Embed Size (px)

Citation preview

113

American Scientific Research Journal for Engineering, Technology, and Sciences (ASRJETS)

ISSN (Print) 2313-4410, ISSN (Online) 2313-4402

http://asrjetsjournal.org/

Currency Risk: Possibility of Its Evaluation and Hedging

in Modern Conditions

Assylkhan Tumanova*

, Wei Wangb

a,bSchool of Sciences, Zhejiang University of Science and Technology, 310023, Hangzhou, China

aEmail: [email protected]

bEmail: [email protected]

Abstract

The purpose of this article is to show the importance of accounting the impact of all types of currency risk on

activities companies. This topic has acquired particular relevance in view of the developing global financial

crisis, influencing the exposure of organizations currency risk, and increasing the attention of its agents hedging.

The article describes methods for assessing currency risk and methods for reducing it using derivatives market

instruments and non-financial strategies and highlights the features of investment in the international the real

estate market.

Keywords: risk management; currency risk assessment; currency risk management; transactional currency risks;

translational currency risks; operational currency risks; currency risk in real estate transactions; value at risk;

hedging of foreign exchange risks; derivative financial instruments.

1. Introduction

Increasing the role of risk management in the development of the strategy and tactics of the bank's development

According to the report of KPMG International "Big Leaders of Financial Sector Executives" shortcomings in

the risk management system, which they have stuck to until now. Among the most vulnerabilities were marked

with incentives to stimulate and a clear system and culture of risk management, and lack of experience in the

application of modern methods of their assessment. Among the use of assessment tools and risk management

transition from the simple establishment of gross limits and the assessment of maximum losses under the current

economic conditions to more detailed models of stress testing and scenario analysis, allowing to take into

account the volatility of the macroeconomic environment.

------------------------------------------------------------------------

* Corresponding author.

American Scientific Research Journal for Engineering, Technology, and Sciences (ASRJETS) (2021) Volume 79, No 1, pp 113-131

114

At the same time, the majority of the respondents agreed that it is preferable at the moment to increase

investment in human capital, that is, training and attracting employees with extensive experience in the field of

risk management. The unfavorable conjuncture of world financial markets and the unpreparedness of most

organizations to implement negative scenarios, as well as the lack of well-developed rapid response measures

increase the role of experts in the field risk assessment and management, from whose decisions in not only

strategy depends a lot, but also tactics business development, and the possibility of its further functioning.

In modern conditions, the importance of assessing almost all types of risks has increased. The financial crisis

affecting banks and other organizations around the world has led to a decline in the availability of credit. It is

becoming more and more difficult to obtain new and roll over old loans due to the increased credit risks of

borrowers and risks of liquidity of lenders. In order to receive sufficient income to continue their activities,

banks strive to retain and attract bona fide customers, but a special Along with the above, attention is paid to

market risks, the parameters of which are most unstable today.

Currency risk as one of the types of market risks and its assessment

Market risks include:

• interest rate risk;

• currency risk;

• stock risk;

• derivatives market risk.

Currency risk is the risk of losses due to unfavorable changes in exchange rates for an economic agent. It is

associated primarily with globalization in the world economy. Most of the economic entities are directly or

indirectly exposed to the influence of foreign exchange risks. First of all, exporters, importers, as well as

financial institutions depend on fluctuations in exchange rates.

Changes in exchange rates affect both current and future cash flows, as well as the profitability, competitiveness

and value of companies. The impact of exchange rates on the activities of organizations depends, on the one

hand, on the structure of foreign exchange flows and the company's competitive position in the market, and on

the other, on the hedging methods used.

There are four main types of currency risks:

1. Translational (calculated, balance sheet, accounting) currency risk;

2. Transactional (contractual) currency risk;

3. Operational foreign exchange risk;

American Scientific Research Journal for Engineering, Technology, and Sciences (ASRJETS) (2021) Volume 79, No 1, pp 113-131

115

4. Hidden currency risks.

translational currency risk

Translational currency risk reflects the mismatch between assets and liabilities of an organization denominated

in currencies of different countries. A typical example is the situation when a Russian company has long-term

foreign currency loans (or issues Eurobonds). As a result, even with a short-term growth in the foreign exchange

rate, a significant balance sheet increase in the credit burden is observed, which makes the company less

attractive to investors. Also, companies with subsidiaries in other countries face translation risk when the net

assets of the divisions are not balanced by liabilities. If there are foreign assets in the company's consolidated

balance sheet significant fluctuations in the value of these assets are possible, while there may be no real change

in cash flow.

transactional foreign exchange risk

Transactional foreign exchange risk reflects the likelihood of foreign exchange losses on specific transactions

(transactions) due to unexpected changes in the foreign exchange rate. It arises from the uncertainty of the value

in the national currency of a foreign exchange transaction in the future. Transactional currency risk arises during

export-import transactions, lending transactions, ie, when receivables or payables in foreign currency arise, if

the debt itself appears before the exchange rate changes, and payment must be made in the period after it.

Transactional currency risks have a direct impact on the cash flows of corporations, and as a result, they must be

regularly forecast and hedged.

operational foreign exchange risk

Operational foreign exchange risk reflects the likelihood of loss of competitiveness, decrease in revenue due to

unexpected changes in the foreign exchange rate.

Operational foreign exchange risk affects a company's position in the market, its competitiveness and, unlike

contractual foreign exchange risk, is most often subjective and probabilistic in nature.

The main factors determining the magnitude of this risk are:

• type of activity of the company;

• industry affiliation;

• elasticity of demand for the firm's product;

• the degree of dependence on imported resources;

• method of pricing.

American Scientific Research Journal for Engineering, Technology, and Sciences (ASRJETS) (2021) Volume 79, No 1, pp 113-131

116

hidden currency risks

There are translational, transactional and operational foreign exchange risks that, at first glance, are not obvious.

For example, a supplier in the domestic market may use imported resources, and the company using the services

of such a supplier is indirectly exposed to operational risk, since the increase in the cost of the supplier's costs as

a result of the depreciation of the national currency would force this supplier to increase prices.

Latent operational and / or translation risks may also arise if a foreign subsidiary is exposed to its own risks.

Changes in foreign exchange rates in the long term do not simply lead to excess profits or losses on individual

transactions (transactional risks). As a result of the realization of currency risks, the assessment of the company

by third-party investors changes (translation risks), the competitiveness of companies or their individual foreign

branches changes (operational risks). As a consequence, the consequence of the realization of currency risks is

the realization of strategic risks. Assessment and management of foreign exchange risks is a non-trivial and

important task for most large enterprises.

One of the most popular methods of market risk management is the calculation of the maximum loss ratio

during a given period at a given level of probability Value-at-Risk (VAR). This method, which is the basis of

the methodologies for assessing the exposure of organizations to market risk, used by regulators to determine

the adequacy of their capital, began to be used when building their own risk management systems in banks.

Many shortcomings of the basic VAR model can be eliminated by including such methods as scenario analysis,

stress testing or exclusion of assumptions about the normal distribution of instrument returns and the density of

losses distribution into the model. The calculation of average losses outside the VAR also provides additional

information about the risks assumed. This indicator is called expected losses

(Expected Shortfall - ES) and can be used to determine the amount of reserves required to insure a portfolio

against losses exceeding VAR. The calculation of the indicator is quite simple: the size of the reserve is equal to

the difference between the amount of expected losses exceeding VAR and VAR.

According to the requirements of regulators, for example, the Basel requirements for calculating market risk, the

confidence interval used in models based on VAR should be 99%. This means that with a 99% probability the

losses will not exceed a certain value in a given period. At the same time, if the magnitude of losses, which is

probable only in 1% of cases, increases, VAR does not change, while ES increases and this should warn risk

managers about impending changes. However, if VAR models are amenable to back testing, that is, to check the

adequacy of the model against historical data, then ES are not a regularity, but rather an exception to the rule.

These events are difficult to predict, since their realizations are quite rare, therefore their testing is difficult and

requires expert judgment. Wong [12] suggested using the saddle point method to overcome this problem, but

this process is quite laborious.

An important task in managing the risks of a bank is the need to forecast the worst-case scenario for the

development of events. Identification of key factors affecting the increase in bank losses and their consideration

American Scientific Research Journal for Engineering, Technology, and Sciences (ASRJETS) (2021) Volume 79, No 1, pp 113-131

117

when developing scenarios allows timely implementation of preventive measures to minimize losses and have

additional reserves to cover them

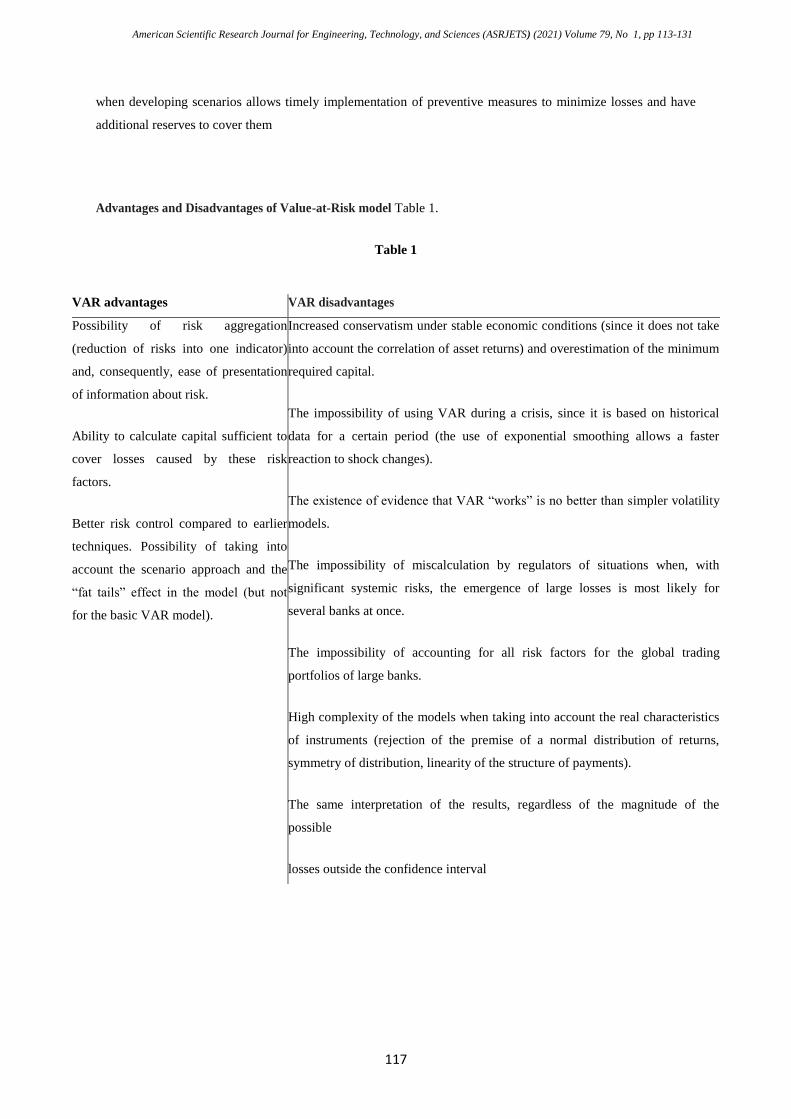

Advantages and Disadvantages of Value-at-Risk model Table 1.

Table 1

VAR advantages VAR disadvantages

Possibility of risk aggregation

(reduction of risks into one indicator)

and, consequently, ease of presentation

of information about risk.

Ability to calculate capital sufficient to

cover losses caused by these risk

factors.

Better risk control compared to earlier

techniques. Possibility of taking into

account the scenario approach and the

“fat tails” effect in the model (but not

for the basic VAR model).

Increased conservatism under stable economic conditions (since it does not take

into account the correlation of asset returns) and overestimation of the minimum

required capital.

The impossibility of using VAR during a crisis, since it is based on historical

data for a certain period (the use of exponential smoothing allows a faster

reaction to shock changes).

The existence of evidence that VAR “works” is no better than simpler volatility

models.

The impossibility of miscalculation by regulators of situations when, with

significant systemic risks, the emergence of large losses is most likely for

several banks at once.

The impossibility of accounting for all risk factors for the global trading

portfolios of large banks.

High complexity of the models when taking into account the real characteristics

of instruments (rejection of the premise of a normal distribution of returns,

symmetry of distribution, linearity of the structure of payments).

The same interpretation of the results, regardless of the magnitude of the

possible

losses outside the confidence interval

American Scientific Research Journal for Engineering, Technology, and Sciences (ASRJETS) (2021) Volume 79, No 1, pp 113-131

118

However, the worst is often associated with what has already been experienced and does not lend itself to

regulation, while unforeseen losses can be much greater.

Risk assessment methods based on VAR calculation are usually very short-term (from 1 day to several weeks)

and assume that tomorrow's situation is more or less similar to what is happening at the moment. Since there

were no crisis phenomena in the housing market in previous years, the forecasts did not take this into account.

VAR did not change, while losses outside the confidence interval increased significantly and became more and

more probable. The same operations were carried out with an ever-increasing VAR, which should have alerted

managers. Experienced specialists in the field of risk management, not only mathematical models, are able to

mitigate the negative consequences of the crisis. However, certain signals available when VAR and ES are

applied simultaneously help to respond in time to changing business conditions.

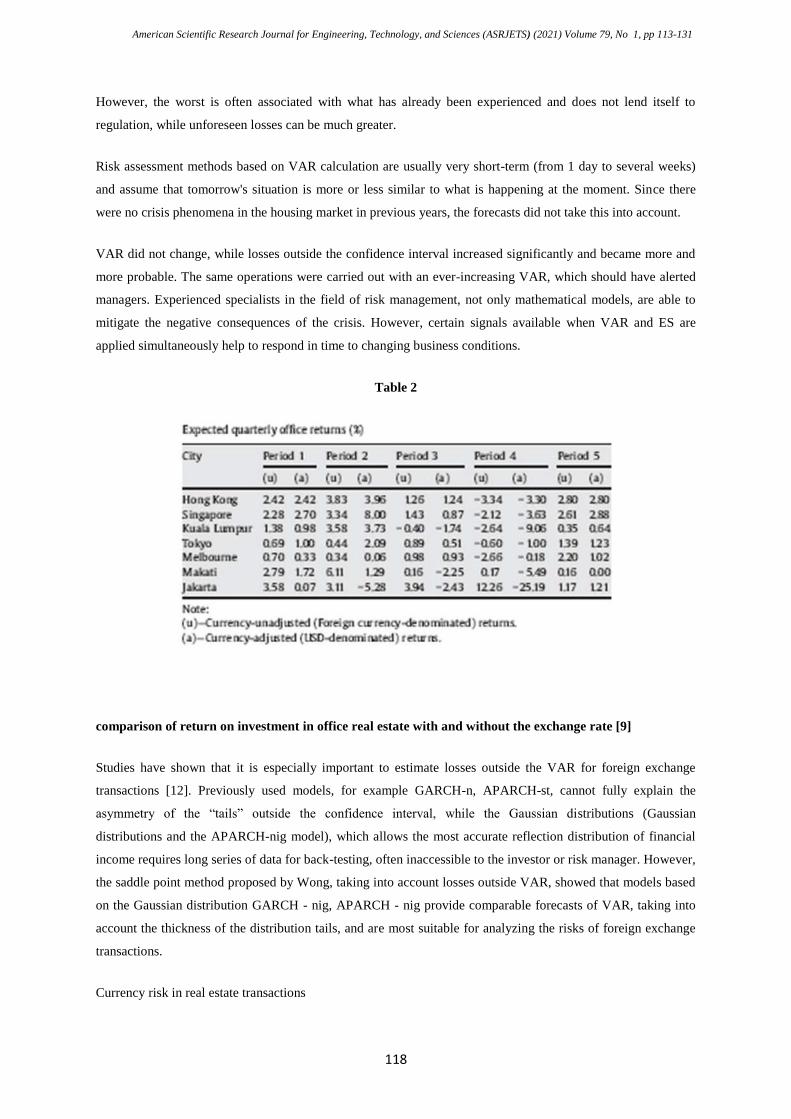

Table 2

comparison of return on investment in office real estate with and without the exchange rate [9]

Studies have shown that it is especially important to estimate losses outside the VAR for foreign exchange

transactions [12]. Previously used models, for example GARCH-n, APARCH-st, cannot fully explain the

asymmetry of the “tails” outside the confidence interval, while the Gaussian distributions (Gaussian

distributions and the APARCH-nig model), which allows the most accurate reflection distribution of financial

income requires long series of data for back-testing, often inaccessible to the investor or risk manager. However,

the saddle point method proposed by Wong, taking into account losses outside VAR, showed that models based

on the Gaussian distribution GARCH - nig, APARCH - nig provide comparable forecasts of VAR, taking into

account the thickness of the distribution tails, and are most suitable for analyzing the risks of foreign exchange

transactions.

Currency risk in real estate transactions

American Scientific Research Journal for Engineering, Technology, and Sciences (ASRJETS) (2021) Volume 79, No 1, pp 113-131

119

In the context of the developing financial crisis in the world markets and the related high volatility of prices of

financial instruments, they are becoming increasingly acquiring popularity alternative investments, such as

venture capital

ny projects, art objects, goods and raw materials (oil, gold), real estate. To diversify investments and reduce risk,

investors often prefer to invest in the global real estate market, so the assessment of the currency risks of such

investments becomes relevant.

The movements of the exchange rate have a significant impact on the profitability of international investments

due to the constantly changing exchange rate of the currencies of the investment object and the national

currency of the economic agent - investor. Let us assume that the investor is rational and has sufficient funds to

invest in the international real estate market. At the same time, two types of investments are made: in foreign

real estate and foreign currency. To compare the profitability with and without the exchange rate, it is necessary

to calculate the profitability of the investment object in foreign currency and taking into account the conversion

of income into national units1.

You need to answer the following questions:

1. Does the exchange rate affect the profitability of international investments (especially during periods of

high exchange rate volatility)?

2. What is its impact - positive or negative?

3. Is it possible to reduce the currency risk of real estate transactions?

The results of real estate research in 7 Pacific cities, presented in Table. 2,

show that in periods 1 (1986 - 1995),

2 (1996-2007), 3 (1996-1998), 4 (1999-2007)

the currency risk in most cases had a negative impact on the profitability of investments in office real estate [9].

For each of the considered periods, this effect is different and in some cases leads to a negative return on

investment. The greatest negative effect from changes in the exchange rate was revealed for investments in

Jakarta - a decrease in profitability from 3.58% (unadjusted) to 0.07% (adjusted for the exchange rate), a

positive one - in Tokyo (0.69% - 1.00 %) for the entire period. But for the entire set of observations, the

previously described currency effect is statistically insignificant.

It is important to remember that foreign exchange risk cannot be hedged when investing in real estate, however,

if possible, investors try to reduce it. As for the possibility of diversifying investments in the international real

estate market as one of the ways to reduce risk, the correlation coefficients of the return on investments illustrate

the low interdependence of markets practically in the real estate market.

American Scientific Research Journal for Engineering, Technology, and Sciences (ASRJETS) (2021) Volume 79, No 1, pp 113-131

120

over the entire period, while the exchange rate adjustment further reduces this value (although in most cases the

differences are statistically insignificant). The correlation of exchange rates is also low, which makes it possible

to reduce the exchange rate risk during diversification of investments and to extract additional profitability in a

period of increased volatility [9].

2. Currency risk when investing in real estate of the cis countries

Considering the possibilities of investing in real estate of the CIS countries, the prices for apartments in the

secondary market of 4 cities were analyzed: Minsk, Astana, Kiev and Moscow. Comparison of investment

returns with and without taking into account the exchange rate of national currencies in relation to the euro are

presented in table. 3 - 6.

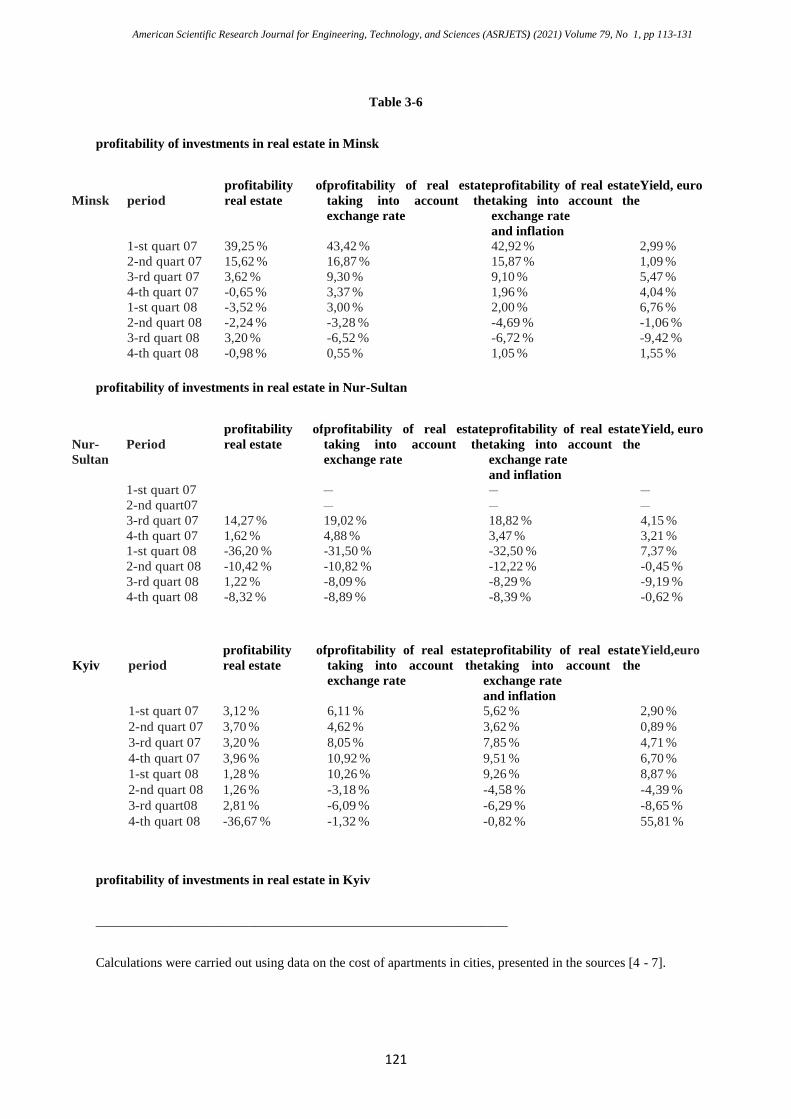

The results show that currency risk predominantly has a positive effect on the profitability of real estate

investments over the period under review. Nevertheless, the magnitude of this effect differs for each sub-period

and for cities. The largest positive effect on the yield on the foreign exchange rate was made in the 4th quarter

of 2007, the greatest negative effect on the 3rd quarter of 2008. However, it should be emphasized that a

decrease in negative profitability is, of course, a positive effect, but not an incentive to invest in this market,

therefore, economic agents should be very careful when choosing objects for compiling an international

portfolio of assets, taking into account their risk and profitability.

As shown by a study of housing markets in 4 capitals of the CIS countries, foreign exchange risk had a different

impact on the riskiness of investments in apartments in different cities, but this influence was mostly negative

(the risk increased). One of the possible options for reducing currency risk, although not completely eliminating

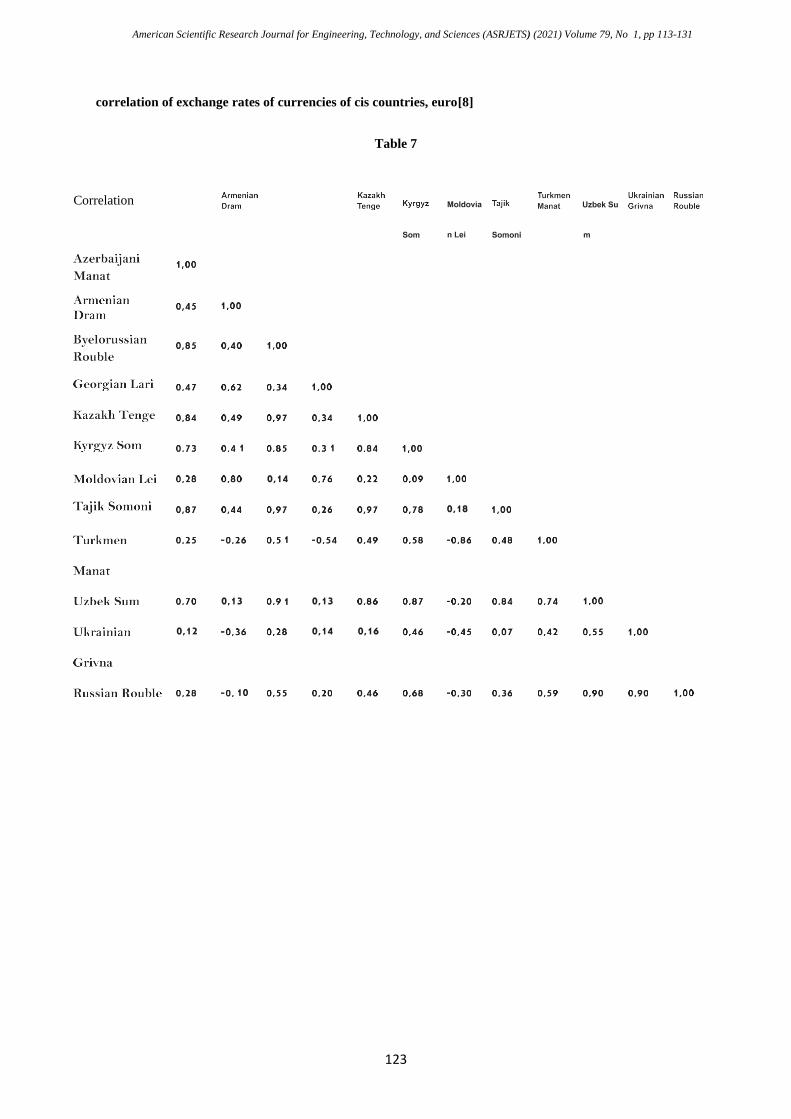

it, is the diversification of investments. Correlation coefficients of exchange rates of the CIS countries are

presented in table

By choosing combinations with negative correlation coefficients, an investor can significantly reduce the

portfolio currency risk. However, other factors also affect the overall risk and return on investment: inflation,

the political situation, tax policy and the general macroeconomic environment.

For Russia, it was found that the negative correlation of exchange rates in the period 2007-2008. was observed

for the pairs: ruble-lei (-0.3) and ruble-dram (-0.1), therefore, the currency risk of a portfolio diversified in the

markets of these countries is lower compared to investments of the full amount in assets in one currency.

As noted earlier, in order to determine which country is more profitable to invest in real estate, it is necessary to

compare not only the values of the assumed foreign exchange risk, but also the overall profitability of these

investments and its correlation across countries (to use the advantages of diversification).

Accounting for exchange rate movements affects the correlation of real estate returns in the cities under

consideration, therefore, if the relationship turns out to be statistically significant at an acceptable level of

significance, economic agents need to

American Scientific Research Journal for Engineering, Technology, and Sciences (ASRJETS) (2021) Volume 79, No 1, pp 113-131

121

Table 3-6

profitability of investments in real estate in Minsk

Minsk

period

profitability of

real estate

profitability of real estate

taking into account the

exchange rate

profitability of real estate

taking into account the

exchange rate

and inflation

Yield, euro

1-st quart 07 39,25 % 43,42 % 42,92 % 2,99 %

2-nd quart 07 15,62 % 16,87 % 15,87 % 1,09 %

3-rd quart 07 3,62 % 9,30 % 9,10 % 5,47 %

4-th quart 07 -0,65 % 3,37 % 1,96 % 4,04 %

1-st quart 08 -3,52 % 3,00 % 2,00 % 6,76 %

2-nd quart 08 -2,24 % -3,28 % -4,69 % -1,06 %

3-rd quart 08 3,20 % -6,52 % -6,72 % -9,42 %

4-th quart 08 -0,98 % 0,55 % 1,05 % 1,55 %

profitability of investments in real estate in Nur-Sultan

Nur-

Sultan

Period

profitability of

real estate

profitability of real estate

taking into account the

exchange rate

profitability of real estate

taking into account the

exchange rate

and inflation

Yield, euro

1-st quart 07 – – –

2-nd quart07 – – –

3-rd quart 07 14,27 % 19,02 % 18,82 % 4,15 %

4-th quart 07 1,62 % 4,88 % 3,47 % 3,21 %

1-st quart 08 -36,20 % -31,50 % -32,50 % 7,37 %

2-nd quart 08 -10,42 % -10,82 % -12,22 % -0,45 %

3-rd quart 08 1,22 % -8,09 % -8,29 % -9,19 %

4-th quart 08 -8,32 % -8,89 % -8,39 % -0,62 %

profitability of investments in real estate in Kyiv

______________________________________________________________

Calculations were carried out using data on the cost of apartments in cities, presented in the sources [4 - 7].

Kyiv

period

profitability of

real estate

profitability of real estate

taking into account the

exchange rate

profitability of real estate

taking into account the

exchange rate

and inflation

Yield,euro

1-st quart 07 3,12 % 6,11 % 5,62 % 2,90 %

2-nd quart 07 3,70 % 4,62 % 3,62 % 0,89 %

3-rd quart 07 3,20 % 8,05 % 7,85 % 4,71 %

4-th quart 07 3,96 % 10,92 % 9,51 % 6,70 %

1-st quart 08 1,28 % 10,26 % 9,26 % 8,87 %

2-nd quart 08 1,26 % -3,18 % -4,58 % -4,39 %

3-rd quart08 2,81 % -6,09 % -6,29 % -8,65 %

4-th quart 08 -36,67 % -1,32 % -0,82 % 55,81 %

American Scientific Research Journal for Engineering, Technology, and Sciences (ASRJETS) (2021) Volume 79, No 1, pp 113-131

122

profitability of investments in real estate in Moscow

it should be taken into account when determining the objects of investment funds.

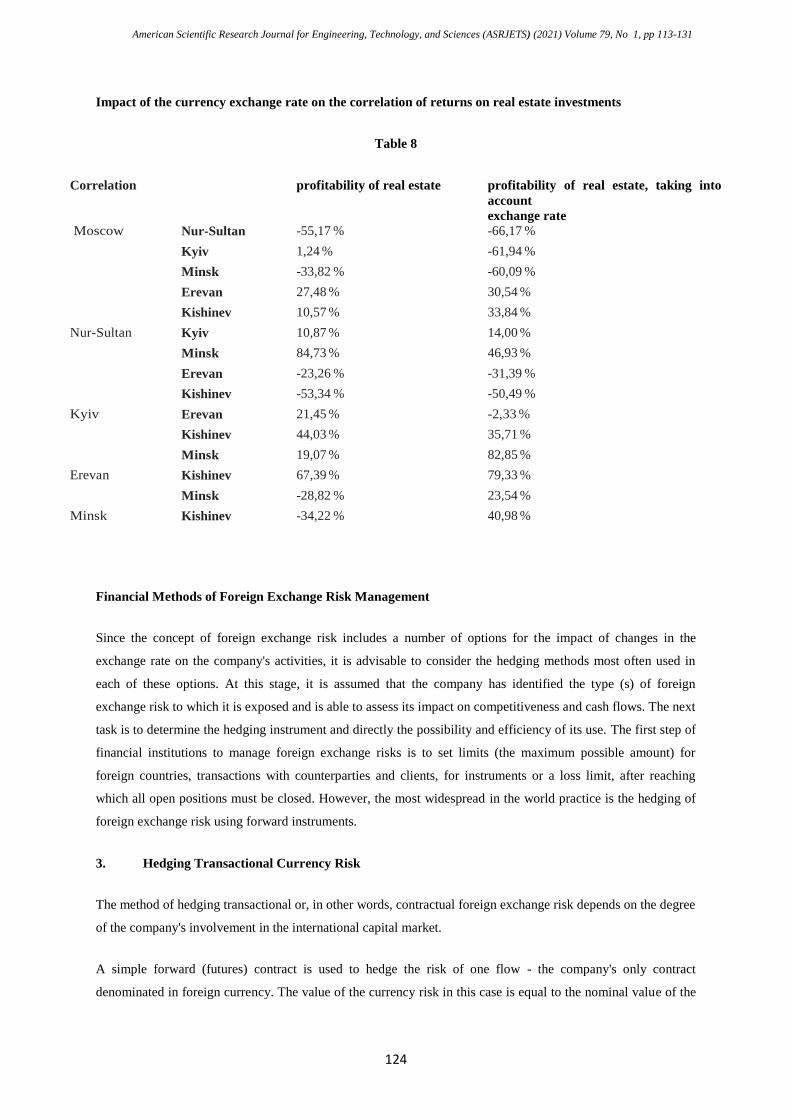

The results of the study of the correlation of profitability of investments in real estate with and without taking

into account

exchange rates show that, despite the possibility of reducing the currency risk with the diversification of

investments in housing in Moscow and Yerevan or Moscow and Chisinau, profitability on the real estate

markets of these countries is associated with a positive relationship, in contrast to the markets of Moscow -

Astana, Moscow - Minsk (taking into account dynamics of the exchange rate, the Moscow - Kiev pair is also

becoming attractive for investment). The significant negative correlation of the returns of the above markets

gives a signal to international investors that this combination can be chosen in order to reduce the risk of

investments in real estate.

Foreign exchange risk hedging

Over the past few decades, there has been an increase in the influence of foreign exchange risks on the activities

of organizations, as a result, approaches to assessing and managing foreign exchange risks have changed

significantly.

Initially, risk management was applied at the level of individual organizational units, and the main objective was

to reduce the costs caused by fluctuations in exchange rates. Today, both short-term and long-term foreign

exchange risk management is carried out throughout the organization, using financial and non-financial

strategies for hedging foreign exchange risks.

___________________________________________________________________________

Data on the exchange rates of the currencies of the CIS countries against the euro. Site of the CIS Statistical

Committee [8].

Moscow period profitability of

real estate

profitability of real estate

taking into account the

exchange rate

profitability of real estate

taking into account the

exchange rate

and inflation

Yield, euro

1-st quart 07 -9,89 % -9,11 % -9,61 % 0,87 %

2-nd quart 07 -3,91 % -4,87 % -5,87 % -1,00 %

3-rd quart 07 -3,49 % -2,33 % -2,53 % 1,20 %

4-th quart 07 1,79 % 3,46 % 2,06 % 1,64 %

1-st quart 08 11,22 % 13,99 % 12,99 % 2,49 %

2-nd quart 08 13,43 % 13,49 % 12,09 % 0,05 %

3-rd quart 08 15,56 % 15,05 % 14,85 % -0,44 %

4-th quart 08 6,70 % 26,19 % 26,69 % 18,26 %

American Scientific Research Journal for Engineering, Technology, and Sciences (ASRJETS) (2021) Volume 79, No 1, pp 113-131

123

correlation of exchange rates of currencies of cis countries, euro[8]

Table 7

Correlation

American Scientific Research Journal for Engineering, Technology, and Sciences (ASRJETS) (2021) Volume 79, No 1, pp 113-131

124

Impact of the currency exchange rate on the correlation of returns on real estate investments

Table 8

Correlation profitability of real estate profitability of real estate, taking into

account

exchange rate

Moscow Nur-Sultan -55,17 % -66,17 %

Kyiv 1,24 % -61,94 %

Minsk -33,82 % -60,09 %

Erevan 27,48 % 30,54 %

Kishinev 10,57 % 33,84 %

Nur-Sultan Kyiv 10,87 % 14,00 %

Minsk 84,73 % 46,93 %

Erevan -23,26 % -31,39 %

Kishinev -53,34 % -50,49 %

Kyiv Erevan 21,45 % -2,33 %

Kishinev 44,03 % 35,71 %

Minsk 19,07 % 82,85 %

Erevan Kishinev 67,39 % 79,33 %

Minsk -28,82 % 23,54 %

Minsk Kishinev -34,22 % 40,98 %

Financial Methods of Foreign Exchange Risk Management

Since the concept of foreign exchange risk includes a number of options for the impact of changes in the

exchange rate on the company's activities, it is advisable to consider the hedging methods most often used in

each of these options. At this stage, it is assumed that the company has identified the type (s) of foreign

exchange risk to which it is exposed and is able to assess its impact on competitiveness and cash flows. The next

task is to determine the hedging instrument and directly the possibility and efficiency of its use. The first step of

financial institutions to manage foreign exchange risks is to set limits (the maximum possible amount) for

foreign countries, transactions with counterparties and clients, for instruments or a loss limit, after reaching

which all open positions must be closed. However, the most widespread in the world practice is the hedging of

foreign exchange risk using forward instruments.

3. Hedging Transactional Currency Risk

The method of hedging transactional or, in other words, contractual foreign exchange risk depends on the degree

of the company's involvement in the international capital market.

A simple forward (futures) contract is used to hedge the risk of one flow - the company's only contract

denominated in foreign currency. The value of the currency risk in this case is equal to the nominal value of the

American Scientific Research Journal for Engineering, Technology, and Sciences (ASRJETS) (2021) Volume 79, No 1, pp 113-131

125

firm's contract, and it is for this amount that the currency is purchased, in which the transaction price is fixed, by

forward, that is, with payment at a fixed price after a certain period of time[4]. When hedging the risk of several

cash flows with different maturities, it is advisable to purchase a single forward contract for the amount of the

total cash flow, taking into account the time value of money and the possibility of changes in interest rates in the

period to maturity of the contracts. The time value of money is accounted for by discounting all of the

company's cash flows to one point in time, and interest rate risk is insured by choosing the correct duration for

the hedging contract, equal to the duration of the cumulative cash flow. It is also possible to hedge all cash

inflows with one forward contract and all outflows of the company with another. This becomes especially

important when the timing of the inflow and outflow of funds does not coincide. In this case, the procedures for

discounting and calculating the duration are carried out separately for positive and negative cash flows and for

each currency. If there are no long-term forward contracts in the market, then the contract with the longest

available term should be used and the capitalized value of all cash flows that will arise after the contract expires

should be hedged. Foreign exchange risk cannot be eliminated completely, but to minimize it, it is necessary to

constantly adjust the used hedging scheme and monitor changes in the duration of cash flows and forward

contracts, which may differ.

___________________________________________________________________________

A futures contract is a unified (exchange) contract that establishes a firm commitment to buy or sell in the

future a standard amount of an asset at a price agreed between the parties. A forward contract is a similar OTC

instrument [1].

It may also be advisable to use money market instruments: take a loan in “home” currency in case of accounts

payable or foreign currency in case of receivables, convert it and invest at interest before settling the contract.

In order not to be bound by the obligation to execute a forward (futures) contract at an unfavorable price,

companies use another risk hedging instrument - an option. Options are exercised only when it is beneficial to

the buyer and provide an opportunity to choose the desired degree of hedging, since they can have different

strike prices (strike prices are higher or lower than the asset price). The cost (premium) paid for an option

consists of two components: intrinsic value - the difference between the current value of the underlying asset

and the price of the strike option - and time value - the excess of the market price of an option by its intrinsic

value5. The underlying asset in hedging foreign exchange risk is the exchange rate.

In practice, hedging strategies are possible in which several options with different strike prices are used

simultaneously. However, it is important to understand that for the buyer an option is a right, and for the seller it

is an obligation to make a deal at a predetermined price, therefore, calculations of the effectiveness of the

strategy should be carried out by specialists. Brokerage commissions for a transaction and costs of holding an

option (the possibility of placing money simply on a deposit account) are also taken into account when deciding

whether to hedge currency risk.

American Scientific Research Journal for Engineering, Technology, and Sciences (ASRJETS) (2021) Volume 79, No 1, pp 113-131

126

Swaps can also be used as a financial instrument for hedging foreign exchange risk. A currency swap is the

exchange of payment obligations denominated in one currency for payment obligations denominated in another

currency. Usually the deal is concluded with the condition of the subsequent buyback (but participation of more

than two counterparties is possible), ie. there are two opposite conversion transactions: the exchange of

currencies now at the spot rate and on a certain date in the future at the forward rate. The parties entering into a

currency swap exchange risks by fixing the future exchange rate of the transaction. This method of hedging does

not create an uncovered foreign exchange position, since the volumes of claims and liabilities in foreign

currency are the same [3].

Hedging of operational foreign exchange risk

The assessment and hedging of operational foreign exchange risk is carried out by identifying cash flows that

depend on changes in the exchange rate under different possible exchange rate scenarios. After determining the

forecast changes in the amount of cash flows in response to exchange rate fluctuations, a decision is made to

buy or sell, for example, a forward contract. To more accurately determine the dependence of a firm's cash

flows on the exchange rate, one can separately consider all components of the profit and loss statement, taking

into account their correlation, and use not only projected income data, but also reporting for past periods.

When using a financial hedging strategy for operational currency risk, it is possible to use both derivatives and

manage the currency structure of debt obligations - creating long-term flows of the opposite direction.

In case of hedging risk with a currency swap for counterparties, the swap hedges cash flows in foreign currency

that they plan to receive during the next periods before the expiration of the contract. The scheme of this swap

provides for the exchange of currencies (borrowings in national currency) in the initial and final periods of time

and the payment of interest in foreign currency at a predetermined price every six months or a year by both

counterparties. At its core, this transaction is a series of forward contracts with a predetermined exchange rate,

but here you can save on commissions and finding an interested counterparty. Separately, when hedging

operational currency risk, options can be used, including strategies with the simultaneous purchase of several

futures contracts at once. The effectiveness of hedging in this case is determined in the same way as when

insuring transaction risk.

Accounting and management of other types of foreign exchange risk: translation risks, conversion risks.

Along with the previously listed companies, in their activities, they also face other types of currency risk, which

must also be taken into account when forming a strategy and tactics for business development. These are

translation and conversion risks. Most often, these risks are not hedged separately, but if there is a certain trend

in the exchange rate change, the company's value and its profitability may have negative dynamics. Unlike

transactional risk, it is actual, not unexpected, fluctuations in the exchange rate that matter.

Exchange rate or conversion risks are the most unpredictable and least manageable among currency risks. These

include possible changes in the foreign exchange policy of states, including restrictions on operations in foreign

currency, the degree of its convertibility. To a large extent, the assessment of this risk is based on international

American Scientific Research Journal for Engineering, Technology, and Sciences (ASRJETS) (2021) Volume 79, No 1, pp 113-131

127

ratings, but their independence and adequacy in times of crisis is questionable.

Hedging foreign exchange risk during a crisis and its cost

According to experts, the adjustment of income for the exchange rate in 2008 accounted for 30 to 40% of the

total amount of income, so many companies began to more extensively apply strategies for hedging foreign

exchange risk. However, the problem they faced was the high credit risks of counterparties, whose the ratings

dropped significantly during the crisis. According to statistics, futures during this period were significantly less

liquid than forwards, and the most fairly priced are foreign exchange options, which allow the option to be

exercised only in a favorable situation for the buyer.

The cost of hedging depends on several factors:

• interest rates and type of yield curve;

• the duration of the contract;

• supply and demand in the derivatives market;

• macroeconomic situation.

Table 9

Risk hedging cost EUR / USD

Data are presented in basis points (one hundredth of a percent) Source: [2].

Non-financial methods of foreign exchange risk management

Initially, it is assumed that the price of a futures contract is based on the condition that there is no arbitrage, that

is, the possibility of risk-free profit. This forms the estimated price of the contract, but the action of market

American Scientific Research Journal for Engineering, Technology, and Sciences (ASRJETS) (2021) Volume 79, No 1, pp 113-131

128

factors affects the real price of the transaction (see figure).

Recently, the cost of hedging has decreased as companies can sell out of the money options 7 at a higher price

than during periods of low volatility in the markets. The use of derivatives is now more related to the desire to

reduce risks rather than to receive speculative income, however, the liquidity of this market has noticeably

decreased over the past year. During a period of high volatility,

We have become such market instruments as deposits in dual currency with increased interest rates, but

allowing banks to pay the amount of the deposit in any of the agreed currencies. There are products that allow

you to get additional income if the currency strengthens to a predetermined level for a certain period or

fluctuations in the exchange rate in some interval with the possibility of revising it every month.

Along with financial hedging methods

Companies often use non-financial mechanisms to mitigate currency risks. Some organizations shift foreign

exchange risk by concluding all contracts in the national currency or in different currencies with opposite trends

in exchange rates, while others share it between counterparties in the event that the exchange rate goes beyond a

certain zone. Foreign exchange clauses, implying different conditions for changing the value of the contract

depending on the prevailing exchange rate, allow companies to more accurately predict inflows and outflows

from such transactions and reduce their riskiness. In the context of globalization, organizations have gained an

additional opportunity to manage currency risks - using the advantages of diversification of both sources of raw

materials and production bases, and markets for products or services, which reduces their dependence on the

exchange rate of individual countries. Companies with subsidiaries can apply a strategy of balancing cash

inflows and outflows. To do this, they facilitate the organization of opposite cash flows from the subsidiary. It

becomes profitable to combine export and import activities to maintain cash flows in the face of exchange rate

volatility.

In practice, it is impossible to completely hedge the foreign exchange risk. Future cash flows are probabilistic

and actual payments may not be as expected. Derivatives contracts are concluded for a specific amount of cash

payments, therefore, if real payments turn out to be more or less, it is necessary to exchange a certain amount of

foreign currency at the spot rate at the time the money is received, which creates an additional foreign exchange

risk. In addition, changes in the volatility of exchange rates in the markets of resources, components, competing

organizations, as well as in the state monetary policy are not precisely predictable, which does not allow to

completely eliminate the currency risk.

It is optional to hedge the entire amount of the transaction, the so-called full hedging, which completely

excludes both possible losses and possible additional profits from changes in the price of the insured asset. If a

company expects only some of its cash flows to be highly dependent on changes in the exchange rate that would

adversely affect its operations, a partial hedging strategy is applied. However, this type of risk insurance is risky,

since there remains the possibility of incurring losses as a result of unfavorable changes in the exchange rate.

In the case of currency risks, the question of correlation between the exchange rate and the profitability of the

American Scientific Research Journal for Engineering, Technology, and Sciences (ASRJETS) (2021) Volume 79, No 1, pp 113-131

129

investment object remains interesting. Some studies have shown that, for example, in the period from 1975 to

2005. the euro, Swiss franc and the bi-currency basket of the US dollar and the Canadian dollar are negatively

correlated with the stock market, which opens up additional opportunities for investment diversification [10].

The economists' particular attention was also drawn to the choice of hedging instruments for different directions

of flows of funds in foreign currency. In the period from April 2004. to March 2008 Currency inflows were

beneficial to hedge with forward contracts in case of currency depreciation and swaps in case of cyclical

fluctuations in the exchange rate, and outflows - with the help of options regardless of exchange rate

movements. While strengthening the currency, the analysis did not reveal the advantages of any strategy of

hedging inflows, since the expected profitability of the transaction was comparable in all the cases considered

[11].

Hedging foreign exchange risk in real estate investments

Investments in real estate in comparison with traditional types of investments are less liquid and most often

long-term. Therefore, it is very difficult to fully hedge the risks of international real estate investments. For

institutional of players, such assets are simply part of the global portfolio and are hedged within it. Individual

investors face a number of challenges. First, you need to decide which cash flow will be hedged: the initial

investment, recurring (lease) payments, or the selling price of the asset at the end of the period. Since the first

two streams are already determined at the time of real estate purchase, a swap contract can be concluded to

insure currency risk by this amount. However, the final cash flow is difficult to predict, and therefore the full

hedging strategy requires additional calculations. There are models based on historical data on the values of

variables that significantly affect the risk and return of real estate investments, but a predictive approach based

on simulations is preferred. This approach treats rental payments, exchange rate and interest rates as random

values. The effectiveness of a hedging strategy is determined by comparing the average of the net present value

of investments, taking into account different scenarios, with net present value without hedging. Research has

shown that while the use of swaps reduces the likelihood of generating additional income from a transaction, it

significantly reduces the risk of adverse exchange rate movements and negative net present value. However,

there are additional hedging costs and difficulties in finding a fixed-term contract for the required period of

time. With regard to hedging cash flow from real estate sales, its effectiveness largely depends on the liquidity

of this market. Since, if the deal is not concluded within a predetermined period, there may be a gap between the

duration of the futures contract and the inflow of funds, which increases the currency risk of the deal. If

possible, it is better to reduce the risk of investing in real estate by diversifying investments among the markets

of different countries, whose exchange rates and, more importantly, the return on investments, taking into

account the exchange rate in the real estate market, are negatively correlated.

In conclusion, it should be noted that foreign exchange risk is only one of the risks that organizations face in

their activities, but its impact is significant and can often be underestimated. During the developing global

financial crisis, volatility exchange rates increased and became one of the determining factors in choosing an

object of investment and a mandatory parameter in the assessment and management of risks by economic

agents.

American Scientific Research Journal for Engineering, Technology, and Sciences (ASRJETS) (2021) Volume 79, No 1, pp 113-131

130

Conducting labor-intensive calculations on the organization's exposure to foreign exchange risk has become not

just a procedure for reporting to regulators or determining the profitability of speculative transactions, but also a

necessity for further successful functioning and developing a strategy and tactics for business development.

Along with the applied mathematical models of risk assessment, during a crisis, it is important to have expert

opinion, which combines both the conclusions of various models and past experience and analysis of trends that

were not taken into account in the basic premises.

There are several ways to mitigate foreign exchange risk: the use of derivatives and money market instruments

and non-financial strategies. The choice of the most optimal of them depends on the conditions of doing

business, cost, market access (derivatives, loans, other countries) and its liquidity, company policy. It is

important not to underestimate the impact of the exchange rate on the organization's activities and constantly

adjust the risk hedging mechanisms used. This minimizes losses from unfavorable changes in the exchange rate

and helps to strengthen the company's position in the market and maintain competitive advantages.

List of references:

[1] .Glossary of options. URL: http://www. perfekt. ru/invest/option.html (date of access:

02/15/2021).

[2].Daily review of the debt market URL:

http://www.akbf.ru/ftproot/files/reports/Daily%20FI/2009/2009_03_06_Daily_fi.pdf (date of

access: 02/15/2021).

[3]. Hedging foreign exchange risks using swaps.URL:http://bankir. ru/analytics/classic/ valuta/171120

(date of access: 02/23/2021).

[4]. Statistics of prices for apartments in Kiev. URL:http:// www.svdevelopment.com/ru/web/flat_costs/

(date of access: 02/23/2021).

[5]. Analysis of the real estate market in Kishinev for 2008. URL:http://www.lara.md/?m=page&id=2

(date of access: 02/23/2021).

[6]. Review of the residential real estate market in Minsk for 2008. URL:http://www.t-s.by (date of access:

02/23/2021).

[7]. Real estate in Moscow. URL: www. irn. ru (date of access: 02/23/2021).

[8]. Exchange Rates of National Currencies Established of National (Central) Banks of the Countries of

the Commonwealth of Independent States. URL: http://www.cisstat.com/eng/macro_an.htm (дата

обращения: 15.03.2009).

[9]. Addae-Dapaah, Kwame, Tan Yong Hwee, Wilfred. The unsung impact of currency risk on the

American Scientific Research Journal for Engineering, Technology, and Sciences (ASRJETS) (2021) Volume 79, No 1, pp 113-131

131

performance of international real property investment// Review of Financial Economics,

Jan2009, Vol. 18 Issue 1, P. 56–65.

[10]. Campbell John Y., Karine Serfaty-de Medeiros, Luis M. Viceira. Global Currency Hedging, 2007.

[11]. Narendra Babu, Mahesh Kodagi, Vivekanand B. Y. An Empirical Study of FOREX Risk

Management Strategies. Indian Journal of Finance, Vol. II, № 8, Dec. 2008.

[12]. Woon K. Wong, Laurence Copeland. Risk Measu- rement and Management in a Crisis-Prone

World/ Cardiff Business School, 2008.