIFIED FINANCIAL PLANNER® professional, SMSF Specialist Advisor

TM. Principal of Elias Financial Services and is an Authorised Representative of Count Financial Limited

Prof Andrew McLachlan BPharm, PhD FPS, FACP

Chair: Sydney Local Health District –Concord Hospital Ethics Committee; Drug and Therapeutics Committee, Concord Hospital; Anti-Doping Rule Violation Panel, Department of Health, Australian Government; Pharmaceutical Subcommittee, Advisory Committee on Prescription Medicines (ACPM), Therapeutic Goods Administration. Member, Australia Therapeutic Goods Advisory Council. Theme Leader, Health Services Research and Patient Safety, Faculty of Pharmacy, The University of Sydney. Secretary, NSW Therapeutics Advisory Group Member, Medication Reference Group, Australian Commission on Safety and Quality in Health Care. Director, McLachlan PK Consulting Pty Ltd (consulting company)

A/Prof Meng Ngu BMed Sc(Hons),MB BS, PhD, FRACP

Senior Staff Specialist, Department of Gastroenterology and Hepatology at Concord Repatriation General Hospital and Clinical Associate Professor, University of Sydney CRGH Clinical School.

Mr Don Rowe OAM, MAICD (Resigned 23/02/2015)

Chairman & Member of State Branch Committees: Hyde Park Inn Board of Management; Reveille and Public Relations; Sir Colin Hines Scholarship; Finance, Audit and Risk Management Committee; Welfare and Benevolent Institution; VP Day Ceremony; Reveille. ANZAC Memorial Building (Trustee); ANZAC House Trust Board of Management; RSL Australian Forces Overseas Fund (NSW Commissioner); Dormant Funds Committee; United Returned Soldiers’ Fund; RSL Custodian; Centenary of ANZAC Committee; RSL LifeCare; National Finance & National Executive Committees; Soldier On (Director)

At this date no director has any interest in the equity of the Foundation.

DIRECTORS’ REPORT 2015

2

PRINCIPAL ACTIVITIES The principal activities of the ANZAC Health and Medical Research Foundation during the year were that of acting as trustee for the ANZAC Health and Medical Research Foundation Trust Fund. There was no significant change in the nature of that activity during the year. OPERATING RESULTS FOR THE YEAR The Company did not trade in its own right, and made neither a profit nor a loss and the company does not incur expenses as they are paid by the Trust Fund. SIGNIFICANT CHANGES IN THE STATE OF AFFAIRS There were no significant changes in the state of affairs of the ANZAC Health and Medical Research Foundation during the year. SIGNFICANT EVENTS AFTER THE BALANCE DATE No matter or circumstances have arisen since the end of the financial period which significantly affected or may significantly affect the operations of the ANZAC Health and Medical Research Foundation, the results of those operations, or the state of affairs of the ANZAC Health and Medical Research Foundation in subsequent years.

LIKELY DEVELOPMENTS

The Company will continue to act as trustee of the ANZAC Health and Medical Research Foundation Trust Fund. REVIEW OF OPERATIONS

ANZAC Health and Medical Research Foundation continue to manage the operations of the ANZAC Research Institute and have progressed successfully in the last Financial Year. Scientific Research Contributions continued to flow with increased grant income earned from Government, charitable foundation and health product companies. Corresponding then was increased expenditure for research activities.

SHORT AND LONG TERM OBJECTIVES The Company’s objective is to foster excellent health and medical research through providing a state-of-the-art facilities and a researcher-friendly working environment.

STRATEGY FOR ACHIEVING THE OBJECTIVES The Company sets to support the research of high quality health and medical research undertaken by researchers based at ANZAC Research Institute in providing research facilities and services.

PRINCIPAL ACTIVITIES ASSIST IN ACHIEVING

THE OBJECTIVES

The Institute’s principal activities are in providing research

facilities and services for the researchers with their scientific

home at the ANZAC Research Institute.

INDEMNIFICATION AND INSURANCE OF

DIRECTORS

The ANZAC Health and Medical Research Foundation during or

since the financial year, in respect of any person who is or has

been an officer, has not been

indemnified or made any relevant agreement for indemnifying against a liability incurred as an officer, including costs or expenses in successfully defending legal proceedings; or

paid or agreed to pay a premium in respect of a contract insuring against a liability incurred as an officer for the costs or expenses to defend legal proceedings

CGU Professional Risks Insurance, a division of CGU Insurance

Limited, insures all directors against liabilities for costs and

expenses incurred by them in defending any legal proceedings

arising out of their conduct while acting in the capacity of director

of the Company, other than conduct involving a wilful breach of

duty in relation to the Company.

EMPLOYEES

The Foundation employed no employees as at 30 June 2015

(2014: nil employees).

ENVIRONMENTAL REGULATION AND

PERFORMANCE

The Foundation is not subject to any environmental regulation.

MEMBER’S GUARANTEE

In accordance with the company’s constitution, each member is

liable to contribute $20 in the event that the company is wound up.

The total amount members would contribute is $220.

MEETINGS OF DIRECTORS

During the financial period, meetings of directors were held and

attendances are tabulated below:

DIRECTORS’ REPORT 2015

3

AUDITOR’S INDEPENDENCE DECLARATION

BOARD MEETINGS 2014-15

Eligible

to Attend

Number

Attended

Approved

leave of

absence

Prof D Horvath (Chair) (Resigned 21.5.15) 4 4 0

Prof R Lusby (Deputy Chair) 4 4 0

Prof D Handelsman 4 4 0

Dr T Anderson 4 3 1

Dr Tim Sinclair 4 2 2

Prof B Robinson (Resigned 21.5.15) 4 0 4

Prof B Freedman (Alt for B Robinson) (Resigned 21.5.15)

4 0 4

Prof A Conigrave (Alt for B Robinson) (Resigned 21.5.15)

4 3 1

Mr P Levins 4 1 3

Ms K Hogan-Ross 4 2 2

Dr K Moore 4 1 3

Dr I Cunningham 4 3 1

Mr G Elias 4 3 1

Prof Andrew McLachlan (Appointed 12.8.14) 4 3 1

A/Prof Meng Ngu (Appointed 12.8.14) 4 3 1

Mr Don Rowe(Appointed 12.8.14 Resigned 23.2.15) 2 0 2

FOUNDATION REPORT 2015

4

AUDIT REPORT

FOUNDATION REPORT 2015

5

FOUNDATION REPORT 2015

6

FOUNDATION REPORT 2015

7

STATEMENT OF COMPREHENSIVE INCOME

FOR THE YEAR ENDED 30 JUNE 2015

Notes 2015 2014

$ $

Expenses 0 0

Revenue 0 0

Operating result 2 0 0

Other Comprehensive Income

Items that will not be reclassified to Operating Result 0 0

Items that may be reclassified to Operating Result 0 0 Total Comprehensive Income For The Year 0 0

The accompanying notes form part of these Financial Statements.

STATEMENT OF FINANCIAL POSITION

AS AT 30 JUNE 2015

2015 2014

$ $

Total Assets 0 0

Total Liabilities

0

0

Net Assets

0

0

Equity Accumulated Funds

0

0

The accompanying notes form part of these Financial Statements.

FOUNDATION REPORT 2015

8

STATEMENT OF CHANGES IN EQUITY

FOR THE YEAR ENDED 30 JUNE 2015 Accumulated Funds

$

Balance at 1 July 2014

Result for The Year 0

Other Comprehensive Income 0

Total Comprehensive Income for the Year 0

Transactions With Owners in their Capacity As Owners

Increase/(Decrease) in Net Assets From Equity Transfers 0

Balance at 30 June 2015 0

Balance at 1 July 2013 0

Result for The Year 0

Other Comprehensive Income 0

Total Comprehensive Income for the Year 0

Transactions With Owners in their Capacity As Owners

Increase/(Decrease) in Net Assets From Equity Transfers 0

Balance at 30 June 2014 0

The accompanying notes form part of these Financial Statements.

STATEMENT OF CASH FLOW

FOR THE YEAR ENDED 30 JUNE 2015 2015 2014

$ $

CASH FLOWS FROM OPERATING ACTIVITIES 0 0

NET INCREASE / (DECREASE) IN CASH

0

0

Opening Cash and Cash Equivalents

0

0

Closing Cash and Cash Equivalents

0

0

The accompanying notes form part of these Financial Statements.

FOUNDATION REPORT 2015

9

NOTES TO THE FINANCIAL STATEMENTS

30 JUNE 2015

CORPORATE INFORMATION

The financial report is for the ANZAC Health and Medical Research Foundation (Foundation) as an

individual entity, incorporated and domiciled in Australia. Foundation is a company limited by guarantee.

These financial statements have been authorised for issue by the Board on 23rd

September 2015.

NOTE 1: SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

(A) BASIS OF PREPARATION

The financial report is a general purpose financial report that complies with the requirements of the Corporations Act 2001, Australian Accounting Standards, Australian Accounting interpretations and other authoritative pronouncements of the Australian Accounting Standards Board and with the requirements of the Public Finance and Audit Act 1983 and its regulations in accordance with the Trust Deed (dated 21 February 1995).

Historical cost convention

The financial statements have been prepared on the basis of historical cost except certain financial

assets are measured at fair value as indicated below.

All amounts are expressed in Australian currency.

Judgements, key assumptions and estimations made by management are disclosed in the relevant notes

to the financial statements.

Comparative figures are, where appropriate, reclassified to give a meaningful comparison with the current

year. Except when an Australian Accounting Standard permits or requires otherwise, comparative

information is presented in respect of the previous period for all amounts reported in the financial

statements.

New Australian Accounting Standards Issued but not Effective

New or revised Australian Accounting Standards effective for the first time or not yet effective in 2014-15

do not have material impact in the financial statements.

(B) INCOME TAX

The Foundation is exempt from income tax.

(C) TRUSTEE

The Foundation acts as trustee for the ANZAC Health and Medical Research Foundation Trust Fund.

The accounting policies adopted by the Company in the preparation of the financial statements for the

year ended 30 June 2015 reflect the fiduciary nature of the Company’s responsibility for the assets and

liabilities of the ANZAC Health and Medical Research Foundation Trust Fund which are set out in Note 4.

FOUNDATION REPORT 2015

10

NOTES TO THE FINANCIAL STATEMENTS (Continued)

30 June 2015

NOTE 2: OPERATING RESULT

The Foundation did not trade during the past financial year.

NOTE 3: STATEMENT OF CASH FLOWS

The Foundation does not maintain a bank account and has no other source of funding that meets the

definition of a cash equivalent.

NOTE 4: ASSETS AND LIABILITIES OF THE FOUNDATION

The Foundation acts as trustee for the ANZAC Health and Medical Research Foundation Trust Fund.

The assets and liabilities of the ANZAC Health and Medical Research Foundation Trust Fund as

disclosed in the financial statements of the Trust are as follows:

2015 2014

$ $

Current Assets 21,860,795 20,823,097

Non-Current Assets 10,603,883 10,941,752

TOTAL ASSETS 32,464,678 31,764,849

Current liabilities 1,627,066 1,570,205

Non-Current liabilities 0 0

TOTAL LIABILITIES 1,627,066 1,570,205

NET ASSETS 30,837,612 30,194,644

Represented by TRUST FUNDS 30,837,612 30,194,644

NOTE 5: GUARANTEE CAPITAL

The Foundation is limited by guarantee of its members and therefore there is no issued share capital.

Every member of the company undertakes to contribute to the assets of the company in the event of it

being wound up during the time they are member or within one year afterwards for:

payment of debts and liabilities of the company contracted before the time at which they ceased

to be a member,

costs, charges and expenses of winding up the company, and

adjustments of the rights of the contributions amongst themselves such amount as may be

required but not exceeding twenty dollars ($20).

At 30 June 2014, the Foundation has 11 members.

FOUNDATION REPORT 2015

11

NOTES TO THE FINANCIAL STATEMENTS (Continued)

30 June 2015

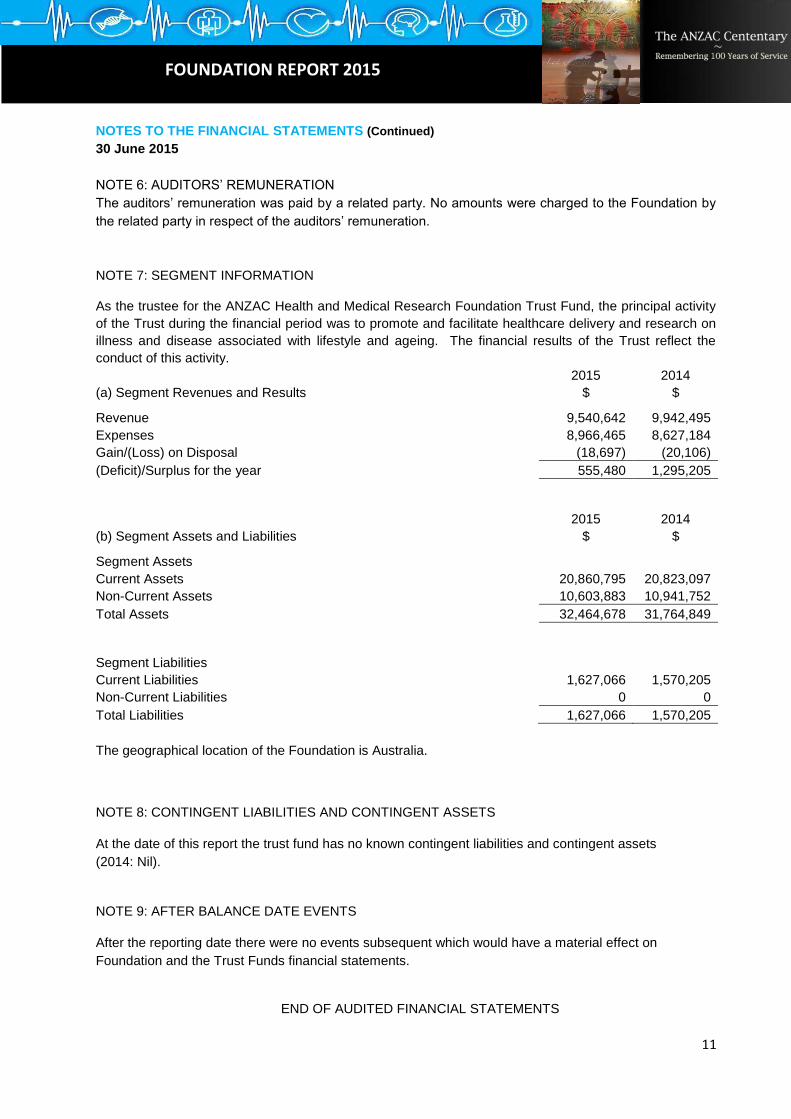

NOTE 6: AUDITORS’ REMUNERATION

The auditors’ remuneration was paid by a related party. No amounts were charged to the Foundation by

the related party in respect of the auditors’ remuneration.

NOTE 7: SEGMENT INFORMATION

As the trustee for the ANZAC Health and Medical Research Foundation Trust Fund, the principal activity

of the Trust during the financial period was to promote and facilitate healthcare delivery and research on

illness and disease associated with lifestyle and ageing. The financial results of the Trust reflect the

conduct of this activity.

2015 2014

(a) Segment Revenues and Results $ $

Revenue 9,540,642 9,942,495

Expenses

Gain/(Loss) on Disposal

8,966,465

(18,697)

8,627,184

(20,106)

(Deficit)/Surplus for the year 555,480 1,295,205

2015 2014

(b) Segment Assets and Liabilities $ $

Segment Assets

Current Assets 20,860,795 20,823,097

Non-Current Assets 10,603,883 10,941,752

Total Assets 32,464,678 31,764,849

Segment Liabilities

Current Liabilities 1,627,066 1,570,205

Non-Current Liabilities 0 0

Total Liabilities 1,627,066 1,570,205

The geographical location of the Foundation is Australia.

NOTE 8: CONTINGENT LIABILITIES AND CONTINGENT ASSETS

At the date of this report the trust fund has no known contingent liabilities and contingent assets

(2014: Nil).

NOTE 9: AFTER BALANCE DATE EVENTS

After the reporting date there were no events subsequent which would have a material effect on

Foundation and the Trust Funds financial statements.

END OF AUDITED FINANCIAL STATEMENTS

FOUNDATION REPORT 2015

12

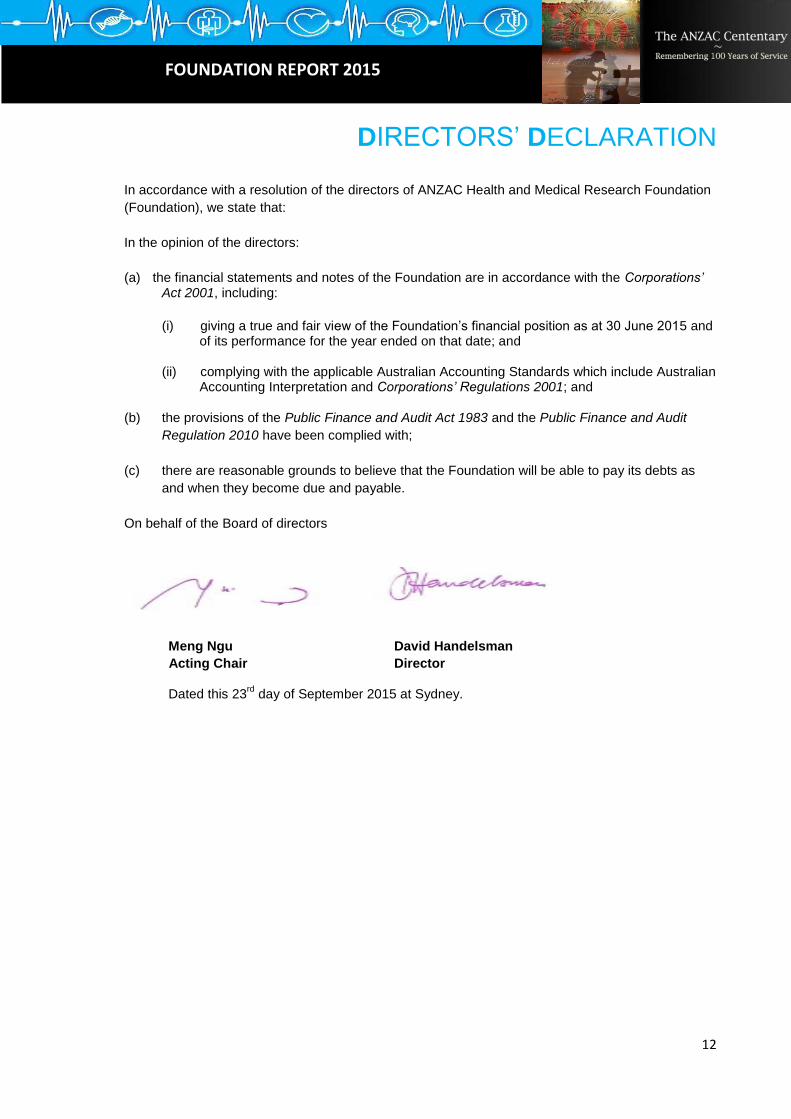

DIRECTORS’ DECLARATION

In accordance with a resolution of the directors of ANZAC Health and Medical Research Foundation

(Foundation), we state that:

In the opinion of the directors:

(a) the financial statements and notes of the Foundation are in accordance with the Corporations’ Act 2001, including:

(i) giving a true and fair view of the Foundation’s financial position as at 30 June 2015 and of its performance for the year ended on that date; and

(ii) complying with the applicable Australian Accounting Standards which include Australian Accounting Interpretation and Corporations’ Regulations 2001; and

(b) the provisions of the Public Finance and Audit Act 1983 and the Public Finance and Audit

Regulation 2010 have been complied with;

(c) there are reasonable grounds to believe that the Foundation will be able to pay its debts as

and when they become due and payable.

On behalf of the Board of directors

Meng Ngu David Handelsman

Acting Chair Director

Dated this 23rd

day of September 2015 at Sydney.

TRUST REPORT 2015

13

AUDIT REPORT

TRUST REPORT 2015

14

TRUST REPORT 2015

15

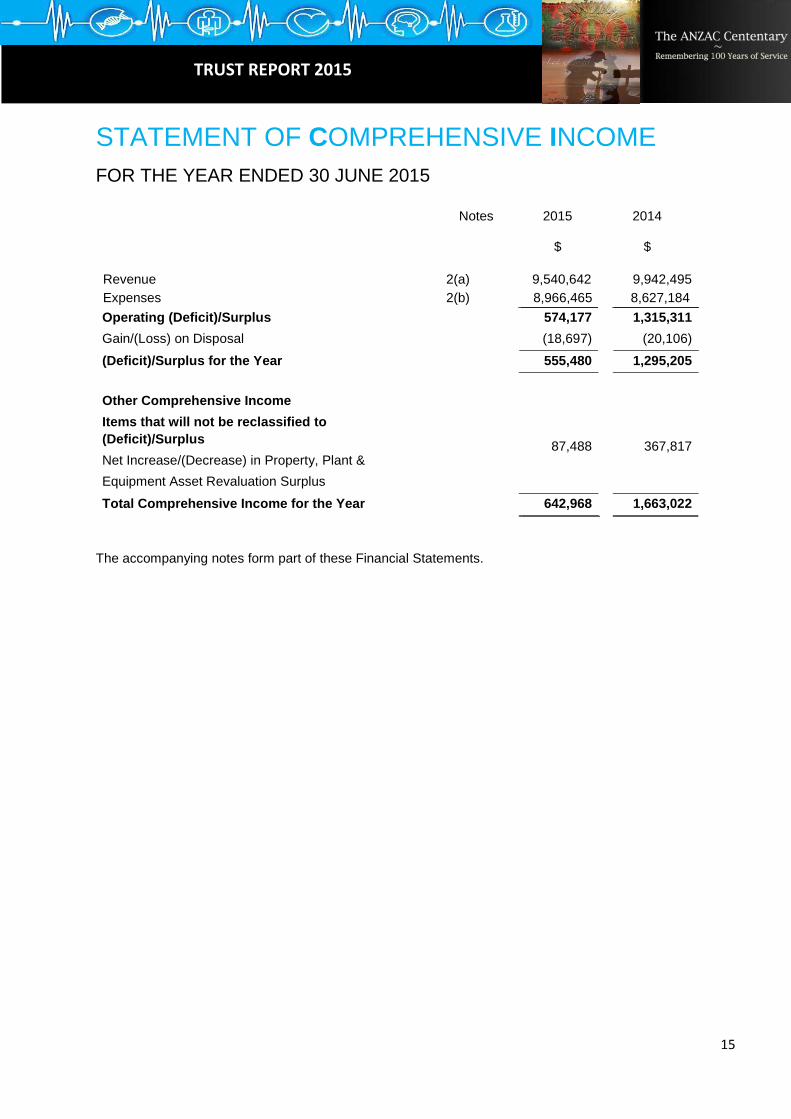

STATEMENT OF COMPREHENSIVE INCOME

FOR THE YEAR ENDED 30 JUNE 2015

Notes

2015

$

2014

$

Revenue

Expenses

2(a)

2(b)

9,540,642

8,966,465

9,942,495

8,627,184

Operating (Deficit)/Surplus

Gain/(Loss) on Disposal

574,177

(18,697)

1,315,311

(20,106)

(Deficit)/Surplus for the Year 555,480 1,295,205

Other Comprehensive Income

Items that will not be reclassified to

(Deficit)/Surplus

Net Increase/(Decrease) in Property, Plant &

Equipment Asset Revaluation Surplus

87,488

367,817

Total Comprehensive Income for the Year 642,968 1,663,022

The accompanying notes form part of these Financial Statements.

TRUST REPORT 2015

16

STATEMENT OF FINANCIAL POSITION

AS AT 30 JUNE 2015

2015

2014

Notes

$

$

CURRENT ASSETS

Cash and Cash Equivalents 4

20,375,453 19,080,647

Financial Assets at Fair Value

5

402,116

374,454

Receivables

6

1,083,226

1,367,996

TOTAL CURRENT ASSETS

21,860,795

20,823,097

NON-CURRENT ASSETS

Property, Plant and Equipment

7

10,603,883

10,941,752

TOTAL NON-CURRENT ASSETS

10,603,883

10,941,752

TOTAL ASSETS

32,464,678

31,764,849

CURRENT LIABILITIES

Payables

Provisions

8

9

900,055

727,011

915,784

654,421 TOTAL CURRENT LIABILITIES

1,627,066

1,570,205

TOTAL LIABILITIES

1,627,066

1,570,205

NET ASSETS

30,837,612

30,194,644

TRUST FUNDS

Settlement Account

100 100

Accumulated Funds

27,355,314 26,799,834

Asset Revaluation Reserve

3,482,198 3,394,710

TOTAL TRUST FUNDS

30,837,612 30,194,644

The accompanying notes form part of these Financial Statements.

TRUST REPORT 2015

17

STATEMENT OF CHANGES IN EQUITY

FOR THE YEAR ENDED 30 JUNE 2015

Accumulated

Funds

$

Settlement

Account

$

Asset

Revaluation

Reserve

$

Total

$

Balance at 1 July 2014 26,799,834 100 3,394,710 30,194,644

(Deficit)/Surplus for the Year 555,480 0 0 555,480

Other Comprehensive Income

Net Increase/(Decrease) in Property,

Plant & Equipment Revaluation 0 0 87,488 87,488

Total Comprehensive Income for

the Year 555,480 0 87,488 642,968

Balance at 30 June 2015 27,355,314 100 3,482,198 30,837,612

Balance at 1 July 2013 25,504,629 100 3,026,893 28,531,622

(Deficit)/Surplus for the Year 1,295,205 0 0 1,295,205

Other Comprehensive Income

Net Increase/(Decrease) in

Property, Plant & Equipment

Revaluation 0 0 367,817 367,817

Total Comprehensive

Income for the Year

1,295,205 0 367,817 1,663,022

Balance at 30 June 2014 26,799,834 100 3,394,710 30,194,644

The accompanying notes form part of these Financial Statements.

TRUST REPORT 2015

18

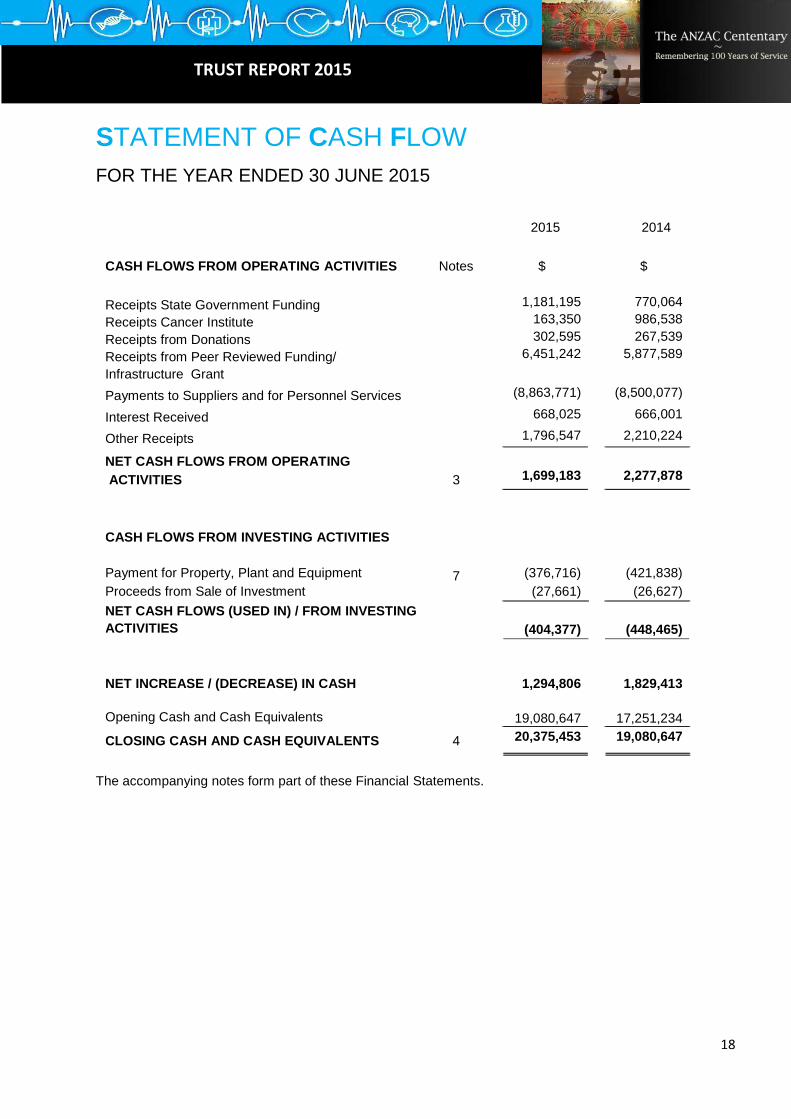

STATEMENT OF CASH FLOW

FOR THE YEAR ENDED 30 JUNE 2015

2015

2014

CASH FLOWS FROM OPERATING ACTIVITIES

Notes

$

$

Receipts State Government Funding

Receipts Cancer Institute

Receipts from Donations

Receipts from Peer Reviewed Funding/

Infrastructure Grant

1,181,195

163,350

302,595

6,451,242

770,064

986,538

267,539

5,877,589

Payments to Suppliers and for Personnel Services

(8,863,771)

(8,500,077)

Interest Received

668,025

666,001

Other Receipts

1,796,547

2,210,224

NET CASH FLOWS FROM OPERATING

ACTIVITIES

3

1,699,183

2,277,878

CASH FLOWS FROM INVESTING ACTIVITIES

Payment for Property, Plant and Equipment

Proceeds from Sale of Investment

7

(376,716)

(27,661)

(421,838)

(26,627)

NET CASH FLOWS (USED IN) / FROM INVESTING

ACTIVITIES

(404,377)

(448,465)

NET INCREASE / (DECREASE) IN CASH

1,294,806

1,829,413 Opening Cash and Cash Equivalents

19,080,647

17,251,234 CLOSING CASH AND CASH EQUIVALENTS

4

20,375,453

19,080,647

The accompanying notes form part of these Financial Statements.

TRUST REPORT 2015

19

NOTES TO THE FINANCIAL STATEMENTS

30 JUNE 2015

REPORTING ENTITY

The ANZAC Health and Medical Research Foundation Trust Fund (ANZAC) is an economic entity whose

principal activity is research and is a not-for-profit organization. It is consolidated as part of the Sydney

Local Health District and NSW Total State Sector Accounts.

ANZAC does not have any employees. It purchases personnel services from Sydney Local Health District

Special Purpose Service Entity (previously part of Sydney South West Area Health Service).

These financial statements have been authorised for issue by David Handelsman and Meng Ngu, Directors,

on 23rd

day of September 2015.

NOTE 1: SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

(A) BASIS OF PREPARATION

The financial statements are a general purpose financial statement that have been prepared in accordance with applicable Australian Accounting Standards (which include Australian Accounting Interpretations) and with the requirements of the Public Finance and Audit Act 1983 and Regulation. Property, plant and equipment and financial assets at fair value through profit and loss are measured at fair value. Other financial statements items are prepared in accordance with the historical cost convention. All amounts are expressed in Australian currency. Judgements, key assumptions and estimations made by management are disclosed in the relevant notes to the financial statements.

(B) COMPARATIVES INFORMATION

Except when an Australian Accounting Standard permits or requires otherwise, comparative information is

presented in respect of the previous period for all amounts reported in the financial statements.

(C) PERSONNEL SERVICES COSTS

ANZAC does not have any employees. It purchases personnel services from Sydney Local Health District

Special Purpose Service Entity.

The accrued salaries and wages component of the Personnel Services Liability is reported as “Current” as

there is an unconditional right to payment.

Annual leave is not expected to be settled wholly before twelve months after the end of the annual reporting

period in which the employees render the related service. As such, it is required to be measured at present

value in accordance with AASB 119 Employee Benefits (although short-cut methods are permitted).

Actuarial advice obtained by Treasury has confirmed that the use of a nominal approach plus the annual

leave on annual leave liability can be used to approximate the present value of the annual leave liability.

The Annual Leave component of the Personnel Services Liability is reported as “Current” as there is an

unconditional right to payment. Current liabilities are based on past trends and known resignations and

retirements. Anticipated payments to be made in the next twelve months are reported as “Short Term”.

TRUST REPORT 2015

20

NOTES TO THE FINANCIAL STATEMENTS (Continued)

30 June 2015

On-costs of 16.7% are applied to the value of leave payable at 30 June 2015, such on costs being

consistent with actuarial assessment (Comparable on costs for 30 June 2014 were also 16.5%).

Defined Benefit Superannuation (State Authorities Superannuation Scheme and State Superannuation

Scheme) and Long Service Leave Liabilities are assumed by the Crown Entity.

Long Service Leave is measured at present value in Accordance with AASB 119 Employee Benefits. This is

based on the application of certain factors (specified in NSW Treasury Circular 15/09) to employees with five

or more years of service, using current rates of pay. These factors were determined based on an actuarial

review to approximate fair value.

(D) PERSONNEL SERVICES LIABILITY

Provisions are recognised when:

the Trust has a legal, equitable or constructive obligation as a result of past transactions or other

past events;

it is probable that a future sacrifice of economic benefits will be required to settle the obligation;

and a reliable estimate can be made of the amount of the obligation.

(E) INCOME RECOGNITION

Revenue arising from the provision of services and the use of the Trust’s assets is recognised when:

a) ANZAC has passed control of the goods or other assets to the buyer;

b) ANZAC controls a right to be compensated for services rendered;

c) ANZAC controls a right relating to the consideration payable for the provision of investment assets;

d) it is probable that the economic benefits comprising the consideration will flow to the entity;

e) the amount of the revenue can be measured reliably.

The following specific recognition criteria must also be met before revenue is recognised:

Grants and Donations

Grants and contributions are generally recognised as revenues when ANZAC obtains control over the assets

comprising the contributions. Control over contributions is normally obtained upon receipt of cash.

Investment income

Interest revenue is recognised using the effective interest method as set out in AASB 139 Financial

Instruments: Recognition and Measurement.

(F) GOODS AND SERVICES TAX (GST)

Income, expenses and assets are recognised net of the amount of GST, except:

the amount of GST incurred by the Trust as a purchaser that is not recoverable from the Australian

Tax Office is recognised as part of the cost of acquisition of an asset or as part of an item of

expense;

receivables and payables are stated with the amount of GST included.

TRUST REPORT 2015

21

NOTES TO THE FINANCIAL STATEMENTS (Continued)

30 June 2015

Cash flows are included in the Statement of Cash Flows on a gross basis. However, the GST component of

cash flows arising from investing and financing activities which is recoverable from, or payable to, the

Australian Taxation Office are classified as operating cash flows.

(G) RESEARCH AND DEVELOPMENT COSTS

Research and development costs are charged as an expense in the year in which they are incurred.

(H) ACQUISITION OF ASSETS

The cost method of accounting is used for the initial recording of all acquisitions of assets. Cost is the

amount of cash or cash equivalents paid or the fair value of the other consideration given to acquire the

asset at the time of its acquisition or construction or, where applicable, the amount attributed to that asset

when initially recognised in accordance with the requirements of other Australian Accounting Standards.

Assets acquired at no cost, or for nominal consideration, are initially recognised at their fair value at the date

of acquisition.

Fair value is the amount for which an asset could be exchanged between knowledgeable, willing parties in

an arm’s length transaction.

Where payment for an asset is deferred beyond normal credit terms, its cost is the cash price equivalent, i.e.

the deferred payment amount is effectively discounted at an asset-specific rate.

(I) CAPITALISATION THREHOLDS

Individual items of property, plant & equipment are capitalised where their cost is $10,000 or above.

(J) DEPRECIATION OF PROPERTY, PLANT AND EQUIPMENT

Depreciation is provided for on a straight-line basis for all depreciable assets so as to write off the

depreciable amount of each depreciable asset as it is consumed over its useful life to the ANZAC.

Depreciation rates on individual assets are reviewed annually.

Details of depreciation rates and useful lives for major asset categories, according to the NSW Department

of Health Accounting Manual rates, are as follows:

Depreciation Rates Rate (%) Life (years)

Leasehold Buildings 4.0 25

Electro Medical Equipment

Costing less than $200,000

Costing more than $200,000

10.0

12.5

10

8

Computer Equipment 20.0 5

Computer Software 20.0 5

Office Equipment 10.0 10

Plant and Machinery 10.0 10

Furniture, Fittings and Furnishings 10.0 10

Depreciation rates are subsequently varied where changes occur in the assessment of the remaining useful

life of the assets reported.

TRUST REPORT 2015

22

NOTES TO THE FINANCIAL STATEMENTS (Continued)

30 June 2015

(K) REVALUATION AND IMPAIRMENT OF PROPERTY, PLANT AND EQUIPMENT

Physical non-current assets are valued in accordance with the NSW Ministry of Health’s "Valuation of

Physical Non-Current Assets at Fair Value" policy. This policy adopts fair value in accordance with

AASB116 Property, Plant and Equipment.

Property, plant and equipment is measured on an existing use basis, where there are no feasible alternative

uses in the existing natural, legal, financial and socio-political environment. However, in the limited

circumstances where there are feasible alternative uses, assets are valued at their highest and best use.

ANZAC revalues leasehold buildings at a minimum of every three years by independent valuation and with

sufficient regularity to ensure that the carrying amount of each asset does not differ materially from its fair

value at reporting date. The last revaluation for assets held by the Trust as at 30 June 2015 was completed

in June 2013 and was based on an independent assessment.

Non-specialised assets with short useful lives are measured at depreciated historical cost, as a surrogate for

fair value.

When revaluing non-current assets by reference to current prices for assets newer than those being

revalued (adjusted to reflect the present condition of the assets), the gross amount and the related

accumulated depreciation are separately restated.

For other assets, any balances of accumulated depreciation existing at the revaluation date in respect of

those assets are credited to the asset accounts to which they relate. The net asset accounts are then

increased or decreased by the revaluation increments or decrements.

Revaluation increments are credited directly to the asset revaluation reserve, except that, to the extent that

an increment reverses a revaluation decrement in respect of that class of asset previously recognised as an

expense in the surplus / (deficit) for the year, the increment is recognised immediately as revenue in the

surplus / (deficit) for the year.

Revaluation decrements are recognised immediately as expenses in the net result for the year, except that,

to the extent that a credit balance exists in the asset revaluation reserve in respect of the same class of

assets, they are debited directly to the asset revaluation reserve. As a not-for-profit entity, revaluation

increments and decrements are offset against one another within a class of non-current assets, but not

otherwise.

Where an asset that has previously been revalued is disposed of, any balance remaining in the asset

revaluation reserve in respect of that asst is transferred to accumulated funds.

Costs incurred in relation to the construction of the ANZAC Health & Medical Research Institute have been

capitalised as leasehold buildings. Leasehold buildings are carried at fair value.

The leasehold buildings have been built on land leased from Sydney Local Health District. The rent during

the initial term of the lease is in the sum of one dollar ($1) per annum. The lease for the land and buildings

is for 25 years which will end in December 2027. The New South Wales’ Minister of Health may terminate

this lease on expiry by effluxion of the term of the lease or for breach of its term, or at any time on

reasonable notice.

TRUST REPORT 2015

23

NOTES TO THE FINANCIAL STATEMENTS (Continued)

30 June 2015

(K) REVALUATION AND IMPAIRMENT OF PROPERTY, PLANT AND EQUIPMENT (continued)

The lease for the ANZAC Foundation Building has been classified as a finance lease based on the following

judgements:

The 25 year lease term represents the major part of the economic life of the building,

The ANZAC Research Institute will occupy the building for the term of the lease,

While the New South Wales’ Minister of Health has the right to terminate the lease at any time with

reasonable notice (as noted above), the economic substance of the lease is that this right will not be

exercised during the term of the lease.

As a not-for-profit entity with no cash generating units, impairment under AASB 136 Impairment of Assets is

unlikely. This is because AASB 136 modifies the recoverable amount test to the higher of fair value less

costs to sell and depreciated replacement cost. This means that, for an asset already measured at fair

value, impairment can only arise if selling costs are regarded as material. Selling costs are regarded as

immaterial.

(L) INCOME TAX

ANZAC is exempt from income tax under Section 11-5 of the Income Tax Assessment Act 1997.

(M) CASH AND CASH EQUIVALENTS

For the purpose of the Statement of Cash Flows, cash and cash equivalent include cash on hand and at call

deposits with banks or financial institutions.

(N) SETTLEMENT ACCOUNT

The ANZAC Health and Medical Research Foundation Trust Fund was made between Robert Edward

McKeown, the settlor, and the ANZAC Health and Medical Research Foundation, the trustee, on 21

February 1995. The Trust has carried out all operating activities in accordance with the provisions of the trust

deed.

(O) MAINTENANCE

Day-to-day servicing costs or maintenance are charged as expenses as incurred, except where they relate

to the replacement of a part or component of an asset, in which case the costs are capitalised and

depreciated.

(P) LOANS AND RECEIVABLES

Loans and receivables are non-derivative financial assets with fixed or determinable payments that are not

quoted in an active market. These financial assets are recognised initially at fair value, usually based on

the transaction cost or face value. Subsequent measurement is at amortised cost using the effective

interest method, less an allowance for any impairment of receivables. Any changes are recognised in the

surplus / (deficit) for the year when impaired, derecognised or through the amortisation process.

Short-term receivables with no stated interest rate are measured at the original invoice amount where the

effect of discounting is immaterial.

TRUST REPORT 2015

24

NOTES TO THE FINANCIAL STATEMENTS (Continued)

30 June 2015

(Q) INVESTMENTS

Investments are initially recognised at fair value plus, in the case of investments not at fair value through

profit or loss, transaction costs. The ANZAC determines the classification of its financial assets after initial

recognition and, when allowed and appropriate, re-evaluates this at each financial year end.

(R) IMPAIRMENT OF FINANCIAL ASSETS

All financial assets, except those measured at fair value through profit and loss, are subject to an annual

review for impairment. An allowance for impairment is established when there is objective evidence that the

entity will not be able to collect all amounts due.

For financial assets carried at amortised cost, the amount of the allowance is the difference between the

asset’s carrying amount and the present value of estimated future cash flows, discounted at the effective

interest rate. The amount of the impairment loss is recognised in the surplus / (deficit) for the year.

(S) PAYABLES

These amounts represent liabilities for goods and services provided to the ANZAC and other amounts.

Payables are recognised initially at fair value, usually based on the transaction cost or face value.

Subsequent measurement is at amortised cost using the effective interest method. Short-term payables with

no stated interest rate are measured at the original invoice amount where the effect of discounting is

immaterial.

Payables are recognised for amounts to be paid in the future for goods and services received, whether or

not billed to ANZAC.

(T) EQUITY

(i) Asset Revaluation Reserve

The asset revaluation reserve is used to record increments and decrements on the revaluation of non-

current assets. This accords with the ANZAC policy on the revaluation of property, plant and equipment as

discussed in note 1(K).

(ii) Accumulated Funds

The category accumulated funds includes all current and prior period retained funds.

(U) FAIR VALUE HIERARCHY

A number of ANZAC’s accounting policies and disclosures require the measurement of fair values, for both

financial and non-financial assets and liabilities. When measuring fair value, the valuation technique used

maximises the use of relevant observable inputs and minimises the use of unobservable inputs. Under

AASB 13, ANZAC categorises, for disclosure purposes, the valuation techniques based on the inputs used

in the valuation techniques as follows:

Level 1 – quoted prices in active markets for identical assets / liabilities that the entity can access at

the measurement date.

TRUST REPORT 2015

25

NOTES TO THE FINANCIAL STATEMENTS (Continued)

30 June 2015

Level 2 – inputs other than quoted prices included within Level 1 that are observable, either directly

or indirectly.

Level 3 – inputs that are not based on observable market data (unobservable inputs).

ANZAC recognises transfers between levels of the fair value hierarchy at the end of the reporting period

during which the change has occurred.

Refer Note 15 and Note 16 for further disclosures regarding fair value measurements of financial and non-

financial assets.

(V) NEW AUSTRALIAN ACCOUNTING STANDARDS ISSUED BUT NOT EFFECTIVE

(i) Effective for the first time in 2014-15

There will be no material implications for the financial statements for new accounting standards issued

but not effective.

(ii) Issued but not yet effective

There are some Australian Accounting Standards and other authoritative pronouncements of the

Australian Accounting Standards Board that have been issued but not yet effective. ANZAC has not

early adopted these and does not consider that the adoption of the Standards and pronouncements will

have a significant impact upon the Financial Statements.

TRUST REPORT 2015

26

NOTES TO THE FINANCIAL STATEMENTS (Continued)

30 June 2015

NOTE 2: REVENUE AND EXPENSES

2015 2014 (a) Revenue

$ $

Donations Corporate

73,760

19,000

Donations RSL 1,750 1,600 Donations Other 151,335 320,309 Fundraising Activities 750 1,630 State Government Funding 1,073,814 700,058 Cancer Institute Grant 148,500 896,853 Interest Income 654,650 667,690 Peer Reviewed Funding Infrastructure Grant

4,450,203 1,567,500

3,767,430 1,162,782

Contribution from Hospital Departments 524,235 385,240 Sponsorship 13,634 28,032 Research Service 255,659 293,944 Research Study 502,050 1,476,824 Other Revenue 122,802 221,103

Total Revenue 9,540,642 9,942,495

(b) Expenses

Personnel Services Costs 5,094,772 4,875,950 Consumables 1,417,926 1,347,177 Administrative

Conference, Training & Travel

202,656

271,442 Advertising 1,530 480 Functions 24,143 24,656 Accounting & Legal Fees 2,708 22,815 Audit Fees 25,650 25,100 Payment of Grants 85,962 185,838 Accreditation Fees 194 352 Scholarships 256,460 253,459 Books & Reference Material 38,660 25,193 Stationery & Office Supplies 33,324 39,441 Freight & Courier 67,502 64,807 Directors & Officers Liability Insurance 3,571 3,586 Miscellaneous Administrative Expenses 739,484 430,037

1,481,844 1,347,206

Depreciation 783,375 830,788 Repairs, Maintenance & Renewals

Equipment 79,762 105,879 Other 108,786 121,184

188,548 226,063

Total Expenses 8,966,465 8,627,184

TRUST REPORT 2015

27

NOTES TO THE FINANCIAL STATEMENTS (Continued)

30 June 2015

NOTE 3: RECONCILIATION OF CASH FLOWS FROM OPERATING ACTIVITIES TO SURPLUS FOR THE

YEAR

2015

$

2014

$

Net Cash Flows from Operating Activities 1,699,183

2,277,878

Gain/(Loss) on Disposal (18,697)

(20,106)

Recognition of Assets Previously Expensed 0

135,000

Depreciation (783,375)

(830,788)

(Increase)/Decrease in Payable for Personnel Services

Liability

23,551

(47,792)

(Increase)/Decrease in Payables (7,822)

(5,754)

(Increase)/Decrease in Provision (72,591)

(123,903)

Increase/(Decrease) in Receivables (284,769) (89,330)

Surplus for the year 555,480

1,295,205

NOTE 4: CASH AND CASH EQUIVALENTS

(a) Cash

General Professional Funds Account 20,847 648,457

Research Professional Funds Account 1,449,754 751,389

Donations Cash Management Account 10,577 7,292

Total Cash 1,481,178 1,407,138

Term Deposits at Bank 18,894,275 17,673,509

Total Cash and Cash Equivalents

20,375,453

19,080,647

Information on the effective interest rate, credit risk and market risk of cash and cash equivalents is

disclosed in Note 16.

(b) Reconciliation of Cash

Cash at the End of the Financial Year as shown in the

Statement of Cash Flows is reconciled to the related

items in the Statement of Financial Position as follows:

Cash at Bank 1,481,178

1,407,138

Term Deposits at Bank 18,894,275

17,673,509

Total Cash and Cash Equivalents 20,375,453

19,080,647

TRUST REPORT 2015

28

NOTES TO THE FINANCIAL STATEMENTS (Continued)

30 June 2015

2015 2014

$ $

NOTE 5: FINANCIAL ASSETS AT FAIR VALUE

Treasury Corporation - Hour Glass Facility 402,116 374,454

Information on the effective interest rate, credit risk and market risk is disclosed in Note 16.

NOTE 6: RECEIVABLES – CURRENT

Accounts Receivable 892,518 1,290,269

Less: Allowance for Impairment 0 0

Interest Receivable 64,351 77,727

Sub Total 956,869 1,367,996

Prepayments 126,357 0

Total 1,083,226 1,367,996

Accounts receivable as at 30 June 2015 and 30 June 2014 are non-interest bearing.

Information on credit risk on Accounts receivable is detailed in Note 16.

NOTE 7: PROPERTY, PLANT AND EQUIPMENT

Leasehold

Buildings Plant & Equipment Total

At 1 July 2015- Fair Value

Gross carrying Amount 13,228,593 4,746,398 17,974,991

Accumulated Depreciation and

Impairment (4,618,284) (2,852,824) (7,371,108)

Net carrying amount 8,610,309 1,993,574 10,603,883

At 1 July 2014 – Fair Value

Gross carrying Amount 13,097,616 4,518,341 17,615,957

Accumulated Depreciation and

Impairment 4,125,153) (2,549,052) (6,674,205)

Net carrying amount 8,972,463 1,969,289 10,941,752

TRUST REPORT 2015

29

NOTES TO THE FINANCIAL STATEMENTS (Continued)

30 June 2015

NOTE 7: PROPERTY, PLANT AND EQUIPMENT (Continued)

2015

Leasehold

Buildings Plant & Equipment

2015

Total

Net Carrying Amount at Start of Year 8,972,463 1,969,289 10,941,752

Additions 0 376,716 376,716

Disposals 0 (18,697) (18,697)

Net Revaluation Increment Less

Revaluation Decrements Recognised in

Reserve 87,488

0 87,488

Depreciation Expense (449,642) (333,734) (783,376)

Net Carrying Amount at End of Year 8,610,309 1,993,574 10,603,883

Leasehold buildings are owned by ANZAC and administered by Sydney Local Health District.

Leasehold buildings were valued by Mark Greenhalgh FAPI (Corporeal Property Valuers) in 2012/2013

financial year (refer Note 1 (K)).

Purpose built health facilities have been valued at fair value for their existing use. As current market prices

are difficult to observe, the assets fair value is measured at depreciated replacement cost based on the

assumption that the asset’s economic life is 25 years.

2014

Leasehold

Buildings Plant & Equipment

2014

Total

Net Carrying Amount at Start of Year 9,047,664 1,820,327 10,867,991

Additions 0 556,838 556,838

Disposals 0 (20,107) (20,107)

Net Revaluation Increment Less

Revaluation Decrements Recognised in

Reserve 367,817

0 367,817

Depreciation Expense (443,018) (387,769) (830,787)

Net Carrying Amount at End of Year 8,972,463 1,969,289 10,941,752

NOTE 8: PAYABLES 2015 2014

$ $

Current Payables

Creditors and Accruals

Unearned Revenue

GST Payable

790,869

49,500

59,686

728,315

0

187,469

900,055 915,784

Information on liquidity risk and market risk, including a maturity analysis of the above payables is disclosed

in Note 16.

TRUST REPORT 2015

30

NOTES TO THE FINANCIAL STATEMENTS (Continued)

30 June 2015

NOTE 9: PROVISIONS

Credit Facility 15,000 15,000

Unused Credit Facility 13,374 14,346

11: CONTINGENT LIABILITIES AND CONTINGENT ASSETS

At the date of this report the Trust Fund has no known contingent liabilities and contingent assets (2015: Nil ;

2014: Nil ).

NOTE 12: CONDITIONS ON CONTRIBUTIONS - RESEARCH PURPOSES

Research 2015 Research 2014

$ $

Contributions recognised as revenues for which

expenditure in manner specified has not occurred

as at balance date

6,282,838

5,722,133

Contributions recognised in previous years that were

not expended in the current financial year

2,333,412

3,561,792

Total amount of unexpended contributions

as at balance date

8,616,250

9,283,925

Further comments on restricted assets are included in Note 13.

Current Provisions

Current Provisions for Personnel Services Liability

Annual Leave – Short Term Benefit

Annual Leave – Long Term Benefit

430,250

296,761

382,423

271,998 727,011

654,421

NOTE 10: CAPITAL EXPENDITURE COMMITMENTS AND

CREDIT FACILITY

Capital expenditure commitments for plant and equipment that

have not been provided for in the accounts:

Payable Not Later than One Year (including GST)

The total of capital expenditure commitments of $223,972

above as at 30 June 2015 includes input tax credits of $20,361

that are expected to be recoverable from the Australian

Taxation Office (2015: $20,361; 2014: $0

223,972

125,165

TRUST REPORT 2015

31

NOTES TO THE FINANCIAL STATEMENTS (Continued)

30 June 2015

NOTE 13: RESTRICTED ASSETS

These financial statements include the following assets that are restricted by externally imposed conditions

e.g. donor requirements. The assets are only available for application in accordance with the terms of the

donor restrictions.

2015 2014

Category $ $

Specific Purposes

Donations for Research Specific Use 1,013,023 1,008,436

Research Grants

Specific Project Grants 6,030,117 2,249,995

Holding Funds 1,573,110 6,025,494

8,616,250 9,283,925

Category Brief Details of Externally Imposed Conditions

Specific Purposes Trust Funds Donations, contributions and fundraisings held for the benefit of

Laboratory groups.

Research Grants Specific research grants.

TRUST REPORT 2015

32

NOTES TO THE FINANCIAL STATEMENTS (Continued)

30 June 2015

NOTE 14: FUNDRAISING AND APPEAL ACTIVITIES

The ANZAC Health and Medical Research Foundation Trust Fund is a certified holder of an authority to raise

funds under the provision of section 16 of the Charitable Fundraising Act, 1991. The net proceeds are held

in ANZAC Health & Medical Research Foundation Trust Fund pending allocation.

INCOME

RAISED

$

DIRECT

EXPENDITURE

$

INDIRECT

EXPENDITURE

$

2015 NET

PROCEED

S

$

2013 NET

PROCEED

S

$ Appeals 750 248 0 502 1,380 Functions 0 0 0 0 0

Total 750 248 0 502 1,380 Percentage of Income 100% 33.00% 0% 67.00% 84.69%

Direct expenditure includes printing, postage, food and beverage.

Indirect expenditure includes additional staff time.

The net proceeds were used for the following purposes:

2015

$

2014

$

Purchase of Equipment 0 0

Purchase of Land & Building 0 0

Research 0 0

Held for Other Purposes 502 1,380

502 1,380

NOTE 15: FAIR VALUE MEASUREMENT OF NON-FINANCIAL ASSETS

Fair value measurements recognised in the balance sheet are categorised into the following levels at 30

June 2015.

a) Fair Value Hierarchy

2015

Level 1

$

Level 2

$

Level 3

$

Total

$

Property, Plant and Equip (Note 7)

- Land and Buildings 0 0 8,610,309 8, 610,309

0 0 8,610,309 8, 610,309

There were no transfers between level 1 and 2 during the period ended 30 June 2015.

2014

Level 1

$

Level 2

$

Level 3

$

Total

$

Property, Plant and Equip (Note 7)

- Land and Buildings 0 0 8,972,463 8,972,463

0 0 8,972,463 8,972,463

There were no transfers between level 1 and 2 during the period ended 30 June 2015 (2014:nil).

TRUST REPORT 2015

33

NOTES TO THE FINANCIAL STATEMENTS (Continued)

30 June 2015

For non-specialised assets with short useful lives, Treasury policy paper 14-01 allows recognition at

depreciated historical cost as an acceptable surrogate for fair value as differences are considered

immaterial. Thus the values for Plant and Equipment are not required to be reported under the fair value

hierarchy.

b) Valuation Techniques, Inputs and Processes

For land, building and infrastructure ANZAC obtains external valuations by independent valuers every

three years. The last revaluation was performed by Mark Greenhalgh FAPI (Corporeal) for the 2012/13

financial year. Corporeal is an independent entity and is not an employee of ANZAC.

At the end of each reporting period a fair value assessment is made on any movements since the last

revaluation, and a determination as to whether any adjustments need to be made. These adjustments

are made by way of application of a 1% index (2014: 2%) as determined in consultation with an

independent valuer.

In accordance with AASB 13 Fair Value Measurement no assets have been found to have a higher and

better use than their current use. Highest and best use takes account of use that is physically possible,

legally permissible and financially feasible.

The following non-current assets categorised in a) above have been measured as level 3 based on the

following valuation techniques and inputs:

For buildings and infrastructure, many assets are of a specialised nature or use, and thus the most

appropriate valuation method is current replacement cost. These assets are included as level 3 as

these assets have a high level of unobservable inputs.

Level 3 significant valuation inputs and relationship to fair value:

The valuation of buildings was computed by suitably qualified independent valuers using a methodology

known as the depreciated replacement cost valuation technique. The following table highlights the key

unobservable (Level 3 inputs assessed during the valuation process, the relationship to the estimated

fair value and the sensitivity to changes in unobservable inputs.

Assets Valuation Technique Significant

Unobservable

Inputs

Relationship between

unobservable inputs and

fair value measurements

Specialised

Buildings

Depreciated replacement cost

approach: this valuation

method involves establishing

the current replacement cost of

the modern equivalent asset

for each type of buildings on a

rate per square metre basis;

depreciated to reflect the

building’s remaining useful life.

Useful life

assessment

Replacement

cost per square

metre

The fair value will

increase/(decrease) if the

estimated:

Useful life assessment

increases/(decreases)

Replacement cost per

square metre

increases/(decreases)

There are no other direct or significant relationships between the unobservable inputs which materially

TRUST REPORT 2015

34

impact fair value.

NOTES TO THE FINANCIAL STATEMENTS (Continued)

30 June 2015

c) Reconciliation of Recurring Level 3 Fair Value Measurements

Land and

Buildings

$

Level 3

Recurring Total

$

Fair value as at 1 July 2014 8,972,463 8,972,463

Additions 0 0

Revaluation increments/(decrements) 87,488 87,488

Depreciation (449,642) (449,642)

Fair value as at 30 June 2015 8,610,309 8,610,309

Land and

Buildings

$

Level 3

Recurring Total

$

Fair value as at 1 July 2013 9,047,664 9,047,664

Additions 0 0

Revaluation increments/(decrements) 367,817 367,817

Depreciation (443,018) (443,018)

Fair value as at 30 June 2014 8,972,463 8,972,463

NOTE 16: FINANCIAL INSTRUMENTS

ANZAC’s principal financial instruments are outlined below. These financial instruments arise directly from

ANZAC’s operations or are required to finance its operations. ANZAC does not enter into or trade financial

instruments, including derivative financial instruments, for speculative purposes.

ANZAC’s main risks arising from financial instruments are outlined below, together with ANZAC’s objectives,

policies and processes for measuring and managing risk. Further quantitative and qualitative disclosures

are included throughout these financial statements.

The Directors have overall responsibility for the establishment and oversight of risk management and

reviews and agree policies for managing each of these risks. Risk management policies are established to

identify and analyse the risk faced by ANZAC, to set risk limits and controls and monitor risks. Compliance

with policies is reviewed by the Audit Committee/internal auditors of Sydney Local Health District on a

continuous basis.

TRUST REPORT 2015

35

NOTES TO THE FINANCIAL STATEMENTS (Continued)

30 June 2015

(a) Financial Instrument Categories

Financial Assets Class: Category Carrying Amount Carrying Amount

2015 2014

$ $

Cash and Cash

Equivalents (note 4)

N/A 20,375,453 19,080,647

Receivables (note 6) Receivables (at

Amortised Cost)1

956,869 1,367,996

Financial Assets at

Fair Value (note 5)

At Fair Value through

Profit or Loss

(designated as such

upon Initial

Recognition)

402,116 374,454

Total Financial Assets 21,734,438 20,823,097

Financial Liabilities

Payables (note 8)

Financial liabilities

Measured at

Amortised Cost 2

790,869

728,315

Total Financial

Liabilities

790,869

728,315

Notes

1. Excludes statutory receivables and prepayments (i.e. not within scope of AASB 7).

2. Excludes statutory payables and unearned revenue (i.e. not within scope of AASB 7).

(b) Credit Risk

Credit risk arises when there is the possibility of ANZAC’s debtors defaulting on their contractual obligations,

resulting in a financial loss to ANZAC. The maximum exposure to credit risk is generally represented by the

carrying amount of the financial assets (net of any allowance for impairment).

Credit risk arises from financial assets of ANZAC i.e. receivables. No collateral is held by ANZAC, nor has it

granted any financial guarantees.

Credit risk associated with ANZAC’s financial assets, other than receivables, is managed through the

selection of counterparties and establishment of minimum credit rating standards. Deposits held with New

South Wales Treasury Corporation (TCorp) are guaranteed by the State.

Cash and Term Deposits

Cash comprises cash on hand and bank balance deposited in accordance with Public Authorities (Financial

TRUST REPORT 2015

36

Arrangements) Act 1987 approvals. Interest is earned on daily bank balances at rates of approximately

NOTES TO THE FINANCIAL STATEMENTS (Continued)

30 June 2015

1.80% to 2.30% in 2014/15 compared to 2.30% to 2.80% in the previous year. Anzac places funds on

deposits with national and reputable commercial bank. The deposits at balance date were earning an

average interest rate of 2.73% (2014: 3.44%). The TCorp Hour-Glass Investment Facilities are discussed in

paragraph (d) below.

Account Receivables

All debtors are recognised as amounts receivable at balance date. Collectability of debtors is reviewed on

an ongoing basis. Procedures as established in the NSW Ministry of Health Accounting Manual and Fee

Procedures Manual are followed to recover outstanding amounts, including letters of demand. Debts, which

are known to be uncollectable are written off. An allowance for impairment is raised when there is objective

evidence that ANZAC will not be able to collect the amounts due. The evidence includes past experience

and current and expected changes in economic conditions and debtor credit ratings. No interest is earned

on debtors.

ANZAC is not materially exposed to concentrations of credit risk to a single debtor or group of debtors. Of

the total debtors at year-end, $348,094 (2014: $924,015) related to debtors that were not past due and not

considered impaired and debtors of $544,424 (2014: $366,254) were past due but not considered impaired.

(c) Liquidity Risk

Liquidity risk is the risk that ANZAC will be unable to meet its payment obligations when they fall due.

ANZAC continuously manages risk through monitoring future cash flows and maturities planning to ensure

adequate holding of high quality liquid assets. The objective is to maintain a balance between continuity of

funding and flexibility through effective management of cash, investments and liquid assets and liabilities.

During the current and prior year, there were no defaults or breaches on any loans payable. No assets have

been pledged as collateral. ANZAC’s exposure to liquidity risk is deemed insignificant based on prior

periods’ data and current assessment of risk.

The liabilities are recognised, for amounts due to be paid in the future for goods or services received,

whether or not invoiced. Amounts owing to suppliers (which are unsecured) are generally settled in

accordance with the policy set by the NSW Department of Health. If trade terms are not specified, payment

is generally made no later than the end of the month following the month in which an invoice or a statement

is received.

In those instances where settlement cannot be affected in accordance with the above, e.g. due to short term

liquidity constraints, terms of payment are negotiated with creditors.

The table below summarises the maturity profile of ANZAC’s financial liabilities together with the interest rate

exposure.

TRUST REPORT 2015

37

NOTES TO THE FINANCIAL STATEMENTS (Continued)

30 June 2015

Maturity analysis and interest rate exposure of financial liabilities

$000

Interest Rate Exposure Maturity Dates

2015

W e i g h t e d Average Effective

Int rate

N o m i n a l Amount

F i x e d Interest

Rate

V a r i a b l e Interest

Rate

N o n - Interest Bearing

<1 Year

1-5 Years

>5 Years

% $’000 $’000 $’000 $’000 $’000 $’000 $’000

Payables:

Creditors - 790 0 0 840 840 0 0

790 0 0 840 840 0 0

2014

Payables:

Creditors - 728 0 0 728 728 0 0

728 0 0 728 728 0 0

Notes:

1. The amounts disclosed are the contractual undiscounted cash flows of each class of financial liabilities

based on the earliest date on which ANZAC can be required to pay. The tables include both interest and

principal cash flows and therefore will not reconcile to the Statement of Financial Position.

(d) Market Risk

Market risk is the risk that the fair value of future cash flows of a financial instrument will fluctuate because of

changes in market prices. ANZAC’s exposures to market risk are primarily through interest rate risk on

ANZAC’s cash holdings and other price risks associated with the movement in the unit price of the Hour-

Glass Investment facilities. ANZAC has no exposure to foreign currency risk and does not enter into

commodity contracts.

The effect on profit and equity due to a reasonably possible change in risk variable is outlined in the

information below, for interest rate and other price risk. A reasonably possible change in risk variable has

been determined after taking into account the economic environment in which ANZAC operates and the time

frame for the assessment (i.e. until the end of the next annual reporting period). The sensitivity analysis is

based on risk exposures in existence at the balance sheet date. The analysis is performed on the same

basis for 2015. The analysis assumes that all other variables remain constant.

Interest Rate Risk

Exposure to interest rate risk arises primarily through ANZAC’s cash holdings.

For financial instruments a reasonably possible change of +/-1% is used consistent with current trends in

interest rates. ANZAC’s exposure to interest rate risk is set out below.

$

-1% +1%

Carrying Amount Profit Equity Profit Equity

2015 Financial Assets

Cash and Cash Equivalents 20,375,453 (203,754) (203,754) 203,754 203,754

2014 Financial Assets

TRUST REPORT 2015

38

Cash and Cash Equivalents 19,080,647 (190,806) (190,806) 190,806 190,806

NOTES TO THE FINANCIAL STATEMENTS (Continued)

30 June 2015

Other price risk – TCorp Hour Glass Facilities

Exposure to ‘other price risk’ primarily arises through the investment in the TCorp Hour-Glass Investment

Facilities, which are held for strategic rather than trading purposes. ANZAC has no direct equity

investments. ANZAC holds units in the following Hour-Glass investment trusts:

Facility Investment Sectors Investment

Horizon

2015

$

2014

$

Medium term

growth facility

Cash, Money Market

Instruments Australian and

International Bonds, Listed

Property and Australian

Shares

3 to 7 years 402,116 374,454

The unit price of each facility is equal to the total fair value of net assets held by the facility divided by the

total number of units on issue for that facility. Unit prices are calculated and published daily.

NSW TCorp is trustee for each of the above facilities and is required to act in the best interest of the unit

holders and to administer the trusts in accordance with the trust deeds. As trustee, TCorp has appointed

external managers to manage the performance and risk of each facility in accordance with a mandate

agreed by the parties. However, TCorp acts as the manager for part of the Cash and Strategy Cash

Facilities and also manages the Australian Bond portfolio. A significant portion of the administration of the

facilities is outsourced to an external custodian.

Investment in the Hour- Glass Facilities limits ANZAC’s exposure to risk, as it allows diversification across a

pool of funds, with different investment horizons and a mix of investments.

NSW TCorp provides sensitivity analysis information for each of the investment facilities, using historically

based volatility information collected over a ten year period, quoted at two standard deviations (i.e. 95%

probability). The TCorp Hour Glass Investment Facilities are designated at fair value through profit or loss

and therefore any change in unit price impacts directly on profit (rather than equity).

A reasonably possible change is based on the percentage change in unit price (as advised by TCorp)

multiplied by the redemption price as at 30 June each year for each facility (balance from Hour-Glass

Statement).

Impact on profit/loss

Change in

Unit Price

2015

$

2014

$

Hour Glass Investment – Medium Term Growth facility +/-6% 24,127 22,467

(e) Fair Value Recognised in the Statement of Financial Position

ANZAC uses the following hierarchy for disclosing the fair value of financial instruments by valuation

technique:

Level 1 – derived from quoted prices in active markets for identical assets/liabilities

Level 2 – derived from inputs other than quoted prices that are observable directly or indirectly.

Level 3 – derived from valuation techniques that include inputs for the asset/liability not based on observable

TRUST REPORT 2015

39

market data (unobservable inputs).

NOTES TO THE FINANCIAL STATEMENTS (Continued)

30 June 2015

Level 1

$

Level 2

$

Level 3

$

2015 Total

$

TCorp Hour-Glass Investment Facility 0 402,116 0 402,116

Level 1

$

Level 2

$

Level 3

$

2014 Total

$

TCorp Hour-Glass Investment Facility 0 374,454 0 374,454

(The table above only includes financial assets as no financial liabilities were measured at fair value in the

Statement of Financial Position).

There were no transfers between level 1 and 2 during the period ended 30 June 2015.

NOTE 17: AUDITOR’S REMUNERATION

2015 2014

$ $

The total remuneration received, or due and receivable by the auditors of ANZAC for

auditing the accounts of the Trust Fund was accrued in the accounts herein.

25,650 25,100

NOTE 18: AFTER BALANCE DATE EVENTS

After the reporting date, there were no events subsequent which would have a material effect on the

ANZAC’s financial statements.

END OF AUDITED FINANCIAL STATEMENTS

TRUST REPORT 2015

40

TRUSTEES’ DECLARATION

Pursuant to Section 41C (1B), in accordance with a resolution of ANZAC Health and Medical Research

Foundation Trust Fund, we state that:

In the opinion of the Trustees:

(a) the financial statements and notes of the Trust:

i. exhibit a true and fair view of the Trust’s financial position as at 30 June 2015 and of its

performance as represented by the results of its operations and its cash flows for the year

ended on that date; and

ii. comply with the applicable Australian Accounting Standards; which include Australian

Accounting Interpretations and (b) the provisions of the Public Finance and Audit Act 1983 and the Public Finance and Audit

Regulation 2010 have been complied with;

(c) there are no circumstances that would render any particulars included in the financial

statements to be misleading or inaccurate.

On behalf of the Trustees

Meng Ngu David Handelsman

Acting Chair Director

Dated this 23rd day of September 2015 at Sydney.