Embed Size (px)

DESCRIPTION

Â

Citation preview

A. Post Credit Crunch EuropeImpact on Small and Medium Enterprises (SMEs)

A macro- and polito-economical approachby Prof. Norbert W. Knoll von Dornhoff, LL.D., Mag.rer.soc.oec

I. Nature and reasons of Credit Crunches 1. Definitions 2. Analytic tools, e.g. Bubble EconomyII. Financial Crisis and Credit Crunch in Europe 1. Underlying reason for Europe’s vulnerability 2. Regional impact on SMEs 3. Video clip Interview with an Investment Banker - DiscussionIII. Polito-economical responses 1. European Union (with video clip) 2. Individual European Countries´Responses 3. European NGOs 4. Forecasts 2009 - 2010IV. Worldbank - Ease of Doing Business (SMEs) - Getting CreditV. Students playing Finance Ministers simulating reforms and seeing instantly the changes in international ranking of the Countries. (An interactive game - Students and Lectors)

IP 2008-2009 LeonCompetencies of SME's in the transforming environment of the enlarged Europe

I. Nature and reasons of Credit Crunches

1. Definitions

a) Micro, small and medium-sized enterprises (SMEs) This category is made up of enterprises which employ fewer than 250 persons and which have an annual turnover not exceeding 50 million euro, and/or an annual balance sheet total not exceeding 43 million euro.’ Extract of Article 2 of the Annex of Recommendation 2003/361/EC

Micro, small and medium-sized enterprises(SMEs) play a central role in theEuropean economy. They are a majorsource of entrepreneurial skills,innovation and employment. In theenlarged European Union of 25 countries,some 23 million SMEs provide around75 million jobs and represent 99% of allenterprises.

SME - DEFINITION -continued

EU Member States traditionally have their own definition of what constitutes an SME, for example the traditional definition in Germany had a limit of 250 employees, while, for example, in Belgium it could have been 100. But now the EU has started to standardize the concept. Its current definition categorizes companies with fewer than 10 employees as "micro", those with fewer than 50 employees as "small", and those with fewer than 250 as "medium".[1] By contrast, in the United States, when small business is defined by the number of employees, it often refers to those with fewer than 100 employees, while medium-sized business often refers to those with fewer than 500 employees.

b) Credit crunch Definitions * A state in which there is a short supply of cash to lend to businesses and consumers and interest rates are high Source: wordnet.princeton.edu/perl/webwn

* A credit crunch is a sudden reduction in the availability of loans (or "credit") or a sudden increase in the cost of obtaining a loan from the banks, investors etc. Source: en.wikipedia.org/wiki/Credit_crunch

* A period of economic recession in which credit and investment capital are difficult to obtain, causing a shortage of liquidity Source: en.wiktionary.org/wiki/credit_crunch

* A period when there is a sharp reduction in the availability of finance from banks and other financial institutions, particularly from small ... Source: www.ampcapital.co.nz/corporate/glossary.asp

2. Analytic tools, e.g. Bubble Economy

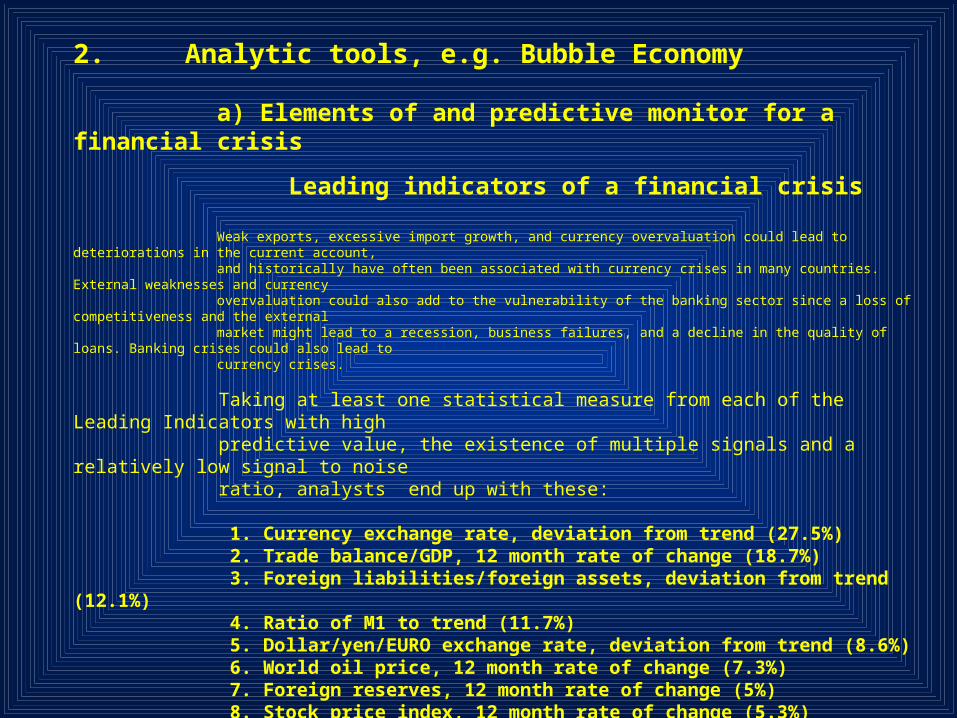

a) Elements of and predictive monitor for a financial crisis Leading indicators of a financial crisis Weak exports, excessive import growth, and currency overvaluation could lead to deteriorations in the current account, and historically have often been associated with currency crises in many countries. External weaknesses and currency overvaluation could also add to the vulnerability of the banking sector since a loss of competitiveness and the external market might lead to a recession, business failures, and a decline in the quality of loans. Banking crises could also lead to currency crises.

Taking at least one statistical measure from each of the Leading Indicators with high predictive value, the existence of multiple signals and a relatively low signal to noise ratio, analysts end up with these:

1. Currency exchange rate, deviation from trend (27.5%) 2. Trade balance/GDP, 12 month rate of change (18.7%) 3. Foreign liabilities/foreign assets, deviation from trend (12.1%) 4. Ratio of M1 to trend (11.7%) 5. Dollar/yen/EURO exchange rate, deviation from trend (8.6%) 6. World oil price, 12 month rate of change (7.3%) 7. Foreign reserves, 12 month rate of change (5%) 8. Stock price index, 12 month rate of change (5.3%) 9. Government consumption/GDP, deviation from trend (3.8%) Source: Source of Leading Indicators from Asian Development Bank: Causes of the 1997 Asian Financial Crisis: What can an early warning system model tell us?

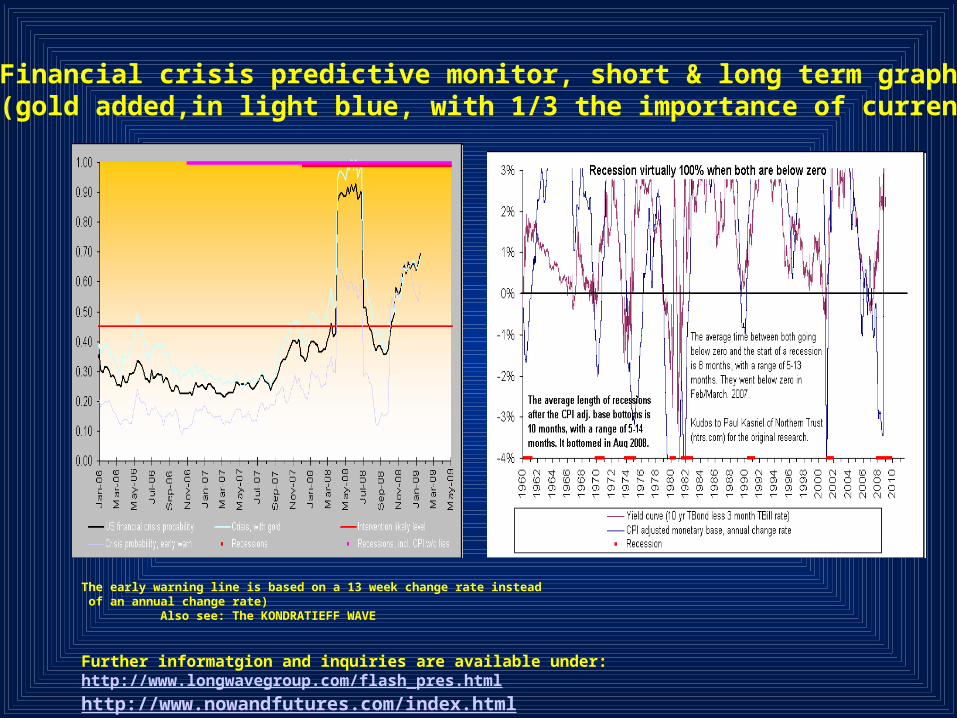

Financial crisis predictive monitor, short & long term graphs(gold added,in light blue, with 1/3 the importance of currency)

The early warning line is based on a 13 week change rate instead of an annual change rate) Also see: The KONDRATIEFF WAVE Further informatgion and inquiries are available under: http://www.longwavegroup.com/flash_pres.html http://www.nowandfutures.com/index.htmlmailto: [email protected]

b) Methods of psychology

Inclusion of human tendencies by methods of psychology

Example:Greed / Fear IndexA tentative index to help track relative fear in the various markets. The gold price is shown for reference. The algorithm behind the index is proprietary, but some of the inputs are the gold price, the VIX, various sentiment indexes and CBOE options data.

II. Financial Crisis and Credit Crunch in Europe

1. Underlying reason for Europe’s vulnerability

Some crucial issues (A) a) The underlying reason for Europe’s vulnerability is rooted not in the U.S. subprime — that is only the proximate trigger — but instead in the importance of banks to the entire European economy. b) Wholly unrelated to exposure to American subprime, Europe’s banking vulnerabilities can be broken down into three categories: the broad credit crunch, European subprime and the Balkan/Baltic overexposure.

c) The euro’s adoption granted this low interest rate environment, which normally only a state of Germany’s strength and heft could sustain, to all of the eurozone. This easy credit environment echoed by affiliation to most of the smaller and poorer (and newer) EU members as well. Cheap credit led to a consumer spending boom — which was stronger in the traditionally credit- poor smaller, poorer, newer economies — leading not only to a real estate expansion, but also to an overall economic boom that, even without the subprime issue and the global credit crunch, was going to burst.

Some fundamental findings (B)

d) Underneath the global credit crunch looms the second problem: the European subprime crisis. cheap credit for the first time. The subsequent real estate boom Spain built more homes in 2006 than Germany, France and the United Kingdom combined — led to the growth of the banking and construction industry. Banks pushed for more lending by giving out liberal mortgage terms — in Ireland the no-down- payment 110 percent mortgage was a popular product.

e) The poorer, smaller and newer European countries gorged the most on this new credit, and none gorged more deeply than the Baltic and Balkan countries, leading to the third problem: Baltic and Balkan overexposure. Growth rates approached 15 percent in the Baltics, surpassing even East Asian possibilities — but all on the back of borrowed money

f) Fueling the surges were Italian, French, Austrian, Greek and Scandinavian banks. Limited as they were by their local domestic markets, they pushed aggressively into their Eastern neighbors. The Scandinavian banks rushed into the Baltic countries and the Greek and Austrian banks focused on the Balkans, while the Italian and French also went to Russia. UniCredit, the Italian behemoth with vast operations across Eastern Europe, announced Oct. 6 that it was facing a credit crisis, and it is hardly alone.

2. Regional impact on SMEs

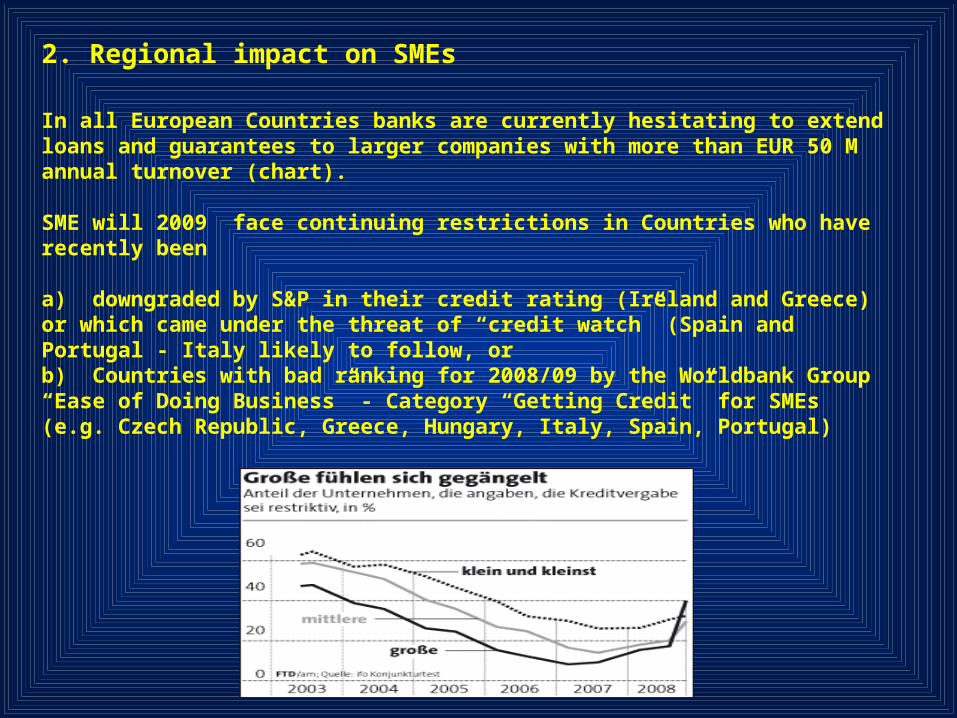

In all European Countries banks are currently hesitating to extend loans and guarantees to larger companies with more than EUR 50 M annual turnover (chart).

SME will 2009 face continuing restrictions in Countries who have recently been

a) downgraded by S&P in their credit rating (Ireland and Greece) or which came under the threat of “credit watch” (Spain and Portugal - Italy likely to follow, orb) Countries with bad ranking for 2008/09 by the Worldbank Group “Ease of Doing Business” - Category “Getting Credit” for SMEs (e.g. Czech Republic, Greece, Hungary, Italy, Spain, Portugal)

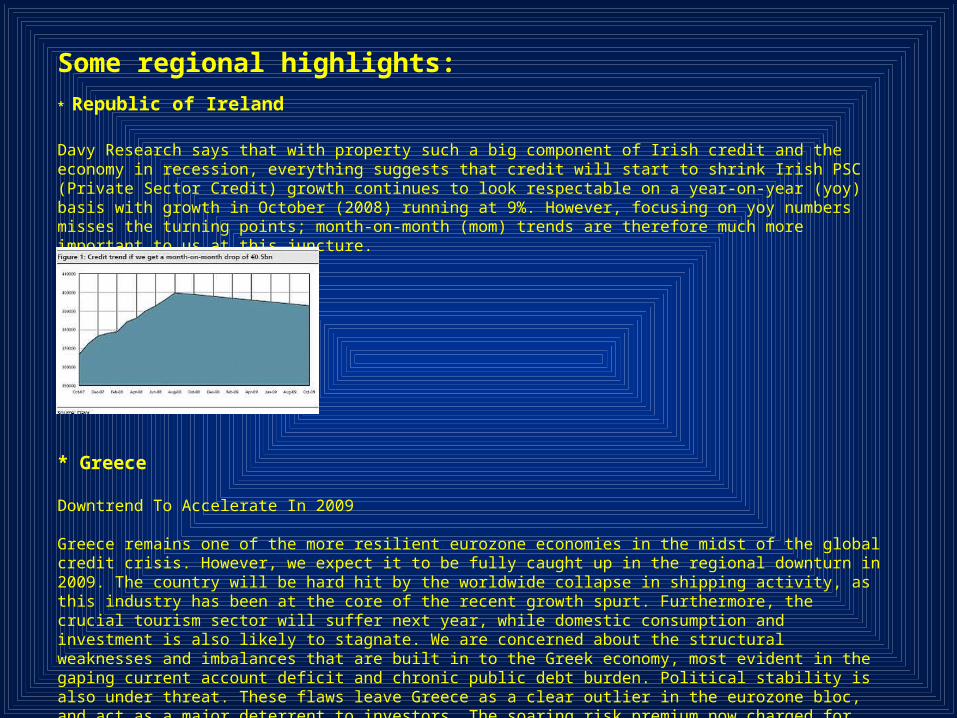

Some regional highlights:* Republic of Ireland

Davy Research says that with property such a big component of Irish credit and the economy in recession, everything suggests that credit will start to shrink Irish PSC (Private Sector Credit) growth continues to look respectable on a year-on-year (yoy) basis with growth in October (2008) running at 9%. However, focusing on yoy numbers misses the turning points; month-on-month (mom) trends are therefore much more important to us at this juncture.

* Greece

Downtrend To Accelerate In 2009

Greece remains one of the more resilient eurozone economies in the midst of the global credit crisis. However, we expect it to be fully caught up in the regional downturn in 2009. The country will be hard hit by the worldwide collapse in shipping activity, as this industry has been at the core of the recent growth spurt. Furthermore, the crucial tourism sector will suffer next year, while domestic consumption and investment is also likely to stagnate. We are concerned about the structural weaknesses and imbalances that are built in to the Greek economy, most evident in the gaping current account deficit and chronic public debt burden. Political stability is also under threat. These flaws leave Greece as a clear outlier in the eurozone bloc, and act as a major deterrent to investors. The soaring risk premium now charged for Greek bonds is testament to this problem, and will leave the country highly vulnerable during this economic crisis.

Regional highlights continued......

* Spain

Pressures on Spain´s public finances and slowing projected growth rate prompted S&P to place the country on credit watch. The rating agency forecasts that Spain´s general government deficit “stay well above” 3 per cent until 2011 and peak above 6 per cent in 2009

* Eastern Europe

Most economists forecast growth in the region of 5.5% to 6% in 2008, which is slower than in 2007, but still considered robust. This is still a fast-growing region with strong fundamentals (EBRD). The Baltics and Balkans remain particularly dependent on foreign capital to finance their huge current account deficits

EBRD recognises "high levels of current account deficits, high exposure to foreign borrowing and political uncertainties in some countries“. Given that the roots of this latest global slowdown lie in tighter credit conditions, it is impossible to ignore the impact of weaker capital inflows on regional prospects.

One of the reasons is that the performance of Eastern Europe will be largely determined by the eurozone economy. The countries of Central Europe look particularly exposed to a sharp slowdown in the euro zone: if growth in the single currency area dips to 1.5%, Hungary could slip into recession.

III. Polito-economical responses

1. European Union (with video clip) a) Presidency Conclusions - Brussels, 11th and 12th Dec 2008 European Economic Recovery Plan - EERP The European Economic Recovery Plan, equivalent to about 1,5 % of the GDP of the European Union (a figure amounting to around EUR 200 billion). The plan provides a common framework for the efforts made by Member States and by the European Union.

The EERP refers to SMEs as follows:

i. As regards action by the European Union, the European Council supports in particular:− an increase in intervention by the European Investment Bank of EUR 30 billion in 2009/2010, especially for small and medium-sized enterprises, for renewable energy and for clean transport, in particular for the benefit of the automotive industry, as well as the creation of the 2020 European Fund for Energy, Climate Change and Infrastructure ("Marguerite Fund") in partnership with national institutional investors;

ii. a temporary exemption of two years beyond the de minimis threshold for State aid in respect of an amount of up to EUR 500 000 and the adaptation of the framework, as required to increase support for enterprises, especially SMEs, and full implementation of the action plan for a Small Business Act adopted by the Council on1 December 2008;

iii. depending on national circumstances, these measures may take the form of increased public spending, judicious reductions in tax burdens, a reduction in social security contributions, aid for certain categories of enterprises or direct aid to households, especially those which are most vulnerable;

European Union - continued.............

b) “Small Business Act" for Europe Adopted in June 2008, the "Small Business Act" for Europe (SBA) reflects the Commission’s political will to recognise the central role of SMEs in the EU economy and for the first time puts into place a comprehensive SME policy framework for the EU and its Member States. It aims to improve the overall approach to entrepreneurship, to irreversibly anchor the “Think Small first” principle in policy making from regulation to public service, and to promote SMEs’ growth by helping them tackle the remaining problems which hamper their development. The Small Business Act for Europe applies to all companies which are independent and have fewer than 250 employees: 99% of all European businesses.

Facilitate SMEs’ access to financeThe European Investment Bank Group will increase its range of financial products offered to SMEs, particularly mezzanine finance. In addition, more funds will be made available by the Commission for micro-credit and access to cross-border venture capital will be facilitated.

Late payments can be crippling for SMEs. To simplify existing provisions and ensure that SMEs get paid within 30 days, the Commission is proposing a revision of the Late Payments Directive.

Source: http://ec.europa.eu/enterprise/entrepreneurship/sba_en.htm

C) European Portal for SMEs (http://www.accesstofinance.eu) Competitiveness & Innovation Framework Programme Video clip - success stories

http://www.sme-finance-day.eu/index.php?id=7

2. Individual European Countries´Responses

Economic stimulus packages in European Countries http://www.tagesschau.de/wirtschaft/konjunkturprogramme102.html

IV. Worldbank - Ease of Doing Business (SMEs) - Getting Credit

1. Doing Business Database

a) The Doing Business project of the World Bank Group

provides objective measures of business regulations and their enforcement across 181 economies and selected cities at the subnational and regional level.

Web: http://www.doingbusiness.org/

b) Economy Rankings

Economies are ranked on their ease of doing business, from 1 – 181, with first place being the best. A high ranking on the ease of doing business index means the regulatory environment is conducive to the operation of business. This index averages the country's percentile rankings on 10 topics, made up of a variety of indicators, giving equal weight to each topic. The rankings are from the Doing

Business 2009 report, covering the period June 2007 through May 2008. See the ranking of a selected Country: http://rru.worldbank.org/businessplanet/#

THANK YOU FOR YOUR ATTENTION

Contact:wus (at) europe.com

![Changes MSPP to MPN- November Update[1]](https://img.dokumen.tips/doc/110x75/552bed8155034658158b461a/changes-mspp-to-mpn-november-update1.jpg)