Embed Size (px)

Citation preview

CUSTOMER SERVICE ENVIRONMENTAL AUDIT OF CITY OF

TSHWANE METROPOLITAN MUNICIPALITY: REGIONS 5 AND 7

Study commissioned by

CITY OF TSHWANE METROPOLITAN MUNICIPALITY Customer Relations Management Division

Study conducted by

B U R E A U O F M A R K E T R E S E A R C H College of Economic and Management Sciences

Project Owner

CUSTOMER RELATIONS MANAGEMENT DIVISION: CITY OF TSHWANE

CUSTOMER SERVICE ENVIRONMENTAL AUDIT OF CITY OF TSHWANE

METROPOLITAN MUNICIPALITY: REGIONS 5 AND 7

May 2012

Study commissioned by

CITY OF TSHWANE METROPOLITAN MUNICIPALITY Customer Relations Management Division

Compiled by

Prof DH Tustin (Executive Research Director)

Prof AA Ligthelm (Research Director) Ms M Goetz (Senior Research Coordinator)

BUREAU OF MARKET RESEARCH College of Economic and Management Sciences

Project Owner

CUSTOMER RELATIONS MANAGEMENT DIVISION: CITY OF TSHWANE

CR036 Pretoria

2012

ACKNOWLEDGEMENTS

The following individuals have contributed to the completion of this research project: Ms M Khaebana (Executive Director: Customer Relations Management Division, Corporate

and Shared Services Department - City of Tshwane)

Ms M Oosthuizen (Deputy Director: Customer Relations Strategy and Process Development - City of Tshwane)

Ms NJ Leriba (Bureau of Market Research: Data capturing)

Ms C Kemp (Bureau of Market Research: Language Editing)

Ms E Koekemoer (Bureau of Market Research: Report typing)

Ms M Goetz and Ms P de Jongh (Bureau of Market Research: Report typing, technical layout, data editing, cleaning and analysis)

Other City of Tshwane officials who played a key role in the success of the project:

Survey Projects Committee

Kishore Bedhesi; Barry Gerber; Melato Chikane; Pieter Cronje; Nico Manyelo; Nkagi Ndlovu; Willemien Hamman; Motladiile Zungu; Veronica Selatole; Thandi Madi; Aubrey Baloyi; Victor Seroka; Prudence Maisela; Terrence Melly;

Region 5 Regional Executive Director: Adv Frederick Lekwane; Goodwill Rahotsi; Veronica Selatole;

Region 7 Regional Executive Director: Oscar Moalusi; Aubrey Baloyi; Thandi Madi; Nonhlanhla S. Magagula; Prudence Maisela

Fieldworkers conducting intercept interviews at customer care walk-in centres/pay points in

regions 5 and 7

City of Tshwane personnel at all the customer interaction points in regions 5 and 7

Interviewers conducting computer-aided telephone interviews

Participating CoT customers

Councillors in regions 5 and 7

Language Services, Strategic Communication Division; Communication, Marketing and Events

The Customer Relations Management Division of the City of Tshwane would like to thank Prof

Deon Tustin and Prof André Ligthelm of the Bureau of Market Research for sharing their

knowledge and experience with us and for once again conducting a professional and exceptional

survey.

Exclusion of claims. Despite all efforts to ensure accuracy in the assembly of information and

data or the compilation thereof, the BMR is unable to warrant the accuracy of the information,

data and compilations as contained in its reports or any other publication for which it is

responsible. Readers of all the publications referred to above are deemed to have waived and

renounced all rights to any claim against Unisa and the BMR, its officers, project committee

members, servants or agents for any loss or damage of any nature whatsoever arising from any

use or reliance upon such information, data or compilations.

i

TABLE OF CONTENTS Page LIST OF TABLES .............................................................................................................................. iii LIST OF FIGURES ............................................................................................................................ iv LIST OF EXHIBITS ............................................................................................................................. v EXECUTIVE SUMMARY .................................................................................................................. vi CHAPTER 1: INTRODUCTION AND STUDY OBJECTIVE 1.1 INTRODUCTION ............................................................................................................... 1 1.2 OBJECTIVE OF THE STUDY ............................................................................................... 2 1.3 OUTLINE OF THE REPORT ................................................................................................ 2 CHAPTER 2: SURVEY METHODOLOGY 2.1 INTRODUCTION ............................................................................................................... 3 2.2 RESEARCH SCOPE ............................................................................................................ 3 2.3 QUANTITATIVE RESEARCH .............................................................................................. 4 2.3.1 Survey population ........................................................................................................... 4 2.3.2 Sampling plan .................................................................................................................. 4 2.3.3 Sample size ...................................................................................................................... 5 2.3.4 Research instrument ....................................................................................................... 6 2.3.5 Fieldwork ......................................................................................................................... 7 2.3.6 Data coding and capturing .............................................................................................. 7 2.4 QUALITATIVE PHASE ....................................................................................................... 7 2.5 CONCLUDING REMARKS ................................................................................................. 7

ii

CHAPTER 3: RESEARCH ANALYSIS 3.1 INTRODUCTION ............................................................................................................... 8 3.2 RESPONDENT PROFILE .................................................................................................... 8 3.3 CUSTOMER INTERACTION ............................................................................................. 10 3.4 PERSONAL INTRACTION WITH THE CoT ....................................................................... 14 3.4.1 Customer satisfaction ................................................................................................... 21 3.5 TELEPHONIC INTERACTION WITH THE CoT .................................................................. 32 3.6 e-MAIL CORRESPONDENCE WITH THE CoT .................................................................. 36 3.7 MUNICIPAL ACCOUNT PAYMENTS ............................................................................... 38 3.8 CUSTOMER RIGHTS ....................................................................................................... 40 3.9 QUALITATIVE RESEARCH ............................................................................................... 42 3.10 CONCLUSION ................................................................................................................. 44 3.11 CLOSURE ........................................................................................................................ 48

iii

LIST OF TABLES

Table Page

2.1 SAMPLE SIZE ....................................................................................................................... 6 3.1 SAMPLE POPULATION BY REGION AND CUSTOMER TYPE ............................................... 8 3.2 SAMPLE POPULATION BY REGION AND SURVEY TYPE .................................................... 9 3.3 NATURE OF INTERACTION BY REGION ........................................................................... 12 3.4 CUSTOMER CARE WALK-IN CENTRES/PAYPOINTS MOST RECENTLY VISITED BY BY REGION ....................................................................................................................... 15 3.5 AWARENESS OF OTHER CUSTOMER CARE WALK-IN CENTRES/PAYPOINTS BY REGION ............................................................................................................................. 16 3.6 CUSTOMER AWARENESS OF OTHER CUSTOMER CARE WALK-IN CENTRES/ PAYPOINTS IN- AND OUTSIDE SURVEY REGIONS ........................................................... 17 3.7 OTHER INTER-REGION CUSTOMER CARE WALK-IN CENTRES/PAYPOINTS USED BY REGION .............................................................................................................. 18 3.8 OTHER CUSTOMER CARE WALK-IN CENTRES/PAYPOINTS USED BY REGION ............... 19 3.9(a) AVERAGE SATISFACTION RATING SCORES FOR PAYPOINT CONSTRUCTS/ ATTRIBUTES BY REGION .................................................................................................. 22 3.9(b) AVERAGE SATISFACTION RATING SCORES FOR PAYPOINT CONSTRUCTS/ ATTRIBUTES BY CUSTOMER TYPE ................................................................................... 25 3.10 CUSTOMER SATISFACTION RATINGS WITH CoT’s HANDLING TELEPHONIC REQUESTS/COMPLAINTS ................................................................................................. 34 3.11(a) PAYMENT METHODS USED ............................................................................................. 39 3.11(b) PAYMENT METHODS PREFERRED ................................................................................... 39 3.12 PERCENTAGE OF CUSTOMERS IN RATING GROUPS REGARDING CUSTOMER RIGHTS .............................................................................................................................. 41

iv

LIST OF FIGURES

Figure Page

3.1 TYPE OF INTRACTIONS WITH CoT BY REGION ................................................................ 11 3.2 PROXIMITY OF CUSTOMER CARE WALK-IN CENTRES/PAYPOINTS ................................ 14 3.3 OVERALL CUSTOMER SATISFACTION RATINGS FOR PERSONAL INTERACTION BY REGION ........................................................................................................................ 29 3.4 MAGNITUDE OF CUSTOMER SATISFACTION FOR PERSONAL INTERACTION BY REGION ....................................................................................................................... 30 3.5 AWARENESS AND USAGE OF CoT TOLL-FREE NUMBER ................................................. 33 3.6 OVERALL CUSTOMER SATISFACTION RATINGS WITH CoT’S HANDLING OF TELEPHONE REQUESTS/COMPLAINTS ............................................................................ 35 3.7 SERVICE EXPERIENCE OF CUSTOMERS CORRESPONDING WITH CoT VIA e-MAIL ......... 37 3.8 OVERALL CUSTOMER SATISFACTION RATINGS WITH CoT IN HANDLING e-MAIL REQUESTS/COMPLAINTS .................................................................................... 37

v

LIST OF EXHIBITS

Exhibit Page

3.1 TOP AND BOTTOM SATISFACTION ITEMS BY REGION ................................................... 24 3.2 TOP AND BOTTOM SATISFACTION ITEMS BY CUSTOMER TYPE .................................... 27 3.3 TOP AND BOTTOM SATISFACTION ITEMS BY REGION AND CUSTOMER TYPE .............. 28 3.4 MAJOR REASONS FOR AVERAGE AND BELOW AVERAGE SERVICE EXPERIENCE ...................................................................................................................... 31 3.5 MAJOR REASONS FOR AVERAGE AND BELOW AVERAGE TELEPHONIC SERVICE EXPERIENCE ....................................................................................................... 35 3.6 AVERAGE CUSTOMER RATINGS REGARDING CUSTOMER RIGHTS ................................ 42

vi

EXECUTIVE SUMMARY

Background Following past trends in the private sector, heightened customer expectations of service quality

and standards have also emerged in the public sector, providing a sound rationale for the

Customer Relations Management Division of the City of Tshwane (CoT) to conduct a research

study on service quality and standards. In fact, the Customer Relations Management Division of

the CoT has taken the lead in conducting customer satisfaction studies since 2009.

After the local municipal elections in May 2011 the Metsweding District Municipality, Kungwini

Local Municipality and Nokeng Tsa Taemane Local Municipality merged with the City of

Tshwane. Previous customer satisfaction studies included only the pre-election demarcated

geographic areas within the CoT. The newly incorporated areas were added to the City of

Tshwane as Region 5 and Region 7 and resulted in changes in the regional borders and existing

wards. These expanded geographic boundaries and resulting changes created a need for

information on public service quality and standards within the newly established regions.

Consequently, the CoT Customer Relations Management Division commissioned the Bureau of

Market Research (BMR) at the University of South Africa (Unisa) to conduct a customer service

quality audit in regions 5 and 7. The aim of the study is to establish customers’ needs and

satisfaction ratings with regard to the standard and quality of services rendered at the different

CoT service interaction points (customer care walk in centre/paypoints ) in regions 5 and 7 and

to inform the planning of the intended new CoT customer satisfaction survey envisaged for

2013.

A service quality audit was conducted in the second quarter of 2012 among 359 customers

serviced across nine different customer care walk-in centres/paypoints within regions 5 and 7.

The research study included a primary survey among both households (90.5% of survey

population) and businesses (9.5% of survey population). These sample units were incorporated

into the research survey that incorporated a combination of computer-aided telephone (25.6%

of survey sample) and paypoint intercept (74.4% of survey sample) interviews to collect

vii

relevant customer data across regions 5 (45.7% of survey sample) and 7 (54.3% of survey

sample). The research methodology resulted in the majority of customers being interviewed

personally at customer care walk-in centres/paypoints (90.3%). However, the research model

designed for the study also ensured the inclusion of customers’ views on service quality and

standards experienced primarily during telephone (7.5% of survey population) and e-mail (2.2%

of survey population) communication with the CoT.

Research analysis When analysing the survey findings among those customers who interacted with the CoT

during the preceding 12 months, it is evident that almost half the customers who were

interviewed, interacted primarily with the CoT to pay municipal accounts (47.6%). Other forms

of interaction included information (36.8%) and service (13.6%) requests and lodging of

complaints (1.9%).

Personal interaction Turning the attention to those customers whose most recent interaction with a CoT paypoint

was in person (90.3% of surveyed population), it is clear that most customers (73.2%) are

located fairly close (less than 5km or 30 minutes’ walking time) to a regional customer care

walk-in centre/paypoint. Of those customers who visited any of the nine customer care walk-in

centres/paypoints in regions 5 and 7 personally, approximately half (53.1%) indicated that they

are also aware of other customer care walk-in centres/paypoints besides the one visited most

recently. Of those aware of other customer care walk-in centres/paypoints, 69.2% also

confirmed that they had used other customer care walk-in centres/paypoints besides the one

visited most recently. This finding not only displays fairly high levels of awareness of other

customer care walk-in centres/paypoints in- and outside the survey regions but also supports

the aim of the survey to capture a broad picture on service quality and standards of multiple

customer care walk-in/paypoint interactions.

viii

With the primary focus of the study on customer satisfaction, the survey findings revealed an

overall ‘average’ satisfaction with service quality attributes such as facilities, account payment

processing, trading hours, counter staff and resolution of queries/complaints. Figure A1 shows

the average satisfaction scores for each service attribute separately where ‘1’ = very dissatisfied

and ‘5’ = very satisfied. It should be noted that the average satisfaction scores relate only to

the most recent personal interactions with at least one of the nine CoT customer care walk-in

centres/paypoints located within regions 5 and 7.

FIGURE A1

AVERAGE SATISFACTION WITH QUALITY OF SERVICE DELIVERY AT CoT CUSTOMER CARE

WALK-IN CENTRES/PAYPOINTS

3.25

3.48

4.31

3.95

3.37

3.63

3.17

3.38

3.91

3.98

2.80

3.52

3.22

3.42

4.08

3.97

3.03

3.56

0 1 2 3 4 5

Facilities

Processing account payments

Trading hours and accessibility

Counter staff

Dealing with queries/complaints

Total

Very dissatisfied Very satisfied

Total Region 7 Region 5

ix

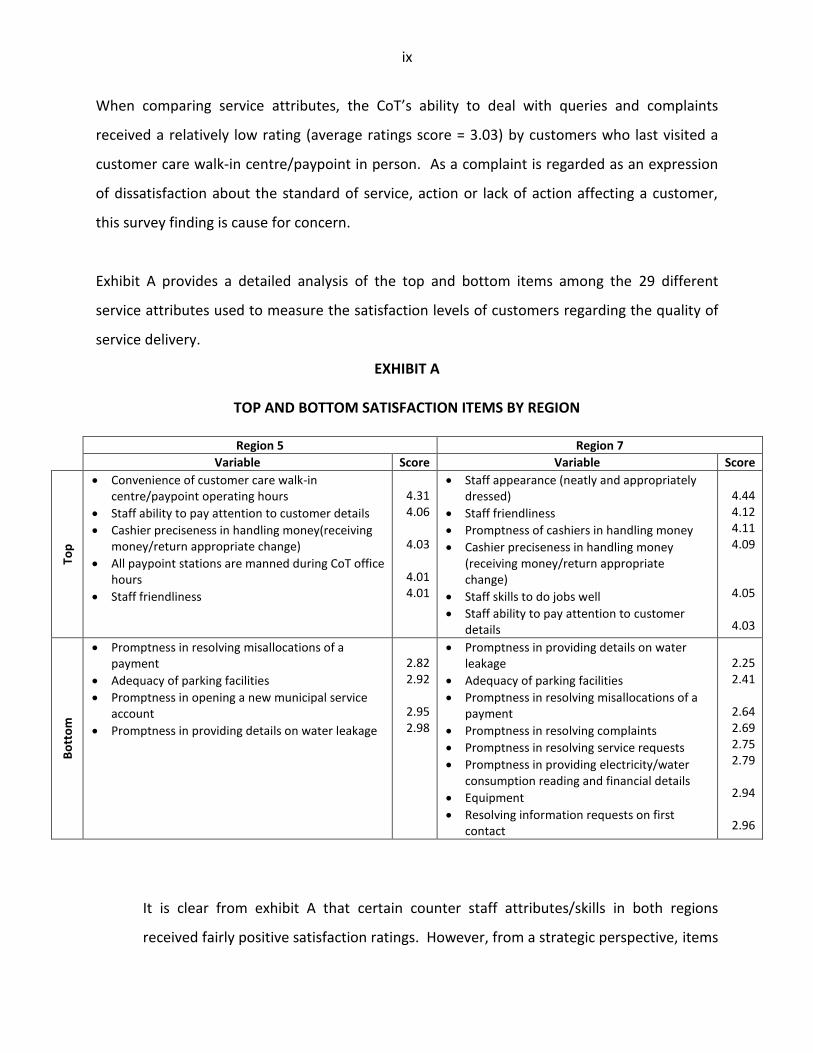

When comparing service attributes, the CoT’s ability to deal with queries and complaints

received a relatively low rating (average ratings score = 3.03) by customers who last visited a

customer care walk-in centre/paypoint in person. As a complaint is regarded as an expression

of dissatisfaction about the standard of service, action or lack of action affecting a customer,

this survey finding is cause for concern.

Exhibit A provides a detailed analysis of the top and bottom items among the 29 different

service attributes used to measure the satisfaction levels of customers regarding the quality of

service delivery.

EXHIBIT A

TOP AND BOTTOM SATISFACTION ITEMS BY REGION

Region 5 Region 7

Variable Score Variable Score

Top

Convenience of customer care walk-in centre/paypoint operating hours

Staff ability to pay attention to customer details

Cashier preciseness in handling money(receiving money/return appropriate change)

All paypoint stations are manned during CoT office hours

Staff friendliness

4.31 4.06

4.03

4.01 4.01

Staff appearance (neatly and appropriately dressed)

Staff friendliness

Promptness of cashiers in handling money

Cashier preciseness in handling money (receiving money/return appropriate change)

Staff skills to do jobs well

Staff ability to pay attention to customer details

4.44 4.12 4.11 4.09

4.05

4.03

Bo

tto

m

Promptness in resolving misallocations of a payment

Adequacy of parking facilities

Promptness in opening a new municipal service account

Promptness in providing details on water leakage

2.82 2.92

2.95 2.98

Promptness in providing details on water leakage

Adequacy of parking facilities

Promptness in resolving misallocations of a payment

Promptness in resolving complaints

Promptness in resolving service requests

Promptness in providing electricity/water consumption reading and financial details

Equipment

Resolving information requests on first contact

2.25 2.41

2.64 2.69 2.75 2.79

2.94

2.96

It is clear from exhibit A that certain counter staff attributes/skills in both regions

received fairly positive satisfaction ratings. However, from a strategic perspective, items

x

with low rating scores require priority attention. Service areas such as promptness in

resolving misallocations of payments, adequacy of parking facilities and promptness in

providing details on water leakages, should receive prompt attention to improve the

quality of future service delivery at CoT customer care walk-in centres/paypoints in both

regions 5 and 7.

The overall satisfaction scores for customers who last interacted with the CoT in person

at a paypoint, are shown in figure A2 by region.

FIGURE A2

OVERALL CUSTOMER SATISFACTION RATINGS

Although the average scores displayed in figure B generally seem satisfactory, a closer analysis

of the satisfaction category frequency distributions show some level of uncertainty and

dissatisfaction among customers in both regions 5 and 7. In this regard, 21.3% of customers

seem dissatisfied with the quality of service delivery at customer care walk-in

centres/paypoints while 17.9% perceive service delivery as ‘average’. A regional analysis shows

11.7 9.6 10.5

8.8

12.3 10.8

13.9

20.9

17.9

41.6

37.4 39.2

24.1

19.8 21.6

0

25

50

Region 5 Region 7 Total

%

Very dissatisfied Dissatisfied Average Satisfied Very satisfied

Average score = 3.45 Average score = 3.58 Average score = 3.51

xi

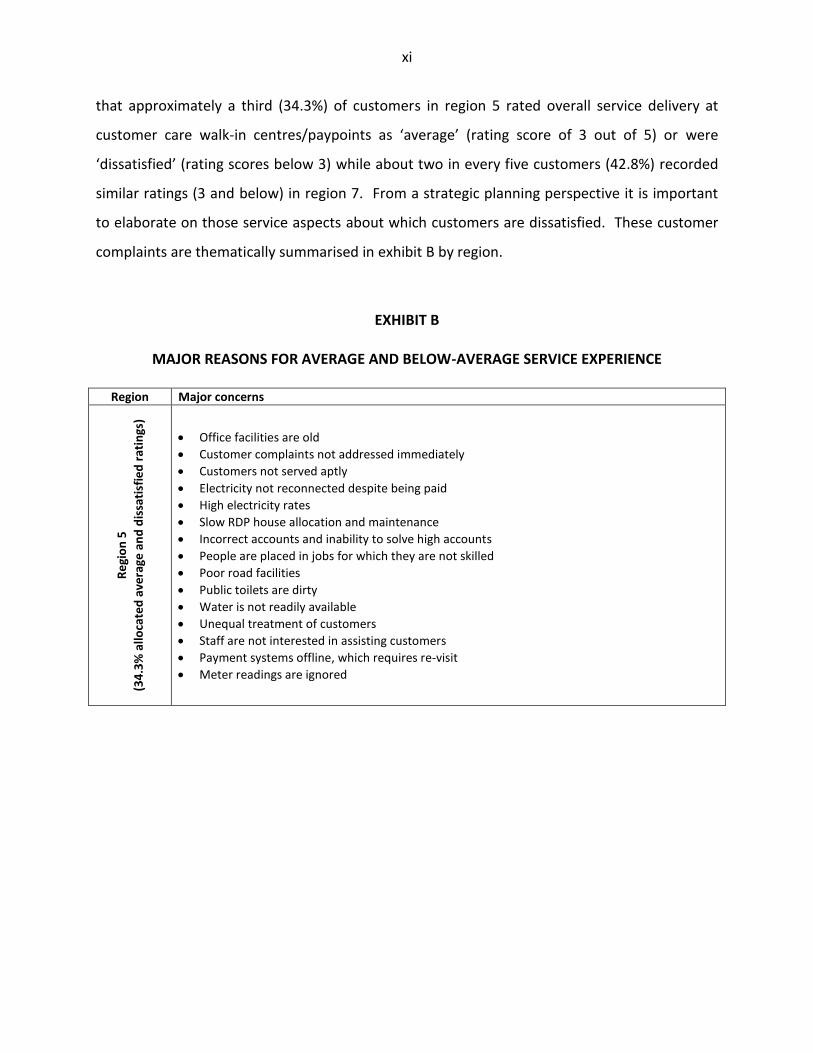

that approximately a third (34.3%) of customers in region 5 rated overall service delivery at

customer care walk-in centres/paypoints as ‘average’ (rating score of 3 out of 5) or were

‘dissatisfied’ (rating scores below 3) while about two in every five customers (42.8%) recorded

similar ratings (3 and below) in region 7. From a strategic planning perspective it is important

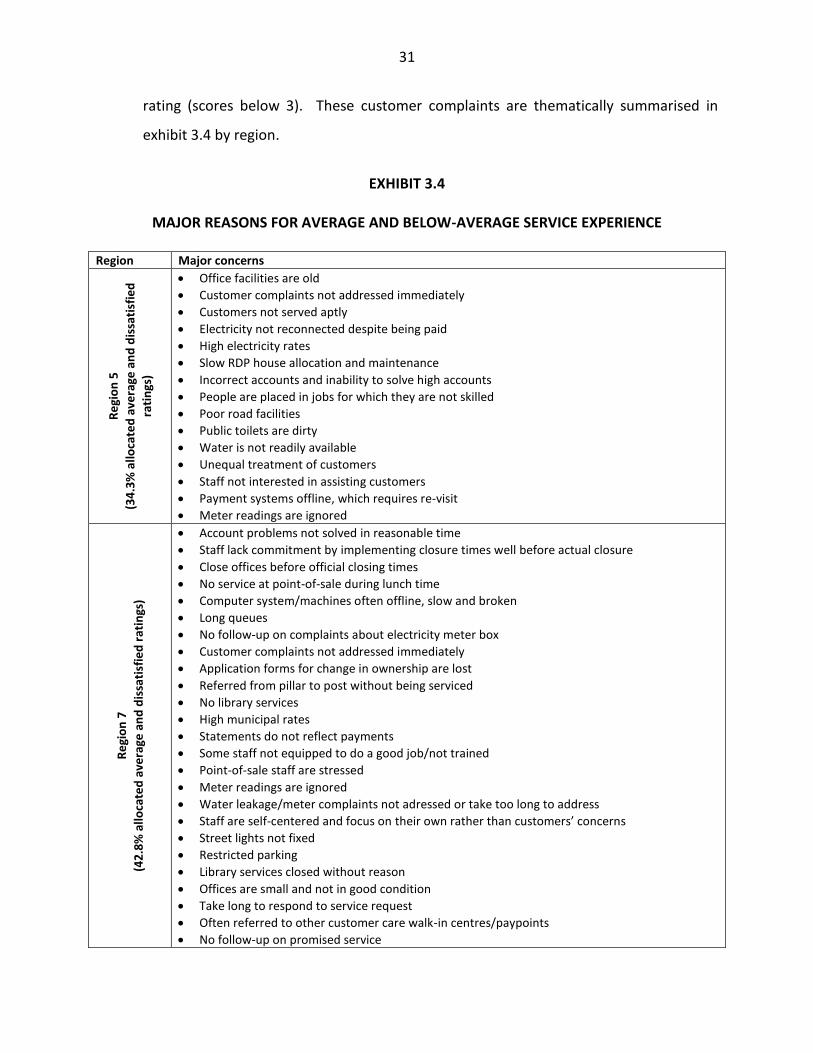

to elaborate on those service aspects about which customers are dissatisfied. These customer

complaints are thematically summarised in exhibit B by region.

EXHIBIT B

MAJOR REASONS FOR AVERAGE AND BELOW-AVERAGE SERVICE EXPERIENCE

Region Major concerns

Re

gio

n 5

(34

.3%

allo

cate

d a

vera

ge a

nd

dis

sati

sfie

d r

atin

gs)

Office facilities are old

Customer complaints not addressed immediately

Customers not served aptly

Electricity not reconnected despite being paid

High electricity rates

Slow RDP house allocation and maintenance

Incorrect accounts and inability to solve high accounts

People are placed in jobs for which they are not skilled

Poor road facilities

Public toilets are dirty

Water is not readily available

Unequal treatment of customers

Staff are not interested in assisting customers

Payment systems offline, which requires re-visit

Meter readings are ignored

xii

Re

gio

n 7

(42

.8%

allo

cate

d a

vera

ge a

nd

dis

sati

sfie

d r

atin

gs)

Account problems not solved in reasonable time

Staff lack commitment by implementing closure times well before actual closure

Close offices before official closing times

No service at point-of-sale during lunch time

Computer system/machines often offline, slow and broken

Long queues

No follow-up on complaints about electricity meter box

Customer complaints not addressed immediately

Application forms for change in ownership are lost

Referred from pillar to post without being serviced

No library services

High municipal rates

Statements do not reflect payments

Some staff not equipped to do a good job/not trained

Point-of-sale staff are stressed

Meter readings are ignored

Water leakage/meter complaints not addressed or take too long to address

Staff are self-centered and focus on their own rather than customers’ concerns

Street lights not fixed

Restricted parking

Library services closed without reason

Offices are small and not in good condition

Take long to respond to service request

Often referred to other customer care walk-in centres/paypoints

No follow-up on promised service

When comparing the experience of customers who last interacted with the CoT personally with

those who last interacted with the CoT via telephone or e-mail, higher satisfaction is evident

among customers who interacted with the CoT personally. This finding is displayed in figure A3.

xiii

FIGURE A3

COMPARATIVE CUSTOMER SATISFACTION RATINGS BY FORM OF INTERACTION

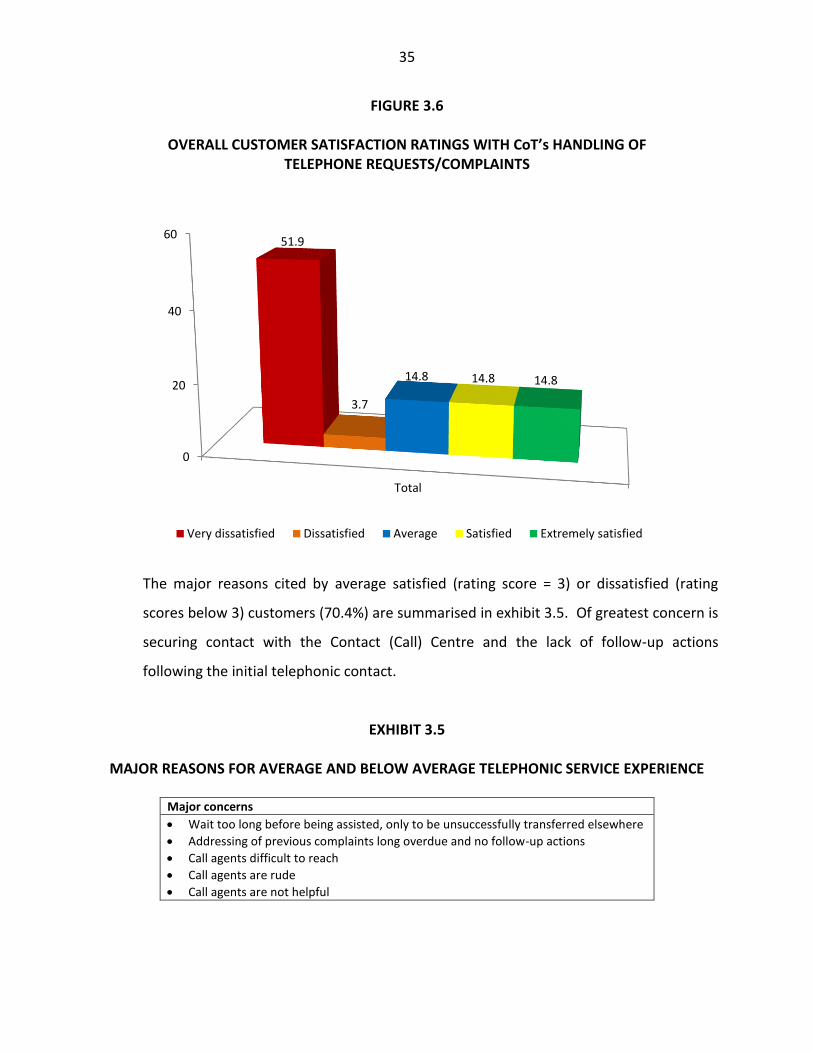

Telephonic interaction Almost a third (29.3%) of the computer-aided telephone interview (CATI) survey population last

interacted with the CoT via the Contact/Call Centre (012 358 9999). The experience of these

customers during their telephonic interaction are summarised in figure A4.

1

2

3

4

5

Personal interactionTelephone interaction

e-Mail interaction

3.51

2.37 2.50

Ver

y d

issa

tisf

ied

V

ery

sati

sfie

d

xiv

FIGURE A4

CUSTOMER SATISFACTION RATINGS FOR TELEPHONIC INTERACTION

A closer analysis of the research findings shows that 55.6% of customers who interacted with

the CoT telephonically were dissatisfied with the service experienced. The major reasons

advanced for dissatisfaction include:

wait too long before being assisted

promptness in resolving service requests

efficiency of requests/complaints follow-up

promptness in resolving complaints

Other major concerns raised by customers included the following:

addressing of previous complaints long overdue and no follow-up actions

call agents difficult to reach

call agents are rude

call agents are not helpful

1

2

3

4

5

Call Centre agentsDealing with

queries/complaintsTotal

2.58

2.10 2.37

Extr

emel

y d

issa

tisf

ied

Extr

emel

y sa

tisf

ied

xv

e-Mail interaction Almost one in every 10 (8.7%) of the CATI respondents last interacted with the CoT via e-mail.

The experiences of these customers through e-mail interaction are summarised in figure A5. It

is clear from the analysis that approximately 62.5% of customers were dissatisfied with the

CoT’s handling of e-mail requests/enquiries. When probed regarding the major reasons for

dissatisfaction, participating customers indicated that the CoT does not respond to e-mails nor

provide feedback on e-mail enquiries.

FIGURE A5

PERCENTAGE OF CUSTOMERS IN SATISFACTION RATING CATEGORIES

FOR CoT’s HANDLING OF e-MAIL REQUESTS/COMPLAINTS

Municipal account payment Besides measuring customer satisfaction, the survey also explored the current and preferred

methods of municipal account payments of participating customers. Although most customers

currently pay accounts at the cashier desk at customer care walk-in centres/paypoints (72.1%),

customers show keen interest in paying accounts at external paypoints and banks or

electronically via Internet banking in future.

0

25

50

Total

37.5

25.0 25.0

12.5

%

Very dissatisfied Dissatisfied Satisfied Very satisfied

Average score = 2.50

xvi

Customer rights The research model was also designed to measure customer views regarding the eight Batho

Pele principles aspired to by the CoT. These survey findings are presented in table A1. The

analysis shows that participating customers regard openness and transparency and value for

money as the most neglected principles. In turn, courtesy and access were identified as the

two best implemented principles.

TABLE A1

CUSTOMER RATINGS REGARDING CUSTOMER RIGHTS

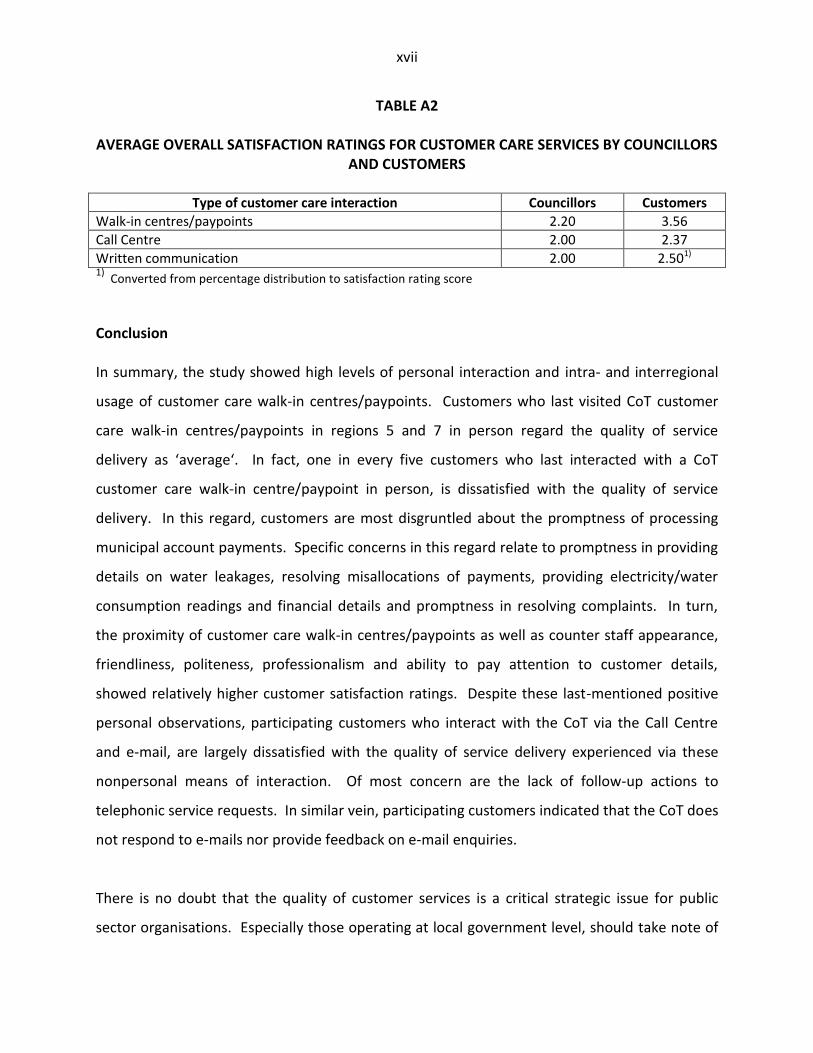

Councillor perspective Table A2 shows that the perceived levels of customer care satisfaction of councillors of regions

5 and 7, that ranged from 2.2 (out of 5) for walk-in centres to 2.0 for Call Centre and written

communication, are slightly lower than those reported by customers themselves.

Statements

Total

Disagree Neither agree

Agree

The Tshwane Municipality makes attempts to consult citizens about the services they need (consultation).

42.3 21.4 36.2

Citizens are told what level and quality of public services they can expect to receive (service standards)

40.9 21.7 37.3

All citizens have equal access to the services to which they are entitled (access) 27.3 26.7 46.0

Citizens are treated with courtesy and consideration (courtesy) 27.6 25.6 46.8

Citizens are given full, accurate information about the public services they are entitled to receive (information)

40.1 23.4 36.5

Citizens are told how services/departments are run, how much they cost and who is in charge (openness and transparency)

44.6 23.7 31.8

It is easy for citizens to lodge a complaint/enquiry (redress) 35.4 23.1 41.5

Citizens who pay for services get value for their money/CoT spends wisely (value for money) 40.9 25.6 33.4

xvii

TABLE A2

AVERAGE OVERALL SATISFACTION RATINGS FOR CUSTOMER CARE SERVICES BY COUNCILLORS AND CUSTOMERS

Type of customer care interaction Councillors Customers

Walk-in centres/paypoints 2.20 3.56

Call Centre 2.00 2.37

Written communication 2.00 2.501)

1) Converted from percentage distribution to satisfaction rating score

Conclusion In summary, the study showed high levels of personal interaction and intra- and interregional

usage of customer care walk-in centres/paypoints. Customers who last visited CoT customer

care walk-in centres/paypoints in regions 5 and 7 in person regard the quality of service

delivery as ‘average‘. In fact, one in every five customers who last interacted with a CoT

customer care walk-in centre/paypoint in person, is dissatisfied with the quality of service

delivery. In this regard, customers are most disgruntled about the promptness of processing

municipal account payments. Specific concerns in this regard relate to promptness in providing

details on water leakages, resolving misallocations of payments, providing electricity/water

consumption readings and financial details and promptness in resolving complaints. In turn,

the proximity of customer care walk-in centres/paypoints as well as counter staff appearance,

friendliness, politeness, professionalism and ability to pay attention to customer details,

showed relatively higher customer satisfaction ratings. Despite these last-mentioned positive

personal observations, participating customers who interact with the CoT via the Call Centre

and e-mail, are largely dissatisfied with the quality of service delivery experienced via these

nonpersonal means of interaction. Of most concern are the lack of follow-up actions to

telephonic service requests. In similar vein, participating customers indicated that the CoT does

not respond to e-mails nor provide feedback on e-mail enquiries.

There is no doubt that the quality of customer services is a critical strategic issue for public

sector organisations. Especially those operating at local government level, should take note of

xviii

and act on pressure to improve customer service on a continuous basis. Some pressure in the

public sector arises internally from a genuine desire by managers to improve the quality of

services while further pressure is imposed through initiatives like the White Paper on

Transforming Public Service Delivery or the so-called ‘Batho Pele’ White Paper that requires

from government departments to improve service delivery in terms of the eight ‘Batho Pele’

service delivery principles. In aspiring to these principles and in demonstrating its resolve to

improve service quality, the Customer Relations Management Division of the City of Tshwane

(CoT) initiated a customer satisfaction survey that presented customers with an opportunity to

provide their perceptions of service delivery and to express their expectations regarding service

quality. The fact that customers typically assess service quality by comparing the service they

actually experience with the service they expect, makes the outcome of this survey of strategic

importance for the CoT. The core survey findings emerging from the 2012 study in regions 5

and 7, display average to below-average satisfaction relative to the type of customer

interaction. The survey revealed key strategic focus areas that the CoT needs to address to

improve future customer satisfaction. It is recommended that the CoT, in regions 5 and 7, focus

primarily on those service items that recorded below-average satisfaction ratings among

customers who participated in the 2012 study. However, the success of any strategies will

depend on management’s commitment as well as the degree to which management proactively

resolves customer complaints through the involvement of the customer. It is therefore

recommended that customers should be consulted and involved when determining service

quality standards and measurement.

1

CHAPTER 1

INTRODUCTION AND STUDY OBJECTIVE 1.1 INTRODUCTION

The incorporation of the Metsweding District Municipality, the Nokeng Tsa Taemane

Local Municipality and the Kungwini Local Municipality into the City of Tshwane (CoT)

created several challenges with regard to the merger of the customer care services

(CCS) functions of the various institutions. Some of these challenges relate to different

CCS systems/procedures followed in the various municipalities prior to the merger,

differences in tariff/cost structures for municipal services, variations in human resources

capacities (levels of staffing) and the strong rural orientation of the newly-incorporated

areas compared to the metropolitan structures of the CoT. The latter may also affect

the capacity of households and businesses to afford the increased tariff structures of

municipal services.

Satisfaction with CCS in the pre-merger five regions of the CoT was measured in an

extensive customer satisfaction survey in January/February 2011. The 2011 study focus

was on satisfaction with services provided by the customer call centre, walk-in centres

and written communication with the CoT. The study in the newly-incorporated regions

(new regions 5 and 7) would not only put the two new regions on par with the previous

CoT regions but would also be valuable in establishing empirically what the needs,

expectations and satisfaction are with regard to customer care provision and service

delivery. Furthermore, the value of such research is important especially in an

environment where different systems and expectations have to be accommodated.

2

1.2 OBJECTIVE OF THE STUDY

In an attempt to enhance service standards and facilitate the merger of customer care

services towards an integrated customer care approach for the newly-structured CoT,

this research study was intended to conduct an environmental scan of customer care

provisioning within regions 5 and 7 of the CoT. More specifically, the aim of the study

was to establish customers’ needs and satisfaction ratings with regard to the standard

of services rendered at the different service points in region 5 and 7. Focus was placed

on all three modes of customer interaction with the CoT, namely personal visits to

customer care walk-in centres/paypoints, telephone interaction with the CoT call centre

and written interaction via post, facsimile or e-mail.

1.3 OUTLINE OF THE REPORT

The executive summary at the beginning of the report highlights the core issues

contained in the report. The first chapter provides background to the study, defines its

objectives and outlines the structure of the report. A detailed description of the survey

methodology is provided in chapter 2. Chapter 3 deals with the findings of the

quantitative survey. Chapter 4 contains the result of the in-depth interviews while

chapter 5 provides a summary and some recommendations based on the customer

service environmental audit among CoT customers in regions 5 and 7.

3

CHAPTER 2

SURVEY METHODOLOGY 2.1 INTRODUCTION

This chapter elaborates on the research methodology applied during the execution of

the customer service environmental audit in regions 5 and 7. The discussion provides a

basis for the scientific foundation of the study and hence the quality, validity and

reliability of the survey findings.

2.2 RESEARCH SCOPE

A multidimensional research method, applying both quantitative and qualitative

methods, was used in conducting the research. These methodologies target different

target groups that are explained in more detail below. Prior to this discussion, it ought

to be mentioned that the design of the research model for the study in CoT regions 5

and 7 was preceded by extensive exploratory research. These activities included the

following:

Discussions with representatives of the former municipalities and the CoT with

regard to the vision, mission and roles of customer relations management.

Secondary research on the service delivery profile and responsibilities of the

customer service regime of the CoT.

Analysis of the customer care service satisfaction measurement of the CoT in

2009 and 2011.

Proper environmental scan of the situation in regions 5 and 7 to ensure an

appropriate approach towards information gathering.

4

2.3 QUANTITATIVE RESEARCH

The research methodology applied to collect primary data from CoT customers, both

households and businesses, residing in CoT regions 5 and 7 is explained below.

2.3.1 Survey population

All the households residing and businesses operating in CoT regions 5 and 7 qualified for

inclusion in the study. However, the sample population was reduced to only those

households/businesses that had interacted with the customer care services of the CoT

during the 12 months preceding the survey. This interaction could have been an in-

person visit to a walk-in centre/paypoint, telephonic contact with the customer care

centre or a written (post, facsimile or e-mail) communication with the CoT. The

rationale for this approach is derived from the fact that satisfaction ratings of a service

are only realistic if supplied by those exposed to a specific service. Respondents in this

study were requested to rate their satisfaction only with their specific mode of

interaction with the CoT (either in-person, telephonic or written).

2.3.2 Sampling plan

The sampling plan was designed to accommodate all modes of interaction with the

customer care services of the CoT. It was also aimed at supporting both telephone and

personal face-to-face interviews. Intercept face-to-face interviews were conducted with

customers at customer care walk-in centres/paypoints after a customer had been

served. All the customer care walk-in centres/paypoints in regions 5 and 7 were

included in the study. These are:

Region 5

Rayton customer care centre

Cullinan Jewel Shop paypoint

Roodeplaat paypoint

Refilwe paypoint

5

Region 7

Bronkhorstspruit customer care centre

Zithobeni paypoint

Rethabiseng paypoint

Ekangala paypoint

Dark City paypoint

These interviews ensured that customers without access to Telkom telephones were

included in the sample.

The intercept interviews at walk-in centres were supplemented with CATI (Computer-

Aided Telephone) interviews. These interviews were aimed at capturing the level of

satisfaction of customers more inclined to interact telephonically and through

post/facsimile/e-mail with the CoT. The following subpopulations were identified for

this purpose:

Households in Bronkhorstspruit

Households in Cullinan/Rayton

Businesses in regions 5 and 7

The Bronkhorstspruit and Cullinan portions of the Pretoria 2011/2012 telephone

directory were used to randomly select households for interviewing. The business

information provided by the CoT was used to randomly select businesses in

Bronkhorstspruit, Cullinan and Rayton for interviews.

2.3.3 Sample size

Table 2.1 shows the distribution of the 360 interviews. In total, 30 interviews were

conducted in each of the selected areas/customer care centres. This resulted in a total

of 270 intercept face-to-face interviews and 90 telephone interviews.

6

TABLE 2.1

SAMPLE SIZE Sample Sample size

(a) Intercept survey (i) Region 5

Rayton customer care centre

Cullinan Jewel Centre paypoint

Roodeplaat, Kameeldrift East paypoint

Refilwe paypoint

270

30 30 30 30

(ii) Region 7

Bronkhorstspruit customer care centre

Zithobeni paypoint

Rethabiseng paypoint

Ekangala paypoint

Dark City paypoint

30 30 30 30 30

(b) CATI interviews

Bronkhorstspruit

Cullinan/Rayton

Businesses regions 5 and 7

90 30 30 30

Total 360

2.3.4 Research instrument

Structured survey questionnaires were designed to measure satisfaction levels and

reasons for dissatisfaction regarding the main CCS delivery aspects of each of the main

customer communication modes (in-person, telephone and written). The design and

structure of the questionnaires used in this study were shaped and guided mainly by the

content of questionnaires used in the previous CoT studies. The rating scale in these

questionnaires used a 5-point Likert scale compared to the 10-point numerical scale

used in previous questionnaires.

Prior to final approval, the questionnaire was circulated among relevant staff in the CoT

for scrutiny, inputs and recommendations. Finally, the questionnaire was transformed

into a Web-based format for conducting the CATI interviews.

2.3.5 Fieldwork

Fieldworkers for the intercept survey were recruited by the CoT while experienced BMR

CATI interviews concluded the CATI interviews. The fieldworkers were trained by the

BMR.

7

The interviews were conducted during the period 26 April 2012 to 11 May 2012.

Although no major problems were experienced during the fieldwork process, it should

be noted that the initial training session and some interviews had to be rescheduled due

to unrest experienced at Ekangala in particular.

2.3.6 Data coding and capturing

The CATI survey approach allowed for electronic data capturing. Face-to-face

questionnaires were coded prior to data capturing. Upon completion of data capturing,

all data were merged into a single dataset. Final electronic editing and verification

checks were conducted prior to storing the data for analysis purposes. In addition,

during the editing process, all open-ended responses (dissatisfaction with service

delivery) were thematically coded.

2.4 QUALITATIVE PHASE

The findings of the survey were summarised in a discussion guide. This guide was

intended to be used for a focus group discussion with ward councillors of regions 5 and

7. Due to logistical and other reasons, the focus group discussion was substituted with

individual in-depth interviews with the councillors. A short questionnaire reflecting on

the councillors’ perception of service delivery levels at customer centres/paypoints, the

Call Centre and communication through written means, was also completed by

councillors.

2.5 CONCLUDING REMARKS

This chapter provides an overview of the research methodology for the customer

service environmental audit among CoT customers of regions 5 and 7 conducted among

360 customers. The outcomes of the research findings are presented in chapter 3.

8

CHAPTER 3

RESEARCH ANALYSIS

3.1 INTRODUCTION

This chapter presents the findings emerging from the 2012 CoT service quality audit

survey among 359 customers (households and businesses). To better contextualise the

findings emerging from the intercept and computer-aided telephonic surveys, the

chapter commences with an overview of the survey participants across the sampled

regions. This overview is followed by a presentation of the outcome of the research

findings. Finally, the chapter concludes with a summary and some recommendations

based on the research findings.

3.2 RESPONDENT PROFILE This section presents an overview of the survey population according to selected

research constructs. Firstly, table 3.1 presents an overview of the survey participants

according to region and customer type.

TABLE 3.1

SAMPLE POPULATION BY REGION AND CUSTOMER TYPE

Region

Customer type

Household Business Total

n % n % n %

Region 5 148 90.2 16 9.8 164 100.0

Region 7 177 90.8 18 9.2 195 100.0

Total 325 90.5 34 9.5 359 100.0

Table 3.1 shows that the sample population comprised 325 (or 90.5%) households and

34 (or 9.4%) businesses. In total, 359 customers were interviewed. Of these,

approximately a quarter (25.6%) were interviewed telephonically (computer-aided

telephone interviews - CATI) while 267 (or 74.4%) of the customers were interviewed at

9

CoT customer care walk-in centres/pay points using intercept interviews. Of the total

sample, 45.7% of all participating customers were interviewed in region 5 while 54.3%

were interviewed in region 7. The distribution of the total sample by region and survey

type is displayed in more detail in table 3.2.

TABLE 3.2

SAMPLE POPULATION BY REGION AND SURVEY TYPE

Region

Survey type

CATI survey Intercept survey Total

n % n % n %

Region 5 46 28.0 118 72.0 164 100.0

Region 7 46 23.6 149 76.4 195 100.0

Total 92 25.6 267 74.4 359 100.0

Table 3.2 shows a fairly equal distribution of the regional sample population by survey

type. Whereas approximately a quarter of the sample was interviewed via telephone

interviews, 74.4% of customers were interviewed in person at the actual municipality

service point (customer care walk-in centres/paypoints).

In profiling the households and businesses the survey findings also revealed the

following:

Approximately a third (32.9%) of the participating households speak Sesotho sa

Leboa. Almost half the Sesotho-speaking households reside in region 5 (49.3% of all

participating Sesotho speaking households). Furthermore, approximately a quarter

(23.7%) of participating households speak IsiZulu, of which just more than a third

reside in region 7 (37.3% of all IsiZulu speaking participating households). More

than 10% of the participating households speak IsiNdebele (13.8%) and Afrikaans

(10.8%). Of the participating households in region 7, approximately one in every

five (21.5%) speak IsiNdebele. Other languages spoken by participating households

included English (1.8%), siSwati (2.2%), isiXhosa (0.9%), Xitsonga (2.5%), Sesotho

(7.1%), Setswana (2.8%) and Tshivenda (1.5%).

10

Approximately seven in every 10 participating households (76.6%) reside in formal

houses while 7.7% reside in informal dwellings. A higher proportion of participating

households who reside in formal houses (81.4%) were included from region 7. In

turn, more participating households who reside in informal dwellings in region 5

(10.8%) were included in the sample when compared with region 7 (5.1%).

Only 12.6% of the participating households live in a security complex.

Approximately a third (35.3%) of the participating businesses are located within

suburban areas, while 29.4% and 5.9% are located in formal townships and informal

settlement areas respectively.

Approximately half (52.9%) the participating businesses are classified as small

enterprises, while 26.5% and 20.6% were medium and large businesses

respectively.

The bulk of participating businesses were wholesalers/retailers (44.2%) and

businesses who operate within the financial insurance, real estate and business

services sectors (44.1%). Other participating businesses operated in the mining and

quarrying (8.8%), manufacturing (2.9%) and community, social and personal

services (2.9%).

3.3 CUSTOMER INTERACTION

This section of the report deals with the type of customer interaction of the 359

customers participating in the survey. Figure 3.1 displays the type of customer

interaction with the CoT during the preceding 12 months. It is important to note that

the table reflects customers’ most recent type of interaction with the CoT. As the bulk

of the interviews occurred at the actual municipal service customer care walk-in

centres/paypoints, most of the recent interactions with the CoT were in person.

11

FIGURE 3.1

TYPE OF INTERACTIONS WITH CoT BY REGION

It is clear from figure 3.1 that most respondents visited a CoT customer care walk-in

centre/paypoint personally during the preceding 12 months. Although measured, no

customers had any postal or facsimile contact with the CoT during the preceding 12

months. Of the total participating respondents, only 7.5% and 2.2% corresponded with

the CoT via the Contact (Call) Centre or e-mail respectively. The relatively high

proportion of walk-in centre respondents relative to those who interacted

telephonically or via e-mail resulted from the sampling methodology (intercept

interviews at walk-in centres represented 74.4% of the total sample population).

It is also interesting to note that the following interaction with the CoT was recorded

from the CATI interviews (ie with households and businesses with access to landline

telephone facilities):

Personal visit to a customer care walk-in centre/paypoint: 62.0%

Telephone contact with the Contact (Call) Centre: 29.3%

Correspondence via e-mail: 8.7%

83.5

12.2

4.3

95.9

3.6

0.5

90.3

7.5

2.2

0.0 20.0 40.0 60.0 80.0 100.0 120.0

Personally visited a CoT regional customer carewalk-in centre/paypoint

Corresponded with the CoT via telephone -Contact (Call) Centre

Corresponded with the CoT via e-mail

Total Region 7 Region 5

12

It was also evident from the CATI interviews that just more than half (57.6%) the

successful telephonic contacts confirmed interaction with the CoT during the preceding

12 months. A more confined analysis of the CATI interviews shows a considerably

higher level of personal contact by households compared to businesses. Businesses are

more inclined to make contact with the CoT via telephone or e-mail as is evident from

the following interaction pattern that emerged from the CATI survey:

Households Business

Personal contact 76.6% 34.4%

Telephone contact 18.3% 50.0%

e-Mail contact 5.0% 15.6%

As mentioned, it is important to note that the data displayed in figure 3.1 reflect only

the most recent interaction of the surveyed customers. The nature of the most recent

interaction with the CoT, irrespective of the mode of interaction, is displayed in table 3.3

by region.

TABLE 3.3

NATURE OF INTERACTION BY REGION

Nature of interaction Region 5 Region 7 Total

n % n % n %

Information request 63 38.4% 69 35.4% 132 36.8%

Service request 34 20.7% 15 7.7% 49 13.6%

Lodge a complaint 2 1.2% 5 2.6% 7 1.9%

Pay municipal account 65 39.6% 106 54.4% 171 47.6%

Total 164 100.0% 195 100.0% 359 100.0%

Table 3.2 shows that almost half the participating customers, who interacted with the

CoT, paid their municipal accounts during their most recent interaction. Approximately

a third of customers sought information during their most recent interaction. When

compared across region, it is clear that more customers in region 5 made service

requests. In turn, a much higher proportion of customers in region 7 paid their

13

municipal accounts during their last encounter with the CoT. The nature of customers’

most recent interaction, is best summarised as follows:

Region 5

Information requests: account enquiries/problems; general billing information;

request (duplicate) statements; explanation of bill; information about

environmental management; personal information (ie proof of residence); RDP

housing allocation and rental accommodation; electricity/water tariffs; prepaid

meters and electricity coupons; title deeds; licensing; sports facilities.

Service requests: power failures/reconnections and water/electricity cut-offs;

licensing; water leakage; faulty meters; meter reading problems; street lights; long

grass; road surface; renewal of proof of residence.

Lodge complaints: street lights out of order and not repaired; inconsistency of

sending of electricity/water bills.

Region 7

Information requests: account enquiries/problems; general billing information;

request statements; explanation of bill; information about environmental

management; personal information (ie proof of residence, updating personal/stand

details); RDP housing allocation and rental accommodation; change of ownership of

stand; property tax; indigent enquiry; electricity/water tariffs; title deeds; vehicle

licensing; social grants; sports facilities; employment opportunities; libraries.

Service requests: Water/electricity cut-offs; water leakage; faulty meters; pre-paid

electricity meter.

Lodge complaints: Power cuts; street lights out of order and not repaired; pre-paid

electricity meter.

It should be noted that the summary above represents a thematic analysis of the open-

ended responses of customers’ most recent interaction with the CoT, irrespective of the

mode of interaction (personal, telephonic or e-mail).

14

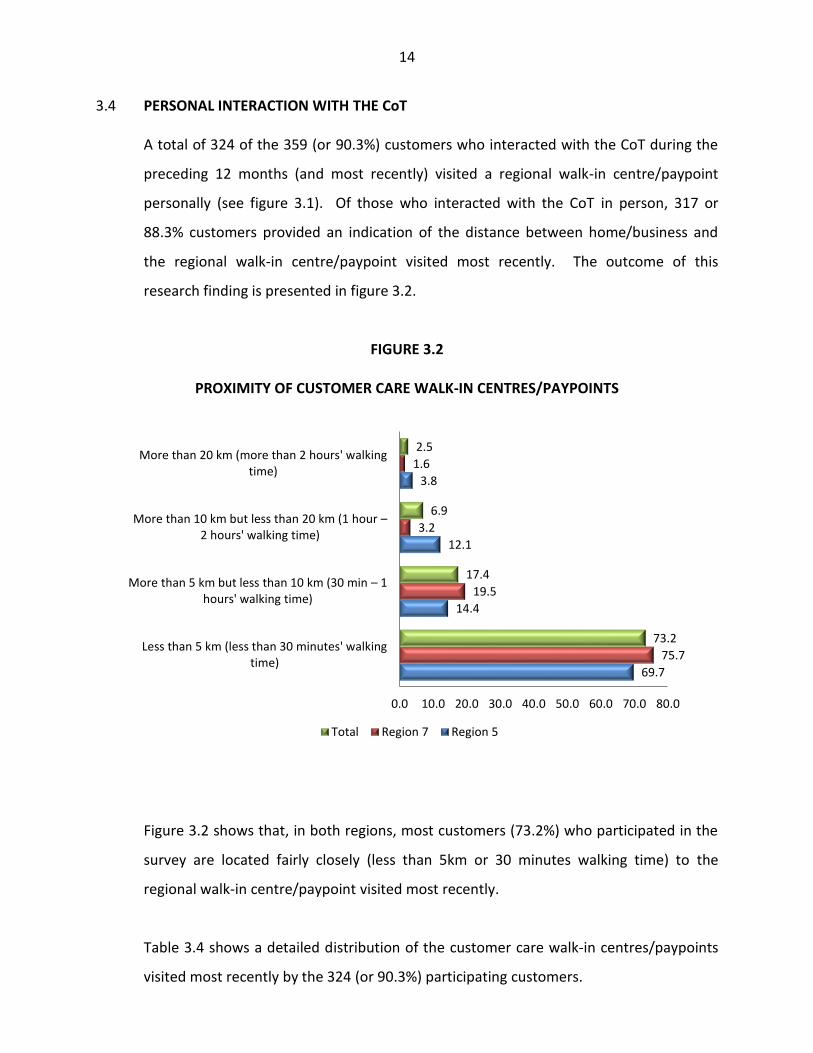

3.4 PERSONAL INTERACTION WITH THE CoT

A total of 324 of the 359 (or 90.3%) customers who interacted with the CoT during the

preceding 12 months (and most recently) visited a regional walk-in centre/paypoint

personally (see figure 3.1). Of those who interacted with the CoT in person, 317 or

88.3% customers provided an indication of the distance between home/business and

the regional walk-in centre/paypoint visited most recently. The outcome of this

research finding is presented in figure 3.2.

FIGURE 3.2

PROXIMITY OF CUSTOMER CARE WALK-IN CENTRES/PAYPOINTS

Figure 3.2 shows that, in both regions, most customers (73.2%) who participated in the

survey are located fairly closely (less than 5km or 30 minutes walking time) to the

regional walk-in centre/paypoint visited most recently.

Table 3.4 shows a detailed distribution of the customer care walk-in centres/paypoints

visited most recently by the 324 (or 90.3%) participating customers.

69.7

14.4

12.1

3.8

75.7

19.5

3.2

1.6

73.2

17.4

6.9

2.5

0.0 10.0 20.0 30.0 40.0 50.0 60.0 70.0 80.0

Less than 5 km (less than 30 minutes' walkingtime)

More than 5 km but less than 10 km (30 min – 1 hours' walking time)

More than 10 km but less than 20 km (1 hour – 2 hours' walking time)

More than 20 km (more than 2 hours' walkingtime)

Total Region 7 Region 5

15

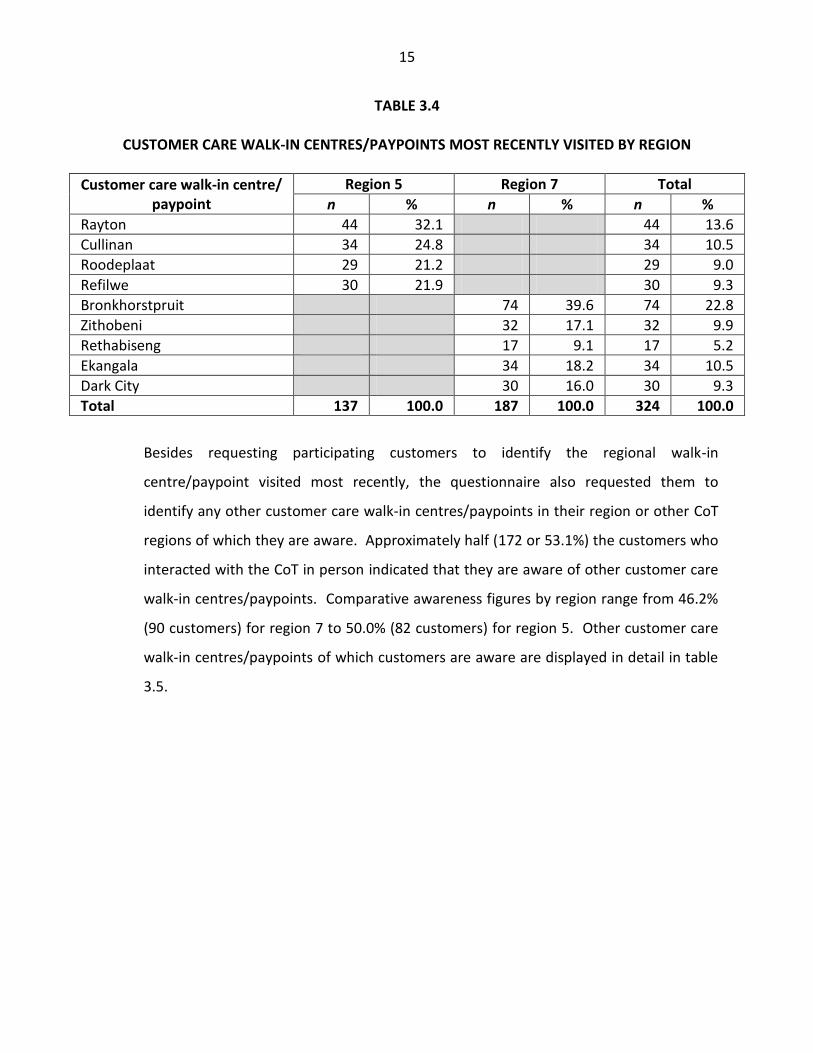

TABLE 3.4

CUSTOMER CARE WALK-IN CENTRES/PAYPOINTS MOST RECENTLY VISITED BY REGION

Customer care walk-in centre/ paypoint

Region 5 Region 7 Total

n % n % n %

Rayton 44 32.1 44 13.6

Cullinan 34 24.8 34 10.5

Roodeplaat 29 21.2 29 9.0

Refilwe 30 21.9 30 9.3

Bronkhorstpruit 74 39.6 74 22.8

Zithobeni 32 17.1 32 9.9

Rethabiseng 17 9.1 17 5.2

Ekangala 34 18.2 34 10.5

Dark City 30 16.0 30 9.3

Total 137 100.0 187 100.0 324 100.0

Besides requesting participating customers to identify the regional walk-in

centre/paypoint visited most recently, the questionnaire also requested them to

identify any other customer care walk-in centres/paypoints in their region or other CoT

regions of which they are aware. Approximately half (172 or 53.1%) the customers who

interacted with the CoT in person indicated that they are aware of other customer care

walk-in centres/paypoints. Comparative awareness figures by region range from 46.2%

(90 customers) for region 7 to 50.0% (82 customers) for region 5. Other customer care

walk-in centres/paypoints of which customers are aware are displayed in detail in table

3.5.

16

TABLE 3.5

AWARENESS OF OTHER CUSTOMER CUSTOMER CARE WALK-IN CENTRES/ PAYPOINTS BY REGION

Customer care walk-in centre/

paypoint

Region 5 Region 7 Total

n % n % n %

Zithobeni 0 0.0 14 15.6 14 8.1

Eersterus 3 3.7 1 1.1 4 2.3

Refilwe 7 8.5 0 0.0 7 4.1

Rayton 43 52.4 0 0.0 43 25.0

Mamelodi 1 1.2 0 0.0 1 0.6

Ekangala 0 0.0 16 17.8 16 9.3

Dark City 0 0.0 10 11.1 10 5.8

Cullinan 22 26.8 0 0.0 22 12.8

Bronkhorstspruit 4 4.9 43 47.8 47 27.3

BKS 1 1.2 6 6.7 7 4.1

Sinoville 1 1.2 0 0.0 1 0.6

Total 82 100.0 90 100.0 172 100.0

A matrix analysis between the paypoint most recently visited and other customer care

walk-in centres/paypoints which customers are aware of is presented in table 3.6 by

region. The table reflects the number of customers who claimed to be aware of other

customer care walk-in centres/paypoints. The fact that 53.1% of customers who last

interacted with the CoT in person indicated that they are also aware of other customer

care walk-in centres/paypoints besides the one visited most recently displays fairly high

levels of awareness of other customer care walk-in centres/paypoints in- and outside

the survey regions. Table 3.6 clearly shows that participating customers who last

interacted with Rethabiseng (100.0%), Cullinan (79.4%) and Refilwe (76.7%), are also

aware of other customer care walk-in centres/paypoints. Of those customers who are

aware of other customer care walk-in centres/paypoints, most claim to be aware of the

Bronkhorstspruit (26.1%) and Rayton (25.0%) customer care walk-in centres/paypoints.

The BKS customer care centre (Pretorius Street) recorded the highest level of awareness

(4.1%) among regions outside the survey areas (regions 5 and 7).

17

TABLE 3.6

CUSTOMER AWARENESS OF OTHER CUSTOMER CARE WALK-IN CENTRES/PAYPOINTS IN- AND OUTSIDE SURVEY REGIONS

Customer care walk-in centre/ paypoint

Region 5 Region 7 Total

Last visited

Aware

Rayton Cullinan Roodeplaat Refilwe Bronkhorstspruit Zithobeni Rethabiseng Ekangala Dark City

n n n n n n n n n n

Region 5

Rayton 0 26 6 11 0 0 0 0 0 43

Cullinan 9 0 1 12 0 0 0 0 0 22

Roodeplaat 0 0 0 0 0 0 0 0 0 0

Refilwe 7 0 0 0 0 0 0 0 0 7

Region 7

Bronkhorstspruit 2 0 2 0 0 11 11 9 12 47

Zithobeni 0 0 0 0 8 0 6 0 0 14

Rethabiseng 0 0 0 0 0 0 0 0 0 0

Ekangala 0 0 0 0 16 0 0 0 0 16

Dark City 0 0 0 0 0 0 0 10 0 10

Other regions

Eersterus 2 0 1 0 1 0 0 0 0 4

Mamelodi 0 1 0 0 0 0 0 0 0 1

BKS 1 0 0 0 2 0 0 4 0 7

Sinoville 0 0 1 0 0 0 0 0 0 1

Total aware 21 27 11 23 27 11 17 23 12 172

Total used 44 34 29 30 74 32 17 34 30 324

% aware 47.7 79.4 37.9 76.7 36.5 34.4 100.0 67.6 40.0 53.1

18

Besides enquiring about the awareness of other customer care walk-in

centres/paypoints, the questionnaire requested customers who last interacted with the

CoT in person to indicate which other customer care walk-in centres/paypoints they had

used (see table 3.7). Of the total customers who are aware of other customer care

walk-in centres/paypoints (172 or 53.1% of customers (n = 324) who last interacted with

the CoT in person), 119 (69.2%) customers indicated that they had also used other

customer care walk-in centres/paypoints in the preceding 12 months.

TABLE 3.7

OTHER INTER-REGION CUSTOMER CARE WALK-IN CENTRES/PAYPOINTS USED BY REGION

Customer care walk-in

centres/paypoints

Aware of other customer care

walk-in centres/paypoints

Used other customer care

walk-in centres/paypoints

% using other customer care

walk-in centres/paypoints

n n %

Region 5

Rayton 43 21 48.8

Cullinan 22 20 90.9

Refilwe 7 7 100.0

Region 7

Bronkhorstspruit 47 31 66.0

Zithobeni 14 10 71.4

Ekangala 16 15 93.8

Dark City 10 8 80.0

Other regions

Eersterus 4 2 50.0

Mamelodi 1 0 0.0

BKS 7 4 57.1

Sinoville 1 1 100.0

Total 172 119 69.2

Table 3.8 provides a more detailed analysis of the use of other customer care walk-in

centres/paypoints besides the latest one used. The exhibit shows that 17.6% of all

customers using other customer care walk-in centres/paypoints (n = 119), last visited

the Bronkhorstspruit paypoint. Most customers who last used Bronkhorstspruit (71.4%)

19

had also used Ekangala. Similarly, most customers (60.0%), who recently visited Refilwe

had also visited the Cullinan paypoint during the preceding 12 months. Likewise, 62.5%

of Rethabiseng customers had previously visited the Bronkhorstspruit paypoint. Table

3.8 clearly shows the highest ‘migration rate’ for Bronkhorstspruit (17.6%), Refilwe

(16.8%) and Ekangala (14.3%).

TABLE 3.8

OTHER CUSTOMER CARE WALK-IN CENTRES/PAYPOINTS USED BY REGION

Other used Latest used

Region 5 Region 7 Other

regions Total %

Rayton Cullinan Roode-plaat

Refilwe Bronkhorst-

spruit Zithobeni Rethabiseng Ekangala

Dark City

Region 5 Rayton

7

7 1

1 16 13.4

Cullinan 9

9 7.6

Roodeplaat 4 1

1 6 5.0

Refilwe 8 12

20 16.8

Region 7

Bronkhorstspruit

4

15

2 21 17.6

Zithobeni

8

8 6.7

Rethabiseng

10 6

16 13.4

Ekangala

6

8 3 17 14.3

Dark City

6

6 5.0

Total 21 20 0 7 31 10 0 15 8 7 119 100.0

The information displayed in table 3.8 shows clear multiple and inter- and intraregional

paypoint usage levels. Intraregional usage is especially notable among Rethabiseng

customers, who indicated that they had also used the Bronkhorstspruit customer care

walk-in centre and Zithobeni paypoint within the same region during the preceding 12

months. In region 5, similar intraregional usage levels are visible where, especially

Refilwe customers, indicated that they had also visited the Rayton customer care walk-

in centre and Cullinan paypoint during the preceding 12 months. With regard to inter-

regional usage levels, it is interesting to note from table 3.8 that customers who last

interacted with a paypoint in region 7, had not visited another paypoint in region 5.

Despite the latter, some interregional usage trends are notable where especially

20

Bronkhorstspruit and Ekangala customers also indicated that they had used customer

care walk-in centres/paypoints (mainly the BKS customer care centre).

The inter- and intraregional exposure to paypoint service delivery and multiple paypoint

usage is regarded as an advantage for the survey as respondents could base their

satisfaction ratings of the quality of service delivery on their experience with more than

one paypoint.

The main reasons cited by participating customers for using other customer care walk-in

centres/paypoints are summarised as follows:

Region 5

No assistance received

Safety issues

Distance (closer to home/work)

Visiting an area close to paypoint

Queuing problems

Other customer care walk-in centres/paypoints more accessible

Referred to other customer care walk-in centres/paypoints

Region 7

Computers offline

No assistance/ poor service

Distance (closer to home/work)

Card facilities not working

Paypoint damaged

Referred to other customer care walk-in centres/paypoints

Queuing problems

Alleged corruption

21

3.4.1 Customer satisfaction

A crucial part of the questionnaire was devoted to measuring the level of customer

satisfaction with the quality of service delivery at the customer care walk-in

centres/paypoints most recently visited in person. The customer ratings for the five

major service quality constructs (facilities, account payment processing, trading hours,

counter staff and dealing with queries/complaints) and individual service attributes are

displayed in tables 3.9a (region) and 3.9b (customer type). Tables 3.9(a) and (b) use a

colour coded analysis approach showcasing the average (mean) rating scores for

customers who last interacted with a CoT paypoint in person and who were requested

to rate the CoT on a 5-point satisfaction scale, where ‘1’ = very dissatisfied and ‘5’ = very

satisfied. Therefore, average scores closer to ‘1’ reflect higher levels of dissatisfaction

while scores closer to ‘5’ reflect higher levels of satisfaction with the various paypoint

constructs/attributes. The following colour codes denote customer satisfaction levels as

follows:

Red (average scores between 1.00 – 2.00): Very dissatisfied

Orange (average scores between 2.01 – 3.00): Dissatisfied

Yellow (average scores between 3.01 – 4.00): Satisfied

Green (average scores between 4.01 – 5.00): Very satisfied

For convenience, the actual number of customers who ranked a specific variable (valid

n) are provided. These additional statistics are important to note as not all customers

experienced (or used) the listed services for which satisfaction ratings were requested.

In fact, respondents were only allowed to provide a satisfaction rating for a specific

service if he/she actually experienced such a service.

22

TABLE 3.9(a)

AVERAGE SATISFACTION RATING SCORES FOR PAYPOINT CONSTRUCTS/ATTRIBUTES BY REGION

Evaluation criteria Region 5 Region 7 Total

Valid n Mean Valid n Mean Valid n Mean

Appearance of facilities 136 3.41 186 3.45 322 3.43

Equipment 136 3.44 186 2.94 322 3.15

Adequacy of parking facilities 108 2.92 128 2.41 236 2.64

Adequacy of security 112 3.23 186 3.89 298 3.64

Average: Facilities 3.25 3.17 3.22

Efficiency of the queuing system 135 3.85 183 3.40 318 3.59

All paypoint stations are manned during CoT office hours hours

127 4.01 164 3.78 291 3.88

Promptness in providing duplicate statements 96 3.46 129 3.26 225 3.35

Promptness in providing electricity/water consumption reading and financial details

93 3.06 139 2.79 232 2.90

Promptness in providing details on water leakage

89 2.98 128 2.25 217 2.55

Promptness in resolving misallocations of a payment

87 2.82 118 2.64 205 2.72

Promptness in opening a new municipal service account

76 2.95 88 3.43 164 3.21

Promptness in processing financial transactions 93 3.43 123 3.62 216 3.54

Efficiency of the cashier payment system 111 3.88 154 3.85 265 3.86

Promptness of cashiers in handling money 113 3.84 151 4.11 264 3.99

Cashier preciseness in handling money (receiving money/return appropriate change)

114 4.03 154 4.09 268 4.06

Average: Processing account payments 3.48 3.38 3.42

Convenience of customer care walk-in centre/paypoint operating hours

133 4.31 170 3.91 303 4.08

Average: Trading hours and accessibility 4.31

3.91

4.08

Staff friendliness 137 4.01 187 4.12 324 4.07

Staff politeness and professionalism with customers

137 3.99 187 4.01 324 4.00

Staff trustworthiness and honesty 134 3.85 182 3.96 316 3.91

Staff skills to do jobs well 135 3.93 186 4.05 321 4.00

Staff appearance (neatly and appropriately dressed)

134 3.90 186 4.44 320 4.21

(continue…)

23

TABLE 3.9(a) (cont)

Evaluation criteria Region 5 Region 7 Total

Valid n Mean Valid n Mean Valid n Mean

Staff ability to pay attention to customer details 133 4.06 187 4.03 320 4.04

Staff helpfulness and sympathy towards customers

136 3.87 187 3.75 323 3.80

Promptness of staff in assisting customers 134 4.00 186 3.85 320 3.91

Staff focus on customers 136 3.99 187 3.83 323 3.89

Availability of staff 136 3.96 186 3.72 322 3.82

Average: Counter staff 3.95 3.98 3.97

Resolving information requests on first contact 121 3.58 171 2.96 292 3.22

Promptness in resolving service requests 119 3.44 170 2.75 289 3.03

Promptness in resolving complaints 106 3.08 165 2.69 271 2.85

Average: Dealing with queries/complaints 3.37 2.80 3.03

Total Average 3.63 3.52 3.56

No statistically significant differences is noted between the overall satisfaction scores

for regions 5 (average score = 3.63) and 7 (average score = 3.52). However, when

ranking the rated scores, a number of clear differences are observed. In order to

identify the top and bottom customer satisfaction items, the average scores for all 29

service attributes were ranked for each region. The top and bottom satisfaction scores

for both regions are displayed in exhibit 3.1.

24

EXHIBIT 3.1

TOP AND BOTTOM SATISFACTION ITEMS BY REGION

Region 5 Region 7

Variable Score Variable Score

Top

Convenience of customer care walk-in centre/paypoint operating hours

Staff ability to pay attention to customer details

Cashier preciseness in handling money(receiving money/return appropriate change)

All paypoint stations are manned during CoT office hours hours

Staff friendliness

4.31 4.06 4.03 4.01 4.01

Staff appearance (neatly and appropriately dressed)

Staff friendliness

Promptness of cashiers in handling money

Cashier preciseness in handling money (receiving money/return appropriate change)

Staff skills to do jobs well

Staff ability to pay attention to customer details

4.44 4.12 4.11 4.09

4.05

4.03

Bo

tto

m

Promptness in resolving misallocations of a payment

Adequacy of parking facilities

Promptness in opening a new municipal service account

Promptness in providing details on water leakage

2.82 2.92 2.95 2.98

Promptness in providing details on water leakage

Adequacy of parking facilities

Promptness in resolving misallocations of a payment

Promptness in resolving complaints

Promptness in resolving service requests

Promptness in providing electricity/water consumption reading and financial details

Equipment

Resolving information requests on first contact

2.25 2.41

2.64 2.69 2.75 2.79

2.94

2.96

It is clear from exhibit 3.1 that certain counter staff attributes/skills in both regions

received fairly positive satisfaction ratings. However, from a strategic perspective, items

with low scores require priority attention. Service areas such as promptness in resolving

misallocations of payments, adequacy of parking facilities and promptness in providing

details on water leakages, should receive prompt attention to improve the quality of

future service delivery at CoT customer care walk-in centres/paypoints in both regions 5

and 7.

As mentioned, the satisfaction ratings were also analysed by customer type

(households/businesses). This analysis is presented in table 3.9(b).

25

TABLE 3.9(b)

AVERAGE SATISFACTION RATING SCORES FOR PAYPOINT CONSTRUCTS/ATTRIBUTES BY CUSTOMER TYPE

Evaluation criteria Household Business Total

Valid n Mean Valid n Mean Valid n Mean

Appearance of facilities 309 3.48 13 2.38 322 3.43

Equipment 309 3.17 13 2.69 322 3.15

Adequacy of parking facilities 223 2.61 13 3.15 236 2.64

Adequacy of security 285 3.67 13 3.00 298 3.64

Average: Facilities 3.23 2.81 3.22

Efficiency of the queuing system 305 3.64 13 2.46 318 3.59

All paypoint stations are manned during CoT office hours

279 3.93 12 2.67 291 3.88

Promptness in providing duplicate statements 212 3.42 13 2.08 225 3.35

Promptness in providing electricity/water consumption reading and financial details

219 2.96 13 1.85 232 2.90

Promptness in providing details on water leakage 205 2.58 12 2.00 217 2.55

Promptness in resolving misallocations of a payment

193 2.78 12 1.75 205 2.72

Promptness in opening a new municipal service account

154 3.27 10 2.20 164 3.21

Promptness in processing financial transactions 204 3.60 12 2.50 216 3.54

Efficiency of the cashier payment system 252 3.91 13 3.00 265 3.86

Promptness of cashiers in handling money 252 4.04 12 3.00 264 3.99

Cashier preciseness in handling money (receiving money/return appropriate change)

255 4.13 13 2.85 268 4.06

Average: Processing account payments 3.48 2.40 3.42

Convenience of customer care walk-in centre/paypoint operating hours

290 4.12 13 3.31 303 4.08

Average: Trading hours and accessibility 4.12 3.31 4.08

Staff friendliness 311 4.11 13 3.15 324 4.07

Staff politeness and professionalism with customers

311 4.04 13 3.00 324 4.00

Staff trustworthiness and honesty 305 3.96 11 2.55 316 3.91

Staff skills to do jobs well 308 4.06 13 2.62 321 4.00

Staff appearance (neatly and appropriately dressed)

307 4.25 13 3.31 320 4.21

Staff ability to pay attention to customer details 307 4.10 13 2.77 320 4.04

(continue…)

26

TABLE 3.9(b) (cont)

Evaluation criteria Household Business Total

Valid n Mean Valid n Mean Valid n Mean

Staff helpfulness and sympathy towards customers 310 3.85 13 2.69 323 3.80

Promptness of staff in assisting customers 307 3.98 13 2.38 320 3.91

Staff focus on customers 310 3.96 13 2.38 323 3.89

Availability of staff 309 3.88 13 2.54 322 3.82

Average: Counter staff 4.02 2.74 3.97

Resolving information requests on first contact 279 3.26 13 2.23 292 3.22

Promptness in resolving service requests 276 3.08 13 2.08 289 3.03

Promptness in resolving complaints 258 2.88 13 2.15 271 2.85

Average: Dealing with queries/complaints 3.07 2.15 3.03

Total average 270 3.61 13 2.58 283 3.56

When analysing the overall average satisfaction scores by customer type, it is clear that

satisfaction with CoT customer care walk-in centres/paypoints is far lower among

businesses than households. Despite this, many of the top and bottom satisfaction

scores of households and businesses are fairly similar. To showcase these findings, the

top and bottom satisfaction scores for both customer types are displayed in exhibit 3.2.

27

EXHIBIT 3.2

TOP AND BOTTOM SATISFACTION ITEMS BY CUSTOMER TYPE

Households Businesses

Variable Score Variable Score

Top

Staff appearance (neatly and appropriately dressed)

Cashier preciseness in handling money (receiving money/return appropriate change)

Convenience of customer care walk-in centre/paypoint operating hours

Staff friendliness

Staff ability to pay attention to customer details

Staff skills to do jobs well

Promptness of cashiers in handling money

Staff politeness and professionalism with customers

4.25 4.13 4.12 4.11 4.10 4.06 4.04 4.04

Staff appearance (neatly and appropriately dressed)

Convenience of customer care walk-in centre/paypoint operating hours

Staff friendliness

Adequacy of parking facilities

3.31

3.31 3.15 3.15

Bo

tto

m

Promptness in providing details on water leakage

Adequacy of parking facilities

Promptness in resolving misallocations of a payment

Promptness in resolving complaints

Promptness in providing electricity/water consumption reading and financial details

2.58 2.61 2.78 2.88 2.96

Promptness in resolving misallocations of a payment

Promptness in providing electricity/water consumption reading and financial details

Promptness in providing details on water leakage

Promptness in providing duplicate statements

Promptness in resolving service requests

1.75

1.85

2.00

2.08 2.08

In summary, exhibit 3.3 presents an overview of the research findings by region and

customer type using the colour code to reflect the various levels of satisfaction. The

analysis shows the number and percentage of attributes for each of the satisfaction

categories. For example, none of the 29 research attributes recorded ‘very dissatisfied’

ratings in regions 5 and 7 among households, while businesses ‘3’ attributes as ‘very

dissatisfied’.

28

EXHIBIT 3.3

TOP AND BOTTOM SATISFACTION ITEMS BY REGION AND CUSTOMER TYPE

Criteria Rating range

Region 5 (n = 164)

Region 7 (n = 195)

Households (n = 325)

Businesses (n = 34)

No of items

% No of items

% No of items

% No of items

%