Embed Size (px)

Citation preview

CREDIT POLICY AND FINANCIAL PERFORMANCE IN BARCLAYS BANK IN

KAMPALA UGANDA

BY

WAZILINDA LONGWE

BBA/41 196/1421DF

A RESEARCH REPORT SUBMITTED TO THE COLLEGE OF ECONOMICS AND

MANAGEMENT IN PARTIAL FULFILMENT OF THE REQUIREMENTS

FORTHE AWARD OF BACHELORS DEGREE IN BUSINESS

ADMINSTRATION (BANKING AND FINANCE) OF

KAMPALA INTERNTIONAL UNIVERSITY

APRIL, 2017

DECLARATIONI WAZILINDA LONGWE, declare that this research proposal entitled “Credit Policy and

Financial Performance in Barclays Bank in Kampala Uganda” with the exception of

references, ideas and concerns is my own personal work and has never been presented to any

organization or institution of higher learning for a degree or any other academic award.

Signature ~ DateS

WAZI LINDA LONGWE

(Candidate)

APPROVAL

This research proposal has been compiled and submitted to the College of Economics and

Management of Kampala International University with my approval.

41SignatureS /

DR. KIRABO JOSEPH. B. K

(Supervisor)

Date:...c2~fr{

TABLE OF CONTENTS

DECLARATION.

APPROVAL ii

TABLE OF CONTENTS iii

LIST OF TABLES vi

LIST OF ACRONYMS vii

CHAPTER ONE 1

INTRODUCTION I

1 .0 Introduction 1

1 .1 Background of the Study

1 .1 .1 Historical perspective

1 .1 .2 Theoretical perspective 2

1 .3 Conceptual perspective 3

1 .1 .4 Contextual perspective 4

1.2 Statement of the problem 4

1.3 The purpose of the study 5

1 .4 General objectives 5

1 .4.1 Specific objectives 5

1 .5 Research questions 5

1.6 1-lypotheses of the study 5

1.7 Scope of the study 6

1.7.1 Geographical Scope 6

1.7.2 Content Scope 6

1.7.3 Time Scope 6

1.8 Significance of the study 6

1 .9 Operational Definition of key terms 7

CHAPTER TWO 8

LITERATURE REVIEW 8

2.0 Introduction 8

2.1 Conceptual Framework 8

2.2 Theoretical review 9

2.3 Review of related literature 10

2.3.1 .1 Credit standards 10

2.3.1.2 Credit risk controls 10

2.3.1.3 Collection policy 11

2.3.2.1 Financial Performance 1 3

2.3.2.2 Liquidity 14

2.3.2.3 Profitability 15

2.4 Related Studies 15

2.5 Gaps 18

CHAPTER THREE 19

METI-IODOLOGY 19

3.0 Introduction 19

3.1 Research design 19

3.2 Population of the study 19

3.3 Sample size 19

3.4 Sampling procedure 20

3.5 Sources of data 20

3.5.1 Primary sources 20

3.5.2 Secondary sources 21

3.6 Research instrument 21

3.6.1 Questionnaire 21

3.6.2 Interview guide 21

3.7 Validity and reliability of the instrument 21

3.7.1 Validity 21

3.7.2 Reliability 22

3.8 Data gathering procedure 22

3.9 Data Analysis 22

3.10 Ethical considerations 23

3.11 Limitations of the study 24

iv

CHAPTER FOUR .25

DATA PRESENTATION, ANALYSIS AND INTERPRETATION OF RESULTS 25

4.0 Introduction 25

4.1 Profile of Respondents 25

4.2 Credit policy 26

4.3 Financial performance 29

4.4 Relationship between credit standards and financial performance 30

4.5 Relationship between Credit risk controls and financial performance 30

4.6 Relationship between Collection policy and financial performance 3 1

4.7 Regression analysis 32

CHAPTER FIVE 33

DISCUSSIONS, CONLUSIONS AND RECOMMENDATIONS 33

5.0 Introduction 33

5.1 Discussions 33

5.2 Conclusions 35

5.3 Recommendation 36

5.4 Areas for further research 37

REFERENCES 38

APPENDICES 41

APPENDIX 1: SECTION A: DEMOGRAPHIC CHARACTARISTICS OF RESPONDENTS ..41

V

LIST OF TABLES

Table 3.1: Population and Sample Size 20

Table 4.1: Profile of respondents 25

Table 4.2A: Extent of credit policy 27

Table 4.2B 28

Table 4.3: Level of financial performance of Barclays Bank 29

Table 4.4. Significant relationship between credit standards and financial performance 30

Table 4.5 Significant relationship between Credit risk controls and financial performance 31

Table 4.6 Significant relationship between collection policy and financial performance 3]

Table 4.7 Regression Analysis between the Dependent and Independent Variables 32

vi

LIST OF ACRONYMS

CAMEL: Capital Adequacy, Asset Quality, Management Quality, Earnings &

Liquidity

LADST: Liquidity Asset Deposit Short Term

NLTA: Net Loan Total Asset

NLDST: Net Loan/Total Deposits and Short Term Borrowings

ROA: Return on Asset

ROE: Return on Equity

EDDB: East Africa Dev’t Bank

LRGL: Loan Reserve Gross Loans

SPSS: statistical Package for Social Sciences

PMS: Performance Measurement System

USA: United States of America

Fl’s: Financial Institutions

PLCC: Pearson’s Linear Correlation Coefficient

VII

CHAPTER ONE

INTRODUCTION

1.0 IntroductionThis chapter will include the background of the study. The background is drawn from the

following perspectives i.e. historical, theoretical, conceptual and contextual perspectives. It

also includes the statement of the problem, general objectives, specific objectives, research

questions, scope of study, significance of the study and conceptual framework.

1.1 Background of the Study

1.1.1 Historical perspectiveThe concept of credit policy can be traced back in history and it was not appreciated until and

after the Second World War when it was largely appreciated in Europe and later to Africa

(Ahmed. 2010). Banks in USA gave credit to customers with high interest rates which

sometimes discouraged borrowers hence the concept of credit didn’t become popular until the

economic boom in (USA in 1 885) when the banks had excess liquidity and wanted to lend the

excess cash (Baxler, 2011). In Africa the concept of credit was largely appreciated in the

1 950’s when most banks started opening the credit sections and departments to give loans to

white settlers. In Africa credit was initially given to the rich people and big companies and

was not popular to the poor. Most suggestions were for the evaluation of customer’s ability to

repay the loan, but this didn’t work as loan defaults continued (Humphrey, 2012). The

concept of credit policy became widely appreciated by financial Institutions (Fl’s) in the late

1990s, but again this did not stop loan defaults to this date (Brand, 2010).

Credit policy is the ability to intelligently and efficiently manage customer credit lines. In

order to minimize exposure to bad debt, over-reserving and bankruptcies, companies must

have greater insight into customer financial strength, credit score history and changing

payment patterns. The ability to penetrate new markets and clients hinges on the ability to

quickly and easily make well-informed credit decisions and set appropriate lines of credit.

According to Brealey (2010), sound credit policy would help improve prudential oversight of

asset quality, establish a set of minimum standards, and to apply a common language and

methodology (assessment of risk, pricing, documentation, securities, authorization, and

ethics), for measurement and reporting of non- performing assets, loan classification and

provisioning. The credit policy set out the bank’s lending philosophy and specific procedures

1

and means of monitoring the lending activity. Credit policy is the general guideline governing

the process of giving credit to bank clients. The policy sets the rules on who should access

credit, when and why one should obtain the credit including repayment arrangement and

necessary collaterals.

Financial performance refers to measuring the results of a firms policies and operations in

monetary terms. These results are reflected in the firm’s return on investment, return on

assets, value added (Bureu & Dijk 2010) performance is a subjective measure of how well a

firm can use assets from its primary mode of business to generate revenues. Performance is a

general measure of a firm’s overall flnancial health over a given period of time, and can be

used to compare similar firms across the same industry or to compare industries or sectors in

aggregation. There are many different ways to measure performance, but all measures should

be taken in aggregation. Line items such as revenue from operations, operating income or

cash flow from operations can be used, as well as total unit sales and debtors/receivable.

Furthermore, the analyst or investor may wish to look deeper into financial statements and

seek out margin growth rates or any declining debt (Obala, 2012).

1.1.2 Theoretical perspective

This study is based on the theory of self-efficacy which was developed by Bandura 1995.

Bandura (1 995) hypothesized that self-efficacy affects choice of activities, effort, persistence,

and achievement. Compared with persons who doubt their capabilities, those with high self-

efficacy for accomplishing a task participate more, work harder, persist longer when they en

counter difficulties, and achieve at a higher level. Self-efficacy is a major component of

Bandura’s social-cognitive theory, which contends that behavior is strongly stimulated by

self-influence. Self-efficacy is also related to goal setting (Farlex, 2012), as well as work in

self-regulation (Finlay, 2010), particularly with respect to leadership (Berger, 2012). People

acquire information to appraise self-efficacy from their performances, vicarious

(observational) experiences, form of persuasion, and physiological reactions. One’s

performances offer reliable guides for assessing self-efficacy.

Successes raise efficacy and failures lower it, but once a strong sense of efficacy is developed

a failure may not have much impact (Bandura, 1999). People also acquire self-efficacy

information from knowledge of others through social comparisons. Those who observe

similar peers perform a task are apt to believe that they, too, are capable of accomplishing it.

2

To remain credible, however, information acquired vicariously requires validation by actual

performance (Home, 1994). Self-efficacy is not the only influence on behavior. High self-

efficacy will not produce a competent performance when requisite knowledge and skill are

lacking. In this instance, a sense of self-efficacy for learning is beneficial because it motivates

individuals to improve their competence, outcome expectations, or beliefs concerning the

probable outcomes of actions, are important because people strive for positive outcomes.

Out-come expectations and self-efficacy often are related (Home. 1994).

1.1.3 Conceptual perspectiveCredit policy was the independent variable in this study while financial performance was the

dependent variable. According to Mishkin (2010), credit policy is the guidelines governing

the process of giving credit to bank clients. Credit policy was conceptualized credit standards.

credit risk control and collection policy, whereas as financial performance was

conceptualized in relation to liquidity and profitability.

Credit standardsCredit standards are a set of terms that a company or bank uses to determine whether to

extend a loan or line of credit to an applicant (Campbell, 2012). Credit standards may include

having a certain FICO score, recent good credit history, and a certain income (Falex, 2012).

According to Pandey (1995), a credit standard is one of the controllable decision variables

that directly influence investment in trade credit.

Credit risk controlsPandey (2010) noted that credit risk controls involve evaluating the creditworthiness of the

prospective borrower. This involves establishing the willingness and ability of the beneficiary

to meet obligations as they fall due. Credit risk controls is an important aspect in designing a

credit policy since it culminates into the seasons regarding the amount of loan granted to the

applicants (Ogilo, 2012).

Collection policy

Collection policy involves monitory receivables to spot trouble and obtaining payment on

past due accounts (Finlay, 2010). Finlay identified 6c’s as measurement parameters in setting

collection policy and these include character, capacity, and condition, control, capital and

collateral.

3

LiquidityAccording to Mishkin (1995), liquidity indicates whether the firm has sufficient funds to

enable it pay its short-term financial obligations as they fall due, and liquidity is the life and

blood of a commercial bank.

ProfitabilityThis indicates the ability of the firm to earn returns on investment. Long—term profitability

derives from the relations between cost and revenue; it is a necessary but not sufficient

condition for growth. Revenues may be held up by entry barriers and costs pushed down by

management ingenuity (Arnold-, 2013). A low-profit firm will lack the finance for expansion,

but a high-profit business may conclude the risk and rewards of expansion are inadequate. In

a life style’ SSB, an owner may trade profitability today against profitability tomorrow

(Ahmed, 2010).

1.1.4 Contextual perspectiveThe study was carried out in Barclays bank in Kampala Uganda. non-performing loans and

increased cost of doing business are some of the negative consequences limiting financial

performance of Barclays bank in Kampala Uganda. Unfavorable government policies on

credit policies, inadequacy resource, customer dissatisfaction and lack of security are

challenges to financial performance of Barclays bank in Kampala Uganda.

1.2 Statement of the problemPoor financial performance is a problem facing commercial banks in Kampala like Barclays

bank in particular. There is a declining trend of average profits for commercial banks, while

their liabilities are increasing (Bank of Uganda, 2012). Unfavorable government policies on

credit policies, poor administration styles, poor cash management, inadequacy resource,

customer dissatisfaction and lack of security are challenges to financial performance of

commercial banks in Kampala Uganda. Non-performing loans and increased cost of doing

business are some of the negative consequences of the problem facing the financial

performance of commercial banks in Kampala Uganda. During the period 20 11-2012,

operating expenses to total assets for majority of commercial banks in Kampala Uganda was

greater 0.114 which indicates a poor financial performance. The average Return on Equity

(ROE) indicates that commercial banks had 24.7%, which indicates that these commercial

banks perform poorly. By the end of 2012, commercial banks had only 17.5% of the market

share which is extremely low. Consequently, the relatively poor performance of commercial

banks in Kampala Uganda needed to be investigated, since it has been observed that failure to

4

recover bad debt from some debtors’ defaulters require thorough commitment on the side of

financial /Banks. Though a number of factors are responsible for the financial performance of

commercial banks in Kampala Uganda. it is important to find out how credit policy affects

the financial performance of commercial banks in Kampala Uganda. Hence the study

proposes to establish the effect of credit policy on financial performance in Barclays Bank in

Kampala Uganda.

1.3 The purpose of the studyThe study will aim at establishing the relationship between credit policy and financial

performance in Barclays Bank in Kampala Uganda.

1.4 General objectivesThe general objective of the study will be to assess the effect of credit policy on financial

performance in Barclays Bank, and generate new knowledge based on the findings of the

study.

1.4.1 Specific objectivesi. To examine the relationship between credit standards and financial performance in

Barclays Bank in Kampala Uganda.

ii. To determine the relationship between credit risk controls and financial performance in

Barclays Bank in Kampala Uganda.

iii. To evaluate the relationship between the collections policy and financial performance in

Barclays Bank in Kampala Uganda.

1.5 Research questionsi. What is the relationship between credit standards and financial performance in

Barclays Bank in Kampala Uganda?

ii. What is the relationship between credit risk controls and financial performance in

Barclays Bank in Kampala Uganda?

iii. What is the relationship between the collections policy and financial performance in

Barclays Bank in Kampala Uganda?

1.6 Hypotheses of the studyThe following hypotheses were developed for empirical testing:

HO1: There is no significant relationship between credit standards and financial performance.

5

HO2: There is no significant relationship between the credit risk controls and financial

performance.

HO3: There is no significant relationship between collection policy and financial performance.

1.7 Scope of the study

1.7.1 Geographical ScopeThe study will be conducted in Barclays Bank in Kampala Uganda. The researcher will have

a case study in the above place due to its accessibility and security.

1.7.2 Content ScopeThe study was basically confined and scrutinized on two variables that are, credit policy (the

independent variable) which was measured in relation to credit standards, credit risk control

and collection policy. Whereas financial performance (the dependent variable) was measured

in terms of liquidity and profitability.

1.7.3 Time ScopeDue to time and resource constraints, the study will be conducted from January to March

20 17. 1-lere the proposal stage will take place in the month of January, data collection and

analysis will take place in February 201 7, then report writing and submission of the report

will be done in March 2017.

1.8 Significance of the studyThe study will be useful in finding out how best the management can identify credit standards

on financial performance, and also help in developing a competitive credit policy that will be

useful for accurate data on financial performance.

The study findings will be paramount to management through improving its credit policy in

Barclays Bank in order to determine the effect of credit risk controls on financial

performance and to improve on its financial reporting, prompt settlement of claims and

further investigations in terms of client appraisal on financial performance.

The findings will be useful to other researchers in future for further research related areas and

the results to the study will be added to the existing literature for reference by scholars,

researchers, firms and other parties interested in the subject.

The study is informative to the financial institutions and others creditors since these

institutions have many roles to play including providing credit to clients and understand the

underlying factors in commercial banks and related financial institutions. The studies will be

6

used to evaluate the effect of collection policies on financial performance of institutions that

will be helpful for administrators and bank managers, also the findings will be used to

provide appropriate problem-solving skills on credit policy.

Information generated will be used by Commercial banks and by others financial

organizations, firms to assist them in coming up with credit policy that enable to evaluate the

effect of credit risk controls measures on financial performance and Finally, the researcher’s

educational requirement for the award of a master degree shall be met and the fact findings

report will be used by other researchers on same topic.

1.9 Operational Definition of key termsCredit policy: Refers to a Clear and written guidelines that set (1) the terms and conditions

for supplying goods on credit, (2) Client qualification criteria, (3) procedure for making

collections, and (3) steps to be taken in case of client delinquency.

Credit Standards: Refers to the guidelines issued by a company that are used to determine if

a potential borrower is creditworthy.

Credit risk controls: Refers to the business guideline of assessing potential risk and lower

overall operating costs while increasing effectiveness and efficiency.

Collection Policy: Refers to the steps taken by a company to follow-up in ensuring timely

payment of its accounts receivable.

Financial performance: Refers to measure of how well a firm can use assets from its

primary mode of business and generate revenues.

Profitability: refers to the ability of the firm or enterprise to generate adequate income

consistently from year to year.

Liquidity: refers to ability of the enterprise to maintain an effective working capital

management.

7

CHAPTER TWO

LITERATURE REVIEW

2.0 IntroductionThis chapter provides a critical review of the issues that was been explored and studied both

theoretically and empirically in the existing literature on credit policy as the independent

variable and financial performance as the dependent variable.

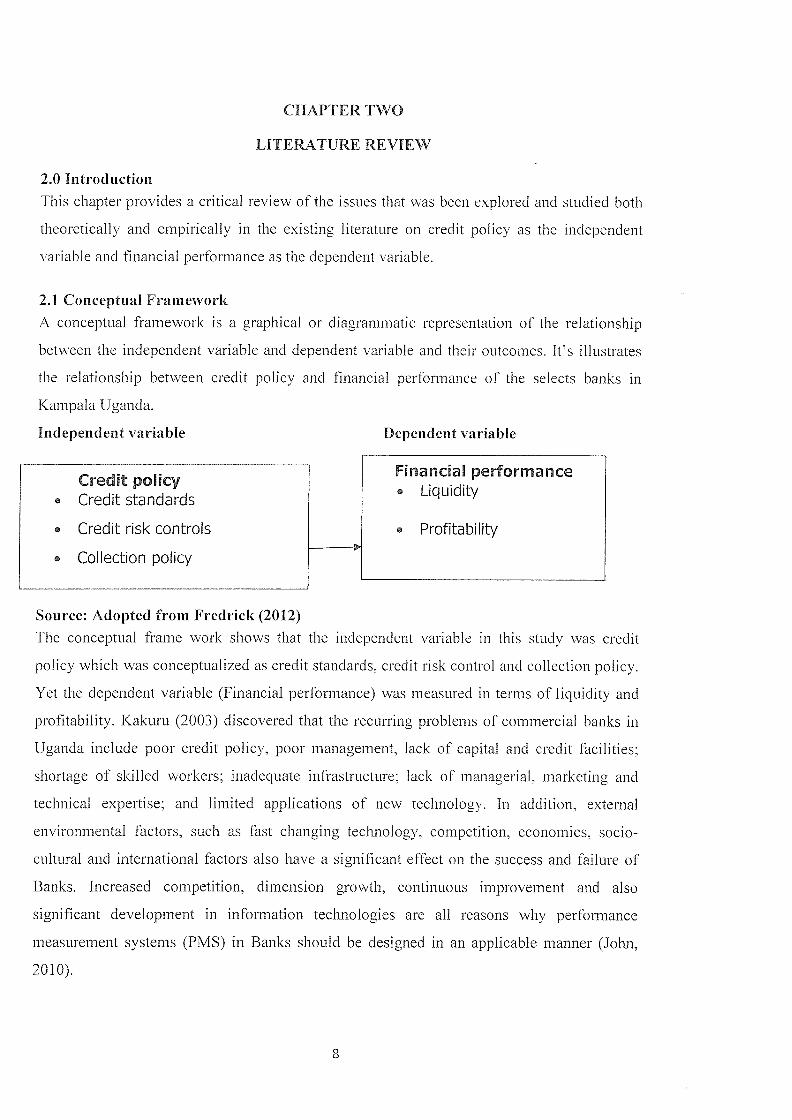

2.1 Conceptual FrameworkA conceptual framework is a graphical or diagrammatic representation of the relationship

between the independent variable and dependent variable and their outcomes. It’s illustrates

the relationship between credit policy and financial performance of the selects banks in

Kampala Uganda.

Independent variable Dependent variable

Financial performanceCredat pohcyLiquidityCredit standards

o Credit risk controls o Profitability

o Collection policy

Source: Adopted from Fredrick (2012)The conceptual frame work shows that the independent variable in this study was credit

policy which was conceptualized as credit standards, credit risk control and collection policy.

Yet the dependent variable (Financial performance) was measured in terms of liquidity and

profitability. Kakuru (2003) discovered that the recurring problems of commercial banks in

Uganda include poor credit policy, poor management, lack of capital and credit facilities;

shortage of skilled workers; inadequate infrastructure; lack of managerial, marketing and

technical expertise; and limited applications of new technology. In addition, external

environmental factors, such as fast changing technology, competition, economics, socio

cultural and international factors also have a significant effect on the success and failure of

Banks. Increased competition, dimension growth, continuous improvement and also

significant development in information technologies are all reasons why performance

measurement systems (PMS) in Banks should be designed in an applicable manner (John,

2010).

8

2.2 Theoretical review

This study was drawn from the theory of self-efficacy postulated by Bandura (1995).

It “refers to beliefs in Bank’s capabilities to organize and execute the courses of action

required to manage prospective situations”. Self-efficacy affects people’s thoughts,

feelings, actions, motivations, efforts, and determinations to confront the obstacles

faced in life. High self-efficacy means that people are more likely to participate in

activities in which they believe they can succeed. It promotes the premise that

individuals have the potential to mitigate and improve their situations. Finally, the

theory identifies factors that affect the success or failure of individuals, including their

collective or group actions (Stephen, 2012).

Bandura’s (2012) key contentions as regards the role of self-efficacy beliefs in human

functioning is that people’s level of motivation, affective states, and actions are based more

on what they believe than on what is objectively true. For this reason, how people behave can

often be better predicted by the beliefs they hold about their capabilities than by what they are

actually capable of accomplishing, for these self-efficacy perceptions help determine what

individuals do with the knowledge and skills they have. This helps explain why people’s

behaviors are sometimes disjoined from their actual capabilities and why their behavior may

differ widely even when they have similar knowledge and skills. For example, many talented

people suffer frequent (and sometimes debilitating) bouts of self-doubt about capabilities they

clearly possess, just as many individuals are confident about what they can accomplish

despite possessing a modest repertoire of skills. Belief and reality are seldom perfectly

matched, and individuals are typically guided by their beliefs when they engage the world

(Gitman, 2011). As a consequence, people’s accomplishments are generally better predicted

by their self-efficacy beliefs than by their previous attainments, knowledge, or skills. Of

course, no amount of confidence or self-appreciation can produce success when requisite

skills and knowledge are absent. It bears noting that self-efficacy beliefs are themselves

critical determinants of how well knowledge and skill are acquired in the first place. The

contention that self-efficacy beliefs are a critical ingredient in human functioning is

consistent with the view of many theorists and philosophers who have argued that the potent

affective, evaluative, and episodic nature of beliefs makes them a filter through which new

phenomena are interpreted (Kakuru, 2003).

9

2.3 Review of related literature

2.3.1.1 Credit standardsThe guidelines a company follows to determihe whether a credit applicant is creditworthy

(Campbell, 2012). Credit standards are a set of terms that a company or bank uses to

determine whether to extend a loan or line of credit to an applicant. Credit standards may

include having a certain FICO score. recent good credit history. and a certain income (Falex.

2012). BPP (2011) considers credit standards to be the criteria, which the firm follows in

selecting clients for credit extension this is a very fundamental credit policy variable that

requires intensive analysis. According to Pandey (1 995), a credit standard is one of the

controllable decision variables that directly influence investment in trade credit. Graham,

(2011) emphasized that individual accounts of credit applicants need a great deal of scrutiny

and that, for this reason, it’s important that standards be set basing on the individual credit

applicants. Forgy (2011) argue that credit standards provide guidelines for determining

whether to extend credit to a client and how much credit should be extended. Kakuru (2010)

noted that it is important that credit standards be set basing on individual credit applicants by

considering credit risk controls, collection policy and credit limit and default rate (Forgy,

2011).

2.3.1.2 Credit risk controls

Before extending credit to any of its operators, sufficient information should be collected

about the clients. This is done in a bid to minimize losses. According to Ogilo (2012), impact

of credit risk controls, reliable and timely of client information is critical to managing the

credit process. If timely and useful information is available, management is much better

equipped to direct and control prudent credit processes. IMF (2012) stresses that a credit

application doesn’t need to be long, but it should be carefully worded after all, it is a legal

contract. With a credit application, the creditor should put emphasis on the following. Be sure

the client provides the company’s legal name and entity type, as well as the names of

principals. If the business structure shields the company’s owners from liability, you may

want to extract a personal guarantee. Ask for the contact information such as telephone and

fax numbers and e-mail and home addresses for the principals, as well as for the person who

will probably be your main contact: the accounts payable manager. Ask for trade references,

ideally in your industry, who can speak to completed transactions with the prospect. Seek

bank account information and contacts. Some lawyers recommend including a form that

authorizes a bank to release the client’s records. Include the terms and conditions, written so

10

that the client has to acknowledge agreeing to them and require a dated signature. Kakuru,

(2010) argues that Credit risk controls is done to minimize losses resulting from investigating

in unrecoverable clients and that Sources of such information include; banks, companies,

associated competitors, supplies and individuals applicants. Kakuru (2010) asserts that

collection of such information is not free but the cost is justifiable (Ahmed. 2010).

Credit risk controls involves evaluating the creditworthiness of the prospective borrower

(Pandey, 2010). This involves establishing the willingness and ability of the beneficiary to

meet obligations as they fall due. It should ensure loans meet credit standards and the policy

guidelines for credit risk controls to be effectively avoided, it should follow a typical

domestic process flow beginning with data collecting and moving to action observing

(Greenberg, 2010). Credit risk controls is an important aspect in designing a credit policy

since it culminates into the seasons regarding the amount of loan granted to the applicants.

Credit standard, this is the maximum amount of credit, which the firm can extend to clients at

any point in time, as this limit is decided, the risk controls should carefully scrutinize the

amount of contemplated sales and the client’s financial strength. There is need to lower the

amount of credit where slow paying tendencies crop up (Ogilo, 2012).

2.3.1.3 Collection policy

Collection Policy is the final element in credit policy. Collection policy involves monitory

receivables to spot trouble and obtaining payment on past due accounts (Business education,

2010). Average Collection Period (ACP); it refers to that period in which debts remain

uncontrollable. It measures the number of days for which a credit transaction remains

outstanding and thus determines the speed of payment by clients, (Finlay, 2010). Default

Rate, this is the measure of the portion of the uncontrollable receivables that is bad debts loss

ratio. This ratio indicates the default risk that is the unlikelihood that clients will fail to pay

their credit obligation, (Finlay, 2010). Basing on experience, the financial manager should be

able to make a reasonable judgment regarding the chance of default. Finlay identified 6c’s as

measurement parameters in setting collection policy and these include character, capacity,

and condition, control, capital and collateral. According to McNaughton, (2011), collateral is

a tangible asset in which a bank takes securing interest. Such security should be safe and

easily marketable. This may include land titles, houses, balances on savings accounts and

guarantees (Mishkin & Fredrick, 2010).

11

The debt collection policy of the bank is built around dignity and respect to clients (Graham.

1990). The policy is built on courtesy, fair treatment and persuasion. Bank staff follows

general guidelines in collection and security repossession. They include- contacting ci ient

ordinarily at the place of his/her choice and in the absence of any specified place, at the place

of his/her residence and if unavailable at his/her residence, at the place of

business/occupation. Identity and authority of persons authorized to represent bank for follow

up and recovery of dues. The bank will document the efforts made for the recovery of clues

and the copies of communication set to clients, if any, will be kept on record; and other

guidelines (Obala, 2012).

Baxley, (2011) noted that insurance, financial institution and leasing companies try to

establish a unique collection policy. What worked out for one company will not necessarily

work well for another company thus the need to follow prime factors while designing a

collection policy. Internal factors that are critical include; the economy. clients mix, and

stability of trade and growth element in the area (Finlay, 2010).

The financial Institutions use the 6Cs model of credit to evaluate the ability of potential

borrower (Mabwe. 2004). The 6Cs help Financial Institutions to increase loan performance.

as they get to know their clients better. These 6Cs are: character, capacity, collateral, capital,

control and condition. Character basically is a tool that provides weighting values for various

characteristics of a credit applicant and the total weighted score of the applicant is used to

estimate his credit worthiness (Forgy, 2011). This is the personal impression the client makes

on the potential lender. The factors that influence a client can be categorized into personal,

cultural, social and economic factors (Ogilo, 2012).

The psychological factor is based on a man’s inner worth rather than on his tangible

evidences of accomplishment. Financial Institution’s consider this factor by observing and

learning about the individual. In most cases it is not considered on first application of credit

by an applicant but from the second time. Under social factors, lifestyle is the way a person

lives (Graham, 2011). This includes patterns of social relations (membership groups),

consumption and entertainment. A lifestyle typically also reflects an individuals attitudes,

values or woridview. Reference groups in most cases have indirect influence on a person’s

credibility. Financial Institution’s try to identify the reference groups of their target as they

influence a client’s credibility. Personal factors include age, life cycle stage, occupation,

12

income or economic situation, personality and self- concept. Under life cycle stage for

example older families with mature children are not likely to default since it’s easier to attach

cofiateral on their assets since they are settled unlike the unsettled young couples. The

financial institutions will consider the cash flow from the business, the timing of the

repayment, and the successful repayment of the loan (Home. 2003).

Mckinsey (2012) defines cash flow as the cash a borrower has to pay his debt. Cash flow

helps the financial institutions to determine if the borrower has the ability to repay the debt.

The analysis of cash flow can be very technical. It may include more than simply comparing

income and expenses. Financial institutions determines cash flow by examining existing cash

flow statements (if available) and reasonable projections for the future position that lenders

review the borrower’s business plan and financial statements, they have a checklist of items

to look at one of the being the number of financial ratios that the financial statements reveal.

These ratios are guidelines to assist lenders determine whether the borrower will be able to

service current expenses plus pay for the additional expense of a new loan. Collateral is any

asset that customers have to pledge against debt (McNaughton. 2011). Collateral represents

assets that the company pledges as alternative repayment source of loan. Most collateral is in

form of hard assets such as real estate and office or manufacturing equipment.

Alternatively accounts receivable and inventory can be pledged as collateral. Lenders of short

term funds prefer collateral that has duration closely matched to the short term loan

According to Amin (1999). Capital is measured by the general financial position of the

borrower as indicated by a financial ratio analysis, with special emphasis on tangible net

worth of the borrower’s business. Thus. capital is the money a borrower has personally

invested in the business and is an indication of how much the borrower has at risk should the

business fail. Condition refers to the borrower’s sensitivity to external forces such as interest

rates, inflation rates, business cycles as well as competitive pressures (John, 2010).

2.3.2.1 Financial PerformanceFinancial performance refers to measuring the results of a firms policies and operations in

monetary terms. These results are reflected in the firm’s return on investment, return on

assets, value added. Financial performance is a subjective measure of how well a firm can use

assets from its primary mode of business to generate revenues. Performance is a general

measure of a firm’s overall financial health over a given period of time, and can be used to

13

compare similar firms across the same industry or to compare industries or sectors in

aggregation. There are many different ways to measure performance, but all measures should

be taken in aggregation. Line items such as revenue from operations, operating income or

cash flow from operations can be used. as well as total unit sales and debtors/receivable.

Furthermore, the analyst or investor may wish to look deeper into financial statements and

seek out margin growth rates or any declining debt (Casu & Girardone. 2013).

In finance, a loan is a debt evidenced by a note which specifies, among other things, the

principal amount, interest rate, and date of repayment. A loan entails the reallocation of the

subject asset(s) for a period of time, between the lender and the borrower. In a loan, the

borrower initially receives or borrows an amount of money, called the principal, from the

lender, and is obligated to pay back or repay an equal amount of money to the lender at a later

time. Typically, the money is paid back in regular installments, or partial repayments; in an

annuity, each installment is the same amount. The loan is generally’ provided at a cost,

referred to as interest on the debt, which provides an incentive for the lender to engage in the

loan. In a legal loan, each of these obligations and restrictions is enforced by contract, which

can also place the borrower under additional restrictions known as loan covenants. In practice

any material object might be lent. Acting as a provider of loans is one of the principal tasks

for financial institutions, for other institutions, issuing of debt contracts such as bonds is a

typical source of funding (Home. 2003).

2.3.2.2 LiquidityAccording to Mishkin (1995), liquidity indicates the ability of the bank to meet its financial

obligations in a timely and effective manner, liquidity indicate the ability of the firm to meet

its short-term obligation as they fall due. They indicate whether the firm has sufficient funds

to enable it pay its short-term financial obligations as they fall due. The liquidity is the life

and blood of a commercial bank. Financial liabilities are attracted through retail and

wholesale distribution channels. Retail generated funding is considered less interest elastic

and more reliable than deposits attracted from wholesale distribution channels (Bandura,

1995). The following ratios are used to measure liquidity. Liquid assets to deposit-borrowing

ratio (LADST) = liquid asset/client deposit and short term borrowed funds. This ratio

indicates the percentage of short term obligations that could be met with the bank’s liquid

assets in the case of sudden withdrawals. Net Loans to total asset ratio (NLTA) = Net

loans/total assets (NLTA) measures the percentage of assets that is tied up in loans. The

14

higher the ratio, the less liquid the bank is. Net loans to deposit and bQrrowing (NLDST)

Net loans/total deposits and short term borrowings. This ratio indicates the percentage of the

total deposits locked into non-liquid assets and a high figure denotes lower liquidity (John

Ratichek, 2010).

2.3.2.3 ProfitabilityThe most common measure of bank performance is profitability. These indicate the ability of

the firm to earn returns on investment. Profitability is measured using the following criteria:

Return on Assets (ROA) a net profit/total asset shows the ability of management to acquire

deposits at a reasonable cost and invest them in profitable investments (Ahmed, 2010). This

ratio indicates how much net income is generated per pound of assets, the higher the ROA,

the more the profitable the bank. Return on Equity (ROE) net profit/total Equity. ROE is

the most important indicator of a bank’s profitability and growth potential. It is the rate of

return to shareholders or the percentage return on each £ of Equity invested in the bank. Cost

to Income Ratio (C/I) = total cost /total income measures the income generated per £ cost.

That is how expensive it is for the bank to produce a unit of output and the lower the cost to

income ratio (C/I), the better the performance of the bank (Ogilo, 2010).

While it is expected that banks would bear some bad loans and losses in their lending

activities, one of the key objectives of the bank is to minimize such losses (Hansen, 1995).

Financial performance evaluates the risks associated with the bank’s asset portfolio i.e. the

quality of loans issued by the bank. Several ratios can be used for measuring credit quality

however, not all information on the loans is always available. Non-performing loans is not

available for all banks therefore this paper use the following ratio: Loan loss reserve to gross

loans (LRGL) = Loan loss reserve/gross loans. This ratio indicates the proportion of the total

portfolio that has been set aside but not charged off. It is a reserve for losses expressed as a

percentage of total loans (Stephen, 2012).

2.4 Related Studies

Baxler (2011) studied credit policy and debt collection performance in developmental banks.

The purpose of the study was to establish the relationship between credit policy and debt

collection performance in East African Development Bank (EADB). The objectives of the

study were to find out the nature of the credit policy that EADB uses. The study was a cross

sectional survey where both qualitative and quantitative in approach. Data was collected from

employees of finance department, risk department and sample size comprised 30 respondents

15

who were purposively selected and simple random sampling was jointly used to minimize

biased results. Self-administered questionnaires were the main instrument of the study and

data was analyzed using frequencies, percentages, regression model and SPSS were used to

establish the relationship between credit policy and data collection performance. The results

of the study indicated that EADB uses credit standards, credit terms and collection

procedures to manage its debts. The study revealed a positive relationship r = 0.750 between

credit policy and debt collection performance (Baxler, 2011).

Mabwe (201 0) studied, a financial Ratio Analysis of Commercial Bank Performance in South

Africa. The studied investigated the performance of South Africa’s commercial banking

sector for the period 2005- 2010. Financial ratios are employed to measure the profitability,

liquidity and credit quality performance of five large South African based commercial banks.

The study found that overall bank performance increased considerably in the first two years

of the analysis. A significant change in trend is noticed at the onset of the global financial

crisis in 2007, reaching it speak during 2012-2010. This resulted in falling profitability, low

liquidity and deteriorating credit quality in the South African Banking sector (Mabwe, 201 0).

Dejene (2012) sought to evaluate the financial performance of Construction and Business

Bank (CBB) of Ethiopia. The study emphasized on financial performance measurement ratios

such as asset utilization/efficiency ratios, deposit mobilization, loan performance, liquidity

ratio, leverage/financial efficiency ratios, profitability ratios, solvency ratios and coverage

ratios to evaluate the bank’s financial performance. The bank achieved significant hike in

revenues over the periods while the cost of operation showed only slight increase

comparatively with the increase in revenues (McNaughton, 2011).

According to Harrison (2012), financial performance refers to measuring the results of a

firm’s policies and operations in monetary terms, these results are reflected in the firm’s

return on investments, return on assets and value added. Financial performance is a general

measure of a firm’s overall financial health over a given period of time, and can be used to

compare similar firms across the same industry or to compare industries or sectors in

aggregation. James (2011) also added that liquidity is the life and blood of any bank and it

indicates the ability of the bank to meet its financial obligations in a timely and effective

manner.

16

James (201 1) noted that ratios are a measure of liquidity and working capital as a measure of

current asset and current liabilities, current ratio is a measure of current asset! current

liabilities, inventory turnover ratio is a measure of cost of goods sold / average inventory.

This ratio indicates the percentage of the total deposits locked into non-liquid assets. A high

figure denotes lower liquidity. Ahmed (2010), states that the most common measure of bank

performance is profitability. Profitability is measured using the following criteria: Return on

assets ratio is a measure of net income / average total assets shows the ability of management

to acquire deposits at reasonable cost and invest in profitable investments. This ratio indicates

how much net income is generated per pound of assets. 1-Jowever credit policy (independent

variable) will be conceptualized in terms of credit standards, credit risk control and collection

policy. Whereas the dependent variable (financial performance) will be conceptualized in

terms of liquidity and profitability.

Therefore, although the need of an appropriate plan to measure Banks performance is

apparent, different problems cause these banks to experience difficulty in implementing such

systems. Use of poor financial practices tops the list of constraints faced by Banks

everywhere. Because of the high transaction costs and inability of Banks to provide large

credit services, Banks find themselves starved for funds at all stages of their development

ranging from start-up to expansion and growth (John, 201 0). In Uganda, it is leasing that has

bridged the current financing gap experienced by Banks by providing commercial and

industrial equipment as it focuses on the lessee’s ability to generate cash from the bank’s

operations to service the lease repayments rather than on the balance sheet or past credit

history (Kakuru, 2003).

Pandey (1 995) endeavored to establish whether there is any significant difference between

the performance of the locally established banks and the foreign banks with operations in

Kenya (John, 2010). Secondary data on financial performance of banks was obtained mainly

from commercial banks financial statements and CBK Bank Supervision. The data was

analyzed using MS Excel statistical package to obtain averages of the various financial

performance ratios for both local and foreign banks. Using the same statistical package, trend

analyses were done over the study period so as to compare the two categories. Finally t-tests

were performed so as to test the hypothesis that there is no significant difference between the

financial performance of local and foreign banks. The results realized from the study showed

that, of the eight ratios used, two indicated that there is no significant difference between the

17

financial performances of the two categories. However, the rest of the ratios (six) showed that

there is a significant difference between the financial performances of the two categories.

Hence the overall conclusion was that there is a significant differeflce in financial

performance of the two categories. The trend analyses showed that the financial performance

of the local banks was poor, just as the general economic situation in the country (Ogilo,

2012).

Schunk (1995) studied Effectiveness of Credit Management System on Loan Performance

using Micro Finance Sector in Kenya. Collection policy was one of the elements of credit

management. The study tested whether there was any significant relationship between

collection policy adopted and loan performance. From the computed chi-square value

(12.736) at I degree of freedom, there is a significant relationship between collection policy

adopted and loan performance since the computed p- value (0.000) is less than 0.05 at 95%

confidence level. This therefore implies collection policy adopted do influence loan

performance, with stringent policy being the best policy for adoption since the percentage of

performance obtained when its adopted is relatively high compared to that of lenient policy,

this therefore makes the findings of the study to be consistent with those of Pandey (2004).

2.5 GapsThe following studies were undertaken as come from the related studies. Horn (2012) studied

effectiveness of credit management system on loan performance using Micro finance sector

in Kenya, Mabwe (2010) studied a financial ratio analysis of commercial bank performance

in South Africa, the study covered 2005- 2010, and was employed to measure credit quality

performance of five large South Africa based commercial banks, Mishkin & Fredrick (2010)

studied credit policy and debt collection performance in developmental banks in Uganda,

Dejene (2012) sought to evaluate the financial performance of construction and business bank

(CBB) of Ethiopia, and The studies emphasized on financial performance measurement ratios

such as asset utilization! efficiency ratios, deposit mobilization, loan performance, Leverage,

efficiency ratios. It was due to all above studies that prompted the researcher to bring into the

attention and explore the credit policy and financial performance and their objectives as a

case study. Another important area is Theory of self-efficacy postulated by Bandura (1995).

18

CHAPTER THREE

METHODOLOGY -

3.0 Introduction

This chapter presented the research design. the research population, and the sample size,

sampling procedures, research instruments, validity and reliability of instruments, data

gathering procedures, data analysis. ethical considerations and limitations of the study.

3.1 Research design

This study followed a descriptive research design, whereby qqualitative and quantitative

research approaches was used to gain insight to variables; credit policy and financial

performance. It was descriptive in that it described the characteristics of respondents. The

descriptive correlational design will be used to determine significant relationship between the

extent of credit policy and financial performance. It will be cross-sectional in that data will be

collected data from all respondents at one time. According to Amin (1999), correlational

research design is one in which measures of association are used to examine the relationship

between the research variables.

3.2 Population of the studyThe target population in this study involved 240 staff in selected branches of Barclays bank;

the researcher selected the bank staff because of easy accessibility and to minimize time and

financial constraints.

3.3 Sample sizeThe study used Slovene’s formula for selected banks to arrive at the sample size. The sample

was comprised of selects bank and computed using the Slovene’s formula below.

Where: - (n) = N1 +N(e)2

n = Sample size

N = Population size

e = (level of significance; the error) =e 0.05 i.e. e2 = (0.05)2 =0.0025

240 = 240 = 240 =1501 +240 (0.05)2 1 + 240 (0.0025) 1.6

19

Table 3.1: Population and Sample SizeS/no Categories Populat Sample Data Sampling

ion size collection methodsmethods

I Barclays bank Kampala road 100 60 Questionnair Simple randombranch e

2 Barclays bank Kikuubo branch 80 50 Questionnair Simple randome

3 Barclays bank Room street 60 40 Questionnair Simple randombranch e

4 Total 240 150

3.4 Sampling procedure

Simple random sampling and purposive sampling was used to select the respondents.

Purposive sampling was used to select employees from the Barclays bank and these included

managers, and bank employees. Simple random sampling was used to select bank employees.

This ensured that all top employees are represented in the study and all had a chance of being

selected to participate in this study as respondents.

3.5 Sources of data

A number of sources of data were used to facilitate data collection from the respondents.

These included questionnaires, interview guide and observation guide and document analysis.

3.5.1 Primary sourcesQuestionnaire

A questionnaire was used as source of data collection since it had instructions on paper to

guide and explain to the participant, according to the response. According to Paul (2013) a

questionnaire is suitable for source of data collection since it goes deep within minds or

attitudes, feeling or reactions of people. Therefore the researcher had to distribute the

questionnaires to the bank staff in order to collect the required information.

Interviews

This is a data collection source which was used in interviewing of respondents. An interview

is a source of data collection in which a researcher obtains information from the respondents

by face-to-face interaction, oral or telephone conversation. It was used because of the

relatively high response rate and suitability to gather information.

20

3.5.2 Secondary sources

This was sourced by reviewing of already existing documented resources such as

newspapers, journals, reports, presentations, magazines. This was done in order to first

identify the existing information on the research topic and to understand how much the

respondents know about the research topic in order to avoid lies.

3.6 Research instrument

3.6.1 QuestionnaireA questionnaire was the malor method used for data collection. The questionnaire was

preferred for this study because it enabled the researcher reach a larger number of

respondents within a short time, thus can make it easier to collect relevant information. The

first section in the questionnaire was the face sheet, to collect data on profile of respondents.

The second section in the questionnaire will be credit policy .The third section of the

questionnaire had questions on financial performance. All the questions are Likert Scaled on

four points ranging from 1= strongly disagree, 2 = disagree, 3 = agree, and 4 = strongly agree.

The questionnaire contained close-ended questions to collect quantifiable data relevant for

precise and effective correlation of research variables. It was preferred to save time. enable

respondents to easily fill out the questionnaires and keep them on the subject and relatively

objective.

3.6.2 Interview guideThe interview guide was used to collect key information about the study from key

respondents who were some of the managers of the Barclays bank from different branches.

The respondents were asked questions including opinions on the subject matter. This aimed at

collecting information that couldn’t be put down in writing.

3.7 Validity and reliability of the instrument

3.7.1 ValidityHere the questionnaire was given to three lecturers (experts) to judge the validity of questions

according to the objectives. After the assessment of the questionnaire, the necessary

adjustments were made bearing in mind the objectives of the study. Then a content validity

index (CVI) was computed using the following formula,

CVI =

21

A minimum of 0.75 of CVI will be used to test validity of the research instrument

3.7.2 ReliabilityTo ensure the reliability of the instrument, the researcher used the test-retest method. The

questionnaire was given to 1 0 people and after two weeks, the same questionnaire was given

to the same people and the Cronbatch Alpha was computed using SPSS. The minimum

Cronbatch Alpha coefficient of 0.75 was used to declare an instrument reliable (>0.75).

3.8 Data gathering procedure

Before the administration of the questionnaires

Before the administration of the questionnaires the researcher had to take an introductory

letter from the College of Economics and Management (CEM). the researcher had to first

seek authorization from the proposed respondents to conduct research and review the

questions to avoid errors and ensure that only qualified respondents are approached.

During the administration of the questionnaires

The respondents were requested to sign and answer the questionnaires. The researcher

emphasized retrieval of the questionnaires within three days from the date of distribution.

And lastly, all returned questionnaires were checked if all were answered.

After the administration of the questionnaires

The data gathered was collected, coded into the computer and statistically treated using the

Statistical Package for Social Sciences (SPSS).

3.9 Data Analysis

The frequency and percentage distribution were used to determine the demographic

characteristics of the respondents. The mean and standard deviations were applied for the

extent of credit policy and financial performance. An item analysis illustrated the strengths

and weaknesses of the respondents based on credit policy and financial performance in terms

of mean and rank. From these strengths and weaknesses, the recommendations were derived.

22

The following mean ranges and descriptions were used to interpret responses:

For credit policy

Mean Range Response Mode Interpretation

3.26-4.00 Strongly agree Very satisfactory

2.51-3.25 Agree Satisfactory

1 .76-2.50 Disagree Unsatisfactory

1 .00-1.75 Strongly disagree Very unsatisfactory

For financial performance

Mean Range Response Mode Interpretation

3.26-4.00 Strongly agree Very satisfactory

2.51-3.25 Agree Satisfactory

1 .76-2.50 Disagree Unsatisfactory

1 .00-1.75 Strongly disagree Very unsatisfactory

The researcher used Pearson’s linear correlation coefficient (PLCC) to analyze the

relationship between credit policy and financial performance.

3.10 Ethical considerations

To ensure confidentiality of the information provided by the respondents and to ascertain the

practice of ethical in this study, the following activities were implemented by the researcher:

1. Requested the respondents to sign in the inform consent form

2. Acknowledged the authors quoted in this study and the author of standardized

instrument through citations and referencing.

3. Presented the findings in a generalized manner.

23

3.11 Limitations of the study

In view of the following threats to validity, the researcher allows 0.05 level of significance.

Measures are also indicated in order to minimize if not to eradicate the threats to the validity

of the findings of the study.

I. Extraneous variables were beyond the researcher’s control such as respondent’s

honesty, personal biases and uncontrolled setting of the study

2. Testing the use of research assistants can bring about inconsistency in the

administration of the questionnaires in terms of time of administration, understanding

of the items in the questionnaires and explanations given to the respondents. To

minimize the threat, the respondents were briefed on the procedures to be done in data

collection.

3. Attrition/Mortality: Not all questionnaires were returned completely answered or

even retrieved back due to circumstances on the part of the respondents such as

travels, sickness, hospitalization and refusal/withdrawal to participate. In anticipation

to this, the researcher reserved more respondents by exceeding the minimum sample

size. The respondents were also reminded not to leave any item in the questionnaires

unanswered and were closely followed up as to the date of retrieval.

24

CHAPTER FOUR

DATA PRESENTATION, ANALYSIS AND INTERPRETATION OF RESULTS

4.0 Introduction

This chapter presents the extent of credit policy, level of performance, significant relationship

between credit standards and financial performance. significant relationship between Credit

risk controls and financial performance and the significant relationship between Collection

policy and financial performance of Barclays Bank in Kampala Uganda.

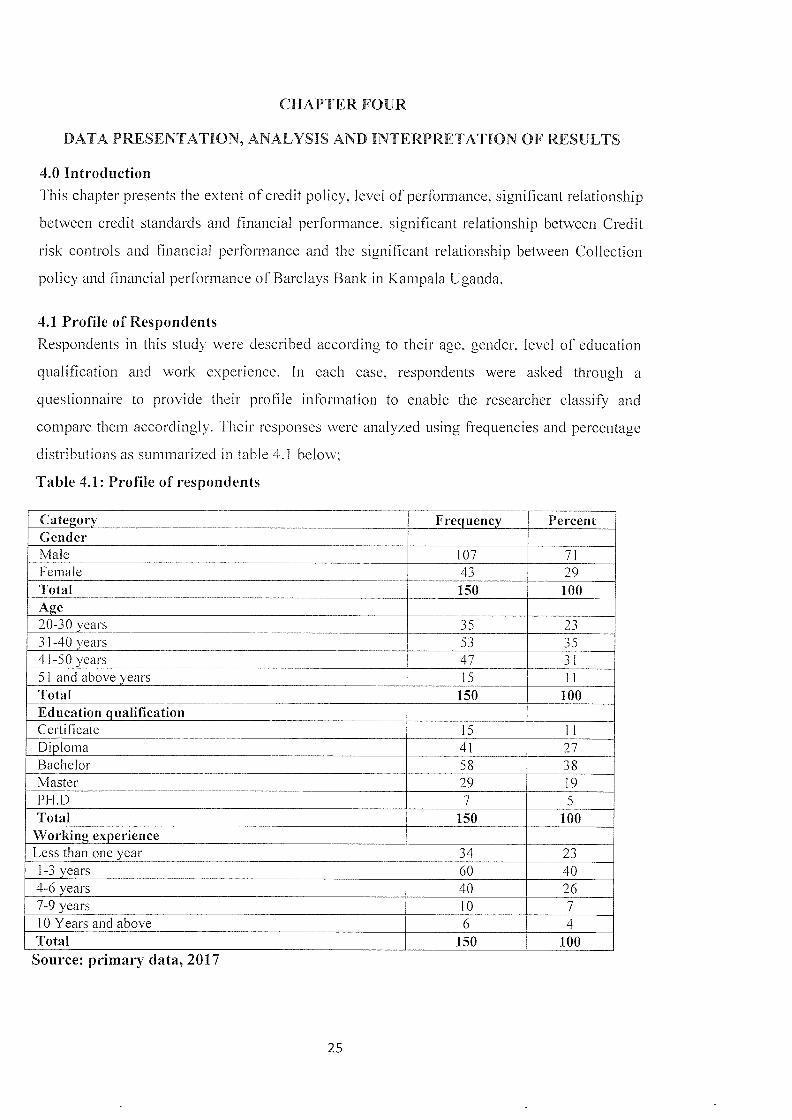

4.1 Profile of Respondents

Respondents in this study were described according to their age, gender, level of education

qualification and work experience. In each case, respondents were asked through a

questionnaire to provide their profile information to enable the researcher classify and

compare them accordingly. Their responses were analyzed using frequencies and percentage

distributions as summarized in table 4.1 below;

Table 4.1: Profile of respondents

Category q~çy_ PercentGenderMale 107 71Female 43 29Total 150 100Age20-30 years 35 233 1-40 years 53 3541-50 years 47 315 1 and above years 15 1 1Total 150 100Education_qualificationCertificate 15 1 1Diploma 41 27Bachelor 58 38Master 29 19PH.D 7 5Total 150 100Working experienceLess than one year 34 231-3 years 60 404-6 years 40 267-9 years 1 0 71 0 Years and above 6 4Total 150 100Source: primary data, 2017

25

The results from the above table indicated that majority of respondents in this sample were

male (71 %) and yet female respondents were 29%. This implied a gender gap among both

employees and customers of Barclays in Kampala Uganda. The findings of the study showed

that 23% of the respondents were between 20-30 years, while 35% were between 31-40

years. 31% were 41-50 years, and also finally 11% of the respondents had 51 years and

above, this implied that majority of respondents in this sample were in their middle

adulthood,

With respect to education background, 11% of the respondents were certificate holders, the

second group of the respondents were diploma holders (27%), 38% of the respondents were

bachelors’ degree holders, 19% were master’s degree holders and finally 5% of the

respondents were PhD holders. This implied that the majority of respondents in this sample

were relatively qualified in academics. In the case of working experience 23% of the

respondents had worked for less than one year, 40% had an experience of 1 to 3 years, 26%

of the respondent worked for 4-6 years, 7% had a working experience of 7 to 9 years, while

4% of the respondent had a working experience of 10 years and above in the same field,

hence implying that the respondents in this sample were relatively experienced in the same

field.

4.2 Credit policyThe independent variable in this study was credit policy which was broken into three

constructs and these were; credit standards (measured with ten questions), credit risk controls

(with ten questions) and collection policy (with ten questions). These questions were based

on a four point Likert scale, in which respondents were asked to rate the extent of credit

policy by indicating the extent to which they agree or disagree with each question in the

questionnaire. The SPSS software was used to analyze their responses using means and ranks

as indicated in table 4.2. To interpret the means in table 4.2, the following mean ranges and

their descriptions were used;

Key to interpretation of means

Mean range Response range Interpretation3.26 - 4.00 strongly agree Very satisfactory2.51 -3.25 Agree Satisfactory1.76 - 2.50 Disagree Unsatisfactory1 .00 - 1 .75 strongly disagree Very unsatisfactory

26

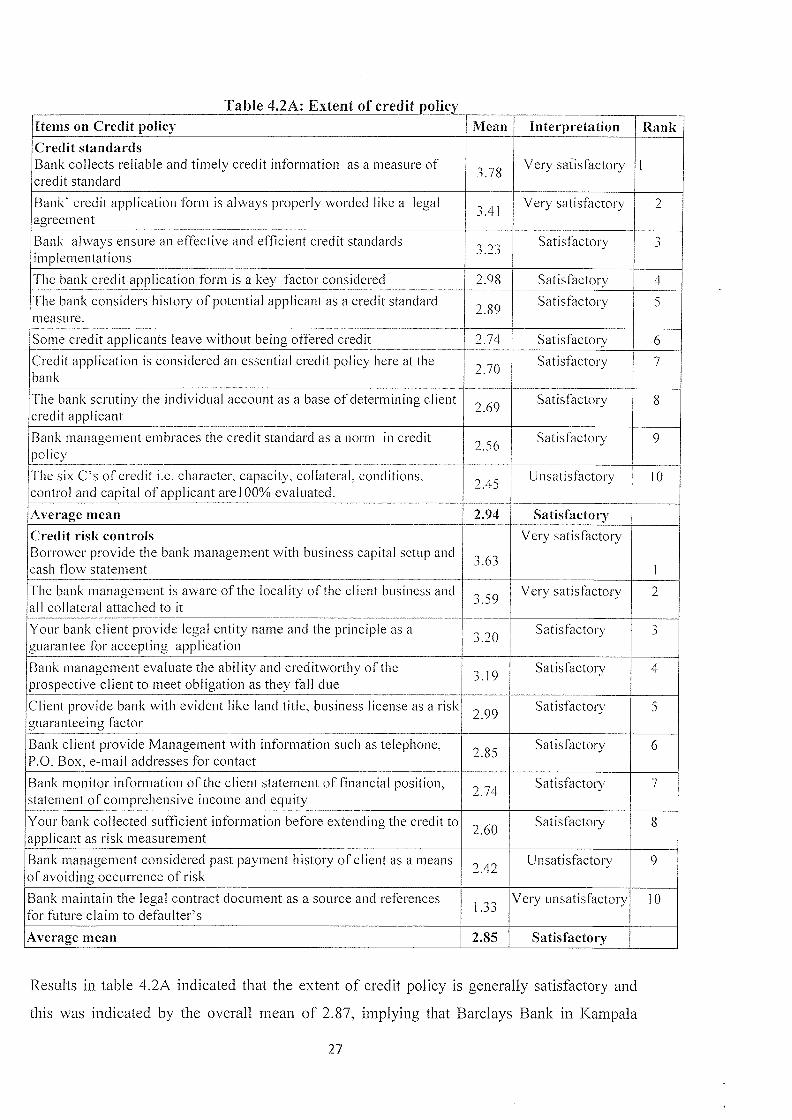

Table 4.2A: Extent of credit policyItems on Credit policy Mean Interpretation RankCredit standardsBank collects reliable and timely credit information as a measure of 78 Very satisfactory Icredit standard

Bank’ credit application form is always properly worded like a legal 41 Very satisfactory 2agreement

Bank always ensure an effective and efficient credit standards Satisfactory 3. .

i m p1 em e ntat ins

The bank credit application form is a key factor considered 2.98 Satisfactory 4

The bank considers history of potential applicant as a credit standard 2 89 Satisfactory 5measure.

Some credit applicants leave without being offered credit 2.74 Satisfactory 6

Credit application is considered an essential credit policy here at the 2 70 Satisfactory 7bank

The bank scrutiny the individual account as a base of determining client 2 69 Satisfactory 8credit applicant

Bank management embraces the credit standard as a norm in credit 2 56 Satisfactory 9policy

The six C’s of credit i.e. character, capacity, collateral, conditions, ~ 45 Unsatisfactory 10control and capital of applicant arel 00% evaluated.

Average mean 2.94 Satisfactory

Credit risk controls Very satisfactoryBorrower provide the bank management with business capital setup and 3 63cash flow statement

The bank management is aware of the locality of the client business and ~ Very satisfactory 2all collateral attached to it 3.

Your bank client provide legal entity name and the prmciple as a Satisfactory 3guarantee for accepting application

Bank management evaluate the ability and creditworthy of the 19 Satisfactory 4prospective client to meet obligation as they fall due

Client provide bank with evident like land title, business license as a risk 2 99 Satisfactory 5guaranteeing factor

Bank client provide Management with information such as telephone, 2 85 Satisfactory 6P.O. Box, e~niail addresses for contact

Bank monitor information of the client statement of financial position, 2 74 Satisfactory 7statement of comprehensive income and equity

Your bank collected sufficient information before extending the credit to 2 60 Satisfactory 8applicant as risk measurement

Bank management considered past payment history of client as a means 2 42 Unsatisfactory 9of avoiding occurrence of risk

Bank maintain the legal contract document as a source and references ~, Very unsatisfactory 10for future claim to defaulter’s

Average mean 2.85 Satisfactory

Results in table 4.2A indicated that the extent of credit policy is generally satisfactory and

this was indicated by the overall mean of 2.87, implying that Barclays Bank in Kampala

27

Uganda have a good credit policy that ensures operational consistency and adherence to

uniform and sound practices. Results further denoted that the extent of credit policy differs on

different items and in different perspectives; for example, credit standards, the respondents

rated this construct generally satisfactory (average mean=2.94), implying that Barclays Bank

in Kampala Uganda always collect reliable and timely credit information as a measure of

credit standard.

With respect to credit risk controls, this variable was rated satisfactory on average and this

was indicated by the average mean of 2.85, hence implying that Barclays Bank in Kampala

Uganda always make sure that the borrowers provide the bank management with business

capital setup and cash flow statement, results in table 4.2A further indicated that of the ten

items used to measure this construct; only two items were rated very satisfactory, six items

were rated satisfactory, one time was rated unsatisfactory and only one item was rated very

unsatisfactory.

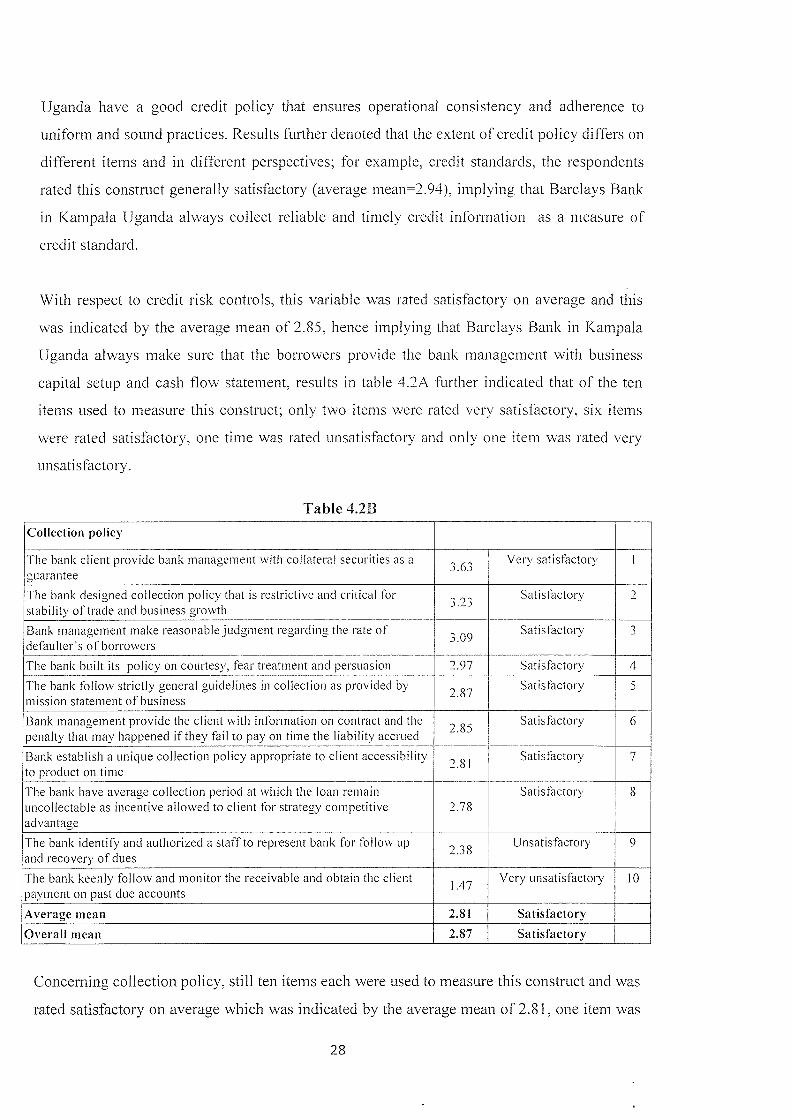

Table 4.2B

Collection policy

The bank client provide bank management with collateral securities as a 63 Very satisfactory iguarantee

The bank designed collection policy that is restrictive and critical for 2~ Satisftictory 2stability of trade and business growth

Bank management make reasonable judgment regarding the rate of 09 Satisfactory 3defaulter’s of borrowers

The bank built its policy on courtesy, fear treatment and persuasion 2.97 Satisfactory 4

The bank follow strictly general guidelines in collection as provided by ~ 87 Satisfactory 5mission statement of business —.

Bank management provide the client with information on contract and the 2 85 Satisfactory 6penalty that may happened if they fail to pay on time the liability accrued

Bank establish a unique collection policy appropriate to client accessibility ‘? 81 Satisfactory 7to product on time

The bank have average collection period at which the loan remain Satiskictory 8uncollectable as incentive allowed to client for strategy competitive 2.78advantage

The bank identify and authorized a staff to represent bank for follow ~ 2 ~8 Unsatisfactory 9and recovery of dues .3

The bank keenly follow and monitor the receivable and obtain the client ~ Very unsatisfactory 10payment on past due accounts

Average mean 2.81 Satisfactory

Overall mean 2.87 Satisfactory

Concerning collection policy, still ten items each were used to measure this construct and was

rated satisfactory on average which was indicated by the average mean of 2.81, one item was

28

rated as very satisfactory, seven items were rated satisfactory, one item was rated

unsatisfactory and one item was rated very un satisfactory. hence implying that the bank

clients always provide collateral securities as a guarantee to bank management.

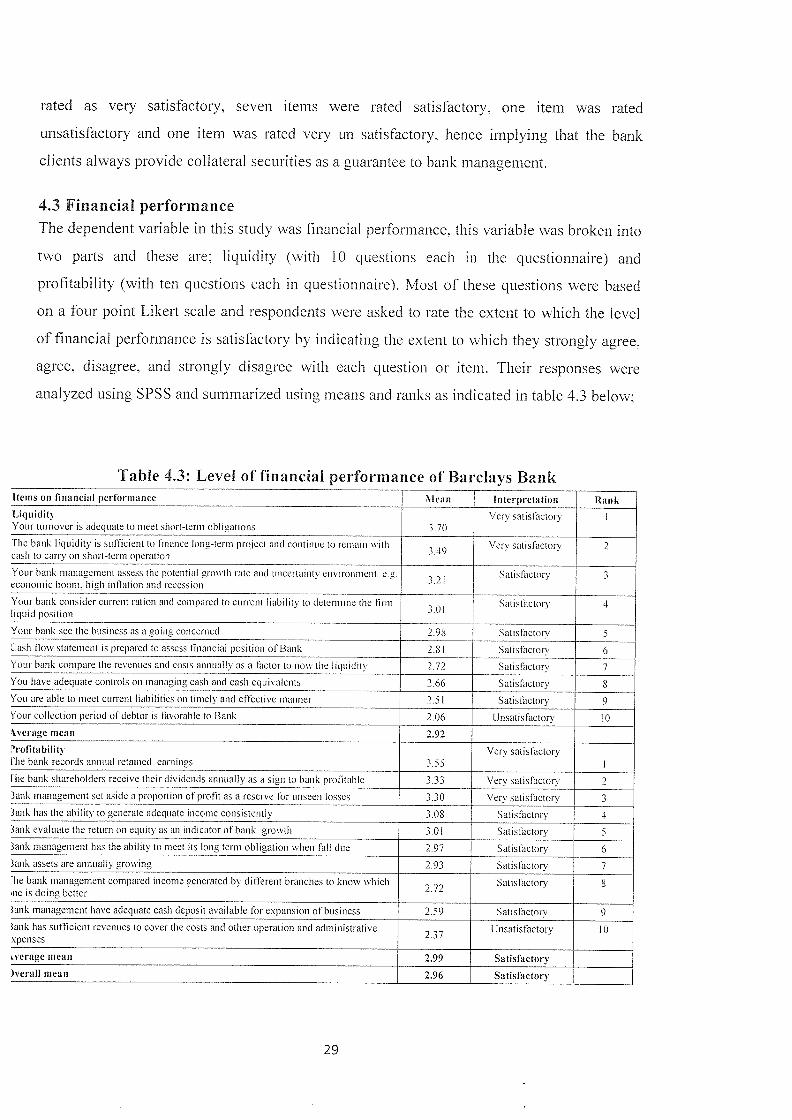

4.3 Financial performanceThe dependent variable in this study was financial performance, this variable was broken into

two parts and these are; liquidity (with 10 questions each in the questionnaire) and

profitability (with ten questions each in questionnaire). Most of these questions were based

on a four point Likert scale and respondents were asked to rate the extent to which the level

of financial performance is satisfactory by indicating the extent to which they strongly agree,

agree, disagree, and strongly disagree with each question or item. Their responses were

analyzed using SPSS and summarized using means and ranks as indicated in table 4.3 below;

Table 4.3: Level of financial performance of Barclays BankItems on financial perform a nec ~ lean In terpreta lion Rank

Liquidity Very satisfactoryYour turnover is adequate to meet short—term obligations 3.70

The hank liquidity is sufficient to finance long—term project and continue to remain with • Very satisfactory 2cash to carry on short—term operation

Your bank management assess the potential growth rate and uncertaint coy i ron ment. e.g. ., Satis factory 3economic boom, high inflation and recession

Your hank consider current ration and compared to current I isbi I tv to determine the firm Satisfactory 4

- ~.0l

I quid pos tion

Your hank see the business as a going concerned 2.98 Satisfactory 5

Cash flow statement is prepared to assess financial position of l3ank 2.81 Satisfactory 6

Your bank compare the revenues and costs annually asa factor to now the liquidity 2.72 Satisihetory 7

You ltave adequate controls on managing cash and cash equivalents 2.66 Satisfactory 8

You are able to meet current liabilities on timely and effective manner 2.51 Satisfactory 9

Your collection period of debtor is favorable to Bank 2.06 Unsatisfactory 10

-~verage mean 2.92

~rotitabilitv Very satisfactoryfhe bank records annual retained earnings 3.55

Flie bank shareholders receive their dividends annually as a sign to hank profitable 3.33 Very satisfactory 2

3ank management set aside a proportion of profit as a reserve for unseen losses 3.30 Very satisfactory 3

3ank has the ability to generate adequate income consistently 3.08 Satisfactory 4

3ank evaluate the return on equity as an indicator of hank growth 3.01 Satisfactory 5

~ank management has the ability to meet its long term obligation when fall due 2.97 Satisfactory 6

tank assets are annually growing 2.93 Satisfactory 7

The bank management compared income generated by different branches to know which ~ 77 Satisfactory Sne is doing better

tank management have adequate cash deposit available for expansion of business 2.59 Satisfactory 9

lank has sufficient revenues to cover the costs and other operation and administrative 737 Unsatisfactory 10xpenses —.

Lverage mean 2.99 Satisfactory

)verall mean 2.96 Satisfactory

29

Results in table 4.3 indicated that the extent of financial performance of Barclays Bank is

generally satisfactory and this was indicated by the overall mean of 2.96, hence implying that

Barclays Bank in Kampala Uganda~always use their assets and other resources effectively

and efficiently. With respect to liquidity as the first construct on the dependent variable was

measured using ten items in each Barclays Bank and this was rated satisfactory on average

(mean=2.92), this implies that the Banks’ turnover is adequate to meet short-term obligations.

Concerning profitability; on average this construct was rated satisfactory and this was

indicated by the average mean of 2.99. this implies that the Banks’ shareholders receive their

dividends annually as a sign to high levels of profits, still results indicated that only one item

was rated unsatisfactory (mean=2.37).

4.4 Relationship between credit standards and financial performanceThe first objective in this study was to establish the effect of credit standards on financial

performance in Barclays Bank in Kampala Uganda, to achieve this objective and to test this

null hypothesis, the researcher used the Pearsons Linear Correlation Coefficient as indicated

in table 4.4;

Table 4.4. Significant relationship between credit standards and financial performanceVariables correlated r-value Sig Interpretation Decision

on HoCredit standards

Vs .896 .000 Significant RejectedFinancial performance correlation

Source: Primary Data, 2017

Results in table 4.4 indicated a positive significant relationship between credit standards and

financial performance, since the sig. value (0.000) was less than 0.05 and which is the

maximum level of significance required to declare a significant relationship. This implies that

good credit standards highly contribute to the financial performance in Barclays Bank in

Kampala Uganda, and unfavorable credit standards reduces it; here the stated null hypothesis

was rejected basing on these results and hence concluding that high levels of credit standards

contribute to the financial performance of Barclays Bank in Kampala Uganda.

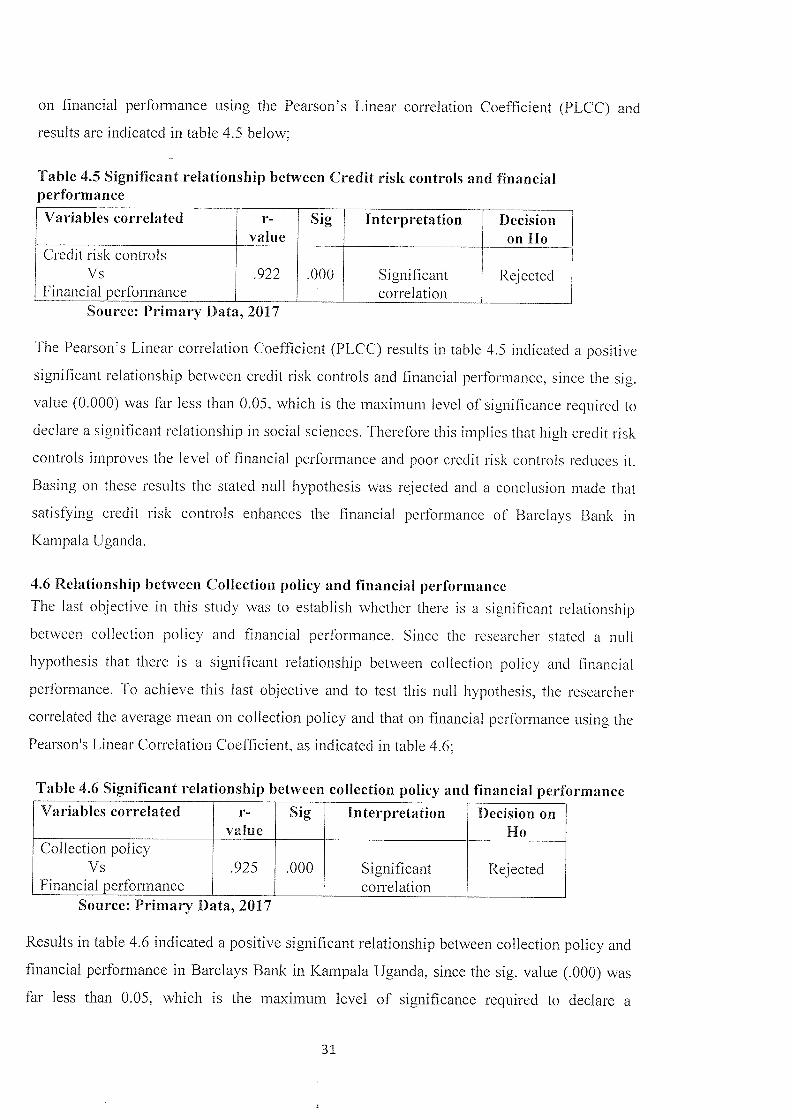

4.5 Relationship between Credit risk controls and financial performanceThe second objective in this study was to establish whether there is a significant relationship

between credit risk controls and financial performance, for which it was hypothesized that

credit risk controls and financial performance were not significantly correlated. To test this

null hypothesis, the researcher correlated the mean indices on credit risk controls and those

30

on financial performance using the Pearson’s Linear correlation Coefficient (PLCC) and

results are indicated in table 4.5 below;

Table 4.5 Significant relationship between Credit risk controls and financialperformanceVariables correlated r- Sig Interpretation Decision

value on HoCredit risk controls

Vs .922 .000 Significant RejectedFinancial performance - correlation

Source: Primary Data, 2017

The Pearson’s Linear correlation Coefficient (PLCC) results in table 4.5 indicated a positive

significant relationship between credit risk controls and financial performance, since the sig.

value (0,000) was far less than 0.05, which is the maximum level of significance required to

declare a significant relationship in social sciences. Therefore this implies that high credit risk

controls improves the level of financial performance and poor credit risk controls reduces it.

Basing on these results the stated null hypothesis was rejected and a conclusion made that

satisfying credit risk controls enhances the financial performance of Barclays Bank in

Kampala Uganda.

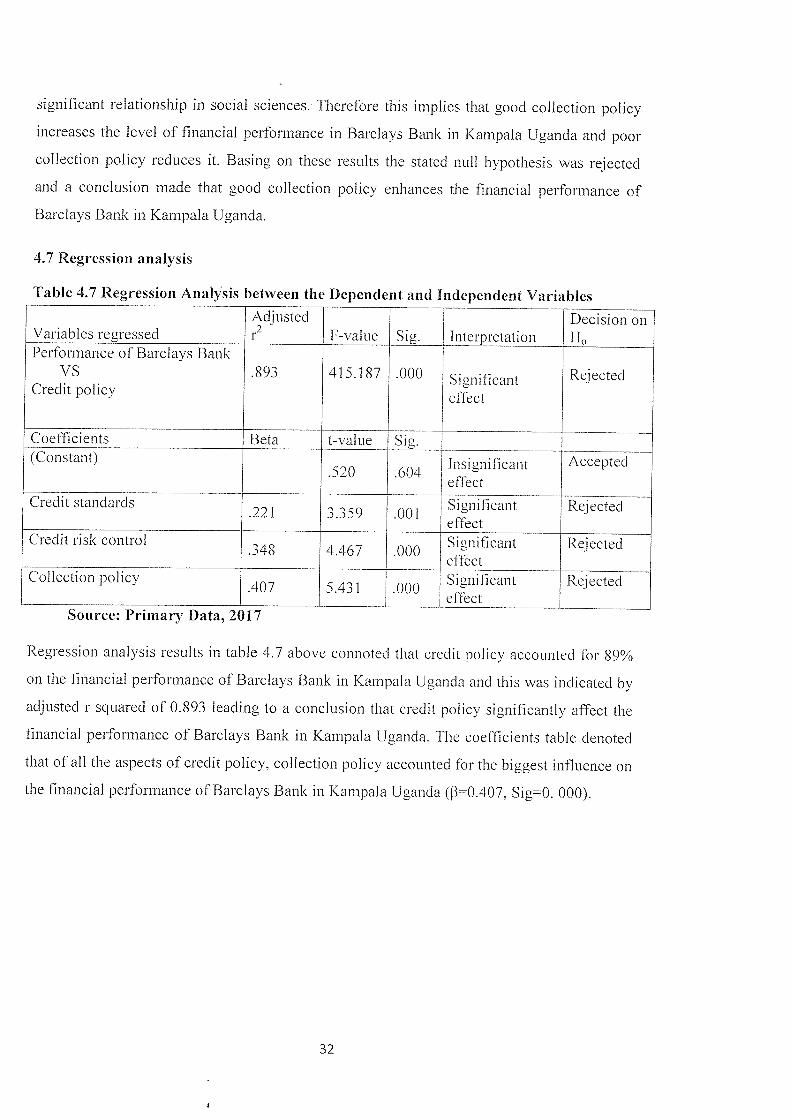

4.6 Relationship between Collection policy and financial performanceThe last objective in this study was to establish whether there is a significant relationship