Embed Size (px)

Citation preview

Crenshaw Corridor Strategic Plan(Draft) Economic Findings

Presented to

The Crenshaw Corridor Stakeholder Task Force

November 15, 2007

November 15, 2007Crenshaw Corridor Strategy Slide 2

Table of Contents

I. IntroductionII. Understanding of the AssignmentIII. Socio-Demographic OverviewIV. Real Estate Market OverviewV. Supportable Development EstimatesVI. Strategic IssuesVII. Discussion

November 15, 2007Crenshaw Corridor Strategy Slide 3

Introduction - ERA Team

David A. Wilcox, FAICPSenior Vice President

10990 Wilshire Boulevard, Suite 1500Los Angeles, California 90024310.477.9585 FAX: 310.478.1950e-mail: [email protected]

Amitabh Barthakur, AICPPrincipal

10990 Wilshire Boulevard, Suite 1500Los Angeles, California 90024310.477.9585 FAX: 310.478.1950e-mail: [email protected]

Judith TaylorAssociate

10990 Wilshire Boulevard, Suite 1500Los Angeles, California 90024310.477.9585 FAX: 310.478.1950e-mail: [email protected]

November 15, 2007Crenshaw Corridor Strategy Slide 4

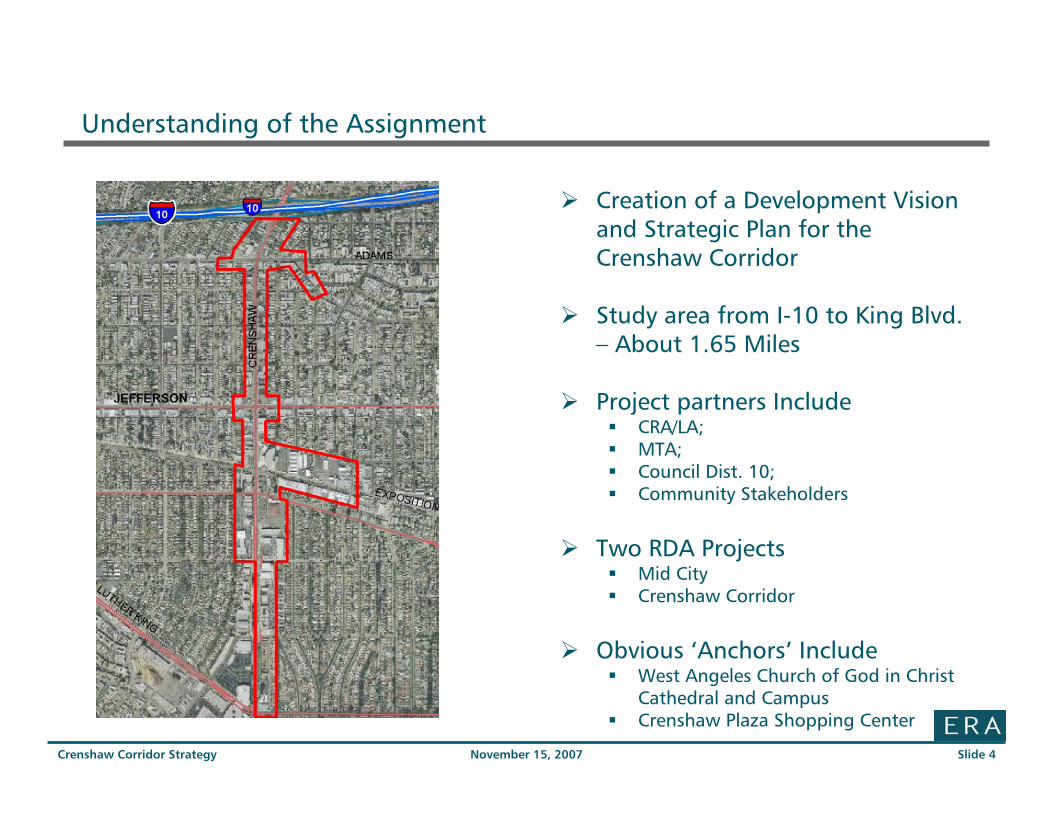

Understanding of the Assignment

Creation of a Development Vision and Strategic Plan for the Crenshaw Corridor

Study area from I-10 to King Blvd. – About 1.65 Miles

Project partners IncludeCRA/LA; MTA; Council Dist. 10; Community Stakeholders

Two RDA ProjectsMid CityCrenshaw Corridor

Obvious ‘Anchors’ IncludeWest Angeles Church of God in Christ Cathedral and CampusCrenshaw Plaza Shopping Center

November 15, 2007Crenshaw Corridor Strategy Slide 5

Understanding of the Assignment

Project Goals

1. Create a regional destination – a pedestrian friendly district

2. Leverages the new light rail extension for transit oriented development

3. Generates employment and supports the local economy

November 15, 2007Crenshaw Corridor Strategy Slide 6

Understanding of the Assignment

Project Opportunities

Exposition Light Rail Transit Station, (operating in 2010)

Participation/Interest of community institutions holding a number of parcels along the corridor, including

• The West Angeles Church of God in Christ and

• Ward EDC

New light rail station with TOD opportunities

Participation/Interest of private land owners

Proven success of redevelopment projects

November 15, 2007Crenshaw Corridor Strategy Slide 7

Analysis Zone

Upper Crenshaw District

The Crenshaw Corridor will Capture Demand for Various Land Uses from a Larger Local and Regional Market

However, the Corridor Itself is a Fairly Narrow Analysis Area in the Context of Regional Market Demand Analysis

For Analysis purposes ERA Defined the Analysis Area as Census Tracts Within a 1-Mile ring of the Corridor Center

This Area Also Represents Primary Resident Market Base

November 15, 2007Crenshaw Corridor Strategy Slide 8

Demographic Profile (2005)

3.08 2.93 2.65 Persons/HH

3,247,0771,322,15325,769Households

9,998,3713,879,96468,333Population

Los Angeles County

City of Los Angeles

Upper Crenshaw District

Source: ESRI 2005, ERA

November 15, 2007Crenshaw Corridor Strategy Slide 9

Demographic Profile (2005) – Age Cohorts

Source: ESRI 2005, ERA

80%

90%

100%

110%

120%

130%

140%

Unde

r 5 ye

ars

5 to 9

years

10 to

14 ye

ars

15 to

19 ye

ars

20 to

24 ye

ars

25 to

29 ye

ars

30 to

34 ye

ars

35 to

39 ye

ars

40 to

44 ye

ars

45 to

49 ye

ars

50 to

54 ye

ars

55 to

59 ye

ars

60 to

64 ye

ars

65 to

69 ye

ars

70 to

74 ye

ars

75 to

80 ye

ars

80 to

85 ye

ars

85 ye

ars an

d ove

r

Crenshaw as % of City of LACrenshaw as % of LA County

The analysis area contains a higher proportion population aged under 14 years and over 60 years compared to regional averages

November 15, 2007Crenshaw Corridor Strategy Slide 10

Demographic Profile (2005) – Racial Distribution

11.7%

56.0%

0.6% 3.9

%

0.1%

22.8%

4.9%

44.6%

10.4%

0.7%

10.4%

0.2%

27.9%

5.8%

46.1%

9.2%

0.8%

12.4%

0.3%

25.7%

5.6%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

White African American AmericanIndian/Alaska

Native

Asian Asian/PacificIslander

Some other racealone

Two or moreraces

Crenshaw DistrictCity of Los AngelesLos Angeles County

Source: ESRI 2005, ERA

The African Americans comprise 56 percent of total population the analysis area compared to 10.4 percent in the City of L.A. and 9.2 percent in L.A. County

November 15, 2007Crenshaw Corridor Strategy Slide 11

Demographic Profile (2005) – Hispanic Population

36.9%

50.6%48.7%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

Crenshaw District City of Los Angeles Los Angeles County

Source: ESRI 2005, ERA

The analysis area contains a lower share of Hispanic population compared to the City of L.A. and L.A. County

November 15, 2007Crenshaw Corridor Strategy Slide 12

Demographic Profile (2005) – Household Income

0%

20%

40%

60%

80%

100%

120%

140%

160%

180%

200%

Less than $20,000 $20,000 - $34,999 $35,000 - $49,999 $50,000 - $99,000 $100,000 or more

Crenshaw as % of City of LACrenshaw as % of LA County

Source: ESRI 2005, ERA

The analysis area contains a significantly higher share of lower households earning under $35,000 annually compared to the City of L.A. and L.A. County

November 15, 2007Crenshaw Corridor Strategy Slide 13

Demographic Profile (2005) – Housing Tenure

29%38%

48%

64%57%

48%

7% 5% 4%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Crenshaw District City of Los Angeles Los Angeles County

VacantRenter-occupiedOwner-occupied

Source: ESRI 2005, ERA

64 percent of the housing units in the analysis area are renter-occupied compared to only 48 percent renter occupied units countywide. 7 percent of total units are vacant

November 15, 2007Crenshaw Corridor Strategy Slide 14

Demographic Profile – Project Annual Growth 2005-2030

0.78%

0.80%

0.82%

0.84%

0.86%

0.88%

0.90%

0.92%

0.94%

0.96%

0.98%

1.00%

Population Households Employment

Crenshaw DistrictCity of Los AngelesLos Angeles County

Source: ESRI 2005, ERA

SCAG’s long term projections for the analysis area show higher growth rates for population, dwelling units and employment compared to the City of L.A.

November 15, 2007Crenshaw Corridor Strategy Slide 15

Corridor and District Business Volumes

Crenshaw Corridor Study Area Vicinity

Tax YearNo. of

EstablishmentsApprox. Revenue

(Mill)2004 356 $1482005 362 $1532006 346 $135

Source: City of Los Angeles, Office of Finance,

Division Establishments Employees Revenue ($ Mill.)Agriculture, Forestry and Fishing 21 102 4Construction 120 553 108Fin. Services, Real Estate, Insurance 193 1,304 264Manufacturing 84 773 73Mining 0 0 0Retail Trade 576 4,937 506Services 903 7,402 640Transportation, Comm., & Utilities 65 809 64Wholesale Trade 66 591 106Total 2,028 16,471 1,765Source: Claritas 2007, Economics Research Associates

November 15, 2007Crenshaw Corridor Strategy Slide 16

Largest Employer Groups (2007)

Source: Claritas, ERA

Largest Employer Groups

- 500 1,000 1,500 2,000

Educational Services

Eating & Drinking Places

Business Services

Social Services

Health Services

Personal Services

General Merchandise Stores

Miscellaneous Retail

Food Stores

Real Estate

Apparel & Accessory Stores

Special Trade Contractors

Jobs

November 15, 2007Crenshaw Corridor Strategy Slide 17

Office Market Profile

Total RBA in the 3 Zip Area (90016, 90018 and 90008) is 990k s.f. while the 1-mile ring contains 370k s.f.No new space added during the last decadeMost of the office inventory is Class B and Class C space with lower vacancies in Class C buildingsWest Angeles EDC is adding 45k s.f. of new space

Period Buildings Total RBAAvg. Annual Vacancy Rate

Delivered RBA Avg. FS Rent/s.f./Yr.

2007 YTD 66 992,905 9.4% 0 $2.562006 66 992,905 2.0% 0 $1.732005 66 992,905 3.6% 0 $1.522004 66 992,905 7.1% 0 $1.272003 66 992,905 8.2% 0 $1.382002 66 992,905 10.3% 0 $1.432001 66 992,905 11.1% 0 $1.592000 66 992,905 17.3% 0 $1.571999 66 992,905 10.8% 0 $1.301998 66 992,905 10.1% 0 $1.191997 66 992,905 7.7% 0 $1.26

November 15, 2007Crenshaw Corridor Strategy Slide 18

Retail Market Profile

Period # Bldgs Total RBATotal Vacant

SFTotal Vacant

%Total Net

Absorption

Direct Average

Rate NNN2007 YTD 148 2,683,611 65,566 2.4% (32,695) $2.69

2006 146 2,677,974 71,406 2.7% 94,918 $3.282005 144 2,611,811 73,130 2.8% 18,516 $2.152004 143 2,601,810 61,934 2.4% (10,105)2003 141 2,588,763 55,700 2.2% 19,9122002 141 2,584,485 30,279 1.2% (58,100) 2001 140 2,571,295 1,500 0.1% 25,409 2000 136 2,480,908 3,125 0.1% 174,553 1999 131 2,375,036 4,875 0.2% 4,724 1998 129 2,369,432 1,500 0.1% 55,106 1997 126 2,315,227 1,625 0.1% 0

Source: CoStar, Economics Research Associates

Total RBA in the 3 Zip Area (90016, 90018 and 90008) is 2.7 million s.f.Total RBA in the 1-mile ring is 1.9 million s.f. (1.2 million s.f. excluding the mall)Only 368k s.f. of retail space has been added in the 3 zip code area since 1997. The $18 Million Coliseum Center is one of the newest developmentsSeveral other retail/mixed use projects are planned including a major refurbishment of the Mall

November 15, 2007Crenshaw Corridor Strategy Slide 19

Housing Market Profile – For Sale Housing

November 15, 2007Crenshaw Corridor Strategy Slide 20

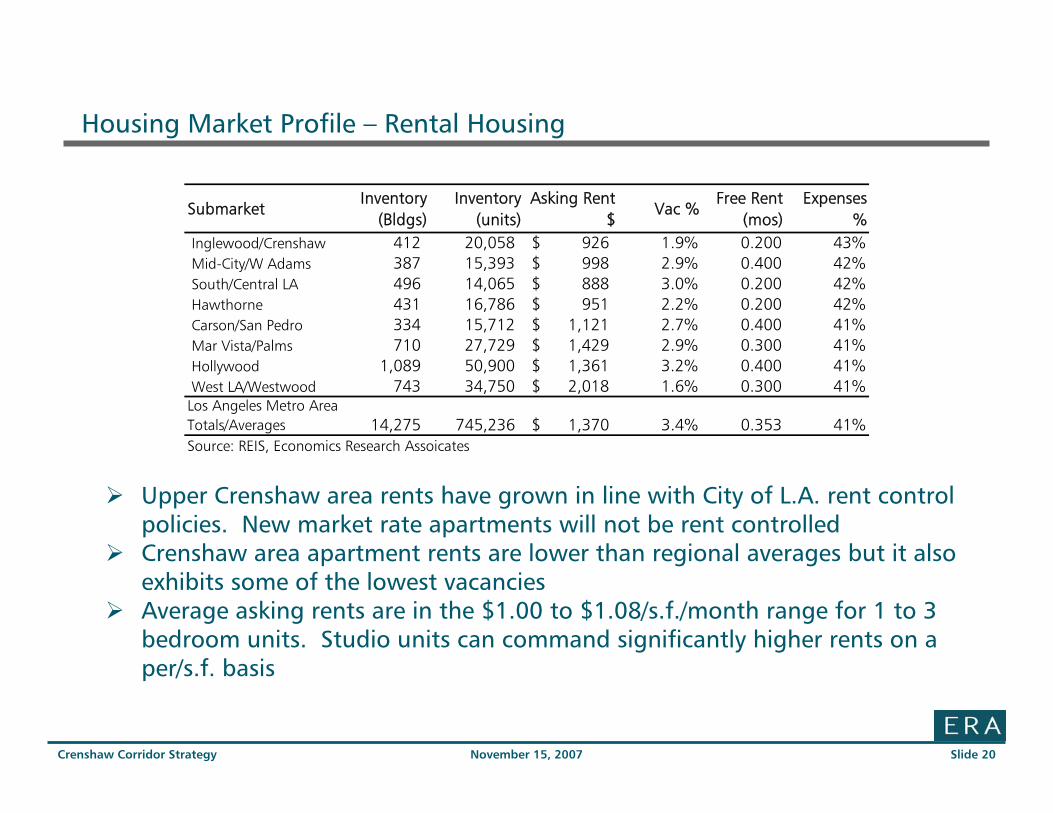

Housing Market Profile – Rental Housing

SubmarketInventory

(Bldgs)Inventory

(units)Asking Rent

$Vac %

Free Rent (mos)

Expenses %

Inglewood/Crenshaw 412 20,058 926$ 1.9% 0.200 43% Mid-City/W Adams 387 15,393 998$ 2.9% 0.400 42% South/Central LA 496 14,065 888$ 3.0% 0.200 42% Hawthorne 431 16,786 951$ 2.2% 0.200 42% Carson/San Pedro 334 15,712 1,121$ 2.7% 0.400 41% Mar Vista/Palms 710 27,729 1,429$ 2.9% 0.300 41% Hollywood 1,089 50,900 1,361$ 3.2% 0.400 41% West LA/Westwood 743 34,750 2,018$ 1.6% 0.300 41%Los Angeles Metro Area Totals/Averages 14,275 745,236 1,370$ 3.4% 0.353 41%Source: REIS, Economics Research Assoicates

Upper Crenshaw area rents have grown in line with City of L.A. rent control policies. New market rate apartments will not be rent controlled Crenshaw area apartment rents are lower than regional averages but it also exhibits some of the lowest vacanciesAverage asking rents are in the $1.00 to $1.08/s.f./month range for 1 to 3 bedroom units. Studio units can command significantly higher rents on a per/s.f. basis

November 15, 2007Crenshaw Corridor Strategy Slide 21

Demand Estimates – Job Space (Crenshaw District)

20,000 22,000 14,000 --Low

64,000 60,000 49,000 17,000 -Mid

80,000 77,000 65,000 47,000 -High

2025-20302020-20252015-20202010-20152007-2010

Source: ERA

5-Year Absorption Estimates (s.f.)

November 15, 2007Crenshaw Corridor Strategy Slide 22

Demand Estimates – Residential Units (Crenshaw District)

658 727 803 855 491 Low

1,480 1,453 1,405 1,283 622 Mid

1,644 1,635 1,606 1,497 753 High

2025-20302020-20252015-20202010-20152007-2010

Rental Units 5-Year Absorption Estimates

Source: ERA

November 15, 2007Crenshaw Corridor Strategy Slide 23

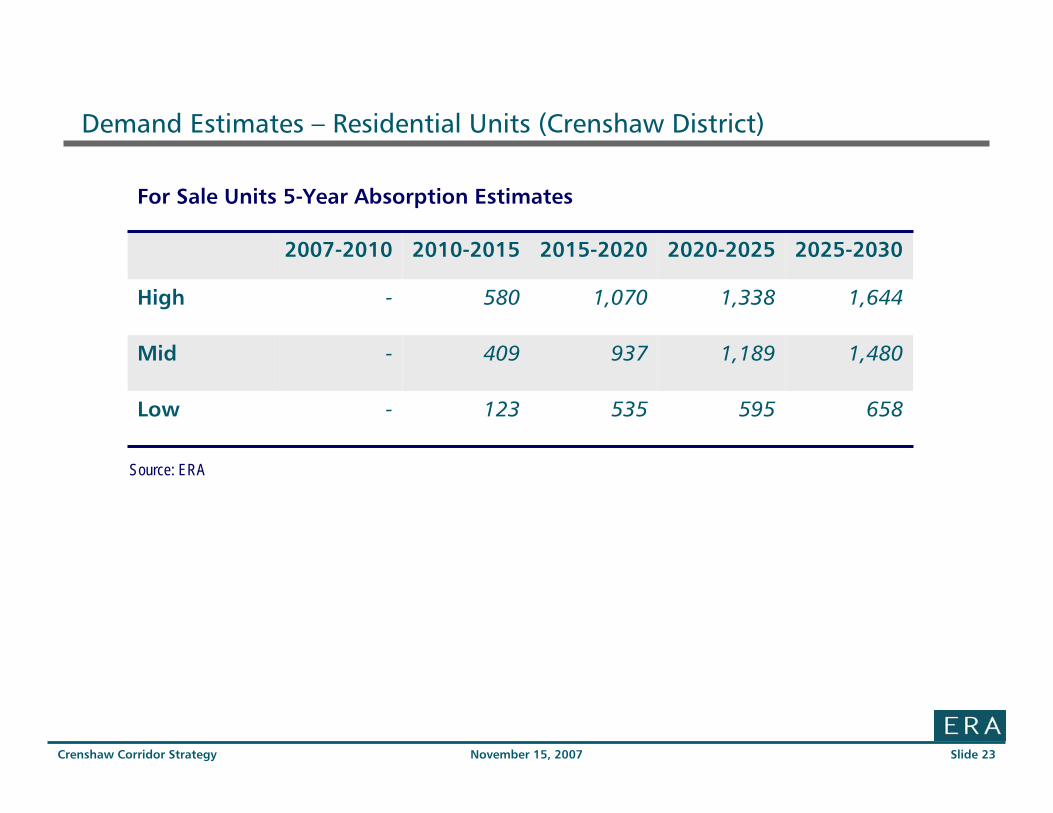

Demand Estimates – Residential Units (Crenshaw District)

658 595 535 123 -Low

1,480 1,189 937 409 -Mid

1,644 1,338 1,070 580 -High

2025-20302020-20252015-20202010-20152007-2010

For Sale Units 5-Year Absorption Estimates

Source: ERA

November 15, 2007Crenshaw Corridor Strategy Slide 24

Demand Estimates – Retail (Crenshaw District)

Estimated Retail Demand (2007-2020)

Additional Capture from Current Residents 65,200 s.f.

New Households (Assuming 5,000 new units) 129,200 s.f.

Additional Capture from Current Area Draw 50,000 s.f.

Total Estimates New Supportable Retail Space (2020) 244,400 s.f.

Source: ERA

November 15, 2007Crenshaw Corridor Strategy Slide 25

Strategic Issues

Apartment Market evolving into ownershipAffordabilityMarket supportRetain / Attract younger workforce

Capture an increased share of community serving office spaceWe are a net exporter of jobsSeniors and emerging businesses demand unique servicesAttract limited medical servicesBusiness services

Live work units to enhance residual on-site activity and catalyze entrepreneurial activities

Already a cluster of regional serving retail – attract a cluster of destination retail and services capitalizing on existing patronage to the area, new employees, and residents

Selective up-front investments in key public improvements – streetscape, landscaping etc., are critical for success

November 15, 2007Crenshaw Corridor Strategy Slide 26

QUESTIONS