Embed Size (px)

Citation preview

CREATING PROFITABLE NEW BUSINESS IN BIOFUELS

Heikki Vappula

President

Energy and Pulp Business Group

| © UPM

BIOFUELS

Four megatrends drive demand for biofuels

2

Energy security Climate change

Higher energy prices Rural development

Biofuels are an effective way to increase

energy security, reduce dependency on oil

imports

Together with improving fuel efficiency,

biofuels are the most important low-cost way

of reducing CO2 emissions in the transport

sector

Biofuels can create new sources of income

for rural areas. Increased competition for

arable land has raised awareness of

sustainability issues

Increasing cost for the marginal barrel of oil

(ultra deep water drilling, oil sand etc.)

supports demand for substitutes including

biofuels

| © UPM

BIOFUELS

Regulation is stabilizing and will favour

advanced biofuels

3

– 2003 2003 – 2010 2010 – 2017 2017 –

Source: Hart Global Biofuels Outlook 2010 – 2020; IEA Technology Roadmap, Biofuels for Transport; Directive 2009/28/EC; UPM

European biofuels

industry is born

Unstable

regulation due to

non-binding

targets and

unhealthy industry

Stable demand

growth from stable

regulation

Tax incentives still

remain a source of

uncertainty

Stable demand

that favours

advanced biofuels

Non-binding

targets

Tax incentives and

import tariffs

Binding targets

with penalties for

non-conformance

Tax incentives and

import tariffs

Advanced targets

• Greenhouse gas

reductions

• Indirect land use

• Sustainability

Taxation driven by

CO2 reductions

Regulatory

framework in

the EU

Implications

for biofuel

producers

No regulation

Biofuels marginal

in Europe

Industry is born in

Brazil in 1970s

with Pró-álcool

program

0

5

10

15

20

25

30

35

40

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Mill

ion

to

nn

es

Biodiesel Ethanol

Up to 2010 use of biofuels driven by voluntary country specific regulation

2010 -17 use of biofuels regulated by EU legisalation

2017- EU legislation favours advanced biofuels

Legislation favours advanced targets beyond 2017 • Greenhouse gas reductions • Indirect land use • Sustainability • Taxation driven by CO2 reductions

BIOFUELS

Use of transportation biofuels in the EU(*

*) Future demand is based on existing legislation, figures from National Action Plans 4

| © UPM

BIOFUELS

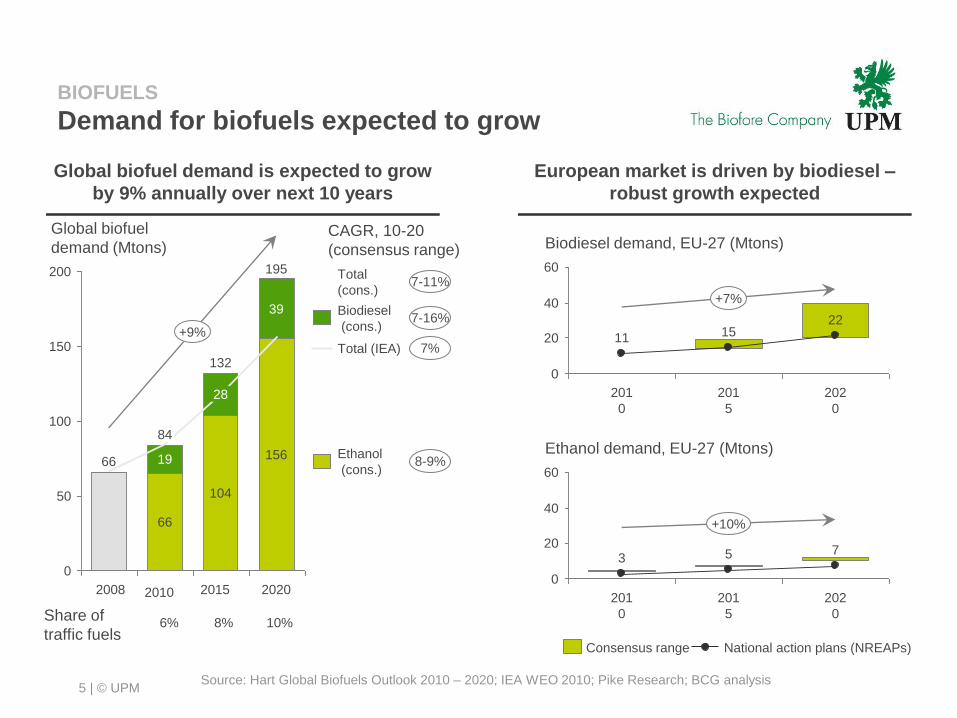

Demand for biofuels expected to grow

Source: Hart Global Biofuels Outlook 2010 – 2020; IEA WEO 2010; Pike Research; BCG analysis

Global biofuel demand is expected to grow

by 9% annually over next 10 years

European market is driven by biodiesel –

robust growth expected

Global biofuel

demand (Mtons)

200

150

100

50

0

+9%

2020

195

156

39

2015

132

104

28

2010

84

66

19

2008

66

Share of

traffic fuels 6% 8% 10%

Ethanol

(cons.)

Biodiesel

(cons.)

Total

(cons.)

Total (IEA)

CAGR, 10-20

(consensus range)

7-11%

7-16%

7%

8-9%

Biodiesel demand, EU-27 (Mtons)

60

40

20

0

+7%

202

0

22

201

5

15

201

0

11

National action plans (NREAPs) Consensus range

Ethanol demand, EU-27 (Mtons)

60

40

20

0

+10%

202

0

7

201

5

5

201

0

3

5

| © UPM

BTL (Gasification and Fischer Tropsch)

BIOFUELS

Several paths from feedstock to biofuels

Feedstock

Corn

Sugarcane

Wheat

Algae

Jatropha oil

Vegetable oils

Animal fats

Other

Sugars & starches

Vegetable oils and animal fats

Advanced feedstock (lingocel., waste, residues)

Wood

biomass

Switch grass

Corn stover

Other

Tall oil

Conversion End product

Fermentation & distillation

Ethanol

Hydrocarbons

Fermentation & distillation Sugar extraction

Bio

-industr

ials

/ c

hem

icals

Transesterification

Hydrotreatment

FAME biodiesel

HVO biodiesel

Pyrolysis and upgrading

Advanced biodiesel

Ethanol

Hydrotreatment

Sugar extraction with advanced pre-treatments,

i.e.. enzymes

Pre-treatment

Fuels with inferior properties to conventional oil products

Fuels with comparable or better properties to conv. oil products

UPM focus

Ad

va

nce

d te

ch

no

logie

s

Con

ve

ntio

nal

tech

no

logie

s

6

| © UPM

BIOFUELS

UPM with clear competitive edge in biofuels

• Ethanol is the most cost efficient way to produce

biofuels. However, ethanol can only be blended to

gasoline and only up to 10% of gasoline volumes

• Advanced biodiesel is highly competitive against 1G

FAME biodiesel due to lower cost, better product

quality and higher sustainability. In addition, the

blending of FAME is limited to 7 %

• Tall oil as a low-cost non-food feedstock is a

competitive solution for advanced biodiesel. The

blending limit of the biodiesel is >50%

• UPM is in a unique position in tall oil based biodiesel

due to its technology IPR and secured access to low

cost feedstock

7

Substitution from ethanol

Competition against 1G

FAME biodiesel

Direct competition in

hydrotreated biodiesel

| © UPM

BIOFUELS

UPM invests in wood-based biodiesel

• UPM invests in the world’s first advanced wood-based biodiesel

production in Lappeenranta, Finland

• Main product is advanced, 2nd generation biodiesel

• Commercial scale industrial investment

− Total investment of approximately EUR 150m

− Production 100,000 tonnes/a of advanced biodiesel

− Production starts in 2014

• Raw material is sustainably produced crude tall oil,

a residue from pulp production

• Technology is based on UPM’s innovations and

long term development work

• Potential for UPM to triple capacity by 2020

8

| © UPM

UPM Biofuels

Low-cost raw material

Valuable end product(*

BIOFUELS

Incentive for distributors to pay a premium for

UPM’s biofuel over reference product

9

Raw material cost Margin

1st generation biofuels

Expensive raw material

Expensive end product

CTO (crude tall oil) fractionation

Low-cost raw material

Cheap end products

*) Deserves a premium on reference product (from tax advantage & product properties)

to get the same value for the distributor.

– +

+ –

+ +

Creating a new value chain

+

| © UPM

BIOFUELS

UPM's biofuels significantly reduce

GHG emissions compared to fossil fuels

10

*Source: Directive of the European Parliament and of the Council on the

Promotion of the Use of Energy from Renewable Sources

0

10

20

30

40

50

60

70

80

90

100

Fossil diesel* Rapeseed biodiesel* Palm oil biodiesel(with/without methane

capture)*

UPM's biofuels

%

EU 2011

EU 2017

EU 2018

(new plants)

62

81

44

20

| © UPM

BIOFUELS

Achievement in key targets

11

1 Vision and business plan in place • Major player in advanced biofuels in Europe • Produce advanced biofuels with premium value

at competitive costs

2 Own process technologies in place • Hydrotreatment of crude tall oil

• BTL (Gasification and Fischer Tropsch) from energy wood

3 Investing into first biorefinery

• EUR 150m investment to produce advanced biodiesel from

crude tall oil, start-up mid-2014

• Raw material sourcing and distribution partnerships

4 New technologies and broader feedstock

• Develop a concept to produce transportation fuels through

pyrolysis and by upgrading of pyrolysis oil

• Potentially cost competitive against fossil oil products

• Process development to operate with broader feedstock