Embed Size (px)

Citation preview

CREDIT RATINGS CONSERVATISM AND EARNINGS MANAGEMENT

A DISSERTATION SUBMITTED TO THE GRADUATE DIVISION OF THE

UNIVERSITY OF HAWAI‘I AT MĀNOA IN PARTIAL FULFILLMENT OF THE

REQUIREMENTS FOR THE DEGREE OF

DOCTOR OF PHILOSOPHY

IN

BUSINESS ADMINISTRATION

AUGUST 2017

By

Kunsu Park

Dissertation Committee:

Jian Zhou, Chairperson

S. Ghon Rhee

John Wendell

Liming Guan

Inessa Love

Keywords: Credit Ratings Conservatism, Earnings Management

ii

DEDICATION

I dedicate this dissertation to my family. A very special dedication goes to my

parents, Jongoh Park and Jeongkeun Oh, who always encourage me to pursue this study

and to continue my education in the fields of economics, management and administrative

science (MAS), finance and accounting. My parents always give me unconditional love

and support. I would like to dedicate this work to my first younger sister Kyeongok Park,

brother-in-law Kitae Hong, and two nephews Hayoon Hong and Haram Hong, for their

unwavering love and support. I would also like to dedicate this work to my second

younger sister Kyungja Park, brother-in-law Wooseong Jin, and two nephews Jonghwa

Jin and Jonghyun Jin, for their constant love and support.

iii

ACKNOWLEDGEMENTS

I would like to thank all my committee members, Dr. Jian Zhou, Dr. S. Ghon

Rhee, Dr. John Wendell, Dr. Liming Guan, and Dr. Inessa Love, for their valuable

comments and inspiring discussions, and continued guidance. In particular, my

dissertation advisor Dr. Jian Zhou has always given me plenty of advice, support, and

encouragement during my Ph.D. studies. I would also like to express my deepest

gratitude and special thanks to Dr. S. Ghon Rhee for his continued support, inspiration,

guidance, and encouragement throughout the journey of this dissertation. He has been an

exceptional academic mentor to me. Without their support and guidance, I would not

have been able to complete this dissertation.

I would also like to thank Dr. Boochun Jung, Dr. Shirley Daniel, Dr. Hamid

Pourjalali, Dr. David Yang, Dr. Tom Pearson, Dr. Roger Debreceny, Dr. Wei Huang, Dr.

Qianqiu Liu, Dr. Sang-Hyop Lee, Dr. Song K. Choi, and Dr. Kentaro Hayashi for their

support, encouragement, and kind assistance during my Ph.D. studies. In particular, Dr.

Song K. Choi has given me invaluable advice and support through all stages of my work.

Dr. Boochun Jung always gives me valuable comments and suggestions regarding my

work. I would like to acknowledge Dr. Mark Anderson, who encouraged me to pursue

my Ph.D. studies in the field of accounting.

I would like to express my appreciation to my Ph.D. colleagues for their

continued support and motivation. Among those who deserve special recognition are

iv

James Youn, Cheol-Rin Park, Jaeseong Lim, Jaisang Kim, Youngbin Kim, and Jin Suk

Park. I also want to express my thanks to my friends for their encouragement and

unconditional love. Those who deserve special thanks are Kyung Sung Jung, Young

Kwark, Jongmin Kim, Tong Hyouk Kang, Soonchul Hyun, Joo Hyung Lee, Jangho Gil,

Jong-Min Oh, Seong K. Byun, Sung Hoon Woo, YoungJae Kim, Hojin Jung, Minwoo

Lee, Sang Baum Solomon Kang, Sung Bok Lee, Jason Shin, Hyunsuk Jang, Chris Choi,

Dong Wook Huh, Kwondo Song, and Soonsup Hong.

I would also like to acknowledge Nicole Kurashige and Avree Ito-fujita for their

assistance and guidance in helping me to improve English writing skills during my Ph.D.

studies. I would like to thank Rosemarie Woodruff and Adam Pang for your continued

encouragement and assistance. I would also like to thank Bumhwan Jeon, Kara

Youngshim Bang, and Dawna Kim for unconditionally supporting me throughout my

studies.

Last but not least, I would like to thank Dr. Young Mok Choi and Dr. Se Hun Lim

for their motivation, support, and assistance during my studies.

v

ABSTRACT

I examine whether ratings conservatism influences a firm’s earnings management.

First, total earnings management, calculated as the sum of real and accrual-based

earnings management measures, increases in response to ratings conservatism. Ratings

conservatism leads to a substitution between real and accrual-based earnings

management, indicating that the increase in real earnings management is greater than the

decrease in accrual-based earnings management. Next, the negative relation between

ratings conservatism and accrual-based earnings management is more pronounced for

firms with low credit quality than for those with high credit quality. However, the

positive relation between ratings conservatism and real earnings management does not

apply to both investment- and speculative-grade firms. The results are robust to sample

selection bias, alternative measures of accrual-based earnings management, alternative

industry classifications, alternative cut-off years employed when measuring ratings

conservatism, the effect of external events, omitted variable bias, and different

specifications for ratings models. In addition, there is no evidence of earnings smoothing

and asymmetric timeliness loss recognition relating to ratings conservatism. Overall, this

study finds that ratings conservatism affects a firm’s incentive to manage its reported

earnings. This study also represents the first step towards understanding how ratings

conservatism influences the earnings management behaviors of managers.

vi

TABLE OF CONTENTS

DEDICATION................................................................................................................... ii

ACKNOWLEDGEMENTS ............................................................................................ iii

ABSTRACT ....................................................................................................................... v

LIST OF TABLES ........................................................................................................... ix

LIST OF FIGURES ....................................................................................................... xiii

INTRODUCTION ..................................................................................... 1 CHAPTER 1

RELATED LITERATURE AND HYPOTHESES DEVELOPMENTCHAPTER 2

............................................................................................................................... 13

2.1 Credit Ratings and Earnings Management .............................................................. 13

2.2 Stringent Trends in Rating Standards (“Ratings Conservatism”) ........................... 16

2.3 Ratings Conservatism and Earnings Management .................................................. 18

RESEARCH DESIGN ............................................................................ 28 CHAPTER 3

3.1 Measuring Credit Ratings Conservatism ................................................................. 28

3.2 Measures of Earnings Management ........................................................................ 31

3.2.1 Accrual-Based Earnings Management (AEM) ............................................. 31

3.2.2 Real Earnings Management (REM) .............................................................. 32

3.2.3 Total Earnings Management (TEM) ............................................................. 35

3.3 Baseline Regression Model ..................................................................................... 35

vii

SAMPLE SELECTION AND ESTIMATION OF RATINGS CHAPTER 4

MODELS ............................................................................................................. 41

4.1 Data Selection ......................................................................................................... 41

4.2 Ratings Models ........................................................................................................ 42

4.2.1 Data Description ............................................................................................ 42

4.2.2 Estimating Ratings Models ........................................................................... 42

RESULTS ................................................................................................. 44 CHAPTER 5

5.1 Descriptive Statistics and Correlations ................................................................... 44

5.2 Relation between Ratings Conservatism and Accrual-Based Earnings Management:

Testing H1 ......................................................................................................................... 46

5.3 Relation between Ratings Conservatism and Real Earnings Management: Testing

H1 50

5.4 Relation between Ratings Conservatism and Total Earnings Management ........... 53

5.5 Investment- and Speculative-Grade Firms (Accrual-Based Earnings Management):

Testing H2 ......................................................................................................................... 54

5.6 Investment- and Speculative-Grade Firms (Real earnings management): Testing H2

58

POTENTIAL SAMPLE SELECTION BIAS ....................................... 61 CHAPTER 6

ADDITIONAL ANALYSES ................................................................... 63 CHAPTER 7

7.1 Ratings Conservatism and Earnings Smoothing (EM_SMOOTH) ......................... 63

7.2 Ratings Conservatism and Asymmetric Timely Loss Recognition ........................ 67

viii

ROBUSTNESS TESTS ........................................................................... 73 CHAPTER 8

8.1 Alternative Measures of Accrual-Based Earnings Management ............................ 73

8.2 Using Alternative Industry Classifications When Calculating Ratings Conservatism

and Earnings Management Proxies ................................................................................... 77

8.3 Alternative Cut-Off Years Employed When Measuring Ratings Conservatism ..... 79

8.4 Controlling for the Effect of the Global Financial Crisis of 2007-2008 ................. 80

8.5 Possibility of Omitted Variable Bias ....................................................................... 81

8.6 Re-estimation of the Regression Equation (8) ........................................................ 82

8.7 Validity of the Ratings Model ................................................................................. 83

8.8 Role of Accounting Quality in the Assignment of Credit Ratings .......................... 84

CONCLUSION ........................................................................................ 86 CHAPTER 9

LIMITATIONS AND FUTURE RESEARCH ................................... 88 CHAPTER 10

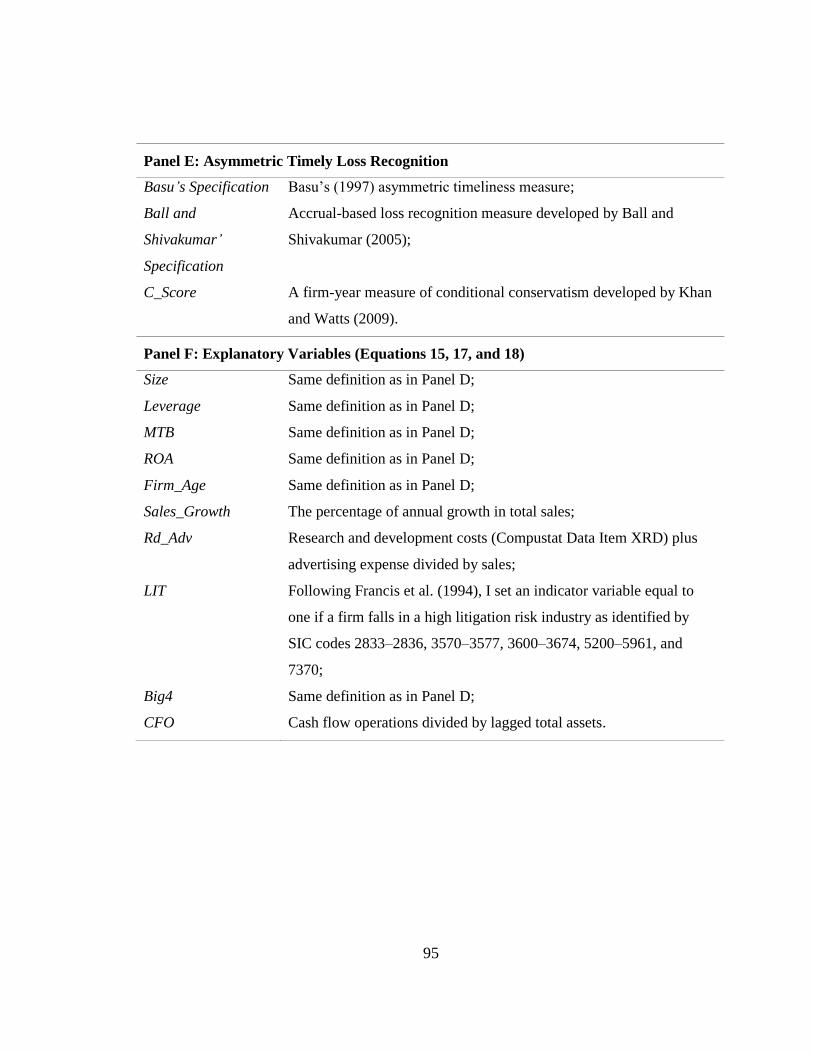

APPENDIX A VARIABLE DEFINITIONS: RATINGS MODEL ............................ 90

APPENDIX B VARIABLE DEFINITIONS: BASELINE REGRESSION MODEL91

APPENDIX C MEASURE OF ASYMMETRIC TIMELY LOSS RECOGNITION:

Khan and Watts’ C_Score (2009, p. 136) .......................................................... 96

REFERENCES .............................................................................................................. 158

ix

LIST OF TABLES

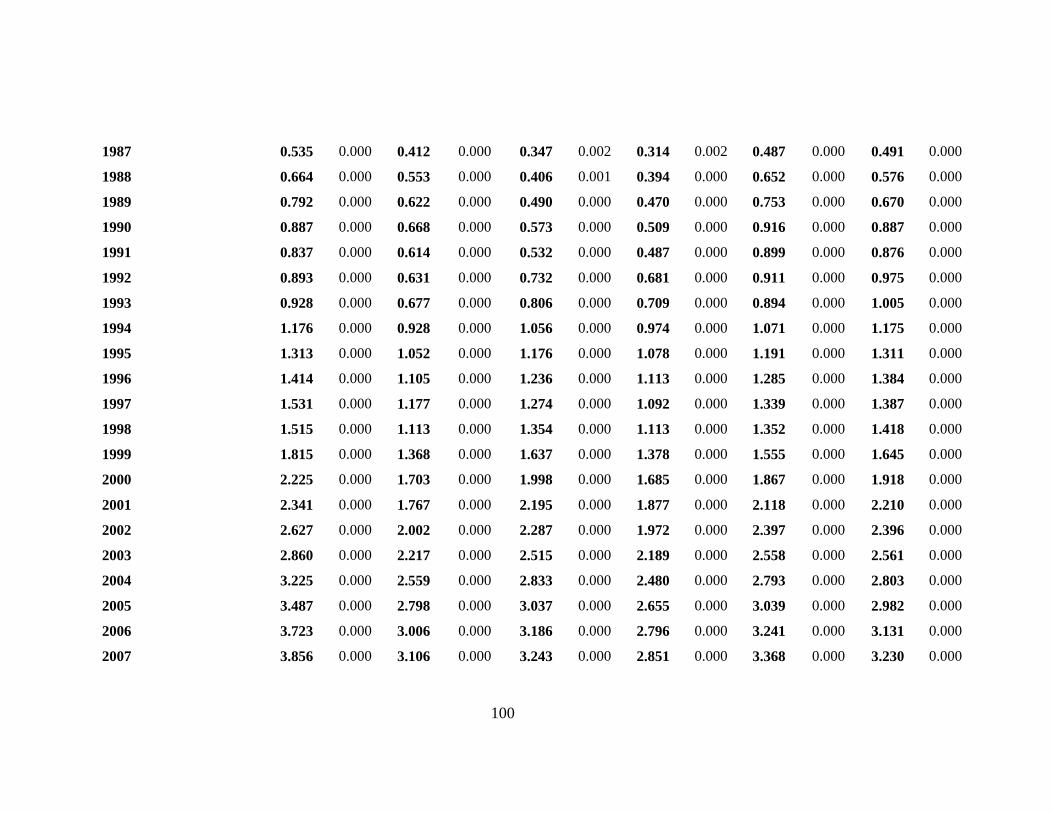

Table 1 Number of Firms by S&P Credit Ratings Categories and Year, 1985-2014

(CHAPTER 4) ........................................................................................................... 97

Table 2 Summary Statistics for Relevant Variables used in Ratings Models

(CHAPTER 4) ........................................................................................................... 98

Table 3 Ratings Models (CHAPTER 4) ....................................................................... 99

Table 4 Descriptive Statistics (CHAPTER 5) ............................................................. 102

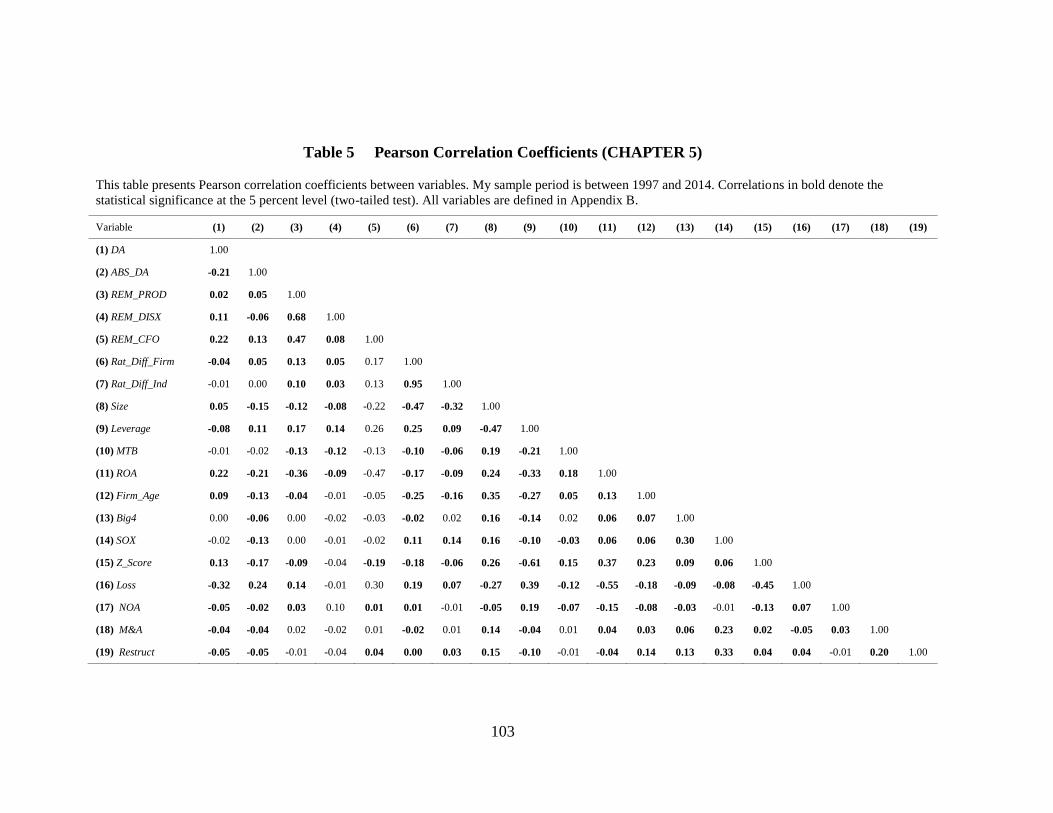

Table 5 Pearson Correlation Coefficients (CHAPTER 5) .......................................... 103

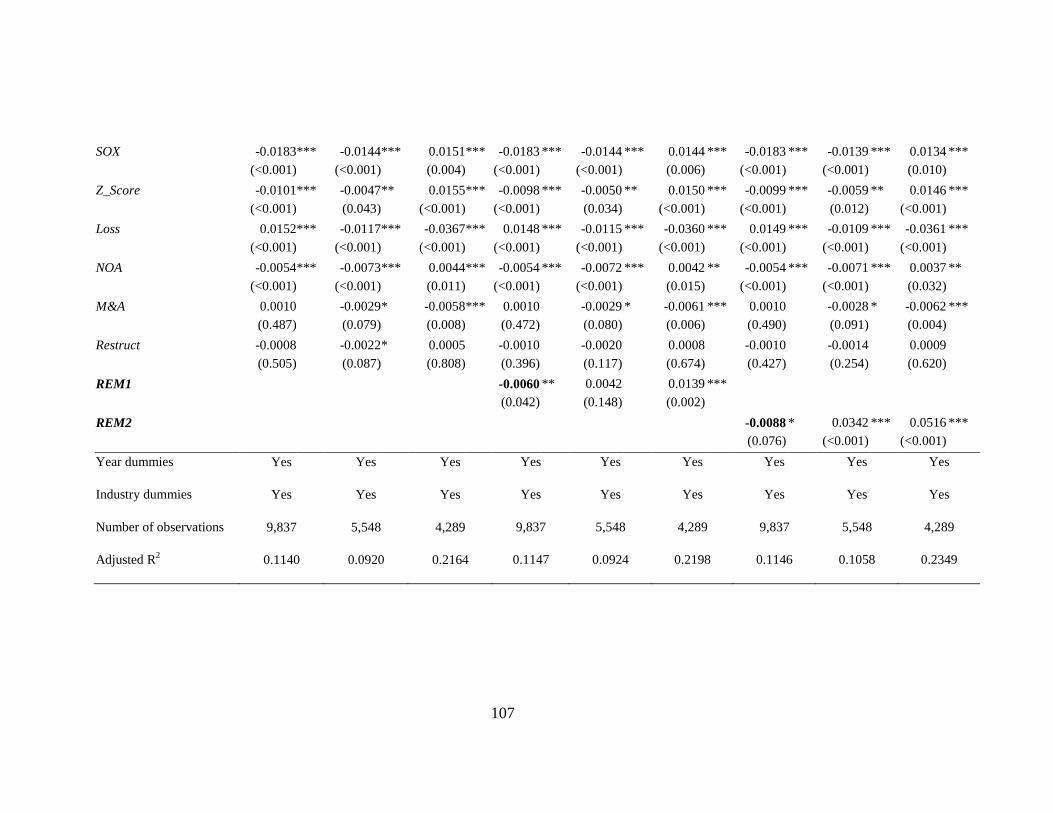

Table 6 Relation between Ratings Conservatism and Accrual-Based Earnings

Management (Testing H1 using the ratings conservatism measure, Rat_Diff_Firm)

(CHAPTER 5) ......................................................................................................... 104

Table 7 Relation between Ratings Conservatism and Accrual-Based Earnings

Management (Testing H1 using the ratings conservatism measure, Rat_Diff_Ind)

(CHAPTER 5) ......................................................................................................... 106

Table 8 Relation between Ratings Conservatism and Real Earnings Management

(Testing H1 using the ratings conservatism measure, Rat_Diff_Firm) (CHAPTER 5)

................................................................................................................................. 108

Table 9 Relation between Ratings Conservatism and Real Earnings Management

(Testing H1 using the ratings conservatism measure, Rat_Diff_Ind) (CHAPTER 5)

................................................................................................................................. 110

x

Table 10 Relation between Ratings Conservatism and Total Earnings Management

(Testing H1 using TEM1) (CHAPTER 5) ............................................................... 112

Table 11 Relation between Ratings Conservatism and Total Earnings Management

(Testing H1 using TEM2) (CHAPTER 5) ............................................................... 114

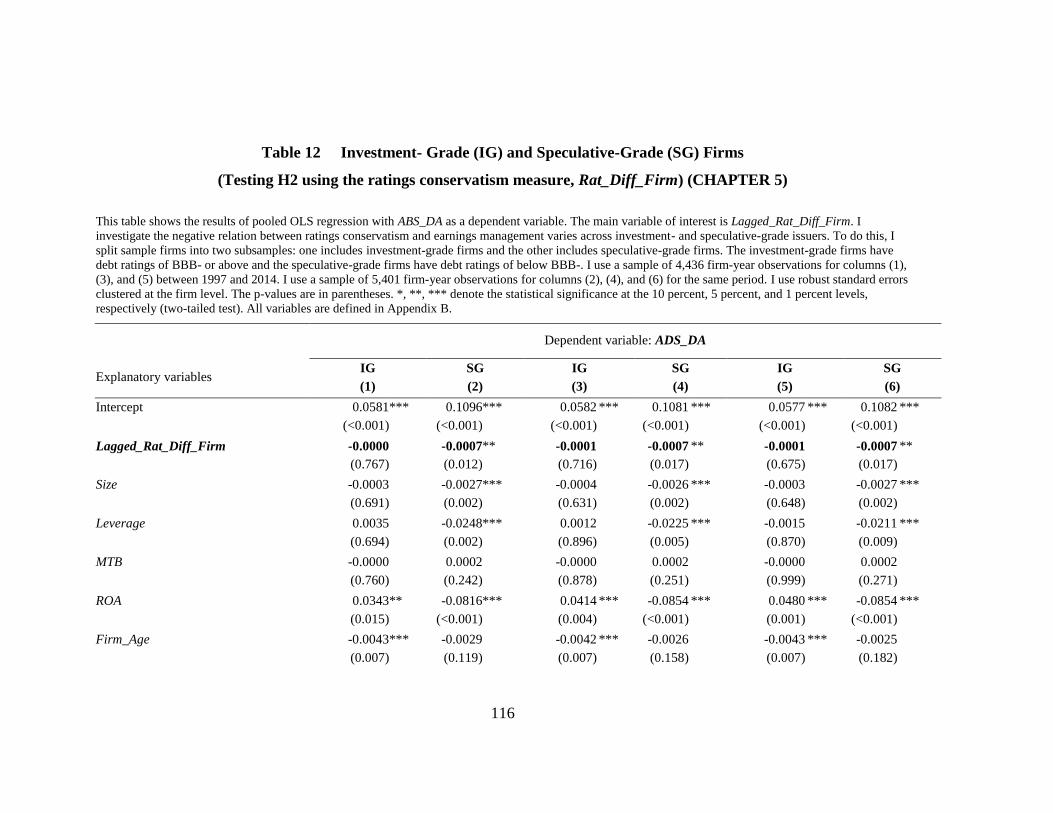

Table 12 Investment- Grade (IG) and Speculative-Grade (SG) Firms

(Testing H2 using the ratings conservatism measure, Rat_Diff_Firm) (CHAPTER 5)

................................................................................................................................. 116

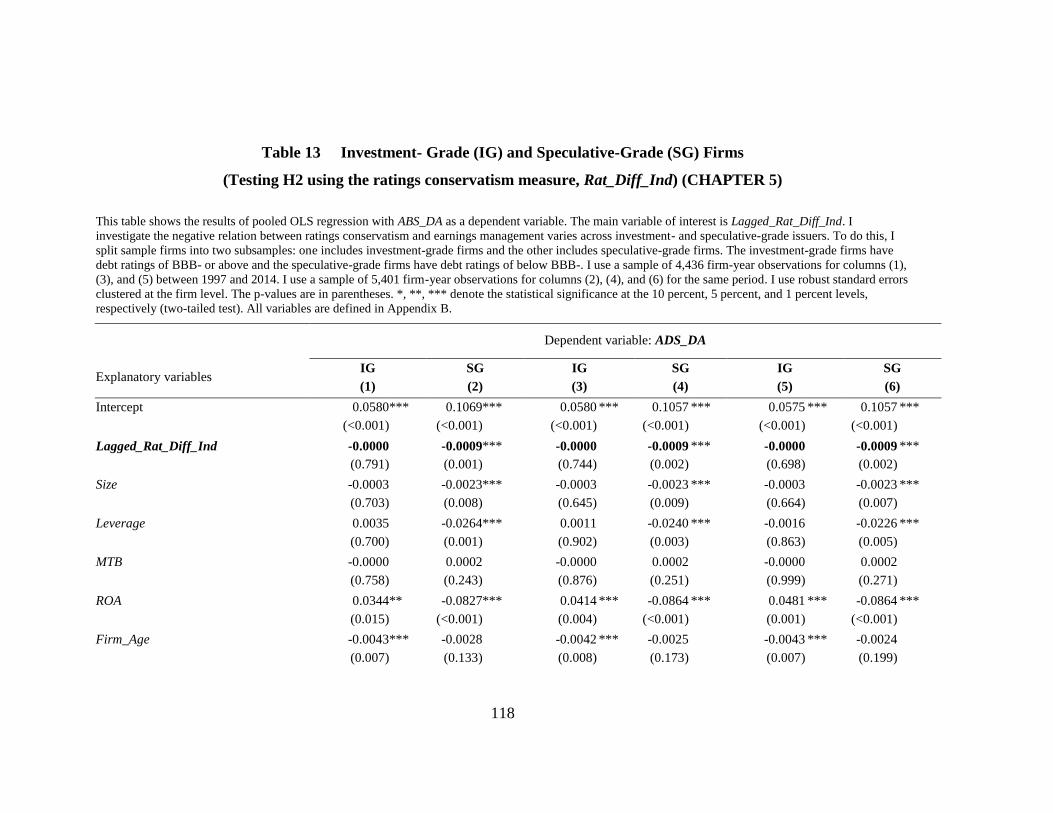

Table 13 Investment- Grade (IG) and Speculative-Grade (SG) Firms

(Testing H2 using the ratings conservatism measure, Rat_Diff_Ind) (CHAPTER 5)

................................................................................................................................. 118

Table 14 Investment- Grade (IG) and Speculative-Grade (SG) Firms

(Testing H2 using REM1) (CHAPTER 5) ............................................................... 120

Table 15 Investment- Grade (IG) and Speculative-Grade (SG) Firms

(Testing H2 using REM2) (CHAPTER 5) ............................................................... 122

Table 16 Potential Sample Selection Bias

(Testing H1 using the ratings conservatism measure, Rat_Diff_Firm) (CHAPTER 6)

................................................................................................................................. 124

Table 17 Additional Analysis

Relation between Ratings Conservatism and Earnings Smoothing (CHAPTER 7) 127

xi

Table 18 Additional Analysis

Relation between Ratings Conservatism and Asymmetric Timely Loss Recognition

(CHAPTER 7) ......................................................................................................... 129

Table 19

Alternative Measures of Accrual-Based Earnings Management 1: Testing H1

(CHAPTER 8) ......................................................................................................... 130

Table 20

Alternative Measures of Accrual-Based Earnings Management 2: Testing H1

(CHAPTER 8) ......................................................................................................... 133

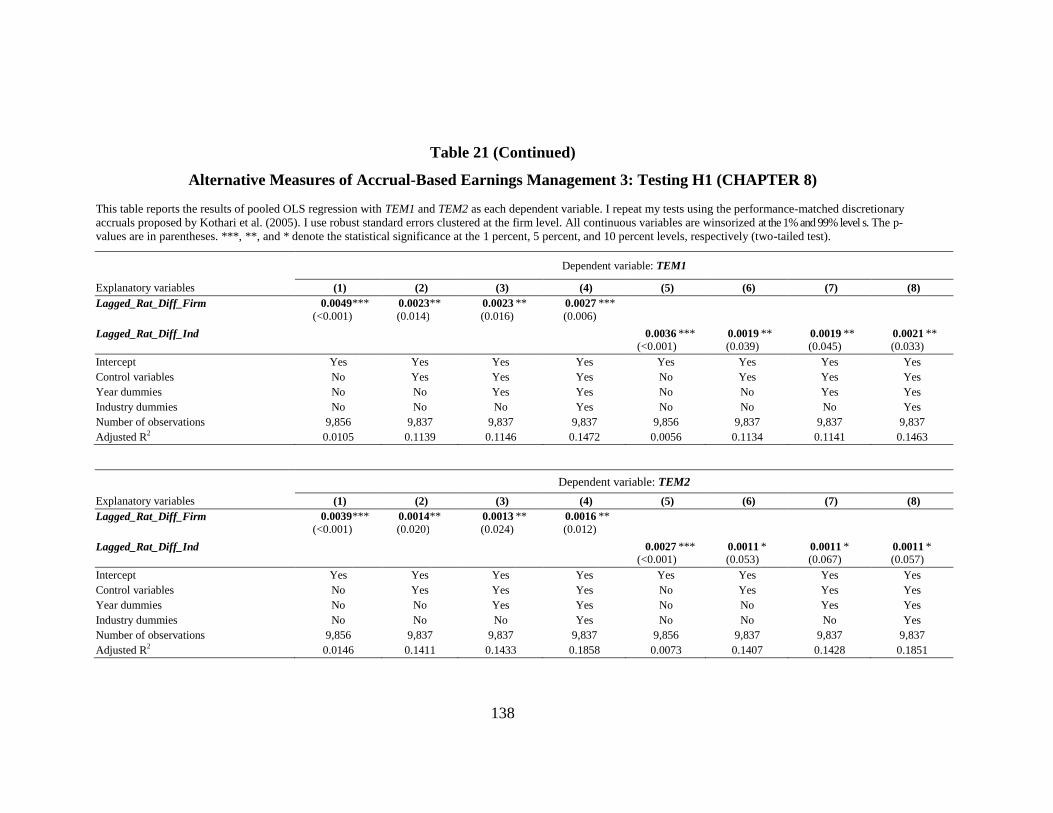

Table 21

Alternative Measures of Accrual-Based Earnings Management 3: Testing H1

(CHAPTER 8) ......................................................................................................... 136

Table 22

Alternative Measures of Accrual-Based Earnings Management 4: Testing H1

(CHAPTER 8) ......................................................................................................... 139

Table 23

Using a Three-Digit SIC Industry: Testing H1 (CHAPTER 8) ............................... 142

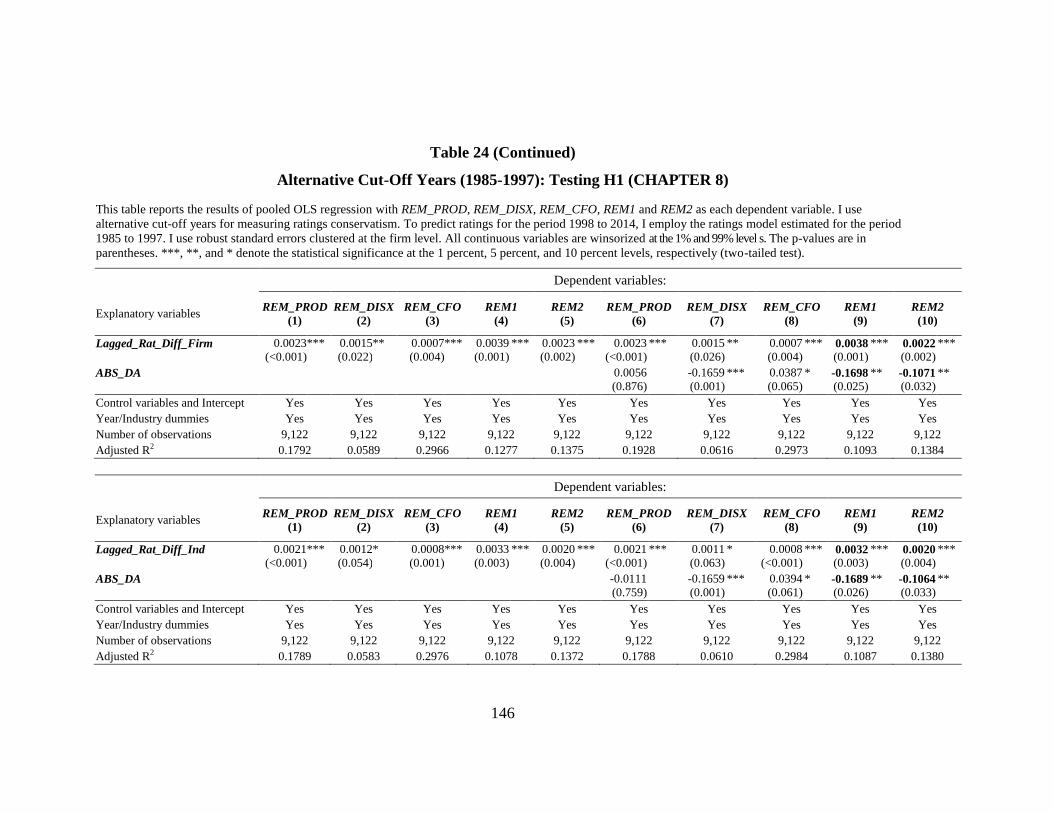

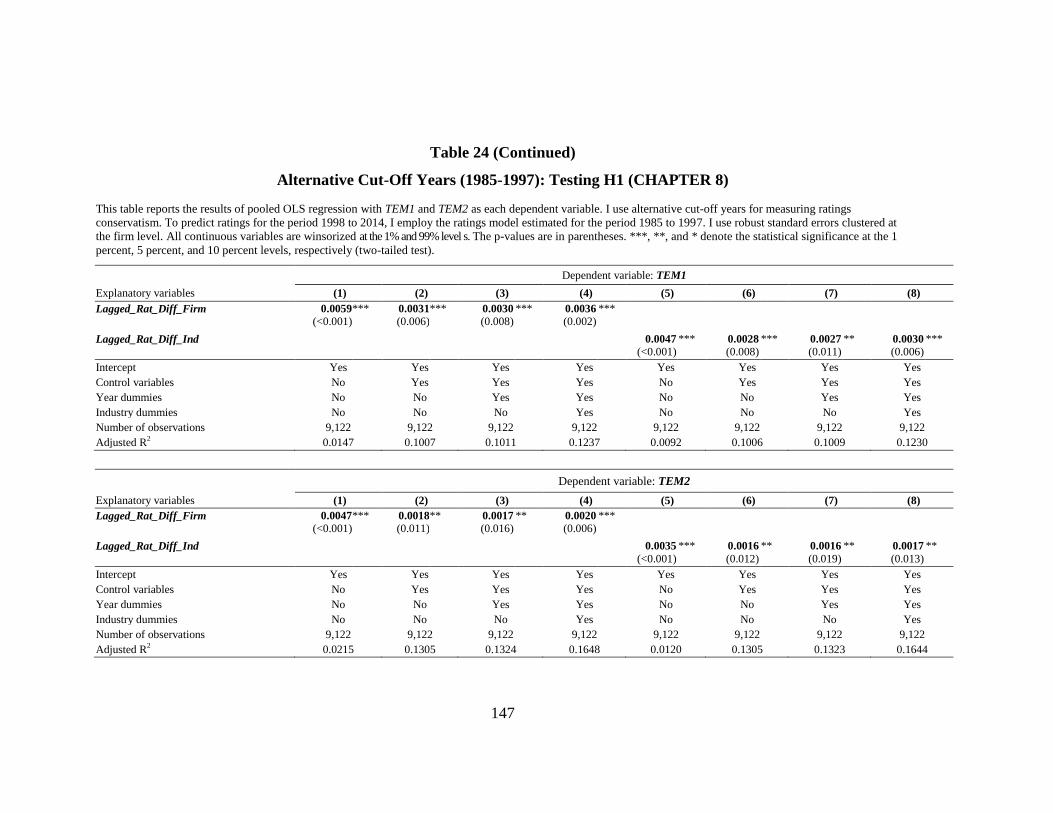

Table 24

Alternative Cut-Off Years (1985-1997): Testing H1 (CHAPTER 8) ..................... 145

Table 25

Alternative Cut-Off Years (1985-1998): Testing H1 (CHAPTER 8) ..................... 148

xii

Table 26

Controlling for the Effect of Global Financial Crisis of 2007-2008: Testing H1

(CHAPTER 8) ......................................................................................................... 151

Table 27

Controlling for the Controlling for Additional Variables: Testing H1 (CHAPTER 8)

................................................................................................................................. 154

xiii

LIST OF FIGURES

Figure 1 Plot of Coefficient on Year Dummies in Ratings Models (CHAPTER 4) ... 157

1

CHAPTER 1

INTRODUCTION

Over the past three decades, credit ratings of U.S. firms, on average, have declined. Prior

research documents that the downward trend in credit ratings is attributed to more stringent credit

standards by credit ratings agencies (Blume et al., 1998; Alp, 2013; Baghai et al., 2014; Afik et al.,

2016).1 The term “ratings conservatism” refers to the tendency for credit ratings agencies

to tighten their credit standards over time. Several studies focus on a firm’s earnings

management in relation to credit ratings and to credit ratings changes (Ali and Zhang, 2008; Alissa

et al., 2013; Jung et al., 2013; Kim et al., 2013; Shen and Huang, 2013). However, the relation

between ratings conservatism and earnings management has yet to be investigated. My study

begins with the following research questions: Does ratings conservatism affect a firm’s earnings

management behavior? If so, does ratings conservatism influence the choice between real and

accrual-based earnings management? In addition to real and accrual-based earnings management,

does ratings conservatism affect other types of earnings management, such as earnings smoothing

and asymmetric timeliness loss recognition? To answer these questions, I examine how ratings

conservatism influences a firm’s incentive to manage its reported earnings through earnings

1 An exception is Jorion et al. (2009), who argue that the downward trend in corporate credit ratings is

due to the decline in accounting quality over time. On the other hand, my study is based on the argument by

previous studies that the decline in credit ratings is primarily caused by the tightening rating standards

applied by ratings agencies (Blume et al., 1998; Alp, 2013; Baghai et al., 2014; Afik et al., 2016). I focus

on the impact of stringent rating standards over time (“ratings conservatism”) on a firm’s earnings

management. I do not, however, explore why bond ratings of U.S. firms have declined over time. To do

this, I first replicate Baghai et al.’s (2014) findings. I then extend the sample period to 2014 and calculate

ratings conservatism proxies proposed by Baghai et al. (2014). Finally, I investigate whether ratings

conservatism influences a firm’s incentive to manage earnings via earnings management.

2

management.

Issues concerning a firm’s earnings management have attracted much interest from

academics and practitioners over several decades.2 Prior literature investigates potential motives for

a firm’s earnings management from different perspectives, such as management compensation

contracts (Healy, 1985; Dechow and Sloan, 1991; Gaver et al., 1995; Hothausen et al., 1995;

Balsam, 1998; Guidry et al., 1999), lending contracts (Watts and Zimmerman, 1986; DeFond and

Jiambalvo, 1994), regulatory motives (Moyer, 1990; Collins et al., 1995), political costs (Watts and

Zimmerman, 1986; Jones, 1991), capital market motives (Teoh et al., 1998a, 1998b), and so on. In

addition to these motives, three recent studies (Ali and Zhang, 2008; Alissa et al., 2013; Kim et al.,

2013) provide an additional incentive for managers to manage their firms’ earnings in the context of

credit ratings and credit ratings changes. Managers are more likely to behave opportunistically.

Specifically, earnings management behaviors in response to credit ratings and credit ratings changes

can affect a firm’s cost of capital and further its stock price. Therefore, credit ratings are one of the

important characteristics that explain a firm’s earnings management behaviors.

Prior research also shows that credit ratings agencies have become more conservative with

their credit standards and provides the testable implications of ratings conservatism for researchers

and managers (Blume et al., 1998; Alp, 2013; Baghai et al., 2014; Afik et al., 2016). One may take

into account ratings conservatism in examining a potential motive for a firm’s earnings

2 Schipper (1989) states earnings management as “a purposeful intervention in the external financial

reporting process, with the intent of obtaining some private gain (as opposed to, say, merely facilitating the

neutral operation of the process)” (p. 92). In a similar way, as described by Healy and Wahlen (1999),

“Earnings management occurs when managers use judgment in financial reporting and in structuring

transactions to alter financial reports to either mislead some stakeholders about the underlying economic

performance of the company or to influence contractual outcomes that depend on reported accounting

numbers” (p. 368).

3

management in the framework of credit ratings. This is indeed what I explore in this paper.

Corporate credit ratings are determined by not only a firm’s financial conditions and operating

performance at a current point in time, but also by ratings agencies’ evaluation criteria or standards.

If the tightening of credit standards by ratings agencies remains persistent over time, such stringent

standards influence the opportunistic earnings management behaviors of managers.

I propose two hypotheses to examine the relation between ratings conservatism and

earnings management. The first hypothesis is: Credit ratings conservatism leads to a substitution

between real and accrual-based earnings management. My hypothesis of the substitution between

real and accrual-based earnings management is based on theoretical, empirical, and anecdotal

evidence.3 Managers use real and accrual-based earnings management either individually or jointly

to achieve one or more objectives (Kothari et al., 2016). I infer that firms pursue alternate means to

manage their reported earnings in response to ratings conservatism. Mangers have incentives to

manage their firms’ reported earnings via real earnings management to meet earnings targets

(Roychowdhury, 2006). Managers in firms more affected by stringent rating standards engage in

real earnings management to meet or beat earnings benchmarks in an attempt to enhance their

credibility with capital markets and to achieve desired credit ratings. For example, survey evidence

provided by Graham et al. (2005) shows that the chief financial officers (CFOs) responded that their

firms try to meet earnings benchmarks in an effort to “achieve or preserve a desired credit rating.”

(p. 25). Firms affected by ratings conservatism engage in more real earnings management and gain

3 Blume et al. (1998), Graham and Harvey (2001), Bartov et al. (2002), Graham et al. (2005),

Ashbaugh-Skaife et al. (2006), Kisgen (2006), Cohen et al. (2008), Jorion et al. (2009), Cohen and Zarowin

(2010), Gunny (2010), Caton et al. (2011), Zang (2012), Shen and Huang (2013), Baghai et al. (2014), Ge

and Kim (2014), and Standard & Poor's (2008, 2015) contribute to the study of this topic. Please see

subsection 2.3 for more details.

4

better credit ratings by meeting earnings benchmarks, which consequently access debt markets at a

more favorable rate.4 Thus, firms that suffer more from ratings conservatism engage in more real

earnings management. On the other hand, I predict that ratings conservatism restrains managers

from engaging in accrual-based earnings management because high accounting accruals are

observable to sophisticated credit rating agencies as well as regulators, auditors and even

institutional investors (Cohen et al., 2008; Dechow et al., 2010; Zang, 2012; Chan et al., 2015).

Firms with high accounting accruals are subject to closer scrutiny from regulators (the SEC),

auditors, and even credit rating agencies. High accounting accruals are more likely to be related to

accrual-based earnings management, which results in a decrease in financial reporting quality and

thus an increase in uncertainty among capital market participants, including credit rating agencies

(Akins, 2017). The high accounting accruals can impede credit ratings agencies from timely and

accurately assigning credit ratings to firms and have a negative influence on a firm’s future credit

ratings (Ashbaugh-Skaife et al., 2006; Jorion et al., 2009; Caton et al., 2011; Bae et al., 2013; Shen

and Huang, 2013; Standard & Poor’s, 2015).5 Accordingly, high accounting accruals are negatively

associated with the assignment of credit ratings by ratings agencies, which likely result in tighter

rating standards. Thus, firms more affected by ratings conservatism have incentives to engage in

less accrual-based earnings management. Collectively, as ratings conservatism increases, real

4 See, for example, Bartov et al. (2002) and Gunny (2010).

5 Based on these prior studies, I infer that credit rating agencies are able to (fully) comprehend a firm’s

accounting accruals process and penalize earnings management behaviors of managers. For example,

Standard & Poor’s (2015) states that accounting quality is considered to be a factor in the process of

assigning bond ratings.

5

earnings management increases while accrual-based earnings management decreases.6 Another

possible explanation for the substitution between real and accrual-based earnings management in

response to ratings conservatism is as follows: Ratings conservatism implies that ratings agencies

apply more stringent requirements (or criteria) on qualitative information (accounting quality) as

well as on quantitative information (past audited financial statements) in their assignment of credit

ratings. Ratings conservatism also implies that, given that financial conditions or operating

performance are comparable with the previous year, firms affected more by ratings conservatism

receive relatively worse ratings than before. Accordingly, due to their ratings disadvantages, firms

experience difficulty in obtaining debt financing, which could lead to lower levels of debt.7

Consequently, firms would deviate from their target debt (or target leverage) ratios. To make up for

the deviation, the firms attempt to revert back to their target debt ratios. These firms have a desire to

improve their credit ratings because improved ratings can signal a lower likelihood of credit risk (or

default risk) to market participants, including investors and creditors, which likely results in lower

debt financing costs. Therefore, in response to ratings conservatism, managers have incentives to

improve their accounting quality (or earnings quality) by engaging in less accrual-based earnings

management in an attempt to achieve desirable or better credit ratings. In other words, these firms

engage in less accrual-based earnings management to improve accounting quality for a better credit

rating to access debt markets at a favorable rate. On the other hand, ratings conservatism can lead

managers to resort real earnings management, which possibly benefits from an increase in earnings

6 Of course, it is possible that firms use the combination of real and accrual-based earnings

management. 7 If capital markets completely take into account the effect of ratings conservatism, firms would not

need to consider it in their debt financing decisions.

6

and thus positively affects debt ratings in spite of its costs.8 In a circumstance that rating agencies

have become more conservative in their assignment of credit ratings, the costs of real earnings

management (e.g., lower subsequent operating performance (Gunny, 2005)) are be less than its

benefits (e.g., the benefits from beating or meeting earnings targets/benchmarks (Graham et al.,

2005; Gunny, 2010; Zang, 2012)) as discussed earlier.9 Taken together, in response to ratings

conservatism, mangers prefer real earnings management to accrual-based earnings management.

The second hypothesis is: The positive (negative) relation between ratings conservatism and real

earnings management (accrual-based earnings management) is more pronounced for firms with

low credit quality than for those with high credit quality. Given that credit ratings agencies consider

accounting quality as an important item for their assignment of credit ratings, I infer that to obtain

better credit ratings and thus access debt markets at a more favorable rate, firms with low credit

quality, i.e., speculative-grade firms, have more (less) incentive to manage their reported earnings

via real earnings management (accrual-based earnings management) than those with high credit

quality, i.e., investment-grade firms.

Using a sample of publicly traded and rated U.S. firms between 1985 and 2014, I

investigate the relation between ratings conservatism and earnings management. I use the

absolute value of discretionary accruals (ABS_DA) as well as positive and negative

discretionary accruals as a proxy for a firm’s accrual-based earnings management. To

calculate discretionary accruals, I follow Dechow et al. (1995) and use the cross-sectional

8 See, for example, Ewert and Wagenhofer (2005).

9 Graham et al. (2005) provide survey evidence on why chief financial officers (CFOs) have a desire to

meet or beat earnings benchmarks. Please see Graham et al. (2005, p. 21-43) for more details.

7

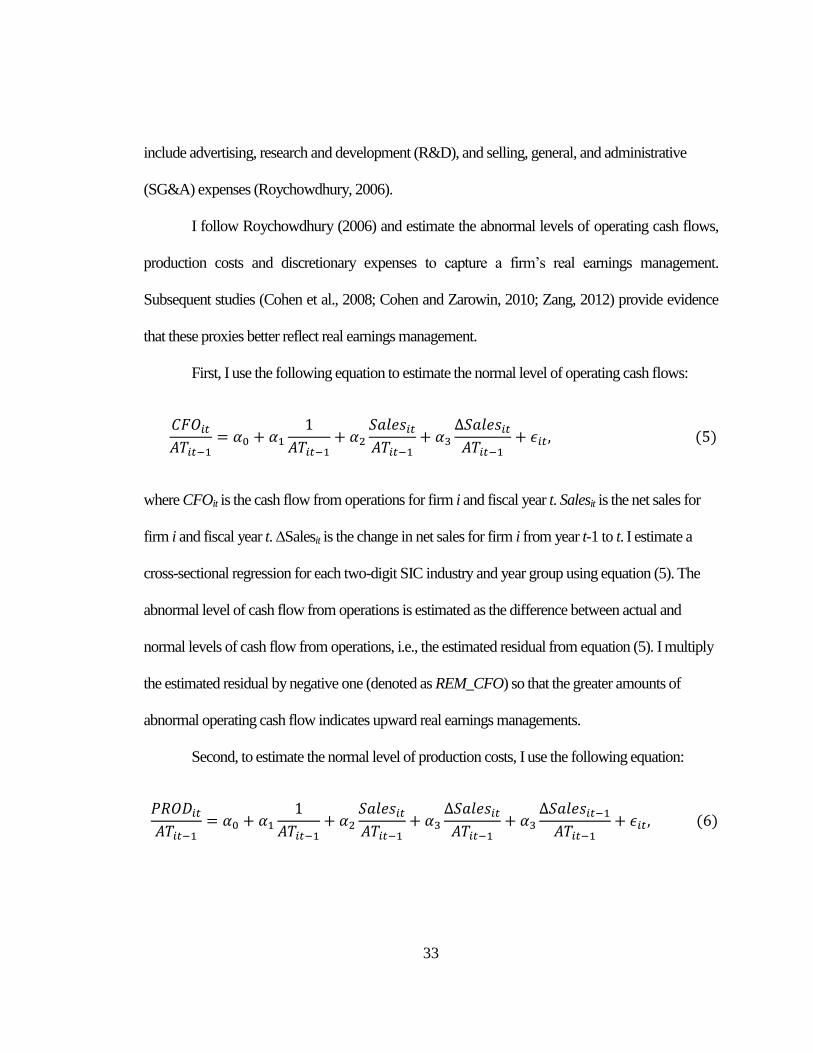

modified Jones (1991) model. Next, following Roychowdhury (2006), I estimate the

abnormal levels of operating cash flows, production costs and discretionary expenditures

to capture a firm’s real earnings management. To capture total real earnings management,

I follow Cohen et al. (2008), Cohen and Zarowin (2010) and Zang (2012), and generate

two alternative measures, REM1 (calculated as the sum of the abnormal level of

discretionary expenses multiplied by negative one and the abnormal level of production

costs) and REM2 (computed as the sum of the abnormal level of discretionary expenses

and the abnormal level of operating cash flows, both multiplied by negative one).

Furthermore, to examine the effect of ratings conservatism on overall earnings

management, I follow Chan et al. (2015) and generate two measures, TEM1 (calculated

as the sum of the signed discretionary accruals (DA) and the aggregate real earnings

management (REM1)) and TEM2 (computed as the sum of the signed discretionary

accruals (DA) and the aggregate real earnings management (REM2)).10

On the other hand,

I employ two measures of credit ratings conservatism developed by Baghai et al. (2014).

The procedures for measuring ratings conservatism are similar to those in Baghai et al.

(2014). Specifically, in the first step, I estimate ratings models between 1985 and 1996 to

predict ratings between 1997 and 2014. In the second step, I obtain two ratings

conservatism proxies, measured as the difference between a firm’s actual and predicted

ratings.

Consistent with the first hypothesis, I find that ratings conservatism is negatively

10

Furthermore, for additional analyses, I use earnings smoothing measures and asymmetric timely loss

recognition measures. See subsections 6.1 and 6.2 for more details.

8

related to accrual-based earnings management, measured through the absolute value of

discretionary accruals and positive discretionary actuals. These findings suggest that

firms affected more by ratings conservatism engage in less accrual-based earnings

management and income-increasing earnings management.11

Furthermore, with respect to

negative discretionary accruals, I find a positive relation between ratings conservatism

and accrual-based earnings management. This finding indicates that firms affected more

by ratings conservatism engage in less income-decreasing earnings management. Taken

together, my evidence suggests that accrual-based earnings management decreases with

ratings conservatism. In contrast, I find that firms affected more by ratings conservatism

engage in more real earnings management, measured as the abnormal levels of production costs,

discretionary expenses, and cash flow from operations as well as aggregate measures of real

earnings management, REM1 and REM2. These findings support my first hypothesis. To

summarize, ratings conservatism leads to a substitution between real and accrual-based earnings

management. Furthermore, given the two opposite effects, I find that ratings conservatism increases

total earnings management. This finding implies that the increase in real earnings management is

greater than the decrease in accrual-based earnings management. Next, consistent with my

second hypothesis, I find that the negative relation between ratings conservatism and

accrual-based earnings management (measured as the absolute value of discretionary

accruals) is stronger for speculative-grade firms than for investment-grade firms.

However, I find that the positive relation between ratings conservatism and real earnings

11

When using the ratings conservatism measure based on firm fixed effects, I find no evidence of

income-increasing earnings management.

9

management does not apply to both investment- and speculative-grade firms. This finding is

inconsistent with my hypothesis that the positive relation is more pronounced for speculative-grade

firms than for speculative-grade firms. With respect to a series of robustness checks, my main

results are robust to sample selection bias, alternative measures of accrual-based earnings

management, alternative industry classifications, alternative cut-off years employed when

measuring ratings conservatism, the effect of external events, omitted variable bias, and

different specifications for ratings models. Finally, regarding additional analyses, I find no

evidence that firms more affected by ratings conservatism tend to engage in more or less earnings

smoothing. I also find inconsistent results regarding the relation between ratings conservatism and

each measure of asymmetric timeliness loss recognition.

My study provides the following several contributions: First, this study contributes to the

literature on ratings conservatism by providing evidence that the tightening of rating standards

affects a firm’s earnings management. Until now, there is little literature on the downward trend in

corporate credit ratings of U.S. firms over time (Blume et al., 1998; Jorion et al., 2009; Alp, 2013;

Baghai et al., 2014; Afik et al., 2016). These studies document that rating standards have become

more stringent over the past decades, except for Jorion et al. (2009). Specifically, Blume et al. (1998)

argue that corporate credit ratings have become more stringent for the period of 1978 to 1995. Their

argument is supported by subsequent studies, including Alp (2013), Baghai et al. (2014), and Afik

et al. (2016). In contrast, Jorion et al. (2009) claim that the tightening of rating standards only

applies to investment-grade firms, suggesting that the downward trend in credit ratings is mainly

due to the change in accounting quality over time, not stringent rating standards by ratings agencies .

10

Unlike Jorion et al. (2009) and Alp (2013), Baghai et al. (2014) develop a measure of ratings

conservatism and further examine whether ratings conservatism affects corporate behaviors, such as

a firm’s capital structure decisions, cash holdings, and debt spreads. I further extend prior studies,

especially Baghai et al.’s (2014), by considering whether ratings conservatism can affect a firm’s

earnings management. This study provides evidence that firms take on different earnings

management strategies in response to ratings conservatism.

Second, this study extends prior literature on the relation between credit ratings (changes)

and earnings management by examining the effect of ratings conservatism on a firm’s earnings

management. Among prior studies (Ali and Zhang, 2008; Alissa et al., 2013; Kim et al., 2013),

Alissa et al. (2013) examine how a manager’s discretion of earnings management affects credit

ratings. They document that when a firm’s current ratings are below (above) expected ratings, the

firm has an incentive to manage its reported earnings upward (downward). My study is, however,

different from theirs in several ways. First, unlike Alissa et al., I examine how ratings conservatism

affects earnings management using a novel measure of ratings conservatism developed by Baghai

et al. (2014). Second, my study takes into account the behaviors of credit ratings agencies using a

measure of ratings conservatism. This study provides evidence that ratings conservatism can be one

of the potential characteristics that affect a firm’s earnings management. Although there are prior

studies on earnings management from the perspectives of credit ratings (change), there is no

evidence of whether the tightening of rating standards by credit ratings agencies influences a firm’s

earnings management. With my study, I hope to fill this gap by providing the impact of ratings

conservatism on earnings management. My study is different from prior literature on the relation

11

between credit ratings (changes) and earnings management in that I take into account both the

opportunistic behaviors of managers and the behavioral changes of credit ratings agencies.

Third, this study complements recent studies on the relation between real and accrual-based

earnings management by providing evidence that ratings conservatism can be one of the potential

factors in explaining the alternation of a firm’s earnings management. I find evidence of a

substitution between real and accrual-based earnings management in my study. Graham et al. (2005)

and Roychowdhury (2006) document a firm’s preference of real earnings management over

accrual-based earnings management. On the other hand, some studies show that firms alternate their

decision to use each earnings management strategies (Cohen et al., 2008; Cohen and Zarowin, 2010;

Badertscher, 2011; Zang, 2012; Chan et al., 2015).12

Finally, this study provides meaningful implications for corporate decision makers,

researchers, and regulators. For corporate decision makers, ratings conservatism by rating agencies

is an important issue because it affects or distorts a firm’s debt financing decisions. For researchers,

ratings conservatism is an interesting topic and worthy of investigation because it broadens their

perspectives and can be applied to other areas. For example, my study represents the first step

towards understanding the role of ratings conservatism in a firm’s earnings management. For

regulators, this study provides evidence that ratings conservatism can positively influence a firm’s

accounting quality (or earnings quality), represented as accrual-based earnings management. This

12

For example, Cohen et al. (2008) document a trade-off between real and accrual-based earnings

management. They show that accrual-based earnings management declines while real earnings

management increases after the passage of SOX. In a recent study, Chan et al. (2015) argue that the passage

of clawback provisions leads a substitution between accrual-based and real earnings management.

Consistent with the argument, they find that after the passage of clawback provisions, accrual-based

earnings management decreases, but real earnings management increases.

12

study also implies that earnings management behaviors of managers are influenced by the extent of

ratings conservatism.

The remainder of this study is organized as follows: CHAPTER 2 reviews relevant prior

literature and develops the hypotheses, CHAPTER 3 discusses research methodologies,

CHAPTER 4 describes the sample selection procedures and data, CHAPTER 5 presents the results,

CHAPTER 6 discusses potential sample selection bias, CHAPTER 7 provides further analyses,

CHAPTER 8 presents robustness checks, CHAPTER 9 concludes the paper by summarizing the

results, and finally CHAPTER 10 discusses limitations and future research.

13

CHAPTER 2

RELATED LITERATURE AND HYPOTHESES DEVELOPMENT

2.1 Credit Ratings and Earnings Management

Empirical findings presented by Ashbaugh-Skaife et al. (2006) imply that there is a relation

between credit ratings and earnings management. They consider the quality of working capital

accruals and the timeliness of earnings as proxies for a firm’s financial transparency. Ashbaugh-

Skaife et al. find that credit ratings are positively related to accrual quality and earnings timeliness.

Their results suggest that there is a negative link between credit ratings and earnings management.

This is because a firm’s earnings management leads to lower accrual quality.

In subsequent years, a stream of literature examines the relation between credit ratings

(changes) and earnings management (Ali and Zhang, 2008; Alissa et al., 2013; Kim et al., 2013;

Jung et al., 2013; Shen and Huang, 2013). Using ratings data from Standard & Poor’s (S&P)

between 1987 and 2005, Ali and Zhang (2008) study whether upgrades (or downgrades) in broad

ratings categories are related to a firm’s earnings management. According to Kisgen’s (2006) article,

they define a broad rating category as the level of ratings without the addition of plus, middle, and

minus specifications. For example, a broad rating category A includes A+, A, and A−. They find

that firms located in the borders of a broad rating category (A+ and A−) are more likely to inflate

their reported earnings and have less conservative accounting compared to their counterparts.

In another study, Alissa et al. (2013) examine whether firms manage their reported earnings

through real and accrual-based earnings management to meet or return to their expected credit

ratings. Based on the literature concerning target leverage, Alissa et al. construct a rating model.

14

They then run an ordered probit regression to estimate expected credit ratings, and measure the

deviation from current credit ratings (i.e., a difference between a firm’s actual and expected credit

ratings). Alissa et al. find evidence that when a firm’s current ratings are below expected ratings, the

firms are more likely to engage in income-increasing earnings management. They also show that

when a firm’s current ratings are above expected ratings, the firms are more likely to be involved in

income-decreasing earnings management. Furthermore, Alissa et al. argue that when there are

deviations from a firm’s expected ratings, managers attempt to revert back to their expected credit

ratings. To test this argument, Alissa et al. further investigate whether income-increasing (-

decreasing) earnings management by firms whose current ratings are below (above) expectations

can influence future rating changes. Consistent with their hypothesis, Alissa et al. document that

income-increasing (-decreasing) earnings management is related to positive (negative) changes in

future credit ratings. Their findings imply that credit ratings agencies do not perceive a firm’s

earnings management, which likely leads to improper assignment of credit ratings to debt issuers.

Furthermore, based on the target ratings hypothesis (Hovakimian et al., 2009), Kim et al.

(2013) study whether a firm’s real or accrual-based earnings management influences changes in

future credit ratings. Using a logistic regression, they find that there is a positive (negative) relation

between real earnings management (accrual-based earnings management) and credit rating

upgrades. These findings suggest that managers are more likely to use real earnings management

than accrual-based earnings management to influence upcoming changes in credit ratings. Their

study implies that changes in credit ratings convey information on a firm’s financial conditions to

market participants (Millon and Thakor, 1985; Kliger and Sarig, 2000; Kisgen, 2006). When a

15

firm’s credit ratings are anticipated to downgrade (upgrade) relative to the previous year, investors

reconsider whether to continue to invest in the firms (vice versa). In addition, creditors demand a

higher return on their investments.

Two recent studies explore the potential relation between credit ratings and earnings

smoothing. Jung et al. (2013) examine whether firms with plus or minus notch ratings (AA+ or

AA−) have an incentive to smooth their earnings through earnings management using three

subsamples: total, investment-grade, and speculative-grade. Jung et al. point out that firms have a

desire to improve or keep their credit ratings because ratings can affect their debt financing and

stock and bond valuations. They find that firms with plus notch ratings engage in more earnings

smoothing. Jung et al. further show that the likelihood of subsequent ratings upgrades increases

with earnings smoothing. Their findings indicate that a firm’s earnings smoothing is an effective

mechanism to improve its credit ratings. On the other hand, using cross-country bank data from 85

countries, Shen and Huang (2013) examine the impact of earnings management on the cost of debt

via credit ratings changes. To do this, they use the following two types of earnings management:

earnings smoothing and discretionary accruals (discretionary loan loss provisions). They find that

banks with higher discretionary accruals are more likely to receive lower credit ratings. Furthermore,

they find evidence that banks engaging in earnings smoothing tend to have lower credit ratings.

These findings suggest that a firm’s earnings management can adversely influence its credit ratings,

which likely increases the firm’s borrowing costs.

16

2.2 Stringent Trends in Rating Standards (“Ratings Conservatism”)

Prior literature documents the decline in credit ratings over time and provides evidence that

ratings agencies have become more conservative in assigning a firm’s credit ratings (Blume et al.,

1998; Alp, 2013; Baghai et al., 2014; Afik et al., 2016).13

Blume et al. (1998) are the first to identify

the decline in credit ratings of U.S. corporations between 1978 and 1995. They argue that the

decline in credit ratings is primarily attributed to more stringent rating standards assigned by ratings

agencies. In another study, Jorion et al. (2009) reexamine the tightening of credit ratings

documented by Blume et al. (1998) between 1985 and 2002. They show that the downward trend

in credit ratings does not correspond to firms with speculative-grade ratings. Jorion et al. argue that,

for those firms with investment-grade ratings, changes in accounting information quality over time

can explain the tightening of rating standards. Jorion et al. conclude that the downward trend in

corporate credit ratings is due to the decline in accounting quality over time, not tightening rating

standards applied by ratings agencies. Their results do not conform to those reported in Blume et al.

(1998).

However, subsequent studies, such as Alp (2013), Baghai et al. (2014), and Afik et al.

(2016), confirm the conclusion of Blume et al. (1998) that the downward trend in corporate credit

ratings over time is attributed to the tightening of credit standards by ratings agencies. Specifically,

Alp (2013) demonstrates that there are structural shifts in credit rating standards between 1985 and

2007. She provides evidence that credit rating agencies apply stricter rating standards for

13

Furthermore, Dimitrov et al. (2015) find that, following the Dodd-Frank Wall Street Reform and

Consumer Protection Act (2010), credit ratings agencies tend to be more stringent in the assignment of

corporate bond ratings. Their finding suggests that credit ratings agencies are more likely to pay strong

attention to their reputation.

17

investment-grade ratings and more relaxed standards for speculative-grade ratings from 1985 to

2002. Turning to the period between 2002 and 2007, she finds that credit rating agencies have

tightened their rating standards for both investment- and speculative-grade ratings. Taken together,

these three prior studies focus on whether credit ratings agencies have tightened their rating

standards over time, but they do not further examine the consequences of the tightening of rating

standards on a firm’s capital structure decisions.

In more recent research, Baghai et al. (2014) also provide evidence that credit ratings

agencies have become more conservative than ever before. Interestingly, when they estimate a

rating model without firm fixed effects, their results are similar to those reported in Alp (2013).

However, after including firm fixed effects in a ratings model, the stringent trend in rating standards

is evident for firms with both investment- and speculative-grade ratings. As Baghai et al. notes, it is

important to control for firm fixed effects when estimating a ratings model because a firm’s credit

ratings can be affected by omitted firm-specific variables. Furthermore, credit ratings agencies

consider qualitative criteria as well as quantitative criteria in their assignment of credit ratings. In

addition to evidence on ratings conservatism, Baghai et al. further provide implications of ratings

conservatism for a firm’s decisions on capital structure. To do this, they develop a measure for

ratings conservatism using the coefficients estimated from the ratings model, and define the

conservatism as the difference between a firm’s actual and predicted ratings. Baghai et al. show that

firms facing increased ratings conservatism tend to have less debt, lower leverage, and higher cash

holdings, compared to their counterparts. Furthermore, they find that such firms are more likely to

receive lower credit ratings and suffer lower growth rates. These results suggest that ratings

18

conservatism by ratings agencies has several important implications for a firm’s capital structure

decisions and for various market participants, e.g., investors and creditors, in capital markets.14

In the most recent study, Afik et al. (2016) confirm prior studies providing evidence that

credit ratings have become more stringent over time (e.g., Blume et al., 1998; Alp, 2013; Baghai et

al., 2014). They argue that the tightening of rating standards is partially attributed to the increase in

rating accuracy. Afik et al. further show that corporate credit ratings are more associated with

market variables than before and are less associated with accounting variables. Their results do not

conform to those of Jorion et al. (2009).

2.3 Ratings Conservatism and Earnings Management

Credit ratings are closely related to the capital structure decisions of firms (Kisgen, 2006;

Hovakimian et al., 2009). Corporate decision makers, especially managers, are more subject to

prioritizing their credit ratings in their capital structure choice. For example, survey evidence by

Graham and Harvey (2001) indicates that chief financial officers (CFOs) consider their firms’ credit

ratings as a priority in their capital structure decisions. These prior studies and evidence provide a

meaningful implication that ratings conservatism by ratings agencies can also affect a firm’s

decisions on capital structure. Baghai et al. (2014) argue that ratings disadvantages due to ratings

conservatism influence a firm’s debt level by providing evidence that firms affected by the

tightening of rating standards tend to have lower leverage (or less debt). Firms with high credit

ratings can more easily access debt markets than those with low credit ratings.

14

In addition, Kisgen (2006) investigates whether credit ratings affect a firm’s capital structure

decisions. He proposes the “credit rating-capital structural hypothesis,” and finds that credit ratings play a

key role in the determination of corporate capital structure.

19

As credit rating agencies become more conservative in the assignment of ratings over time,

firms that are subject to more ratings conservatism likely experience difficulty in their debt

financing. Thus, those firms have a lower debt level than before.15 Ratings conservatism, therefore,

distorts a firm’s debt financing decisions. As a result, firms deviate from their target or optimal debt

ratios (leverage ratios). That is, such firms have lower leverage ratios than their targets. According

to the trade-off theory of capital structure, firms set a target capital structure to meet.16 In a survey by

Graham and Harvey (2001), about 80% of chief financial officers (CFOs) responded that their firms

have optimal or target debt ratios. Therefore, in this situation, managers would attempt to move

back to their initial target leverage ratios to compensate for the deviations from their target or

optimum. Ratings conservatism implies that firms receive relatively lower credit ratings than

expected regardless of their financial conditions (e.g., balance sheet perspectives) and operating

performance (e.g., income statement perspectives). Accordingly, firms affected by increased ratings

stringency respond to ratings conservatism because they have relatively higher credit risk (or default

risk) in capital markets and therefore have higher costs associated with their debt financing than

before. To adjust their deviated leverage ratios, such firms have a desire to improve their credit

ratings because improved ratings signal a lower likelihood of credit risk (or default risk) to market

participants, including investors and creditors, which likely results in lower debt financing costs.

Given the above situation, firms more affected by ratings conservatism seek either real or

accrual-based earnings management or both to benefit from improved credit ratings and to move

15

If the capital market “fully” incorporates the effect of ratings conservatism into firm’s debt pricing,

then firms do not need to consider the effect in their debt financing decisions (see Baghai et al. (2014)). 16

The trade-off theory argue that firms determine the optimal level of leverage by balancing the

benefits of debt (e.g., interest tax shields and reductions in the agency costs of equity) against its costs (e.g.,

the costs of bankruptcy and the agency costs of debt).

20

back to their initial target leverage ratios. That is, a manager’s decision whether to use earnings

management is affected by increased ratings conservatism. At this point, I tentatively posit that

ratings conservatism is associated with a firm’s earnings management. Prior research suggests that

firms undertake real and accrual-based earnings management as alternative means to manage their

reported earnings (Roychowdhury, 2006; Cohen et al., 2008; Cohen and Zarowin, 2010; Zang,

2012; Chan et al., 2015). Given the tightening standards on credit ratings by rating agencies, these

two types of earnings management, however, have different implications for a manager’s incentive

to manage their reported earnings. Cohen and Zarowin (2010) explain why managers prefer real

earnings management to accrual-based earnings management.17 Zang (2012) shows the trade-off

between accrual-based and real earnings management. In addition, from the perspective of a real

business environment, managers are less reluctant to manage their reported earnings through real

earnings management rather than through accrual-based earnings management. For example, in

their survey, Graham et al. (2005) reveal that 78% of participants (i.e., CFOs) are willing to sacrifice

their long-term value to meet short-term earnings targets.18 Therefore, the relation between ratings

conservatism and each type of earnings management has different outcomes in response to the

tightening of rating standards.

17

Cohen and Zarowin (2010, p. 4) describe the managers’ preference of real-earnings management

over accrual-based earnings management as “First, accrual-based earnings management is more likely to

draw auditor or regulatory scrutiny than real decisions, such as those related to product pricing, production,

and expenditures on R&D or advertising. Second, relying on accrual manipulation alone is risky.” 18

Graham et al. (2005, p. 32-35) state as follows: “We find strong evidence that managers take real

economic actions to maintain accounting appearances. In particular, 80% of survey participants report that

they would decrease discretionary spending on R&D, advertising, and maintenance to meet an earnings

target. More than half (55.3%) state that they would delay starting a new project to meet an earnings target,

even if such a delay entailed a small sacrifice in value.”

21

Building on the statement above, I posit that managers in firms affected more by the

tightening of rating standards engage in more real earnings management. Unlike accrual-based

earnings management, real earnings management is not easily identified because it is directly

related to a firm’s operating activities, production costs, and discretionary expenses (e.g., research

and development (R&D), advertising, and selling, general, and administrative (SG&A) expenses).

Thus, real earnings management is less subject to auditor or regulatory scrutiny than accrual-based

earnings management (Roychowdhury, 2006; Cohen et al., 2008; Lo, 2008; Gunny, 2010; Cohen

and Zarowin, 2010; Zang, 2012). While credit ratings agencies recognize accounting quality as an

important item, they are unable to capture and reflect a firm’s real earnings management in their

assignment of credit ratings.

Given the above, I argue that managers in firms affected by increased ratings conservatism

would manage their reported earnings through real earnings management to compensate for ratings

disadvantages. Firms affected by ratings conservatism will adjust their current leverage ratios

toward their target levels. Ratings conservatism results in a lower level of debt. In this situation,

firms seek to boost their sales and earnings (and thus increasing cash flow) through real earnings

management because such numbers could appear to be indicative of good operating performance

and rapid sales growth and thus likely have a positive impact on their credit ratings. Managers take

advantage of their improved credit ratings to adjust their current leverage ratios toward their target

ratios through lower debt financing costs. The rationale behind the possibility that real earnings

management positively influences a firm’s credit ratings is as follows. For example, credit ratings

are influenced by a firm’s earnings performance or profitability (Ge and Kim, 2014). Credit ratings

22

agencies perceive a firm’s earnings and cash flows as crucial financial components for evaluating its

creditworthiness (Standard & Poor’s, 2008).19 Credit ratings agencies consider not only a firm’s

earnings but also its sales in the assignment of ratings. Unlike accrual-based earnings management,

real earnings management could enhance a firm’s sales and production in the process of managing

their earnings. Real earnings management can also positively affect firm performance that is

incorporated into its future credit ratings.20 For example, Gunny (2010) argues that managers

engage in real earnings management to signal superior future earnings in an attempt to (just) meet

earnings targets. Gunny (2010) finds that real earnings management positively influences firm

performance. This finding is consistent with prior studies showing that managers undertake real

earnings management to meet earnings targets for the purpose of gaining credibility and reputation

from stakeholders (Bartov et al., 2002), which consequently results in better future firm

19

According to the news article “S&P Raises Harley-Davidson’s Credit Rating,” increased sales and

earnings positively influence credit ratings: “Harley-Davidson Inc.’s (HOG) credit rating was upped to ‘A-

’from ‘BBB+’ by Standard & Poor’s (S&P) Ratings Services. Thus, the rating agency has assigned a stable

outlook for the company. The revision in Harley-Davidson’s rating is based on the company’s solid second

quarter performance together with the company’s recovery from the impact of recession. In addition,

Harley-Davidson emphasizes on boosting manufacturing efficiency and selling its higher priced

motorcycles. Rating affirmations or upgrades from credit rating agencies play an important part in retaining

investor confidence in the stock as well as maintaining credit worthiness in the market. Harley-Davidson

posted a 13.1% rise in earnings to $1.21 per share in the second quarter of 2013 from $1.07 in the same

quarter of prior year. Earnings surpassed the Zacks Consensus Estimate by 4 cents. Net income increased

9.9% to $271.7 million from $247.3 million a year ago” (September 23, 2013). Source:

http://www.nasdaq.com/article/sp-raises-harleydavidsons-credit-rating-analyst-blog-

cm279547\#/ixzz3oPAVbt1Y. 20

In contrast to Gunny’s (2010) findings, it is argued that real earnings management is negatively

related to subsequent operating performance (Eldenburg et al., 2011; Cohen and Zarowin, 2010), and

thereby be detrimental to firm value in the long-run (Ewert and Wagenhofer, 2005; Gunny, 2005). In spite

of potential costs of real earnings management, survey evidence presented by Graham et al. (2005) shows

that the chief financial officers (CFOs) prefer real earnings management over accrual-based earnings

management. Graham et al. conclude that “The most surprising finding in our study is that most earnings

management is achieved via real actions as opposed to accounting manipulations. Managers candidly admit

that they would take real economic actions such as delaying maintenance or advertising expenditure, and

would even give up positive NPV projects, to meet short-term earnings benchmarks” (p. 66).

23

performance and thus possibly better credit ratings. Gunny (2010) concludes that real earnings

management “is not opportunistic, but consistent with the firm attaining current-period

benefits that allow the firm to perform better in the future.” Furthermore, in their survey

study, Graham et al. (2005) find that chief financial officers (CFOs) try to meet earnings

benchmarks in an attempt to achieve their desired credit ratings.21 Based on this logic, I

infer that managers in firms more affected by ratings conservatism engage in more real

earnings management to meet earnings benchmarks in an effort to gain better or desired

credit ratings. Therefore, I predict that managers in firms affected more by the tightening of rating

standards have incentives to manage their reported earnings through real earnings management.

On the other hand, given desirable or achievable sales and earnings as well as meeting

earnings benchmarks, to obtain better credit ratings than before, firms also enhance accounting

quality (or earnings quality). A firm’s accounting quality is generally considered an important factor

in the process of credit rating assignments. In their assignment of credit ratings, credit ratings

agencies make an effort to accurately analyze and assess not only financial statements and audited

annual reports of the issuer (‘quantitative information’), but also accounting quality (‘qualitative

information’). This view is consistent with prior evidence that credit rating agencies take into

account a firm’s accounting quality in their rating assignments (Ashbaugh-Skaife et al., 2006;

Jorion et al., 2009; Caton et al., 2011; Bae et al., 2013; Shen and Huang, 2013; Standard & Poor’s,

2015).22 To understand the intuition behind this, consider the following simple equation: Net

21

See Graham et al. (2005, p. 25) for more details. 22

For example, Ashbaugh-Skaife et al. (2006) show that credit ratings are positively related to accrual

quality, measured as abnormal working capital accruals. This finding implies that credit ratings are

24

income = cash flows from operations + total accruals = cash flows from operations + non-

discretionary accruals + discretionary accruals. In other words, net income is calculated as the sum

of total accruals and cash flows from operations, where total accruals can be decomposed into non-

discretionary and discretionary accruals (Jones, 1991; Dechow et al., 1995; Kasznik, 1999). Part of

discretionary accruals is related to a firm’s earnings management. Higher earnings management,

represented as discretionary accruals, indicate lower accounting quality (or earnings quality). Based

on the above equation, assume that, ceteris paribus, two firms, A and B, achieve comparable

earnings or net income. Suppose also that firm A has greater discretionary accruals, while firm B

has lower discretionary accruals. In this situation, although the two firms achieve equivalent net

income, firm A exhibits lower accounting quality (or earnings quality) than firm B. Thus, if credit

ratings agencies regard accounting quality as a crucial evaluation item in their ratings assignment,

firm A is likely to receive lower credit ratings than firm B. This example illustrates the potential

trade-off between the benefits and costs associated with a firm’s earnings management. Ratings

conservatism influences such potential trade-offs. Ratings conservatism also implies that ratings

agencies have strengthened their rating standards and possibly considered accounting quality (or

earnings quality) as an important component in the assignment of credit ratings. Firms more

affected by ratings conservatism engage in less accrual-based earnings management because higher

negatively related to a firm’s earnings management. The implication is consistent with Shen and Huang

(2013), who indicate that credit ratings agencies are likely to downgrade ratings when they are aware of a

firm’s earnings management. In another study, Jorion et al. (2009) highlight the role of accounting

information quality in the process of credit rating assignment. Furthermore, Standard & Poor’s (2015)

demonstrate that they reflect aspects of a debt issuer’s accounting principles and practices in evaluating

accounting quality.

25

accounting accruals tend to draw regulatory scrutiny (e.g., the SEC), auditors, or credit ratings

agencies (Cohen et al., 2008; Dechow et al., 2010; Zang, 2012; Chan et al., 2015). It is likely that

higher accounting accruals give firm mangers discretion to engage in more accrual-based earnings

management. Such accrual-based earnings management, however, negatively affect a firm’s

accounting quality, which potentially leads to the decline in its credit ratings. Consequently, in

response to ratings conservatism, firm mangers have incentives to improve their accounting quality

(or earnings quality) by engaging in less accrual-based earnings management. This implies that

ratings conservatism decreases a firm’s incentive to manipulate earnings through accrual-based

earnings management.23

To summarize, based on the above discussion, I expect a trade-off between real and

accrual-based earnings management in response to the tightening standards on credit ratings by

rating agencies. Thus, I propose and test the following first hypothesis (in alternative form):

H1: Ceteris paribus, as ratings conservatism increases, real earnings management

increases while accrual-based earnings management decreases.

Second, I further examine whether a positive (negative) relation between ratings

conservatism and real earnings management (accrual-based earnings management) varies across

firms with high and low credit quality. I predict that, in the situation of stringent rating standards

over time, the positive relation between ratings conservatism and real earnings management is

stronger for firms with low credit quality than for those with high credit quality. In contrast, with

23

Alternatively, as Zang (2012, p. 676) points out, real earnings management must happen for a fiscal

year and “is realized by the fiscal year-end.” Managers adjust their accrual-based earnings management

according to the degree of real earnings management.

26

respect to accrual-based earnings management, I predict that ratings conservatism and earnings

management are greatly influenced by credit quality, which strengthens the negative relation

between ratings conservatism and earnings management. The trend in stringent rating standards

enables firms to improve their accounting quality to compensate for ratings disadvantages.

Furthermore, firms with high and low credit quality respond differently to ratings conservatism.

Firms with high credit quality are less likely to be sensitive to ratings conservatism than those with

low credit quality. For example, Ashbaugh-Skaife et al. (2006) argue that firms with high credit

quality are perceived as having a higher level of earnings quality than those with low credit quality,

which is associated with better credit ratings. Their argument is based on accrual-based earnings

management that captures a firm’s accounting quality and thus earnings quality. It is, however,

argued that one cannot either fully or partially captures a firm’s earnings quality, represented as real

earnings management. One of these reasons is that managerial actions are harder to detect than

those through accrual-based earnings management (see, for example, Cohen et al. (2008) and Zang

(2012)).

With respect to accrual-based earnings management, in response to ratings conservatism,

firms with high credit quality are less likely to reduce earnings management compared to their

counterparts. Thus, the reduction in accrual-based earnings management is expected to be smaller

than those with low earnings quality. For firms with low credit quality, the positive effects (i.e.,

credit ratings upgrades through the improvement in earnings quality) associated with less accrual-

based earnings management are expected to outweigh the negative effects (i.e., a decrease in

reported earnings) related to earnings. For example, firms increase their reported earnings in the

27

current period through accrual-based earnings management in order to influence their credit ratings.

However, this pattern in earnings is not persistent. Thus, given that rating standards have become

more stringent over time, such earnings management can negatively influence their credit ratings.

Instead, those firms will attempt to improve their earnings quality by engaging in less accrual-based

earnings management. With respect to firms with low credit quality, the negative relation between

ratings conservatism and accrual-based earnings management is stronger than those with high credit

quality. Likewise, similar logic can explain the positive relation between ratings conservatism and

real earnings management.

Therefore, I predict that if firms are more affected by stringent rating standards, then the

positive (negative) relation between ratings conservatism and real earnings management (accrual-

based earnings management) is stronger in firms with low credit quality than in those with high

credit quality.24 This prediction and discussion results in the following second hypothesis (stated in

alternative form):

H2: The positive (negative) relation between ratings conservatism and real earnings

management (accrual-based earnings management) is more pronounced for firms

with low credit quality than for those with high credit quality.

24

My prediction is based on prior literature providing evidence that credit ratings agencies consider

accounting quality as an important evaluation item in their assignment of ratings (Ashbaugh-Skaife et al.,

2006; Jorion et al., 2009; Caton et al., 2011; Bae et al., 2013; Shen and Huang, 2013; Standard & Poor’s,

2015). These prior studies are based on the assumption that credit ratings agencies perceive and adjust for

the quality of accounting information when they assign ratings to debt issuers. In addition, credit ratings

agencies evaluate not only quantitative information (e.g., earnings and profits), but also qualitative

information (e.g., accounting quality) in the ratings process.

28

CHAPTER 3

RESEARCH DESIGN

To examine whether ratings conservatism affects a firm’s earnings management, I employ

the following proxies for credit ratings conservatism and earnings management. In the analysis, I

use two measures of ratings conservatism proposed by Baghai et al. (2014). On the other hand, I

depend on prior literature to measure a firm’s real and accrual-based earnings management. In

addition to these earnings management measures, I further estimate a firm’s earnings smoothing

and asymmetric timely loss recognition based on prior literature.

3.1 Measuring Credit Ratings Conservatism

Based on previous literature and industry practice, I employ the rating conservatism

measures developed by Baghai et al. (2014). The main variable of interest is credit ratings

conservatism. The sample period in this study is from 1985 to 2014. The estimation procedures for

predicted ratings are discussed below.

As a first step, using ordinary least square (OLS) regressions, I estimate a ratings model for

the period of 1985 to 1996. I also use robust standard errors clustered at the firm level. The ratings

model is as follows:25

𝐶𝑟𝑒𝑑𝑖𝑡_𝑅𝑎𝑡𝑖𝑛𝑔𝑠𝑖𝑡 = 𝛼𝑗 + 𝛽′𝑋𝑖𝑡 + 𝜖𝑖𝑡, (1)

25

I use the sample period 1985 to 1996 to calculate the rating model (1) and the sample period 1997 to

2014 to compute ratings conservatism. In addition to these periods, I further employ alternative cut-off

years from 1994 to 2003. See subsection 8.2 that discusses different cut-off years employed when measuring ratings

conservatism.

29

where Credit_Ratingsit denotes Standard & Poor’s (S&P) long-term issuer credit ratings of

firm i in year t. I transform the letter ratings into numerical equivalents using an ordinal

scale ranging from 1 for the highest rated firms (AAA) to 21 for the lowest rated firms

(C). The 𝛼𝑗 is the intercept. The 𝛽′ is the vector of slope coefficients. The Xit includes

columns with explanatory variables, such as leverage (Book_Lev), convertible debt ratio

(Conb), rental payments (Rentp), cash holdings (Cash), debt-to-EBITDA (Debt_Ebitda),

a dummy variable for negative debt-to-EBITDA (Net_Debt_Ebitda), EBITDA-to-interest

(Ebitda_Int), profitability (Profit), volatility of profitability (Vol_Profit), firm size

(Firm_Size), asset tangibility (Tangibility), capital expenditures (Capex), the firm’s beta

(Beta), and the firm’s idiosyncratic risk (Idiosyncratic_Risk).

Specifically, Book_Lev is book leverage, measured as the sum of long- and short-

term debt divided by total assets. Conb is calculated as the ratio of convertible debt to

total assets. Rentp is computed as the ratio of rental payments to total assets. Cash is the

sum of cash and marketable securities divided by total assets. Debt_Ebitda is measured as

the ratio of total debt to earnings before interest, taxes, depreciation and amortization

(EBITDA). Net_Debt_Ebitda is a dummy variable equal to one if the ratio of total debt to

EBITDA is negative, and zero otherwise. Ebitda_Int is calculated as the EBITDA divided