Embed Size (px)

Citation preview

CURRENCIES

Currency Market Monitor 1st Quarter 2014

APRIL 3, 2014

John W. Labuszewski Sandra Ro Bluford Putnam

Managing Director Executive Director Chief Economist

Fin’l Research & Product Development

312-466-7469

FX Research & Product Development

011 (44) 203-379-3789

Research & Product Development

212-299--2302

1 | Currency Market Monitor 1st Quarter 2014 | April 3, 2014 | © CME GROUP

An ongoing debate has long persisted in the global

currency or FX markets – is FX an “asset class” akin

to stocks and bonds? While practitioners and

academics may debate this point at length, perhaps

the most practical answer is – does it really matter

provided that investors may draw a return from

currency investments?

The performance of the currency or FX markets is

found in the exchange rates and cross-rates

associated with the world’s myriad currencies. The

total return associated with a currency is driven by

interest income associated with fixed income

instrument investment in the particular currency; as

well as pure price performance.

Many fundamental factors, including national

economic conditions, monetary and policies, current

and capital account flows, to name just a few,

impact the returns associated with the world’s

currencies.

This document represents a review of these factors

as they played out in the most recently completed

calendar quarter. We include consideration of the

so-called “carry trade” as well as a look at the

theory of “purchasing power parity” as it impacts FX

markets.

While we cover activity in a broad spectrum of

currencies, we focus on the currencies underlying

some of the most liquid of CME Group FX futures.

This includes the U.S. dollar (USD), Euro (EUR),

Japanese yen (JPY), British pound (GBP), Swiss

franc (CHF), Canadian dollar (CAD), Australian dollar

(AUD) and Mexican peso (MXN).

In addition, we have special interest in the

currencies of significant emerging market economies

including the Brazilian real (BRL), Russian ruble

(RUB), Indian rupee (INR) and Chinese yuan or

renminbi (CNY) – the so-called “BRIC” nations.

Finally, we highlight several CME Group FX Indexes

including a USD Index, a Carry Trade Index,

Commodity Country Index and BRIC Index.

Market Fundamentals

As a general rule, FX analysts will evaluate the

fundamental value of any particular currency by

reference to a number of national economic factors.

These factors including growth and inflation

prospects; monetary and fiscal policies; and, current

and capital account balances.

To illustrate, we include a brief discussion of the

economic situation prevailing in the United States as

of the conclusion of the most recently completed

calendar quarter. Of course, the U.S. dollar (USD)

may be just one side of any currency pair that may

be traded using CME FX futures.

A brief summary of economic conditions in various

nations, organized along similar lines, is included in

Appendix 1 of our document below. One may

compare and contrast these conditions as they exist

in the two countries whose currency pairing one may

be interested in to draw an appreciation of the

fundamental factors that impact currency markets.

Growth and Employment

The 1st calendar quarter of 2014 was marked by

mixed economic results. On the one hand, economic

growth appears to have slowed as a result of

seasonally inclement weather. The housing market

seems to be in a stall pattern while fiscal policy may

be putting on the brakes. On the other hand, labor

markets show signs of improvement while consumer

spending is reasonably strong.

Concerns regarding tensions in the Crimea and a

general slowdown in the emerging markets likewise

played a role in shaping the character of 1st quarter

results.

The Fed summarizes the domestic situation nicely …

“growth in economic activity slowed during the

winter months, in part reflecting adverse weather

conditions. Labor market indicators were mixed but

on balance showed further improvement. The

unemployment rate, however, remains elevated.

Household spending and business fixed investment

continued to advance, while the recovery in the

housing sector remained slow. Fiscal policy is

restraining economic growth, although the extent of

restraint is diminishing. Inflation has been running

below the Committee’s longer-run objective, but

longer-term inflation expectations have remained

stable.” 1

1 Federal Reserve Press Release dated March 19, 2014.

2 | Currency Market Monitor 1st Quarter 2014 | April 3, 2014 | © CME GROUP

GDP was reported at +2.6% in the 4th quarter but

slipped from the 3rd quarter’s recent peak at +4.1%.

This growth drove the February unemployment rate

down to 6.7%, an uptick from January’s 6.6% but a

1% improvement from the 7.7% reported a year

earlier in February 2013. These levels are

approaching the 6.5% rate cited in the Fed’s

previous forward guidance regarding the trigger for

a tighter monetary policy.

While this represents improvement, labor force

participation remains at anemic levels of only 63.0%

in February 2014 and at levels not seen since the

late 1970s.

Further, the total number of employed at 137.699

million as of February 2014 remains less than the

pre-financial crisis peak of 138.056 million seen in

January 2008. This means that we have now seen

73 months pass by without recovering to exceed

pre-crisis levels. This represents the most extended

recovery from recession by a wide margin during the

past 35 years.

Still, the Fed is encouraged and “expects that, with

appropriate policy accommodation, economic activity

will expand at a moderate pace and labor conditions

will continue to improve gradually, moving toward

those the Committee judges consistent with its dual

mandate” of fostering maximum employment and

price stability. 2

The Fed’s most recent statement alluded to

advances in household spending. However, this is

not borne out by an examination of data regarding

either retail sales or light vehicle sales.

Retail sales slipped 1.2% to $181.651 billion during

February 2014 from a November 2013 peak of

$183.779 billion. Similarly, sales of cars and light

trucks fell 6.3% to 15.275 million units in February

2014 from the November peak of 16.309 million

units. Still, the longer-term trend has been steadily

pushing upwards since the major trough seen in

early 2009.

A general propensity to loosen the purse strings is

reflected in the personal savings rate. The rate

appears generally to be drifting downwards and was

reported at 4.3% in February 2014 after drifting up

in the wake of the financial crisis. Note, however,

that this does not fully reflect the complete winter

2 Ibid.

4%

5%

6%

7%

8%

9%

10%

11%

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

Q1 0

5

Q4 0

5

Q3 0

6

Q2 0

7

Q1 0

8

Q4 0

8

Q3 0

9

Q2 1

0

Q1 1

1

Q4 1

1

Q3 1

2

Q2 1

3

Q1 1

4

Unem

plo

ym

ent

Rate

Qtr

ly C

hange in G

DP

Growth and Employment

Real GDP (SA) Unemployment Rate

Source: Bureau of Economic Analysis (BEA) & Bureau of Labor Statistics (BLS)

62%

63%

64%

65%

66%

67%

68%

4%

5%

6%

7%

8%

9%

10%

11%

Jan-0

2

Jan-0

3

Jan-0

4

Jan-0

5

Jan-0

6

Jan-0

7

Jan-0

8

Jan-0

9

Jan-1

0

Jan-1

1

Jan-1

2

Jan-1

3

Jan-1

4

Labor

Forc

e P

art

icip

ation

Unem

plo

ym

ent

Rate

Employment Statistics

Unemployment Rate Labor Force Partcipation

Source: Bureau of Labor Statistics (BLS)

93%

94%

95%

96%

97%

98%

99%

100%

101%

1 5 9

13

17

21

25

29

33

37

41

45

49

53

57

61

65

69

73

NFPs a

s %

of Peak

Months Since Peak NFP

NFP Recovery from Recession

Apr - Dec-80 Aug-81 - Oct-83Jul-90 - Jan-93 Mar-01 - Jan-05Feb-08 -

3 | Currency Market Monitor 1st Quarter 2014 | April 3, 2014 | © CME GROUP

weather experience, which has certainly diminished

or possibly just deferred consumer spending.

While consumer spirits seem to have been

dampened by unseasonably cold weather, the

industrial sector has shown further advances. The

Index of Industrial Production was reported at

101.6276 in February 2014. This is 2.8% above the

February 2013 mark and represents a new peak,

advancing above pre-crisis levels.

Similarly, capacity utilization is on the upswing,

reported at 78.8% in February 2014. This is just a

bit off of the 78.9% from November 2013 but

decidedly above the 78.2% reported a year earlier in

February 2013. The figure is rising but remains a bit

below the key 80% mark at which point many

economists believe that inflationary pressures may

be expected to be observed.

This activity is reflected in domestic corporate

profitability which is deep into all-time high territory.

The Department of Commerce reported $1,904.5

billion in 4th quarter profitability or +6.0% on a

year-on-year basis. Some analysts suggest that this

profitability is primarily responsible for the new all-

time highs recorded in equities – while others point

to low rates held in place by QE programs.

The Fed further remarked upon slowness in the

housing markets. This is underscored by slight dips

in housing values in Chicago, Boston and Los

Angeles in January 2014 from the prior month. Still,

gains were shown in Miami, Washington and San

Francisco. Further, the S&P/Case-Shiller 10-City

Composite index held its ground in January and as

advanced 13.54% on a year-on-year basis and

22.96% since the trough of March 2012.

9

10

11

12

13

14

15

16

17

$155

$160

$165

$170

$175

$180

$185

$190

Jan-0

7

Aug-0

7

Mar-

08

Oct-

08

May-0

9

Dec-0

9

Jul-

10

Feb-1

1

Sep-1

1

Apr-

12

Nov-1

2

Jun-1

3

Jan-1

4

Vehic

le S

ale

s

Reta

il S

ale

s (

Bil $

)

Consumer Sector Activity

Real Retail Sales SA Light Vehicle Sales

Source: U.S. Census Bureau and Dept.of Commerce

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

Jan-0

7

Jul-

07

Jan-0

8

Jul-

08

Jan-0

9

Jul-

09

Jan-1

0

Jul-

10

Jan-1

1

Jul-

11

Jan-1

2

Jul-

12

Jan-1

3

Jul-

13

Jan-1

4

% o

f D

isposable

Incom

e

Personal Savings Rate

Source: St. Louis Federal Reserve FRED Database

66%

68%

70%

72%

74%

76%

78%

80%

82%

80

85

90

95

100

105

Jan-0

7

Aug-0

7

Mar-

08

Oct-

08

May-0

9

Dec-0

9

Jul-

10

Feb-1

1

Sep-1

1

Apr-

12

Nov-1

2

Jun-1

3

Jan-1

4

Capacity U

tilization

Industr

ial Pro

duction I

ndex

Industrial Sector Activity

Index of Industrial Production Capacity Utilization

Source: St. Louis Federal Reserve FRED Database

$600

$800

$1,000

$1,200

$1,400

$1,600

$1,800

$2,000

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

120%

Q1 0

4

Q4 0

4

Q3 0

5

Q2 0

6

Q1 0

7

Q4 0

7

Q3 0

8

Q2 0

9

Q1 1

0

Q4 1

0

Q3 1

1

Q2 1

2

Q1 1

3

Q4 1

3

Pre

-Tax P

rofits

(Billions)

Annualized C

hange

U.S. Corporate Profitability

Annual Change Corporate Profits (Bil)

Source: Department of Commerce

4 | Currency Market Monitor 1st Quarter 2014 | April 3, 2014 | © CME GROUP

But building permits, housing starts and housing

completions continue to hover in the vicinity of 900

thousand to 1 million units. This is a little less than

half of the peak pre-crisis era figures near 2.2

million units.

Inflation

The Fed concedes that inflation is well below their

long-term objectives. It further “recognizes that

inflation persistently below its 2 percent objective

could pose risks to economic performance, and it is

monitoring inflation developments carefully for

evidence that inflation will move back toward its

objective over the medium term.” 3

3 Ibid.

The seasonally adjusted read of the Consumer Price

Index (CPI) from February 2014 was at only 1.1%

with the CPI ex-food and energy holding up at 1.6%

on an annualized basis. These figures have

generally trended down over the past few years,

raising some concerns of deflation. Still, capacity

utilization at 78.8% and starting to challenge that

key 80% mark seems to support the Fed’s attitude

towards these risks.

Monetary Policy

The Fed’s quantitative easing (QE) programs called

for the purchase of some $85 billion of Treasuries,

agency debt and agency mortgage backed securities

(MBS) on a monthly basis, in an innovative attempt

to keep intermediate- to long-term rates at modest

levels. But the 4th quarter saw the Fed begin to

scale back or taper the program by $10 billion per

month.

Consistent with its judgment that “there is sufficient

underlying strength in the broader economy to

support ongoing improvement in labor market

conditions … [and] … in light of the cumulative

progress toward maximum employment and the

improvement in the outlook for labor market

conditions,” the Fed announced another $10 billion

round of tapering. Specifically, “beginning in April,

the Committee will add to its holdings of agency

mortgage-backed securities a a pace of $25 billion

per month rather than $30 billion per month, and

will add to its holdings of longer-term Treasury

securities at a pace of $30 billion per month rather

than $35 billion per month.” 4 Further tapering may

be expected contingent upon the pace of economic

recovery.

Tapering was further supported by updated Fed

projections of 6.1-6.3% unemployment in 2014,

down to 5.6-5.9% in 2015 and 5.2-5.6% in 2016. 5

Of course, the target Fed Funds rate has long been

the primary monetary policy tool. But the Fed

“reaffirmed its view that a highly accommodative

4 Ibid. 5 See Summary of Economic Projections of Board of

Governors of the Federal Reserve System, (March 2014).

80

120

160

200

240

280

320

Jan-0

0

Dec-0

0

Nov-0

1

Oct-

02

Sep-0

3

Aug-0

4

Jul-

05

Jun-0

6

May-0

7

Apr-

08

Mar-

09

Feb-1

0

Jan-1

1

Dec-1

1

Nov-1

2

Oct-

13

S&P/Case-Shiller Housing Indexes

Los Angeles San Diego San FranciscoDenver Washington DC MiamiChicago Boston Las VegasNew York Comp-10

Source: Standard & Poor's

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

6%

Jan-0

4

Jan-0

5

Jan-0

6

Jan-0

7

Jan-0

8

Jan-0

9

Jan-1

0

Jan-1

1

Jan-1

2

Jan-1

3

Jan-1

4

Year-

on-Y

ear

Change

Consumer Price Index (CPI)

CPI - All Urban Consumers SA CPI ex-Food & Energy SA

Source: Bureau of Labor Statistics (BLS)

5 | Currency Market Monitor 1st Quarter 2014 | April 3, 2014 | © CME GROUP

stance of monetary policy remains appropriate. In

determining how long to maintain the current 0 to ¼

percent target range for the federal funds rate, the

Committee will assess progress—both realized and

expected—toward its objectives of maximum

employment and 2 percent inflation … The

Committee continues to anticipate … that it likely will

be appropriate to maintain the current target range

for the federal funds rate for a considerable time

after the asset purchase program ends, especially if

projected inflation continues to run below the

Committee’s 2 percent longer-run goal, and

provided that longer-term inflation expectations

remain well anchored.” 6

Note that the Fed’s longer-run projection for PCE

inflation is reported at 2.0%.7 It is further

noteworthy that the Fed has backed away from

previous suggestions that it would consider more

aggressive action when unemployment reached

6.5% … “[w]ith the unemployment rate nearing 6-

1/2 percent, the Committee has updated its forward

guidance.” 8 Still, this is consistent with the Fed’s

indications from December 2013 to the effect “that it

likely will be appropriate to maintain the current

target range for the federal funds rate well past the

time that unemployment rate declines to 6-1/2

percent, especially if projected inflation continues to

run below the Committee’s 2 percent longer-term

goal.” 9

6 Op. cit., Fed Statement of March 19, 2014. 7 Op. cit., Summary of Economic Projections. 8 Op. cit., Fed Statement of March 19, 2014. 9 Ibid.

Fiscal Policy

Once more, the Fed acknowledges that “[f]iscal

policy is restraining economic growth, although the

extent of restraint is diminishing.”10 This is

underscored when we consider that Federal fiscal

deficits of $1.4, $1.3, $1.3 and $1.1 trillion in 2009-

12, respectively, shrunk to just $680 billion 2013.

Washington was able to avert another in a string of

chronic debt ceiling crises. Specifically, the Senate

approved a House measure on February 12th that

provides funding for Federal activities through March

2015.

It was hailed by President Obama who was “pleased

that Republicans and Democrats in Congress have

come together to pay for what they’ve already

spent, and remove the threat of default form our

economy once and for all.” He further expressed

hope that “this puts an end to politics by

brinkmanship.”

But this represented something of a blow to fiscal

conservatives including the Tea Party. House

Speaker John Boehner criticized the measure,

suggesting that “[i]t’s the President driving up the

debt and the President wanted to do nothing about

the debt that’s occurring … so, let his party give him

the debt ceiling increase that he wants.”

In further fiscal news, the deadline for signing up for

Obamacare was marked on Monday, March 31,

2014. An extension into April has been granted to

those who have experienced difficulty accessing the

10 Ibid.

0%

1%

2%

3%

4%

5%

6%

Jan-0

7

Jul-

07

Jan-0

8

Jul-

08

Jan-0

9

Jul-

09

Jan-1

0

Jul-

10

Jan-1

1

Jul-

11

Jan-1

2

Jul-

12

Jan-1

3

Jul-

13

Jan-1

4

Benchmark U.S. Rates

Target Fed Funds 2-Yr Treasury5-Yr Treasury 10-Yr Treasury30-Yr Treasury

-$1,600

-$1,400

-$1,200

-$1,000

-$800

-$600

-$400

-$200

$0

$200

$400

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Federal Surplus/Deficit(Billions USD)

Source: Office of Management and Budget (OMB)

6 | Currency Market Monitor 1st Quarter 2014 | April 3, 2014 | © CME GROUP

websites and signing up. Still, a reported 6 million

Americas have acquired health insurance since

October 1st through the Federal and State

exchanges. Still, we may expect debate on this

issue to be ongoing.

Current & Capital Account Flows

The 4th quarter 2013 current account deficit

improved further, reported at only $81.1 billion and

15.9% less than the $96.4 billion reported in the 3rd

quarter. This is less than the $86.982 billion deficit

reported in the 2nd quarter 2009 at the height of the

sub-prime crisis.

The total 2013 current account balance was reported

at only $360.7 billion and 2.2% of estimated 2013

GDP of $16.72 trillion. This is the most optimistic

figure seen for well over a decade.

Another interesting source of flow of funds data may

be found in the U.S. Treasury Department’s

Treasury International Capital (or “TIC”) database.

This database tracks flows into and out of the U.S.

The data is broken into foreign stocks, foreign

bonds, U.S. stocks, U.S. corporate bonds, U.S.

government agencies and U.S. Treasuries.

U.S. vs. overseas capital flows have generally been

characterized over the past decade by substantial

influx of funds into U.S. Treasuries. This

phenomenon peaked in 2010 as overseas investors

purchased some $704 billion in U.S. Treasuries on a

net basis. The figure tailed off to $433 and $417

billion in 2011 and 2012, respectively, but that still

represents sizable values.

But net inflows in U.S. Treasuries slowed to only

$42.88 billion in 2013. January 2014 actually saw a

net outflow of $0.57 billion. Interest in Treasuries

was replaced by large scale interest in U.S. equities

where foreign investors directed a net $522.20

billion into domestic markets. This remarkable shift

was obviously driven by fears of rising rates

alongside a continued strong surge in U.S. stocks.

Mutual Fund Flows

The flow of equity and fixed income investments

may be examined per data published by the

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

5.5%

6.0%

6.5%

-$900

-$800

-$700

-$600

-$500

-$400

-$300

-$200

-$100

$0

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

% o

f G

DP

Billions

US Current Account Balance

US Current Account % of GDP

-$800

-$400

$0

$400

$800

$1,200

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Jan-1

4

Net US/Foreign Capital Flows (Billions USD)

US Treasuries US Gov't Agencies US Corporates

US Stocks Foreign Bonds Foreign Stocks

Source: U.S. Treasury TIC Database

-$40

-$30

-$20

-$10

$0

$10

$20

$30

$40

Jan-1

2

Mar-

12

May-1

2

Jul-

12

Sep-1

2

Nov-1

2

Jan-1

3

Mar-

13

May-1

3

Jul-

13

Sep-1

3

Nov-1

3

Jan-1

4

Equity Fund Cash Flows (Billions USD)

Domestic Equities Foreign EquitiesSource: Investment Company Institute (ICI)

7 | Currency Market Monitor 1st Quarter 2014 | April 3, 2014 | © CME GROUP

Investment Company Institute (ICI) which tracks

activity in the mutual fund industry. 11

Investors added some $159.8 billion into equity

funds during the 2013. But only a scant $17.7

billion was directed into domestic equity funds,

despite their generally strong performance while

another $142.1 billion was added to foreign equity

funds. This trend continued in January through

February 2014 with another $43.3 flowing into

equity funds.

Funds had generally been flowing into bond funds

through May 2013. But June saw the reversal of

this trend as investors began to believe that interest

rate advances, fueled by economic growth and

expectations of tapering of Fed easing programs. By

the conclusion of 2013, some $80.5 billion had been

withdrawn from bond funds. But some $8.9 billion

flowed back into these markets in January through

February 2014.

Global Economic Performance

Emerging market (EM) economies have been the

stars of the investment world for some years now.

Still, it was the developed market (DM) economies

that provided some of the most positive growth

surprises in 2013. While the EM countries generally

exhibit higher growth rates than DM countries, that

11 These indicators are often highly correlated with price

action as retail investors may “chase” the market by buying in response to a bull trend. Or, they may exhibit a “herd mentality” by liquidating investments in response to significant market breaks.

growth has generally decelerated relative to DM

economies in recent years.

Actual and Forecast GDP Growth

2011 2012 2013

2014

(f)

2014

-19

(f)

2020

-25

(f)

Developed Markets (DMs)

Australia 3.4% 3.7% 2.7% 2.6% 2.3% 2.2%

Canada 2.5% 1.7% 1.4% 2.1% 2.0% 1.8%

France 2.0% 0.0% 0.2% 0.9% 1.4% 0.9%

Germany 3.3% 0.7% 0.4% 1.7% 1.6% 1.4%

Japan -.06% 1.9% 1.8% 1.5% 1.0% 0.6%

UK 1.1% 0.1% 1.3% 1.9% 1.9% 1.1%

US 1.8% 2.8% 1.9% 3.0% 2.4% 1.7%

Emerging Markets (DMs)

Brazil 2.7% 0.9% 2.0% 2.3% 2.9% 2.8%

Mexico 3.9% 3.8% 1.5% 3.1% 2.9% 3.1%

Russia 4.3% 3.4% 1.5% 2.5% 1.8% 1.2%

India 6.2% 5.0% 4.2% 4.4% 4.8% 2.6%

China 9.3% 7.7% 7.5% 7.0% 5.9% 3.5%

Source: The Conference Board Global Economic

Outlook 2014 (February 2014)

NOTE: (f) = forecast data

According to the Conference Board’s Global

Economic Outlook, growth in Germany is expected

to run at a very moderate +1.6% on an annual basis

from 2014-19. Similarly modest growth is expected

in much of the developed world including Japan

(+1.0%), the United Kingdom (+1.9%) and the

United States (+2.4%).

While GDP growth has slowed in many of the

emerging economies, such growth has nonetheless

generally surpassed that of the DMs. This is

expected to continue, according to Conference Board

forecasts, albeit the gaps may narrow.

Note that the trade surpluses that have supported

many emerging market economies are shrinking

along with trade deficits in the U.S. and Europe. As

discussed above, the U.S. current account deficit

shrank to 2.2% of GDP in 2013 from a peak deficit

of 5.76% in 2006. The Chinese trade surplus

similarly shrank from a peak of 11.00% of GDP in

2007 to 2.30% in 2013.

Arguably, these trade imbalances have been a

fundamental driving engine behind much emerging

market growth over the past several decades.

-$80

-$60

-$40

-$20

$0

$20

$40

Jan-1

2

Mar-

12

May-1

2

Jul-

12

Sep-1

2

Nov-1

2

Jan-1

3

Mar-

13

May-1

3

Jul-

13

Sep-1

3

Nov-1

3

Jan-1

4

Equity & Bond Fund Cash Flows (Billions USD)

Equity Funds Bond Funds

Source: Investment Company Institute (ICI)

1 | Currency Market Monitor 1st Quarter 2014 | April 3, 2014 | © CME GROUP

Price Performance

The factors discussed above exert an obvious impact

upon the price performance of the U.S. dollar vis-à-

vis other world currencies. In order to monitor this

price impact, CME Group has developed the “CME

USD Index” as one in a family of similarly

constructed FX Indexes. 12

The CME USD Index ended calendar year 2013 at a

value of 1,042.66 and remained virtually unchanged

over the course of the 1st quarter to end at

12 The CME USD Index represents a basket of equally

weighted positions (as of December 31, 2010) of the USD vs. the Euro (EUR), Japanese yen (JPY), British pound (GBP), Swiss franc (CHF), Canadian dollar (CAD), Australian dollar (AUD) and Chinese yuan (CNY). It is (arbitrarily) established at a value of 1,000.00 as of December 31, 2010.

1,0401.10. As such, the 1st quarter proved to be a

relatively quiet market in terms of price or spot

return performance.

The Euro generated a spot return of +0.25% vs. the

USD; the British pound (GBP) posted a return of

+0.76%; while the Japanese yen (JPY) was seen

+2.04% for the quarter, bouncing back a bit from its

-17.62% plunge during the course of 2013.

Mixed and more dramatic movements were seen

amongst emerging market currencies where the

Brazilian real (BRL) posted a spot return of +6.62%;

the Russian ruble weighed down by tensions in the

Crimea saw a spot return of -4.86%; the Indian

rupee (INR) was seen +9.25%; while the onshore

Chinese yuan or renminbi (CNY) posted a spot

return of -2.62%.

-1%

0%

1%

2%

3%

4%

5%

2010

2011

2012

2013

2014

14-1

9

20-2

5

Annual GDP Growth (Mature Economies)

Germany Japan UK US

Source: The Conference Board

-6%

-4%

-2%

0%

2%

4%

6%

2006

2007

2008

2009

2010

2011

2012

2013

Current Acct Balance (% GDP)(Mature Economies)

US Euro Area UK Japan

0%

2%

4%

6%

8%

10%

12%

2010

2011

2012

2013

2014

14-1

9

20-2

5

Annual GDP Growth(BRIC Economies)

Brazil Russia India China

Source: The Conference Board

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

2006

2007

2008

2009

2010

2011

2012

2013

Current Acct Balance (% GDP)(BRIC Economies)

Brazil Russia India China

2 | Currency Market Monitor 1st Quarter 2014 | April 3, 2014 | © CME GROUP

Note that we may distinguish the “spot return” of a

currency, or the outright price movements, from the

“total return” inclusive of price movements plus

interest accrual considerations, as discussed in more

detail below.

Total Return

One of the most popular long-term FX trading

strategies over the past decade is known simply as

the “carry trade.” This practice simply suggests

that one might exploit “cost of carry” by borrowing

in countries with low nominal interest rates to invest

in countries with high nominal interest rates. Thus,

one might sell the “low-rate” currency and buy the

“high-rate” currency.

Carry trade � Sell low-rate currency & buy high-rate currency

By so doing, one hopes to capitalize on discrepant

interest rates, and by implication, divergent

investment opportunities, in the two countries. This

strategy further recognizes that total currency return

consists of 2 components, specifically, exchange rate

or price movement plus the accrual of interest.

The implicit assumption is that these interest rate

relationships will endure. As such, carry traders

implicitly discount classical exchange rate theories

by assuming that the interest rate relationships may

endure over extended periods of time. This

suggests that low-yielding currencies that are sold

will not advance; and, that high-yielding currencies

that are purchased will not decline.

Total Currency Return

= Price Movement

+ Interest

Historically, such relationships have been known to

endure for extended periods of time, reinforcing

interest in the carry trade. In particular, vast sums

of money totaling in the trillions of U.S. dollars were

invested in the carry trade prior to the outbreak of

the subprime crisis, specifically by shorting the

Japanese yen (JPY) and investing in other currencies

including the Icelandic krona (ISK).

Appendix 2 depicts the total return associated with

various currencies, relative to the U.S. dollar, during

the most recently completed calendar quarter.

Amongst the mature economies, the EUR generated

a total return of +0.25% for the quarter; the GBP at

+0.76%; and, the JPY was at +2.04%. To the

extent that interest rates remain at near zero levels

in these mature economies, the total returns are not

much different than spot returns as reported above.

But interest accruals may exert a much greater

influence in less mature economies. The BRL posted

a total return of +6.62% for the 1st quarter; the RUB

was seen at -4.86%; the INR at +5.57%; and, the

CNY at -2.33%.

The Argentine peso (ARS) generated a spot return of

-18.53% for the quarter. But the total return was

much more muted at -7.57% as a result of the

extremely high prevailing 3-month rate of 29.20%.

Because the carry trade has become such an

important and widely followed transaction in the

900

950

1,000

1,050

1,100

1,150

1,200

1,250

Jan-0

7

Jul-

07

Jan-0

8

Jul-

08

Jan-0

9

Jul-

09

Jan-1

0

Jul-

10

Jan-1

1

Jul-

11

Jan-1

2

Jul-

12

Jan-1

3

Jul-

13

Jan-1

4

CME USD Index

Long Short14.3% EUR 100% USD14.3% JPY14.3% GBP 14.3% CHF 14.3% CAD14.3% AUD14.3% CNY

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

USD-ARSUSD-RUBUSD-CADUSD-CLPUSD-CNYUSD-TWDUSD-COPUSD-KRW

USDEUR-USDUSD-MXNUSD-ZARGBP-USDUSD-CHFUSD-JPYUSD-TRYUSD-ISK

AUD-USDUSD-INRNZD-USDUSD-BRL

Carry Return (Q1 2014)

3 | Currency Market Monitor 1st Quarter 2014 | April 3, 2014 | © CME GROUP

global FX markets, CME Group has developed the

CME FX Carry Index.

This novel index is designed to follow the

performance of a basket of currencies that offer

relatively high interest rates and have, on an

historical basis, generated favorable total returns. 13

The CME FX Carry Index closed the 1st quarter at

828.38 and +2.49% from its 2013 ending value of

808.21. This reflects the generally good

performance of the BRL (total return = +6.62%),

AUD (+4.58%), NZD (+6.26%) and TRY (+3.06%)

during the 1st quarter.

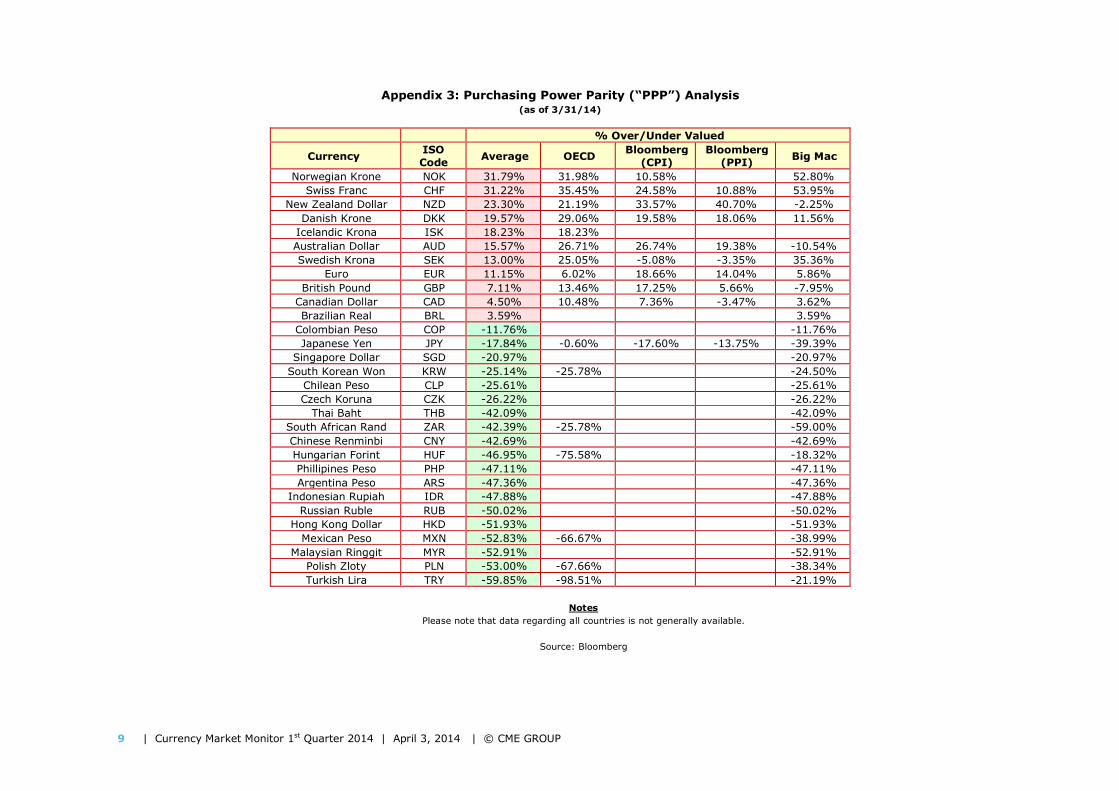

Purchasing Power Parity

The theory of purchasing power parity (PPP) dates to

the 16th century and the School of Salamanca but

was further developed in the early 20th century by

economist Gustav Cassel. 14 The theory is based

upon the assumption that exchange rates are in

13 The CME FX Carry Index represents a basket of equally

weighted positions (as of December 31, 2010) which is effectively long a basket including the Australian dollar (AUD), Brazilian real (BRL), Mexican peso (MXN), New Zealand dollar (NZD), South African rand (ZAR) and Turkish lira (TRY) vs. short positions in the USD and EUR. It is (arbitrarily) established at a value of 1,000.00 as of December 31, 2010. The long components of the CME FX Carry Index were selected in light of the high local interest rates that prevailed in those countries during the post-financial crisis era through 2010. The short components of the index were identified because of the low interest rates offered.

14 See Cassel, Gustav, “Abnormal Deviations in International Exchanges” (December 1918).

equilibrium when purchasing power is equivalent in

the two countries.

On a granular level, PPP is based on the “law of one

price” or the notion that identical products should be

priced at the same level in different national markets

adjusted for exchange rates. Typically, this law is

qualified by the absence of significant trade barriers

or other artificial constraints on commerce.

But the theory of PPP expands the application of the

law of one price from any single good or product to

generalized prices in any particular economy as

measured by inflation indexes, e.g., Consumer Price

Index (CPI) or Producer Price Index (PPI). The

implication of this theory is that inflation rates and

exchange rates should exhibit negative correlation.

If inflation increases

� Currency value should decline

If inflation decreases

� Currency value should advance

Thus, if inflation as measured by an inflation index

increases, the value of the currency should generally

decline to maintain price equilibrium. Similarly, if

inflation declines, the value of the currency should

advance.

The theory of PPP is closely related to another

classic theory that addresses exchange rate values

known as the International Fisher Effect (IFE). This

theory suggests that the disparity between nominal

interest rates in two countries drive the future path

of exchange rates.

Per this theory, one might expect that the value of a

currency with a low nominal interest rate might

increase into the future. Or that the value of a

currency with high nominal rate might decline.

IFE further assumes that real interest rates (i.e., the

risk-free interest rate less inflation) should generally

be equal across countries. This implies that nominal

interest rates and inflation are positively correlated.

If inflation increases

� Rates

increase �

Currency value should decline

If inflation decreases

� Rates

decrease �

Currency value should advance

700

750

800

850

900

950

1,000

1,050

Jan-0

7

Jul-

07

Jan-0

8

Jul-

08

Jan-0

9

Jul-

09

Jan-1

0

Jul-

10

Jan-1

1

Jul-

11

Jan-1

2

Jul-

12

Jan-1

3

Jul-

13

Jan-1

4

CME FX Carry Index

Long Short16.7% BRL 50% USD16.7% AUD 50% EUR16.7% ZAR 16.7% NZD16.7% TRY16.7% MXN

4 | Currency Market Monitor 1st Quarter 2014 | April 3, 2014 | © CME GROUP

The IFE suggests interest rates and exchange

negatively correlated. Similarly, PPP suggests

inflation and exchange rates are negatively

correlated. As such, the IFE theory is generally

consistent with the PPP theory.

Putting the classic theory of purchasing power parity

into practice requires a measurement of inflation in

order to calculate the proportion by which any

particular currency is (theoretically) over- or under-

valued relative to the norm. There are three popular

methodologies that have been referenced in this

regard.

• OECD - The Organization for Economic Co-

operation and Development (OECD) provides data

that is useful in this regard by comparing price

changes in a representative basket of goods in

various countries.

• Bloomberg - Bloomberg offers an analytical tool

that is grounded in a very long-term assessment

of inflation, as measured by either CPI or PPI in

various countries extending from January 1982

through June 2000.

• Big Mac - Finally, the Economist’s “Big Mac PPP”

methodology compares the price of a (almost)

universally available product with verifiable pricing

in the form of the McDonald’s Big Mac hamburger

in various countries.

All three methodologies may readily be referenced

on Bloomberg quotation devices. Appendix 3 below

provides data from all three methods. Further, we

have taken the average of the three assessments

(where available) for a variety of national currencies

and rank-ordered the set from most over-valued to

most under-valued.

The Norwegian krone (NOK) stands out as the most

over-valued currency per this analysis at +31.79%.

The NOK is followed by the Swiss franc (CHF) at

+31.22%; the New Zealand dollar (NZD) at

+23.30%; the Danish krone (DKK) at +19.57%;

and, the Icelandic krona (ISK) at +18.23%.

Under-valued currencies, per our analysis, include

the Turkish lira (TRY) at -59.85%; the Polish zloty

(PLN) at -53.00%; the Malaysian ringgit (MYR) at -

52.91%; the Mexican peso (MXN) at -52.83%; and,

the Hong Kong dollar (HKD) at -51.93%.

One might generally recommend creating “baskets”

of several currencies to buy and sell on the basis of

this analysis in order to diversify risks to a certain

extent. However, it is important to recognize that

currencies might remain in apparent states of over-

or under-valuation for extended periods of time. In

fact, the carry trade, as discussed above, takes a

completely opposite approach to the classic PPP

theory by buying high-rate currencies and shorting

low-rate currencies.

Impact of Commodities

As a general rule, the nations whose currencies have

remained top performers over the past decade may

be identified as those whose national income is tied

heavily to commodity production.

Commodity prices have generally advanced, often

sharply, over the past decade as seen in the rise in

the value of energy, grain, livestock, precious metals

and industrial metals. These price advances have

largely been driven by emerging market demand in

nations including China and India.

But those trends have corrected over the past year.

Gold values fell sharply during 2013 to the extent

that economic recovery in the developed economies

led to much reduced economic anxiety. West Texas

Intermediate (WTI) crude oil drifted a bit higher

during the 1st quarter following a moderately

buoyant 2013. Grain values including corn,

soybeans and wheat were off a bit on a productive

growing season coupled with moderating global

demands.

$600

$800

$1,000

$1,200

$1,400

$1,600

$1,800

$2,000

$20

$40

$60

$80

$100

$120

$140

$160

Jan-0

7

Sep-0

7

May-0

8

Jan-0

9

Sep-0

9

May-1

0

Jan-1

1

Sep-1

1

May-1

2

Jan-1

3

Sep-1

3

Gold

($ p

er

troy o

z)

Cru

de O

il (

$ p

er

Bbl

Crude Oil & Gold

Crude Oil Gold

Source: Bloomberg

5 | Currency Market Monitor 1st Quarter 2014 | April 3, 2014 | © CME GROUP

CME Group has developed the CME FX Commodity

Country Index to follow the performance of a basket

of currencies from nations that rely heavily upon the

exportation of commodities and other raw materials.

To the extent that commodities have been in great

demand over much of the past decade, these

currencies have, on a historical basis, generated

favorable total returns. 15

The CME FX Commodity Country Index drifted up

2.01% to 875.19 by the conclusion of the 1st quarter

from the year-end 2013 value of 857.91.

CME Group has further developed the CME FX BRIC

Index to follow the performance of select “emerging

market” economies and their national currencies,

namely the Brazilian real (BRL), Russian ruble

(RUB), Indian rupee (INR) and Chinese yuan (CNY),

that have created much of the demand for

commodities in the world today. 16

15 The CME Commodity Country Index is constructed to be

effectively long Australian dollar (AUD), Brazilian real (BRL), Canadian dollar (CAD), Norwegian krone (NOK), New Zealand dollar (NZD) and South African rand (ZAR) vs. a short position in the U.S. dollar (USD). It is (arbitrarily) established at a value of 1,000.00 as of December 31, 2010.

16 The CME BRIC Index is constructed of equal weightings of long Brazilian real (BRL), Russian ruble (RUB), Indian rupee (INR) and Chinese yuan (CNY) vs. a short position in the U.S. dollar (USD). Like other CME FX indexes discussed above, the BRIC Index was equally weighted and calibrated to equal an arbitrary 1,000.00 as of December 31, 2010.

The CME FX BRIC Index ended the 1st quarter at

852.35 and virtually unchanged from the year-end

2013 mark at 858.26.

Conclusion

CME offers a broad array of currency futures and

option contracts covering a wide range of currency

pairings (where one side is the U.S. dollar) and

cross-rate pairings (which do not involve the U.S.

dollar). These products provide facile and liquid

vehicles with which one may express a view on

prospective market movements. Or, to manage the

risks associated with currency holdings or

international investments during turbulent times.

For more information please visit our website at

www.cmegroup.com/trading/fx.

$2

$4

$6

$8

$10

$12

$14

$16

$18

Jan-0

7

Jul-

07

Jan-0

8

Jul-

08

Jan-0

9

Jul-

09

Jan-1

0

Jul-

10

Jan-1

1

Jul-

11

Jan-1

2

Jul-

12

Jan-1

3

Jul-

13

Jan-1

4

$ p

er

Bushel

Grains

Corn Soybeans Wheat

Source: Bloomberg

650

700

750

800

850

900

950

1,000

1,050

1,100

Jan-0

7

Jul-

07

Jan-0

8

Jul-

08

Jan-0

9

Jul-

09

Jan-1

0

Jul-

10

Jan-1

1

Jul-

11

Jan-1

2

Jul-

12

Jan-1

3

Jul-

13

Jan-1

4

CME FX Commodity Country Index

Long Short16.7% AUD 100% USD16.7% BRL 16.7% CAD 16.7% NOK16.7% NZD16.7% ZAR

800

840

880

920

960

1,000

1,040

1,080

1,120

Jan-0

7

Jul-

07

Jan-0

8

Jul-

08

Jan-0

9

Jul-

09

Jan-1

0

Jul-

10

Jan-1

1

Jul-

11

Jan-1

2

Jul-

12

Jan-1

3

Jul-

13

Jan-1

4

CME FX BRIC Index

Long Short25% BRL 100% USD25% RUB 25% INR 25% CNY

6 | Currency Market Monitor 1st Quarter 2014 | April 3, 2014 | © CME GROUP

Appendix 1: Summary of World Economic Conditions

Australia Brazil Canada

Growth,

Inflation

& Fiscal

Policy

Australia’s economy may suffer from further deceleration of growth in China and by

potential problems in China’s shadow banking system.

Economic growth has been slow in Brazil, but there are signs of incremental improvement.

Water shortages, especially around Sao Paulo, though, may be a risk to growth.

Canada is benefiting from the continued jobs expansion in the US. On the negative side, the domestic oil sector has some challenges

and delays in the US decision on the Keystone pipeline are not helping economic confidence.

Monetary

Policy

Monetary policy now appears to be on hold in Australia. Short-term interest rates offer a small premium to the near-zero rates in the

US, Europe, and Japan.

Short-term interest rates around 10% now provide solid support for the currency. As

emerging market currency pressures abate, there may be room for rate cuts later in 2014.

Canada’s rates are low. There are no inflation pressures. The Bank of Canada seems

comfortable with the current set of policies, at least so long as the US keeps its federal funds

rate near zero.

Special

Factors

The Australian dollar managed a small appreciation in Q1/2014, even with uncertainties relating to China and

commodities prices.

Brazil hosts the World Cup in 2014 and the Olympics in 2016. A successful World Cup

has the potential to give the markets a boost of confidence in the Brazilian real.

Rate differentials with the US are too small to support the Canadian dollar. The big risks are in the energy sector. Weaker oil prices or a US decision against the Keystone pipeline

would probably hurt the currency.

China European Union India

Growth,

Inflation

& Fiscal

Policy

China may decelerate further to around 6.5% to 7% real GDP growth in 2014. The

economy is likely to avoid a hard landing but continues to face challenges in its shadow

banking system.

Europe is likely to post some small gains in economic growth in 2014. The rise in the

euro over the past 12 months of a little more than 7%, however, appears to be contributing to a risk of slipping into deflationary territory.

India’s economy is growing at only about half the pace it once did. At the same time,

monetary policy was tightened to defend the currency in 2013.

Monetary

Policy

Monetary policy remains in flux. The central bank has to decide how much support to give a struggling shadow banking system. Also,

the weaker RMB means that China is unlikely to be a buyer of US Treasuries, as it was in periods of upward pressure on the currency.

The ECB faces two big policy challenges (a) supervising banks and completing a round of

stress tests, and (b) deciding how to deal with deflationary pressures. Some form of

expanded policy accommodation is possible.

Short-term interest rates above 8% worked to stabilize the currency in Q1/2014. A

prolonged period of currency stability could potentially allow for rate cuts down the road.

Special

Factors

China has widened the bands for currency volatility, and the RMB weakened during

Q1/2014, joining the ranks of other emerging market currencies that had previously

experienced weakness.

The EU Parliamentary elections in May 2014 could prove very interesting. Fringe parties appear to be gaining ground, such as the UK Independence Party and the National Front in

France.

The India has parliamentary election in 2014 that could bring a shift of power. Despite

election uncertainties, though, stability at the central bank is likely to mitigate any market

concerns.

7 | Currency Market Monitor 1st Quarter 2014 | April 3, 2014 | © CME GROUP

Appendix 1: Summary of World Economic Conditions, cont.

Japan Mexico Russia

Growth,

Inflation

& Fiscal

Policy

Japan’s hike in its national sales tax is expected to lead to weaker real GDP for a few quarters. There is possibility of Prime Minister

Abe bringing forward more fiscal stimulus if economic growth is too depressed by the sales

tax hike.

Mexico is benefiting from improved growth in the United States. Mexico has also increased its imports of relatively inexpensive natural

gas through its pipeline link with Texas.

Russia’s annexation of the Crimea will come at a price of expanded spending and potential

sanctions. Slower economic growth and even possibly a recession seem quite possible.

Monetary

Policy

The Bank of Japan may also consider expanding its quantitative easing (asset

purchase) program if real GDP shrinks in the April-June quarter.

The Bank of Mexico has been able to allow for small rate reductions as the currency has

stabilized.

The political uncertainties over the Crimea takeover have led to a weaker Ruble and higher

interest rates.

Special

Factors

A 2% inflation target by the Bank of Japan is not likely to be achieved in a short time frame unless there is further yen depreciation toward

the 120-140 yen/dollar rate. There is the possibility the government and central bank

would welcome another round of yen weakness.

In the emerging market currency sell-off in 2013, the Mexican peso did not lose as much ground as many of its peers. And now that pressures have abated, the peso is poised to

regain some lost ground.

Russia’s annexation of the Crimea has dominated the headlines in Q1/2014. And, Russia is likely to put more pressure on the Ukraine through higher

natural gas prices.

Switzerland United Kingdom United States

Growth,

Inflation

& Fiscal

Policy

Switzerland is seeing some benefits from Europe’s stabilization. Moreover, stronger growth in the US may also help exports.

The UK’s growth prospects are steadily improving. The budget deficit as a percent of

GDP is also declining.

The US economy suffered through a tough winter in midwest and northeast, but a bounce back seems in progress as spring has arrived. And,

surprising to many, the Federal budget deficit is on track to be balanced on an operating basis in

FY2015.

Monetary

Policy

As the EU debt crisis has morphed into a long-term banking capital adequacy problem, the

Swiss have little flexibility, and they are likely continue to keep a lid on the Swiss franc

relative to the euro.

The Bank of England has indicated it plans to keep rates low and focus its efforts on financial

supervision. A stronger economy than expected by the BoE could change that

guidance later in 2014.

The Yellen-led Federal Reserve immediately moved to alter its forward guidance process at its first FOMC meeting after Bernanke’s retirement. Indicator-based guidance is out, replaced by a

more nuanced view of labor market conditions and potential inflation pressures. QE is on track to

end in Q4/2014.

Special

Factors

The post-2008 financial crisis has led to increased regulation of financial institutions all

over the world. On net, this increased regulation poses additional challenges for the

traditional model of Swiss secrecy and the overall role of Switzerland in the world’s

financial system.

The vote in Scotland on independence in September is starting to cast a shadow over the British pound. The outcome will depend on the tug of war between the pocket book

and the heart strings. Economics says independence would hurt Scotland and the UK. But Scots can achieve at the ballot box what

eluded Robert Bruce and William Wallace.

The US dollar may hold the key to whether inflation pressures emerge in the US. The 1970s

saw a weak dollar and rising inflation, and the early 1980s saw dramatic declines in inflation with

a strong dollar. During 2013, a weak yen and weak emerging market currencies contributed to

deflationary pressures in the US.

8 | Currency Market Monitor 1st Quarter 2014 | April 3, 2014 | © CME GROUP

Appendix 2: Select Currency Performance (1st Quarter 2014)

Currency Ticker Spot Quote

(3/31/14) Quote

Convention 3-Mth Rates

(3/31/14)

1st Quarter 2014 2014 Year-to-Date

Total

Return1

Spot

Return2

Interest

Return3

Total

Return1

Spot

Return2

Interest

Return3

Argentine Peso USD-ARS 8.0014 USD per 1 ARS 29.20% -7.57% -18.53% 13.46% -7.57% -18.53% 13.46%

Australian Dollar AUD-USD 0.9264 AUD per 1 USD 2.70% 4.58% 3.89% 0.67% 4.58% 3.89% 0.67%

Brazilian Real USD-BRL 2.2720 USD per 1 BRL 6.62% 3.97% 2.55% 6.62% 3.97% 2.55%

British Pound GBP-USD 1.6662 GBP per 1 USD 0.50% 0.76% 0.63% 0.12% 0.76% 0.63% 0.12%

Canadian Dollar USD-CAD 1.1050 USD per 1 CAD 1.08% -3.59% -3.86% 0.28% -3.59% -3.86% 0.28%

Chilean Peso USD-CLP 548.50 USD per 1 CLP -3.39% -4.37% 1.02% -3.39% -4.37% 1.02%

China Renminbi USD-CNY 6.2181 USD per 1 CNY 4.75% -2.33% -2.62% 0.29% -2.33% -2.62% 0.29%

Colombian Peso USD-COP 1,971.94 USD per 1 COP -1.43% -2.11% 0.70% -1.43% -2.11% 0.70%

Euro EUR-USD 1.3770 EUR per 1 USD 0.26% 0.25% 0.19% 0.06% 0.25% 0.19% 0.06%

Icelandic Krona USD-ISK 112.79 USD per 1 ISK 5.85% 3.62% 2.12% 1.47% 3.62% 2.12% 1.47%

Indian Rupee USD-INR 0.0167 USD per 1 INR 9.25% 5.57% 3.19% 2.31% 5.57% 3.19% 2.31%

Japanese Yen USD-JPY 103.23 USD per 100 JPY 0.04% 2.04% 2.01% 0.02% 2.04% 2.01% 0.02%

Mexico Peso USD-MXN 13.0585 USD per 1 MXN 3.81% 0.58% -0.16% 0.74% 0.58% -0.16% 0.74%

New Zealand Dollar NZD-USD 0.8671 NZD per 1 USD 3.19% 6.26% 5.47% 0.75% 6.26% 5.47% 0.75%

Russian Ruble USD-RUB 35.0653 USD per 1 RUB 8.38% -4.86% -6.55% 1.81% -4.86% -6.55% 1.81%

South Africa Rand USD-ZAR 10.5807 USD per 1 ZAR 6.05% 0.61% -0.37% 0.99% 0.61% -0.37% 0.99%

South Korean Won USD-KRW 1,064.24 USD per 1 KRW -0.82% -1.40% 0.59% -0.82% -1.40% 0.59%

Swiss Franc USD-CHF 0.8851 USD per 1 CHF -0.05% 0.93% 0.94% -0.01% 0.93% 0.94% -0.01%

Taiwanese Dollar USD-TWD 30.471 USD per 1 TWN 0.87% -2.02% -2.23% 0.21% -2.02% -2.23% 0.21%

Turkish Lira USD-TRY 2.1407 USD per 1 TRY 11.48% 3.06% 0.35% 2.70% 3.06% 0.35% 2.70%

United States Dollar USD 1.0000 USD 0.23% 0.06% 0.06% 0.06% 0.06%

Notes

(1) Return from price movement and interest (2) Return from currency price movement vs. USD as “base currency”

(3) Return from interest at prevailing 3-month rates or implied NDF rate

Source: Bloomberg

9 | Currency Market Monitor 1st Quarter 2014 | April 3, 2014 | © CME GROUP

Appendix 3: Purchasing Power Parity (“PPP”) Analysis (as of 3/31/14)

% Over/Under Valued

Currency ISO

Code Average OECD

Bloomberg

(CPI)

Bloomberg

(PPI) Big Mac

Norwegian Krone NOK 31.79% 31.98% 10.58% 52.80%

Swiss Franc CHF 31.22% 35.45% 24.58% 10.88% 53.95%

New Zealand Dollar NZD 23.30% 21.19% 33.57% 40.70% -2.25%

Danish Krone DKK 19.57% 29.06% 19.58% 18.06% 11.56%

Icelandic Krona ISK 18.23% 18.23%

Australian Dollar AUD 15.57% 26.71% 26.74% 19.38% -10.54%

Swedish Krona SEK 13.00% 25.05% -5.08% -3.35% 35.36%

Euro EUR 11.15% 6.02% 18.66% 14.04% 5.86%

British Pound GBP 7.11% 13.46% 17.25% 5.66% -7.95%

Canadian Dollar CAD 4.50% 10.48% 7.36% -3.47% 3.62%

Brazilian Real BRL 3.59% 3.59%

Colombian Peso COP -11.76% -11.76%

Japanese Yen JPY -17.84% -0.60% -17.60% -13.75% -39.39%

Singapore Dollar SGD -20.97% -20.97%

South Korean Won KRW -25.14% -25.78% -24.50%

Chilean Peso CLP -25.61% -25.61%

Czech Koruna CZK -26.22% -26.22%

Thai Baht THB -42.09% -42.09%

South African Rand ZAR -42.39% -25.78% -59.00%

Chinese Renminbi CNY -42.69% -42.69%

Hungarian Forint HUF -46.95% -75.58% -18.32%

Phillipines Peso PHP -47.11% -47.11%

Argentina Peso ARS -47.36% -47.36%

Indonesian Rupiah IDR -47.88% -47.88%

Russian Ruble RUB -50.02% -50.02%

Hong Kong Dollar HKD -51.93% -51.93%

Mexican Peso MXN -52.83% -66.67% -38.99%

Malaysian Ringgit MYR -52.91% -52.91%

Polish Zloty PLN -53.00% -67.66% -38.34%

Turkish Lira TRY -59.85% -98.51% -21.19%

Notes

Please note that data regarding all countries is not generally available.

Source: Bloomberg

10 | Currency Market Monitor 1st Quarter 2014 | April 3, 2014 | © CME GROUP

Futures and options trading is not suitable for all investors, and involves the risk of loss. Futures are leveraged investments, and because only a percentage of a contract’s value is required to

trade, it is possible to lose more than the amount of money initially deposited for a futures position. Therefore, traders should only use funds that they can afford to lose without affecting

their lifestyles. And only a portion of those funds should be devoted to any one trade because they cannot expect to profit on every trade. All matters pertaining to rules and specifications

herein are made subject to and are superseded by official CME rules. Current rules should be consulted in all cases concerning contract specifications.

The information within this presentation has been compiled by CME Group for general purposes only. Although every attempt has been made to ensure the accuracy of the information within

this presentation, CME Group assumes no responsibility for any errors or omissions. All data is sourced by CME Group unless otherwise stated.

CME Group is a trademark of CME Group Inc. The Globe logo, E-mini, E-micro, Globex, CME and Chicago Mercantile Exchange are trademarks of Chicago Mercantile Exchange Inc. All other

trademarks are the property of their respective owners.

Copyright © 2014 CME Group. All rights reserved.