Embed Size (px)

Citation preview

Criteria CaixaHolding, S.A.U.

Financial Statements for the year ended

31 December 2013 and Directors' Report

Translation of financial statements originally issued in Spanish

and prepared in accordance with the regulatory financial

reporting framework applicable to the Company (see Notes 2 and

25). In the event of a discrepancy, the Spanish-language version

prevails.

- 2 -

Balance sheets ......................................................................................................................................................... 3

Income statements ................................................................................................................................................. 5

Statements of changes in equity ............................................................................................................................. 6

Statements of cash flows ........................................................................................................................................ 8

Notes to the financial statements

1. Company activities ....................................................................................................................................... 9

2. Basis of presentation of the financial statements ..................................................................................... 12

3. Distribution of profit/Allocation of loss ..................................................................................................... 16

4. Accounting policies .................................................................................................................................... 17

5. Intangible assets ........................................................................................................................................ 27

6. Property, plant and equipment .................................................................................................................. 28

7. Investment property ................................................................................................................................... 29

8. Leases ......................................................................................................................................................... 32

9. Non-current investments in Group companies, jointly controlled entities and associates ........................ 33

10. Non-current financial assets ...................................................................................................................... 39

11. Non-current assets classified as held for sale ............................................................................................. 40

12. Inventories .................................................................................................................................................. 42

13. Current financial assets - Dividends receivable .......................................................................................... 43

14. Cash and cash equivalents .......................................................................................................................... 44

15. Equity .......................................................................................................................................................... 44

16. Financial liabilities (current and non-current) ............................................................................................ 46

17. Tax matters ................................................................................................................................................ 47

18. Income and expenses ................................................................................................................................. 52

19. Related party transactions .......................................................................................................................... 57

20. Note to the statement of cash flows .......................................................................................................... 63

21. Information on the environment ................................................................................................................ 63

22. Risk management policy ............................................................................................................................. 63

23. Segment reporting ...................................................................................................................................... 66

24. Events after the reporting period ............................................................................................................... 66

25. Explanation added for translation to English .............................................................................................. 67

APPENDIX I Disclosure requirements of Article 93 of the Consolidated Spanish Income Tax Law in relation to the merger of the Company and Criteria CaixaHolding (the absorbed company). ................................................ 68

APPENDIX II Investments in Group companies ...................................................................................................... 71

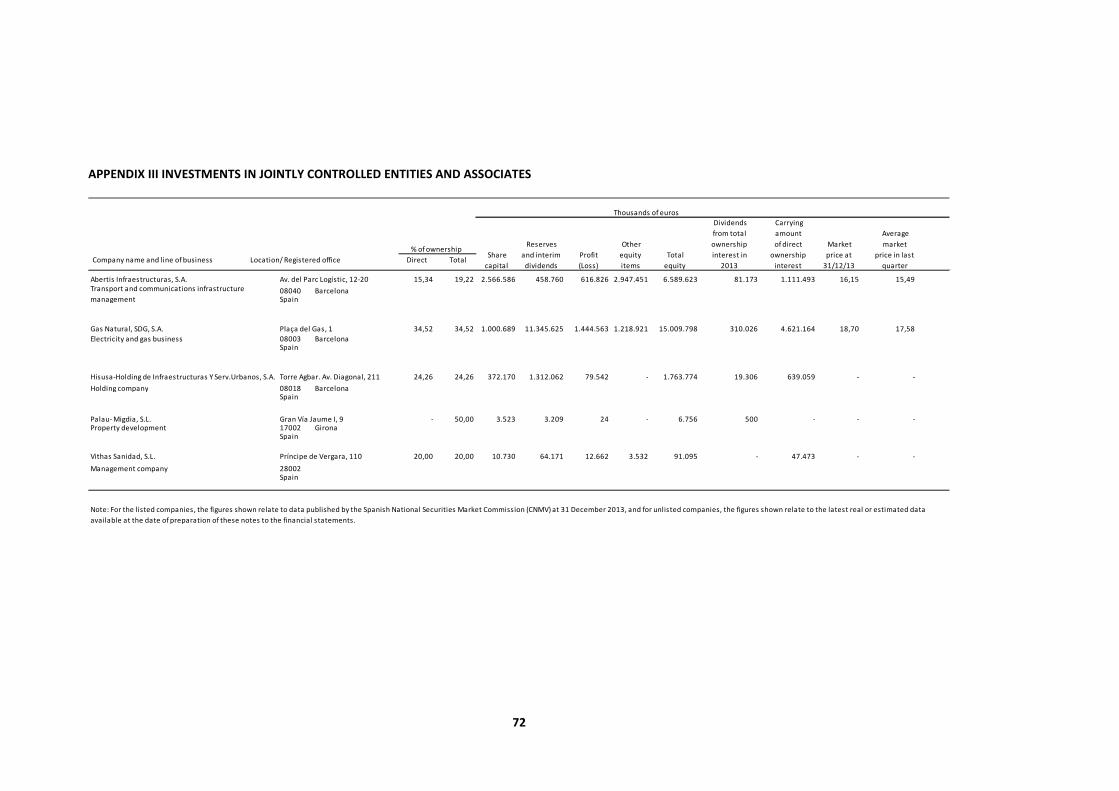

APPENDIX III Investments in jointly controlled entities and associates ................................................................. 72

APPENDIX IV Available-for-sale financial assets - Equity instruments ................................................................... 73

2013 Directors’ Report

3

The accompanying Notes 1 to 25 and the Appendices are an integral part of the balance sheet at 31 December 2013.

(*) The figures at 31 December 2012 are presented for comparison purposes only.

Translation of financial statements originally issued in Spanish and prepared in accordance with the regulatory financial reporting framework applicable

to the Company (see Notes 2 and 25). In the event of a discrepancy, the Spanish-language version prevails.

CRITERIA CAIXAHOLDING, S.A.U.

BALANCE SHEETS AT 31 DECEMBER 2013 AND 2012

Thousands of euros

ASSETS Notes 31/12/13 31/12/12(*)

NON-CURRENT ASSETS

Intangible assets (Note 5) 301 4,563

Property, plant and equipment (Note 6) 1,750 47,626

Investment property (Note 7) 596,509 526,071

Non-current investments in Group companies, jointly controlled entities and associates

(Note 9) 8,061,409 622,269

Investments in Group companies (Note 9.1) 453,977 242

Investments in associates and jointly controlled entities (Note 9.2) 6,726,938 1,856

Other financial assets (Note 9.3) 880,494 620,171

Non-current financial assets (Note 10) 16,030 4,744

Equity Instruments 14,065 3,411

Other non-current financial assets 1,965 1,333

Deferred tax assets (Note 17) 1,005,072 258,118

Total non-current assets 9,681,071 1,463,391

CURRENT ASSETS

Non-current assets classified as held for sale (Note 11) 1,242,812 -

Inventories (Note 12) 187,438 2,111,713

Trade and other receivables 88,972 417,967

Trade receivables for sales and services 386 390

Receivable from Group companies and associates (Note 19) 81,464 417,569

Sundry accounts receivable 17 -

Employee receivables - 8

Other accounts receivable from public authorities (Note 17) 7,105 -

Current investments in Group companies and associates (Note 9.3) 315 43

Loans to companies 315 43

Current financial assets 135,864 515

Dividends receivable (Note 13) 135,762 -

Loans to companies 1 515

Other 101 -

Cash and cash equivalents (Note 14) 207,949 5,150

Total current assets 1,863,350 2,535,388

TOTAL ASSETS 11,544,421 3,998,779

4

Translation of financial statements originally issued in Spanish and prepared in accordance with the regulatory financial reporting framework applicable

to the Company (see Notes 2 and 25). In the event of a discrepancy, the Spanish-language version prevails.

CRITERIA CAIXAHOLDING, S.A.U.

BALANCE SHEETS AT 31 DECEMBER 2013 AND 2012

Thousands of euros

EQUITY AND LIABILITIES Notes 31/12/13 31/12/12(*)

EQUITY:

Shareholders’ equity

Registered share capital 1,381,520 3,453,800

Share premium - 33,500

Legal and bylaw reserves 24,587 5

Other reserves - (12,575)

Merger reserves 7,143,452 (5,673)

Other shareholder contributions - (57,959)

Retained losses - (1,189,410)

Profit (Loss) for the year 110,055 (815,581)

Interim dividend paid during the year (81,000) -

Valuation adjustments 2,416 -

Available-for-sale financial assets 2,416 -

Total equity (Note 15) 8,581,030 1,406,107

NON-CURRENT LIABILITIES

Long-term provisions (Note 9.1) 150,472 67,794

Non-current payables (Note 16) 2,302,611 2,250

Deferred tax liabilities (Note 17) 318,846 -

Total non-current liabilities 2,771,929 70,044

CURRENT LIABILITIES

Current payables (Note 16) 33,882 2,436,107

Current payables to Group companies, associates and jointly controlled entities

- 12

Trade and other payables 157,580 86,509

Payable to suppliers 40,718 67,457

Payable to suppliers - Group companies and associates

(Note 19) 13,768 7,053

Accounts payable 3,579 -

Remuneration payable - 1,550

Other accounts payable to public authorities

(Note 17) 615 1,219

Customer advances 6,293 9,230

Deposits received as security (Note 9.2) 91,434 -

Other 1,173 -

Total current liabilities 191,462 2,522,628

TOTAL EQUITY AND LIABILITIES 11,544,421 3,998,779

The accompanying Notes 1 to 25 and the Appendices are an integral part of the balance sheet at 31 December 2013.

(*) The figures at 31 December 2012 are presented for comparison purposes only.

5

Translation of financial statements originally issued in Spanish and prepared in accordance with the regulatory financial reporting framework applicable

to the Company (see Notes 2 and 25). In the event of a discrepancy, the Spanish-language version prevails.

CRITERIA CAIXAHOLDING, S.A.U.

INCOME STATEMENTS FOR THE YEARS ENDED 31 DECEMBER 2013 AND 2012

Thousands of euros

Notes 2013 2012(*)

Revenue 713,969 456,181

Revenue from equity investments (Note 18) 432,407 -

Changes in fair value of financial instruments (2,127) -

Net gains on disposals of financial instruments (Note 18) 244,434 -

Sales (Note 18) 34,650 386,048

Services (Note 18) 4,605 70,133

In-house work on non-current assets (Note 7) 101,548 193,286

Inventories included in investment property 101,548 193,286

Procurements (Note 18) (107,438) (1,507,751)

Purchases of land, developments in progress and completed developments

(107,438) (654,997)

Impairment of land, developments in progress and completed developments

- (852,754)

Other operating income 362 342

Staff costs (Note 18) (8,555) (9,729)

Other operating expenses (44,371) (98,949)

Outside services (26,679) (82,406)

Taxes other than income tax (11,987) (14,850)

Losses on, impairment of and changes in allowances for trade receivables

(5,705) (1,693)

Depreciation and amortisation charge (10,648) (9,407)

Changes in provisions 1,058 -

Impairment and gains or losses on disposals of non-current assets (Note 18) (583,556) (8,245)

Impairment and other losses (552,114) (3,908)

Gains or losses on disposals and other (31,442) (4,337)

Impairment and other losses on financial instruments (Note 18) (87,172) (30,478)

Other gains or losses 743 (263)

LOSS FROM OPERATIONS (24,060) (1,015,013)

Finance income (Note 18) 62,078 3,723

Finance costs (Note 19) (102,925) (114,135)

FINANCIAL LOSS (40,847) (110,412)

LOSS BEFORE TAX

(64,907) (1,125,425)

Income tax

(Note 17) 174,962 309,844

PROFIT (LOSS) FOR THE YEAR 110,055 (815,581)

The accompanying Notes 1 to 25 and the Appendices are an integral part of the income statement for 2013.

(*) The figures for 2012 are presented for comparison purposes only.

6

Translation of financial statements originally issued in Spanish and prepared in accordance with the regulatory financial reporting framework applicable

to the Company (see Notes 2 and 25). In the event of a discrepancy, the Spanish-language version prevails.

CRITERIA CAIXAHOLDING, S.A.U.

STATEMENTS OF CHANGES IN EQUITY FOR THE YEARS ENDED 31 DECEMBER 2013 AND 2012 A) STATEMENTS OF RECOGNISED INCOME AND EXPENSE

Thousands of euros

Notes 2013 2012(*)

A) PROFIT (LOSS) PER INCOME STATEMENT 110,055 (815,581)

(8,895) B) INCOME AND EXPENSE RECOGNISED DIRECTLY IN EQUITY (4,549) -

I. Arising from revaluation of financial instruments (Note 15) (6,499) -

II. Arising from cash flow hedges - -

III. Grants, donations and legacies received - -

IV. Arising from actuarial gains and losses and other adjustments - -

V. Tax effect (Note 15) 1,950 -

C) TRANSFERS TO PROFIT OR LOSS (Note 15) (4,346) -

VI. Arising from revaluation of financial instruments (6,208) -

VII. Arising from cash flow hedges - -

VIII. Grants, donations and legacies received - -

IX. Tax effect 1,862 -

TOTAL RECOGNISED INCOME AND EXPENSE 101,160 (815,581)

The accompanying Notes 1 to 25 and the Appendices are an integral part of the statement of recognised income and expense for 2013.

(*) The figures for 2012 are presented for comparison purposes only.

7

- 7 -

Translation of financial statements originally issued in Spanish and prepared in accordance with the regulatory financial reporting framework applicable to the Company (see Notes 2 and 25).

In the event of a discrepancy, the Spanish-language version prevails.

The accompanying Notes 1 to 25 and the Appendices are an integral part of the statement of changes in total equity for 2013.

(*) The figures for 2012 and 2011 are presented for comparison purposes only.

CRITERIA CAIXAHOLDING, S.A.U.

STATEMENTS OF CHANGES IN EQUITY FOR THE YEARS ENDED 31 DECEMBER 2013 AND 2012

B) STATEMENTS OF CHANGES IN TOTAL EQUITY

Thousands of euros

Share Share Merger Retained Other Profit (Loss) Interim Shareholders’ Valuation Total

capital premium Reserves reserves losses shareholder for the year dividend equity adjustments equity

Ante. contributions

Balance at 31 December 2011 3,453,800 33,500 (12,566) - (615,855) (57,959) (573,555) - 2,227,365 - 2,227,365

I. Total recognised income and expense - - - - - - (815,581) - (815,581) - (815,581)

II. Transactions with shareholders - - - - - - - - - - -

Decrease in equity resulting from merger (Note 1) - - (4) (5,673) - - - - (5,677) - (5,677)

III. Allocation of loss - - - - (573,555) - 573,555 - - - -

Balance at 31 December 2012 3,453,800 33,500 (12,570) (5,673) (1,189,410) (57,959) (815,581) - 1,406,107 - 1,406,107

I. Total recognised income and expense - - - - - - 110,055 (81,000) 29,055 (8,895) 20,160

II. Transactions with shareholders - - - - - - - - - - -

Increase in equity resulting from merger (Notes 1 and 2) - - - 7,727,452 - - - - 7,727,452 11,311 7,738,763

Capital reduction (Note 15) (2,072,280) (33,500) 37,157 5,673 2,004,991 57,959 - - - - -

Distribution of reserves - - - (584,000) - - - - (584,000) - (584,000)

III. Allocation of loss - - - - (815,581) - 815,581 - - - -

Balance at 31 December 2013 1,381,520 - 24,587 7,143,452 - - 110,055 (81,000) 8,578,614 2,416 8,581,030

8

Translation of financial statements originally issued in Spanish and prepared in accordance with the regulatory financial reporting framework applicable

to the Company (see Notes 2 and 25). In the event of a discrepancy, the Spanish-language version prevails.

CRITERIA CAIXAHOLDING, S.A.U.

STATEMENTS OF CASH FLOWS FOR THE YEARS ENDED 31 DECEMBER 2013 AND 2012

The accompanying Notes 1 to 25 and the Appendices are an integral part of the statement of cash flows for 2013.

(*) The figures for 2012 are presented for comparison purposes only.

Thousands of euros

2013 2012(*)

A) Cash flows from operating activities 437,266 166,852

1. Loss for the year before tax (64,907) (1,125,425) 2. Adjustments for: 52,156 961,148

Depreciation and amortisation charge 10,648 9,407 Impairment losses 552,114 856,662 Changes in provisions 91,819 (19,597) Net losses on derecognition and disposal of non-current assets 31,442 4,337

Net gains on derecognition and disposal of financial instruments (244,434) (73) Changes in fair value of financial instruments 2,127 - Revenue from equity investments (432,407) - Finance income (62,078) (3,723) Finance costs 102,925 114,135

3. Changes in working capital 76,215 413,289 Inventories 5,890 411,317 Trade and other receivables 3,579 4,774 Current liabilities 74,635 (150) Other non-current assets and liabilities (7,889) (2,652)

4. Other cash flows from operating activities 373,802 (82,160) Interest paid (109,914) (82,160) Dividends received 438,418 - Interest received 7,964 - Income tax recovered (paid) 37,334 -

B) Cash flows from investing activities 396,245 (31,150)

Payments due to Investment (-) (255,116) (45,195) Intangible assets and property, plant and equipment (1,128) (4,414) Investment property (9,256) (22,396) Group companies and associates (210,836) (10,586) Non-current assets classified as held for sale (33,893) - Other financial assets (3) (7,799)

Proceeds from disposal (+) 651,361 14,045 Investment property 6,370 13,025 Subsidiaries, joint ventures and associates 542,999 1,020 Available-for-sale financial assets 8,042 - Non-current assets classified as held for sale 93,950 -

C) Cash flows from financing activities (760,261) (149,785)

Dividends and returns on other equity instruments paid (665,000) - Interim dividend for current year (81,000) - Distribution of reserves (584,000) -

Proceeds and payments relating to financial liability instruments (95,261) (149,785) Proceeds from issue of bank borrowings - Group companies 270,000 1,490,380 Proceeds from issue of borrowings from Group companies 950,000 - Repayment of bank borrowings - Group companies (1,045,261) (1,640,165) Repayment of borrowings from Group companies (270,000) -

NET INCREASE/DECREASE IN CASH AND CASH EQUIVALENTS 73,250 (14,083)

Cash at beginning of year 5,150 13,560 Business unit (Note 2) 129,549 5,673 Cash at end of year 207,949 5,150

9

Translation of financial statements originally issued in Spanish and prepared in accordance with the regulatory financial

reporting framework applicable to the Company (see Notes 2 and 25). In the event of a discrepancy, the Spanish-language

version prevails.

Criteria CaixaHolding, S.A.U. Notes to the financial statements for the year ended 31 December 2013

1. Company activities

Criteria CaixaHolding, S.A.U. ("the Company" or "Criteria"), formerly Servihabitat XXI, S.A.U. (and prior to that Gestora de Microfinances, S.A.U.), was incorporated on 16 December 2003. The resolutions adopted by the Board of Directors on 16 July 2007 whereby the company name was changed from Gestora de Microfinances, S.A.U. to Servihabitat XXI, S.A.U. were executed in a public deed on 25 July 2007. On 18 December 2013, as a result of the merger of Servihabitat XXI, S.A.U. and Criteria CaixaHolding, S.A.U. explained in this same Note, Servihabitat XXI, S.A.U. adopted the name Criteria CaixaHolding, S.A.U.

Its registered office is at Avenida Diagonal 621-629 Barcelona.

The object of Criteria CaixaHolding, S.A.U., per Article 2 of its bylaws, is to carry on the following business activities:

a) the acquisition, sale and management of marketable securities and equity interests in other companies (with both officially listed and unlisted securities);

b) the administration and management of companies and the management and administration of securities representing the equity of entities resident in Spain and non-resident entities;

c) the provision of financial, tax, technical, stock market and any other advisory services;

d) the performance of activities as consultants, advisers and promoters of industrial, commercial, property development, agricultural and any other projects;

e) the construction, refurbishment, maintenance, acquisition, administration, management, development, sale and lease, except under finance lease, of, and provision of technical assistance in relation to, all manner of real property owned by the Company itself or by others.

f) the marketing of real property, for the Company's own account or for the account of third parties, in the broadest terms and by all possible means, including the Internet through the management and use of websites.

The Company may also have interests in other companies, even participating in their incorporation, forming associations with them or having any kind of involvement with them.

The Company forms part of the Caixa d’Estalvis i Pensions de Barcelona Group ("the “la Caixa” Group"), the parent of which is “la Caixa”, whose registered office is at Av. Diagonal, 621-629, 08028, Barcelona and which prepares consolidated financial statements. The consolidated financial statements of the “la Caixa” Group are deposited at the Barcelona Mercantile Registry and are authorised for issue by the legally established deadline, i.e. before 31 March each year. The consolidated financial statements of the “la Caixa” Group for 2013 were formally prepared by the directors of "la Caixa" at the Board of Directors Meeting held on 27 February 2014.

10

In 2013 the following transactions were performed:

Spin-off of the real estate management line of business

On 19 February 2013, the plan for the spin-off of the Company's real estate management line of business was approved, and the assets and liabilities of this business were contributed to the newly-formed company Servihabitat Gestión Inmobiliaria, S.L.U. (see Notes 2 and 9). The spin-off public deed was registered at the Mercantile Registry on 27 March 2013.

Sale of Servihabitat Gestión Inmobiliaria, S.L.U.

On 26 September 2013, it was announced that the Boards of Directors of ”la Caixa”, CaixaBank, S.A., Servihabitat XXI (the absorbing company) and Criteria CaixaHolding, S.A.U. (the absorbed company) had approved the sale, by the Company, of all the shares of Servihabitat Gestión Inmobiliaria, S.L.U. owned by it to CaixaBank, S.A. This transaction was executed in a public deed on 31 October 2013 (see Note 9.1).

Merger of Servihabitat XXI (now Criteria) and Criteria CaixaHolding (see Note 2)

Background

Servihabitat XXI had, itself or through wholly-owned subsidiaries, traditionally been engaging in (i) the acquisition, ownership and sale of all manner of real property –including the assets awarded to ”la Caixa” in payment of debt (up to the date of the reorganisation of the ”la Caixa” Group in 2011, when the ”la Caixa” Group's foreclosed assets were acquired by BuildingCenter (wholly owned by CaixaBank))–; and (ii) the administration, management, operation and marketing, through sale or lease, except under finance lease, of all manner of real property owned by it or by third parties.

As a result of the growing interest of foreign investors in investing in real estate service management platforms (“servicers”) in the Spanish real estate market, the ”la Caixa” Group took the decision to facilitate the entry of an investor in the real estate management business carried on by Servihabitat XXI.

For this reason, in March 2013 Servihabitat XXI span off the real estate asset management business to a wholly-owned subsidiary Servihabitat Gestión Inmobiliaria, S.L.U. (“SGI”). As a result, the acquisition management, development, asset management and marketing business activities that had historically been carried on by Servihabitat XXI started to be carried on by SGI. Therefore, SGI began to provide real estate services for the account of third parties, with no property assets in its balance sheet, managing principally the property assets owned by CaixaBank and Servihabitat XXI.

On 26 September 2013, it was announced that the Boards of Directors of ”la Caixa”, Criteria, Servihabitat XXI and CaixaBank had approved the sale and transfer by SVH XXI to CaixaBank of all the shares of SGI. In addition, on that same date it was made public that the Board of Directors of CaixaBank had approved the sale ‒immediately after the acquisition of SGI from Servihabitat XXI‒ of the business of SGI to a newly-formed company (Servihabitat Servicios Inmobiliarios, S.L.) owned 51% by the fund Texas Pacific Group (TPG) and 49% by CaixaBank. Also, on 26 September 2013 these transactions were published as a “relevant event” on the website of the Spanish National Securities Market Commission (CNMV).

By means of a "relevant event" of 31 October 2013, CaixaBank notified the market (i) that it had acquired all the shares of SGI from a subsidiary of Criteria (Servihabitat XXI); and (ii) that, after having received authorisation from the European competition authorities, it had formalised the sale of SGI's real estate management business to Servihabitat Servicios Inmobiliarios, owned 51% by TPG and 49% by CaixaBank.

11

Accordingly, Servihabitat XXI became a company engaging mainly in the mere ownership of real estate assets.

Raison-d'être for the merger

Based on the circumstances described in the preceding paragraphs, the purpose of the merger was to simplify the part of the ”la Caixa” Group's legal structure in which both Criteria and Servihabitat XXI were included in order to improve the efficiency of the management and business activities of the two companies, since, as a result of the transfer of the real estate management business, the business activities of the two companies were now similar, as they both engaged mainly in the ownership of assets, equity investments in various companies in the case of Criteria, and real estate assets in the case of Servihabitat XXI.

Moreover, having these two companies with separate legal personalities gave rise to unnecessary duplication in terms of their management and administration.

In this context, the directors of Criteria and Servihabitat XXI considered it advisable to promote this merger, with the aim of integrating their assets and thus streamline and rationalise their management structure, taking advantage of economies of scale, facilitate the assignment of resources (human and financial) and simplify the management and control of their businesses.

As a result, on 14 November 2013 the sole shareholders of Servihabitat XXI, S.A.U. and Criteria CaixaHolding, S.A.U. resolved to carry out the merger, in the terms provided for in Articles 22 et seq. of the Spanish Law on structural changes to companies formed under the Spanish Commercial Code, through the absorption of Criteria (the absorbed company) by Servihabitat XXI (the absorbing company), with the dissolution without liquidation of the absorbed company and the transfer en bloc of all its assets and liabilities to the absorbing company, which acquired, by way of universal succession, the assets, rights and obligations of Criteria.

In this regard, Criteria (the absorbed company) now owns directly all the shares of Servihabitat XXI (the absorbing company). The structure chosen is therefore that of a so-called "downstream merger”, whereby a subsidiary absorbs its parent. A downstream merger was chosen rather than an upstream merger because, from the material legal and financial standpoint it makes no difference whether one or other structure is used, since in both cases the post-merger company will have both, in completely equal terms, the assets and liabilities of Criteria (the absorbed company) and Servihabitat XXI (the absorbing company). A downstream merger was chosen for technical reasons in order to simplify the formalities relating to the transaction.

The draft terms of merger were executed in a public deed on 17 December 2013 and were filed at the Barcelona Mercantile Registry on 18 December 2013. The merger was effective for accounting purposes from 1 January 2013.

The sole shareholders of Servihabitat XXI and Criteria resolved to apply to the merger the special tax regime provided for in Chapter VIII of Title VII of the Spanish Income Tax Law.

Also, as a result of the merger, the Company's name was changed and the absorbing company adopted the name of the absorbed company (Criteria CaixaHolding, S.A.U.).

In 2012 the following transactions were performed:

12

Merger of Servihabitat XXI (now Criteria) and Estuimmo, S.A.U., Estuillogimmo, S.L.U., Estuinvest, S.L.U., Estuvendimmo, S.L.U., Norton Center, S.L.U. and Servihabitat Alquiler III, S.A.U.

On 31 May 2012, Criteria CaixaHolding, S.A., the Company's then sole shareholder, resolved to merge the Company's wholly-owned subsidiaries Estuimmo, S.A.U., Estuillogimmo, S.L.U., Estuinvest, S.L.U., Estuvendimmo, S.L.U., Norton Center, S.L.U. and Servihabitat Alquiler III, S.A.U. (the absorbed companies) into Servihabitat XXI, S.A.U. (the absorbing company). The draft terms of merger were executed in a public deed on 6 July 2012 and were filed at the Barcelona Mercantile Registry on 13 July 2012.

Criteria CaixaHolding, S.A.U. meets the requirements in current legislation releasing it from the obligation to present consolidated financial statements provided for in Royal Decree 1159/2010, of 17 September. However, consolidated financial statements in accordance with International Financial Reporting Standards are voluntarily prepared and authorised for issue.

The accompanying financial statements do not reflect the financial position of the group headed by Criteria. These aggregates are presented in the consolidated financial statements prepared, in conjunction with the separate financial statements, in accordance with International Financial Reporting Standards (IFRSs) as adopted by the European Union, the main aggregates in which at 31 December 2013 were as follows:

Millions of euros 2013

Consolidated equity 9,192

Profit for the year attributable to the Group 472

Total consolidated assets 13,091

Revenue 349

2. Basis of presentation of the financial statements

a) Regulatory financial reporting framework applicable to the Company and fair presentation

The accompanying financial statements, which were formally prepared by the directors from the Company's accounting records, are presented in accordance with the regulatory financial reporting framework applicable to the Company, which consists of:

a) The Spanish Commercial Code, the Spanish Law on structural changes to companies formed under the Spanish Commercial Code and all other Spanish corporate law.

b) The Spanish National Chart of Accounts approved by Royal Decree 1514/2007, of 16 November, and its industry adaptations.

c) The mandatory rules approved by the Spanish Accounting and Audit Institute in order to implement the Spanish National Chart of Accounts and the relevant secondary legislation.

d) All other applicable Spanish accounting legislation.

The accompanying financial statements, which were obtained from the Company's accounting records, are presented in accordance with the regulatory financial reporting framework applicable to the Company and, in particular, with the accounting principles and rules contained therein and, accordingly, present fairly the Company's equity, financial position, results of operations and cash flows for 2013.

13

These financial statements, which were authorised for issue by the Board of Directors at its meeting held on 27 March 2014, will be submitted for approval by the sole shareholder, and it is considered that they will be approved without any changes.

The financial statements for 2012 were approved by the sole shareholder on 21 February 2013. The financial statements for 2012 of the absorbed company were approved by the sole shareholder on 11 April 2013.

As a result of the merger indicated in Note 1, the ordinary activities of the Company, understood to be those carried one by the Company regularly and from which revenue was earned on a regular basis in 2013, corresponds to that of a holding company. Therefore, as regards the amounts corresponding to 2013, the Company's directors took into account the ruling published in Official Gazette nº. 79 (published on 28 July 2009) of the Spanish Accounting and Audit Institute (ICAC) in relation to the accounting classification in separate financial statements of the income and expenses of holding companies and to the determination of the revenue of entities of this nature.

Under this ruling, all the income obtained by a company as a result of its holding activities will constitute “Revenue” provided that these activities are considered to be ordinary activities. Therefore, both dividends and income obtained from the disposal of the investments in Group companies, jointly controlled entities and associates, their derecognition or changes in their fair value constitute, on the basis of the foregoing, "Revenue”.

Based on the foregoing and on the premise that the Company's ordinary activities include the strategic and long-term ownership of equity investments in other companies, certain reclassifications were made in the presentation of the Company's income statement.

Following is a detail of the line items forming an integral part of "Revenue":

- "Services": these include the services rendered to other companies;

- "Revenue from Equity Investments": this includes dividends received as a result of the ownership of equity investments in other companies;

- Change in fair value of financial instruments; and

- "Net Gains on Disposals of Financial Instruments".

Impairment and other losses on financial instruments and any exchange differences are included in the Company's profit or loss from operations.

Accordingly, at 31 December 2013 "Inventories" includes solely the land and property developments in progress held by the Company and "Non-Current Assets Classified as Held for Sale" includes the other properties recovered from lending transactions which, at 31 December 2013, the Company expects to recover through sale. The other property assets arising from lending transactions that are rented or are included in the Company's operating assets are classified as "Investment Property" and "Property, Plant and Equipment", respectively.

Pursuant to the ruling of the ICAC, "Financial Loss" is introduced, in which the finance income earned and the finance costs incurred during the year are included. The finance income earned on loans granted to subsidiaries is retained under "Financial Loss", since financing to subsidiaries is not a part of the Company's ordinary activity.

14

b) Non-obligatory accounting principles applied

The directors formally prepared these financial statements taking into account all the obligatory accounting principles and standards with a significant effect hereon. All obligatory accounting principles were applied. No non-obligatory accounting principles were applied.

c) Comparative information

The information contained in these notes to the financial statements at 31 December 2012 is presented for comparison purposes with that relating to 31 December 2013.

Spin-off of the real estate management line of business

Within the framework of the restructuring of the business activities carried on to date by the Company, on 19 February 2013, and effective for accounting purposes from 1 January 2013, Criteria CaixaHolding, S.A.U., the Company's then sole shareholder, approved the plan for the spin-off of the assets and liabilities associated with the Company's real estate management business to a newly-formed company Servihabitat Gestión Inmobiliaria, S.L.U. The spin-off plan was registered at the Barcelona Mercantile Registry on 27 March 2013.

The detail of the asset and liability items included in the spin-off is as follows:

Thousands Thousands

of euros of euros

NON-CURRENT ASSETS:

Intangible assets (Note 5) 4,563

Property, plant and equipment (Note 6) 524

CURRENT ASSETS:

Inventories 1,350

Advances to suppliers (Note 12) 1,350

Trade and other receivables 6,575 CURRENT LIABILITIES:

Receivable from Group companies and associates 6,567 Trade and other payables 2,318

Employee receivables 8 Payable to suppliers - Group companies and associates 624

Cash and cash equivalents 4,820 Remuneration payable 1,550

Cash 4,820 Other accounts payable to public authorities 144

Total assets 17,832 Total liabilities 2,318

Through the aforementioned non-monetary contribution, the Company subscribed and paid all the new shares of the newly-formed company Servihabitat Gestión Inmobiliaria, S.A. (see Note 9.1).

The transaction qualified for taxation under the tax neutrality regime provided for in Chapter VIII of Title VII of the Consolidated Spanish Income Tax Law approved by Legislative Royal Decree 4/2004, of 5 March, since it constitutes a contribution of a line of business in exchange for shares of the beneficiary company regulated by Article 83.3 of the Consolidated Spanish Income Tax Law.

Merger of Servihabitat XXI (now Criteria) and Criteria CaixaHolding

As indicated in Note 1, the Company was the beneficiary of the merger with Criteria CaixaHolding, S.A.U., a ”la Caixa” Group company. This transaction was effective for accounting purposes from 1 January 2013.

15

As a result of this merger and pursuant to Recognition and Measurement Standard 21 of the Spanish National Chart of Accounts, the assets and liabilities of the absorbed company were measured at the amounts that would correspond to them in the consolidated financial statements of the ”la Caixa” Group. The positive difference of EUR 151,170 thousand that arose as a result of the application of the aforementioned method, was allocated, pursuant to that standard, to a reserve account.

The detail of the amounts included in the accounting records of Servihabitat XXI (now Criteria) is as follows:

Criteria CaixaHolding,

S.A.U.

Effect of measurement

per the consolidated

financial statements

Merger

adjustment

Total amounts

included

1 January 2013

Intangible assets (Note 5) 233 - - 233

Property, plant and equipment (Note 6) 1,180 - - 1,180

Non-current investments in Group companies and associates (Note 9)

8,570,478 260,993 (1,360,090) 7,471,381

Non-current financial assets (Note 10) 29,482 - - 29,482

Deferred tax assets (Note 17) 399,574 - - 399,574

NON-CURRENT ASSETS 9,000,947 260,993 (1,360,090) 7,901,850

Trade and other receivables 9 - - 9

Current financial assets (Note 13) 136,778 - - 136,778

Cash and cash equivalents 134,369 - - 134,369

CURRENT ASSETS 271,156 - - 271,156

TOTAL ASSETS 9,272,103 260,993 (1,360,090) 8,173,006

EQUITY (Note 15) 8,947,683 151,170 (1,360,090) 7,738,763

Deferred tax liabilities (Note 17) 216,811 109,823 - 326,634

NON-CURRENT LIABILITIES 216,811 109,823 - 326,634

Current payables 383 - - 383

Payable to Group companies and associates 103,863 - - 103,863

Trade and other payables 3,363 - - 3,363

CURRENT LIABILITIES 107,609 - - 107,609

TOTAL EQUITY AND LIABILITIES 9,272,103 260,993 (1,360,090) 8,173,006

The effects of the measurement of the assets and liabilities at the amounts that would correspond to them in the consolidated financial statements of the ”la Caixa” Group relate basically to the undistributed profits obtained by the Criteria Group companies through 31 December 2012. The merger adjustment relates to the elimination of the investment in Servihabitat XXI held by Criteria (the absorbed company) when the merger took place.

d) Use of judgements and estimates

In preparing the accompanying financial statements estimates were made by the Company's directors in order to measure certain of the assets, liabilities, income, expenses and obligations reported herein. These estimates relate basically to the following:

- The measurement of investments in Group companies, jointly controlled entities and associates (see Note 9)

- Impairment losses on investment property, inventories and non-current assets classified as held for sale (see Notes 4-c, 4-g and 4-h).

16

- The calculation of provisions and contingent liabilities (see Note 9).

- The recognition of tax assets and the recoverability thereof (see Note 17).

- The useful life of and impairment losses on intangible assets and property, plant and equipment (see Notes 5 and 6)

The respective estimates and assumptions are reviewed on an ongoing basis; the effects of the reviews of the accounting estimates are recognised in the period in which they are made, if these only affect that period, or in the period of the review and in future periods. Although these estimates were made on the basis of the best information available at 2013 year-end, events that take place in the future might make it necessary to change these estimates (upwards or downwards) in coming years. Changes in accounting estimates would be applied prospectively.

e) Grouping of items

Certain items in the balance sheet, income statement, statement of changes in equity and statement of cash flows are grouped together to facilitate their understanding; however, whenever the amounts involved are material, the information is broken down in the related notes to the financial statements.

f) Changes in accounting policies

In 2013 there were no significant changes in accounting policies with respect to those applied in the preparation of the information for 2012.

g) Correction of errors

In preparing the accompanying financial statements no significant errors were detected that would have made it necessary to restate the amounts included in the financial statements for 2012.

3. Distribution of profit/Allocation of loss

The distribution of the profit for 2013 proposed by the directors of Criteria CaixaHolding, S.A.U. and the allocation of the loss for 2012 are as follows:

Thousands of euros

2013 2012

Basis of appropriation:

Profit (Loss) for the year 110,055 (815,581)

Appropriation:

To retained losses - (815,581)

To legal reserve 11,006 -

To voluntary reserves 18,049 -

Interim dividends 81,000 -

Total 110,055 (815,581)

17

The Board of Directors of the absorbed company, at its meeting held on 13 June 2013, approved the distribution of an interim dividend of EUR 81,000 thousand out of the profit for 2013, which was paid to ”la Caixa” on 17 June 2013.

The provisional accounting statement prepared in accordance with legal requirements to evidence the existence of sufficient liquidity for the distribution of the aforementioned interim dividend is as follows:

(Thousands of euros)

Date of resolution to pay the interim dividend 13/06/13

Date of accounting close used 31/05/13

Profit obtained from 1 January 2013 272,051

Appropriation to legal reserve -

Maximum amount distributable 272,051

Interim dividend proposed (81,000)

Remainder 191,051

Amounts available in demand deposits 166,234 Projected changes in cash up to date of payment of dividend (172)

Interim dividend (81,000)

Remaining liquidity at date of payment of dividend 85,062

Projected changes in cash in following 12 months 155,172 Remaining liquidity 12 months later 240,234

4. Accounting policies

The principal accounting policies used by the Company in preparing the financial statements for 2013, in accordance with the Spanish National Chart of Accounts in force, were as follows:

a) Intangible assets

Intangible assets are initially recognised at cost and include basically the cost of developing new computer software, the useful life of which was estimated to be three years. They are subsequently reduced by any accumulated amortisation and any accumulated impairment losses.

Whenever there are indications of impairment, the Company tests the intangible assets for impairment to determine whether the recoverable amount of the assets has been reduced to below their carrying amount.

Recoverable amount is the higher of fair value less costs to sell and value in use and, wherever possible, the impairment tests are performed individually for each asset.

Where an impairment loss subsequently reverses, the carrying amount of the asset is increased to the revised estimate of its recoverable amount, but so that the increased carrying amount does not exceed the carrying amount that would have been determined had no impairment loss been recognised in prior years. A reversal of an impairment loss is recognised as income.

b) Property, plant and equipment

Property for own use, furniture and office equipment are recognised at cost less any accumulated depreciation and any accumulated impairment losses.

18

Historical cost includes the expenses directly attributable to the acquisition of property.

Subsequent costs are included in the carrying amount of the asset or are recognised as a separate asset only when it is probable that future economic benefits associated with the item will flow to the Company and the cost of the item can be measured reliably. Other repair and maintenance expenses are recognised in the income statement for the year in which they are incurred.

The Company depreciates its property, plant and equipment for own use and other non-current assets by the straight-line method at annual rates based on the following years of estimated useful life:

Years of estimated useful life

Property:

Buildings 30 - 50

Plant 5 - 12.5

Computer hardware 2 - 3

Other items of property, plant and equipment 4-10

The gains or losses arising on the sale or derecognition of an asset are calculated as the difference between its carrying amount and its selling price, and are recognised under “Impairment and Gains or Losses on Disposals of Non-Current Assets” in the income statement

c) Investment property

“Investment Property” in the balance sheet reflects the values of the land, buildings and other structures held either to earn rentals or for capital appreciation.

Investment property is recognised at cost less any accumulated depreciation and any accumulated impairment losses.

The costs of expansion, modernisation or improvements leading to increased productivity, capacity or efficiency or to a lengthening of the useful lives of the assets are recognised as additions to the cost of the related assets , whereas upkeep and maintenance expenses are charged to the income statement for the year in which they are incurred.

In relation to projects in progress, only the costs of construction and borrowing costs are capitalised, provided that they had been incurred before the assets became ready for their intended use and the duration of the construction work exceeded one year.

The Company did not capitalise any borrowing costs in 2013 or 2012. No borrowing costs had been capitalised at year-end.

Investment property in the course of construction is transferred to "Investment Property" when the assets become ready for use.

The Company depreciates its investment property by the straight-line method at annual rates based on the following years of estimated useful life:

19

Years of estimated useful life

Property:

Buildings 50

Plant 12.5

The rental income earned in 2013 from the aforementioned investment property amounted to EUR 26,667 thousand (2012: EUR 12,599 thousand) (see Note 18-a), and is recognised under “Revenue - Sales” in the accompanying income statement.

Also, most of the repair and maintenance expenses incurred by the Company as a result of the operation of its assets are passed on to the corresponding lessees of the properties (see Note 4-p).

The gains or losses arising on the sale or derecognition of an asset are calculated as the difference between its carrying amount and its selling price, and are recognised under “Impairment and Gains or Losses on Disposals of Non-Current Assets” in the income statement Impairment of investment property and property, plant and equipment-

Periodically, the Company compares the carrying amount of the various items of its investment property with their recoverable amount, which is the higher of value in use and fair value less costs to sell. In order to determine the recoverable amount, the directors considered mainly the appraisals undertaken by independent valuers and whether or not the property was being leased at year-end. Therefore, at the end of each period, the fair value reflects the market conditions of the items of investment property at that date. When the aforementioned recoverable amount of the asset is less than its carrying amount, the Company recognises the appropriate impairment loss with a charge to the income statement.

d) Leases

Leases are classified as finance leases whenever the terms of the lease transfer substantially all the risks and rewards incidental to ownership of the leased asset to the lessee. All other leases are classified as operating leases.

At 31 December 2013, all the leases held by the Company were classified as operating leases.

Operating leases

Lease income and expenses from operating leases are recognised in income on an accrual basis.

Also, the acquisition cost of the leased asset is presented in the balance sheet according to the nature of the asset, increased by the costs directly attributable to the lease, which are recognised as an expense over the lease term, applying the same method as that used to recognise lease income.

A payment made on entering into or acquiring a leasehold that is accounted for as an operating lease represents prepaid lease payments that are amortised over the lease term in accordance with the pattern of benefits provided.

20

e) Investments in Group companies, jointly controlled entities and associates

Group companies are defined as companies with which the Company constitutes a decision-making unit because it owns, directly or indirectly, more than 50% of the voting power, or, even if this percentage is lower, because there are agreements with other shareholders of these companies that give the Company the majority of the voting power.

Jointly controlled entities are defined by the Company as entities that are not subsidiaries but which, under a contractual arrangement, are jointly controlled by it and other unrelated shareholders.

Associates are companies over which the Company directly or indirectly exercises significant influence but which are not subsidiaries or jointly controlled entities. In most cases, significant influence exists when the Company holds 20% or more of the voting power of the investee. However, if less than 20% of the voting power is held, significant influence is deemed to exist when the Company expressly states that it exercises such significant influence and if any of the circumstances provided for in accounting legislation exists, such as (i) the voting rights corresponding to other shareholders are held; (ii) there is sufficient representation on the governing bodies; or (iii) there are agreements among entities.

Equity investments in Group companies, jointly controlled entities and associates are initially recognised at cost, which is equal to the fair value of the consideration given, plus any directly attributable transaction costs. The initial measurement also includes the amount of any pre-emption rights acquired.

These investments are subsequently measured at cost less any accumulated impairment losses.

At least at each reporting date, and whenever there are indications that the carrying amount might not be recoverable, the Company conducts the related impairment tests to quantify the possible write-down. The impairment loss is calculated as the difference between the carrying amount of the investment and its recoverable amount, which is the higher of fair value at that date less costs to sell and the present value of the future cash flows from the investment. Unless there is better evidence of the recoverable amount, it is based on the value of the equity of the investee, adjusted by the amount of the unrealised gains existing at the date of measurement.

Impairment losses recognised and reversed are charged and credited, respectively, to the income statement.

Where an impairment loss reverses, the carrying amount of the investment is increased, but so that the increased carrying amount does not exceed the carrying amount that would have been determined had no impairment loss been recognised.

f) Financial instruments

The Company recognises a financial instrument in its balance sheet when it becomes a party to the contract or legal transaction giving rise to it.

21

a. Financial assets

Financial assets

The Company accounts for its current and non-current financial assets as follows:

a) Loans and receivables

These are financial assets arising from the sale of goods or the rendering of services in the ordinary course of the Company's business, or financial assets which, not having commercial substance, are not equity instruments or derivatives, have fixed or determinable payments and are not traded in an active market.

The Company initially recognises financial assets included in this category at fair value, which is generally the price of the transaction. Transactions maturing within twelve months where there is no contractual interest rate, dividends receivable and capital calls on equity instruments expected to be received at short term are measured at face value, since the effect of not discounting the cash flows is not material.

These financial assets are subsequently measured at amortised cost, and the accrued interest is recognised in profit or loss using the effective interest method. At least once a year, and whenever there is objective evidence that a loan or account receivable has become impaired, the Company conducts an impairment test. Based on these tests, the Company recognises such impairment losses as might be required.

Impairment losses on these financial assets are measured as the difference between their carrying amount and the present value of the future cash flows that they are expected to generate, discounted at the effective interest rate.

Impairment losses recognised and reversed are charged and credited, respectively, to the income statement. Where an impairment loss reverses, the carrying amount of the receivable is increased, but so that the increased carrying amount does not exceed the carrying amount that would have been determined had no impairment loss been recognised.

b) Held-for-trading financial assets

These relate to assets acquired with the intention of selling them in the near term and assets that form part of a portfolio for which there is evidence of a recent actual pattern of short-term profit-taking. This category also includes financial derivatives that are not financial guarantees and that have not been designated as hedging instruments.

These assets are measured at their fair value without deducting such costs to sell as might be incurred. Changes in fair value are recognised in profit or loss.

c) Available-for-sale financial assets

The Company includes in this category financial assets that are not held-for-trading financial assets, financial assets classified as at fair value through profit or loss, held-to-maturity investments, loans and receivables or investments in Group companies, jointly controlled entities and associates. At 31 December 2013, this category included mainly equity investments in listed companies.

Available-for-sale financial assets are initially recognised at the fair value of the consideration given, plus transaction costs.

22

Subsequently, available-for-sale financial assets are measured at fair value and the gains and losses arising from changes in fair value are recognised in equity until the asset is disposed of or it is determined that it has become (permanently) impaired, at which time the cumulative gains or losses previously recognised in equity are recognised in the net profit or loss for the year. In this regard, (permanent) impairment is presumed to exist if the market value of the asset has fallen by more than 40% or if there has been a prolonged fall in market value over a period of 18 months without the value having recovered.

At least at each reporting date the Company tests financial assets not measured at fair value through profit or loss for impairment. Objective evidence of impairment is considered to exist when the recoverable amount of the financial asset is lower than its carrying amount. When this occurs, the impairment loss is recognised in the income statement.

Cash and cash equivalents

The Company recognises under “Cash and Cash Equivalents” cash on hand and in bank accounts, short-term deposits and other highly liquid investments that will mature within three months from the date on which they were arranged.

Derecognition of financial assets

The Company derecognises a financial asset when the rights to the cash flows from the financial asset expire or have been transferred and substantially all the risks and rewards of ownership of the financial asset have also been transferred, such as in the case of firm asset sales, factoring of trade receivables in which the Company does not retain any credit or interest rate risk, sales of financial assets under an agreement to repurchase them at fair value and the securitisation of financial assets in which the transferor does not retain any subordinated debt, provide any kind of guarantee or assume any other kind of risk.

However, the Company would not derecognise financial assets, and would recognise a financial liability for an amount equal to the consideration received if transfers of financial assets were to arise in which substantially all the risks and rewards of ownership were retained, such as in the case of securities loans, note and bill discounting, with-recourse factoring, sales of financial assets subject to an agreement to buy them back at a fixed price or at the selling price plus a lender's return and the securitisation of financial assets in which the transferor retains a subordinated interest or any other kind of guarantee that absorbs substantially all the expected losses.

b. Financial liabilities

Financial liabilities include accounts payable by the Company that have arisen from the purchase of goods or services in the normal course of the Company's business and those which, not having commercial substance, cannot be classed as derivative financial instruments.

Accounts payable are initially recognised at the fair value of the consideration received, adjusted by the directly attributable transaction costs. These liabilities are subsequently measured at amortised cost.

The Company derecognises financial liabilities when the obligations giving rise to them cease to exist.

c. Equity instruments

An equity instrument is a contract that evidences a residual interest in the assets of the Company after deducting all of its liabilities.

23

Equity instruments issued by the Company are recognised in equity at the proceeds received, net of issue costs.

g) Inventories

Inventories, consisting of land and property developments in progress are measured at acquisition or construction cost.

The costs of construction include the direct and indirect expenses required for construction, together with the borrowing costs incurred in financing the building work during the construction phase, provided that the work takes longer than one year to complete.

The Company did not capitalise any borrowing costs in 2013 or 2012. No borrowing costs had been capitalised at year-end.

Advance payments received as a result of purchase option agreements are recognised as advances on inventories and are made on the assumption that the conditions attaching to the options will be fulfilled.

The Company recognises the appropriate write-downs of inventories if their net realisable value is lower than their carrying amount. For the purpose of determining the net realisable value, the Company's directors considered the fair value of the inventories obtained from appraisals performed by independent third-party valuers and the Company’s intention to realise the assets in the short and medium term, for which purpose expectations regarding the evolution of the Spanish property market in the short and medium term were taken into account.

Therefore, at 31 December 2013 the impairment losses recognised reflected both the effects of the appraisals conducted by independent third-party valuers and the other factors referred to above.

h) Non-current assets classified as held for sale

“Non-Current Assets Classified as Held for Sale” includes assets or groups of assets the value of which will be recovered mainly through a sale transaction that is highly likely to occur. The Company includes under this heading items of property, plant and equipment which were not intended for own use or classified as investment property and for which, in any case, there is a disposal plan.

If the assets remain in the balance sheet longer than originally planned, their value is revised in order to recognise any impairment loss that the difficulty in finding buyers or reasonable offers may have brought to light.

These assets or disposal groups are measured at the lower of carrying amount and fair value less costs to sell. The impairment losses arising after capitalisation of these assets are recognised under “Impairment and Gains or Losses on Disposals of Non-Current Assets” in the income statement. If their value subsequently recovers, the increase may be recognised under the same heading in the income statement up to the limit of the impairment losses previously recognised. The assets classified under this heading are not depreciated.

At the reporting date, the Company recognises the appropriate impairment losses when the net realisable value of the assets is lower than their carrying amount. For the purpose of determining the net realisable value, the Company considered the fair value obtained from appraisals performed by independent third-party valuers and the Company’s intention to realise the assets in the short and medium term, for which purpose expectations regarding the evolution of the Spanish property market in the short and medium term were taken into account.

24

Therefore, at 31 December 2013 the impairment losses recognised reflected both the effects of the appraisals conducted by independent third-party valuers and the other factors referred to above.

i) Current / Non-current classification

In the accompanying balance sheet, assets and liabilities maturing within no more than twelve months are classified as current items and those maturing within more than twelve months are classified as non-current items, except for “Inventories”, which are classified as current assets, since they are assets that will be realised in the Company's normal operating cycle. The normal operating cycle is the time between the acquisition of assets for inclusion in the various property developments and the realisation of the related goods in the form of cash or cash equivalents.

Also, bank borrowings are classified as non-current if the Company has the irrevocable right to meet the related payments within more than twelve months from the reporting date.

j) Foreign currency transactions

The Company's financial statements are presented in thousands of euros, since the euro is the Company's functional currency.

All foreign currency transactions are initially translated to euros by applying the exchange rates prevailing at the date of the transaction. Monetary items are translated at year-end at the exchange rates then prevailing. Both foreign exchange losses and exchange gains arising in this process and those arising when the related items are settled are recognised in income in the year in which they arise.

k) Provisions and contingencies

Provisions cover present obligations at the date of preparation of the financial statements arising from past events which could give rise to a loss for the Company that is considered likely to occur and which is certain as to its nature but uncertain as to its amount and/or timing.

Contingent liabilities are possible obligations that arise from past events and whose existence will be confirmed only by the occurrence or non-occurrence of one or more future events not wholly within the Company's control.

The Company's financial statements include all the significant provisions with respect to which it is considered more likely than not that the obligation will have to be settled. Contingent liabilities are not recognised in the financial statements, but rather are disclosed, unless the possibility of an outflow in settlement is considered to be remote.

Provisions are measured at the present value of the best possible estimate of the amount required to settle or transfer the obligation, taking into account the information available on the event and its consequences. Where discounting is used, adjustments made to provisions are recognised as interest cost on an accrual basis.

The compensation to be received from a third party on settlement of the obligation is recognised as an asset, provided that there are no doubts that the reimbursement will take place, unless there is a legal relationship whereby a portion of the risk has been externalised as a result of which the Company is not liable; in this situation, the compensation will be taken into account for the purpose of estimating the amount of the related provision that should be recognised.

25

l) Income tax

The current income tax expense or income is calculated by aggregating the current tax arising from the application of the tax rate to the taxable profit (tax loss) for the year, after deducting the tax relief and tax credits allowable for tax purposes, plus the change in deferred tax assets and liabilities recognised. In this regard, the current tax expense or income is the estimated amount payable or recoverable on the basis of the tax rates in force at the balance sheet date.

Deferred tax assets and liabilities are recognised for all temporary differences between the tax base of assets and liabilities and their carrying amounts. Therefore, the Company recognises a deferred tax liability for all taxable temporary differences that do not constitute the exceptions established in accounting legislation for being able not to recognise such a liability. Deferred tax assets are recognised for all deductible temporary differences, tax assets and tax credits and tax loss carryforwards, to the extent that it is probable that there will be a taxable profit against which the related tax asset can be utilised. The Company files consolidated tax returns (see Note 17) and, accordingly, the deferred tax assets and deferred tax liabilities arising from the eliminations of the results obtained from the transactions performed with other Group companies for the calculation of the consolidated tax base and which may be included in the future are recognised.

Deferred tax assets and liabilities are measured at the tax rates that are expected to apply in the period when the asset is realised or the liability is settled, based on the tax rates and tax laws that have been enacted or substantively enacted by the end of the reporting period.

The tax benefit relating to double taxation and reinvestment tax credits is deducted from the income tax expense for the year in which entitlement to the tax credit arises or is exercised (see Note 17). Compliance with the requirements set forth in current legislation is required in order to be able to use these tax credits.

The income tax expense is recognised in the income statement, unless the tax relates to items recognised directly in equity, in which case the income tax is also recognised in equity.

m) VAT

The Company is taxed under the deductible proportion VAT regime. Therefore, non-deductible input VAT forms part of the acquisition cost of current and non-current assets and of services the supply of which is subject to VAT. n) Revenue and expense recognition

General approach

Revenue and expenses are recognised on an accrual basis, i.e. when the actual flow of the related goods and services occurs, regardless of when the resulting monetary or financial flow arises. Revenue is measured at the fair value of the consideration received, net of discounts and taxes.

Revenue from sales is recognised when the significant risks and rewards of ownership of the goods sold have been transferred to the buyer, and the Company retains neither continuing managerial involvement to the degree usually associated with ownership nor effective control over the goods sold.

Revenue from the rendering of services is recognised by reference to the stage of completion of the transaction at the end of the reporting period, provided the outcome of the transaction can be estimated reliably.

“Revenue” includes the dividends received from financial investments, which are recognised as revenue in the year in which the dividends are declared by the Board of Directors of the related investee.

26

Recognition of sales of property developments and land

The Company recognises revenue from sales of property developments and land when the significant risks and rewards of ownership of the goods sold have been transferred to the buyer.

In all other cases, the cost incurred in the construction of the development is retained in “Inventories”, and the amount received on account of the total selling price is recognised under “Customer Advances” in the accompanying balance sheet.

o) Related party transactions

The Company performs all its transactions with related parties on an arm's length basis. Also, the transfer prices are adequately supported and, therefore, the Company's directors consider that there are no material risks in this connection that might give rise to significant liabilities in the future.

p) Costs charged to lessees

The direct costs of transactions relating to investment property that generated rental income in 2013 and 2012, recognised under “Profit (Loss) from Operations” in the accompanying income statement, amounted to EUR 1,789 thousand and EUR 1,991 thousand, respectively. The amount of these expenses associated with investment property that did not generate rental income is not material.

q) Statement of cash flows

The statement of cash flows was prepared using the indirect method and is made up of the following items:

- Cash flows: inflows and outflows of cash and equivalent financial assets, which are short-term, highly liquid investments that are subject to an insignificant risk of changes in value. They also include the Company’s payments and collections, including interest payments, dividends received and taxes, together with other activities that are not investing or financing activities.

- Operating activities: the principal revenue-producing activities and other activities that are not investing or financing activities.

- Investing activities: the acquisition and disposal of non-current assets and other investments not included in cash and cash equivalents.

- Financing activities: activities that result in changes in the size and composition of the equity and borrowings of the Group companies that are not operating activities. They include the proceeds received as a result of the acquisition by third parties of securities issued by the Company or from loans and other financing instruments granted by banks or third parties, together with the payments made to repay such loans and financing instruments. They also include the dividends paid to shareholders.

r) Termination benefits

Under current legislation, the Company is required to pay termination benefits to employees terminated under certain conditions. Therefore, termination benefits that can be reasonably quantified are recognised as an expense in the year in which the decision to terminate the employment relationship is taken. The accompanying financial statements do not include any provision in this connection, since no situations of this nature are expected to arise.

27

5. Intangible assets

The changes in "Intangible Assets” in the balance sheet in 2013 and 2012 were as follows:

2013

Thousands of euros

31/12/12

Additions due to merger (Note 2)

Disposals due to

spin-off (Note 2)

Additions 31/12/13

Cost: 11,216 769 (11,216) 212 981

Computer software 11,216 769 (11,216) 212 981

Accumulated amortisation: (6,653) (536) 6,653 (144) (680)

Computer software (6,653) (536) 6,653 (144) (680)

Total 4,563 233 (4,563) 68 301

2012

Thousands of euros

31/12/11

Additions due to merger (Note 2)

Additions Disposals 31/12/12

Cost 7,251 18 3,981 (34) 11,216

Computer software 7,251 18 3,981 (34) 11,216

Accumulated amortisation: (4,026) - (2,646) 19 (6,653)

Computer software (4,026) - (2,646) 19 (6,653)

Total 3,225 18 1,335 (15) 4,563

The additions in 2012 relate to improvements to the computer systems that manage the volume of business relating to the property owned by the Company prior to the spin-off of the real estate business in 2013.

The cost of the fully amortised assets still in use at 31 December 2013 amounted to EUR 372 thousand (31 December 2012: EUR 2,263 thousand).

28

6. Property, plant and equipment

The changes in 2013 and 2012 in “Property, Plant and Equipment” in the balance sheet and the most significant information affecting this heading were as follows:

2013

Thousands of euros

31/12/12

Additions due to merger (Note 2)

Reductions due to

spin-off (Note 2) Additions Disposals

Transfers (Note 7) 31/12/13

Cost: 57,590 2,140 (1,361) 916 (246) (56,020) 3,019

Land 18,597 - - - - (18,597) -

Buildings 35,574 - - - (44) (35,530) -

Plant 2,099 999 - 797 (196) (1,893) 1,806

Other 1,320 1,141 (1,361) 119 (6) - 1,213

Accumulated depreciation: (3,198) (960) 837 (543) 71 2,524 (1,269)

Buildings (2,244) - - (180) - 2,424 -

Plant (157) (154) - (237) 66 100 (382)

Other (797) (806) 837 (126) 5 - (887)

Net: 54,392 1,180 (524) 373 (175) (53,496) 1,750

Land 18,597 - - - - (18,597) -

Buildings 33,330 - - (180) (44) (33,106) -

Plant 1,942 845 - 560 (130) (1,793) 1,424

Other 523 335 (524) (7) (1) - 326

Impairment (6,766) - - - - 6,766 -

Total 47,626 1,180 (524) 373 (175) (46,730) 1,750

"Property, Plant and Equipment" included basically an office building located at calle Provençals 39 in Barcelona, in which the Company, together with other companies in the ”la Caixa” Group, carried on their business activity and a building located at the Paseo de la Castellana 186, Madrid, two commercial premises in Marbella (El Capricho shopping centre) and commercial premises in Mallorca located at Gabriel Alomar Villalonga 3. As a result of the transaction to spin off the property management business to Servihabitat Gestión Inmobiliaria, S.L.U. described in Note 2, the Company transferred all of the assets previously intended for own use, to "Investment Property" (see Note 7).

29

2012

Thousands of euros

31/12/11 Additions Disposals

Transfers (Note 7) 31/12/12

Cost: 57,173 433 (16) - 57,590

Land 18,558 39 - - 18,597

Buildings 35,409 165 - - 35,574

Plant 2,097 2 - - 2,099

Other 1,109 227 (16) - 1,320

Accumulated depreciation: (2,142) (1,062) 6 - (3,198)

Buildings (1,404) (840) - - (2,244)

Plant (102) (55) - - (157)

Other (636) (167) 6 - (797)

Net: 55,031 (629) (10) - 54,392

Land 18,558 39 - - 18,597

Buildings 34,005 (675) - - 33,330

Plant 1,995 (53) - - 1,942

Other 473 60 (10) - 523

Impairment (1,186) (2,928) - (2,652) (6,766)

Total 53,845 (3,557) (10) (2,652) 47,626

The cost of the fully depreciated assets still in use at 31 December 2013 amounted to EUR 681 thousand (31 December 2012: EUR 442 thousand).

The Company takes out insurance policies to cover the possible risks to which its property, plant and equipment are subject. At the end of 2013 and 2012 the property, plant and equipment were fully insured against these risks.

7. Investment property

The changes in 2013 and 2012 in “Investment Property” in the balance sheet and the most significant information affecting this heading were as follows:

30

2013

Thousands of euros

31/12/12 Additions Disposals Transfers

(Notes 6 and 12) 31/12/13

Cost: 613,549 9,256 (10,536) 183,543 795,811

Land and buildings 612,695 2,726 (10,536) 181,649 786,534

Plant 854 6,530 - 1,893 9,277

Accumulated depreciation: (13,354) (9,961) 294 (2,525) (25,546)

Land and buildings (12,811) (9,459) 294 (2,425) (24,401)

Plant (543) (502) - (100) (1,145)

Net: 600,195 (706) (10,242) 181,018 770,265

Land and buildings 599,884 (6,733) (10,242) 179,224 762,133

Plant 311 6,028 - 1,793 8,132

Impairment (74,124) (69,154) 2,263 (32,741) (173,756)

Total 526,071 (69,860) (7,979) 148,277 596,509

2012

Thousands of euros

31/12/11

Additions due to merger (Note 1) Additions Disposals

Transfers (Notes 6 and 12) 31/12/12

Cost: 331,186 35,069 22,396 (19,717) 244,615 613,549

Land and buildings 330,395 35,069 22,285 (19,669) 244,615 612,695