Embed Size (px)

Citation preview

Critical Illness TrainingCritical Steps

Module 3: Presenting the CI Solution

Tailoring Your Message

For agent use only. Not for use with consumers.

15-425-02251 C (12/12)

What does a good salesperson

and a good lawyer have in common?

Now we present the CI product

• Four questions/statements meeting

• Product– Amount?

• Premium?• Definitions?• Most importantly– Tailoring your message

People hate to be sold, but they love to buy.

What’s the secret?

The four questions CI meeting

• Do you know anyone…?

• Did they plan on it? Or, was it unexpected?

• Was there unplanned emotional or financial strain on the household/ business?

• Would cash have helped?

CI amounts?

• No obvious needs analysis like life or DI insurance

• “If you were diagnosed, what are your immediate concerns?”

• “If you knew you were going to be diagnosed in 3 months, how much coverage would you buy today?”

• “If it was me, this is how I would like it to look.”

$50,000 – not a lot of money?

CI: a doctor’s design

If the insurance industry would have invented it, the plan could have been:

1) Prove to us the critical illness happened, then

2) Show us how your life was impacted by medical bills or time missed from work, then

3) We will give you some of the benefit for which you have been paying premium.

Car and home insurance...run through examples

Influence of the doctor’s design

• You suffer a critical illness that meets the insurance company’s contractual terms.

• The insurance company gives you the benefit.

• You decide how the money can best help you.

The definitions–a positive

• Rigidity is a positive at claim

• Invented by a doctor

• No subjectivity by a claims person at the home office

• Definition – Doctor’s report: Yes or no

• Read this booklet

Presenting CI premium

• As a percent of benefit

• Not $900/year for $100,000

• “About” __ percent of whatever benefit you think is right…

• “About” __ percent pre-sells ratings in an underwritten rate-able product

Tailoring your message

• Product ownership• Business owners• Wealth• Personality types

Very important with buying NEW products, services and decisions

like CI.

Critical illness funds

• Uses of critical illness insurance benefits vary widely

Hotel towels

• Create an expectation• This is how other business

owners used funds

Current client…Monday morning phone call introduction

Think of your longstanding client(s) who do not own CI.

Monday morning phone call:

“If you were to have called me this morning and said, ‘I’ve bought everything you have ever put in front of me…on Friday I was diagnosed with cancer… what do you have for me?’...that’s not a conversation I want to have with you yet.”

Didn’t die, haven’t missed 4 months of work…

noninsurance-worthy event?

Current client – strategy completion

1.Review planning strategy and re-confirm rationale

2.Introduce how major health change represents risk

3.Introduce how CI can be a solution for a small percentage of the risk

Life insurance: why?

• Major illness or event takes your life—ensure family…

• What if it does not take your life?...a different goal

• And, you will be around to see outcome…

Script

Life insurance: goal?

Why are you buying life insurance?

– Because you think something bad is

going to happen?– You need to have it because it

would be irresponsible or burdensome not to have it.

Likely?

What’s more likely?

– Becoming an angel prematurely?– Being diagnosed with a critical

illness?

Life insurance client

• New vs. old planning• Modern planning• A leading Canadian seller

—the banks

A leading seller of CI in Canada?

Would you like the old type of mortgage insurance or the new?

•The old one helps pay off your mortgage if you die; the new one also helps pay it off if you are diagnosed with invasive cancer, heart attack or stroke.•Statistically, before the recession, almost half of mortgage foreclosures were caused, in part, by a disability.* •Which would you like, the old or new?

What if every life insurance inquiry OPENED a CI discussion?

* "Get Sick, Get Out: The Medical Causes of Home Mortgage Foreclosures, HEALTH MATRIX Vol. 18:65, Christopher Robertson, Richard Egelhof and Michael Hoke. (2008)

Medical coverage

• Brakes/Airbags – Should there be significantly more relief, fewer

deductibles, co-pays and maximums if it’s cancer?

• Trading deductibles for downside protection... It is insurance, right?

• Push out deductible– Funded by CI if it’s a covered event

• Comforts…created expenses - spouse, hotel, nanny, etc.

Disability client

DI: Why not 100% replacement?

–More claims– Longer claims– Human nature of other people

Group/individual disability income —usually a deal-killer

• Is a critical illness insurance opportunity

• “My clients” vs. “people for whom ratio required”

– Unfair, wrong, deserve

–Minimum standard for ethical people with real claims

• “I have always been frustrated that good, honest people....”

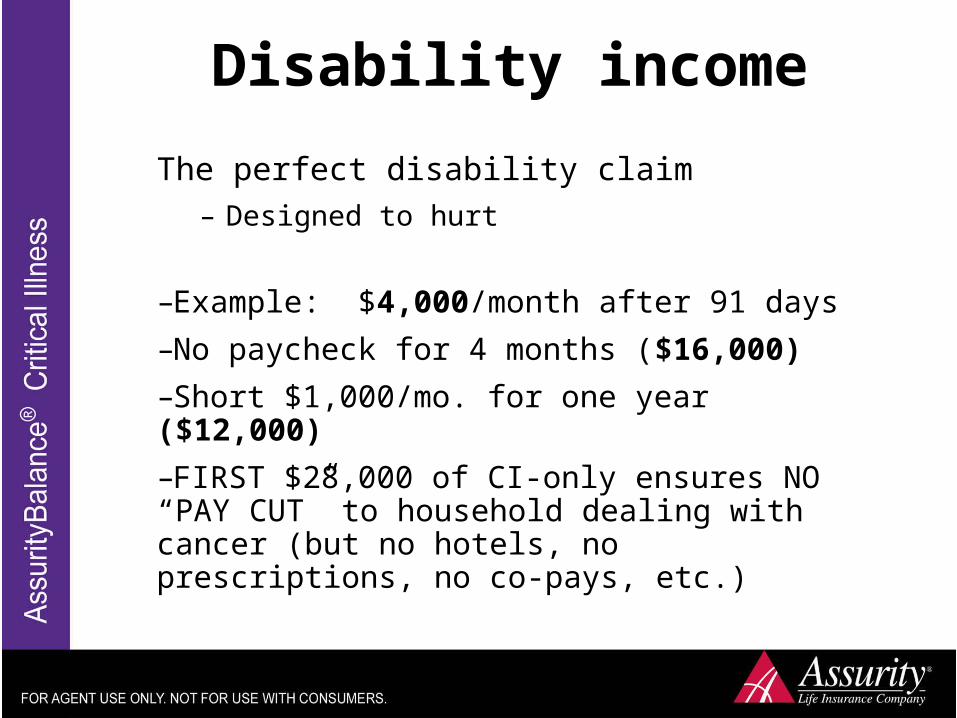

Disability income

The perfect disability claim– Designed to hurt

–Example: $4,000/month after 91 days

–No paycheck for 4 months ($16,000)

–Short $1,000/mo. for one year ($12,000)

–FIRST $28,000 of CI-only ensures NO “PAY CUT” to household dealing with cancer (but no hotels, no prescriptions, no co-pays, etc.)

Disability client

“It might just be me, but I see a difference between...”

– Sore back and cancer– Broken leg and stroke

Critical illness and DI – a great match

• Think of disability insurance as the brakes on your car…

• Think of critical illness insurance as the airbag

– Also, DI writers love this…if I had to choose between two cars…I choose brakes

– But most cars today have both!

CI & the quality accountant

• Question: How good is your accountant?

• The “better” a client feels their accountant…the more likely they are short on their Disability coverage and need some Critical Illness.

Script

Blue collar

Show pricing (use actual figures, gender, policy amount, elimination period, etc…example below):

•Disability – Premium for your category: $200/month– Premium for lawyer/accountant:

$80/month•Critical Illness ($100,000)

– Premium for you: $50/month– Premium for lawyer/accountant:

$50/month

Investment client

• Non-market risk

– Is your portfolio subject to health risk?

• Irony of “it” working

• Illness “timing”

Investment clients –two ways to earmark for this

1. Block off a big health care emergency fund and use the balance to live on, and for travel, entertainment and the things you have earned

2. Block off a small monthly amount for CI insurance and use the bigger balance to live on and for travel, entertainment and the things you have earned

Wealthy clients – “I am self insured/can use my own money” is covered in the Objections Module in series

Script

Performance-based

• Self-employed or salary plus bonus

• If your client can’t work, they’re not just down 20% due to reduced disability benefits

• “Bonus” insurance?

Script

Students and young adults

• “Becoming” independent

• Very little financial margin (illness)

• No “rent” insurance like “mortgage insurance”

• Independence insurance/pride

“Smokers’ & lung cancer” coverage

“What would you pay for a product that paid you $___, if you were diagnosed with lung cancer?”

Script

Business owner’s unique risks & opportunities

• Impact of your absence

• Unscheduled 4-month vacation?

Script

CI and the business owner

What might keep you from work?

• Flu

• Sore back

• Broken leg

Are there some things that keep your employees from coming to work that wouldn’t stop you?

•Script

Disability coverage and owners

• Higher incomes often not adequately covered– Group plan maximums

Script

Attachment – business owners• You said …• But they heard: “This is like lump-sum

disability coverage, and I only need to be away from my company for one month to get the money.”

• You need to run the calendar.

• I would be delighted to deliver the check to you… – at your office/on the job site.

Script

Business owners:

• “Do you make your business go?”

• “Does your staff think that?”

• “Does your banker think that?”

• “Do your clients think that?”

Script

3 key points

1. --2. --3. --

• Best Sales Idea

Frank Bettger

“How I raised myself from failure to success in selling”

Summary of the six elementsof this training

Element Client Question Advisor Talking Point

1 What’s this CI product all about? CI: A Doctor’s Concept

2 Why are we talking about this CI product NOW? The Three Realities of Health

3 What can this CI product do for ME? What CI Does: Attachment

4 What could this CI product look like for me? Solution Building

5 What to do now? Action

6 What happens now? Process Description/implementation

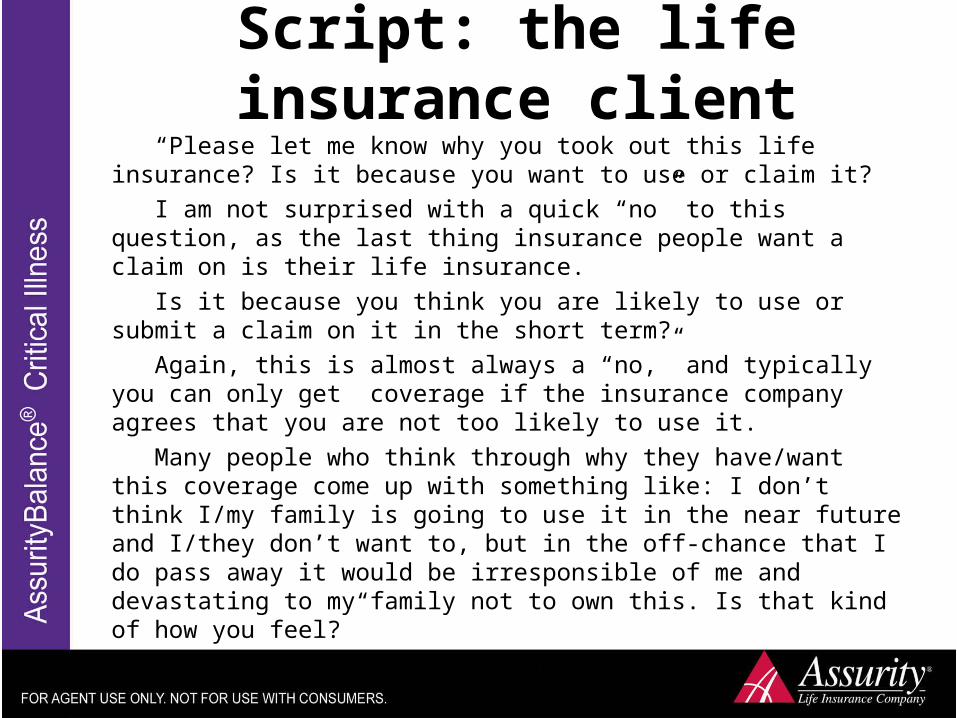

Script: the life insurance client “Please let me know why you took out this life insurance? Is it because you want to use or claim it? I am not surprised with a quick “no” to this question, as the last thing insurance people want a claim on is their life insurance. Is it because you think you are likely to use or submit a claim on it in the short term? Again, this is almost always a “no,” and typically you can only get coverage if the insurance company agrees that you are not too likely to use it. Many people who think through why they have/want this coverage come up with something like: I don’t think I/my family is going to use it in the near future and I/they don’t want to, but in the off-chance that I do pass away it would be irresponsible of me and devastating to my family not to own this. Is that kind of how you feel?”

(continued)

Script: the life insurance client “I think that is smart and admirable, and I think this coverage is important for those reasons. It is unfortunate that many people buy this coverage for an event they think won’t happen. And if it does, everyone else but them benefits (because they are gone), and they are never presented with an important complementary product covering a risk far more likely to occur in the short term—a product the client (and the family) can benefit from. A question for you, what do you think is more likely in the short term to occur to you—dying or a major health scare like cancer, heart attack or stroke that knocks your world on its side financially and emotionally for a period of time?”

Script: the quality accountant “One reason some business owners can’t get the amount of DI coverage they want is due to the way that they take their income. With employees, it’s transparent what they earn. They show the insurance company their salaried income and the insurance company typically gives them a set percentage of that in a disability benefit. With owners, the good news is compared to straight-salaried income, they have different ways by which they can be paid. There are dividends, travel and expense accounts, income splitting, etc. The challenge is when the amount of DI insurance is determined, insurance companies often don’t count many of these types of income or personal expenses that get paid by your business.”

(continued)

Script: the quality accountant “As one person put it…the better a business owner’s account, the tougher it is for that owner to get a level of disability income coverage that is really representative. While I cannot make insurance companies change their rules and give you an extra $__ a month in disability coverage, I can make sure that if something big happened to you like cancer, heart attack or stroke, the insurance companies would send you an additional check so you can focus on your recovery. Does it make sense that we make sure you don’t end up relatively worse-off than your employees when facing a major health event?”

Script: investment client “I think we have done an excellent job in structuring a plan for your retirement planning. Our plan to put aside ___ with the goal of building a nest egg of $__ by age __, all so you can do things like ___, ___ and ___ in your retirement years. There is a risk, which has nothing to do with investment or market performance, that can severely impact people’s investment plans, and that most do not recognize or contemplate addressing until it is too late.”

(continued)

Script: investment client “Very few investment plans factor in how an investment strategy would compensate for a major health event like cancer, heart attack or stroke sometime over the next ___ years. I’m referring to an event that either disrupts a client’s contribution pattern or worse—requires them to withdraw funds to help them with their health recovery. Using the innovative product we are going to talk about today, we have a way of shifting that risk off your portfolio and yourself and onto the insurance company. With the odds of someone your age having a major illness in the next __ years being ___, I think it’s important to not minimize that risk. Does that make sense?”

Script: performance-based “What’s the breakdown of your income each year between guaranteed salary and performance compensation? (For example, $75,000 base and an average $75,000 bonus) As a person in a performance-based position and as a achiever in a performance-based business, you have extra exposure to the impact of a major illness—that a straight salaried employee does not have. It’s an exposure that many people don’t realize exists until it’s too late. The straight-salaried employee battles through a major health issue with most of their income replaced by their DI insurance. People like you, who are paid based on performance, typically also get their base salaries covered with DI coverage, but here’s the problem…”

(continued)

Script: performance-based “If you had to go through a health scare beyond your control—like cancer, heart attack or stroke—and it either kept you from working full time or impacted your ability to perform while working, do you think it would be fair that you might get your bonus or commission? I don’t. We can transfer that health risk off your back and onto the insurance company with a rapidly growing product called Critical Illness insurance. For people like you, we could even call it “performance insurance”… you keep the responsibility of having to perform to make your targets when you’re healthy, but if you have to deal with a major critical illness, a cash benefit is paid from the insurance company, which can help replace your income if your targets are not met. Does it make sense to take the uncontrollable health risk off your plate?”

Script: smokers “You probably get tired of people reading you the sides of cigarette boxes and telling you that smoking is bad for you. I suspect you get that already–right? What would you be willing to pay for an insurance policy that paid you a payment of say $50,000 if you were diagnosed with lung cancer? What’s amazing is that such a product exists, and you can get it even if the insurance company knows how much you smoke. But more importantly, the policy pays out that lump sum not just for lung cancer, but the other life-threatening cancers, heart attack, stroke and all the other conditions listed in the policy.”

(continued)

Script: smokers

“If you saw value in the concept of shifting the risk of some of the financial consequences of just lung cancer off your back and onto an insurance company using a policy, doesn’t it make significantly more sense to shift some of the costs of these other health conditions as well? Further, a year after you do quit smoking, if you are still healthy, you can apply to have your rates dropped to the same rates as someone who never smoked…not bad.”

Script: four-month vacation? “If you decided today to take a 4-month vacation, and starting tomorrow, without pre-planning with your staff or working while you were away, how might the business be impacted? You can control your choice to take a four-month, unannounced vacation, and I suspect you never would take one, but what none of us can control is the possibility that a random illness like cancer will take us out of our business while we battle through and recover. I think it makes sense, with all the work you have put into the business, to shift that health risk off you and onto an insurance company. Does that make sense to you?”

Script: CI and the business owner “It may be the biggest reason business owners are drawn to this product is they have a hard time envisioning themselves away from their business while afflicted with the illnesses or conditions that cause many disability insurance claims and drive up that insurance’s pricing. If I asked you to name some things that could happen to your health and knock you out of work, I suspect that a mild back problem or stress, two of the biggest causes of disability claims, would not be at the top of the list, correct? It’s uncanny, but the things that business owners think could impact them are the health scares beyond our control—like the conditions covered by this Critical Illness product: cancer, heart attack, etc. What many business owners like about this product is their premium is only paying for protection against these big things, and is not being used to cover things like back strain—things they would never file a claim for.

Script: disability coverage and business owners

“Critical illness insurance is often more important for business owners, compared to their employees, when it comes to managing the risk of illness. The reason is: Typically, the higher someone’s income, the lower the percentage of that income that’s covered by disability income insurance. What this means is the business owner takes a bigger percentage drop in income, if they become disabled, compared to their lower-paid employees. Does that make sense to you? Many owners are anxious to hear how they can remedy this situation.”

Script: running the calendar “Sometimes people either misinterpret the way this product works, or in the case of business owners like you, they think it sounds “too good to be true.” Many think CI Insurance sounds like lump-sum disability insurance that must still require time away from running their business to receive a payment. I cannot stress the following point enough to business owners: If you are diagnosed with any of the covered illnesses or conditions, you do not have to miss any time, whatsoever, from running your company to get paid your Critical Illness Insurance benefit.

(continued)

Script: running the calendar “This is important to most business owners because it means you can work as much as you want or are able while recovering, without impacting the insurance company’s benefit payout.” “So to be crystal clear, a business owner like you could be diagnosed on March 1 with cancer or any other covered condition, and go to work March 2, 3 and 4, then take a day off for treatment on March 5, then be back at work at the business on March 6, 7 and 8, and so on, for the rest of the month. On April 1, or around a month after diagnosis, I would be delighted to deliver the benefit check, wherever you are—whether at the hospital, home recovering, at your office, on the roof of your next project, etc.”

Script: how valuable are you?This approach is particularly effective when the owner either truly drives, or perceives he or she drives, the success of the business. The scripting plays off this perception by indicating it would take a team of people to replace the owner’s efforts should a health crisis take them away for a period of time. This is another example of the ripple effect of illness—where the business owner is impacted, but so are many people around them.

“If you were pulled from your business for a period of time, how long would it be before the business started to feel the negative consequences? Would it be easy to find or attract the right caliber of interim replacement to help step in for a period of time? If it were a major illness like cancer that pulled you away, would it help bridge the business if you had a pot of extra money to bring in additional help in the form of a number of people, until you were healthy and back full time?”

Questions?

For agent use only. Not for use with consumers.

15-425-02251 C (12/12)